Abstract

Traditional retail practices are under stress as retailers ponder various ways of setting up a sustainable omnichannel business model. A significant challenge in their endeavor relates to the blurring lines between physical and digital worlds. This article analyzes three retailers’ exploratory efforts of alternative physical retail spaces. There are five key innovation areas to revamp for such a retail store: in-store technology, the role of sales associates, leveraging a mobile channel, data analytics, and collaborations. Moreover, physical retail space can serve as an aggregation hub that connects various retailer-customer interaction points across physical and digital spaces.

However, in the efforts to innovate their business models and adapt their businesses to the omnichannel reality, retailers are faced with the uncertain nature and purpose of a physical retail store. 2 In fact, many retailers are exploring different digital technologies in their commitment to transcend the distinctions between physical and digital spaces, 3 but they are still faced with multifaceted challenges pertaining to the establishment of a sustainable omnichannel business model. In other words, enabling a customer experience that is well integrated across physical and digital space has its implications for retailers’ organizations, 4 especially when long-established business models—which are built around the siloed nature of retail channels—are in place. 5

This article therefore explores the changing nature and purpose of physical retail space and its increasing interplay with the digital world. In doing so, it aims to reveal various business model innovation activities that facilitate customers’ omnichannel experience through such revamped physical retail spaces.

By studying three retailers that are in the process of reshaping their value architecture (i.e., their business model) in line with their omnichannel strategies, this research highlights the physical retail space as the hub that aggregates various retailer-customer interaction points across physical and digital spaces. In addition, customer relationship building achieved through matching the proposed offer with customers’ needs and values is acknowledged as a driver for both value creation and value appropriation. Finally, the change in value delivery activities plays an important role and revolves around the premise that collaboration and partnerships are necessary in order to co-create and deliver value to the customer.

Business Models in Retailing

An omnichannel strategy is a base on which to establish a competitive advantage in the current retailing environment. A firm’s business model and its innovation can be the source of that competitive advantage. 6 However, as a tool that bridges the gap between the strategy that sets a firm’s goals and the implementation of ways to move toward these goals, the business model has had many interpretations over the years. Nevertheless, most researchers acknowledge Teece’s 7 definition of a business model as the architecture of the value creation, delivery, and capture mechanisms.

In retailing, the focus of a business model is not only on what is offered but also on how it is sold. 8 It is that how that is often the reason behind retailers’ strong value proposition (sometimes referred as “the offer” 9 ) that turns a customer to one retailer rather than another. 10 Therefore, in addition to Teece’s three value dimensions, value proposition represents another important dimension to be considered. Moreover, the concept of customer value proposition and value creation is closely linked with the service experience and the role the customer has in co-creating the value via the service. 11 Increasingly, scholars claim that the locus of value creation is moved outside the organizational borders and is co-created with a firm’s partners and customers. 12 Therefore, retailers’ business model innovation is believed to be a co-creating response to changing customers’ needs and values—that is, a way for retailers to match those needs with a new value proposition. Such innovation is in business model literature considered to be a novel and nontrivial change to one or more business model dimensions and to the value architecture linking them. 13

In addressing retail business model innovation, Sorescu and her colleagues refer to the retailing format, business activities, and the governance of the actors that deliver the proposed value. Others similarly suggest that the retail format is an expression of a business model by relating firm’s activities to its business context. 14 Therefore, in line with the idea that a retail format demarks a “place of transaction” (which is an aspatial concept and thus may be a physical or digital retail space 15 ), the very nature and purpose of the physical retail space becomes essential in understanding business model innovation activities. 16 It is thus worth mentioning that today, the physical retail space has a different purpose from a strictly fulfillment one and is now communicational, experiential, and transactional. 17 The digital retail space refers to environments 18 in which individuals and organizations interact in virtual, nonphysical spaces.

Furthermore, in order to support the value proposition via various retail formats, the choice and organization of different business activities are considered in this study because they describe how value is created and later appropriated for the firm itself and for its partners. These activities also refer to a firm’s key partnerships and collaborations and its first-line employees—that is, in-store sales associates and their activities during the delivery of the proposed value. 19 Therefore, coordination and collaboration with different actors in a retailer’s ecosystem need to be considered under the business model framework. Finally, value appropriation—as in “making money from the products and services offered to the market” 20 —is an essential dimension, but it is also the dimension that brings a debate concerning the proportion of the value that is captured by each of the businesses that participates in the value delivery.

Research Approach

Omnichannel retailing is an emerging phenomenon. As such, many aspects remain to be discovered and are yet to be conceptualized, which calls for an exploratory research approach. This study is based on case study research, 21 which has been used in many retail studies. 22 In particular, three companies that engaged in rethinking the formats of their physical retail spaces are studied. Two are natively online retailers that ventured into testing alternative retail spaces to fit their pursued omnichannel business model—the first being a startup men’s fashion retailer ASKET, and the second being an electronics retailer Dustin. The third one is the brick-and-mortar international fashion retailer Hennes & Mauritz (H&M) that began to explore ways to redo their existing physical stores. Furthermore, these companies have all envisioned the focus of the physical retail spaces to be the customer, and everything that was done in (re)designing the spaces was done with the customer in mind. The cases also complement each other in terms of customer segments—that is, business-to-business (B2B) and business-to-consumer (B2C) and whether they had physical stores prior to engaging in the explorative efforts of alternative physical retail spaces.

