Abstract

Does terrorism inhibit a country’s ability to attract international direct investment? If so, terrorism may have large costs in terms of employment losses, macroeconomic instability, and missed development opportunities. However, do investors fear terrorism because of direct risks to their assets, or because the opportunities in the host country deteriorate? And how do they adjust investments? We study the impact of terrorism on merger and acquisition decisions of 8,872 firms over 116 countries over 16 years. The firm-level perspective allows the isolation of host-country terrorism from firm-level characteristics such as size or experience as an explanation, by comparing decisions for the same firm across destinations. It also allows separation of investment responses into reductions or entire withholding of investment. A sample standard deviation increase in terrorism reduces merger and acquisition investment by around 30%. Firms do not generally reduce the size of their investment in the face of terrorism – instead, they decide not to enter the country altogether. We find no evidence to suggest that multinational firms are more sensitive to attacks on local business assets. A country-level analysis, which necessarily does not control for firm-level characteristics, yields materially different conclusions.

Introduction

Do terrorist attacks discourage multinational investment? Multinationals probably wish to avoid the risk to their personnel, physical damages, and reputational costs of presence in terrorism-ridden countries. For instance, the rise of Boko Haram in Nigeria led local multinationals like Nestlé and Heineken to raise concern over the local logistics, access to local inputs, and the value of their local assets. 1 Intuitively, various recent results suggest that the impact of terrorism is substantial. Abadie & Gardeazabal (2008) conclude that a one standard deviation increase in terroristic risk reduces the net foreign direct investment (FDI) position of the country – a measure of multinational investment – by approximately 5% of gross domestic product. Similarly, Enders & Sandler (1996) find that terrorism reduced annual country-level FDI by 13.5% and 11.9% in Spain and Greece, respectively. Enders, Sachsida & Sandler (2006), on the other hand, report that US FDI flows show modest responses to terrorist attacks in host counties. Strikingly, even if the physical costs of terrorist attacks to firm assets are often low compared to many other risks, the response of multinationals is strong. One explanation is that international investments are particularly mobile and respond sensitively to small differences in (risk-adjusted) returns across countries (Abadie & Gardeabazal, 2008).

The indirect costs of terrorism may be sizable, if terrorism discourages foreign investments. Foreign investment generates employment opportunities, alleviates credit constraints, fills shortages of local savings, and brings knowledge and skill to the country, so it is often heralded as a pathway to economic development (e.g. Di Giovanni, 2005; Javorcik, 2004; Keller, 2010; Haskel, Pereira & Slaughter, 2007). These opportunities are wasted if terrorist attacks deter international investments.

The response of international investment to local conflict is also fundamental to theories of commercial liberalism and (external) capitalist peace. Foreign traders and investors can amplify penalties on conflict, poor institutions or human rights violations, thus encouraging peace (Schneider, 2014; Faber & Gerritse, 2012; Greenhill, Mosley & Prakash, 2009; Blanton & Apodaca, 2007). Economic openness might also increase the levels of development and contracting quality, and eliminate incentives for conflict or rebellion (e.g. Weede, 2005; Mousseau, 2010; de Soysa & Fjelde, 2010). Some argue that capital mobility in particular has a disciplining effect (Gartzke, Li & Boehmer, 2001; Polachek, Seiglie & Xiang, 2012; Kim & Trumbore, 2010): international investors penalize local conflict severely. Recent results suggest, however, that multinationals do not care about local conflict as much as they care about potential attacks on businesses (Powers & Choi, 2012). If multinationals only avoid direct hostility towards themselves but do not avoid destructive conflict in general, their role in capitalist peace may be small. This argument also links to potential conflict traps. Once a state falls prey to terrorism or other conflict, international investment withdraws, diminishing any force of punishment of the conflict. A state might thus end up in an undesirable equilibrium, both unable to decrease local conflict and unable to attract investment (e.g. Collier, 2006; Bussmann, 2010). The contribution of international investment to such a conflict trap, however, rests on the precise way in which investors turn away local conflict.

In this article, we study the impact of terrorism on international merger and acquisitions decisions (the majority of FDI decisions; Antras & Yeaple, 2014; Davies, Desbordes & Ray, 2016) of a large set of firms. Hence, we add to the literature that studies effects of terrorism on international investment flows, which by and large takes a national perspective. It generally documents negative impacts of terrorism, although the estimated sensitivity varies (Abadie & Gardeazabal, 2008; Enders & Sandler, 1996; Bandyopadhyay, Sandler & Younas, 2014; Enders, Sachsida & Sandler, 2006). There are two arguments for focusing on firm-level decisions.

First, the firm-level analysis allows us to compare the investment decisions of the same firm for different locations. Thus, we keep the characteristics of the firm – the supply side of the decision – constant in the analysis. This approach rules out that firm differences in, for example, ability, quality of management, control, risk appetite, or the need for resources from terrorism-affected countries explain the relation we find between terrorism and investment decisions (Chen & Moore, 2010; Yeaple, 2013; Witte et al., 2017). We show that failing to control for firm-specific characteristics (as an analysis of nationally aggregated flows would) yields results that may under- or overstate the investment sensitivity to host country terrorism. Our results suggest that a sample standard deviation in terrorism leads to around 30% lower expected investment. That is in line with the literature, which puts the number between 10 and 50%.

Second, the firm-level analysis provides a closer picture of the dynamics by which firms adapt their entry strategies. Our results imply that when faced with terrorism, firms might decide not to enter at a country at all (i.e. they adapt through the ‘extensive margin’). The evidence for adjustments of the size of investments, the ‘intensive margin’, is far less convincing. Arguably, investment adjustment along the extensive margin rather than the intensive margin is more dramatic, because extensive margin adjustment may lead to loss of technology and supply chains, tends to increase host country volatility, and complicates recovery of investments (Bergin, Feenstra & Hanson, 2009; Bernard et al., 2009). Moreover, we investigate what forms of terrorism most evidently discourage firm entry. In contrast to related literature (Powers & Choi, 2012), we find that terrorism that targets businesses is not significantly more or less discouraging than other forms of terrorism. Nor do attacks on local firms’ assets have stronger impact than other types of attacks. That suggests that indirect adversities of terrorism, such as logistical disruptions or a paralyzed business environment, may be as important as the risk of direct damages.

The next sections briefly review theories of multinational entry strategies in light of host countries’ terrorism, before discussing the data, methodology, and results.

