Abstract

Patrons of think tanks—for example, governments, corporations, philanthropists, NGOs, and so forth—may control think tanks’ boards, that is, their highest decision-making body. Whether patrons are likely to control boards is a question that remains under-explored and under-theorised in public administration and governance scholarship. It is posited that patrons are likely to control boards when the marginal benefit of partaking in decision-making does not exceed the cost of information transfer. The comparative examination of International Relations think tanks’ statutes shows that patron control is substantial. However, patronage does not always guarantee board control. Patron control is moderated by the nature of the transaction. The conclusion assesses patron control concerning decision-making processes in the think tank and the idiosyncratic character of policy advice.

Points for practitioners

Practitioners can assess events of goal displacement in think tanks by learning about mechanisms that facilitate or hinder patron control over think tanks. Laying out the conditions under which patrons exercise control, the latter turns out to be substantial despite not all patrons having control over think tank boards. Patron control is shown to depend on the position of stakeholders in the decision-making chain and the nonlinear relation between effort and influence in policy advice.

Introduction

In 2016, the International Institute for Strategic Studies (IISS) made headlines after receiving significant funding from Bahrein's royal family (Evans, 2016). The funding, which was supposed to remain secret, was reportedly destined to organise conferences that prominent politicians attended to discuss regional issues. That year also marked public awareness of think tank funding by foreign governments and private interests in many countries (Bruckner, 2017; de Haldevang, 2019; Lipton and Williams, 2016; Toosi, 2020).

This situation points to a fundamental question about public policy: namely, whose interests are represented by the organisations supplying policy advice? That question, we argue, underlines the importance of studying the governance of think tanks, that is, decision-making structures that establish internal control processes and external commitments that shape stakeholder control, or its lack thereof.

We propose that an examination of patron control over decision-making reveals the terms of the relationship between think tanks and patrons, that is, the degree of authority exercised by founders, members, and donors on think tank boards. Boards are the central decision-making body, as established in the statutes of think tanks. They set the direction of the organisation and outline the rules for the appointment of board members. The statutes establish who has the right to a seat on the board and who has the right to appoint directors. Consequently, the statutes determine the terms of patron control (Leardini et al., 2017).

The IISS, for example, is currently governed by a board of 10 trustees and its board is self-perpetuating, that is, no other entity but the trustees has the right to appoint incoming trustees. The board's term of service lasts three years, although it can be extended exceptionally upon request by the Chair or by a majority of trustees. The lack of a body to oversee the actions of non-profit boards, similar to annual shareholder meetings in corporations, increases the risk of collusion and expropriation of patrons (Fama and Jensen, 1983b). Rules such as qualifications for the post, conflict of interest, board proceedings, liability, audit, and board tenure—some of which are covered by the IISS Articles of Association—help to temper this risk. The example of the IISS board suggests, however, that patron control over think tank decision-making is weak.

The incentives of patron control are mitigated by the non-distribution constraint, that is, profit cannot be distributed but must be reinvested or donated (Hansmann, 1980). Since patrons contract think tank services, these organisations are operated ‘on behalf of’ patrons (Hansmann, 1980: 230). Patrons are not the ‘owners’ of think tanks in the corporate sense. As long as the non-distribution constraint applies, non-profits are ownerless organisations (Hansmann, 2013). However, extant scholarship argues that patrons occupying board seats may signal their commitment to putting patron donations to good use (Glaeser and Shleifer, 2001).

The policy advisory systems scholarship has addressed the question by studying government control as the distribution of authority among government bodies, where policy advisors enjoy less autonomy the closer they are to the government (Halligan, 1998). Craft and Howlett (2012: 85) contend that this view fails to account for the transformation of ‘policy-making circumstances to a more fluid, pluralised and polycentric advice-giving reality’. Accordingly, we argue that the problem may lie in the neglect of the mechanisms governing the relations with stakeholders, not only the government.

Accounting for patron control begins at the mesocosm—that is, the organisation level—where lie the internal mechanisms governing the organisation's priorities concerning stakeholders’ preferences (Figure 1). Examining these internal mechanisms helps anchor hypotheses about control to evidence related to policy advisory systems, epistemic communities, and advocacy coalitions.