The primary data collection consisted of semi-structured interviews with C-level, business development, and store managers with extensive experience (totaling 400 minutes of interview data) and observations at physical stores and virtual locations (i.e., online stores and mobile apps). While the interviews provided exclusive insights into different retailers’ activities, the observations served to complement the information and point out the aspects that were potentially overlooked or ignored by the interviewees. The observations also helped to inform the discussion regarding different activities retailers engaged in to enable physical retail space for an omnichannel business model. In addition, archival data stemming from a broad range of sources (e.g., published presentations, reports, press releases on webpages of the studied retailers, news articles, and expert pieces) were also used to create a comprehensive understanding of the studied business model innovation activities that the retailers engaged in. Therefore, the data collection process involved diverse sources of information that together provided insights into the retailers’ perspectives while acknowledging consumers’ and partners’ aspects.

The data analysis followed Eisenhardt’s 23 recommendations for within-case analysis and subsequent cross-case analysis. First, each of the cases was analyzed independently, where case write-ups allowed for the emergence of insights into the peculiarities of the cases. During and after the interviews, a partial analysis was done by recognizing patterns across the different sources of data. The field observations served as a conscious commentary of what was happening in the physical retail spaces and allowed the researcher to probe emergent themes and to design specific questions for future interviews. This overlap of data collection and analysis gave a head start in identifying cross-case similarities and differences and in acquiring hunches about relationships between concepts. Second, as the tendencies of each of the cases were countered, the cross-case patterns emerged. 24 Here, relevant concepts in the data were grouped into first-order codes (i.e., terms used by the informants), after which axial coding was carried out wherein relationships among first-order codes were assembled into higher-order themes. This process yielded five key innovation areas that were refined based on multiple data sources, insights into prior literature, and reviewer comments. 25 Finally, practical examples and observed activities within key innovation areas were distilled into overarching value dimensions, therefore driving the discussion on business model innovation in retailing.

Description of the Three Analyzed Companies

ASKET

The main priorities for the company’s founders have always been the quality of the garments and that their production is carried out in a sustainable way, as well as promoting conscious shopping behavior and customer care for previously purchased garments. Their business logic is that by utilizing an online channel, they can sell products directly to the customer and thus reduce their price. However, communicating quality and giving consumers a sensory experience over the Internet were not possible. Therefore, to enable consumers to touch, feel, and try the products, they have tested different pop-up locations, both in their hometown of Stockholm and abroad. They exhibited products in different ways, from a few days to a couple of months. First, they had a pop-up location in Stockholm for a few weeks. Then, they were a part of a marketplace-based pop-up store 26 where they had their products on display for three months. Finally, they traveled abroad and exhibited in hotels in different cities where they had identified a potential customer base. As of the end of 2018, they have a permanent physical location that serves as office space and an interaction point between employees and customers. However, they have always stayed true to their main logic—ordering online. Therefore, after a customer visits the location, they receive a personalized email with their size chart and instructions on how to proceed with ordering online.

Dustin

This electronics company, which has operated exclusively online 27 for more than three decades, has a B2B and B2C focus. In this article, only the B2B focus has been studied because the physical store (which opened at the end of 2014) has been mainly dedicated to these customers. The decision to focus the store offering on small and medium enterprises (SMEs) and providing a space for them to get inspired, find information technology (IT) solutions, and work (if needed) was made after one of the traditional expos that the company organizes. However, they realized that this was not enough for B2B relationships. One of their identified business model risks was customer loyalty. Therefore, with the input of the product development team, it was decided to have a physical concept store dedicated to SMEs. The store employees were tasked to report to the communications department because the store had the purpose of being the “face” of the company. Moreover, before settling on the exact location in the city, research was carried out to understand which area was the most populated with SMEs. Opened even before omnichannel became a common direction, the store continues to develop and adapt to customers’ needs and values. It currently features four inspirational areas for customers to explore: buy immediately, experience mobile devices, experience workstations, and take advantage of meeting rooms (where customers can book and use rooms to conduct off-site meetings and/or tryout equipment).

H&M

The second-largest fashion brand in terms of the number of physical stores worldwide has had difficulties matching the physical store format with the values of contemporary, digitally savvy customers. The Laboratory team at H&M Group has worked closely with the new concept store in Stockholm’s upmarket neighborhood that opened at the beginning of 2018 in the local department store. This store is one of the first attempts to understand what can be done with existing physical retail spaces in order to cater to customers’ needs. The focus of the store is on the customer experience—providing superior assistance during the in-store customer journey and offering a relevant product range (consisting of products from other companies as well). The location was chosen because there was already an adequate H&M store. In addition, the analysis of what people in that neighborhood had been buying was carried out and the product offering was tailored to the customers’ preferences. Finally, the layout of the merchandise is planned and mapped into the radio frequency identification technology (RFID) system, which then enables the provision of services that are intended to enhance the customer experience. The store features 12 advanced RFID readers attached to the ceiling.