Conceptual framework

Terrorism has come to play a big role in economic decisions, including the location choices of people, organizations, and businesses. Terrorism is often defined as ‘the premeditated use or threat of use of extranormal violence or brutality by individuals or subnational groups to obtain a political, religious, social, or ideological objective through intimidation of a large audience, usually not directly involved with the decision making’ (Enders & Sandler, 2012: 3, among others). Terrorist acts are on the rise worldwide and they are increasingly targeted at businesses (LaFree, Dugan & Miller, 2014; Brandt & Sandler, 2010). Moreover, firms’ location choices are surprisingly sensitive to terrorist activity, compared to other risks with similar damages (Abadie & Gardeabazal, 2008; Blomberg & Mody, 2005). Altogether, this suggests that terrorism has increasingly large impacts on the allocation of multinational enterprises across countries.

In our analysis, we explore two dimensions of the impact of terrorism on firm location choices – a context is sketched below. First, we question what types of terrorism firms fear: hostility towards businesses (implying that their assets are in the line of fire), or general terrorist attacks, including those targeting governments or civilians, that cause turmoil such as depressed demand and an uncertain environment. Second, we explore how firms adjust their investment after terrorist attacks: by scaling down the size of the investment, or by deciding to withhold the investment entirely.

Firms’ fear of host-market terrorism: Local assets at risk or a local market at risk?

Multinationals can be discouraged directly by terrorist hostility: the risk of becoming a terrorist target. Applying the Dunning ‘ownership, location and internalization’ (OLI) framework, as in Powers & Choi (2012), ownership has direct disadvantages in countries where terrorism targets businesses. Local assets may be in the ‘line of fire’, with higher probability of being destroyed or damaged (Li, Tallman & Ferreira, 2005; Sandler & Enders, 2008; Fielding, 2004). An increased likelihood of being targeted risks the value of local buildings, machinery, products, personnel, and brand value (Gaibulloev & Sandler, 2011; Spich & Grosse, 2005; Czinkota et al., 2010; Powers & Choi, 2012). Drawing on economic theories of multinational investment (Barba Navaretti & Venables, 2006), the risk of damage to host-country plants and (human) capital directly reduces the profitability of the international investment decision. A firm’s assets and resources are not limited to the items on its balance sheet: the risk extends to upstream and downstream suppliers and the supply chain, its data infrastructure, and its local transport networks (Li, Tallman & Ferreira, 2005; Sheffi, 2001). The costs of operations in a prospective location are likely to go up, too. Wages of employees at firms likely to be targeted by terrorism tend to be higher (Frey, Luechinger & Stutzer, 2007), and insurance premiums significantly increase after terrorist attacks, particularly for targetable buildings and structures (Lenain, Bonturi & Koen, 2002). Firms also tend to spend more on securing their sites and staff (Gaibulloev & Sandler, 2011). Recent evidence additionally shows that the threat of terrorist attacks on a firm stresses its employees to such extents that performance substantially declines (Bader, Berg & Holtbrügge, 2015).

However, terrorist attacks, even if they do not target firms directly, deteriorate the circumstances for operations in the host country in general. Hence, the indirect impacts of host country terrorism on multinationals may be substantial, too. The indirect channel of discouragement operates differently from the direct terrorist threats to local assets. Terrorist attacks in general could be considered as locational disadvantages in the OLI framework (Powers & Choi, 2012). Firms pay risk premia in wages and real estate prices, even if they are not targeted directly (Abadie & Dermisi, 2008). Similarly, high levels of overall terrorism tend to damage local infrastructure, frustrating the distribution networks of firms as a side-effect. The rise of terrorism coincides with problems in transactions and contracting, forming a barrier to exploiting local opportunities for sourcing, selling, and partnering (Nitsch & Schumacher, 2004; Gaibulloev & Sandler, 2011). Governments tend to tighten policy and regulations, complicating the business environment (Czinkota et al., 2010). Terrorist attacks can also shock the (local) economy, leading to lower economic performance and demand, and redirecting government budgets (e.g. Abadie & Gardeazabal, 2008; Gaibulloev & Sandler, 2008). Standard economic theories of FDI mostly interpret such indirect impacts as a reduction in effective market size, leading to lower host-market expenditure (Barba Navaretti & Venables, 2006). For horizontally motivated (market-supplying) investments, that implies that the potential returns to an international investment decline with terrorism. For vertically motivated investment seeking low-cost production locations, market size is less important and the corresponding reductions in wages might even encourage investment, provided that contract, legal, and logistical frictions do not outweigh the labor cost reductions. For multinationals, operations in a location associated with terrorism or conflict may also come with reputational damages and issues of legitimacy (Driffield, Jones & Crotty, 2013). Pressure from press or consumers in and outside the host country may convince multinationals to exit. The mechanisms listed so far suggest that terrorism discourages firm entry, but some theories suggest that general terrorism (not targeted at individual firms) offers investment opportunities. The ownership decision in the OLI paradigm might favor investment when terrorism rises, because firms wish to exert more control (Li, Tallman & Ferreira, 2005 – the ownership decisions contradict the locational decision). 2 In recent trade theories, multinationals are better equipped to deal with uncertain environments. For instance, multinationals tend to have higher productivities, profit margins, and resilience, so they may be more likely to survive shocks, relative to weakened local competition in affected areas (Mayer & Ottaviano, 2008). Similarly, multinationals are more likely to possess useful experience from operations in other conflict locations (Li, Tallman & Ferreira, 2005). Moreover, times of terror may erode the ties of incumbent firms to the political establishment or free up the natural resources of the country, both of which favor multinationals over domestic firms (Witte et al., 2017; Guidolin & La Ferrara, 2007). Or, on occasion, multinational firms may see opportunities that stem directly from conflict in outright ‘follow the flag strategies’ (Biglaiser & DeRouen, 2007).

Compared to domestic firms, multinational firms might more easily deal with threats of terrorism to their local assets. Multinationals are the largest, most productive firms, best equipped to deal with difficult markets (Chen & Moore, 2010) with more resources and market power. They are also more likely to organize their security privately, in particular in countries where police services or property rights are imperfect. Moreover, multinational firms have a limited exposure to the affected market, relative to firms that only operate in the affected country (Li, Tallman & Ferreira, 2005). Thus, multinationals might have a competitive advantage in maintaining operations or access to credit relative to local firms when businesses are under threat. Following these arguments, multinationals may have more control than local firms over the potential damages when facing terrorism that is hostile particularly to the firm. As a consequence, multinationals may perform well in terrorism-affected areas compared to local firms. On the other hand, multinational firms may be more likely targets of business-related terrorism, particularly if their operations are controversial, if they have low levels of legitimacy, or if terrorism is driven by nationalist motives, for instance (Driffield, Jones & Crotty, 2013).

