Abstract

We examine the two-way links between foreign direct investments (FDI) in services and trade in services for 26 emerging economies from 2003 to 2015 using sectoral and sectoral disaggregated FDI data. Within a multivariate framework, we use panel unit root tests, recently developed heterogeneous panel cointegration and panel vector error correction model (VECM). Our results confirmed the cointegrating relationship between trade in services, FDI in services, financial services FDI and nonfinancial services FDI. We find the existence of long-run unidirectional causality from trade in services to FDI in services. However, the disaggregated analysis shows a bidirectional link between nonfinancial services FDI and trade in services in the short run. Still, there is no causality between financial services FDI and trade in services both in the short run and long run. The result also shows the evidence of unidirectional causality running from trade in services to nonfinancial services FDI in the long run. It implies that sectoral decomposition matters in the FDI–trade nexus in emerging economies.

Introduction

According to UN World Investment Report (UNCTAD, 2015), worldwide flows of foreign direct investment (FDI) have grown at unprecedented rates, to reach a total outflow of US$1.7 trillion in 2015 compared to the US$159 billion in 1991. This spurt in recent years can be attributed to the expansion of FDI in service industries. For example, FDI in services accounted for a quarter of worldwide FDI stock in 1970; by 1990, the percentage of services FDI had risen to 50%, and by 2005, the share of services FDI in global stock had risen to two-thirds (UNCTAD, 2015). The multinational company’s share in the world trade increases steadily over a period. These changes in the world led to changes in the overall trade pattern and performance of many countries, including emerging economies. The last two decades witnessed the emergence of the services sector as the most prominent sector in the global economy with more than 60% of total output and a larger employment generating sector (Hoekman & Mattoo, 2008). In addition to the employment and output generation, it also attracts a generous portion of total FDI (UNCTAD, 2009). Along with these, the tremendous increase of trade in services leads to an increase in productivity and large-scale production, leading to economic growth in both developed and emerging economies. This trend is more or less visible in world trade statistics; the ratio of services trade in goods trade was around 20% in 1980, which was increased to 27% in 2010 (WDI, 2011). This phenomenon is directly visible in emerging economies regarding improvements in service-led growth in the last three decades. FDI plays a vital role in trade in services across emerging economies and among developed economies.

The Industry Commission (Hardin & Holmes, 1997) argues that there is a high chance of complementarity between FDI and services trade, mainly because of the characteristics of the services sector. In trade literature, the contribution of FDI flows for trade in emerging economies has emerged as a subject undergoing intense study. Higher FDI inflows may influence the export pattern and export performance of the emerging economies, depending on the country-specific factors. Given these facts, we can observe both direct and indirect effects of FDI on exports. Zhang and Song (2001) argued that multinational firms could be considered a primary source to increase exports in the short run, especially if the domestic firms are lagging the multinational firms in terms of technologies and skilled labour. In terms of updated technology, international safety criteria and international social and distribution norms, the presence of multinational corporations has spilled over to local firms. The indirect benefits of FDI on exports or trade include the enhancement of domestic businesses’ competitiveness, which leads to a rise in indigenous firms’ exports. The export of domestic firms will also increase via vertical linkages of FDI. In the case of domestic firms, FDI is considered the main source for the upgradation of technology, quality of production and improved exports (Din, 1994). Because of the perishability, inseparability, intangibility, heterogeneity and commercial presence of the service sector, there has been no consensus on the relationship between FDI in services and commerce. When services are obtained from an international corporation rather than a domestic company, domestic customers perceive a higher level of risk. In the case of the service sector, commercial presence characteristics play a key role in the FDI–trade nexus.

Theoretical literature expects the linkages between FDI and trade will be strong. Still, it is less evident whether the relationship between FDI and trade holds at the sectoral and sub-sectoral levels. For example, countries with more manufacturing FDI may react differently to trade flows than countries with more service sector FDI. At the same time, the dimension of the FDI–trade nexus may change based on the motives and sources of FDI. We can find two kinds of FDI in the literature such as horizontal and vertical FDI. Horizontal FDI is nothing but the replication of the same production facility in the host countries. In contrast, the cheap raw materials and cost gaps tend to attract the foreign producers to split their production activities and invest in labour-intensive part of production in labour abundant countries and more capital-intensive part of production activities in capital abundant economies. This type of FDI is termed vertical FDI. The differences between the two motives determine the relationship between trade and FDI: vertical FDI and trade complement, whereas horizontal FDI substitutes trade. We can suggest that vertical FDI is more prevalent between developed and emerging economies based on the FDI inflows. However, in practice, we find hybrid patterns. Interestingly, we can find that the relationship between FDI and trade varies within the country since the motives of investing in particular host countries depend on several factors such as resources, cheap labour, market seeking and efficiency-seeking.

