Abstract

In the backdrop of COVID-19-induced geo-political backlash against China, the article makes an assessment of the nature of economic interdependence of South Asian nations with China. Though COVID-19-induced lockdown led to a decline in trade with China, it recovered quickly in subsequent months. In the case of India, even after imposing restrictive measures, trade with China was found to bounce back indicating to a greater dependence on China. Further, asymmetry in economic engagement with China could be observed for several of the South Asian nations. Chinese investment in the region remained muted during the pandemic. However, strategic involvement in South Asia by China, and other powers, increased considerably which has been manifested by her provisioning of economic incentives and COVID-19-related aid. In the light of increasing strategic influence, South Asian countries desirous of benefitting from foreign trade and investment in their respective economies will need to encourage free and fair competition rather than towing geo-political lines so that sustainable economic gains can be made, which will require strengthening of various market supporting institutions in the respective economies. India’s economic strategy will also assume significance in boosting confidence and increasing the level of integration within South Asia.

Introduction

Amid the COVID-19 pandemic, the geo-political importance of South Asia has increased substantially. Not only have the great powers shown interest in dealing with South Asian countries but also taken steps to exert economic and strategic influence. China continues to play a significant role in South Asia through trade, investment, development aid, cultural and strategic engagements.

In the economic space, South Asia contains world’s sixth largest economy (in terms of dollar GDP) and some of the smallest economies. However, GDP per capita (in 2019) of South Asian countries ranged from USD 502 (Afghanistan) to USD 10,791 (Maldives). The two largest economies, India and Bangladesh, of the region had GDP per capita of USD 2,104 and USD 1,855, respectively. COVID-19 has had severe impact on most of the economies. Due to COVID-19, per capita income in India fell in 2020 below that of Bangladesh. Further, K-shape recovery (which implies rich recovering quickly whereas poor continues to suffer) is expected in many of these economies, whereas V-shaped recovery in South Asia could be hampered by weak global demand and business uncertainty (Wignaraja et al. 2020).Such a recovery is driven by dependence on low-skill and contract-intensive manufacturing and services, uneven progress in COVID-19 vaccination, digital and technology divide and economic capability gaps (UN ESCAP 2021). Further, economic integration in South Asia is one of the lowest in the world with intra-regional trade at 5.6% of total trade in 2017 (Banik and Gilbert 2008; Hashim and Razzaque 2016; Sinha and Sareen 2020). The region is marked by poor logistics and high trade cost.

It is observed that China’s presence in South Asia has got a boost, especially through BRI. It has lent money to countries participating in the connectivity initiative. However, there are serious concerns over debt-trap experienced in countries such as Maldives and Sri Lanka. To boost its presence, China seems to have a pragmatic approach towards South Asia and the World at large (Pei 2006). Such a pragmatic mode of engagement throws up a challenge for India’s neighbourhood policy, wherein the neighbouring countries could play the China card against India (IDSA 2019). China is seen to offer concession (even bail out) for bolstering its presence in the region.

With the changing geo-political scenario at the global scale, South Asian countries are confronted with balancing the relations with powerful countries such as China and the USA. The presence of India, a large economy and an emerging power, in the region adds further dynamism in both economic and geo-political fronts. In this article, we examine the economic and geo-political relationship of South Asian countries with China in the context of changing regional and global scenario. In particular, we first review the economic relationship and programmes, and discuss strategic alignments of these countries. Finally, we discuss the implications for South Asian integration in the presence of the China factor.

The narrative structure of the article is as follows. Although India is a pre-eminent force in South Asia but she has not fully engaged with the region despite economic rise and proximity. While India’s healthy relationship with some of the South Asian countries has slipped, China has made inroads into these countries in South Asia through implementation of several projects, but there are allegedly many concerns about the contractual practices. As a result, there has been a strategic reinvigoration of the South Asian region. The spread of COVID-19 pandemic across the region has further changed the nature of economic interplay with China, among others. While there was a transitory decline in the volume of trade with China immediately after COVID-19 struck these nations, a quick rebound could be observed albeit there persists asymmetry in bilateral exports and imports. Further, the relative share of China in South Asian nation’s exports and imports has remained intact. On the contrary, there has been a slowdown in Chinese investment in the region for a variety of reasons. This was compensated by increase in COVID-19 support by China. Nevertheless, India has been able to match China’s COVID-19 offerings in the region to a large extent that include, but not limited to, the supply of vaccines. However, growing inwardness of India’s economic strategy, for example, self-reliance pitch and lack of confidence in engaging with mega regional trade blocks, raises questions about whether India will continue to be a reliable economic partner vis-a-vis China. These aspects are discussed with a South Asian perspective and what India could do to engage better with the region, to retain confidence, and to improve the level of integration within South Asia.

The reminder of the article is organised as follows. South Asia’s economic engagement (both trade and investment) with China is discussed in the second section . COVID-19-related development aid to South Asia by China and India is discussed in the third section. Strategic reinvigoration of South Asia is discussed in the fourth section. Implication for South Asian integration is discussed in the fifth section.

Economic Relationship with China

Covid-19 and Dip in Trade?

There are two forces at work behind changes in volume of trade during COVID-19. First, lockdown induced a reduction in trade of every country due to logistical challenges. Second, some of the countries started reducing trade dependence on China following economic and emotional blockage on account of opaque handling of the virus outbreak. Due to these forces, South Asian nations have experienced varying degrees of consistency in the trade relation with China.

