Abstract

The emerging growth of the sharing economy demonstrates the need to understand the factors driving this growth and the business models and practices of sharing economy service (SES) companies. Using case vignettes as the research method, this article analyzes the operations of a large number of these companies and presents a set of building blocks that are useful for generating the business models of SES companies. An examination of the successes and failures in the practices of SES companies provides a number of managerial recommendations.

Sharing economy services (SESs) represent a new wave of businesses that use cloud-based technology to match customers with providers of services such as short-term apartment rentals, car rides, and household tasks. 1 These SESs are one of the fastest growing segments of the economy and are part of the larger information-intensive services sector, which is also growing rapidly. The information economy as a percentage of the total GDP in the United States has grown from 46.3% in 1967 to 60.2% in 2007, and information-intensive services such as those in finance, business, education, and health care have grown at even faster rates. 2 Although the growth in the information economy in the previous century was primarily driven by the increasing use of information technology in the operations of traditional businesses, the growth in the current century has come about mainly as the result of more customer-facing transactions in innovative, new industries.

Being a part of this broader trend, the sharing economy traces its origins to the beginning of this century as advances in technology have continued to facilitate communication between individuals and as the individual customers have become more comfortable with the use of technology in day-to-day transactions. Botsman and Rogers were among the first to recognize the growing importance of the sharing economy and its growing impact on business as SESs like Uber and Airbnb started to have an impact on traditional businesses in their respective industries. 3

Airbnb, HomeAway, Uber, and Lyft are some of the best known and most successful SES companies. A study concluded that a majority of people in the United States own far more assets than they actually need or use; as a result, the average cost of owning those assets is unnecessarily high. 4 However, if individuals could, at their own discretion, share their underutilized assets with others, they would recover at least the marginal cost of using those assets, resulting in lower average costs. This notion of sharing underutilized assets and recovering the marginal cost of using them, plus a portion of the fixed cost of owning these assets, is one of the main drivers of today’s sharing economy.

The reason that we did not observe more SES companies in the past can be attributed to “transaction costs,” 5 which are the transaction-related costs that the buyer and seller of a service incur in finding/locating each other, establishing trust, entering into a contract, delivering the service, and making payments. The significant reduction in these transaction costs due to the advances in information technology has served as a catalyst for the rapid growth of today’s sharing economy.

The sharing economy has grown significantly in the past decade and is expected to continue growing rapidly for the foreseeable future. Foye estimates that the sharing economy will grow from $18.6 billion in 2017 to $40.2 billion in 2022. 6 Williams believes that this rapid growth in the sharing economy is being fueled by millennials, who in 2015 represented the biggest population group in the United States with 75.4 million. The combination of their familiarity with state-of-the-art technology (specifically mobile technology), the larger value they place on having experiences as compared with owning goods, and a willingness to share their belongings with others all relate directly to the growth in the sharing economy. 7

Another driver of that growth has been the large amount of venture capital funding that the industry has received in the last decade. As estimated in 2017 by Boston Consulting Group, a total of about $23 billion in venture capital funding had been invested in sharing economy companies since 2010. 8 Travel-related SES companies such as Airbnb, Uber, and Lyft have experienced particularly explosive growth in both their market valuations and the size of their operations. For example, in 2017, the market valuation of Airbnb was about $31 billion, which was comparable to the valuation of about $38 billion for Marriott/Starwood, the world’s largest hotel chain. In the same year, Uber had about 600,000 drivers in the United States while the taxicab industry employed only about 232,000 taxi drivers around the country. 9

A Time magazine poll published in January 2016 estimated that 44% of Americans had used a SES. 10 PricewaterhouseCoopers also reported similar results in its survey. That survey also found that among adults familiar with the sharing economy, more than 80% agreed that sharing services made life more affordable, convenient, and efficient, and that trust between customers and providers is very important for the sharing economy. 11

Cooperstein suggests that we are now in the “Age of the Customer,” with the power in the marketplace shifting from the producer to the customer. 12 A major cause for this shift is the emergence of information-intensive services (including SES companies) and the ease of access to the information they provide through their digital platforms to both the providers and the customers of the service. Because of this shift, an increasing number of companies are now focusing more on how they interface with their customers and how they restructure their supply chains. There appear to be two major approaches to accomplishing this. Companies such as Tesla, Apple, and Dell, which are often referred to as full stack companies, tend to be vertically integrated; that is, they design, produce, and deliver complete products and services while simultaneously managing their customer interactions in a more direct manner. 13 In contrast, a much faster growing trend that is being adopted by companies is what we call thin stack companies. These thin stack firms typically control only a small portion of their respective supply chains, focusing primarily on the interface with both their suppliers and customers through digital platforms. The reason for their significant growth is the relatively low entry barriers to designing a digital platform and subsequently collecting, managing, and disseminating information. SES companies are prime examples of thin stack companies that link customers in need of a service with the suppliers of that service.

Although the sharing economy has evolved over time and has many definitions, in our view, SES companies have three main characteristics: they link customers in need of a service with the suppliers of that service, they operate through digital platforms such as a website or a mobile app, and they offer services based on underutilized physical assets and/or labor.

In essence, SES companies provide a matchmaking service where individual customers or businesses can take part on either or both sides of a service transaction. Today, examples of SES companies are found in all types of service settings, including peer-to-peer (P2P), business-to-consumer (B2C), and business-to-business (B2B) services. However, this article primarily focuses on P2P services, which were the genesis of the sharing economy and still exist in large part today.

The sharing economy clearly serves as a good example of the democratization of business, which allows individuals to enter markets for the first time and compete almost immediately as equals with larger, well-established companies. SESs have facilitated this democratization through their digital platforms, which have significantly reduced transaction costs to both the individual providers and customers while simultaneously opening up new, previously untapped markets for both.

The P2P services in the sharing economy are not only about using underutilized resources; they can also provide an attractive and more profitable option for households and private individuals. For example, in an Airbnb investment property the landlord can collect higher rents in total as compared with traditional long-term tenancy. Interestingly, this can also lead to a lower occupancy rate. Thus, in the sharing economy, in some instances, the resource may actually become less utilized as compared with traditional approaches.

