Abstract

In the context of current debates on sustainable public service provision, austerity, debts and cutback management, the governance and management of and in state-owned enterprises is a crucial issue. An aggregate holdings report is an important tool for public administrations to provide accountability and the necessary overall view on the institutional service provision structures of core administration and state-owned enterprises. On the basis of a developed quality index with 175 test criteria, this study analyses the diffusion of aggregate holdings reports in 17 countries and the quality of 12 existing reports at the national level. First, the study provides a conceptual contribution for assessing aggregate holdings reports and future research on the issues of the model categories. Second, for an empirical contribution, the analysis enhances our state of knowledge on aggregate holdings report diffusion and quality patterns. Findings show that, in many cases, public administrations do not meet the requirements from theory and practice. Newer Organisation for Economic Co-operation and Development and European Union members reach comparably higher quality scores. This comparative study offers new insights that can enhance the sustainable public management and control of state-owned enterprises.

Points for practitioners

The Organisation for Economic Co-operation and Development’s OECD Guidelines on Corporate Governance of State-Owned Enterprises, which were published after an intensive consultation process in 2005 and revised in 2015, demand public authorities to develop aggregate holdings reports that cover all SOEs, and make them a key disclosure tool directed to the general public and politicians. This study develops a quality model for assessing the quality of aggregate holdings reports. The model can also answer questions that are often raised in reform debates, such as ‘Which is the best aggregate holdings report?’ or ‘Which aggregate holdings report can I use as a reference to further develop my own aggregate holdings report?’. The model is a conceptual contribution and the empirical results can be used for international bench-learning. They are also useful for international organisations such as the European Union, Organisation for Economic Co-operation and Development, World Bank, International Monetary Fund, Chartered Institute of Public Finance & Accounting and development aid/cooperation agencies in each country. The results of this study indicate that policymakers at the national and international levels should give more emphasis to the diffusion and quality of aggregate holdings reports and should reflect on establishing and revising legal obligations for aggregate holdings reports because the recommendations of the Organisation for Economic Co-operation and Development guidelines, as a soft-law approach, are often not put into practice.

Introduction

Reforms in the provision of public services with new institutional arrangements have made state-owned enterprises (SOEs) increasingly relevant in many countries. Studies for different countries demonstrate the significant role of SOEs in terms of their economic relevance and for providing public services (Bruton et al., 2015; Millward, 2011). For public management research and for the big societal issues such as sustainability, debt crises, cutback management and citizen engagement, the governance and integrated management of core administration and SOEs is a crucial issue (Askim, 2007; Haque, 1999; Kwon et al., 2013; OECD, 2015; Osborne, 2014). The changes in the institutional arrangements of public service provision have led to new requirements in accountability and transparency. Governance deficits have raised discussions in various countries about the control and transparency of SOEs (Bach and Jann, 2010; Grossi et al., 2015; Massey, 2009; OECD, 2015; Verhoest et al., 2012; Veselý, 2013; Whincop, 2005). The Organisation for Economic Co-operation and Development (OECD) requires public administrations to publish an annual aggregate holdings report (AHR) on SOEs (OECD, 2015: s. VI, C). An AHR is the necessary basis for citizens to obtain a systematical overview (OECD, 2015; Verhoest et al., 2012). For these reasons, it is necessary and rewarding to examine how public authorities report on the performance, debts/credits and governance of their SOEs (Grossi et al., 2015; OECD, 2015). Despite this relevance, studies on this issue are sparsely available, and internationally comparative studies are especially missing. By now, there has only been one publication which assesses AHRs at the local level in three countries based on a first-quality model with 75 criteria (Papenfuß, 2014).

The aim of this study is to assess the diffusion and quality of AHRs in 17 countries at the national level. For this, a new model with 175 criteria is developed as a conceptual contribution for assessing the quality of AHRs. After a section with definitions, the study derives requirements for AHRs from theory and practice. In the following, the empirical design is described and findings are presented. The study concludes with key results, implications for practitioners and needs for further research.

