Abstract

This article reports on a research effort that looked at the future of agricultural financing in sub-Saharan Africa (SSA) toward 2055. The real-time Delphi method was used to verify key megatrends that should define the future of agriculture and agricultural development in the region. The implications of these trends for agricultural financing, together with potential game-changing forces with regard to the future delivery of financial services to agricultural producers, were also prioritized. The real-time Delphi method was employed to check both the future importance and probability of occurrence of the identified trends and corresponding disruptive technologies, business models, innovations in value-chain financing, market configurations, and institutional innovations. In addition, the method was also used to investigate the future perspectives of experts and to identify any specific, promising technological areas, innovations, and business models. Key elements of a desired future for agricultural financing in SSA were also confirmed.

Keywords

Introduction

While there has been much research done on the facilitating role of agricultural financing within the global development agenda, the search for key sources and grand patterns of change within the sub-Saharan Africa (SSA) context is limited. The financial services sector currently finds itself in the middle of the greatest information and communication technology (ICT) revolution in human history (World Bank, 2016), with dramatic developments in digital, nano, and neuro technologies that have resulted in a decision environment, where change has become the norm (Adendorff, 2013; Inayatullah, 2013). This also has implications for decision-making in agricultural financing, which, according to Glenn et al. (2014: 60), is further challenged by the “acceleration, complexity, interdependency, and globalisation of change.” This article addresses this shortcoming by using the real-time Delphi method to validate and prioritize specific trends and potential game-changing forces with regard to the future delivery of financial services to agricultural producers in the region. In addition, the method was also used to aggregate expert knowledge and insight into the future of agricultural financing and to identify any specific, promising technological areas, innovations, and business models.

A structured process of identifying the game-changing trends and forces for agricultural financing

Sources of change in agricultural financing

Change originates from various sources. Change can come from how we see the world, from changing the laws that govern society (institutional change), and from the use of new technologies (Inayatullah, 2013). The latter fundamentally changes the way we do things and is supported by various authors as a major source of change toward the future (Dator, 2007; Inayatullah, 2013; World Bank, 2014). According to the 2014 Global Financial Development Report, it is evident that high transaction costs and geographical barriers are major constraints regarding the delivery of financial services to the poor (World Bank, 2014), with the development of innovative technologies that are expected to play a significant role in financially including them. A significant share of future technological innovations is, however, expected to be originated from outside the formal financial services sector (Sutton and Jenkins, 2007). Changes in agricultural financing can also be expected to manifest themselves at various levels, such as the enterprise level (individual, organization, and community), the immediate transactional environment (the environment with which we deal on a regular basis), and the global environment (Bishop and Strong, 2010).

Environmental scanning

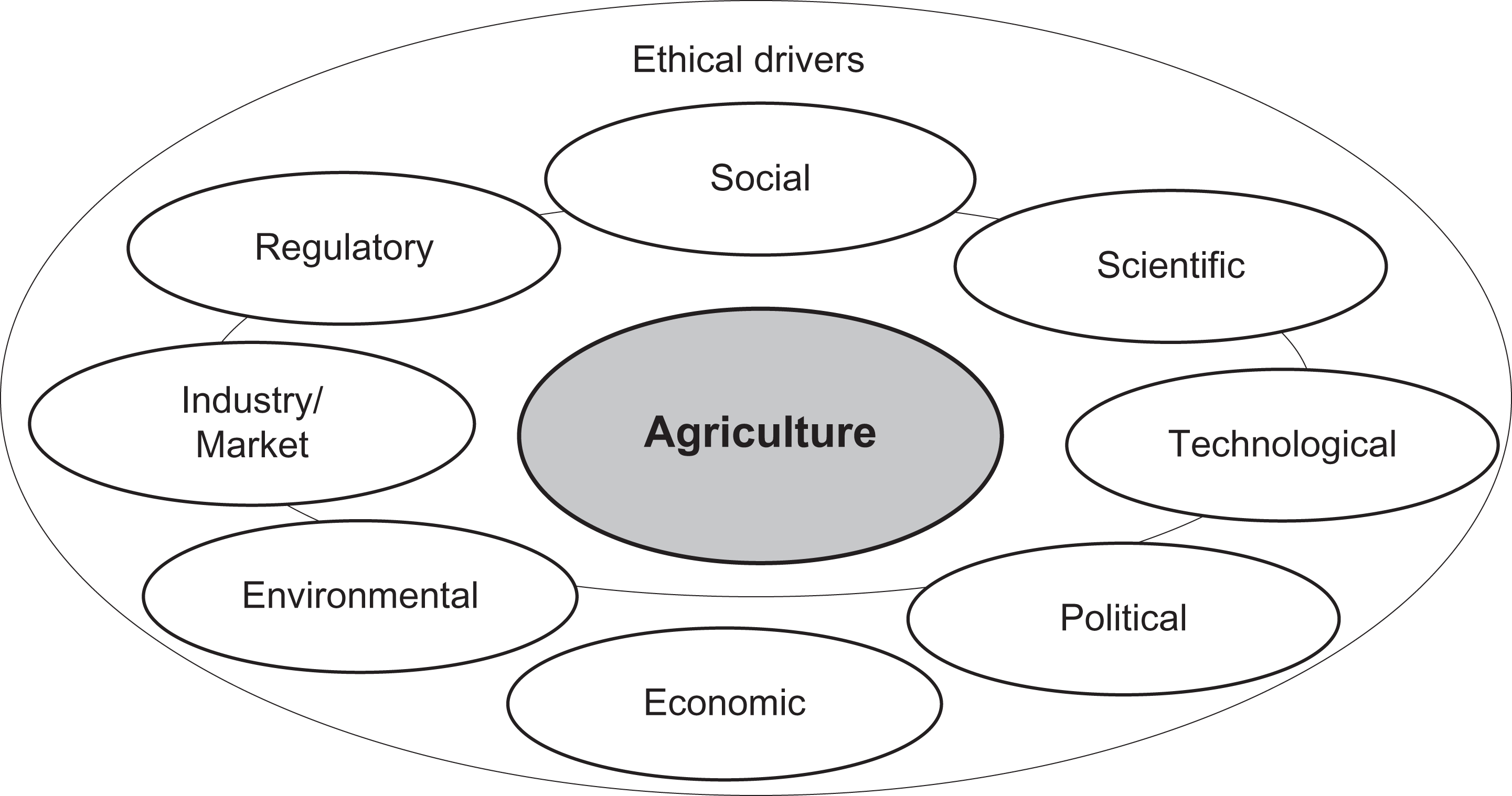

Albright (2004) proposes that industry-specific environments as well as the technology, regulatory, economic, social, and political environments be included in a comprehensive environmental scan. It is also proposed by Sutherland and Woodroof (2009) to include additional categories such as ethical drivers and the natural environment, which is necessary because of the unique nature of agricultural production systems.