Although much empirical work has focused on aggregate FDI–trade nexus, the study which deal with the implications of sectoral and sub-sectoral effects of FDI on trade in services have received considerably less attention. Our article provides new insights on FDI–trade nexus in emerging economies. Minimal research has examined the sectoral FDI–trade nexus with little or no significant literature on services trade and services FDI, trade in services and sub-sectors (financial services and nonfinancial services) of services FDI in the context of emerging economies. Our aim is to provide an empirical assessment of the service sector, sub-sectoral relationships and trade relationships based on the aforementioned facts. In two ways, this study contributes to the existing literature. It begins by attempting to examine FDI in services and trade linkages in emerging economies. Second, our article is one of the first to investigate the FDI–trade nexus utilising sectoral and more precise sectoral disaggregated data, with a specific focus on developing economies.

The remaining portion of the article is divided into five sections. The second section presents a summary of the available literature on the FDI–trade relationship. The data description and descriptive statistics are covered in the third section. The fourth discusses econometric methods and empirical findings. The fifth section concludes the article.

Literature Review

While there has been no consensus on the nexus between trade and FDI, the empirical literature of this relationship provides mixed results. Some studies are in line with the theoretical expectation that FDI improves exports (Leichenko & Erickson, 1997; Xuan & Xing, 2008), while some other studies show that the impacts of FDI on host country’s export need not always be positive (Sharma, 2003; Lall & Mohammad, 1983). The presence of foreign affiliates will improve the export performance of host countries (Javorcik et al., 2018). At the same time, many studies find that FDI inflows are considered an essential factor in export upgrading for both the host and recipient countries (Harding & Javorcik, 2012; Javorcik et al., 2018; Sharma, 2003). A stratum of the existing literature finds a complementary relationship between FDI and host country exports (Blake & Pain, 1994; O’Sullivan, 1993).

Contrarily, FDI has some adverse effects on the host country’s exports by substituting domestic investment. Domestic suppliers of entrepreneurs find it difficult to take up the latest technologies due to lack of human capital and unavailability of funds, especially in the case of emerging and developing economies. FDI also affects the export pattern and performance of host countries, and one of the main reasons for this negative effect is the host country’s comparative advantage (Lin et al., 2009). Most of the studies in existing literature reveal that there exists a positive relationship between FDI and export (Grossman & Helpman, 1989; Hejazi & Safarian, 2001; Helpman, 1984; Lipsey & Weiss, 1981; Pfaffermayr, 1994). In contrast to this, a stratum of existing literature finds that FDI has negative impacts on the host country’s export (Mundell, 1957; Svensson, 1996). Young and Hood (1976) examine the role of MNCs in the export of manufactured goods and find that the relationship between export and FDI varies from country to country. Findings indicate that foreign ownership improves the export performance of less developed economies. In opposition to this fact, the potential of MNCs is comparatively less in the case of developed economies.

One of the contributing factors for the above observable divergence in results of FDI–trade nexus may be the aggregation of data. Most of the existing studies use the aggregate data for FDI and export to examine the relationship. However, the FDI–trade nexus may vary from sector to sector, and we may even encounter variations within the sector. According to Alfaro (2003), the use of aggregated data of FDI in the analysis does not give the actual impacts of FDI. Blonigen (2001) argues that the complementary relationship between the FDI and trade can also be due to the aggregation bias. By analysing the impact at the industry level, Lipsey and Weiss (1981, 1984) find a positive causal relationship between FDI at the industry level and trade flows. Total exports were divided into three categories by Onyekwena et al. (2017): primary, intermediate and final goods. They discover that foreign direct investment has a negative and large influence on intermediate goods exports, a favourable impact on primary products and a negligible impact on final goods. FDI has a favourable and large influence on aggregate exports, according to Liu and Shu (2003), and this link is strong across sectoral exports. Gu et al. (2008) and Liu and Shu (2003) examined the impact of FDI on several types of exports in China using a similar technique. Gu et al. (2008) obtained the same results after segregating the total exports into 14 categories. In 13 out of these 14 categories, FDI has a positive and significant impact on exports. The results are in tandem with Leichenko and Erickson (1997), who find that the effects of FDI on exports are positive in all except two of the manufacturing industries. Given the backdrop, we can observe that the impacts of FDI on export vary from one sector to another and may not be the same across all export categories.