Definition and relevance of SOEs and AHRs

SOEs are defined as enterprises where the public authority has significant control through full, majority or significant minority ownership (OECD, 2015). According to some categorisations, SOEs are classified as type 2 (i.e. non-departmental public bodies) or type 3 agencies (e.g. public corporations), in contrast to type 1 agencies (i.e. next steps agencies) (Van Thiel, 2012). This study assesses the reporting on agency types 2 and 3.

Worldwide, SOEs represent approximately 10% of global gross domestic product (GDP) (Bruton et al., 2015). For Germany, empirical studies show that 50% of the employees in the public sector work not in the core administration, but in SOEs and comparable public organisations. SOEs undertake more than half of the public sector’s investments and the debt ratio of SOEs is often even higher than that of the core administration (Bertelsmann Foundation, 2008, 2013). For other countries, studies show similar tendencies (Millward, 2011).

The OECD’s Guidelines on Corporate Governance of State-Owned Enterprises, which were published in 2005 and revised in 2015, state that: The ownership entity should develop aggregate reporting that covers all SOEs and make it a key disclosure tool directed to the general public, the legislature and the media. This reporting should be developed in a way that allows all readers to obtain a clear view of the overall performance and evolution of the SOEs. In addition, aggregate reporting is also instrumental for the ownership entity in deepening its understanding of SOE performance and in clarifying its own policy. (OECD, 2015: s. VI, C)

Theory perspectives and conceptualisation of AHR diffusion and quality

Theoretical perspectives on the diffusion of AHRs

For this study, diffusion is understood as the public availability of AHRs on the public administrations’ websites. For explaining the diffusion of public management reforms and instruments, neo-institutionalism is a common theoretical approach (DiMaggio and Powell, 1983; Lægreid et al., 2007). DiMaggio and Powell (1983) identify three types of isomorphism that explain a possible similarity of organisations: coercive isomorphism, which results from political or legitimation pressure; mimetic isomorphism as a result of uncertainty; and normative isomorphism associated with professionalisation. For this study, these theoretical types can help to discuss the findings on the diffusion and quality of AHRs and to reflect on whether the empirical data show form(s) of isomorphism or not.

Since OECD and European Union (EU) guidelines and directives should or have to be adopted by member states, there could be a tendency for coercive isomorphism in the form of political or legitimate pressures. Furthermore, it is also of relevance whether legal obligations, the economic situation (national debt and GDP per capita) or population size determine AHR implementation. Due to the economic relevance of SOEs, countries with a high national debt could insist more on the transparency of SOEs and thus publish AHRs more frequently. Regarding legal obligations, it is relevant whether soft laws are sufficient to meet the requirements or whether hard laws are necessary. Moreover, it is rewarding to consider GDP and population size since interesting and significant developments occurred in other contexts in countries with different GDP and population size.

