Abstract

Chief executive officers (CEOs) have a substantial influence on the decision-making processes of the top management team (TMT) and the performance of the firm in general, and this influence is particularly important in small-sized family firms. By integrating research on CEO qualities and the CEO–TMT interface to explain how they interact in ways that drive firm performance, we provide a first attempt to highlight the importance of CEO capacity to implement decisions that were made following a comprehensive process (i.e., strategic decision comprehensiveness, SDC) for the performance of small-sized family firms. In so doing, we provide a micro-foundation lens and also direct research attention to decision implementation, a key issue in the field of strategic management, which unfortunately has relatively been overlooked in the extant literature. Results of multisource survey data collected from CEOs and TMT members of 131 small-sized family firms indicate a positive interaction effect between CEO implementation capacity, the TMT SDC, and the performance of small-sized family firms.

Keywords

Introduction

Evidence suggests that strategic decisions often fail, not because of inappropriate strategy formulation, but rather because of poor implementation (e.g., Hitt et al., 2017). In addition, we know that some firms are more comprehensive in their decision-making processes than others, inclusively and exhaustively considering alternative choices (Fredrickson & Mitchell, 1984, p. 402), and the literature offers inconsistent results regarding their performance implications (Miller, 2008). Further, decision scholars have underscored the importance of studying not only how decisions are formed and made, but also how they are enacted and implemented (Dholakia & Bagozzi, 2002). Finally, scholars advocate a focus on a leader's change competency to better understand how leadership facilitates change processes (Krummaker & Vogel, 2013), and we believe that strategic choices often involve change in behaviors and actions, thus enabling a better understanding of the chief executive officers’ (CEOs) capacity to implement their strategic decisions.

Strategic leadership theorists point to the CEO–TMT (top management team) interface as a promising avenue of research that has the potential to advance theory (Cao et al., 2010; Ling et al., 2008). Specifically, this line of research links CEO managerial capacities (Carpenter et al., 2004) and the dynamics within the TMT. Here, we treat a TMT as composed of a family CEO and other executives with whom the CEO makes strategy decisions. Research on CEOs focuses on the traits and qualities that they possess (Busenbark et al., 2016) and examines whether and how certain qualities affect team- and firm-level processes and outcomes (e.g., Carmeli et al., 2011; Nadkarni & Herrmann, 2010). This is a highly “fertile (research) terrain in the organization sciences” (Hambrick et al., 2005, p. 503). Advancing this line of research on TMT dynamics, scholars advocate a focus on the social and cognitive processes within the executive team and their implications for strategic decisions and performance outcomes (e.g., Hambrick, 1998; Lubatkin et al., 2006).

This is because the focus on both the CEO and TMT dynamics helps enhance our understanding of the decision-making processes that the CEOs and their TMTs cultivate and enact to drive firm performance. In particular, research offers both negative and positive implications of strategic decision comprehensiveness (SDC) on firm performance, and has tended to reconcile these mixed results by focusing on the environmental conditions in which decision makers engage comprehensively in this decision-making process (Miller, 2008). However, micro-level (behavioral and cognitive) processes that underpin firm performance are still in the early stages of development, both theoretically and empirically (Carmeli et al., 2012). In particular, research has tended to overlook the micro-level capabilities of the CEO and specifically the CEO's capacity to implement decisions. In this research, we address a key issue concerning the capacity of CEOs effectively implement strategic decisions of the TMT, through the micro-level cognitive processes occurring in the interactions between them (Alexander, 1985; Dean & Sharfman, 1996).

We advance this contextualization by focusing on small-sized family firms. To conceptualize and define small-sized family firms here, we integrate previous conceptualizations (Anderson & Reeb, 2003; Chua et al., 1999; Villalonga & Amit, 2006) and refer to those business entities with fewer than 100 employees that are governed (controlled and/or managed) by the founders and/or member/s of their family, bonded by either blood or marriage, with the intention to endow the organization to their children in an attempt to maintain the family's name and legacy. This adds specificity to research on the ways by which decision-making processes unfold by considering the very context of these entities. First, these processes in family firms differ from those in nonfamily firms because of the dual goals, economic and noneconomic of the family firms, as well as the relationships between family members that direct the courses of action in these entities (Gómez-Mejía et al., 2011). Revealing the decision-making processes in family firms is thus a fundamental, theoretical and practical issue that can help explain various strategic choices and actions (Ensley, 2006). Studying decision-making processes in family firms is more complex not only because of their consideration of both economic and noneconomic issues (Gómez-Mejía et al., 2011), but also due to the practical difficulty of gaining access to small, privately held firms (Lubatkin et al., 2006) and especially family-owned enterprises (Kotlar et al., 2018). Second, small-sized firms suffer from a lack of formalization (Sine et al., 2006), particularly in decision-making processes (Mellahi & Wilkinson, 2004).

In an attempt to contribute to this line of research, we develop a model that examines how CEOs utilize their capacity to implement strategic decisions in ways that allow the decision-making processes in the TMT to be more fully realized, such that they positively influence the relative financial, operational, and growth performance of small-sized family firms. We capture micro-cognitive processes by considering the extent to which the TMT is comprehensive in its decision-making processes (i.e., SDC) and argue that this is a crucial, yet not sufficient, mechanism for driving firm performance (Atuahene-Gima & Li, 2004). Micro-cognitive processes are a form of microfoundations and capture the decision-making processes—how the team engages while making strategy decisions. We advance this literature by explaining why CEO implementation capacity is crucial for realizing such decision-making processes and driving firm performance. To capture the firm performance of small-sized firms, which do not make their financial reports public, we assess two key dimensions as perceived by the CEO—operational and financial performance. In so doing, we shift the focus from the firm-level processes to the micro-foundations of decision-making processes in family firms, a key advancement in this field (De Massis & Foss, 2018), and focus on the CEO as having the most influential authority in the decision-making processes in ways that enhance firm performance. This allows us to develop and examine a variance model explicating whether and why dynamics within a TMT and the CEO's implementation capacity interact to positively influence firm performance.

