Abstract

As soon as the sovereign debt crisis began, it was widely understood that Germany’s response would dictate its ultimate resolution. Whereas the initial round of bailouts stabilized markets and preserved the Euro, the purpose of the second Greek bailout is less clear. We argue that the German government’s decision to support a second Greek bailout reflected domestic political calculations. While a bailout would involve short-term political costs, Merkel’s government also recognized the social and economic consequences of potential Greek default. In particular, a default entailed the prospect of a massive inflow of migrants from Southern Europe into Germany, which would have hurt labor markets and, in turn, could have cost Merkel’s coalition electoral support. To evaluate the political, economic, and social costs of the second Greek bailout, we use models of credit default swap spreads, studies of international migration, and research on vote intention.

As soon as the sovereign debt crisis began, it was widely understood that Germany’s response would dictate its ultimate resolution. If Germany chose to provide assistance to shore up other economies or to support bailouts, then it was possible that Portugal, Ireland, Italy, Greece, and Spain (PIIGS) would be able to survive within the Eurozone. If Germany chose not to support any sort of assistance or if it insisted on excessive conditionality, it would force costs of adjustment on the PIIGS that would create enormous hardships for those economies and likely result in a larger wave of financial sector failures. Ultimately, this may have led countries to default and, possibly, to exit the Eurozone.

German policy makers weighed the costs and benefits of action carefully. A bailout would entail costs—both in terms of taxes and credibility. Germany would have to provide taxpayer money to cover the bad habits of governments that did not manage their economic policies with Teutonic fastidiousness. Almost as importantly, bailouts would require the German government to go back on historic pledges to not bailout profligate Euro member states, reducing its credibility and, hence, its ability to prevent future abuses.

However, failure to support these economies could plunge the periphery into a severe depression that could spread to northern Europe. Default would have also endangered German banks and bondholders with exposure to government debt from the PIIGS. Depression in southern Europe could also trigger massive immigration into Germany as people would move north looking for employment. These immigrants could adversely affect German labor markets, provoke social unrest and conflict, and place pressures on social insurance.

Failure to support a bailout might also endanger the broader European project, the cornerstone of Germany’s foreign policy since the 1950s. Without a bailout, some countries were likely to leave the Euro, dealing a blow to the ideal of European solidarity. This was not merely a symbolic cost as, for Germans, the European Union (EU) is more than just an economic club. It represents an invaluable security commitment, the fundamental institutional mechanism to prevent the outbreak of war and hostility on the European continent.

These stark policy choices created tension within the governing parties as German policy makers grappled to find the best response to a rapidly evolving situation. The prospect of a bailout aroused a passionate response from German voters. Indeed, a new anti-government and anti-Euro party—the Alternative for Deutschland (AfD)—quickly developed, calling for Germany to rid itself of the single currency. Other voters recognized the value of the European commitment and, though annoyed at the profligacy of southern governments, accepted the costs of a bailout as the price of solidarity.

During the early months of the crisis, Chancellor Merkel walked a fine line between support for Euro and demanding accountability from Eurozone member states. Ultimately, Merkel worked with the European Central Bank (ECB) and the International Monetary Fund to arrange bailouts for Greece, Ireland, and Portugal, thus ensuring the survival of the Euro. As part of the bailout, the ECB and other solvent governments assumed the debt held by private banks, transferring the associated risk from the private sphere to the balance sheets of public institutions. Although the initial bailout of Greece did little to stabilize that market, by late 2011, bailouts of Ireland and Portugal led to calmer markets across the Eurozone, saving the Euro from a total collapse.

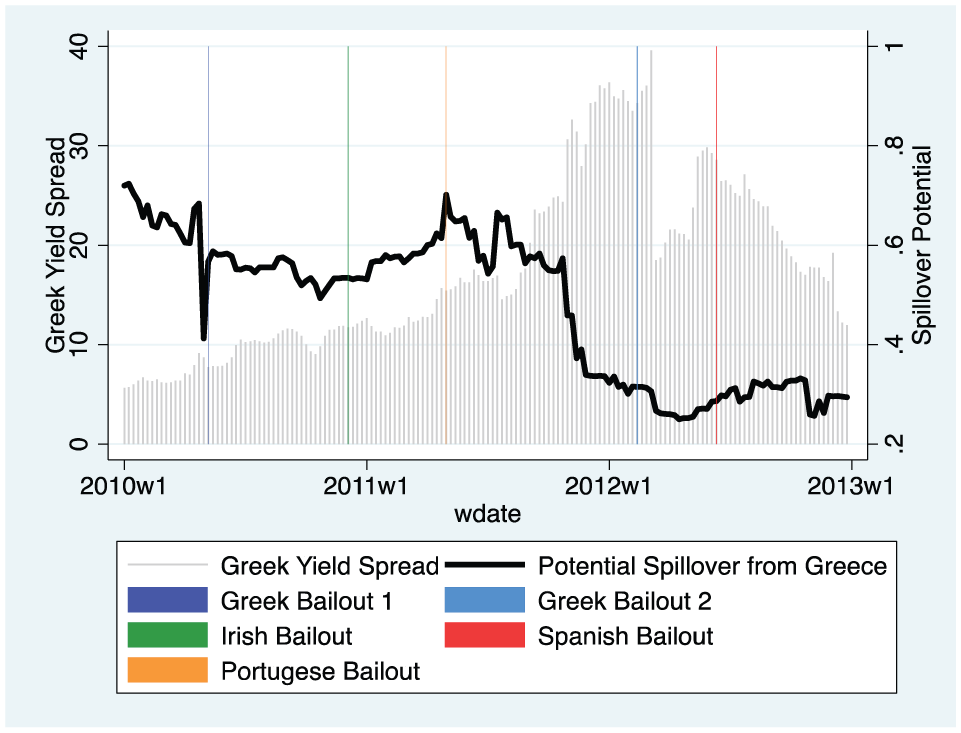

As financial markets calmed, however, the domestic position of the Greek government weakened. The Greek populace rebelled against budget cuts and higher taxes. This domestic political turmoil in Greece, which resulted in the resignation of Prime Minister Papandreau in November 2011, threatened the ability of the Greek government to maintain its fiscal promises even as markets appeared to become more confident in the Euro (see Figure 1). 1 Greek bond spreads began to increase, even as the spreads of other government bonds were falling. And, as shown in Figure 2, the risk of contagion within the Eurozone—that is, the risk of financial market volatility spilling over from Greece to other countries—was negligible by the fourth quarter of 2012. 2

Euro/dollar volatility.

Likelihood of spillover from Greece to Portugal, Ireland, Cyprus, and Spain.

Moreover, the fact that German banks had become less exposed to Greek debt meant that the financial and economic consequences of a potential Greek default would be limited (see Figure 3). 3 It seemed as if the markets had decided that the Euro would survive, even if Greece would have to default. Indeed, the Eurozone—its currency as well as its banking system—might even be stronger and more viable without Greece.

German bank exposure.