Conceptualisation and derivation of the quality model

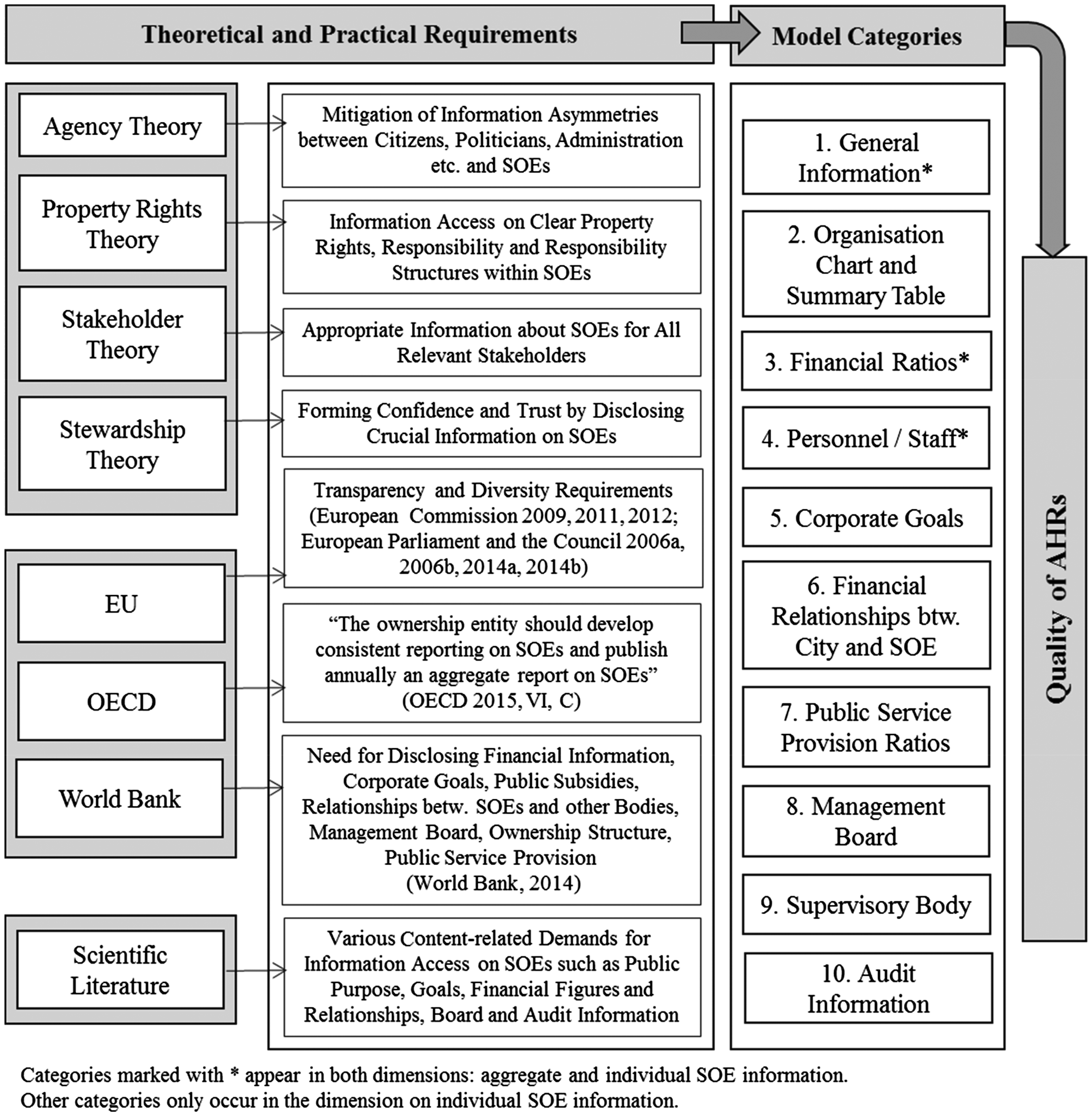

Quality is a latent construct and therefore has to be operationalised for specific contexts. In line with scientific literature, we define the quality of AHRs as properly fulfilling theoretical and practical requirements and fitness for use by practitioners (Bovaird and Löffler, 2003; Crosby, 1992; ISO, 2015: 3.6.2; Juran, 1988). The quality model developed for this study consists of 13 categories with 175 criteria (see Appendix 1). The criteria of the quality model on AHRs are derived from the concept of accountability, theoretical requirements and practitioners’ demands (see Figure 1).

Derivation of quality model categories and criteria for AHRs.

An AHR is a valuable tool for enabling and enhancing the accountability and transparency of SOEs for citizens (Bernier, 2015; Bovens, 2007). Fostering the accountability of SOEs is especially important for preventing loss of control by the core administration, which can result from SOEs becoming more autonomous (OECD, 2015; Schillemans, 2008; Whincop, 2005).

In the perspective of agency theory, task delegation to different public sector organisations leads to increased information asymmetries between principals, such as the public administration, and agents, such as the SOEs, where possible opportunistic behaviour of the agent can appear (Hodges et al., 1996; Whincop, 2005). An AHR therefore has to minimise neuralgic information asymmetries between those actors (Van Slyke, 2007; Whincop, 2005). AHRs need to provide carefully targeted information in those areas where the monitoring of SOEs is difficult and opportunistic behaviour is particularly likely to appear. All principals must have access to necessary information without high efforts, loss, delay or distortion.