Hence, whether multinationals respond more strongly to business-targeting terrorism than to other forms of terrorism is up for discussion. We examine this question in our empirical strategy. The article most closely related on this point, Powers & Choi (2012), takes up this question in nationally aggregated data, using another source of terrorism data. They document that international investment flows are particularly sensitive to terrorist attacks that have explicit business targets, while they are far less sensitive to terrorism with other targets. Enders, Sachsida & Sandler (2006) raise this possibility to explain the difference between their results and those of Enders & Sandler (1996).

Entry decisions and scale decisions

There are several ways in which multinationals can adjust their international investment decisions in the face of terrorism. They may withhold their investments entirely (the ‘extensive margin’) or adjust the size of their investments (the ‘intensive margin’). Understanding these margins of adjustment is relevant for several reasons. First, they inform policies to ameliorate the impacts of terrorism. If firms scale down but remain present following terrorist attacks, policymakers may support their economy with efforts to reduce costs or other firm burdens, or prop up demand. The complete withdrawal of investment (extensive margin adjustment), on the other hand, may point to unfathomable barriers to local operations, in the face of which local policymakers are probably powerless. Second, extensive margin adjustments change the firm population of a country more dramatically, especially given the fact that most investment and employment by international firms is accounted for by a few ‘superstar firms’ (Mayer & Ottaviano, 2008). Firms leaving the country, instead of downscaling their investment, leads to graver consequences in the variety of foreign technologies brought into the country, making it more likely that the country drops out of a supply chain altogether and leading to geographically concentrated employment losses in the areas they leave behind. Evidence from trade patterns suggests, moreover, that the recovery of investment by attracting new firms is more difficult than recovering the pre-existing relations (Bernard et al., 2009). Third, adjustments of international investment along the external margin lead to more volatility in the economy and employment in the host country than do adjustments on the internal margin (Bergin, Feenstra & Hanson, 2009), so that the macroeconomic consequences of extensive margin adjustment are more severe.

Theories of international firms suggest that the choice of whether to invest in a country differs materially from the decision how much to invest. Consequently, terrorism may have different impacts on the two decisions. Most theories of multinational firms accept that substantial investment in local (fixed) assets is required to operate in a country. If assets such as buildings, machinery, and knowledge are exposed to terrorism, marginal adjustments to the size of production barely limit the firm’s exposure – but exiting the country would (Buch et al., 2009). Similarly, being associated with violence and terrorism may damage firms’ reputations and legitimacy irrespective of their size – as does corruption, for instance (Rodriguez, Uhlenbruck & Eden, 2005). In recent trade theories of trade and investment (Chen & Moore, 2010), the most capable firms sort into difficult locations, and under adversities like terrorism, the least able drop out. According to these theories, most adjustment would be through firm entry and exit (a parallel mechanism is outlined for trade and terrorism in Bandyopadhyay, Sandler & Younas, 2018). Trade and investment theories might predict an adjustment along the intensive margin too, but generally only if terrorism affects per-unit costs of production, rather than fixed assets like buildings or infrastructure. In more business-oriented models of firms, that study internationalization by stages, the entry decision differs from the decision on investment size, too (Delios & Henisz, 2003). Firms may ‘test the water’ – they enter a country with limited exposure to see if they can handle difficult, uncertain or violent environments. Only in a later stage does the choice for optimal scale take place. Following that interpretation, terrorism may drive out the firms that are testing the environment, but it has less impact on the operations of firms that have learned to deal with uncertainty in the host country.

Terrorism is more likely to affect the extensive margin than the intensive margin, following these theories. Much of the firm’s exposure in terms of local assets, reputation, and legitimacy is tied to their presence, rather than to the size of their local investment. Moreover, multinationals that mastered the management of uncertainty in the host country might be less likely to leave after attacks. The argument for intensive margin adjustment is somewhat less obvious, as the decision on the firm’s operational size is less obviously connected to the risks of terrorism. An empirical analysis of these margins of adjustment has not been done for multinational investments, to our knowledge. On this point, related analyses focus on nationally aggregated flows of investment, which cannot distinguish between the external and internal margin of adjustment.

Empirical strategy

To establish whether terrorist attacks reduce mergers and acquisitions (M&As), our analysis explains investment decisions by international firms from the number of terrorist attacks in the potential host country. We focus on M&As for several reasons. First, M&As account for the larger shares of direct international capital flows, making it the most representative type of FDI. Second, M&As closely measure responses of firms. Firms may be sluggish to invest or divest their existing stock following incidents, and their book values may differ from the physical capital or operations in the country. Focusing on the presence or absence of big acquisitions between parties minimizes these concerns. Third, accurate numbers of firms’ capital stocks of location are scarcer, so that data on mergers and acquisitions provide a more comprehensive dataset.

Our empirical analysis explains a firm’s investment decision in a particular location from proxies of terrorist activity in that location. This shows whether terrorist incidents are significantly associated with lower investment values or probabilities. As these are bilateral observations (from every firm to every potential location), the regression equation is reminiscent of a standard gravity model:

In this equation,

We use firm-year fixed effects to focus on variation across destinations within investment decisions for the same firm. A merger or acquisition can be considered a result of the supply of assets in the host country, and the demand for such assets by international firms. Terrorism may reduce the effective supply of assets, or make them less appealing. The fixed effects approach focuses on the shocks originating from the host market, as we compare investment flows across host markets for the same firm in the same year. Consequently, we do not infer whether overall investment was lower or higher for individual countries, but we compare whether one country receives more or less investment than the other country from the same firm, given that one country experiences more terrorism than the other.

As we do not cover the population of firms or countries, the fixed effects structure may also correct for an unobserved variable bias. If

The decision to invest is associated with a lot of zeros, as firms engage in mergers or acquisitions in at most a few countries at a time. We deal with a high share of zeros using two strategies. First, we estimate a Poisson model, incorporating zero-outcomes in the log-form regression. Effectively, we estimate

Second, we split the investment decision into an extensive margin (entry) and an intensive margin (the quantity of investment). The split unearths the dynamics that comprise the aggregate flow. To see this, we write the aggregated flow of mergers and acquisition value of country j into country c as:

where

Given our firm-level approach, we can estimate the two margins separately.

Data and controls

Our data on mergers and acquisitions are from Bureau van Dijk’s Zephyr database. We focus on firms completing deals of at least one million dollars in a cross-border merger or acquisition in the years 2000 to 2015. If a firm has multiple investments in a country in a given year, we use the sum of the value of those investments. The dataset comprises observations on 8,872 investing firms in 116 host countries (the list of countries is in Online appendix OA1).