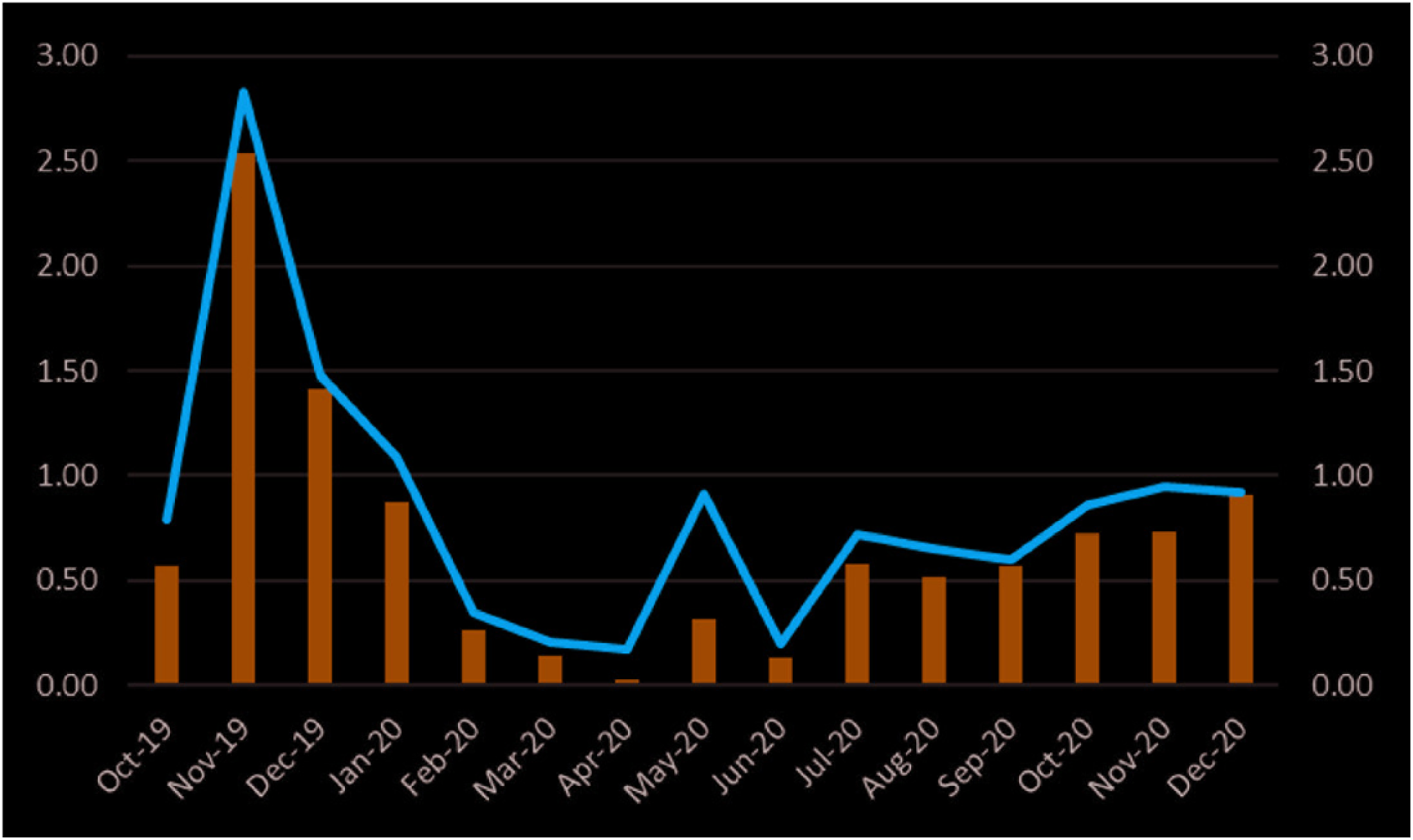

Nonetheless, India’s export to China was a pleasant surprise despite supply chain disruptions and souring of bilateral relations due to border standoff in June 2020. India exported more than what it did in the corresponding months of the previous year. Despite deadly clash between the two armies, the exports to China even after June 2020 have been exceeding the figures corresponding to the same months of the previous year (Figure 1).

On the flip side, India’s imports since of 2020 has been below the corresponding months of 2019 (Figure 2). However, the reduction in import in April–June can primarily be attributed to COVID-19-induced lockdown in India when economic activities came to a halt due to the strictest lockdown imposed by the central government. Since May 2020, India embarked on a Self-reliant India Movement (Atmanirbhar Bharat). The July to September (2020) imports remained below the corresponding month the previous year but the gap was much smaller since it was hard to undo import dependence in a short span of time, where China accounted for more than 80% of those imports in several segments. Import dependence on China has remained higher in sectors such as pharmaceuticals (Palit and Khun 2020; RIS 2015), electronics, etc. It may be seen that India introduced production-linked incentive (PLI) scheme in more than 10 sectors. These sectors include (till November 2020) advanced chemistry cell battery storage, large scale electronics manufacturing, automobiles and auto-components, pharmaceuticals, telecom and networking products, textiles, food processing, Solar PV modules, white goods and speciality steel. Under the PLI scheme, eligible companies can apply to receive financial incentives 1 for a specified period subsequent to a base year (e.g., financial year 2019–20) based on incremental sales (over base year) of goods manufactured in India and covered under targeted segments. Eligible companies are subject to thresholds of incremental investment and incremental sales of manufactured goods. 2