There are a number of reasons why it is interesting and important to study SES companies: they are innovative businesses that represent a fast-growing part of the economy with a relatively low cost of entry 14 ; they have generated a tremendous amount of interest as well as controversy in recent years 15 ; they typically have a major impact on the traditional businesses with which they compete 16 ; and they tend to have a positive impact on sustainability and the environment since they utilize existing underutilized resources. 17

The objectives of this article are to study a range of SES companies in selected service industries to better understand the innovative approaches they use and the plausible reasons behind their successes and failures, develop a set of proposed business model building blocks that can be used to generate, describe, and analyze the business models of SES companies, and offer managerial recommendations for SES companies as well as for the traditional businesses they compete with.

Survey of Literature Related to Sharing Economy

The Evolving Sharing Economy

A 2010 book by Botsman and Rogers 18 described the vision of “sharing,” which was the main attraction behind the rise of the sharing economy movement. Since then, innumerable articles about the sharing economy have been published in the popular press and consulting company reports, 19 essentially painting a rosy picture of the movement. Most of those articles do not contain any hard-nosed analysis and often just reiterate the original vision about the benefits of sharing and the claims made by websites and promoters of SES companies. A report by Brookings India, 20 however, provides an interesting insight into the emergence of the sharing economy in the other parts of the world. Since most customers in underdeveloped economies, such as India, cannot afford to acquire even moderately expensive assets, the opportunity to use those assets through the sharing economy concept is highly appealing. Thus, sharing economy companies are likely to have a very bright future in the underdeveloped economies of the world. A recent book by Sundararajan provides a thoughtful survey of the developments in the sharing economy in the United States and in Europe. 21

In the past few years, however, articles and blogs have started to raise red flags about the disconnect between the current reality and the original vision in the sharing economy. 22 Two recent books on the sharing economy, one by Hill 23 and the other by Slee, 24 argue that the business practices of some of the largest and most successful SES companies, such as Airbnb and Uber, have evolved into something different than that envisioned by the early SES firms. The leading companies have become large corporations themselves, and the profit-making motive now seems to be the only driver in carrying out transactions in an unregulated, free market sense. The researchers argue, with convincing evidence, that the success of SES companies stems primarily from their objectionable business practices, such as not following, to the extent possible, the rules and regulations under which their traditional competitors operate—thereby avoiding the associated expenses—and keeping the suppliers of the service (such as drivers of a ride-sharing service) off the payroll, treating them instead as independent contractors—thereby minimizing costs by not paying benefits such as pension obligations, vacation time, or worker insurance against injury.

Transaction Cost Economics

A basic assumption in neo-classical economics is that all economic agents have access to full information about the quantities and prices of all products and services, as well as about all production and consumption possibilities, and that the only costs to be considered are the costs associated with production and consumption. 25 Coase changed this basic assumption by introducing the real-world view that economic agents only have access to limited information and that they incur many costs in transacting in markets. 26 He argued that due to the existence of “transaction costs,” which can be quite large at times, economic agents find it beneficial to organize large economic entities (such as corporations) to produce goods and services and thereby lower transaction costs. Thus, Coase offered transaction costs as the primary explanation for the existence of large-scale enterprises. Were there no costs of transacting between the agents in markets, the structure of industries would be composed of individual buyers and sellers of goods and services.

Williamson further developed the concept of transaction cost economics by building on Simon’s bounded rationality hypothesis. 27 Williamson argued that transaction costs are created due to the fact that all economic agents exhibit bounded rationality and act opportunistically, that assets have specificity in their use, that transactions are carried out with smaller or larger frequencies, and that uncertainties cannot be avoided.

Applying transaction cost economics to the sharing economy, Henten and Windekilde 28 explain that the main innovations offered by SESs are the multisided platforms 29 they provide that easily link buyers and sellers of services to significantly reduce transaction costs. This reduction in transaction costs is the main reason why there has been an explosion of innovative service economy enterprises in the United States.

The transaction costs have also been significantly reduced by SES companies that are taking advantage of a concept known as “service inventories.” This concept was first introduced by Chopra and Lariviere 30 and subsequently expanded upon by Davis, Field, and Stavrulaki. 31 The goal in creating service inventories is to facilitate and/or reduce the steps (and time) in the service delivery process, which lowers transaction costs and creates customer value during a service encounter.

Another factor that has been facilitated by technology, especially cloud technology, is the ease of access to these SESs. Berry et al. 32 identified service innovations—in terms of how firms provide access to their core services—as opportunities for companies to either develop previously untapped markets, as with SESs, or gain a competitive advantage, exemplified by Amazon’s online book sales in contrast to Borders’ (which is now defunct) store-based retail sales.

The ease with which SES companies can collect payments from their customers and pay their service providers has had a significant positive impact on their growth and this can also be attributed to advances in technology. It is not a coincidence that online payment system companies such as Stripe (used by Lyft and TaskRabbit) and Braintree (used by Uber), among many others, emerged around the same time as the SES companies. The payment processing APIs (Application Programming Interfaces) of the payment system companies are easy to embed within the digital platforms of SES companies, and that has made it easier for the SES companies to receive payment from its customers and to pay their service providers, such as Uber drivers and Airbnb homeowners. Moreover, some of these online payment system companies are also able to split payments from customers. This ability enables services where a group of customers sharing a service (such as an Uber ride or an Airbnb home) can each pay for his or her use separately using their individual apps.

The Service Triads

Although a dyad consisting of a buyer and a seller of goods or services has been the focus of research in business and economics for a long time, the study of triads has gained considerable importance and momentum in the last two decades. Earlier work by Smith and Laage-Hellman described the importance of small networks as a basis for understanding particular aspects of network structure and processes. 33 Subsequently, studies in manufacturing by Choi and Wu, 34 informed by social network theory, brought the triad to the forefront as an object of investigation, while Li and Choi extended the study of triads to service settings. 35 In their lead article in a special issue on service triads, Wynstra et al. provide a review of different strands of research and various theoretical frameworks that are useful for studying service triads. 36 They find that service triads are currently studied in several fields including operations management, supply chain management, management and organization studies, and the social sciences. Another useful survey article by Sengupta et al. identifies ten themes of research in service triads. 37