In the search for grand patterns and sources of change in agricultural financing, the social, scientific, technological, political, economic, environmental, market, and regulatory environments were included in an in-depth environmental scan (Figure 1). As sustainable agricultural development heavily depends on inclusive and equitable economic growth, the values, processes, and systems generally associated with justice and fairness (ethical issues) were also included.

Scope of the environmental scan to explore the external environments affecting agriculture and its future financing needs. Source: Adapted from Albright (2004) and Sutherland and Woodroof (2009).

Emerging drivers of change for agricultural development in SSA toward 2055

From the environmental scan, various drivers of change for agricultural development in SSA toward 2055 emerged, and which were then grouped under specific themes (Table 1). The identification of these drivers of change was also guided by the definition of Kreibich et al. (2011: 10), who describe the drivers of change as “those forces, factors and uncertainties that are accessible to stakeholders and create or drive change within one’s business or institutional environment.” The authors also highlight that these drivers tend to be relevant and distinct for different types of stakeholders and which, according to Oberholster (2014), are especially relevant to agricultural financing and the increased awareness of the role of multiple stakeholders in the development of new and innovative agricultural financing solutions.

The key drivers of change for agricultural development in SSA toward 2055.

SSA: sub-Saharan Africa.

Source: Authors’ own construction based on the outcome of the environmental scan.