The data on terrorist events are from the Global Terrorism Database (GTD, 2016). We use observations for which three criteria for a classification as terrorism are satisfied: (1) The incident must be intentional; (2) the incident must entail some level of violence or immediate threat of violence; (3) the perpetrators of the incidents must be subnational actors. Moreover, we exclude observations for which the terrorist motive is doubted. We also split these according to whether the target was a business (patron) or not. If the target was a business, we also split these events by whether the attack type was personal (assassination or assault against people associated with the business), on physical assets (facility or infrastructure attack or vehicle hijack) or indiscriminate (bombing/explosions, assault, or hostage taking not directly involving business facilities or employees).

For our proxy of terrorist activity, we use the number of attacks in a country. We scale the number of attacks to the population of the country (from the WDI world governance indicators). The literature is divided over this choice (Ouyang & Rajan, 2017; Bandyopadhyay, Sandler & Younas, 2014; Powers & Choi, 2012). Our prior is that the attacks per capita better reflect the probability of being affected by an attack for a given firm – a single attack may have comparatively lower impact in Nigeria than in Burundi. 3 The strategy is confirmed in the data: in the preferred specifications, the absolute number of attacks has no explanatory power conditional on the number of attacks per capita. The number of attacks per capita is highly skewed, so we exclude observations with over 50 attacks per million inhabitants. 4 We use the number of attacks in the year preceding the investment, to avoid attributing investment behavior to terrorist attacks that occurred in the same year, but later than the investment decision. A sensitivity to check for this choice is discussed in the Results section.

Terrorist attacks have risen over the course of our sample, from 0.2 to 1.2 per million inhabitants. The standard deviation across the sample is just over three attacks per million inhabitants. Business-targeting terrorism has remained more stable (it rose from 0.03 to 0.10 attacks per million inhabitants, the standard deviation is 0.06) and varied between 9% and 21% over the years. The number of business attacks correlates strongly (0.84) to the overall number of attacks.

Terrorist attacks may correlate to other characteristics of the host country, which could also explain investment behavior. We include a set of controls to rule out confounding explanations conventional to the literature (Di Giovanni, 2005; Ouyang & Rajan, 2017; Powers & Choi, 2012; Wang, 2008). To control for the level of development that might confound with terrorist activity, we include GDP and GDP per capita measures of the host. To account for the fact that terrorism might be less discouraging to firms located close to the host country, we consider common gravity variables from articles explaining international mergers and acquisitions (Ouyang & Rajan, 2017; Erel, Liao & Weisbach, 2012; Di Giovanni, 2005). They include bilateral distances weighted by population, indicators for common language, colonial relationship, common religion, from the CEPII. We also incorporate the real effective exchange rate (from Darvas, 2012) and the exchange rate volatility, calculated according to Di Giovanni (2005). We include the trade openness (import and export over GDP) to control for the ease of shipment.

Several political developments may correlate with entry decisions and terrorism, obscuring the cause-and-effect relation. To ascertain that these do not explain our results, we control for several aspects of (confounding) host country investment climate. We include governance indicators controlling for corruption, quality of government, political representation, rule of law, and regulatory quality (from the WDI world governance indicators). We exclude absence of violence for its obvious overlap with the terrorism variable. At times, terrorism may lead to overthrow of government, and an associated policy change toward multinational firms. We control for regime transitions as identified by the Polity 4 dataset (Marshall, Gurr & Jaggers, 2017). Terrorism may also be associated with violent conflict in general, so that terrorist attacks conflate with overall violence. We control for battle-related deaths in the host country taken from the Uppsala Conflict Data Program (UCDP) (Petterson & Eck, 2018) to rule out that violent conflict in general explains our results. Descriptive statistics for the firm-level sample are in Online appendix AO2.