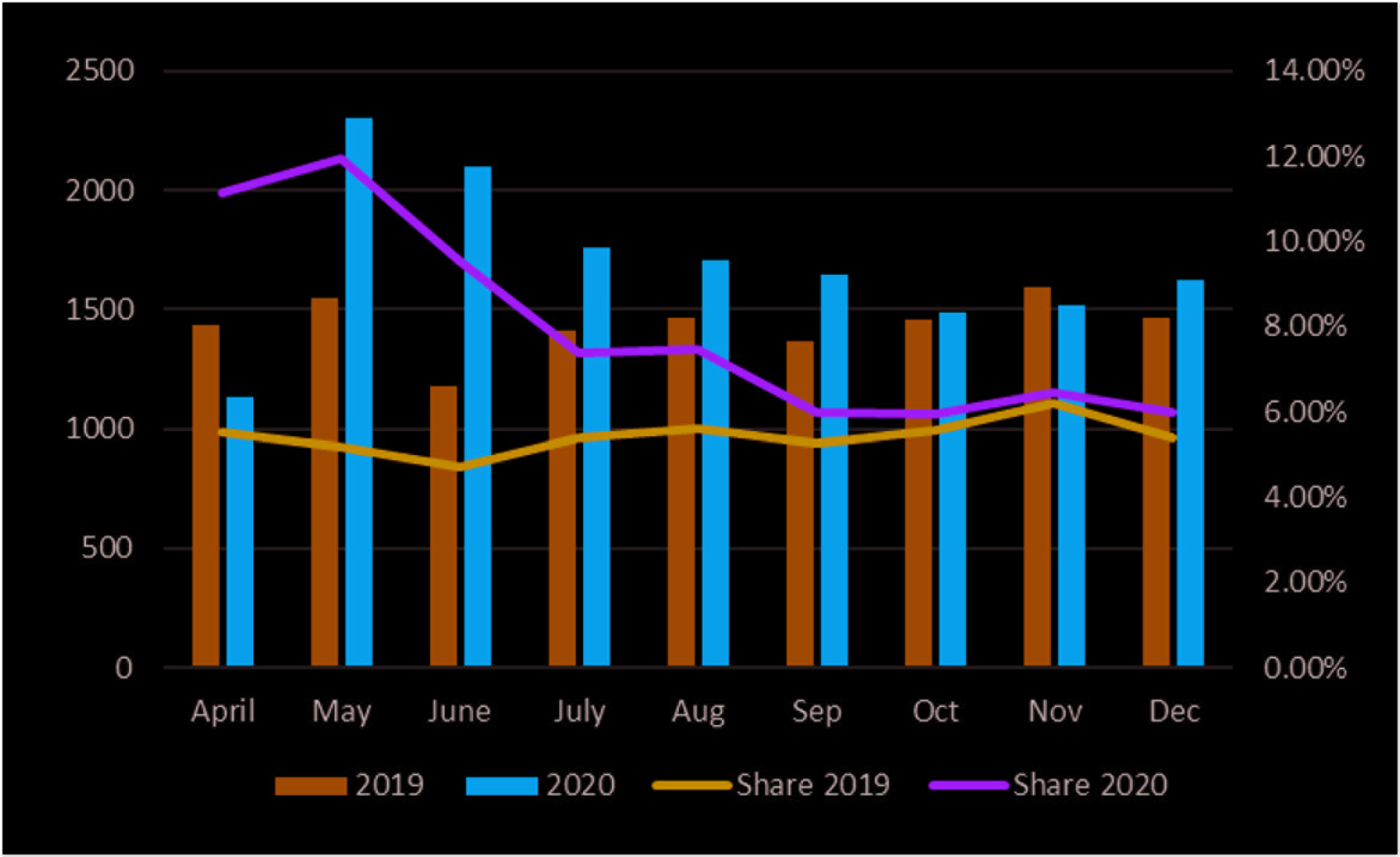

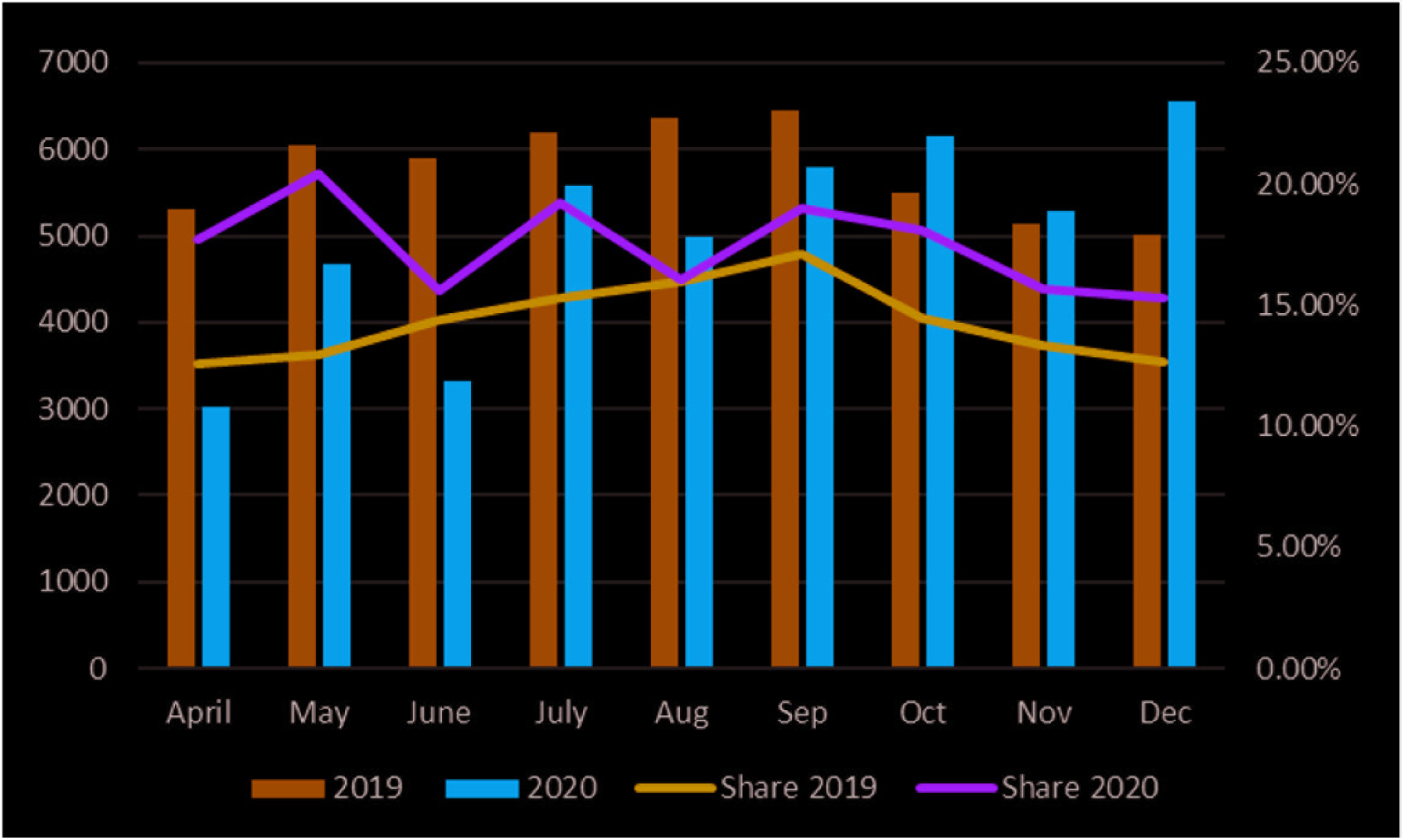

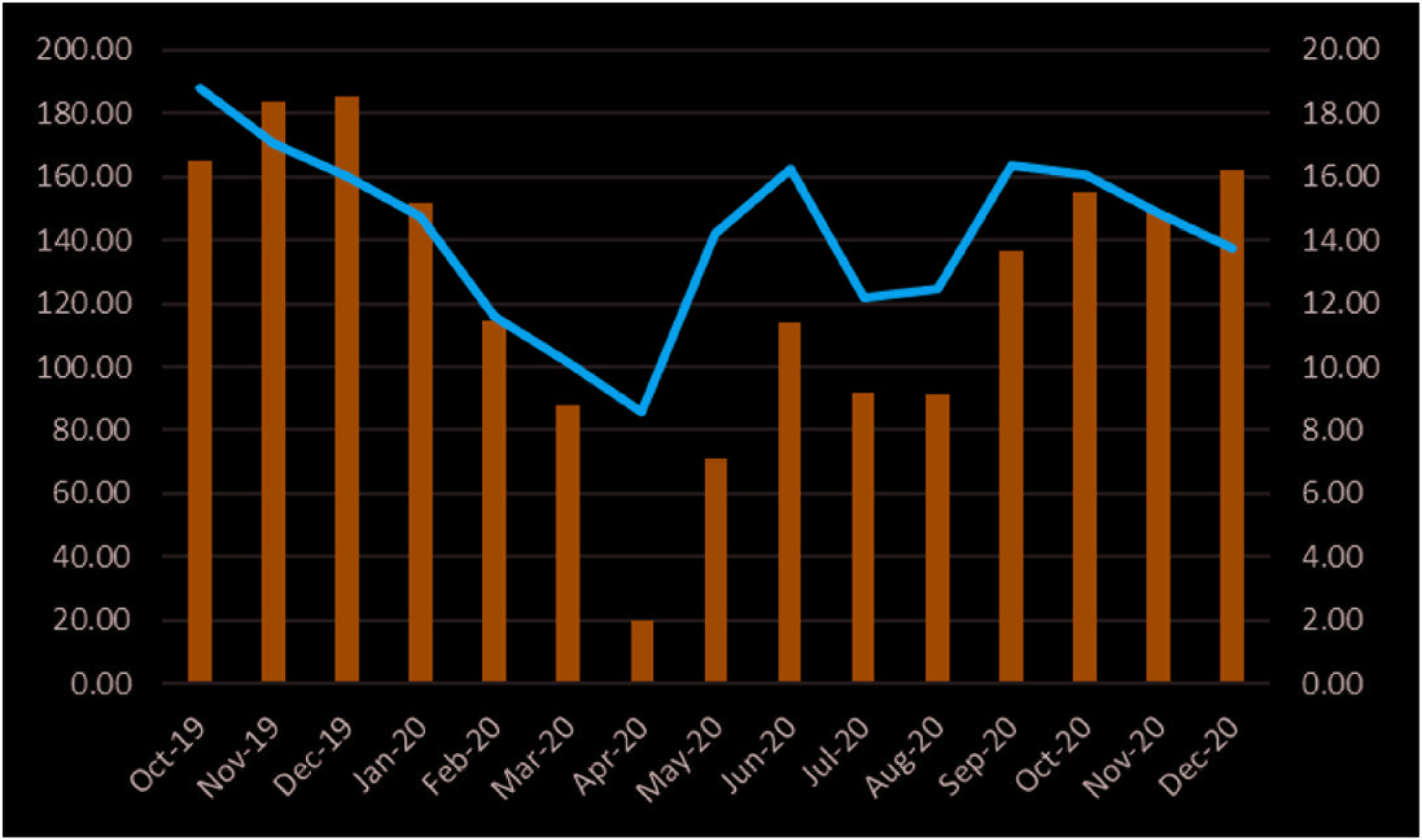

Bangladesh’s trade with China declined in April–June quarter (Figures 3 and 4). Export almost halved compared to corresponding period of the previous year. The trade volume registered an increase but remained below the corresponding quarter of the previous year. However, exports to China amounted to 1.36% of total exports from the country in July–September 2020, that is, down from 1.69% in the previous quarter. The share improved to 1.51% in the October–December quarter but remained marginally lower than the corresponding quarter of the previous year. Import too declined (by about one-third) compared to same period of the preceding year (Figure 4). In terms of share, China accounted for approximately 25% of total imports into the country since April–June 2020, which is an increase of 3% compared to the January–March 2020. This import and export shares reflect the huge asymmetry that has prevailed in the bilateral trade relations between the two countries. It can be seen that from July 2020, China offered to import from Bangladesh on duty-free basis. The move is discussed in a later section.

