Abstract

This article assesses the relationships between race, gender, and parental college savings. Some prior studies have investigated race differences in parental college savings, yet none have taken an intersectional approach, and most of these studies were conducted with cohorts of students who predate key demographic changes among U.S. college goers (e.g., the reversal of the gender gap in college completion). Drawing on theories of parental investment and data from the High School Longitudinal Study of 2009 (HSLS:09), we show that both race and gender are associated with whether parents save for college, as well as how much they save. Both black boys and black girls experience savings disadvantages relative to their white peers. However, black girls experience particularly striking disparities: Black girls with the strongest academic credentials receive savings equivalent to black girls with the weakest academic credentials. Results suggest this is due, at least in part, to the fact that high-achieving black girls tend to come from families that are much less well-off than high achievers in other race-gender groups. As a result, parents of black girls frequently rely on funding sources other than their own earnings or savings to pay for their children’s college. These funding sources include private loans that may pose financial challenges for black girls and their families across generations, thus deepening inequalities along the lines of gender, race, and class. These findings demonstrate the power of taking an intersectional approach to the study of higher education in general and college funding in particular.

Paying for college is harder than it used to be. As tuition and fees have increased at universities across the country, students and their parents have made greater sacrifices to pay for higher education (Dwyer 2018; Dwyer, McCloud, and Hodson 2012; Houle 2014a, 2014b; Houle and Warner 2017). As of 2018, Americans have amassed $1.5 trillion in student loans, surpassing credit cards and auto loans to become the second-highest debt category, behind only mortgages (Federal Reserve Bank of New York 2018). Although rising college costs have affected all college students, data suggest students of color—and especially black students—are disproportionately affected. Compared to their white peers, black students have higher debt balances, have higher interest rates, and are more likely to default on their loans (Houle and Addo 2019; Jackson and Reynolds 2013; Scott-Clayton and Li 2016).

Social scientists have investigated many causes of black-white differences in college funding and outcomes, such as race differences in the type and quality of postsecondary institutions attended (Carnevale and Strohl 2013; Iloh and Toldson 2013). In this article, we assess one factor that has received comparatively less attention, especially since the beginning of the student debt crisis: parental college savings. In many ways, parental college savings is a product of historical and contemporary racial disadvantages that have already played a role in shaping families’ finances by the time their children begin to think about college. Parents’ ability to save for their children’s college education is a product of many factors, including not only income but also wealth, which differs substantially by race and compounds across generations (Addo, Houle, and Simon 2016; Darity et al. 2018; Herring and Henderson 2016).

Aside from race, gender is a key factor that may shape parental college savings. Girls have better academic performance than boys throughout the K–12 years, and women are more likely than men to earn bachelor’s degrees (Buchmann and DiPrete 2006). White women’s rates of bachelor’s degree completion surpassed white men’s beginning with cohorts born after 1960, and black women have outpaced black men in this regard since as early as the 1930 birth cohorts (DiPrete and Buchmann 2013). At the same time, theories of parental investment suggest parents might invest more resources in boys’ education, given that social and economic opportunity structures continue to advantage men (Raley and Bianchi 2006). This evidence suggests parental college savings is likely to vary by gender, whether due to parents’ beliefs about their children’s abilities or broader attitudes toward gender socialization.

In this article, we take a quantitative, intersectional approach to the study of parental college savings. Drawing on the perspective that race and gender have multiplicative effects on numerous dimensions of life chances (Collins 1990; Crenshaw 1989, 1991; McCall 2005; Wingfield 2009), we contend that both race and gender are likely to affect whether parents save for their children’s college education, as well as how much they save. We use theories of parental investment to make this argument, as well as empirical findings that point to persistent race and gender differences in how students pay for college. To investigate these dynamics, we use data from the High School Longitudinal Study of 2009 (HSLS:09), a survey conducted by the National Center for Education Statistics (NCES). The HSLS is the most recent nationally representative survey with rich data on parental college savings and precollege social and academic experiences, making it an ideal dataset for our study. In addition to the main analyses that assess parental college savings among 11th graders, we also examine the other funding sources parents anticipate using to pay for college. Depending on whether these funding sources must be repaid—not to mention their interest rates, repayment schedules, and who is responsible for repaying them—these anticipated funding sources can have long-term implications for financial well-being across race-gender groups. In total, our findings reinforce the idea that college funding is a mechanism through which higher education reproduces inequality. We show that these inequalities emerge at the nexus of race, gender, and precollege achievement—a combination of factors that is underexamined in the literature on funding for higher education.

Race, Gender, and Parental College Savings

Although research on college funding remains nascent, several recent studies have considered how students pay for college (Dwyer et al. 2012; Hamilton 2013; Quadlin 2017; Quadlin and Rudel 2015) and how these funding arrangements differ by race (McCabe and Jackson 2016). Most of this research focuses on student loan debt—and rightly so, given that racial differences in student loans are large and have persistent effects throughout the life course. Black college students accrue substantially more educational debt than do white students (Addo et al. 2016). Although these gaps in student loans emerge during college, they continue to grow after students leave, as black students face more barriers in making loan payments (e.g., discrimination in the labor market, which contributes to lesser returns to educational attainment), and their loans carry higher interest rates than those of their white peers (Scott-Clayton and Li 2016). We therefore focus on black-white comparisons in this article, as have many other scholars, but other racial groups (such as Latinx, Asian, and Native American youth) warrant investigation in future work.

Less research has focused on gender differences in borrowing, but recent estimates indicate that women graduate with more debt than men. The average woman graduates with about $21,000 in student loans, versus about $19,500 for men (Miller 2019). There is also evidence that men and women respond to debt differently. Both men and women have diminished chances of graduating when they have high debt balances, but men tend to drop out at lower debt levels than women, suggesting women have a higher tolerance for indebtedness (Dwyer, Hodson, and McCloud 2013).

Despite this growing emphasis on student loan debt in the social science literature, relatively little research has considered the issue of parental college savings (but see Turley and Desmond 2011). Even less research has focused on race and gender differences in parental college savings—and we are aware of no research that takes an intersectional approach to this topic. In some ways, this scholarly focus on debt rather than parental savings is justified, given that disparities in parental savings frequently morph into disparities in student loan debt as students seek to cover their unmet financial need (Rauscher 2016). Yet, saving for college is a distinct social process shaped not only by parents’ ability to pay for college (itself a product of intergenerational processes influenced by structural racial inequality) but also by parents’ forecasting of their children’s academic potential for college (discussed in detail in the next section). Research on parental college savings thus provides additional insight into family decision making and historical and contemporary racial inequality that is related to, but distinct from, the issue of student loans.

A handful of studies have considered racial differences in parental college savings using data on earlier cohorts of students. Steelman and Powell (1993) use data from High School and Beyond and the National Education Longitudinal Study of 1988 (NELS:88) to show that black parents invest just as much (if not more) in college than white parents once background characteristics are controlled for. Other scholars have similarly used NELS:88 data to show that black-white differences in social class account for racial gaps in parental savings and, in turn, college attendance (Charles, Roscigno, and Torres 2007). These studies provide key insight into race and parental college savings, but the data used in these analyses are now more than 30 years old. Many demographic changes have occurred in the intervening period—including, but not limited to, the reversal of the gender gap in college completion among whites (which was only beginning to emerge in the 1980s) and black women continuing to grow their advantage in college completion over black men (DiPrete and Buchmann 2013). This warrants an updated investigation into parental college savings that emphasizes both race and gender.

Assessing Economic and Academic Factors

Drawing on theories of parental investment and prior empirical findings, we contend that two main sets of factors are responsible for shaping patterns of parental college savings in the United States. The first is economic and family factors, which encompass opportunities and constraints that affect parents’ ability to save for their children’s college education. The second is academic factors, which reflect a student’s academic preparation for college. Parents may use academic indicators to make an educated guess about their children’s likelihood of attending college, which, in turn, may affect parents’ tendency to save. Next, we outline these two sets of factors and discuss how they may vary by both race and gender (i.e., in an intersectional manner) in shaping parental savings for college.

