Abstract

Idiosyncratic shocks, mainly health shocks, are common among rural households in developing countries, and as a result, many non-poor households fall into poverty and poor households remain poor. This study investigates the impact of a universal public health insurance policy, namely Rashtriya Swasthya Bima Yojana (RSBY), on household vulnerability to poverty (VtP) in rural India. Using 17,468 national-level household data, household VtP has been estimated using feasible generalised least squares (FGLS), and the impact of a health insurance policy on household VtP has been investigated using propensity score matching (PSM) and endogenous switching regression (ESR). FGLS estimates show that VtP is found to be 33 per cent compared to a currently classified poverty headcount rate of 27 per cent. PSM and ESR results indicate that access to RSBY significantly reduces household VtP, especially in less developed states.

JEL

Keywords

1. Introduction

In developing countries, rural households are highly exposed to different types of shocks such as weather and demographic shocks (Dercon, 2005; Günther & Harttgen, 2009; Khosla & Jena, 2023). These shocks can cause households to remain in or fall into poverty due to their limited mitigating ability (Dercon, 2005; Günther & Harttgen, 2009; Khosla, 2022; Vo & Van, 2019). The shocks include loss of assets, jobs, floods, droughts and incidents such as disease and death (Carter et al., 2008). Among these, illness has always been at the forefront of the shocks tormenting poor households (Atake, 2018; Khosla et al., 2023; Vo & Van, 2019), and these households remain poor for an extended period due to a lack of access to health services and financial inability to seek hospitalisation and buy health insurance (DeLoach & Smith-Lin, 2018; Vo & Van, 2019). In India, public health insurance programmes have been introduced to help the poor access good-quality health services. However, there is little evidence on whether such health insurance policies—as a capacity enhancement tool—are able to reduce vulnerability to poverty (VtP) (DeLoach & Smith-Lin, 2018; Vo & Van, 2019).

Despite massive investment by the Indian government to provide health care services to its citizens, millions of people still fall into poverty every year due to poor health (Berman et al., 2010; Garg & Karan, 2009; Goyanka et al., 2019; Shahrawat & Rao, 2012). The situation is exacerbated by the fact that only 14 per cent of rural households are covered by any health insurance (Planning Commission, GoI, 2019). This figure of low insurance coverage underscores the critical role public health insurance policy could play in reducing poverty and VtP in India. Expanding the reach and effectiveness of these policies could not only mitigate health-related financial shocks but also improve overall economic resilience in rural areas.

Studies in India have mainly examined the impact of health policy on reducing out-of-pocket expenditure (OOPE), related to the implementation of the schemes and utilisation, and are mainly related to ex-post poverty reduction (e.g., Azam, 2018; Boyanagari & Boyanagari, 2019; Shahrawat & Rao, 2012; Singh & Kumar, 2017; Taneja & Taneja, 2016). Studies from other countries show a similar focus. In China, Lei and Lin (2009) found no reduction in OOPE or increase in healthcare utilisation, while Wagstaff et al. (2007) reported no impact on OOPE in Vietnam, and Ataguba and Goudge (2012) found no reduction in South Africa. However, other studies show positive effects. In China, Wagstaff (2010) and Axelson et al. (2009) reported reduced OOPE, with Wagstaff and Yu (2007) noting lower ex-post poverty. Galárraga et al. (2010) found healthcare insurance reduced OOPE for Mexico’s poor. In Ghana, Aryeetey et al. (2016) observed reduced OOPE, catastrophic expenditure and poverty. Liu and Zhao (2014) and Peng and Conley (2016) found health insurance lowered OOPE and increased utilisation in China, while Atake (2018) reported reduced VtP in South Africa. Similarly, Habib et al. (2016) highlighted reduced OOPE, borrowing and poverty across various contexts. However, there is relatively scant evidence of the economic impact of health insurance policy, especially on reducing VtP in developing countries in general and India in particular. One exception is Vo and Van (2019), who assessed VtP and found that health insurance reduces VtP in Vietnam.

This study investigates whether access to public health insurance policies reduces the likelihood of households falling into poverty in India. It contributes to the literature on estimating VtP and the role of social protection in reducing it in the following ways. First, unlike previous studies that provide an ex-post poverty impact of the health insurance programme, this study investigates the potential impact on ex-ante households VtP. Second, given the scant evidence of the impact of health insurance policy on ex-ante VtP, to the best of our knowledge, this study is the first to assess the impact of public health insurance policy on the reduction of VtP in India. The findings of the study provide causal impacts of Rashtriya Swasthya Bima Yojana and insights for possible revision of policies.

The remainder of the article is as follows: Section 2 explains the brief details of RSBY. Section 3 presents the material and methods used in the study. The interpretation of the findings is presented in Section 4. The concluding observations are presented in the final section.

2. Health Insurance Policies in India

The Indian government has implemented several health insurance policies since independence to help people who cannot afford private health insurance: for instance, the Employees’ State Insurance Scheme (ESIS) in 1948 and the Central Government Health Scheme (CGHS) in 1954. On 1 April 2008, the government launched a health insurance policy called Rashtriya Swasthya Bima Yojana (RSBY) intending to expand and help the poor and households working in unorganised sectors to access health facilities (Shahrawat & Rao, 2012). The goal of the scheme is two-fold: to provide financial protection against catastrophic health costs to the explicitly poor and workers belonging to unorganised sectors by reducing out-of-pocket hospitalisation expenses and to improve the access of poor households to quality health care.

Under the RSBY scheme, the government identifies households below the poverty line and those that belong to unorganised sectors are identified and issued a digital card to enrol them in the scheme. To identify beneficiaries, the government uses data from the National Sample Survey Organisation (NSSO) and household consumption/income. Further, employment-related household data collected by NSSO is used to identify households in unorganised sectors such as street vendors, beedi workers, Mahatma Gandhi National Rural Employment Guarantee Act (MNREGA) workers, sanitation workers, domestic workers, mineworkers and ragpickers.

Conceptual Framework

Beneficiaries need to pay ₹30 per family as an annual registration fee at the time of enrolment. The scheme covers hospitalisation expenses up to ₹30,000 on a floater basis for a family of five. Transport charges of ₹100 per visit—up to a maximum of ₹1,000—are also provided (Shahrawat & Rao, 2012).

On 15 August 2018, the Indian government announced the Ayushman Bharat‑National Health Protection Mission (AB‑NHPM), which will incorporate the ongoing centrally sponsored RSBY scheme. However, nationwide household data is yet to come into public notice for analysis (Planning Commission, GoI., 2018b).

3. Material and Methods

3.1 Data Source

The data comes from the India Human Development Survey (IHDS) 2011–2012. The survey was carried out by the National Council of Applied Economic Research (NCAER), New Delhi, India, with technical support from Maryland University, USA. The IHDS data is nationally representative data that contains 42,362 household data across the country supplemented by individual data. In addition to detailed demographic information on household members, the survey includes data on assets, health issues, employment, migration and insurance policies (Desai et al., 2018).

We restrict our sample to rural household data because urban household data are not available for several states and union territories. Having cleaned the data by removing missing data and outliers, the final dataset for our study consists of 17,468 households.

Rural data is particularly relevant for our analysis because of the high incidence of poverty in these areas. Poverty is more pronounced in rural areas, where 25.70 per cent of the population is poor, compared to 13.70 per cent in urban areas. About 83.3 per cent of households still live in rural areas (Planning Commission, GoI, 2018a). Productivity and income in the agriculture sector are low compared to other sectors of the economy. Agricultural income contributes 18 per cent to the average annual gross income; however, more than 70 per cent of households in rural areas still depend on the agriculture sector for their livelihood (Planning Commission, GoI, 2011).

Since the poverty threshold level is necessary for the calculation of VtP, we have used a state-specific poverty line laid down by the Indian government. It comes from the state-specific poverty line for each state defined by the Suresh Tendulkar Committee for the year 2011–2012 (Planning Commission, GoI, 2014).

The poverty incidences are based on Foster et al. (1984). The equation is as follows:

where pα is the Foster Greer and Thorbecke (FGT) index (0 > pα < 1), N is the total number of sampled households considered for the study, z is the predetermined poverty line, yi is the monthly per capita expenditure of the ith household,

3.2 Analytical Framework and Econometric Specification

3.2.1 Conceptual Framework

Measuring vulnerability enables the identification of people who are not poor but may become poor, as well as those who will remain poor. Once identified, appropriate policies can be designed to prevent the former from falling into poverty and to help the latter to escape poverty. Clearly, measures that are focused on the current profile of poverty may be ineffective for those vulnerable individuals and households. By obtaining a vulnerability profile, both existing and future poverty can be targeted.