Results

Impacts on overall investment

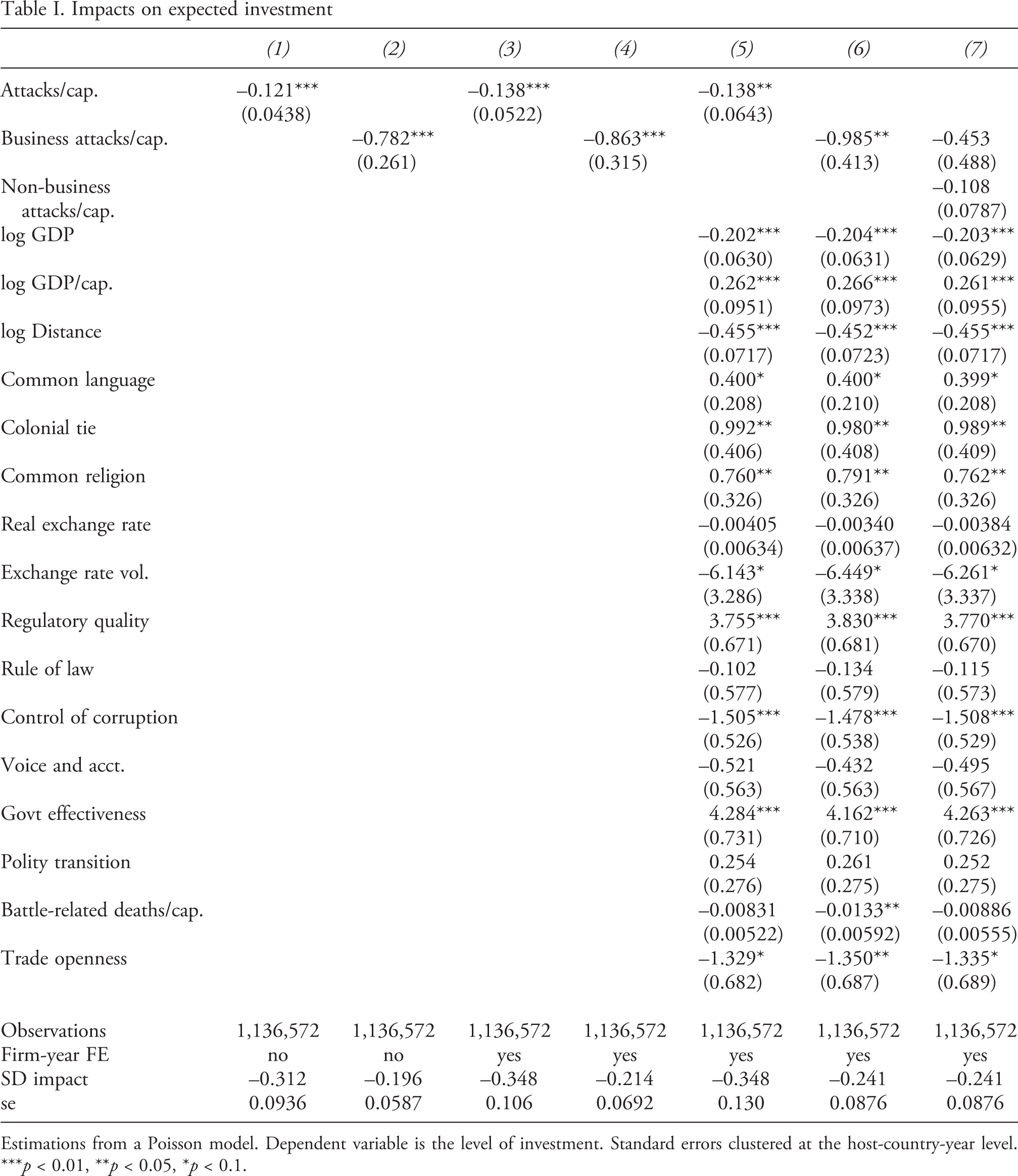

The first column of Table I reports the Poisson estimates of the effects of the number of terrorist attacks on merger and acquisition flows without controls or fixed effects. The Poisson count model has a gravity interpretation, suggesting that one extra terrorist attack per million inhabitants is linked to a 12% decrease in value of mergers and acquisitions. As terrorist attacks are generally rare (the number per capita is typically low), we also report the effect of an increase in terrorist attacks of one sample standard deviation on the relative change in investment (the log difference in the M&A flow). A one sample standard deviation increase in terrorism is associated with a decline of 31% in the expected investment flow, with a standard error of 9%.

Column 2 of Table I reports the same regression, adding terrorist attacks directed against businesses. The coefficient is larger, suggesting that one extra attack per million inhabitants reduces the investment flow by around 78%, which is a larger impact than the general attacks. Business attacks are rare, however, and one sample standard deviation in attacks leads to less impact: a 20% reduction in the flow.

Columns 3 and 4 report the estimates with firm-year specific effects. Effectively, the variation exploited here is from comparisons of the same firm in the same year, observing investment decisions in multiple locations. The regression thus controls for the supply of funds from the firms, isolating host country-specific drivers of the M&A flow of firms. That increases the magnitude of the estimated impact by about 15%.

Impacts on expected investment

Estimations from a Poisson model. Dependent variable is the level of investment. Standard errors clustered at the host-country-year level. ***p < 0.01, **p < 0.05, *p < 0.1.

The model of column 7 nests business-targeting attacks per capita with the sum of all other attacks. The coefficients of both variables are estimated with larger standard errors, possibly because of the correlation between the number of business-targeting attacks and other attacks. The coefficient for business-targeting attacks falls substantially compared to column 6, while the coefficient for other attacks is somewhat smaller than the coefficient for the sum of attacks reported in column 5. As both variables are measured on the same scale, we use a Wald test for the equality of the two coefficients which does not reject (p = 0.77), suggesting that the coefficients of business-targeting and non-business-targeting terrorism on investment do not differ significantly.

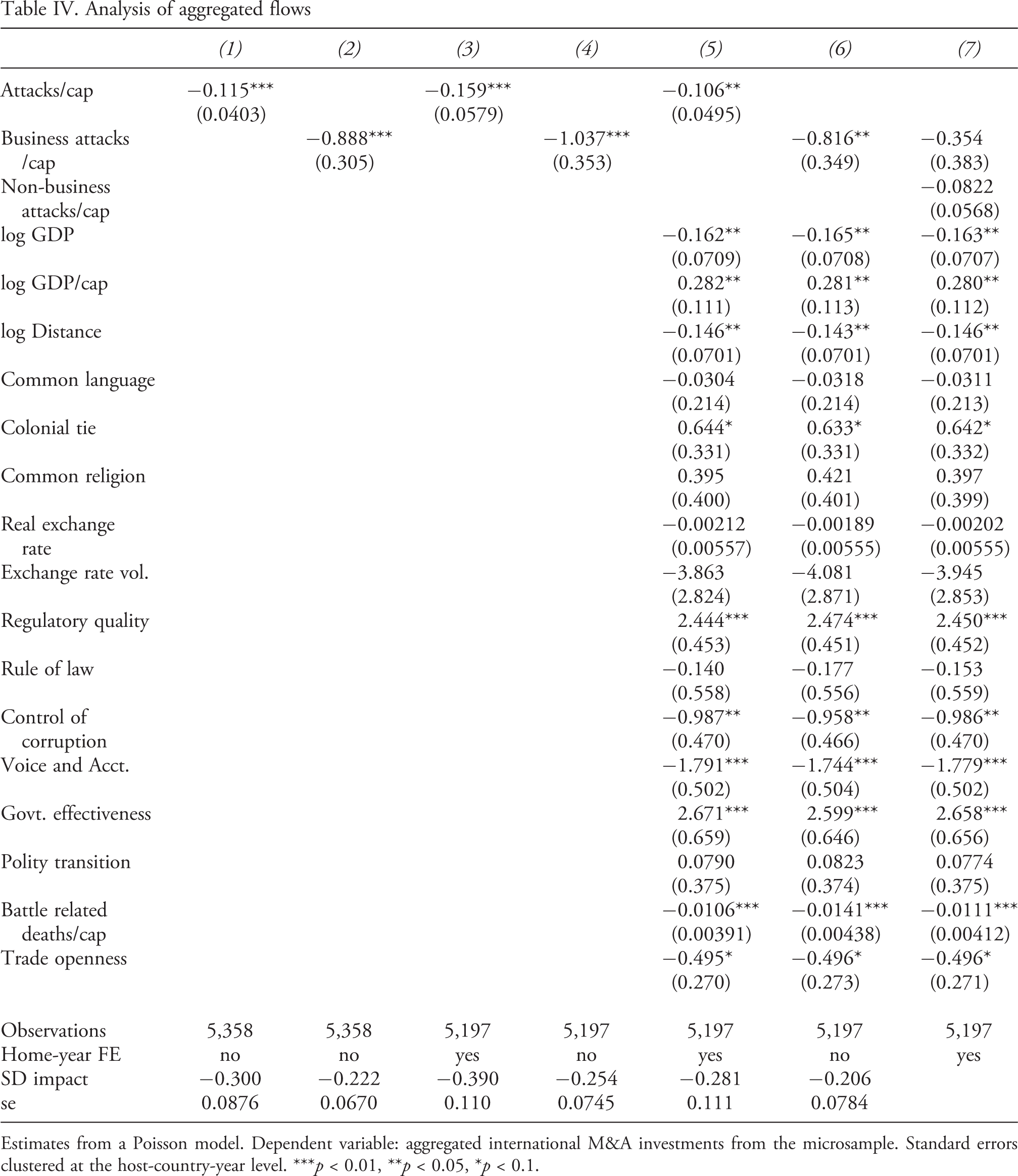

Do the estimates reported here differ from an analysis on aggregate, country-level flows of mergers and acquisitions? To investigate the differences, we aggregated our microdata by origin-destination country pair and year, and ran the same regressions at the country-level. The results are reported in Table IV in Appendix A. The estimates without fixed effects or controls provide a similar coefficient to the micro-level estimates. With home country-year fixed effects, the nationally aggregated data suggest far stronger impacts than the micro-level data. That difference shrinks when controls are added, with the estimated impact in the national data now 30% smaller than in the microdata.