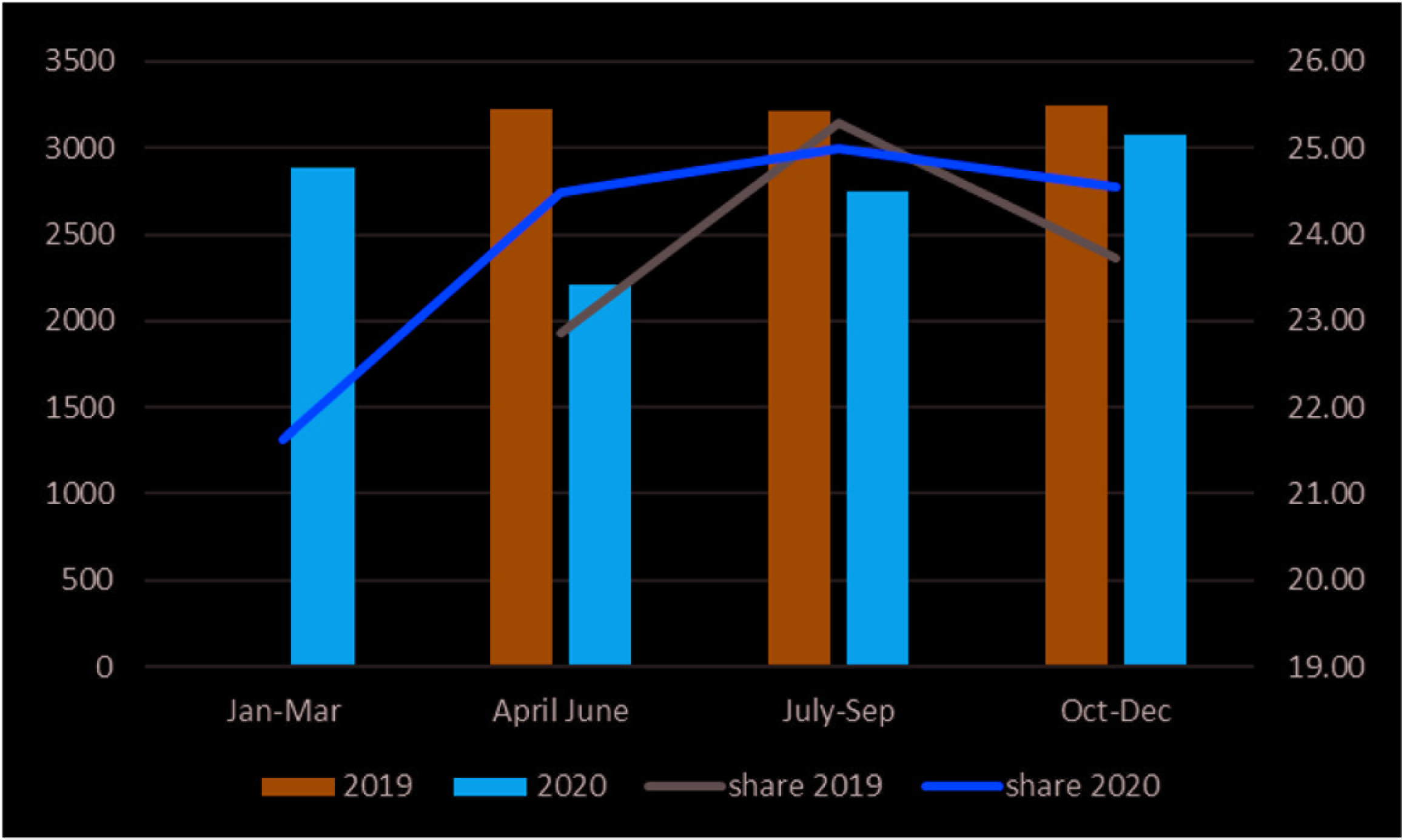

Contrary to the expectation, Nepal’s trade with China remained subdued during the first wave of COVID-19 pandemic in the first-half of 2020 (Figures 5 and 6). Imports were lowest in April but recovered quickly, whereas export showed mild recovery during July and September, that is, after a huge disruption during April and June. Further, both value and share have risen since the mid-2020 towards the pre-COVID-19 levels. However, trade asymmetry and dependence on China for imports remain a concern for Nepal too. Overall, though Nepal’s trade with China has remained below the monthly peak recorded prior to the pandemic, the latter’s share in both exports and imports has recovered from the trough, thereby maintaining her relative position as a trade partner of Nepal.

It is evident that China’s export to South Asian economies suffered during the COVID-19. While China’s exports to South Asia recovered, both in terms of volume and share (though below pre-pandemic level) with respect to the major economies of the region, imports were higher especially from India. Overall, the negative impact in the trade front is higher for the smaller economies. More importantly, trade deficit and dependency continue to be the core concerns especially for the smaller economies of the region. This implies that China will have to provide more market access to these economies to sustain the economic integration with the South Asian countries.

Covid-19 and Dip in Investment?

Chinese investment in South Asia (since 2013) can be classified into BRI-related investment and non-BRI-related investment. The former can be seen exclusively in countries that have welcomed BRI projects, whereas non-BRI-related investment can be seen in most of the South Asian countries. Among these, India has been a major recipient of non-BRI investment from Chinese investors, which is much higher than what Indian investors have invested in China (Das 2020). Before India made changes in policy (since June 2020) to discourage Chinese investment in the economy, FDI equity inflows were to the tune of 229 million in 2018–19, which was 494.75 million in 2014–15.

Other than FDI equity inflows, India received several high-value venture capital investments in the Indian start-ups. An estimate suggests that the value of such investments is close to USD 10 billion (ICS 2020). Many of them have backtracked since special regulatory changes were promulgated. These changes include introduction of land border criteria to approve FDI. The FDI policy was reviewed for curbing opportunistic takeovers/acquisitions of Indian companies in the light of COVID-19 in April 2020. This was followed by the announcement of Atmanirbhar Bharat mission in May 2020. In order to curb Chinese participation and to promote local suppliers, Indian government introduced similar land border criteria in public procurement by government organs. The banning of Chinese companies from public procurement tenders led to increased cost (e.g., BSNL case), which is based on strategic reasons rather than economic ones. Further, the standoff in Ladakh on June 15/16 of 2020 was followed by economic retaliation in the form of banning the use of Chinese applications in India during June (59 apps), July (47 apps) and September (118 apps).

Chinese investment in South Asia has been growing whereas intra-regional FDI is still very low, even though there could be strong link between trade and investment. This is evident from the fact that India, the largest economy of the region, does not figure in the top five investors in Bangladesh. Before COVID-19, China became the largest investor in Bangladesh. Out of 2.87 billion FDI in the country in 2019, China invested the highest amount (USD 625 million), followed by UK (USD 416 million), Singapore (USD 272 million), USA (USD 198 million), Norway (USD 194 million) and Netherlands (USD 192 million). However, the fiscal year (July to June) data from the country’s central bank suggest to a lower FDI volume suggesting to a fall in FDI in the January–June period as the inflow was severely affected by the COVID-19 pandemic. Gross FDI during the fiscal year was recorded at USD 147.53 million by China compared to 141.42 million by India. However, the inclusion of Hong Kong (199.89) increased Chinese FDI in the country to USD 347.42 million. There is an expectation that China’s investment could be advantageous for Bangladesh as long as regional and economic issues associated with the BRI are addressed (Saimum 2020), which makes the outcomes conditional.

Similarly, Chinese investments in Pakistan, Nepal and Sri Lanka have been significant attractions. While Chinese investment in Pakistan, particularly in the multi-billion dollar CPEC project is well-documented, Choudhury (2018) observed that there exists no bilateral direct investment between India and Pakistan. However, several investments were made by Indian companies through their overseas subsidiaries. Although there is business interest in several potential sectors in both the economies, where either side can invest, the geo-political relationship is much unfavourable between the two neighbours.

