Abstract

In this article, we provide evidence that civilian and military government spending have specific characteristics that can affect private consumption differently. Our vector autoregressive (VAR) estimates for the US economy for the period 1960–2013 show that civilian expenditure induces a positive and significant response on private consumption, whereas military spending has a negative impact. We also analyze the effects of these public spending components for the subsamples 1960–79 and 1983–2013, respectively. Our results show that the main transmission channels of both civilian and military expenditures have changed over time. We adopt a new Keynesian approach and develop a dynamic stochastic general equilibrium (DSGE) model in order to simulate the empirical evidence. Both the larger persistence of shocks in military spending and the different financing mechanisms, which account for the propensity of policymakers to use budget deficits to finance wars, mimic the differences in the empirical responses of private consumption. Simulated impulse response functions of alternative specification models prove the robustness of our analysis. In particular, we assess the impact of civilian and military shocks in the presence of different (i) shares of heterogeneous households, (ii) price rigidities, and (iii) monetary reactions in response to different government shocks.

Keywords

Introduction

Recently, US public opinion has shown renewed interest in the economic impact of fiscal policy. At the end of 2013, an intense debate and media coverage concerned the US federal government shutdown. The tensions that ultimately produced this shutdown arose due to the different perspectives of policymakers concerning the deficit reduction through a simultaneous increase in tax rates and decrease in government spending. 1 The main motivation of this debate is that the economic literature did not provide conclusive results regarding how public expenditure and its financing mechanism can affect the economic performance of the private sector. In general, contrasting results mainly depend on the theoretical perspective and the empirical methodology used (Cogan et al., 2010).

The neoclassical approach suggests an intuitive explanation to account for the economic effects of large cyclical rises in government spending. Based on major unexpected political events, it assumes that the periods of increased military spending correspond to the dates of war or threats of war. Ramey & Shapiro (1999), later extended by Ramey (2011), proposed a so-called ‘narrative’ approach, which selected the start of the three wars in which the USA actively intervened (i.e. Korean, Vietnam and the Soviet invasion of Afghanistan) and the 2001 terrorist attack, to identify empirically large exogenous increases in US defense spending. The significant criticism of this approach (modeled by the ‘expectations augmented vector autoregressive’ – EVAR – specifications) is that other substantial fiscal shocks may have occurred at the same time. In turn, these other shocks may interfere with the identification of military shocks, implying distorted results. 2

The economic literature has proposed an alternative approach to test the effects of fiscal policy on economy. In particular, a large set of studies has focused on structural vector autoregressive (SVAR) models with differences in the identification issues of fiscal shocks. 3 Although Bouakez, Chihi & Normandin (2014) have recently criticized this approach, Perotti (2014) has clearly shown that SVAR models properly identified achieve the same results as the EVAR by Ramey (2011).

In this article, we review the economic consequences of changes in US fiscal policy following a baseline SVAR model extended for the fiscal components of military and civilian spending. The main question of interest is whether unexpected military and non-military expenditures produce ‘contractionary’ or ‘expansionary’ effects on private consumption, respectively. We contribute to the existing literature by showing that differences in private consumption effects are based on how the shocks of government spending components are driven by their persistence and types of financing mechanisms.

We base our hypotheses on the findings of Gali, Lopez-Salido & Valles (2007) who show that a positive government spending shock leads to a significant increase in private consumption when defense expenditure is excluded. Accordingly, they infer the hypothesis that military spending has a negligible or negative impact on consumption. However, previous literature found conflicting empirical results about the effects of different public spending components on consumption and other macroeconomic variables. Using a partial equilibrium model, Pieroni (2009) has shown that private consumption responds negatively to military expenditure increases. In terms of private investment, the findings by Smith (1980) showed the so-called ‘crowding-out’ effect. On the contrary, Aschauer (1989) provided evidence that positive government spending shocks induced an increase in private investment. More recently, F-de-Córdoba & Torres (2016), using a DSGE model with a security factor in the utility function, have found that the increase in the external threat induced a rise in military spending, investment and output while it reduced consumption. Finally, Malizard (2015) provided evidence of a positive effect on private investment due to military equipment spending (considered as public investment) for the case of France.

As in Blanchard & Perotti (2002), who estimated output fiscal effects, we report a comparison of the vector autoregressive (VAR) effects of military and civilian spending shocks on consumption for the USA: although we estimate a negative effect of military expenditure on consumption, our results show that civilian government purchases have a largely positive effect on private consumption. In order to check the robustness of our empirical analysis, we compare the different impacts of civilian and military spending for two subsamples that correspond to the periods before and after the ‘great moderation’. 4 Our results indicate that the transmission channels of both civilian and military shocks have changed over time. Regarding civilian spending, we find that the responses of macroeconomic aggregates are less significant in the post-1980 sample. On the contrary, the effects of military shocks are mostly significant in the second subsample.

In this article, following the most recent literature (see, among others, Jacob, 2015), we develop a new Keynesian model to mimic the empirical results. This framework offers the advantage of taking into account forward-looking expectations of households and firms, and encompasses many ingredients of modern dynamic optimizing sticky-price models, although it is modified by allowing for the presence of consumers subject to credit constraints. In particular, we consider an economy populated by a continuum of infinitely lived households that are divided into Ricardians and non-Ricardians. Ricardians can trade securities and accumulate physical capital, whereas non-Ricardians do not have access to capital markets and simply consume their current labor income. 5 The advantage of such an approach is straightforward. Despite the negative wealth effect associated with an increase in the tax burden, the response of aggregate consumption to a spending shock can be positive under the presence of non-Ricardian consumers (Gali, Lopez-Salido & Valles, 2007).