Economists define vulnerability as ‘exposure to negative shocks to welfare’ (Glewwe & Hall, 1998). One of the most popular approaches to measuring VtP is ‘vulnerability as expected poverty’ (VEP) developed by Chaudhuri et al. (2002), which uses cross-sectional data. The VEP model defines vulnerability ‘within the framework of poverty eradication, as the ex-ante risk that a household will, if currently non-poor, fall below the poverty line, or if currently poor, will remain in poverty’ (Chaudhuri et al., 2002).

Given the risks and shocks and lack of coping mechanisms, the government has undertaken several policy actions and interventions to either reduce or alleviate poverty through food security, employment, credit facilities and insurance for the poor and vulnerable (Azeem et al., 2019).

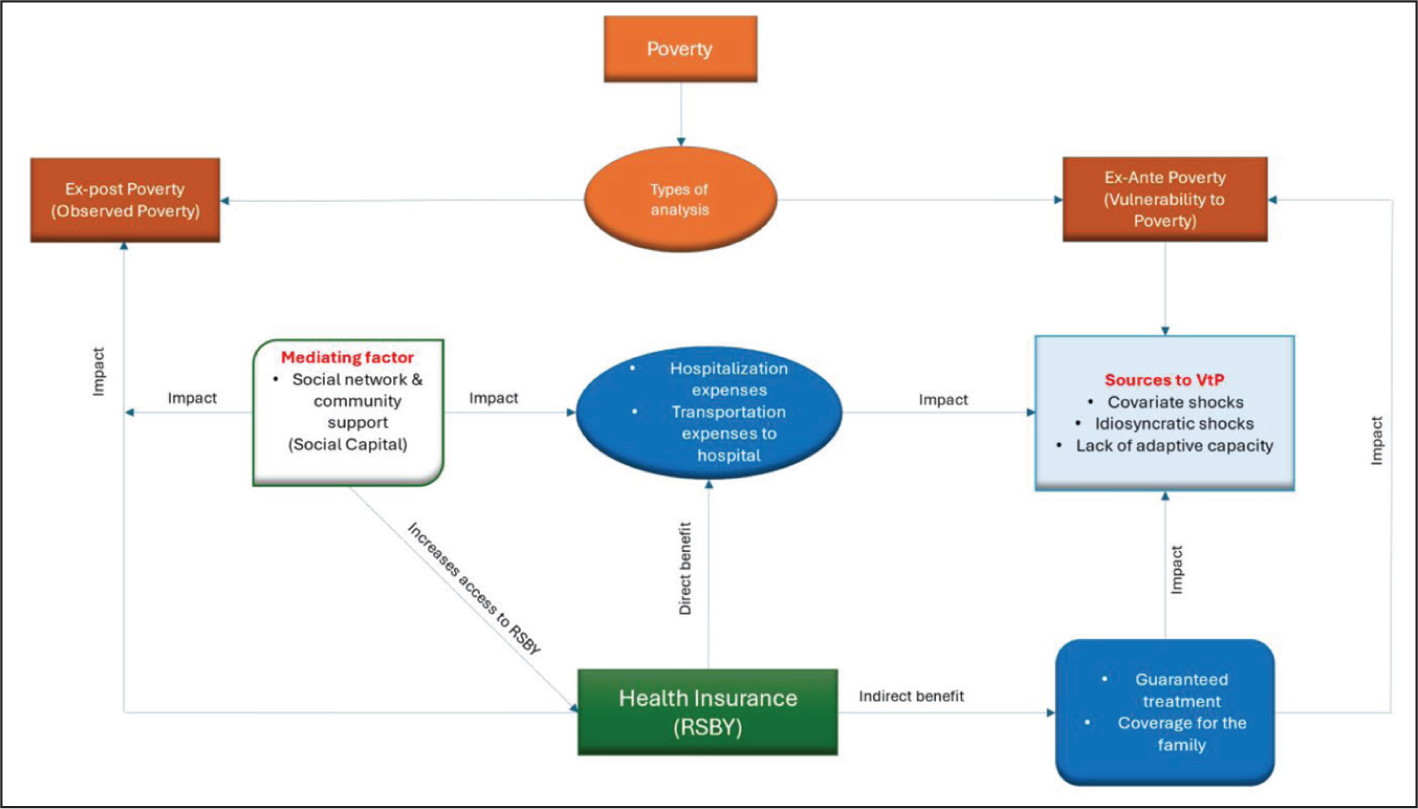

The conceptual framework of the study is presented in Figure 1. Poverty can be divided into two categories: ex-post poverty and ex-ante poverty. In the second part of the investigation, both ex-post and ex-ante vulnerabilities were estimated. Additionally, we utilised social capital as a mediating factor, which enhances access to RSBY by facilitating the dissemination of information and raising awareness about the social protection programme. This network-driven exchange of knowledge plays a crucial role in overcoming barriers to participation and improving the overall reach of the scheme. Finally, we investigated the effect of health insurance on the likelihood of being poor.

3.2.2 Vulnerability as Expected Poverty

The study estimated household vulnerability to expected poverty by employing the VEP approach devised by Chaudhuri et al. (2002). There is a growing body of evidence on estimating household VtP using this model (Chaudhuri et al., 2002; Günther & Harttgen, 2009; Jamal, 2009).

Given the absence of household panel data and detailed information on risks and shocks, the VEP approach has the advantage of estimating VtP by applying it to cross-sectional data. The following model has been adopted from the study by Chaudhuri et al. (2002).

The probability of household h being below the poverty line at time t + j. This can be expressed as

where Vht denotes the vulnerability of a household at the present time t, Pr represents the probability of a household falling into poverty in a time of t + j, In Ch, t + j represents the future consumption level of household h at time t + j and z shows the pre-specified poverty line. To estimate VtP, a model must be defined (Haughton & Khandker, 2009). The model can be written as

where Ch is the monthly consumption per capita of household h, β0 is the intercept, β1 is the slope coefficient, Xh is observable household characteristics (Table 1) and eh is the zero-mean disturbance random error term that captures the variability of household consumption due to idiosyncratic factors. Chaudhuri et al. (2002) estimated VtP following the three-step feasible generalised least squares (FGLS) approach introduced by Amemiya (1977). We do not provide a detailed estimation of the VEP approach, as it is a standard approach to estimate VtP.