China emerged as the leading source of FDI and official development assistance in Sri Lanka. During 2005–15, funds worth USD 15 billion flew to Sri Lanka, but a majority of the flow is in the form of loans and grants (Bhatia et al. 2016). Annual FDI flow in Sri Lanka is USD 1.5 billion in 2019/20 as per Board of Investment, Sri Lanka (bifurcation not available publicly).

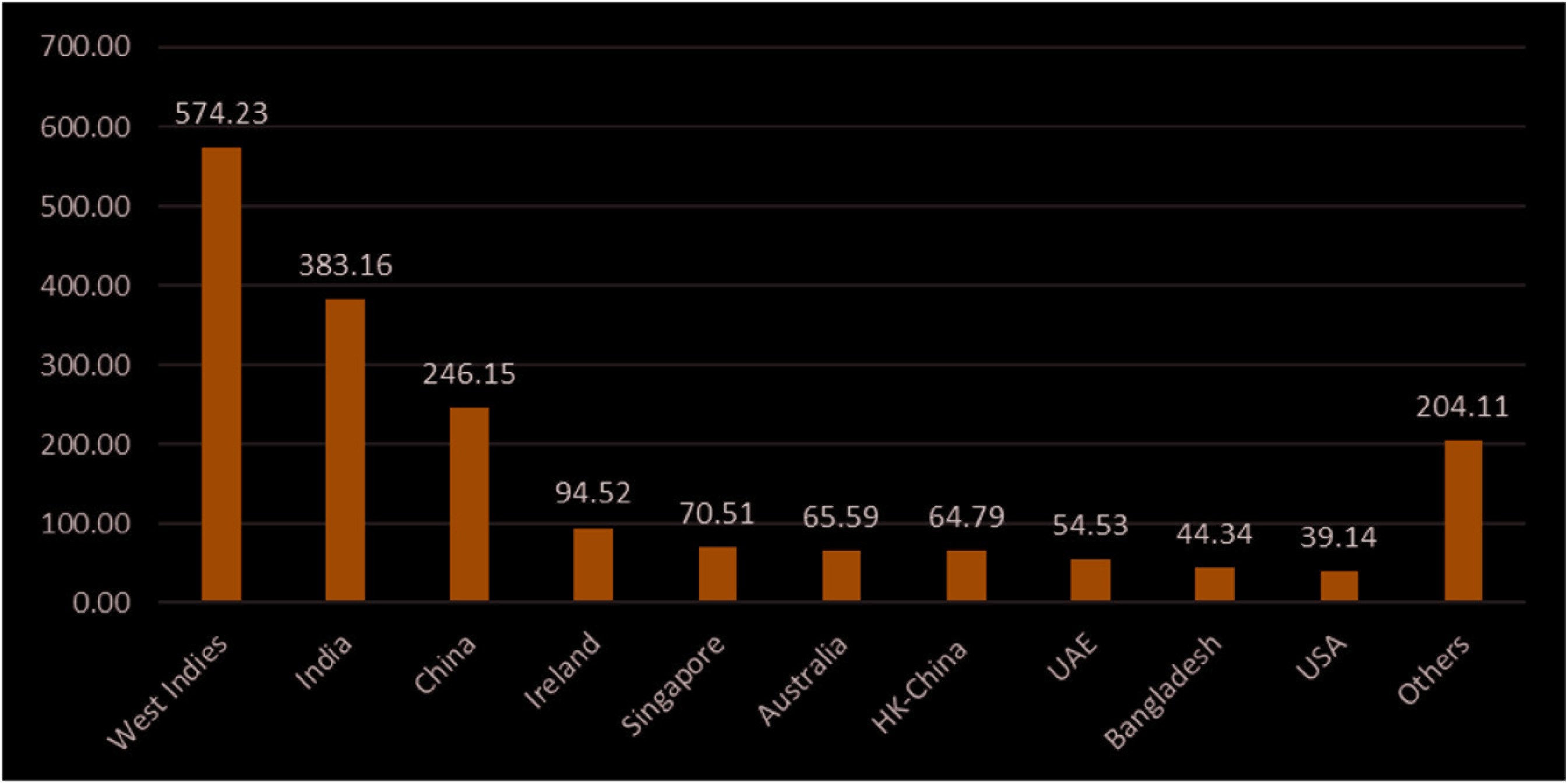

China has emerged as the third largest investor in Nepal. FDI stock in Nepal from China was USD 246.15 million till mid-2018 (Figure 7). The Stock of Indian FDI in Nepal was USD 383.16 million. West Indies appearing as the major source of FDI in Nepal is due to its offshore financial centre character, which contains jurisdictions like the Bahamas. Other than that, Nepal has received a major chunk of FDI from both India and China.

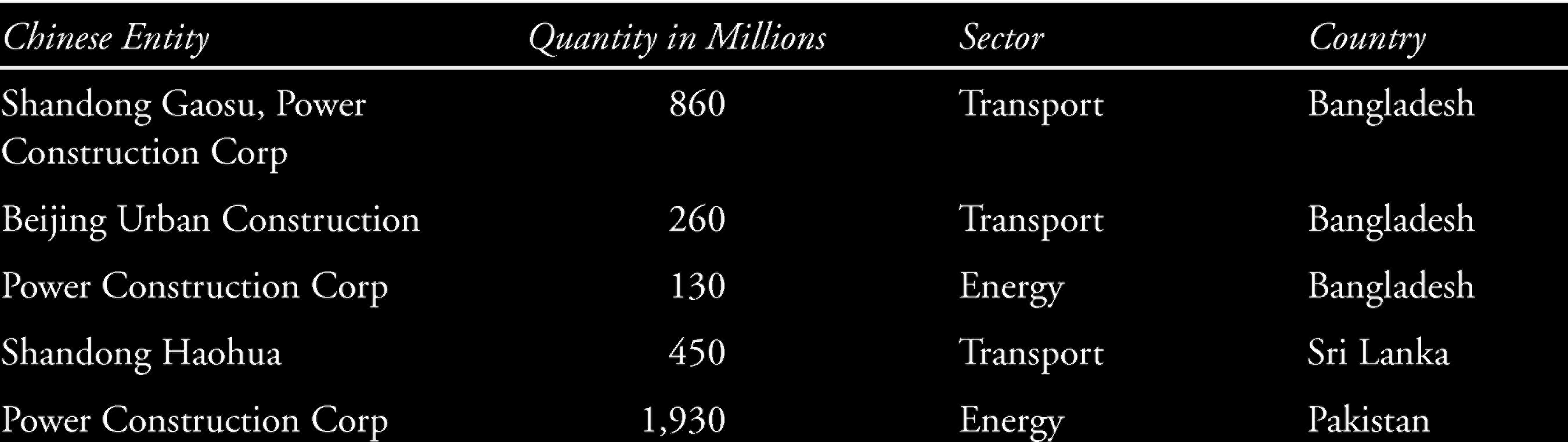

The implementation of BRI has changed China’s investment dynamics in South Asia. A look at BRI investment suggests a strong Chinese presence in South Asian countries, excepting India and Bhutan. The yearly number of BRI projects in South Asia increased from five in 2013 to 14 in 2019 (Table 1). The value of annual investment in these projects increased from USD 1.65 billion to USD 9.78 billion, respectively. While there are no BRI projects in Bhutan and India, these investments have sprawled in rest of South Asia. Till Spring 2020, the total BRI investment in South Asia is to the tune of USD 87.15 billion. Country-wise breakdown suggests that Pakistan (USD 48.16 billion) and Bangladesh (USD 24.59 billion) have received the highest amount of BRI investment (inclusive of projects developed under the China-Pakistan Economic Corridor). This is followed by Sri Lanka, Nepal and Maldives. BRI investment in Afghanistan remains negligible. China and Afghanistan’s involvement in BRI is found to be rooted in vastly different interests (Hatef and Luqiu 2017). Further, majority of projects are construction contracts (107 out of 141) which are primarily executed by Chinese firms. Investment flow to South Asia under BRI during 2013–20 was to the tune of 23.1 billion, which accounted for 26.5% of total BRI fund involving investment and construction contracts. Similar scenario prevails at the country level. For example, Pakistan received 12.86 billion as investment and 36 billion as construction contracts (a table is available upon request). Similarly, Bangladesh received 6.35 billion as investment and 18.24 billion for construction contract. However, getting Chinese finance has become more difficult for countries such as Bangladesh (Mardell 2020b). It is worth noting that investments in several South Asian countries is found to be partisan and fluctuate with political regime change (e.g., Maldives, Nepal, Sri Lanka).

