Abstract

Interest rate hike as an instrument for inflation-targeting has been adopted quite aggressively in recent times by the Fed Bank of the United States, which has some far-reaching implications for emerging market economies like India. In such a context, this article explores implications of interest rate hike by a large foreign country for wage inequality between skilled and unskilled workers in a domestic economy. We focus on the supply side channel: hike in foreign interest rate affecting wage inequality through its impact on domestic investment, capital formation and consequent changes in the composition of aggregate output. We show that the wage inequality worsens if capital-cost share in a composite traded good is larger than the capital-cost share in a skill-based export-good Z. Domestic policies such as credit expansion by changing the cash-reserve ratio and increase in money supply help mitigate this worsening wage-inequality effect of interest hike abroad. This issue assumes relevance because of rising concerns among the major central banks the world over about the income distributional impacts of monetary policies, whereas most of the recent income inequality trends seem to have been contributed largely by rising skill premiums.

Introduction

In recent years, as the International Monetary Fund observes, central banks of some of the major industrialised countries across the world have been largely resorting to inflation-targeting techniques to control rising inflation rates in their countries and thereby improve economic stability. For example, according to the IMF, Canada, Australia and Japan are among the many economies that have set 2% as their inflation rate targets. This 2% inflation target is also key to the Federal Reserve’s vision for stable prices in the US economy, according to the Federal Reserve Bank of St. Louis. Given such a target, in the face of alarming inflation rates in the past couple of years, being the highest in the last 40-year, the US Fed Bank has raised the Fed funds rate by more than five percentage points during 17 March 2022–2027 July 2023 (see Table 1). In his speech at Jackson Hole in August 2022, Federal Reserve Chair Jerome Powell said that ‘without price stability, we will not achieve a sustained period of strong labor market conditions that benefit all’.

Fed Fund Rate Hikes.

Though Federal Reserve kept the Fed funds rate steady at 5.25%–5.5% for a third consecutive meeting in December 2023, further hike in federal funds rate in the future cannot be ruled out since annual inflation rate appears to be 3.1% in November 2023, still well above the Federal Reserve’s stated long-term target of 2%.

Such inflation-targeting monetary policies in advanced economies often have far-reaching implications for global financial markets and, through inter-dependencies of countries, for external and internal balances in their trading partners, particularly in emerging market economies (EMEs). And these transmission effects may be quite severe at times. Dating back to 1980s, the Volcker shock—the interest rate shock originating in the USA—largely causing the Debt Crisis in Latin American countries and resulting in stalling their development for almost a decade, is a glaring example (Ocampo, 2014). 1 A more contemporary example of effects of monetary policy changes in advanced countries spilling over to EMEs is the Quantitative Easing (or unconventional monetary policies) adopted by Federal Reserve Bank, the European Central Bank, Bank of England and Bank of Japan after the Global Financial Crisis (2007–2008). Such policies had some far-reaching effects on the real exchange rates and current account balances in EMEs including India. Banerjee and Goyal (2020) in their recent empirical study found that monetary expansions in the advanced economies led to over-valuation of real exchange rates primarily through portfolio reallocations, higher prices and rebalancing of current account surpluses in the EMEs. 2 Moreover, they observe that there had been a larger impact of US monetary policies than other advanced economies, which means that policy changes in the United States, seem to have significant adverse impacts on the EMEs through transmission of adjustment costs of such policies.

US Fed Bank’s recent inflation-targeting interest rate hikes have raised similar concerns of adverse impacts on external and internal balances in EMEs and other developing countries, primarily through wealth-holders’ asset-portfolio reallocations, capital flights and consequent exchange rate fluctuations. India being a prominent trading partner of the United States with economic exchange ties that have progressively strengthened over the last two decades, many economists opine that the INR–USD exchange rate fluctuations during the period coinciding with the US interest rate hikes, is partly, if not largely, the effect of inflation-targeting monetary policies adopted by the United States (see Figure 1). Note that these large depreciations were despite moderation attempts by the Reserve Bank of India through interventions in the foreign exchange market under its current regime of managed float.

While depreciation of INR may boost India’s exports, import bills for intermediate goods (as well as POL) essential for production of manufactured goods, be it traded or non-traded, are causing concerns for domestic inflation, purchasing power of the poor and thus for income inequality. There can be further implications of Fed Bank’s inflation-targeting policies for domestic factor-income distribution in countries like India arising from reallocation of scarce resources from non-traded to traded sectors that depreciations of INR may lead to. Asset trading and change in allocation of asset-portfolio in favour of USD-denominated assets may also cause fall in domestic investment leading to further changes in resource allocation across traded and non-traded sectors and consequently factor-income distribution.

In this article, we focus on this particular dimension of ramifications of the US Fed Bank’s inflation-targeting policy for its trading partners like India through these channels. More precisely, and generally speaking, we examine how wage inequality between skilled and unskilled workers change in an open economy due to hike in foreign interest rate as inflation-targeting policy through its impact on domestic investment, capital formation and consequent changes in the composition of aggregate output. To the best of our knowledge, not only does this dimension of policy effect remain unexplored, the inter-relationship between money supply, exchange rate and domestic factor incomes has not been taken into account either in the general equilibrium and/or in the macroeconomic literature.

In a more general context, this exploration assumes relevance in recent times as income inequality in both advanced economies and the emerging markets of developing countries has been on the rise. Rising inequality trends, be it in the developed or the developing economies, is a major structural challenge that is closely related to other economic concerns that a country might be facing and fuels the worry of policy makers and political leaders due to political conflicts therefrom. Realising its far-reaching implications for the entire global economy, substantial research has gone behind establishing the existence and finding cause and mitigation of income inequality over the years. Evidences of growing income inequality the world over have been sampled and studied by many; the most influential work in recent times being that of the French economist Thomas Piketty (2014). The World Inequality Report 2022 also projected India as one of the most unequal countries in the world, with rising poverty and an ‘affluent elite’. The report highlights that the top 10% in India hold 57% of the total national income, respectively, while the bottom 50% hold only 13%. In addition, many researchers have argued that these recent inequality trends are related primarily to the rising skill premium or wage inequality between skilled and unskilled or low-skilled workers (Acemoglu & Robinson, 2014; Mare, 2016; Maura & Mulas-Granados, 2015). In this context, a recent ILO—2018 report reveals that while wage-earnings of workers in India in the lowest-skilled occupation, medium-skilled occupations and high-skilled occupations are respectively 60% of the average earnings, between 0.7 and 1.8 times higher than average earnings, and between 1.9 and 4.3 times higher than average earnings, respectively. Further, while the daily wages for low-skilled occupations grew by 47%, those for high-skilled occupations increased by 98% and 89%, respectively, from 1993–1994 to 2011–2012. In a different study, Sharma (2022), on the other hand, found that wages are highest for workers in non-routine cognitive occupations, followed by routine cognitive occupations, whereas the lowest average wages are earned by workers in non-routine manual occupations. She used the routine or non-routine classifications of occupations to capture technology adoption, and cognitive or non-cognitive classifications of occupations to capture the education levels.

Given these observations, examining inflation-targeting interest rate hikes in a large foreign country, such as the current Fed Bank hikes, on the wage inequality in a developing country seems worthwhile and relevant. Furthermore, we also examine how domestic monetary policies can be used to manage the exchange rate fluctuations caused by foreign interest shock and thereby to mitigate worsening wage inequality caused by such external shocks.

The theoretical analysis in this article also generalises and extends the small but growing literature that looks into the interplay of monetary policy and within-country income inequality. The extant literature in this context has mainly focused on channels like the heterogeneity in income sources, financial market segmentation, portfolio and asset price effects, the heterogeneity in labour income responses, differential response of borrowers versus savers to rise in interest rates and so on (Andersen et al., 2021; Bernanke, 2015; Coibion et al., 2014; Dossche et al., 2021; Draghi, 2016; Schnabel, 2021). Studies on the effect of exchange rate volatility on income distribution (Aye & Harris, 2019; Carnevali et al., 2022; Goldberg & Tracy, 2001), on the other hand, have examined effects of exchange rate changes as exogenous shocks. But the central banks in many developing as well as developed countries use monetary policies to moderate or manage exchange rate fluctuations arising from external shocks for a variety of reasons. In light of this, our research question here is much broader in scope than analysing the effects of exogenous shocks in exchange rates.

For this purpose, we use a simplified version of the analytical structure developed ion Ganguly and Acharyya (2022). 3 The real sector of the economy produces two traded goods—a composite traded good (T) and a skill-based export good (Z)—and a non-traded good (N). The composite traded good and non-traded goods are produced by capital and unskilled labour, while the Z good that is entirely exported, uses skilled labour and capital. Flexibility of all factor prices ensures their full employment. In contrast to Ganguly and Acharyya (2022), and given our specific purpose here, we simplify the production structure by assuming away land, and allow unskilled money wage to change in response to external as well as domestic monetary shocks to maintain full employment of unskilled labour. While the endowments of skilled and unskilled workers are exogenously given, the stock of capital is endogenous and determined by the level of investment financed by borrowing loanable funds from the banks, which they receive from the domestic wealth-holders as an outcome of their portfolio choices over cash, domestic assets and foreign assets.

In this set-up, we show that a hike in the interest rate abroad may worsen wage inequality in the domestic economy if the capital-cost share in the skill-based export sector is larger than that in the homogeneous composite traded sector. Under such circumstances, a credit expansion in the domestic economy—achieved through lowering the cash-reserve ratio (CRR) for the commercial banks—and/or an increase in the domestic money supply can help mitigate the worsening wage inequality. Extending the benchmark analysis by considering the skill-based export good as a quality-differentiated good, we found similar cost-share conditions underlying worsening wage-inequality due to hike in the foreign interest rate. However, now the level of initial quality may also matter.

The rest of the article is organised as follows. The second section elaborates upon the model. The third section discusses the effect of an inflation-targeting foreign interest rate hike on the income distribution in domestic economy; while the fourth section discusses how domestic monetary policies may mitigate adverse effects on wage inequality. Finally, the fifth section concludes the article.

The Model

The real sub-system of the small open economy under consideration comprises three final-good production sectors producing a composite traded good (T), a non-traded good (N) and a skill-intensive good Z. The composite traded good is the composite of all low-skill intensive export and import-competing goods. Goods T and N are produced by a primary factor of production—unskilled/low-skilled labour (L)—along with capital (K), which is created through investment as specified later. The export good Z is produced using skilled labour (S) and capital. The supply of unskilled/low-skilled and skilled workers are exogenously given: There are S̄ number of skilled workers and L̄ number of unskilled workers, each supplying one unit of labour inelastically. 4 Domestic markets for goods and factors are perfectly competitive. Thus, the rate of return to capital (r), the unskilled money wage (w) and the skilled money wage (ws), all expressed in domestic currency, are fully flexible and adjust to clear the relevant factor markets. Production technologies for the composite traded and non-traded goods follow CRS, and per unit input requirements are technologically fixed. The economy under consideration being small faces given world prices of all its traded goods.

Free entry of firms in the three production sectors implies that firms break-even, which is given by the following price-equals-average-cost condition:

where

On the demand side, without any loss of generality, we assume that tastes are homothetic and that good Z is not domestically consumed.

5

Thus, the relative demand for N being influenced only by the relative price of the non-traded good, the domestic market clearing condition for N can be written as

where p = PN / PT denotes the relative price of non-tradables or reciprocal of the real exchange rate; and XN and XT are the output levels of non-traded good and composite traded good, respectively.

Small and competitive investment firms invest in capital formation by borrowing money from banks or financial intermediaries. Without delving into the process of capital formation, we assume that investment worth of one domestic-currency unit generates units of physical capital. Thus, total capital stock generated through investment worth I units of domestic currency by all the investment firms taken together is given by

With no initial stock of capital, K in Equation (5) also means addition to capital stock. The proportionality rule assumed in Equation (5) is a simplification and does not alter our results derived later. The banks/financial intermediaries lend funds to investment firms at the rate ib. Setting aside any other costs of capital formation whatsoever, if each investment firm borrows funds worth

The banks’ lending rate is higher than the market interest rate i that they pay on bonds and deposits held by the domestic income earners (or wealth-holders). Banks have no influence on this market interest rate (i), which is determined by the money market equilibrium condition stated later. The premium or the margin over the market interest (ib − i) charged by the banks for each unit of investment fund borrowed by the investor firms is determined by three factors. First, it covers the institutional costs and service charges. Institutional costs include payments to skilled workers employed in the banks for managing the investment funds and other related banking operations, such as processing applications for investment loans. To keep things simple, we assume that one skilled worker is required per unit of investment fund supplied to the banks to carry out these tasks. Thus, the skilled-wage is the operational cost per-unit worth of loanable funds that the banks receive in the form of deposits and bonds. Second is interests that has to be paid to the depositors on the fraction of deposits that banks are mandated to maintain in liquid cash. As per the stipulations of the central bank, the banks can lend out only a fraction R of total loanable funds that it receives, with rest (1 − R) fraction, the so-called CRR, to be kept with the central bank in liquid cash. Since banks cannot lend this amount to potential investors or borrowers, they do not earn any interest income either though must pay depositors the market interest rate, i. Thus, they must cover this costs as well. Third, banks also charge a variable markup α per unit of investment fund it lends out over and above these operational costs and deposit rate i. This markup is determined and varied by the banks according to the demand for and supply of loanable funds. Banks are owned by skilled workers and thus this profit margin α per unit of investment fund lent out is appropriated by them. Again, as a simplification, we assume that skilled workers own equal share of banks, and thus each of them gets αI/S as her share of banks’ profit margins for investment fund worth I units. Therefore, if total deposits and value of bonds held by the domestic wealth-holders is Is, then the lending rate ib must be such that

That is,

The total value of investment (I) by the investment firms and the consequent capital stock available for production of the three goods as per Equation (5), however, depends on the loanable funds that can be borrowed from the banks or financial intermediaries. Following Krugman (1979), suppose foreign wealth-holders do not buy bonds denominated in home-country currency. Then the supply of such loanable funds comes entirely from the domestic wealth-holders buying domestic bonds, which are issued by these banks or financial intermediaries themselves, and/or holding deposits with banks. This supply of lonable funds to the banks is an outcome of optimal allocation of wealth (W) over a portfolio. Each income earner or wealth-holder holds l proportion of wealth in zero return domestic currency, or cash, and the remainder (1 − l) proportion on the interest-bearing assets available. Part of the cash requirement is to carry out consumption expenditure, that is, to cover the total expenditure on consumption of T and N by the domestic consumers. On the other hand, (1 − l) proportion of wealth is spent on two types of assets: m proportion of (1 − l)W is held in domestic-currency-denominated assets (bonds and/or bank deposits, all yielding the same domestic interest rate); and (1 − m) proportion on foreign-currency-denominated assets/bonds. These l and m proportions are outcomes of utility maximisations given the wealth-budget constraint, and are the same for all agents under the assumption of identical and homothetic preferences for portfolio-choice over cash and the two types of assets/bonds. If e̴ is the exchange rate expected by the wealth-holders at any point of time, then the expected rate of return on a unit of foreign bonds equals

where i is the rate of return on domestic bonds held; i* is that on foreign bonds held in foreign currency; and e̴ is the exchange rate expected by the wealth-holders at any point of time.

Accordingly, the proportion of wealth held in cash would vary inversely with these interest earnings:

where

Under the assumption that the two types of assets are perfect substitutes, the (uncovered) interest parity condition, on the other hand, determines optimal allocation of (1 − l)W over domestic and foreign bonds:

6

Thus, optimal proportion in which the domestic assets/bonds are held can be written as

The signs of the partial derivatives in Equation (9) are self-explanatory.

Given these optimal allocations, the aggregate demand for cash, for domestic bonds and for foreign bonds can be written as

Keeping with the observations of quite large magnitudes of bequests in aggregate wealth (Kotlikoff & Summers, 1981; Lord, 1992; Modigliani, 1988), the aggregate stock of wealth of the economy is assumed to consist of the stock of domestic money (M) supplied exogenously by the central bank, and the sum of bequests (W) that some of the citizens are endowed with:

Bequests are received by the wealth-holders in the form of domestic financial assets which, depending on their portfolio choice, can be converted into cash and/or foreign assets.

Two observations are in order at this point. First, by the specifications and assumptions above, the aggregate consumption expenditure, and correspondingly demand for cash Md = l(i, i* + E)W, increases proportionately with the aggregate wealth (W) as well as due to a fall in i and/or i*. Lower i, for example, causes a fall in aggregate savings and corresponding increase in consumption expenditure. Second, allocation of total consumption expenditure on the goods T and N consumed domestically is determined by the relative price or the RER,

Third, assumption of homothetic taste also means that even if we had assumed that the total consumption expenditure, and the money demand to carry out such transactions, increases with the income levels as well, that would have no impact on the relative demand for goods, and thus on PN from the demand-side. But, a higher income would change the domestic interest rate, ceteris paribus, and thus would affect domestic savings, investment and capital formation.

Fourth, part of the aggregate savings by domestic income-earners and wealth-holders held in domestic assets (or demand deposits) is channelised through banks to finance the investment expenditure and correspondingly equal the value of capital stock at the market rate of return as mentioned earlier: rK = ib Rm(.) [1 – l(.)]W.

By the above specifications, the money market equilibrium can be stated as

It is straight-forward to check that by the interest-parity condition (8) and demand for foreign bonds in Equation (11b), the exchange rate varies with the changes in i, i* and the stock of wealth for any given value of e̴:

A larger stock of wealth of the economy raises the demand for foreign-currency-denominated assets or bonds, which in turn raises the demand for foreign currency and consequently causes the domestic currency to depreciate. On the other hand, a higher domestic interest rate and/or lower foreign interest rate causes the domestic currency to appreciate by lowering the demand for foreign assets through the portfolio-allocation effect.

We close the real sector of the economy with the following full employment conditions for skilled labour, capital and the unskilled labour as follows:

where Sb is the employment of skilled workers in the banking sector, which by the simplifying assumption is equal to the total supply of loanable funds held by this sector, IS.

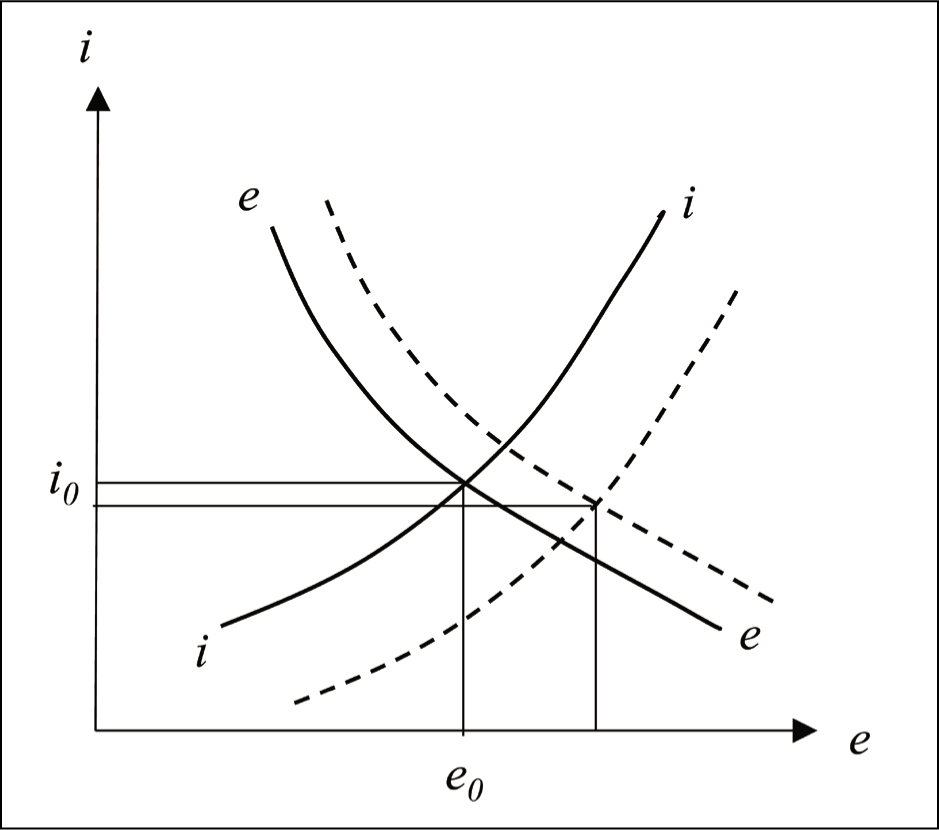

Given the values of the technology and policy parameters, the 12 independent Equations (1)–(6), (11a), (12), (13) and (15)–(17) determine the 12 variables— r, w, wS, i, e, PN, W, α, I, K, XT, and XN. The market clearing condition for non-traded good (4), the money market equilibrium condition (13) and the asset market (or foreign exchange market) equilibrium condition (8) are the three key conditions of the model reflecting interdependence of the three variables of interest—domestic interest rate i, price of the non-traded good PN, and the nominal exchange rate e.

There is an asymmetry in the relationship between equilibrium values of these three key variables of the model though. The domestic interest rate and the exchange rate are dependent on each other, and thus have to be solved simultaneously, but are independent of the value of PN . Once, these values are determined, the supply of loanable funds to the banks—that is, value of domestic bonds held by the domestic citizen—determines the level of investment, capital formation and then the value of PN from the domestic-market clearing condition for the non-traded good.

Diagrammatically, the money market equilibrium condition (13) and the asset market equilibrium condition (8) gives us a positive and a negative relationship, respectively, between i and e. A depreciation of the exchange rate induces domestic wealth-holders to convert part of their holding of foreign assets in cash, and thus raises the demand for money. The interest rate thus rises, given the supply of money. Though there will be conversion of some foreign assets into domestic assets as well, but these will have only dampening effects on the interest rate (and exchange rate). This positive relationship emerging from the money market equilibrium is depicted in Figure 2 by the ii schedule.

Simultaneous Determination of i and e.

On the other hand, a higher domestic interest rate, ceteris paribus, causes an appreciation of the domestic currency by lowering the demand for foreign assets through the asset portfolio-allocation effect. There emerges, therefore, a negative relationship between e and i, which is denoted by the ee schedule in Figure 2.

Equilibrium i and e are thus determined corresponding to the point of intersection between ii and ee curves.

Inflation-targeting Interest Hike Abroad and Domestic Wage Inequality

Consider now an inflation-targeting policy adopted by the central bank of the foreign country through a hike in interest rates on dollar-denominated assets. With the domestic money supply fixed at its initial level, and with no change in the amount of bequest either, this external shock will generate only portfolio allocation effects. First, given everything else, it will raise the opportunity cost of holding cash and thereby lower the demand for cash holdings. At the initial allocation of the wealth over domestic and foreign assets (or, bonds) at the rate m and (1 − m), respectively, the excess cash holdings will be spent on both these assets, thereby raising their demands equi-proportionately. Second, a higher interest rate on foreign bonds will lower the proportion of wealth held in domestic assets, and correspondingly raise the proportion of wealth held in foreign assets. These are the direct or initial cash-asset and asset portfolio allocation effects respectively of an increase in i*.

Note that the initial fall in the desired holding of cash lowers the domestic interest rate. In Figure 3, this is shown by the downward shift of the ii curve. On the other hand, a larger demand for foreign assets by these two types of portfolio allocation effects—a fall in l proportion and a fall in m proportion—raises the demand for foreign currency and thereby causes the domestic currency to depreciate in value. This is shown by the rightward shift of the ee curve. The rise in the value of e causes the domestic interest rate to rise and this makes overall change in the domestic interest ambiguous, which is apparent from the following expression:

Impact of Foreign Interest Rate Hike.

where ‘hat’ over a variable denotes its proportional change;

However, usually the initial or direct effect of an increase in i* that lowers i is stronger than its subsequent or induced effect that raises i. But, again this cannot be guaranteed, and thus to rule out any possibility on the contrary, we assume that

On the other hand, as it appears from Figure 3, the exchange rate depreciates unambiguously as a consequence of an increase in i*:

Given these changes, lower domestic interest rate at the new equilibrium reinforces the initial adverse asset portfolio effect of a higher i*, causing the demand for domestic assets to decline further. It also makes the initial favourable cash-asset portfolio allocation effect on the demand for domestic assets weaker since a larger proportion of wealth is held in cash on this account. Depreciation of the nominal exchange rate at the new equilibrium, on the other hand, raises the demand for domestic assets by the asset-portfolio effect but lowers it by the cash-asset-allocation effect.

Overall, taking into account all these initial and induced effects of an increase in i*, it appears that a fall in the demand for domestic assets and correspondingly decline in the supply of loanable funds to the banks are more likely. The condition for this is given as (see Appendix):

where the parameters are as defined earlier.

We summarise this in the following Lemma:

The effects on factor prices depend on how the relative price of the non-traded good changes. In this regard, first of all, due to fixed input coefficients, the depreciation of the nominal exchange rate proportionately raises PN at the initial stock of capital. Depreciation of e raises the relative demand for N at initial PN. But, with relative supply of N being fixed for any given capital stock (and endowment of unskilled labour), the excess demand for N needs to be wiped out by an equi-proportionate increase in PN. The capital stock, however, declines by Lemma 1. In face of a smaller supply of loanable funds under condition (20), the banks raise the premium α to balance the demand for loans from the investment firms at the initial rate of return to capital. The level of investment and capital formation thus decreases. The consequent smaller capital stock triggers an output magnification effect by which the output of the composite traded falls and that of the non-traded good rises if the composite traded good is relatively capital intensive than the no-traded good

7

:

The consequent excess demand of the non-traded good raises its price for any given e.

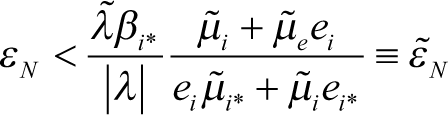

Two observations are in order. First, if the magnitude of this excess-supply caused fall in PN is large enough, PN falls at the new equilibrium outweighing the initial rise in PN proportionate to the rise in the value of e. Since larger is the price elasticity of demand for N, smaller is the fall in PN necessary to restore equilibrium by adjusting demand to the excess supply, so how much does PN fall depends on how elastic the (relative) demand for N is. More precisely, as shown in the Appendix,

where

Hence,

Second, from Equation (22) it appears that the relative price of the non-traded good declines under condition (20), regardless of whether condition (23) holds or not (that is, whether PN is lower or higher at the new equilibrium). This is because when Equation (23) does not hold so that the excess-supply caused fall in PN is small in magnitude, its increase at the new equilibrium is less than proportionate to the depreciation of the nominal exchange rate.

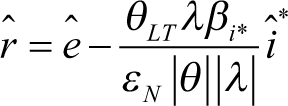

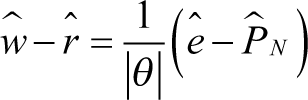

Turning now to factor prices, it is easy to check that whereas lower relative price of the non-traded good raises the rate of return to capital, unskilled wage may rise or fall. However, the ratio of unskilled wage to the rate of return to capital falls. All these can be verified from the following algebraic expressions (see Appendix):

where | θ |= θLTθLK – θKTθLN = θKN – θKT < 0 under the assumption in Equation (21); and θij is the share of factor i in unit cost of producing good j.

At the initial stock of capital, the exchange rate depreciation, as a consequence of a rise in i*, raises PN, w and r proportionately as are evident from the first terms in Equations (22), (24) and (25). Subsequently, as lower capital stock due to smaller investment causes an excess supply of the non-traded good and lowers its price, the unskilled wage falls and the rate of return to capital rises by the standard price magnification effect. Thus, the initial rise in r gets reinforced whereas w may fall. And, since by the price magnification effect 1% fall in PN leads to a more than 1% fall in w, so it may fall even for fall in PN that is not as large as under condition (23). This can be confirmed from Equation (24):

Note that, since by Equation (22),

On the other hand, as the higher rate of return to capital induces producers of good Z to contract production, the demand for skilled workers and their wages decline on this account. But, depreciation of the nominal exchange rate incentivises production expansion as producers earn more in domestic currency per unit of exports, which in turn raises the skilled wage. Overall, change in the skilled wage is ambiguous:

Thus, like the unskilled wage, at initial stock of capital, depreciation of nominal exchange rate raises the skilled wage proportionately. Subsequent supply-effect lowers it given condition (20). Hence, overall,

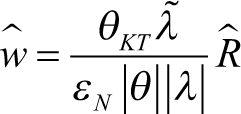

Finally, subtracting Equation (24) from Equation (27) and using relevant values we obtain change in the wage inequality as

This result is summarised in the following proposition:

Note that the worsening of wage inequality as stated in Proposition 1 does not depend on the factor intensity ranking of the composite traded good and the non-traded good as specified in Equation (21), but on the capital cost shares in the composite traded good and the skill-based export good. The condition that

Further, comparing the critical values of the demand-elasticity as specified in Equations (23a) and (27a), it can be verified that

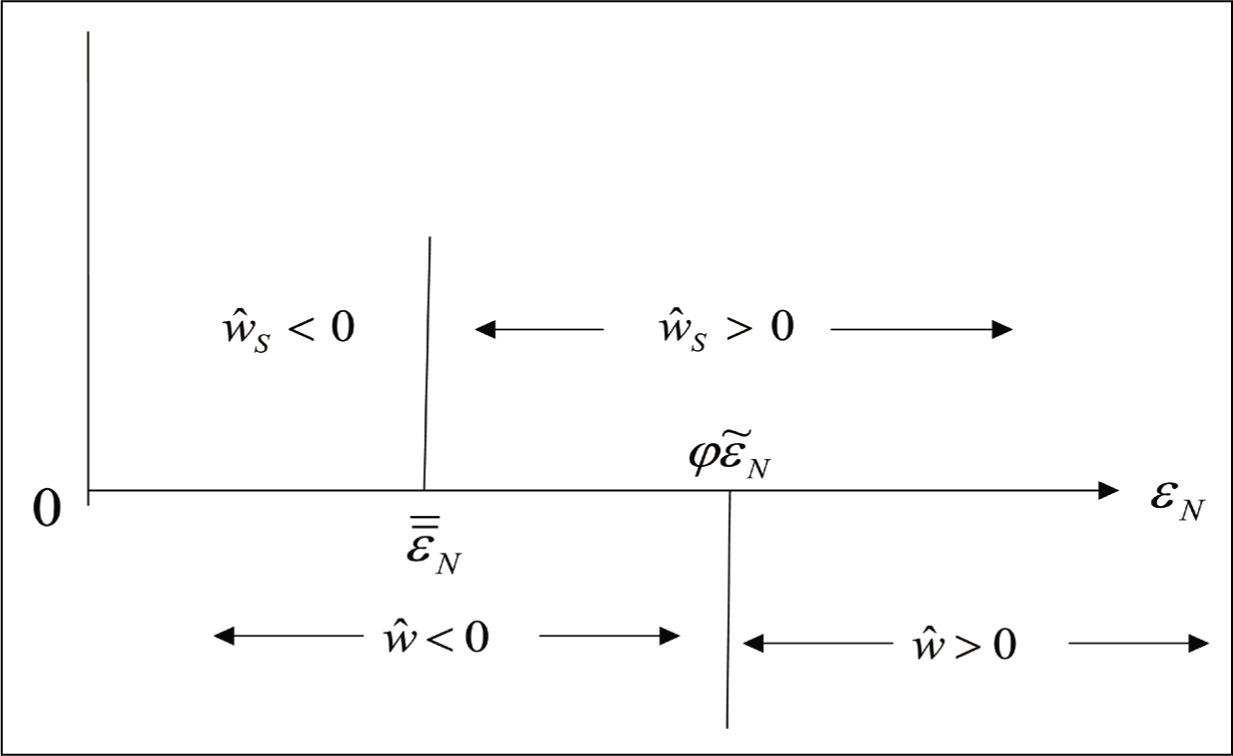

This special case of worsening wage inequality is illustrated in Figure 4.

Worsening Wage Inequality.

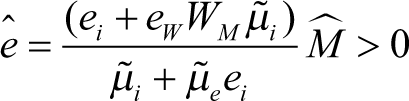

Before proceeding further, note that since part of the premium charged by the banks accrue to the skilled workers, so their total per-capita income ys is larger than the wage they get:

which using Equation (6a) can be written as

where

Thus, for any given CRR,

Note that

Domestic Monetary Policy to Mitigate Effect of Foreign Interest Hike

By Proposition 2, it appears that the inflation-targeting policy abroad through interest-rate hike is a cause for concern if the capital cost-share is largest in production of the composite traded good and least in that of the non-traded good with price elasticity of demand for non-traded good not very high. In such a case unskilled workers lose on absolute as well as relative terms. On the other hand, even when the elasticity value is quite high, so that unskilled wage does not fall, they can still be worse off relative to the skilled workers as stated in Proposition 1. Since we envy others, that is, value our relative positions more, so this possibility is no respite for the policy makers. Share of bank-profits appropriated by the skilled workers may further widen the income gap.

In the context of such a policy concern, we explore in this section whether domestic monetary policies help mitigate the adverse effect of foreign interest rate hike abroad on domestic unskilled wages and on wage inequality. Two policies of the home-country central bank are considered for the purpose: a change in the CRR that is mandatory to be kept with the central bank in liquid cash; and an increase in the money supply (

Change in the CRR

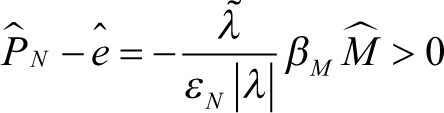

Suppose the central bank allows a credit expansion by lowering the CRR, that is,

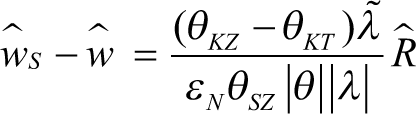

Thus, now the wage inequality declines if

The second part of the proof follows from Equation (31).

Thus, a credit expansion through lowering of the CRR, and corresponding increase in the domestic investment, helps mitigate the adverse effect of the inflation-targeting policy of the foreign country not only by raising the unskilled wage but also by lowering the wage inequality.

Change in the Money Supply

An increase in money supply by the central bank by putting into circulation new currency notes has additional impacts on factor incomes as it impacts both the domestic interest rate and the nominal exchange rate. First, it increases the aggregate wealth of the economy proportionately. Accordingly, at the initial equilibrium domestic interest rate, the cash holding and demand for domestic and foreign assets all increase equi-proportionately by the wealth-effect. Domestic investment thus rises by this wealth-effect. The wealth-effect triggers subsequent portfolio-allocation effects, which change domestic investment further. A larger demand for foreign assets due to wealth-effect raises the demand for foreign currency and thereby causes the domestic currency to depreciate in value. The expected domestic currency return on foreign currency deposits thus falls, which induces the domestic wealth-holders to hold a larger proportion of their wealth in domestic assets. Domestic investment thus rises on this count too. But, increase in the bond price and corresponding fall in the domestic interest rate caused by the increase in demand for domestic bonds due to the wealth effect, lowers the proportion of wealth held in domestic assets. Domestic investment thus falls by this cash-asset portfolio allocation effect.

These wealth effects triggered a rise in the value of e (at initial i) and fall in i (at initial e) can be illustrated by the same rightward shift of the ee curve and the downward shift of the ii curve respectively as in Figure 3. The overall change in the values of exchange rate and the domestic interest rate are given as (see Appendix):

Overall, it appears that the effect on domestic investment is ambiguous. But, since the portfolio allocation effects are triggered by the wealth-effect, so even if the net portfolio-allocation effect is adverse—by which the domestic investment falls—it is likely to be weaker. Hence, an increase in the money supply should raise the domestic investment. More precisely, as shown in the Appendix, this is ensured by the following condition:

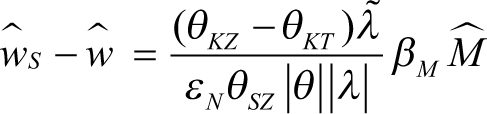

Larger domestic investment thus raises capital formation, and the capital stock, which raises the price of the non-traded good, and reinforces its rise due to depreciation of the nominal exchange rate per se by the logic explained in the earlier section. Thus, now the real exchange rate will appreciate ambiguously under the factor-intensity ranking Equation (21):

Again the unskilled wage will rise unambiguously whereas the wage inequality will decline for

Thus, an expansionary monetary policy, like a credit expansion through lowering of the CRR, helps mitigate the adverse wage-effects of the inflation-targeting policy of the foreign country.

Conclusion

In this article, we have examined the effect of inflation-targeting interest rate hike by a foreign country on the wage inequality between skilled and unskilled workers in its trading partner. In a competitive three sector general equilibrium framework with endogenous capital formation financed by the supply of loanable funds by the domestic wealth-holders, we have shown that an interest hike in the foreign country may worsen the wage inequality by lowering the domestic investment, capital formation and changing thereby the composition of aggregate output if capital-cost share in the composite traded good is larger than the capital-cost share in the skill-based export-good. The domestic central bank can mitigate such adverse effects through credit expansion by lowering the CRR or through an increase in money supply.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.