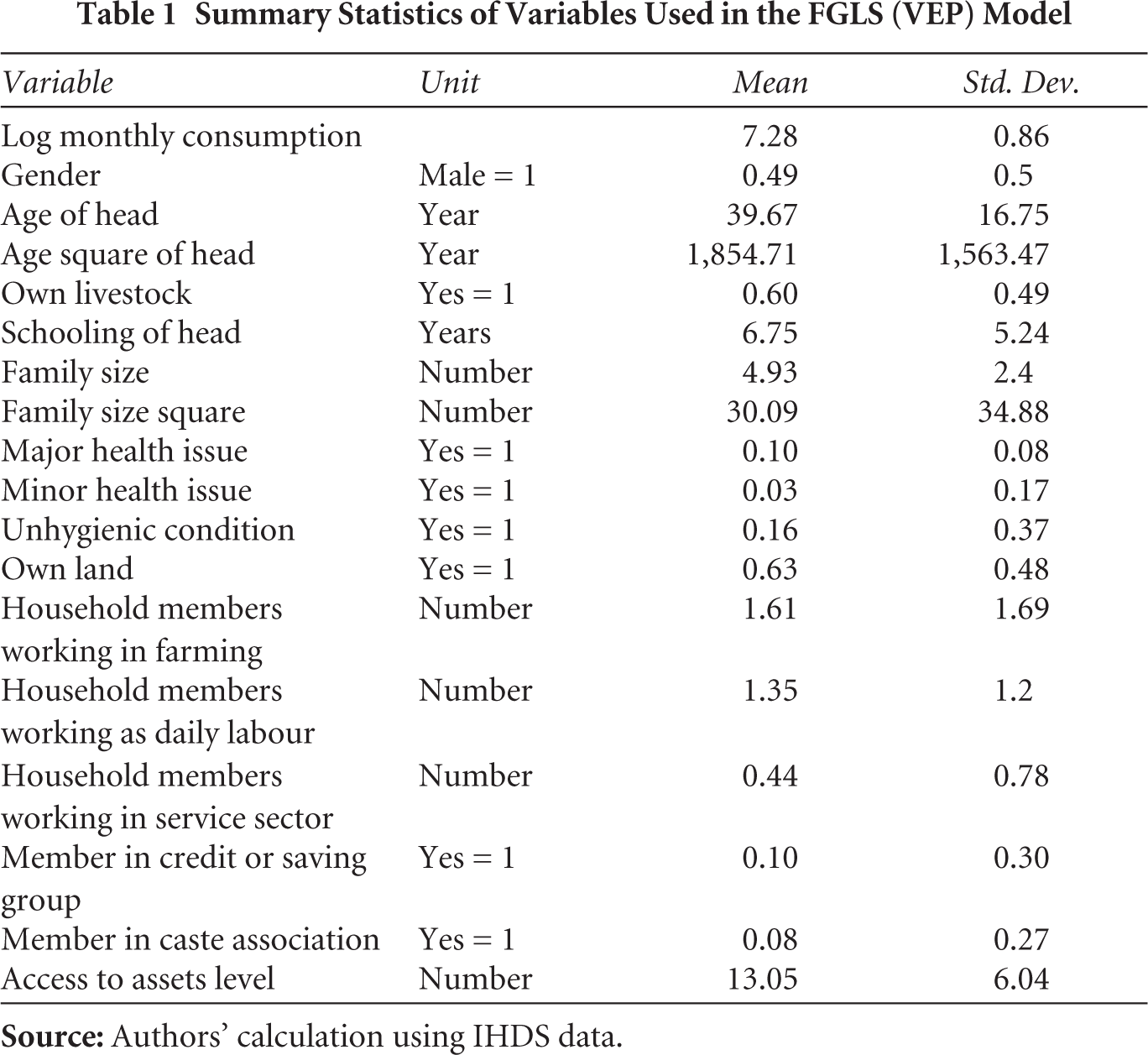

Summary Statistics of Variables Used in the FGLS (VEP) Model

After estimation of the expected mean and variance, VtP is estimated using the following equation:

where is the estimated ex-ante vulnerability of household h, indicates the probability

Further, a vulnerable threshold must be defined to estimate vulnerable or non-vulnerable households, which is arbitrary and generally considered 0.5 (50 per cent probability) (Günther & Harttgen, 2009; Haughton & Khandker, 2009). The details on choosing VtP threshold are presented in Chaudhuri et al. (2002). This study used the vulnerability threshold of 0.5 to estimate vulnerable or non-vulnerable households.

3.2.3 Propensity Score Matching Approach

The propensity score matching (PSM) approach has been used in the present study to evaluate the impact of health insurance policy—RSBY—on household VtP. Cross-sectional data usually has non-experimental biases such as selection bias (Wooldridge, 2002). PSM corrects for selection bias by matching a sub-sample of access to RSBY and non-access to RSBY that have similar observable characteristics and by making comparisons in the region of common support (Becker & Ichino, 2002). The present study assessed the impact of RSBY on only VtP households (estimated using the FGLS approach), showing similar characteristics. The average treatment effect on the treated (ATT), which is the impact of RSBY on those VtP households that have access, has been estimated as follows:

where Ti refers to treatment status of VtP household i and takes two values:

Matching requires building a new control group with similar characteristics so that for every treated observation (households with access to RSBY), there is an untreated one (households without access to RSBY). PSM constructs a probability that a household’s access to RSBY is conditional on its characteristics. This is done by running a logit model of ‘with access to RSBY’ and ‘without access to RSBY’ on the set of observable baseline characteristics. It can be written as

where

3.2.4 Endogenous Switching Regression

We used endogenous switching regression (ESR) analysis to address hidden bias. ESR distinguishes two regimes: one for households that have accessed RSBY and the other for households that have not accessed RSBY. The ESR is estimated in two stages, and Equation (7) for the latent variable model is estimated as follows:

When the expected gain of participation exceeds the value of non-participation, an i household participates in RSBY. Let A*i be a latent variable that captures the benefit of participation by the ith household. Zi is a vector of explanatory variables that describes how the regimes are selected. The parameter vector is α, and the error term is vi. In the second step, the outcome equation is estimated. The first-stage selection equation’s observations are used to determine which of the two regimes to join. The outcome equations for the two regimes are as follows: accessed and non-accessed, corrected for endogenous selection:

In both regimes, where Y1i and Y2i, i = 1,….,N, represents the dependent variables. X1i and X2i are each regime’s explanatory variables, β1 and β2 are the parameters that need to be estimated, and the corresponding error terms are u1i, u2i. λ1i and λ2i are the inverse Mill’s ratios (IMR) estimated from the equation of first stage selection and used in the equations for correction of selection bias (7a) and (7b).

Four estimates are computed by the second-stage outcome regressions: (a) actual results from the accessed scenario, (b) real results of the non-assessed scenario, (c) counterfactual outcome scenario from accessed and (d) counterfactual outcome scenario for non-accessed. The ATT is computed as (a)–(c), and the average treatment effect on the untreated (ATU) is computed as (d)–(b).

4. Results and Discussion

4.1 Household Characteristics

Table 1 provides descriptive statistics on the variables used in the analysis. Results from demographic characteristics of respondents show that women household heads are in the majority (51 per cent), the mean age of household heads is about 40 years and their average years of schooling are about 7 years. Household members affected by a major health issue, such as a severe accident, as well as minor health issues, such as short sightedness, are also reported. At least 16 per cent of households live in a house that is considered unhygienic, 63 per cent have access to land and about 60 per cent own livestock. On average, 13 assets are held by the households.

More members work in farming, followed by those in the daily wage and service sectors. On social capital, 10 per cent and 7 per cent of households are part of savings and caste association groups, respectively.