Entry decisions: Intensive and extensive and intensive margin

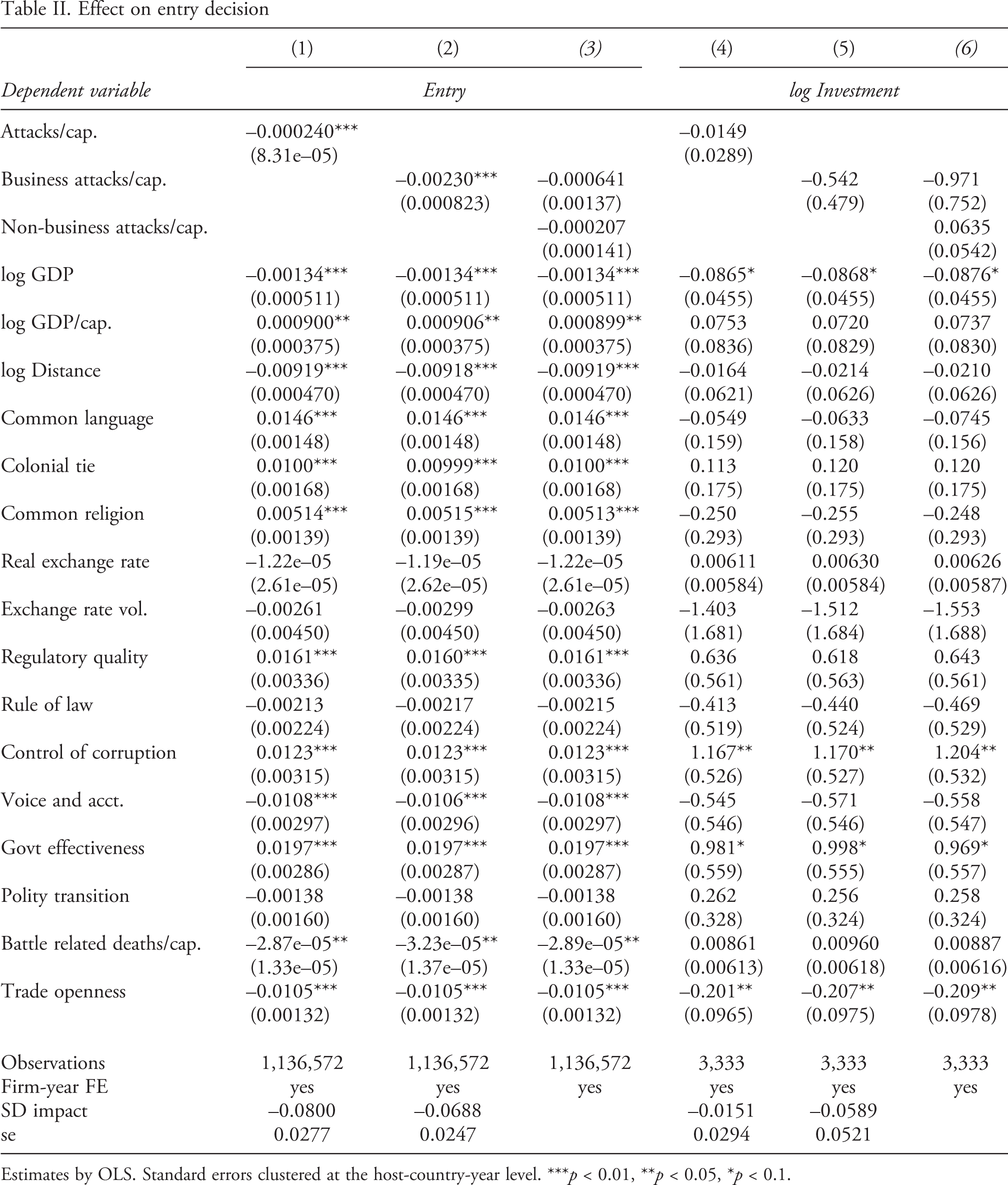

To estimate the impact of terrorism on the extensive margin, we use the selection into M&A in a host country – a dichotomous variable – as the dependent variable and repeat the same analysis.

Given the intensive fixed effects structure, we opt for a linear probability model over a logit model. This choice makes different assumptions about the underlying distribution of the error term, and about the theoretical assumption whether the dependent variable could be outside the 0 to 1 range. For the regressions reported below, the linear probability model predicts outside the range of 0 to 1 for less than 10% of the cases. For the intensive margin, we restrict the sample to observed investments. We regress the log of the invested sum on measures of terrorist activity.

Columns 1–3 of Table II report the results of regressions on the entry decision. The OLS model shows negative significant effects of both general and business-targeting terrorist attacks on the likelihood of entry. As entry is a rare event, we report the relative change in entry probability if the terrorism measure increases by one standard deviation: it is –8% for general attacks and –7% for business-targeting attacks. Nesting the count of attacks per capita targeting business with the count of other attacks (in column 3) and testing the coefficient equivalence with a Wald test again suggest no significant differences in their impact on the entry decision.

The intensive margin decision is reflected in columns 4–6. They show no significant impact of any of the measures of terrorism on the size of the investment. This also occurs in the (unreported) specification with no fixed effects and controls. Moreover, other determinants, like institutional quality measures, do affect the investment size. Hence it seems that conditional on investing, firms hardly adjust the size of their investment to terrorist activity. 6

The extensive margin impact at sample averages seems smaller than the combined margin model suggests in Table II. By Equation (2), given that intensive margins do not adjust, one might expect relative changes in the extensive margin to equal the overall margin. That expectation only holds, however, if the entry probability and the size of potential investment are uncorrelated across destinations. A likely explanation for this difference is that terrorism deters entry more strongly in destinations where large investments would be expected (note that the Poisson model and the extensive margin model use the same sample and covariates).