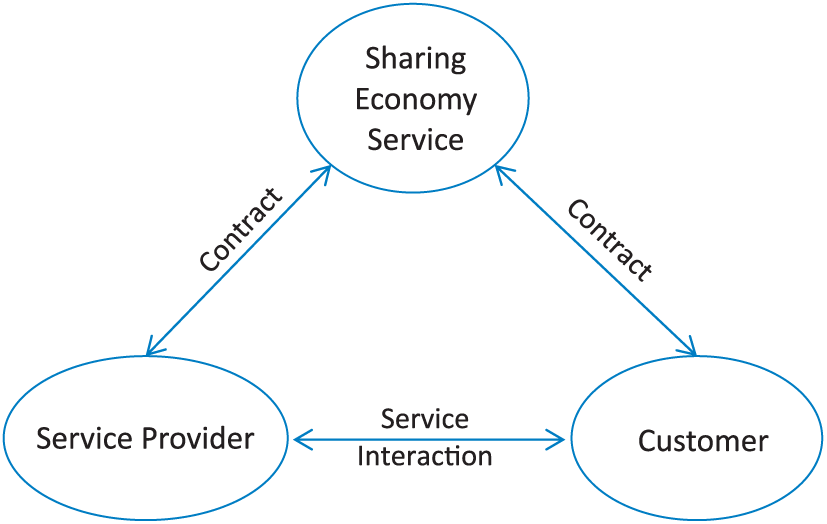

In service triads, the end customer contracts with an intermediary firm (exemplified by an SES company such as Airbnb), but the service is provided to the end customer by a subcontractor of the intermediary firm (such as a homeowner willing to rent a room in the case of Airbnb). Here, the service interaction takes place essentially between the service provider and the end customer. Figure 1 shows the basic structure of the service triad in the sharing economy. Since the intermediary firm does not provide the service, it needs to establish and nurture its relationship not only with the customer but also with the service provider. Thus, in a service triad, the intermediary firm faces what Eisenmann et al. call a two-sided market. 38

Service triad with sharing economy service.

Li and Choi have examined the dynamics of service triads. 39 Among a number of findings, they argued that the role of the service provider is potentially critical and that the ongoing interactions between the service provider and the customer, after service delivery begins, can undermine the relationship between the intermediary and the customer in the long run. Hence, unless the intermediary firm, that is, the SES company, offers a unique value, it can face a risk of disintermediation, whereby the customer establishes a direct relationship with the service provider in accessing the service in the future.

The service triad is a unique form of the service constellation concept that was introduced by Normann and Ramirez, 40 who suggested that value creation in services is not linear as defined by Porter’s value chain, 41 but rather requires cocreation with several entities (including customers), which often occurs simultaneously. (The concept of value cocreation involving both producers and customers is one of the major components in the seminal work on Service Dominant Logic [SDL] that was introduced by Vargo and Lusch. 42 ) The recognition that the cocreation of value by both suppliers and customers is especially important for SES companies is demonstrated by the fact that both suppliers and customers often have the opportunity to evaluate each other through surveys.

As Kwan and Hottum point out, 43 these triads are part of a larger service system that often involves many players. Thus, the multisided platforms that SES companies operate are designed to accommodate additional players. Examples of these additional players include credit card companies for payments and social media companies such as Facebook and Yelp that provide customers’ evaluations of the services. Multisided platforms and two-sided markets are key concepts associated with sharing economy companies in that they shape their economics of the industry and influence the competitive dynamics. It is important to keep in mind the relationship and differences between these key concepts. The two-sided markets represent an economic/actor perspective about actions taken, while multisided platforms are the organizations (and their products or services) that create value by linking and enabling direct interactions (between two or more sides) that improve the ease of conducting business and reduce the transaction costs.

The Sharing Economy: An Empirical Inquiry into the Phenomenon

To achieve the goals of our exploratory research, we used the case study approach, defined by Yin as a research method involving empirical inquiry that investigates a phenomenon within its real-life context. 44 However, as Yin suggests, the evidence from multiple cases is likely to be far more compelling and robust. Hence, we adopted the case vignette methodology followed by Kleinbaum and Stuart. 45 Specifically, we used secondary data to study business models and operations of 53 SES companies to understand their innovative approaches. Of the 53 SES companies we studied, ten companies had failed and the remaining 43 were still in operation at the time of our study. Studying both types of companies allowed us to better understand the plausible reasons behind the successes and failures of SES companies and provided us with some insights in developing managerial recommendations.

In selecting specific companies to study, we started with a classification scheme that is based on the resource being shared with customers: physical, labor, or a combination of both. Within each class, we chose industries in which SES companies have been launched in reasonably large numbers. In compiling the case vignettes, we relied on secondary data.

SESs: A Classification

We identify three categories of SES companies based on the resources they offer to their customers.

Physical assets

Airbnb and HomeAway are examples of companies that facilitate the sharing of underutilized assets. They help homeowners rent out their underutilized rooms, apartments, and houses to customers in need of short-term lodging. Another example is Roost, which makes it feasible for homeowners to rent out excess storage capacity available in their homes or apartments.

Physical assets and labor combined

The next category of SES companies involves those that allow sharing of physical assets and labor combined. The SES companies that occupy this space include Uber and Lyft, which provide digital platforms linking available drivers with vehicles to the customers seeking transportation.

Labor

We further divide the category of SES firms that enable sharing of labor into three subcategories, while acknowledging that there is some overlap among the three. The different types of labor being shared in these subcategories are physical labor, SES companies (such as Wag and Taskrabbit) that focus primarily on those individuals who are willing to offer their available time in the form of physical labor; skilled labor, SES companies (such as Angie’s List and HomeAdvisor) that link individuals/firms with specific skill sets to customers in need of these skills; and intellectual/creative labor, SES companies that offer professional services (such as health care, legal advice, and tutorial services). Given that the focus of this research is on P2P companies, we exclude service providers that are businesses.

The Evolution, Business Practices, Industry Economics, and Impact of SES Companies

The term sharing economy suggests two things that are somewhat contradictory to each other. 46 On one hand, the idea of “sharing” suggests noncommercial, person-to-person or P2P exchanges that involve no money and that are driven by the desire to help others by sharing resources. On the other hand, the term “economy” suggests market transactions involving an exchange of goods or services for money. Interestingly, the contradiction between the first and the second words in the term sharing economy also reflects the evolution of the sharing economy itself.