Stewardship theory places higher values on mutual alignment with overall objectives and assumes the collective, cooperative and pro-organisational behaviour of actors. Intrinsic motivation, trustworthiness and information exchange are underlying motives for action (Van Slyke, 2007). In view of this theory, AHRs are necessary to develop trust between actors through transparent communication and reporting (Van Slyke, 2007). This could be achieved by disclosing information on strategic, operative and outcome goals, as well as information on public purpose fulfilment.

Property rights theory demands clear responsibilities, rights and obligations of the relevant actors of SOEs to be displayed in AHRs (Demsetz, 1967; Klein et al., 2012). In this perspective, AHRs must clearly show which actors have which property rights. This includes information on clear responsibility structures for controlling and reporting on SOEs but also the responsibilities of individual persons and committees within the management board and supervisory body. Therefore, AHRs should include information on board member names and meaningful information on compensation. In the perspective of the stakeholder theory, all stakeholders need to be adequately informed about SOEs (Bryson, 2004; Donaldson and Preston, 1995).

In addition to those theoretical requirements, the quality model criteria have also been derived from relevant requirements from international organisations such as the OECD, EU and World Bank, as well as from scientific literature.

General information/organisation chart and summary table

Among others, the OECD, the European Commission and the World Bank require aggregate and individual information on SOEs to be disclosed. Direct and indirect holdings with majority interest and capital shares, balance sheet totals, and turnover and employee information should be displayed in organisation charts and tables (Bovens, 2007; European Commission, 2011; OECD, 2015; Whincop, 2005; World Bank, 2014).

Financial ratios and relationships between the public authority and SOEs

Financial, operational and non-financial results of SOEs, as well as costs to fulfil the public purpose, should be disclosed. In particular, this includes balance sheet totals, total investments, expected liabilities and several other relevant financial ratios. In addition, financial relationships between the public administration and SOEs have to be transparent (OECD, 2015; Whincop, 2005; Wong, 2004; World Bank, 2014).

Personnel/staff

SOEs’ staff structure and gender-equality aspects, like representation of women on boards and further management levels, as well as in the whole staff, should be disclosed (Bovens, 2007; European Commission, 2012; European Parliament and the Council, 2006a, 2014a).

Corporate goals and public service provision ratios

Regarding corporate goals, strategic, operative and especially outcome goals, as well as the public purpose of the SOEs, should be stated. AHRs should also disclose service provision ratios and sustainability and environment-related information (Christensen and Yoshimi, 2000; European Parliament and the Council, 2014a; Jung, 2014; OECD, 2015; Schedler and Proeller, 2010; Wong, 2004; World Bank, 2014).

Management board and supervisory body information

Disclosed information should include names and detailed statements on compensation structures. Furthermore, board/body member qualifications, selection process and board diversity should be explained (European Commission, 2009, 2011; OECD, 2015; Tricker, 2012).

Audit information

Regarding international discussions on the audit of SOEs, it is also especially important that AHRs disclose the names of audit companies, the cost for audit and potential parallel consulting by the auditor, and for how many years the company has conducted the audit (European Parliament and the Council, 2006b, 2014b; OECD, 2015; Tricker, 2012).