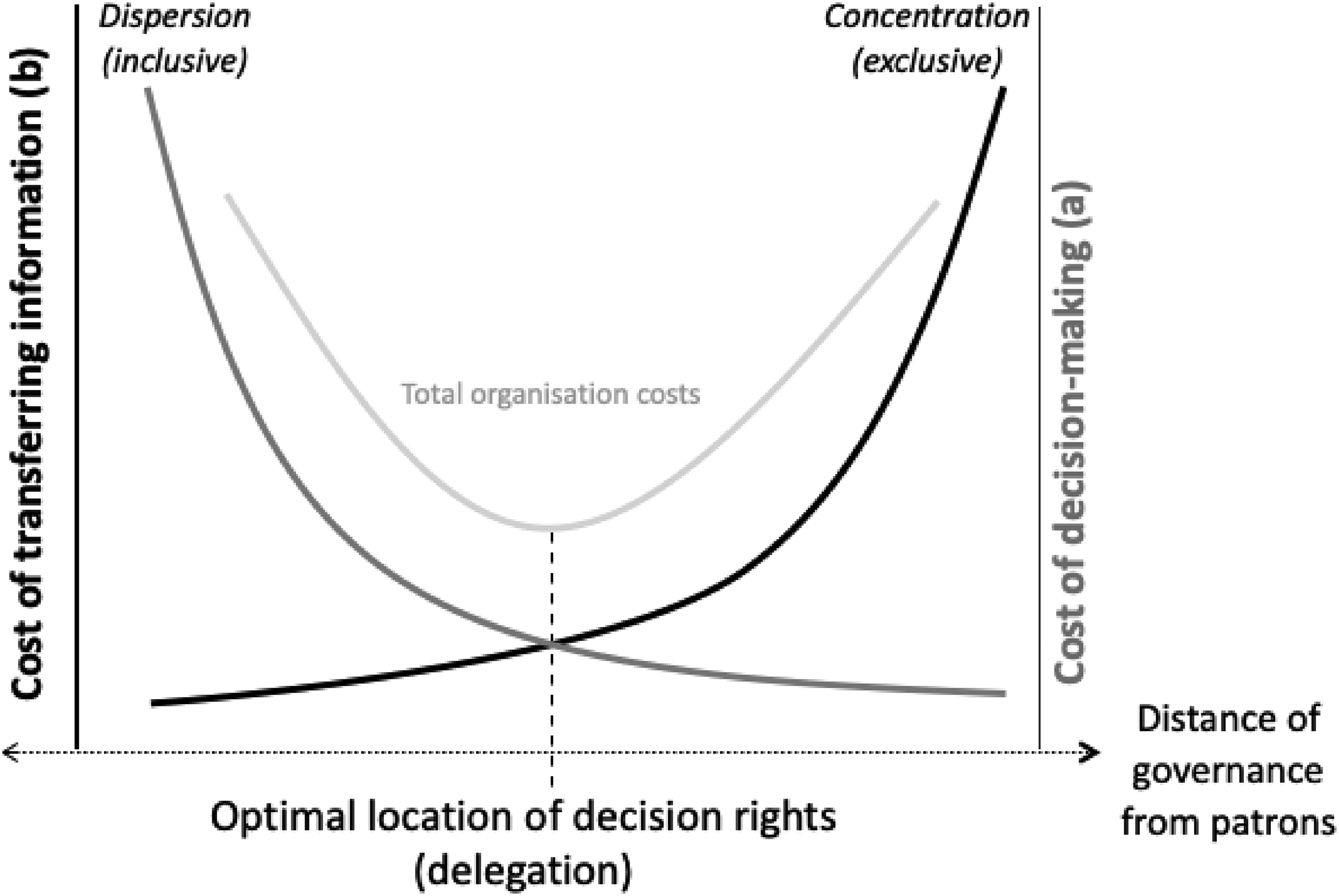

Patron control represented as the cost of decision-making and the cost of information.

We posit that board allocation of authority is a function of both the cost of transferring information (Jensen and Meckling, 1998) and the cost of decision making (Buchanan and Tullock, 1999). This arguably determines how much effort a patron, such as Bahrein's royal family or Whitbread, is willing to spend in analysing information and attending board assemblies of think tanks (Evans, 2016; Gornall, 2019). As will be expounded in the first section, for a given patron there is a point at which the marginal benefit of participating in decision-making does not exceed the marginal cost of gathering and analysing information, that is, the point where a given patron is willing to take part in decision-making. Thus, our research sheds light on the patterns of patron control of think tanks.

The second section describes the analysis of European International Relations (IR) think tanks. The analysis draws on data obtained from the statutes and from which we constructed two indexes to examine patron control: one for board appointment and one for board composition. This is complemented with a comparative analysis of two organisational traits: membership and non-membership (associations and foundations), and government-affiliated organisations.

In the third section, differences in patron control are assessed, showing that founders and members are patrons with substantial control, while donor control is weak. The article concludes with a discussion of the implications for the policy advice industry and further research.

The logic of decision making

The cost of ownership consists of the cost of risk bearing and the cost of exercising control over management and decision making (Hansmann, 1980). The second is a function of both (a) the cost of managing information and (b) the cost of the process of reaching an agreement (Buchanan and Tullock, 1999; Hansmann, 1980) (Figure 1).

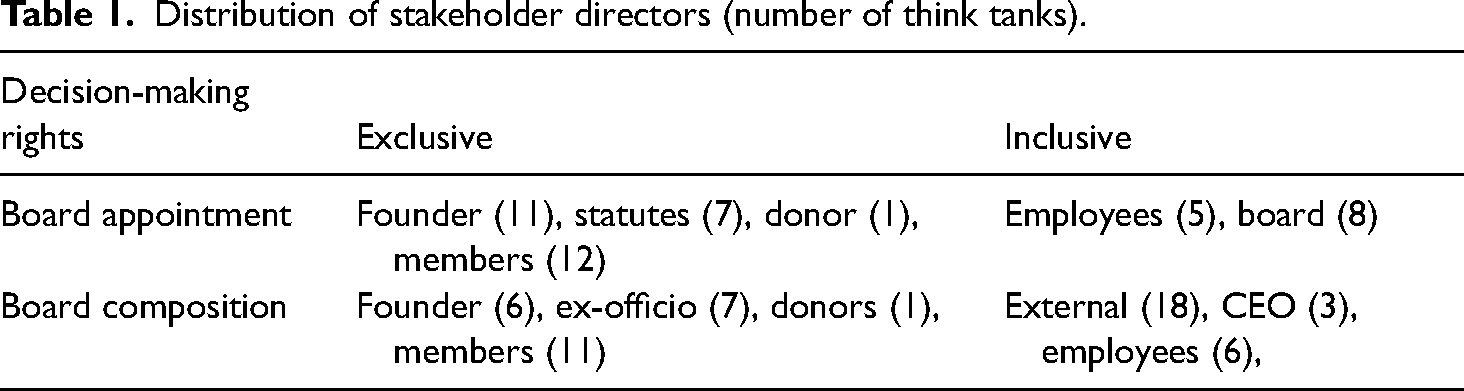

The management of information ((a), in Figure 1) amounts to the effort of gathering and processing information to make reliable decisions about the operation of the organisation (Hansmann, 2013; Jensen and Meckling, 1998). The limits to gathering and processing information are set by uncertainty, bounded rationality, and costly specific knowledge. Therefore, the likelihood of making an informed decision that considers stakeholder preferences diminishes as governance grows exclusive, because of the increased difficulty for directors to gather and process information. Thus, a limited number of interests are salient in decision-making. As patrons are likely to appoint directors who represent their interests, the cost of information is examined as the degree of patron control of the appointment of directors (Table 1).