Impact by business targets

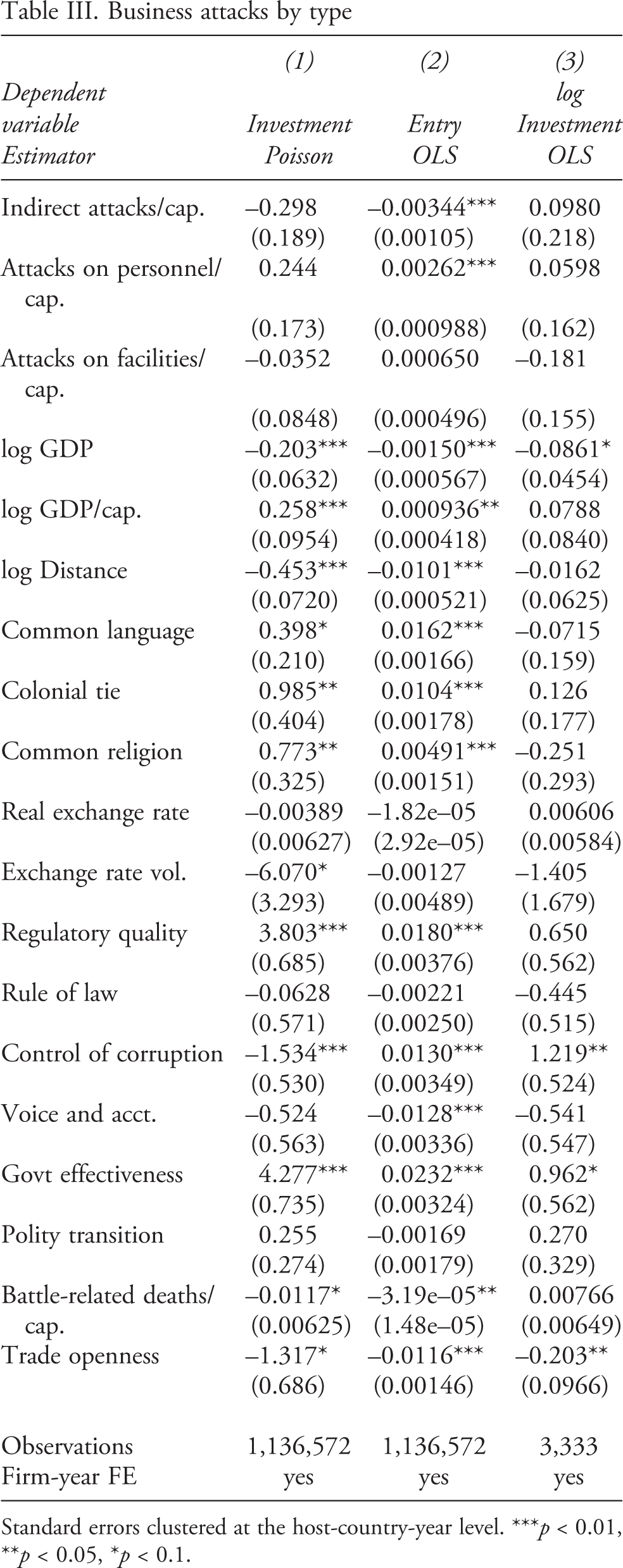

A finding in contrast to earlier results (Powers & Choi, 2012) is that business attacks seem to have no different impacts, compared to other attacks. From the arguments surveyed in the literature review, one might expect the two impacts to differ. The risk of direct damages to local assets possibly plays a different role in firm decisions than the more indirect risk of poorer business climate or societal disruption, such as logistical problems.

The GTD, the source of terrorism data, allows further data disaggregation related to these mechanisms. In addition to the targeted party, it records the object or persons threatened to generate leverage, including a firm’s building or staff. To see if firms fear direct attacks on their physical assets or personnel, we split up business-targeting attacks into (i) those directed at people (assassinations and assault), (ii) physical assets (facility, infrastructure, and vehicle hijackings), and (iii) indirect attacks – attacks that aim to terrorize businesses, but do not directly target their possessions or staff.

Effect on entry decision

Estimates by OLS. Standard errors clustered at the host-country-year level. ***p < 0.01, **p < 0.05, *p < 0.1.

These results suggest that when splitting up business-targeting effects, international investments are not particularly sensitive to the risk of damages to property and personnel. Instead, the entry decision seems more sensitive to attacks on related parties or bystanders.

Business attacks by type

Standard errors clustered at the host-country-year level. ***p < 0.01, **p < 0.05, *p < 0.1.

Robustness

We use the rest of this section to discuss the stability of our baseline results with respect to modeling choices. For reasons of space, we discuss the diagnostics and leave the detailed results in an Online appendix.

First, there is a large number of zeros for firm-specific destination years. The zero outcome might occur because investment is entirely unlikely for some combinations of firms and host countries, or because unobserved motivations drive the selection into a positive number. To account for potential excess zeros, we employed a zero-inflated Poisson model on the same data. The results for that model are very similar. Moreover, using an HPC test 7 (Silva, Tenreyro & Windmeijer, 2015), we find no evidence that the zero-inflated model statistically outperforms the regular Poisson model.

Second, the baseline specification employs the number of terrorist attacks in the year preceding the investment. To check if investment responds more sensitively to contemporaneous attacks or possible expectations of attacks, we introduce the contemporaneous attacks and the number of attacks in the year following the investment. A second motive to check sensitivity to future attacks is as an informal check of unobserved variables. If firms respond to unobserved trends or variables relating to the host country development that correlates with attacks, one might expect the future values of attacks – conditional on current attacks – to show up as significant. Table OA3 in the Online appendix introduces the lagged, contemporaneous, and one-year forward number of attacks. The coefficient for the number of contemporaneous attacks is negative (at about half the size of the lagged number attacks) but insignificant. This is consistent with the possibility that for an investment in a given year, a substantial number of attacks registered that same year after the investment takes place. Introducing the one-year forward number of attack (columns 3 and 4) yields an insignificant coefficient close to zero for the impact of future attacks.

Third, we report the number of attacks as our preferred measure of terrorist activity. One might argue that the impact of the attacks is better measured by the wounds and deaths they inflict. The number of casualties might better measure the social impact of the attack, as well as the scale and complexity of the operations. On the other hand, many attacks, in particular those targeted at businesses, may not intend to cause casualties at all, but rather physical or reputational damage.

To test for this difference, we have added measures of the number of killed and wounded to our baseline regressions, in addition to the simple count of attacks. Table OA4 in the Online appendix reports the results. Both on the combined margin and on the extensive margin, the number of attacks has a significant negative impact, while the number of killed and wounded has a positive impact. These estimates need to be interpreted keeping in mind the correlation between the two – the number of casualties in a country does not generally increase the likelihood of entry, because they imply a larger number of attacks, which reduces the likelihood of entry. We find no significant results for the intensive margin. Altogether, this suggests that the casualty number is not a better measure of deterring force than the number of attacks.

