Abstract

Although firms in diverse industries increasingly adopt private regulation of labor standards for workers in their global supply chains, growing scholarly evidence suggests that this approach has not generated sustainable improvements in working conditions for those workers. The authors draw on recent developments in institutional theory regarding the development of opaque institutional fields that cause the decoupling between practices and outcomes to develop a new explanation for the lack of sustainable improvement in labor practices in supply chains. Using qualitative and quantitative data from a global apparel supplier and a global home products retailer, they demonstrate the various ways in which opacity causes decoupling between private regulation practices of global firms and outcomes for workers in supply chains.

Keywords

A variety of private regulation models were adopted by global apparel and footwear companies in the early 1990s in response to pressure from activists and consumers over sweatshop conditions in global supply chains. The most popular model consists of three elements. The first element concerns the setting of standards regarding labor practices in global supply chains through a code of conduct that is generally based on International Labour Organization (ILO) conventions. The second element, auditing, involves checking whether supplier factories comply with the code of conduct and is carried out directly by the brands or subcontracted to specialist auditing firms. The final element incentivizes suppliers to improve compliance with the code by linking future sourcing decisions to their compliance records (penalizing or dropping noncompliant suppliers and rewarding more compliant ones).

On the one hand, this model has diffused among many industries such as horticulture, home furnishings, furniture, fish, lumber, fair trade coffee, and others, while also spawning a complex, burgeoning supportive ecosystem of actors and institutions (multi-stakeholder initiatives, auditing firms, critical nongovernmental organizations [NGOs], and consulting firms). On the other hand, there is steadily mounting scholarly evidence that the model has not generated sustainable improvements in living standards of workers in the global supply chains (Appelbaum and Lichtenstein 2016). Thus, we have a puzzling situation in which this private regulation model continues to be adopted despite reports of its ineffectiveness. The research question this article addresses is: Why is there a gap between policies and practices of private regulation and the intended outcome of sustainable improvements in labor standards in global supply chains?

Two general explanations have been advanced for such a gap. The first, popular among critics, has focused on “symbolic adoption,” whereby companies adopt private regulation primarily as a strategy to minimize reputational risk, without seriously implementing it (see Esbenshade 2004). A second explanation points to faulty assumptions underlying the model’s design and a variety of problems in each step of its implementation (e.g., Locke 2013; Amengual, Distelhorst, and Tobin 2019). The symbolic adoption thesis does not fully fit the facts given that many global companies have not only adopted but have, to varying degrees, implemented a private regulation strategy. It is also unlikely that the few cases of specific implementation problems found can account for the policy-practice-outcomes gap noted in the organizational field of private regulation as a whole. Therefore, we draw on recent developments in institutional theory regarding organizational decoupling (Bromley and Powell 2012; Wijen 2014) to explain the general policy-practice-outcomes gap in private regulation with respect to labor standards.

Our argument is that actor heterogeneity in private regulation of labor standards generates opacity that results in practice-outcomes decoupling. More specifically, we develop propositions regarding how heterogeneous actors contribute to the three characteristics of field opacity identified by institutional scholars. These include practice multiplicity (the diversity of practices adopted by actors across sociopolitical and geographic spaces), behavioral invisibility (the difficulty in assessing the behavior of actors such as suppliers), and causal complexity, whereby a “multitude of interconnected heterogeneous actors and factors interacting in non-linear ways creates uncertainty about cause-effect relations” (Wijen 2014: 306–7). We test our argument using novel qualitative and quantitative data from two “best of breed” sources of data.

Our qualitative evidence is drawn from a detailed analysis of two factories of a global supplier and is used to show how suppliers face practice multiplicity and decoupling as a result of brands’ diverse rating scales and rating methodologies. Our quantitative data is drawn from audit records provided by a highly reputable global retailer combined with data from payslips of 1,543 workers from 30 of its suppliers in China. The analysis of this data shows that the global retailer experiences behavior invisibility and decoupling in auditing suppliers in diverse locations even when auditing supposedly easy-to-measure outcomes such as wages and hours. Finally, we demonstrate that well-established causes of compliance identified in prior private regulation literature have uncertain effects in this case, when examined in conjunction with a variety of other variables such as supplier and worker characteristics, suggesting some uncertainty regarding cause-effect relations.

In showing how field opacity and the decoupling of practices and outcomes exist in even highly progressive leading brands and suppliers, our contribution to the private regulation literature is to outline an alternative, systemic explanation for the gap between practices and outcomes noted. In essence, we suggest that it is not only the problems with symbolic adoption or individual elements of the private regulation model that contribute to its lack of effectiveness, but that the complex ways in which actors interact in an opaque field also play an important role. In so doing, we also make a modest contribution to institutional theory by testing and extending recently advanced arguments to private regulation of labor standards in global supply chains.

Relevant Literature

As is well established (e.g., Elliott and Freeman 2003; Bartley 2007), the inability of governments to effectively enforce their labor laws in apparel sourcing locations, coupled with pressure from activists and consumers, forced global apparel firms to adopt private regulation in the early 1990s. Although private regulation takes many forms, such as certification and reporting systems (e.g., Goodweave, Global Reporting Initiative, UN Global Compact), the most common form is through corporate codes of conduct. The key elements of the model are that companies articulate a code of conduct for their supply chain (either directly or adopting the code of conduct of a multi-stakeholder institution), engage in “auditing” (again directly or through third parties) to evaluate the extent to which supplier factories comply with their code, 1 and then use these results to direct the factories to “remediate,” rewarding the factories that do and punishing those that do not. These three design elements have not changed significantly since their introduction in the early 1990s, and this form of private regulation has been widely adopted in many industries such as toys, electronics, accessories, jewelry, aquaculture, food processing, furniture, household products, office supplies, pharmaceuticals, and many more.

Consequently, the associated ecosystem of private regulation has grown. The ecosystem includes a number of independent “social auditing” businesses (e.g., Verite, SGS, Intertek, ELEVATE); multi-stakeholder standard-setting organizations (e.g., Fair Labor Association [FLA], Ethical Trading Initiative [ETI), Social Accountability International [SAI]); organizations involved in providing platforms for sharing of auditing information (e.g., Sedex); private foundations (e.g., C&A Foundation); student organizations (e.g., United Students Against Sweatshops); and critical NGOs (e.g., Oxfam, Labor Behind the Label) that focus on pressuring global brands to improve labor and environmental standards in their supply chains. More recently, new multi-stakeholder organizations have evolved to facilitate coordination among brands, such as the Bangladesh “Accord” on Fire and Building Safety.

Researchers increasingly believe, however, that the growth in the private regulation ecosystem has not been accompanied by a steady improvement in labor standards in global supply chains. Although the number of empirical studies is limited, they point to only a modest increase in overall compliance, but with continuing violations of many labor standards. This is evident in several studies, for example, the analyses of auditing scores from Nike and HP (Locke, Qin, and Brause 2007; Distelhorst, Locke, Pal, and Samel 2015); the analysis of audit data from specialized auditing firms (e.g., Toffel, Short, and Ouellet 2015); the analysis of audit data from multi-stakeholder initiatives such as the FLA (Anner 2012; Stroehle 2017) and Fair Wear Foundation (Egels-Zandén and Lindholm 2015); and semi-public auditing reports by ILO’s Better Factory Cambodia (BFC) project (Oka 2010a, 2010b; Ang, Brown, Dehejia, and Robertson 2012). A variety of investigative reports from NGOs reach similar conclusions (e.g., Oxfam, Labor Behind the Label).

These studies indicate that compliance varies across the different audit data sets and across different labor issues. The variation in overall compliance with specified standards across industries is large, ranging from low levels of compliance in the toy sector (Egels-Zandén and Lindholm 2015: 35) to an average compliance level of approximately 65% among Nike’s 575 suppliers from 2002 to 2005 (Locke et al. 2007: 10). Compliance is generally weaker with respect to “enabling rights” such as freedom of association and collective bargaining, relative to other rights such as freedom from child labor (e.g., Bartley and Egels-Zandén 2015). Steady improvement is generally absent. Locke (2013: 31) noted that supplier factories “cycle in and out of compliance” and that average compliance rates of all Nike suppliers between the 2001 to 2004 period and the 2009 to 2012 period look remarkably similar, suggesting a plateau effect. Evidence from qualitative case studies complements the evidence from the previously noted empirical studies (Esbenshade 2004; Ngai 2005; Rodríguez-Garavito 2005; Barrientos and Smith 2007; Egels-Zandén 2007; Locke et al. 2007; Yu 2008; Koçer and Fransen 2009; Anner 2012; Lund-Thomsen et al. 2012; Egels-Zandén and Lindholm 2015; Appelbaum and Lichtenstein 2016), as does evidence from worker surveys (e.g., Chan and Siu 2010).

Prior research has generated explanations for the lack of compliance and identified compliance correlates. Studies have identified problems with each of the three elements in the model. An early criticism focused on the multitude of codes and standards adopted by companies, which results in audit fatigue for multi-brand suppliers, affecting their ability to comply effectively. The auditing element has attracted the most attention as a cause for compliance failure. Locke (2013) argued that the assumption that reliable high-quality information can be gleaned through the auditing process is unwarranted, given the differential interests of buyers and suppliers. Buyers often want suppliers to invest in greater compliance while simultaneously reducing the price they pay for the product. This condition provides incentives to suppliers to cheat by preparing alternate sets of records, and to coach workers to give desired responses to auditors’ questions. These actions are made easier because audits are announced in advance. Alternatively, suppliers will subcontract production to second-tier and third-tier factories that are not the subject of brand auditing. Thus, auditing becomes an adversarial “cat and mouse” game, whereby auditors try to obtain “the elusive real data while factory managers offer suspicious or partial records and workers parrot answers that auditors suspect are coached” (Bartley et al. 2015: 163).

The relatively short duration of most audits (1–2 days) makes it difficult to uncover compliance violations, especially because auditors do not triangulate with off-site worker interviews. Auditors are generally poorly trained, and given that auditing has become a low-cost commoditized activity, auditors tend to “satisfice” by cursory checks of documents and to engage in “check the box” exercises without focusing on root causes. Finally, audit fraud is commonplace (e.g., auditors are paid bribes to overlook violations, or audit records are falsified). Extensive reviews of such auditing problems can be found in Locke (2013: 36); Bartley et al. (2015); and Short, Hugill, and Toffel (2017).

Finally, little evidence has shown that companies link future sourcing to supplier compliance records. This topic has been the least researched, given that brands have not shared their sourcing data. We note two specific problems here. First, it is not at all clear that corporations have modified their business models to reward more compliant factories with more orders. As Bartley et al. (2015: 162) suggested, “some brands and retailers have well-staffed and well-meaning compliance departments, but these departments rarely have the power to shape decisions of the production/sourcing departments.” Amengual et al.’s (2019) case study (in this special issue) of a company determined to link sourcing and compliance found that suppliers who complied received fewer orders than did suppliers with lower compliance. This lack of connection between compliance and sourcing is a key failure in private regulation, consistent with Locke’s (2013) dismissal of the assumption that incentives can be designed in ways that meet all actors’ interests. A second problem is that sourcing practices are often the root cause of noncompliance. Through low prices and short turnaround times, brands squeeze suppliers (Anner 2018), who react by violating labor standards (Oxfam International 2010; Barrientos, Gereffi, and Rossi 2011). Short turnaround times, coupled with unpredictable order changes often lead to excessive overtime (Locke 2013), as managers drive workers to fulfill orders out of fear of losing the customer’s business. Yet, the private regulation model does not build in sourcing practices as a key element.