Distribution of stakeholder directors (number of think tanks).

The cost of transferring information ((b), in Figure 1) involves the effort invested in reaching an agreement (Buchanan and Tullock, 1999; Hansmann, 2013). The greater the number of decision-makers and heterogeneous interests, the higher the cost of reaching a decision. Accordingly, the advantage for any patron diminishes as governance grows inclusive and the objectives of stakeholders become progressively inconsistent. The cost of decision-making is examined as patron control of board composition, where a majority of directors representing patrons constitute an exclusive board (Table 1).

Figure 1 shows that the cost of decision-making moves slantwise, in the opposite direction to the cost of information. The intersection of the curves shows that, for any given patron, there is a point where the marginal benefit of having its interest represented does not exceed the marginal cost of information. The point in question represents the kind of governance whose cost the patron is willing to bear.

Exclusive and inclusive governance

To study the logic of decision-making, we focus on two fundamental decision-making rights coded in think tank statutes: board appointment and board composition (Table 1). Examining statutes is central to the study of patron control because, together with the law, they govern the conduct of stakeholders. Therefore, they are the basis for state supervision and legal enforcement in lawsuit filing. Scholars and practitioners would have difficulties assessing events of goal displacement without reference to the rules of governance detailed in statutes.

Board appointment establishes who has the right to appoint board directors, and board composition defines who has the right to a seat on the board, that is, to be a director. Table 1 shows the stakeholders identified in board appointment and board composition, and the following paragraphs define their role in terms of their inclusive/exclusive character (Figure 1).

Board appointment

The law usually gives founders of foundations and associations the liberty to create boards tightly controlled by themselves or boards to which significant competence is delegated. Foundational patrons have two mechanisms of board control: one is keeping a seat on the board; the second is statutorily assigning seats to entities who would guarantee that their interests are duly represented (see ‘ex-officio,’ below).

These decisions influence the preferences of incoming patrons, who will choose between committing to a think tank with a tightly/loosely controlled board or granting a restricted or an unrestricted donation. The incoming patrons will consider the transaction—that is, the service contracted—and apply the decision-making logic (Figure 1). The statutes of Elcano Royal Institute (RIE) are an example, because they grant director rights to ‘the entities that commit an economic contribution to the Foundation under the terms established for this purpose by the Board of Trustees’, namely, major incoming donors. RIE's board in 2021 had 19 directors representing major firms.

On the opposite end of patron control are self-perpetuating boards, where the governing board appoints the new directors. No other entity has the right to appoint directors and they are not necessarily inclusive. These boards would be concerned with patron interests owing to their fiduciary obligations (care, loyalty, and prudence) to the mission statutorily established by the founders (Hopt and von Hippel, 2010). However, boards may develop their own idiosyncrasy at the expense of patrons (Hansmann, 1980; Jensen and Meckling, 1998; Van Puyvelde, 2016). Because we focus on patron control of board appointments and seats, self-perpetuating boards are not included in the exclusive side of control in Table 1, notwithstanding their exclusive mode of governance (Jensen and Meckling, 1998).

Finally, employee appointment of directors, called co-determination, has been adopted in European corporate law and became a practice in some non-profits (Hopt and von Hippel, 2010). Granting appointment rights to employees drives the governance of the organisation away from the right axis, because employees are likely to offer boards details about the operation of the organisation, which helps to counterbalance patron bias (see below).

Board composition

Patron presence on boards may signal to other patrons that their interests are duly represented (Fama and Jensen, 1983b; Ostrower and Stone, 2006). This has to do with the public-good character of monitoring, although the larger the number of patrons, the more likely patrons will free-ride on their efforts to monitor (Hansmann, 1980). In addition, the continued presence of patrons on boards guarantees a stable income for the organisation (Selee, 2013).

A director may be appointed by virtue of the position occupied somewhere else, called ex-officio, rather than the director's credentials as an individual (see external directors). For instance, the think tank Stiftung Wissenschaft und Politik (SWP) statutorily establishes that the Head of the Federal Chancellery must occupy the seat of President or Deputy President on the board. Here, ex-officio directors are those external directors with voting rights assigned by virtue of the position they occupy somewhere else.

Figure 1 establishes that, as governance moves to the left, patrons defer decision rights to directors who efficiently manage key information, for example, external directors. To guarantee that conflicts of interest are suitably managed, external directors are nowadays frequently required in corporate law and stock exchanges where criteria of independence have been established. External directors guarantee that sensitive tasks such as audits, compensation, and nomination can be handled autonomously. However, this trend has been questioned, as it emphasises expertise for the task, rather than knowledge of the line of business, and thus it may ultimately run against board duties to steer the business (Brody, 2010; Cornforth, 2003).

Requirements for external directors in non-profit law are largely absent for the reason that the qualification of independence escapes definition, and there is no market for external directors. External directors may be hard to attract towards non-profit boards, since they work without remuneration and scantily perceive low-powered incentives. Therefore, the implementation of burdensome requisites to qualify external directors may leave boardrooms empty (Brody, 2010). While it is accepted that the absence of executive duties in the organisation is a fundamental requisite for external directors, the skills and representative qualities required remain undefined. Consequently, the qualification for external directors rests in the hands of the organisation (Brown, 2020; Ostrower and Stone, 2010), and is vaguely incorporated in the statutes, if it is included at all.

