Abstract

Does the recurrence of wars suggest that we fail to recognize dangerous situations for what they are, and are doomed to repeat the errors of the past? Or rather that policymakers correctly anticipate the consequences of their actions but knowingly choose conflict? Unfortunately, little is known about how well wars are anticipated. Do conflicts tend to come as a surprise? I estimated the risk of war as perceived by contemporaries of all interstate and intrastate conflicts between 1816 and 2007. Using historical financial data of government bond yields, I find that market participants tend to underestimate the risk of war prior to its onset, and to react with surprise immediately thereafter. This result illustrates how conflict forecasts can be self-fulfilling or self-defeating. Present predictions may affect future behavior, such that wars may be less likely to occur when they are predicted, but more likely when they are not. I also show that the forecasting record has not improved over the past 200 years, and that wars involving democracies lead to greater market shocks. These findings also have implications for the way decisionmakers respond to new information, and how audiences perceive the risk of war and hence their leaders’ actions.

The recurrence of wars, despite their tremendous economic, social, and institutional costs, may suggest that we are doomed to repeat the errors of the past. Time after time, policymakers seem to mispredict the consequences of their actions and fail to recognize dangerous situations for what they are. Can the risks of war be correctly estimated, or do we really only learn from history that we do not learn from it?

Unfortunately, little is known about how well wars are anticipated. Do conflicts indeed tend to come as a surprise to their contemporaries? Or are they correctly anticipated, but decisionmakers choose to engage in them anyway? Using financial data, I examine the reaction of market participants to the onset of all civil and interstate conflicts from 1816 to 2007. If wars are correctly predicted, then those who have a stake in them should not be surprised by their onset. Yet, we find the opposite: investors have historically underestimated the probability of war prior to its outbreak and the onset typically led to a large correction. Market participants, in particular, could often have obtained better returns had they correctly estimated the risk of war.

Whether observers correctly estimate the risk of war matters for several reasons. First, understanding how past observers have fared is a first step in identifying possible ways to improve future forecasts. Second, are there types of war or attributes of the warring countries that increase the predictability of conflict? And are forecasts improving? Third, the findings are relevant to the large literature on the public’s reaction to their leaders’ foreign policy choices. One important assumption in that literature is that the leaders’ choices are clearly and unambiguously understood by those who decide their fate. Audiences may, for example, punish leaders for reckless actions that escalate the risk of war. Yet, if observers misestimate the risks of war, then there are important implications for our understanding of audience costs and costly signals, for example. Can leaders really tie their hands or more generally signal their intentions if the associated risk of war is misestimated?

Finally, the (in)ability of contemporaries to predict might in fact not be an indictment of their predictive ability, but actually be a sign of the reactivity of policy. Indeed, if policymakers adjust their policies by incorporating predictions and reacting to them – perhaps by trying to avoid the war or instead by precipitating it – then wars would not happen when they are expected, and hence would appear to be difficult to predict. Far from implying that we do not learn from history, then, it may in fact suggest that wars are difficult to anticipate precisely because decisionmakers incorporate current predictions into their assessment and react accordingly.

Our results also relate to the evaluation of applied research on forecasting. To assess the quality of our predictions, we must acknowledge their possible effect on policy. This endogeneity means that the difficulty lies not only in forecasting war, but also in evaluating our performance doing so. Forecasts that are based on static variables are unlikely to perform well, and our results therefore call for more dynamic estimation of risk.

The article proceeds in three steps. I first discuss the relevant literature and present hypotheses relating regime type, war type, and predictability of the onset of war. I then review the data used to test this conjecture, including data on government bond yields and control variables. Finally, I show three main results: contemporaries tend to underestimate the risks of war; our ability to estimate this risk has not improved over the past 200 years; and conflicts involving democracies lead to greater shifts in market prices than others.

Markets’ estimation of geopolitical risk

Conflict forecasting has received increasing attention in political science (Beck, King & Zeng, 2000, 2004; De Marchi, Gelpi & Grynaviski, 2004; Gleditsch & Ward, 2013; Hegre et al., 2013). The availability of increasingly fine-grained spatio-temporal data in particular has allowed more refined predictions (Brandt, Freeman & Schrodt, 2011). Data range from stock market prices (Schneider, Hadar & Bosler, 2017), to news reports (Chadefaux, 2014), urban violence (Bhavnani et al., 2014), or climate data (Witmer et al., 2017).

However, we know little about how well wars are predicted by their contemporaries. The existing literature focuses instead on the detection of early warning signals. Yet showing that, say, market fluctuations can help improve forecasts (Schneider, Hadar & Bosler, 2017; Chadefaux, 2015) does not mean that the market’s forecasts were accurate. For example, a small but systematic change in the price of an asset before the onset of war may be sufficient to improve the researcher’s forecasts, but the large shift in price following war would still suggest that the market had misestimated the probability of war.

Guidolin & La Ferrara (2010) do study the reaction of markets to conflict onsets, but are concerned with what can be inferred about their economic costs rather than the adequacy of the market’s forecasts itself. Their goal is to estimate the cost of the conflict by using market reactions as a metric, and not to study the quality of the market’s forecast itself. More importantly, the data they use are not country-specific, with the exception of the USA, the UK, France, and Japan. As a result, these data are not fine-grained enough to infer the market’s reaction to a particular war, except for those involving these four countries. Finally, the limited time span of their data (1974–2004) precludes the analysis conducted here on the evolution and possible improvement over time of forecasts. Other studies that focus on the reaction of financial markets to the onset of conflict are limited to case studies (Rigobon & Sack, 2005; Leigh, Wolfers & Zitzewitz, 2003; Amihud &Wohl, 2004; Hall, 2004; Chen & Siems, 2004; Schneider & Troeger, 2006; Schneider, Hadar & Bosler, 2017; Brune et al., 2015). Tetlock (2005) is more specifically focused on the quality of forecasts, but has no data on conflict and also a more limited time frame.

What we need is an estimate of contemporaries’ beliefs around the time of the onset. Several measures are possible. Reading newspapers, for example, might give us a sense of the perceived probability of war (Ramey, 2011; Chadefaux, 2014). News reports, however, suffer from a major drawback. They are likely to respond to novelty more than to reflect true underlying concerns. Thus, the number of articles about the war after its onset is likely to increase sharply, but that need not indicate surprise – simply that its onset has put it to the fore. That interest may wane once the novelty wears out (see Figure A4 in the Online appendix).

What we need instead is the perception of those who have an incentive to reveal their true perception of the risks of war. Financial markets are particularly well suited for that purpose, because they aggregate the opinion of a large number of participants who have a stake in correctly estimating risk. Through prices, then, market participants reveal their true beliefs about geopolitical risk.

Government bond yields, in particular, are an ideal source of information about the market’s perception of a country’s probability of war. Government bonds (or ‘sovereign’ bonds) are the standard way by which national governments borrow from the market. They are typically issued in exchange for regular interest payments and the promise to repay the principal once the bond reaches its maturity. The price of the bond (and hence its yield) depends on the perceived sovereign risk. A high yield will be demanded when the perceived risk is high, whereas ‘safe’ countries will be able to borrow at low interest rates. If the yield is too low in relation to the perceived risk, investors will prefer other financial assets such as equities, commodities (e.g. gold), or even cash.