Kessler pointed out that while sharing is a much-loved idea, the companies formed in the earlier years that were based on the idea of sharing in its purest form have been mostly unsuccessful. 47 Consider, for example, SES companies based on sharing a power drill, which probably is used for only 15 minutes total in its entire lifetime. That being the case, why not rent a power drill or rent out your own power drill to other people and make a little money? The argument makes perfect sense. However, of the eight SES companies that were launched based on this idea, only one company, NeighborGoods, survived for a few years, and that too eventually folded. The reason behind these failures is the relatively high transaction cost. It seems that most customers who need a power drill prefer to simply buy it at a cost of, say, $30 and not spend an hour of their time to locate, pick up, and return the tool, plus pay a small rental fee. Hence, it is essential that even when the idea of sharing is highly attractive, an SES company must carefully evaluate and minimize the transaction cost involved in sharing.

Two companies that have become successful despite their primary focus on sharing have appealed to an inherent human tendency, as social creatures, to share with others what they have, while explicitly making clear that the company’s main aim is to help share and not make money. These companies are BlaBlaCar, a French SES company that helps passengers undertake inexpensive, long-distance, intercity travel, practically at cost, and CouchSurfing, which allows travelers to stay for free as guests with locals. Interestingly, CouchSurfing decided to change its status from a nonprofit to a for-profit company, and that move has led to serious objections by many members and to a string of ongoing problems for the company.

As is expected in any new industry, SES companies have experienced their share of failures. For example, FlightCar, a P2P airport car-rental company, was launched in 2013 to connect visitors interested in renting cars at the airport with locals looking to park their cars before flying out. The idea was promising, but the company was closed in 2016, primarily because it was focusing mainly on growth before putting in place a reasonable business process for achieving a good service-market fit, and due to its patchy and poor service quality. 48 Another example is Sidecar, which started as a ride-share company in 2011. Being a late entry into this market, it struggled to compete with Uber and Lyft and ultimately closed in 2015 after trying to deliver groceries and food before its closure. The main reasons behind Sidecar’s failure were legal/regulatory problems, a lack of focus and perseverance, and an inability to achieve scale and efficiency in a reasonably short time.

Although it is true that the sharing economy is growing fast, and this growth is forecasted to continue, the sharing economy faces significant challenges going forward, which include the following 49 :

Network effects: In Uber’s case, the more drivers there are, the more convenient Uber’s service becomes to its customers. However, the more customers there are, the more likely the drivers are to sign up to drive for Uber. This positive feedback loop potentially offers increasing benefits to Uber’s customers and drivers, as well as to Uber. However, the network effects for Uber are somewhat weak since they are local. Having more drivers in New York City does benefit customers in that city. However, the benefits to customers living elsewhere are rather limited in the sense that they are realized only when those customers visit New York City.

Economies of scale: It takes a large investment to develop a digital platform, but once the platform is ready, it can be made available to additional customers without incurring any additional cost. Thus, economies of scale do exist, but they are somewhat limited since new ventures also need to spend large sums of money on marketing and sales to continue attracting new customers and on incentives to attract additional service suppliers.

Switching costs: The cost of switching from one SES company to another is small for both the customers and the providers. For example, a customer (or a driver) can easily switch from Uber to Lyft without incurring any penalty.

Uber, Airbnb, and Taskrabbit are perhaps the best-known companies in the three categories of SES companies proposed earlier, and they represent a major portion of the total revenue and market valuation of the sharing economy. As mentioned earlier, all three companies have come under severe scrutiny concerning their questionable business practices in recent years. 50

Uber has been highly successful in terms of its phenomenal growth in both market share and revenue, but what is not particularly well-known is that it also happens to be one of the largest loss-making private companies in the tech industry. As the Associated Press recently reported, in 2017, the company lost $4.5 billion on an annual gross revenue of $37 billion. 51 With the need to maintain a two-sided marketplace involving passengers and drivers, the company offers low fares to attract customers and sign-up bonuses to drivers to maintain a large enough pool of drivers. This has significantly hurt its profitability. Uber does have economies of scale in its operation, but evidently it has yet to reach a scale sufficient to start making a profit, raising the question of whether the company is ever going to make a profit.

Uber has also run afoul of livery regulations in almost all the cities in which it offers its services. Uber’s history of scandals and disregard for local rules finally caught up with it in September 2017 when London’s transportation authority ruled that Uber is not a “fit and proper” operator and declined to renew the company’s license to operate in the city, Uber’s largest European market. 52 The reasons cited by the authority when explaining its decision include the company’s questionable safety record, its bypassing of regulations that licensed taxi services have to follow (screening of drivers, inspection of vehicles, and employment laws), and its avoidance of tax payments by registering the company in another country. In addition, in December 2017, the European Union’s court ruled that Uber should be regulated like a taxi company and not a technology service, a decision that is likely to constrain Uber’s activities in European countries. 53

Roose reported that, at present, most SES companies are small, are losing money, and are mainly surviving on venture capital. Dozens of “Uber for X” start-ups that raised millions of dollars to launch SES companies in industries such as laundry, parking, and grocery delivery have run out of capital before reaching the necessary break-even volumes. 54 Since many SES companies face the same problems that Uber did—spending more than their revenues or subsidies, and marketing and sales to get additional customers and providers—a bumpy road is not necessarily out of the picture for the industry.

Although the current size of the sharing economy, relative to the total economy, is small, SES companies have had a measurable impact in the service sectors where they have established themselves. For example, a study that examined hotel revenues in Texas showed that in those areas where Airbnb had a major market penetration, the revenues of hotels had significantly reduced in comparison to no decrease in revenues in similar hotels in areas where Airbnb had not established a presence, with economy or budget hotels being the most affected. 55 Another study in the hotel industry, as reported by Gerdeman, 56 confirms that in those geographical areas where Airbnb had significant market penetration, hotel room bookings and revenues had decreased. This is attributed to the fact that during peak periods, hotels typically charge a premium for rooms, but individuals, through Airbnb, seeing the opportunity to make higher than normal income from renting out their rooms and apartments during these peak periods, make them available when they otherwise would not. This is one of the major advantages that SES firms have over traditional services: the costs that are fixed for traditional services (i.e., for rooms, cars) are variable costs for SES firms. An increase in rates, be it for a room or a ride, increases the available capacity for SES firms.