If the survival of the Euro was not in doubt by late 2011, why then did Germany’s governing coalition decide to support a second Greek bailout? We argue that the decision to bailout Greece reflected domestic political calculations on the part of Germany’s policy makers. While bailing out Greece would result in short-term political costs, Merkel’s government recognized the social and economic consequences of a potential Greek default. These social and economic costs—including the prospect of a massive inflow of migrants from Southern Europe and the fiscal repercussions of serial default—would have longer-term political consequences that may have led to Merkel’s coalition losing electoral support. Thus, we argue that support for a second bailout represented a political choice, a balance between the short-term costs of bailing out Greece against the potential implications of inaction.

Our contention rests on counterfactual reasoning—that is, we make arguments about how the German electorate would have reacted if German policy makers had decided to forgo bailing out Greece in March 2012. To build this counterfactual, we draw on three literatures: models of the determinants of bond spreads, studies of international migration, and research on vote intention.

The Argument

Standard political science models of vote intention for the government emphasize the role of macroeconomic fundamentals in shaping the public’s perception of the incumbent government. Voters typically rely on domestic economic indicators, such as inflation, unemployment, and stock market performance, not only to assess the government’s competence, but also to form expectations about the trajectory of the economy. These retrospective and prospective evaluations of the economy, in turn, shape voters’ decisions about whether to support the government. 4

We contend that the financial crisis reshaped this basic calculation of political support. First, the nature of the crisis broadened the electorate’s focus to include economic and financial factors beyond the domestic context. 5 Given Germany’s central role in Europe, voters were understandably concerned about the effect of the crisis on their pocketbooks. As the crisis in the periphery worsened, German voters became acutely aware of the fiscal conditions in the other economies. 6 As the fiscal condition of the PIIGS were likely to affect their own economy, debt conditions in other countries entered into electoral calculations of political support for the Merkel government.

German voters understood that the debt crises of other EU countries would likely affect the German government’s fiscal balances, German policy makers were also aware that the collapse of the periphery economies could affect the German economy in other ways, particularly by unleashing waves of immigration into Germany. Germany has always been a key destination country for migrants in search of better economic opportunity. In fact, Germany is the destination for the largest number of migrants in the EU. Research shows that migration into Germany decreases the wages of native workers, even though the estimated impact is small (Steinhardt, 2009). 7 Even a small effect on wages, however, can be perceived as a significant problem by mass publics and influences how they assess the causes of unemployment. Immigration also contributes to cross-cultural frictions (Boeri, 2009; Facchini & Mayda, 2009a). Indeed, immigration has always been an important, hot button political issue in Germany (Joppke, 1996). 8

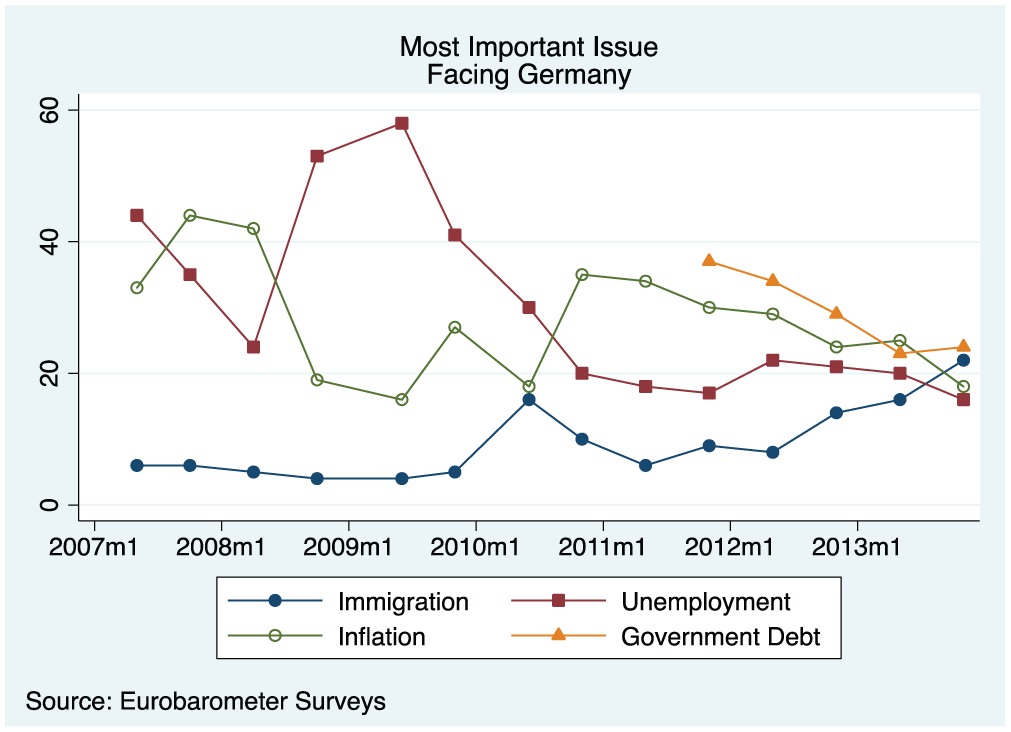

Although polls show that voters continued to identify economic problems such as inflation and unemployment as more pressing topics, it is notable that concerns over immigration spiked in the early part of 2010 as both Greece and Ireland had their sovereign debt ratings downgraded and sought bailouts from the Troika (see Figure 4). German policy makers, therefore, had incentives to consider the possible immigration outcomes as they weighed the policy response. Deterring immigration would keep the issue off the public’s agenda and insulate the government from any political fallout associated with it.

German attitudes toward immigration.

Thus, the financial crisis broadened the concerns of the electorate, beyond domestic conditions to encompass the performance of other European countries. Policy makers were also acutely aware that the crisis had the potential to grow even beyond straightforward budgetary consequences to affect the labor market and social cohesion. These concerns shaped the Merkel government’s policy choices, challenging them to balance the fiscal costs of the bailout and the potential political costs of increased immigration into Germany.

Models, Data, and Method

Our argument that the Merkel government had a political incentive to bailout Greece the second time relies on counterfactual reasoning—on the “what if” scenario had Germany not bailed out Greece in March 2012. Bond spreads at the time, made it appear that Greece was on the precipice of default. A default, in turn, could have produced massive migration into Germany which would have, all else equal, damaged the governing coalition’s public support as elections loomed. We contend that the expected cost of Greek default has a direct and indirect effect on vote intention for Germany’s governing coalition. Directly, voters expect to bear the costs of bailing out fiscally profligate countries. The indirect effect works through the labor market channel—in the absence of a bailout, we expect there to be a dramatic increase in migration from defaulting countries into Germany.

To evaluate these claims, we proceed in three steps. First, we examine the effectiveness of Troika bailouts on the evolution of sovereign spreads—measured as credit default swaps (CDSs)—in Eurozone countries. CDS provides a real-time measure of the market’s perception of a particular country’s default risk. 9

In our second step, we use a pseudo-gravity model to evaluate the effect of bailouts on Eurozone migration into Germany. We anticipate that bailouts have both direct and indirect effects on migration. Directly, bailouts may provide (re)assurances that the government is taking steps to restore economic stability; likewise, bailouts may also signal the beginning of severe austerity measures. Indirectly, as noted above, bailouts may influence CDS spreads, which, in turn, serve as a proxy for expectations of relative economic performance.