A simple model of bond pricing will be useful to understand the effect of the onset of war on bond yields. The price at time t of a government bond with periodic interest payment C (coupons), N payments (e.g. 40 payments for a ten-year bond with quarterly payments), market interest rate rt (typically the central bank’s rate), and value at maturity M (typically 100) can be evaluated as the time-discounted sum of coupon payments plus the discounted value of the repayment at maturity:

The current yield is then simply the nominal value of the coupon C as a percentage of the current bond price Pt, that is,

Wars, in turn, generate three main kinds of sovereign risks for investors. First, the government may fail to pay its debt back, for two main reasons: (a) it may incur so much debt to finance the war that it is unable to repay the principal fully once the bond matures; and (b) the economy may contract so much as a result of the war that the government’s fiscal receipts will plummet and the burden of repaying the debt will become too high. In the notation above, this implies that the expected value of M – the value at maturity – decreases or vanishes entirely, thereby driving down the prices of bonds (and hence increasing their yields, as bond prices and yields move in opposite directions). A second type of sovereign risk is that periodic interest payments might be reduced or cut entirely (i.e. the number or value of C above may decrease). Finally, even if the government honors the terms of repayment without any ‘haircut’, a third risk is the inflation in the currency of the bond that is likely to be associated with a costly conflict. In Equation (1), the market interest rate i, mostly determined by the central bank and inflation, may increase. This inflation reduces the investor’s real return, and hence a higher nominal yield will be demanded today to compensate for this risk. Note that this last scenario implies that central bank rates may mediate the effect of the onset of war on bond yields – a possibility I explore using proper controls and by estimating mediation models (see Online appendix A.3).

Together, these risks imply that a bondholder aware of a forthcoming war should demand a higher yield today. Investors calculate the expected (and discounted) return from a given bond, and all information available is immediately incorporated into the price (Fama, 1991). They trade to reconcile residual differences in their beliefs, and shocks in the yield of bonds therefore signal the emergence of new information that was not expected by market participants. Shocks (or ‘jumps’) in bond prices – changes in prices over a short period of time – therefore mean that new information is at odds with the market’s prior belief. Just as well-anticipated central bank announcements have no effect on asset prices (Poole, Rasche & Thornton, 2002), wars should also not cause any unusual variation if correctly anticipated. A shock then implies either a surprise at the onset of war, or at least that markets believed until the end that war was avoidable. Either way, it means that they misestimated the risk of war. An illustrative example can be found in Online appendix A.1.

Regardless of what drives the jump, a simple way to consider the problem is to think about a ‘no-regret’ clause. Savvy investors who had anticipated the war (or the central bank rate hike associated with it) should have no regret over their investment decision once the war has started. A jump in prices, however, necessarily implies regrets, as many will wish they had sold before the price drop (remember that yields move in opposite direction from prices) and stored their wealth in cash. Even if inflation is a concern, and hence cash is a risky choice, gold, commodities or other assets classes would have been preferable options.

Hypotheses

My first hypothesis relates to observers’ estimates of the risks of war. I conjecture here that wars will be poorly predicted on average, and that investors will tend to underestimate their probability. That is because the estimated probability of war at time t may affect the actions taken by leaders, and hence change the actual probability of war at time t + 1. Leaders assess the future and base their choices on what they have learned from history and their rational expectations given available information. Those who recognize the risks might adjust their behavior and strategy. For example, aggressive states may tone down their rhetoric, demands may be softened, troops might be withdrawn from the border, or rising states may make concessions to alleviate the fears their growth generates (Chadefaux, 2011). Alternatively, forecasts of a distant war may prompt countries to attack now, perhaps before a power shift, so that the initial predictions are again invalidated. On the contrary, states who underestimate the risk of war may behave more recklessly or demand larger concessions in negotiations.

This endogeneity makes it particularly difficult to predict wars with any certainty, as predictions are based on available information, but that information also affects behavior and hence is likely to invalidate the initial prediction – a point related to Lucas’s critique of macroeconomic forecasting based on parameters that are not policy-invariant (Lucas, 1976). I conjecture in particular that predictions of a coming war increase the probability that decisionmakers alter their plans, and hence reduce the probability that war will actually happen then. As a result, wars will be less likely to occur when they are predicted, but more likely when they are not. Therefore, I expect the probability of war to be underestimated on average.

2

Hypothesis 1 (Shock): The onset of a war involving country i leads on average to a sudden increase in the yield of its government bond.

Second, market participants buy or sell assets such as bonds based on the expected revenue stream and price. Expectations of a costly war should therefore lead to a larger impact on the price of the asset. I therefore anticipate that the expected cost of war will negatively affect the yield.

Hypothesis 2 (Costly wars): The onset of a war with large initial fatalities leads, on average, to a larger increase in yields than for wars with low initial fatalities.

Third, if indeed political decisionmakers constantly incorporate newly available information into their policy choices, then counter-intuitively I expect to observe that wars will be very difficult to forecast. Indeed, state leaders informed of a looming war are likely to take steps that will affect its onset. They may strive to prevent it altogether, delay its onset, or on the contrary rush its preparation. These steps will affect the path leading to the onset, and hence possibly invalidate the initial prediction. Because of this feed-forward effect, the wars that are left are those that may not have been predicted, perhaps because they are particularly hard to forecast. In other words, because information and forecasts affect behavior itself, wars may always be ‘in the error term’, and no matter how much our prediction ability improves, the wars that do occur would always come as a surprise. If they had not, they might have been prevented, postponed, or rushed. If that is the case, that is, if wars are indeed in the error term because of this feed-forward mechanism, then the lessons from history may help prevent wars, but they will not avoid our surprise at those wars that do occur – the wars that we failed to forecast. An implication of this argument is that the wars that we do observe should be as surprising today as they were at the beginning of our sample in 1816, and no significant pattern should emerge over time.

Hypothesis 3 (Constant predictability): The average magnitude of the shock associated with the onset of war is constant over time.

My next hypothesis relates to regime type. The effect of regime type on forecast is difficult to assess a priori. On the one hand, democracies tend to be more transparent, and hence their policies and decisions are more easily and reliably observable, both to other states and to domestic audiences. This would intuitively lead to easier predictability of their actions. Yet transparency implies that their policies are also more likely to be challenged domestically or to receive unwanted attention from the media. This has two effects. First, policy will tend to be nimbler, and hence more reactive to updates in the perceived probability of war. Just as liquid financial markets are less predictable than illiquid ones, decisionmakers who incorporate new information or parameters rapidly push the current policy to the point where it is no longer easily predictable. The public’s reaction to the expectation of war, for example, may lead to adjustment in the government’s policies, making prediction more difficult (e.g. the Fashoda crisis, see Schultz 2001: 175–196). A second effect is that this attention and the potential challenges from the opposition and the media may lead democratic leaders to be particularly discreet about their plans, so that their opponents may not discover them, and wars are therefore more likely to come as a surprise. As a corollary, autocracies and their leaders may be more predictable, and their preparation for war more obvious. Counter-intuitively, then, the transparency that characterizes democracies may lead to a lower predictability of their foreign policy choices.

Hypothesis 4 (Regime type): The onset of conflict in democracies is associated with a larger average shock than in autocracies.