4.2 Household Vulnerability to Poverty

4.2.1 Correlates of Vulnerability to Poverty

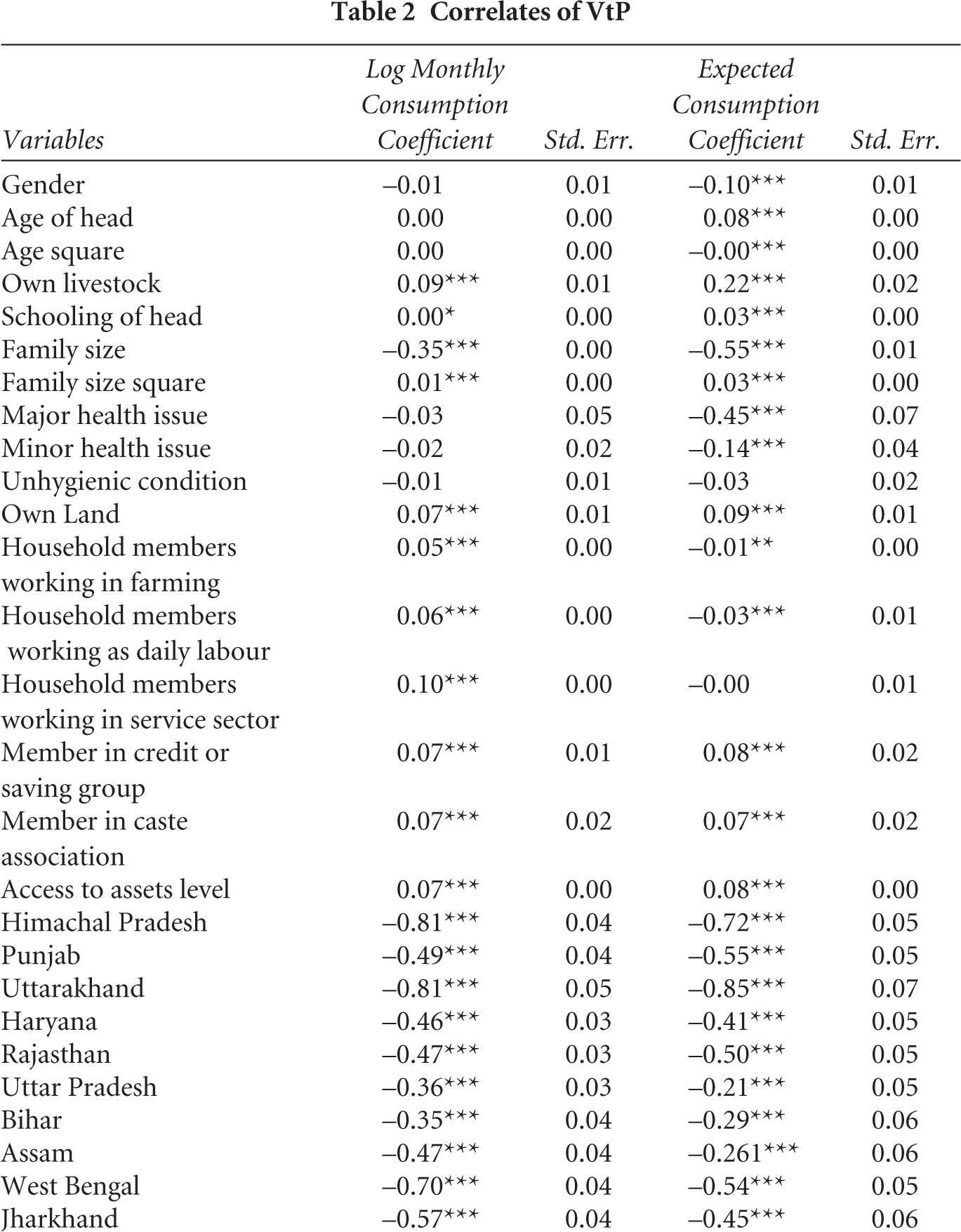

Table 2 presents the results for the estimates of ‘vulnerability as expected poverty’ using the FGLS approach. State dummies have been added to account for some of the unobserved factors arising from each state. Consistent with other studies, the coefficient for the years of schooling of the household head is positive and significant (Azeem et al., 2019; Günther & Harttgen, 2009; Jamal, 2009; Jena et al., 2024). Higher education of the household head plays a key factor in increasing consumption, reflecting that they have a higher per capita income.

Correlates of VtP

With respect to household size, the coefficient of household size is negative and significant, but its squared term (household size square) shows a positive association with household well-being, suggesting a non-linear association with consumption per capita. This finding is consistent with the past empirical VtP studies, which observed a negative association between household size and household consumption expenditure (Azeem et al., 2019; Jamal, 2009). The results also show that ownership of livestock increases consumption in the household by 9.3 per cent. Generally, livestock is considered to be a major livelihood asset in rural areas that works as a major coping strategy during adverse events.

On household occupation, households are generally categorised as the number of members working in farming, daily wage and service sectors. The findings show that the coefficients of household members working in all these sectors are positively significant, suggesting a positive association with consumption per capita. However, as observed from Table 2, household members in the service sector are more likely to increase consumption than with farming and daily wage earners. The regression results also indicate that the land ownership coefficient is positive and significant, which suggests that keeping other factors constant, ownership of land increases the household consumption level. This finding is consistent with previous studies that observed a positive association between land ownership and consumption per capita (Iqbal, 2013; Jha & Dang, 2009).

Social capital within the community is expected to play a key role in disseminating information. Social capital plays a significant role in escaping poverty and reducing VtP (Khosla & Jena, 2020, 2022). The findings show that households that are members of saving and caste association social groups are more likely to increase consumption by 6.7 per cent and 7 per cent, respectively. The regression results also indicate that households that possess more assets are more likely to increase their consumption level by 7 per cent. This finding is consistent with a study that observed lower vulnerability for households with higher assets (Jha & Dang, 2009). Recently, the estimation of poverty has been shifted to asset ownership, suggesting that households with better access to assets have more chances to escape poverty (Carter et al., 2008). Our findings bring further evidence of the criticality of maintaining a strong asset base to reduce poverty and vulnerability. In the case of the state dummy, states provide different levels of facilities to the population, with developed states providing better facilities to households.

4.2.2 Vulnerability Estimates

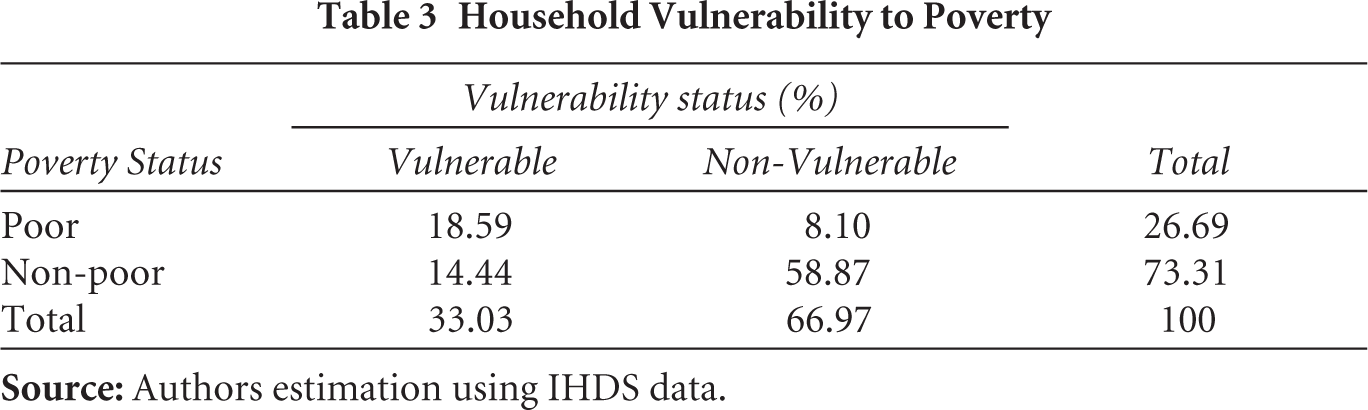

The estimates from the FGLS show that 33 per cent of the households have a greater than 50 per cent chance of falling into poverty (Table 3). The results show that the percentage of vulnerable households exceeds that of the currently classified poor by 27 per cent. This finding is consistent with previous VtP studies (Azeem et al., 2019; Chaudhuri et al., 2002; Vo & Van, 2019). Further, about 19 per cent of poor households are likely to fall into extreme poverty, and 14 per cent of non-poor households are likely to fall into poverty. Although the rate of households likely to remain poor is relatively high, the incidence of households at risk of falling into poverty underscores the importance of health shock in rural India. The findings suggest that policies that target only the poor should also consider VtP households to reduce the likelihood of falling into poverty.