For instance, the statutes of the Barcelona Center for International Affairs (CIDOB) establish that, in addition to six ex-officio directors, the board is ‘formed of natural and legal persons’. The statutes of the Hellenic Foundation for European and Foreign Policy (ELIAMEP) establish that directors must represent ‘academic, diplomatic, military, business and journalistic sectors’.

The control function in non-profits, embodied by the board, is separated from the management function, embodied by the CEO. Thus, the control consists of monitoring management, which takes risks on behalf of the principal (Fama and Jensen, 1983b). The separation of both functions constitutes an essential mechanism for the survival of non-profits because it guarantees that profit is not siphoned away from its intended purpose. Furthermore, the non-distribution constraint is considered a check on opportunistic behaviour from management (Fama and Jensen, 1983b).

Although CEO directors would be unconventional because stakeholders internal to the organisation increase the risk of collusion and expropriation (Fama and Jensen, 1983a; Hopt, 2010), they can align with patron interests and provide insight into the operation of the think tank (Fama and Jensen, 1983b; Glaeser and Shleifer, 2001). Which of these paths CEOs take throughout the lifespan of a think tank is an unpredictable matter, but since the costs of misconduct are non-negligible, CEOs may often sit on the inclusive side of Table 1.

In labor-intensive non-profits like think tanks, employees have an informational advantage in the operation of the organisation that can be brought to bear in board decision-making. However, employees perform a job that is difficult to monitor, which increases the risk of expropriation (Fama and Jensen, 1983a; Glaeser and Shleifer, 2001; Hansmann, 1980). For instance, in France, the employees of non-profits can be directors but cannot hold the posts of president, vice-president, secretary-general, or treasurer (Deckert, 2010). Either offering insight into the operation of the organisation or counterbalancing patron control, employee directors on boards would be a sign of inclusive governance worth accounting for, since it would be rather exceptional among non-profits (Fama and Jensen, 1983b; Hansmann, 2013; Hopt, 2010).

Data and methods: comparing boards

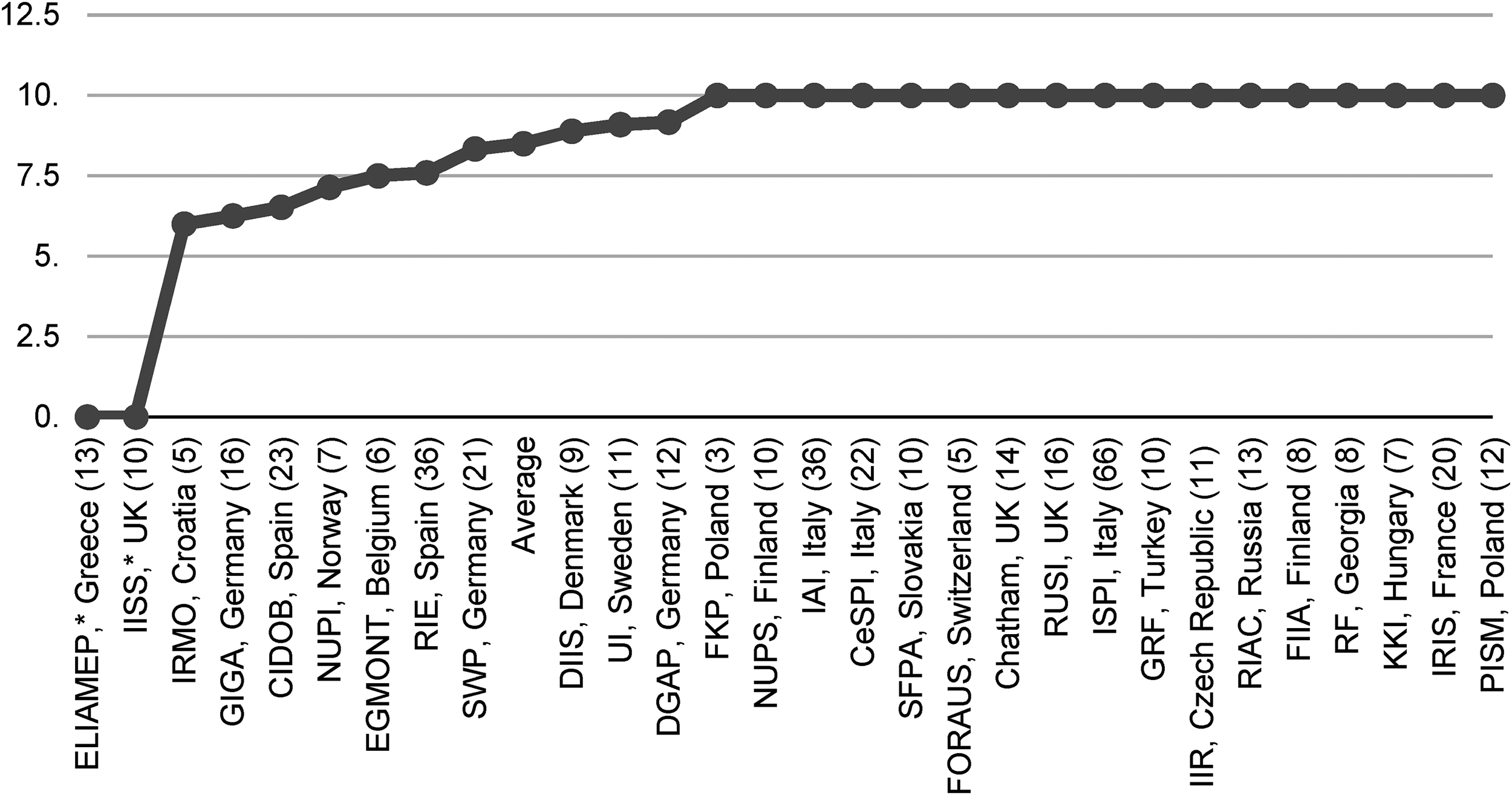

In March 2021, our online search of IR think tanks in Europe produced a list of 43 organisations in 28 countries. Because think tanks seldom publish their statutes on their websites, we contacted the organisations requesting the documents and collected the statutes of 29 think tanks in 20 countries, that is, close to two-thirds of the IR think tanks in Europe (Figure 2). The data collected from the statutes have been contrasted with additional sources such as national regulations, board minutes, annual reports, and think tank websites. The sample represents one-third of the 89 IR think tanks in 53 countries worldwide estimated in our search.