Revamped Physical Retail Space

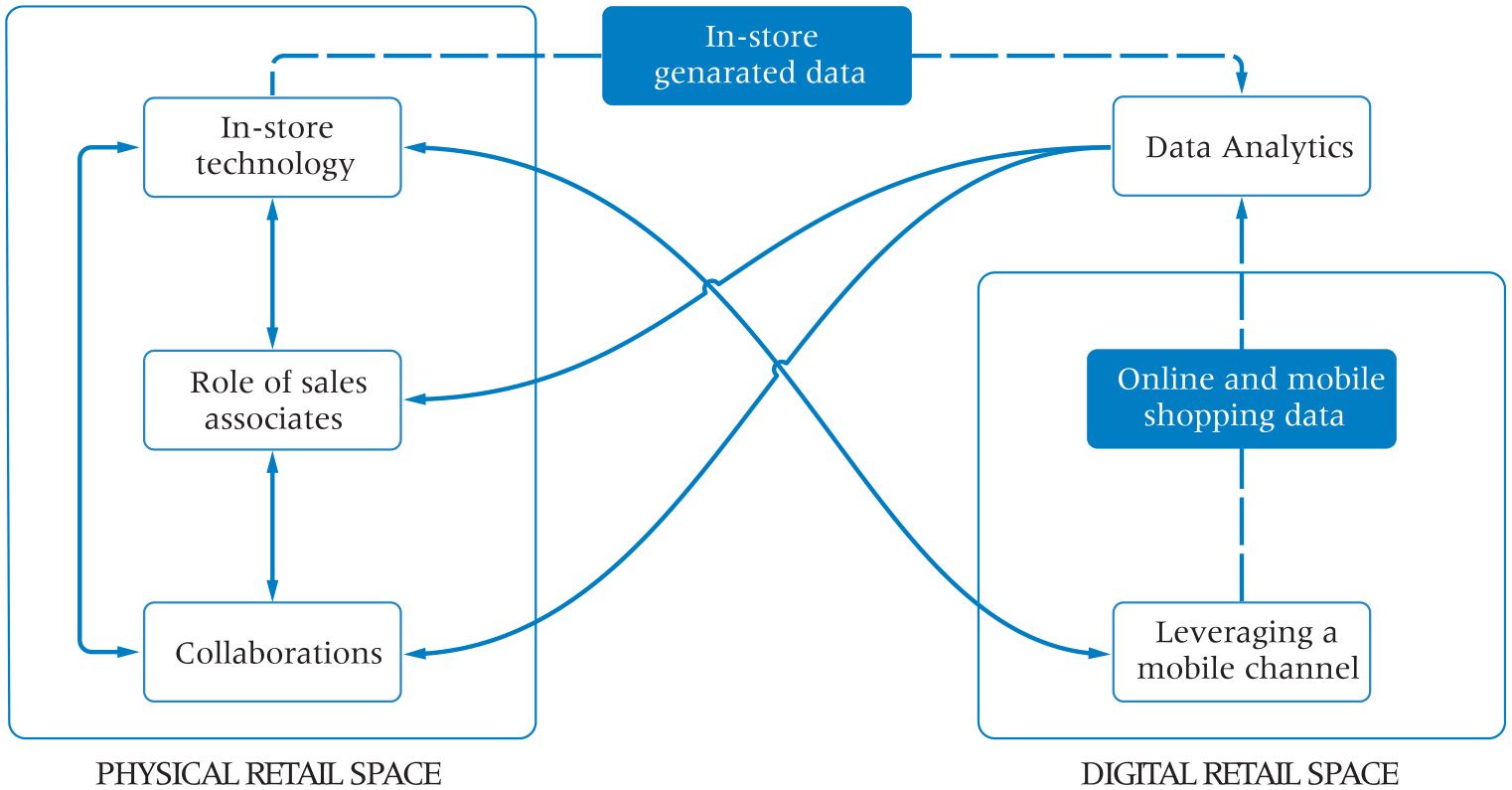

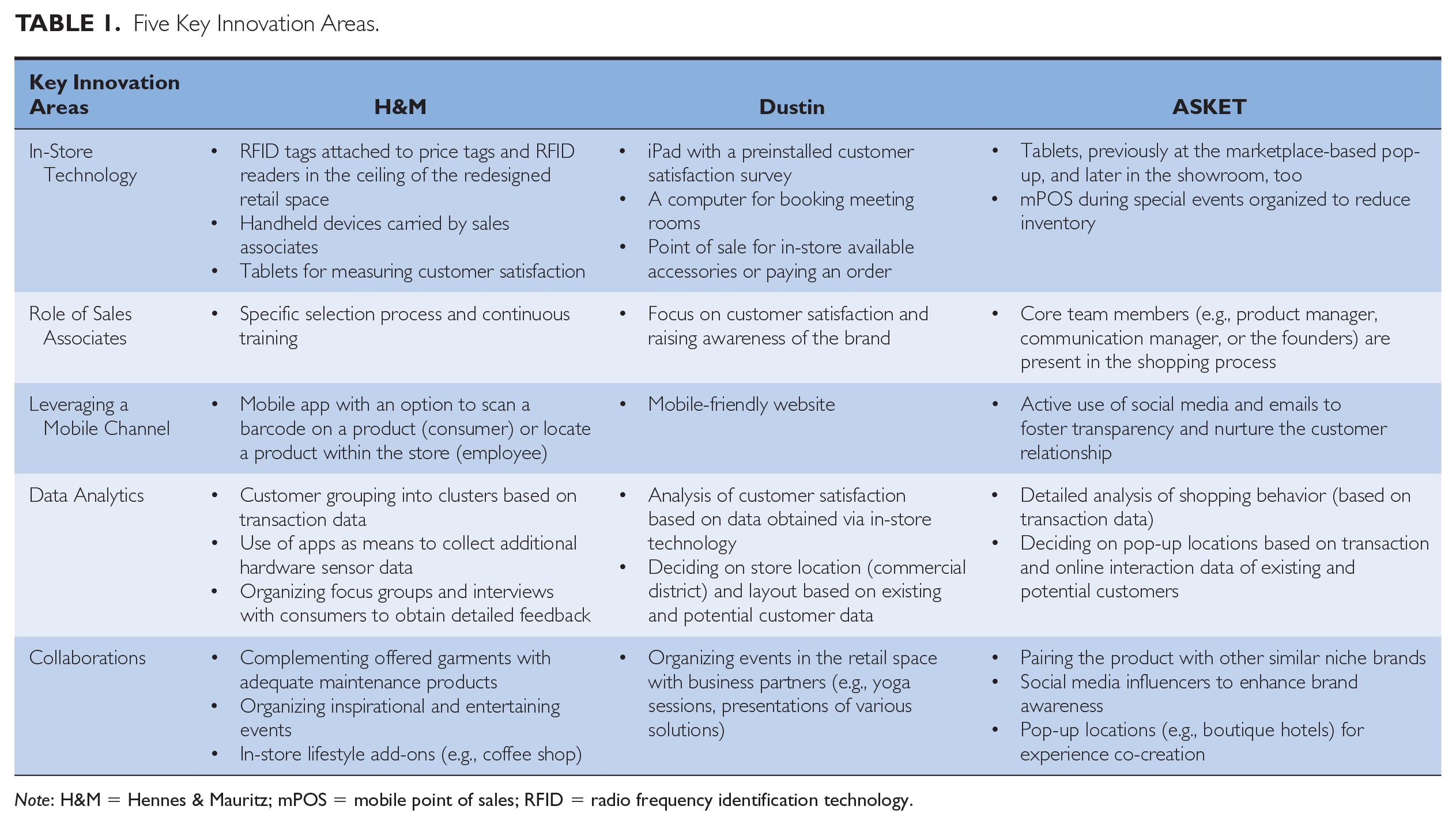

There are five key innovation areas that drive the revamping of physical retail spaces in the transition to omnichannel retailing: in-store technology, the role of sales associates, leveraging a mobile channel, data analytics, and collaborations. These areas and their interplay are the cornerstone of the changing physical retail space that connects various touchpoints (physical and digital) and that requires business model innovation that is not channel-based but rather spans all retailer-customer interaction points. The interrelatedness among them is depicted in Figure 1 and a comprehensive summary of the five areas across the three studied companies is provided in Table 1.

Illustration of the interrelatedness among the five key innovation areas.

Five Key Innovation Areas.

Note: H&M = Hennes & Mauritz; mPOS = mobile point of sales; RFID = radio frequency identification technology.

In-Store Technology

One of the key areas explored predominantly by H&M is the use of in-store technology. While, in the other two cases, there has only been evidence of the use of iPads to collect feedback (Dustin) or make an online order (ASKET), H&M puts a significant emphasis on the use of in-store digital technologies to create value for customers.

First, H&M uses RFID that allows operational improvements. Tracking the products with an RFID tag helps improve product availability and inventory control, and could potentially help with theft control as well. Monitoring can be done automatically using the RFID devices on the ceiling of the new concept store or with handheld machines used by employees. The employees usually use the app to help customers locate the products they are looking for—thus taking on an enabler role, a role that has arisen in recent years through interrelatedness with in-store technology (Figure 1). In other words, sales associates enable consumers to smoothly interact with the technology or help them to overcome potential challenges. Furthermore, the technology is primarily used for stock availability—to have better traceability of where the garments are and to know what quantity of a particular product is in the store. This is important because only a limited number of products can be kept on display at this store so as not to clutter the space and