Economic/Family Factors and Parental College Savings

Generally speaking, parents in higher socioeconomic status (SES) groups provide children with more college funding than do parents in lower-SES groups. Of course, there are some exceptions to this rule, such as affluent parents who would prefer their children work their way through college to have some “skin in the game” (Hamilton 2016). However, research typically finds a positive relationship between parental SES and their spending on children’s college education (Hamilton 2013; Quadlin 2017; Turley and Desmond 2011). Studies also suggest that family configuration plays a role when it comes to children’s receipt of economic resources for college. According to resource dilution theories of parental investment, as the number of children in a family increases, the amount of parental investment that can be provided to any one child decreases (Downey 1995; Gibbs, Workman, and Downey 2016; Steelman et al. 2002). Higher education is especially prone to resource dilution because it is so challenging for parents to pay for multiple children (or even one child, for that matter) to attend college. Gender composition of sibship also matters: Some research shows that children’s resources for college are most diluted when they have multiple brothers (but not sisters), presumably because parents are more motivated to provide college funding for sons than for daughters (Powell and Steelman 1989; but see Quadlin 2019).

Although both race and gender are linked to constraints on parental college savings, race typically is considered a more salient factor because race is strongly linked with economic status. A long line of research shows black families are disadvantaged relative to white families across multiple economic indicators, including income, wealth, and educational attainment. These disparities are a reflection of historical and contemporary processes of racism and discrimination in the labor market, housing, access to credit, and other linked institutions (Wilson 1978, 2011, 2012). There is also evidence to suggest that racial differences in parental college savings vary across the economic spectrum. For example, research shows that black-white differences in student loan debt are largest at the highest levels of parental wealth, in part because high-wealth white families have exponentially more assets than their black counterparts (Addo et al. 2016). This pattern implies we would also observe a racial gap in parental college savings among the most advantaged families.

By comparison, less research has focused on race differences in parental college savings among the least-advantaged families. In contrast to trends among the most affluent, we might expect black parents to have an advantage here, in light of prior research showing that black parents save more than white parents once background characteristics are controlled for (Steelman and Powell 1993). It may be that the black advantage in parental college savings (net of controls) found in previous work is driven by relatively high savings in lower-income black families. In this article, we further tease apart differences in parental college savings by considering how savings varies across the economic spectrum—thus showing how race and gender are associated with college savings for those with many and also few economic resources.

Academic Factors and Parental College Savings

Aside from economic factors as predictors of parental college savings, students’ academic qualifications also play a key role. Here it is important to acknowledge that students’ academic achievement is highly correlated with their family’s economic circumstances, such that students from higher-SES families generally have much stronger academic credentials than their lower-SES peers (see, e.g., Reardon 2011)—although the relationship between parental SES and student outcomes is stronger for whites than for blacks (Bumpus, Umeh, and Harris 2020). Notwithstanding these relationships, academic factors are fundamental to the study of parental college savings because parents use academic information to project their children’s chances of college success—a process that generations of social scientists have considered (for a review, see Steelman and Powell 1991; Quadlin 2015). Scholars in the human capital tradition have long posited that high achievers receive more parental resources than low achievers because they are more likely to succeed in college and, eventually, the workforce (Becker 1964). In this theoretical perspective, parents may see high-achieving children as “safe bets” who are likely to yield a high return on investment. The status attainment model similarly predicts a positive relationship between children’s academic performance and parental investment (Sewell, Haller, and Portes 1969). It follows, then, that parents may save additional resources for children with strong academic credentials, over and above what their economic resources would normally dictate.

In particular, recent research highlights the relationship between gender and academics. Throughout the K–12 years, girls and women generally have stronger academic performance than boys and men (Buchmann and DiPrete 2006). If parents are motivated to reinforce strong academic performance when setting aside resources for college, then it follows that girls should have more savings than boys, on average. Yet, social and economic opportunity structures continue to advantage men in the United States (Ridgeway 2011). This dynamic could encourage parents to designate additional resources for boys, if parents are motivated to support children who will experience fewer obstacles in adulthood (Raley and Bianchi 2006).

We expect the intersection of race and gender is particularly important in the case of academics. As noted earlier, research shows that gender gaps in college completion are outsized among black students. Of the bachelor’s degrees conferred to black students in 2016–17, over 64 percent were conferred to women (versus 57 percent among whites; Snyder, de Brey, and Dillow 2019; also see DiPrete and Buchmann 2013; McDaniel et al. 2011). Despite having fewer economic resources, on average, than their white peers, black women achieve relatively high rates of college completion, and thus they outperform what would normally be projected for students with their economic profiles. This may put black girls in a challenging situation, however, when it comes to parental college savings. Even if parents of black girls are adjusting their college savings upward to be in line with their daughters’ academic performance, as human capital theories would predict, these adjustments may eventually hit the ceiling of black parents’ economic circumstances. As a result, black girls—and especially high-achieving black girls—would disproportionately bear the brunt of any average racial differences in parental college savings. If this is the case, then black girls may face acute economic challenges in funding higher education that can potentially have broader consequences, such as suppressing their college completion rate and deepening racial inequalities in debt and assets.

The Current Study

To reiterate, this article assesses race and gender differences in parental college savings. To account for the fact that students have different chances of attending college—and parents theoretically calibrate their savings to reflect those differential chances—our models incorporate students’ chances of attending college as determined by both economic/family factors and academic factors. In addition to the main analyses that examine parental college savings in students’ 11th-grade year, we also investigate the additional funding sources parents anticipate using to pay for their children’s college. These analyses investigate race-gender differences in students’ chances of using a range of financial instruments, including liquid earnings and savings, grants and scholarships, and government-backed and private loans (issued to either the student or the parent). We devote less space to these analyses in this literature review because we focus mostly on the issue of parental college savings. However, depending on whether these other funding sources must be repaid—not to mention who is responsible for repaying them—these anticipated funding sources can have lasting implications for economic well-being across race-gender groups.

Data and Methods

Data

We use data from HSLS, the most recent nationally representative survey with information on parental college savings and precollege social and academic experiences (N = 23,503). HSLS is a survey sponsored by the National Center for Education Statistics (NCES) that focuses on students’ pathways through high school and postsecondary education. 1 Respondents were first recruited in fall 2009, and follow-up interviews were conducted in 2012, 2013 (an abbreviated survey on students’ college plans), and 2016. An additional follow-up is planned for 2025. Most of the variables we use come from the first student and parent follow-up surveys, conducted in 2012, when most students were juniors in high school. HSLS is unique among NCES surveys because of its focus on students’ interest and experiences in STEM (i.e., science, technology, engineering, and mathematics). Although our primary interest is not STEM, the survey’s STEM focus has implications for some of the items we used (e.g., NCES conducted a math assessment but not assessments for other subjects that have historically been included in NCES surveys). The main limitation of the HSLS dataset for our purposes is that it does not contain information on parental wealth (aside from wealth that parents specifically report as college savings). We discuss this limitation more throughout.