As another example, consider the impact of Uber on the taxi industry in New York City. There has been a drop in the average price of a taxi medallion in New York City from $1.3 million in 2013 to $900,000 in March 2017. 57

Common Characteristics of SES Companies

The SES companies we studied had several common characteristics:

They are the intermediaries in the traditional service triangle connecting customers in need of services with suppliers providing the services. The primary value added by these firms is their ability to establish networks for both suppliers and customers; to collect, aggregate, and disseminate data; and to collect payments from customers and pay suppliers for their services. All digital platforms created by the SES companies are cloud-based, making them readily accessible at any time and from anywhere in the world. In effect, these firms are using internet-based mediation to inject themselves into the supply chains.

The service suppliers are typically amateurs (with no formal experience) in the respective industries in which these SES firms operate. SES companies are creating new opportunities for the amateur suppliers to earn money.

The SES companies tend to carry out transactions on a P2P basis where individual service providers offer services to individual customers. Self-employed farmers and craftsmen were the norm in the preindustrial era. During the industrial revolution, emerging manufacturing automation technologies displaced the craftsmen, and modern management practices enabled the formation of large corporations that started offering goods and services to customers. 58 However, the emerging digital platforms of SES companies have facilitated direct interaction between the individuals offering services and the customers of those services, possibly going back to preindustrial era practices in a small way.

The services offered by SES companies are typically simple, single-stage services rather than complex or multistage services.

In many respects, in comparison with traditional service providers, SES companies exhibit large flexibility in managing their capacity. In fact, they do not own the service capacity they need to serve their customers; hence, other than the extra incentives they offer to attract suppliers in special situations, the SES companies incur virtually no incremental cost in adding capacity because the burden of providing capacity rests with their suppliers.

In many instances, the SES companies that include physical assets in their service offerings can be viewed as being environmentally friendly, because they require no additional resources for satisfying additional customer demand.

Business Model for SES Companies

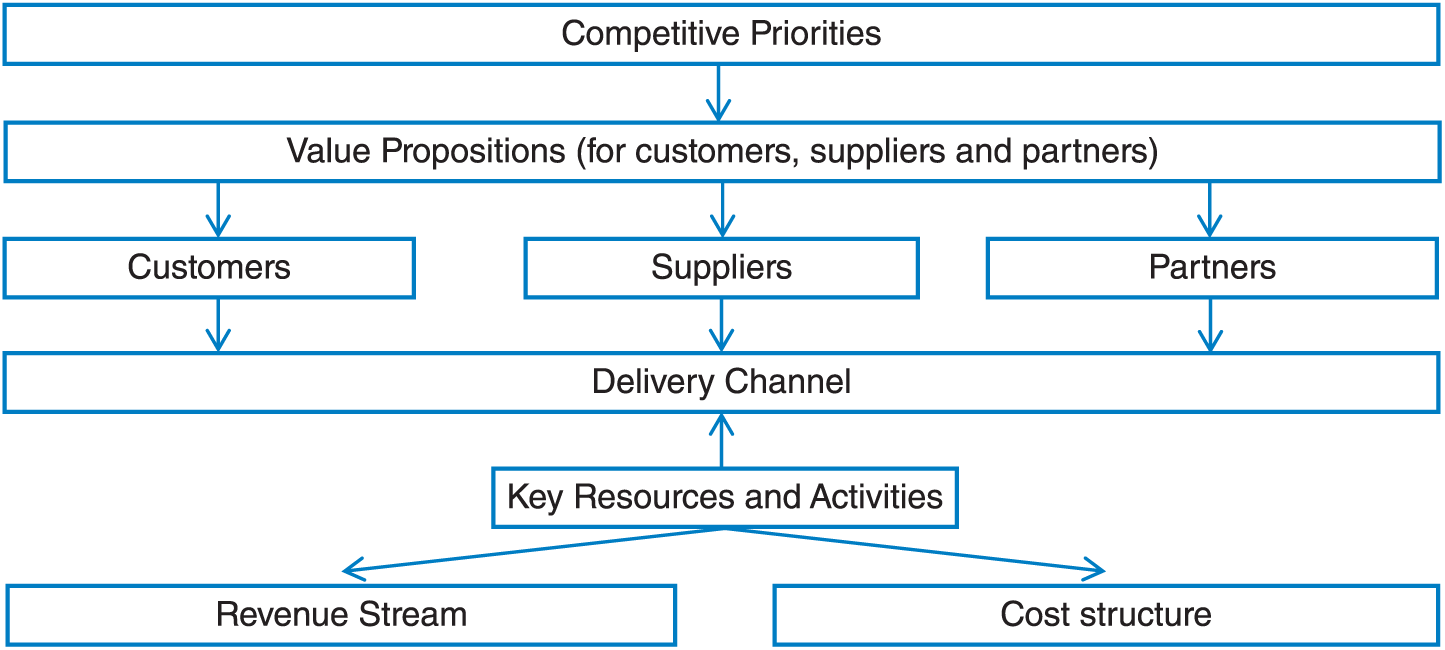

A business model is defined by Teece as “a design or architecture of the value creation, delivery and capture mechanism.” 59 Over the past two decades, business models have received increased attention among practitioners and researchers. However, as Foss and Saebi state in their survey article, 60 “emerging business model innovation literature lacks theoretical underpinning and empirical inquiry is not cumulative.” Since developing a proposed set of business model building blocks for SES companies is a goal of this empirical study, we had an opportunity to address these gaps. Accordingly, we selected the business model by Osterwalder and Pigneur 61 as a starting point in developing the proposed business model. The Osterwalder and Pigneur model, well-known in the practitioner world, consists of nine basic building blocks: Customer Segments, Value Proposition, Channels, Customer Relationships, Key Resources, Key Activities, Partnerships, Revenue Streams, and Cost Structure. In addition, we also referred to a survey of business models of e-businesses by Zott et al. to become familiar with the building blocks proposed by researchers. 62

Proposed business model building blocks

To investigate whether Osterwalder and Pigneur’s business model building blocks are suitable for adequately describing the business models of SES companies, we applied those building blocks to several SES companies we had studied. This exercise made it clear to us that to properly describe the way SES companies create, deliver, and capture value, the best approach would be to add two new building blocks and make slight adjustments to the original set of building blocks in Osterwalder and Pigneur’s model.

