Abstract

Collaboration between two groups that may invest their resources in a common productive activity has the potential to lead to conflict over the output of that activity. This article examines the stakes of such conflict as well as the willingness for parties to subject themselves to a third-party arbiter. The model highlights three determinants of conflict and of investment in credibility-enhancing institutions: the value of the output, the relative endowments of the parties, and the mutual benefits of collaboration. In particular, the analysis shows that complementarity between the groups’ resources lowers the stakes of political conflict and increases the incentives to commit. The model thus suggests a new mechanism through which we can understand the frequency of conflict and the poor institutions associated in countries with mineral resources. The model’s predictions also help us to understand how Mauritius avoided the resource curse and was able to develop sustainable economic growth.

Introduction

The discovery of mineral resources in poor regions of the world is not always good news. In fact, an abundance of mineral resources generally hinders growth and asset accumulation (see Van der Ploeg [2011] for a survey). It also feeds into more frequent and more violent periods of conflicts (Collier and Hoeffler 2004; Fearon 2005). Finally, it seems to be associated with poorer institutions (Bates 2007), though the evidence on the last point is thinner.

Why is mineral extraction associated with such negative outcomes? Dal Bó and Dal Bó (2011) suggest that mineral extraction generates conflict because it is capital intensive. While a labor-intensive activity may attract idle young men away from fighting, they argue that a capital intensive one encourages them to attempt “appropriation.” The literature has suggested a number of other features of productive activities that may also fuel armed conflict, including the point-source nature of some resources, economies of scale, direction of technical change, and networks of suppliers and clients.

A precursor to this work, Jha (2013, 2014) is first to argue that conflict or peace between ethnic groups depends on whether their resources are complements or substitutes. He exploits evidence drawn from medieval Hindu–Muslim relations and provides an intuitive sketch of the mechanism linking complementarity to peace and even better institutions. More recently, Becker and Pascali (2016) show that anti-Semitism is exacerbated when the division of labor between Jews and Christians is blurred. Their evidence draws upon the episode of the Protestant Reformation, after which Protestants were allowed to compete against Jews for the moneylending sector, while Catholics remained barred from lending at interest.

While factor intensity, economies of scale, and so on, may capture some aspects of how certain activities fuel conflict, complementarity seems to be at the heart of the mechanism in each case. A resource-scarce country needs to integrate its economy in order to grow. Agricultural development is labor intensive and favors the creation of supply chains. Even more characteristically so, industrial clusters tend to create external economies of scale. In both cases, this translates into complementarity at the macrolevel. In such a country, the discovery of mineral resources creates new incentives. Internal economies of scale generate large rents for whoever successfully consolidates the mineral sector. Entrepreneurs and rent seekers alike are drawn into the conflict over the control of the resources. Their efforts used to be complements, but mineral resources made them substitutes.

This article buttresses this argument: I provide a formal exposition of a model where complementarity favors peace and also investment in state capacity. In the model, a conflict arises over the distribution of a joint output. Complementary inputs encourage cooperation, which in turn reduces the scope for conflict. In the process, I shed new light on two other determinants of conflict: the distribution of the resources and the value of the output. I consider two features of conflict: the intensity of conflict itself and the willingness to invest in dispute settlement institutions. 1 These two features are treated in separate models, although the two models have several building blocks in common.

In the first model, I embed the distribution of a joint output in a contest game. Two groups can allocate their assets in a common productive activity. The distribution of that output is the object of the conflict. The contest game determines whose preferences over how to divide the output prevail. I assume that the groups have solved the collective action problem and that their members invest their assets homogeneously. To discuss the role of complementarity,

2

I use a constant elasticity of substitution (CES) function to describe the production technology. Each group also has an outside option, allowing it to allocate its resources to a specific productive activity that yields a constant rate of return. This outside option sets the opportunity cost of investing in the common activity. Two parameters of the CES function provide interesting intuitions. The profitability parameter captures the market value of the output (for instance, the export price of a mineral commodity), and the elasticity of substitution is an inverse index of the complementarity between the assets. To summarize, the sequence of play has three steps and assumes perfect information: both groups invest resources in a contest game, the winner of the contest game sets the sharing rule for the joint output, and the groups invest in the productive activities. The output is shared as planned.

The first model yields the central result of this article: conflict abates when the two assets are more complementary. The sharing rules that each group would offer the other should it win the contest are increasingly favorable to the other, thus lowering the stakes of political competition. It is interesting to note that this would correspond to a politically stable situation, where institutions evolve over a longer time horizon than investment and production. An alternative setup, where the contest game follows production, complementarity would favor the joint production, thus increasing the stakes of conflict. This would be an adequate framework to describe an output over which property rights remain to be defined (Spar 2001), generally a transitory situation.

This model also replicates (and nuances) several predictions of the literature on conflict. A tradable commodity price shock increases the intensity of conflict. The underlying intuition is straightforward: the more the groups have to gain from being in power, the more they are willing to spend in order to win the contest. 3 The effect of the price increase is compounded if complementarity decreases, which suggests an explanation for why different categories of production technologies seem to yield such variation in conflict outcomes. Finally, taking endowment asymmetry as a proxy for endowment inequalities, I show that inequality also fuels conflict. This last point suggests a new definition of inequalities insofar as they may affect conflict.

In the second model, one group has undisputed control of the sharing rule. Although the group in power has incentive to ensure the other’s participation in the joint production, it may fail to convince the other of the credibility of its promises. Better institutions help the group to commit more credibly. This model shows that structural characteristics of the production process may thus affect the incentives to invest in institutions. The second sequence of play is: the group in power invests in institutions and sets the sharing rule, the groups invest in the productive activities, and the group in power tries to renege on the sharing rule. If it succeeds, it keeps the output for itself. Otherwise, the sharing rule is implemented.

The second model yields a second central result: the incentives to invest in property rights institutions increase as the complementarity of the groups’ assets increases. As a result, better institutions arise when assets are more complementary to each other. In particular, this characterizes situations in which labor is in short supply or joint production activities are embedded in a wider industry.

This model also replicates several findings of the literature on institutions. First, price shocks reduce the incentives to invest in institutions. Again, the underlying intuition is simple: better institutions arise when the collaboration is not overly profitable. Second, the model predicts that both the group in power and the other group benefit from the powerful group’s ability to commit.