Third, we estimate a model of government vote intention in Germany that allows us to evaluate how different paths of Eurozone sovereign risk and migration into Germany affect the governing coalition’s political standing.

With these three pieces in place, we then engage in counterfactual analysis to understand the consequences for German electoral politics if Greek bailout in March, 2012 had not occurred.

For the CDS and migration models, we utilize a monthly sample of Eurozone countries—Austria, Belgium, Estonia, Finland, France, Greece, Ireland, Italy, the Netherlands, Portugal, Spain, Slovakia, and Slovenia from January 2007 to September 2013. Cyprus is omitted due to lack of comparable CDS data. Some models omit Estonia due to lack of data.

Modeling Sovereign Bond Spreads

Building on the finance literature, we interpret the spread of a country’s CDS spread vis-à-vis a risk-free asset as a measure of sovereign default risk. The risk-free asset in this case is a German CDS of similar yield. Monthly data for the countries in our sample are from Bloomberg. 10 Because the CDS series are non-stationary for all markets, we use the change in CDS spreads as the dependent variable. We also take the log of the CDS spread to decrease the influence of outlying observations—this, for the most part, prevents Greek CDS spreads from overly determining the results.

Theoretical models of sovereign spreads focus on both economic fundamentals and on the global appetite for risk. Following Beirne and Fratzscher (2013) and Heinz and Sun (2014), we proxy for a country’s fundamentals using monthly changes in inflation and the level of the real effective exchange rate (which taps the potential for productivity). 11 To measure the global appetite for risk, we use the change in the CBOE Volatility Index (VIX).

Markets respond not just to economic fundamentals but also to political events as these often provide market actors with a sense of the future course of economic policy. 12 We include three kinds of political events in the CDS models—elections, cabinet dissolutions, and protests. Data on elections and cabinet dissolutions come from Anderson, Bergman, and Ersson (2014) and are coded as dummy variables for the month when the event in question occurred. For protests, we draw on the Integrated Crisis Early Warning System (ICEWS) project (Lautenschlager, Shellman, & Ward, 2015) which provides data on the number of anti-government protest events each month. We expect all three of these events to increase CDS spreads.

We also include the lagged value of the level of the CDS spread to control for persistent changes (long swings) in country-specific spreads as well as potential ceiling or floor effects (when very high or very low values can influence the range of a dependent variable). Because we examine spreads across a panel of countries, we also include a set of country-specific dummy variables which capture unmeasured, but country-specific, influences on yield spreads.

To determine the effect of bailouts on CDS spreads, we code the bailouts of Greece, Portugal, Ireland, and Spain in two ways. 13 First, we create “country-specific” bailouts and code these variables equal to “1” for the country-month when a bailout occurred. Thus, the first Greek bailout is coded “1” only for Greece in May 2010. Second, to evaluate whether bailouts had spillovers across countries, we code the bailout dates as “1” for all countries. That is, the first Greek bailout is coded “1” for all sample countries in May 2010, and so on. A negative and statistically significant coefficient on these bailout variables indicates that the offer of financial assistance is associated with calmer markets either within the country or across the sample.

We estimate the spread model using ordinary least squares (OLS) and report robust standard errors clustered by the country.

Modeling Migration Into Germany

We obtained monthly data on flows of migrants into Germany from the German Federal Statistical Office. The data begin in January 2006 and count the number of permanent migrants entering Germany based on their country of nationality/citizenship. It is important to note that citizenship/nationality does not necessarily correspond to the migrant’s country of birth.

Our point of departure is the standard microeconomic model of immigration. 14 The basic intuition of these models is that migration occurs when the expected wage in the host country exceeds the expected wage in the home country less the cost(s) of moving. Empirically, these models have been implemented within the context of pseudo-gravity models. 15 Gravity models of international migration control for the economic conditions that exist within a source and destination country and the distance between the two countries. To capture economic conditions, we include three variables: the difference in per-capita GDP in country i and Germany at time t − 1, the unemployment rate in country i at time t − 1, and the unemployment rate in Germany at time t − 1. The inclusion of fixed effects for the migrant’s countries of origin make it unnecessary to include standard gravity controls such as the existence of a common border with Germany, whether the official language of the country of origin is German, or the distance between Germany and the migrant’s country of origin as these values do not vary over time.

The literature on diaspora networks and global migration (Beine, Docquier, & Ozden, 2011) argues that migrants flow to countries where there are already a large number (stock) of co-ethnics from their homeland. Thus, we use a measure of the flow of migrants from country i into Germany a year prior. We also include a lagged endogenous variable to account for persistence in migration flows—and as a proxy that could potentially capture changes in German migration policy. Finally, we include a set of monthly dummy variables to capture seasonal variation in migration flows.

The migration model contains two variables of interest. The first is the CDS spread in the migrant’s country of origin vis-à-vis Germany. Although the CDS spread has been used as an indicator of the global market’s assessment of default risk, we argue that it reasonably proxies for economic expectations within that country. Unlike contemporaneous measures of income differentials, the CDS spread is future looking and is correlated with national prospective economic assessments. In Figure 5, we plot the log of CDS spreads against national level assessments of the economy in the coming year using data from the Eurobarometer surveys. 16 There is a clear positive relationship between the CDS spread and the share of the public who expect that the economic situation in the coming year will get worse. This effect does not go away if we eliminate the high CDS countries—Greece and Portugal. 17

CDS spreads as an indicator of economic insecurity.

The second variable of interest is a dummy variable for the timing of a bailout. This variable not only measures the direct effect of a bailout on migration into Germany, but it also deals with a potential problem of omitted variables. One potential omitted variable in the migration model results from the possibility that austerity policies borne from conditions associated with the bailouts may increase the demand for outmigration. Although we do include a measure of unemployment in the source country, optimally we would have an aggregate measure of austerity conditions in the bailout countries. Measures of government spending and/or government employment, however, are available only at an annual frequency. It is also important to recognize that the terms of each bailout differed, so it is likely that an aggregate measure would be unable to capture the “true” extent of the conditions associated with the bailouts.

Thus, we construct a dummy variable coded “1” for the months following the bailout to signal that we anticipate a change in average number of migrants due to austerity measures associated with a bailout. As none of the bailout countries had met all terms of the bailout before the end of the sample (June 2013), this dummy variable is coded “1” for the entire period after the bailout. The exception is Greece which received two bailouts during our sample period; consequently, post–Greek Bailout 1 is coded “1” until Greek received its second bailout in March 2012.

As with the CDS model, we also include a set of political events measuring elections, cabinet dissolutions, and protests in the migrant’s country of origin. We do not have a strong set of theoretical priors regarding these variables. At a minimum, their inclusion will produce cleaner estimates of the effect of CDS spreads on migration.

We estimate Poisson and negative binomial models of migrant inflows into Germany. To deal with unequal error variance across observations, we cluster standard errors by country.