Research approach and methodology

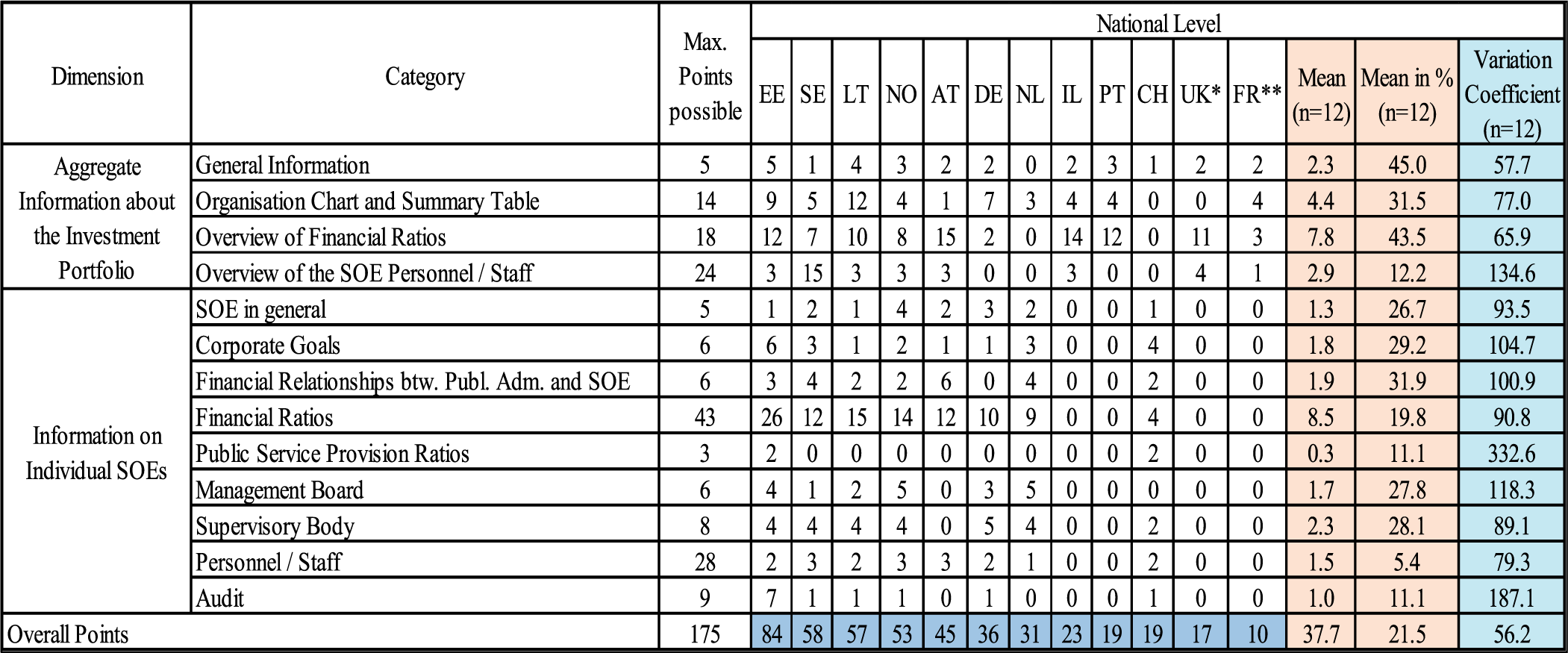

Overview of the quality scores of AHRs.

Notes: AT – Austria; CH – Switzerland; DE – Germany; EE – Estonia; FR – France; IL – Israel; LT – Lithuania; NL – Netherlands; NO – Norway; PT – Portugal; SE – Sweden; UK – United Kingdom. No AHRs could be identified for Australia, Belgium, Greece, Spain and the US. * For UK: whole-of-government accounts. ** For France: government as shareholder report.

A criterion was coded as ‘fulfilled’ if at least 70% of the respective SOEs within an AHR fulfilled this criterion. This limit of 70% was both necessary and useful. For instance, if information on one criterion was missing for only one of 30 SOEs, this single SOE should not be decisive in the quality assessment of the whole AHR concerning this criterion. The limit of 70% ensured that the information was available for more than half of the SOEs, but also left enough space for single SOEs that were in the AHR without information.

All criteria have been derived from theoretical and practical requirements. The importance of a single criterion depends on the information purpose and perspective of different user groups. For this reason, all criteria are treated equally important. Therefore, this study uses an unweighted disclosure index approach and scores the criteria on a dichotomous basis (1 point if criterion is fulfilled; no point if criterion is not fulfilled).

In the model, not all categories contain the same number of criteria for the following reasons. An analysis of the scientific literature and discussions in the administrative and political spheres shows that there are many more requirements and demands for the theme of some categories than for other categories (Bruton et al., 2015; OECD, 2015; Whincop, 2005). This should also be represented by the number of criteria in the different categories. Furthermore, the model enables differentiated category analysis according to the information needs and aims of different user groups. For example, users who look at which service needs are fulfilled by SOEs or could be provided by private actors or if the same service is provided several times by different companies might put different emphasis on individual criteria and categories than users with a focus on national debt or gender equality.