In our theoretical model, we extend the original framework of Bilbiie, Meier & Muller (2008) by disentangling civilian and military spending shocks. We motivate our framework according to the two main findings of our empirical estimates. First, we observe a stronger persistence of military spending shock than civilian spending shock. In particular, the high persistence of the military spending shock increases the negative wealth effect on Ricardian households and further lowers their consumption spending. As a consequence, we observe the fall in aggregate consumption in response to this shock. Second, our empirical estimates show the effects of a different financing mechanism of civilian and military expenditures. The former is mainly financed by the increase in taxation rate, while the latter is mainly funded by government budget deficit. In this regard, the heterogeneity of consumers also implies different transmission channels through which fiscal policy affects the economy. In our analysis, this issue is particularly important in order to examine the different effects of military and civilian spending. In contrast to Favero & Giavazzi (2007), who explicitly include the long-run government budget constraint, the new Keynesian model presented below comprises, along with a taxation rule, a deficit financing rule.

Our simulated results of the baseline new Keynesian model show that private consumption responds positively to civilian spending whereas military expenditure negatively affects private consumption. Some robustness tests are presented in order to compare the dynamic responses of private consumption to a different persistence and financing mechanisms of civilian and military spending shocks. We also analyze the impact of these two components of government spending on private consumption in the cases of different shares of Ricardian households and degrees of price rigidities. Finally, we assess the effects of different fiscal shocks when monetary policy changes.

The rest of this article is organized as follows. First, we discuss the basic literature and some stylized facts of how the USA finances government spending. Second, we present our empirical specifications illustrating the data and discussing the empirical results. Third, we present our theoretical framework and the model calibration. Fourth, we examine the simulated impulse responses of consumption to the different government spending shocks and the robustness analysis. Finally, we offer a concluding discussion.

Private consumption and the financing mechanism of military expenditure

Barro (1979, 1981) conducted several studies highlighting the economic effects of government spending and the alternative methods and impacts of financing this expenditure. In particular, Barro (1981) stressed the fact that government expenditures can provide direct welfare to economic agents and that variations in the level of government expenditure may have an impact on the consumption decisions of households. Based on this work, one strand of the literature shows that different financing sources of public sector components lead to heterogeneous effects on private consumption when consumers are constrained in their asset purchases.

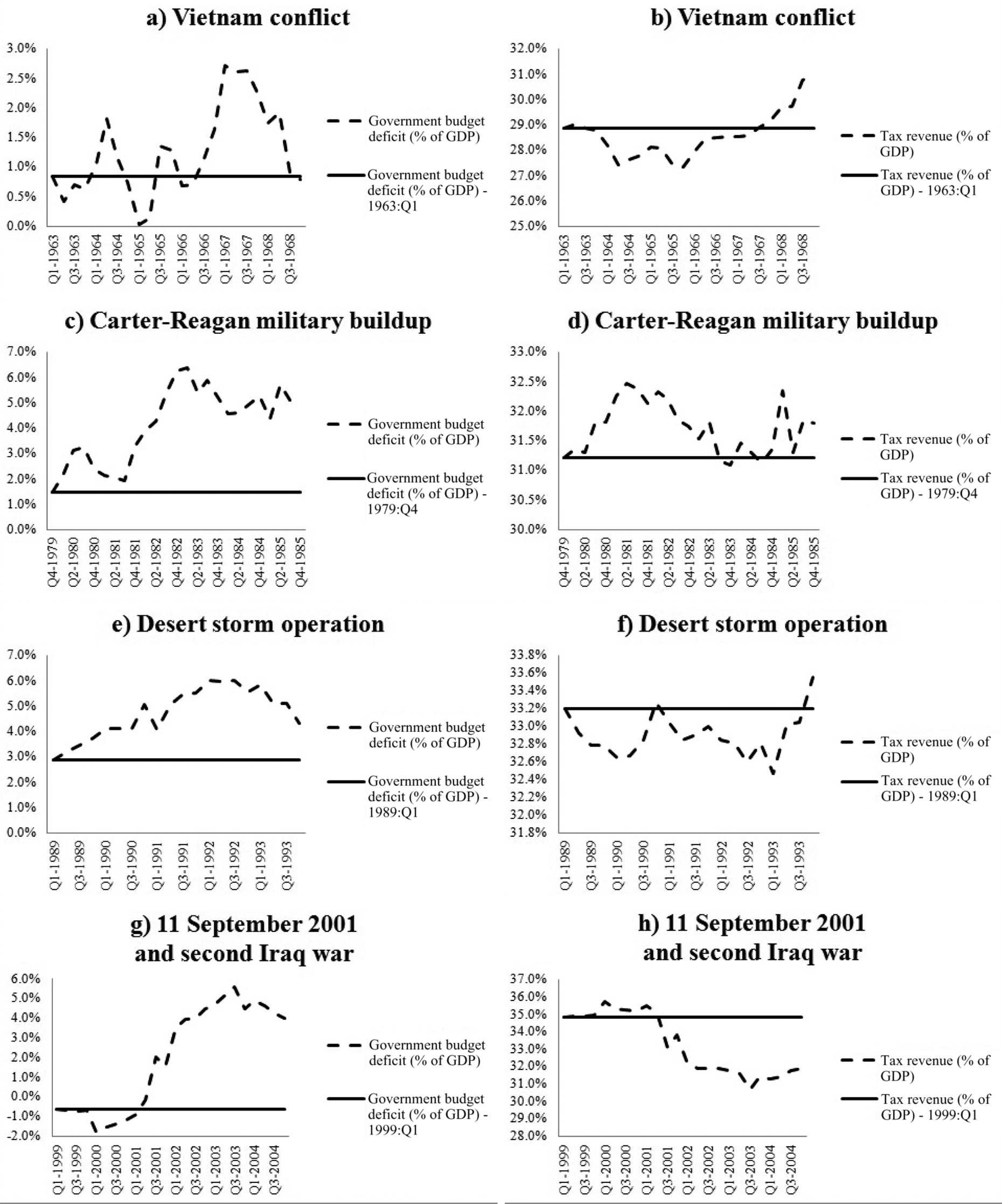

In this section, we focus on the different mechanisms used to finance military spending in the USA. We focus on the shocks near wartime, including threats of war. Our analysis follows the US war episodes described by Ramey (2011) except for the Korean War, which is outside our sample. In particular, we focus on the patterns of government budget deficit and tax revenues. In this regard, in the left column of Figure 1, dashed black lines indicate the ‘actual’ patterns of US government deficit in each war episode. As a comparison, solid black lines denote the ‘counterfactual’ levels of government budget deficit, assuming no change relative to the first quarter of each war episode. Similarly, the right column of Figure 1 shows the same comparison in the case of tax revenues. We observe that government deficit substantially increases in all these episodes. On the contrary, tax revenues fall over the same periods. The only exception is the Carter–Reagan military buildup. However, we note that this increase is much lower (about 1%) than the rise in government deficit (about 6%) implying that almost the whole burden of military outlay has been financed through borrowing from the public.