to give the store an airy feel. In this case, RFID technology enables H&M to fulfill its value proposition in terms of the design and purpose of the physical retail space. However, RFID technology can also be used in three additional use cases that have not been explored further. These are used in dressing rooms as a security measure, tracking the movements of customers across the store while carrying the products, and integrating the technology into the point of sale (POS) to speed up the process of purchasing and ease the workload of sales associates. These use cases are valid sources for increasing operational efficiency and capturing value.

Second, all H&M sales associates in the new concept store have handheld devices with which they can help customers find the product within the store, order products to be delivered to that store (click & collect) or to the customer’s home, and—if the customer is in the changing room—make a payment. In collaboration with the fintech company iZettle, it is possible to purchase a particular product directly in the changing room via a mobile POS (mPOS). On the same note, Dustin’s first-line employees can also help with the order and have the products delivered to the store or to the customer’s office, while ASKET generally does not support in-store sales or deliveries to their pop-up location. In addition, Dustin’s concept store features a computer that can be used by customers to book a meeting room.

The Role of Sales Associates

Dustin puts a lot of emphasis on its employees, training them both on different available vendor products and on solutions created by the company itself. In the physical concept store, it is not sales that are measured, because these numbers are significantly lower than the ones from the online store, but rather customer satisfaction and store experience. This is why employees are trained to provide a high level of customer experience and to communicate the company’s message that the physical location should be thought of as an inspirational place where customers can always come to work or use meeting rooms for an off-site meeting. In addition, Dustin has a stronger relationship with certain vendors, so those vendors also organize training for the sales associates to understand the products they are selling. In turn, they influence the sales associates’ roles as they become evangelists for that product.