Theoretical Background and Research Hypotheses

Strategic Decision Making: A Micro-foundation Lens

Strategic decisions are characterized as decisions that commit substantial resources (Mintzberg et al., 1976), ones that are nonroutine and complex (Schwenk, 1988), as well as those that are unusual and all-pervading (Hickson et al., 1986) and as such affect organizational performance (Child, 1972; Finkelstein & Hambrick, 1996). Hambrick and Mason (1984) articulated the notion that an organization is a “reflection of its upper echelon”, suggesting that a firm's processes and outcomes may be, at least in part, explained by the background, values, norms, attitudes, and behaviors of its top executives (CEO and TMT members). Following this line of thinking, scholars have provided useful findings as regards the links between TMT decision processes and organizational outcomes (e.g., Boeker, 1997; Eisenhardt & Schoonhoven, 1990; Kunc & Morecroft, 2010; Pollanen et al., 2017).

In recent years, researchers have drawn on the micro-foundation movement (Felin & Foss, 2005; Felin et al., 2015) and directed increased attention to the micro-processes that underlie the strategic decision making of executives and TMTs (e.g., Carmeli et al., 2013). By micro-foundations we mean the “interactions of individuals, processes, and structures that contribute to the aggregation and emergence of the collective constructs” (Felin et al., 2012, p. 3), which we see as holding great promise for developing and advancing the theory of and research into family firms (De Massis & Foss, 2018) and strategic leadership (Carmeli et al., 2016; Friedman et al., 2016). We view the decision-making process in a TMT of family firms as a manifestation of micro-level dynamics between executive members by focusing on the strategy-making process and further integrate it with the micro-level capacity of the CEO to implement decisions. This line of research promises to advance theory on TMTs, decision-making processes, and firm outcomes (Atuahene-Gima & Li, 2004; Barrick et al., 2007; Friedman et al., 2016; Li & Hambrick, 2005; Lubatkin et al., 2006) as it is still unclear how “processes by which executive profiles are converted into strategic choices” (e.g., Hambrick, 2007, p. 337), or why these choices are pursued and how “team inputs are transformed into outcomes” (Mathieu et al., 2008, p. 412). Furthermore, with its micro-foundation lens a multilevel perspective burgeons research that captures the individual leader's capacities and their influence on these team-level processes. Our focus here is on the capacity of the CEO to implement strategic decisions. Such a focus is important because it remains unclear why in some small-sized firms, CEOs are more capable than others of realizing the decision-making processes in a TMT in general, and in small-sized family firms in particular. This is because CEOs in family firms, particularly in small-sized ones, have greater managerial discretion, and are thus in a position to influence the decision making (Mitchell et al., 2009). An emphasis on the CEO's capacity rather than the TMT level is suitable because of the CEO's centrality in the context of small-sized family firms (Brockmann & Simmonds, 1997; Jennings & Beaver, 1995). Specifically, in small-sized family firms managerial decision-making processes are often characterized by “highly personalized preferences, prejudices and attitudes” and their success is highly dependent on the manager's ability to implement (Jennings & Beaver, 1995).

We start out by theorizing about the essence of being comprehensive in the strategic decision-making process and the implications for firm performance, following with a discussion on the importance of CEOs with the capacity for implementation.

SDC and Firm Performance

SDC refers to the “extent to which firms attempt to be exhaustive or inclusive in making and integrating strategic decisions” (Fredrickson & Mitchell, 1984, p. 402). A comprehensive approach to strategic decision making is likely to improve effective organizational decisions and subsequent organizational performance (Dean & Sharfman, 1996; Forbes, 2007; Miller, 2008). Thus, it is important to understand how strategic decision processes materialize.

A TMT that is characterized by SDC is “inclusive in making and integrating strategic decisions” (Fredrickson & Mitchell, 1984, p. 402), such that while confronting strategic issues its members thoroughly and inclusively evaluate underlying reasons, mechanisms, and potential consequences. As a systematic examination of a wide range of alternatives, objectives, costs, risks, alternative actions, data and information, intensive assessment of positive and negative consequences of alternatives and subsequent planning, SDC is key in the development of theorizing about a firm's strategic choices, decision-making theory and practice (Atuahene-Gima & Li, 2004; Forbes, 2007; Fredrickson, 1984; Janis & Mann, 1977; Miller, 2008; Papadakis, 1998).

While SDC may have some limitations such as slowing the decision-making process, a growing body of evidence suggests that it is beneficial in promoting organizational performance (e.g., Mitchell et al., 2016). This is because rigorous attempts to provide multiple alternatives are crucial for accurately understanding situations, making high-quality decisions (e.g., Bourgeois & Eisenhardt, 1988; Dean & Sharfman, 1996; Nutt, 1998, 1999; Papadakis, 1998; Papadakis & Barwise, 2002) and subsequently performing in the marketplace. Further, in the specific context of small-sized firms, because of the absence of adequate formalization and organizational design, a TMT that applies a more inclusive process is likely to reach a deeper understanding of the situation and make better assessments of multifaceted issues emerging from the competitive environment (Sniezek, 1992). Scholars have also noted the importance of questioning the chosen paths, a key aspect of decision comprehensiveness, as a means of improving competitiveness of family businesses (Ensley, 2006). More specifically, in small-sized family firms with goals that seemingly capture opposing orientations (Gómez-Mejía et al., 2011; Mustakallio et al., 2002) and specific emergent social contexts (Zahra, 2010), inclusiveness in the decision-making process can help reconcile potentially conflicting demands and needs. This is important because it helps in managing these multiple agendas in ways that enhance the performance of the firm. Thus,

CEO Implementation Capacity

Execution is key to organizational success, especially for smaller, capital-deficient companies. Comprehensiveness in the decision-making process is vital to identify and seize opportunities and address emerging demands and thus is likely to drive firm performance. However, we extend this line of thinking and argue that the ability to reach high-quality decisions and subsequent performance is not sufficient unless the decisions are fully realized. Following previous research, we point to the particular role of CEOs in realizing the decisions they and their TMTs make and more specifically refer to the CEO's capacity to execute the decisions at hand (i.e., CEO implementation capacity). We treat the CEO as part of the TMT but for empirical purposes treat him/her separately from other TMT members.