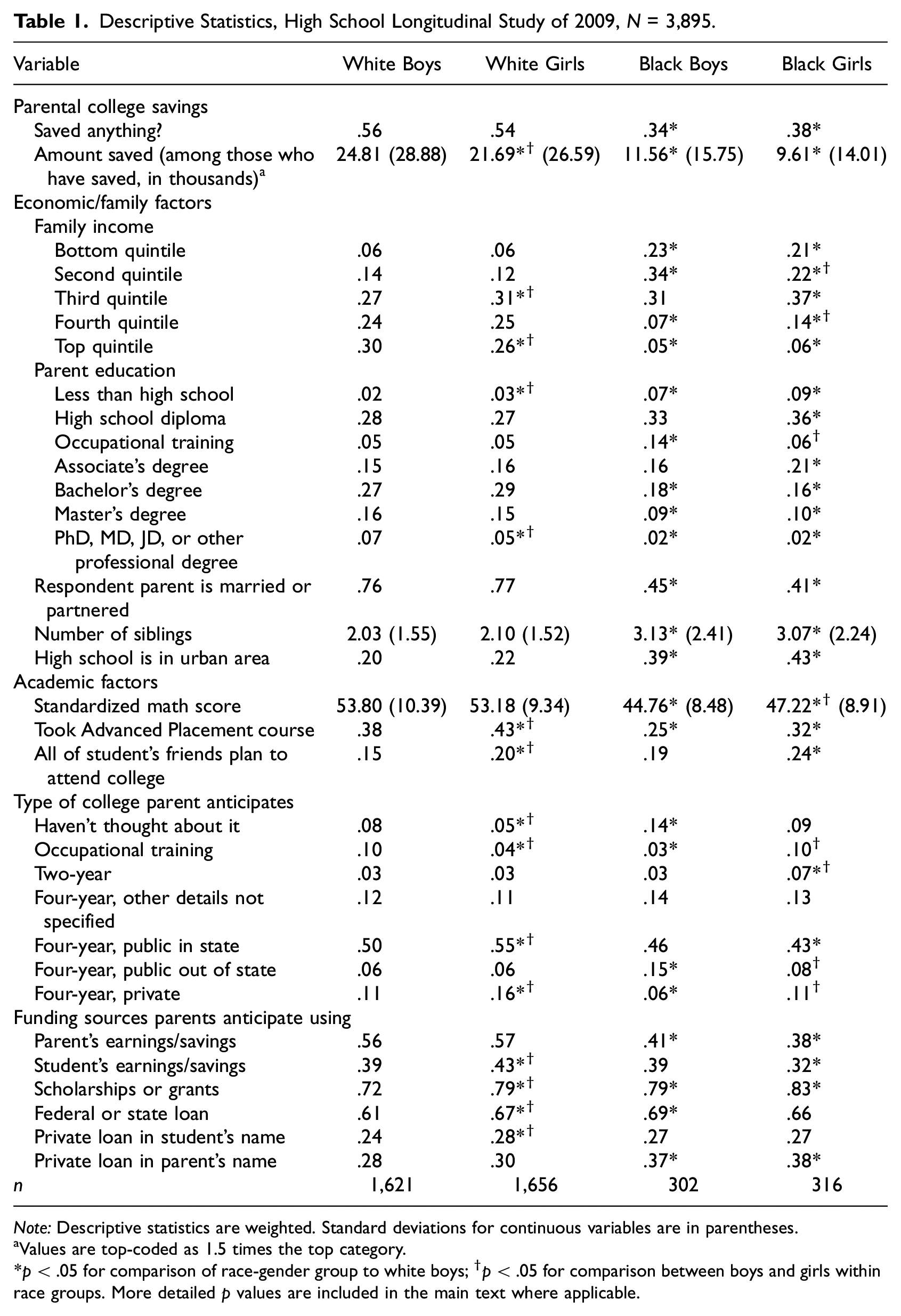

The sample is limited to students who identify as either black or white, given that most research on race, debt, and assets addresses the black-white divide, and we focus on squaring these findings with research on gender differences in college completion among black and white students. 2 The sample is smaller than that for other studies using HSLS data because the item about parental college savings was administered to a random sample of respondent parents (n = 7,426). Once we account for this element of the survey design (and participation in a future round of HSLS, as discussed later), item nonresponse in HSLS is low, and we lose only 418 cases (less than 2 percent of the total) to missing data on the covariates. The final sample of 3,895 consists of students who are either white or black, with complete data on all outcomes and covariates. Table 1 shows descriptive statistics for the variables, separated by our race-gender groups of interest.

Descriptive Statistics, High School Longitudinal Study of 2009, N = 3,895.

Note:Descriptive statistics are weighted. Standard deviations for continuous variables are in parentheses.

Values are top-coded as 1.5 times the top category.

p < .05 for comparison of race-gender group to white boys; †p < .05 for comparison between boys and girls within race groups. More detailed p values are included in the main text where applicable.

Parent-Reported College Savings

The main dependent variable is parental college savings, which parents reported in the 2012 follow-up, when most students were in the spring of their 11th-grade year. This measure represents the financial resources explicitly reserved for college at a time when many students are starting to make concrete plans for their education beyond high school.

We use this variable in two forms. First, we examine whether any money is saved for the child’s college education (yes/no). Second, we examine the amount of money saved among parents who have saved for their child’s college education, which removes the large number of respondents who reported zero savings. 3 College savings is reported categorically in HSLS. We assigned each respondent the median value for their category, and we top-coded this variable as 1.5 times the top category for those who reported savings in the highest range. Some parents may have made errors when reporting the amount they had saved, as is sometimes the case for financial measures that are commonly included in surveys, such as household income. Assuming classical measurement error, the results we present here should be considered conservative estimates of differences between our groups of interest. Despite the possibility of measurement error, the parent-reported data included in HSLS are far preferable to student estimates of their parents’ college savings, which are reported in some surveys.

Funding Sources Parents Expect to Use for College

We also examine whether parents expect to use each of six funding sources to pay for their children’s college, as measured in the 11th-grade parent survey. These funding sources are listed in the bottom section of Table 1. Parents’ or relatives’ earnings/savings and student’s earnings/savingsreflect the economic resources available to parents and students. Scholarships or grantsare typically either need-based or merit-based and do not need to be repaid. Federal or state loanseventually do need to be repaid, but their interest rates and repayment plans are more forgiving than private loans in the parent’s name or private loans in the student’s name(Consumer Financial Protection Bureau 2012). Each of these funding sources was measured as a binary variable, where 1 indicates the family plans to use the funding source, regardless of the amount they intend to use. Although we do not have information on how much parents anticipate drawing from each of these sources, parents’ engagement with each funding source is an indicator of their financial opportunities and constraints, as well as their broader approach toward parental investment. Importantly, these outcomes are not mutually exclusive, as families must often piece together multiple funding sources to pay for higher education.

Independent Variables

As discussed earlier, prior research has conceptualized parental college savings as a function of a child’s chances of attending college. These chances are largely (although certainly not entirely) determined by parents’ ability to pay and children’s precollege academic performance. To quantify these two dimensions, we adapt a method used by Brand and Xie (2010) to estimate each student’s predicted probability of enrolling in college. Specifically, we take an outcome measured in a future round of the HSLS survey—whether the student was enrolled in college full-time in fall 2013—and estimate each student’s predicted probability of achieving that outcome. 4 This method allows us to model a student’s chances of attending college (which mirrors our theoretical argument about parents calculating their children’s chances of college attendance) while also allowing us to combine multiple predictors into more succinct measures of economic and academic background.

We separate Brand and Xie’s (2010) predictors into two models, representing the two separate dimensions we theorize throughout. As listed in Table 1, economic/family factors include family income, the highest level of education completed by either parent, whether the respondent parent is married or partnered, number of siblings, and whether the student’s high school is located in an urban area. Academic factors include the student’s score on an NCES-administered math test, whether the student took at least one Advanced Placement course, and whether the student believes “all” their friends plan to attend a four-year college. We use these two sets of variables as predictors, with future college enrollment as the outcome, to generate two separate measures: students’ predicted probability of attending college as determined by (1) economic/family factors and (2) academic factors, which we use separately in the analyses. Most of our predictors are the same as those used in Brand and Xie (2010), but there are some differences and omissions because we use different datasets—we compare our variables with Brand and Xie’s in Appendix A in the online supplement. Of course, economic/family and academic factors are highly interrelated, and we recognize it is not possible to isolate the effects of one set of factors without also introducing aspects of the other. Yet, we use these factors separately in models to understand to what extent they are related to parental college savings independently.

Figure 1 shows the distributions of each of these predicted probabilities for our four race-gender groups of interest: white boys, white girls, black boys, and black girls. Predicted probabilities of attending college based on economic/family factors are shown in the left column, and predicted probabilities based on academic factors are shown in the right column. These distributions show a clear divide between white and black students. White boys and girls generally have higher predicted probabilities of attending college than their black peers. Black boys’ probabilities are perhaps the closest to normally distributed, with many students having moderate predicted probabilities of attending college. Black girls’ probabilities, in the bottom row, tend to be normally distributed when we consider economic/family factors, reflecting their moderate economic circumstances. At the same time, black girls’ probabilities are more negatively skewed when we consider academic factors, reflecting their strong academic qualifications. This apparent contradiction between the economic and academic circumstances of black girls is an important dynamic that we will consider further throughout the analyses.

Distributions of predicted probabilities of enrolling in college, based on economic/family factors (left column) and academic factors (right column).

In addition to the predictors described already, the models account for the type of college parents expect their children to attend in the fall after high school graduation, if any (see Table 1). We control for this measure because different types of colleges are generally linked to different costs of attendance, and parental savings could be dialed up or down depending on what parents expect to pay (although high sticker prices do not necessarily translate to high out-of-pocket costs, especially for low-income students, which we discuss throughout the Results and Conclusion).