Fourth, we check the logged version of the number of attacks per capita. While this offers benefits in interpretation and possibly in functional fit, a major downside is that it causes sample selection: countries without attacks are dropped from the sample. Table OA5 in the Online appendix reports the results for the logged measures of terrorism. The results are fairly similar – there are negative impacts on the combined margin and the extensive margin, and the impacts of a sample standard deviation change are comparable. On the extensive margin, the impact of a one standard deviation increase in terrorism is stronger when estimating in logs. This is not due to sample selection – in the same sample, the standard deviation impact is around –10%, in line with earlier results. Given the sample losses, we report level impacts, but the impact along the extensive margin may be slightly stronger when measured in logs, in fact explaining the combined margin.

Discussion and conclusion

Terrorist attacks prevent countries from attracting international investment. Studying a large sample of firms engaging in cross-border mergers and acquisitions, we document that a one sample standard deviation increase in terrorist attacks reduces the expected investment in the country of a given firm by roughly 30%.

Methodologically, our results contribute to the literature by employing a firm-level analysis rather than a nation-level analysis. We compare decisions by the same firm through means of a fixed effects strategy, which rules out that variation among investing firms explains these results. We also show that a comparable analysis at aggregated level may put the estimated impact 30% higher or lower, depending on the choice of control variables. Related literature, mostly based on country-level analyses, reports a similar magnitude for a one standard deviation increase in terrorism, although the bandwidth is large. Powers & Choi (2012) on the one hand report a roughly 56% decline in investment following a one standard deviation increase in terrorism, 8 but Abadie & Gardeazabal (2008) 9 and Ouyang & Rajan (2017) report 21% and 11%, respectively.

The firm-level analysis also allows us to study entry choices in more detail. In our sample, firms respond to terrorism by withholding the entire investments – an extensive margin. There is little evidence to suggest that firms adapt the size of their investment. Arguably, this amplifies the negative consequences of terrorism, as recent insights from the trade and investment literatures suggest that the complete exits are harder to reverse, and have substantial macroeconomic costs.

We find no evidence that firms are more fearful of business-targeting attacks than of other attacks, nor that they fear attacks on businesses’ physical assets or personnel more than other forms of attacks. This suggests that the indirect costs of terrorism, for instance in terms of disrupting overall business environments, hampering local trade and logistics, and damaging reputations, may be as large as the direct costs of damaged property and risks to staff. This runs counter to the findings of Powers & Choi (2012).

These results are relevant to theories of capitalist peace. They confirm that international investors are sensitive to local terrorism, and may punish conflicts or poor policies to prevent them with exit. Importantly, our results also suggest that it is not just hostility to (foreign) firms that makes investors leave. Rather, terrorist attacks in general are discouraging, suggesting that economic openness may punish many different types of internal conflict.

A non-negligible qualification to our results is that they still leave room in the interpretation of the causal effects of terrorism. Despite differencing out firm-level fixed effects to rule out potential endogeneity from firm-level characteristics and shocks, endogeneity may remain in our results. At the country level, terrorism may respond to investment decisions, for instance, and unobserved country-level shocks correlated to terrorism and investment may be imperfectly controlled for. Hence, our estimates employing firm-level fixed effects should be seen as complementary to efforts to eliminate endogeneity deriving from the host country through time-series instrumentation of terrorism (e.g. Bandyopadhyay, Sandler & Youvas, 2014).

Footnotes

Appendix A

Analysis of aggregated flows

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | |

|---|---|---|---|---|---|---|---|

| Attacks/cap | −0.115*** | −0.159*** | −0.106** | ||||

| (0.0403) | (0.0579) | (0.0495) | |||||

| Business attacks | −0.888*** | −1.037*** | −0.816** | −0.354 | |||

| /cap | (0.305) | (0.353) | (0.349) | (0.383) | |||

| Non-business | −0.0822 | ||||||

| attacks/cap | (0.0568) | ||||||

| log GDP | −0.162** | −0.165** | −0.163** | ||||

| (0.0709) | (0.0708) | (0.0707) | |||||

| log GDP/cap | 0.282** | 0.281** | 0.280** | ||||

| (0.111) | (0.113) | (0.112) | |||||

| log Distance | −0.146** | −0.143** | −0.146** | ||||

| (0.0701) | (0.0701) | (0.0701) | |||||

| Common language | −0.0304 | −0.0318 | −0.0311 | ||||

| (0.214) | (0.214) | (0.213) | |||||

| Colonial tie | 0.644* | 0.633* | 0.642* | ||||

| (0.331) | (0.331) | (0.332) | |||||

| Common religion | 0.395 | 0.421 | 0.397 | ||||

| (0.400) | (0.401) | (0.399) | |||||

| Real exchange | −0.00212 | −0.00189 | −0.00202 | ||||

| rate | (0.00557) | (0.00555) | (0.00555) | ||||

| Exchange rate vol. | −3.863 | −4.081 | −3.945 | ||||

| (2.824) | (2.871) | (2.853) | |||||

| Regulatory quality | 2.444*** | 2.474*** | 2.450*** | ||||

| (0.453) | (0.451) | (0.452) | |||||

| Rule of law | −0.140 | −0.177 | −0.153 | ||||

| (0.558) | (0.556) | (0.559) | |||||

| Control of | −0.987** | −0.958** | −0.986** | ||||

| corruption | (0.470) | (0.466) | (0.470) | ||||

| Voice and Acct. | −1.791*** | −1.744*** | −1.779*** | ||||

| (0.502) | (0.504) | (0.502) | |||||

| Govt. effectiveness | 2.671*** | 2.599*** | 2.658*** | ||||

| (0.659) | (0.646) | (0.656) | |||||

| Polity transition | 0.0790 | 0.0823 | 0.0774 | ||||

| (0.375) | (0.374) | (0.375) | |||||

| Battle related | −0.0106*** | −0.0141*** | −0.0111*** | ||||

| deaths/cap | (0.00391) | (0.00438) | (0.00412) | ||||

| Trade openness | −0.495* | −0.496* | −0.496* | ||||

| (0.270) | (0.273) | (0.271) | |||||

| Observations | 5,358 | 5,358 | 5,197 | 5,197 | 5,197 | 5,197 | 5,197 |

| Home-year FE | no | no | yes | no | yes | no | yes |

| SD impact | −0.300 | −0.222 | −0.390 | −0.254 | −0.281 | −0.206 | |

| se | 0.0876 | 0.0670 | 0.110 | 0.0745 | 0.111 | 0.0784 |

Estimates from a Poisson model. Dependent variable: aggregated international M&A investments from the microsample. Standard errors clustered at the host-country-year level. ***p < 0.01, **p < 0.05, *p < 0.1.

Replication data

Acknowledgements

We would like to thank Caroline Witte, Sjoerd Beugelsdijk, Steven Brakman, and Gerrit Faber for comments that substantially improved the article.