Abstract

Over the past 25 years, significant New Public Management (NPM) reforms, particularly towards accrual accounting, have characterized the public sector in many countries. The diversity in public financial information systems created a need for harmonization, resulting in the elaboration of the International Public Sector Accounting Standards (IPSAS). Despite their relevance, little is known on the adoption process of IPSAS. This study aims to examine to what extent IPSAS(-like) accrual accounting is adopted in central/local governments worldwide as well as to investigate which factors affect the differing level of their adoption. Methodologically, a specific questionnaire constructed to obtain relevant information from local experts was sent worldwide to a sample of countries. The study reveals an important move to accrual accounting, particularly to IPSAS accrual accounting, for which there still remains a level of reluctance mainly in central governments, especially in countries where businesslike accrual accounting has been developed.

Points for practitioners

IPSAS have become the international reference for the development of public sector accounting systems worldwide. For this reason, IPSAS deserve the attention of accounting policy-makers, practitioners and scholars. The current study offers a comparative study of the level of adopting IPSAS worldwide as well as an explanation of the reasons behind the differing levels of adoption. The present study reveals that the transition towards IPSAS necessitates a long period of implementation whereby existing local business accounting regulations hinder jurisdictions from implementing international standards. The explanatory findings provide input for reformers and legislators when designing and developing financial information reforms.

Introduction

One of the most important aspects of New Public Management (NPM) is the trend to reforms in financial information systems. These changes are an essential element in improving the management and decision-making of government institutions, which is also called New Public Financial Management (NPFM) (Guthrie et al., 1999). The cornerstone of reforming financial information systems is the introduction of accrual accounting in the public sector, at the expense of traditional cash accounting systems (Lapsley, 1999). Several governments have adopted and implemented accrual accounting systems. Various authors (Groot and Budding, 2008; Pina and Torres, 2003) emphasize the advantages of introducing accrual accounting in a governmental context. Accrual accounting, as defined and introduced by NPM reforms, provides more and accurate information about government solvency, patrimonial goods and the costs of public services (Pina and Torres, 2003: 335). In the last decade, the International Public Sector Accounting Standards Board (IPSASB), which used to be the Public Sector Committee (PSC) of the International Federation of Accountants (IFAC), has developed a set of International Public Sector Accounting Standards (IPSAS) in order to streamline and support these reforms.

Based on a former comparative study limited to the European situation (Christiaens et al., 2010) and on newly gathered evidence in countries worldwide, this study aims to shed a light on the actual level of reforms of the financial information systems, particularly with regard to the adoption of the IPSAS. Second, and particularly for European countries, this article compares the current situation with the level of adoption found in 2009 (Christiaens et al., 2010).

This article attempts to contribute to the comparative studies in public sector accounting. Some authors, such as Benito et al. (2007) and Brusca and Condor (2002), have made contributions to comparative accounting studies in the public sector. Most of them, however, focus on a small sample of countries or on a particular aspect of the accounting legislation. There are also a few surveys mostly developed by consulting firms (e.g. Ernst & Young, 2012; PWC, 2013) presenting an international overview and highlighting current practices, but these are not meant to serve a scientific purpose. It is the aim of this article to compare the adoption of accounting systems in relation to IPSAS within a broader international context. Furthermore, while other articles focus only on the actual state of the adoption or implementation of an accounting system, this study also attempts to point to the reasons why governments choose a specific accounting system.

Following this introduction, a theoretical explanation of accrual accounting reforms is given and the literature on reasons for differences in accounting practices is presented, as well as the environmental characteristics of the continents observed. Emphasis is placed on the efforts concerning the international harmonization of accounting standards. The third and fourth sections provide the research objectives and the methodology of this article. Next, the results are presented. Finally, the main findings of this research article are summarized.

What affects financial information systems? A literature review

The worldwide process of globalization in economic activity has pushed for globalization also in accounting principles and practices: it is a fact that in the private sector there is a demand for harmonization, as demonstrated by the enlarged adoption of IAS/IFRS (International Accounting Standards/International Financial Reporting Standards) and the convergence project of FASB/IASB (Nobes, 2011). The process of converging accounting standards aims to enhance the international comparability of financial statements, in order to satisfy the information needs of different kinds of stakeholders in international markets (Choi, 2003). Nevertheless, as highlighted by the environmental theory (Choi and Mueller, 1992; Nobes and Parker, 2004; Zeff, 2012), the application of accounting standards differs for different purposes. Even in the public sector there is a growing interest in the widespread adoption of generally accepted accounting principles, resulting in the unique IPSAS. These standards aim to improve comparability at different governmental levels. For many years budgetary accounting has been the mainstream accounting and financial information system in the public sector (IFAC, 2008; IFAC PSC, 2000). Most governments need budgetary accounting to manage budget appropriations, i.e. in the context of the yearly discussion and approval as well as the follow-up of their budgets. During recent decades and driven by NPM, many governments have reformed their accounting system into accrual accounting. The work of the IPSASB has revived the discussion about harmonization in the public sector. Similarly to previous research in the business sector, some studies (Brusca and Condor, 2002; Pina and Torres, 2003) have demonstrated that the development of national accounting systems tends to be a function of different institutional attributes and environmental factors. Culture has been defined by Hofstede as ‘the collective programming of the mind which distinguishes the members of one human group from another’ (1980: 25). In addition, environmental factors – including legal systems, sources of external finance, taxation systems, and representation by professional accounting bodies, historical inflation, economic and political events – have been largely adopted to help explain international differences in accounting practices (Nobes and Parker, 2004: 17–31). In any case, most of the studies try to identify patterns and influential factors with reference to business accounting (Gray, 1988; Muller, 1967; Nobes 1998; Zeff, 2012) while very few studies have examined the public sector (see the synthesis in Baker and Barbu, 2007). Despite a large number of New Public Management (principles and criteria) reforms around the world, different accounting systems are still in evidence worldwide. As the present study highlights, these NPM reforms tend to adopt accounting systems based on accruals as a tool to gain wider accountability in a democratic system and in a free market (Chan, 2003).