Interestingly, considerable attention has been directed to decision-making processes, but only limited efforts have been made to unveil strategic decision implementation (Dean & Sharfman, 1996; Greer et al., 2017; Lampaki & Papadakis, 2018). The relatively scant existing research shows that effective implementation depends on the existence of a supportive context (Alamsjah, 2011), which following Edmondson (1999) is referred to as a work environment in which members have access to and get vital information, as well as resources conducive to learning and performing the tasks at hand.

Most past research has referred to the implementation act itself, and to the actions rendered by the implementing executives (Brenes et al., 2008; Elbanna et al., 2014). However, following recent research on effective change leadership (Higgs & Rowland, 2011; Krummaker & Vogel, 2013), we take a different stance and focus on the CEO's implementation capacity as an intricate construct, an ability of the CEO involving several important organizational and personal facets:

Transforming vision into action. The CEO's ability to transform the organizational vision into practical outcomes seems to be of high importance. While executives often struggle to form a coherent vision, CEOs with adequate implementation capacity transform their visions into day-to-day action and implement the devised strategy in competitive moves in the marketplace.

Harnessing coalitions (managing organizational politics). A CEO's implementation capacity must also include the ability to navigate through organizational politics and build coalitions to help support and transform the goals into actions. This is done by recruiting managers and employees to promote the decision implementation, obtaining support of multiple stakeholders and harnessing them to promote chosen courses of actions (Lampaki & Papadakis, 2018).

Being decisive. Another important element is the decisiveness with which the CEO operates. Decisiveness refers to “the ability to take the unconventional and unprecedented course of action whenever it is called for” (Ishida, 2008, p. 1), or to “ the degree to which the leader is willing to make decisions or take decisive action (House et al., 1971)” (in: Williams et al., 2009, p. 74). Conversely, indecisiveness occurs when a decision maker is reluctant to make decisions because of low self-esteem, insecurity, or a preference not to bear responsibility and feeling regret (Mulki et al., 2012). The CEO's ability and power to decide on a specific action when needed is essential to enable a quick and effective response to market threats. However, this does not mean that one needs to rush into decisions (Simpson et al., 2002), but rather be willing to engage in the decision task at hand, make choices, and bear the responsibility for a chosen course of action, which is key for effective leadership (Williams et al., 2009).

Handling the TMT. The CEO's ability to handle the TMT efficiently is required for effective implementation. Managerial awareness and an ability to solve intrateam problems as well as dealing with predicaments of individual executives is of immense importance to the team's well-being, dynamics, and SDC.

CEO self-efficacy. The CEO's belief in his or her ability to achieve most of the targets set has been shown to highly influence the organizational ability to execute. Self-efficacy is defined as a general perception of one's capability. Self-efficacy components shape thoughts and beliefs, which in turn influence behaviors and specific action (Bandura, 1989). Research suggests that efficacious CEOs are likely to perform better because they tend to both engage and persist in situations that others tend to avoid, and shows that CEO self-efficacy is positively related to market performance (Westerberg et al., 1997). Thus,

The Interactive Influence of CEO Capacity for Implementation and the TMT Strategic Decision Comprehensiveness

We suggest that when the CEO possesses the capacity to implement decisions made following a comprehensive process (i.e., SDC), and the TMT comprehensively engages the decision-making process, the performance of the firm is likely to improve. These two mechanisms manifest formulation and implementation processes, which are conducive to higher levels of firm performance. Conversely, when the CEO lacks implementation capacity, it is unlikely to expect that the decision-making process will be fully realized, and this hampers firm performance. Thus,

Method

Research Setting

Small-sized family firms (defined as family firms with fewer than 100 employees) are a relevant research context for exploring the decision processes of executive teams and CEOs since these firms are perceived as a key vehicle for economic and social growth and are known to be extremely fragile (Freeman et al., 1983). Our definition is slightly different from the definition of small-to medium-sized firms (SMEs), entities that usually employ not more than 250 members in most developed countries (in the Unites States, the figures revolve around 500 employees). Small-sized family firms provide a suitable context for our research because they lack (1) the economic resources needed for their development and growth (each firm employing fewer than 100 employees in our sample applied for a loan to allow for better cash flow management and opportunities for new growth-oriented investments) and (2) the resources and formal administrative system and thus rely more heavily on the ability of their CEOs and TMT members (Ling et al., 2008; Lubatkin et al., 2006).

In addition, family firms, which are the most ubiquitous form of ownership (Boyd & Solarino, 2016), also seem to be a fitting context to test our model as their managers and CEOs are known to identify strongly with their organization, are often more motivated to assure its long-term survival, are disposed to be deeply embedded in its socioeconomic context (Le Breton-Miller et al., 2011), and are thus likely to appreciate the importance of good management and organization.

While effective strategic decision-making processes, implementation capacities, and performance are important in all organizations, scholars have reasoned that because of their lack of formalization (Sine et al., 2006), these decision-making processes are even more crucial in small-sized firms. Thus, scholars have called to develop a fuller understanding of strategic decision making in smaller organizations (Johnson et al., 2003). In this study, we attempt to address these calls and promote scholarly understanding of small-sized family firms’ strategic decision-making processes.

Sample and Procedure

Small-sized family firms are influential entities in both developed and emerging economies. Despite their prevalence, these organizations have gained rather limited research attention largely because data about their management teams and the ways they function and influence organizational outcomes (e.g., performance) are not readily available for researchers. Furthermore, compared to large firms, small-sized family firms lack the resources and hierarchical organizational systems that can help in addressing complex issues, and they largely depend on the more direct influence and abilities of the CEOs and individual members of their TMT (Lubatkin et al., 2006).