Existing literature indicates that the FDI–trade nexus is too ambiguous to draw any conclusive findings and varies across the country’s economic condition and sectors. Reviewing the vast literature, two important insights emerge. First, the empirical review shows that we cannot generalise the impacts of aggregate FDI on trade in terms of its effect. The effects of FDI on trade tend to vary across and within the sectors. Second, studies pertaining to sectoral FDI–trade nexus and its disaggregated analysis, explicitly focusing on emerging economies, are lacking in the existing literature. Our study tries to fill this gap by examining the impacts of sectoral FDI and sub-sectoral FDI on trade in emerging economies.

Data Description

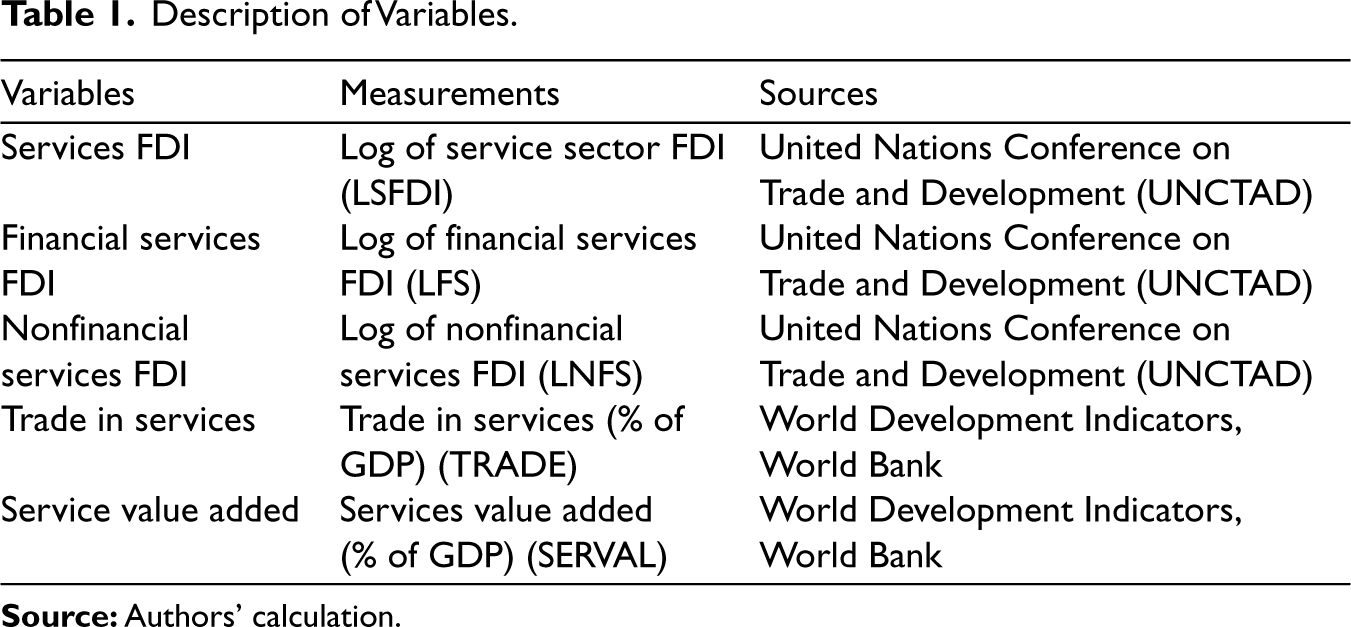

The data of our variables of importance such as FDI in services, FDI in financial services and nonfinancial services are collected from United Nations Conference on Trade and Development (UNCTAD). Trade-in services and service value-added are sourced from the World Development Indicators (WDI), World Bank. The unbalanced panel data is made up of observations from 26 emerging economies from 2003 to 2015. A list of the selected countries is provided in the Appendix A. The selection of nations and time periods was determined by two factors: (a) availability of data and (b) to incorporate a period of world economy that witnessed economic growth and turbulence driven by capital flows. Table 1 shows a list of variables and their respective data sources.

Description of Variables.

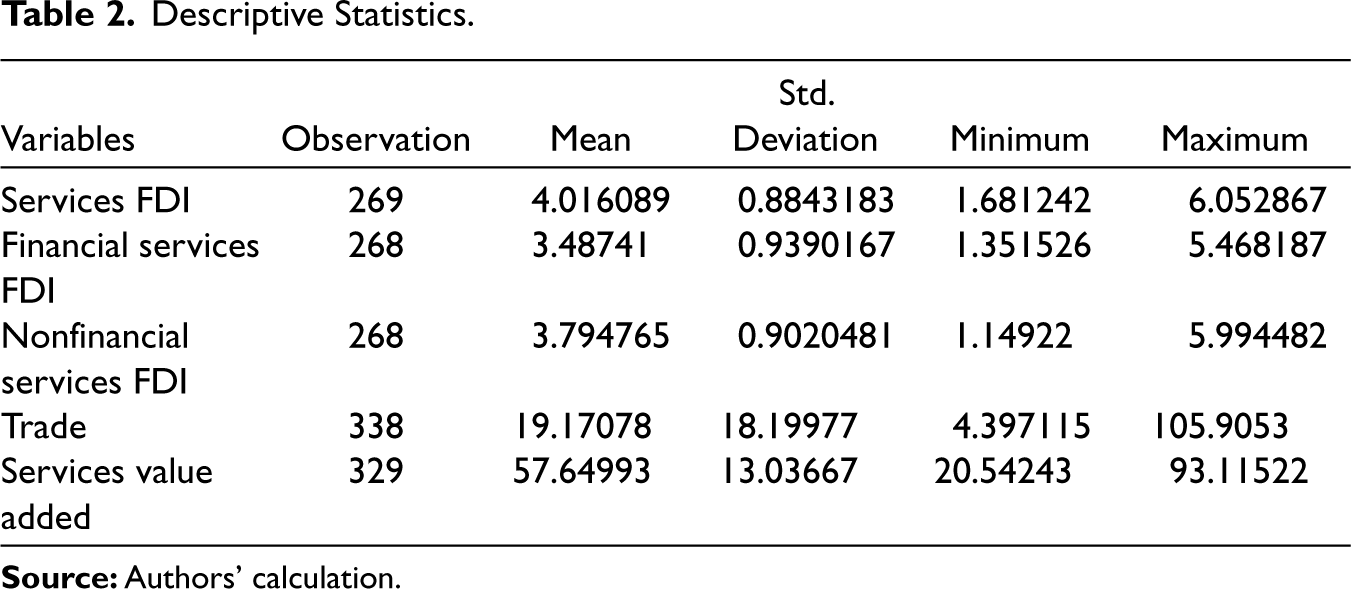

The descriptive statistics in Table 2 illustrate that there is heterogeneity across emerging economies, since the variables vary widely from nation to nation. As the standard deviations of these variables are high, variables like trade and services value-added vary a lot between developing economies.

Descriptive Statistics.

Econometric Methodology and Empirical Results

To examine the long-run properties of time series, traditional unit root and cointegration methods are commonly used. Our panel data consists of only 13 years’ data, which is a relatively shorter time span, so the power and efficacy of conventional time series models are limited. For this reason, we employ the panel unit root and cointegration testing approach of Pedroni (1999, 2004) and Kao (1999) to analyse the relationship between trade in services and FDI in services. In addition, we use the sectoral decomposition to examine the long-run link between trade in services, financial services FDI and nonfinancial services FDI to see if it matters for this relationship. The causality between trade in services and FDI in services, FDI in financial services and FDI in nonfinancial services is investigated using the panel vector error correction model (VECM). Three steps make up the empirical analysis. To begin, we demonstrate that our variables, trade in services, foreign direct investment in services, financial services FDI, nonfinancial services FDI and services value-added, all have unit roots. In the second step, we use panel cointegration tests such as Kao’s panel cointegration test and Pedroni’s heterogeneous panel cointegration test, allowing for fixed and time effects to test the long-run linkages between our variables. When the individual time series are stationary at first difference, cointegration tests are commonly used to examine the long-run connection between time series. We used heterogeneous panel cointegration to account for cross-sectional interdependence and country-specific effects because there is heterogeneity in our selected emerging economies’ trade, FDI and economic development. Third, we use the Granger causality test and the panel vector error correction model to examine the causal link between trade in services, FDI in services and sectoral breakdown (VECM).

Panel Unit Root

The stationarity of the variables is a necessary condition in the empirical analysis since the existence of nonstationarity of variables can lead to spurious regression in the conventional OLS method. The order of integration of the variables plays a vital role in cointegration analysis. Nonstationarity is a sufficient condition for cointegration analysis, which implies that all variables should be integrated at first difference. Nonstationary panels have become extremely popular in the macroeconomic literature over the last two decades. In recent years, Levin et al. (2002; hereafter LLC, 2002), Maddala and Wu (1999), Im et al. (2003; hereafter IPS, 2003), Breitung (2001) and Choi (2001) constructed new methodologies in panel unit-roots. To analyse the stationarity or integration properties of the variables, FDI in services, FDI in financial services, FDI in nonfinancial services, trade in services and services value-added, we use the panel unit root test developed by Maddala and Wu (1999), LLC (2002) and IPS (2003).

The LLC (2002), panel unit root test has the following form:

where k is the lag length and Δ is the first difference operator. θi and δt are unit-specific fixed and time effects, respectively. The null hypothesis of ρ = 0 for all, the alternative hypothesis and is ρ < 0 for all i. If we reject the null hypothesis, then the variables will be stationary. The speed of adjustment process may vary across sectional units towards long-run equilibrium, but the main assumption of LLC is homogeneous ρ so that it does not take into consideration the different speeds of adjustment.

To evaluate the stationarity of the variables, IPS (2003) used modified Dickey–Fuller regression. It incorporates both time series and cross section dimension, therefore the test just needs a few time series to be effective. When it came to analysing the long-run relationship in panel data, IPS was shown to have greater test power.

where zit is a vector of deterministic terms, explaining the fixed effects or individual trends, ki is the lag length. Δ

i

is the corresponding vector of coefficients. The hypothesis of this test can be expressed as

IPS test the hypotheses with the standardised t-bar statistic

As they developed a cross sectional demeaned version, the IPS (2003) test has a superiority over other tests when N and T are modest. It’s beneficial when there’s a common time-specific component in errors across several regressions.

Maddala and Wu (1999) proposes the ADF-fisher test which combines the p values of the test statistics for unit root in each cross-sectional units. If φi is the p-value from the individual unit root test for any cross section will be I. The tests statistics has the following form:

Table 3 shows the test statistics of unit root at both level and first difference. As evident from the table, the results indicate the uniform conclusion that the null hypothesis of unit root can be rejected for the variables at first difference. It implies that variables are stationary in the first difference form. We may conclude that the variables are integrated of order one based on our findings. The findings suggest that trade in services, FDI in services, financial services FDI, FDI in nonfinancial services and services value-added may have a long-term relationship.

Panel Unit Root Tests.

We find that the variables with individual intercepts and trends are nonstationary in levels at 1% and 5% significance levels, and stationary or integrated of order one I(1), based on unit root test findings. As a result, we use cointegration for our analysis since the required criterion is met. We can use panel cointegration analysis to study the long-run connection between trade in services, FDI in services, financial services FDI, FDI in nonfinancial services and services value-added based on the supplied panel unit root tests.

Panel Cointegration

Our variables are integrated at I(1), implying that they may have a cointegrating relationship or a long-run relationship. In FDI, financial and nonfinancial services FDI, we use a panel cointegration methodology to account for heterogeneity across 26 countries. We estimated two separate cointegrations to analyse whether the direction of the relationship between FDI and trade in services changes within the sector or not. We use Pedroni (1999, 2004) and Kao (1999) in our analysis is to check whether the cointegrating relationship between trade in services, FDI in services, financial services FDI, nonfinancial services FDI and service value added is robust across estimations. Pedroni’s (1999, 2004) cointegration test allows heterogeneity across individual members of the panel and individual-specific fixed effects and deterministic trends. We estimate the cointegrating relationship of our variables using the following equation:

where θi (i = 1, 2, 3, …, 26) is country specific effects, δi t refers to time effect; ϵit is the estimated residual which measure the deviations from the long-run steady state relationship. Xit is an m-dimensional column vector for each member i. βi is an m-dimensional row vector for each member i of the panel. If ϵit is turned out to be stationary or consistent with I(0), there exists a long-run cointegrating relationship between trade in services and FDI in services. If ϵit is found to be stationary or consistent with I(0) in sub-sectoral analysis, it indicates the existence of cointegrating relationship between FDI in financial services, nonfinancial services and trade in services.

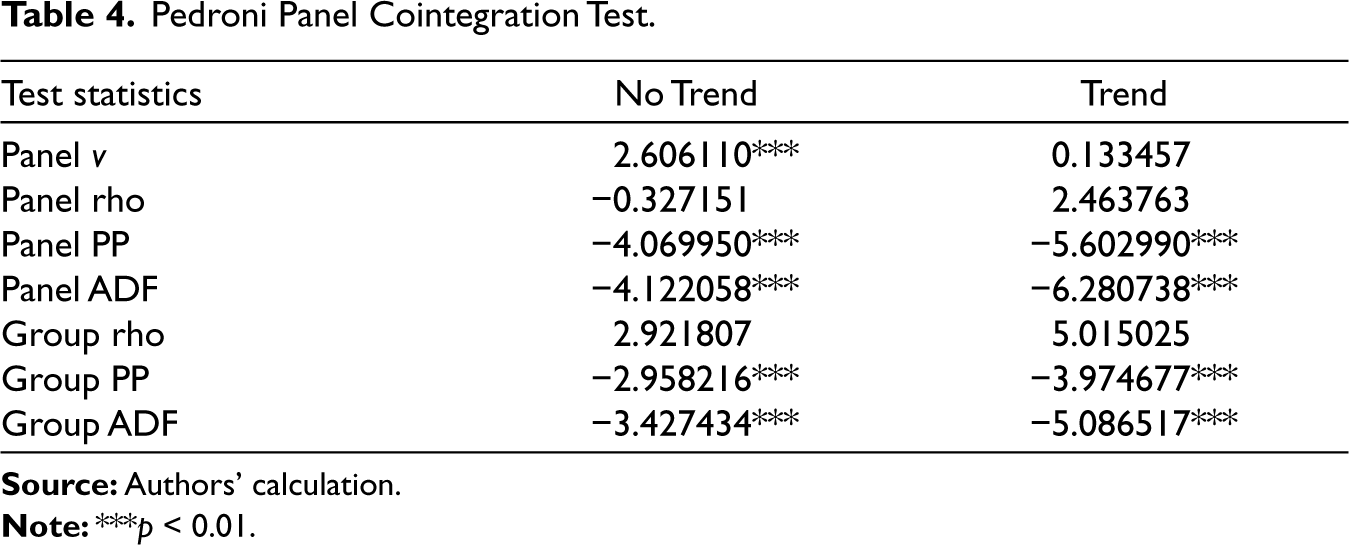

Pedroni (1999) uses seven test statistics to estimate the residuals to determine if the variables have a cointegrating relationship. The seven statistics under different model specifications for the trade in services and FDI in services are reported in Table 4. In the analysis, four out of seven statistics are significant, implying that the statistics for various parameters of interest support null rejection at 1% level. As a result, we infer that FDI and trade are cointegrated in the long run. Therefore, the inference is that there is co-movement exists among trade in services, FDI in services and services value-added.

Pedroni Panel Cointegration Test.

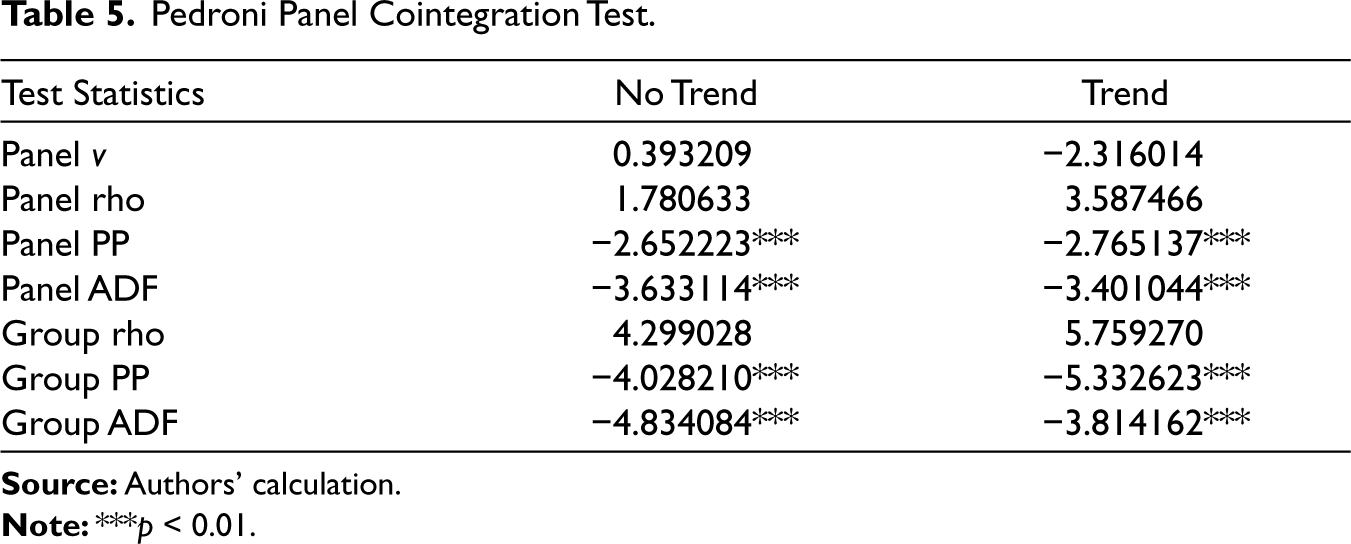

All the seven statistics for the sub-sectoral analysis are reported in Table 5. It is evident from the analysis is that there exist a long run cointegrating relationship between FDI and trade in services as four out of seven Pedroni’s test statistics are statistically significant. Our findings reveal that trade in services, financial services FDI and nonfinancial services FDI are all moving in the same direction. Based on the findings, we conclude that trade in services and service sectoral FDI have a long-term relationship that is consistent at the sub-sectoral level.

Pedroni Panel Cointegration Test.

Kao (1999) proposes two kind of unit root test like Dickey–Fuller (DF) and augmented Dickey–Duller (ADF). Kao’s DF type test follows the following model:

where

The Dickey–Fuller test can be applied to the estimated residual using

Null and alternative hypothesis can be written as

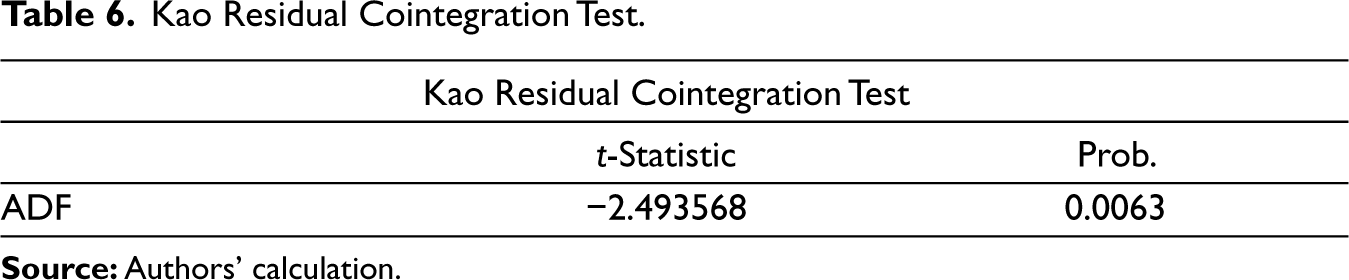

The results of the Kao cointegration test for trade in services and service sector FDI is reported in Table 6. Our results show that the Kao panel cointegration rejects the null hypothesis of nonstationarity of ϵit under all specifications at 1% level. It indicates the presence of a cointegration relationship between trade in services and FDI in services. Kao cointegration results for the sub-sectoral analysis is reported in Table 7. We find that trade in services, FDI in nonfinancial services and financial services FDI share a long-run cointegrating relationship.

Kao Residual Cointegration Test.

Kao Residual Cointegration Test.

Panel Causality Test

As FDI in services, nonfinancial services FDI, FDI in financial services and trade in services are cointegrated, the next step is to estimate the two-way relationship between these variables. We employ the Granger causality test to examine the causal relationship between trade in services and FDI in services for sectoral FDI and trade in services, financial services FDI and nonfinancial services FDI for sub-sectoral FDI. Given the variables are cointegrated, we perform the Granger causality two-step procedure using panel vector error correction models (VECM), which account for the long-run relationship. The two-step procedure is explained in Engle and Granger (1987) and demonstrated by Granger et al. (2000). It is a two-step estimation procedure; in the first step, we estimated the long-run model using

By estimating Equations (7) and (8) we obtained the estimated residual. We will incorporate the residual εit as a right-hand side variable, the dynamic error correction model is estimated in the second step to draw the inferences on causal relationship between the variables. The dynamic error correction model takes the following form:

where k, ∆ denotes the lag length and first difference respectively.

The significance of the dependent variables in Equations (9)–(13) provides the causation between the variables. Therefore, the parameters of our interest in the error correction model as follows:

λ1i: Long-term impacts of FDI in services innovations on services trade. λ2i: Long-term impacts of service trade innovations on FDI in services. λ3i: Long-run impacts of innovations in financial services FDI and nonfinancial services FDI on services trade λ4i: Long-run effects of innovations in services trade on financial services FDI λ5i: Long-run effects of innovations in services trade on nonfinancial services FDI θ12ik: Granger causation from FDI in services to services trade in the short term. θ22ik: Granger causation from services trade to FDI in services in the short term. θ32ik: Granger causation from FDI in financial services to trade in services in the short term θ33ik: Short-run granger causality from nonfinancial services FDI to trade in services θ42ik: Short-run granger causality from services trade to financial services FDI θ52ik: Short-run granger causality from services trade to nonfinancial services FDI

For long-run causality, the source of causation is the εit – 1 in Equations (9)–(13). The coefficient of the error correction term, λ, is known as speed of adjustment, and it describes how quickly deviations from long-run equilibrium are erased when each variable is changed (Mehrara, 2007). Below are the panel causality results for FDI in services, FDI in financial services, nonfinancial services and trade in services.

Our results show that there exists a unidirectional causality running from FDI in services to trade in services in the short run. At the same time, the significance of the error correction term indicates the long-run causality between the variables. It implies that there exists a causal relationship between trade in services and FDI in services that is a unidirectional causality running from trade to FDI in services in the long run. The results indicate no causal relationship between the financial services FDI and trade in services, which implies that it is not causing each other. Based on the results, we can conclude that financial services FDI is market-seeking FDI than resource-seeking since it does not have a causal relationship between trade in services. As evident from Table 8, there is bidirectional causality between trade in services and nonfinancial services FDI in the short run. It indicates that both trade in services and nonfinancial services FDI have a reinforcing causal relationship. Therefore, policymakers have to target both at the same time to induce trade in services. Concomitantly, there exists a unidirectional causality running from trade in services to FDI in nonfinancial services in the long run. It means that services trade can operate as a stimulus for attracting FDI in nonfinancial services. It indicates that nonfinancial services FDI is mainly resource seeking as it has a causal relationship between trades in services both in the short and long run.

Results of Panel Causality Test.

***p < 0.01, **p < 0.05 and *p < 0.1.

Because the sub-sectoral analysis demonstrates a bidirectional causality between nonfinancial services FDI and trade in services, our findings show that the sectoral decomposition matters for the trade in services and FDI in services connection. In the case of FDI in financial services, it is still absent. It suggests that the causal association between FDI in services and trade in services would be greater if the sectoral decomposition is tilted towards nonfinancial services.

Concluding Remarks

With a focus on emerging economies, this article empirically explores the long-run relationship and direction of the causal link between the service sector and sub-sectors FDI and trade in services. Although much of the current literature claims that FDI has positive and significant effects on trade, the disaggregated FDI analysis is meager. We have used the panel VECM to analyse the long-run relationship between FDI in services, sub-sectors of FDI in services and trade in services. The results validated the cointegration between trade in services, FDI in services, financial services FDI and nonfinancial services FDI using sectoral and sub-sectoral data for 26 emerging economies for 2003–2015. It shows that services trade, FDI in services, FDI in financial services and FDI in nonfinancial services share long-run relationships.

We find that there exists a unidirectional causality between FDI in services and trade in services in the short run, running from FDI in services to trade in services. However, there exists a long-run unidirectional causality running from trade in services to the FDI in services. Nevertheless, the sectoral disaggregated analysis shows no causal relationship between trade in services and FDI in financial services; it implies that the financial services FDI does not have a significant impact on trade in services and vice versa. In the case of nonfinancial services FDI, the results exhibit a bidirectional relationship between trade in services and FDI in nonfinancial services in the short run. Unidirectional causality runs from trade in services to FDI in nonfinancial services. Given the backdrop, we can conclude that financial services FDI is mainly market-seeking FDI while nonfinancial services FDI is resource-seeking.

Our empirical results find the long-term cointegrating relationship between FDI in nonfinancial services and trade in services in the context of emerging economies. The main finding of our analysis is that the sectoral disaggregation does matter for the FDI–trade nexus both in the short run and long run. Our results align with Blonigen (2001) and Alfaro (2003), who find the complementary relationship between the FDI and trade can be due to the aggregation bias. Considering the sectoral disaggregated FDI impacts on trade in services, it implicitly recommends that the emerging economies make policies for the sectoral disaggregated level to ensure economic development. Therefore, we conclude by suggesting that sectoral and sub-sectoral level policies for FDI could be implemented in emerging economies, but they should be carefully formulated.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.