Emerging agricultural megatrends in SSA toward 2055

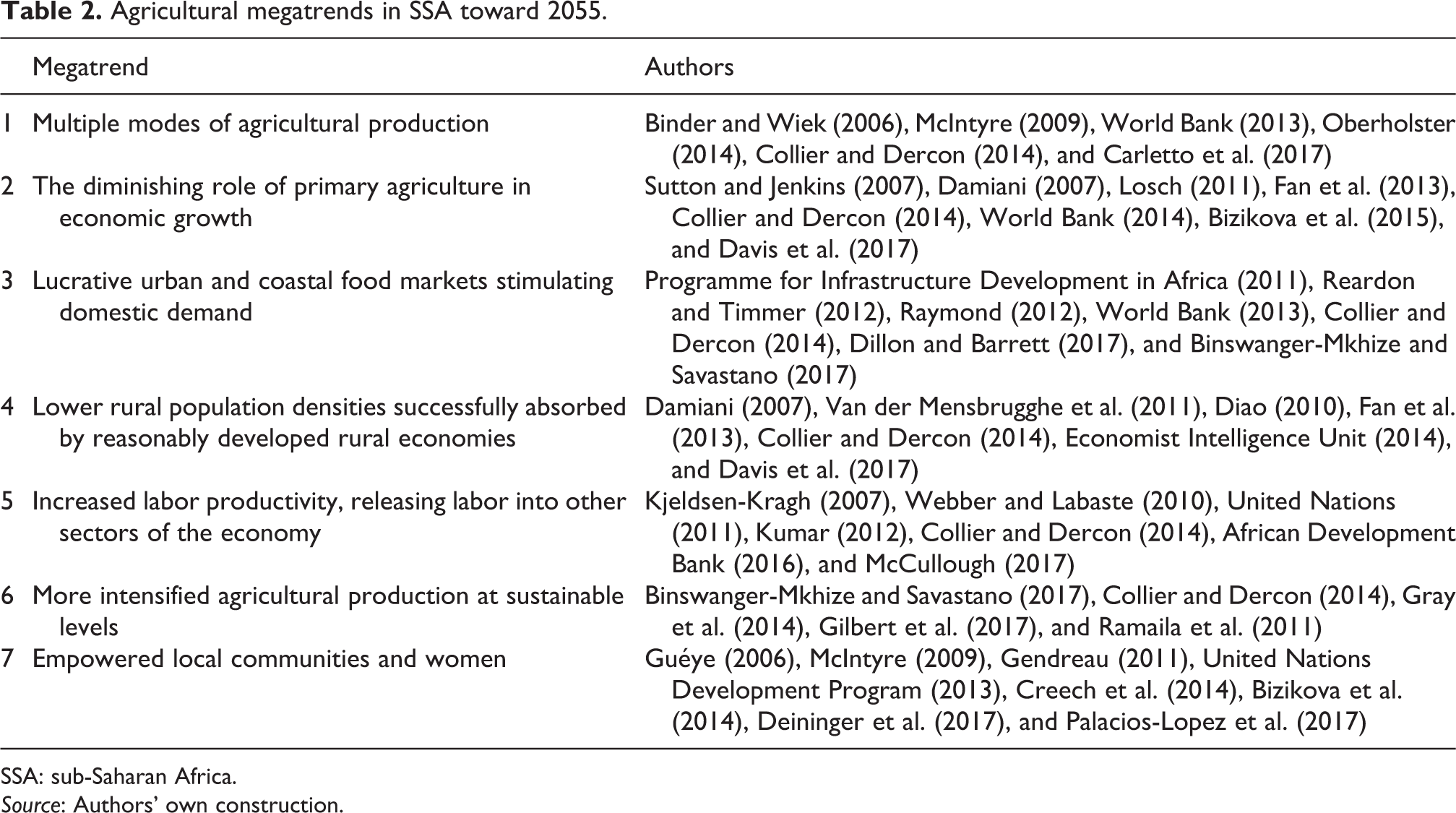

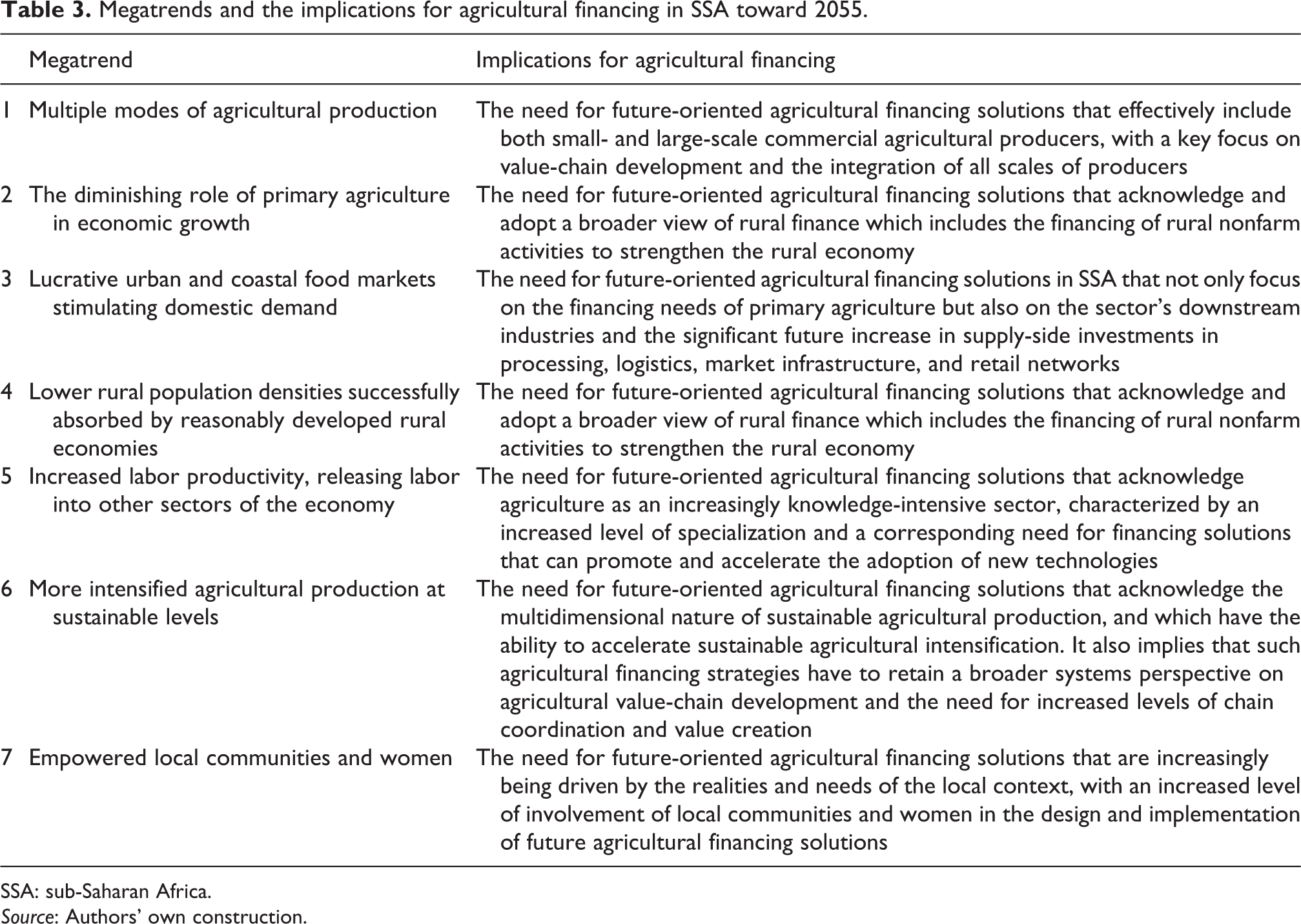

The various driving forces, factors, and uncertainties collectively contribute toward very distinct megatrends that are expected to significantly impact on the agricultural sector in SSA toward 2055 (Table 2). The formulation of these trends was guided by the description of John Naisbitt, who describes a megatrend as a long-term, transformational process with global reach, broad scope, and a fundamental and dramatic impact (Naisbitt, 1982). The process was further guided by the definition of Kreibich et al. (2011: 10), who define trends as “those change factors that arise from broadly generalisable change and innovation.” From this description, it is evident that a megatrend has different dimensions (time, reach, and impact), has a global reach, and creates broad parameters for shifts in attitudes, policies, and business focus over the long term. These megatrends also have significant implications for agricultural financing (Table 3) and they pose significant challenges for financial service providers.

Agricultural megatrends in SSA toward 2055.

SSA: sub-Saharan Africa.

Source: Authors’ own construction.

Megatrends and the implications for agricultural financing in SSA toward 2055.

SSA: sub-Saharan Africa.

Source: Authors’ own construction.