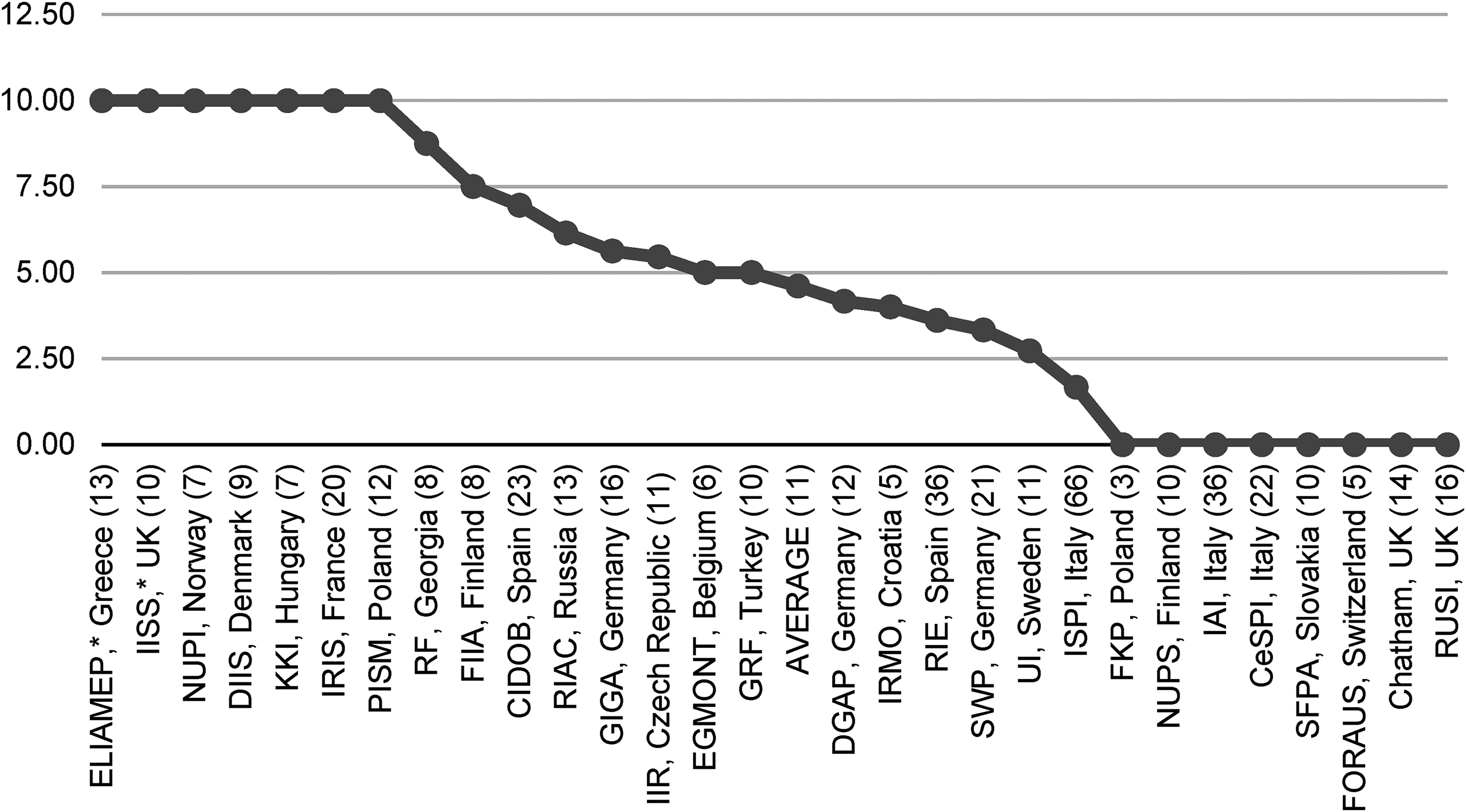

Appointment: average share of seats appointed by patrons, 10 most exclusive (directors in 2021). *Self-perpetuating boards.

The study focuses on IR think tanks because the data-intensive quality of statutes requires a manageable sample. Virtually any think tank may address international issues, but the sample collects the rather classic form of IR think tanks (Stone, 2021). IR think tanks are among the earliest to arrive on the policy advice scene (Parmar and Yin, 2021; Roberts, 2015). Some have been operating for a century, such as the Royal United Services Institute (RUSI), the Royal Institute of International Affairs (Chatham), and the Institute for International Political Studies (ISPI), created in 1831, 1920, and 1934, respectively. Others have recently arrived, such as the Global Relations Forum (GRF), the Russian International Affairs Council (RIAC), and the New Foreign policy Society (NUPS), created in 2009, 2011, and 2021, respectively. Overall, the think tanks in the sample encompass several historical waves and forms of operation (Abelson, 2019; Roberts, 2015).

The examination of the statutes focused on four variables. First, six dichotomous items identify the stakeholders with the statutory right to appoint the board (board appointment): founder, member, donor, statute, board, and employee (Table 1). Second, seven continuous items identified the number of stakeholders with a statutory right to a seat in the board (board composition): founder, member, donor, CEO, ex-officio, employee, and external (Table 1).