Household Vulnerability to Poverty

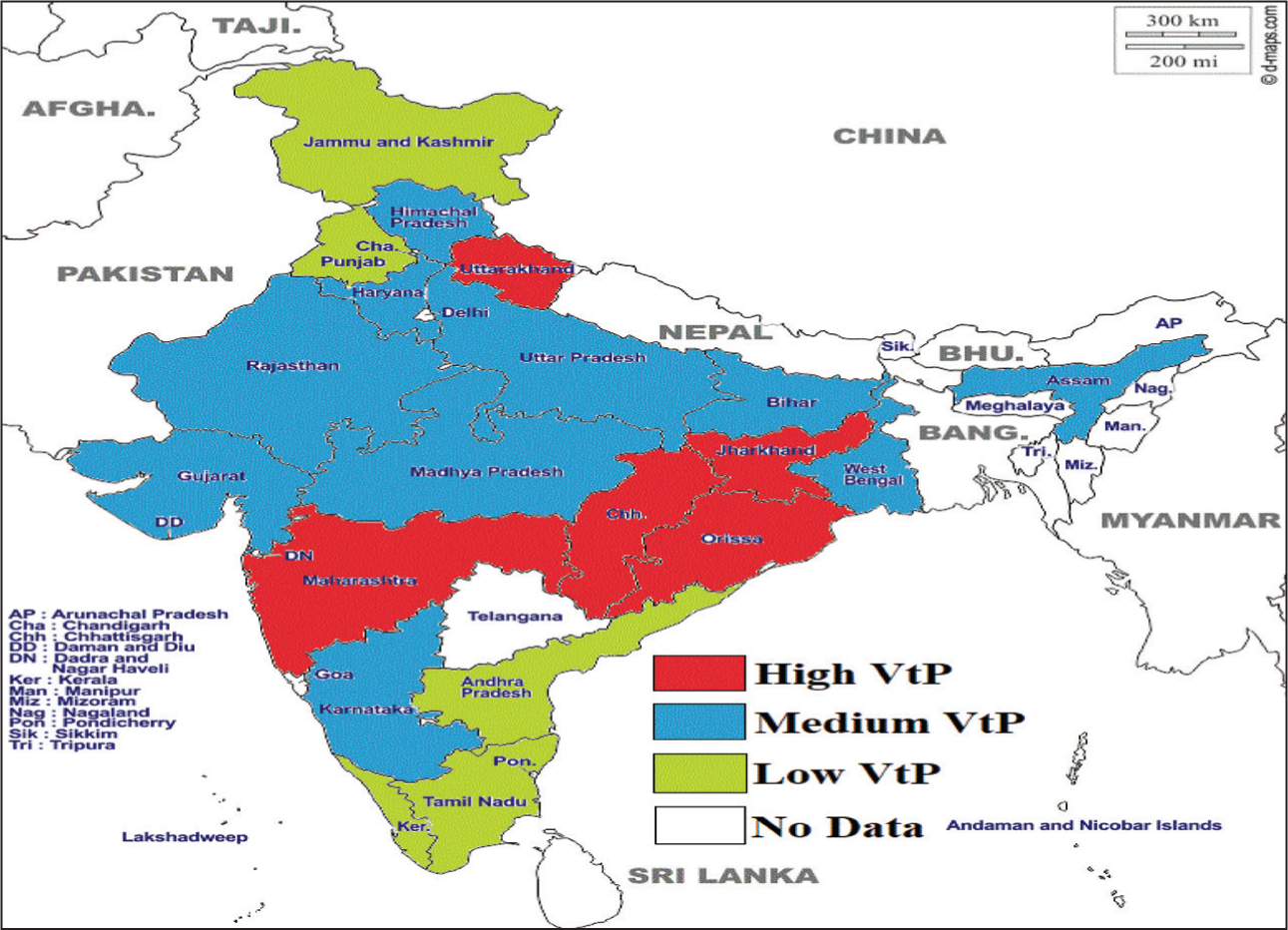

The VtP estimation shows that households in economically backward states are more vulnerable (Figure 2 and Table 4). Uttarakhand, Chhattisgarh, Odisha, Maharashtra and Jharkhand are extremely vulnerable states where between 40 per cent and 54 per cent of households have a chance of falling into poverty, whereas Tamil Nadu, Jammu & Kashmir, Kerala and Andhra Pradesh are less vulnerable states. This suggests that households in developed states are better at accessing public facilities for health and transportation, which are provided in a developed state and help reduce poverty (Charlery et al., 2016).

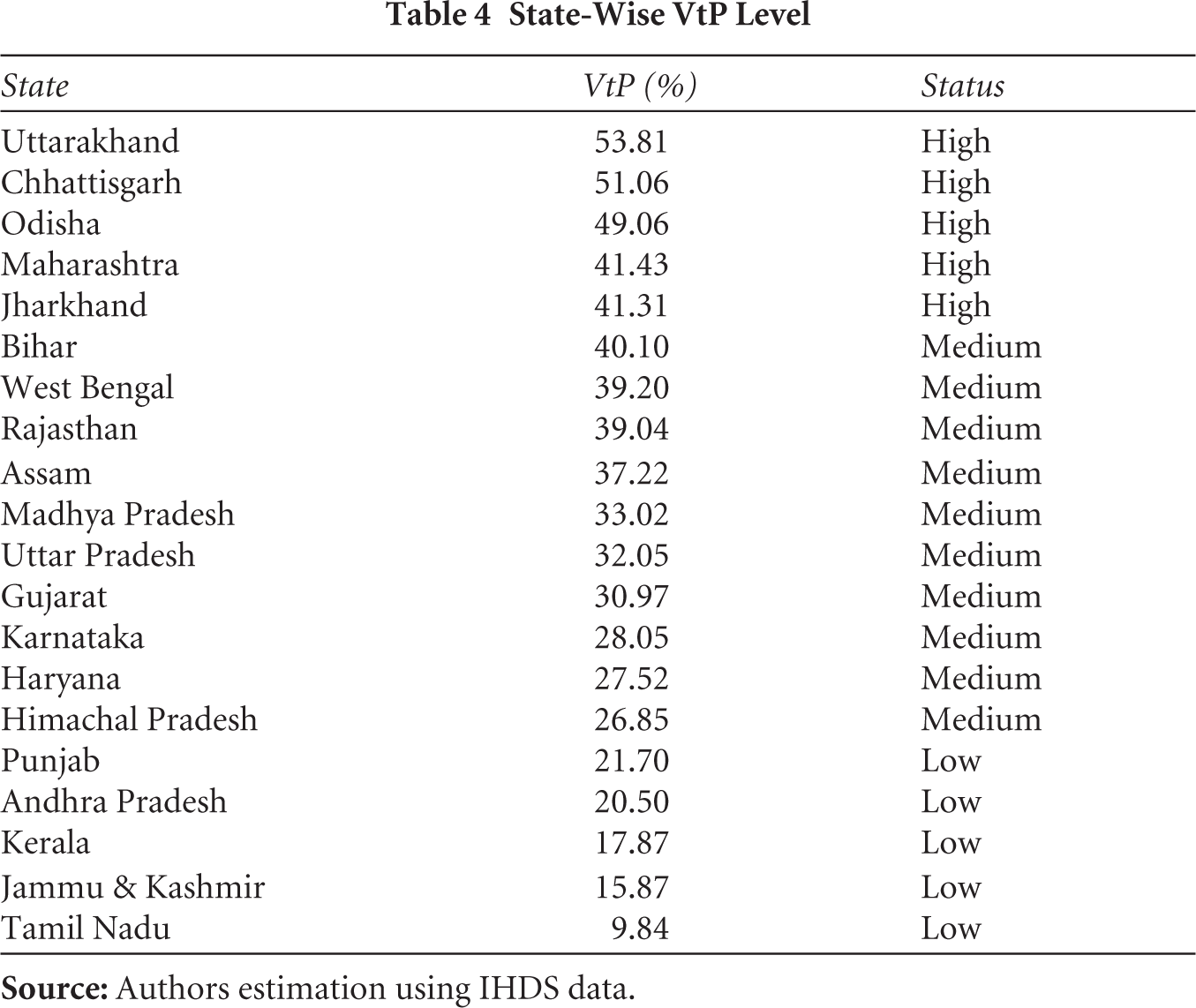

State-Wise VtP Level

However, households in developed states can also fall into poverty. The heterogeneous impact of policies and other adverse events can pull many households into poverty. Maharashtra fell among the top VtP states. The possible reasons could be severe health issues in rural areas, followed by adverse events such as recurring drought. In this study, we consider only household consumption per capita as the well-being indicator, which may differ when we use HDI indicators (education, health and the standard of living) to estimate VtP.

Chhattisgarh, Odisha and Jharkhand are known for the high poverty rate. In these states, economic growth and development are quite retrograde. Households in these states are mostly dependent on the agriculture sector, literacy rates are low (Planning Commission, GoI, 2011) and infant mortality rate (IMR) is high (NIMS, ICMR, & UNICEF, 2012).

4.3 Impact of Health Insurance on VtP

This section explains the empirical results of PSM. The comparison among adopters and non-adopters of RSBY and the determinants of RSBY adoption are presented in Tables A1 and A2.