I also expect civil wars to be more predictable than interstate wars. First, actors in civil wars are less clearly defined than in interstate wars. For rebels to even identify themselves may be risky, and their forces may need to build over a significant period of time before they reach a size sufficient to challenge the central government. These buildups will therefore be more visible and predictable than the sudden mobilization that characterizes interstate wars. In addition, low-level skirmishes, which do not reach the level of conflict per se, may be more frequent than in interstate wars, thereby signaling the rising level of tensions to market observers. Bargaining tends to be stickier. Moreover, civil wars often rely on deep animosities and built-up tensions. These may be harder to reverse than in the case of interstate wars, where a clear chain of command will help prevent escalation and accidents. Civil wars, then, are expected to be easier to predict because their dynamic may be harder to reverse and their buildup slower and more visible.

Hypothesis 5 (Conflict type): The onset of interstate conflicts is associated with a larger average shock than the onset of intrastate conflicts.

Do wars really come as a surprise?

Demonstrating surprise is difficult. In the absence of an explicit estimate from market participants of their beliefs about the probability of conflict, we must infer them from observed valuations and fluctuations. I adopt a threefold strategy. First, I estimate a regression of changes in bond yields on the onset of conflict using the entire sample. Second, I examine the evolution of yields in the time surrounding the onset of war. Finally, I address the possibility that the corrections I observe simply reflect the stochasticity of the war process, and would hence not be indicative of any market underestimation of the risk of war. Just like weather forecasters may be correct in predicting a 90% chance of rain when in fact it ended up not raining, markets may correctly estimate the pre-onset probability of war, and react with an upward correction once the event is certain. If that were the case, then markets’ forecasts would be correct on average. Yet I find that their forecasts are systematically lower than the actual probability of war, and hence conclude that markets do, in fact, underestimate the risk of war.

Effect of the onset on yields

Data on government bond yields from 1816 to 2007 were collected from Global Financial Data, a leading provider of financial data. The country-level time series are either weekly or monthly depending on the country and period. The ten-year bond was used to the extent it existed, and instruments with shorter maturities were used otherwise. 3 Because many countries never issued them, or only recently started to, data are limited to 45 countries and an average of 3,788 observations by country (see Table A1 in the Online appendix for details). Even though this sample may be biased towards countries with well-established financial systems (typically advanced democracies), it still exhibits significant variation in terms of GDP, polity, and historical background. 4

I first estimate the effect of the onset of war on yields using the full sample of bond yields from 1816 to 2007. This allows us to compare the effect of onsets to other types of events. The dependent variable

Control variables include: the lag of the dependent variable (

Bond yields of a country’s relevant network will also have an effect on that country’s own yields, for two main reasons. First, a change in bond prices in its network may indicate that those countries are likely to engage in conflict. Because allies are more likely to be dragged into a war, such changes in bond yields abroad may suggest an upcoming conflict and hence may push the yields up at home. A second mechanism works in the opposite direction: looming conflict abroad will push investors to search for safer alternatives. ‘Neighboring’ countries are a likely outlet for these investors, who are therefore likely to push down the yields of members of the warring country’s network. To include these effects, I therefore need to incorporate in the model the yields of the members of the network. To that end, I adopt a simple spatial regression framework. First, I obtain a measure of foreign policy similarity (fps) from Häge (2011), from which I infer a connectivity matrix of each country’s network, Wi, an n × n matrix whose i, j element is

Finally, more severe conflicts tend to be costlier, and hence will likely lead to a larger shift. I would therefore like to include a measure of severity, but information about those variables remains undefined at the time of the onset – they will only be known at the end of the war. What we need then is information about severity that was available at the time of the onset. 6 Unfortunately there are no data that documents the breakdown of casualties over the course of the conflict. I address this difficulty in two ways. First, I limit my attention to conflicts of a very short duration. Indeed, if the conflict lasted less than, say, a week, then the market’s correction will reflect information about severity that was available to the market at the onset. I therefore focus on those short conflicts only and include the (logged) number of casualties in that week (fatalities, dispute) and alternatively a dummy variable coded 1 if this short dispute generated any casualties, and 0 otherwise. While this approach deprives us of another important dimension of the cost of conflict, its duration, it allows us to isolate the effect of the fatalities dimension of the cost. My second approach is to use incident-level data from the Correlates of War, which document the number of casualties associated with a specific incident (a dispute may include several incidents). While these data are only available post-1993, they allow us to examine the effect of the onset of all wars (not only the short ones) on yields while controlling for the severity of the initial event. Summary statistics of all variables are reported in Table A4 in the Online appendix. Finally, I note that similar tests using instead the entire sample of all conflicts and measures of duration and fatalities for the entire conflict yield very similar results.