Analytic Strategy

We begin by assessing basic differences in parental college savings. Here we consider how race, gender, and their intersections, along with the other predictor variables of interest, are associated with parental college savings. Then we incorporate our predicted probability measures to determine how students’ chances of attending college, as dictated by economic/family and academic factors, are related to college savings. As a final component, we examine how students’ predicted probabilities of enrolling in college are associated with the funding sources parents expect to use to pay for college. We assess how these anticipated funding sources differ at various probabilities of college enrollment (again, separately for economic/family and academic predictors) and across race-gender groups.

Results

Race, Gender, and Patterns of College Savings

We first look at mean differences in parental college savings for white boys, white girls, black boys, and black girls. Before turning to the multivariable models that account for sociodemographic controls, the descriptive statistics in Table 1 show average parental college savings across race-gender groups. As indicated in Table 1, saving for college is by no means universal among parents. Fifty-six percent of parents of white boys had saved anything by their child’s 11th-grade year, versus 54 percent of parents of white girls. This figure drops to 34 and 38 percent for parents of black boys and black girls, respectively (both p < .001 compared to white boys). 5

Table 1 also reveals significant race-gender differences in the amount parents have saved for college, conditional on having saved. Parents of white boys report saving an average of $24,810, compared to $21,693 for white girls (p < .05). Parents of black boys ($11,559) and black girls ($9,611) report saving substantially less than parents of white boys (both p < .001).

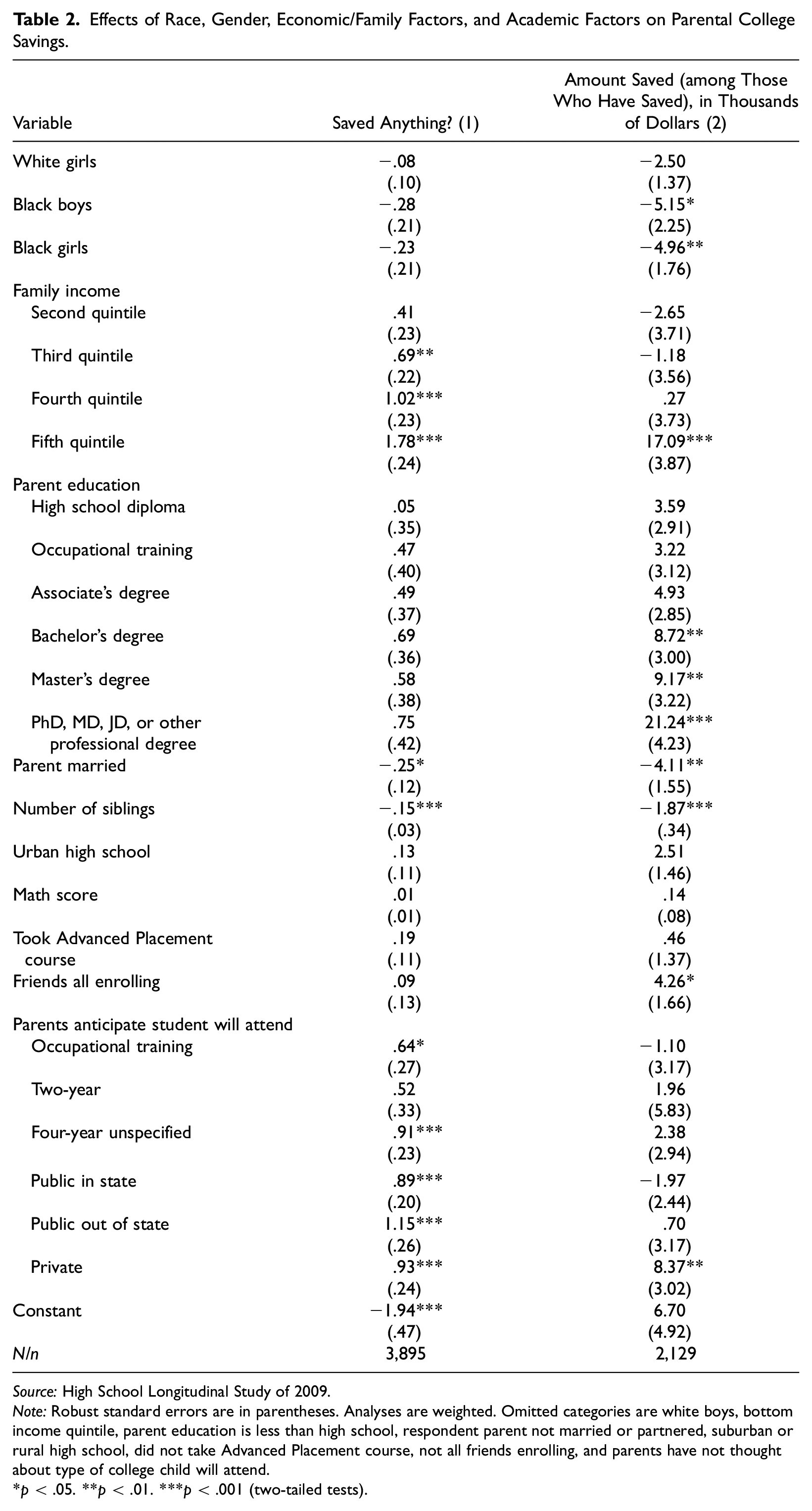

The multivariable models in Table 2 assess the extent to which these significant mean differences diminish once other control variables are accounted for. Model 1 examines whether parents saved anything for college, using logistic regression. Here we see that the significant race-gender gaps dissipate once other control variables are included in the model—particularly economic and family factors, such as family income and number of siblings. Model 2 is a linear regression that gauges parents’ amount saved, conditional on having saved. The difference between white boys and girls again dissipates, but here we see a gap between white boys and black boys and girls. When we include controls—including a control for black students’ substantial family income disadvantage relative to white boys—black students continue to face a savings disadvantage, equal to approximately $5,000 for both black boys (p < .05) and black girls (p < .01). To summarize, after accounting for a comprehensive set of economic, family, and academic factors, parents of students in all four race-gender groups are equally likely to have put away at least some money for college—but even these extensive controls do not account for the disparities in the amount saved between race-gender groups, with race emerging as the main stratifying factor.

Effects of Race, Gender, Economic/Family Factors, and Academic Factors on Parental College Savings.

Source:High School Longitudinal Study of 2009.

Note:Robust standard errors are in parentheses. Analyses are weighted. Omitted categories are white boys, bottom income quintile, parent education is less than high school, respondent parent not married or partnered, suburban or rural high school, did not take Advanced Placement course, not all friends enrolling, and parents have not thought about type of college child will attend.

p < .05. **p < .01. ***p < .001 (two-tailed tests).

Accounting for Predicted Probability of Enrollment

These initial models are important for understanding how parental college savings is associated with race, gender, and other factors on average. But how are these processes further complicated by students’ chances of attending college? Prior research posits that parents save for college in accordance with their children’s realistic chances of actually attending college, as determined by their ability to pay and their children’s academic performance. Accordingly, we assess parental college savings for white boys, white girls, black boys, and black girls along those two dimensions.