Key change areas for agricultural financing in SSA toward 2055

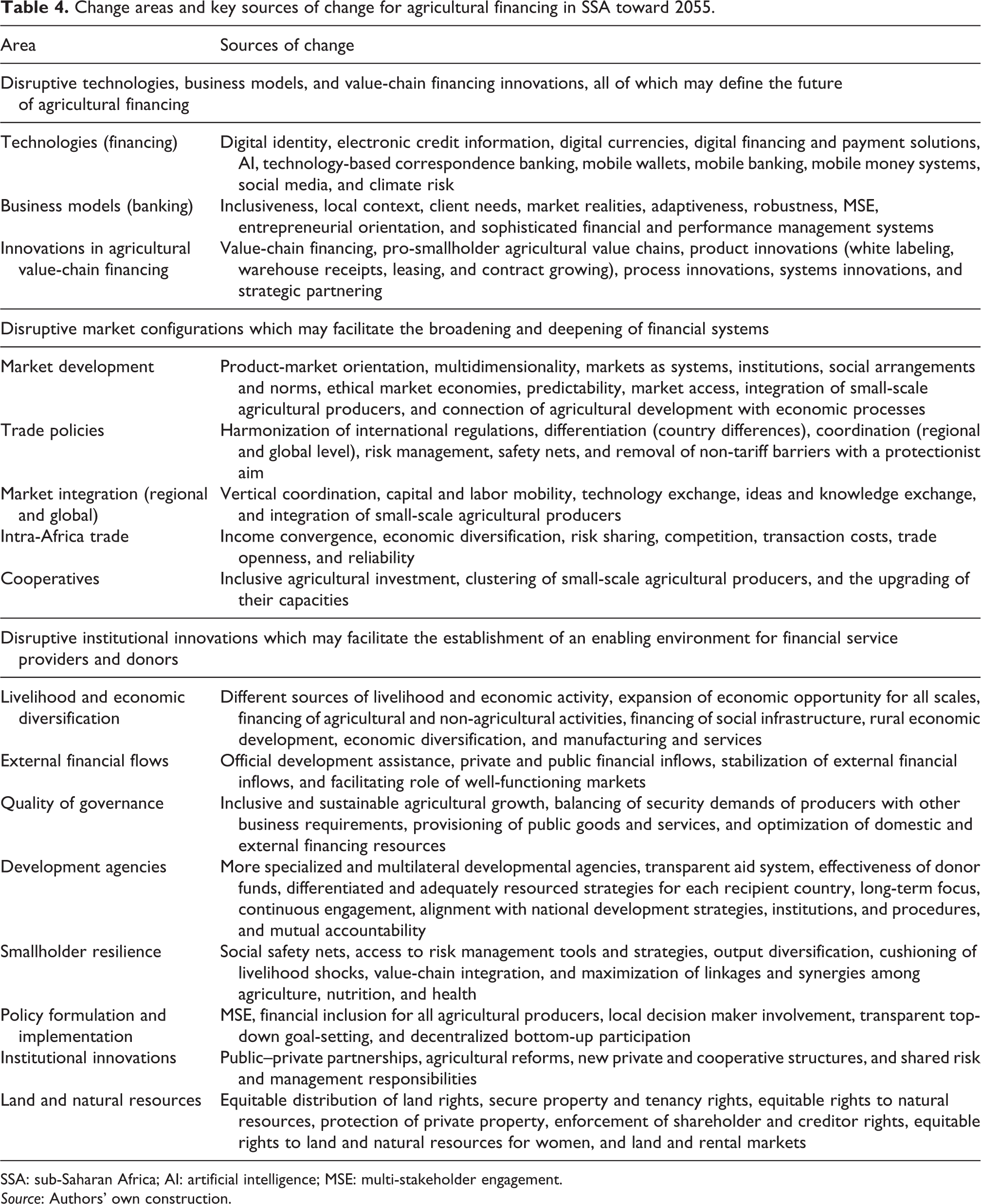

In the process of knowledge creation about the future of agricultural financing in SSA toward 2055, an emerging issue analysis was done on the identified key driving forces. This was done to identify possible disrupters or high-impact surprises that may reshape the delivery of financial services to the agricultural sector (Kreibich et al., 2011), which ultimately will assist in swifter responses to emerging challenges and opportunities (Inayatullah, 2013). From the analysis, five change areas emerged, namely, disruptive technologies, disruptive business models (banking), disruptive innovations in agricultural value-chain financing, disruptive market configurations, and disruptive institutional innovations.

Guided by these change areas, the key sources of change for agricultural financing in SSA toward 2055 were identified, as presented in Table 4. The presented summary gives a clear indication of the critical contribution of new entrepreneurial-oriented business models (banking), increased levels of financing innovations, digital technologies, ethical market economies, and institutional innovations that ensure equitable rights to land and natural resources for agricultural producers. This also confirms the multidimensionality of agricultural financing in SSA and the need for maintaining a global orientation to agricultural development and agricultural financing. It also implies that for the expected change to be effective, it needs to be manifested at the transactional level, the enterprise/community level, and the global level. A key aspect that also surfaced from the emerging issue analysis is that financing innovations, driven by new technologies and value-chain developments, have already become a growing trend.

Change areas and key sources of change for agricultural financing in SSA toward 2055.

SSA: sub-Saharan Africa; AI: artificial intelligence; MSE: multi-stakeholder engagement.

Source: Authors’ own construction.

Verifying and prioritizing the game-changing trends and forces for agricultural financing through the real-time Delphi method

Key aspects of the Delphi method

The Delphi method was introduced in the 1950s as a solution to address the inefficiencies generally associated with traditional group meetings (Green et al., 2007). The method is designed to explore the participating experts’ knowledge and opinions (Green et al., 2007) and ultimately aims to achieve consensus or a convergence of opinion on the specific real-world issue under investigation (Hsu and Sandford, 2008). The goal is also to enhance creative thinking (Diab and Abdel-Ghany, 2014) and to reach a group result that is greater than the individual contributions by each of the experts (Campos-Climent et al., 2012). It, therefore, has become a widely used and generally accepted method for collecting data from the participants within their domain of expertise.

The real-time Delphi as an alternative to the conventional Delphi method

The conventional Delphi method has certain weaknesses such as complicated facilitator tasks, lack of real-time presentation of the results, and difficulties in tracking progress over time (Gnatzy et al., 2011). The real-time Delphi method, on the other hand, has become the preferred method for forecasting and prediction, especially in research which seeks to develop an agreed-on or shared view of an emerging and more complex topic or issue (Campos-Climent et al., 2012; Diab and Abdel-Ghany, 2014; Schuckmann et al., 2012). Added benefits, from a process perspective, also include increased efficiencies (immediate participant feedback) and expert availability regardless of their physical location (Diab and Abdel-Ghany, 2014).

The research framework for the real-time Delphi study

The purpose of the study

In this research, the real-time Delphi study was to validate and prioritize the identified agricultural megatrends as well as certain disruptive technologies, business models, value-chain financing innovations, market configurations, and institutional innovations, all of which could define the future of agricultural financing in the region over the next 35 years. In addition, the study was also used to generate new ideas from the group of experts.

Number of rounds

The Delphi technique is usually repeated until a predefined stopping criterion is attained or until consensus has been achieved (Hsu and Sandford, 2008; Schuckmann et al., 2012) but is usually restricted to two or three rounds (Campos-Climent et al., 2012; Day and Bobeva, 2005). With the real-time Delphi study, however, there is only one round (Gordon, 2009). Although restricted to one round, it was decided to keep the real-time Delphi running for an extended period of 8 weeks. During this period, participants received regular reminder e-mails and were also encouraged to revisit the questionnaire and to provide qualitative feedback on the reasoning behind their judgments.