This study is part of a larger research project (Friedman et al., 2016) involving TMT members from a random sample of 131 small-sized family firms in Israel that applied for a loan from Israel's small- and medium-sized enterprises (SMEs) Agency's State Guaranteed Fund. The study involved first-generation family businesses. The Israeli SMEs Fund is a government-backed, regulated entity of the Ministry of Economics, which provides bank loans to small- to medium-sized firms in need of either cash flow or growth funds. Candidate firms are required to supply detailed financial information. The CEOs are interviewed in the process, and the firms must demonstrate a need for additional financial resources to grow but also the ability to repay the loan.

A random sample of 316 applicant firms was contacted, and their CEOs and TMTs were asked to participate in a study about their organization's attributes, decisions, and activities. Each TMT member was informed (in a face-to-face meeting) that the questionnaire data were being collected as part of a research project exploring the function of decision-making processes in small-sized firms’ operations. To identify TMT members from each firm in our sample, we implemented a procedure often used by researchers of strategic leadership (e.g., Hambrick & Mason, 1984) in which senior managers are asked to name the people with whom the CEO shares strategic decision-making functions. A TMT consists of the CEOs and the executives they include in the strategic decision-making process and who usually report directly to them (Castanias & Helfat, 1991; Hambrick & Mason, 1984). Thus, the CEOs in our sample were asked to identify the TMT members they consulted in such processes and assist us in recruiting them for this study. The CEO and the TMT members were then asked separately to complete a structured questionnaire and return it to the first author.

Overall, complete data were obtained from 41% of the targeted firms. As in previous studies (e.g., Lubatkin et al., 2006), data from firms with less than a 50% response rate from TMT members were excluded from the sample. The TMTs in the sample were relatively small, and usually consisted of three or four executives, with only a handful consisting of two executives. Completed questionnaires were obtained from 131 firms, including 131 CEOs and 186 of their TMT members (the average firm size was only 21 employees, and the average number of respondents per firm was 2.42). The firms in the sample originated from various sectors, including services, manufacturing, wholesale trade, and construction. No significant differences were found between participating and non-participating organizations (either in terms of number of employees or in early vs. late response, p > .10). Except for three firms, all CEOs and TMT members were family members. The average organizational tenure of the CEOs and TMT members in the sample was 15 years. Forty CEOs and TMT members (13%) were female. To minimize potential response bias associated with data collection from a single source, the data were obtained as follows. The CEO and his or her TMT members provided data on the team's SDC. Relative performance levels were provided by the CEOs, while the CEO's capacity to implement was reported by TMT members.

Finally, we followed Brislin’s (1986) guidelines for translation and back-translation to ensure construct measurement validation using three experts and a professional copy editor. We then asked senior executives to review the items and assess their clarity and accuracy in measuring the intended concept.

Measures

Strategic Decision Comprehensiveness

Following Miller (2008), SDC was measured by 10 items, which were obtained by asking executives to designate the degree to which decision making in their firm was comprehensive. The executives were told that strategic decisions included significant, potentially high impact decisions. This captures the conceptualization of strategic decisions as those that “address complex and ambiguous issues that involve large amounts of organizational resources (Mason & Mitroff, 1981)” (In Amason, 1996, p. 123). They include decisions of mergers and acquisitions (M&A), entering a new market, or augmenting a substantial new product line (e.g., Alexander, 1985). All the firms in our sample had made at least one of these decisions in the three years prior to the study (data were collected in 2012). We requested the respondents to specify the extent to which they concurred with items such as “When making significant decisions, the management conducts a thorough analysis and testing and compares several alternatives.” The Cronbach alpha of this measure was 0.87.

CEO Implementation Capacity

CEO implementation capacity was assessed by five items constructed for this work, reflecting how the TMT perceives the CEO's implementation capacity, in connection with the strategic decisions taken. In constructing the items, we started by performing word searches (e.g., CEO implementation and managerial implementation) of the ISI Web of Knowledge citation database. The search did not yield much relevant research but allowed for a better understanding of potential routes for construct formation. We envisioned CEO implementation as covering several facets, including: the CEO's ability to transform the organizational vision into practical outcomes, the CEO's ability to harness organizational politics and recruit managers and employees to promote decision implementation, the decisiveness with which the CEO operated (i.e., the ability and power to decide on a specific action when needed), the CEO's ability to handle the team efficiently (i.e., being aware and solving intrateam problems as well as dealing with predicaments of individual executives), and the CEO's self-efficacy. In order to validate this measure, we sent it to seven objective experts (professors and PhD students), who assessed it and asserted construct validity. Exploratory factor analysis confirmed that the measure loaded on a single factor with the items.

We found it may be less problematic to assess the CEO's capacity through the TMT members as often done in both leadership and strategic leadership research. Nevertheless, given the long-standing work relationships and potentially family relations these subjective assessments provided by TMT members may be associated with response bias. Sample items include: “The CEO knows how to transform the firm's vision into an executable strategic plan” and “The CEO believes that s/he can achieve most of the targets s/he has set.” The Cronbach alpha of this measure was 0.90.

Firm Performance

Following previous research (Lubatkin et al., 2006), we collected data on the relative firm performance by asking the CEO to compare the performance of his or her firm relative to that of focal competitors on profitability and growth. Specifically, we focused on two facets of performance—financial and operational—because we had learned that in these small-sized firms, leaders tend to direct particular attention to the efficiency of work processes and meeting financial goals. Thus, our measure consists of items capturing the firm's financial performance (net profitability and gross profitability) and operational performance (operational efficiency). The Cronbach alpha of this measure was 0.81.

Family Firms

The family firms in our sample were identified utilizing the number of family members involved in managing the firm divided by the total number of managers in the firm. We also controlled for the percentage of the business owned by members of the founding/controlling family (Chua et al., 1999). Both measures ensured that the firms in our sample had a majority of family members in their management and were controlled by the owning family.

Control Variables

As the sample firms were relatively similar in that they were all small-sized family firms, we controlled for organizational size, represented by the number of employees in the organization as well as for organizational age, estimated by the natural log of the number of years since the establishment of the firm, which was used to compensate for skewness in the raw measure across firms. Previous studies (Lubatkin et al., 2006) indicate that organizational size and age are important control variables because of their linkage to inertia and more bureaucratic processes (particularly information processing), and lower levels of adaptability.

Level of Analysis

It has been demonstrated that utilizing multiple respondents is more reliable than utilizing a sole respondent (Bowman & Ambrosini, 1997), but it necessitates the calculation of within-team consistency. We commenced by running a one-way analysis of variance on each item using organizational affiliation as the independent variable to ascertain whether there was indeed more substantial variability in the ratings between firms than within firms (Winer, 1971). Only then did we aggregate the scores from each executive, including the CEO. We found support for this aggregation as the F ratio for each model item was indeed significant (p < .001).

We confirmed greater variability in the between-teams ratings than the within-teams ratings using a one-way analysis of variance, which resulted in p < .01 (James, 1982; Smith et al., 1994). We further calculated both interrater agreement index values (RWG) as well as intraclass correlations (ICCs) to evaluate agreement and consistency of group member response. The reliability of the individual-level score as a representation of group agreement was assessed using ICC(1), while the reliability of the group-mean score was measured using ICC(2) in order to distinguish between the various groups. TMT SDC values were between 0.702 and 0.784 for ICC(1) and between 0.876 and 0.896 for ICC(2) with a mean RWG of 0.964. ICC(1) and ICC(2) for CEO implementation capacity were between 0.871 and 0.885 for ICC(1) and between 0.903 and 0.939 for ICC(2) with a mean RWG of 0.966. These indications support aggregating individual questionnaire responses for team level analysis in field research, according to the conventional standards indicated in Bliese (2000).

Data Analysis

The model proposed here was estimated using structural equation modeling (SEM) with Mplus 8.0 (Muthén & Muthén, 1998–2013) to create a latent variable representing the interaction of the latent variables and other constructs.

We employed Anderson and Gerbing’s (1988) standard two-step approach to SEM. This involves first assessing the measurement model using confirmatory factor analysis, then sequencing alternative structural models. Several goodness-of-fit indices for the research model are reported below. These indices include the χ2 statistic divided by the degrees of freedom (χ2/df), the comparative fit index (CFI), the Tucker–Lewis coefficient (TLI), and the root mean square error of approximation (RMSEA). Jöreskog and Sörbom (1993) and Kline (1998) suggested that the χ2/df ratio should be less than three, the values of CFI and TLI should be greater than 0.90, and RMSEA should ideally be below 0.05 but is acceptable if less than 0.08.

Finally, we employed a test for variance inflation factors (VIFs) to determine whether the data suffered from multicollinearity, which is said to exist when the VIFs exceed a value of 10 (Belsley et al., 1980). The highest VIF in the data was estimated to be 5.014 (for CEO implementation capacity), indicating no multicollinearity problem in our data and showing none of the variables to be linearly predicted from the others to any significant degree.

Results

The fit of the three-factor model developed in this section was assessed by confirmatory factor analysis (CFA). The model, estimated by the maximum likelihood method with robust standard errors (hereafter, MLR), yielded a good fit with the data (χ2(62) = 107.065, p = .0003, with a scaling correction factor for MLR c = 1.076). Parsimony-adjusted goodness-of-fit statistics (CFI = 0.946; TLI = 0.932; RMSEA = 0.074; SRMR = 0.071) were also adequate. The standardized coefficients from factors to items ranged from 0.56 to 0.93 The CFA indicated that all relationships between indicators and their corresponding latent variables were highly significant (p < .000).

We started with a two-factor model in which the observed items of SDC and CEO implementation capacity were loaded onto one latent factor and the observed items of perceived performance onto another. The results of this two-factor model generated the following fit indices: χ2 (64) = 203.89, p < .001 with a scaling correction factor for MLR c = 1.09. The goodness-of-fit of this two-factor model deteriorated relative to that of the three-factor model, p < .000 with a scaling correction factor for MLR = 1.0996; CFI = 0.832; TLI = 0.795; RMSEA = 0.129; SRMR = 0.092 (see Hu & Bentler, 1999). Next, a one-factor model was tested in which all observed items were loaded onto one latent variable (measuring the extent of the overall common method variance). The results of the one-factor model yielded the following fit indices: χ2 (65) = 312.004, p < .000 scaling correction factor for MLR = 1.1194; CFI = 0.703; TLI = 0.644; RMSEA = 0.12; SRMR = 0.106. In sum, the two-factor and one-factor models exhibited poor fit compared to the three-factor model.

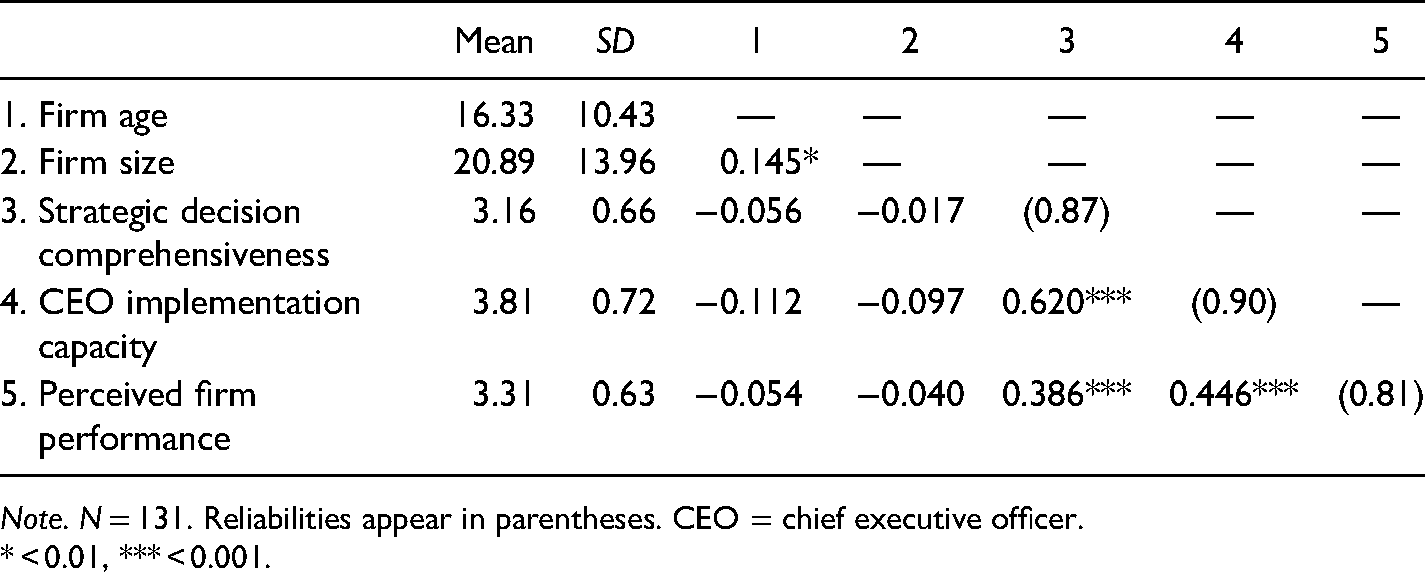

Table 1 presents the means, standard deviations, reliabilities, and correlations among the research variables. The results indicate positive relationships between all three main variables—strategic decision comprehensiveness, CEO implementation capacity, and perceived performance.

Means, Standard Deviations (SD), and Correlations.

Note. N = 131. Reliabilities appear in parentheses. CEO = chief executive officer.

* < 0.01, *** < 0.001.

Model Test

A structural linear model (without interactions) was tested next. This model included the control variables mentioned above (firm size, organizational age). The χ2 for this model was significant with χ2(86) = 146.72; p < .001 (with a scaling correction factor for MLR c = 1.051); CFI = 0.93; TLI = 0.92; RMSEA = 0.73; and SRMR = 0.74.

A nonlinear model was analyzed next. In addition to the variables included in the linear model, this model added the moderating effect of CEO implementation capacity on the relationship between SDC and perceived performance. A latent variable representing the interaction of the CEO's implementation capacity with strategic decision comprehensiveness was also added to the model. This interaction was significant and improved the model fit (B = 0.269, p = .027). Note that the use of such an interaction as a latent variable has been shown to be effective for testing moderating relationships in structural equation models (e.g., Klein & Moosbrugger, 2000; Mathieu et al., 2009). To this end, we followed the two-step method proposed by Maslowsky et al. (2015). In sum, the nonlinear model yielded a better fit than the linear model.

As is customary in such models and since it is not possible to employ fit statistics such as χ2, CFI, TLI, or RMSEA in models that contain latent interaction terms, the model fit was compared by the Akaike information criterion (AIC) and sample-size-adjusted Bayesian information criterion (BIC) (hereafter, SABIC). For the nonlinear model, we obtained AIC = 3214.095; SABIC = 3201.148. These measures for the linear model were AIC = 3217.834 and SABIC = 3205.175, thus indicating the better fit of the interaction model (Akaike, 1987).

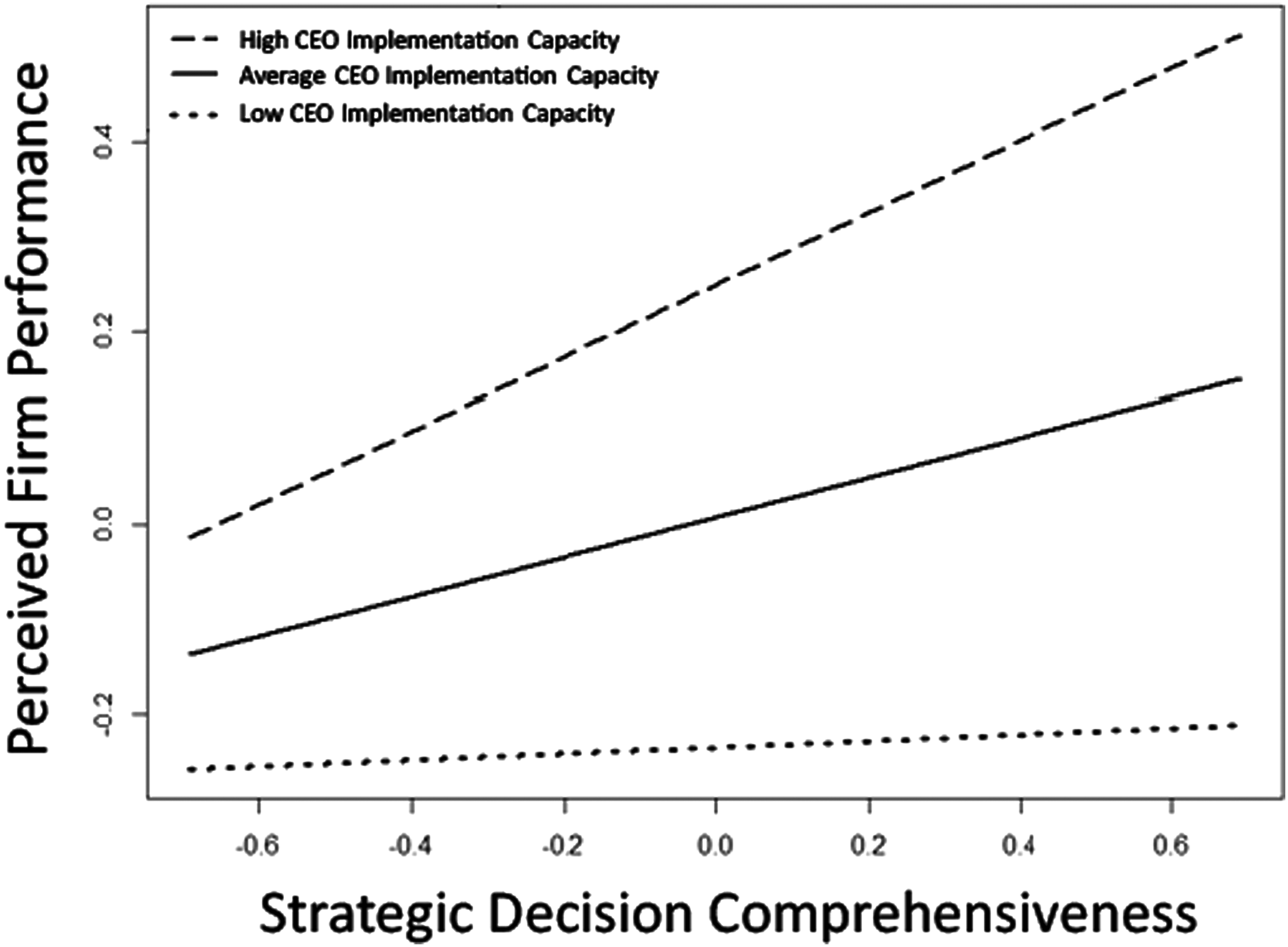

Finally, the interaction was plotted using common formulas (in the R program environment) for depicting relationships at low (one standard deviation below the mean), medium (at the mean) and high (one standard deviation above the mean) values of the moderator (see Cohen et al., 2003). This plot is shown in Figure 1.

The link between strategic decision comprehensiveness and perceived firm performance at different levels of chief executive officer (CEO) implementation capacity.

Simple slope analyses (Aiken & West, 1991) indicated that when CEO implementation capacity is high, SDC is positively and significantly related to perceived firm performance (b = 0.38, t = 2.067, p < .039); when CEO implementation capacity is at its mean, SDC is positively and insignificantly related to perceived firm performance (b = 0.208, t = 1.371, p = .17), and when CEO implementation capacity is low, SDC is positively and insignificantly related to perceived firm performance (b = 0.03, t = 0.213, p = .832), though the coefficient is lower than the high- and medium-level conditions. Figure 1 illustrates these relationship patterns.

Discussion

The findings of this paper indicate that both CEO implementation capacity and TMT SDC are positively related to the relative performance of small-sized family firms. We further find a positive interactive effect of CEO capacity for implementation and SDC on family firm performance.

Our research contributes to the literatures on strategic leadership, strategic decision-making processes, and small-sized family firms in several ways. First, examining processes within TMTs is likely to help refine strategic leadership research and theory by providing a more nuanced understanding of the dynamics within a TMT that allow more effective functioning and optimal outcomes (Hambrick, 2007). Our conceptual model informs this line of research by revealing micro-behavioral and cognitive mechanisms that improve the performance of small-sized firms. Second, TMT decision-making processes are crucial for the functioning of both the executive team and the organization (Hambrick & Mason, 1984). We advance this research by unveiling situational conditions under which SDC may enhance performance (Atuahene-Gima & Li, 2004). We expand on the micro-foundation perspective and explain why CEO implementation capacity is a key micro-foundation that we should focus on when explaining how decision-making processes unfold and influence firm performance. Specifically, we allude to implementation qualities that effective CEOs possess (Greer et al., 2017; Lampaki & Papadakis, 2018) to more fully realize the decision-making process their TMT engages in. Finally, we extend research on small-sized firms by highlighting how in such contexts where there are seemingly opposing goal orientations (Gómez-Mejía et al., 2011; Mustakallio et al., 2002), the decision-making processes of the CEO and the TMT interact to drive firm performance.

Our study shows that for SDC to drive firm performance, the CEO must have a capacity to implement the strategic decisions at hand. In order for a small-sized family firm to perform well, it may need a combination of both effective TMT decision-making processes (in the form of SDC), as well as high managerial implementation capacities. Such a combination, however, is hard to develop, which partially explains the high mortality rates of these fragile firms that tend to face significant challenges (e.g., liability of smallness) as compared with larger firms (OECD, 2018) which has been reinforced amid the COVID-19 pandemic crisis (OECD, 2020).

While the established link between TMT SDC and performance also conforms to the findings of other scholars (Mitchell et al., 2016), we bring to light the situational conditions in which such a decision-making process can help a firm to perform at higher levels. We highlight the importance of having a CEO with an implementation capacity that more fully and appropriately applies the decision-making processes. In so doing, we enrich our knowledge about a micro-foundation of strategic decisions in family firms (De Massis & Foss, 2018); that is, we explain the role of CEOs in the organizational effort as both facilitative (in promoting SDC in the firm's TMT) and operational (in implementing the strategic decision). This is important as scholars have noted that “we are left with a gap in understanding of micro-level conditions leading family firm actors and decision-makers to execute the firm strategy” (De Massis & Foss, 2018, p. 392). Improved organizational processes, such as seeking more alternatives (Siegel & Hambrick, 1996) may promote better strategic decisions, but our research shows that the CEOs have a particular role in integrating various political, operational, managerial, and interpersonal elements in the quest for driving higher levels of performance. Similarly, we tend to hold the inaccurate view that in small-sized family firms there are family relationships that relax the demands, whereas the opposite is often true as family CEOs and other family executive members need to pursue different goals and bear almost the entire accountability burden of the entity. Additionally, there is evidence to suggest that TMTs that are effective in making strategic decisions are key for the success of small-sized firms, but we extend this view to underscore that it is vital for the CEO (who is part of the team but has a unique role) to utilize his/her implementation capacity to fully realize the decision-making processes. We believe that this is particularly important because more professionally capable CEOs in a family business may be better equipped to favorably position the firm in the industry (Lin & Hu, 2007).

Finally, when assessing potential SDC outcomes (Meissner & Wulf, 2014), though the linkage with performance may seem intuitive there are two potential counter effects: internally—high-quality decisions may not always be easy to execute, and externally—performance is subject to a multitude of external factors, which are exogenous to the strategy process (Dean & Sharfman, 1996). We enrich our knowledge of SDC in that we not only focus on the implications of decision comprehensiveness for firm performance (Forbes, 2007), but highlight a key complementary micro-foundation mechanism, CEO implementation capacity, which helps in driving performance. This is a key theoretical advancement as our endeavor expands on the efforts of Meissner and Wulf (2014) to promote the analysis of SDC and organizational performance, which they see as a fruitful way to refine the strategy process. We do this through a focus on micro-processes (Felin et al., 2012, 2015) that are key in explaining how the strategic decision-making processes in TMTs unfold (e.g., Carmeli et al., 2012, 2013), and drive firm performance.

Practical Implications

The findings presented here depict how the CEO and the TMT can facilitate improved organizational decision processes and subsequent performance. This issue is especially crucial for small-sized family firms since they tend to have relatively small management teams and lack the bureaucratic organizational systems that larger firms build and use in their day-to-day activities as well as in their strategic decision-making processes. As small-sized firms appear to be highly fragile and face major challenges vis-à-vis larger entities (OECD, 2018) particularly in times of crisis (OECD, 2020), such organizations should attempt more extensively to promote decision-making processes and not simply rely on individual capacity (Lubatkin et al., 2006) and in parallel strive to improve the implementation capabilities of their CEOs.

Lastly, this study suggests that CEOs and their TMT members should pay closer attention to actively advancing and promoting more comprehensive and extensive decision-making processes while acknowledging that there are costs in terms of time and resources consumed by decision-making processes (Forbes, 2007). Measures that may prove effective include the study of best practices (promoting improved decision making through the study of highly successful organizations) as well as fostering and promoting organizational learning (Da Silva & Roglio, 2015).

Limitations and Future Research Directions

This study has several limitations and some important questions require answers. First, this work is contextual (focused on small-sized family firms in Israel) and caution should be exercised when attempting to generalize our findings on small-sized family firms to other contexts since small-sized family firms are seldom multinational and center in specific geographical areas. Thus, the Israeli setting may differ in terms of leadership capacity, decision-making processes, risk taking, and other attributes. Expanding this research to additional countries and cultures can improve the generalization of our results and will likely shed further light on differences (and similarities) among small-sized family firms in different settings. In addition, the decision-making mechanisms may be qualitatively different in small-sized family firms than those of large organizations (Huang & Wang, 2012). However, Israel is also similar to other nations in which family firms, including those small in size, account for the majority of the business population. The results may also be applicable to small-sized family firms around the world and particularly to the strategic decision-making processes and the importance in the capacity of the CEO to follow a chosen course of action. They may further advance our knowledge about small-sized family firms since these entities often rely on the CEO's capabilities in their early stages of development. Thus, our research opens up a new window of opportunity about the ways the CEO can transform decisions into actions to drive firm performance.

Second, the data are cross-sectional (relating to behavior and performance in the three years prior to the research), and examination of TMT processes at numerous points in time will likely strengthen the results. Caution is advised when drawing conclusions from survey-based data, particularly when evaluating causal inferences. Although a crude test was used to assess the appropriateness of the proposed model in connecting the variables, reverse models, involving SDC and performance cannot be ruled out. Thus, additional research is needed to assess the causal direction of the proposed model. For example, we cannot rule out at this point that higher levels of performance do not positively influence TMT dynamics and decision processes rather than vice versa. Finally, there may be other, unobserved, variables which could affect the observed organizational outcomes.

Regardless of these limitations, this paper also raises some significant questions and research avenues. We are still at the beginning of the learning process of understanding the ways in which CEOs shape processes (O’Reilly et al., 2010) such as SDC. Further, scholars have much to learn about the conditions under which the connection between SDC and organizational outcomes can be strengthened or weakened, and mediating constructs still need to be explored. In particular, as many small-sized family firms fail to survive in the long term, which is a key priority in many countries (OECD, 2020), the question of resilience (Sutcliffe & Vogus, 2003) and the ability of small-sized family firms to cope and bounce back from experiences of failure and adversity seems imperative and important to study. We also believe that research can further advance by focusing on founder-CEOs as well as when founder-CEOs are replaced by the second generation in family firms. Research on decision processes in small-sized family firms is also scant despite their importance as a vital component of every economy. Smaller business fragility (USSBA, 2006; ASBFEO, 2015) may only be mitigated by effective strategic decision-making, and gaining insights into these processes should make a significant contribution to our understanding of this discipline (Johnson et al., 2003). We acknowledge the richness of each facet of our concept of implementation capacity. For example, handling a TMT is much more complex and multidimensional than we portray, and requires a set of skills and behaviors from effective communication patterns, conflict-resolution skills, and relationship-building capability, among others. However, we also believe that handling a TMT allows a CEO to implement a strategic decision by harnessing the support of members (“bring them on board”). Finally, our research captures the dynamics and particularly the decision-making processes within a TMT but applies a variance theoretical explanation. Thus, a process model can further advance our research on how the decision-making process unfolds over time such that we can more precisely capture choice events and activities over a period of time (Langley, 2009).

Conclusion

This paper advances research and theory of strategic leadership, strategic decision making, and family businesses by explicating how CEO implementation capacity interacts with TMT decision-making processes to drive the performance of small-sized family firms. In so doing, we shed light on the situational conditions in which a comprehensive decision-making process can help a firm to perform at higher levels. Our study showed that in small-sized family firms CEOs, who possess implementation capacity, help in realizing the strategic decision-making process in their TMTs and positively influencing firm performance. Specifically, we adopted a micro-foundation lens to explicate why CEOs capable of implementation can optimize comprehensiveness in the strategic decision-making process, thus allowing the firm to perform at higher levels.

Footnotes

Acknowledgments

We are thankful to the Associate Editor and our anonymous reviewers for their helpful comments and suggestions. We also acknowledge the financial support of the Raya Strauss Family Business Research Center at Tel Aviv University. All remaining errors are entirely our own.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Raya Strauss Family Business Research Center at Tel Aviv University (grant number 2019-1).