ASKET always has one of the core team members available in the showroom to introduce the brand to the customer and build customer relationships. However, the situation was different during a period when the brand was present at a marketplace-based pop-up store. Therefore, sales associates were employed to work permanently at the location and for all exhibited brands equally. ASKET’s owners only had half an hour to train those members of staff, and therefore, it felt a little uncomfortable giving away ownership of the customer touchpoint to the collaborating firm. This is an exceptional case because on all other occasions, and at all other pop-up locations, properly trained staff were present. However, this explains how owning the narrative and communicating with the customer, especially when the story of the product is a key element of the offering, is important to completing the picture of the brand and to engaging and inspiring the customer.

Finally, the people who manage the H&M concept store had a particular hiring process. In addition to well-established hiring criteria, job applicants needed to have a passion for “perfect customer experience” and be versed in digital technology so as to be able to enable customers to use their mobile devices for in-store shopping or interaction with in-store technology. Moreover, the recurring training of sales associates is done differently in comparison with the training provided for sales associates of other stores. In addition, these sales associates are there (be it in the open space or in the changing rooms) to give advice and suggestions about the fit of a particular garment, sometimes referring to previous purchases and offering personalized suggestions.

Leveraging a Mobile Channel

The use of a mobile channel was seen to encompass communicational and transactional aspects of the retailer-customer interaction. On one hand, the mobile channel serves as a medium for customers to exchange information with retailers and other customers via social media, while on the other, it serves as a platform for the development of a mobile app that can be a tool to save an item in a “favorites” folder or make a purchase. Different practices and levels of attention given to the mobile channel were observed in each of the case companies. ASKET focuses solely on social media in order to increase the transparency of the production process and to give customers a chance to meet the people behind the brand. Its co-founders revealed that most of the retailer-customer interactions that they can measure originate from customers’ mobile devices, while the majority of the completed purchases are still made in a desktop environment. They leverage the mobile channel to reach their customers, but they had to change their payment partner to a major Swedish fintech company in order to provide frictionless mobile checkout and to increase the conversion rate on mobile devices. This was done to streamline the purchasing stage of the customer journey and to have a global solution and a unique payment provider as a partner.

Unlike ASKET, which predominantly uses a mobile channel for communication purposes, H&M in its 2017 annual report stated that it would like to continue to develop its mobile app so that it can be used for transactional purposes as well. Part of H&M’s strategy is to develop the mobile app and use it as a key resource in all applicable business aspects, but as their representative stated, multiple things have to be sorted out “under the hood” first. Furthermore, leveraging a mobile channel and enabling customers to use their mobile devices—for example, to finish the purchase (which started in-store) online or to locate a product within the physical store—are an important add-on for retailing, especially for established, global retailers. Conversely, Dustin has discontinued its app since in a B2B environment face-to-face communication proved to be essential for customer engagement. 28 Nevertheless, as Dustin’s respondent admits, there is a dedicated team working on an online presence in a desktop environment, which has been increasingly refocusing on a mobile presence.

Moreover, the findings suggest that the checkout process—either with customers’ devices or with mPOS devices carried by sales associates—can help to increase operational efficiency and customer effectiveness, in turn contributing to both value creation and value appropriation. Dustin’s concept store features a cashier desk where customers can get advice on products and place an online order, ASKET utilizes the iZettle solution at special events (because, under normal conditions, purchases are not possible at the physical location), and H&M has the same mPOS solution (i.e., iZettle) in the changing rooms of the concept store (for the greater convenience of its customers). In this way, additional value can be created by leveraging mobile technology (i.e., mPOS). This changes in-store activities (see Figure 1), and value may be appropriated through the optimized use of retailers’ resources by minimizing in-store assistance in favor of self-service via mobile devices.

Data Analytics

Customer data analytics can be a powerful tool for understanding their shopping behavior and can provide insights into where to open a concept store (as in the case of Dustin) or to join a marketplace-based pop-up store (as in the case of ASKET). Dustin carried out its own research and, based on the results, decided where to open its concept store. Similarly, ASKET’s managers analyzed where their potential and existing customers work and live and thus decided to exhibit their products in a marketplace-based permanent pop-up location, directly changing the activities related to business collaborations (see Figure 1). Moreover, analyzing customer data can be used to create offerings that are more relevant, or to develop a product. For example, Dustin’s sales associates leverage data analytics to understand whether the customers have fixed working desks or are mainly mobile, or whether they have grown as a company and need a different solution. ASKET uses its network of influencers and loyal customers to try out the first release of a new product, it collects feedback, and then it updates its collection and organizes a sale on the “outdated” products. Furthermore, thanks to its large number of customers, H&M is able to collect a massive amount of customer-generated data through its online and mobile touchpoints. What is used currently is mainly transactional data in order to classify customers into groups, but not yet to cater to individual behaviors and needs. For example, H&M’s customers might expect recommendations on the web or in the mobile app that are based on purchases made by other customers with similar interests. Additional profiling is possible through the loyalty club, which has a long tradition in Sweden and has recently been digitized and embedded into the mobile app. The intention with this is to offer relevant products based on both inspirational suggestions by fashion designers and the customer’s previous purchases. However, the findings point out that the process of profiling and related data analytics needs to be further developed.