BRI Investment and Construction Contracts in South Asia (2013–20) (USD millions)

BRI investment in South Asia received a setback in 2020 even in countries that favoured Chinese projects. The new investment flows declined to USD 3.63 billion involving five projects till Spring 2020 (3 in Bangladesh, 1 each in Sri Lanka and Pakistan). As before, the projects are in the area of energy and transportation (Table 2). Chinese private investment too did not flow to South Asia during COVID-19. There has been caution in allowing Chinese investment in developed countries since COVID-19 hit these economies. The USA has blacklisted several Chinese companies in its own turf. It may be noted that Chinese investment has faced completion challenges even before the BRI phase due to state ownership of businesses (Das and Banik 2015). Major Chinese investments in South Asia (with the exception of venture capital investment in India) are still led by State Owned Enterprises in sectors such as energy, telecom and transportation.

BRI Investment in South Asia in 2020 (till Spring)

A notable feature of BRI is that it is not only about trade and investment, but also about people-to-people bond (NDRC 2015). While China has encouraged people-to-people contact especially welcoming foreign students to its academic institutions, through the BRI China has spread its culture and language to many countries (Gong et al. 2020; Salem 2020). Gong et al. (2020) reported that BRI has also impacted the expansion of Chinese universities overseas along the route. In South Asia, Nepal introduced mandarin as one of the languages in its school curriculum with China’s financial assistance. On the contrary, India discouraged its higher educational institutions from collaborating with Chinese counterparts. Further, India reviewed the presence of Confucius institutes in the country.

However, when it comes to labour movement, China has gained by exporting workers to project sites and this has led to less job opportunities for the locals in many countries (Das 2018; Heydarian 2018). BRI Investment is accompanied by development assistance as it is a strategic initiative (Jacob 2017). Some of the assistance is in the form of loans while others are pure aid. During the COVID-19 pandemic, while investment remained subdued, the flow of loans and pandemic-related aid increased.

Development Assistance in South Asia

Aid Dynamics in South Asia since Covid-19?

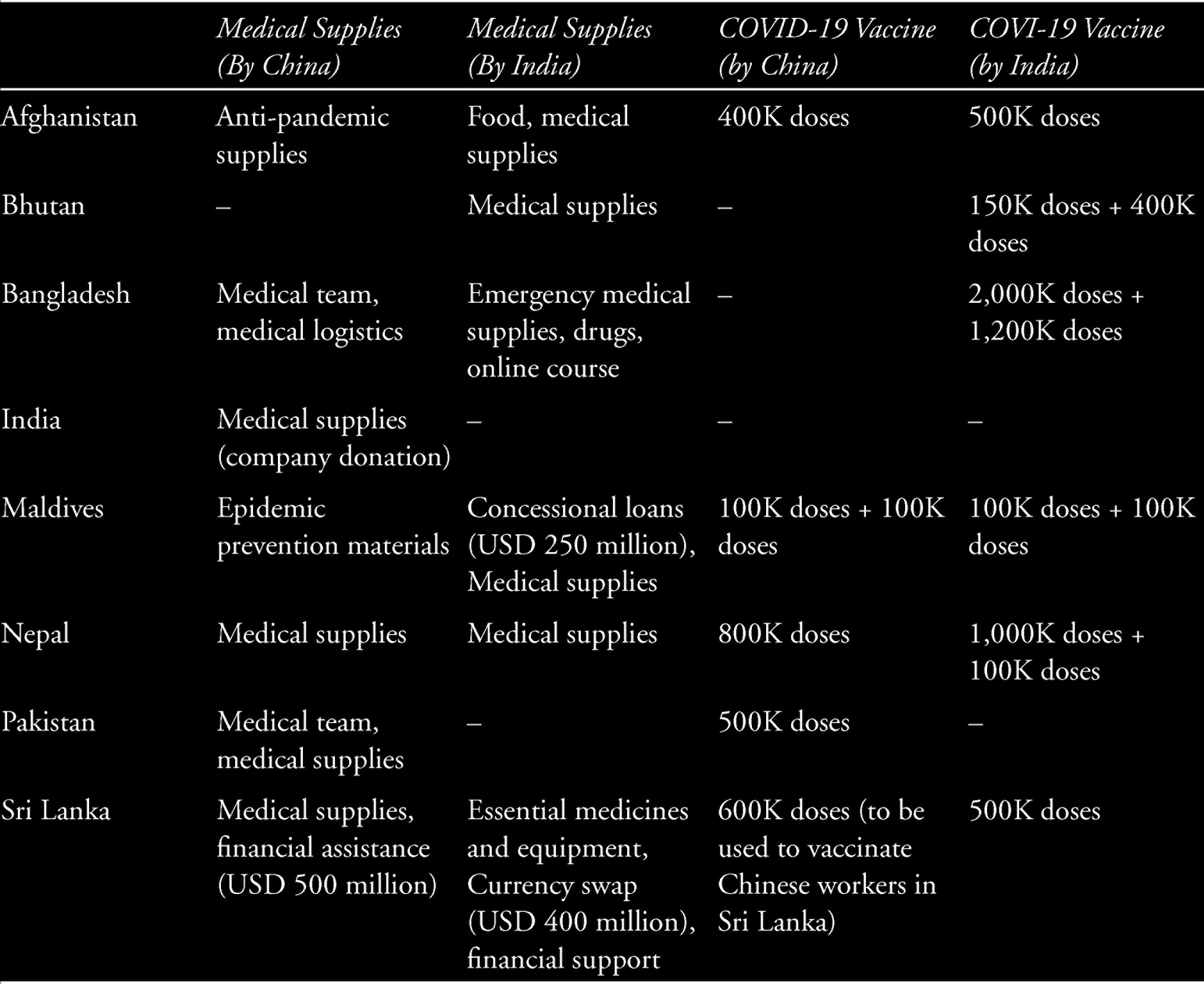

In the backdrop of COVID-19, China extended financial assistance to many countries around the world. 3 Aid to South Asia assumes special significance in the light of decline in trade and investment since COVID-19. Apart from sending medical teams and medical supplies, China offered financial assistance to some of the South Asian nations (see Table 3).

COVID-19 and Development Assistance in South Asia (till March 2021).

In March 2020, China Development Bank and Finance Ministry of Sri Lanka signed an agreement by which the island nation was given USD 500 million financial assistance to combat COVID-19. The assistance is in the form of loan and has variable interest rate. China sent 600,000 vaccine doses to the island nation primarily to vaccinate the Chinese workers living in the country.

India to Sri Lanka: India’s financial assistance to Sri Lanka was in the form of currency swap (USD 400 million). The agreement was concluded in July 2020 under the SAARC Currency Swap Framework. The repayment shall be based on fixed exchange rate agreed upon at the time of borrowing. India provided a grant of 500,000 doses of COVID-19 vaccine to the country under the Neighbourhood First policy. India to Bangladesh: India was prompt in reaching out to Bangladesh in combating COVID-19. Several tranches of emergency medical supplies were sent starting from 25 March 2020 to equip the country to fight the pandemic (under the SAARC COVID-19 Emergency Fund).