In the study, the quality model is used to assess the quality of publicly available AHRs in Australia, Austria, Belgium, Germany, Greece, Estonia, France, Israel, Lithuania, Netherlands, Norway, Portugal, Spain, Sweden, Switzerland, the UK and the US. The sample is composed according to older and newer OECD and EU membership and complemented by the US and Australia as model and reform pioneers. Moreover, the sample considers the reform or development state of the respective public administrations to allow for the benchmarking of relevant public administrations with a long tradition and newer ones. The focus is on the national level since the national government has a special responsibility in this field and can in some countries be seen as a role model for other government levels. Furthermore, in an international comparative study with many countries, government structures and responsibilities, as well as the structures of national reporting systems on SOEs, are more comparable at the national level than at the local or regional level.

The AHRs are identified on the webpage of the coordinating public administration. In case no English reports are available, reports in the native language are analysed with the help of native speakers. If no AHR could be identified, the public administrations were contacted in order to receive the documents. The study also examines if there are laws or soft laws such as public corporate governance codes (PCGCs) that demand the publishing of an AHR (German Federation, 2009; Grossi et al., 2015; OECD, 2015; Tricker, 2012).

Empirical results

For 12 of the 17 analysed countries, AHRs are available on the public administration websites. In many cases, not only the current, but also the reports of previous years, are accessible (e.g. Israel, Norway and Portugal).

Regarding the quality of AHRs, the results of the 12 available AHRs differ between 10 and 84 out of 175 possible points, with a mean of 37.7 (standard deviation of 21.2) (see Table 1). Even though none of the reports reaches the full overall score, in some categories, such as corporate goals, financial relationships between public administrations and SOEs, and the management board, some reports fulfil most criteria. Overall, financial information is disclosed best, especially in the AHR of Estonia, which reaches 26 out of 43 points here. Information on SOE personnel is disclosed least; some AHRs get 0 points in both dimensions. Among the sample, very low fulfilment rates are reached in the category audit (11.1%) and public service provision ratios (11.1%). However, there is great discrepancy in the quality of AHRs concerning information on personnel, public service provision and audit. Eastern European and Scandinavian countries have the most points and Central European countries such as the UK and France obtain the lowest scores. Some reports (Portugal, Israel and the UK) strongly concentrate on aggregate (financial) information and score comparatively well here, whereas information on individual SOEs is completely missing.

In most AHRs, the emphasis is clearly on financial figures. Often, the AHR lacked the comparison of ratios and indicators over time (e.g. Estonia, Switzerland). Table 1 also provides more insight into good practice examples in different categories. Exemplary quality in the category ‘Management board’ is in the AHRs of Norway and the Netherlands, and for ‘Public service provision ratios’ in the Estonian and Swiss reports. Various AHRs offer rewarding approaches in different categories, such as the AHRs of Sweden and the Netherlands, which contain company-specific sustainability standards and initiatives that have been put in concrete terms and adjusted from general EU but also global reporting initiative (GRI) requirements. Similar good example tendencies are the portrayal of privatisation projects (Israel), owner goals (Switzerland), gender aspects and comparisons (Sweden), and state grants (Portugal). Each criterion has at least been reported once in the sample, which underlines the feasibility of the quality model.

Laws for preparing and publishing AHRs could only be found for Austria, Israel and Sweden. PCGCs that recommend AHRs could only be found for Germany and Norway.

Discussion

Regarding diffusion, five out of 17 countries do not publish AHRs, which shows that requirements to publish an AHR are not yet met in several cases. Among those five countries are Spain and Greece, which have been facing serious national debt crises and discussions about privatisation recently. However, especially for countries with great national debt and cutback debates, an AHR would be important to obtain a better overall view on debts and the performance of a public authority. For differences in GDP and population size, there is no clear pattern concerning AHR quality.