Concerning determinants of compliance, scholars have suggested that leverage, that is, the percentage of a factory’s production purchased by the brand, is an important driver of compliance (Fitjar 2011). But leverage is not typically high as suppliers tend to apportion their capacity among many brands to diversify market risk, consistent with Locke’s (2013) argument that the assumption of asymmetric power relations wherein large buyers have tremendous influence over their suppliers may be unwarranted. Some evidence exists that long-term, collaborative relationships (relational contracting) could improve compliance (Frenkel and Scott 2002; Locke et al. 2007; Locke and Romis 2010; Oka 2010b; Knudsen 2013; Distelhorst et al. 2015; Toffel et al. 2015).

Other correlates of compliance include the institutional context. Compliance is generally better in host countries with stronger protective and effective labor law enforcement (Koçer and Fransen 2009; Toffel et al. 2015), or in factories in countries where leading brands are involved in multi-stakeholder initiatives (Oka 2010a, 2010b), such as the ILO’s Better Work Program. Organizational characteristics of brands and suppliers have also been linked to compliance; for example, larger suppliers often exhibit better compliance, given their managerial capacity and resources to invest in better working conditions (Moran 2002; Baumann-Pauly, Wickert, Spence, and Scherer 2013). MNC-owned suppliers comply more than independently owned factories (Mosley 2010). An argument has been made that corporate governance matters, with privately owned companies more likely to have better private regulation programs than publicly listed companies (Quinn 1997; Fülöp, Szegedi, and Hisrich 2000). Furthermore, He and Perloff (2013) found that auditing results in better compliance for Chinese migrant workers.

Summing up existing research, Bartley and colleagues (2015: 161) noted that existing evidence suggests that they [private regulation programs] have had some meaningful but narrow effects on working conditions and the management of human resources. But the rights of workers have been less affected, and even on the issues where codes tend to be most meaningful, standards in many parts of the [apparel] industry remain criminally low in an absolute sense.

We still do not have many examples of sustained improvement in all labor standards in the global apparel supply chain, which likely accounts for the growing consensus that the private regulation model has failed to deliver (Nova and Wegemer 2016). Considerable gaps in our knowledge remain given that the vast majority of companies have been generally unwilling to publicly share compliance and sourcing data (private regulation, after all, is private). Consequently, we know relatively little about the variation in practices within and across industries, what constitutes best practice, or why there has not been sustainable progress in labor standards in global supply chains generally. As more and more companies adopt the model in diverse industries, it becomes crucial to explain why the general practice-outcomes gap exists. To do so, we turn to recent developments in institutional theory.

Theory and Arguments

Institutional theorists have studied organizations’ responses to regulatory and normative rules. Within this domain, organizational decoupling has received extensive attention, building on Meyer and Rowan’s (1977) explanation for the observed gap between formal policies and actual practices. Much of the literature has focused on this policy-practice gap, specifically why organizations adopt policies but do not implement them (Bromley and Powell 2012). Institutional scholars have argued that policy-practice gaps typically occur when organizations respond to rationalizing pressures from the environment, for example, adopting an externally induced rule to gain legitimacy or to avoid legal sanction through symbolic adoption, meaning that policies are adopted but not implemented at all or implemented so weakly “that they do little to alter daily work routines” (Bromley and Powell 2012: 7, 15). The argument is also that policy-practice decoupling is more evident early in the adoption process, where there is weak capacity to implement policies, and where internal constituents do not reinforce the external pressures for the policies (pp. 13–14). With time, however, even policies that are symbolically adopted sometimes become integrated into the organization, particularly if they are monitored through hard and soft law channels. This is clearly the case with private regulation regarding labor practices, as most firms have implemented their regimes, with formal organizational structures (such as corporate social responsibility [CSR]/labor practice departments) and practices. Hence the symbolic adoption argument may not fully explain the general ineffectiveness of private regulation.

A new strand of institutional theory posits that a second form of decoupling exists. Means-ends decoupling refers to situations in which formal structures are adopted, work activities are changed, and policies are implemented, but where scant evidence exists to show that these activities are linked to organizational effectiveness or outcomes, resulting in practice-outcome gaps (Briscoe and Murphy 2012; Bromley and Powell 2012; Wijen 2014). This form of decoupling is argued to be more prevalent in opaque institutional fields whereby external pressures are institutionalized via hard or soft law. Opacity exists when “observers have difficulty identifying the characteristics of prevailing practices, where observers have difficulty in establishing causal relationships between policies and outcomes and where observers have difficulty precisely measuring the results of policy implementation” (Wijen 2014: 302). These issues are much clearer and easier to observe in more transparent institutional fields. Therefore, field opacity contributes to means-ends decoupling such that even if the problem of symbolic adoption were resolved, inconsistencies would still exist between adopted practice and outcomes. Such decoupling does not necessarily indicate organizational failure, but it “could well be the most functionally effective path in the face of constraints, and it may nonetheless confer legitimacy” (Bromley and Powell 2012: 6). Field opacity and means-ends decoupling may explain why the private regulation model continues to be adopted, despite reports of its ineffectiveness.

Wijen (2014) identified three features of opaque institutional fields that impede compliance with sustainability standards on socioenvironmental issues. The first is practice multiplicity—the diversity of practices adopted by actors spreading across varying geographic, institutional, economic, and cultural contexts that makes it difficult to identify and engage in compliant behavior. Simply put, “the higher the number of divergent practices encountered in a field, the more difficult it is for adopters to exhaustively understand and compare the merits and limitations of different practices” resulting in ambiguity (p. 307). A second characteristic is behavioral invisibility—the difficulty of observing and measuring the behavior of actors, especially when actors operate in remote locations (most suppliers are located in the Third World). Behavioral invisibility enables suppliers who have a low incentive to disguise their noncompliance or pretend to be substantively compliant (p. 307). The third key feature of field opacity is causal complexity (uncertainty regarding cause-effect relations) because heterogeneous actors and practices interact in a given context in complex ways (p. 306). The existence of complex causes and uncertain effects (p. 306) undermines adopters’ ability to understand what drives compliant behavior and hence, inhibits their ability to implement effective practices.

Wijen’s (2014) major contribution to this literature was to suggest that adopters and regulators (he calls them institutional entrepreneurs) in opaque fields face a trade-off in their efforts to induce compliance. On the one hand, the three features of opaque fields may drive adopters to introduce concrete and uniform rules and verification systems to reduce opacity and induce compliance (p. 304) in order to solve the symbolic adoption problem. On the other hand, these standardized rules and verification systems are also more likely to cause practice-outcome decoupling because the complexity and diversity of actions and contexts call for “context-contingent approaches” (p. 305). Hence, remedying policy-practice decoupling may result in practice-outcomes gaps as the typical compliance-oriented institutions will constrain the agency of adopters to act appropriately in diverse contexts.

Wijen approached the problem of decoupling in opaque fields mainly from the regulator’s perspective, that is, how to design rules and mechanisms to reduce the trade-off. He suggested three solutions. The first is the need to develop a systemic mindset to deal with the multilevel complexity in opaque fields. The second is the need to stimulate internalization among those actors who are more likely to decouple policies and practices (such as suppliers) through supplier clubs and capability-building to reduce behavioral invisibility. Finally he suggested the development of niche institutions to translate universal approaches to more context-sensitive ones.

We draw on these ideas in this article, but we extend them in two ways. First, while Wijen alluded to heterogeneous actors when explaining causal complexity and practice multiplicity, he focused more on adopters’ dilemmas and rule design, rather than how heterogeneous actors create opacity. We extend his argument by focusing more on how actor heterogeneity results in field opacity. This is a minor shift in emphasis, but it helps us uncover new implications for practice such as the need for coordination among heterogeneous actors to improve labor conditions. Second, although Wijen’s arguments concerned socioenvironmental regulation generally, we develop specific arguments regarding the pathways through which heterogeneous actors cause opacity in the organizational field of private regulation regarding labor practices in supply chains.

Our general argument is that actor heterogeneity contributes to field opacity in ways that result in practice-outcome decoupling. Specifically, we propose that diverse global firms contribute to practice multiplicity in four ways. First, firms adopt different private regulation policies, resulting in diverse demands on suppliers. Second, firms use diverse audit practices to assess suppliers. Third, firms use a multiplicity of rating scales to assess supplier compliance, resulting in conflicting grades for the supplier. Finally, firms assign varying weights for different violations. Together, these result in inconsistent ratings that make it difficult for suppliers to comply with conflicting demands from brands and achieve divergent goals at the same time, enhancing the gap between firms’ multiple practices and intended improvement in labor standards.

We further argue that supplier heterogeneity increases the difficulty for auditors of detecting violations of code-of-conduct provisions, thereby contributing to behavioral invisibility (the inability to readily observe the behavior of actors). Supplier heterogeneity manifests in three ways. First, suppliers are typically located in different countries and regions, posing measurement challenges to auditors who need to be aware of the variety of local laws and standards affecting code provisions with respect to labor issues. For instance, codes of conduct normally stipulate that suppliers should comply with social insurance regulations, but with regard to China, these regulations vary across provinces, and change frequently. Second, suppliers (especially those supplying to multi-product global retailers) vary in terms of the products they produce and the industries in which they operate. This variation poses measurement challenges for auditors using a standard code of conduct, given that industry rules and regulations vary widely, particularly with regard to health and safety issues. Third, employment practices of suppliers vary. Shift work, flexible work schedules, payment of different allowances, and patterns of record-keeping, among others, make it difficult for auditors to readily assess overtime hours, wage compliance, and leave-taking, because a standardized code of conduct does not take into account such variations. These types of heterogeneity make it difficult to accurately assess even relatively easy-to-measure issues such as wages and hours, and especially given the short time frame of a typical audit. Given these measurement difficulties, we suggest that audit score (the usual metric that global companies rely on to assess their private regulation efforts) may not be the most reliable indicator.

Finally, we argue that actor (worker, supplier, and brand) heterogeneity contributes to causal complexity such that it is difficult to causally attribute worker outcomes to elements of private regulation. As industrial relations scholars have long known, numerous interrelated factors (institutional factors, employer characteristics, and workforce attributes) can affect workplace outcomes. These complex causes of worker outcomes may overshadow the effects of concepts such as long-term buyer–supplier relationships and high leverage (the share of a supplier’s capacity accounted for by a brand), which have been linked with compliance in prior private regulation studies. Complicating this further, the variation in the way lead firms interact with their suppliers creates uncertainty regarding what effective practices are in that context.

In sum, these new institutional perspectives constitute a promising approach to examining private regulation in action because they outline how field opacity occurs, and why it results in organizational decoupling. This permits the articulation of an alternative organizational-field-based explanation for the practice-outcomes gap with regard to private regulation of labor standards. Whereas Wijen (2014) and others have made several suggestions to increase coupling, such as the need for more transparency and niche institutions, Bartley and Egels-Zandén (2015: 233) have pointed to how unions and others could leverage symbolic commitments to create a more “contingent coupling.” Our recommendations take these approaches into consideration. But our key contribution is to illustrate how opacity is created by extending Wijen’s arguments to emphasize the role of actor heterogeneity in fostering practice multiplicity, behavior invisibility, and causal complexity in the labor practice organizational field.

Research Strategy and Methodology

We draw on two sources of data from reputable actors who have implemented private regulation practices. Our first source of data is from a qualitative investigation of how brand heterogeneity creates practice multiplicity for a large supplier (hereinafter ZZZ) manufacturing for 74 global brands. ZZZ is a vertically integrated manufacturer of woven and knit shirts, with annual revenues in excess of $1.2 billion. ZZZ is reputed to be a technological leader in shirt manufacturing, with a proven managerial capacity and a well-developed sustainability strategy. 2 As such, ZZZ is a very different entity from the stereotypical depiction of a low-cost garment supplier. We collected general data regarding audits at ZZZ by its customer brands from its nine factories, and specific data from its two most advanced factories: Factory A and Factory B in Guangdong, China. Factory A, established in 1992, has 4,038 employees (81% female) with mainly local (73%) rather than migrant workers. It employs relatively advanced equipment (RFID identification tags, pattern sewing machines, button machines, auto-run collar and cuff machines) and several processes are automated (folding, cutting, and spreading). Factory A had also met ISO 9000 and ISO 14001 quality standards. Factory B was similar to Factory A in most respects, except that it was founded in 1998 and had 6,400 employees.

We interviewed two marketing managers and three officers of the supplier’s own CSR department, including the head of sustainability, and 10 plant-level sustainability executives (five per factory) who were responsible for implementing sustainability initiatives, as well as ensuring compliance with the codes of conduct of their global customers. We also interviewed the head and deputy head of manufacturing. The focus of our interviews, which were largely unstructured, was to understand how the factories experience the audits conducted by the brands. Each of the factories supplied (at the time of our visit) approximately 16 brands. As such, they constitute an appropriate location to view practice multiplicity of heterogeneous brands.

Our second source of data, drawn from a global home furnishing retailer (hereinafter BBB), examines how supplier heterogeneity contributes to measurement difficulties. BBB was an early adopter of the private regulation model (2001) and has a reputation for a well-functioning CSR and compliance program. One of BBB’s auditors provided us with extensive detail regarding BBB’s audit protocol and how it measures supplier compliance. By 2012, BBB had required that its suppliers comply with 98.6% 3 of its 75-item code, allowing suppliers leeway to violate its code only on overtime hours. BBB’s own in-house auditors monitor supplier performance once every 12 months. The audit lasts two days and involves two auditors. BBB’s audit manager informed us that the company prided itself on setting a bottom-line compliance target for suppliers in addition to its linkage of audit results with sourcing decisions, suggesting that it goes beyond symbolic adoption. BBB provided us access to their audit data because they wanted to understand how their audits affected outcomes for workers at their suppliers. Their audit data contained a number of contextual attributes of suppliers, such as ownership, location, workforce characteristics, the length of relationships with suppliers, and the share of supplier production purchased by BBB.

We focus here on the audits of wages and hours, given that these “outcome” standards (in contrast to process rights such as collective bargaining) are considered more easily measurable (Anner 2012; Drebes 2014: 1264). The six items in BBB’s code concerning wages and hours include 1) suppliers shall pay wages according to local laws and average hourly wage shall not be lower than the local minimum; 2) suppliers shall pay overtime compensation according to local laws; 3) weekly working hours shall not exceed 60 hours; 4) workers shall have at least one day off in seven days; 5) workers shall enjoy paid leave according to laws and local customs; and 6) payment of benefits such as social security shall comply with local laws.

We then requested and received 1,549 payslips belonging to an average of 52 workers in each of the 30 suppliers. These were randomly selected by an auditor from the payrolls for the month of May 2013. The payslips show workers’ total wages, basic wages, attendance, working hours, overtime hours and pay, social insurance contribution, various allowances, and others (see Appendix). In the audit process, BBB requires that each worker’s payment information on the payroll must be signed by the worker together with his or her written legal identification number to ensure authenticity.

Our strategy was to systematically measure compliance regarding four items on wages and hours from payslips. We focus on four items based on 1,549 payslips from 30 suppliers because some issues such as paid leave and one day off in seven found in BBB’s code cannot be assessed with payslips for just one month. Our calculations of compliance (the share of workers for whom there were violations) take into account differing local and regional regulations and employment practices in the industries in which these 30 suppliers operate. We then calculate a compliance score on these items and compare it to the audit score that BB’s auditors provided. Our analytical task here is to show the challenges involved in measuring supplier behavior by examining discrepancies between BBB’s audit score and our calculations of compliance. Note that the payslips are generated on the basis of payroll records that the auditors have assessed. The only difference is that in calculating compliance we take into account local regulations and employment practices.

Finally, in order to demonstrate causal complexity, we examine the causes of compliance using both our data sources. In a quantitative analysis of our second source of data, we evaluate the effect on compliance of various supplier and worker characteristics as well as private regulation–related variables, such as leverage and long-term buyer–supplier relations. Given that Wijen (2014: 306) emphasized both complex causes as well as uncertain effects of different factors on compliance, we hypothesize that the effect of private regulation variables could have uncertain effects in this data. We supplement our analysis through interviews with marketing managers of ZZZ, who also report considerable variation among brands with regard to the importance of long-term buyer–supplier relations.

We thus illustrate our specific arguments regarding how actor heterogeneity drives opacity via practice multiplicity, behavioral invisibility, and causal complexity, which results in the decoupling of practices and outcomes. We have chosen to examine two leading cases in which private regulation efforts are relatively well developed. If these cases also exhibit opacity, it would lend support to institutional theorists’ argument that when the means and ends are unclear, technical procedures such as auditing become “ends in themselves” (Bromley and Powell 2012: 36).

Results

Buyer Heterogeneity and Practice Multiplicity

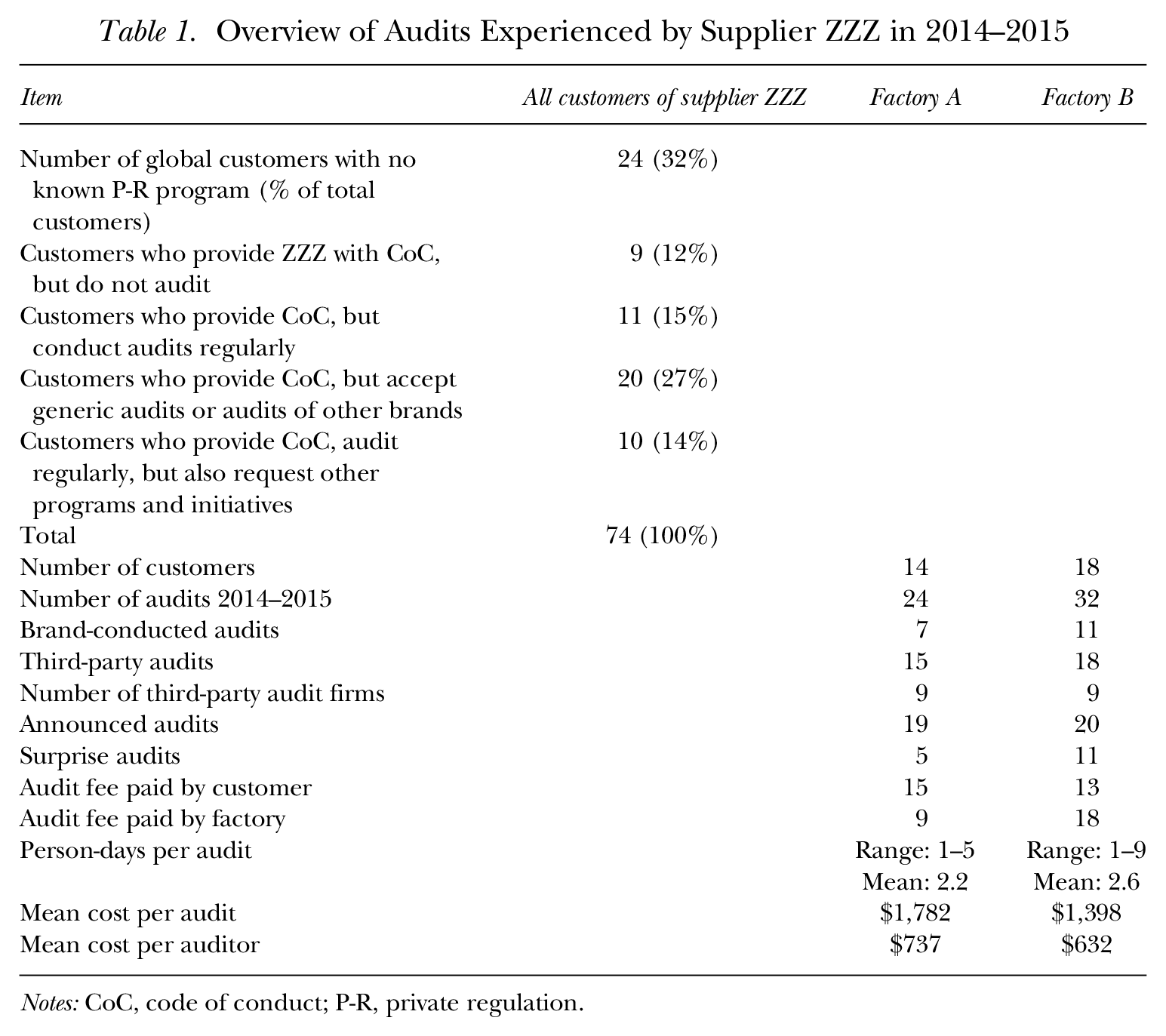

As argued, we report here the distinct ways in which buyer heterogeneity increases practice multiplicity and decoupling for suppliers. In general, considerable variation exists in how ZZZ’s customer brands have instituted their private regulation programs, and even more variation exists in how they evaluate supplier performance. Table 1 lists the variation in its customers’ private regulation approaches.

Overview of Audits Experienced by Supplier ZZZ in 2014–2015

Notes: CoC, code of conduct; P-R, private regulation.

As Table 1 suggests, although all of its customers are well-known global brands, they differ in their approach to private regulation. Of the 74 customers, eight are members of the FLA, and 17 are members of the Sustainable Apparel Coalition, and hence, leading adopters of the private regulation model. However, 24 customers did not have a private regulation program with regard to ZZZ.

The two factories of ZZZ that we examined (Factory A and Factory B), serviced 14 and 18 global brands, respectively. These factories experienced a total of 24 and 32 audits over the 2014–2015 period, roughly an audit or more every month, with more than four audits in some months. 4 Some brands audit the factories themselves, while a majority subcontract to third-party auditing firms. The majority of the audits were announced in advance, although a surprisingly large number were unannounced. In 27 out of 56 cases, the brand required the factory to pay the auditors, a serious design flaw that could result in collusion between factory management and auditing firms. Finally, the time and costs of audits varied widely, from as little as one person-day to nine person-days, while the average cost per audit varied from as little as $645 to as much as $3,700. Finally, a key way in which auditing varies across customers is the extent to which auditor’s function as “coaches who are interested in removing root causes of violations” versus those who simply “check the box” (Interview 2: ZZZ Sustainability Officer).

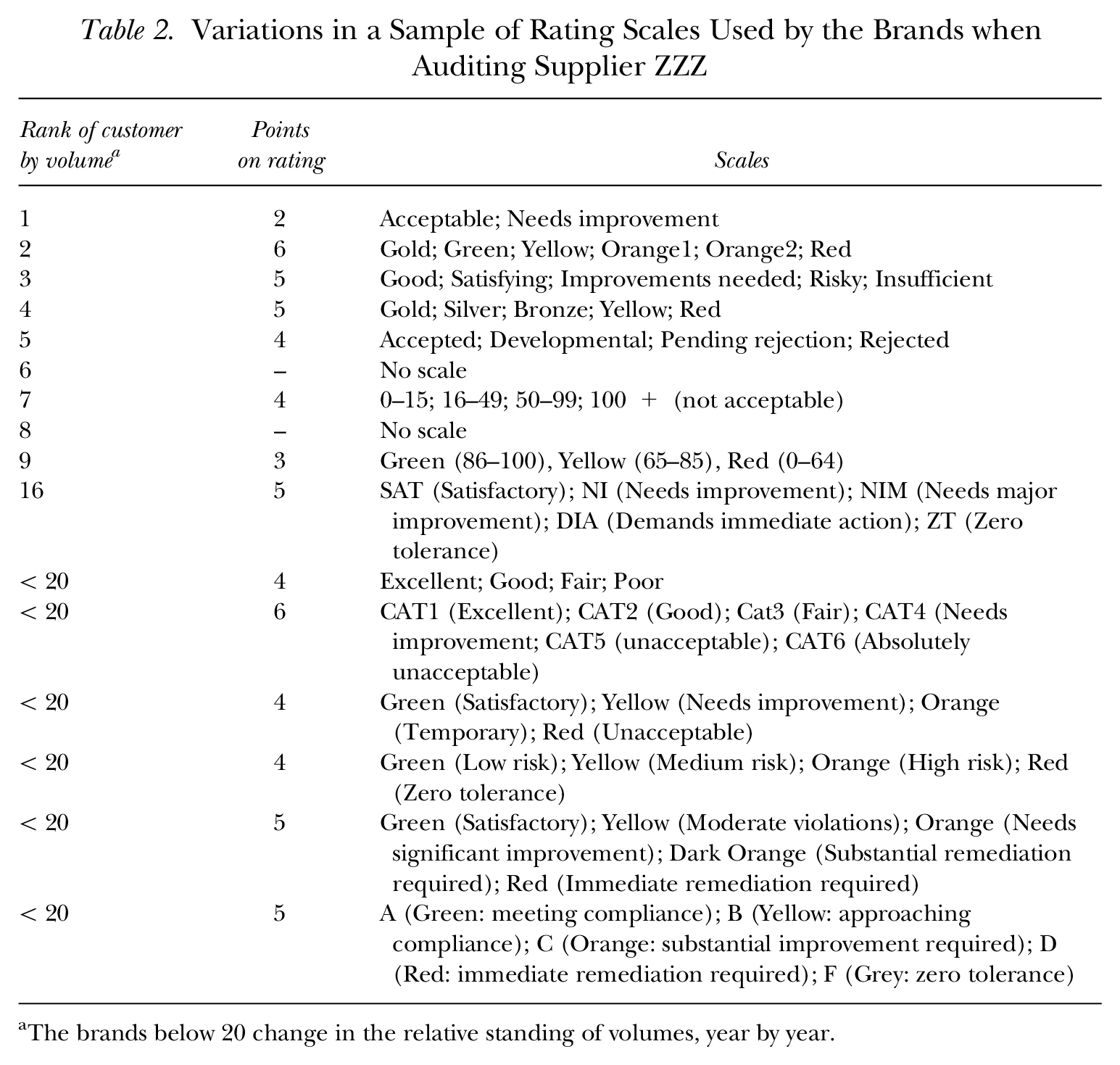

Practice multiplicity is even more apparent in the evidence of variation in how brands conduct audits. Conducting an audit requires that auditors provide an overall rating of the factory (brands require the rating so that it could potentially be factored in to their sourcing decisions). Our interviews with factory management indicated their frustration with the problems caused by the different rating scales used by different brands/auditors and by the lack of a clear connection between audit violations and the final rating. Table 2 lists the rating scales used by various brands who source from ZZZ. We have listed the rating scales used by the ZZZ’s top 9 customers (by volume) as well as others. The variation in rating scales used means that the factory might receive a rating of “acceptable” by one brand, and “unacceptable” by another brand in audits conducted during the same time frame. Further, factory CSR representatives suggested that the brands and auditors made little effort to link their rating scales to the findings of the audit. In fact, the brands shared the rationale for the ratings in only 57% of the audits.

Variations in a Sample of Rating Scales Used by the Brands when Auditing Supplier ZZZ

The brands below 20 change in the relative standing of volumes, year by year.

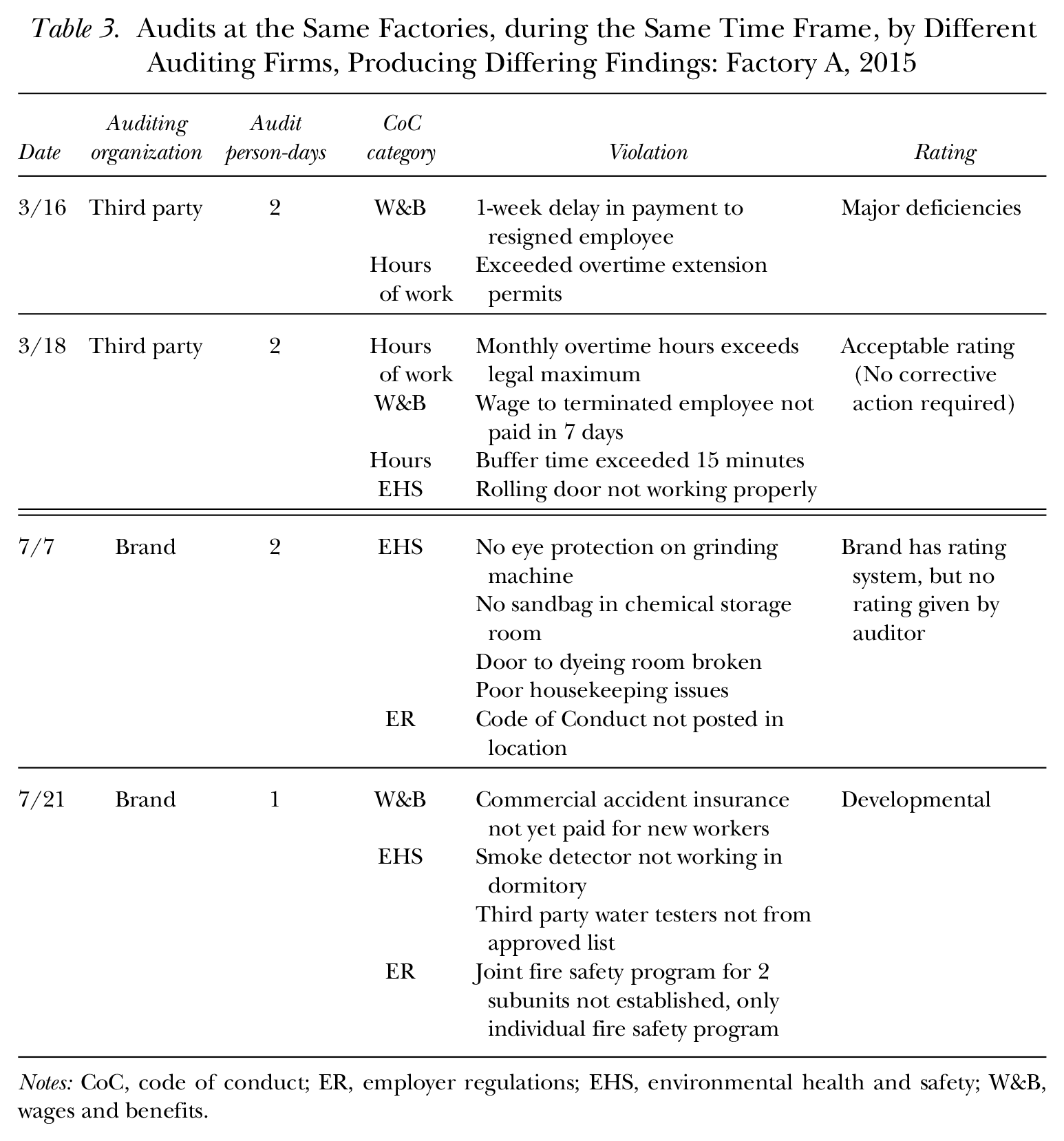

We also found variation in the practices of auditors that results in varying findings. We provide data in Tables 3 and 4 for two scenarios. In the first case, reported in Table 3, we examined audits done at Factory A during the same time frame (March 16 and 18, 2015, and July 7 and 21, 2015) by different brands/auditing firms. The number and type of findings vary significantly, as do the ratings. Note the variation in a two-day period (the top panel of Table 3) and the variation in a two-week period (the bottom panel of Table 3). In the first panel, audits conducted just two days apart show vastly different violations for conditions that do not usually change that much. This variation suggests that either auditors of different brands and audit companies are not uniformly trained or they are looking for very different things in an audit, despite the fact that brands typically use similar codes of conduct.

Audits at the Same Factories, during the Same Time Frame, by Different Auditing Firms, Producing Differing Findings: Factory A, 2015

Notes: CoC, code of conduct; ER, employer regulations; EHS, environmental health and safety; W&B, wages and benefits.

Audits by the Same Auditing Company, during the Same Time Frame, Producing Differing Results and Ratings: Factory B, 2014

Notes: CoC, code of conduct; EHS, environmental health and safety; HRS, hours; W&B, wages and benefits.

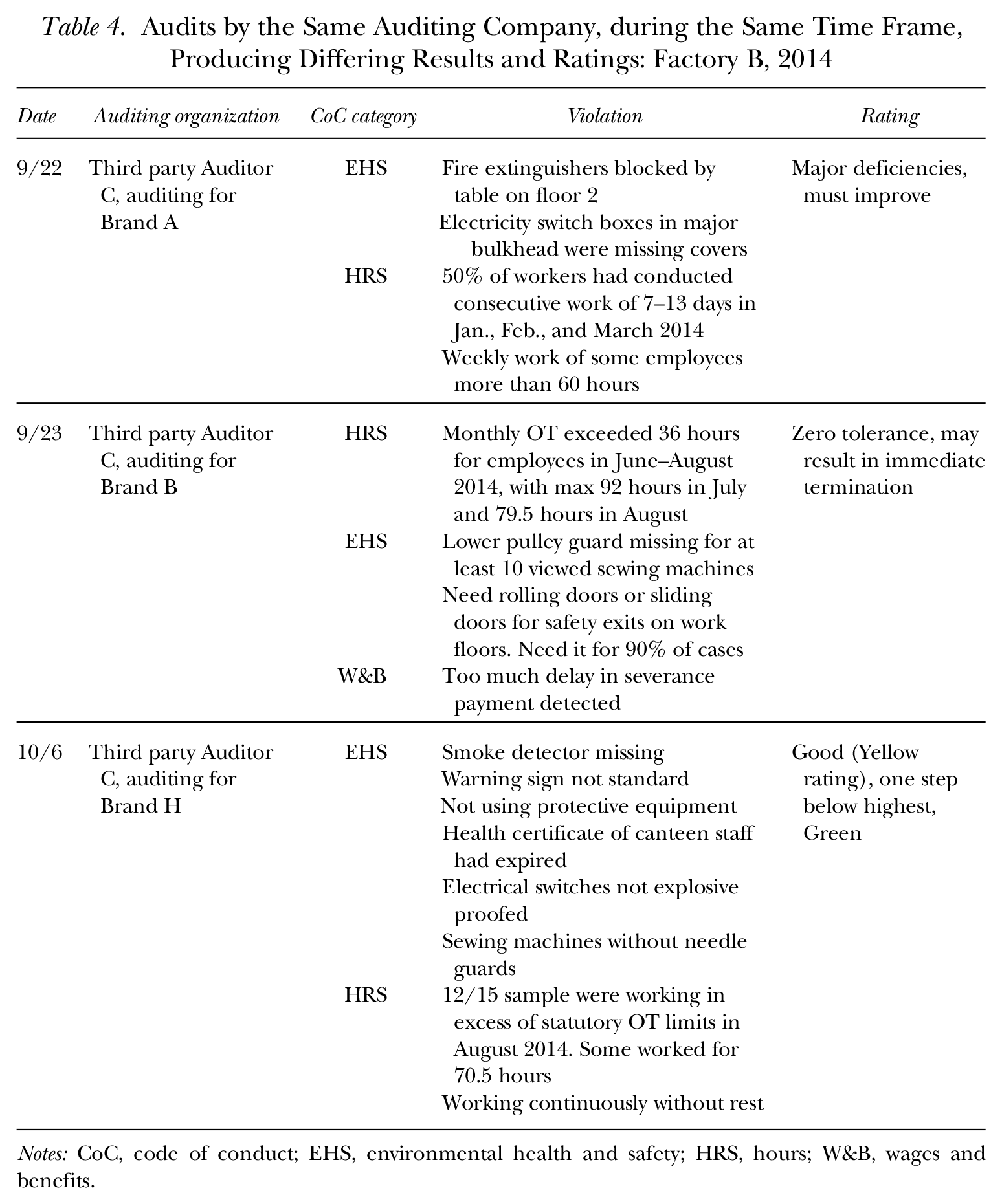

Therefore, we examined a second scenario (reported in Table 4), looking at audits in Factory B by the same auditing firm, representing three brands, during the same time frame (September 22 and 23, and October 6, 2014). We found that the same auditing firm (we do not know if the specific auditors who visited on that day were the same) found quite different violations, even one day apart. More important, those variations led to quite dissimilar compliance ratings. For example, although the auditors classified two of the ratings as “major deficiencies,” one rating was classified as “good.”

The auditors failed to provide any indication of the weight attached to each individual item (of more than 200 items in most audits) in arriving at their overall rating. It is possible that individual auditors have leeway to exercise their judgment on this issue, but it is also possible that brands give their auditors generalized guidance in arriving at these decisions. These findings suggest considerable variation in 1) what auditors look for, 2) what they actually find during their audits, and 3) how much weight they assign to each violation. Our interviews with ZZZ’s sustainability staff suggest that what auditors look for is often influenced by brand experiences at other factories or countries. For instance, following the tragic Rana Plaza fire in Bangladesh, most brands focused more on fire safety issues relative to other issues, and fire safety violations tended to be given greater weight in overall ratings in these factories during the time frame that we collected data. Similarly, one brand experienced a chemical safety issue in one of their supplier factories elsewhere, and that was reflected immediately in heightened focus on chemical issues in the auditing of this factory.

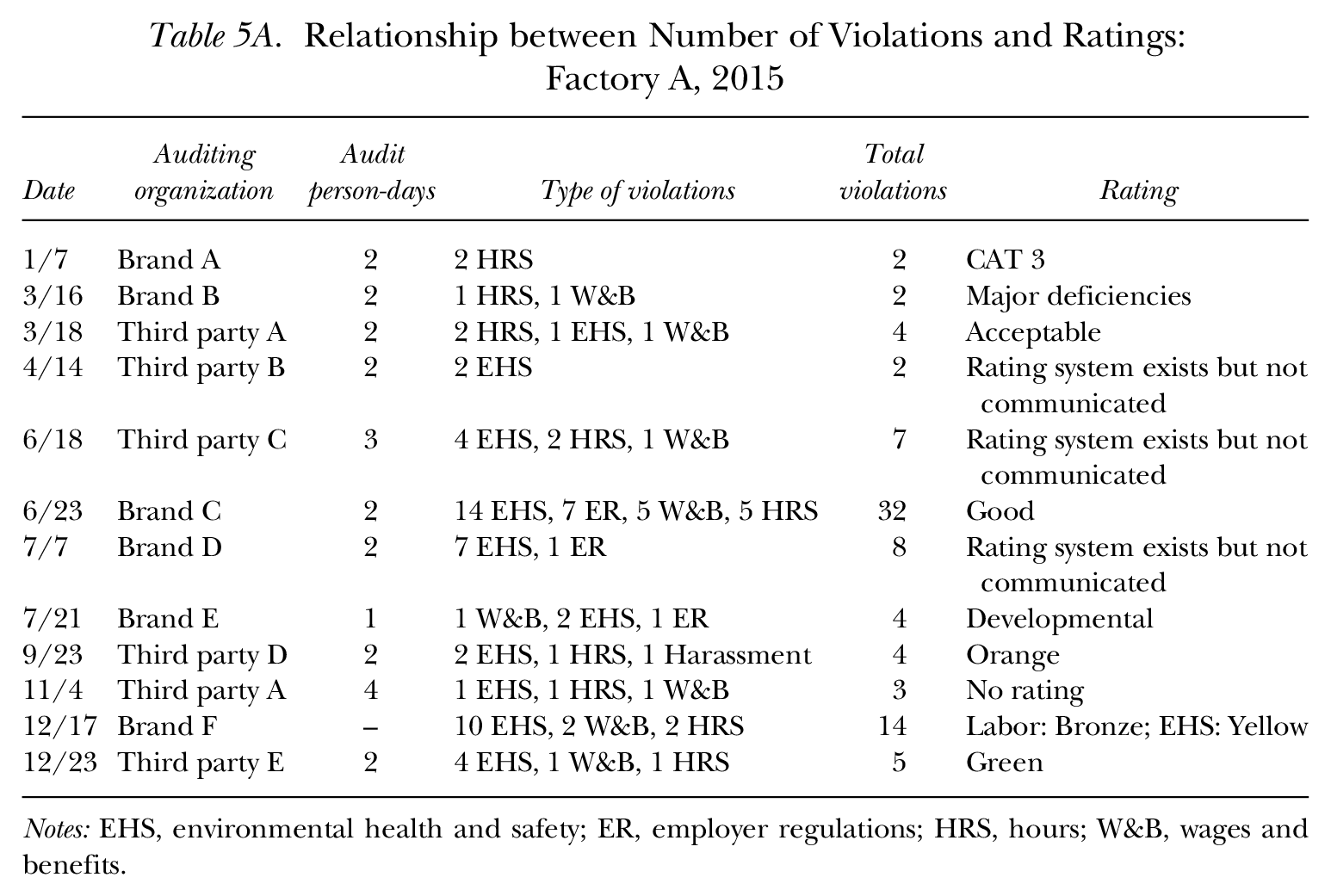

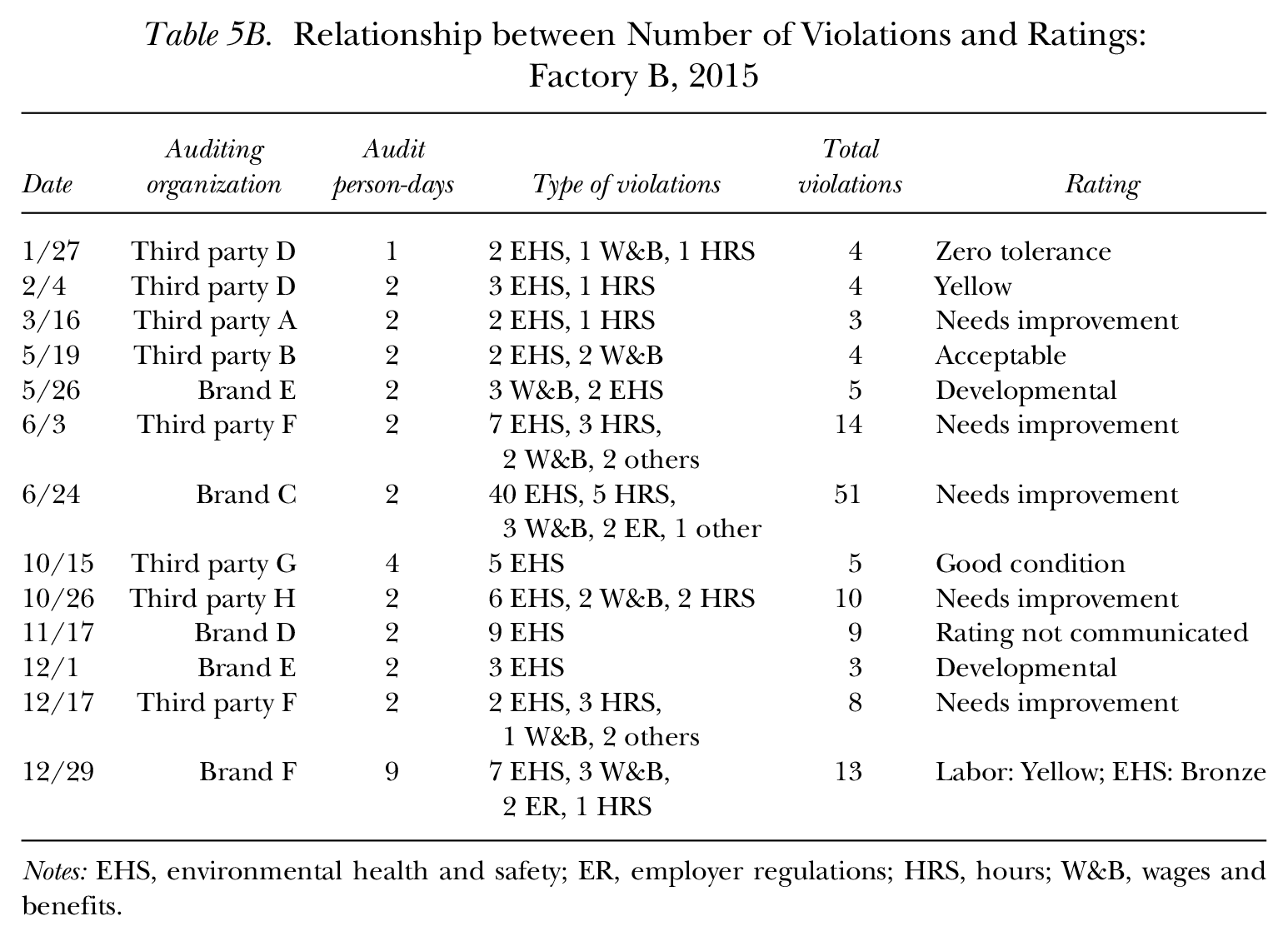

We found no relationship between the number of instances of noncompliance reported and the overall ratings provided by the auditors in the 56 audits of ZZZ. Note that the number of instances of noncompliance is less important than the severity of those issues. It was impossible to judge severity by examining the audit reports, however, given the absence of weightage information, and given that one auditor’s conception of severity might differ from that of another. Nevertheless, it is reasonable to hypothesize that the audit reports that find a higher number of instances of noncompliance would result in a lower final rating. This does not appear to be the case, however, as the data in Tables 5A and 5B suggest.

Relationship between Number of Violations and Ratings: Factory A, 2015

Notes: EHS, environmental health and safety; ER, employer regulations; HRS, hours; W&B, wages and benefits.

Relationship between Number of Violations and Ratings: Factory B, 2015

Notes: EHS, environmental health and safety; ER, employer regulations; HRS, hours; W&B, wages and benefits.

Tables 3 through 5B suggest considerable heterogeneity in the way brands practice private regulation. Auditors also vary in what they look for, and find, during the same period. The findings are not always systematically linked to the rating scales; the rating scales differ from company to company; and as discussed earlier, auditors do not communicate the rationale for the ratings given to the factory. As noted, in 43% of audits, the purpose of educating the supplier seems to be absent. As ZZZ’s chief sustainability officer noted, “Our customers fall variously into two camps. One wants to do good and is often willing to work with us, while others just follow rigid rules, with a ‘check-off mentality’ that does not address the root causes of problems.” She added that the “brands differ in terms of priorities and how much compliance is important to them” (Interview 3). An initiative by the supplier to regulate the multiplicity of audit practices by suggesting to its long-term clients that they simply accept an audit done by someone else were adopted by just two global brands (detailed later in Table 9). Thus, the multiplicity of practices among heterogeneous brands provides diverse or conflicting signals to the supplier, making it difficult, even for a leading multi-brand supplier such as ZZZ, to effectively align its work conditions with diverse brand requirements.

Supplier Heterogeneity and Behavioral Invisibility

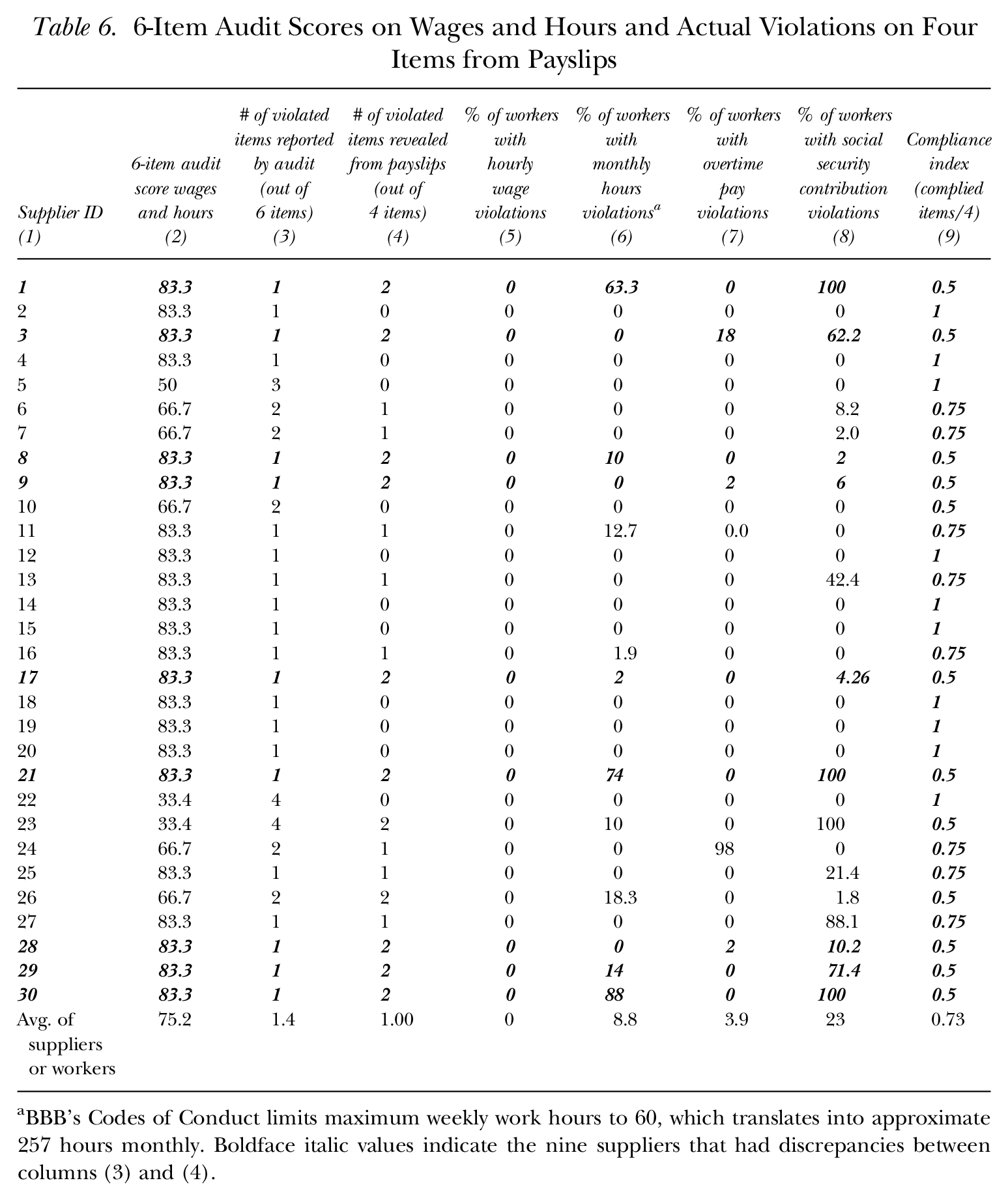

Recall that our analytical strategy was to compare BBB’s audit scores on wages and hours with the compliance scores calculated by us from workers’ payslips drawn from payroll records that the auditors assess. Although drawn from the same underlying data, our calculations of compliance take into account the effect of local regulations and employment practices, whereas we are uncertain whether BBB’s auditors do the same.

Column (3) in Table 6 shows BBB’s audit scores for the six items on wages and hours, and column (4) shows our calculation of compliance for four of these six items (hourly wage, monthly hours, overtime pay, and social security). Comparing these two columns reveals discrepancies with regard to monthly wages, overtime pay, and social security contributions. BBB’s audit scores underreport violations in nine 5 out of 30 suppliers (30%) shown in bold and italic font in this table. For instance, supplier 1 received an audit score of 83.3% with only one violation being detected by the BBB’s audit, but our calculation shows two violations (on weekly hours and social security contributions). Social security payments appear to be a particular problem, as 16 of 30 suppliers were not in compliance, and the severity of the violation on social security varies (i.e., share of workers affected by this violation ranges from 1.8% in some suppliers to 100% in others). All of the nine suppliers noted above violate social security contributions based on payslip information.

6-Item Audit Scores on Wages and Hours and Actual Violations on Four Items from Payslips

BBB’s Codes of Conduct limits maximum weekly work hours to 60, which translates into approximate 257 hours monthly. Boldface italic values indicate the nine suppliers that had discrepancies between columns (3) and (4).

Explaining instances in Table 6 in which BBB audits reveal more violations than do our computation is relatively easy because their auditors are evaluating six items relative to our four, and because our computations rely on a month’s payslip data, whereas BBB’s auditors have access to payroll data for several months. Explaining why BBB’s audit scores underreport in the four cases is more complicated because a number of factors could be relevant here.

The discrepancy noted in monthly wages is largely attributable to the fact that national rules in China require that wages and hours are reported on a monthly basis. BBB’s code, which is standardized for all countries, sets maximum standards on a weekly basis (60 hours) for the monthly wage issue (item 3). Hence, auditors must translate BBB’s weekly hours into a monthly hour standard and then compare this monthly standard to each worker’s recorded hours. Several errors could arise in this translation. First, it may underreport the violation since it is unknown whether in a specific week the 60-hour-maximum standard is followed. Second, inaccuracy can occur in terms of how to translate weekly hours into monthly hours (depending on the number of days and weeks in each month). Third, errors may arise given that auditors have to go through the records of hundreds (or thousands) of workers in a short time. The same measurement challenge arises when assessing “one day off in seven” (item 4) because suppliers maintain records of total days off in a month. It is thus impossible to tell when the days off are taken and whether item 4 is fulfilled based on payroll records.

Assessing supplier compliance with overtime pay (item 2) is more complicated in China. Chinese labor law specifies three separate rates for overtime pay (1.5 times wage for overtime on weekdays, 2 times wage for overtime on weekends, and 3 times wage for overtime on national holidays). The auditors must obtain detailed overtime records from suppliers and compute, for each worker, whether they have been paid accurately, an impossible task given the short audit duration and large number of workers.

Locational heterogeneity within China creates intra-country variations that make measurement difficult for auditors operating with a standardized code. BBB’s auditors have to check relevant regulations in each of the 19 cities (which may vary year by year) in order to measure supplier compliance with items 1 and 6. We have taken these regulations into account to compute compliance, but it is not clear that BBB’s auditors have done so, potentially accounting for the discrepancies we find with regard to these items. In the case of social security, for example, some cities allow different wage bases for calculating social security contributions, giving employers leeway to choose. Moreover, five of these cities specify social security contribution rates that differ for migrant workers versus local workers.

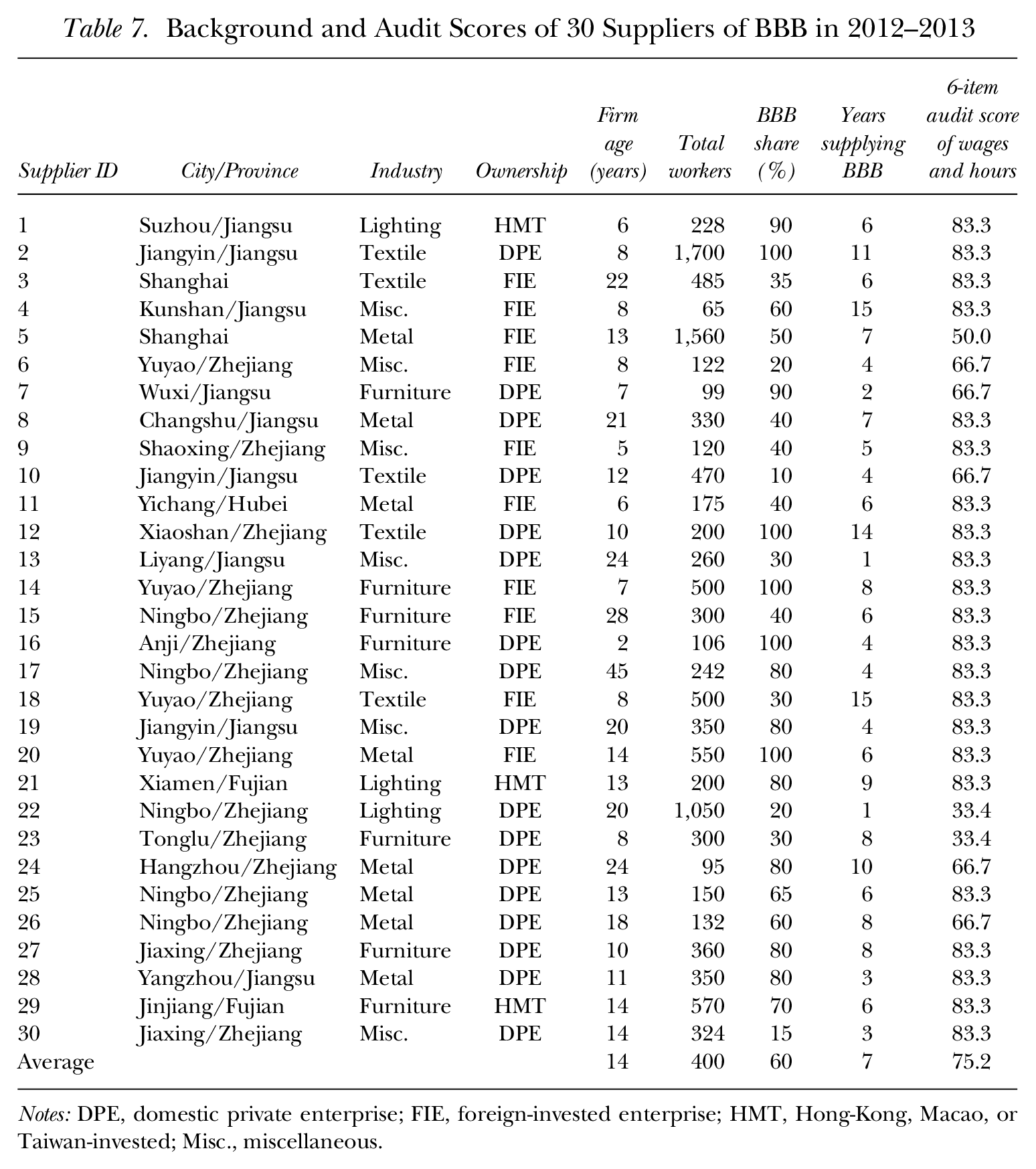

In addition, suppliers vary in terms of product type and industry. As Table 7 suggests, the 30 suppliers of BBB are in a variety of industries such as textiles, metal, and lighting, for which working environments and safety and health standards vary. First, auditors should be aware of whether workers (or a proportion of workers) need to be, and are, compensated for the industry-specific health and safety risks as mandated by local laws. Second, because legally mandated allowances must be excluded from minimum wage standards according to Chinese law, auditors must check whether suppliers comply with minimum wage standards after these allowances are deducted. Our calculations take into account these industry and firm nuances, whereas it is unclear that BBB’s auditors are aware of them. 6

Background and Audit Scores of 30 Suppliers of BBB in 2012–2013

Notes: DPE, domestic private enterprise; FIE, foreign-invested enterprise; HMT, Hong-Kong, Macao, or Taiwan-invested; Misc., miscellaneous.

Finally, employment practices of suppliers vary, complicating accurate measurement by auditors. In many industries, employers are allowed to adopt flexible work schedules or irregular-working-hours systems to adjust to fluctuating orders. Under these regimes, suppliers do not need to comply with the monthly overtime regulations for any specific month, as long as the average monthly overtime hours in a quarter or in a year meet the legal standards. Alternatively, they may be given compensatory hours off in lieu of overtime payments. Auditors, however, will look for maximum hours per week, without considering these nuances, as they are not easily apparent in payroll records. Auditors are also unlikely to be able to accurately assess the sophisticated compensation management practices many Chinese employers use to circumvent tax and labor regulations, such as including various allowances in total wages to artificially increase the wage level. 7

In sum, we suggest that measuring supplier performance on wages, hours, and social security payments can be quite complex given supplier heterogeneity with regard to location, industry, and employment practices. This complexity occurs in the context of an extremely short audit duration of two days, and the need for BBB’s auditors to measure supplier behavior on 75 distinct items, some of which take even longer to audit than wages and hours. The difficulties highlighted here concern issues that hitherto have been considered easy to measure. These difficulties have not been addressed in prior research on auditing. Such heterogeneity likely accounts for the discrepancies between audit scores and our analysis of payslip information.

Actor Heterogeneity and Causal Complexity

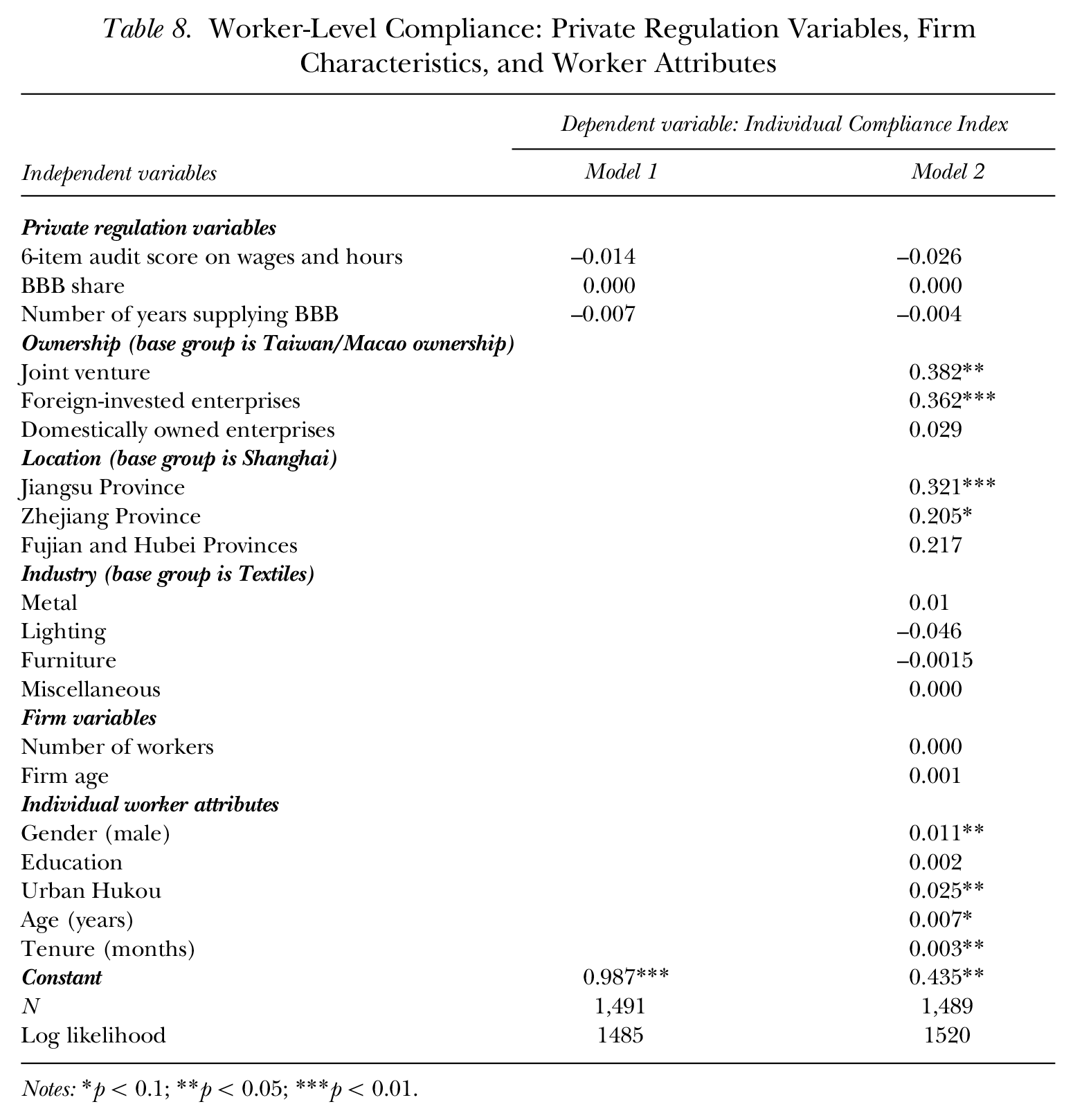

We have argued that worker outcomes are a function of many complex causes, including supplier characteristics and worker attributes as well as private regulation variables. Furthermore, these various causes may have uncertain effects in complex fields, resulting in the “effect uncertainty” or “response uncertainty” that Wijen alludes to in his conception of causal complexity (2014: 306). In our quantitative analysis, which includes appropriate controls for supplier and worker characteristics, we examine whether three private regulation variables are related to compliance: the audit scores, leverage (the percentage of supplier production accounted for by the global buyer), and the length of the relationship between buyer and various suppliers.

To measure compliance, we compute a compliance index for each worker based on their payslips from BBB. For instance, a worker would receive a compliance index score of 0.75 if he or she experienced only one violation out of four items on wages and hours. Because compliance outcomes for individual workers are nested within 30 suppliers, we use multilevel 8 linear regression to analyze antecedents of compliance outcomes for workers. Table 8 reports these results.

Worker-Level Compliance: Private Regulation Variables, Firm Characteristics, and Worker Attributes

Notes:*p < 0.1; **p < 0.05; ***p < 0.01.

Models 1 and 2 of Table 8 test the effects of private regulation–related variables: audit scores, BBB leverage (share in the supplier’s production ranging from 15–100%), and years supplying BBB (between 3 and 15 years). None of the variables are statistically significant predictors of better compliance, with or without controlling for other causes of compliance. This suggests that private regulation’s effect is uncertain, at best.

Interestingly, model 2 in Table 8 shows multiple contextual causes of compliance beyond private regulation variables. Several supplier characteristics and worker attributes are significantly associated with better compliance. These include supplier ownership (with foreign-owned or foreign-invested suppliers showing higher compliance than suppliers owned by Taiwanese or Macao companies/individuals), location (suppliers located in Jiangsu and Zhejiang exhibit higher compliance than those in Shanghai), and size (positively related to compliance). Among worker attributes, Hukou (household registration), gender (male), tenure, and age relate positively and significantly with better compliance. Compliance was generally better for workers who have an urban Hukou relative to a rural Hukou. Taken together, models 1 and 2 reveal complex causes of compliance for workers including supplier and worker heterogeneity, whereas the effects of private regulation–related variables are uncertain in this sample.

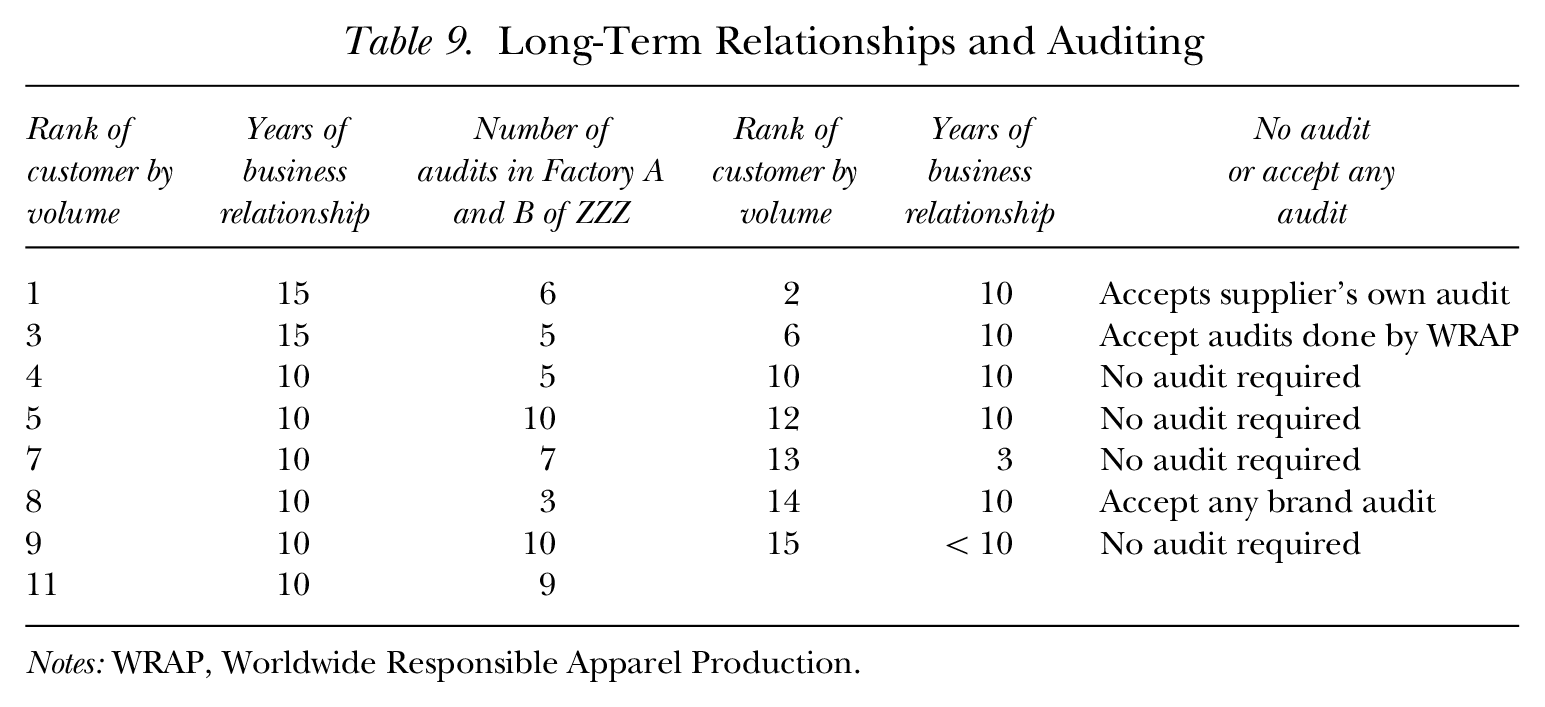

Qualitative evidence from ZZZ complements our analysis in a more indirect way. ZZZ has had long-term relationships (more than 15 years) with many of the brands. Prior research has suggested that long-term relationships result in better appreciation and knowledge of the supplier’s ability to comply with the code. An outcome of long-term, trust-based relationships is the reduced need for auditing. In the case of Factories A and B, the results are quite mixed. As Table 9 suggests, eight out of 15 brands with relationships exceeding 10 years continue to do audits regularly, whereas seven of the brands do not require an audit or are content to accept a generic audit or ZZZ’s internal audit. These heterogeneous responses from buyers make factory managers uncertain about the benefits of long-term relationships because they do not seem to know how brands make decisions to conduct or not conduct audits.

Long-Term Relationships and Auditing

Notes: WRAP, Worldwide Responsible Apparel Production.

Marketing managers of ZZZ, a leading and highly compliant supplier, suggest that their experience with auditing shows that there is little or no coupling between brands’ auditing practices and sourcing practices. Hence, the aspect of rewarding compliant suppliers with orders, a key element of the private regulation model, seems absent in this case. One marketing manager indicated that the “idea that long-term relationships will result in repeated/advance orders is ludicrous” and that customers “see themselves as free to make changes anytime.” Another noted that even long-term customers “will often defect” after placing their orders. As such, brands’ unpredictable behavior makes factory managers uncertain about what conditions help secure stable orders, without which it is difficult to continuously improve compliance and outcomes for workers. Because the link between auditing and sourcing is crucial to compliance through the incentive effects, the absence of this link in cases where leverage is high and relationships are long term (both best-case scenarios) is problematic. Taken together, these results suggest that the causes of compliance are complex, the effects of private regulation are uncertain in different contexts, and supplier factory managers are uncertain about what works—illustrating causal complexity that creates decoupling of private regulation and outcomes.

Discussion

The key contribution of this article is to demonstrate how actor heterogeneity generates field opacity through practice multiplicity, behavioral invisibility, and causal complexity in ways that result in decoupling of private regulation practices from outcomes for both brands and suppliers. In doing so, we provide support for the construction of an organizational-field-based explanation for the general lack of sustained improvements in worker outcomes in global supply chains. This field-level explanation does not mean that the critiques of individual elements of the private regulation model identified in prior literature (Locke 2013) lack explanatory power. The value of the institutional approach is that it provides a more systemic explanation for low compliance across diverse institutional contexts and company supply chains. Furthermore, it suggests several specific and general implications for the practice of private regulation, while also allowing us to evaluate contemporary developments in the field.

In specific terms, based on our evidence regarding brand heterogeneity that creates practice multiplicity for supplier ZZZ, a key element is the need for multi-brand coordination in terms of auditing approaches for factories that supply multiple brands. At present, such coordination is absent. Such a collaboration is consistent with Wijen’s (2014: 314) notion of niche institutions “tailored to specific contexts.” In this case, the context is multiple brands sourcing from the same supplier and could serve to reduce practice multiplicity. Contemporary examples of such niche institutions include the Bangladesh Accord on Fire Safety and its sibling organization, the Alliance for Bangladesh Safety, both of which involve collaboration between global brands to improve safety in Bangladesh factories. The Indonesian Freedom of Association protocol is another contemporary example of a context-specific niche institution. Our results regarding supplier and worker heterogeneity suggest that brands in the apparel or home retailing company chains could collaborate to establish regional or provincial consortia with their suppliers to devise effective frameworks for auditing with regard to wages and hours, regionally and locally.

Furthermore, such consortia of brands and their suppliers in a particular region may stimulate the suppliers to internalize the principles and goals of private regulation, another solution recommended by Wijen to decrease opacity and the trade-offs between the two forms of decoupling. At a more general level, consistent with his arguments (2014: 313), such internalization could also be stimulated by stricter selection procedures by multi-stakeholder institutions, of which global companies are members. For example, they could require their members to more closely integrate sourcing with compliance as a condition of membership, which they currently do not do.

We acknowledge, of course, that such coordination among global buyers will not solve the many other issues that cause behavioral invisibility (such as auditors’ inability to process information in the short time frame provided). The variety of difficulties involved in measuring suppliers’ performance in labor practices suggests that the labor practice field may be more opaque than the environmental field, given that information on labor practices and intended outcomes are dispersed among thousands of workers across diverse suppliers, whereas environmental effects can be much more easily observed. Wijen (2014) treated social (including labor) and environmental issues similarly in making his argument. In this sense, it is important for future research to develop specific hypotheses regarding the causes of opacity in labor practices, as we have done in this article.

Using a decoupling lens permits us to evaluate a contemporary development in labor practices in global supply chains. One effort currently underway is that of the Social and Labor Convergence Project (SLCP), a consortium of brands and large suppliers that aims to develop an audit tool and a uniform verification (auditing) methodology for the universe of global suppliers. More than 75 global companies and suppliers have signed on to this initiative, which is in the early stages of development. Wijen’s arguments regarding causal complexity suggest that such an effort, at best, might solve symbolic adoption issues, but will otherwise fail to realize its expected outcomes, given that it hews toward uniformity across multiple contexts that require a more differentiated approach, potentially constraining actor’s agency to act in context-dependent ways.

Our results regarding the importance of worker heterogeneity raise the question of how workers might be involved in private regulation. Because workers are the ones who know their work situation and working conditions better than any other actor, involving them in the auditing process, or providing them with a role in implementing codes of conduct, would help reduce opacity caused by behavioral invisibility. Indeed, recent research by Bartley and Egels-Zandén (2015) suggested that worker and union agency could shrink (though not eliminate) the gap between practices and outcomes, a process they call “contingent coupling.” Involving workers (key actors affected by private regulation who have been hitherto left out of the process) would also contribute to the generation of a systemic mindset, given Wijen’s (2014: 313) argument that collaboration among all relevant actors could accomplish this objective.

More generally, creating a systemic mindset among diverse interconnected actors also requires identifying major and minor causes and uncertain effects of important variables (Wijen 2014: 313) if we are to transform the opaque field of labor practices under private regulation to a more transparent one. One way causal complexity could be reduced is if actors such as global companies, multi-stakeholder initiatives, and auditing firms would publicly disclose the data and their analyses regarding the effects of their private regulation practices. This level of transparency does not exist in the private regulation field currently, as most brands and multi-stakeholder institutions do not publicly disclose any data. 9 Over the 25 years since private regulation was adopted, various multi-stakeholder institutions, such as the Fair Factories Clearinghouse, have amassed a large amount of data, but it is unclear how their analyses (which are private) provide evidence of the direct and indirect effects of causal variables in diverse contexts. More transparency through public disclosure is a necessary step to reduce the causal complexity that generates opacity and decoupling. In the few cases such data were made available to the research community, Locke (2013), Toffel et al. (2015), Short et al. (2017), and Amengual et al. (2019), for example, have made invaluable contributions in identifying causal relationships.

If the institutional approach used in this article has been useful in showing how actor heterogeneity generates practice multiplicity, behavioral invisibility, and causal complexity to produce the opacity that results in the practice-outcomes gap, it also has the potential to explain why global firms continue with the private regulation model despite its demonstrated ineffectiveness in the labor standards arena. For example, Bromley and Powell (2012) argued that in opaque institutional fields, when the link between means and ends is unclear, monitoring and evaluation become ends in themselves because they serve to confer legitimacy in the face of normative external pressures. Although we do not specifically test this idea, our results with regard to ZZZ show that the brands sourcing from it practice auditing as an annually recurring, low-cost, outsourced, “check the box” activity, which does not seem to be related to actual compliance and is clearly decoupled from their sourcing practices.

In sum, our article suggests that institutional theory has much to offer as a theoretical anchoring for examining private regulation in the labor standards arena. In ways that prior explanations do not, it offers an alternative and systemic field-level explanation for the practice-outcomes gap, and generates implications for how private regulation can be improved in the future.

Conclusion

Private regulation of labor standards in global supply chains has been increasingly adopted in diverse industries since the 1990s. However, scholarly evidence suggests that the private regulation model has not generated sustainable improvements in working conditions in the global supply chain, evidenced by a continuing gap between the practices adopted and the expected outcomes. Violations of labor standards continue to be quite common. One explanation for the lack of sustained improvement rests on the idea that organizations “symbolically adopt” private regulation practices, while other explanations point to flaws in the individual elements of private regulation or organizational failures in implementation.

Using new arguments from institutional theory regarding field opacity and decoupling, and data from a global apparel supplier and a home products retailer, we demonstrate how actor heterogeneity creates field opacity in ways that result in decoupling in private regulation regarding labor standards. Specifically, we argue and show that brand heterogeneity in terms of different auditing practices, rating scales, and conflicting ratings causes practice multiplicity that results in opacity for the supplier. We also highlight that supplier heterogeneity in locations and employment practices creates measurement challenges for brands to even accurately assess wages and hours that were considered easy to measure (behavioral invisibility), resulting in gaps between brand audit scores and worker payslip data. Finally, we argue and show that the complex configuration of actors in private regulation contributes to causal complexity, such that it is difficult to attribute worker outcomes to private regulation practices in some contexts, and that characteristics of local actors also affect worker outcomes. In so doing, we develop the building blocks of a plausible alternate organizational-field-level explanation for the lack of sustainable progress in labor standards in global supply chains.

Although our analysis is limited in many ways, particularly given that our qualitative examination spans only two supplier factories and our quantitative analysis compares audit scores to workers’ payslips in only one month for a small sample of suppliers, we are able to demonstrate the potential of an institutional theory lens to understand progress in private regulation of labor standards. Future research may move beyond our efforts and study additional pathways through which field opacity is generated, and examine how contextualized brand-supplier collaboration efforts can reduce opacity and decoupling to improve labor standards.

Footnotes

Appendix

Sarosh Kuruvilla acknowledges the helpful comments of Matt Amengual, Greg Distelhorst, Duanyi Yang, Matt Fischer-Daly, and Anna Burger, as well as participants of workshops conducted at MIT, Kings College, the International Labour Organization, and Cardiff University. This research is partly supported by the New Conversations Project: Sustainable Labor Practices in the Global Economy, Cornell University. Mingwei Liu acknowledges partial research support for this project by the Major Research Program of Chinese National Philosophy and Social Science Foundation titled Research on China’s Participation in Enacting New Rules on International Labor Standards (Project No. 19ZDA136), the National Social Science Foundation of China (Project No. 17BGL106), and a Rutgers Global collaborative research grant. Chunyun Li acknowledges support from the Natural Science Foundation of Guangdong Province (Project 2016A030310343).

For further details about the data and interviews used in this article, please contact either Chunyun Li at

1

Hence the use of the term compliance. A fundamental assumption is that better compliance leads to better outcomes for workers.

2

These details are available from the authors.

3

BBB allowed one year for existing non-confirming suppliers to meet this bottom-line compliance level.

4

This is broadly consistent with the frequent complaint of “audit fatigue” by suppliers who service multiple brands.

5

These are suppliers 1, 3, 8, 9, 17, 21, 28, 29, and 30.

6

Given this discrepancy, we acknowledge that our own assessment of compliance with overtime hours and compensation based on information from payslips cannot be accurate for all suppliers.

7

This is a common practice. Chinese law provides that allowances for commuting, meals, and dormitory should be excluded from minimum wage standards, whereas allowances for skills, seniority, and cell phone plans must be included. However, these allowances are not differentiated and indicated in payroll records, making it impossible to assess compliance accurately.

8

Multilevel modeling is designed to test relationships between features at higher and lower levels of analysis (![]() ) and is especially appropriate for nested data in which observations are not independent from each other, violating the assumption of ordinary least squares (OLS) regression. In our data set, the auditing process and employment conditions of workers in one supplier may systematically differ from those in another supplier. Given the potential supplier nesting effect (supplier-level variables may influence individual-level outcomes), it is important to use a multilevel model to more accurately test the relationships we are studying.

) and is especially appropriate for nested data in which observations are not independent from each other, violating the assumption of ordinary least squares (OLS) regression. In our data set, the auditing process and employment conditions of workers in one supplier may systematically differ from those in another supplier. Given the potential supplier nesting effect (supplier-level variables may influence individual-level outcomes), it is important to use a multilevel model to more accurately test the relationships we are studying.

9

The FLA does disclose a percentage of their audit results.