Financing mechanisms in the US for military conflicts and episodes

We emphasize our article’s contribution arguing that the effect of military spending on private consumption also depends on the financing mechanism. In particular, unplanned episodes such as wars are generally financed by budget deficits. Thus, from a Keynesian perspective, since greater military outlay is not offset by the contraction induced by higher taxes, wars typically cause a short-term economic boom boosting aggregate demand and consumption. As argued by Nincic & Cusack (1979) and Krell (1981), this is one of the main economic explanations of increases in military spending. However, Barker, Dunne & Smith (1991) have shown that such increases have contractionary effects on the UK economy. In particular, these authors assumed that the defense reductions are matched by balanced increases in other public expenditures. As a consequence, they found that consumption expenditures and GDP increase in response to cuts in military spending. Given these conflicting findings, our main objective is to provide a more formal assessment of the effects of different public spending components on private consumption, accounting for the several transmission channels through which these shocks affect the US economy.

Empirical evidence

In this section, we empirically analyze several transmission mechanisms through which public spending components affect private consumption. In particular, we estimate the impulse response functions based on the shocks to civilian and military expenditures.

Specification and identification

As a baseline specification of our model, we adopt a SVAR. Its reduced form is defined by the following dynamic equation:

where Yt indicates the vector of variables specified below, A(L) is an auto-regressive lag polynomial, c is a constant term and Ut is the vector of reduced-form innovations. Our analysis is focused on the US economy and our sample period is 1960:Q1 to 2013:Q4, which is chosen for reasons of data availability. In particular, we use the OECD Economic Outlook no. 90 database as primary source for most of our variables. 6 The quarterly series for military and civilian spending are taken from the Bureau of Economic Analysis. As a limitation of our analysis, the absence of long time series at quarterly frequency for government spending components in other countries different from the USA does not allow us an international comparison.

Our empirical strategy based on quarterly data is in line with the new Keynesian perspective, which maintains that a discretionary fiscal policy plausibly does not respond within a quarter to a change in the economy. 7 From an empirical point of view, a substantial issue is associated with the perspective that private agents receive signals about future changes in government spending before these changes take place. This, in turn, should affect the validity of the SVAR representation. In particular, the anticipation effect of the expenditure in the military sector argued by Ramey (2011) may lead to differences in the shock effects of this component on the economy. Therefore, following previous economic literature on this topic, we include dummy variables in the ‘military’ VAR system controlling for anticipation effects. 8 More specifically, these dummies correspond to the dates accounting for the major military events, as described in Ramey & Shapiro (1999). These dates are: 1965:Q1, 1980:Q1, 2001:Q3. 9

We estimate the impulse responses of military and civilian spending shocks separately with a five-variable VAR because they are not significantly linked, identifying different transmission effects on the economy. Following the strategy outlined in Equation (1), first we specify the model analyzing the effects of the civilian component:

where Ct denotes the log of real private consumption, Wt the log of real wage, DINCt the log of real disposable income, BDt the government budget deficit and NMt civilian spending. More specifically, civilian spending is obtained as the difference between government consumption expenditure and national defense data. 10 Both civilian spending and budget deficit enter the VAR as a ratio of current GDP. Our choice is motivated both by the easier interpretation in terms of measurement of consumption responses that are expressed as unit changes and in order to be consistent with our DSGE model (see, for example, Gali, Lopez-Salido & Valles, 2007; Bilbiie, Meier & Muller, 2008). All the remaining real variables are expressed in per capita terms. 11

As an identification strategy for fiscal policy shocks, we adopt a Cholesky factorization in order to recover the vector of structural shocks ∊t (and its variance Ω) from the reduced-form error Ut in Equation (1). It is worthwhile noticing that the structural identification of Blanchard & Perotti (2002) of government spending shocks is identical to a Choleski decomposition, in which government spending is ordered before the other variables. 12 In particular, we assume the following set of conditions. We consider civilian spending as the most exogenous variable. The interaction between civilian expenditure and taxation rate influences the budget deficit: if the civilian spending increase is financed by tax rises, the budget deficit may be negative. Conversely, if a civilian expenditure rise is not followed by a corresponding increase in taxation rate, the budget deficit is positive. We implicitly allow for heterogeneous consumers (namely, Ricardians and non-Ricardians). Because household demand for goods depends on the expected value of taxes (i.e. disposable income), each household subtracts its share of this present value (real wage) from the expected present value of income in order to determine a net wealth position. Lastly, we consider private consumption as the most endogenous variable, which is therefore affected by all contemporaneous values of all the variables in the VAR.

Since our main focus is on the comparison of the private consumption effects of civilian and military shocks, we repeat the same experiment substituting civilian expenditure (NMt) with military spending (Mt) in the VAR model. In this case, the vector of variables Yt in Equation (1) may be expressed as:

Similar to the civilian spending case, military spending enters the VAR as a ratio of current GDP. Again, we adopt a Cholesky factorization in which private consumption, real wages, disposable income and budget deficits are allowed to depend on the fiscal variable (in this case, military expenditure) and are ordered, respectively.

Finally, we focus on one issue that has been highly disputed in the recent literature on the effects of fiscal components on the economy. In particular, many authors (see, for example, Leeper, Plante & Traum, 2010) have argued that the specific characteristic of the government expenditure in VAR models is its persistence driven by the presence of trends. In this regard, military spending has a clear downward trend, while civilian spending is more stationary. 13 In general, the presence of trends in fiscal series (as shares of GDP) is not limited to non-defense spending, but is pervasive. For instance, in the dataset used by Leeper, Plante & Traum (2010) to estimate a DSGE model using Bayesian techniques, tax revenues, transfers and government spending (all as shares of GDP) have different trends. Therefore, we deal with those trends, including the linear trend in the model specification.

Results

We estimate two VAR models according to Equations (2) and (3) in order to obtain the empirical impulse response functions (IRFs). According to the Schwarz information criterion, the number of lags is set to two. Diagnostic tests indicate the absence of serial correlation in the residuals by a Lagrange multiplier test. We do not reject the hypothesis of normality of residuals with Jarque-Bera statistics and check the stability condition of the VAR, finding that all eigenvalues lie comfortably inside the unit circle.

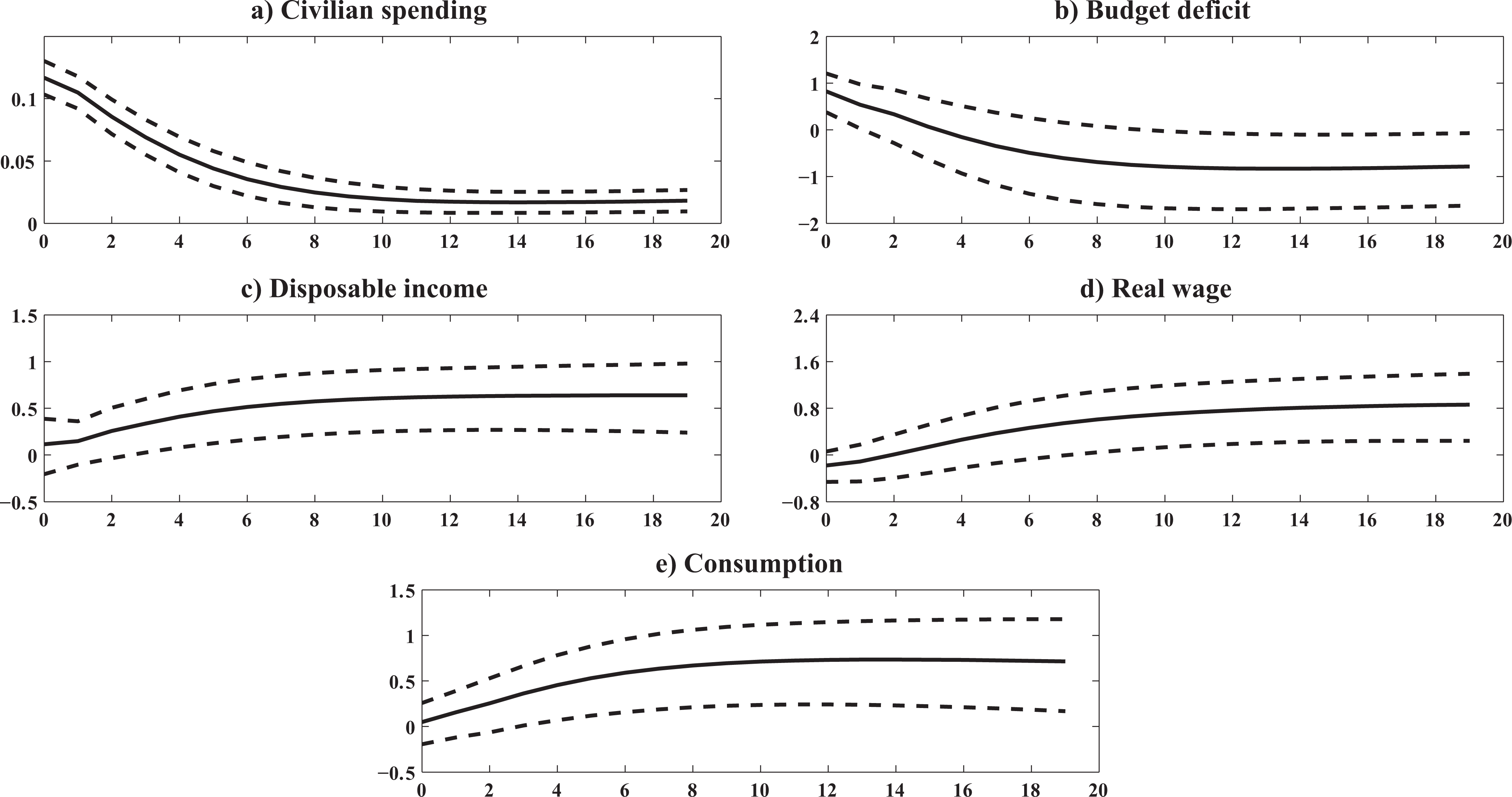

Figure 2 shows the effects of civilian spending on the endogenous variables in Equation (2). In order to derive the 5th and 95th percentiles of the impulse response distribution in the graphs, error bands are computed by Monte Carlo simulations assuming normality in the parameter distribution. Accordingly, we construct t-tests based on 10,000 different responses generated by simulations and check whether the point estimates of the mean impulse responses are statistically different from zero. The responses of the five variables are expressed by multiplying the estimated parameters of the VAR by the sample average share of civilian spending in GDP.

Response of the VAR model to a civilian spending shock

We note that civilian spending (graph a) increases significantly and does not display a large persistence. In contrast to military spending shock, the pattern of persistence decreases with a half-life of about two years. The response of the budget deficit variable (graph b) indicates a contrasting pattern: although it starts positively, it decreases and remains significantly negative, suggesting that unexpected civilian expenditure is financed by an increase in the taxation rate. We observe a positive response for disposable income (graph c) for the time-length considered. This result is in line with the prediction of the new Keynesian models, where the low persistence of civilian spending shock along with constraints in asset market participation reduces the wealth effect on Ricardian households. As predicted by the new Keynesian models, real wage (graph d) shows a positive and persistent response to a unitary shock of civilian spending. Most interestingly, the effect of a civilian expenditure shock on consumption is shown to be significant for a large timespan, persistently above zero (graph e). As we can observe, the response of consumption follows that of disposable income.

Figure 3 displays the IRFs obtained from the VAR expressed in Equation (3) as a response to a positive shock in military spending. Defense expenditure response (graph a) rises significantly, showing a higher persistence with respect to the civilian shock. From the patterns of IRFs, we estimate that the half-life period is above eight years. Graph b pertains to the estimated response of the budget deficit variable, reproducing the evidence that, in the USA, the defense sector is largely financed by budget deficits. The response of disposable income is negative (graph c); this effect is driven by the high persistence of military spending shock that strengthens the wealth effect on Ricardian households. The point estimates shown in the IRFs indicate that the real wage decreases in response to the military spending shock (graph d). Interestingly, as found in the neoclassical literature, the pattern of consumption also decreases its impact (graph e), and the point estimates reveal that the shock may produce a significant effect. The consumption follows the pattern of the real disposable income response.

Response of the VAR model to a military spending shock

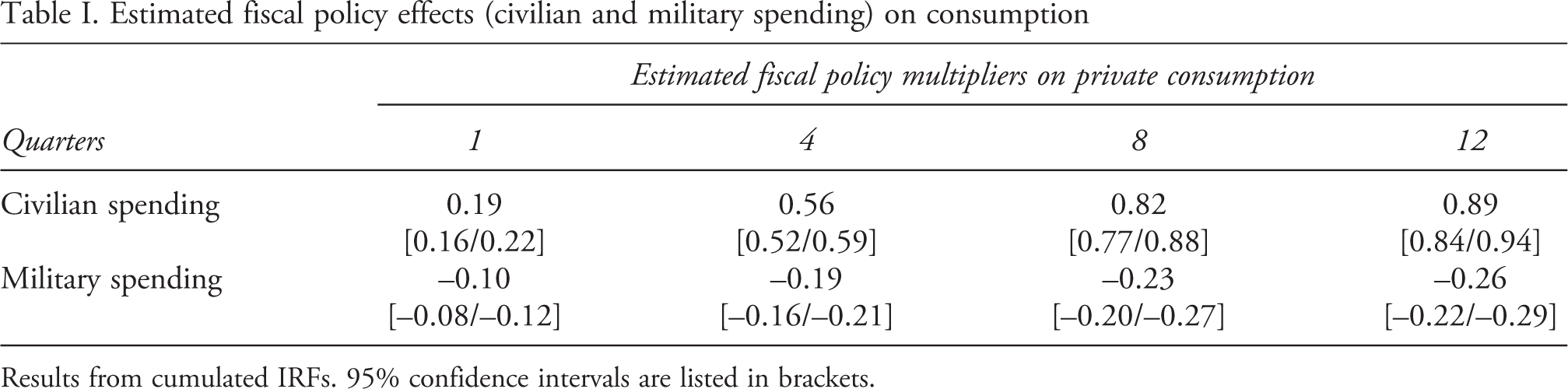

Following the recent literature investigating the stimulative effects of fiscal actions (Drautzburg & Uhlig, 2015; Leeper, Traum & Walker, 2015; Canzoneri et al., 2016), we test the estimated impact multipliers on consumption. In particular, the impact multiplier on consumption measures the change in the level of consumption k periods ahead in response to a change in the fiscal variable of interest given by ΔFt at time t: 14

Thus, the civilian spending impact multiplier is given by

Estimated fiscal policy effects (civilian and military spending) on consumption

Results from cumulated IRFs. 95% confidence intervals are listed in brackets.

Overall, our findings related to civilian spending are in line with the results by Ricco & Ellahie (2012). In particular, we provide evidence that increases in the non-military component positively influence US GDP. Moreover, we confirm the predictions of two articles that have analyzed the impact of military spending on the macroeconomy. First, as in Nincic & Cusack (1979), we find that private consumption falls in response to military spending increases. Second, as in Barker, Dunne & Smith (1991), we show the negative impact of defense expenditure on both consumption and GDP.

Pre- and post-great moderation: Subsample estimates

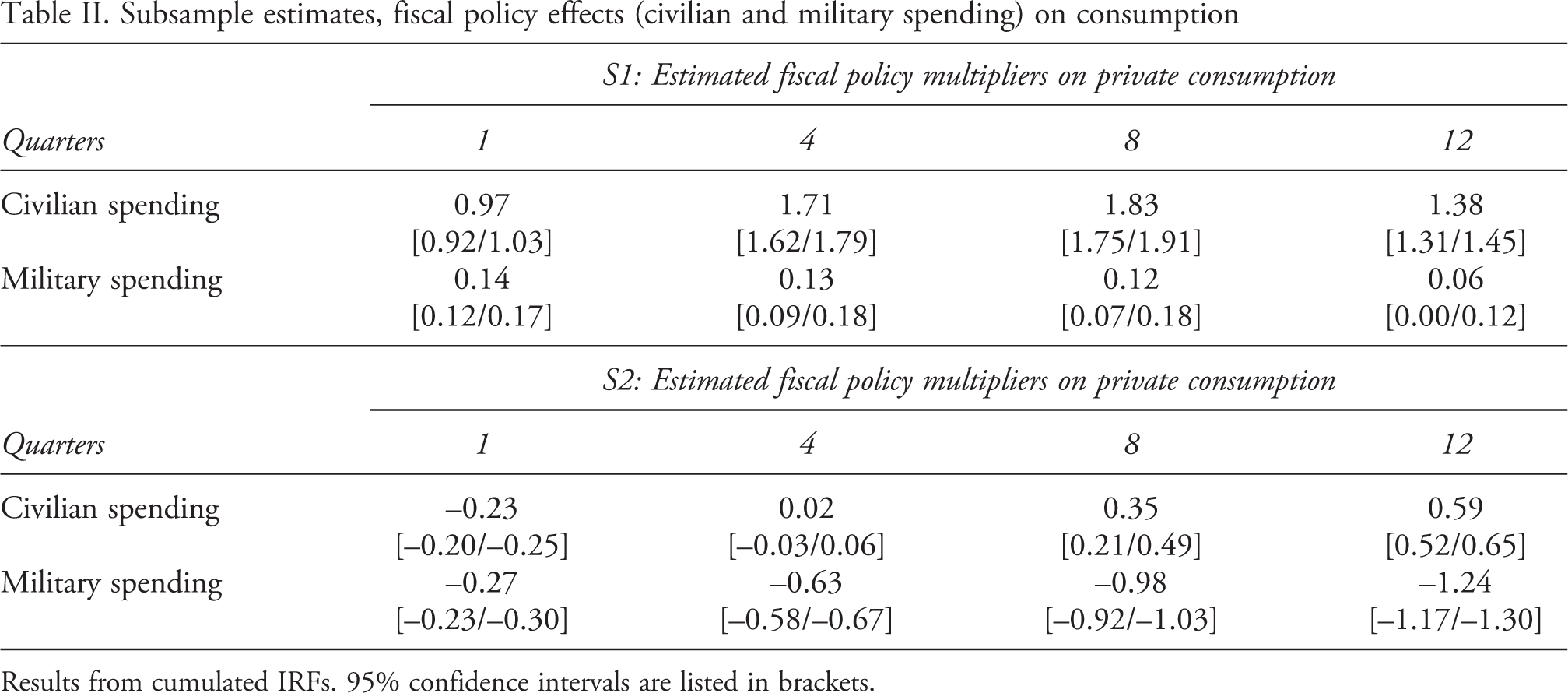

In this section, we compare the different impacts of civilian and military spending for two subsamples in order to check the robustness of our empirical analysis. Our sample choice reflects the well-established hypothesis of a structural break in the early 1980s (see, among others, Smets & Wouters, 2007; Bilbiie, Meier & Muller, 2008). In particular, we assume that the first sample period, the so-called ‘great inflation’, ends in 1979:Q2, namely, the beginning of the Volcker chairmanship. 16 The second subsample starts in 1983:Q1 and corresponds to the more recent period of the ‘great moderation’ in which inflation was relatively low and stable. This sample split captures the general changes in US business cycle dynamics. Therefore, we estimate our civilian and military VARs for the two samples: 1960:Q1–1979:Q2 (S1) and 1983:Q1–2013:Q4 (S2). In the Online appendix, Figures E.2 and E.3 show the estimated IRFs for both the subsamples that we obtained applying the same technique as above.

First, we observe that the persistence of the civilian shock is higher in S2 than in S1. Moreover, government budget deficit falls following this shock in both subsamples. This pattern confirms that, historically, civilian expenditure has been financed through increases in taxation. Disposable income and real wage responses are significantly positive in S1 but not in S2. Interestingly, we find an evident ‘crowding-in’ effect on private consumption in S1, whereas the response is not significant in S2. Accordingly, these results confirm that the differences in the persistence of the civilian shock in S1 and S2 crucially influence the response of private consumption.

Turning to the effects of military spending, we find that the military shock is more persistent in S2 than S1. Moreover, the responses of the US macroeconomic aggregates are negligible and not significant in the pre-1980 sample. On the contrary, the responses of S2 are mostly significant for an extended period. An increase in military spending induces a rise in the government budget deficit. This result confirms the estimated finding of the overall sample, namely, military spending is financed through the increase of budget deficit. Both disposable income and real wage show a negative response to an increase in military expenditure. As a consequence, private consumption falls after the shock.

Finally, we compute the consumption multipliers for both subsamples (Table II). In general, we find that the transmission mechanisms for the different shocks of fiscal components have changed over time. With regard to civilian spending, the stronger persistence of the shock in S2 with respect to S1 implies that the estimated multipliers are systematically higher in the pre-1980 sample. Turning to military expenditure, the lower persistence of the shock in the ‘great inflation’ period induces slightly positive consumption multipliers for all the quarters considered. 17

Subsample estimates, fiscal policy effects (civilian and military spending) on consumption

Results from cumulated IRFs. 95% confidence intervals are listed in brackets.

Theoretical model and calibration

Our theoretical framework is fully consistent with the empirical strategy of the previous section. Indeed, we adopt a solution of our DSGE model that implies that the several variables are expressed as their respective log deviations from the model steady state. Therefore, an unanticipated shock to civilian (or military) spending causes the temporary change of any given variable of our model before returning to its steady state. Accordingly, this interpretation of civilian and military shocks fits consistently with the results of the impulse response analysis of our estimated structural VARs. In what follows, we briefly describe the key features of our model, which follows the framework of Gali, Lopez-Salido & Valles (2007). 18 In particular, the model consists of an economy in which households are divided into Ricardians and non-Ricardians.

As regards labor market structure, it is assumed that there is an economy-wide union setting wages in a centralized manner. Hence, hours worked are not chosen optimally by households, but are determined by firms, given the wage set by the union. The economy produces a single final good and a continuum of intermediate goods. The aggregate production function includes both capital and labor inputs. The total factor productivity is assumed to follow a first-order autoregressive process. The final goods sector is perfectly competitive and is consumed by households.

There is monopolistic competition in the markets for intermediate goods, each of which is produced by a single firm. Moreover, we assume that each intermediate goods producer faces restrictions in the price setting process, as in Calvo (1983). The model encompasses a monetary authority that sets its policy instrument, the nominal interest rate, according to a generalized Taylor (1993) rule.

Turning to the fiscal sector, we assume that the government finances its public spending by issuing bonds and raising lump-sum taxes. Moreover, government purchases are separated into civilian and military components. Accordingly, we assume a fiscal policy rule that includes two different public spending components. 19 Civilian and military expenditures evolve exogenously, following two distinct first-order autoregressive processes. Indeed, we assume that the resources destined for civilian and military sectors are AR(1) processes in line with the dynamic responses of our VAR-based estimates. 20

Finally, the goods market clearing condition requires that the final goods market is in equilibrium if production equals demand by total household consumption, aggregate private investment and total government spending.

We propose a model calibration with quarterly data starting from ‘standard’ parameters extracted from new Keynesian literature. Table III summarizes their values and sources. In what follows, we focus only on the parameters describing the fiscal sector which are estimated from our sample. In particular, the values of the responses of taxes to civilian (φnm) and military (φm) expenditures are obtained as the difference of the estimated effects of the VAR in civilian/military expenditures and the budget deficit. In line with the findings in the literature, the estimates for our sample are of φnm=0.16 and φm=0.18.

Calibrated parameters of the model

Calibration of the parameters based on quarterly data.

We also estimate the persistence parameters of civilian and military expenditures, ρnm and ρm, according to the procedure proposed by Marques (2005), in which the absence of mean reversion of a given series is measured by using the following statistic:

where

Finally, we calibrate the parameter φb such that it is consistent with the necessary and sufficient condition for non-explosive deficit dynamics. Thus, we set φb equal to 0.1. In this regard, the value of the parameter indicating the response of taxes to budget deficit has been estimated by a large number of empirical works (see, among others, Bilbiie, Meier & Muller, 2008; Leeper, Plante & Traum, 2010). In our specific case, since our fiscal rule is very similar to that adopted by Gali, Lopez-Salido & Valles (2007), we chose a value that lies in the range of estimates provided by these authors.

Impulse response analysis of the simulated model

In this section, we present the impulse response analysis for the theoretical model described above. Our objective is to compare simulated IRFs with those obtained from the SVAR. We present the key figures of our analysis in detail in a supplementary Online appendix and summarize those results below.

Implications for the model with heterogeneous fiscal policy shocks

We first discuss the implications of the model in the case of a positive civilian spending shock. In the Online appendix, Figure E.4 shows that the persistence of this shock is very low. Interestingly, this result confirms our empirical findings. In particular, the low persistence of civilian spending shock reduces the negative wealth effect on Ricardian agents. These perceive that the increase in the tax burden in present value terms is only temporary, and they do not significantly change their consumption level.

In addition, one year after the shock, the budget deficit becomes negative and remains persistently below zero for all the horizons considered. Thus, the reduction of the budget deficit moves further resources to consumption of Ricardian agents.

Real wages increase after the shock to civilian spending. This result can be explained by the substantial rise of labor demand, since the civilian spending shock causes an increase in the aggregate demand. Due to sticky prices, not all firms can adjust their prices after the shock. Firms that cannot change their prices are forced to change their production quantity. Thus, in order to increase their output, firms raise their demand for labor and the new equilibrium in the labor market implies a higher real wage. As a consequence, the disposable incomes of both non-Ricardians and Ricardians increase. Accordingly, we observe the so called ‘crowding-in’ effect on total consumption spending. The higher disposable income of non-Ricardians induces a substantial increase in their consumption level, which leads to the rise of private consumption expenditure.

Turning to the effects of a rise in military spending, from Figure E.5 in the Online appendix, we note a high level of persistence of military expenditure in line with our estimated results. As a consequence, the negative wealth effect on Ricardian households is substantial. Indeed, these agents decide to postpone their consumption because they perceive that the increase in the tax burden will last for a long period.

The budget deficit expands after the shock. This result is in accordance with the idea that policymakers in periods of uncertainty, such as wars or threat episodes, react to the conflict challenges and their uncertainty by developing preferences to postpone taxation to future generations. However, the increase of budget deficit further reduces the incentive for consumption in the Ricardian households that end up holding all the bonds issued by government.

The increase in military spending causes a reduction of real wage. This effect is mainly due to a positive shift of labour supply. Non-Ricardians choose to increase their hours worked because of the rise in the tax burden. Similarly, Ricardian households increase their labour supply for a given wage. The new equilibrium in the labour market implies a lower real wage. Therefore, we observe that the military spending shock reduces the disposable income of non-Ricardian and Ricardian households, inducing the ‘crowding-out’ effect on consumption.

Robustness

In line with recent new Keynesian models, our theoretical framework includes several features that allow us to analyze several transmission channels through which civilian and military shocks affect private consumption. First, we focus on the implications of the different persistence of each fiscal shock. Second, we assess the importance of distinct financing mechanisms of public spending. Third, we study the impact of different fiscal shocks in the presence of price rigidities and heterogeneous households (Ricardians and non-Ricardians). Finally, we analyze the impact of different monetary policy approaches in response to distinct government shocks.

Different persistence of shocks and financing mechanisms

We begin by describing the behaviour of private consumption in response to different persistence values of civilian spending shocks.

22

The ‘crowding-in’ effect clearly emerges in the benchmark case (

Focusing on military spending, we consider the following exercise. We start by fixing ρm equal to 0.93. We then decrease it to 0.81 and, finally, we reset it to 0.99. Private consumption responds negatively in the presence of high shock persistence, whereas it increases when ρm is low.

A crucial aspect of our impulse response analysis is also related to the different financing mechanisms of civilian and military spending. As we explained before, in our benchmark calibration, we consider the responses of taxes to civilian ( φnm) and military (φm) expenditures equal to 0.16 and 0.18, respectively. As regards the response of taxes to budget deficit (φb), we assume it equal to 0.1. In the following exercise, we change the values of the parameters φnm and φm, keeping fixed the parameterization for φb. As we show in Figure E.7 in the Online appendix, our objective is to assess the different reactions of total private consumption to these changes.

We start by analyzing the case of a positive shock to civilian expenditure. We assume three different values for φnm, that are 0.01, 0.16 (benchmark case) and 0.99. The ‘crowding-in’ effect on private consumption remains unchanged in all three cases. However, the magnitude of the rise in total consumption expenditure changes substantially. Interestingly, when the response of taxes to civilian spending is particularly high, the increase of private consumption is modest compared with the case of a low φnm. In order to explain the last result, we need to take into account the negative wealth effect on Ricardian households caused by the increase of the tax burden. The high response of taxes to a rise in civilian spending generates a substantial wealth effect on Ricardian agents, postponing their current consumption. On the contrary, if φnm is low, the increase in tax burden is small and Ricardian households do not significantly change their level of consumption. As a consequence, the ‘crowding-in’ effect is larger.

Turning to the military spending shock, the ‘crowding-out’ reduces if the value of φm increases. A low value of φm implies a sharp increase of the budget deficit in response to the military spending shock. This siphons further resources away from potential consumption of Ricardian households because they end up holding all the government bonds. On the contrary, with a high value of φm, the increase of budget deficit is less accentuated. The latter, in turn, reduces the ‘crowding-out’ effect on private consumption.

Heterogeneous households, price rigidities and monetary policy

Although the distinction between Ricardian and non-Ricardian households is crucial for our setup, it is not the only difference between our framework and standard real business cycle (RBC) models assessing the effects of government shocks on private consumption. Indeed, price rigidities and monetary policy play an important role in the response of private consumption to fiscal shocks. In what follows, we provide several robustness checks in order to clarify these aspects. In order to save space we show the IRFs related to these sensitivity analyses in the Online appendix (Figures E.8–E.10).

We begin by analyzing the dynamic responses of private consumption to positive civilian and military spending shocks under our baseline calibration and with different parameterizations of λ. The main results of our analysis do not change if we assume a lower value of λ equal to 0.3. The last result confirms that our model is able to predict the ‘crowding-in’ effect without the presence of a substantial share of non-Ricardian consumers. On the contrary, under the standard assumption of RBC models (accounting only for Ricardian households), our model generates a negative response of private consumption to the increase in civilian spending. Evidently, this is in sharp contrast with the empirical evidence we have shown above.

Focusing on price rigidities and assuming lower values of the Calvo price probability (0 and 0.3, respectively), we find that private consumption falls in response to a rise in civilian expenditure. In the case of military spending, moving from our new Keynesian benchmark toward models with neoclassical characteristics, we find that the negative response of consumption is strengthened. Interestingly, the magnitude of the negative impact is in accordance with the findings in the defense economics literature using partial equilibrium specification. 23

Monetary policy is also a relevant transmission channel of government spending shocks on private consumption. In particular, we assume the case in which all the model parameters have the same values as in Table III except for the policy rate response to inflation (φπ) that varies from 1.5 (benchmark case) to 5 and 10. A high value of φπ implies a more aggressive monetary policy. In the presence of an aggressive monetary policy, the effect of an increase in civilian spending on private consumption is negative. In this case, Ricardian households increase their labor supply as a consequence of the intertemporal substitution effect. This occurs when a rise in inflation triggers an increase in the real interest rate, thus providing incentives for Ricardians to postpone consumption. On the contrary, a less aggressive monetary policy (low value of φπ) implies a lower real interest rate and thereby weakens Ricardians’ incentives to postpone consumption. Finally, as expected, higher values of φπ strengthen the ‘crowding-out’ effect in the case of military spending shocks.

Conclusions

This article analyzed the effects of US fiscal policy shocks on private consumption over the period 1960:Q1 to 2013:Q4. The contribution of our analysis is that we distinguished between civilian and military spending shocks. Our empirical approach allowed us to assess several transmission channels through which these different government components affect the US economy. In this regard, we found that civilian spending shocks are less persistent than military ones. Moreover, our VAR estimates provided evidence that military expenditure is usually financed through increases in government deficit. As a consequence, our impulse response analysis showed that civilian spending shocks have a largely positive effect on private consumption. On the contrary, a negative impact was found between military spending shocks and consumption responses. We also assessed the effects of civilian and military shocks on the US economy for two subsamples corresponding to the ‘great inflation’ and the ‘great moderation’ periods, respectively. Our results indicated that the transmission channels of civilian and military spending shocks have changed over time. In particular, the persistence of civilian shocks is larger in the post-1980 period, implying less significant effects on the several macroeconomic aggregates. On the contrary, the negative effects of military spending shocks are stronger in the ‘great moderation’ period.

As a second step of our analysis, we adopted a new Keynesian DSGE model in order to replicate our empirical findings. In this regard, focusing on increases in military spending, we were able to simulate the negative consumption response of the VAR estimates reproducing the same main transmission channels. First, the high persistence of this expenditure increases the negative income effect on Ricardian households. Thus, these agents reduce drastically their consumption implying the ‘crowding-out’ effect. Second, a positive response of the budget deficit, through which military spending is generally financed, leads to a further reduction in the consumption of Ricardian agents that prefer to hold government bonds. Our model also predicts that the lower persistence of civilian expenditure from its own shocks reduces the negative wealth effect associated with Ricardian agents. When this effect is associated with a strong rise in the real wage, we observe a positive response of aggregate consumption. Indeed, a high real wage stimulates the consumption of non-Ricardians that dominates the fall in consumption of Ricardian households.

Although we believe that this analysis is a useful contribution to more effective management of fiscal policy tools on the expenditure side, it does leave several interesting questions open for future research. In particular, issues in estimating the DSGE model parameters have received increasing interest in the macroeconometric literature. Accordingly, a theoretical framework that includes Bayesian estimation provides promising opportunities for future research.

Footnotes

Replication data

Acknowledgements

Previous versions of this article have been presented several times at the Economics Seminars of the University of Perugia and at the International Conference on Economics and Security in 2011 and 2014. We appreciate the feedback on this article from Paul J Dunne, Ronald P Smith, Fabio Milani and Achim Ahrens. Finally, we would like to thank the Editor of JPR and the three anonymous referees for their comments.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.