Modeling Vote Intention for the German Government

Our third step is to model vote intention for the governing coalition. Opinion polls ask the question: “If parliamentary elections were held tomorrow (or next Sunday), how would you vote?” Respondents then identify which party they would choose to support. The frequency of these polls vary depending on the time of the year and the length of time before an election is due, but there were at least two polls in every month during our sample period—and often more. We created monthly averages of vote intention for the four major parties. As Germany had a coalition government throughout the sample period (although the identity of the governing parties changed), we added the vote intention for the parties in government to form one measure of vote intention on the assumption that those parties were most likely to be held accountable for the government’s policy performance. 18

Because vote intention may have floor and/or ceiling effects, we include the lagged level of vote intention. In addition, we measure the performance of the German economy through the inclusion of measures of domestic unemployment and inflation. We also include dummy variables for periods of political campaigns, elections, coalition formations, and new government honeymoons as well as two variables that capture the length of time that a specific coalition has been in power (electoral clock and electoral clock2).

Including measures of Eurozone default risk and the potential inflow of migrants from other EU countries is complex because the weight of these variables depends on other country-specific factors. An increase in default risk in Denmark, for example, would not strike the German electorate as significant because the size of that country’s budget deficit is small relative to that of one of the PIIGS. Likewise, an increase in Spanish spreads is a far more significant event in 2011, after government debt had exploded, than in 2005, when it was assumed that Spain’s debt-to-GDP ratio was below 60%. To measure how spreads would potentially affect the German electorate, therefore, we use the average of CDS spreads for each Eurozone member for each month, weighted by the respective country’s debt-to-GDP ratio.

As with spreads, we expect the impact of migrants from different countries to have heterogeneous effects on the native population. Germans may be more sensitive to migrants from countries that are culturally distinct from themselves (e.g., Greece or Hungary) than they are to migrants from countries that are culturally and ethnically similar (e.g., Austria or the Netherlands). Bridges and Mateut (2014), indeed, find that opposition to immigration is a function of cultural dissimilarity between the native and immigration populations even after controlling for socioeconomic, political, and fiscal variables. Using an experimental set-up, Ben-Nun Bloom, Arikan, and Courtemanche (2015) find that ethnic and religious differences between natives and migrants drive anti-immigrant sentiment. That said, an influx of migrants from all these countries could have economic and social (and ultimately political) consequences for the governing coalition.

To create a measure of the possibility of social dislocation due to an inflow of culturally dissimilar migrants, we construct two measures. First, we take the total number of migrants entering Germany each month and weight it by the migrant country’s genetic distance from Germany. This measure, applied by Spolaore and Wacziarg (2013) within the context of economic development, identifies the ease with which ideas and traits are transferred across different populations. 19 The more distant two populations, the more likely that communication will be difficult and conflict more likely to ensue. Our second measure is similar but rather than weighting inflows by genetic distance, we weight inflows by cultural distance based on data from the World Values Surveys. Figure 6 contains descriptive information about the values of genetic distance and cultural distance. 20

Genetic and cultural distance from Germany.

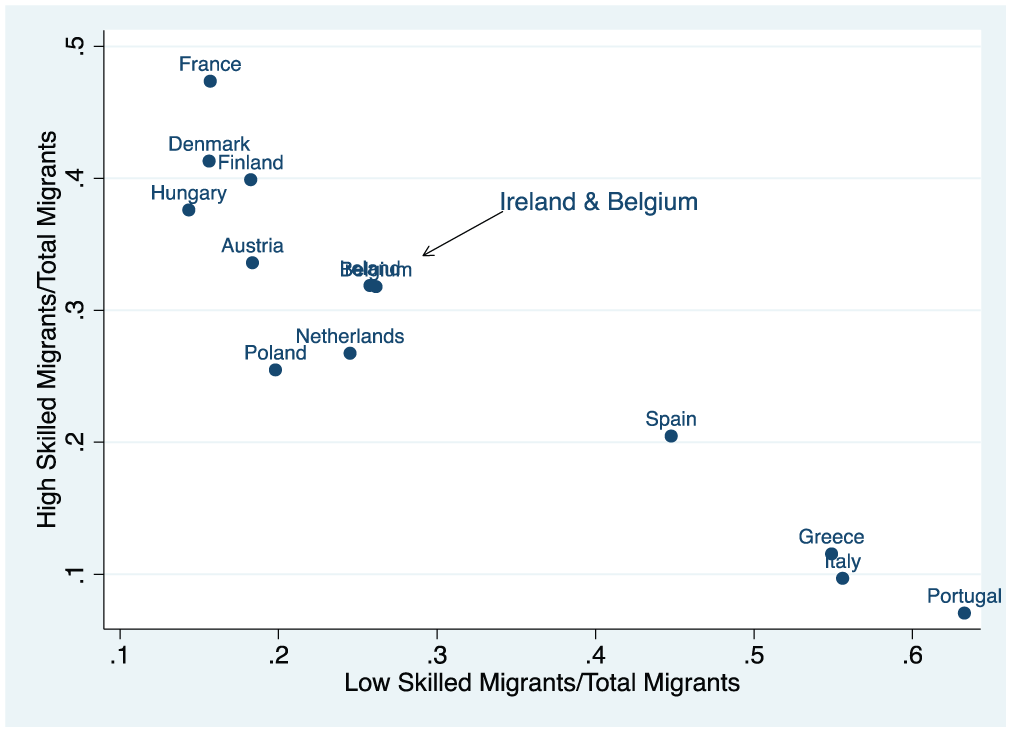

It may be that the German electorate is not concerned with cultural differences; rather, they may be reacting to competition in the labor market. To assess this scenario, we also weight migrant inflows by the share of migrants from the origin country in Germany that are unskilled. 21 Figure 7 displays the unskilled/skilled ratio. A quick glance at Figures 6 and 7 make it clear that it would be difficult to disentangle cultural from labor market concerns as the largest shares of unskilled migrants hail from the countries that are the most culturally different from Germany—those of Southern Europe.

Skilled and unskilled labor flows into Germany (2010).

Finally, as a control for potential omitted factors that may influence vote intention, we include a set of month dummy variables. These dummies also control for potential correlation between migration and vote intention that could be associated with seasonality in both data series.

Results

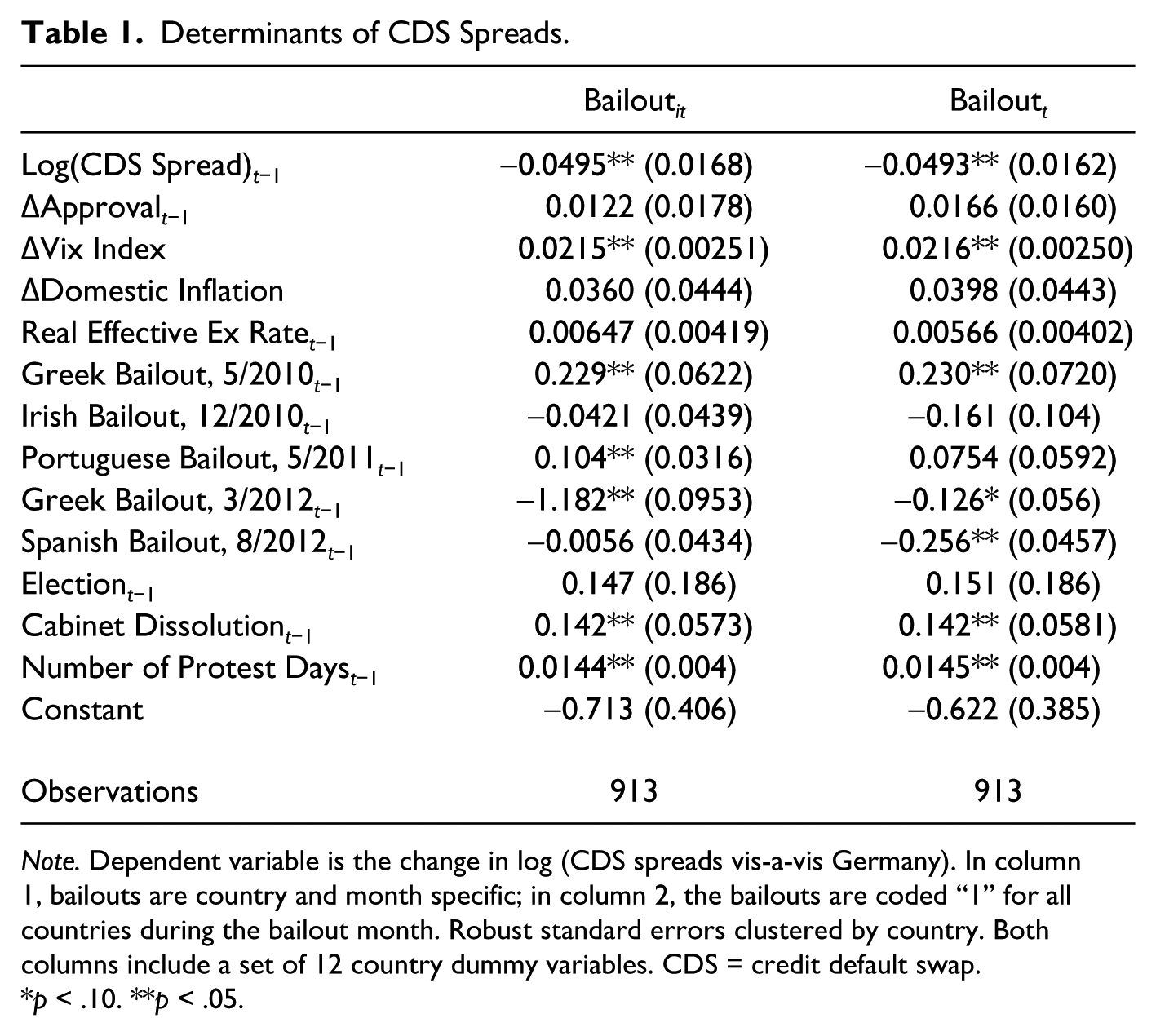

Table 1 contains the results for the CDS spreads—that is, the difference between local CDSs vis-à-vis a comparable CDS in Germany—equation. In it, we estimate the impact of political events and bailouts on the likelihood of sovereign default. The control variables are in the expected directions. Lagged levels of spreads and the change in the VIX index are statistically significant predictors of current changes in CDS spreads. Even during the height of the financial crisis, a ceiling on spreads was present as the lagged level has a negative effect. Inflation also has a positive effect on CDS spreads as does increased productivity—as measured by the country’s real effective exchange rate—though neither of these variables is statistically significant.

Determinants of CDS Spreads.

Note. Dependent variable is the change in log (CDS spreads vis-a-vis Germany). In column 1, bailouts are country and month specific; in column 2, the bailouts are coded “1” for all countries during the bailout month. Robust standard errors clustered by country. Both columns include a set of 12 country dummy variables. CDS = credit default swap.

p < .10. **p < .05.

We include the change in vote intention for the incumbent German government. Interestingly, political conditions in Germany do not affect default risk throughout the Eurozone. This is surprising, as we would have envisioned bond traders inferring that a weak German government would be less able to come to the rescue.

As anticipated, political events in the source countries influence CDS spreads. Cabinet dissolutions and political protests increase default risk. Elections, however, do not have a statistically significant effect on default risk. These findings are consistent with the notion that investors and speculators incorporate all available economic and political information when pricing risk: Elections, for the most part, have predictable outcomes, whereas cabinet dissolutions and political protest are less anticipated. 22

Did the bailout influence perceptions of government default in the Eurozone? Recall that we code bailouts in two different ways—both country-specific (column 1) and sample-wide (column 2). In column 1, the results indicate that rather than blunting CDS spreads, the 2010 bailout of Greece increased spreads in that country 25% whereas the 2011 bailout of Portugal was associated with a 10% increase in Portuguese spreads. In fact, the first bailout of Greece not only increased Greek spreads, but, as seen in column 2, it is associated with an increase in spreads across Eurozone countries. It is difficult to make a causal claim here—the early part of 2010 was a period of high uncertainly about the stability of the Euro in general and there were significant fears of contagion from Greece to other PIIGS. The second Greek bailout, however, was associated with a decrease in spreads of more than 70%. 23

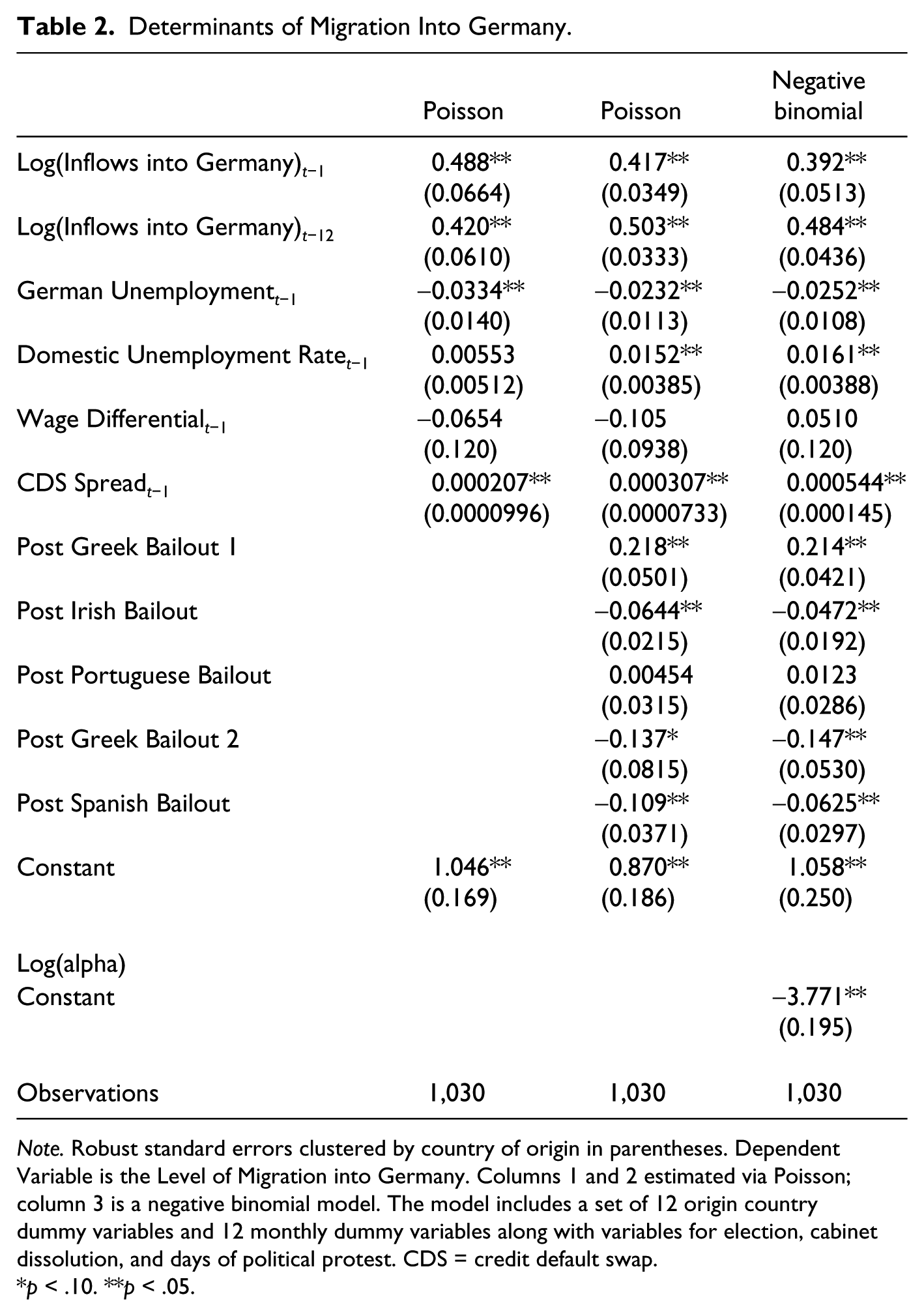

Given that the first attempt to stabilize markets in Greece failed, why did Germany push for a second bailout of that country? Our argument is that Germany pursued this strategy, not just because of a fear of contagion, but to stabilize a country that was a source of migration pressure. We model the flow of migrants into Germany in Table 2. In columns 1 and 2 of Table 2, we use Poisson regression to evaluate the effect of covariates on the number of migrants from Eurozone member countries into Germany. Results from the model indicate that migrant flows into Germany are persistent and seasonal—both the 1-month and the 12-month lags are statistically significant.

Determinants of Migration Into Germany.

Note. Robust standard errors clustered by country of origin in parentheses. Dependent Variable is the Level of Migration into Germany. Columns 1 and 2 estimated via Poisson; column 3 is a negative binomial model. The model includes a set of 12 origin country dummy variables and 12 monthly dummy variables along with variables for election, cabinet dissolution, and days of political protest. CDS = credit default swap.

p < .10. **p < .05.

There is mixed support for the importance of economic conditions in shaping migration flows. Although lagged unemployment in Germany sends a negative and significant signal about employment prospects there and unemployment in the sending country is also statistically significant, there is no evidence that income differentials drive immigration into Germany. While at odds with the existing literature, this result is likely the consequence of a more homogeneous set of countries in terms of per-capita GDP than typically found in models of bilateral migration.

We argued above that CDS spreads are a reasonable indicator of prospective economic evaluations within countries. Even after controlling for a multitude of factors—including monthly and country dummy variables—we find a statistically significant and positive effect of the log of CDS spreads on immigration into Germany. The larger the spread, the more migrants move into Germany. Clearly, CDS spreads provide an indicator of future economic conditions, giving people incentive to vote with their feet. To get a sense of this effect in context, consider that prior to the first Greek bailout, the average CDS spread of Eurozone countries was around 4%; this is associated with an inflow of approximately 600 migrants per sending country-month. At the height of the crisis, when spreads were at their peak, migration into Germany is predicted to increase to almost 2,000 migrants per sending country-month. Thus, worsening economic conditions and the prospect of default spurred more migration into Germany from the European periphery.

We find a similar result in column 2 where we add dummy variables to proxy for the potential impact of austerity conditions in the bailout countries. Conventional wisdom suggests that the austerity conditions would drive migrants to leave the bailout countries in hopes of finding work elsewhere. Although we cannot measure whether austerity increases aggregate emigration, we can identify its effect on migration into Germany. Consistent with the results of the CDS spread model, the first bailout of Greece in 2010 actually increased resulted in increased migration from Greece to Germany. What is interesting—and confirmed in the negative binomial regressions in column 3—is that the subsequent bailouts in Ireland, Greece, and Spain decreased migration from those countries into Germany.

This result may be at odds with conventional wisdom that argues that a decrease in government spending—a defining feature of austerity programs associated with bailouts—would lead to a large increase in emigration. Surprisingly, the austerity programs implemented by the Greek government either before or after the bailouts did not generate a large flow of outmigration. This was because, at least in part, most of the conditions associated with the Troika’s bailout hit those who are the least likely to emigrate: Government employees and older workers who were tied to what remained of their government pensions or who, all else equal, were unlikely to move due to the transactions costs associated with leaving one’s home. 24

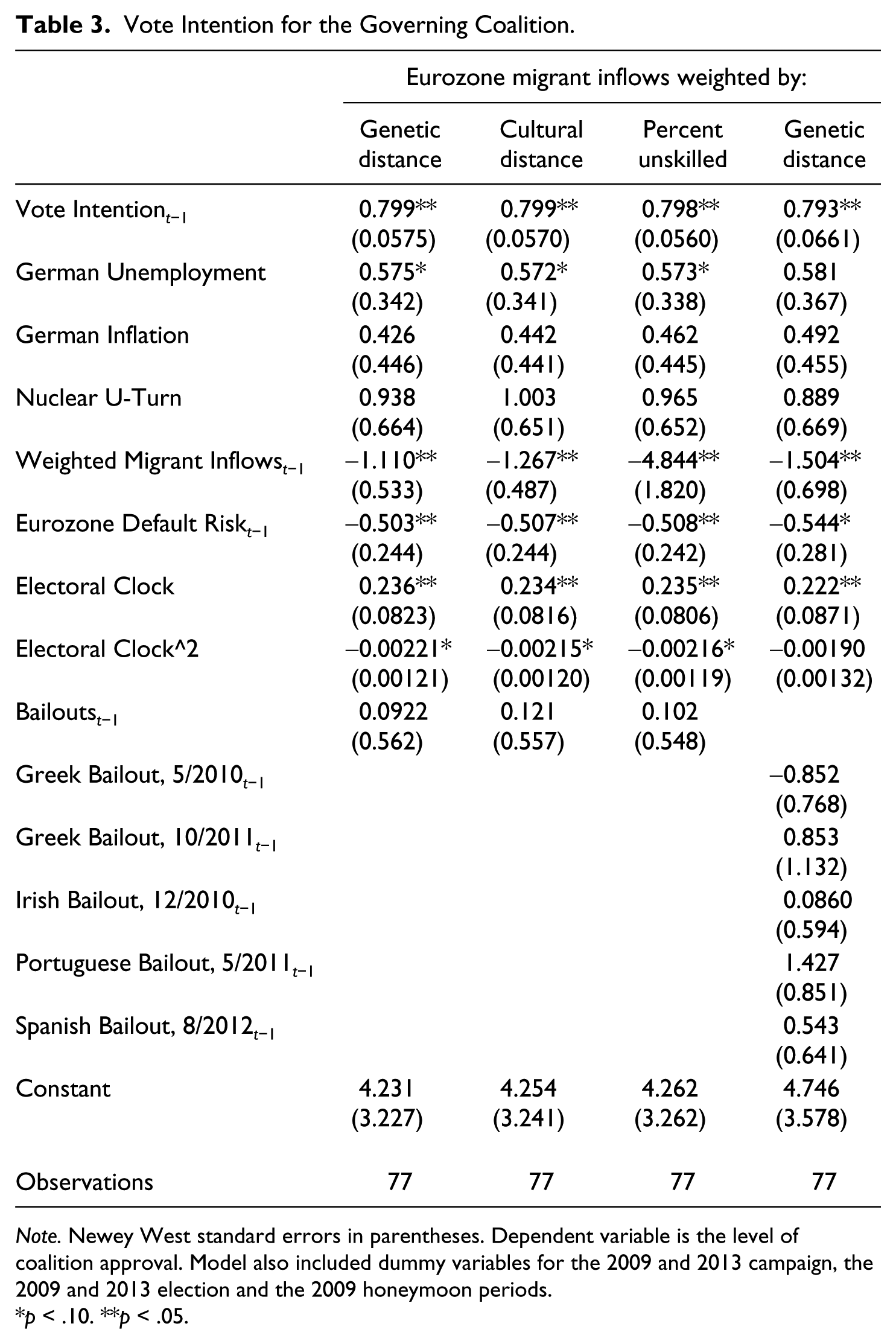

So far, we have shown that the second Greek bailout reduced bond spreads and that bond spreads influenced migration into Germany. We next model vote intention for Germany’s governing coalition (Table 3). Before turning to our variables of interest, we first discuss the control variables. The “electoral clock” variables—which measure the length of time that the incumbent government is in power—are statistically significant and suggest that popular support for a coalition levels off, the longer it is in office. Somewhat oddly, we obtain a positive coefficient on the unemployment rate suggesting that the German public does not punish the coalition during bad labor markets as the literature would suggest. Inflation, however, is not statistically significant nor is the dummy variable for Merkel’s U-turn on the nuclear issue.

Vote Intention for the Governing Coalition.

Note. Newey West standard errors in parentheses. Dependent variable is the level of coalition approval. Model also included dummy variables for the 2009 and 2013 campaign, the 2009 and 2013 election and the 2009 honeymoon periods.

p < .10. **p < .05.

The decision to bailout Greece, Portugal, Spain, and Ireland did not have a statistically significant effect on vote intention for Germany’s governing coalition. In column 1 of Table 3, we club together all these bailouts into a single dummy variable whereas in column 4, we separate them to ascertain whether the electorate was concerned with individual bailouts. In neither case are the bailout variables statistically significant.

We do find, consistent with our expectation, that the German electorate punishes the incumbent government when there is an increase in default risk within the Eurozone. An increase in the risk of default—measured as the deficit weighted average CDS spread within the Eurozone—decreases government approval. Substantively, our results indicate that a 1% increase in default risk is associated with a decrease in government approval of approximately five percentage points.

The results also show that the German electorate holds the government responsible for an increase in migrant inflows. Regardless of how we weight these inflows—genetic distance, cultural distance, or the share of unskilled workers—increasing migration from Eurozone countries into Germany by one standard deviation results in a drop in vote intention for the governing parties of almost four percentage points.

Taken together, these results tell a compelling story: Although bailouts may have had short-term negative consequences for approval of the Merkel government, they did reduce spreads which, in turn, decreased immigration into Germany. An increase in CDS spreads combined with an increase in immigration would have, all else equal, been costly over the long term for the Merkel government. The magnitude of that long-term loss is explored in the next section.

What If There Had Been No Bailout?

We argue that the potential political consequences of immigration provided an incentive for the Merkel government to support bailouts for the governments in the periphery. And yet, immigration was not a major issue in Germany’s 2013 election. Although bailouts were discussed in the campaign—Merkel dismissed the possibility of future bailout; her Finance Minister Wolfgang Schauble suggested that Greece would need a third bailout—the other main parties did not press concerns about the bailout actions, other than to note that they perhaps cost too much. Only the upstart Alternative for Germany party (AfD) dared to suggest that Germany would be better off outside of the Eurozone.

We argue that immigration and bailouts did not play a larger role in the election because the bailouts worked: They had the desired effect of preventing a flood of immigrants into Germany. Thus, none of the parties could raise that as a compelling issue against the Merkel-led government. It is straightforward to imagine that it would have been a hot button issue if the bailouts had not worked to relieve pressure on the periphery economies.

This conjecture can be subjected to a more rigorous analysis using the models developed thus far. Our counterfactual asks, what would have happened to vote intention had the Merkel government not bailed out Greece in March 2012? 25 To evaluate this counterfactual, we focus only on Greece because, as noted above, by this point in time the European economy had stabilized significantly. We use three-stage least squares to estimate this as a simultaneous equation model with Greek CDS spreads, migration from Greece into Germany, and German approval as endogenous variables (see Appendix). 26

Table 4 presents the results of the simultaneous equation model. Note that these results are consistent with the findings reported earlier. In the first equation, the bailouts of Greece decrease CDS spreads. In the second equation, higher CDS spreads are associated with a larger flow of migrants from Greece to Germany. Finally, in the vote intention model we find a statistically significant negative effect of both CDS spreads and migration on German government approval.

Simultaneous Equation Model: Greece.

Note. Model estimated via three-stage least squares using Greek spreads and (unweighted) migration into Germany. Vote intention model includes dummy variables for the 2009 Campaign, Election, and Honeymoon and the 2013 Campaign and Election periods. CDS = credit default swap.

p < .10. **p < .05.

We use this model to engage in dynamic forecasting. To do dynamic forecasting, we have to make the timing of the second bailout endogenous or, at a minimum, specify that it is determined variables outside of the model. We argue that the timing of the second bailout is a function of the direct cost to German bondholders who are exposed to a Greek default along with the potential threat to the German labor market. 27

Figure 8 illustrates the counterfactual by assuming that in March 2012, the bailout of Greece did not occur. For purposes of comparison, we plot the observed vote intention series along with dynamic in-sample forecasts assuming that all variables take their observed values. Note that the dynamic in-sample forecast and the observed vote intention series match closely; this gives us confidence that the vote intention model is well specified.

Counterfactual forecast: No Greek bailout in March, 2012.

We construct 95% confidence intervals for this dynamic counterfactual forecast using bootstrap resampling. The counterfactual—if spreads had increased absent a bailout of Greece—is telling. The immediate effect of this spread shock is a large and sustained decrease in vote intention for the governing coalition: There is an immediate decrease in support of almost 10 percentage points. When vote intention begins to stabilize in early 2013, it reaches only 40%. This decrease would possibly have been sufficient for Merkel’s coalition to lose the subsequent election.

As a robustness check, we estimate three-stage least squares model separately for each Eurozone country. The results for the effect of spreads and immigration in the vote intention models are summarized in Figure 9. These results square with our expectations: In almost all cases, an increase in CDS spreads—our proxy for the likelihood of Eurozone default—decreases support for the German incumbent. That effect becomes larger as the size of the fiscal deficit in the country in question increases. Likewise, immigration from countries that are culturally different from Germany and/or that send a large share of unskilled labor to Germany also decreases support for the incumbent government.

Country-specific 3SLS results for approval equation.

The results in Figures 8 and 9 are compelling: Absent a bailout, bond spreads and migration to Germany would have increased dramatically, causing an enormous long-term loss of public support for the Merkel government. The 95% confidence intervals associated with the counterfactual forecasts are well below both the observed approval series and the in-sample prediction. Domestic political considerations clearly played a role in Merkel’s decision to support the second Greek bailout. While migration did not receive any attention in the run-up to the 2013 election, it is highly likely that this would have been a huge campaign issue had the bailout not occurred.

Implications and Conclusion

We argue that the German government weighed social, political, and economic factors when deciding whether to bailout Greece in 2012. While a bailout created short-term fiscal costs and problems associated with moral hazard, failing to bailout Greece would have generated far greater social and political fallout due to the possibility of migration from southern Europe into Germany. Our counterfactual analyses demonstrate the enormous electoral cost that the Merkel government would have confronted had it not bailed out Greece.

Indeed, the 2015 refugee crisis in Europe illustrates the potential political fallout over immigration in Germany. As Middle Easterners arrived in Germany, public support for migration dropped. Between September and October 2015, polls showed a sharp increase—almost 10 percentage points in the course of a single month—in the number of Germans expressing concern about the large number of migrants entering the country. There was a corresponding decline in Merkel’s popularity and support for the governing coalition. 28 Keeping migration off the agenda with the bailout, therefore, was in Merkel’s interest as she prepared to fight for election in 2013.

What does the mean for the future of German politics? The main parties—the Christian Democrats and the Social Democrats—share a commitment to Europe and to the Euro. Thus, it was often difficult to see significant differences between them on the bailout. An SDP-led government likely would have acted in a similar manner, perhaps being even more aggressive in bailing out the peripheral economies to prevent immigrant inflows that would hurt their working-class constituents. Yet, there are costs to this consensus on the Euro and Europe. Germans must pay for bailouts and structural funds or accept that migrants will come to Germany to work and live.

Given the centrist consensus around Europe, political outlets for voters opposed to the consensus will have to be found outside of the main parties. The AfD, composed largely of defectors from the Christian Democratic Union (CDU), offered an alternative on the right. The AfD adopted a populist stance that rejects the Euro and seeks limits on immigration. The AfD did not fare well in the 2013 federal elections, failing to meet the 5% electoral threshold. Yet, since then, the party has gained in popularity, winning seats in the European elections and in recent state-level elections. Given the relative consensus between the CDU and Social Democratic Party (SDP), it is unsurprising that there is room in the political space for the development of this type of party.

More generally, our findings have a number of implications for understanding the relationship between global financial markets, cross-border migration, and domestic politics.

The Euro and the Free Movement of People

Neofunctionalists argued that a rationale for the adoption of the Euro was to guarantee the gains from trade brought about the removal of trade barriers. By removing exchange rate risk within the EU, member states could trade without the potential distortions of a competitive devaluation. In a similar fashion, our argument suggests that the credibility of the Euro relied on the existence of free movement of people in the Eurozone.

As the Euro was being negotiated, member state governments had wildly different fiscal positions: Italy and Belgium, in particular, had debt-to-GDP ratios in excess of 100. Reflecting these fiscal differences, bond spreads throughout the late 1980s and 1990s were relatively large. European policy makers recognized that these fiscal differences created the potential for problems under a single currency: A profligate government could find itself in a vulnerable financial position and require a bailout. To deter this possibility, a no-bailout clause was explicitly negotiated. Despite these very different fiscal positions, once the Euro was adopted, bond spreads quickly converged, suggesting that market actors believed that the Euro reduced the risk of a government default, even though government debt still varied widely.

What made it credible that governments would not default or that someone would come to the rescue to save a defaulting government? Our analysis implies the threat of internal migration from the periphery made any sort of promise not to bailout incredible. 29 Market actors understood that northern European countries would not want to deal with the flood of immigrants that would happen if a periphery government defaulted. They calculated that the northern European countries would rather pay for a bailout than accept increased immigration.

Thus, the free movement of people within the EU helped guarantee the credibility of the Euro and reduced bond rates for debt-ridden EU countries. Without the free movement of people, northern European countries would not have had the same incentives to bailout the periphery countries. And if the EU had not sequenced the institutional reforms in this manner—free movement first, Euro second—then bond spreads would not have fallen as quickly or as far as they did. The free movement of people, therefore, provided debtor governments with increased fiscal flexibility as the bond rates were lower than anticipated.

Debtors Near and Far

Our argument has implications that extend beyond the sovereign debt crisis and Germany. The threat of immigration into a creditor country may prompt that government respond more aggressively to credit crunches in other countries. Consider the cases of Mexico and Argentina. Both are middle-income countries with important trade linkages to the United States. Both countries experienced debt crises in the 1990s. Yet, the United States hurried to Mexico’s aid, providing a generous bailout package while it stood on the sidelines and allowed the IMF to negotiate with Argentina over the terms of its rescue package.

Our argument suggests that the key difference between the two cases is the threat of immigration in the event of an economic meltdown. Mexico’s proximity to the United States meant that a tidal wave of immigrants was quite possible—immigration that would have been politically unpopular for the Clinton administration. 30 Although Argentina has a sizable ex-pat community, its emigrants are spread around the world. And given its remote proximity to the United States and other creditor countries, the United States was not faced with the imminent threat of increased immigration from Argentina. Hence, there was much less urgency to the Argentine bailout from the U.S. perspective.

Or consider the decisions made by the United Kingdom in the initial days of the crisis. The United Kingdom chose to provide funds to help Ireland with its fiscal crisis, but neglected to provide similar support to Iceland, even though British depositors were exposed to bank closures in both countries. Our argument suggests that potential immigration into the United Kingdom explains this response. Whereas Irish workers could easily move to Britain to find work, Iceland’s small population and relative distance from British shores meant that it was unlikely that Icelandic immigrants would arrive in enough numbers to affect the British labor market. Thus, from a domestic political perspective, it was less pressing to come to Iceland’s aid.

Our counterfactual argument shows that we cannot examine the implications of capital mobility and labor mobility in isolation. Potential migration pressure is an important factor in how governments in creditor countries respond to financial crises. Just as importantly, the potential for migration shapes how creditor countries offer assistance to deter that possibility. 31

Footnotes

Appendix

Acknowledgements

We are grateful to Andy Baker, Sonal Pandya, Christina Schneider, Tom Pepinsky, and the seminar participants at University of Zurich, University of Virginia, The College of William and Mary, Duke University, and the London School of Economics, as well as audience members at the International Political Economy Society for helpful comments. We are also grateful to Jennifer Fitzgerald and Frigyes Ferdinand Heinz and Yan Sun for sharing data and to Gabriel Noronha, Isabelle Merritt, and Julia Janka for their excellent research assistance.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.