Many scholars have highlighted how the implementation of accrual-based accounting systems, as an alternative to cash-based or obligation-based systems, would not be necessarily consistent with the main characteristic of public entities (Christiaens and Rommel, 2008; Mack and Ryan, 2006). On the other hand, it has also been pointed out (Christiaens et al., 2010; Fédération des Experts Comptables Européens, 2007) that cash-based accounting does not allow for obtaining the necessary information in order to provide better support for planning and managing resources and more generally for decision-making processes, allowing greater comparability, even between different entities.

It has also been hypothesized that a significant boost towards harmonization can be derived from the financial market and rating agencies; nevertheless, according to Ingram (1983), this boost is effective especially for countries that need to approach financial markets, where a decrease in financial costs can cover the costs arising from a change in the accounting systems. This hypothesis, even if fascinating in our context, with a financial crisis affecting almost all countries, is difficult to test empirically. As already highlighted by Chan (2006), relevant citizens’ expertise and awareness as well as their socioeconomic status can be relevant as well as the role played by politicians and managers in the adoption of change in accounting systems.

In organizational studies, scholars have emphasized the existence of isomorphism in trying to explain changes, especially the ones related to international standardization (Burns and Scapens, 2000), within neo-institutional theory (Meyer and Rowan, 1977). According to this approach, similar organizations tend to conform to each other and they became more similar, in order to obtain institutional legitimacy. According to DiMaggio and Powell (1983), the adaptation process is stronger when the organization depends on external resources and, at the same time, has certainty over their own goals. Essentially, while some scholars prefer to consider institutional factors, others give more relevance to behaviour and culture.

In relation to the adoption of IPSAS – more than for the adoption of a single standard – the problem arising is the effective need for harmonization. Looking at the literature on the matter, it seems that accounting harmonization could not be avoided, it is self-explanatory and somehow inherent to the idea that any transaction would be accounted for according to the same rules everywhere (Pina et al., 2009).

Different authors state that the international trend towards modernizing the financial information system is likely to continue in coming years (Grossi and Soverchia, 2011; Lüder and Jones, 2003). An important stimulus in this evolution is the support of international organizations such as the OECD, NATO, the United Nations, the European Commission and Interpol. All these influential organizations promote sound financial management and accountability. Such ‘good practices’ have a moral influence on different countries around the world. In addition, the International Organization of Supreme Audit Institutions (INTOSAI, 2005) promotes the use of IPSAS (Algemene Rekenkamer, 2003). In light of the above literature review, the present research aims to highlight differences in the adoption of (IPSAS-(like)) accrual accounting worldwide.

Research objective

Although the trend towards adopting accrual-based accounting systems in the public sector occurs, different systems are adopted. These differences are situated at three levels: (1) the content, (2) the timing of the adoption and (3) how accrual accounting will be applied. Both national (Carvalho et al., 2007) and international studies (Christiaens et al., 2010) show that there is a great diversity in the way the accounting reforms are implemented in local governments within one country as well as in local governments in different countries. Due to the non-enforceable mechanisms of IPSAS and the lack of penalties, many governments look at their own needs and do not fulfil all of the requirements prescribed by IPSAS. If each country adopts accrual accounting systems according to their own particular necessities, accrual accounting reforms will not be homogenous. It can be stated that, in spite of the international implementation of accrual accounting, the financial information systems in the public sector are still relatively divergent (Benito et al., 2007; Brusca and Condor, 2002; Carvalho et al., 2007; FEE, 2007; Lüder and Jones, 2003; Pina and Torres, 2003).

There is also a significant diversity in the timing of the adoption process. Some countries are investing intensively in modernizing their accounting systems. Countries that lead the bunch are mainly Anglo-Saxon (Australia, New Zealand, the United Kingdom and the United States), while other countries choose a more conservative approach (Benito et al., 2007; Carlin, 2005; Christiaens et al., 2010; Groot and Budding, 2008; OECD, 2002; Van der Hoek, 2005).

A third difference refers to the way in which accrual accounting is adopted. Some countries have a decentralized vision, which means that the accrual accounting reforms are first developed at the municipal level before they are introduced into central government (e.g. Sweden). Other jurisdictions impose the introduction of NPFM reforms in a more centralist way (e.g. New Zealand) (Groot and Budding, 2008; Guthrie et al., 1999; Olson et al., 1998).

This study can be seen as a sequel to the comparative European study of Christiaens et al. (2010) from a worldwide perspective. The aim of this article is to study the different levels of adopting accrual accounting across different countries. The focus is on the level to which accrual accounting is adopted. This study does not aim to focus on the content-related differences in accrual accounting. This work has already been done by other authors such as Benito et al. (2007). Therefore the first research question is the following: RQ 1: To what extent is (IPSAS-like) accrual accounting adopted in central/local governments in countries worldwide and, particularly for European countries, what are the changes between the situation found in 2009 and the current situation?

This study focuses on the adoption of new governmental information systems, i.e. the decision of the legislator or standard-setter to prescribe a specific accounting system. The adoption is an important issue as it is the first step in the whole reform process. The implementation of the prescribed accounting system is the next phase of the reform process. Some authors (Benito et al., 2007; Brusca and Condor, 2002; Pollitt and Bouckaert, 2004) have shown that there is great diversity in the implementation of structural (accounting) reforms. However, the way and the status of implementing the accounting regulations is beyond the scope of this research article and could be a topic for further research. It is the preceding phase of developing and adopting modernized information systems, in the light of international standards, that will be examined in this article.

For local as well as for central governments the study by Benito et al. (2007) reveals that there is a reasonable degree of concordance with the IPSAS, but they also prove that there is a lack of homogeneity between different accounting systems in the European Union. The study even states that diversity is a main characteristic of financial reporting in local and central governments. The current article tries to enrich the accounting literature by investigating the reasons for this diversity. Therefore the second research question is defined as follows: RQ 2: What explains the differing level of adopting IPSAS at different levels of government?

Methodology

In order to investigate these research questions, a field study across 81 countries/jurisdictions was set up by means of a survey (Christiaens et al., 2010). The UN list of countries 1 was taken as the sampling frame, and a first selection was made by excluding all countries with fewer than 1 million inhabitants, because of their limited size. Second, the possibility of contacting certain academics, practitioners and officials (the three groups of experts) was taken into account, which further decreased the list of potential target countries. For reasons of comparison, it was ensured that all countries included in the previous study (Christiaens et al., 2010) were also part of the current sample. 2

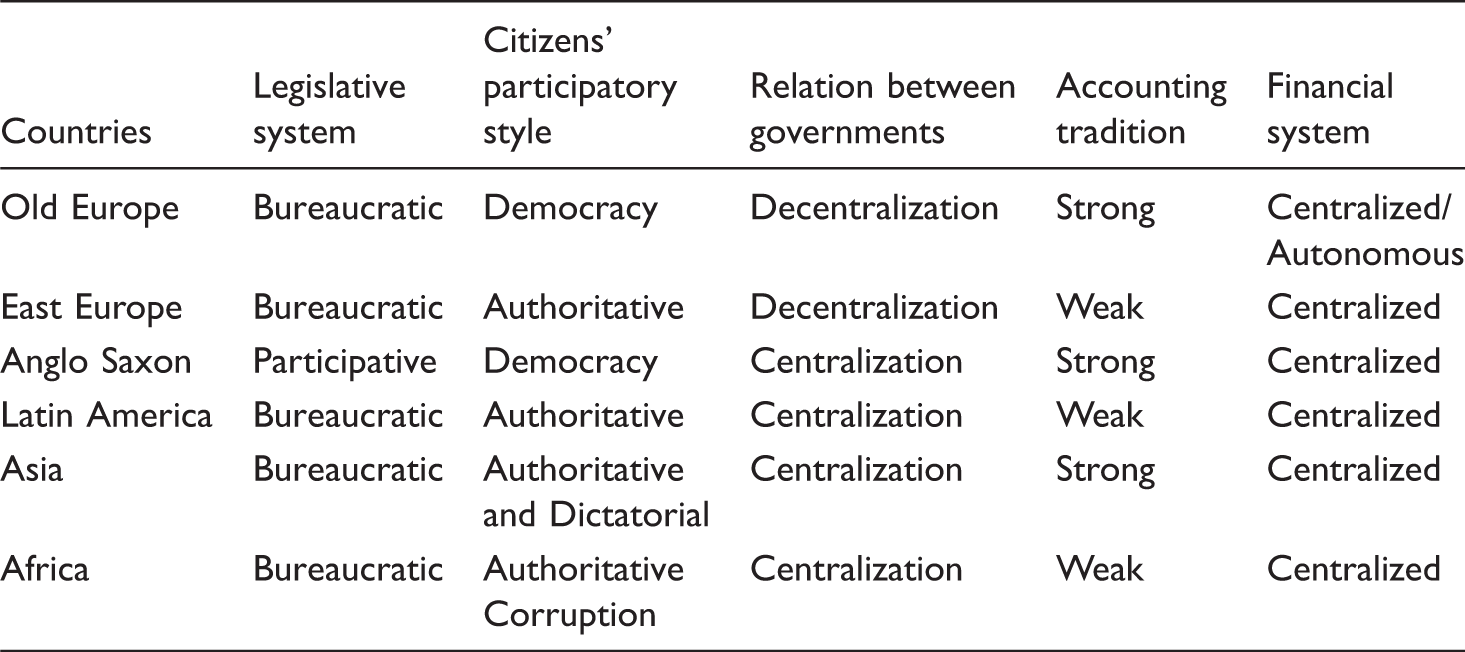

The differences in culture, historical context or in structural elements of each country may influence the public sector reforms and the accounting systems (Benito et al., 2007; Pina et al., 2009). To explain the different features of public sector reforms undertaken all over the world, the countries are divided into six groups according to their different styles of public management (Brusca and Condor, 2002; Pina et al., 2009): old Europe, New Europe, Anglo-Saxon countries, Latin America, Africa and Asia.

The study covers local governments as well as their overall central governments. In most countries the central government is the national government. However, in Germany and in Belgium the so-called Bundesländer and Communities are very independent and differ greatly with respect to the adoption of accrual accounting and IPSAS. Both of the communities in Belgium as well as two representative Bundesländer were selected.

Based on a number of credentials (publications, years of experience, etc.) a sample of three experts, i.e. an academic, a professional and a consultant, were selected in each jurisdiction or country. The academics are mainly professors and researchers specialized in public sector accounting. They were selected on the basis of previously published research documents and articles. The professionals (of central and local governments) are people of at least a middle level, who are involved daily in governmental accounting issues. All selected consultants belong to a big-four accounting firm and are experienced in public sector accounting activities. The questionnaire remains mainly the same as in previous research (Christiaens et al., 2010) except for some slight improvements.

The responses to the questionnaire were not the only source of data. Because of the increasing occurrence of, for example, IPSAS Board reports and presentations as well as social media such as LinkedIn IPSAS groups, additional information regarding ongoing accounting reforms in certain countries/jurisdictions was gathered to supplement the responses to the questionnaires.

Results

Overview of financial information systems in Europe

A▪ = Local government, B□ = Central government

Overview of financial information systems in the rest of the world

A few Anglo-Saxon countries opted for IFRS unless certain accounting issues are not regulated by IFRS and reference needs to be made to IPSAS; IFRS are very close to IPSAS.

Reasons to link the accrual accounting legislation to IPSAS4

Reasons for not linking the (planned) accrual accounting legislation to IPSAS4

Table 1 gives an overview of the financial information systems in European governments and in governments of the rest of the world, respectively. Panel A shows the situation in local governments, and panel B gives the same information for the central governments. The first column enumerates all the countries/jurisdictions. The second column (i.e. ‘IPSAS’) shows those jurisdictions that fairly match IPSAS, implying a reasonable conformity with all of the 32 actual IPSAS standards covering the accounting measurement basis, valuation rules as well as the annual accounts. It is possible that some of them have minor exceptions to IPSAS (e.g. one of the standards has not yet fully been adopted, regarding the valuation of plant and equipment certain goods are excepted, etc.), but in general they are based on IPSAS.

The third column shows the jurisdictions that currently account on a cash basis but are planning to introduce an IPSAS(-like) accrual accounting system in the near future. This column is also relevant because the transition to IPSAS or to accrual accounting often requires a number of years to consider, prepare, plan and decide its adoption.

Column four (i.e. ‘accrual accounting’) represents jurisdictions that do not choose IPSAS, but apply another form of accrual accounting. IPSAS is a form of accrual accounting derived from the IAS/IFRS standards, but as shown in Christiaens et al. (2010) in a number of countries governments apply accrual accounting inspired by their business accounting rules. The ‘planned accrual reform’ column lists the jurisdictions that still account on a cash basis, but are planning to transform their accounting system to a non-IPSAS accrual version. Those jurisdictions that account on a cash basis and do not plan to introduce an accrual accounting system are shown in the last column.

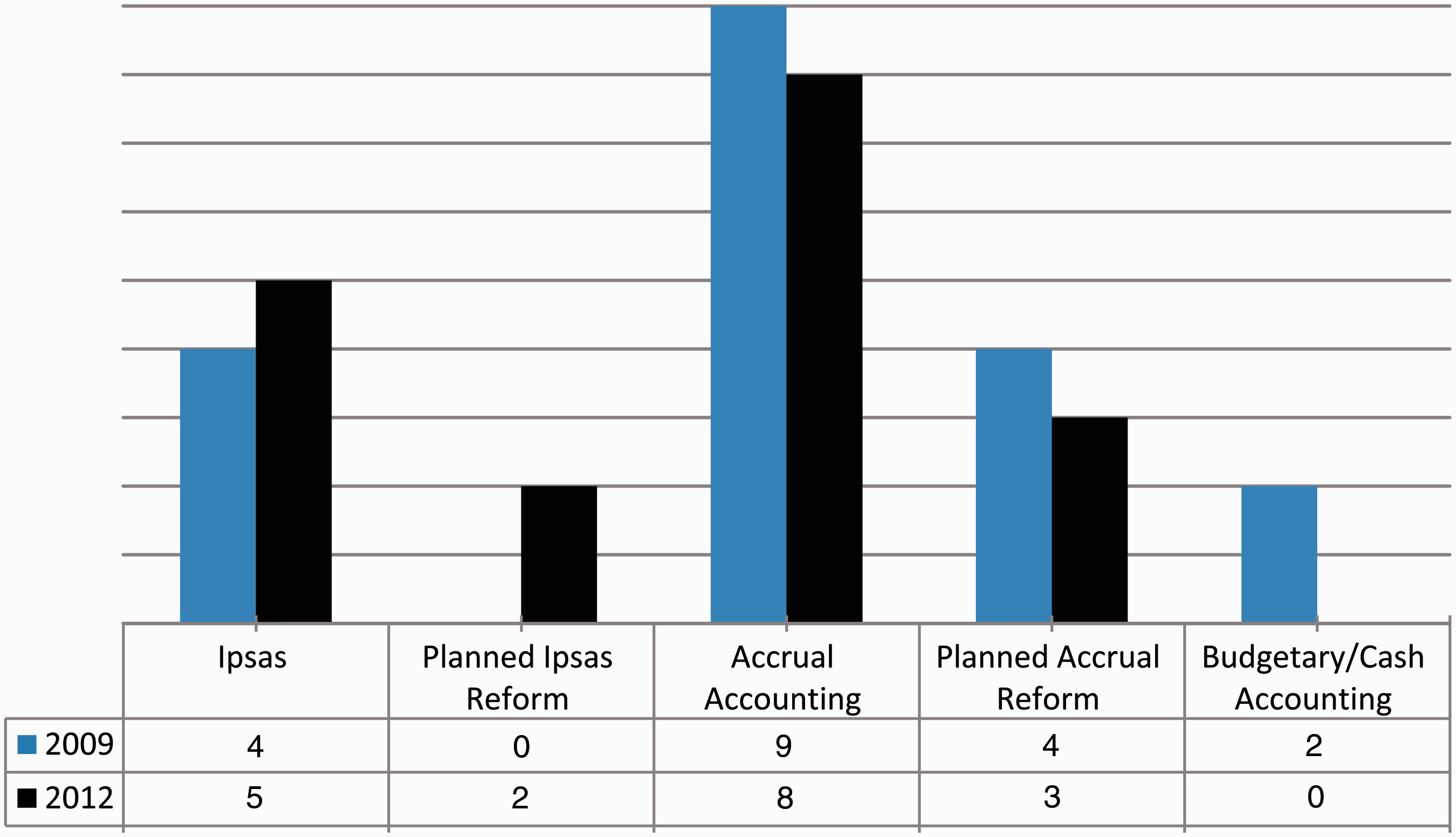

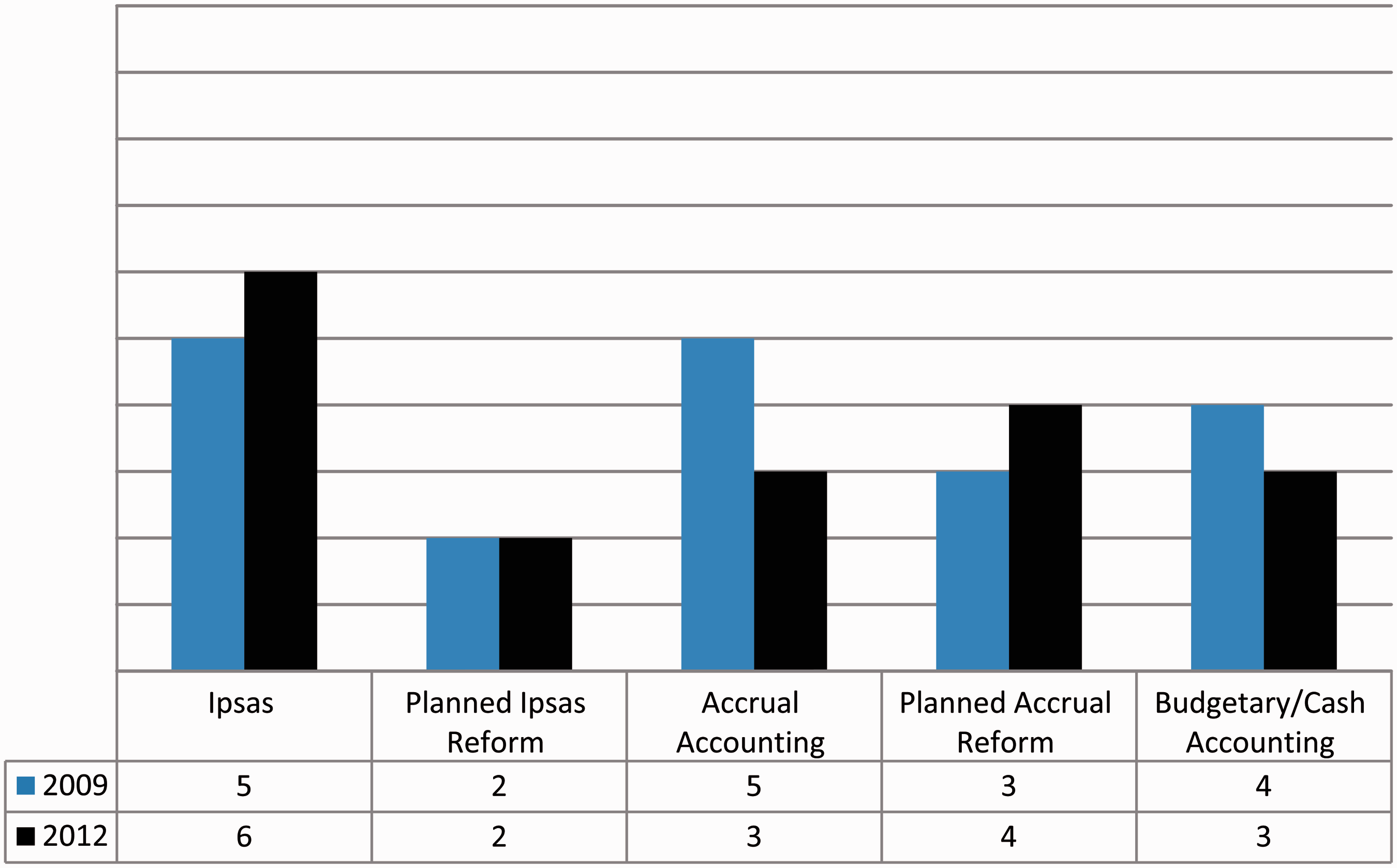

Figures 1 and 2 show the comparison of the 2009 study for ‘old’ Europe (Christiaens et al., 2010) with the corresponding 2012 figures for ‘old’ Europe. This comparison in time reveals that for local governments financial information systems move from budgetary accounting to accrual accounting and even to IPSAS. As a matter of fact, in ‘old’ Europe none of the local governments still apply just the cash accounting system. Regarding central governments, this effect is less prevalent and about 17 percent of the ‘old’ European central governments still resist any change to their cash accounting system. In the sample examined there are even a few jurisdictions that have turned the clock back. On the other hand, the adoption of accrual accounting, particularly IPSAS, is rising, albeit slightly. These findings are in line with the recently published results in Public Consultation – Assessment of the Suitability of IPSAS for the EU Member States (EC Eurostat, 2012). Thirty-eight percent of the 68 respondents answered that they considered IPSAS to be suitable for implementation. However, 28 percent were against and 31 percent of the respondents were only partly in favour. Apparently, there remains an important level of resistance and this confirms the findings in current study.

Financial information systems in ‘old’ Europe local governments Financial information systems “old” Europe central governments

In the majority of these countries, the weak internal harmonization (among different levels of government) reflects on the external harmonization among states (Caperchione, 2012). For example, vertical harmonization is strong in the UK and Sweden and it is weak or only partial in Italy, France and Spain. Nordic countries such as Sweden, Finland, Denmark and the Netherlands were leaders in NPM developments, and the introduction of accrual accounting into central government is related both to management devolution and to territorial decentralization (Oulasvirta, 2014; Pina et al., 2009).

In countries of the new Europe the public sector accounting reforms have undergone multiple changes in order to modernize the financial information system. For some of them (e.g. Romania and Ukraine) the transition has not been easy particularly in the years after the end of communism and the beginning of the capitalist era (Albu et al., 2010). On the other hand, the former Eastern European countries appear to adopt the IPSAS system more intensively. This can be explained by their striving to adhere to the EU as well as by the ‘Law of stimulating arrears’ 3 (de Wit, 2011). 4

As could be expected based on previous research (Pina et al., 2009), the Anglo-Saxon countries are used to applying accrual accounting in their central as well as local governments. Some have explicitly decided to implement IPSAS; others prefer IFRS, being very close to IPSAS. The USA have their own accrual accounting system, being GASB (Governmental Accounting Standards Board) for local authorities or FASAB (Federal Accounting Standards Advisory Board) for the central state. The second exception is Ireland because of their general tendency not to embrace NPM ideas with excessive enthusiasm (Connolly and Hyndman, 2009). Although some countries actually have somewhat Anglo-Saxon roots (e.g. Kenya), African countries mostly adhere to the cash accounting system. The majority of African countries have a bureaucratic and centralized system; the accounting traditions are weak because African countries have been strongly colonized with the consequent influence of English, French, etc. traditions (Muiu, 2010). Historically, developing countries have lacked a rigorous public sector accounting framework and this has probably been a contributing factor to high levels of wastage and corruption in some of these countries (Jreisat, 2010). According to Chan (2006), the adoption of IPSAS in developing countries often requires a large investment in educating and training people to develop a new range of accounting skills. This is not always possible in countries where governments have only limited resources.

Latin America reveals a favourable situation for accrual accounting, particularly for IPSAS. This finding is in line with the so-called second-generation reforms whereby public budgets and modernization of management and public finance became necessary (Caba Pérez and López Hernández, 2007). This is also the case on the Asian continent where many jurisdictions strive to implement accrual accounting and IPSAS. In recent years, Asian countries have undertaken significant economic and political reforms aimed at improving the quality of democracy, strengthening the accountability and transparency of the public sector and combating corruption (Prasojo et al., 2007).

From a worldwide perspective, 44 percent of the local governments have developed an IPSAS-like accounting system, whereas 39 percent are involved in accrual accounting. For central governments, the former is about 51 percent and the latter 22 percent. One can conclude that there are still an important number of central governments applying cash accounting compared with local governments, but in the group of governments that have opted for accrual accounting-like systems, central governments prefer the IPSAS-like accrual accounting system.

Table 3 shows the reasons why jurisdictions make use of IPSAS when reforming their financial information system. Apparently, the majority of the jurisdictions that apply IPSAS do this to enhance (inter)national comparability of financial information, also facilitating the consolidation of financial statements. However, one could argue that this important worldwide expectation in the mind of governments will not be sufficiently achieved by adopting IPSAS because the IPSAS do not define the structure of financial statements. As a matter of fact the IPSAS also leave a number of valuation options, for example, IPSAS 17 Property, plant and equipment allows two different valuation policies, being the cost model or the revaluation model. On the other hand, the IPSAS are almost unique worldwide and provide a common platform to enable converging practices. This convergence is necessary because financial reporting should be harmonized to become comparable and the current sometimes divergent adoption of IPSAS explains somehow why entities chose not to apply IPSAS.

Also important in Table 3 is the concordance with international organizations. The comparison between the public and private sectors seems to be less important. The ranking of the reasons is almost the same between local and central government, although the different items of motivation are more stressed for central governments. In other words, the adoption of IPSAS(-like) systems in central governments is considered to be more relevant than in local governments. Regarding the geographic regions examined, there does not appear to be a relevant difference. The responses from the different geographic regions indicate more or less the reasons, for example, the maximum level of 21 for the reason ‘To enhance (inter)national comparability of financial information’ for local governments is shared by ‘Old’ Europe, Africa and the Americas as their most important reason, and the minimum of 9 for the reason ‘To improve public/private comparability’ for local governments is shared by ‘Old’ Europe, the Americas and the Anglo-Americans as their least important reason.

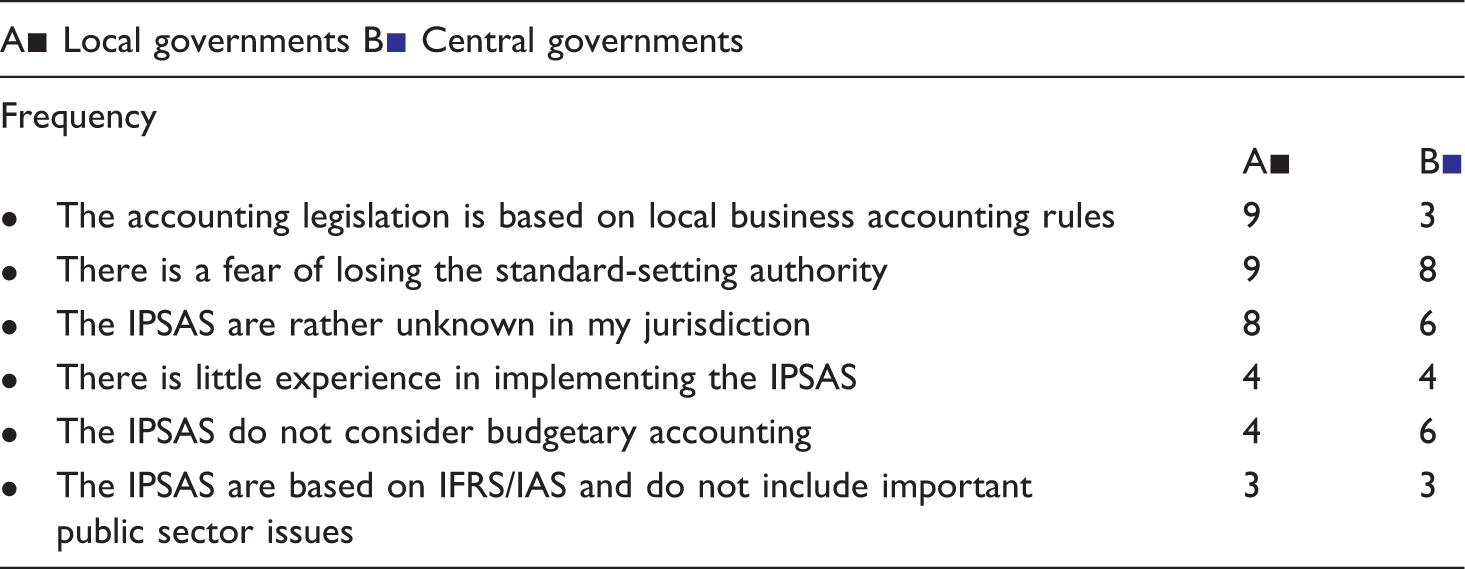

The main reasons why some jurisdictions are interested in consulting IPSAS when reforming their accounting legislation are summarized in Table 4. Similar to a previous study (Christiaens et al., 2010), one of the most important reasons for not adopting IPSAS is the existence of dominating local or country-wise business accounting rules. Countries in which such business accounting rules are well known and accepted will strive to transfer them to their governmental sector, whereas countries that are not used to accrual accounting systems appear to change their accounting systems more fundamentally to internationally accepted standards, those being IPSAS. Examples can be found in Eastern European countries formerly dominated by communist influences. As such, governments applying the local business accounting rules deliver more comparable financial reports next to the IPSAS-like countries, albeit that often the local business accounting rules are often country-bound and are less comparable. Other crucial factors in not applying IPSAS still are the fear of losing its standard-setting authority, the unfamiliarity with IPSAS and the lack of attention to budgetary accounting.

A positive conclusion is the fact that Table 3 exceeds the number of answers shown in Table 4, which implies a general favouring of IPSAS more than a disregard for them. However, a number of understandable negative assessments remain.

Institutional factors explaining the worldwide public sector accounting situation

Conclusion

The intention of this research was to develop a follow-up study regarding the level of adopting IPSAS in the previously examined European governments (Christiaens et al., 2010) to all local and central governments worldwide. This offers two new perspectives, being a comparison of the previously examined European situation in 2009 vs 2012 and the possibility to extend the European situation to a worldwide comparison.

Apart from data coming directly from the IPSAS Board and the corresponding notes and publications, a survey sent to three kinds of experts in the jurisdictions sampled resulted in data collection from 59 jurisdictions worldwide. The survey mainly consisted of factual questions next to a set of questions regarding perceptions. The importance of the interpretation of the results coming from the three different experts is clear. A revision of the few mismatches was conducted, whereby these experts were contacted for clarification. The answers of the experts were complementary and quite coincident.

When comparing the European situation 2009 and 2012, the examination undoubtedly reveals an important move to accrual accounting, particularly to IPSAS. All of the ‘old’ European local governments have adopted accrual accounting and in the ‘old’ European central governments only about 17 percent are still limited to just cash accounting. On the other hand, it can be seen that there remains an important number of local (about 28 percent) as well as central governments (about 33 percent) that have planned to implement accrual accounting, particularly IPSAS. In other words, the length and importance of the planning stage should not be underestimated. Second, the 17 percent of central governments who keep their cash system unchanged indicates some reluctance probably due to their more explicit political need for budgetary accounting and their important macro-economic perspective.

The figures in the ‘new’ European countries reveal a differing situation, which can be explained by the different timing of state reforms those countries underwent. Second are the emerging economies, which often need IMF support and which make use of the IPSAS when reforming their financial information systems from a resource dependence theory point of view.

Although one can argue about the definition of countries belonging to the Anglo-Saxon world, it is quite clear that the tendency towards accrual accounting and IPSAS or IFRS, which is close to IPSAS, appears. This is probably also due to the ‘principles-driven’ character behind IFRS and IPSAS, which is an Anglo-Saxon feature instead of the rather ‘rules-driven’ legally defined accounting prescriptions existing in continental European countries and in their former colonies.

As in the previous study (Christiaens et al., 2010), the main reasons for using the IPSAS standards is the conviction that the adoption of IPSAS will improve the (inter)national comparability of financial information and to facilitate the consolidation of financial statements. Some jurisdictions, on the other hand, choose to not apply the IPSAS. The reasons for this are twofold. First, important weaknesses are the fear of losing their standard-setting authority and the fact that the IPSAS are still relatively unknown. The second reason why some jurisdictions choose not to apply the IPSAS is because they have chosen to implement their own business accrual accounting regulations, which fits in with the ‘Law of the handicap of a head start’. This slows down the IPSAS compliance process. In order to overcome this, a cultural change as well the necessary enforceability of the IPSAS is necessary.