Participants and panel size

Individuals are considered eligible to participate in a Delphi study if they have related backgrounds and experiences with regard to the issue/s under investigation (Hsu and Sandford, 2008). Heterogeneity among the group of participating experts is also proposed (Rowe and Wright, 2011), as well as the inclusion of representatives from all the relevant stakeholder groups (Campos-Climent et al., 2012; Schuckmann et al., 2012). In this research, the selection of participants focused on industry experts in the field of agriculture, agricultural financing, and futures studies. In addition, executive managers and decision makers in the financial services sector, and who potentially may use the outcome of the research, were also included. A total of 57 experts were participated. This included a significant number of highly qualified experts from various countries (including SSA).

Anonymity of the participants

A key characteristic inherent to the real-time Delphi method is that the anonymity of the participants is maintained throughout the process (Gordon, 2009; Gnatzy et al., 2011). In addition, it also reduces the effects of dominant individuals and prevents group thinking (Campos-Climent et al., 2012). The online platform that was chosen for this research was the Global Futures System (GFS) of the ‘Millennium Project’, which provided full anonymity of the participants.

Structuring of the questionnaire

The final questionnaire consisted of 67 worded statements or items linked to the identified megatrends and potential disruptive technologies, businesses models, financing innovations, market configurations, and institutional innovations. The participants were requested to measure these megatrends (questions 1–7) against their potential (importance) to transform the agricultural sector in SSA toward 2055, as well as the probability of occurrence by 2055. The participants were also requested to measure the potential (importance) of the implied financing needs to facilitate the expected transformation.

Questions 8 to 67 correspond to the identified disruptive technologies, businesses models, agricultural value-chain financing innovations, market configurations, and institutional innovations, all of which may define the future of agricultural financing in SSA. The participants were requested to measure these developments against the potential (importance), in order to define the future of agricultural financing in SSA toward 2055, as well as its probability of occurrence by 2055.

A 10-point Likert-type interval scale, which is popular for measuring attitudes or judgments (Welman and Kruger, 2001; Zikmund, 2003), was used to allow the experts to provide a more precise evaluation of each megatrend and driving force. The participants were requested to indicate their judgment with regard to each statement, which ranged from 1 (least importance or a low probability of occurrence) to 10 (most importance or a high probability of occurrence). The GFS platform also provided participants with a comment space (qualitative assessments) next to each megatrend or driving force. This was especially useful in supporting the aim of the Delphi study to generate new ideas from the group of experts.

Evaluation of the real-time Delphi study

Credibility of the real-time Delphi study

Various requirements are proposed to guarantee the credibility of the real-time Delphi study. These include aspects such as the suitability of the method to address the issue under investigation, the choice of experts, the data management process, trustworthiness, and the level of expertise (Day and Bobeva, 2005; Van Vuuren, 2016). In order to strengthen the credibility of the real-time Delphi study, multiple participants were used. To address both components of credibility, namely, expertise and trustworthiness (Flanagin and Metzger, 2008), various industry experts, academics, and futurists were included. As a result, the participants in the real-time Delphi study represent industry experts with a long track record, highly educated people, as well as a significant number of individuals in senior and executive roles.

Relevance and plausibility

Different judgments and opinions can, however, be expected and which, according to Flanagin and Metzger (2008), can be attributed to the ability of each participant to comprehend the formulated megatrends and driving forces from his/her own worldview and the different contextual settings in which each individual functions. It is, therefore, suggested that the results of a real-time Delphi study also be examined for their relevance and plausibility, and which can be achieved through the inclusion of qualitative perspectives in the form of reason or comments (Gordon, 2009). This was complied by providing the participants with a comment space next to each megatrend or driving force.

Rationale for the inclusion of each statement in the questionnaire

Day and Bobeva (2005) suggest the provisioning of a detailed rationale of how the questionnaire was initially established and employed. In this research effort, the trends and driving forces were identified through an in-depth environmental scan which was guided by the scanning framework presented in Figure 1. The scan was also done as part of pillar one of the Six-Pillar approach of futures studies developed by Inayatullah (2013), and which aimed to provide insight into the multidimensional nature of agricultural development and agricultural financing. In addition, various futures studies methodologies, concepts, and techniques were integrated and applied throughout this research effort, and this provided a chain of evidence through the data-analysis stages.

Data analysis

According to Hsu and Sandford (2008), the measures of central tendency (means, median, and mode) and the level of dispersion (standard deviation and inter-quartile range) are the most frequently used statistical analysis in Delphi studies to present information concerning the collective judgments of the respondents. The median, as a measure of the degree of consensus among the participating experts (Campos-Climent et al., 2012; Hsu and Sandford, 2008), was used in this research study. Subsequently, a median Likert score was calculated for each megatrend and driving force in terms of its importance and probability of occurrence. A summary of the worded statements included in the questionnaire, together with the associated Likert scores, is available on request.

These quantitative judgments were also supported by the qualitative assessments that were provided in the comment space on the GFS platform. In total, 826 written comments or qualitative assessments of the megatrends and driving forces were provided. These written comments or qualitative assessments were also analyzed in terms of key arguments as to whether specific megatrends and driving forces are important, or not, for the future of agricultural financing in SSA. Similarly, the written comments were also evaluated in terms of the key factors influencing the probability of occurrence of each megatrend and driving force.

Key findings and implications for agricultural financing toward 2055

Agricultural megatrends toward 2055

The seven agricultural megatrends, together with the key change areas and driving forces within each megatrend, were confirmed by the output of the real-time Delphi study. These trends and factors have the potential to ultimately define agricultural development and the future of agricultural financing in the region. It not only indicates the need to depart from a too narrow view of small-scale agricultural production but also to reconstruct the assumptions about the way in which the delivery of financial services to the agricultural sector is constituted. Gaining a broader systems perspective will ultimately assist in the adoption of a broader view of rural finance, which will likely become a key element of future financing solutions that have the ability to address the constant tension between growth and the expected development role of agricultural.