China followed suit, immediately after India’s aid reached Bangladesh on 26 March 2020. China sent a medical team and provided medical supplies to Bangladesh. However, plan to conduct clinical trials of vaccine developed by Chinese company (Sinovac Biotech Ltd.) was met with controversy over the financial resource contribution.

China provided assistance to Nepal to fight COVID-19. These were in the form of medical supplies. India assisted Nepal by providing various medicines and equipment to fight COVID-19. In April 2020, Indian ambassador to Nepal handed over 23 tonnes of essential medicines. In May 2020, India provided Nepal with COVID-19 test kits. In August 2020, 10 ventilators were provided to the Nepal army. India initially offered a grant of one million doses to Nepal in January 2021, which turned out to be insufficient. As a result, the vaccination programme in the country was on hold. The vaccination was resumed after China provided 800,000 doses by the end of March 2021.

India’s assistance to Afghanistan for the post-war reconstruction and development is unprecedented. To tackle the challenges of COVID-19, India offered assistance in the form of supply of 75,000 MT of wheat between April and September 2020.

Aid from China also followed. China provided Afghanistan with anti-pandemic supplies to fight against COVID-19 between April and October 2020.China supplied epidemic prevention materials to Maldives despite souring geo-political relations with the island nation.

India provided not only medical supplies to Maldives, but also offered concessional loans (USD 250 million) to mitigate the impact of the COVID-19.

While India–Pakistan relation is at its low, China offered much-needed medical supplies to the country. It has been reported that Pakistan was the first country in the world to get testing kits from China. This reflects the deep-rooted relationship between the two countries; both are all-weather partners.

India assisted Bhutan through material and services under the (SAARC) Coronavirus Emergency Fund.

While India led COVID-19-related aid efforts in South Asia, assistance from China to South Asian countries followed quite promptly to most of the SAARC countries. However, when it comes to financial assistance, the terms and conditions are drastically different in terms of the nature of concessions. Apart from official development assistance, there were instances of foreign aid from private individuals and organisations (such as Jack Ma Foundation, Alibaba Foundation, Xiaomi).

While vaccine diplomacy was seen to be pervasive since its development and trial phase, India had the early gains in supplying vaccines (both as aid and on commercial terms) to South Asian neighbours. While diplomatic efforts were effective, trust on Indian vaccine and the absence of quid pro quo played a major role in its adoption. On the contrary, issues regarding cost sharing pushed some of the South Asian countries to decide against the use of vaccines developed by Chinese firms.

It remains to be seen how and to what extent the post-COVID-19 economic recovery in South Asian countries will be aided by Chinese and Indian support. In the given scenario of decline in trade, a boost in investment in health, infrastructure and clean energy projects can revive these economies. While development aid can sidestep some of the short-run hiccups, its impact on economic growth in South Asia remains to be seen. Available evidence suggests that foreign aid does not impact economic growth significantly (Sethi et al. 2019). What South Asia needs is investment in skill building and critical infrastructure which can bring about sustained economic growth. Further, connectivity initiatives that are designed to create efficient supply chain linkages can enhance employment opportunities and the standard of living in South Asia.

Strategic Reinvigoration of South Asia and Strategic Shifts

South Asia’s strategic importance has raised manifold due both to BRI and the Indo-Pacific Strategy (IPS). The former is a signature project of China, whereas the latter is a counter initiative by the USA, Japan, India and Australia. In a way, both BRI and IPS manifest China’s rivalry with India in South Asia as the latter has longstanding bilateral issues and feels encircled by the former in a strategic way. While China’s involvement in South Asia through BRI, or through other modes, has increased, the IPS has provided further strategic heat to the region. Besides, the initiatives led by India, albeit at sub-regional scale, have provided further strategic rejuvenation in South Asia. We have presented a brief discussion of this trinity in the following sub-sections.

Projects by China/ Bri

In one of the preceding sections, we have discussed about BRI investment in South Asia. Although many South Asian countries were in dilemma to participate in BRI (Das 2017), over time, the involvement in BRI has become clearer. It could also be seen that there are more to the investment story in terms of how some of the South Asian countries are choosing to integrate with China. China has been getting its acts together in offering Nepal access to (four) ports for shipment by opening border routes such as Rasuwagadhi-Kerung, and Tatopani-Zhangmu. Further, China is working for reviving a train project that will connect Kathmandu from Lhasa. Nepal expects to be the gateway between Central and South and Southeast Asia by developing the Trans-Himalayan economic corridor with several trading routes with both China and India (Rana 2017).

China’s tariff concession for Bangladesh amid COVID-19-induced slowdown is another case in point. China offered to exempt 97% of Bangladeshi products from tariff (effective from 1 July 2020). The move will give further fillip to export sectors in Bangladesh. The tariff action has the potential to make Bangladesh part of the supply chain for Chinese producers, particularly in the labour-intensive manufacturing. China has been moving such production facilities outside its own turf due to rising labour cost and trade friction (Banik and Das 2014). Bangladesh has also received Chinese investment in these sectors from China (Hossain et al. 2018; Islam et al. 2013). However, higher trade cost and inadequate supply of infrastructure might lower the attractiveness of the country compared to other counterparts. Further, China’s tariff action is unlikely to reduce exports to India. Bangladesh has been enjoying duty-free exports to Indian market since 2011 under South Asian Free Trade Agreement (SAFTA) except the negative list items.

Sri Lanka is perturbed by external debt situation. Yet, it turned to China rather than IMF to avoid defaulting on foreign debts. Many nations still want to be in China’s debt (as they are easy to obtain, which is not possible from traditional lenders), which is essential to develop infrastructure in their respective countries (Ranjan 2019). The growing presence of Chinese investment in Sri Lanka has not only provided China with increased leverage in South Asia but also impacted the dynamics of Sri Lanka–India relations (Singh 2018). The failure of multilateral development institutions to lend adequately in less developed countries has left space for such country-led initiatives that can lead to unsustainable debt-trap. Unless alternate sources of financing projects in these countries are forthcoming, the debt-trap concerns will remain. Though multilateral development financing institutions, such as the World Bank, provide technical assistance, grants and loans to less developed countries, but it remains inadequate. Further, the graduating less-developed countries have to forgo many benefits that were previously available including concession on loans. On the other hand, The World Bank has called for deep policy reforms from BRI-participating countries and more transparency for the BRI as it has the potential to speed up economic development and reduce poverty for dozens of developing countries (World Bank 2019). However, without easy and timely access to finance and expertise, both less developed and graduating ones are likely to turn to China for their infrastructure investment needs. 4 The World Bank could device special mechanism to deal with the changing scenario of development finance.

Maldives’ economy has been severely impacted by COVID-19. High levels of debt owed to China (approximately USD 1.4 billion), owing to involvement in BRI-linked projects, has raised the debt-servicing burden. Contrary to previous dispensation’s close relationship with China in economic matters, the government led by President Solih has focussed on rebuilding good relations with India by adopting ‘India first’ policy. India provided unconditional concessional loans to Maldives in September 2020 to mitigate the impact of the COVID-19 pandemic in the island nation. A press release issued by High Commission of India Male, Maldives reads ‘The budgetary support of USD 250 million is extended without conditions; the government of Maldives is at liberty to use the money in repairing the domestic economic situation in line with its own priorities’ India also extended support to the development of Greater Male Connectivity Project (GMCP). However, the relations with the island nation are vulnerable to domestic political changes as the political parties have different approach towards international relations. Without consistency in domestic political front, these engagements often turn risky and may fail to yield desired developmental benefits in the recipient nations.

