Abstract

The present research analyzes national corporate interlock networks and their causal conditions. The objective is two-fold: 1) to specify types of corporate networks, and 2) to pinpoint the causal configurations that give rise to each type of corporate network. First, corporate networks on basis of interlocking directorates are analyzed and compared using social network analysis to empirically derive a typology. The results show two types of corporate networks: cohesive corporate networks which are based on unification, centralization and strength ties; and dispersed corporate networks which are characterized by fragmentation, decentralization and single ties. Second, combinations of causal conditions that explain the emergence of each type of corporate networks are identified using fuzzy set qualitative comparative analysis (fsQCA). Finally, avenues of research on corporate interlock networks are suggested.

Keywords

Introduction

How corporate interlock networks vary across the world and the causes of this variation are challenging questions that call for comparative research on the national networks of interlocking directorates. However, for such a comparative analysis to be fruitful, two challenges must be met: methodologically, working out ways to compare corporate networks; and conceptually, determining how best to identify the causal conditions that generate different corporate networks. This article addresses these challenges by applying fuzzy set qualitative comparative analysis (fsQCA) to pinpoint the causes that give rise to the different types of corporate interlock networks across 12 countries.

Although there are a variety of interpretations as to exactly what networks of interlocking directorates represent – arenas of power (Scott, 1991a), relational strategies of the upper class (Zeitlin, 1974), structures connecting powerful actors (Domhoff, 1967; Hunter, 1953), or business communities (Useem, 1984) – corporate networks analysis is more relevant at the macro-level rather than on the level of individual firms. By examining the corporate network as a whole, researchers can explore questions such as how networks develop, how inter-organizational ties are managed, and ultimately whether the ties between economic elites are cohesive or dispersed. Social network analysis allows us to study and visualize inter-corporate patterns and analyze the characteristics of these whole structures in our attempt to identify varieties of corporate networks across the world.

National corporate network analyses are undertaken around the world, especially in the USA and West Europe. Asian studies are burgeoning (Peng et al., 2001; Ren et al., 2009) and research on Latin American networks is emerging (Paredes, 2011; Santos et al., 2009; Vidal and Wendes-Da-Silva, 2010). However, comparisons of corporate networks in different countries are limited. The most significant comparative studies are those of Stokman et al. (1985), Windolf (2002) and Kogut (2012). The ‘Research Group of Intercorporate Structure’ set up by Stokman et al. (1985), analyzed the interlock network of the 250 largest companies in nine European countries and the United States. A large study was also carried out by Windolf (2002), who compared the corporate networks of six European and North American countries using data from the 1990s. Kogut (2012) and his colleagues analyzed board and ownership networks between 1990 and 2002 across the world, and showed the heterogeneity of national corporate networks. 1

While these comparative studies are praiseworthy, a general typology of corporate networks that would allow researchers to understand and catalogue individual cases is still lacking. A typology is also essential in providing an empirical basis for future theoretical and empirical research, laying the groundwork for studying the causal conditions giving rise to corporate networks, and the network impacts on political, economic and social spheres. For these reasons, there is a need for a systematic comparative analysis of corporate networks on a worldwide basis.

Similarly, research on the causes of network patterns is rare, despite the widespread attention to interlocking directorates in studies in the area of resource dependence theory (Hillman and Dalziel, 2003; Pfeffer, 1972), institutionalism (Haunschild, 1993; Palmer et al., 1993), elite theories (Domhoff, 1975; Useem, 1984) and management (Pettigrew, 1992; Zajac, 1988). The few studies that do address causes analyze the reconstitution of interlocks broken by the death or retirement of shared directors (Ornstein, 1984; Palmer et al., 1986). The rapid reconstruction of interlocks in such cases suggests that they serve as vehicles of intercorporate communication and control. When interlocks are not reconstituted, it suggests that they are mechanisms of class cohesion and coordination. Nevertheless, these investigations have focused on studying the factors leading to the formation of individual interlocks (at the dyadic level), rather than on the configuration or shape of the network as a whole (at the macro-level).

While numerous studies of corporate networks have focused on describing the shape, few have looked at causal conditions. The only two cross-national studies that address the factors which give rise to corporate networks are those of Windolf (2002) and Aguilera (2008). Windolf explains differences and similarities in corporate networks through an institutional contingency model, and states that the institutional environment (antitrust laws or policies to promote cartels) influences corporate networks. Aguilera (2008) compares the cases of Spain and Italy in the 1970s and 1990s, and highlights the importance of ‘historical legacy and the role of the state’. While both these authors provide causal models, research using fuzzy set qualitative comparative analysis (fsQCA) provides more reliable and compelling empirical evidence on the factors which lead to the configuration of corporate networks.

This article aims to demonstrate how the different forms of institutional embeddedness among large corporations influence the formation of different corporate networks. The type of corporate network can derive from the embeddedness of large corporations in the financial, political, ownership and international institutional structures. This analysis utilizes fuzzy set approach and qualitative comparative analysis (fsQCA) (Ragin, 2000, 2008a) to explore the institutional conditions (causal conditions) which lead to particular types of corporate networks (outcomes). FsQCA permits holistic comparisons of cases as configurations and provides a means to portray their patterns of similarities and variations. In fsQCA, variables are treated as fuzzy sets (values range from 1 to 0), and cases are viewed as members of multiple sets (configurations of attributes). By comparing configurations, it is possible to identify the causal conditions which give rise to the corporate networks, and also find out how these different factors fit together to generate the outcome (corporate network). Corporate interlock networks can be affected by multiple and interdependent factors, and one of the key advantages of fsQCA is that it allows for conjunctural causation, meaning that a combination of conditions produce the outcome. FsQCA employs a set-theoretic approach in examining cause-effect relationships, that is, institutional configurations that lead to corporate networks (Ragin 2008a; Fiss, 2007).

The identification of types of corporate networks and the study of causal conditions using fsQCA are, relatively speaking, methodological novelties in sociology and social network research. FsQCA applied to a comparative analysis of national networks helps us understand the interaction and combination of causes that might affect the networks. Linear and logistic regression analyses have been applied in analyzing the causes and effects of network patterns (Cantner and Graf, 2006; Mizruchi and Stearns, 1988; Ornstein, 1984; Palmer et al., 1986; Peng et al., 2001). However, studies involving a small number of cases are not suitable for statistical causation techniques. Moreover, complex interactions of variables cannot be tested with regression models because of too few degrees of freedom and multicollinearity (Vis, 2012). The introduction of fsQCA is a welcome innovation which will be helpful in making inferences regarding complex causation in small-N comparative studies. The use of fsQCA opens new avenues of research in studying the causes of the networks at the macro-level.

Therefore, the objective of this article is ultimately to compare corporate networks around the world to identify the conjunctural causes that produce different types of networks. This work is extremely relevant in designing networks in that it promotes the institutional settings that develop a specific type of corporate network. The research for this project is carried out in two large stages. First, I examine corporate interlock networks using standard social network analytic techniques – showing the similarities and differences among corporate networks of several countries. Using these results, I also apply multivariate techniques to propose a typology of corporate networks. At the second stage, I specify which combinations of causal conditions determine each type of corporate network using fuzzy set qualitative comparative analysis.

Case selection

The challenge to a broadly conceived comparative analysis is to move beyond contrasting Germany and USA, which can be seen as opposite ideal types (Hall and Soskice, 2001; Windolf, 2002), and to conduct a larger analysis of several countries and to capture the most variation (Griffin et al., 1991). I choose the most similar and the most different cases taking into account the literature on varieties of capitalism. Although in the past the varieties of capitalism approach was criticized for providing anecdotal evidence in demonstrating differences between economies, more recent empirical studies mapped the different nation-based institutional configurations of capitalism across time (Amable, 2005; Casey, 2009; Geffen and Kenyon, 2005; Hall and Gingerich, 2009). Furthermore, the varieties of capitalism approach also informs this research as to the relevant variables or causal conditions that may affect the corporate networks.

This approach is also useful in its rejection of a uniform view of capitalism and arguing that economies face common challenges, but develop different institutional arrangements in attempting to solve them (Hall and Soskice, 2001). National systems are conceptualized in terms of interdependent institutional configurations and they are distinguished by their underlying logics, developed to resolve problems of market coordination (Amable, 2005; Schneider, 2008). In coordinated market economies, firms coordinate their activities via non-market relationships (Hall and Soskice, 2001), and analysts have further distinguished three subtypes: 1) the Rhenish managed capitalism variant typical of Central European economies where market arrangements are consensus-oriented by stakeholders, 2) state capitalism, in which the state directly intervenes in the economy, and 3) Asian capitalism, where firms depend on business groups to coordinate their endeavors (Amable 2005; Moerland, 1995). In liberal market capitalism – characteristic of Anglo-Saxon economies – coordination problems are solved by competitive market arrangements. For each underlying logic or type of capitalism I select paradigmatic and similar cases.

From liberal market economies I select the USA and the analogous cases of United Kingdom, Canada, and Australia; from Rhenish managed-capitalism I include Germany as a paradigmatic case and the similar cases of Switzerland and Netherlands; from state capitalism the study incorporates France, Italy, Spain, and Sweden; and I also select Japan to cover Asian capitalism based on business groups. 2 Thus, the comparative analysis includes 12 countries: USA, United Kingdom, Canada, Australia, France, Italy, Spain, Sweden, Germany, Netherlands, Switzerland, and Japan. This study therefore permits an interpretation of findings beyond particular nations because the comparisons are grounded in the different institutional arrangements and networks of interlocking directorates within nations.

To construct the corporate networks, the 50 largest corporations are selected on the basis of annual income 3 in 2005 for each country. 4 The database records the individual members of board of directors, with which I construct two-mode matrices, where corporations are in columns and directors in rows. Since this study is concerned with the networks of interlocking directorates, those directors who sit on two or more boards are retained and the rest are omitted from the analyses. The two-mode matrix is transformed into a one-mode matrix where corporations are placed in columns and rows and the values in the affiliation matrices indicate the absence (0), presence (1), or strength of the relation (above 1) between corporations. Corporate networks are visualized and analyzed with UCINET 6 (Borgatti et al., 2002). Nodes represent the corporations and lines portray the shared directors; tie strength indicates more than two shared directors (multiple interlocks).

Stage one: Typology of corporate networks

Analysis of corporate networks

Four attributes are analyzed to characterize and systematically describe the corporate networks –connectivity, compactness, centralization and multiplicity – which were developed by social network analysis as key indicators of social structure (Rodríguez, 2005; Scott, 1991b; Wasserman and Faust, 1994). Each of these attributes is evaluated using macro-level indicators of the network. In order to know if the network attributes were dependent on the size of corporate sector, I checked for this confounding variable by correlating network indicators with the number of largest corporations in each country. 5 Since no substantive nor significant associations were found – the largest coefficient was 0.389 (Sig. 0.211) and the correlation average was 0.282 – these results indicate that network patterns and shape are not a matter of the size of the corporate sector. This suggests there may be institutional conditions that underline the variety of corporate networks.

Connectivity is measured by network density, the ratio of existing ties over the total possible number of ties. High connectivity or density indicates greater integration and might be associated with opportunities for collective action, coordination and articulation of interests. Compactness, namely distance-based cohesion, is the probability of complete cohesiveness at one-step based on the shortest paths between any two pair of nodes. Compact networks suggest easier communication since actors are linked through a shorter sequence of ties. Both measures of connectivity and compactness range from 1 to 0, larger values indicate greater cohesiveness (Scott, 1991b; Wasserman and Faust, 1994).

Centralization (or global centrality) reflects the extent to which a network is organized around a focal point (Freeman, 1978/1979), and is measured by the indicator of normalized degree centralization which varies from 1 to 0, and it achieves its maximum score in star-networks. However, a network with high degree centralization can have either a few connected nodes with many ties or few nodes with many ties but not connected between them. To address this ambiguity, I also employ the indicator of reachability of the actor with the highest degree, which measures the percentage of reachable actors at one-step by the most central actor. This indicator gives us insight into the ‘real’ control of the network’s core. High centralization indicates a situation in which the connections are monopolized by a few actors, and the cohesion of the network is therefore based on a few very central actors. Low centralization suggests less dependence, more flexibility, and larger participation of a greater number of actors in the communication flows.

Multiplicity is the ratio of relations that converge on the same tie and denotes the strength of ties. A corporate interlock can be single (a shared director joins two corporations) or multiple (the two corporations are joined by two or more directors). Multiplicity is measured through the percentage of the total multiple relations. The proportion of multiple interlocks is calculated by dividing the number of ties (degree sum) based on a dichotomized matrix with the amount of ties (degree sum) based on a valued matrix. The result is the proportion of single interlocks, taking the inverse I obtain the proportion of multiple interlocks. In multiple interlocks, the information between corporations is redundant, thus Windolf (2002) suggests that multiple interlocks between two firms give members of one the opportunity to monitor, influence and master the corporate decisions and strategies of the other firm. Krackhardt (1992) states strong ties provide mutual support and trust, and can be interpreted as consequences of resource dependency or value contagion (Watts, 2004). Although I elected to ignore the direction of the control or dependency, a high percentage of multiple interlocks (multiplicity) specifies robustness, trust relations, aims of control, and also larger cohesiveness.

The identification of types

Given that the five network indicators are highly interdependent (Cronbach’s alpha = 0.87), factor analysis is performed for developing an empirical typology and creating a scale. Only one underlying factor is identified along which the cases vary (eigenvalue above 1). 6 Factor scores are constructed using regression to rank and classify cases on an index scale. The factor scores ranges from -1.37 (UK) to 1.63 (Italy) and are shown in Table 1: scores below 0 indicates corporate networks with low density, compactness, centralization and multiplicity (UK, Japan, USA, Switzerland, Australia, Netherlands, and Sweden); and above 0 denotes corporate networks with high density, compactness, centralization and multiplicity (Italy, France, Germany, Spain, and Canada). In order to assess the robustness of the index, I also conducted cluster analysis at two-steps, and two groups were identified with the same membership of cases.

Social network indicators

The two types of corporate networks

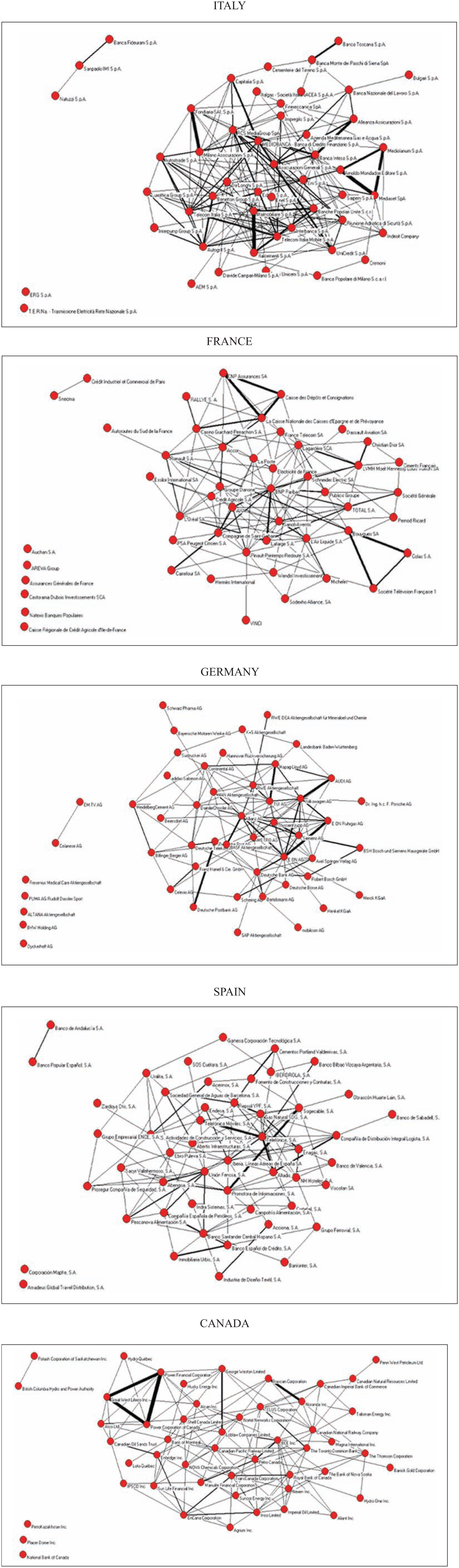

The factor and cluster analyses show the existence of two types of corporate networks. The first type grouped networks with high density (high number of corporate interlocks) which can encourage unification of perspectives and coordination of strategies, high compactness (short distances among actors), which suggest opportunities for cooperation, high centralization which indicates the likelihood of monopolization and dependence on a select group of actors, whose relational capabilities make them the core, and high multiplicity that might promote control relations and strengthen alliances. I label this type of corporate network ‘cohesive’ to underscore the view that the power structure is based on unity, concentration and control. Within this type are included the corporate networks of Italy, France, Germany, Spain and Canada (see Figure 1).

Cohesive corporate networks.

The second type grouped networks with low density, individual activity prevails over collective action, and low compactness – that is, longer distances among corporations. These networks are not centralized. Within the corporate network there are different cores and focal points which suggest fragmentation and absence of monopolization. The proportion of multiple relations is low, so corporate ties are not redundant, suggesting communication ties rather than control. I label this type of corporate network ‘dispersed’ in order to highlight the characteristics of fragmentation, decentralization, and single ties (Figure 2).

Dispersed corporate networks.

Stage two: The causal conditions

After identifying the varieties of corporate networks, the next analytical stage is intended to specify which causal conditions explain the differences and similarities between the corporate networks of various countries.

Institutional configurations determine corporate networks

Corporations are simultaneously embedded in various networks and institutions (Granovetter, 1992; Halinen and Törnroos, 1998; Rooks et al., 2000). First-order embeddedness involves corporate interlock networks. Second-order embeddedness concerns the participation of corporations in financial, political and international institutional structures. By institutions I mean the regulative, normative and cognitive structures that constrain and stimulate behavior (Scott, 2008). In this section, I show the extent to which the corporate networks are influenced by their institutional environment – namely, the variations in fundraising patterns, state intervention, ownership structures and economic internationalization.

The first institutional arrangement to be considered is the financial structure and refers to the fundraising patterns of corporations. Depending on the source and intermediation of financial capital, an economy is based on banks or on capital markets. This dichotomy is commonly accepted in the literature of financial systems (Deeg, 1999; Demirgüç-Kunt and Levine, 2004; Prowse, 1996; Rajan and Zingales, 2001; World Bank, 2001). In bank-based structures, the bulk of financial assets and liabilities consist of bank deposits and direct loans. In market-based financial systems, securities that are tradable in financial markets are the dominant form of financial assets (Vitols, 2001). In bank-based financial structures stock markets tend to be smaller and less liquid, and bank loans account for a greater proportion of company liabilities (Vitols, 2005).

Within bank-based financial structures, banks play a leading role in allocating capital and monitoring investments, and interlocking directorates become a vehicle to control and influence corporations. The interlocks reduce transaction costs and strengthen confidence between the actors involved. As a consequence, the corporate network should be denser, more compact, centralized on banks, and with a higher proportion of control interlocks (high multiplicity), that is, it will be cohesive.

Bank-based financial structures → Cohesive corporate network

In contrast, market-finance arrangements which focus on the purchase and sale of tradable securities are arm’s length transactions and should result in less direct involvement in corporate governance (Chakraborty and Ray, 2006). Market credentials and reputation are more important than control ties. In economies with market-based financial systems, legislation protects investments (La Porta et al., 1998). For this reason, overseeing corporations are not as necessary. The main space of interaction is the market, not the board of directors. The corporate network in market-based economies will have fewer interlocks (low density), low centralization and few control relations (low multiplicity), that is, it will be dispersed.

Market-based financial structures → Dispersed corporate network

Corporate networks are also embedded within political institutions. States provide a framework of regulations and rules within which corporations interact with each other. States can reproduce or shift patterns of directorship interlocks through facilitating or disrupting activities. Fligstein distinguishes between interventionist states, which are directly involved in the corporate sector – that is, own firms, enact protectionist laws, intercede in hostile takeovers, and promote national holdings, for example, France – and regulatory states which ‘create agencies to strengthen overall standards in the market, but do not decide who can own what and how investments proceed’, for example, United States (1996: 661).

Fligstein (1996) argues that an interventionist state, encouraged by the corporations themselves, promotes coordination and cooperation among firms to reduce competition and stabilize markets for the largest firms. Therefore, the interventionist state tends to promote compact and centralized corporate networks to more easily control the corporate sector. Since interlocking directorates are mechanisms to coordinate the corporate sector, interventionist states contribute to cohesive corporate networks.

Interventionist state → Cohesive corporate network

Regulatory states regulate at arm’s length and govern the economy to uphold market competition. The corporate interlocks are constrained by such political institutions as antitrust laws, restrictions on corporate control by large shareholders, and high tax burden on large stocks. In regulatory states, the corporate network will have low levels of connectivity, compactness, centralization and multiplicity and will approach the dispersed type.

Regulatory state → Dispersed corporate network

The third set of institutional arrangements is ownership embeddedness – that is, the pattern of relations between the corporation and their shareholders. According to Fligstein and Brantley, these arrangements are ‘likely to be a more important cause of actions of firms than anything else’ (1992: 303). This question – who controls large corporations, shareholders or managers? – has been a topic of debate ever since Berle and Means (1932) promulgated the ‘managerial revolution’ view pointing to the separation of ownership and control within firms. When corporations are held by large shareholders (blockholders), they are active in running the corporations. However, when firms have a large number of minority shareholders, managers run corporations. The different patterns of ownership give rise to different incentives to create interlocking networks. Shareholders with a large stake in the corporation have the opportunity to control board of directors’ decisions and positions. Because of the diversification of investment portfolios, blockholders create interlocks among their owned companies. A higher proportion of firms with blockholders in the nation will foster connectivity, centralization and control interlocks (high multiplicity), that is, it will encourage cohesive corporate networks.

Corporations with blockholders → Cohesive corporate network

Minority shareholders on the other hand – despite the diversification of ownership – cannot link their properties. Owners are not able to control corporate board of directors and cannot assume direct executive positions. For this reason, in economies with high percentage of widely held corporations, the corporate network will be fragmented, and interlocks will serve as the managers’ mechanisms of communication rather than control (low multiplicity), that is, it will result in a dispersed corporate network.

Widely held corporations → Dispersed corporate network

The international economic structure, that is, the international relations of the corporations with foreign investors, can also affect the national corporate networks. Researchers of corporate networks attribute to economic internationalization a range of effects, from a dismantling of national corporate networks (Höpner and Krempel, 2003; Windolf, 2002), to a redefinition (Barnes and Ritter, 2001; Heemskerk, 2007; Rodríguez, 2003). These investigations indicate that the increased internationalization changes national networks, but they neither empirically measure foreign investments, nor specify if this change is homogeneous in the all national economies. Therefore, the question emerges as to how cohesive and dispersed corporate networks deal with the inflow and outflow of foreign capital.

Stark and Vedres (2006) analyze the evolution of the Hungarian network of interorganizational ownership ties in relation to foreign direct investment (FDI). They observed that foreign-owned firms participate in the domestic ownership network in Hungary and that increasing FDI does not involve a separation of networked domestic firms and isolated foreign companies. In other words, economies are not necessarily forced to choose between networks of global reach and those of local embeddedness. Nevertheless, one can expect that in developed economies high internationalization will involve a reduction of national interlocks and a decline of multiplicity since national elites want to emancipate themselves from national state control and local embeddedness. Economies with high economic internationalization will promote dispersed corporate networks.

High economic internationalization → Dispersed corporate network

On the other hand, domestic-based economies – low economic internationalization – will tend to strengthen social cohesion and control in order to close and protect national market.

Low economic internationalization → Cohesive corporate network

Fuzzy set qualitative comparative analysis (fsQCA)

As noted above, this research seeks to understand which configurations of causal factors actively play a role in the formation of cohesive or dispersed corporate networks. In order to do so, I employ fuzzy set qualitative comparative analysis (fsQCA). FsQCA is chosen as the analytical tool to study the conjunctural causes of corporate networks because it offers five important advantages. Statistically, fsQCA first overcomes the limitations of regression analysis that assumes linear causation and typically requires large N samples. Second, it moves beyond anecdotal evidence to empirically assess cause–effect relationships. Third, by creating fuzzy sets (scales from 1 to 0) researchers can measure the degree of existence or nonexistence of a practice, and thereby reduce the complexity of phenomena. More importantly, fsQCA allows one to identify interaction between causal conditions, and fifth, it studies the possibility of multiple paths leading to the same outcome.

In fsQCA, each case is transformed into a configuration of causal conditions (independent variables) and an outcome (dependent variable), and all variables are scaled from complete development (presence) to its negation or complete underdevelopment (absence). The outcome (dependent variable) type of corporate network is labeled COHESIVE 7 and its negation is labeled DISPERSED. Similarly, each of the four causal conditions – financial structure, state intervention, ownership structure and economic internationalization – are labeled as follows. Bank-based financial structure is labeled (BANK-BASED) and its negation (bank-based) indicates the type of market-based financial structure. Interventionist state is labeled (STATE) and its negation (state) refers to the form of regulatory state. Economies where large firms are held by blockholders are labeled (BLOCKHOLDERS) and its negation (blockholders) means prevalence of widely held corporations. Finally, high economic internationalization is labeled (INTERNATIONAL) and its negation is labeled (international).

The four causal conditions and the outcome are transformed into fuzzy sets. Fuzzy sets can be seen as continuous variables that indicate scaling membership in sets. Fuzzy sets range between 1.0 and 0.0, where scores close to 1 indicate strong membership in a set (strong presence of the attribute in the case); scores close to 0 indicates more out of the set (weak presence of the attribute); 0.5 neither in nor out. Finally, scores of 1 and 0 indicate full membership (presence or complete development) and non-membership (absence or complete underdevelopment), respectively. Fuzzy membership scores, between 1 and 0 according to the degrees of development of the institutional conditions, are assigned to cases (calibration in fsQCA terminology).

To compare systematically financial structures and assign membership in the set of bank-based financial structure (BANK-BASED) I use Demirgüç-Kunt and Levine’s (2004) conglomerate index, based on measures of size, activity and efficiency of banks, non-bank intermediaries and capital markets. States are classified between interventionist (STATE) and regulatory (state) by reviewing research on political intervention 8 and measuring the percentage of state-controlled large firms (La Porta et al., 1999). To analyze ownership structure of large corporations and distinguish between countries with high percentage of firms with blockholders (BLOCKHOLDERS) or high percentage of widely held corporations, La Porta et al.’s (1999) data are employed. These researchers have identified the ultimate controlling shareholders of large corporations using a voting right measure. Economic internationalization is measured by both FDI inflow and outflow between 1995 and 2004 controlled by the size of the economy (GDP) (Christiansen and Bertrand, 2005). FDI is selected because this form of international capital flow implies a lasting interest and a long-term relationship between the foreign investor and the firm, and a substantive degree of influence by the investor on the management of the firm. Calibration of the raw data into fuzzy-set membership scores are based on theoretically and empirically grounded thresholds (full membership, cross-over point, and full non-membership), and log-odds estimations are used to transform values of scale variables into fuzzy scores (Ragin, 2008a). This information is summarized in a data matrix of fuzzy membership scores (Table 2) and detailed in the Appendix 1.

Fuzzy-set membership scores

The analysis of necessary conditions individually reveals that for all the eight situations (four causes and their negations for the outcome) the highest consistency value is 0.83. Given the small number of cases (N = 12), this value is too low to support the claim of necessity (Schneider, 2009). None of the conditions explain individually the presence of cohesive or dispersed networks. Consequently, I look for combinations of sufficient conditions for the outcome. The fuzzy truth table algorithm is applied to transform the fuzzy set membership scores into a truth table (Ragin, 2008b). 9 Each combination of causal conditions is represented as a row with the related truth value of the outcome. These combinations of causes and outcomes are compared with each other and logically simplified following set-theoretic rules. 10 The final result of this simplification process is a logical expression of the causal conditions that are associated with a specific outcome. The complex solution is reported to privilege complexity and do not permit counterfactual cases.

The most complex solution to explain cohesive corporate network yields one combination: bank-based financial structure, interventionist state, firms with blockholders, and low economic internationalization. Cases with membership in this combination are Italy, France, Germany and Spain. 11

BANK-BASED * STATE * BLOCKHOLDERS * international → COHESIVE (Consistency: 0.91; Coverage: 0.51)

The most complex solution to explain dispersed corporate network (DISPERSED) reveals the conjunction of non-interventionist state, market-based financial structure and widely held corporations (state * bank-based * blockholders). Cases with strong membership in this combination are the USA, United Kingdom, Switzerland, Australia and Canada. 12

state * bank-based * blockholders → DISPERSED (Consistency: 0.87; Coverage: 0.63)

Canada displays the combination to dispersed corporate network but this outcome is not reproduced. This particular case is a contradiction and in-depth research of the Canadian case is required. Although it is beyond the scope of this article to unveil the institutional causes of the formation of the Canadian corporate network, a plausible explanation might involve the transnational alliances of Canadian corporations with French firms, and social embeddedness in clubs and policy groups. 13

Japan is not covered by any of these solutions. Japanese corporate network is totally specific and our hypothetical model is not appropriate to predict it. The corporate network in Japan reflects the traditional model of keiretsu. The general structure of the keiretsu is an association of companies formed around a bank. These corporations cooperate with each other and own shares of each others’ stock (Gerlach, 1992). Similar business structures are found in South Korea and Taiwan. South Korean business groups – chaebols – are family-controlled and rely on a complex system of interlocking ownership. However, chaebols are prohibited from owning private banks. In Taiwan the business groups are smaller than in Japan and less familiar than in South Korea (Numazaki, 1996). Therefore, it appears that Asian corporations tend to cluster in order to avoid having to deal with entities out of their trusted allies or family. Comparative research among Japan, South Korea, China and Taiwan, and a new causal model which incorporate the social and family embeddedness of corporations may provide better understanding of the Japanese network.

FsQCA provide two measures to assess the degree to which the empirical evidence is consistent with the configuration identified: consistency and coverage (Ragin, 2006). Consistency assesses the degree to which cases sharing a combination of conditions agree in displaying the outcome in question. Coverage is a measure of how important a causal combination is to the outcome – it resembles an R-square by indicating the number of cases that take this path to the outcome. Overall consistency of the configuration associated with COHESIVE corporate network is 0.91 and coverage is 0.51; the consistency of the configuration related to DISPERSED corporate network is 0.87 and coverage is 0.63. Consistency scores below 0.75 indicate absence of empirical evidence to support the configuration identified (Ragin, 2006). Therefore, the two configurations explain corporate networks to a large extent. However, the difference in the coverage indicates that our hypothetical causal model better fits to explain the dispersed corporate networks.

Dixon et al. (2004) suggest the use of more conventional and statistical techniques to validate fsQCA results such as t-tests. Accordingly, I calculate the ratio between the fuzzy score mean of the cases in the configuration identified and the fuzzy score mean of cases not captured by this configuration, and assess whether they are significantly and statistically distinct. 14 The configuration associated with cohesive corporate network (BANK-BASED * STATE * BLOCKHOLDERS * international) presents a ratio of 9.88 which indicates that countries with this configuration are almost 10 times more likely to produce cohesive corporate networks relative to those without this configuration. Comparing the fuzzy score mean of cases that fit in the configuration associated with dispersed corporate network (state * bank-based * blockholders) to the fuzzy score mean of cases that do not reproduce this configuration, a ratio of 6.06 is obtained, which denotes that countries with this configuration are six times more likely to produce dispersed networks relative to those without this configuration. These differences are large and statistically significant at 0.001 alpha level.

Discussion and avenues of research

Using data from 2005 this research shows that there are distinct varieties of corporate networks in the developed countries and that there is little evidence for the convergence of corporate interlock networks. The categorization between cohesive and dispersed networks may also correspond to different approaches to power and the meaning of interlocking directorates. Cohesive corporate networks are based on unity, compactness, centralization and strength ties. Moreover, high social cohesion also means higher rates of social control, that is, corporations are accessible and therefore more likely to be controlled by the rest of the firms. In low cohesion networks, the firms are more autonomous and less susceptible to external influences and social control. Dispersed corporate networks are characterized by greater corporate autonomy, fragmentation, decentralization and single ties.

In predicting the type of corporate network using fsQCA, the results of this study underscore the interplay of causal conditions as opposed to single factor explanations. Accordingly, the findings show instances in which an outcome depends on the value of other variables, whose values are, in turn, mutually dependent. The conjunction of these factors illustrates the institutional interdependencies empirically demonstrated by political economy scholars. 15 Such institutional interactions are conceptualized as institutional complementarities within the varieties of capitalism literature by Amable (2005) and Hall and Soskice (2001). Proponents of this view argue that the stability and reproduction of particular capitalisms are achieved by their institutional complementarities: the presence of one institutional form leads to the adoption, functioning and efficiency of another institutional form. The present study contributes to the institutional complementarities hypothesis by showing the joint effect of financial systems, state intervention, ownership structure and economic internationalization in the formation of corporate networks. Consequently, corporate interlocks should be included within the sphere of political economy in future research on varieties of capitalism. In addition, fsQCA should be used to map and analyze types of capitalisms beyond linear indexes (Casey, 2009; Hall and Gingerich, 2009) and cluster analysis (Geffen and Kenyon, 2005).

The results of this study suggest that the fit of institutional settings and type of corporate network is the result of underlying mechanisms. Cohesive corporate networks are brought about by the combination of bank-based finance, interventionist state, firms with blockholders, and low economic internationalization. If the financial system is based on banks, interlocks between financial and non-financial corporations are the means to reduce transaction costs, and thus, networks are valuable as mechanisms of investment control. When a state is highly interventionist, it tends to foster cohesive and centralized networks because these are easier spaces to control. Blockholders build networks to control the firms they own. In these countries – Italy, France, Germany and Italy – there is an emphasis on relational control. The configuration of cohesive corporate networks can be attributed to control from the financiers to financed firms, from the state to corporate sector, from blockholders to corporations. In countries with dispersed corporate networks, control is imposed by the market itself. The external control of corporations can be the mechanism between institutions and corporate networks. Further research should investigate whether the changes in external control of corporations following the financial crisis of 2008 have modified the corporate interlock networks.

Consequently, the main contribution of this article is that it demonstrates the utility of employing fsQCA in conjunction with social network analysis. Both social network analysis and fsQCA use a macro-level and configurational approach, social network analysis describes the whole case as a configuration of relations and actors, and fsQCA holistically conceives the cases as configurations of conditions and outcomes. However, a social network approach does not provide techniques for assessing causation and needs complementary methods to study causes and consequences (Fischer, 2011; Yamasaki and Spreitzer, 2006). FsQCA is a promising tool for comparative research that is well suited for evaluating combinatorial cause–effect relationships. As seen in this article, the dual approach combining fsQCA and social network analysis generates an innovative avenue that might boost research on the comparison of networks, and above all on the conjunctural causal conditions that determine network structure.

Footnotes

Appendix 1. Calibration process

In order to establish fuzzy membership scores for financial structure (BANK-BASED), I employed the Demirgüç-Kunt and Levine’s (2004) index of financial structure which establishes the ratios of banking sector development in relation to the development of capital markets in 150 countries. The financial structure index ranges in our sample from -0.92 to 2.93, lower ratios reflect bank-based financial structures and higher ratios market-based economies. The threshold for full membership in the set of bank-based financial structures (BANK-BASED) is -0.5 and below. Full exclusion of the set is 1.5 and above, and the cross-over point is 0.3. Scores close to 1 designate bank-based financial structure, for example, Italy, and close to 0 market-based financial system, for example, USA. I adopted this hard threshold to distinguish economies such as United States, where more than 9000 companies are listed in the stock exchange, compared to nearly 700 listed in Germany (Franks and Mayer, 2001).

Fuzzy membership scores for interventionist state (STATE) are assigned by reviewing research about political intervention, specifically in the corporate sector (Aganin and Volpin, 2004; Amable, 2005; Costas and Germà, 2001; Della Sala, 2004; Gámir, 1999; Gerlach, 1992; Schmidt, 2002) and measuring the percentage of state-controlled large firms (La Porta et al., 1999). States are highly interventionist when: a) have managed strategically privatization of state-owned companies to consolidate national large shareholders, b) have protected corporations against hostile takeovers and foreign acquirers, c) have financed corporate firms, d) have not promoted anti-trust laws, and d) are blockholders of the large firms. If states have undertaken these five major policies, full membership (1) is assigned to the set (STATE), for example, Italy. When none of these actions have been accomplished, cases are fully out of the set of interventionist state, for example, United Kingdom. I use a six-value fuzzy set (1; 0.8; 0.6; 0.4; 0.2; 0) to calibrate.

To measure ownership structure, particularly who owns large corporations, I again turn to the La Porta et al.’s (1999) study. They divide firms into those who are widely held and those who have ultimate owners using a 10 percent threshold of voting right control. The variable ranges from 100 percent of large firms controlled by blockholders to 0. I then created the set of countries where firms have blockholders (BLOCKHOLDERS). For the point of full membership into the set I employed 100 percent. A percentage of 20 percent renders the case fully out of the set and the cross-over point is 60 percent. Countries with high percentage of firms with blockholders are attributed high fuzzy scores, for example, Sweden; ownership structures with high percentage of widely held corporations are scored close to 0, for example, UK.

To measure economic internationalization I use both FDI inflow and FDI outflow between 1994 and 2004 controlled by GDP (Christiansen and Bertrand, 2005). The variable ranges between 1 and 0.06 for the sampled cases. Based on these data I created the fuzzy set of countries highly internationalized (INTERNATIONAL). The score that qualifies a country for full membership in the set of high internationalized countries is 0.8; the score for fully exclusion from this set is 0.2; and the cross-over point is 0.5. Fuzzy scores close to 1 indicate higher economic internationalization, for example, Netherlands; and close to 0 point lower economic internationalization, for example, Japan.

Finally, the scale cohesive-dispersed corporate network is calibrated using the regression based factor scores, which were transformed into a log-odds metric. Scores above 1 indicate full membership to COHESIVE (the highest density, compactness, centralization and multiplicity); scores below -1 are out of the set cohesive (low density, compactness, centralization and multiplicity), that is, DISPERSED networks. The crossover point is 0 as this indicates neither in nor out.

I also explored different thresholds for the causal conditions and the outcome by lowering and raising cut-offs. The identified combinations remained stable. Appendix Table A1 summarizes thersholds for calibration of fuzzy-set memberships scores.

Acknowledgements

This article would not have been possible without the comments and suggestions of Roy Barnes, Josep A. Rodríguez, Christian Oltra, Josep Lluís C. Bosch, Cesar Guzmán and anonymous reviewers.

Funding

This research has been financed by Spanish Ministry of Science and Technology (SEC2003-02353).