Megatrend 1: Multiple modes of agricultural production

Toward 2055, agricultural development strategies in SSA will likely take into account the dominant perspectives and goals of sustainability at each scale of agricultural production. While acknowledging the need for sufficient scale in high-value commercial agriculture, it will ultimately open up new forms of commercialization for small-scale producers (high score of 8.0). Although progress with regard to their integration into agricultural value chains is expected to be slower, small-scale producers will increasingly be considered within the larger commercial context of agriculture (high score of 8.0). More inclusive financing solutions, together with an increased role for the larger commercial agricultural component, will speed up the process and allow small-scale producers to access credit through their value-chain linkages (high score of 9.0).

Megatrend 2: A continued facilitating role of primary agriculture in economic growth

Toward 2055, many sub-Saharan African economies will most likely transform from an agricultural base to manufacturing and services, with agricultural growth continuing to benefit from broader economic growth. The number of people engaged in primary agriculture is likely to be reduced, with the share of primary agriculture’s contribution to GDP also reducing (score of 8.0). As a result of the consolidation of smaller units, the number of primary commercial producers is expected to increase slightly, with a corresponding decrease in the number of semi-subsistence producers. It is also expected that, as agricultural producers seek value addition to remain competitive, the contribution of secondary agriculture and other downstream activities will increase. A need, therefore, exists for future financing solutions that focus on both the developing of the primary agricultural sector and the sector’s downstream industries such as manufacturing (score of 8.0).

Megatrend 3: Lucrative urban and coastal food markets stimulating domestic demand

Toward 2055, a massive increase in the urban and coastal population of SSA is likely to occur, which will open up new and lucrative urban food markets in the region. Urbanization will have a significant impact on the agricultural marketplace and the regional economy as a whole (high score of 8.0). Consequently, a significant increase in supply-side investments in processing, logistics, market infrastructure, retail networks, and seawater agriculture will be required. Infrastructure, including the sector’s downstream industries, will continue to be a key focus of future financing solutions (score of 8.0). Investments in rural infrastructure, education, and skills development will likely continue to be an aspect of the sustainable supply of agricultural produce.

Megatrend 4: Lower rural population densities successfully absorbed by reasonably developed rural economies

Toward 2055, a notable reduction in the size of the SSA population living in areas relatively far away from urban and coastal areas will most likely occur (high score of 8.0). Policy interventions will continue to focus on the strengthening of the rural economy and the diversification of household income through the creation of nonfarm employment opportunities. The significant need for rural infrastructure, including social infrastructure, will, however, continue to challenge the development of the rural economy (score of 7.0). These significantly higher levels of investment back into the rural areas will likely only happen if the private sector starts to become involved in the creation of nonfarm employment opportunities. Future-oriented agricultural financing solutions need to adopt a broader view of rural finance and will likely include the financing of rural nonfarm activities to strengthen the rural economy (score of 8.0).

Megatrend 5: Increased labor productivity, releasing labor into other sectors of the economy

Toward 2055, labor productivity in SSA will likely increase considerably with agriculture in many countries in the region in an advanced stage of development (score of 8.0). The sector will most likely enjoy the benefits of increased levels of specialization and improved technologies that boost labor productivity, and as a result, effectively raise the income of the poor. However, in some countries, political risk will likely continue to scare away much needed capital to facilitate the adoption of new technologies (lower score of 7.0). Although the readiness of the African culture to embrace this trend will remain a concern, education and training will continue to play a key role in the adoption of new and productivity enhancing technologies. Future agricultural financing solutions will likely acknowledge agriculture as an increasingly knowledge-intensive sector, characterized by an increased level of specialization and higher adoption rates of new technologies (score of 8.0).

Megatrend 6: More intensified agricultural production at sustainable levels

Toward 2055, a considerable increase in agricultural intensification will most likely occur. Agricultural intensification, driven by the continuous pressure on natural resources, will continue to transform the agricultural sector (high scores of 8.0 and 9.0.). The retention of a broader systems perspective on agricultural value-chain development, in which new technologies, land, capital, and the conservation of natural and environmental resources are effectively being used to produce plentiful and affordable food, will be a key contributing factor to increased sustainability levels. Agricultural financing solutions of the future will continue to acknowledge the multidimensional nature of sustainable agricultural production and will most likely focus on facilitating increased levels of chain coordination and value creation (high score of 9.0).

Megatrend 7: Empowered local communities and women

Toward 2055, the local context (country and community level) and the empowerment of local communities and women will probably be key contributing factors to increased levels of sustainability (high score of 8.0). Pressure, emanating from the global concern regarding equitable participation, will most likely drive this trend. Although slower progress is expected (lower score of 7.0), the more equitable distribution of power and the gains of increased agricultural growth will lead to social stability and significant human development progress. Although not the sole responsibility of the financial services sector, a need will arise for agricultural financing solutions that are increasingly being driven by the realities and needs of the local context. Increased levels of involvement of local communities and women in the design and implementation of future agricultural financing solutions will most likely occur (score of 8.0), with financing interventions increasingly being supported through the training of local community members.

Key change areas for agricultural financing in SSA toward 2055

Disruptive technologies

Technology will most likely continue to define the future of agricultural financing (high scores of 9.0 and 8.0). Technology has the ability to address the issues of high banking costs and to reduce lending risks. Although SSA is lagging behind in terms of economic development, the region is more ready for technological development and adoption than any of the other emerging economies. Innovation, and the need for increased security levels and lower costs, is likely to drive these developments which are expected to intensify in the future. Mobile banking and internet-based solutions are most likely to be the single biggest gateway to SSA and the rest of the world in terms of access to finance. This phenomenon will always evolve and will eventually become cheaper.

Disruptive business models (banking) and strategies

Toward 2055, the financial services sector in SSA will most likely be characterized by new business models that are inclusive of small-scale agricultural producers and which can adapt to different cultures, climates, and scales of production (score of 8.0). These models and strategies will increasingly be defined by client needs and market realities. Agricultural value-chain financing will most likely be successfully used as a financing framework that can facilitate this change, especially in its ability to mitigate credit risk and to facilitate the provisioning of financial services to the sector through different role players in the financing sphere.