The primary business of SES companies is to create a match between customers and suppliers of a service. Hence, we suggest using “suppliers” as a new building block, which was not explicitly included in the original set. In addition, because SES companies typically enter existing markets with entirely new business models in terms of how they operate, analyzing traditional competitors and defining competitive priorities for these companies become highly important. Hence, we introduce “competitive priorities” as the second new building block. Furthermore, since we invariably found it easier to think through “customer relationships” while defining the “customers” building block, we decided to merge these two to create a single modified building block having the same name, “customers.” With the same consideration, we also merged “key resources” with “key activities” into a single modified building block titled “key resources and activities.” Thus, we believe that using all the original building blocks by Osterwalder and Pigneur, albeit in terms of seven as opposed to nine blocks, along with two new building blocks added to the set, will be suitable for describing the business models of SES companies. To confirm the validity of this assertion, we used our modified set of nine building blocks to describe the business models of all the SES companies in our study. We found that the set was indeed sufficient and suitable. We emphasize that this is an empirical finding and to that extent, the set of building blocks we propose is perhaps not the only way to describe the business models of SES companies, but what we propose was perfectly suitable for describing the SES companies we studied. Figure 2 presents a schematic diagram of the proposed business model building blocks, which is then followed by their short descriptions:

Competitive priorities: There are several well-known frameworks for determining an organization’s competitive priorities. Two of the more popular frameworks developed by Porter and by Treacy and Wiersema offer a low-cost alternative as a specific strategy that firms can adopt. 63 Low cost appears to be the strategy, at least initially, that SES firms typically adopt. The low-cost approach is also the preferred alternative for new businesses with a novel approach for creating customer value in a vast array of industries, 64 primarily because the technology adopted by SES companies readily supports this strategy.

Value propositions (for customers, suppliers, and partners): For the long-term success of an SES company, it is important to use its competitive priorities as the basis to clearly define its value propositions to customers, service providers, and partners, and ultimately to deliver them in practice. The primary value that SES companies create for their customers is the company’s ability to quickly link customers seeking a specific service to a supplier that can provide the desired service. Value to the customer is therefore measured along several dimensions, including convenience in locating a suitable supplier, response speed (whether it is to an inquiry for a house rental or a request for transportation), and variety of offerings (which, with respect to rental properties, can be location and types of properties; for labor it can be the different skill levels that can be provided).

Customers: For SES companies, customer demand is obviously created through the cloud. Consequently, one could argue that the customers for SES companies are segmented by their ability to use technology in one form or another. The way an SES company manages its relationships with its customers through the digital platform to increase trust and loyalty of customers is very important for the company’s long-term success.

Suppliers: Since the SES companies do not create and deliver the service themselves, it is critical that they recruit, monitor, and nurture the best set of suppliers who are responsible for the creation and delivery of the service. The business development activities toward that end are therefore very important. Managing relationships with suppliers is also critically important.

Partners: For SES companies, a partner refers to an organization that plays a supportive role in the service creation and delivery process. Typical SES partner companies are payment systems companies, credit card companies, insurance companies, and rating services such as Yelp and Trip Advisor that provide feedback on previous customer experiences.

Delivery channel: Creating the best possible match between the customer and the service provider is the fundamental value-add of SES companies. Accordingly, the use of internet and mobile app software platforms for that purpose is the distinguishing characteristic of SES companies. It is therefore critical that this software platform be carefully developed and continually improved to offer the best service and value to customers and service providers.

Key resources and activities: An SES company should acquire all the needed resources, such as information technology assets, so that it is able to perform the activities required for its business models to work. The key activities in the delivery process must be designed to maximize efficiency and minimize transaction costs for the customers, deliver on value propositions, and create and nurture a network of customers, suppliers, and partners. Key activities common to almost all SES companies are the development and maintenance of a software platform that can suitably match customers and suppliers in a timely manner, the maintenance of a database of customers and suppliers, and the establishment of performance monitoring systems by seeking feedback from customers and suppliers.

Revenue stream: As is true for all companies, generating revenues and profits are the primary goals of SES companies. Hence, understanding the revenue stream that an SES company can generate—through such means as transaction-based commissions, membership fees, rental or advertising fees, and profit margins on suppliers used in service creation—is important.

Cost structure: SES firms provide the networks that link customers wanting specific services to individuals or firms that provide them. Consequently, their primary costs are the fixed costs associated with creating the digital platform and the variable costs associated with maintaining the platform, increasing the number of customers, and enlarging the supplier base. This results in economies of scale in operation.

Business model building blocks for SES companies.