To conduct a comparative analysis following the logic expressed in Figure 1, we created a score of patron control. On a 0–10 scale, 10 represents high exclusiveness of board appointment (right axis in Figure 1) and high inclusiveness of board composition (left axis in Figure 1). The inversion of scales for board appointment and board composition facilitates superposing on and comparing with the curves in Figure 1. A 0–10 scale has been selected because it is concise and close to the median number of directors in the sample (11 is the median and 15 is the average), which corresponds with most non-profits (BoardSource, 2010; Ostrower and Stone, 2006). The think tank with the smallest board is the Casimir Pulaski Foundation (FKP) with three directors, and the largest is the Institute for International Political Studies (ISPI), a membership organisation with 66 directors.

Board composition is a continuous variable that records the number of directors corresponding to the categories of founder, member, donor, CEO, ex-officio, employee, and external. The data were represented in a 0–10 score that shows the share of seats not allocated to patrons.

The score of control of appointment was calculated in three steps. First, the seats held by patrons and their representatives were calculated as a share, similar to the control board composition. Second, patrons’ disposition of forgoing appointment rights was calculated as a division of the share of inclusive seats by the number of stakeholders with appointment rights (founder, member, donor, board, and employee). Third, a 0–10 score representing patron control of appointment results from the sum of the first two steps. The stakeholders with appointment rights were recorded as a dichotomous item, indicating whether the type of patron has appointment rights. It is questionable whether continuous data would have produced more accurate results, since they tend to be incommensurable—for example, the board of the Finnish Institute of International Affairs (FIIA) is appointed by the Finnish Parliament with 199 elected members, while the board of the Rondelli Foundation (RF) is appointed by one founder.

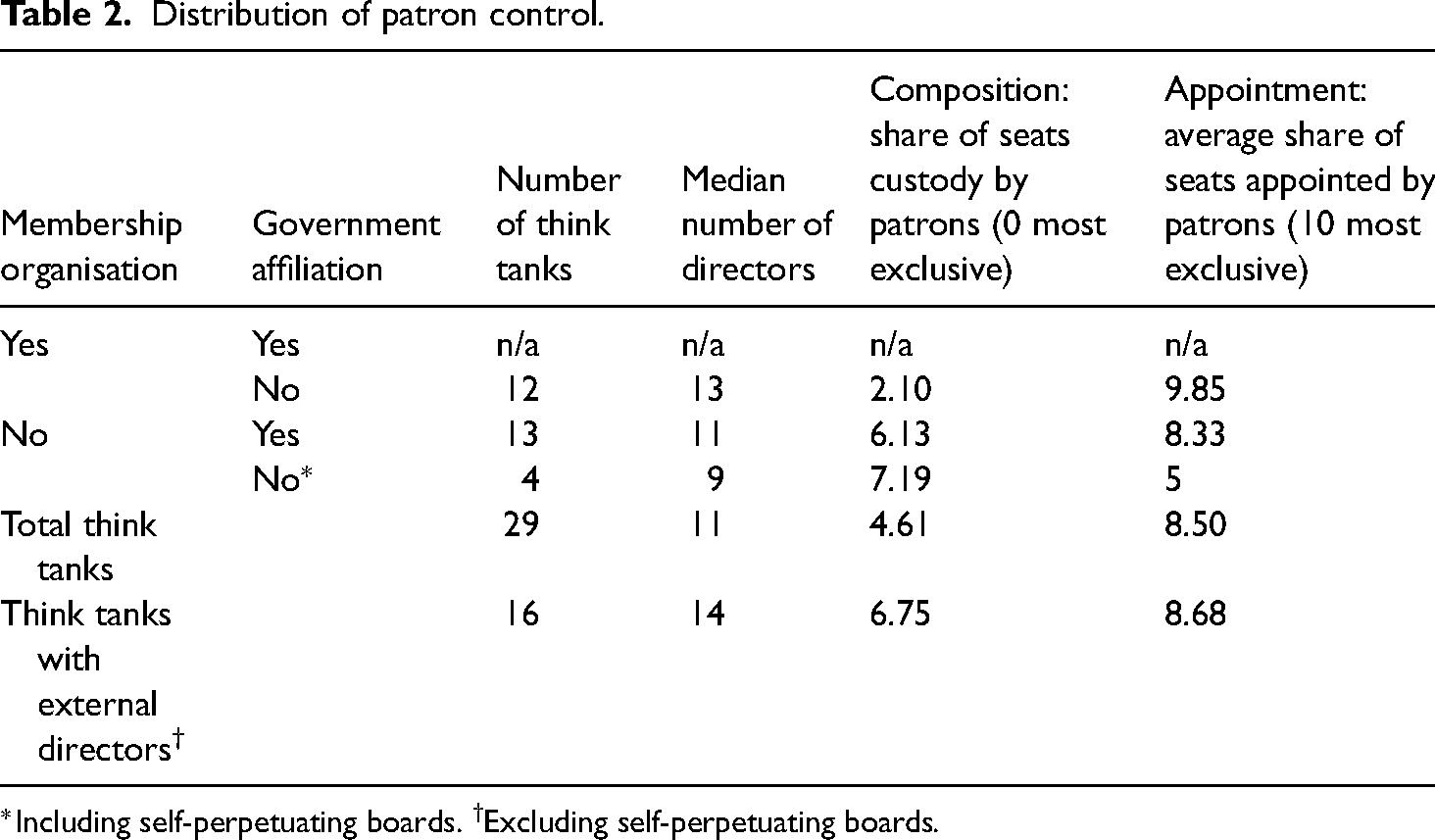

We also sought to identify patterns of patron control for two organisation traits. First, public debates on patron control of think tanks have emphasised the role of governments and private entities (Baertl, 2019; Lah, 2017; McLevey, 2014). Therefore, we identified 13 organisations affiliated with governments, that is, think tanks where the government had a statutory role in the decision-making rights examined (Table 2).

Distribution of patron control.

*Including self-perpetuating boards. †Excluding self-perpetuating boards.

Second, we identified 12 think tanks statutorily structured around membership where the statutes establish that the general assembly of members is the main decision-making body (on foundations and associations, see Hopt and von Hippel, 2010; Van Puyvelde, 2016; Van Puyvelde et al., 2016). It is necessary to consider whether associations follow a distinct pattern of control because they operate under the logic of mutual benefit, that is, all members are involved in achieving a common goal. However, a large membership may be inclined to free-ride on their efforts to monitor or even defer decision-making rights (Thomsen, 2014).

Results and discussion

The prevalence of patron control of board appointments suggests that the matter requires more attention from scholars. Figure 2 shows that patrons find the marginal benefit of participating in decision-making exceeds the marginal cost of gathering and analysing information. In other words, patron control of board appointments remains close to the exclusive axis in Figure 1, as patrons hold an exclusive right of appointment in 17 think tanks and are the principal stakeholder with voting rights in the remaining 10 think tanks.

Only two think tanks rely on self-perpetuating boards: ELIAMEP and IISS. These results diverge from the scholarship, which has only made a passing observation that patron appointment is associated with boards’ predisposition toward goal alignment (Ostrower and Stone, 2006) and has mostly conjectured that self-perpetuating boards would prevail in non-profits (Fama and Jensen, 1983a; Hopt and von Hippel, 2010; Thomsen, 2014; Van Puyvelde, 2016).

Because associations are by law allowed to statutorily cede the control of appointment to another body than the general assembly—for example, the board (Hopt, 2010)—the strong control of appointment observed in the sample is hardly tautological. The prevalence of members in board composition may be characteristic of small membership organisations (compared, for instance, with political parties, labour unions, or international associations), where there is close identification with mutual, attainable benefits, and management is separated and professionalised (Thomsen, 2014; Van Puyvelde et al., 2016). Nevertheless, how such control is exercised deserves research. Consider the 288 members of NUPS in early 2021 (its website states), who keep exclusive control of appointments. Given the public-good character of board oversight, it is worth studying patrons’ disposition to free ride.

The remarkable control by members and the absence of donors found in the results (Table 1) show the advantages of an organisational examination of the distribution of control among stakeholders. The comparison among patrons—that is, founders, members, and donors—elucidates the heterogeneity of a stakeholder class and indicates how their stakes are managed through different mechanisms. Therefore, an organisational analysis addresses questions about the variability in stakeholder salience and impact (Fassin, 2009) and caters to the puzzle-solving needs of scholars and practitioners assessing events where goal alignment seems displaced (Bruckner, 2017; de Haldevang, 2019; Evans, 2016).

Finally, the extension of co-determination to non-profits and government inclusion of employees to demonstrate accountability (Harrow and Phillips, 2013; Phillips and Smith, 2011) must be surveyed, since four out of five think tanks granting appointment rights to employees are government-affiliated: the Institute for Development and International Relations (IRMO), the Institute for International Relations (IIR), the Danish Institute for International Studies (DIIS), and the Norwegian Institute of International Affairs (NUPI).

The board composition scores in Figure 3 show dispersion, although Table 2 suggests that patrons of foundations find the marginal benefit of participating in decision-making exceeds the marginal cost of gathering and analysing information, that is, these tilt to the middle-right in Figure 1. These results do not follow studies observing that large boards of sizeable wealthy non-profits tend to include different constituencies (Brown, 2020; Ostrower and Stone, 2006).

Composition: share of seats custody by patrons, 0 most exclusive (directors in 2021). *Self-perpetuating boards.

While external directors constitute at least half of the board in 13 think tanks, the right of appointment of 10 of those boards rests exclusively in patrons’ hands. Moreover, the think tanks with the most inclusive scores of appointment are not unambiguously among the think tanks with the most inclusive board composition. Therefore, the question of board inclusiveness must be considered in light of the qualification of external directors.

Consider the board of RIE, with ex-officio, donor directors, and external directors, all with appointment rights. In 2021, the external directors consisted of four former Prime Ministers, three former chairmen of the institute, one academic, one member of the opposition party in the Parliament, one former Minister of Foreign Affairs, and a former representative for the Ibero-American General Secretariat. It appears that the external directors represent stakes different than ex-officio and donor directors. The same trend applies to, for example, FIIA, the Barcelona Center for International Affairs (CIDOB), DIIS, the Institute de relations internationales et stratégiques (IRIS), and the Russian International Affairs Council (RIAC). Whether patrons are strategic in these appointments can be only addressed through an individual examination of conflicts of interest, loyalty, and motives.

Meanwhile, the self-perpetuating boards in the sample seem the most professionalised. IISS's board comprises one scholar, two media managers, and seven members with corporate affiliations and expertise in investment management. ELIAMEP's board comprises three academics, one lawyer, one CSR expert, five business executives, one corporate advisor, and one former high official in the IR field.

The expected exclusion of the CEO with voting rights on the board is adopted in most of the statutes, but further research must verify whether this implies board-dominant governance (Cornforth, 2003; Ostrower and Stone, 2006, 2010).

Finally, the government-affiliated trait leaves unanswered the question of whether governments create more inclusive boards (Harrow and Phillips, 2013; Phillips and Smith, 2011) or more exclusive boards (Guo, 2007). Systematic research is necessary, as the results suggest that the organisational form has more bearing than the government–private character of patrons (Table 2).

Conclusion

Every year, newspapers publish stories of private and public, foreign and national interests supporting think tanks in exchange for influence in policy-making. These transactions deserve consideration given think tanks’ commitments to different stakeholders.