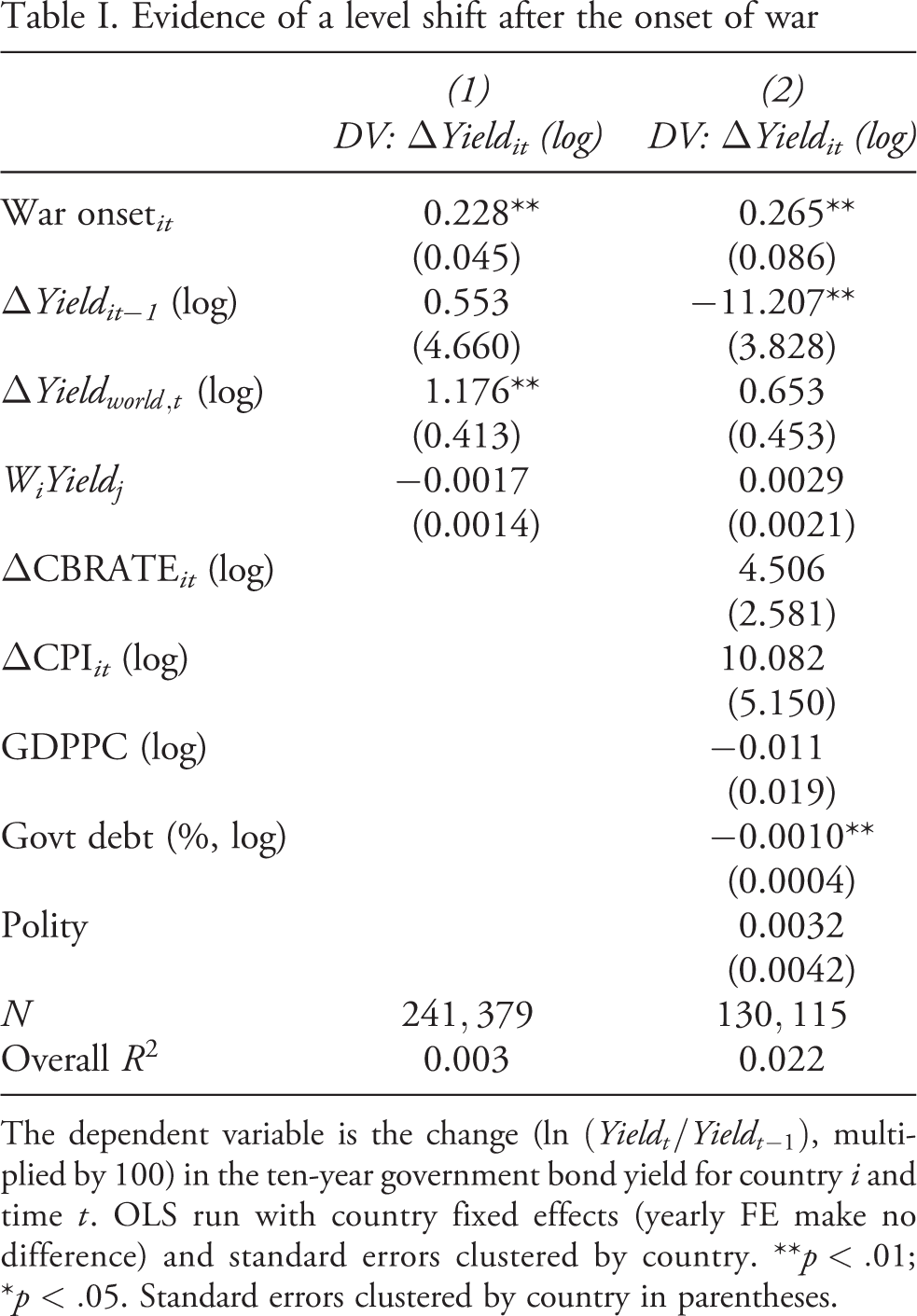

I estimated a simple OLS with standard errors clustered by country (clustering by year as well made no difference), with country-level fixed effects (adding yearly effects also had little effect). The results are reported in Table I. Two things should be noted. First, overall R-squared is low (it ranges from 0.3% to 2.3%), but not surprisingly so. I am explaining fluctuations in bond yields – that is, financial market returns – which typically are stochastic. Campbell & Thompson (2008), for example, review variables listed in the financial literature to account for variations in monthly stock market returns, and show that these variables lead to in-sample R-squared values ranging from 0.02% to a maximum of 2.6%.

Evidence of a level shift after the onset of war

The dependent variable is the change (ln

Second, I find that the onset of a war in a given week has a positive and strongly significant effect on that country’s yields. The effect is small, but keep in mind that we are dealing with the change in yield over a single week. 7 This shows that even when looking at the universe of all changes in yield, which are caused by countless factors – economic crises, exchange rate regime changes or regime changes – war onset has a positive and significant impact on yields. This result strongly supports Hypothesis 1.

However, the setup also has major disadvantages. First, it compares the change in yield associated with the onset of war to all changes in history. Many of these shifts have causes that are of no interest here, including financial crises or changes in exchange rate regime (still, I note that controlling for the gold standard or the type of exchange rate regime had no substantive effect on the results). That is, the absolute size of the shift tells us little about the extent of the investors’ surprise. While it is remarkable that I find a positive and significant shift even when compared with all shifts in the time span covered, the ultimate goal is not to compare the shock of war with other shocks, and hence the model’s interpretation is limited. Second, this model is inflexible. As it is, the setup focuses only on the week of the onset, but fails to inform us about the path leading to war and what happens after the onset – not just in that very week. I therefore now evaluate the hypotheses using yields around the onset of conflict.

Fluctuations around the onset

Here I study the evolution of yields shortly before and after war to assess the market’s reaction to the onset. For each of the 2,516 conflicts in the data, the dependent variable in this section is the yield of that country’s sovereign bond three months before and after the onset of conflict. I standardize these time series as z-scores based on the prewar distribution. 8

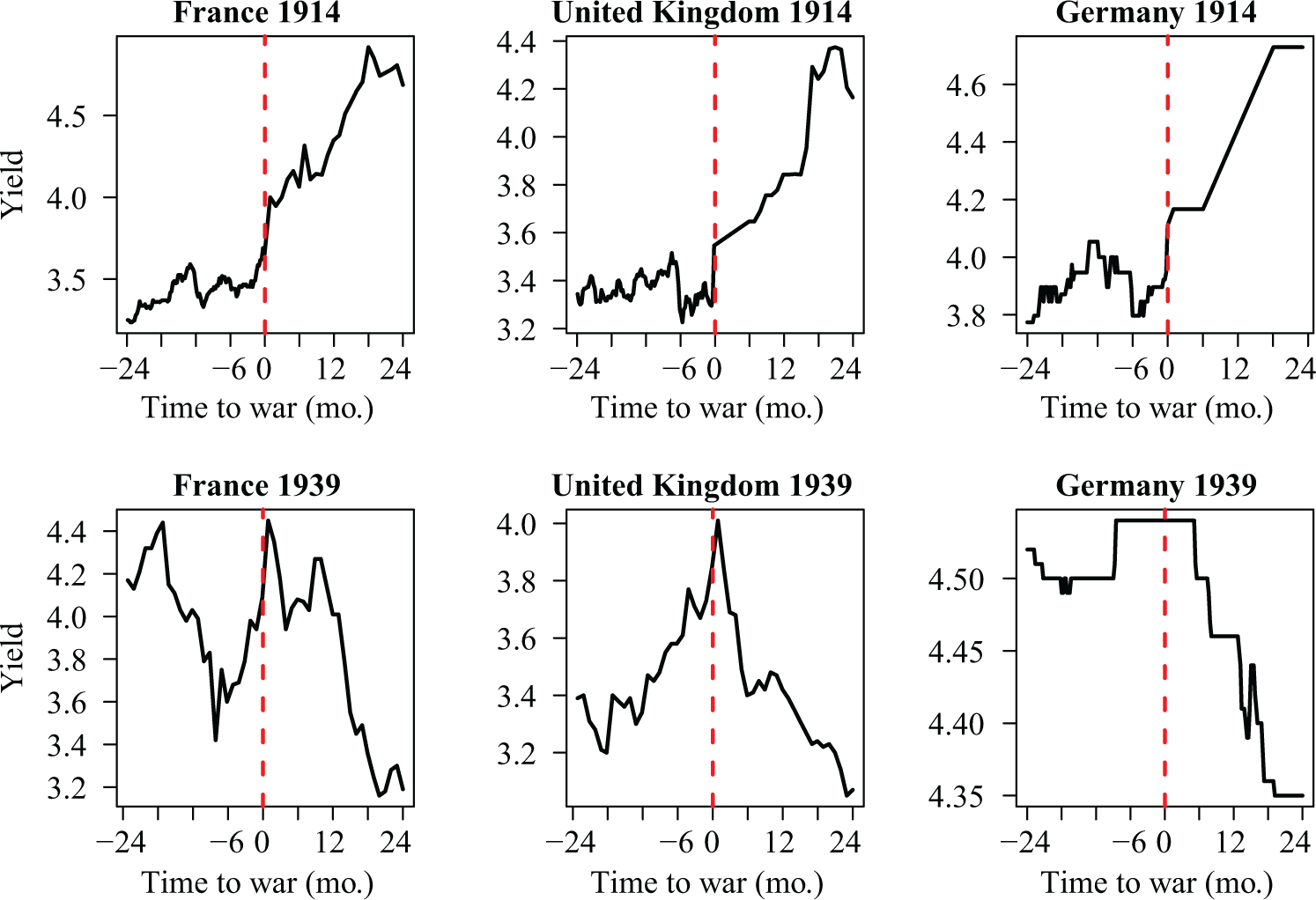

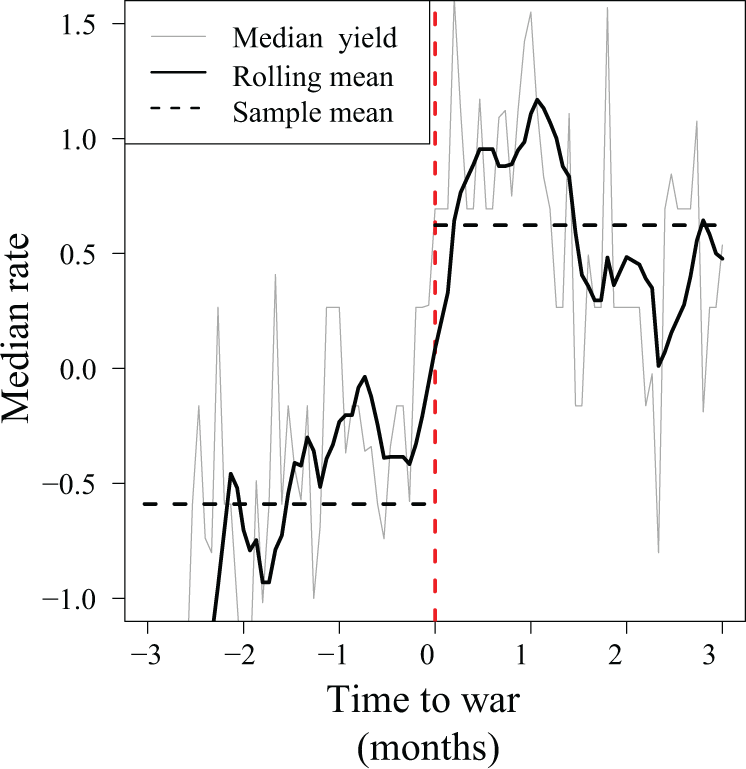

Figure 1 illustrates the data by plotting the evolution of the ten-year government bond yield around the onset of the two World Wars for three different countries. The time series are standardized over the interval for the purpose of comparability. I note that WWI, for example, led to a large jump in bond yields, whereas the slow escalation of the 1930s and Hitler’s clear intentions left no one incredulous in 1939. For illustration purposes, I also aggregated these standardized time series for all 176 large wars in the sample (those with at least 10,000 deaths). 9 Overall, the pattern shows a clear jump immediately before war and following its onset (Figure 2). 10

Evolution of government bond yields around the onset of WWI and WWII

Median bond yields around the onset of large conflicts

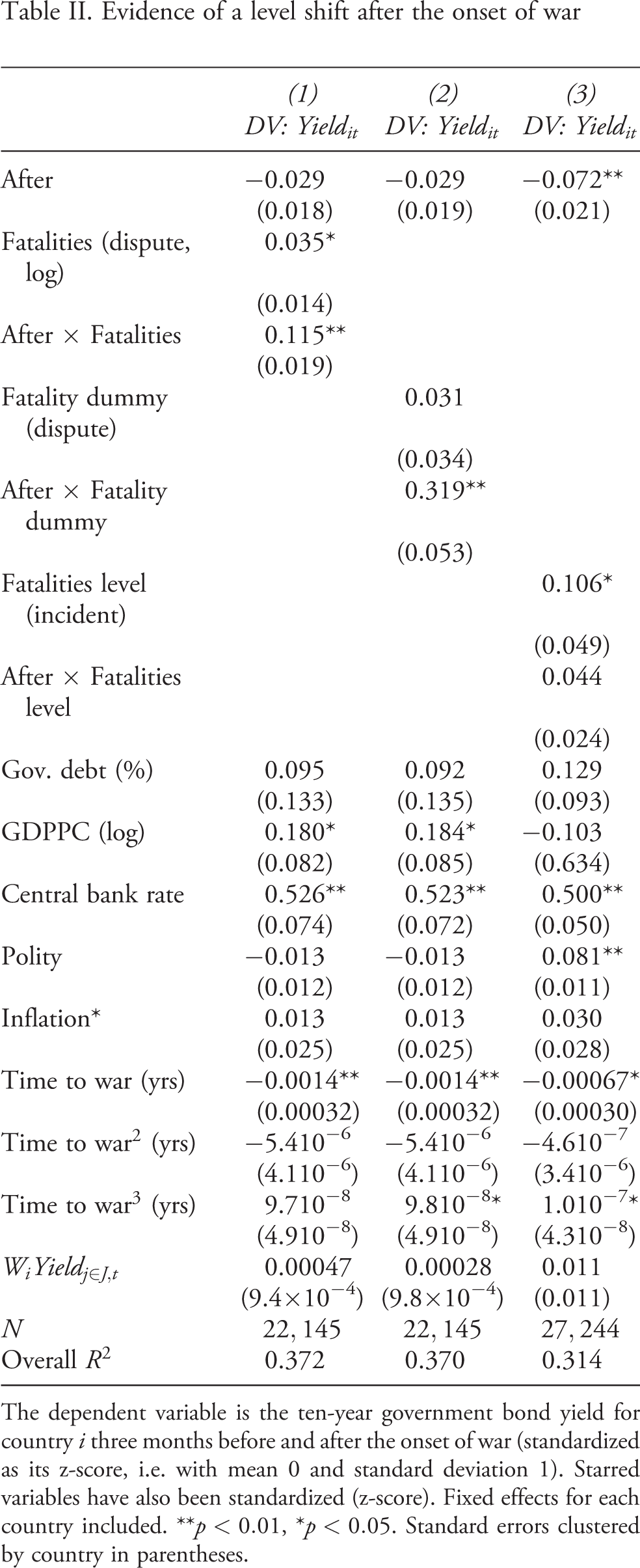

I now confirm these results more formally by estimating a model in which time series of bond yields for all 2,516 conflicts (standardized as z-scores) were regressed on a dummy variable coded as 0 before the onset, and 1 thereafter (After). In addition, I include a variable measuring the number of days until or since war (Time to war).

11

Because markets may not worry about small skirmishes, I expect only severe incidents to lead to a jump and therefore interact the After dummy with three different measures of conflict severity, all of which avoid the ‘hindsight’ fallacy that would use information that was not available at the time. For robustness purposes, I also controlled for the central bank’s rate, inflation levels (see above), the country’s government debt levels as a percentage of GDP, its GDP per capita and Polity score, and the yields of countries in the network, weighted by their policy similarity (

The idea behind this regression design is that if markets correctly estimate the risk of war, then I should not observe a jump in yields around the time of the onset. In other words the Time to war variable would be significant – a smooth increase towards the value it takes after the war – but the After war dummy would not, since there would be no jump. Yet I find the opposite: the interaction between After and either measure of severity is strongly significant, with a substantial effect, which indicates that the onset of wars with at least some casualties does lead to a level shift in yields (Table II). 12 This result holds for all three measures of severity, that is, even when looking only at short wars or incidents for which the number of casualties was known from the start.

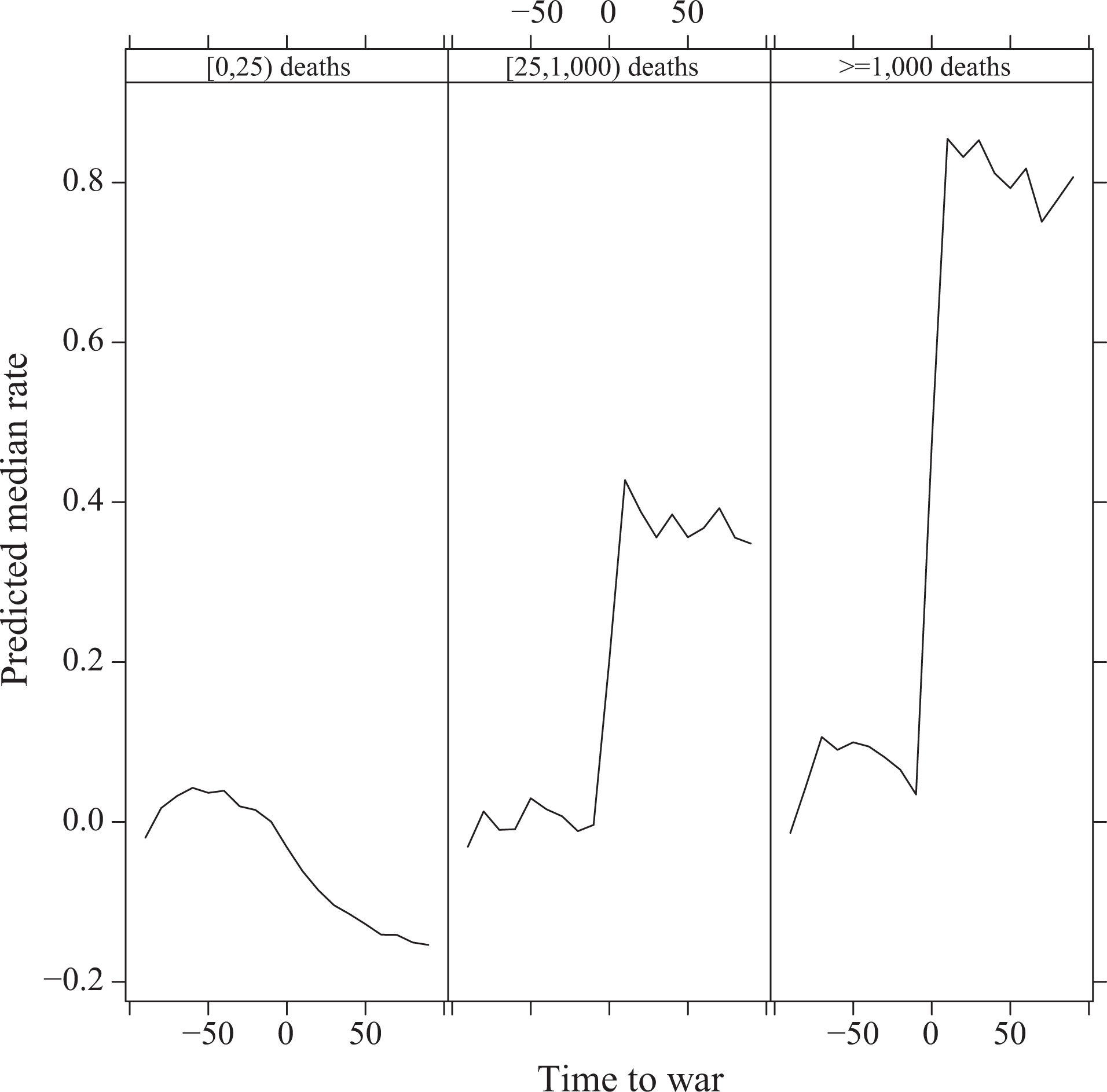

Following Central bank rate, After × Fatality dummy is the variable with the largest effect on yields (Fatality dummy here refers to whether there were any fatalities in the dispute, keeping in mind that I only look at very short – less than one week – disputes to avoid using any information that will only become available later in time). 13 Finally, I note that the effect of the onset on yields might be indirect, in the sense that the war leads the central bank to increase its rate, which in turn leads to a jump in yields. This is an issue that I address in Online appendix A.3. Using a mediation analysis, I show that the effect of the onset on yields is in fact even stronger than the regression results would lead to believe. Overall, then, these findings strongly support Hypothesis 1 that conflicts will tend to be surprising, and Hypothesis 2 that the correction is larger for more severe events. Figure 3 illustrates the predicted values of standardized bond yield values as a function of time to war, for different numbers of casualties in the first week of the conflict.

Evidence of a level shift after the onset of war

The dependent variable is the ten-year government bond yield for country i three months before and after the onset of war (standardized as its z-score, i.e. with mean 0 and standard deviation 1). Starred variables have also been standardized (z-score). Fixed effects for each country included. **p < 0.01, *p < 0.05. Standard errors clustered by country in parentheses.

In-sample median of predicted values of bond yield (standardized), as a function of time to war (in days) and number of casualties in the first week of conflict

Markets underestimate the risk of war

So far I have aimed at showing the existence of a correction around the time of the onset of wars. Yet the correction that I observe may not necessarily reflect the market’s underestimation of the probability of war, but rather the simple fact that the uncertainty about the onset of war was resolved. Just like a bookmaker could correctly estimate the probability of a horse winning to be 90%, even though the horse ends up losing (an outcome that we would expect to happen 10% of the time), markets may correctly anticipate the probability of war, and adjust the price with a correction once the war happens for certain. If the onset of war is a stochastic process, the correction may be a sign not of underestimation, but rather of a move to certainty.

To ensure that markets do in fact underestimate the probability of war, what we need to test is not only whether they react to the onset of war, but also whether their pre-onset estimates were actually biased. Obviously there is no way to assess whether the estimated probability of a single event was correct. If we say for example that a coin has a 20% chance of landing on Tail, and the result of a single flip is Head, we still cannot establish that our 20% estimate was incorrect. After recording multiple flips, however, we might be able to determine whether our predicted probability was correct. What we need, in other words, is to measure the market’s estimation of the risk of war in repeated samples, and to compare the average estimate to the actual overall probability of onset. In short, war should happen 50% of the time when the predicted probability is 50%.

I therefore estimate the predicted probability of war onset implied by the value of bonds at time t by estimating a simple model of the form:

where ui is a fixed effect for state i at time t and ε

it

is the error term. β is a parameter to be estimated. I estimated this model using a simple logistic regression and calculated out-of-sample predicted probabilities on a rolling basis (Chadefaux, 2014; see also Colaresi & Mahmood, 2017). For example, I use data prior to 1920 as a learning set, and calculate predicted probabilities for the following year. I therefore end up with predicted probabilities for the period 1920–2007, which I can then compare to the true probability of onset over the same period. For reference, I compare the predictions of the model based on bonds data to those based on the number of conflict-related news (i.e.

I first note that the model using bonds is good at discriminating between cases in which a war is coming and those where it is not. Indeed, its area under the receiver-operating characteristic curve (ROC) is nearly indistinguishable from the one generated using data derived from news (Figure 4a). The area under the precision-recall curve is also very comparable (Figure 4b). 14

Out-of-sample forecasting performance

However, I find that the calibration of the ‘bonds’ model is poor. The calibration of a test refers to its capacity to accurately predict absolute risk levels by comparing the predicted risk to the observed occurrence rate (Steyerberg et al., 2010). If markets were unbiased, I should observe that war happens 20% of the time when markets predict a 20% probability of conflict. On a calibration plot, with predicted probabilities on the x axis and actual occurrence rate on the y-axis, in other words, data points should fit neatly on the 45-degree line. Yet this is not at all what I observe. While the model based on news (a very simple model using a count of conflict-related news and fixed effects) performs well on calibration metrics, the same model based on bonds does poorly. Thus when predictions derived from the bonds model forecast a 40% probability of conflict (i.e.

This result, combined with the jump that I observe following the onset, confirms that markets tend to underestimate the risk of war. I now turn my attention to explaining the variation in that level of surprise.

Which wars are surprising?

On average, then, wars lead to a jump in bond yields. Yet many do not. How often are they surprising? The answer obviously depends on the threshold we set for a ‘surprise’. Figure 5, for example, displays the proportion of cases followed by a jump in yield of at least x standard deviations. Of course the larger the threshold for a ‘surprise’, the fewer wars qualify as surprises. The answer also depends on the size of the war, since larger wars tend to lead to larger jumps. Wars with at least 10,000 battle deaths, for example, lead to an increase in government bond yield in more than 80% of cases (i.e. in 80 large wars out of 100, the average yield in the three months following the onset of war is larger than the yield in the preceding three months), but almost no conflict led to an increase of more than 2 standard deviations.

Probability (observed data) of a post-onset increase in bond yield as a function of the threshold selected (i.e.

Regardless of the threshold I adopt, the variance in jump is puzzling. What affects whether some wars come as a surprise when others do not? I now change the dependent variable to consider the shock itself. The dependent variable, Δ3Yield, is now the change in a country’s government bond yields following each of the 2,516 wars for which data are available. It is obtained by subtracting the average yield in the three months that precede the onset of war from the average yield in the three months that follow it. Whereas the previous section was concerned with whether a shock occurred at all, here I am interested in the size of the shock as a function of various covariates.

Variables used to test my hypotheses include Date, an index of time (in decades), where 1 January 1816, takes value 0 and 12 December 2007, value 19.2. I include this variable to estimate the effect of time on the severity of shocks to test Hypothesis 3. Furthermore, dummy variables reference the type of war (Inter) – interstate wars are coded as 1, and intrastate wars as 0. Democracies are also expected to be more reactive with a more transparent bargaining process, so that conflicts involving them should be more difficult to predict than those involving autocracies (Hypothesis 4). I use the Polity IV score (Marshall, Jaggers & Gurr, 2002) (Polity). The variable Peace decades (together with its square and cube) denotes the number of decades since the onset of the previous conflict (Carter & Signorino, 2010), as I expect markets in countries with recent conflicts to be less surprised about the onset of war than countries in which conflicts are a distant memory. I also include measures of expected cost in the form of the trade ratio (Imports

ij

/

Other control variables include the size of the prior change in bond yields for that country (Δ3Yield (lag)). This variable measures the magnitude of increase or decrease in bond yields in the three months preceding the war. 15 I include this variable because I expect some time-dependence in shocks. I also control for the average change in bond yields in the world in that year, since average bond yields might decrease over time, independently of the onset of war. I also control for the country’s national material capabilities (NMC) using the Correlates of War’s Composite Index of National Capability (Singer, 1988, v. 4.0).

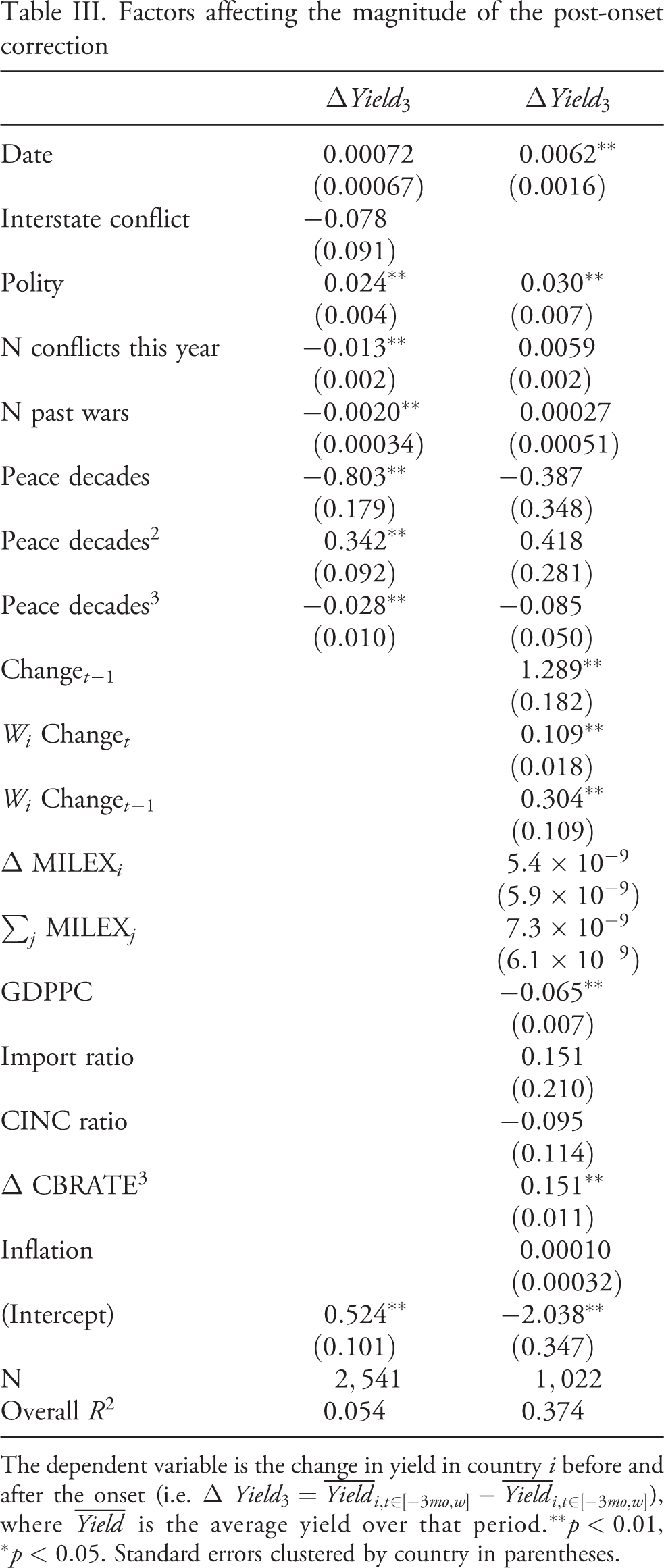

Finally, I also include an index of the worldwide number of conflicts in a given year as a proxy for the level of risk associated with that period (N conflicts this year). A large number of conflicts may indeed indicate a dangerous system, perhaps because of multipolarity, shifts in power, or various idiosyncratic events such as the end of the Soviet Union. If conflicts are widespread, observers of international relations are less likely to be surprised at the onset of yet another one, and markets will therefore already have incorporated the risk. A larger number of conflicts in the world should therefore reduce the surprise associated with conflicts. Summary statistics are reported in Table A6 in the Online appendix. I regressed the size of the shock following each conflict on the covariates described above. The results are reported in Table III (see also Figure A6 in the Online appendix).

Factors affecting the magnitude of the post-onset correction

The dependent variable is the change in yield in country i before and after the onset (i.e. Δ

I find that my hypotheses are largely supported. In particular, the coefficient on date has a small and statistically insignificant effect on the size of the surprise, in support of Hypothesis 3. For models in which it is significant, the coefficient is actually positive, suggesting again that the prediction record has not improved over the past two centuries. 16

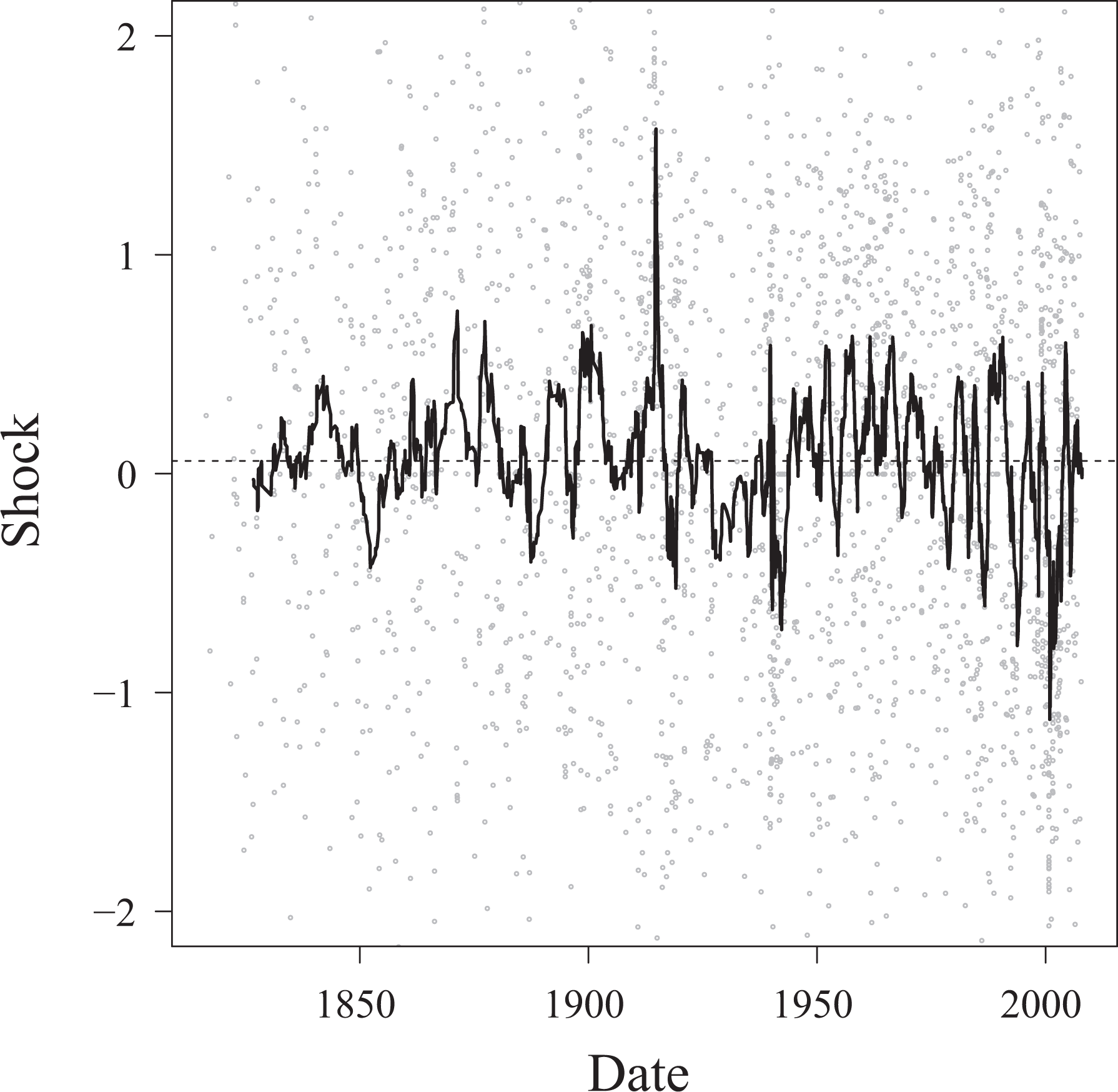

Figure 6 provides visual intuition for this result by displaying the shock that followed each of the 2,516 wars in the sample, and the absence of pattern over time. The same result applies if we consider large wars only, or the absolute value of the shock instead of the raw change. This matches my conjecture that continuous learning and policy adjustments may lead to ever changing or more complex patterns prior to conflict, and hence to the fact that the wars that do occur are those that could not have been easily predicted. Just as markets are essentially random walks because participants continuously incorporate new information in such a way that no arbitrage is possible, I conjecture that leaders also adopt decisions in reaction to what they know from the past and the information available. This constant process of adjustment means that wars cannot be easily forecasted. 17

Change in yield (‘shock’) following the onset of conflict, and its evolution over time

In line with my expectations, I also find the magnitude of the shock to be larger in democratic countries than in autocratic ones, supporting Hypothesis 4. This effect is strongly significant and substantial. On the other hand, while interstate wars do lead to a larger average increase in yields than intrastate wars, as expected, the effect is not significant, and hence I find little in support of Hypothesis 5.

One possible concern is that the set of variables included may have been intentionally selected to support certain hypotheses, or may simply be a lucky combination. I address these concerns about model uncertainty by running a Bayesian model averaging (BMA), a technique used for example in Warren (2014) and Ward & Beger (2017). The outcomes of the BMA are reported in Online appendix A.4 and strongly support the results.

Conclusion

Policymakers and students of international relations have long sought to anticipate and prevent the onset of conflict. Yet results presented here suggest that even those who have a financial interest in their accurate prediction have been rather unsuccessful. This does not imply that contemporaries are oblivious to the escalation of tensions (Chadefaux, 2014), but that they do tend to underestimate the risk of war.

Yet this seemingly damning result may in fact not be an indictment of markets’ forecasting ability. Rather, because conflicts that are anticipated well ahead may be more likely to be avoided, only the difficult cases are left in the sample. The apparent recurrent failure to estimate the risk of war may in that sense simply be a selection effect. If policymakers incorporate some of the available information – including lessons from the past and forecasts given available data – then their behavior will be constantly adapting to new information. As a result, markets may always be one step behind and will tend to be taken by surprise by policymakers’ decisions. The fact that wars are, on average, just as surprising today as they were in 1816 further supports this idea of a selection process, by which only the wars that are the most difficult to predict occur. As a corollary, countries with more transparent and possibly reactive regimes such as democracies should be better at incorporating new information, and hence predicting their behavior should actually be more difficult – a hypothesis for which I found strong support here.

These findings may also suggest a ‘policy efficiency’ hypothesis. If the evidence for market efficiency is the quasi-impossibility to predict future changes in asset prices based on current patterns, then the constant inability of markets to correctly assess the risks of war may also mean that policymakers incorporate existing information rapidly into their decisions, and hence that policy in that sense is ‘efficient’. Additional work on how leaders incorporate new information and forecasts into their decisions may lead to further insights on this subject.

Wars are, at least in part, failures of predictions. They often occur when their participants fail to predict the consequences of their actions. Far from being a depressing diagnostic, then, these results show the importance of prediction as one possible instrument of conflict prevention, and the role of scholars in bridging the gap between basic and applied research.