In light of these observations, there are three particular types of individual customer data that retailers can collect for data analytics and for understanding customer behaviors and values. The first and most common are transactional data that originate in the act of making a purchase. Depending on the means and location of payment, different information is shared with the retailer (e.g., the billing address). Then, the hardware sensor data can be collected via sensors on personal mobile devices (e.g., the location of the customer, mobile payment, and customer journey) or via RFID sensors placed in physical retail spaces and/or on products. Finally, the most descriptive and insightful data come from the customers themselves—observing their in-store behavior, organizing panel sessions or interviews, and looking into the answers that they provide on in-store devices with preinstalled customer satisfaction surveys. These data can be collected via different retail-customer interactions (e.g., in-store, online, or mobile app—as depicted in Figure 1). Among these, in-store-generated data are the least utilized and thus have the highest opportunity to contribute to business development.

Another interesting aspect to be considered is the action that can be taken as a result of data analytics. During the interviews, two terms kept coming up: “personalization” and “relevance.” While the first is more in line with sending personalized emails to customers or helping the customer in a personal way, the second is about offering what the customer wants to buy in an engaging and interesting way. 29 Although the interviewees highlighted offering relevant products to customers, personalization also has potential, especially because there has been less focus on personalization within combined mobile and in-store experiences and because it can actually prove to be a useful tool for being relevant. Therefore, there is an opportunity to exploit a tactic where, for example, a sales associate would have much more information on the customer (e.g., previous purchases, wish list, and typically worn size) provided through data analytics and could therefore be able to offer a more relevant product. This would mean, however, that all sales associates would need to develop digital skills and be able to leverage technology to provide such personalized services. In addition, such services could also be used to maintain a connection with the customer, in addition to established means, such as emails, invitations to events, and push notifications through the app.

Collaborations

Each of the businesses has relied on partnerships with different actors in order to be able to deliver the proposed value. For example, ASKET collaborated with various hotels in different cities during a pop-up tour. Hotels would provide a location, for example, a room that would be turned into a retail space, and ASKET would invite influencers to spread the word and join the pop-up tour. These collaborations worked well for ASKET because they enabled them to have temporary showrooms in the cities where they already had interested customers. In addition, there are a few other brands that complement ASKET’s offering, so sometimes they feature each other on social media or are present at the same marketplace-based pop-up in order to enhance each other’s value proposition. At these marketplace-based locations, the store layout and in-store technology are controlled by the facilitators of the physical retail space (ASKET’s collaborators), which exemplifies the influence such partnerships have on the activities related to in-store technology (which would otherwise be controlled by ASKET at its location). Figure 1 depicts this interrelatedness.

As a way to complement its offerings and increase revenue, Dustin had events organized by different vendors. After expressing interest in presenting a new product or a service, vendors were given a time slot to organize an engaging event (e.g., a yoga session). This situation is a “win-win” for both parties. On one hand, it gives vendors an additional touchpoint and a moment of interaction at a prime location in the city and at a unique store that is highly focused on SMEs. On the other hand, it gives Dustin an opportunity to increase brand awareness among customers and to show that the physical store is not a traditional store, but rather an inspirational location.

Finally, H&M’s focus in their concept store is on the customer experience—superior assistance and offering a relevant product range (not only H&M’s products). For example, if there is a delicate piece of clothing, customers can buy environmentally friendly laundry products or a steamer. Prints from a local photography museum or flowers can also be bought, and there is a coffee shop within the store. All these features, along with a few organized events, are unique in this store and are there to create an inspirational shopping environment.

Business Model Innovation for Omnichannel Retailing

Traditional retail practices are under stress, and as a response, many retailers are beginning to integrate physical interaction points with those available in the digital space, thus changing the nature of retailing. Such a change requires previous business models to adapt and transform into models that blur the lines between the physical and digital worlds, and it is in such models that the physical retail space emerges as an inspirational and experience-based hub that aggregates all available customer touchpoints.