4.3.1 Uptake of RSBY Across States

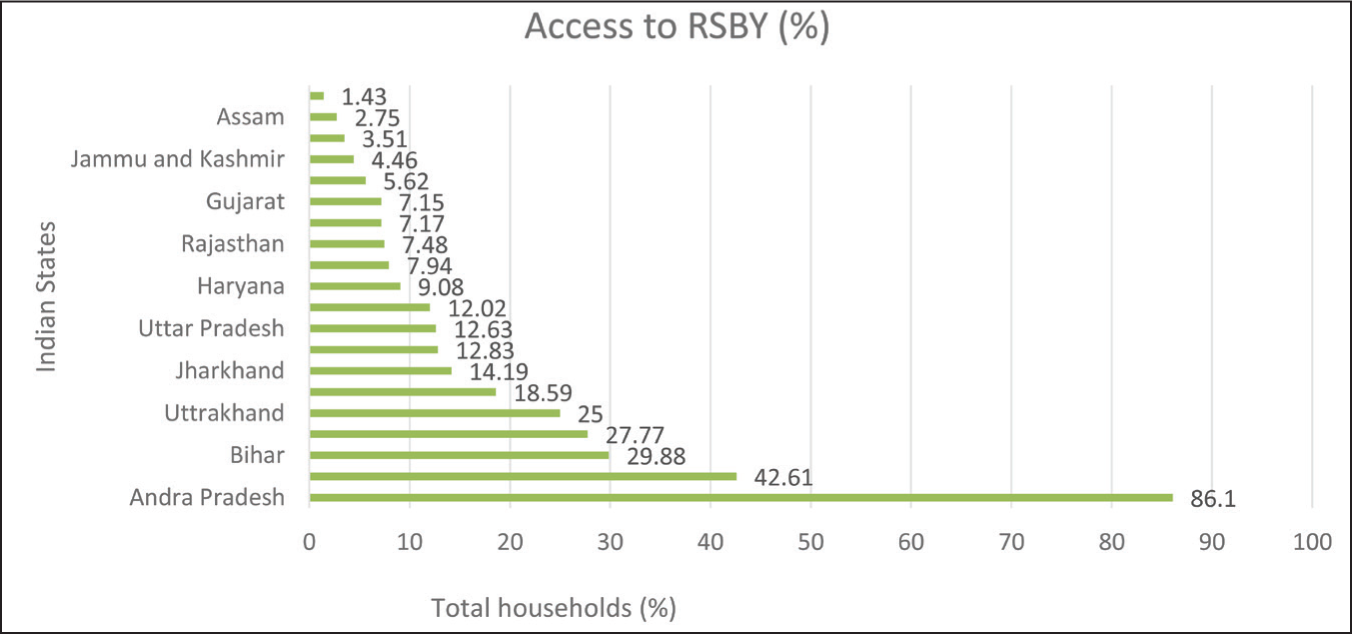

Figure 3 represents the state-wise household access to RSBY. There is a significant difference in the distribution of RSBY cards among states: Andhra Pradesh (86.1 per cent) has the highest fraction of households with access to RSBY cards, while Tamil Nadu (1.43 per cent) has the lowest. The top five states in terms of percentage of access to RSBY cards are Kerala (42.61 per cent), Bihar (29.88 per cent), Chhattisgarh (27.77 per cent) and Uttarakhand (25 per cent), whereas Assam (2.75 per cent), Punjab (3.51 per cent), Jammu & Kashmir (4.46 per cent) and Maharashtra (5.62 per cent) sit at the bottom.

It is also observed that RSBY card distribution is lower for many less-developed states such as Assam, Odisha and Rajasthan. In contrast, households in developed states such as Kerala, Uttarakhand and West Bengal have higher access to RSBY cards. Chakrabarti and Shankar (2015) show that there is a heterogeneous distribution of RSBY cards within the country.

4.3.2 Impact of RSBY on Household VtP

To assess the impact of public health insurance policy on household VtP, we first analysed the entire VtP dataset. However, the results were not significant. We then divided the states into two categories of less developed and developed states using an HDI value of 0.5 as the cut-off (Planning Commission, GoI, 2011) and performed the estimation for both categories. The results are statistically significant only for less developed states.

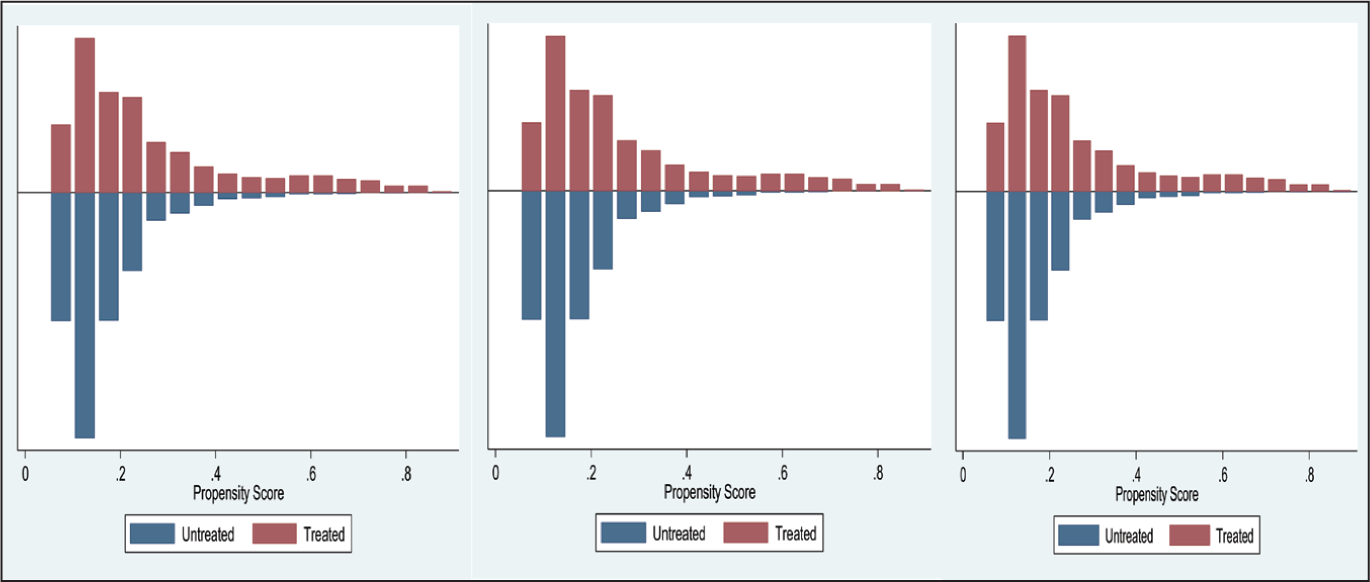

Table 5 reports the average effects of accessing RSBY on household VtP, estimated using the PSM approach. All three estimators—nearest neighbours (5), kernel matching and radius matching—yield similar results. For all the first-stage logit model’s explanatory variables, the differences after matching are statistically insignificant, which is a desired property for a good matching algorithm, which shows that the results are reliable. For the three matching methods, the PS graphs are shown in Figure 4.

Impact of RSBY on Household VtP, PSM Results

Table 5 also shows the ATT of accessing RSBY for VtP households in developed states, less developed states and the whole VtP sample. Accessing RSBY reduces VtP for all groups, but it is found to be statistically significant only for households in less developed states (states that have a lower HDI). The results indicate that households’ access to RSBY helps them cope with health shocks. Under all three algorithms, the decrease in VtP score ranges from 1.4 per cent to 1.7 per cent. These findings are consistent with previous studies on the impact of health insurance on VtP. Atake (2018) observed that access to health insurance reduces VtP in three African countries, namely Burkina Faso, Niger and Togo. Recently, Vo and Van (2019) have shown that health insurance reduces VtP in Vietnam with a 16 per cent reduction of VtP.

The findings in our study show that the public health insurance policy in India has a partial impact on VtP; that is, access to RSBY has resulted in a decline in VtP in less developed states (states with a lower HDI) compared to developed states. One possible reason for this finding could be the better infrastructure facilities available in developed states. Better facilities in terms of sanitation, roads and other facilities can result in higher income (Charlery et al., 2016). In developed states, rural households have access to free and better health care near their residents. The better-connected transportation facilities help them avail themselves of treatment at the early stage of health issues. However, given the poor living standards, it is quite difficult for poor households to spend on even a minor health issue. Further, considering the poor infrastructure facilities in rural areas, visiting a health centre may take an entire day to avail of the treatment. Since RSBY also provides transportation charges, it helps very poor households from less developed states. Another possible reason could be the poor standard of living of households in backward states. Poor people cannot afford to buy adequate amounts of nutritious food, preventive and curative health care, quality and affordable housing and education (Atake, 2018).