Multi-stakeholder engagement approach

Future financing models and strategies in agricultural financing will most likely be characterized by higher levels of engagement between multiple stakeholders, and subsequently the development of strategic partnerships between bank and nonbank stakeholders (scores of 7.0 and 8.0). These partnerships will address critical skills shortages regarding previously unbanked customers and locations and will also serve as source of innovation in agricultural financing. Multi-stakeholder engagements will likely be facilitated by policy interventions focusing on the establishment of public–private partnerships and the co-sharing of risk throughout the agricultural value chain. Given the existence of too many platforms and a lack of transparency at government level, progress toward 2055 is expected to be slow (lower score of 6.0). Efforts to increase the level of participation will likely be an ongoing process that will continue well until 2055 and beyond, and which will require a relatively stable socio-political environment.

Entrepreneurial orientation

Toward 2055, SSA will be in need of creative and entrepreneurial financing models that are characterized by specificity (score of 8.0). These models will depart from traditional approaches and will likely be driven by entrepreneurs who use ICT to innovate both the channels and the instruments through which financial services are delivered to the agricultural sector. However, it will require a conducive environment where investors and financial services providers feel secure about their investment and there is clarity and stability from a policy and political perspective. Progress, therefore, is expected to be slower (lower score of 7.0).

Disruptive innovations in agricultural value-chain financing

Innovations in agricultural value-chain financing will likely continue to disrupt the delivery of financial services to the agricultural sector (high scores of 9.0 and 8.0). Product, process, and systems innovations in agricultural value-chain financing will increasingly be driven by ICT, which is expected to become more accessible and affordable. Agricultural value-chain financing is likely to be used as both a financing and development framework (score of 8.0), both of which are likely to facilitate the development of strategic partnerships between financial services institutions and leading agricultural value-chain actors in SSA. Advances in ICT will allow effective communication and exchange of information between strategic partners, and this is likely to facilitate the development of more comprehensive and holistic financing solutions such as insurance and risk-sharing solutions.

Disruptive market configurations

Market development

Toward 2055, more sophisticated and developed product markets in SSA will most likely complement the financial markets, and this will drive higher demand for credit and an opportunity to finance agricultural value chains (high score of 8.0). These market developments will also support socio-economic development in the region. As markets in the region are underdeveloped, these developments are likely to continue until 2055 and beyond. In the process, traditional markets are likely to become more efficient as they start to adopt more commercial market strategies.

Markets as intricate systems

Toward 2055, a significant portion of agricultural production will be market led, which will drive innovations in agricultural value-chain financing. The wider market environment in SSA will most likely be developed into an intricate network or system of institutions and social arrangements, and that will link agricultural development with economic processes (high score of 8.0). This broadening and deepening of the financial system in the region, accompanied by a strong ethical market economy, are likely to allow more nontraditional financial services providers to enter the agricultural market. Given the persistently high levels of corruption, inequality, and unstable governments, progress will most likely be slow (lower scores of 6.0 and 6.5).

Trade policies

Social changes and the global concern regarding equitable participation will continue to challenge current market realities. Toward 2055, significant progress will be evident regarding the removal of non-tariff barriers with a protectionist aim. Intra-regional and multilateral trade agreements will increasingly focus on the preservation of rules and standards that are necessary to protect public health within the region. The trade policy environment will most likely have a stronger development focus, with an increased focus on the provisioning of risk management services and safety nets to vulnerable, rural agricultural producers and households (high score of 8.0). Given the influence of larger, dominant market players, persistently high levels of corruption, and the ineffectiveness and unwillingness of governments in the region, the removal of trade barriers with a protectionist aim is most likely to be very slow (low score of 5.0).

Market integration and intra-Africa trade

Toward 2055, SSA will most likely be transformed into a powerful trading block within the global market. Higher levels of market integration, driven by the anticipated increase in the global demand for food and advances in ICT, are likely to facilitate the integration of financial systems and ultimately broaden and deepen them (high score of 8.0). Increased levels of intra-Africa trade are also likely to open up a trading platform for the rural producers and ultimately stimulate agricultural production, quality of produce, and increased levels of efficiencies (high scores of 8.0 and 9.0). Access to new sustainable markets, with correspondingly higher levels of relative competitiveness, is likely to reduce lending risk, and that will open up agricultural financing possibilities. The pace and effectiveness of these market developments will most likely be influenced by factors such as advances in ICT, the removal of trade barriers, cross border agreements, and the development of transport systems and ease of travel (e.g. visas and checkpoints). Given the lack of political and economic leadership, corruption, regional inequality, smallholder vulnerability, as well as country-specific rules and regulations, progress will most likely be slow (lower score of 6).

The future role of cooperatives

Toward 2055, cooperatives and cooperative structures will most likely continue to be used as an effective development tool (high score of 8.0). As a business model, they have the ability to address capacity issues, skills shortages, aggregate small volumes, and will ultimately be likely to increase the bargaining power of small-scale producers. They are also likely to be used as a mechanism to access credit and to assist in the creation of more sophisticated and reliable markets for investors in the region. The role of cooperatives and cooperative structures is expected to continue (scores of 7.0 and 7.5) and will be evident, especially during the early stages of economic development in economies heavily dependent on agriculture.

Disruptive institutional innovations

Livelihood and economic diversification

As a whole, the region is most likely to continue to be agrarian centered and will need a policy environment that strategically supports both agricultural and non-agricultural activities. Transformational policies which acknowledge different sources of livelihood and economic activity will continue to play an important role in this regard (high score of 8.0). Policy interventions, aiming at the expansion of economic opportunity and the financing of non-agriculture activities, will likely continue to promote rural economic development and, to a degree, counter the rural impact of urbanization. Attempts to economically empower the individual will likely continue to define the future of agricultural financing (scores of 7.0 and 8.0), but transformation will be slow (score of 6.5). Success is likely to be conditional on the redefinition of the key roles and responsibilities of agricultural value-chain actors and, subsequently, the successful integration of small-scale producers into these chains.