Steps taken under Indo-Pacific Strategy

The USA along with Australia, India and Japan spearheaded the quadrilateral (QUAD). The US’s aim to counter China in Sri Lanka and Maldives could be seen in action during COVID-19. Just before the US presidential election of November 2020, Pompeo visited Sri Lanka, Maldives and Indonesia. QUAD is seen as a balancing force to limit Chinese influence in the rule-based international order and in the maritime domain. Among the QUAD members, Japan and India have fairly long history of conflicts with China, whereas USA–China rivalry has intensified ever since trade war was initiated by Trump presidency. Australia–China relation has been marked by friction from time to time involving issues such as Beijing’s aggressive policy in the South China Sea and alleged involvement in Australian political affairs. Both political and economic relations between the two countries worsened steadily amid COVID-19 as Australian Prime Minister, Scott Morrison, demanded international probing on the origins and initial handling of COVID-19 in China. Further, Australia’s participation in the Malabar exercise by QUAD navies was not perceived well in China. China imposed economic pain by delaying clearance of containers (lobsters) arriving from Australia. The second phase of Malabar exercise was also done to signal the growing coordination among the quadrilateral (QUAD) members. This was preceded by Basic Exchange and Cooperation Agreement (BECA) between India and the USA during 2+2 ministerial dialogue in New Delhi.

Since COVID-19, Europe’s pushback against China has gained foothold in the economy. Although EU and China concluded, in principle, the negotiations for a Comprehensive Agreement on Investment (CAI) in December 2020, subsequent bilateral developments have created uncertainty in the rectification process that is originally due to complete by 2022. In response to EU’s punitive measures on four Chinese nationals and one entity over alleged involvement in human rights violation in the Xinjiang Autonomous region, China took counter measures and imposed sanction on 10 European individuals (including Members of the European Parliament) and four European institutions for allegedly spreading rumours about Xinjiang. This phase is described as the toughest moment in China–EU ties in over a decade (Global Times 2021). With such pushback, China’s strategic influence could be limited to countries with limited retaliatory power, particularly, the developing world. This further raises the geo-strategic significance of South Asia.

The inking of RCEP has made the West (particularly EU) rethink about the engagement with the Indo-pacific as the region is of strategic interest (Borrell 2020). Amid COVID-19, the resilient supply chain initiative (Australia, Japan and India) was also floated. However, the signing of RCEP by both Japan and Australia makes it difficult for India to spearhead such an alternative supply chain initiative. Being outside the block implies that tariff-induced cost will discourage many businesses to deal with Indian production facilities vis-a-vis those in the RCEP member countries. However, subsequent introduction of the production-linked incentives scheme is expected to have an effect on neutralising India’s tariff disadvantage and arrests the decline of the industrial base. However, such neutralising effect will at best be partial since the scheme is limited to identified sectors, and the incentives are conditional and time bound.

From the South Asian perspective, such geo-political heat is less likely economically rewarding unless it is accompanied by non-debt creating economic package from the major powers. It will be in the interest of South Asian nations to pursue economic objectives with strategic neutrality and independence, which can revive the regional integration in South Asia in the economic front. Without such integration, South Asia will not be able to unlock its potential in the economy and business, and the concern of low levels of development will remain.

South Asian nations will have to deal with multiple power equations in the years to come. However, strategic engagements come with risk in many fronts. It is imperative to maintain liberalism with strategic independence and neutrality and to focus on economic engagement in a mutually beneficial way. However, the practice of realism will not allow that to happen.

Initiatives by India

South Asia has long been considered as India’s sphere of influence (Yuan 2019). India expedited Sagarmala project after discarding participation in BRI. As a part of Sagarmala, India has identified more than 574 projects for implementation during 2015–35. The composite project aims to bring about comprehensive development of India’s maritime sector that includes 7,500 km coastline and 14,500 km potentially navigable inland waterways.

As BRI investments made inroads, except in India and Bhutan, the South Asian region experienced strategic reinvigoration. India stepped up connectivity and infrastructure efforts involving Bangladesh, Bhutan and Nepal. The BBIN initiative promotes ease of transportation and connectivity in the four countries. India has also invested in energy projects especially in Bhutan.

Nepal’s logistical challenges kept the country far from realising the true potential. India granting Nepal the access to Kolkata and Vizag port could ease some of the hardships. More needs to be done to smoothen transportation and logistics between Nepal and ports in the East coast of India. BBIN motor vehicle agreement has been signed in 2015. The development of BBIN corridor will not only benefit the South Asian neighbours, but also boost eastern states of India. The trilateral connectivity between Nepal and Bhutan via India needs further improvement. Similarly, Nepal–Bangladesh corridor (via India) can create much needed growth in the sub-region. India’s involvement in such connectivity projects got a boost in recent years. Multimodal projects are being started (at Jogighopa) to improve internal and international logistics in the region. However, time-bound completion will be the key. Delay could be seen in such regional connectivity projects (e.g., Kaladan through Myanmar). It may be noted that several connectivity projects in the region went to China which were initially available to India due to delayed response and inadequate funding, for example, Padma bridge project in Bangladesh (see Malhotra 2020).

Along with physical connectivity, digital infrastructure will need to be augmented in the sub-region. Within South Asia, other trade agreements are also pursued (APTTA). As per the agreement, Pakistan will allow Afghanistan to send goods to India using its land border. This can improve the trade and bring about development in the sub-region, if implemented in letter and spirit.

Further, problem remains in the area of air connectivity (some bottlenecks), especially with South Asia. Rising tariff is a spoiler to intra-South Asian trade. Nepal’s border row with India (involving Lipulekh, Kalapani and Limpiyadhura) is another sign of discontent in the South Asian integration.

Implication for South Asian Integration

To be able to trade and invest in each other’s market is important for South Asian nations to increase prosperity. However, the reality is that strategic divide has widened among South Asian nations. Such divides need to be mitigated to bring about South Asian synergies and an element of South Asian centrality. In the presence of China factor, BRI and IPS (among others) will have to be pursued to achieve development benefits for its people and not merely for strategic rivalry which is undue for a region that has common cultural and historical past. Strengthening various market institutions and political coherence to reduce regime instability are crucial.

South Asia needs to get intra-south Asia connectivity right. India holds a key spot in this regard in promoting connectivity and logistics. Even India’s ban on exports (say onion and potato) can magnify the shortage in countries like Bangladesh and Nepal. Such conflicting options are unlikely to cease unless there is better trade integration and risk management practices at sub-regional level.

With RCEP being signed by 15 countries, India missed another opportunity to be part of mega regional blocks. However, signing of RCEP has become a cause of concern for trade-dependent South Asian economies as India decided not to be part of it. Fears that countries will lose export market share to competitor RCEP members from Southeast Asia have been expressed (Rahman 2020). Further, India’s self-reliance could impact South Asia, though it remains to be seen, which can have far reaching implication on regional trade and investment. India’s absence from RCEP coupled with its self-reliance programme raises question about India’s role in Southeast Asia. In that case, the emerging South Asian economies might have to look for trade agreements with countries outside South Asia. To be unchallenged by China in South Asia, as part of its South Asia strategy, India will have to develop thriving relationship with the South Asian nations in economic front.

In the second-best scenario, although the regional institutional mechanism in South Asia is weak, the bilateral mechanism is found to be robust (Pattanaik 2018). There is a possibility of integration among sub-set of South Asian countries (and practicable) in view of geo-political constraints. These sub-sets can be BIM, BBIN, BIMSTEC, etc., that are workable.

What applies to individual also applies to country. Each of the South Asian nations needs to maintain strategic neutrality and independence to maximise economic benefits and opportunities that can come from multiple quarters. Strengthening infrastructure and capacity without compromising strategic neutrality will hold the key in establishing and thriving win–win South Asian integration.

Footnotes

Acknowledgements

The author thanks Rajat Kathuria and Arindam Banerjee for discussion and comments. Thanks are also due to anonymous referees for insightful comments during the review process. Usual disclaimer applies.

Declaration of conflicting interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.