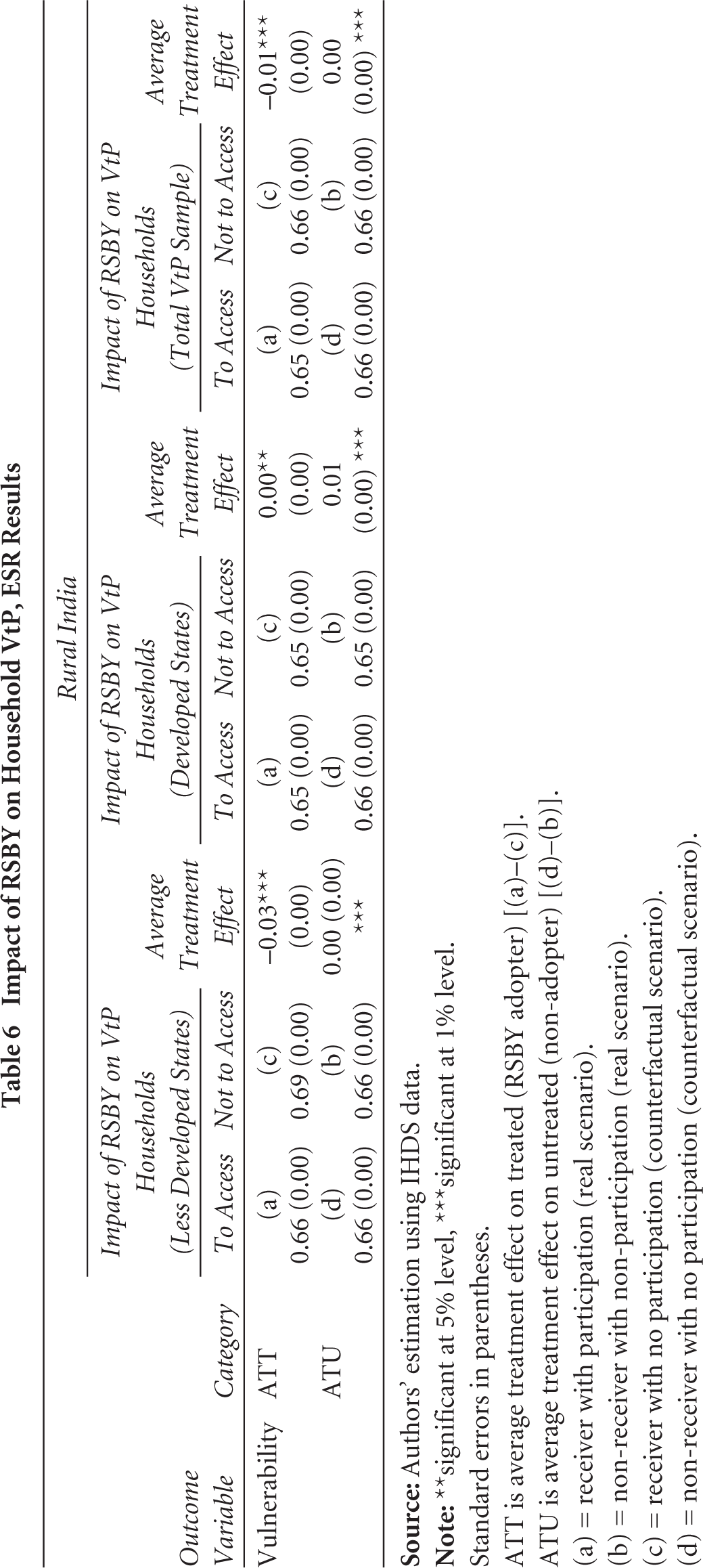

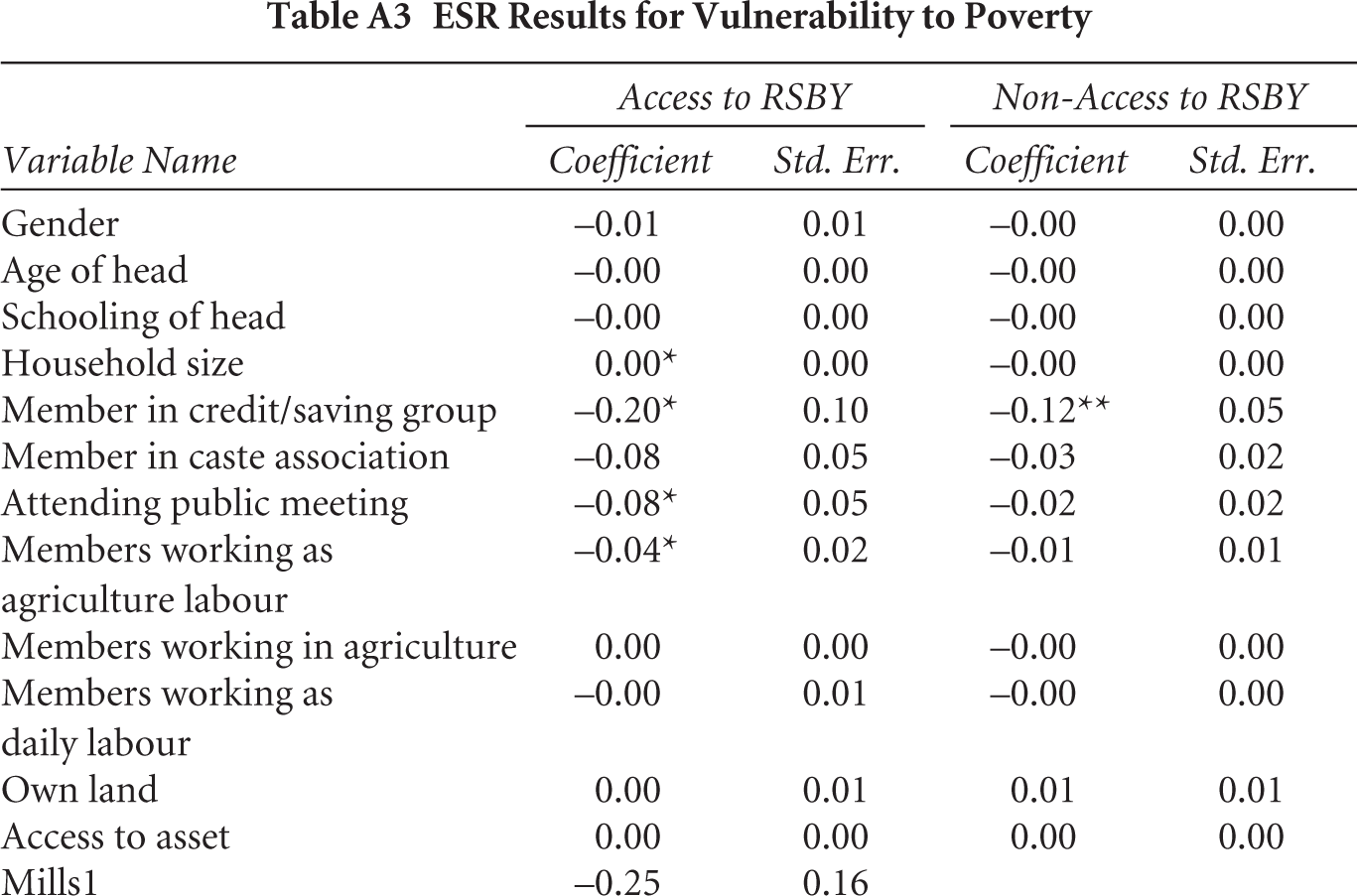

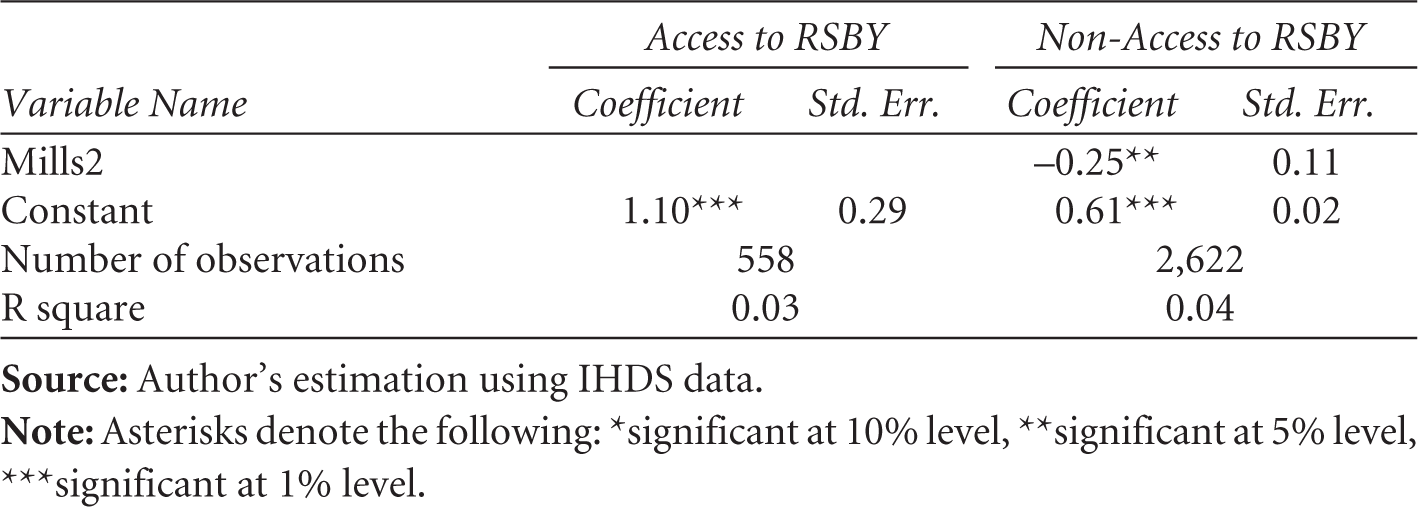

4.4 Results from the ESR Model

As the results of the PSM model may be biased due to unobserved factors, the ESR model was used to check the robustness of the estimated effects obtained from the PSM model. The advantage of the ESR model over the PSM model is that it can estimate the potential gain for the non-accessed had they accessed RSBY. The ATT and ATU of RSBY estimated from the ESR models are presented in Table 6, and the second stage ESR estimation results are presented in Table A3. These estimates corroborate the PSM model findings, showing that the ESR-based ATU is close to PSM-based estimates. There is a negative and statistically significant ATT of RSBY on household VtP, especially for the less developed and total VtP sample households. More specifically, the VtP effect for the RSBY access is –0.03 and –0.01, suggesting that RSBY reduces their probability of falling below the poverty line by 3 per cent and 1 per cent, respectively. Similarly, the ATU for the non-accessed is positive, indicating that if they had decided to access RSBY, their household VtP would have declined.

Impact of RSBY on Household VtP, ESR Results

Standard errors in parentheses.

ATT is average treatment effect on treated (RSBY adopter) [(a)–(c)].

ATU is average treatment effect on untreated (non-adopter) [(d)–(b)].

(a) = receiver with participation (real scenario).

(b) = non-receiver with non-participation (real scenario).

(c) = receiver with no participation (counterfactual scenario).

(d) = non-receiver with no participation (counterfactual scenario).

In the case of developed states, the ATT is positive and significantly associated with VtP (ATT = 0.00), which implies that the participation of households in RSBY has not reduced their probability of falling below the poverty line. This result corroborates the PSM estimates, which suggest that access to RSBY has no significant impact in developed states.

4.5 Confounding Factors: The Role of Rapid Economic Growth and Key Economic Policies (2000–2010)

The results suggest that households with access to RSBY are less likely to fall into poverty. However, the implementation of RSBY in India from 2008 onwards coincided with a period of rapid economic growth and significant economic policy changes, introducing several confounding factors that may have influenced its outcomes. During the 2000–2010 decade, India experienced robust economic growth, averaging about 6–7 per cent annually (Ministry of Finance, GoI, 2024). This economic surge led to increased household incomes, improved living standards and greater access to services, which could have indirectly enhanced the effectiveness of RSBY. For instance, higher household incomes might have improved the ability of beneficiaries to utilise health services, while economic growth likely spurred investments in healthcare infrastructure, both from private and public sources. Such improvements would enhance the healthcare environment in which RSBY operated, making it difficult to attribute changes in health outcomes or poverty reduction solely to the insurance scheme.

Moreover, various economic policies implemented during this period, such as the National Rural Health Mission (NRHM), Mahatma Gandhi National Rural Employment Guarantee Act (MGNREGA) and Public Distribution System (PDS), also likely influenced RSBY’s impact. These policies aimed to improve healthcare delivery, increase employment, provide food security and reduce poverty, thereby providing complementary benefits to RSBY’s objectives. For example, NRHM aimed to strengthen rural healthcare infrastructure, potentially increasing the availability and quality of services for RSBY beneficiaries. Similarly, MGNREGA helped increase rural incomes, which could enable households to afford indirect healthcare costs not covered by RSBY. The PDS aimed to improve the quality of life in rural areas by providing affordable access to essential food grains, thereby reducing hunger and enhancing food security for low-income households. Therefore, the observed outcomes may be the result of a combination of RSBY and these broader policy interventions, complicating causal inference. Although we controlled for state-level heterogeneity using state dummies, fully isolating the effect of RSBY requires more rigorous methods. Future studies should consider employing advanced econometric techniques, such as difference-in-differences (DiD) or instrumental variable (IV) approaches, to better disentangle the effects of RSBY/public health insurance policy from the broader socio-economic changes and policy interventions.

4.6 Limitations of the Study