The control of patrons begins at the apex of the organisation, namely, the board. When patrons contract think tanks, they must decide the costs of decision-making that they are willing to bear. The costs of decision-making are a function of both the costs of managing information and the costs incurred in the process of reaching an agreement.

We have examined patron control of the boards of 29 European IR think tanks, where patron control is defined as the magnitude of patron forgoing of decision-making rights, namely, control over the appointment of directors and the control of seats in the board.

The results raise questions and invite further research on modes of patron control across countries and fields—for example, security, technology, and the environment—which contribute to identifying regional traits of think tanks (Abelson, 2019; Lah, 2017; Rastrick, 2021). It is also necessary to expand on statutory rules that may strengthen or weaken patron control (Leardini et al., 2017). For instance, a part of the ex-officio members of the board of Egmont is excluded from the quorum required to vote, which poses questions on goal alignment among directors.

The results show that think tank patrons expect the marginal benefit of controlling appointment rights and holding board seats to exceed the marginal cost of managing information. In other words, patron control of boards is substantial. These results divert from the premises of the scholarship except when control constitutes a consumption item of value, that is, control has utility for patrons.

The value for patrons is defined in the realm of political control. Political compromise and uncertainty incentivise political control for long-term structural gain (Moe, 2013). Uncertainty about who would control politics during the next term of office incentivises policy actors to seek policy arrangements (goal alignments) that resist control from subsequent authorities who may want later to reverse the gain.

Consider the FIIA, founded by the Finish parliament, which also exclusively controls the appointment of a board of six external directors. As stated on its website, ‘The purpose of the research carried out by the Institute is to produce focused information of a high standard for use by the academic community and decision-makers, and in public debate’. How can the Finish parliament, as patron, ensure that the institute will be steered to serve its needs for ‘focused information of a high standard’ and that it will not be co-opted by any other authority—or stakeholder, we would argue—such as the Ministry of Defense? While directors must fulfil the duty of obedience, that is, fulfil the mission statutorily established by the founders, boards are likely to develop their own idiosyncrasy the more attenuated control is. The logic of political control supports that statutory control of appointment may constitute an effective tool to guarantee that the FIIA's objectives are pursued in accordance with the intention of the parliament when it founded the think tank.

The same logic applies to NUPS, a Finnish association of which individuals and organisations can become members upon the board's approval. As long as members control the board, they can prevent a takeover by members whose goals are misaligned.

Whether patrons strategically use their appointment rights merits attention. While patrons may seek to prevent the think tank from being coopted by other stakeholders, they may also be wary of preempting the quality and utility of policy advice with undue control. As Roberts (2015: 2) has pointed out, ‘credible’ and ‘respected’ IR think tanks have become a sign ‘of a country's international standing, prestige, and soft power’, although some regimes—we would argue, some stakeholders—may give in to the temptation to overcontrol. The think tanks giving in to that temptation will show a displacement of the goals and distribution of value appropriation.

To equate patron control with control of the policy advice that think tanks supply would mean ignoring the decision-making processes across stakeholders and the sometimes-conflicting nature of those stakes (Fama and Jensen, 1983b). The board's tasks concern monitoring and ratifying management, while management's tasks concern initiating and implementing policies. While patron control may prevent the think tank from being seized by other stakeholders—for example, management, employees, transient donors, and so forth—patrons rarely possess the specific knowledge of managers as to how to run the business, not to mention the specific knowledge that experts accumulate to deliver policy advice (Struyk, 2021).

Think tanks operate in the policy advice industry, where advice ‘need[s] to be made to matter’ (Stone, 2015: 2). IR think tanks, including many in our sample, have withstood transformations in the world order that demand the reordering of agendas (Parmar and Yin, 2021; Roberts, 2015; Stone, 2021) and the emergence of new governance structures that demand the redefinition of strategies (Stone, 2015). Think tank experts’ capacity to engage with policy communities, politicians, and the public to shape, steer, and validate policy analysis has been crucial to think tank survival. Therefore, the work of the think tank expert is subject to the expectations of diverse stakeholders, including patrons, who are in a weak position to judge the quality of expert output owing to the nonlinear relationship between expert effort and influence (Abelson, 2019, 2021; Struyk, 2021).

The policy advice industry involves a vast ecology of organisations competing for strategic recognition and legitimacy of their intellectual authority (Craft and Howlett, 2012; Stone, 2015, 2021). Through think tank patronage, policy actors may seek to address legitimacy deficits of their agendas, develop the capacity to address uncharted issues, and access new policy markets (Stone, 2021). Whether the experts can successfully pursue the objectives set by patrons has less to do with patrons controlling their work than with the mobilisation of coalitions creating favourable circumstances (Parmar and Yin, 2021; Roberts, 2015; Stone, 2015).

To equate patronage with control of policy advice would mean ignoring the diversity of transactions that think tanks engage in (Hansmann, 1980, 2013) and overlooking the heterogeneity of their stakeholders with their variability in salience and impact (Fassin, 2009). While patronage has been primarily examined under the general category of donors (Baertl, 2019; McLevey, 2014; Rastrick, 2021; Van Puyvelde et al., 2016), the results open the black box of think tanks showing that patrons represent a diversified category of stakeholders whose variability in salience and impact lies in the governance of the transactions they commit.

Examining a sector largely overlooked in management research—namely, the policy advice industry—the field can capitalise on a catalogue of modes of patron control to address questions such as the re-orientation of think tank services towards advocacy (Abelson, 2019) and how the distribution of control among different patrons leads to distinctive business models of think tanks (Baertl, 2019; Lah, 2017; McLevey, 2014; Rastrick, 2021).

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data availability

The data that support the findings of this study are available from the corresponding author, Marybel Perez, upon reasonable request.