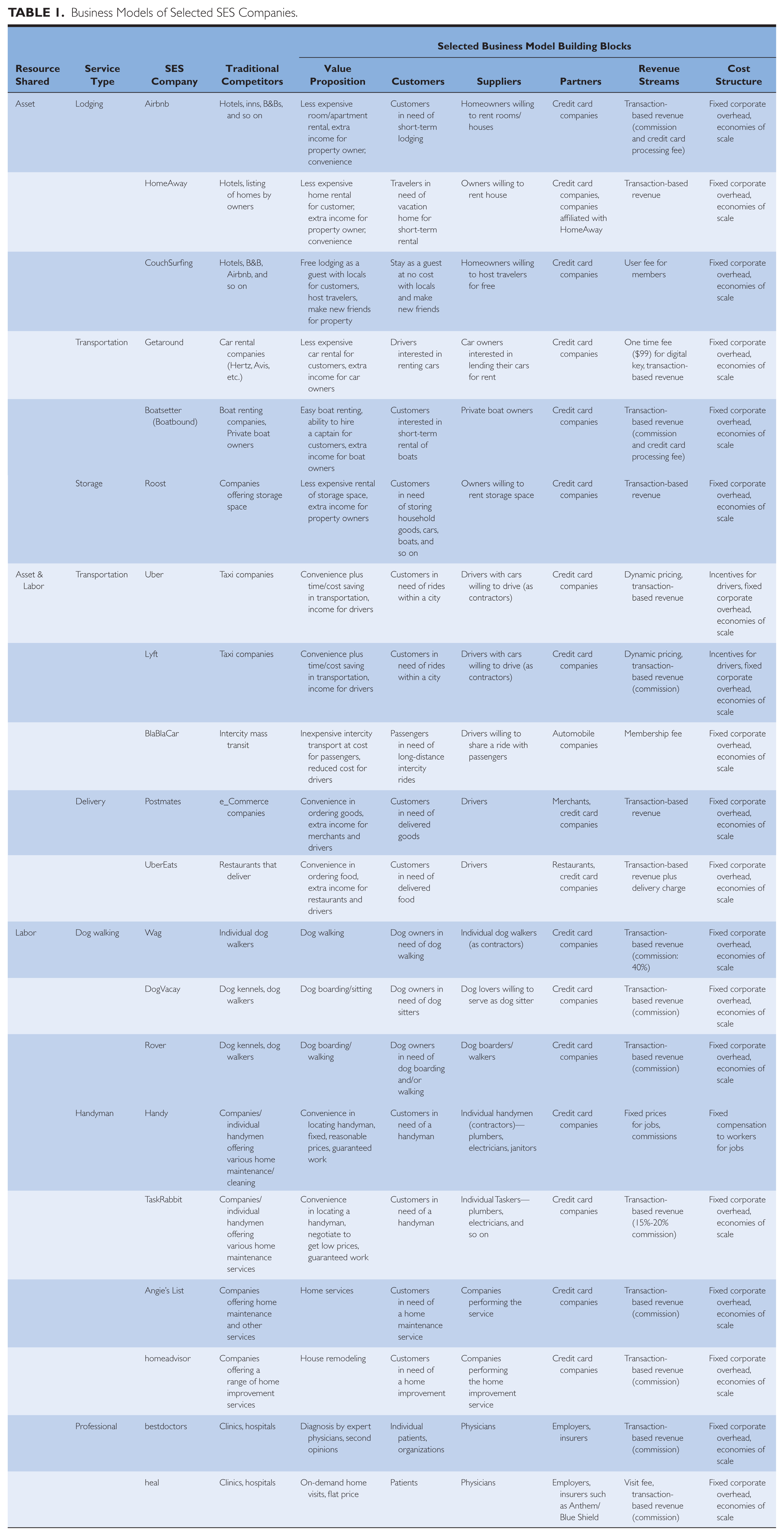

As mentioned earlier, we used the proposed set of building blocks to describe the business models of 43 SES companies that were in operation at the time of our study. We found that the business models of SES companies offering the same type of service were highly similar. For example, Getaround and Turo are both P2P car-rental companies that allow private car owners to rent out their vehicles to individual customers via their digital platforms. The business models of these two companies are essentially the same. Hence, we felt that illustrating the business model of only one of these two companies was sufficient for the purpose of this article. Applying the same logic, we present in Table 1 the business models of 25 selected SES companies as a sample that represents a large number of companies across all service types included in the study. The remaining 18 SES companies belonged to several service types (the number of companies studied for each service type is shown in parenthesis): transportation (3), delivery (1), dog walking (1), parking (1), laundry (2), miscellaneous trades (5), and professional services (5).

Business Models of Selected SES Companies.

Note: For brevity, three building blocks—competitive priorities, delivery channel, and key activities—are not shown in this table. SES = sharing economy service.

It should be noted that for the sake of brevity, we have not presented information about three building blocks in Table 1: competitive priorities (since most SES companies seem to use low cost as the main competitive strategy), delivery channel (internet and mobile apps were invariably the main delivery channel), and key resources and activities (based on our understanding of the industry and service operations we did prepare lists of key resources and activities, but those lists were rather detailed and long).

SESs: Managerial Challenges and Recommendations

Unlike most traditional businesses, SES companies offer neither products nor services of their own. Rather, the value they generate is the way they collect, aggregate, and present information to potential customers and service providers in creating a match. To the extent that the operational characteristics of SES companies are significantly different from those of traditional companies, the entrepreneurs and managers of these firms face a unique set of challenges.

Managing Growth Is Critical

As an intermediary in the service triad, the SES companies operate in a “two-sided marketplace.” Consider, for example, the experience of Uber. As mentioned earlier, the more riders there are on Uber’s platform, the better it is for drivers because they can earn more money. Conversely, the more available drivers there are, the better it is for riders because they can obtain rides in shorter times at lower prices. This positive feedback cycle implies not only first mover advantages but also the potential for winner-take-all dynamics. Kick-starting this positive feedback cycle is a primary challenge for any SES company. Uber seems to have met this challenge by raising huge sums of money from venture capitalists and using it to nurture its two-sided marketplace and growing rapidly in over 60 cities around the world. However, this has also led to continued, significant losses for Uber.

In managing growth, an SES company should carefully evaluate whether the industry it operates in and the competitive situation it faces are favorable for a winner-take-all outcome, in which only one platform survives. In general, a networked market will be served by the single platform only when the costs of enrolling in multiple platforms are too high for both sides of the market. 65 In the case of a ride-sharing service, the cost of switching from Uber to, say, Lyft is rather low for customers, and it is not particularly high for drivers either. Hence, the ride-sharing service is not conducive to a winner-take-all outcome, and it is likely that several platforms will survive and thrive in that market. In addition, as discussed earlier in the ride-sharing service, the network effects are weak. SES companies are well-advised to take calculated, measured steps in growing their businesses versus burning large amounts of capital to grow very rapidly in service markets where multiple platforms are likely to survive.

The final consideration in managing growth is the need to reach a sufficiently large volume of business in a reasonably short time. Essentially, all start-ups must reach a financial break-even volume before they burn all their start-up capital. Otherwise, their fate will be like that of many start-ups that went bust in the dot-com era of the late 1990s and early 2000s.

First Develop a Supplier Base and Then Attract Customers

SES companies focus on connecting customers with service providers, but they themselves do not create and deliver these services. Hence, the process for selecting and managing the supplier base that provides these services is critical to ensure a consistently high level of service quality. This is a major factor in the long-term success of SES firms (as it is for all firms). As we have found in our case studies, and as Andruss 66 and Blanding 67 argue, the first ideal step is to develop a reliable set of suppliers for the service that the SES company plans to provide; the next step is to then focus on attracting the right customers for these suppliers.