External financial flows

Stable external financial flows into SSA (private and public) are most likely to continue to be a key source of financing for the agricultural sector (high score of 8.0). The sustainability of these inflows will likely depend on the effective utilization of the region’s own financial resource base, with development assistance being used in a supporting/supplementary way. Governments will continue to play an important role, but interference in agricultural markets may impact negatively on the attraction and effective use of development assistance (score of 6.0). The stability of these inflows will likely depend on policy interventions that effectively address key issues such as the effective functioning of markets, institutional capacity, corruption, lack of transparency, and the mismanagement of donor funds.

Quality of governance

Toward 2055, quality of governance will be required to ensure that agricultural growth that stems from external financial inflows is inclusive and more sustainable (high score of 9.0). The sustainability of agricultural development and financing strategies will likely depend on strong political leadership that demonstrates the ability to convince other countries, investors, and donors to provide expertise and to invest in the region. Given the persistence of economic instability and political insecurity in a number of SSA countries, and which discourage investors and donors, progress is expected to be slower (lower scores of 6.0 and 7.0). Faster progress is likely to be conditional on proper governance, focusing on the effective delivery of goods and services.

Aid systems/development agencies

Agriculture, as a specialized sector, will require a certain degree of specialization regarding development strategies and their associated aid systems. Toward 2055, specialization, and subsequently the development of a differentiated, adequately resourced strategy for each recipient country, will most likely become a key factor in increasing the level of financial inclusions in the agricultural sector (high score of 8.0). The nature of aid is likely to change a more integrated approach which will require increased transparency, a more holistic approach to economic development, and higher levels of coordination between multiple stakeholders. However, the restoration of trust will most likely become conditional (lower score of 6.0), with SSA countries that need to prove that they can be reliable development partners. The development of quality institutions and governance, supported by competent management and strong political leadership, will likely be a first step in this regard.

Smallholder resilience

Policy support for the integration of small-scale producers into agricultural value chains, together with the provisioning of social safety nets, will most likely become key facilitating factors regarding higher levels of financial inclusion in agriculture (high score of 8.0). Small-scale producers will remain an essential part of the agricultural system in SSA and need to be integrated to ensure their sustainability and continued contribution toward development and food security. Sustainable momentum is likely to be conditional on policy interventions that promote more inclusive and equitable agricultural growth. Although slower progress is expected (lower score of 7.0), these policy developments are likely to continue to define the future of agricultural financing.

Policy formulation and implementation

Toward 2055, multiple stakeholders will most likely become involved in policy formulation and implementation (high score of 8.0). Such levels of engagement will likely be a combination of both top-down and bottom-up approaches and will provide multiple perspectives on the future of agricultural financing. Given a better understanding of the local community and market dynamics, it will ultimately assist in higher buy-in levels and more effective implementation. The accommodation of all relevant stakeholders, together with the generally accepted challenges of policy implementation in an economically and socially dysfunctional environment, will mean that progress will most likely be slow (lower score of 6).

Institutional innovations

Institutional innovations such as public–private partnerships, which have the ability to stimulate creative initiatives through entrepreneurial thinking (private) and social responsibilities (public), will most likely become a key success factor regarding higher levels of financial inclusion in agriculture (high score of 8.0). However, the different agendas and objectives of different stakeholders are likely to slowdown progress (lower scores of 6.0 and 7.0). Profit disparity, where private sector parties mitigate high levels of risks by very high profit margins, will likely be a key policy focus area. The ability of these innovations to effectively redefine the individual as an answer to an autocratic system will most likely have significant implications for agricultural development.

Equitable rights to land and natural resources

Tenure insecurity is a socio-political condition engineered intentionally by policies and it is most likely to be remediated by policies. Toward 2055, land and natural resource policies will, therefore, most likely become critically important for higher levels of financial inclusion in agriculture (high score of 8.0). Land and other private rights will become fundamental in increasing the productivity of small-scale agricultural producers and in providing an incentive for ecosystem stewardship. Private ownership is also likely to secure a fundable model for small-scale agricultural producers. The level of complexity, and the occasional use of agricultural land as a political tool, will have a negative impact on effective policy implementation. Therefore, progress will most likely be slower (low score of 6.0).

A desired future confirmed for agricultural financing in SSA

The desired future for agricultural financing in SSA, shaped by the identified trends and driving forces, is also confirmed by the output of the real-time Delphi study. The desired future is set against a transformed financial services sector, which truly extends their focus beyond large-scale commercial agricultural. The desired future is characterized by the widespread use of financial intermediaries in the agricultural sector. Technology-driven banking correspondence models are successfully being adopted and are effectively being supported by secure and innovative digital payment solutions, which significantly reduce banking costs.

Simultaneously, commercial banks will be likely to have successfully adopted agricultural value-chain financing as both a financing and development framework. Strategic partnerships between commercial banks and leading agricultural value-chain actors will commonly occur, and this allows banks to leverage from the existing financial and product–market relationships between these actors and agricultural producers in the region. Digital and mobile technologies are likely to be effectively used to innovate both the channels and the instruments through which financial services are delivered to the agricultural sector. Access to credit will further be supported by transformational innovations, such as digital identities, electronic credit information, and automated credit-scoring solutions in which machine learning or artificial intelligence is playing a key role.

Conclusion

The outcome of the real-time Delphi study confirms the identified agricultural megatrends and the key role of agricultural financing for these trends to manifest themselves. The judgments and opinions of the participating experts give a clear indication of the critical contribution of new and innovative technologies, new entrepreneurial business models in banking, increased levels of innovation in agricultural value-chain financing, ethical market economies, and institutional innovations that ensure equitable rights to land and natural resources. A key outcome is the expected high impact of ICT and agricultural value-chain financing to promote financial inclusion in the agricultural sector, with consistently high scores of 8.0 and 9.0 (importance and probability of occurrence). It also confirms the multidimensionality of agricultural financing in SSA and the need for maintaining a global orientation toward agricultural development and agricultural financing. The need for an increased focus on agricultural value-chain development and value creation is also confirmed.

The process of verification and prioritization provides financial services providers with valuable insights into the future of agricultural financing in the region, which, ultimately, can assist them in effectively dealing with the future conditions of uncertainty. The methodical exploration of what the future of agricultural financing in SSA might also provide them with valuable information on previously unbanked customers and locations and the factors influencing their financing needs. Ultimately, it is expected to inform on more appropriate business models and strategies to increase banking reach in the region.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.