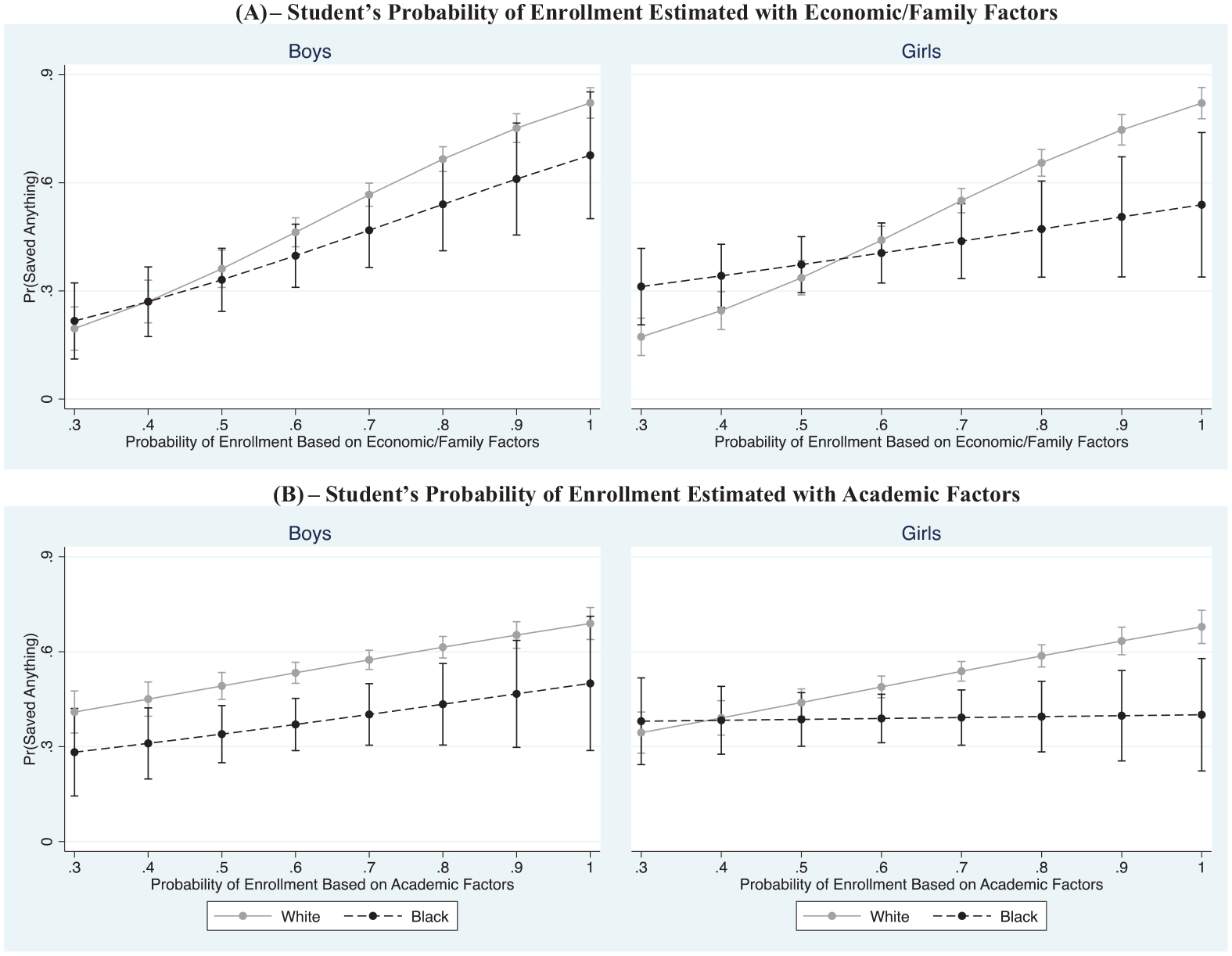

Figure 2 shows parents’ chances of having saved anything for college, over the range of students’ predicted probabilities of enrollment. 6 The top panels illustrate how students’ predicted probability of enrolling in college, as determined by economic/family factors, is related to their parents’ chances of having saved. The trend lines for white boys and girls show a clear positive relationship between chances of enrollment, based on family circumstances, and savings. As students’ economic and family circumstances are more favorable, and their chances of enrollment increase in turn, their parents’ chances of having saved also increase substantially. This is also the case for black boys, although their positive slope is muted by comparison. Black girls have the flattest trend line: We observe no difference in the probability of having saved between black girls with the highest versus lowest chances of college enrollment (p = .09; not shown). This pattern suggests black girls experience null returns to their economic and family circumstances when it comes to having a college savings account, which is not the case for any of the other race-gender groups. As a result, we observe clear differences in parents’ chances of saving between black girls and students in other race-gender groups who have equal economic probabilities of attending college. To give one example, among students whose economic circumstances make them almost certain to attend college (i.e., economic probability = .90), black girls have just over a .50 probability of having any money saved, compared to nearly .75 for white girls.

Predicted probability of parents having saved for child’s college education, N = 3,895.

We also find racial differences among girls at both the top and bottom of the distribution. At the top of the distribution (at about the .80 probability level and above), parents of white girls are more likely to have saved. But at the bottom of the distribution, parents of black girls are more likely to have saved. Thus, black girls do not experience clear returns to economic and family circumstances; however, when their chances of college enrollment are relatively low as dictated by these circumstances, black girls are more likely than their white counterparts to receive at least some amount of parental investment.

The bottom panels of Figure 2 show the relationship between students’ probability of enrolling in college, as predicted by academic factors, and their parents’ chances of having saved. Again, we see a distinct positive relationship for white boys and girls. But from the perspective of disparities in savings, the more consequential pattern here relates to the trend lines for black boys and, especially, black girls. For black students, academic advantages do not translate to savings advantages in the same way they do for white students. Among both black boys and black girls, we find a null relationship between probability of enrollment based on academic factors and parents’ chances of saving for college. In other words, parents of the most academically successful black boys and girls are no more likely to have saved than parents of the least academically successful. The trend line for black girls, in particular, is virtually flat. To continue with the example given earlier, a black girl whose academic credentials make her virtually guaranteed to attend college (i.e., academic probability = .90) is nearly equally likely to have college savings as a black girl with a .30 academic probability of attending college. This translates to increasingly large gaps in savings between black and white girls who are academically equivalent.

Figure 3 builds on these patterns by examining the amount saved (conditional on having saved), over the range of students’ predicted probabilities of enrollment. The top panels show estimates over the range of students’ probability of enrollment, as predicted by economic/family factors. For all race-gender groups, we see a clear positive relationship between economic and family circumstances and college savings. Students with more favorable economic and family circumstances generally have higher balances in their college savings accounts, conditional on having savings. Yet, the amount saved differs substantially by race. Toward the top of the distribution, parents of white boys and girls have saved substantially more than their black counterparts, with an especially large gap of about $24,000 between white boys and black boys. At the bottom of the distribution, black boys and black girls both experience a savings advantage. Thus, among families with few economic resources, black parents tend to make greater investments in their children’s college education than do white parents.

Amount parents have saved for child’s college education, n = 2,129.

The bottom panels of Figure 3 show estimates over the range of students’ probability of enrollment, as predicted by academic factors. As white boys and black boys have stronger academic records, and their chances of college enrollment increase in turn, their parents tend to save more for college (conditional on having saved). Yet parents of white boys save significantly more than parents of black boys. This pattern generally holds for white girls, in the right panel. Yet, this is clearly not the case for black girls. In terms of the amount of parental college savings, the most academically successful black girls are virtually no different than the least academically successful black girls. As a result, white girls at the top of the distribution have more than double the college savings of equally qualified black girls (about $28,000 versus about $12,000). 7