The recommendations regarding AHR by the OECD and other organisations are, in most countries, not yet adequately implemented in national laws. Among the sample, countries with respective laws publish AHRs more often. However, since there are also AHRs in countries without legal obligations (Estonia, Lithuania, Norway and Germany) that reach comparable higher quality scores, laws do not in all cases seem to be a necessary factor for the diffusion of AHRs, but support the realisation of formulated transparency aims.

Regarding the quality of AHRs, in the perspective of agency theory, the findings show that, in particular, neuralgic information asymmetries are not sufficiently reduced in many countries. In many cases, it is not suitably possible for the principals to observe the action of the agents with information in the AHRs. Also, some principals in the multistage principal–agent chain do not act according to agency theory requirements concerning information disclosure. With respect to stewardship theory, the public administrations often do not make use of the chance to develop trust in important fields. Regarding property rights theory, AHRs do not sufficiently inform as to which actors have which property rights. According to stakeholder theory, the information rights of relevant stakeholders are not adequately implemented. As current AHRs have a strong focus on providing financial figures and only disclose little information on public service provision and outcome goals, they do not yet make use of the potential of AHRs to contribute to outcome orientation (Proeller, 2007; Schedler and Proeller, 2010).

Looking at the overall quality scores, diverse structures and focuses of AHRs, there is no isomorphism between the reports. However, regarding the results of individual categories, there are some common patterns. This is most obvious for financial figures, which have been reported comparably better and more homogeneously. There is also resemblance in the non-reporting of criteria, especially for the public service provision ratios, audit and personnel information of individual SOEs. Coercive isomorphism might be one explanation for the comparably good results in the AHRs of Estonia and Lithuania. Political and legislative pressure might arise from complying with high direct and indirect requirements for Estonia regarding the entry into the EU or OECD for Lithuania.

Regarding potential determinants on the quality of AHRs, the quality differs between countries with different national debt but there is no clear pattern for differences in GDP and population size. Countries in the sample with only little debt per capita, such as Estonia, Lithuania and Sweden, publish better reports.

Some limitations of the study have to be taken into account. Even though the analysis of 12 AHRs already provides structural findings, many countries where AHRs could be different are not included in the sample. Furthermore, the aim and design of this study and the results do not allow for more detailed insights on the determinants of the quality of AHRs.

Conclusions

Despite these limitations, the study provides a model for assessing the quality of AHRs as a conceptual contribution, as well as empirical evidence on the diffusion and quality of AHRs at the national level in 12 countries. Overall, despite individual examples that are worth following, the findings show that, in many cases, public administrations do not meet the derived requirements. Administrations, citizens, politicians and other relevant stakeholders often cannot get the necessary and important overall view on SOEs that is crucial for prioritising and improving decisions about the sustainable provision of public services and for cutback management. However, existing good practice examples enable bench-learning and could give support to actors engaged in pushing for improvements.

For the scientific debate on sustainable public service provision, austerity, debts and cutback management, the study provides a concrete model for assessing AHRs and opportunities for future research on the issues of the model categories. For instance, the category ‘Audit’ consists of crucial information that could be used for research on this specific theme.

For policymakers at the national and international levels, the results indicate that they should put more efforts into the diffusion and quality of AHRs. The results show that laws are necessary to ensure the diffusion and quality of AHRs. Researchers and policymakers should analyse how laws could be designed in order to increase the diffusion and quality of AHRs.

Future studies should analyse determinants for the diffusion, quality and isomorphism/variation of AHRs in more detail. Longitudinal studies would help to understand more about the development, underlying motives and drivers for implementing AHRs. Studies should also investigate more countries and the local level for an even broader international comparison.

For some countries with high scores, such as Lithuania, Estonia and Sweden, it would be enriching for reforms in other countries to analyse how it was possible to publish AHRs with comparable high quality. Furthermore, it should be analysed how different decision-makers and stakeholder groups use AHRs and if the preparation processes and/or the publication of the reports change the awareness and action of decision-makers and citizens. Clearing the fog for an overall view on SOEs and core administration with high-quality AHRs is relevant for the ‘big issues’ of public administration, public management and public policymaking.

Footnotes

Funding

This research received no specific grant from any funding agency in the public, commercial or not-for-profit sectors.