The outline of the article is as follows. The next section reviews the related literature. The third section examines a simple productive framework where one group sets a sharing rule to distribute a joint output; it also provides a normative assessment of its decisions. The fourth section considers a political contest over the sharing rule and derives a number of structural predictors of conflict (first model). The fifth section introduces the possibility that the group in power may renege on the promised sharing rule. Since this is anticipated by the other group, the group in power may find it profitable to invest in a costly commitment mechanism (second model). The sixth section compares the predictions of the two models to the history of Mauritius, and the seventh section concludes.

Literature Review

This study highlights the theoretical role of complementarity in conflict and state capacity building. Unfortunately, empirical estimates of complementarity have proven elusive. Most empirical studies consider capital and labor, mostly considered as national aggregates. A few consider a segmented workforce, usually across the white-/blue-collar divide and no further. When they do, they emphasize the conceptual difficulty associated with multifactor production functions, and they generally focus on the United States, where the data exist. Finally, even the existing studies would now require updating. To my knowledge, little has been written since Hamermesh and Grant (1979) reviewed the existing literature and showed that the estimates are inconsistent across empirical strategies. I can only echo their call for further research on substitution between disaggregated groups, but it might be optimistic to hope for a breakthrough any time soon.

A few recent papers, both theoretical and empirical, simplify this tricky issue. They consider assets which are complements or substitutes, but they do not distinguish between more or less complementary assets. In this article, complementarity is characterized by the elasticity of substitution: this is arguably an accurate definition of complementarity, and it makes comparative statics possible. Bourguignon and Verdier (2009, 2012) study complementarity thanks to the cross-derivatives of the production function relative to the factors of production. This allows them to categorize three-factor economies and their corresponding institutions. They do not consider conflict nor compare different levels of complementarity.

Jha (2013, 2014) is a precursor to this work. He considers that ethnic groups may hold complementary or substitutable assets and predicts that complementary assets favor the peaceful coexistence in the long run. He also hints at institutions that favor a peaceful resolution. In the mechanism he sketches, cooperation is sustained thanks to a repeated game and to a critical mass of agents from the other ethnic group. This article shows his insight, that complementarity favors cooperation, to be robust to alternative real-world scenarios. He suggests a repeated game, which opens the range of possible equilibria to cooperation but does not show why cooperation should be the actual outcome. In this article, cooperation is sustained as an equilibrium of a static model, a sufficient condition for cooperation to be sustained as the equilibrium of the repeated framework. He considers multiple agents, exposing his mechanism to the threat of coalitions across ethnic lines and defections within ethnic groups. This article considers individual interactions, which explains how defections and coalitions are dominated strategies. Finally, he mentions institutions that reinforce the incentives for peace. This article provides a mechanism to explain how such institutions come to exist.

In a closely related paper, Dal Bó and Dal Bó (2011) predict that a capital intensive activity is more likely to generate conflict. Dube and Vargas (2013) provide empirical evidence, which they argue supports the mechanism uncovered by Dal Bó and Dal Bó. It is interesting to note, however, that their study opposes the effects of agriculture and extractive industries on conflict and do not mention manufacturing, heavier industries, or services. This is unfortunately common in the literature (for reviews, see Sambanis 2002; Blattman and Miguel 2010). They focus on oil extraction (capital intensive) and coffee production (labor intensive). Their empirical results could be equally reinterpreted, however, to support the more general mechanism of this article. Capital intensity in the oil sector also means internal economies of scale, which encourages consolidation. Entrepreneurs and rent seekers are substitutes when it comes to the control of the consolidated industry. Meanwhile, decreasing returns to scale and labor intensity generates complementarity within the agricultural sector and positive spillovers on downstream and upstream industries.

Two articles provide compelling evidence to support complementarity as a decisive factor. First, Jha (2013) considers Hindu–Muslim relations in medieval ports to show that the Muslim minority was tolerated as long as they provided a nonexpropriable, nonreplicable, and complementary input to the Hindu majority. Towns where Muslims did not provide such an input were much more prone to Hindu–Muslim rioting. Second, Becker and Pascali (2016) consider anti-Semitism in Germany between 1300 and 1900. The Jews had no competition in the moneylending industry prior to the Protestant Reformation. The latter allowed Protestants to compete in that sector, while Catholics remained to charge interests. Becker and Pascali show that anti-Semitism was stronger in areas where the Jews had lost their monopoly.

Dal Bó and Dal Bó’s model is based on Haavelmo’s (1954) trade-off between production and appropriation. Interestingly, the trade-off is also at the heart of a body of literature interested in the origins of the state (Tilly 1985; Skaperdas 1992) and of property rights (Grossman and Kim 1995; Baker 2003; Muthoo 2004; Hafer 2006). They account for the resource curse and for the higher likelihood of conflict in locations where mineral extraction is an important source of wealth, but they do not account for a possible impact on institutions.

To study the economic determinants of political conflict, it is common to rely on various electoral rules. For instance, Acemoglu, Robinson, and Verdier (2004) and Robinson, Torvik, and Verdier (2006, 2014) consider an economic rent accruing to the group in power, which allows them to buy off their competitors or voters. This model uses instead a contest game to focus more specifically on the costs and benefits of conflict. Skaperdas (1992) introduced contest games to model political competition, building on the production/appropriation trade-off. His contribution proved seminal. For instance, Aslaksen and Torvik (2006) built on his work to model the political competition in a rentier economy. In order to compare civil war with democracy, they claimed that a contest game could only describe an armed civil conflict. This is contentious, however, as contest games may be thought to account for features of any form of political selection process, from elections to outright civil war.

The last feature of the model is related to the growing body of literature on the determinants of state capacity. This literature focuses on one dimension of state capacity: fiscal capacity defined as the ability to raise taxes (Besley and Persson 2009; Bourguignon and Verdier 2009; Cárdenas and Tuzemen 2011). A notable exception is Besley and Persson (2010): they also consider a regulatory dimension of state capacity. They are in fine interested in accounting for property rights but focus on a rather unorthodox definition of property rights enforcement: the regulatory capacity of the state is presented as the extent to which individuals can pledge their assets as collateral. In this article, I consider property rights enforcement in a perspective which is more frequent in empirical works: protection from state predation (Jones 1981; De Long and Shleifer 1993; Acemoglu, Johnson, and Robinson 2001). Here, state capacity is thought of as the state’s ability to restrain itself. This modeling choice was already mentioned in Besley and Ghatak (2010).

The Economic Model

The economy, restricted to its productive sector, is composed of two groups, A and B, that have solved the collective action problem. They each control a different productive asset in quantities RA and RB. To simplify the exposition, the main text will assume RA = RB = R (except in the discussion on inequalities). A and B may account for special individuals, who are in a position to mobilize others’ assets, as well as to other categories of productive assets such as capital, skilled versus unskilled labor, and so on. A and B are thus assumed to provide a simple description of the economic structure of society. Each invests the assets, it controls in two possible productive activities. Each group has access to a specific technology, fA and fB, respectively. The technology f may combine both assets. The three activities produce a commensurate consumption good. Total production is therefore

where

To study the effects of asset substitution or complementarity, the joint production is described by a CES function:

First-best Allocation of the Assets

A social planner with full control of asset allocation would simultaneously choose xA and xB to maximize Y. Formally, her program can be written:

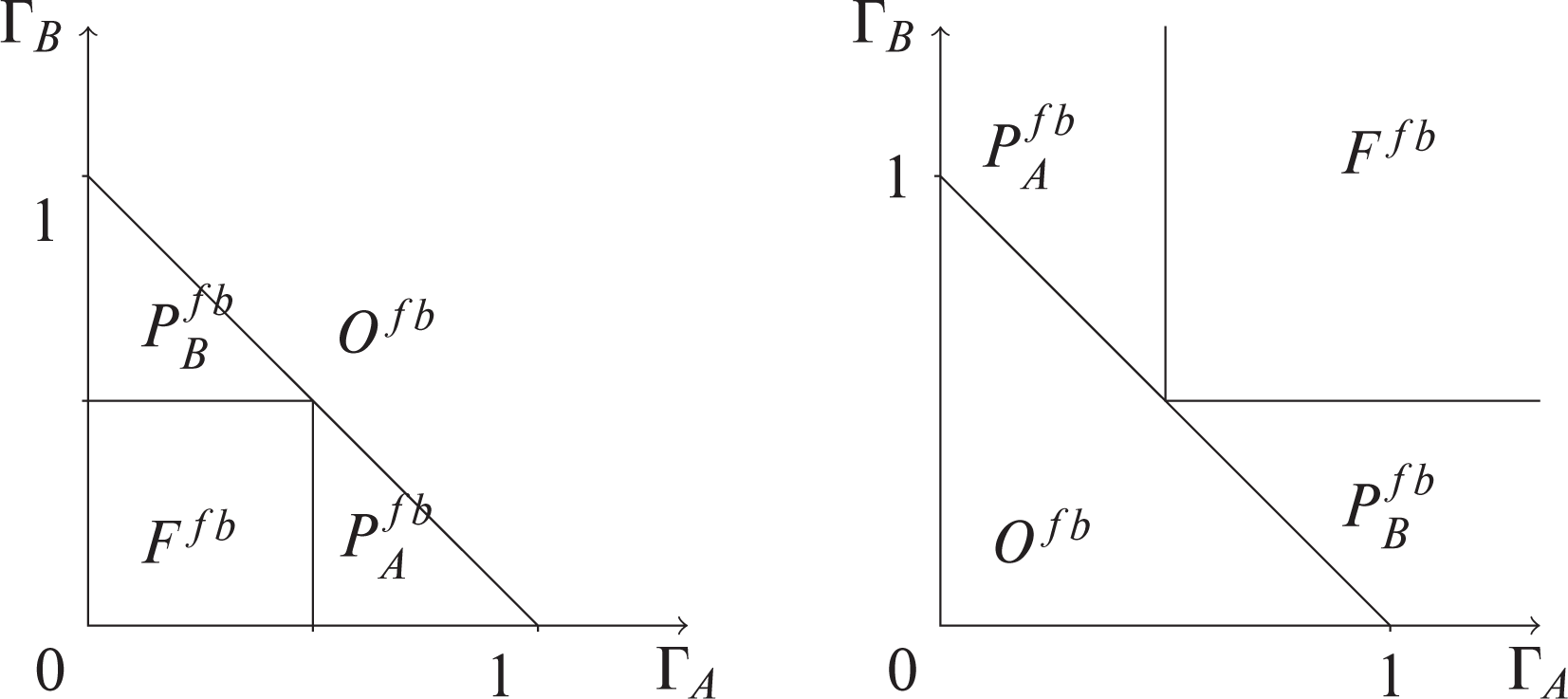

It is convenient to introduce four ranges of parameters: Ffb characterizes full investment by both group in the common production, Ofb no investment by either,

otherwise, one asset i is profitably invested

The first-best efficient asset allocation (left: complements, right: substitutes).

Feasible Investments and Second-best Allocation

Let me now consider a social planner, who would not directly control the allocation of the two assets but could define the rule according to which the joint output is to be shared between the two groups. The rule can be described by the shares

For a given xj, ηi increases with Γi and with αi. It decreases with σ. (0, 0) is the unique and stable Nash equilibrium iff

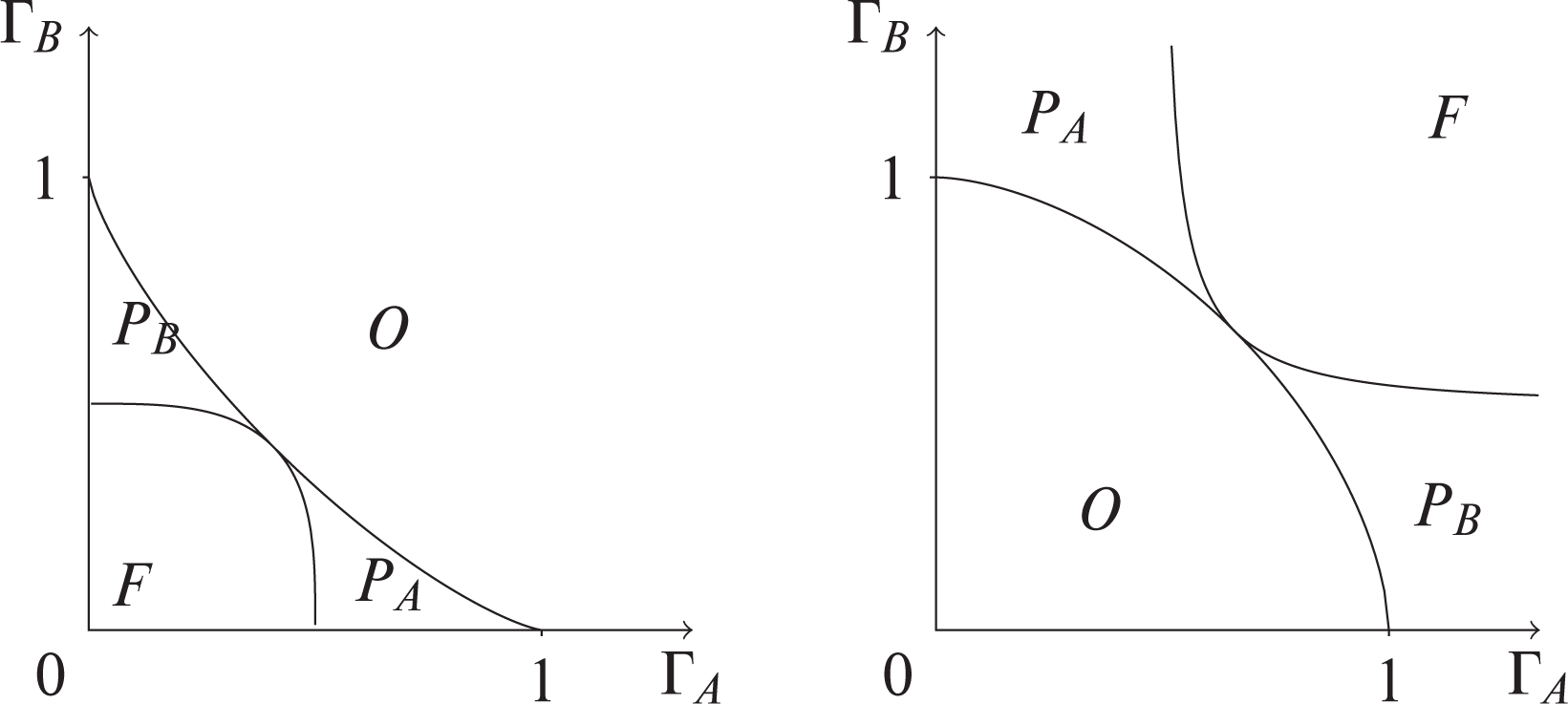

As in the first best, four situations

5

arise from this characterization (cf. Figure 2), with one stable Nash equilibrium

Four possible Nash equilibria resulting from different values of the parameters.

By analogy, I define four ranges of parameters. F is the range where full investment of both assets, for example,

Ranges of feasibility (left: σ < 1, right:

The construction of Figure 3 is explained in the Online Appendix. Rather obviously, i’s asset is more readily fully invested when i finds the joint production profitable (for σ > 1, e.g., when the assets are substitutes, Γi high enough, and the converse for σ < 1, when they are complements). Investment of one asset makes investment of the other more profitable. This positive spillover is higher if the two assets are more complementary. As a consequence, as complementarity increases, the share that each group demands in order to fully invest decreases, and the range of parameters for which both assets are fully invested increases. Conversely, the more the two assets are substitutable, the higher the share one group demands in order to fully invest.

Comparing Figure 3 with Figure 1, it is interesting to note that except when σ = 1, decentralized investment decisions are inefficient (in terms of production maximization) for several ranges of parameters. When σ = 1, the assets are neither complements nor substitutes. In the absence of transfers, when σ ≠ 1, the two agents do not internalize the negative (substitutes) or positive (complements) spillovers they have on the other agent. As a result, we notice a larger O where neither agent invests, and a smaller range F where both agents invest their assets fully.

With this constraint, what would the social planner do? Her output-maximizing program can now be written:

in F, the social planner sets

in O, setting the sharing rule is pointless (

in Pi, she maximizes investment of i while ensuring full investment of j.

Comparing Lemma 2 with Lemma 1 illustrates how the introduction of property rights, in other words how decentralizing investment decisions, constrained the possible investment outcomes whenever σ ≠ 1. For σ ≠ 1, the social planner will only be able to reach the first-best investments for limited ranges of parameters, specifically, under the first-best no-investment threshold

Optimal Sharing Rule

Assume it is one of the two groups’ privilege—A’s for instance—to set the sharing rule. It faces a trade-off between enticing B with a fair share of the joint output and keeping as much as possible. Formally, its program can be simplified into

Their indirect utility VA is a nonconstant continuous function on [0, 1]. It therefore has a maximum

Full participation by B may not be feasible (in PB) or it may (in F and PA): in each case, when the assets are complements, A’s best option is always to maximize B’s participation. When full participation of B is feasible, A wishes, as a secondary objective, to maximize its own share of the joint output. When the assets are substitutes, and B is harder to attract in the joint endeavor (low ΓB), it is not necessarily optimal for A to maximize B’s participation anymore. As a matter of fact, as substitutability increases (σ > 2) and B is hard to motivate, it may even become too costly to include it in the joint endeavor at all.

It is interesting to compare this behavior with that of the social planner. For complementary assets, both maximize the production. The only difference in that case is that A cares about the distribution of the joint output, which matters in range F. For substitutable assets, A still wants to involve B, so as to appropriate a share of the joint output; however, maximizing the production may mean giving away too much to an uninterested B. When substitutability increases even more, the mere participation of B becomes too costly to A.

Conflict

The Stakes of Political Power

For the reasons just outlined (asymmetric profitability of investing the assets, redistributive issues), A and B often do not set the same sharing rules. While for a given state of the world A would set

The interpretation of Proposition 1 is straightforward. An increase in the world price of an exported commodity, a currency depreciation, as well as any mechanism which increases the profitability γ of the joint production would increase the potential value of its production. Investment of both assets has been shown to be nondecreasing in γ: the value of the joint output increases through both channels. Meanwhile, the share each group needs to offer the other to motivate his investment decreases with γ. Those effects combine themselves to increase the stakes of the conflict over control of the sharing rule.

The model then yields what is possibly this article’s main contribution.

Proposition 2 is central in addressing the question raised in this article: why different activities, even if they are similarly profitable, can have vastly different political and economic outcomes. Mineral extraction, in particular, though sometimes handsomely profitable, generates few positive economic spillovers. It creates few opportunities for related business. It often has international, rather than national, networks of suppliers and clients. A relatively narrow group is enough to take advantage of the full opportunities of a mine. As a consequence, there is little incentive for them to redistribute widely its proceeds. This raises the stakes of controlling the extractive process. As already mentioned in the Introduction section, Proposition 2 is intuitive once the true nature of the complementary of substitutable assets has been grasped. A powerful A will find it all the more profitable to involve B in the joint production as the complementarity between their assets increases. As a consequence, A will offer B a higher share of its output. If B is in power, the reasoning is similar, so that when σ decreases, one expects the gap between the two alternative sharing rules to diminish, thus reducing the stakes of political power. The following result is an easy corollary, which only serves to reinforce the argument.

Corollary 1 shows that while profitability and substitutability are both at the heart of the possible conflict between A and B, they tend to in fact reinforce one another as factors of discord. Propositions 1 and 2, taken in isolation, suggest a potential for conflict in both profitable activities and activities which easily substitute factors for one another. This corollary suggests that the stakes of control are disproportionally higher for activities which display both characteristics at the same time.

It is interesting to introduce here an important distinction between two kinds of activities, both arguable highly profitable, both highly capital intensive: mineral extraction on the one hand and technology-intensive industry on the other hand. According to Dal Bó and Dal Bó (2011), we might expect both activities to generate substantial conflict. To some extent, both did generate a degree of conflict, though hardly of the same magnitude. The civil wars and the abuses reported in mineral-rich developing countries are hardly comparable to the social protests often witnessed in industrial societies. What characteristics of these activities may account for this difference in outcomes? This article suggests to take a closer look at the degree of complementarity that the two activities generate. In comparison with mineral extraction, industrial activities commonly associate many different branches of activity, individuals with complementary human capital, and create substantial opportunities for new activities, which would effectively translate into high complementarity in the model here. Proposition 2 and its Corollary 1 therefore provide a tentative explanation for the difference.

Inequalities

So far, the only asymmetry between the two agents is their outside option (in the main text), that is, the best alternative they have outside of the joint endeavor. It is useful to shortly discuss the role of ex ante inequalities. In a marketless model, inequalities can be approached from the angle of distribution of assets and the distribution itself, characterized according to the importance the production gives to each input. With that in mind, let me lift for this section two assumptions: that of equal endowments

a higher βi should be interpreted as indicating a higher abundance of i’s asset relative to j’s. Resources do not reflect wealth in themselves, though a group with a high γi and abundant Ri could be considered to have a high potential wealth if only thanks to their specific activity. But this model is intended to study the common activity, for which the relevant parameters to describe inequalities would be the profitability of investing Γi and the endowment parameter βi. For the purpose of considering the role of endowment inequalities on the stakes of political competition, I hold ΓA and ΓB, as well as σ constant. To avoid having to consider more parameters, I restrict my attention to F, the range of parameters where both assets are profitably invested. In that range, I also work holding the total output constant. We then have the following result.

Political Competition

So far, the model does not include a mechanism to select who gets to decide. Here political competition is modeled as a contest game. Each contestant group k provides an outlay bk in order to win a prize. The prize is the utility gain they would derive from setting the sharing rule rather than the other setting it. The probability of them winning increases with their own outlay and decreases with the other group’s. Outlays are sunk costs, which can be considered as pledges on the future joint output on financial markets (which are not explicitly modeled). 6

An extensive literature has identified numerous contest success functions (the technology that translates the individual efforts into probabilities of winning the contest). The most common is perfect discrimination—the highest outlay wins—and the Tullock contest—group i provides an outlay bi with probability of winning

Additionally,

Another way to formulate Corollary 2 is that higher profitability, less complementarity, and higher inequality result into more rent dissipation. First, the intensity of the conflict for political power (measured here as the amount of resources spent in the political process) increases with an exported commodity price shock. Dal Bó and Dal Bó derive a similar result from their different framework. An increase in the price of the capital intensive good (which corresponds in the framework under consideration to the joint production) results in higher conflict as formalized in their Proposition 9. Our mechanisms are different but should be thought as complementary rather than competing explanations. Indeed, theirs crucially depends on the diversion of labor from the productive sector; mine focuses only on the negotiating position of the individual in power, increased when the profitability of the common production increases.

Second, more complementarity between the assets also reduces conflict—equivalently, it will restrain rent dissipation. Since profitability and substitutability tend to reinforce one another as causes of conflict, this model thus offers a tentative explanation of why different productive technologies tend to have widely differing outcomes in terms of civil conflicts as discussed previously.

Finally, gentle prodding of the model has shown that endowment inequality increases the intensity of the fight for political control. This result holds for the simple contest functions examined here. They might not for other shapes of the conflict technology. For instance, Skaperdas (1992) introduces technology functions which would yield more nuanced predictions. All things considered, I would remain cautious against interpreting that result too literally.

It is interesting to consider the effect of the contest technology on the intensity of conflict. At the end of the game, A and B derive together a utility which is total production minus the pledges made on this production and spent as outlays. If we assume a Tullock contest characterized by parameter r, in the range FAB, the expression of the resulting aggregate utility is

This model can therefore not be thought to account for the resource curse strictly speaking. To account for the resource curse, the productive assets would have to be adversely impacted by the conflict over political power, for instance, if the individuals could not pledge future wealth to provide outlays, but instead faced a trade-off in using their asset to fight or to produce. However, this assumption would make the whole model intractable, and the mechanism has now been known for over half a century. However, the mechanism outlined here shows that even without destruction of productive assets, and no trade-off between fighting and producing, the additional profits derived from a profitable joint production opportunity or a price shock can be wasted in their totality in the competition over political power. It is easy to see how this trade-off would only reinforce the mechanism under scrutiny here.

Property Rights Institutions

In the previous model, any sharing rule, once set, is enforced with certainty. The group in power never reneged once production had taken place. In other words, I had implicitly assumed perfect protection from the predation of the state. This makes sense especially when involvement in the production process is renegotiable anytime as between several groups of workers or competing firms. Some assets, however, do not display such flexibility. Physical capital, once invested, can be easily grabbed. There is indeed a growing consensus among economists that expropriation by the government or powerful elites is a decisive hindrance to development. Checks against state predation—in other words, institutions of property rights protection—have indeed been shown to be good predictors of long-run economic development (Acemoglu, Johnson, and Robinson 2001, 2002; Acemoglu and Johnson 2005).

While the previous section examined the political features of a simple productive framework, I now turn to the second model announced in Introduction section, where I relax the assumption of perfect property rights or, equivalently, of effective enforcement of the sharing rule. These two sections are independent. From now on, one group is assumed to be in power; the second model does not consider how it came to be in that position. In particular, I do not consider how the prospect of having to invest in property rights institutions may affect the stakes of winning the contest game introduced in the previous section.

If there is no property rights protection, assuming group A is in power, it cannot be counted upon to meet its commitment after production has taken place. Group B expects that whatever sharing rule A offers, it might in fact get nothing. Without credible enforcement of the sharing rule, there can therefore be no common production.

If property rights protection is imperfectly enforced, B now expects A to renege on the initial offer with probability p. In this case, it gets only its own specific production. With probability 1 − p, though the sharing rule is effectively enforced. This situation corresponds for instance to an uncertain judicial or political environment: A may be able to corrupt the judge or the politician (but they cannot count upon successfully doing so) or maybe the enforcement scheme is itself found lacking. Such a scheme can also rely on an exterior third-party enforcer, such as in the case of conditional development aid: in that case, reneging on the contract may provoke the interruption of financial disbursements and thus entail immediately adverse consequences in terms of A’s utility. Coming back to the model, a high p means poor property rights enforcement, and a low p good property rights. As announced in Introduction section, the sequence of play is now:

A invests in institutions and sets the sharing rule both groups invest and produce, and

A tries to renege. If it succeeds, its members share the joint output. Otherwise,

If A offers the sharing rule

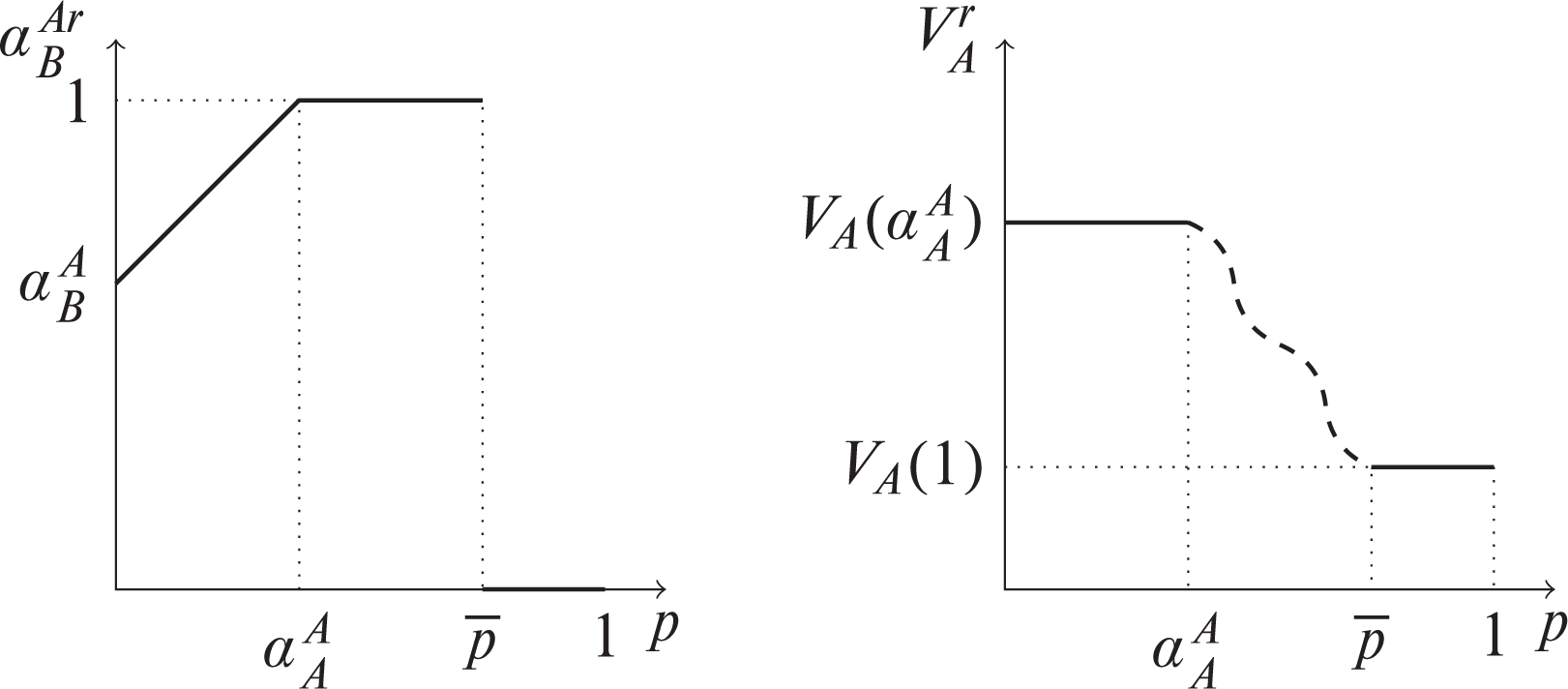

Let me write αA, the sharing rule they would have implemented under perfect property rights protection. Whenever possible, they would set

Notice that if p is high enough, the resulting investment may leave A worse off than if it simply retained the full common production, even at the cost of B’s participation. Let me define

A’s optimal offer with imperfect commitment (left) and his resulting utility (right) as functions of p.

The utility derived by B from A being in power but constrained by p also is nonincreasing in p. As a result, we get that

I have until now considered institutions as exogenous. Let me now consider the incentives to invest or possibly disinvest in such institutions. Assume that it is possible to invest in the commitment capacity of the state. Formally, the state commits to restrain itself from predation. To increase the credibility of the professed sharing rule, group A, who is in control of the state, reduces the likelihood of himself reneging by investing in an external commitment mechanism. To reach a level p, they pays a cost C(p), nondecreasing: a higher commitment involves higher costs. This typically may correspond to the cost of an independent judicial system as third-party enforcer. 9 Formally, their full program can thus be written:

Previous computations remain valid, and A’s final valuation can be written

Proposition 4 offers two essential conclusions. First, a group in power has a higher incentive to commit to upholding their sharing rule offer (lower

Second, a positive profitability shock may reduce the incentive of the group in power to commit to upholding their sharing rule offer. The more profitable the common activity is, the less likely the emergence of good property rights. Anecdotal evidence of successful businesses taken over by relatives of the ruling elites abound in developing countries, and it may even be possible to argue that some patterns of taxation follow the same rule in developed countries: the state (for which the group in power accounts in this model) has a tendency to increase rent extracting as an activity becomes more profitable and on the contrary to reduce it as it becomes less so.

Note that the mechanisms which are highlighted here are not only very intuitive, they are also static. Previous works have highlighted other possible motives to invest or disinvest in institutional quality (Bourguignon and Verdier 2009; Besley and Persson 2010; Bourguignon and Verdier 2012) in a dynamic context. It is interesting, however, that a static framework is already sufficient to provide some important insights into these motives.

The Case of Mauritius

The theoretical results presented above offer new insights into the stylized facts mentioned in Introduction section: the discovery of mineral resources generates internal economies of scale within the mineral sector. Internal economies of scale create large rents when the sector is consolidated in few hands. In the terminology of this work, entrepreneurs and rent seekers aspiring to consolidate it are substitutes. This article shows how that fuels conflict and possibly discourages investment in state capacity. Conversely, changes in the technology of production can have an opposite effect. For instance, improvements in manufacturing and industry may create supply chains and transformation industries and external economies of scale. Industrialization, or tertiarization, of a country transforms distinct individuals or groups, from substitutes, to complements. Even without a technological change, a shock affecting the profitability of one activity over another changes the interaction between groups. This provides a more general interpretation to the empirical results of Dube and Vargas (2013).

Given the negative consequences of political competition over mineral resources, it is surprising then that some countries have managed to develop in spite of macro conditions that at face value would seem likely to make them fall prey to the resource curse. Barro’s (1991) cross-country growth regressions identify several such success stories, including Mauritius. Based on its demographic characteristics, geographic location, and resource endowments, one would expect its development to track that of comparable countries, which is to say, it should have remained poor and marred by civil conflicts. Yet not only did Mauritius achieve high and sustained levels of growth since independence, but all indicators of governance, competitiveness, and democracy position it at the top of African countries. To date, there have been very few successful attempts to explain the peculiarity of such a success story (Silve [2012] provides a review of the literature on the development of Mauritius and offers a more detailed assessment of its success). The theoretical results of this article shed light on several factors that underline its seemingly oddly triumphant development trajectory.

Mauritius is a densely populated, fertile island in the Indian Ocean, with no known mineral resources. At independence, in 1968, its economy was among the poorest in the world; sugar cultivation was the main economic force, representing as much as 20 percent of its Gross Domestic Product and 60 percent of export receipts. A few years earlier, the Governor of Mauritius had commissioned future Nobel Prize winner James Meade and his team to study the potential for development of the small island. Their conclusion was damning: “Heavy population pressure must inevitably reduce real income per head (…) That surely is bad enough in a community that is full of political conflict (…) the outlook for peaceful development is poor” (Meade 1961). More than a decade later, a more literary assessment still read: “The disaster has occurred (…) now given a thing called independence and set adrift, an abandoned imperial barracoon, incapable of economic or cultural autonomy” (Naipaul 1972, 270).

Until recently, Meade’s and Naipaul’s general intuition, that ethnic heterogeneity at the country level usually hinders growth, seemed to find good support in the academic literature (for a review, see Alesina and La Ferrara 2005). The peaceful development of ethnically diverse Mauritius was all the more surprising. Some unrest in 1999 was attributed to enduring ethnic tensions. However, in hindsight, it was only an isolated occurrence. In other words, Mauritius seems to indicate that ethnic heterogeneity is not a sufficient condition for conflict to arise. The mechanism presented here qualifies that intuition. Heterogeneity and substitutability may indeed generate conflict, hinder growth, and favor bad institutions. But heterogeneity and complementarity may on the contrary encourage peace, growth, and investment in good institutions.

More recent research go precisely in that direction. First, city-level studies tend to find a positive association between growth and heterogeneity (Ottaviano and Peri 2005, 2006; Sparber 2010; Lee 2011, 2015; Alesina, Harnoss, and Rapoport 2016). All these studies were conducted in industrialized countries, which arguably generate complementarity, whereas Alesina and La Ferrara (2005) had emphasized low income to be a condition to trigger the negative impacts of heterogeneity. Montalvo and Reynal-Querol (2016) rightly emphasize that both cross-country and city-level analyses generate endogeneity concerns. They also point out that the size of the community under consideration matters, which is consistent with the fact that the same activity can generate positive externalities locally, and negative ones at the national level.

Sugar cultivation was the historical activity and source of wealth in the country. It is an unskilled labor-intensive activity. Sugar cultivation, despite being historically dominated by a Franco-Mauritian elite, is relatively decentralized (23 percent of the production is accounted for by planters whose plot size is less than four hectare). Early, it generated a sugar processing industry famous for its special sugars (light and dark Muscovado, dry, fine, and standard demerara, light and dark brown soft, molasses, etc.). Direct positive spillovers of the sector included the production of electricity from bagasse and ethanol from the molasses and the shaping and the preservation of the landscape of the island.

Meanwhile, the prospect of the Multi-Fibre Agreement was leading overseas investors, from Hong Kong in particular, to look for adequate investment destinations to make up for the quotas imposed on Asian textile exports. The capital accumulated in the sugar sector, and the managerial expertise already present in the country, made Mauritius a choice destination. Soon, the textile sector came to be composed of vertically integrated factories from the spinning stage to the final fabric. The textile industry fueled related industries such as clothing manufacturing. More importantly, the textile industry helped develop the export infrastructure of the country, both physical and institutional, with positive spillovers in other industries.

Indeed, in 1971, Mauritius passed the export processing zone (EPZ) act. Its intention was to help textile manufacturers explore niche markets overseas, and two decades later, half of the firms in the EPZ were engaged into garment making, employing up to 80 percent of labor in the zone. Quickly, though, the EPZ came to cover a number of other manufacturing activities, in particular electronics and small machinery, which benefited from the capital accumulated in the sugar and textile sectors, from the probusiness institutional setup, and from an increasingly educated workforce. This diversification was fueled by important capital inflows in the 1980s, attracted by the political stability of the country as much as by the legal and fiscal advantages given to Foreign Direct Investment.

Traditional accounts of Mauritius’s successful development rest on five “pillars” of its economy: sugar, textiles, the EPZ, tourism, and offshore business. The pervasive bilingualism of Mauritians is certainly key to the success of the last pillar. But the quality of the workforce and the attractive business conditions, both a consequence of the EPZ, are equally important factors. While the success of tourism is arguably less reliant on the success of the other pillars, certainly the visibility and reputation of the island, thanks in large part to its commercial and financial ties with other countries, did not harm. Finally, economic growth in Mauritius has remained inclusive over the decades, and the resulting economic inequality in the population is low from an international perspective.

Sugar cultivation, the textile industry, tourism, the export-processing zone, and finally offshore business are increasingly capital-intensive activities. Capital-to-labor ratios in Mauritius increased steadily over the decades. In this context, the mechanism suggested by Dal Bó and Dal Bó would suggest to look for increasing tensions. However, according to the Economic Intelligence Unit, a London-based company within the Economist Group that publishes an index of democracy around the world, Mauritius is ranked first in Africa for the quality of its democratic process, on par with most Organization for Economic Co-operation and Development countries. Power has been peacefully transferred several times between competing political parties since independence, a unique achievement among countries in Africa and in the Indian Ocean. The consensus is that the country managed to grow fast for a long period of time and avoid the social conflicts that some believed would be inevitable in such an ethnically diverse polity.

This article offers a mechanism to explain why: as I have argued, the five pillars generated opportunities for complementary industries to emerge. Complementarity between groups reduced the potential for conflict. Proposition 2 and its Corollary 1 predict that conflict should in fact be limited in Mauritius.

Furthermore, Proposition 4 predicts that complementarity would provide an incentive to invest in the regulatory capacity of the state. How does this prediction compare to the facts? Prominent indicators of institutional quality (Doing Business and World Governance Indicators of the World Bank, Global Competitiveness indicator of the World Economic Forum and the Ibrahim index of governance) all position Mauritius within the first three spots in Africa along all dimensions. Complementarities indeed seem to have paved the way for peaceful development and also to have encouraged the emergence of good regulatory institutions.

Hong Kong and Singapore offer a similar story. The capital-to-labor ratio increased quickly, but conflict never erupted to derail their dynamic process of development. Both countries focused on attracting multinational corporations and on setting up free economic zones to encourage export-oriented industries with positive spillovers. Unemployment remained very low from the 1960s until the Asian crisis of the late 1990s, a consequence of the complementarities discussed throughout this article. In line with the predictions of this article, no major civil conflict erupted in either country, and both built state institutions thought to be extremely reliable by investors: the World Economic Forum ranks Singapore second in the world for its overall competitiveness and Hong Kong seventh.

Conclusion

This article has demonstrated that mineral extraction is indeed a productive opportunity that creates high substitutability between groups of workers and, presumably, is highly profitable. I have provided a mechanism whereby abundant mineral resources tend to be associated with more frequent and more violent conflicts, as well as a new intuition for why mineral-rich countries do not develop good property rights institutions and, more generally, regulatory state capacity. Political competition is motivated by the potential for economic gain from controlling the proceeds of the common production, a gain that is worth less when the two groups’ assets are more complementary. Since conflicts are costly, mineral wealth may be hard to take advantage of, and this mechanism goes so far as to explain why additional wealth created as the result of an exported commodity price increase may be wasted entirely. Going one step further, if the conflict is destructive or if, as is likely, there is a trade-off between fighting and producing, the resource curse appears immediately: a price increase might indeed result in reduced social welfare for certain technologies of conflict.

The mechanism extends to encompass any kind of formal productive activity, which it characterizes by the level of complementarity between available productive resources. The history of Mauritius is one of the several possible narratives of how activities with positive spillovers on further investment and employment promoted inclusive growth, a peaceful democratic process, and good property rights institutions. Microeconomic evidence is scarcer. Jha (2013, 2014) and Becker and Pascali (2016) are notable exceptions, with their work on the medieval ports of South Asia and on the competition in the banking industry in Germany. Future research could extend the work of Dube and Vargas (2013) to also account for a capital-intensive industrial activity. The first model proposed in this article would predict that if that activity also generates complementarity between groups, it may actually have the reverse, appeasing effect.

Finally, let me call to mind that the two models presented here are static. This creates opportunities for future research. In particular, Proposition 3 on inequalities is treated almost as an afterthought in the main text (though the Online Appendix provides an assessment of inequalities in more detail). It would be especially interesting to explore how complementarities contribute to the accumulation of the two assets, and how complementarities might increase or reduce inequality, in a dynamic version of the setup.

Supplemental Material

Supplemental Material, Onlineappendix - Asset Complementarity, Resource Shocks, and the Political Economy of Property Rights

Supplemental Material, Onlineappendix for Asset Complementarity, Resource Shocks, and the Political Economy of Property Rights by Arthur Silve in Journal of Conflict Resolution

Footnotes

Acknowledgments

My gratitude goes to Gani Aldashev, Sylvain Dessy, James Fenske, Jeffry Frieden, Perrin Lefebvre, David Martimort, David Pérez-Castrillo, Steve Rankin, and especially Thierry Verdier and two anonymous reviewers for their help in improving the article. I also thank participants to the CRED workshop in Namur, the Cooperation or Conflict conference in Wageningen, the ISNIE conference, and the DIAL development conference for their comments.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplementary material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.