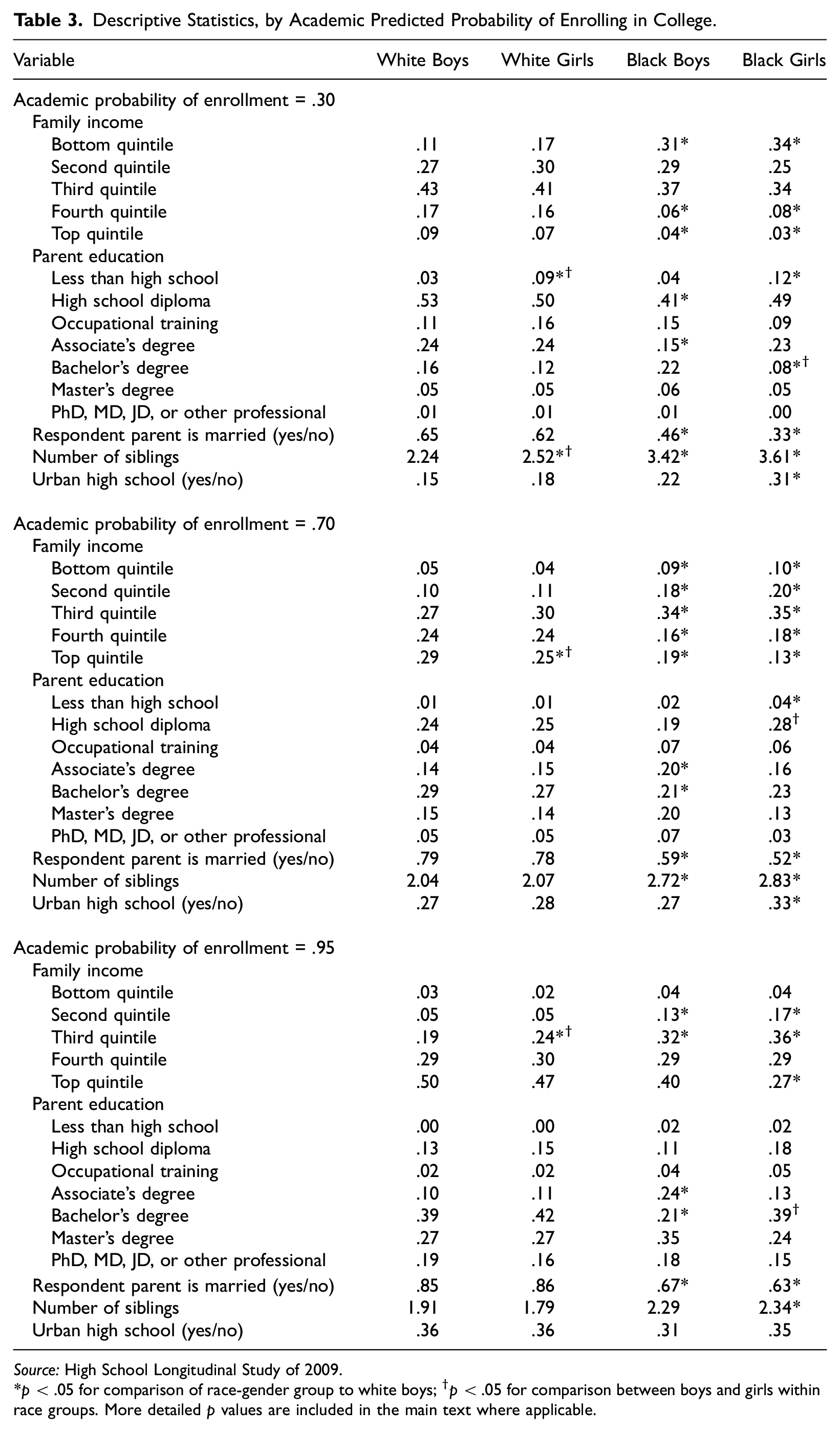

Why do black students’ chances of enrolling in college often have a null relationship with their parents’ chances of saving or the amount saved? One possible explanation is that black students with a high academic probability of college enrollment have relatively low college savings because they are disadvantaged in terms of economic and family factors. To investigate this dynamic, we compared the economic and family circumstances of students in different race-gender groups at various levels of predicted college enrollment. Table 3 shows results from this supplemental analysis. Cell sizes would normally be too small to produce reliable descriptive statistics for each race-gender group and especially to conduct significance tests across groups. To navigate this issue, we used regressions to estimate predicted values for each of our economic/family predictors for students at different academic probabilities of attending college (i.e., academic probabilities of .30, .70, and .95). 8 These regressions use the full sample of respondents to make estimates at the academic percentiles of interest, essentially producing estimates that are more stable than if we were to use data only from students in a given probability band. 9

Descriptive Statistics, by Academic Predicted Probability of Enrolling in College.

Source:High School Longitudinal Study of 2009.

p < .05 for comparison of race-gender group to white boys; †p < .05 for comparison between boys and girls within race groups. More detailed p values are included in the main text where applicable.

The results in Table 3 help explain why black boys, and especially black girls, tend to receive less college savings than white boys and girls with similar academic qualifications. In each panel, black students experience more economic and family constraints than their white peers. Specifically, in each probability band, black girls (in terms of sheer point estimates and compared to those in other race-gender groups) are the most likely to be in the bottom quintile and least likely to be in the top quintile of parental income; are the most likely to have parents with only a high school diploma and least likely to have parents with advanced degrees; are the least likely to have married parents; and are raised in households with the largest number of siblings.

These constraints are perhaps most pronounced in the bottom panel, which shows estimates for students with a .95 academic probability of attending college. Substantively, one can think of these students as some of the most academically qualified 11th graders in this nationally representative sample. Here we see that the most academically qualified black students come from families that are much less well-off than comparable white students, and black girls are again particularly disadvantaged—including relative to equally high-achieving black boys. The modal white boy, white girl, and black boy in this probability band comes from a family in the top income quintile. The modal black girl, however, comes from a family in the third income quintile, which clearly demonstrates the exceptionality of high-achieving black girls compared to their peers in other race-gender groups.

In summary, academic credentials may only take black students so far when it comes to their college savings accounts. Even when they are among the most highly qualified from an academic standpoint, black students—and particularly black girls—may have relatively little college savings because they have far fewer economic advantages, and face far more family constraints, than their white peers.

How Do Parents Anticipate Paying for College?

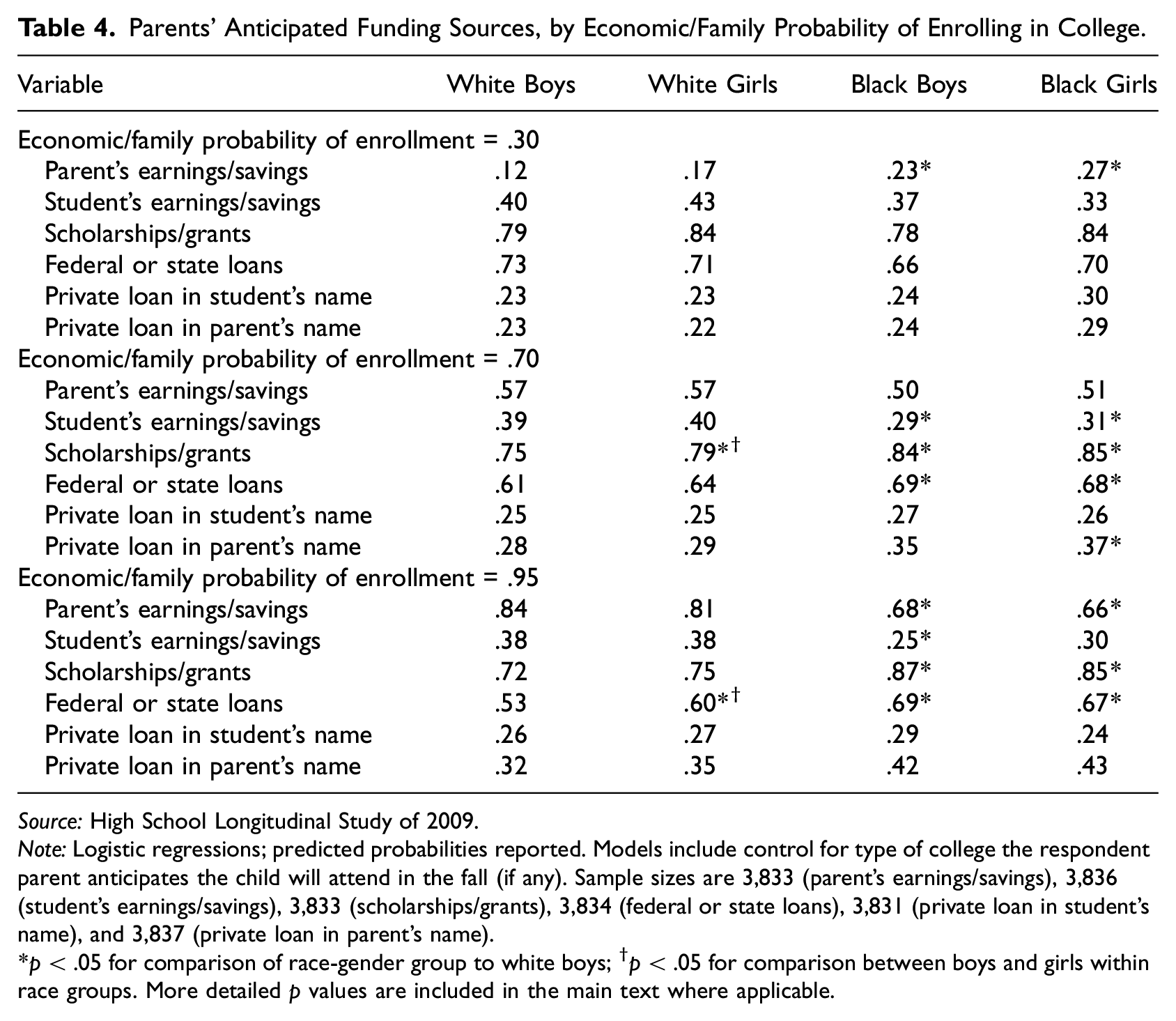

As a final component of the analysis, we assessed how race, gender, and students’ chances of attending college are associated with the funding sources parents plan to use to cover their children’s college costs. As discussed earlier, we use data on six funding sources: parents’ earnings/savings, student’s earnings/savings, scholarships or grants, federal or state loans, private loans in the student’s name, and private loans in the parents’ names. These anticipated funding sources reflect financial opportunities and constraints across race-gender groups as well as parents’ broader approaches toward parental investment.

Table 4 shows parents’ anticipated funding sources stratified by students’economic/family probability of enrollment—in other words, how parents plan to pay for their children’s college costs at three levels of economic advantage and constraint. 10 The top section shows predictions for parents who face considerable economic constraints. In general, these parents have similar plans for paying for higher education across race-gender groups. In one notable exception, parents of black boys (p < .05) and blacks girls (p < .001) are more likely than parents of white boys to anticipate using a parent’s earnings or savings. This finding is consistent with our earlier observation that the most financially disadvantaged black students tend to receive more college savings than their white counterparts.

Parents’ Anticipated Funding Sources, by Economic/Family Probability of Enrolling in College.

Source:High School Longitudinal Study of 2009.

Note:Logistic regressions; predicted probabilities reported. Models include control for type of college the respondent parent anticipates the child will attend in the fall (if any). Sample sizes are 3,833 (parent’s earnings/savings), 3,836 (student’s earnings/savings), 3,833 (scholarships/grants), 3,834 (federal or state loans), 3,831 (private loan in student’s name), and 3,837 (private loan in parent’s name).

p < .05 for comparison of race-gender group to white boys; †p < .05 for comparison between boys and girls within race groups. More detailed p values are included in the main text where applicable.

The bottom section of Table 4 shows parents’ anticipated funding sources among the most economically advantaged families. Although these families are virtually guaranteed to send their children to college as dictated by their economic and family circumstances, we see distinct differences in funding sources across race-gender groups. Most notably, nearly all parents of white students expect to pay for at least part of college with their own earnings or savings—but this is not the case for parents of black students (both p < .01). This pattern is consistent with our earlier results regarding lack of college savings among affluent black parents. Notably, parents of black students are more likely than parents of white boys to expect scholarships or grants (both p < .01). This pattern is suggestive of two potential causal mechanisms: Either black parents are hopeful their children will receive scholarships to make up for their lack of savings, or black parents have been less intentional about saving because they are enthusiastic about their children’s academic performance and are optimistic they will receive scholarships.

In addition, parents of black boys are less likely than parents of white boys to expect children to contribute their own earnings or savings (p < .01). Perhaps black boys have few personal resources to draw on at the time of college enrollment, or their parents would prefer to pay for college through other sources that impose less of a personal burden. Finally, we find that compared to parents of white boys, parents of white girls (p < .05), black boys (p < .01), and black girls (p < .05) are more likely to anticipate use of government loans. Thus, among students from relatively affluent families, white boys may be least often affected by the burdens of educational debt.

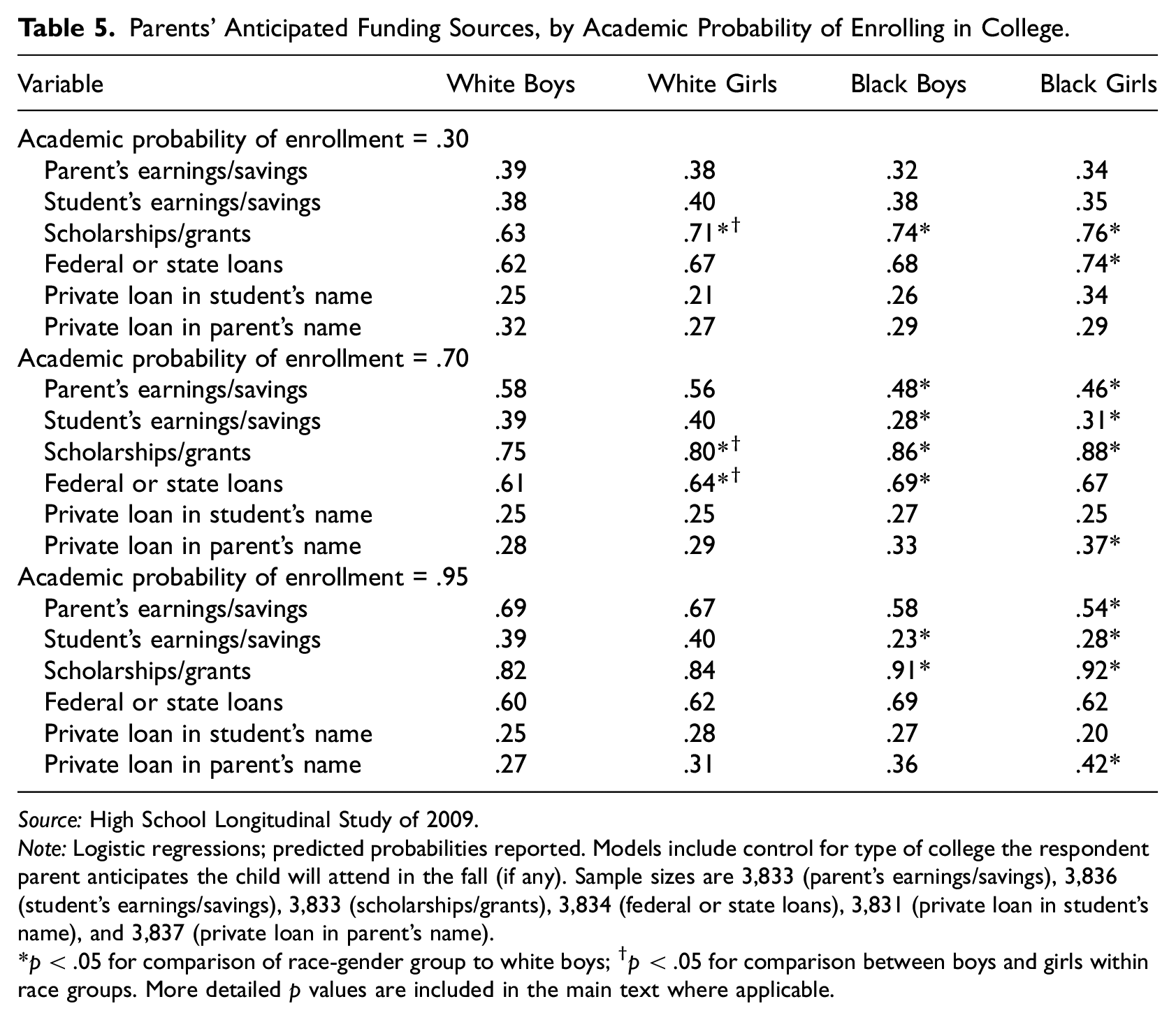

Table 5 shows parents’ anticipated funding sources, this time stratified by students’academic probability of enrollment. 11 The top section of the table shows anticipated funding sources for students with weaker academic credentials. Among parents of these less qualified students, most anticipated funding sources are comparable across race-gender groups, with the exception of scholarships. Compared to parents of white boys, parents of white girls, black boys, and black girls (all p < .05) are more likely to indicate they will pay for at least part of college with a scholarship or grant.

Parents’ Anticipated Funding Sources, by Academic Probability of Enrolling in College.

Source:High School Longitudinal Study of 2009.

Note:Logistic regressions; predicted probabilities reported. Models include control for type of college the respondent parent anticipates the child will attend in the fall (if any). Sample sizes are 3,833 (parent’s earnings/savings), 3,836 (student’s earnings/savings), 3,833 (scholarships/grants), 3,834 (federal or state loans), 3,831 (private loan in student’s name), and 3,837 (private loan in parent’s name).

p < .05 for comparison of race-gender group to white boys; †p < .05 for comparison between boys and girls within race groups. More detailed p values are included in the main text where applicable.

The bottom section of Table 5 shows parents’ anticipated funding sources for students with the strongest academic credentials. Here we see clear black-white differences in parents’ plans for college funding and, in particular, distinct patterns of college funding for highly qualified black girls. Parents of black girls are considerably less likely than other parents to anticipate paying for college with their own earnings or savings—with a predicted probability of only .54. The rest of the table gives some clues as to how parents of highly qualified black girls plan to make up for their lack of parental funding. Compared to parents of white boys, parents of black girls are more likely to anticipate scholarships (p < .001; as are parents of black boys, p < .01). We also find that parents of highly qualified black girls are more likely than parents of white boys to anticipate use of a private loan in the parent’s name (p < .01). This is a troubling pattern, considering that private loans tend to have much higher interest rates than government-backed loans and cost much more over the life of repayment (Consumer Financial Protection Bureau 2012). Overall, parents of highly qualified black girls are in the unique situation of having little earnings or savings to contribute for college. As a consequence of their lack of savings, these parents may turn to high-cost loans—a situation that may contribute to their own household’s economic insecurity, as well as threaten their ability to assist their daughters financially in later years.

Conclusion

By all accounts, paying for college is harder than it used to be. A growing body of research demonstrates inequalities, particularly by race, in the effect of student loan debt on long-run economic returns to college completion. Yet, less is known about parental college savings among recent cohorts of students, particularly using an intersectional framework. Drawing on theories of parental investment, as well as research that points to persistent race and gender inequalities in economic resources and educational attainment, this article assessed how parental college savings differs across race-gender groups. We used models that account for students’ chances of college enrollment, considered separately by economic/family factors and academic credentials, to parse out race and gender differences in savings across these spectrums. The analyses point to stark differences in parental college savings between white boys, white girls, black boys, and black girls, as well as differences in the funding sources parents anticipate using to supplement their savings.

Perhaps the most striking patterns we find pertain to black girls—in particular, a distinct lack of parental college savings for black girls with the strongest academic credentials. For white boys, white girls, and black boys, we find a positive relationship between students’ academic credentials and parental college savings. But for black girls, parental college savings is virtually unresponsive to their academic qualifications. To investigate why this happens, we compared economic resources across race-gender groups for students with different academic profiles. These analyses suggest highly qualified black students, and especially highly qualified black girls, come from families that are considerably less well-off than their white peers. Because most parents generally save in accordance with their ability to save, highly qualified black girls may end up with less savings by virtue of coming from relatively disadvantaged families.

This finding is consistent with prior research showing that black girls are particularly resilient when it comes to academics, as they tend to enroll in and complete college even in the face of challenging economic circumstances (DiPrete and Buchmann 2013). We show that, as a potential consequence of their overindexing in terms of academic performance, black girls may enroll in college with little parental savings to draw on—even if they have among the strongest academic credentials. This pattern underscores the idea that college funding is a mechanism through which higher education reproduces inequalities on account of race, gender, and class. Families of high-achieving black girls are positioned to save relatively little, and to take on loans that are relatively high risk, thus resulting in funding schemas that disadvantage black girls and their families across generations. Although black girls tend to overindex in terms of academic performance, our findings demonstrate that black girls face continued challenges in achieving economic mobility through higher education.

Other (unmeasured) factors likely play a role in this story, as well. Although we find clear economic differences between highly qualified black girls and those in other race-gender groups, there may be other explanations for these distinct patterns of savings among parents of black girls. This is not just a race effect, as we see key differences between parents of black girls and black boys; and this is not just a gender effect, as we see key differences between parents of black girls and white girls. Rather, parental college savings is an intersectional issue at its core, and thus it requires intersectional explanations. It may be that parents of black girls are more optimistic than other parents about their children’s ability to receive a sizeable college scholarship—large enough to cover all or nearly all of their children’s tuition and fees. We find that parents of highly qualified black girls and black boys are equally likely to expect to pay for at least part of college with a grant or scholarship, but the size of the expected grant might differ (we cannot assess this with the HSLS data). Future research should also assess the extent to which family configuration (e.g., the effect of having brothers; Powell and Steelman 1989) explains black girls’ savings disadvantage (which, again, we are unable to assess with HSLS). All of this is to say that other factors are likely driving at least part of this lack of college savings among high-achieving black girls, and additional work is needed to shed light on this issue.

Our data do, however, make clear the long-term economic implications for parents of highly qualified black girls. To counter the lack of earnings or savings earmarked for their children’s college education, these parents are more likely than parents in other race-gender groups to anticipate using a private loan in their name. Private loans tend to have higher interest rates and less forgiving repayment schedules than government-backed loans, and thus they are considered a risky financial tool. This may make parents of black girls vulnerable to economic insecurity in the long run. These patterns also have negative implications for the financial circumstances of black girls themselves, and their families, should they choose to form them (although research shows that debt and other financial obligations may delay young women’s marriage and fertility; Addo 2014; Nau, Dwyer, and Hodson 2015). If parents of highly qualified black girls are using their resources to service these private loans, then their children stand to benefit even less from any subsequent potential intergenerational wealth transfers or gifts. Of course, research consistently shows that when attempting to make these types of transfers, black families start from a much smaller pool than otherwise economically similar white families (Darity et al. 2018; Herring and Henderson 2016; Killewald and Bryan 2018). For these reasons, the racially unequal economic constraints that prevent parents from saving for college may have economic implications that affect multiple generations.

In addition, we find that among those with few economic resources, black parents tend to make greater investments in their children’s college education than white parents. This pattern holds for both boys and girls, and it echoes research on racial differences in parental college savings using earlier cohorts of students. Prior studies show that black parents invest just as much (if not more) in college than white parents once background characteristics are controlled for (Steelman and Powell 1993), and our findings update this research by showing this effect is concentrated among less advantaged families. At the top of the economic distribution, we find a clear savings advantage for whites, likely driven by high-income whites having greater average net worth than similarly high-income blacks (Darity et al. 2018; Smith 1995). Our estimates are likely conservative, given that the HSLS captures savings accounts specifically earmarked for higher education, but high-income whites tend to have additional resources that can be used for college if needed (e.g., investments, home equity).

Our findings also have implications for debates about the “match” between students’ academic credentials and the characteristics of the college they attend. This debate often centers on high-ability black students who are potential beneficiaries of race-based affirmative action for admission to selective colleges. One side of this debate argues that black students are better off attending colleges where most students are at or below their level of academic ability, and those who shoot too high are “mismatched” to their institutions and may have negative experiences and outcomes, such as low grades or dropout. The balance of scholarly evidence refutes this claim, demonstrating that black students benefit from attending selective institutions in terms of outcomes such as college completion and eventual earnings (Alon and Tienda 2005; Bowen and Bok 2000; Massey et al. 2011).

Our results further inform this debate by calling attention to the interplay between institutional characteristics and intersectionally varying linkages between students’ academic profiles and family economic circumstances. At a given level of high school academic success (e.g., among high achievers who may have the option to attend a highly selective college), black students, on average, come from much less affluent families than equally qualified white students. Thus, to the extent that elite colleges’ institutional resources allow them to offer more financial aid or fewer loans (see, e.g., Rimer and Finder 2007), there may be multigenerational financial advantages for high-achieving black students who attend an elite college. Further, our intersectional lens allowed us to demonstrate that high-ability black girls, in particular, stand to benefit most from institutional selectivity, to the extent selectivity is correlated with financial support.

The data provide clear evidence of parental college savings differences across race-gender groups, but we should emphasize two main data limitations. First, as noted previously, parental college savings is an imperfect measure of both parental economic resources and parents’ expectations for their children’s college attendance. Some parents might save less than others in similar economic circumstances because they work for a university where their children will receive a tuition benefit. Others might dial down their savings because they expect their children to receive a merit-based scholarship, or they anticipate receiving financial aid because they believe their children will attend a prestigious college and receive a generous aid package (this is probably not common, however, given research showing that the population of highly qualified low-income students applying to selective colleges is quite small; Hoxby and Avery 2012). Thus, although we consider parental college savings to be a reasonable proxy for these constructs, this measure is imperfect.

Second, HSLS does not include information on parental net worth. This is an important omission, not only because net worth differs so dramatically across black and white families, but also because wealth has been shown to affect college attendance net of income (Conley 2001). It is reasonable to assume that some aspects of wealth are captured in the dependent variable, as college savings accounts often include investments that are not classified as yearly income. Future research should incorporate data on other types of assets (not to mention other racial groups) to understand further how race and gender shape college funding and exposure to its multigenerational implications.

Supplemental Material

Quadlin_and_Conwell_online_supplement – Supplemental material for Race, Gender, and Parental College Savings: Assessing Economic and Academic Factors

Supplemental material, Quadlin_and_Conwell_online_supplement for Race, Gender, and Parental College Savings: Assessing Economic and Academic Factors by Natasha Quadlin and Jordan A. Conwell in Sociology of Education

Footnotes

Acknowledgements

We are grateful to Brian Powell and Rachel Dwyer for comments on a previous version of this article.

Research Ethics

The High School Longitudinal Study of 2009 is a publicly available anonymized dataset.

Supplemental Material

Supplemental material is available in the online version of this journal.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.