For example, consider Uber, whose process for screening drivers has recently come under severe fire in a CNN investigation that reported that a large number of Uber drivers have been accused of sexual assault or abuse of female passengers. 68 At the other end of the spectrum is Rover, a dog boarding and walking service that connects dog owners with a network of dog lovers for hire. Rover is known for its rigorous screening and training program for its service providers. 69 Rover uses an extensive review process that involves checking references, conducting background checks, and verifying social media accounts. The company also conducts online training and a review to ensure that every supplier applicant interested in providing the service has the personality, experience, and environment suitable for the dog-sitting or walking service. We believe that undertaking such a rigorous screening of suppliers to eliminate undesirable service providers must be viewed as a critical success factor by an SES company; otherwise, the company risks unfavorable press concerning poor service quality immediately after the launch of the service.

Design the Service Delivery Process to Add Value to Customers and Reduce Transaction Costs

In our study, the successful SES companies were those that were able to make the service delivery process as efficient as possible. The design and development of the software is of paramount importance in this regard, but there are several other factors to consider in designing the operational processes:

Two alternate modes of delivery in fulfilling demand are observed: an immediate, real-time delivery of service (e.g., Uber) or a scheduled delivery of service at some time in the future (e.g., Vetpronto). The logistics infrastructure needed to offer immediate real-time delivery is usually more demanding and more expensive.

There appear to be at least two approaches in creating the match: the customer chooses among several service providers (e.g., TaskRabbit), or the company finds the best possible match between the customer and the service provider (e.g., Uber).

Developing a suitable supplier base is critically important. One option is to develop a contractual relationship (exclusive or otherwise) with a set of service providers; the other is to have the ability to call upon the suppliers with whom there is no exclusive contract. The cost, quality, and reliability trade-offs should be considered in choosing the option.

Another operational design choice is whether the service is to be provided at the customer’s site or if a customer is to travel to the service provider’s site to access the service.

Ensure Service Quality, Create Good Customer Experience, and Foster Trust

Ensuring a high and consistent level of service quality is very challenging because it is highly subjective, being primarily dependent on the perceptions of the customer. Parasuraman, Zeithaml, and Berry, in their seminal research project, identified five dimensions of service quality: reliability, tangibles, responsiveness, assurance, and empathy. 70 They also introduced the Service Quality Gap Model, which provides service practitioners with a viable framework for improving the service quality of their offerings. 71

SES companies that are able to perform well on these dimensions are more likely to be successful in the marketplace. In addition, tangibles are particularly important for certain SES companies when physical assets are involved, such as rooms, apartments, or vehicles. Hence, proper maintenance and care of such physical assets is important for those SES companies. As discussed earlier, the research in service triads indicates that SES companies run the risk of being disintermediated. Given this finding, we believe that it is all the more important for an SES company to consistently deliver high-quality service and ensure long-term customer loyalty.

Another challenge for these thin stack companies is ensuring the quality and consistency of the experience received by the customers. Each of the suppliers typically operates independently of the other suppliers in the network, and often, these suppliers are relative novices, such as residential owners offering their homes/apartments for rent for short periods of time. Consequently, these suppliers may not have had the proper training necessary to create great customer experiences. Some firms, such as HomeAway and Airbnb, provide reviews by previous customers, but many suppliers do not have any reviews, and those that do typically have only a small number of reviews available, which are not necessarily highly reliable. Therefore, SES companies should ideally provide a certain degree of training to suppliers and make customer reviews available to their suppliers to ensure that a high and consistent level of service quality is provided to all customers.

Offering great customer experiences goes hand-in-hand with fostering trust. But building trust with customers can be somewhat difficult for an SES company because it primarily interacts with its customers via an online digital platform, and not via face-to-face contact. However, an online platform also offers the capability to show customers photos or videos of the service delivery in action, which can be used to foster trust. For example, Rover offers the ability to share photos of dog sitters interacting with dogs. In addition, it offers 24/7 veterinarian consultations to ease dog owners’ worries about their pets, thereby fostering trust among its customers.

Recommendations for Traditional Service Firms That Compete with SES Companies

For traditional firms to successfully compete with the SES companies, Cusumano offers a few suggestions, 72 including the following: work with local governments to level the playing field with respect to rules and regulations by ensuring that these are not being violated by SES companies; provide a significantly higher level of service and greater standardization across locations that, at least in the short run, the SES firms will not be able to match because their suppliers are typically inexperienced independent operators; and continue to segment the market, focusing on those segments where SES firms cannot compete, like large groups and conferences in the hotel industry.

Traditional service companies also need to recognize that SES companies are not a passing fad; rather, in many cases, they represent the future direction of business in terms of emerging business models and new market segments, often cannibalizing the business of existing traditional firms. The traditional businesses do, however, have some options, as noted above, for competing with these SES firms, but they must be willing to adapt, be flexible, and adjust their businesses accordingly.

Summary and Conclusion

The significant growth of SESs can be attributed mainly to the reduced transaction costs in the matching of customers and service suppliers made possible by SES companies. The ability of SES companies to facilitate the sharing of underutilized assets with others to recover part of the cost of owning the assets is another important driver of the emerging sharing economy.

The idea of “sharing” has been the primary attraction and the driver behind the rise of the sharing economy. After all, what is there not to like about using the power of the internet to help a friend—give a car ride, or help save a neighbor some time by running an errand—and also make some money in the process? Although SES companies are essentially based on that vision, as discussed earlier, there is often a disconnect between the vision and the reality—as demonstrated by the questionable business practices of at least a few SES companies. These aberrations will most likely get corrected through market forces or regulatory actions as the industry matures.

Using secondary data, we analyzed the business operations of a large number of SES companies in several industries, and subsequently developed the proposed business model consisting of nine building blocks—Competitive Priorities, Value Propositions, Customers, Suppliers, Partners, Delivery Channels, Key Activities, Revenue Stream, and Cost Structure—that can be used to generate and describe a business model for SES companies. Based on the analysis of 53 case studies and of the successes and failures in business practices of those SES companies, we made four specific recommendations to the entrepreneurs and managers of SES companies and three specific recommendations to the managers of traditional firms in industries in which the SES companies compete.

Footnotes

Notes

Author Biographies

Uday M. Apte is the Distinguished Professor of Operations Management at the Graduate School of Business and Public Policy, Naval Postgraduate School, Monterey, California (email:

Mark M. Davis is a professor of Operations Management at Bentley University in Waltham, Massachusetts (email: