Abstract

In Indian economy, the cashless transaction is not a new phenomenon. However, the pandemic gave a sizeable push in the endeavour to marginalise cash transactions. The objective of this article is to discover the actual impact of Covid-19 on the preferences of people while making transactions. For primary data collection, Google questionnaire was sent all over India to all age-groups. Respondents are from all types of socio-economic status. Graphical and tabulation approach was used as a data tool. In this research article, a comparative study has been done for analysis. It has been observed that when the cases of Covid-19 were on the rise in India, the digital mode of payment became a lifesaver as it not only eliminated the risk of social contact but also provided safety from leakage in the economy with better security as well as an easy and convenient way of transferring money.

Keywords

Introduction

The Coronavirus pandemic shook the overall economy of the world, so there was no way for India to be left unharmed by this major shock. According to the Ministry of Statistics, Government of India, a downfall of 3.1% in growth was experienced during the fourth quarter of fiscal year 2021. As per the Chief Economic Advisor to the Government of India, this drop was mainly due to the Coronavirus pandemic, and in the opinion of the World Bank, ‘the current coronavirus pandemic has magnified pre-existing restraints on India’s economic outlook’. The recently revised India’s growth rate by the World Bank and other rating agencies for FY 2021 turns out to be the lowest figures that India has experienced since India’s Economic Liberalisation in 1990s. Cybernated transactions refer to digital transactions. India’s digitalised economy experienced a boom, with Indians taking interest in advanced and easy-to-use cashless transaction methods for shopping, paying bills and purchasing day-to-day items, including the transfer of funds. The rising inclination of Indians towards digital transactions was further catalysed by the Corona pandemic situation and constant lockdowns, which made more and more people acknowledge and utilise cashless transaction methods. People have started preferring cashless transactions over cash payments, and there has been a sudden increase in quantity as well as frequency of cashless transactions. It is evaluated that the number of cashless transactions per capita has soared as high as 22.42 (January 2021). Keeping this in view, a survey was also conducted to analyse the current situation. The outcomes and results of the survey are included in this article.

Objectives

The objectives of this article are as follows: to discover the actual impact of Covid-19 on the preferences of the people while making transactions, to analyse the situation of cashless transactions in India and prevalent methods used to do such payments, to ascertain the number of users indulging in digital transactions, to evaluate and compare the cashless transactions per capita per annum over 5 years to evaluate and compare digital transaction volumes by various cashless transaction methods every year to get a glimpse of how Corona pandemic gave a boost to cashless transactions and to discuss various initiatives taken by the government to increase the volume of digital transactions in India to facilitate the public in general amidst the Covid-19 pandemic.

Research Methodology

This research article is based on a quantitative research approach. For primary data collection, Google questionnaires was sent across India to various age-groups of people. Respondents were of different types of socioeconomic status. There were ten multiple-choice questions in the questionnaire. A total of 532 responses were received. Graphical and tabulation approaches were used as data analysis in a comparative study.

Cashless Transactions in India at A Glance

The inception of cashless transactions in India took place in 1990, when the Government of India came up with the concept of online banking, which greatly transformed the perspective of financial services. Further, cashless transactions in India became more prevalent during the time of demonetisation, when India was striving to become a cashless economy. The pandemic served as a catalyst for these cashless transactions.

As per the forecast done by Accenture, there an estimated 9.5 trillion rupee aggregator market in the Payment Gate-way of India. It was also estimated that about 66.6 billion transactions worth $270.7 billion would be transferred from cash to cards and cashless transactions by 2023 in India would, and will further increase to $856.6 billion by 2030.

This indicates that the point of stagnation for the industry of digitalised payments is nowhere in the near future, but this industry has a lot of potential for growth and development, and the various estimates by rating agencies (like Credit Rating Information Services of India Limited (CRISIL)) prove that these cashless transactions are increasing continuously both in frequency and in volume.

Cashless transactions have been readily adopted by the general public of India as they include various advantages such as consumer convenience, safety, protection, speedy transactions, financial gains and no financial leakages. This leads to a win–win situation for the customers of cashless transactions.

The various modes of cashless transactions available in India are as follows: Unstructured Supplementary Service Data (USSD) channel; mobile wallets (e.g., Paytm, Freecharge, Mobikwik, Oxigen, mRupee, Airtel Money, Jio Money, SBI Buddy, Citrus Pay, Vodafone M-Pesa, Axis Bank Lime, ICICI Pockets, SpeedPay, etc.); mobile banking, Aadhaar-enabled payment system (AEPS); banking cards, including debit cards and credit cards; unified payments interface (UPI) and internet banking.

Impact of Covid-19 on Preferred Mode of Transaction

Keeping in view the recent emerging trends in change of mode of transaction, the authors conducted a survey to check in reality the current status of cashless transactions in India.

In the survey, an attempt was made to ascertain: the impact of Covid-19 on the preferred mode of payment by respondents, the hindrances in the adoption of digitalised payments distribution of the sample population making transactions by the attributes of age and future expectations of respondents.

The survey insights are as follows:

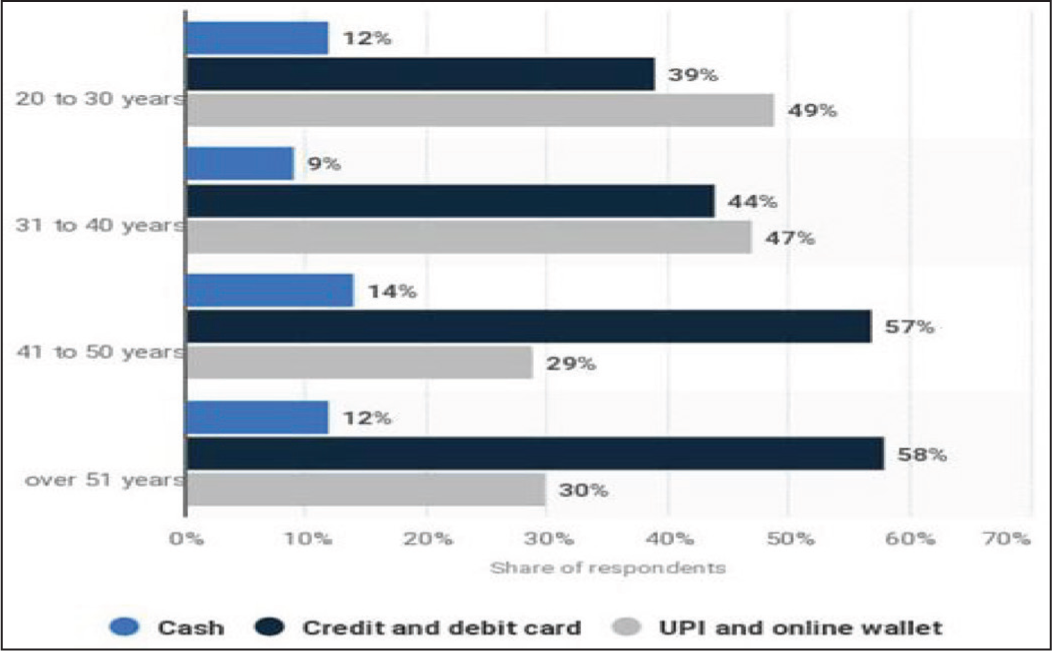

A total of 532 respondents formed the sample population for which the online survey was conducted. The respondents from the age group of 20 to 30 years constituted the maximum number of respondents. The survey depicted that about 88% of the participants from the age-group of 20 to 30 years, 91% of the participants from the age-group of 31 to 40 years, 86% of the participants from the age-group of 41 to 50 years and 88% of the participants from the age-group of 51 and above used digitalised payments (credit card debit cards and UPI payments) as their mode of transaction. This implies that the majority of all age-groups preferred digitalised transaction over cash payments (Table 1 and Figure 1). Age No Barrier: Survey Reveals Digital Payments Preferred Across All Age Groups.

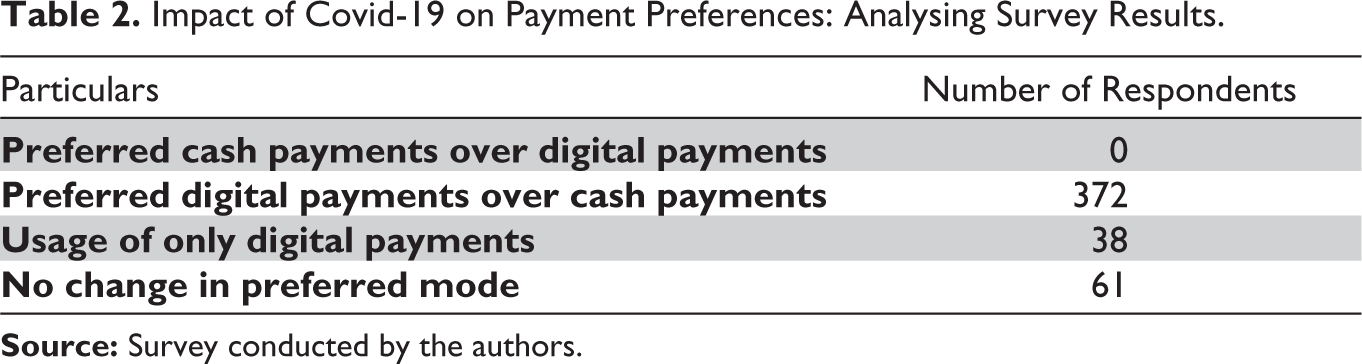

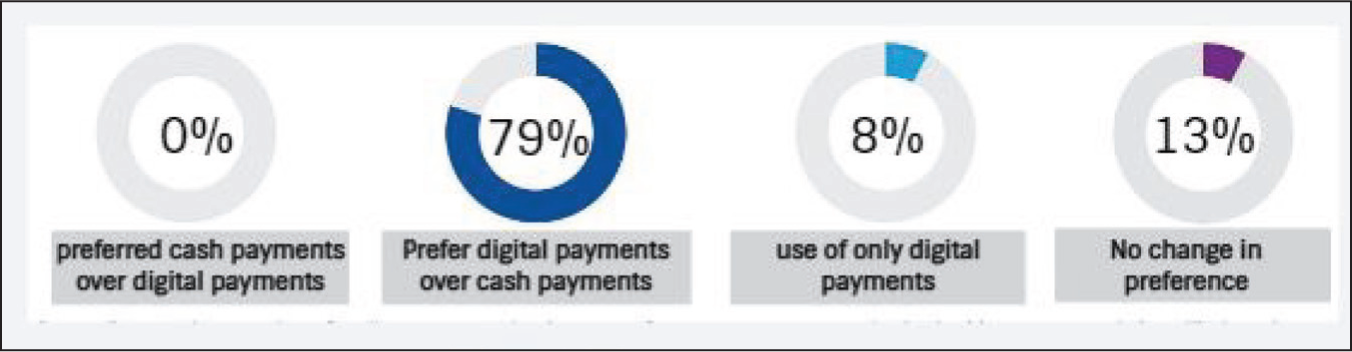

The data about the impact of Covid-19 on preferred modes of payment are presented in Table 2 and Figure 2 for ease of comprehension of the outcome of the survey conducted.

Impact of Covid-19 on Payment Preferences: Analysing Survey Results.

The results of the online survey portray that a majority of 79% of respondents reportedly preferred cashless transactions over cash payments during the Covid-19 pandemic. This change, however, was not due to an insignificant reason but contained a series of reasons, some of which were the maintenance of physical distance for convenience and safety. Some respondents, amounting to 8% of the total sample population, responded that they only used cashless transactions during the Covid-19 pandemic.

The survey also showed that there was no backward flow from digital transactions to cash transactions, as about 13% of the total respondents stated that there had been no change in their preferred mode of transactions, whether cash or digital.

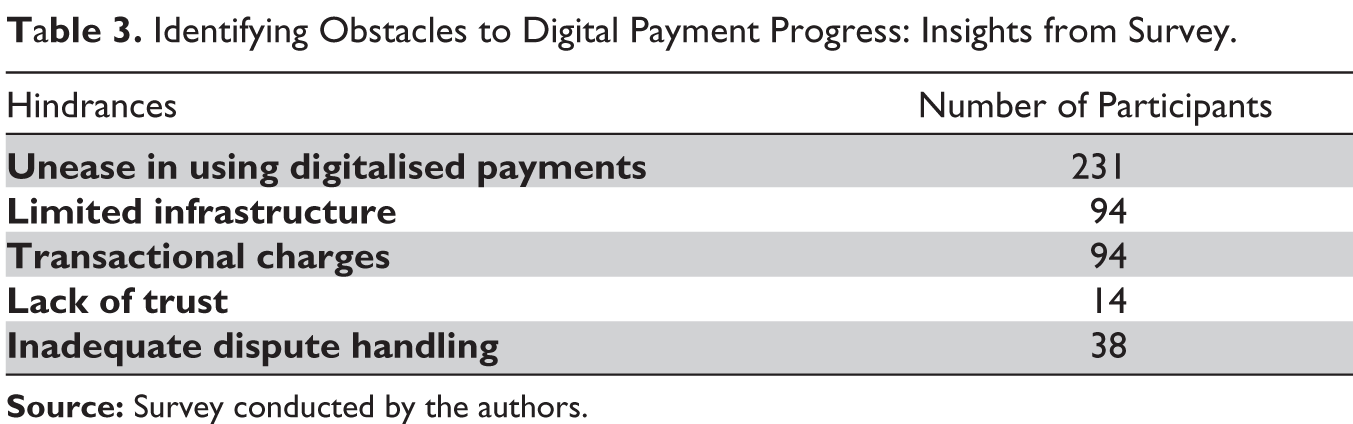

The survey conducted gave insights regarding the impediments to digitalisation progress in the case of payments. It became necessary to determine the obstacles to solve them and promote the use of digital platforms for transactions (Table 3).

Identifying Obstacles to Digital Payment Progress: Insights from Survey.

The prominent limitations encountered by people in general (of India) have been depicted in Figure 3.

The obstacles highlighted by the respondents in the adoption of cashless transactions in India included unease with using digitalised payments, limited infrastructure, transactional charges, a lack of trust and inadequate dispute handling. Amongst all these hindrances, most participants indicated a lack of awareness across various aspects in using digitalised payments, such as the transactional mechanism, use of vouchers and discount codes, as major obstacles. However, only 3% of the respondents reported a lack of trust as a hindrance. A considerable number of respondents, amounting to 20% of the sample population, were concerned with the transactional charges, and 20% of the sample population had limited infrastructure as their obstacle to adopt digitalised payment.

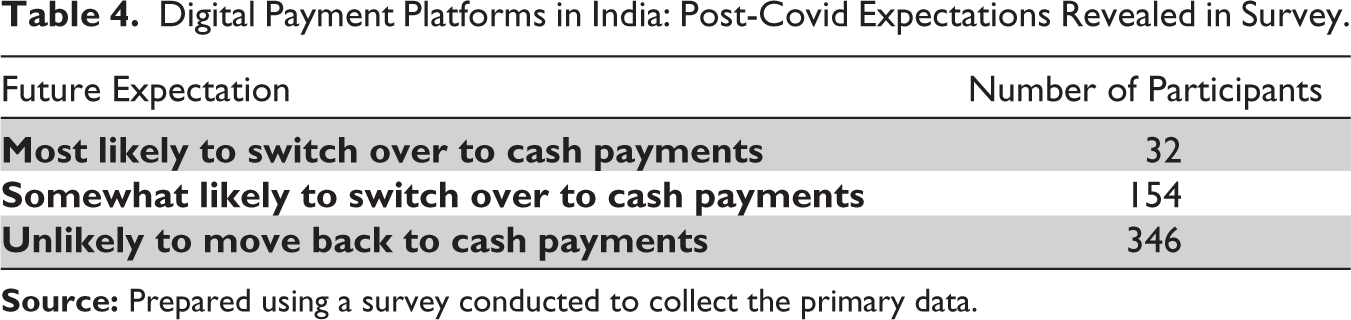

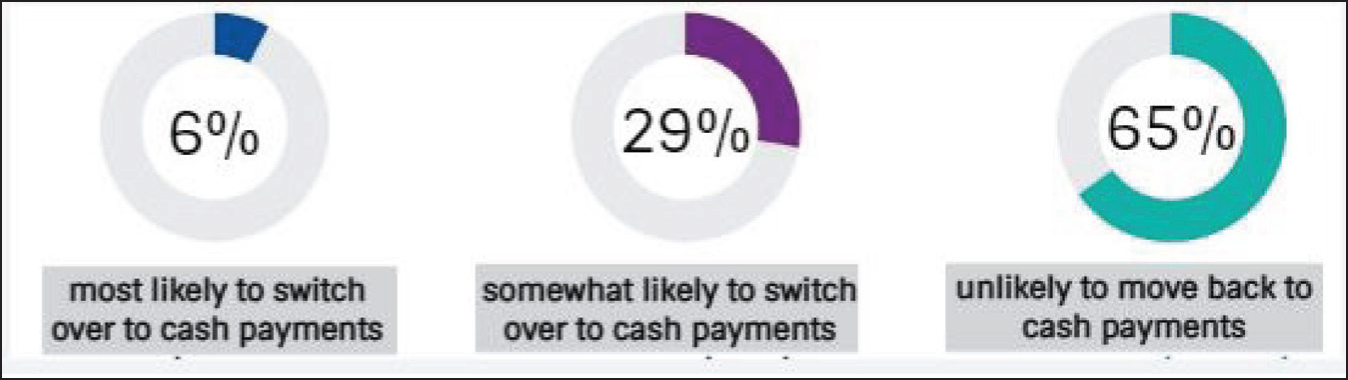

Table 4 gives an insight into the probable expectation of people in India, surveyed regarding the furtherance of using digital payment platforms after Covid-19 pandemic.

Digital Payment Platforms in India: Post-Covid Expectations Revealed in Survey.

Figure 4 depicts (in percentages) the furtherance of using digital payment platforms after Covid-19 pandemic, based on the responses received from the survey.

When given an option to the respondents about their future expectations regarding the change in the preferred mode of payment after the Covid-19 scenario, the majority of the participants, amounting to 65%, were certain about not moving from cashless transactions to cash payments. However, about 29% of the participants were somewhat likely to switch over to a cash mode of payment, and only 6% of the participants were most likely to switch over to cash payments after the Covid-19 pandemic.

Figure 5 depicts the frequently used applications for digital payments (as per the responses received in the survey conducted).

As per the reports of Statista Data Collection Committee, an online survey was conducted on 2,345 participants to find out about various cashless transaction apps used in India, amongst which Paytm was used by the majority of 33% of the Indian sampled population who use digital transactions.

Despite the controversies surrounding the Google Pay app, a significant portion of the population uses it. The BHIM and PhonePe apps are also used, but they are not as popular among the Indian population. Amazon Pay is also spreading its wings in the Indian cashless transaction market, and there are still 33% of people using other apps for cashless transactions in India.

Figure 6 depicts a comparative analysis of per capita digital payments as sourced from the website of The Times of India.

According to the recent data from the source of The Times of India about comparative analysis of per capita cashless transactions, there has been an evident rise from 2014 to 2020 in the per capita cashless transaction. While in 2014 it was just 2.38, there was a significant rise in the year 2019 of about 22.42. However, the most significant rise was between the years 2019 and 2020, which showed more than a 50% rise in the per capita cashless transaction.

Recent Initiatives by the Government of India to Boost, Monitor and Measure Cashless Transactions

Promotion of Digital Payments in Government Sectors

For the purpose of promoting cybernated transactions in every sphere of the economy in India, the Government of India, in 2017 took the first step by digitalising all the transactions withheld within the government periphery through electronic modes. There was a target recommended that was time-bound to be implemented on citizens to make sure that all the citizens were aware of and well-educated to avail the e-services of government ministries and departments by the Apex Committee on Digital India. For the promotion of hassle-free digital or electronic payments and receipts, the Ministry of Electronics and Information Technology (MeitY) of India is now working towards advertising paperless, cashless and faceless services all over the country, giving special importance to the rural and remote parts of the country. Further, the Ministry has envisaged a common e-governance infrastructure offering a front-end and back-end cashless transactional experience to citizens, businesses and internal government functions. E-Mitra has also been established and brought into functioning in every nook and corner of India. Central Public Sector Undertakings, state governments, autonomous bodies and municipalities have been notified of the guidelines for electronic payments and receipts to swiftly implement appropriate mechanisms in order to enable cashless payments and receipts. In a nutshell, the various objectives to be fulfilled by these guidelines for departments are as follows: to examine and evaluate diverse services involving payment and receipts that can be converted into cybernated mechanisms; to provide such instructions on the adoption of digitalised modes, those are universally adopted and actionable and furnished with such guidelines that enable rightful and appropriate engagements with various payment service providers.

Such guidelines for electronic transactions shall only be implemented after a thorough assessment of the department’s overall status of services offered, and then a depository of services offered by such departments will be maintained. This depository will be used for measuring and tracking of the adoption level of electronic payments across departments in India. This particular depository also fulfils the objectives of setting up an integrated system that will be shared by government and private sector payment systems for empowering digitalised modes and channels of such payments.

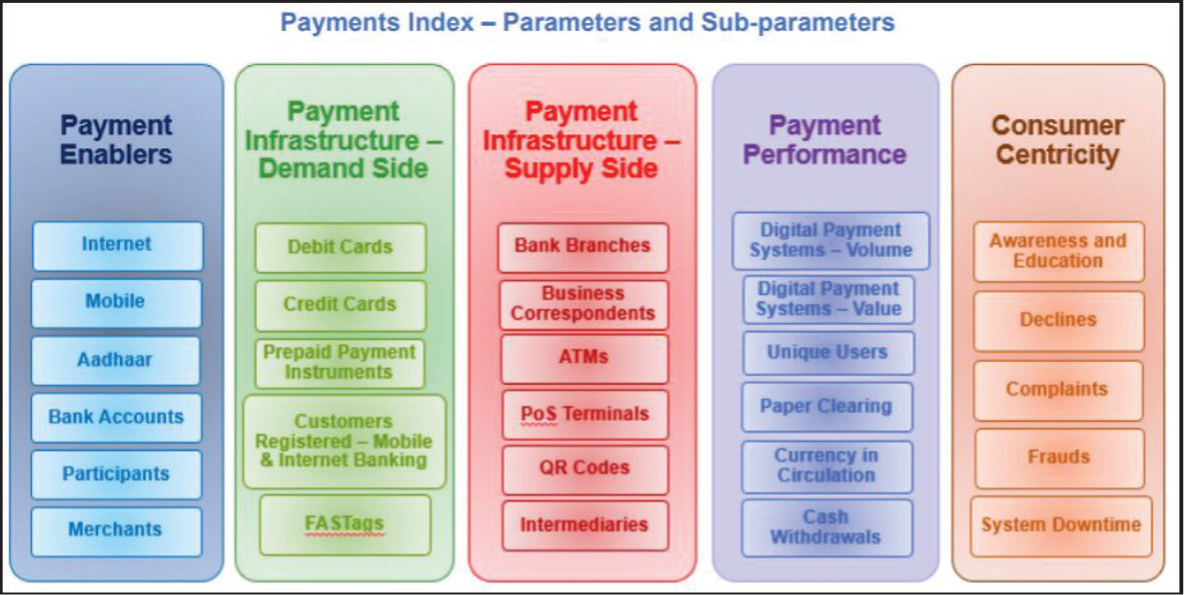

Introduction to Digital Payment Index

With the intention of capturing the extent of digitalisation of payments in the country, the Reserve Bank of India introduced a composite digital payment index. With the help of this RBI digital payment index, it would be possible to measure the area and volume of penetration of digital payments in India quarterly. To achieve this objective, the index has covered five broad parameters, namely payment enablers, payment infrastructure of demand-side factors, payment infrastructure of supply-side factors, payment performance and consumer centricity. Keeping in view that different parameters have different impacts, weights are also assigned to these parameters to facilitate authentic and accurate calculation.

Figure 7 presents all the parameters and sub-parameters used to calculate the Digital Payment Index in a brief.

As per the official site of RBI, the payment performance parameter has the most weight of 45%, whereas consumer-centricity has the least weight of 5%. Payment infrastructure on demand-side factors is given a weight of 10%, and payment infrastructure on supply-side factors is given a weight of 15%. Payment enablers have a weight of 25%. The base year for DPI is March 2018 and its value is 100. The digital payment index is to be published on RBI website on a semi-annual basis from March 2021 onwards quarterly. The digital payment index for March 2019 is calculated as 153.47 and for March 2020 is 207.84, which shows remarkable growth in digital payments. With the help of the digital payment index, certain data have emerged showing that in the second quarter of the year 2020–2021, UPI payments jumped up to 99% in value as compared to 82% recorded in the same quarter last year.

According to the Worldline India Digital Payments Report, there were 174 Banks providing UPI services in September 2020. India is also ranked seventh among 24 countries engaged in tracking digital payments by the Bank of International Settlements.

Use of Low-Cost Digital Models

The government made it mandatory for any business entity whose annual turnover was more than 50 crores to offer low-cost digital mode of payments, and there cannot be imposed any charges for this from customers as well as merchants. India is thriving in the field of digitalised payments, but there is still a segment of people who are unaware and uneducated about such payment modes. In order to promote digital platforms, the government of India is driving a low-cost, inclusive digitalisation model. For the purpose of bringing out a larger economic perspective of the manufacturing industry along with digital India mission, ‘Voice of Manufacturing Edition 6-Digital Transformation in Manufacturing Value Chain’ was organised by National Association of Software and Services Companies (NASSCOM).

As per the NASSCOM report, the session of Voice of Manufacturing 6 emphasised on industry economic growth and digital vision and was graced by the participation of Dr Ajai Garg, Senior Director, MeitY; MP Dubey, Joint Director, Software Technology Parks of India (STPI) Andhra Pradesh (AP); Pranjal Sharma, economic analyst, author and advisor, World Economic Forum (WEF); Dr Shishir Shrotriya, Counsellor (science and technology), Embassy of India in Moscow; and Ravi Aggarwal, President, Automation Industry Association (AIA).

The government has always played a pro-active role in promoting digitalised payment, and now after lockdown, that can be seen as significant growth in pre-Covid and post-Covid eras. The digitalised payment sector is slowly transitioning from a monopoly regime to a concept of trusted global supply-chain partners. Along with this low-cost, inclusive digitalisation model, India is bound to improve productivity in all of the key economic centres. This is a huge step towards the techno-domain outlook of Indian industry, giving easy access to funds and resources to 50,000 startups that came into existence during the lockdown.

Lucky Grahak Yojana and Digi-Dhan Vyapar Yojana

These programmes are initiatives taken by the Government of India to attract more and more consumers as well as merchants towards digital transactions by offering cash rewards for personal consumption expenditures.

To motivate the people in the direction of higher usage of digital transactions, the Government of India launched two schemes: Lucky Grahak Yojana for consumers and Digi-Dhan Vyapar Yojana for merchants. The Lucky Grahak Yojana and the Digi-Dhan Vyapar Yojana offered cash awards to consumers and merchants who utilised digital payment instruments for personal consumption expenditures. These schemes were implemented by the National Payment Corporation of India (NPCI), focusing on bringing the poor, lower-middle class and small businesses into the digital payment scenario. The scheme was operational from 25 December 2016 to 14 April 2017.

The criteria to participate in this yojna were as follows:

All transactions from consumers to merchants, consumers to governments and all Aadhar Enabled Payment System (AEPS) transactions done from 8 November 2017, were eligible. Person-to-person and business-to-business transfers were not eligible. Customers and merchants using RuPay Card, BHIM, UPI (Bharat Interface for Money/Unified Payment Interface), USSD-based service and AePS were eligible to participate in the daily and weekly lucky draws. Transactions through credit cards/e-wallets were not eligible. Transactions between ₹50 and ₹3,000 are only considered valid for availing benefits of the scheme.

Procedures for the programme were as follows:

The winners were identified through a random draw of the eligible transaction EDs (which were generated automatically as soon as the transaction was completed) by software specially developed by the National Payments Corporation of India (NPCI) for this purpose. The winners of the lucky draw receive a message from their banks, and the reward money is credited into their bank accounts over the next 24 hours. The draws for these events took place in 100 different cities around India, with an event at each of these cities where Digi-Dhan Mela was also organised. The presence of various stakeholders of the digital payment ecosystem, like banks, wallets, telecom service-providers, other financial service providers and the Unique Identification Authority of India (UIDAI) at these Digi-Dhan Melas provided the opportunity for the citizens—both consumers and merchants—to get educated about the digital payment options available, the ease of use and also the benefits from handholding provided by the service-providers, which would encourage wide-scale adoption of digital payment methods. In the long-term, such a mass movement is expected to shift large sections of the consumer and producer sections, which were hitherto in the informal sector, to the formal fold of the economy.

Other Measures Taken by the Government to Promote Cybernated Transactions

The Government of India has been keen on increasing the proclivity of people towards digital payment platforms since 2017, and to ensure growth in the number of digital payers, there are various initiatives taken, which are as follows:

₹

Findings

When cases of Covid-19 were on the rise in India, the digital mode of payment became a lifesaver as it not only eliminated the risk of social contact but also provided safety from leakage in the economy, better security and an easy and convenient way of transferring money. Some of the recent findings from the survey conducted are as follows:

There has been a sudden increase in cashless transactions all over India when all the industries were combating the situation of Covid-19 and struggling to even survive in this scenario. The industry of cashless transactions has grown rapidly in the past few years. One of the most important findings is that most of the digital transactions are done by people between 20 and 30 years old, as they are somewhat advanced and have the technical know-how to do the transactions digitally, contributing to about 48% of the total digitally active population. The number of digital transactions in India is spreading at a massive rate and has reached 31.1 8 per capita in cashless transaction. The companies of Paytm and Google Pay are the preferences of the Indian population, and about 40% of the total population who are digitally active are using the above-mentioned apps. From the survey, it was evident that 94% of the population of India in urban areas had switched over to cashless transactions from cash had no intention of moving back to cash payments. Indian population is still apprehensive about cashless transactions because of security and trust issues, which lead to disinterest in cashless transactions. With the government’s initiatives to boost cashless transactions in India, there is no doubt that there will be rapid growth in the cashless transaction industry. Cash is not expected to disappear in the near future as people have difficulty in making digital transactions due to inappropriate infrastructure, lack of awareness and cash payments not being in their comfort zone. The Covid-19 Pandemic has played a great role in moving people from cash-based transactions to digital-based transactions, leading to an unprecedented rise in transaction volume in digital transactions post-lockdown.

Conclusion

Cashless economy is not a new phenomenon in India. Cashless transaction system in India has witnessed a steady transformation since the 1990s with the liberalisation of the banking industry and the introduction of new technologies. Thereafter, various payment products and service providers were launched from time-to-time. With demonetisation and introduction of GST, the people of India are bound to be IT-friendly. Covid-19 has given a sizeable push to the endeavour to marginalise cash transactions. But in this cashless mode, consumer awareness and security are the major issues and need to be regulated by governments. The increased adaptation in the short-term is likely to accelerate the sustained shift towards cashless transactions.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.