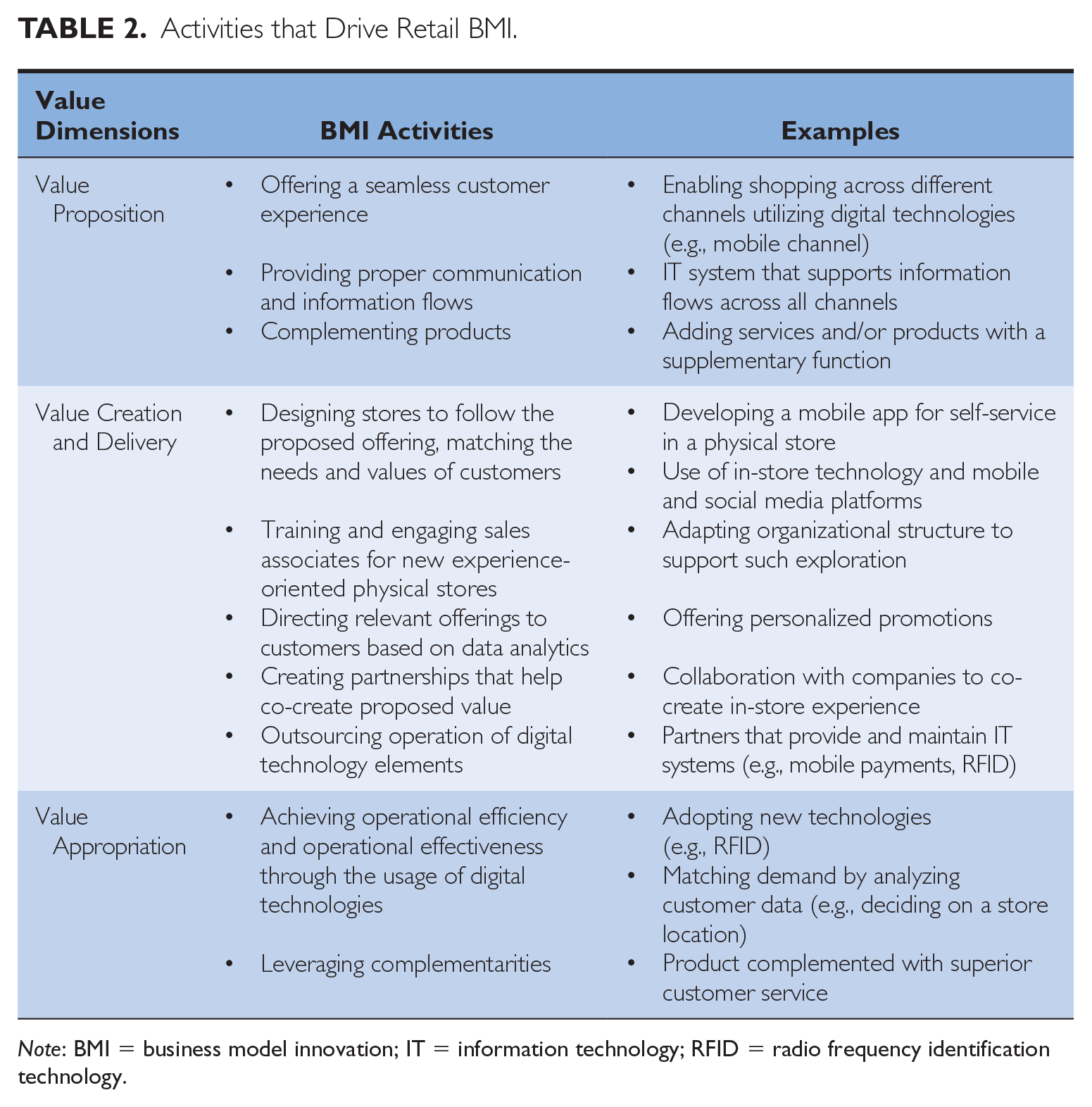

In order to make such changes, the five key innovation areas need to be explored in the process of revamping physical retail spaces. Although some authors have emphasized individual areas related to the future of brick-and-mortar stores, 30 this study puts them together, highlighting the interrelatedness among them as a critical factor toward understanding business model innovation in retailing. The activities and examples that drive this shift in a retailer’s value architecture (i.e., its business model) are presented in Table 2.

Activities that Drive Retail BMI.

Note: BMI = business model innovation; IT = information technology; RFID = radio frequency identification technology.

As has been suggested, the value architecture shift is driven by the changing nature and purpose of the physical stores into hubs that aggregate various customer touchpoints and foster seamless customer experience. A part of that shift is the customer value proposition, which is no longer only the product, but rather an experience that surrounds that product. Characterized by the very how things are sold, this experience is changing mainly due to greater levels of employee attentiveness and the use of digital technologies.

The first is attributed to additional and specific training for sales associates or the founders’ passion for the product (in the case of a startup). If the employees are engaged, they will develop a sense of belonging and thus become evangelists for the brand. This engagement leads to a greater focus on customers and the creation of a unique experience across both physical and digital retail spaces. This is emphasized by the transformation in employees’ roles, which should be in line with the pursued omnichannel strategies. The second driver, the use of digital technologies, refers to the use of the back-end integration of the information systems to enable front-end technology (e.g., mPOS, RFID tags, and iPads) to be used by first-line employees and by customers. For example, this allows the customer to check the availability of a particular product (in an online or another physical store) by scanning a barcode or to locate the product within the store (thanks to an RFID map). Such human-computer interactions were envisioned years ago 31 but have only recently been enabled by retailers. On one hand, they provide a source of value appropriation through operational efficiency, while on the other, they can make building relationships with customers more difficult unless the sales associates are trained on how to leverage in-store technology to improve the customer experience. For example, sales associates could leverage customers’ data collected through in-store sensors (e.g., RFID) or through their mobile devices in order to provide a seamless experience highlighting the understanding of the customers’ general shopping preferences.

Moreover, part of this experience is also to challenge what is being sold. Complementing the product range with supplementary products (e.g., laundry products in a fashion store) or with services (e.g., computer maintenance) is also changing the core of the customer value proposition (see Table 2). Such changes provide an empirical support for the ongoing discussion 32 regarding the role of complementarities in business model innovation.

These innovations in the value proposition, which follow the revamping of physical retail spaces, are accompanied by adapted activities for value creation and appropriation. The value creation includes all the activities and resources that the retailer needs to have or to develop through collaboration in order to co-create and deliver the proposed value for the customer. Table 2 highlights three business model innovation activities that follow the previously mentioned value proposition changes. First, retailers can leverage mobile technologies to create a seamless customer experience, for example, by developing a mobile app that a customer can use purposefully within a physical store or by installing in-store technology to support both information flow and retail operations. Second, the store staff training needs to be planned and executed with the support of managers higher up in the organization (in the case of large firms). Startup staff have an intimate and dedicated role in communication and in building customer relationships. Third, the collection and use of customer data from both physical and digital retail spaces should be fostered so as to understand the customer and to make data-driven decisions.