The econometric approaches employed in the study, such as PSM and ESR, offer notable advantages in estimating impact evaluation. While the model controls selection bias arising from both observed and unobserved factors to quantify the impact evaluation of RSBY when employing cross-sectional data, they still face potential challenges. The experimental approach is regarded as the gold standard; nonetheless, acquiring such data is infrequent. Hence, the integration of panel data and methodologies such as DiD augments the precision of estimated values and fortifies the credibility of the findings.

Another limitation arises from potential biases in data collection and reporting. Households benefiting from multiple programmes might over-report improvements, while those less impacted by economic growth or policy measures may under-report benefits. Though we used state dummies to control such unobserved factors, future research should use more robust methodologies, such as randomised controlled trials, DiD or IV regression econometric techniques to better isolate RSBY’s effects amid these confounding factors.

5. Summary and Conclusion

The available quantitative evidence of the impact of health policy on reducing the likelihood of falling into poverty is scant. Using the PSM and ESR econometric approaches, we contribute empirical evidence for the impact of a health policy —RSBY—on reducing VtP in rural India. The findings indicate that households that have access to RSBY are better able to cope with the situation than households without it.

The empirical part of this article follows two steps. In the first step, the FGLS econometric approach has been applied to estimate household VtP using nationally representative data from rural India. The FGLS analysis identifies key factors that reduce VtP, including education, livestock ownership, landholding, social capital and employment in the service sector. Among the states analysed, Uttarakhand, Chhattisgarh, Odisha, Jharkhand and Maharashtra stood at the top of the VtP states, linked to economic backwardness and low adoption of public health insurance (RSBY). The second step investigates the impact of RSBY on VtP using PSM and ESR methods. The results consistently show that RSBY significantly reduces VtP, particularly in less developed states. In contrast, RSBY appears to have no noticeable impact in developed states.

Our findings lead to policy implications for VtP reduction in rural India, given that the government is planning to promote public health insurance to protect the low-income group from health shocks. States like Assam, Odisha and Rajasthan have less uptake of RSBY, suggesting the need to upgrade the RSBY system by improving the coverage, enrolment practices, awareness and provision of better service in these states. Identifying the right beneficiaries is a significant challenge even now; a significant proportion of identified beneficiaries is excluded from the list in almost every state (Boyanagari & Boyanagari, 2019; Chakrabarti & Shankar, 2015; Taneja & Taneja, 2016). From the findings, we recommend a forward-looking approach (VtP approach) to identify beneficiaries, as it correctly estimates the different categories of VtP.

Such a forward-looking approach requires a data-driven approach in which precise data regarding livelihood choices, assets, income and consumption are collated to identify vulnerable households. Finally, considering the partial impact of RSBY and limited study on VtP reduction, further research is needed to understand the welfare effect of health insurance policy in India in VtP reduction. We, therefore, recommend further research on the impact of health policy on VtP in India using panel data.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

Appendix

ESR Results for Vulnerability to Poverty

| Variable Name | Access to RSBY | Non-Access to RSBY | ||

| Coefficient | Std. Err. | Coefficient | Std. Err. | |

| Gender | –0.01 | 0.01 | –0.00 | 0.00 |

| Age of head | –0.00 | 0.00 | –0.00 | 0.00 |

| Schooling of head | –0.00 | 0.00 | –0.00 | 0.00 |

| Household size | 0.00* | 0.00 | –0.00 | 0.00 |

| Member in credit/saving group | –0.20* | 0.10 | –0.12** | 0.05 |

| Member in caste association | –0.08 | 0.05 | –0.03 | 0.02 |

| Attending public meeting | –0.08* | 0.05 | –0.02 | 0.02 |

| Members working as agriculture labour | –0.04* | 0.02 | –0.01 | 0.01 |

| Members working in agriculture | 0.00 | 0.00 | –0.00 | 0.00 |

| Members working as daily labour | –0.00 | 0.01 | –0.00 | 0.00 |

| Own land | 0.00 | 0.01 | 0.01 | 0.01 |

| Access to asset | 0.00 | 0.00 | 0.00 | 0.00 |

| Mills1 | –0.25 | 0.16 | ||

| Mills2 | –0.25** | 0.11 | ||

| Constant | 1.10*** | 0.29 | 0.61*** | 0.02 |

| Number of observations | 558 | 2,622 | ||

| R square | 0.03 | 0.04 | ||