Abstract

In this study, we examined financial stress and general anxiety in college students (N = 304) with attention to the moderating roles of different types of social support (i.e., family support, social support) and gender, as assessed via moderated moderation. Results indicated that financial stress was moderately-to-strongly associated with symptoms of general anxiety. A three-way interaction revealed that perceived family support and gender were moderators of financial stress in relation to general anxiety. Consistent with a stress-buffering effect, for male college students financial strain was positively associated with general anxiety at low levels of perceived family support, but unrelated at high levels of family support. For female college students, a significant financial stress–anxiety link was present regardless of level of family support. This study highlights the potential mental health costs of financial stress faced by college students, with implications for tailoring mental health interventions that target financial stress.

Anxiety and stress rank as the top two client concerns observed by clinicians in college counseling centers (Center for Collegiate Mental Health [CCMH], 2016). As anxiety concerns have steadily increased in recent years for college students (CCMH, 2016), financial stress also has emerged as a prevalent concern in this population. For instance, approximately seven out of 10 college students endorsed experiencing stress about their personal finances in a multisite study (Heckman, Lim, & Montalto, 2014). The stress–coping literature suggests that having positive social supports, including support provided by family or kin (i.e., family support) or by one’s social network more generally (i.e., general social support), can buffer against stress (Cohen & Wills, 1985). Other research indicates women are more likely to report financial stress than men (e.g., Brougham, Zail, Mendoza, & Miller, 2009). However, it is unknown if there are gender variations in the potential roles of social supports in disrupting the link between financial stress and general anxiety among college students. Using a moderated moderation model, the current study examined the links between financial stress and general anxiety in a college student sample, with specific attention to the potential moderating roles of social support (including perceived family support and general social support) and self-identified gender. Specifically, this study aimed to address the research question: Is there a buffering effect of social support (i.e., general support, perceived family support) on the relation between perceived financial stress and general anxiety, and does this buffering effect differ by gender? At a time when financial burdens in college are receiving increased national attention, financial stress among college students remains an understudied empirical topic, with even less attention paid to its mental health correlates.

Financial Stress and Social Support From a Stress–Coping Perspective

Personal financial concerns repeatedly rank as a top source of stress among adults in the United States, with nearly three-quarters of adults (72%) endorsing stress about money and nearly one in three adults (29%) reporting increased stress about money (American Psychological Association [APA], 2015, 2016). Young adults, including college students, are emerging as a cohort reporting some of the highest levels of stress about money (APA, 2015; Heckman et al., 2014; Tran, Mintert, Llamas, & Lam, 2018). Financial stressors for many college students are diverse and can include typical living expenses, tuition and academic expenses, overspending or credit card debt, student loan debt, work–school–life balance, financial pressures from family, and uncertain employment after graduation (Beiter et al., 2015; Heckman et al., 2014; London, 1989; Nelson, Lust, Story, & Ehlinger, 2008; Wisconsin HOPE Lab, 2016).

The emergence of financial concerns as a major, widespread source of stress for young adults comes at a time when general anxiety and stress have reached peak levels among college students (American College Health Association [ACHA], 2017; Association for University and College Counseling Center Directors, 2016; CCMH, 2016). Well over half of college students (61.9%) report feeling “overwhelming anxiety” in the past year; more than a quarter (26.5%) describe that past-year anxiety has influenced their academic performance, and nearly one in five (19.7%) characterize their anxiety as reaching clinical levels for which they received a diagnosis or were treated by a professional (ACHA, 2017). Moreover, a gender difference is notable, as the estimated rate of “overwhelming anxiety” for female college students (67.7%) far exceeds that of male students (47.4%; ACHA, 2017).

Among the potential contributing factors, financial stressors have been linked to health and adjustment concerns, including mental health issues such as anxiety and depression (APA, 2015; Kahn & Pearlin, 2006; Tran et al., 2018). In a multisite investigation, 78% of college students who attempted suicide cited financial stress as a reason (Westefeld et al., 2005). In the college context, financial stress has been linked to reduced course load or dropout and poorer academic performance (Dwyer, Hodson, & McLoud, 2013; Joo, Bagwell Durband, & Grable, 2008). In short, the mental health and adjustment implications of financial stress for college students should not be dismissed, and general anxiety may be among the most proximal health correlates of financial stress.

Stress–coping models underscore that the presence of stress does not guarantee an aversive health outcome, as adaptive coping can disrupt the stress–health link (e.g., Lazarus & Folkman, 1984). Social support has long been regarded as a major coping resource for individuals who are experiencing a stressor such as financial stress (Cohen & Wills, 1985; Pearlin & Schooler, 1978; Thoits, 1995). Support from others can be instrumental (e.g., supplying tangible resources), informational (e.g., providing advice to guide problem-solving), and/or emotional (e.g., caring, building esteem, providing encouragement, offering sympathy, fostering a sense of belonging) and has been cited as a buffer against major stressful life events or chronic difficulties (Peirce, Frone, Russell, & Cooper, 1996; Shor, Roelfs, & Yogev, 2013; Thoits, 1995).

Adults who indicate having emotional social support report lower stress and stress-based depression symptoms than those who indicate having no emotional social support (APA, 2015). Results from meta-analyses on social support and mortality indicate the risk of death for individuals with high social support is approximately 11% lower compared to those with low levels of social support (Shor et al., 2013). Social support from one’s family or kin network has been found to be particularly robust in promoting well-being. For instance, meta-analytic research indicates that low levels of family support were associated with greater mortality risk compared to high levels of support from family; and the health benefits associated with family support are greater than those derived from support provided by friends or acquaintances (Shor et al., 2013). From a stress–coping perspective, more social supports—including family support—may have a stress-buffering role in the relation between financial stress and general anxiety among college students.

Gender Contexts of Financial Stress and Gender Socialization Theory

According to gender socialization theory, men and women are socialized with emphasis on different roles, values, thoughts, and behaviors (Fagot, Rodgers, & Leinbach, 2000). Limited research has suggested that money is a more central component of the socialization processes and identities of men compared to women (Newcomb & Rabow, 1999), although there is not clear evidence that financial concerns are necessarily more influential for men. For instance, financial stress has been tied to greater chronic illness (e.g., high blood pressure, heart disease) in women but not men in a general Canadian sample aged 20 years and older (Denton, Prus, & Wills, 2004). Other research on a Canadian adult sample found that financial stress (i.e., lack of money for necessities) was linked to chronic illness and distress for both men and women (McDonough & Walters, 2001). There is also evidence that men and women in college face different financial experiences that could result in gender differences in health sequelae, but it remains unclear which group would be more adversely influenced by financial stress. For example, female college students, in comparison to their male counterparts, are more likely to take out loans and persist in obtaining their degrees despite debt (Dwyer et al., 2013). These findings could imply that student loan debt may be less aversive for female than for male students’ mental health. Conversely, the findings may mask the financial stress faced by males if those males most burdened by student loan debt leave college prematurely, leaving a unique sample of male college students who are able to persist in their college education despite debt. Comparatively, then, females who persist in college may be doing so with heavy psychological and financial burdens. Thus, gender appears to be an important factor in conceptualizing the health impact of financial stress, but extant research has yielded mixed findings on the nature of gender effects, suggesting a need for further investigation.

Furthermore, gender differences and variations in gender socialization processes may be relevant when conceptualizing social support as a protective factor. Men are traditionally socialized to be self-reliant (e.g., Addis & Mahalik, 2003), whereas women are more likely to be socialized to seek support (e.g., Fivush & Buckner, 2000); this may prime men to be less likely to utilize, and benefit from, social support than women. However, research is mixed as to whether the links between social support and health outcomes differ for men and women, with some results suggesting both men and women similarly benefit from social support, and others providing inconsistent results (see Shor et al., 2013 for a review; see also Uchino, Cacioppo, & Kiecolt-Glaser, 1996).

Although there is evidence suggesting gender variations in the stress-buffering effect of social support in relation to financial stress, the research again is unclear regarding which gender group experiences the protective benefits. Past research documents gender differences in levels of personal financial stress, with women being more likely to endorse greater stress about money than men (e.g., APA, 2015; Åslund, Larm, Starrin, & Nilsson, 2014; Brougham et al., 2009). These differences may suggest greater potency of, and greater exposure to, financial stress in women, which may place them at heightened risk for general anxiety stemming from financial stress. For example, it is possible the stress–health link is so strong as to persist in spite of social supports for women. Research has shown that women are more likely to report having emotional support than men (APA, 2015), and meta-analytic research suggests that women are more likely than men to seek social support for instrumental and emotional coping reasons (Tamres, Janicki, & Helgeson, 2002). However, compared to men, women report higher levels of past-month isolation and loneliness due to stress, as well as higher levels of unmet need for more emotional support in the last year (APA, 2015). Furthermore, in the limited research focused on family support, poorer family support has been implicated in loneliness for women, but not for men (Lee & Goldstein, 2016). These findings render it plausible that women may not derive the stress-buffering effect expected of social supports in the context of financial stress.

On the other hand, there is also evidence suggesting that men may be especially at risk for negative outcomes associated with financial stress in college. For instance, men are more likely to drop out of college at lower levels of student loan debt than women, perhaps signaling a lower threshold of tolerance for the financial stress associated with debt (Dwyer et al., 2013). Outside of the college context, men have been found to report higher levels of stress than women about financial factors (e.g., Denton et al., 2004; McDonough & Walters, 2001). Despite such risk, there is limited evidence suggesting social support may be more effective in combating financial stress in men than in women. For instance, research on a general Swedish adult sample demonstrated that greater instrumental social support had a more prominent buffering effect for men than women with regard to the inverse relation between financial strain (i.e., difficulty paying monthly expenses and raising emergency funds) and psychological well-being (Åslund et al., 2014). Although it is uncertain if this finding would apply to a college sample in the United States, altogether the limited evidence and mixed findings suggest it is possible that the stress-buffering effect of social supports may vary across men and women in the relation between financial stress and general anxiety, but the direction remains unclear.

The basis of gender socialization theory and its applications is the socially constructed nature of gender. Whereas sex represents male or female biological traits (e.g., reproductive organs), gender reflects the socially constructed self-identification and internalization of oneself as a man, woman, or as having a non-binary identity, that is developed through an individual’s observations of, and interactions with, others in their environment (APA, n.d.; Bem, 1981). As individuals are socialized and, therefore, treated differently based upon sex or perceived sex, gender as reflected by one’s self-identification as a man or a woman (or other non-binary identity) may be a more influential determinant than biological sex in the links between social processes and mental health (APA, 2011; Unger, 1979). In this study, we draw on a definition and associated terminology of gender identity based on participants’ self-identification as “male” or “female” to examine gender differences in the moderating effects of social support on the link between financial stress and general anxiety (APA, n.d.). We recognize that in some literature male/female is used exclusively to denote sex and man/woman to identify gender. In the remainder of this article, we use the terms male, female, man, woman, and their plural forms interchangeably to refer to gender.

Present Study

In the current study, we aimed to understand financial stress and its relevance to mental health, specifically general anxiety, for male and female college students. The study examined moderated moderation models in which perceived family support and general social support are each considered for their potential stress-buffering effects, and the possibility of variations in these effects is considered for males and females. Current literature suggests that social support provides a buffering effect against stressors (e.g., financial stress) and the manifestation of stress (e.g., general anxiety). Given that meta-analytic research has found family support stands out as particularly influential (i.e., Shor et al., 2013), we considered it valuable to isolate its effect by examining it separately from general social support. Furthermore, research appears to show that men and women tend to utilize social supports differently, and therefore, may have different health outcomes as a result.

We hypothesized financial stress would be associated with greater self-reported symptoms of general anxiety. For both family and general social support, we further hypothesized that more support would mitigate the anxiety associated with financial stress, and that there would be gender variations in this stress-buffering effect. As there is neither clear nor robust empirical or theoretical basis to hypothesize the direction of these differences, we did not make specific predictions regarding the proposed moderating effect of gender within the moderated moderation model.

Method

Sample and Procedures

The sample was comprised of 304 college students drawn from a larger online study. The larger study, the Financial and Social Stress Study, was comprised of a single primary data collection focusing on adult financial and social experiences; this study is the first manuscript from the larger research project (Tran & Mintert, n.d.). Adults (18 years old and older) were recruited across multiple forums, including universities nationwide (e.g., email distribution to student groups, instructors, campus registrars), listservs, and social media outlets (e.g., Reddit). At survey completion, college students received one extra credit point when allowed by the instructor, and all participants were given the opportunity to enter a raffle drawing for Amazon gift cards. Participants indicated consent via a digital consent process and completed the online survey using Qualtrics. All items related to the primary study variables required responses, resulting in no missing values for these items. Of the 357 students who identified as currently enrolled in college, 50 participants (14%) were excluded due to inaccurate responses on validity questions (e.g., “Mark 3 for this question”). This exclusion rate is consistent with rates of careless responding in existing research on college student samples (approximately 10–60%; Meade & Craig, 2012).

Within the final sample, 71.7% self-identified as female (n = 218) and 28.3% self-identified as male (n = 86). Those who self-identified their gender as “other” (n = 3) were excluded due to insufficient sample size to allow for meaningful comparison and interpretation. The age of the participants ranged from 18 to 61 years old (M = 20.98, SD = 4.91). Four participants indicated they were not within the range of 18–28 years, but did not complete an open-ended field for their age either voluntarily or because an administrative error that resulted in the space for the open-ended response not being available to initial respondents of the survey. The self-identified racial and/or ethnic breakdown of the sample was 61.8% non-Latino White/European American, 18.8% Latino, 8.9% Multiracial, 6.6% Asian/Asian American, 1.6% African American/Black, 2.0% other, and 0.3% Middle Eastern/Arab American. Approximately a quarter of the sample was in the first year (26.3%), second year (28.3%), or third year (24.7%) in college; the remainder was in their fourth year (15.1%), or fifth year or later (5.6%). More than half of the sample (55.6%; 52.3% of males and 56.9% of females) described their current financial situation by selecting the statement “it’s tight but I’m doing fine,” whereas 27.6% of the sample (36.0% of males and 24.3% of females) described “finances aren’t really a problem.” By contrast, a sizeable minority (16.8%; 11.6% of males and 18.8% of females) characterized their current financial situation as “it’s a financial struggle.”

Measures

General anxiety

The seven-item Generalized Anxiety Disorder scale (GAD-7; Spitzer, Kroenke, Williams, & Lowe, 2006) is among the most widely used measures of frequency of general anxiety symptoms (e.g., “Over the last 2 weeks, how often have you been bothered by the following problems?”. . . “Feeling nervous, anxious or on edge;” “Becoming easily annoyed or irritable”). Response options were given on a 4-point frequency scale (1 = not at all, 4 = nearly every day). Higher mean scores indicate greater anxiety. The GAD-7 was previously validated and demonstrated good internal reliability (α = .92) in a sample of patients of primary care locations in 12 states (Spitzer et al., 2006). Most (89%) clinical patients with generalized anxiety disorder report summed GAD-7 scores of 10 or greater, and the scale has been shown to correlate with medical outcomes (i.e., mental health, social functioning), disability days, and healthcare use (Spitzer et al., 2006). In the present sample, approximately two-thirds (66.4%) had summed GAD-7 scores of 10 or greater, which is consistent with rates of past-year endorsement of “overwhelming anxiety” (61.9%) in national samples of college students (ACHA, 2017). The reliability score was good in the present sample (α = .91).

Financial stress

The seven-item Financial Anxiety Scale (Archuleta, Dale, & Spann, 2013) was developed largely based on items from the GAD-7 adapted to be specific to financial stress (e.g., “I feel anxious about my financial situation” or “I feel fatigued because I worry about my financial situation.”). Responses indicated frequency on a 7-point scale (1 = never, 7 = always), with higher mean scores indicating greater financial stress. The scale was initially developed and tested on a sample of college students and correlated positively with student loan debt, other debt, and total debt and correlated negatively with financial satisfaction. In the original validation study (Archuleta et al., 2013), the Financial Anxiety Scale had a mean score of 2.84 (SD = 2.43) in a sample of college students, which is relatively consistent with the current sample (M = 2.57, SD = 1.39). The scale was found to have good reliability (α = .94) in the original study, as well as the current study (α = .94).

Perceived family support

The 13-item Kinship Social Support scale (Taylor, Casten, & Flickinger, 1993) was used to measure perceived social and emotional support from family and/or relatives. Sample items included “I can count on my family/relatives to help when I have problems” and “One of the good things in life for me is to talk and have fun with my family/relatives.” Responses are reported on a 4-point Likert-type scale (1 = strongly disagree, 4 = strongly agree). The measure was developed in samples of African American adolescents (e.g., Taylor, 1996; Taylor et al., 1993), in which perceived family support was found to correlate positively with self-reliance, authoritative parenting, parental involvement in schooling, family organization, and grades; and to correlate negatively with behavioral problems. In the original study by Taylor et al. (1993), the reliability estimate was acceptable (α = .72). In the current sample, the scale yielded a good reliability score (α = .90).

General social support

In a study of social capital and college students, Ellison, Steinfield, and Lampe (2007) utilized a five-item measure of “bonding social capital” that indexed students’ social support in their local context (i.e., Michigan State University). Adaptations to the five items were made for use in the present study that centered on making the items generalizable to a national context, making them less about social capital (i.e., the resources derived from social networks within a given community) and more about individual perceptions of social support (see Uphoff, Pickett, Cabieses, Small, & Wright, 2013 for a discussion). Additionally, the dollar value referenced in one item (“If I needed an emergency loan of $100, I know someone at Michigan State University I can turn to”) was updated to $500 to obtain more variation in hardship and social resources (“If I needed an emergency loan of $500, I know someone I can turn to”). Other sample items include: “The people I interact with would be good job references for me,” and “There is someone I can turn to for advice about making very important decisions,” with a response scale ranging from 1 (strongly disagree) to 5 (strongly agree). The scale scores correlated positively with self-esteem and satisfaction with life scores in the original study, yielding an acceptable reliability estimate (α = .75). In the current sample, the reliability score was α = .68.

Demographic measures

Participants reported on standard demographic items such as gender, age, race and/or ethnicity, year in college, and employment status. In addition, a single item from the 2015–2016 Healthy Minds Study (an annual online survey of the mental health of university students; Healthy Minds Network, 2017) asked respondents to describe their current financial situation with three choices: “It’s a financial struggle,” “It’s tight but I’m doing fine,” and “Finances aren’t really a problem.”

Results

Descriptive Statistics and Preliminary Analyses

An a priori statistical power analysis with a medium effect size (α = .05; power = 0.80; Cohen, 1988) was performed for sample size estimation via G*Power version 3.1. The projected sample size needed with eight predictor variables was approximately N = 109, suggesting the final sample size of 304 was adequate.

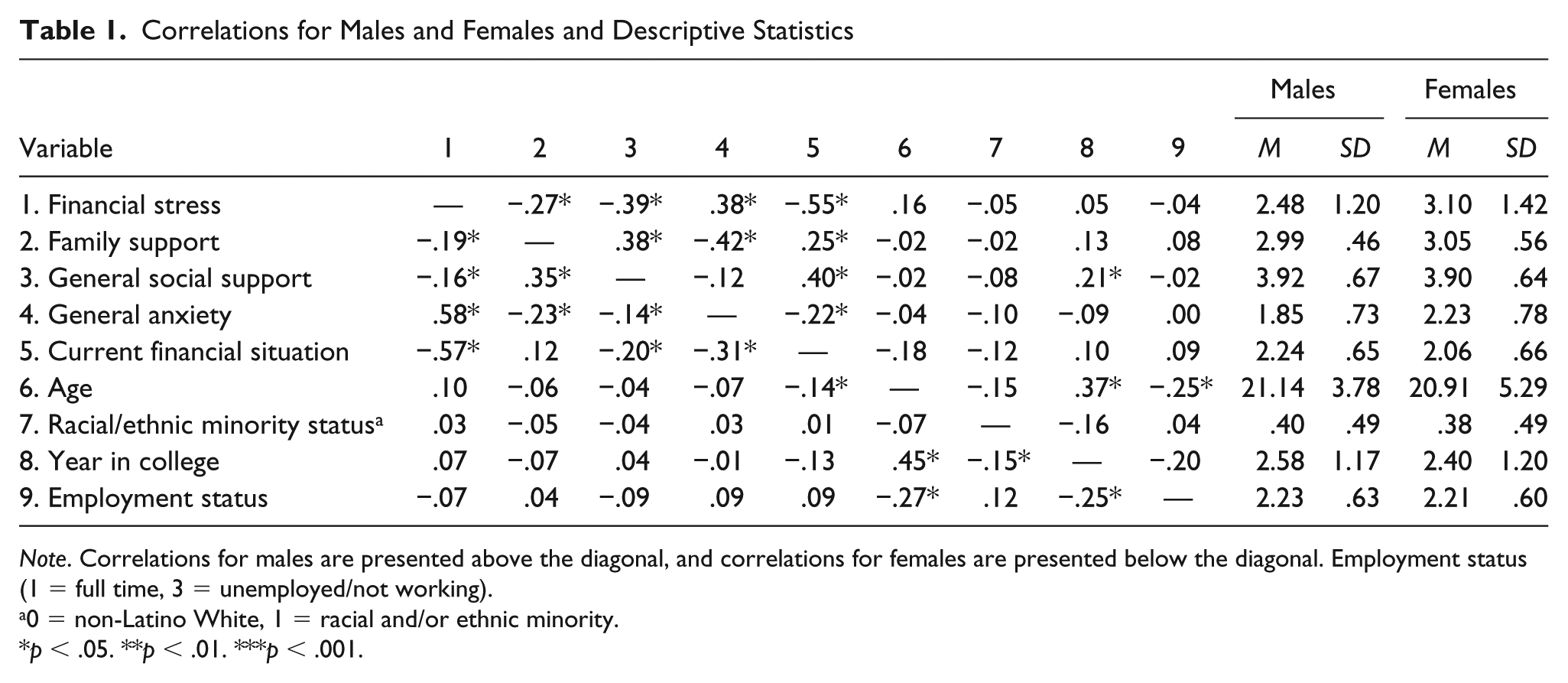

Table 1 presents descriptive statistics and correlations for the study’s primary variables. Pearson correlations suggested financial stress was moderately tied to general anxiety for males, and strongly correlated with general anxiety for females, using Cohen’s (1992) conventions as guides for characterizing small (r = .10), medium (r = .30), and large (r = .50) effect sizes for correlations.

Correlations for Males and Females and Descriptive Statistics

Note. Correlations for males are presented above the diagonal, and correlations for females are presented below the diagonal. Employment status (1 = full time, 3 = unemployed/not working).

0 = non-Latino White, 1 = racial and/or ethnic minority.

p < .05. **p < .01. ***p < .001.

Across participants of both genders, there was a moderate positive correlation between perceived family support and general social support. Lower family support was linked to greater financial stress and general anxiety at moderate effect size levels for males and small-moderate effect size levels for females. For females, there were small, negative associations for general social support with financial stress and general anxiety, whereas for males, general social support was moderately correlated with financial stress but uncorrelated with general anxiety. Demographic variables were assessed for their relations to the study criterion variable (general anxiety) for consideration as covariates. For males and females, a better current financial situation was moderately associated with lower general anxiety. No other demographic variables were correlated with anxiety. Based on these results, current financial situation was included as a covariate in the moderated moderation analyses.

Independent samples t-tests indicated significant gender differences in financial stress and general anxiety. The female sample reported higher mean levels of financial stress relative to the male sample, consistent with a medium effect size, Cohen’s d = 0.47, per Cohen’s (1992) guidelines (small: d = 0.20, medium: d = 0.50, large: d = 0.80). Females also exhibited higher levels of anxiety symptoms, on average, than males, Cohen’s d = .50. There was no significant gender difference in family support, Cohen’s d = .12, or in general social support, Cohen’s d = .03. Chi-square tests of independence suggested no gender differences in current financial situation, χ2(2) = 5.20, p = .074. Independent samples t-tests and chi-square tests suggested that male and female participants did not differ on other demographic variables (i.e., age, racial and/or ethnic minority status, year in college, employment status).

Moderated Moderation: Tests of the Buffering Effect of Social Supports

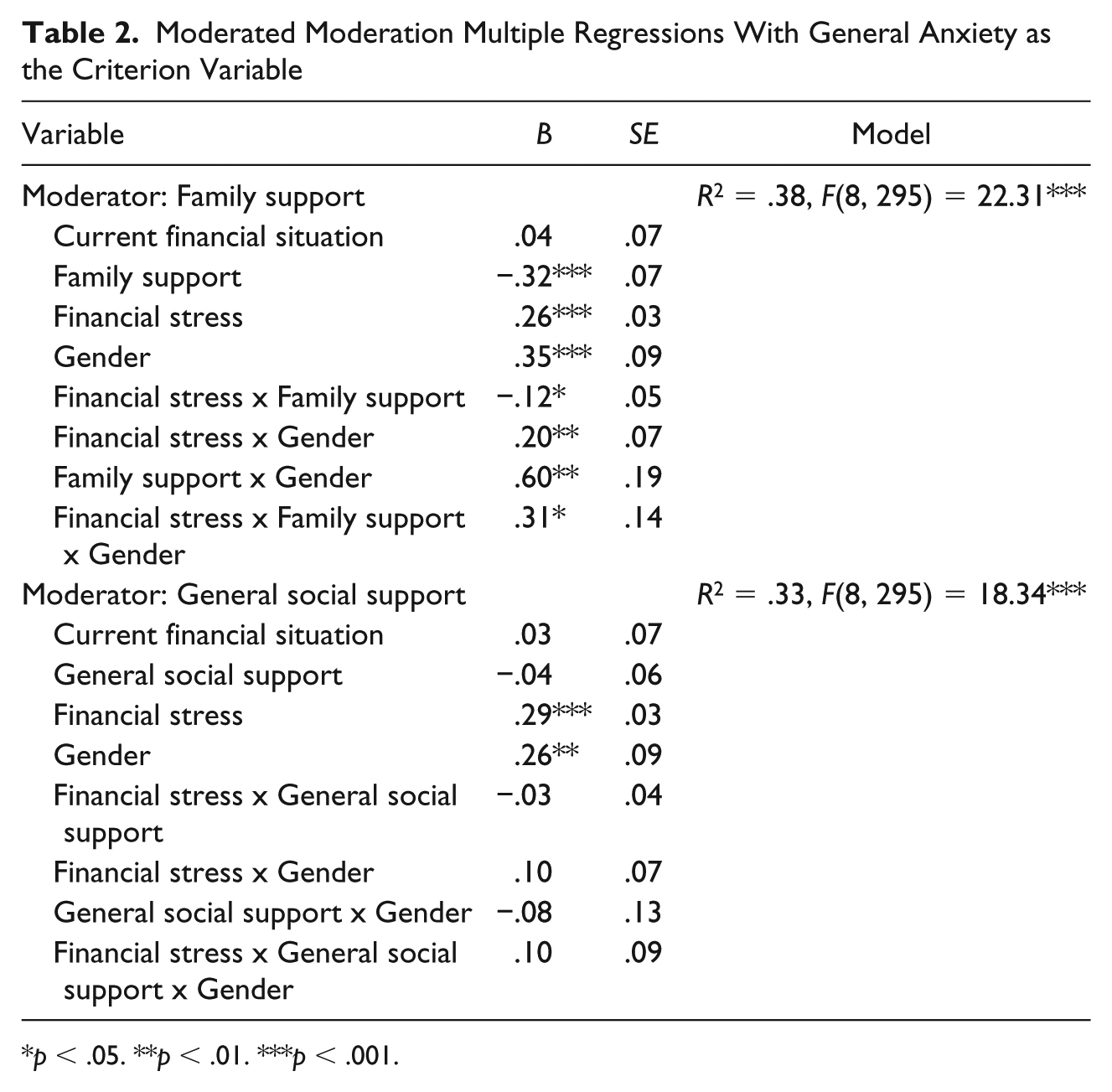

The three-way interactions [financial stress x social supports (perceived family support or general social support) x gender (1 = male; 2 = female)] with current financial situation as a covariate were examined with moderated moderation models (X x M x W→Y) using the PROCESS macro (version 2.16.3 for SPSS [v. 24]; Hayes, 2012). The PROCESS macro provided three-way multiple regression results based on centered predictor data, as well as follow-up simple slopes analyses of significant three-way interactions for males and females at high (+1 standard deviation) and low (-1 standard deviation) levels of support (see Table 2). In a visual inspection of the residual scatter plots, P-P plots, and histograms, we found no evidence of nonlinear associations, significant departures from normality, or concerns regarding heteroscedasticity. Tolerance (> .71) and VIF (< 1.42) values indicated no major issues regarding multicollinearity.

Moderated Moderation Multiple Regressions With General Anxiety as the Criterion Variable

p < .05. **p < .01. ***p < .001.

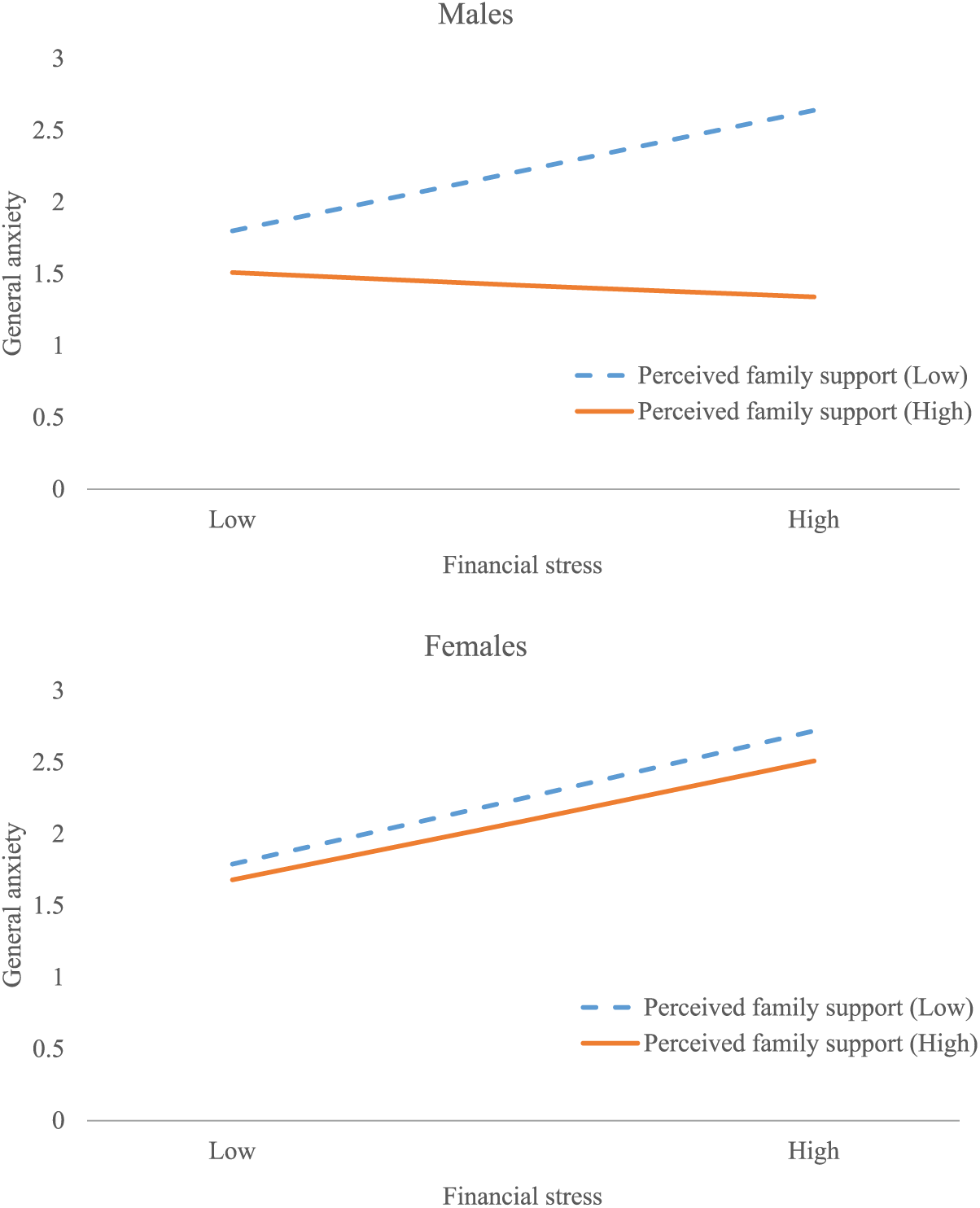

In testing the moderated moderation model with perceived family support, main effect results were consistent with preliminary correlational and t-test results. Greater financial stress was associated with greater general anxiety symptoms; more family support was tied to lower general anxiety; and females endorsed greater general anxiety than males, controlling for current financial situation. All two-way interactions (financial stress x family support, financial stress x gender, and family support x gender) were significant. The main effects and two-way interactions were qualified by the hypothesized three-way interaction, ΔR2 = .01, F(1, 295) = 4.70, p = .03. Follow-up analyses indicated the financial stress x family support interaction was significant for male college students (B = -.34, SE = .13, p = .01), but not female college students (B = -.03, SE = .05, p = .48). Simple slopes analyses (Figure 1) indicated financial stress was not significantly related to general anxiety for male college students reporting high family support (B = -.06, SE = .12, p = .60). By contrast, for male college students who reported low family social support, the significant association between financial stress and general anxiety persisted (B = .30, SE = .08, p < .001). In other words, the moderating effect of family support for the male college student sample was consistent with stress-buffering. For female college students, the positive association between financial stress and general anxiety remained significant regardless of high (B = .30, SE = .04, p < .001) or low (B = .33, SE = .04, p < .001) family social support. In the case of general social support, financial stress also was related to greater general anxiety in main effect analyses, and females reported greater general anxiety when controlling for current financial situation. Interestingly, general social support was not linked to anxiety. There were no significant two-way or three-way interactions, ΔR2 = .003, F(1, 295) = 1.31, p = .25.

Interaction between financial stress and perceived family support.

In post hoc analyses, general social support was entered as a covariate in the perceived family support moderated moderation model, and perceived family support was controlled for in the general social support moderated moderation model. 1 The results were consistent with initial analyses without these controls, supporting the robustness of the effects for the specific source of social support. Analyses were also conducted without current financial situation as a covariate, yielding the same pattern of findings (significant three-way interaction for family social support with the same pattern of simple slopes; nonsignificant three-way interaction for general social support).

Discussion

When facing stress related to personal financial resources, many college students might turn to their social resources. The present study examined whether there is a buffering effect of social support (i.e., general support, perceived family support) on the relation between perceived financial stress and general anxiety, and whether this buffering effect differs for male and female college students. The results were significant for affirming the link between financial stress and general anxiety among college students, while also revealing that perceived family support may nullify the link for male college students. Specifically, we found a moderated moderation effect for perceived family support, but not general social support, in which family support appeared protective in the context of financial stress for males. This study highlights the psychologically aversive nature of financial stress in the college context, but offers hope that factors such as family support may serve as protective factors for some individuals.

The first major consideration that emerges from the study is the affirmation that stressful financial circumstances are tied to general anxiety for college students. Previous literature has emphasized the role of financial factors (e.g., financial aid) in academic outcomes, including nonpersistence (e.g., Nora, Cabrera, Serra Hagedorn, & Pascarella, 1996), but the link to mental health has not been well-established empirically. Although this finding may seem intuitive, college students generally are not regarded as vulnerable to the risks associated with financial stress, particularly given the financial resources implied in being able to attend college and the relatively auspicious financial prospects of obtaining a college degree versus not obtaining one (e.g., Hershbein & Kerney, 2014). Thus, the financial stress and mental health correlates of college students could be underestimated or overlooked. Our findings along with other research (e.g., Tran et al., 2018; Westefeld et al., 2005), supports that stressful financial circumstances can be common among college students and can have significant mental health and academic costs (e.g., Joo et al., 2008).

The present study further offers nuanced perspectives on the complex circumstances surrounding the conditions in which financial stress is tied to anxiety for college students, including gender contexts. Although the anxiety levels of both our male and female college student subsamples appeared to be adversely tied to financial strains (i.e., poorer current financial situations, financial stress), females demonstrated unique risk in that they reported moderately higher levels of financial stress despite no group-level gender differences in current financial situation; the correlation between financial stress and anxiety was stronger for females relative to males; and female college students in the present sample were not similarly benefited by a stress-buffering effect of perceived family support as their male counterparts. The persistence of the strong correlation between financial stress and general anxiety for female college students, regardless of level of perceived family support, suggests that financial stress may be especially harmful to their mental health.

Although a number of studies have documented greater availability and use of social support among women relative to men (e.g., Denton et al., 2004; Tamres et al., 2002), some scholars question the assumption that women would benefit from social supports, as women’s social network involvement can be conceptualized as a liability (McDonough & Walters, 2001; Walen & Lachman, 2000). Kawachi and Berkman (2001) proposed that more frequent social network involvement may place women at risk of “contagion of stress” (p. 462). Indeed, women have been found to have higher levels of social life stress than men (McDonough & Walters, 2001). Kawachi and Berkman (2001) further argued that women with fewer socioeconomic resources are particularly at risk because, compared to those with more resources, they may have greater difficulty in responding to the needs of significant others, may be less likely to receive support from their social network, and may be encumbered by obligations within their social networks. One way in which the current findings might be extended is by offering a multifaceted analysis of both the supports and strains of family and general social networks within the context of financial stress and mental health among college students (e.g., Walen & Lachman, 2000). Moreover, as the present results do not shed light on a stress-buffering mechanism for female college students faced with financial stress, a pressing direction for future research is the identification of protective factors that address their unique financial experiences.

In contrast, the moderated moderation results revealed that the stress-buffering effect of perceived family support was restricted to male college students facing financial stress. For male college students who reported low levels of family support, the link of greater financial stress and higher general anxiety suggested in the extant literature persisted. However, for male college students reporting high levels of family support, this link was disrupted, suggesting family support may be protective for this population. Our findings could suggest that men who counter traditional gender-socialized values emphasizing self-reliance may be better enabled to enjoy the psychological benefit of close kinship ties and resources (e.g., DeFranc & Mahalik, 2002).

The results showed that perceived family support demonstrated stress-buffering potential against financial stress, whereas general social support did not, among male participants. These findings held when controlling for the other respective type of social support (e.g., controlling for general social support in the perceived family support analysis), suggesting some robustness of the effects. The important role of family support is consistent with previous research that demonstrates a compelling positive health benefit of family support, and no benefit for friend or acquaintance support (Shor et al., 2013). It is also consistent with other research suggesting that connections with family have a different effect on health than connections with peers (e.g., Carter, McGee, Taylor, & Williams, 2007). Understandably, family may provide a safety net for college students, particularly male college students, who may be navigating a number of financial concerns for the first time. Family also may be uniquely equipped to provide trusted socialization, advisement, and emotional support in the specific case of financial matters (Lyons, Scherpf, & Roberts, 2006). It is notable in the present study that family support was operationalized with items spanning emotional, informational, and instrumental forms of support, suggesting family support generally may be valuable to males faced with financial stress during college. Thus, the study findings challenge a specificity hypothesis of social support, which contends a person experiencing a given life stressor benefits from support aimed at alleviating that specific type of stress (i.e., individuals suffering from financial stress benefit the most from instrumental or tangible family supports specifically targeting financial needs; Peirce et al., 1996). More research is needed to test the relative contribution of each type of family support in combating the effects of financial stress on female and male college students.

Practical Implications

The significant links between current financial situation, financial stress, and anxiety draw attention to the mental health costs and clinical relevance of financial strain faced by many college students. The findings emphasize that placing a major focus on stressful financial circumstances is important for those working with college students, including counseling psychologists providing direct mental health services, as well as college staff, educators, and administrators. Counseling psychologists might engage in outreach efforts with financial aid offices to alert staff to mental health risks for students, facilitate mental health referral processes, and generate interrelated financial and mental health services. Additionally, there are documented financial stressors that are specific to the developmental context of being in college, such as being unable to afford the same activities as peers, and experiencing worry about impending student loans postgraduation (Heckman et al., 2014). These concerns could be addressed by offering frequent and widely accessible no- or low-cost campus recreational activities, and by providing programming focused on financial planning.

Our results also have practical implications for targeted interventions for men and women. When conceptualizing clients’ mental health needs, counseling professionals should recognize women college students as a group with heightened susceptibility to the mental health risks of financial stress. These students may benefit from targeted mental health interventions and campus outreach that aim to assess and alleviate financial pressures and strains. For example, university mental health professionals and financial aid officers could present psychoeducational lectures to student organizations predominantly composed of women, such as sororities, highlighting the relevance of financial stress on mental health. A financial skills-based counseling group for college students experiencing financial stress may be beneficial, as financial educational programs provided in a group format have shown beneficial outcomes, such as increasing financial knowledge and well-being among participants (e.g., Garman, Kim, Kratzer, Brunson, & Joo, 1999; Kim, 2007).

In working with college students, the results also suggest it is important to explore men’s perceptions of, and access to, family supports. It is important for clinicians to recognize that low levels of family support may pose concerns for male college students in the context of financial stress and mental health. Unfortunately, a quarter of young adults report having no emotional support, and a third report that stress has contributed to their sense of loneliness and isolation in the past month, placing students at risk (APA, 2015). Gender theory and research have long considered that men, especially, may face sociocultural pressures (e.g., gender socialization, masculinity stereotypes) that discourage them from seeking help from others (Addis & Mahalik, 2003; O’Brien, Hunt, & Hart, 2005). Male clients should be encouraged to draw on family support as they contend with financial stress, and clinicians may utilize different interventions (i.e., modeling, role-playing) to help these clients work through barriers to seeking support. Counseling psychologists might also partner with university financial aid services to create financial education programs for students’ families that bolster both parental socialization of financial knowledge relevant to the college context and parents’ awareness of the importance of family support in mitigating financial stress, especially for men.

Limitations and Future Research

As with other cross-sectional research, we cannot infer causal pathways from the findings. For instance, it is plausible college students with higher levels of anxiety may be more likely to perceive financial stress. Although longitudinal research is needed, additional cross-sectional studies examining different socioeconomic groups, including low-income, moderate-income, and high-income college students, would help to clarify how socioeconomic status may drive these processes differently. In addition, this study focused on the college student population, and the results may not be generalizable to others beyond this specific developmental context. It is also important to recognize that the amount and nature of financial stress and social supports change in later stages of adulthood (Walen & Lachman, 2000).

There are also a number of measurement considerations. The present study offers a limited perspective on participants’ current financial situation (i.e., a single item with three fairly general response options). In contrast, more nuanced analyses could incorporate more objective financial functioning measures (e.g., personal and family income), financial aid information, and student loan debt and repayment data. The study’s perspective on gender was also limited in its focus on a binary conceptualization of gender. It is possible that the gender item’s response option (male, female, other) may not have been reflective of other gender terminology and conceptualizations (e.g., man, woman); thus we cannot rule out the possibility that some individuals may have been reporting their biological sex rather than their gender self-identity. It is also worthwhile to note that the internal consistency score of the general social support scale was marginal (α = .68), which may have influenced the results. Future replication with different general social support instruments would help to strengthen confidence in the potential buffering role, or lack thereof, of general social support.

Although the present study makes important inroads in shedding light on the mental health costs of financial stress for college students in terms of general anxiety, which is currently among the top mental health concerns afflicting college students, it is critical for future studies to examine other mental health indicators. Gender variations in stress reactivity have been demonstrated depending on health outcomes. For instance, in a rural Midwestern sample, financial stress was tied to hostility in men, whereas it was linked to greater likelihood of somatic symptoms in women (Conger, Lorenz, Elder, Simons, & Ge, 1993). There could be variations in results depending on the mental health indicator measured, such as depression—another top mental health concern for college students (ACHA, 2017). Future research should also assess financial stress manifested in ways beyond self-perceptions, including physiological stress responses (e.g., cortisol levels).

Conclusion

Existing trends suggest current college students are faced with rising costs for attending college without an equivalent increase in financial aid (College Board, 2016). Thus, it could be expected that anxiety related to financial issues will continue to be an important factor affecting the mental health of college students. Our study is among the first to document the mental health correlates of financial stress among college students and to draw attention to possible protective mechanisms, such as family social support.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Notes

Author Biographies

![]() ) examines socioeconomic disparities, financial stressors, discrimination, ethnic–racial socialization, and ethnic minority psychology.

) examines socioeconomic disparities, financial stressors, discrimination, ethnic–racial socialization, and ethnic minority psychology.