In order to deliver the proposed value, the biggest development is seen in the governance element of the retail business model, where partnerships with different actors can be observed. These can be collaborations in order to co-create the proposed value (e.g., hotels as locations for pop-up stores) or to outsource the operations of a technological system (e.g., RFID in the case of H&M or the mobile checkout process in the case of ASKET). These considerations are an integral part of a retailer’s business model and are key to enabling a business network that supports the new proposed value in a shift to omnichannel retailing.

None of the above-mentioned changes would be reasonable without adequate value appropriation, that is, a financial perspective to follow such changes. The findings presented here suggest that brick-and-mortar retailers can benefit from operational efficiency and effectiveness by adopting new technologies (e.g., RFID, mPOS) and developing data analytics capabilities. The first would lead to lowering the costs for a retailer, and the second to a better understanding of customers’ needs so as to be able to match them, and thus potentially lead to increased revenues. 33 In addition, when developing new mobile apps for customers to (eventually) use in all the stores, staff need to be appropriately trained to understand and use digital devices in order to complement the product offering with advanced customer service. Furthermore, there is a potential to increase revenues for purely online retailers that venture into having showrooms, with increased attentiveness of staff and high product quality that emphasizes transparency and sustainable production. This can be achieved, for example, by leveraging the complementarities of a premium product and a superior customer experience based on the aforementioned production process and in-store assistance.

Finally, these findings contribute to the retail management literature by addressing a gap in our understanding of business model innovation concerning the changing nature and purpose of physical retail space. As such, the findings presented here offer a way to see business model innovation opportunities through the five key innovation areas that span physical and digital retail spaces. Moreover, as inferred from Table 2, the new offerings are based on redesigned formats of physical stores. Sometimes equipped with in-store technology and sometimes serving as low-tech showrooms, physical retail spaces have become hubs that aggregate different channels and facilitate shopping across various touchpoints, ultimately offering an omnichannel experience for customers. This experience would not be possible without in-store and mobile technology that allows retailers to collect customer data from both physical and digital environments and thus inform their decisions and activity changes through data analytics.

Managerial Implications: Thinking about the Physical Retail Space as an Aggregation Hub

The quest for a physical retail space that matches customers’ needs and values is not a straightforward journey. Retailers need to embrace an experimental approach, testing several possible physical store formats during their transition to an omnichannel business model. However, this process of step-by-step exploration will depend on the starting point, that is, the availability of the physical location (brick and mortar or natively online) and the customer base (B2C or B2B). Therefore, an understanding of the current retail industry dynamics, the competitors’ activities, and customer characteristics (e.g., their locations, needs, and shopping behavior patterns) is necessary in order to formulate the initial purpose of the revamped physical retail space (i.e., the role it has within the overarching omnichannel business model). This role might be communicational, where the intention is to create brand awareness and test various locations, or experiential where one would aim to present shopping in a more engaging manner (possibly at a previously existing retail space).

Nevertheless, the purpose should not be seen as set in stone, but rather should be adapted by constantly observing customers’ reactions. As mentioned, the exploration process will depend on whether a retailer already has a physical space with which to explore different store formats that support the envisioned purpose, or whether it needs a new space and thus needs to collaborate with different location owners (e.g., marketplace-based pop-ups or hotels). Moreover, the customer segment (B2B or B2C) will determine the type of interaction that is planned within the store and thus the roles that sales associates will take.

In conclusion, all of these adaptations and the changing nature of the physical stores have consequences for retailers’ established business models. The revamping of the stores envisions the physical retail space as an aggregation hub that connects various touchpoints and thus requires business model innovation that is not channel-based but rather spans across all mediums of interaction (both physical and digital). Therefore, retailers need to redesign the value architecture of the firm by integrating new ways of doing things with the old ways. Namely, they should

restructure departments and establish positions for managers who will guide the organization in line with its omnichannel strategy;

carefully plan customer interfaces across all channels and touchpoints to foster a seamless and inspiring customer experience that matches customers’ needs and values; and

train sales associates in line with the revamped nature and purpose of a physical retail space.

In summary, retailers need to adopt a customer-centric approach, matching contemporary customers’ needs and values with the help of analytics of data collected from both physical and digital retail spaces.

Footnotes

Acknowledgements

The author is grateful to the guest editors, anonymous reviewers, and Prof. David Vogel for constructive guidance during the review process. I would like to thank Dr. Emrah Karakaya for his helpful comments on the earlier version of this work and express my deep appreciation to Dr. Marin Jovanović for his ideas and our scholarly discussions. Finally, I gratefully acknowledge the expert informants without whose input this research would not be possible.

Funding

The author(s) received financial support for the research, authorship, and/or publication of this article: This work is part of the EMJD European Doctorate in Industrial Management (EDIM) funded by the European Commission under the Erasmus Mundus Action 1 program.

Notes

Author Biography

Milan Jocevski holds a double PhD degree in Industrial Engineering and Management from the KTH Royal Institute of Technology (Sweden) and Politecnico di Milano, Italy (email: