Abstract

This paper utilises a reduced-form equilibrium model to investigate the possible sources of real estate investment differentials among 22 provinces, five autonomous regions and four municipalities of the People’s Republic of China. The model is estimated using panel data from 2001 to 2006, yielding a total of 186 observations. Specifically, empirical results suggest that demographic, economic and planning factors are the major determinants to cause real estate investment to vary among Chinese regions. The relatively small coefficient estimate of real interest rates indicates that it has a significant but modest impact. Based on the coefficient estimates, this paper finally suggests that the Chinese government should focus and work on several policy parameters in order to achieve a more balanced state of real estate investment across Chinese regions.

1. Introduction

Previous research has suggested that real estate investments are interrelated to any country’s economic growth, of which residential investment Granger-causes GDP, 1 and a change in this type of investment can be used as an indicator to predict a change in the latter (Green, 1997). China’s real estate market, particularly its residential market, first emerged in the late 1980s and subsequently evolved and developed during the 1990s. It is not yet a mature market environment, although it is an integral component of the political and economic transition from a socialist to a market economy. Its development was promoted by a relatively stable political environment and strong economic performance which have ensured continuous economic growth and political stability in turn (Mak et al., 2007).

Real estate markets provide an interesting field for economic research. On the one hand, the forward businesses of the real estate market include property sales, mortgage, insurance, maintenance, improvement and management, while the backward businesses comprise timber, cement, steel and other material markets. As the Chinese economy has been progressing rapidly since 1998, the relationship between the real estate market and its related businesses will become more interactive than ever. On the other hand, real estate investment is highly volatile, subject to exogenous shocks in the political and socioeconomic environment. Out of real estate investment, residential investment is one of the most fluctuating components of GDP. During an economic boom, it is not surprising to observe a more than 20 per cent growth rate in residential investment in a single year, while this type of investment may fall by a similar magnitude during an economic recession. Although real estate investment comprises only 4.7–8.4 per cent of GDP in China as a whole, its disproportionate influences on the latter should not be overlooked (Browne, 2000).

In the Chinese real estate market as a whole, 2 it was estimated that gross investment rose from ¥410.32 billion in 1999 to ¥1942.29 billion by 2006 (an average compound growth rate of 21.45 per cent over 8 years), contributing some 4.69–8.41 per cent towards GDP for the 1999–2006 period (National Bureau of Statistics of China, 2007, see Figure 1). Real estate investment, which has comprised approximately 14.16–18.99 per cent of investment in fixed assets, has escalated since 1999, mainly due to the surge in investment in buildings, especially those for residential use.

Real estate investment, gross investment in fixed assets and GDP of 31 Chinese regions (¥ billion).

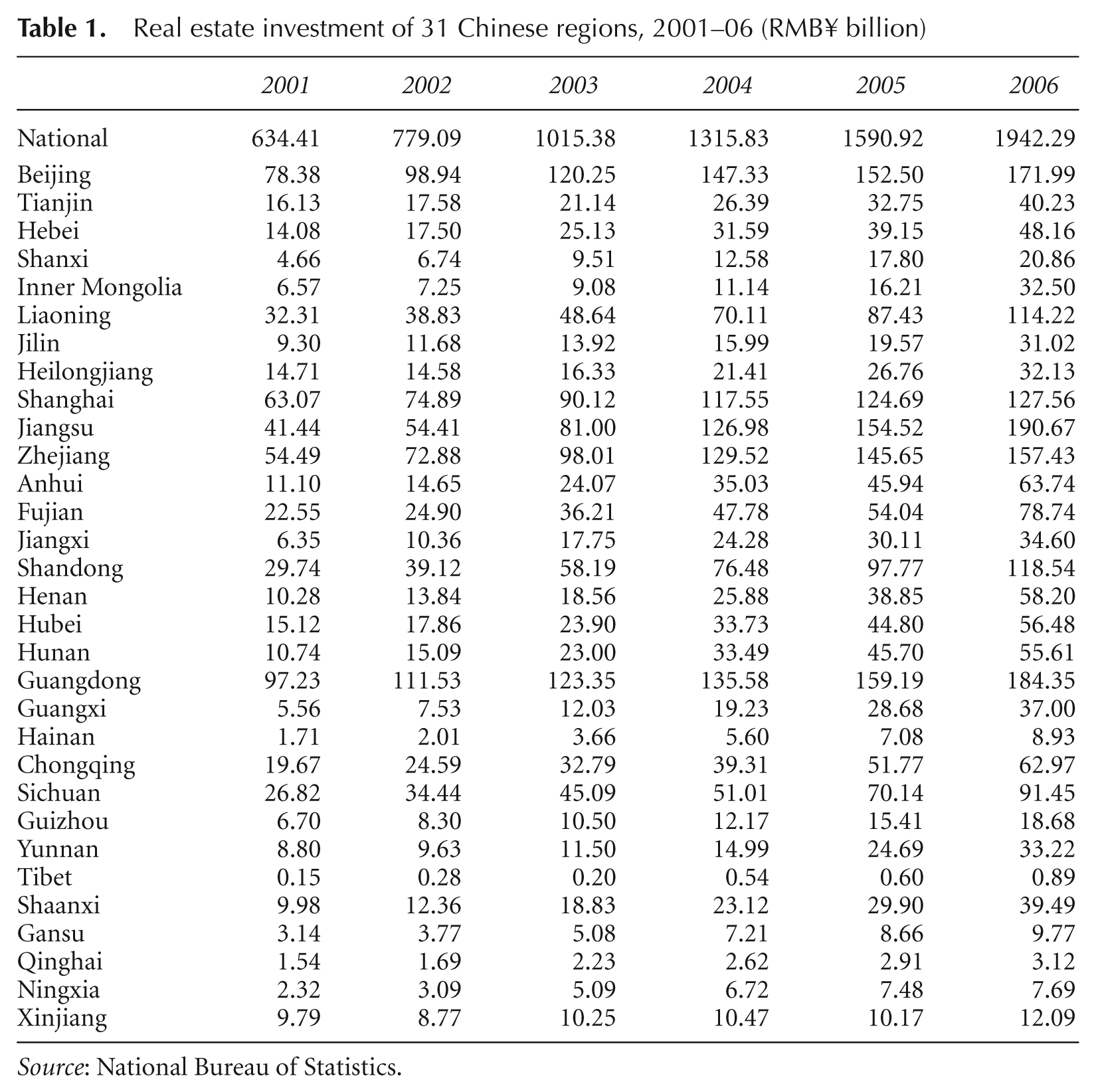

Even in a well-developed country, real estate investment, however, varies greatly from region to region and excessive investment in one region will probably develop speculative bubbles within that area (Choy et al., 2011). For example, this type of investment in 2006 ranged from ¥0.89 billion in Tibet to ¥190.67 billion in Jiangsu (see Table 1). Such differentials in real estate investment have originated from the great variations in regional economic development and the extent to which they are exposed to the Western world (Wang and Wang, 1996). In 2003, the top 10 cities on the mainland for real estate development potential were selected by an organisation called the China Real Estate Top Ten Research Group. They were ranked in order: Shanghai, Beijing, Shenzhen, Guangzhou, Xiamen, Ningbo, Hangzhou, Nanjing, Chengdu and Tianjian (Yang, 2004). Chengdu is the only one not located in the east.

Real estate investment of 31 Chinese regions, 2001–06 (RMB¥ billion)

Source: National Bureau of Statistics.

Unfortunately, empirical studies of Chinese real estate market have been relatively few and there are even fewer empirical investigations of the real estate investment differentials among the 31 Chinese regions. Previous studies which combine some ingredients have been relatively common in the US and Canada (Choy et al., 2011), such as the modelling of residential investment (Egebo et al., 1990; Edge, 2000; McCarthy and Peach, 2002, Berger-Thomas and Ellis, 2004; Demers, 2005; Dynan et al. 2006; Fisher and Gervais, 2007) and the intermetropolitan differentials of house prices and rentals, land prices and housing supply (Rosen, 1978; Ozanne and Thibodeau, 1983; Fortura and Kushner, 1986; Manning, 1989; Potepan, 1996; Green et al., 2005; Miller and Peng, 2006). With the purpose of filling this research gap, the objective of this paper is to identify empirically the sources of interregional real estate investment differentials, with special reference to China. This paper develops a regional model of real estate investment and this type of investment for the 31 regions is then regressed on the determinants of the model to explain the variations in investment.

2. Literature Review

The main indicator of the quantity of new housing supplied to the economy is the real estate investment series from the national accounts (Krainer, 2006). Real estate investment comprises expenditure on new construction, maintenance and building improvement and equipment purchased for use in residential, office, commercial, retailing and warehouse structures. Real estate or residential investment has been hypothesised as a supply-side equation and aggregate supply becomes a function of demographic factors, income, real interest rates, housing prices and legal land use constraints.

Easton and Patterson (1987) estimate a supply-side equation of residential fixed investment for the UK, with house prices, producer costs, labour costs and short-term interest rates being explanatory variables. The short-term interest rates reflect the cost of borrowing by house builders to finance residential construction. The positive impact of the ratio of house prices over labour and manufacturing costs reflects the profit potential for the house builders. Empirical results show that a 2 percentage point cut in the base interest rates increases residential investment by 3 per cent. If the base rates keep falling, the long-run steady state effect would be to raise this type of investment by 9.8 per cent.

Empirical results presented by Egebo et al. (1990) for the seven major OECD economies (the US, Japan, Germany, France, the UK, Italy and Canada) relate to the determination of housing stocks, an approach which is considered to be more sophisticated on theoretical grounds, with more transparent long-term properties. Using a second-order stock-adjustment model, the empirical estimates confirm that real after-tax income is one of the major determinants of residential investment, with the estimated long-run elasticity for real housing stock demand being quite close to unity for most of the countries under investigation. Financial market factors have been found to have an important impact on housing activity, as suggested by the significance of the real interest rate estimates obtained for most countries.

The Ministry of Finance and Corporate Relations, British Columbia (1999) develops and maintains the British Columbia macroeconomic model to provide medium-term economic forecasts and policy simulation capabilities. One of the important topics under investigation is the residential investment that can be separated into that for new housing and other (transfer costs and alterations and improvements). The study suggests that the residential construction expenditure can be modelled as a function of housing starts, its lagged values and a time-trend. However, the equation was not estimated explicitly. 3

To model residential investment, Demers (2005) proposes the use of multivariate specifications that model the joint process of residential investment and prices and that exploit the long-run relationships between housing investment and fundamentals. Their specifications allow for a structural change to influence the co-integrating vectors for housing investment. Empirical results suggest that the fundamentals explain variations in housing investment in both the long run and short run. However, Demers (2005) could not establish a long-run relationship that links the relative price of housing to fundamental variables. His study suggests that the growth of relative housing prices can only be explained by the growth of wealth. In supplement, his results suggest that the fundamentals seem to support the high levels in investment observed since 2000 and confirm that housing sector is not driven by speculative behaviour.

Dynan et al. (2006) suggest that, while previous research has focused primarily on the role played by milder economic shocks, improved inventory management and better monetary policy, their study explores another potential explanation offered by financial innovation. Such innovation includes developments in lending practices and loan markets that have improved the ability of households and firms to borrow, and changes in banking policy such as the lifting of Regulation Q, an interest rate ceiling imposed on deposit accounts by the Federal Reserve Bank system in the 1930s. Particularly, Dynan et al. (2006) begin with a model in which the log differences of real aggregate residential investment are specified as a function of four lags each of log differences of real residential investment, real disposable personal income and the 30-year fixed mortgage rate. The response of residential investments to movements in mortgage rate was noticeably smaller after the mid 1980s than before, a phenomenon being consistent with the lifting of Regulation Q.

There have been relatively few empirical studies of Chinese real estate markets using macroeconomic data, with the exception of Barnett and Brooks (2006). This research provides a simple model to estimate the change in residential investment utilising 30 Chinese regions from 1996 through 2004. Empirical results suggest that, while change in residential investment is positively but weakly related to real household income growth, it is negatively related to real interest rates and change in unemployment rates, with the estimated coefficients of -0.03 and -0.07 respectively. The authors argue that it might be because of weakness in the provincial data, that urban population growth has not been found to cause change in residential investment to vary among Chinese regions. Unfortunately, these estimates are subject to a wide margin of error, given the relatively low explanatory power of the static panel data model.

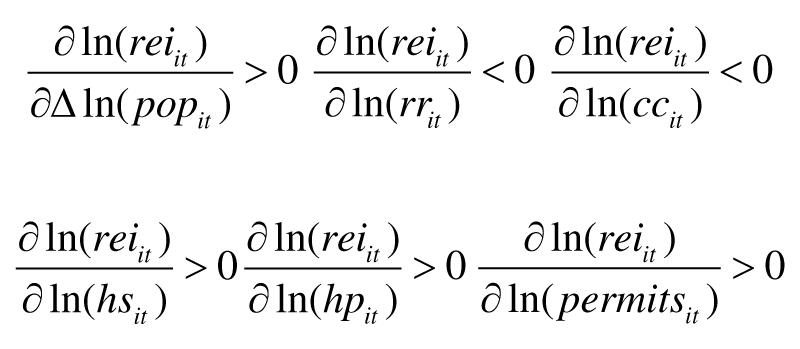

With respect to the interrelated relationships among real estate investment, city growth and the general economy, the current study identifies and estimates the sources of interregional comparisons of one of the important real estate issues—specifically, the real estate investment differentials. In general, the existing literature has utilised time-series (annual or quarterly) data for one single country, such as Germany, Japan, the UK or the US, for about 20–30 years to investigate the possible sources of variations in real estate or residential investment. The current study, however, utilises annual data for the Chinese regions from 2001 to 2006 and estimates the real estate investment equation with the fixed effects regression. Established on previous studies, this paper hypothesises real estate investment as a function of a population factor, real interest rates, construction costs, gross floor area sold, house prices and housing permits.

Particularly, the sale of commodity housing (measured in terms of square metres) enters the picture as business confidence perceived by property developers. If property sales are good and the developers are confident about the real estate market, they will be eager to invest more, ceteris paribus. Following Ozanne and Thibodeau (1983), Fortura and Kushner (1986), Manning (1989) and Potepan (1996), land use constraints imposed by the governments are incorporated into our real estate investment equation (see also Pollakowski and Wachter, 1990). To allow for its effect, housing permits are taken as a proxy for land use constraints that influence the determination of real estate investment. These contrived restrictions raise the price of urban land and hence reduce the supply of commodity housing in the region. More commodity housing permitted implies a less stringent government land use restriction and vice versa. The idea comes from the planning literature that, while permission for housing completion increases (regulation is less stringent), developers are able and willing to invest more in real estate markets when there is a strong market demand, whereas the regulation may not be binding when the housing market is sluggish. It follows that there exists a positive relationship between permitted commodity housing and real estate investment, other things being constant.

Our empirical data contain 31 panels, starting from the period between 2001 and 2006. Due to the short data series, the use of the co-integration, vector autoregressive model (VAR) or the dynamic panel data model, together with their diagnostic tests, are all inappropriate and therefore we resort to utilising a simple static panel data model to estimate the relationship between real estate investment and demographic, economic and planning variables. It is expected that our estimated results will yield important theoretical as well as empirical insights into real estate investment determination in China, which is of specific interest to academics, real estate development company management, financial institutions and policy-makers as well.

3. Model Specification

The aim of this section is to arrive at a set of determinants for real estate investment in the People’s Republic of China. A reduced-form real estate investment equation is specified as a function of change in population, real interest rates, construction costs, floor area of commodity housing sold, housing prices and housing permits. An econometric model is then estimated and formal tests of significance are conducted to determine the uniqueness of the model. Specifically, the estimated equation takes the following form

where, rei it represents the amount of real estate investment completed per 1000 persons in region i during time-period t, inflation-adjusted; Δpop it represents the change in total resident population in region i during time-period t; rr it represents the short-term real interest rates in region i during time-period t; cc it represents the construction cost of commodity housing per square metre in region i during time-period t, inflation-adjusted; hs it represents the gross floor area of commodity housing sold per 1000 persons in region i during time-period t; hp it represents the price of commodity housing per square metre in region i during time-period t, inflation-adjusted; permits it represents the allowable floor area of commodity housing permits per 1000 persons approved by the local governments in region i during time-period t; λ i is the unobserved heterogeneity; a1, …, a6 represent the regression coefficients associated with their respective variables; ε it is the idiosyncratic errors that change across t and i; and represents the natural logarithm of the continuous variables already described.

The static panel data model is then estimated in linear form, together with the use of OLS, fixed effects and random effects respectively. A panel approach has a number of advantages over a single time-series or cross-section method of estimation, for it allows researchers to employ more observations and have a greater degree of freedom. In a fixed effects model, it intends to control for omitted variables that vary among cases but are constant over time and it allows for the use of the changes in the variables over time to estimate the effects of the independent variables on the dependent variable. This is equivalent to generating dummy variables for each case and then incorporating them in a standard linear regression to control for these fixed case effects. Its major shortcoming is that this model employs a large number of dummy variables that use up the degree of freedom.

Alternatively, the random effects model considers the omitted individual specific factors as random variables rather than the constant term. It implies that the unknown region-specific factors are better explained through the error term rather than the constant term. If the omitted variables are fixed between cases but vary over time, then the random effects model should be employed to estimate the relation. This model has a very strong assumption that cov(λ i x i ) = 0, which implies that the intercept terms are not related to the regions’ specific explanatory variables, and the random-effects estimator is a weighted average of fixed and between effects. If the panel data contain data for a very long time-period, both fixed and random effects models should produce similar results.

Hausman (1978) proposes a test based on the difference between the random effects and fixed effects estimates. Since the latter are consistent when λ i and explanatory variables are correlated, but random effects are inconsistent, a statistically significant difference is interpreted as evidence against the random effects assumption (Wooldridge, 2002). While fixed effects always produce consistent results but they may not be the most efficient estimators, random effects will provide better p-values as they are a more efficient estimator. The Hausman test checks a more efficient model against a less efficient but consistent model to ensure that the more efficient model also produces consistent results. It tests the null hypothesis that the coefficients estimated by the efficient random effects estimator are the same as the ones estimated by the consistent fixed effects estimator. If the tests are statistically significant, then it is recommended to use the fixed effects; random effects otherwise.

This section concludes by discussing the a priori expectations for the signs of the coefficients. It is expected that a bigger population increase will raise the demand for commodity housing (residential properties, office, commercial and retail properties, etc), thus making real estate construction by private builders more profitable and boosting real estate investment in turn. It follows that the variable ‘change in population’ should bear a positive sign. Developers are expected to increase the supply of commodity housing when the risk-adjusted spread between expected selling prices and construction costs widens. Hence, wages, material and financing costs have a direct effect on real estate investment as developers will cut their production when the risk-adjusted spread shrinks. It follows that real interest rates and construction costs should have negative coefficients. Housing prices and the sale of commodity housing reflect the business confidence of the real estate market. An escalation in housing prices and/or the gross floor area sold will signal to developers that the general public has confidence towards the real estate market, thus reinforcing developers’ incentives to invest more in the market, other things being constant. In supplement, housing permits can be seen as a government land use constraint which is designed to regulate the real estate market. If the land use constraint is tight (i.e. gross floor area permitted is restricted), then real estate investment will be halted, and vice versa. It follows that this variable should have a positive relationship with real estate investment.

4. Data Description

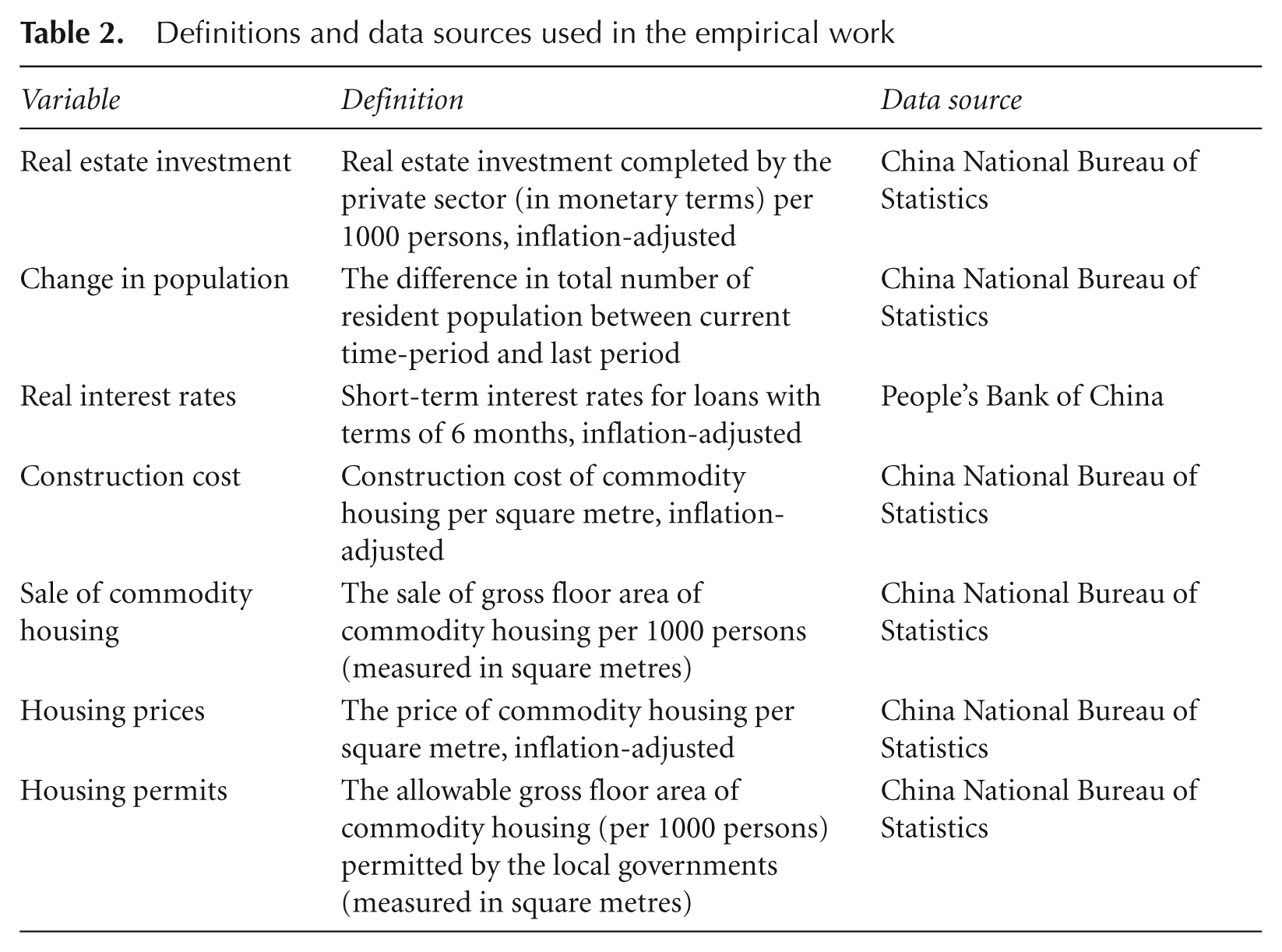

The components of much of the data utilised in this study were collected by and obtained from the National Bureau of Statistics of the People’s Republic of China. These include yearly data on real estate investment, population, short-term interest rates, construction costs, gross floor area of commodity housing sold, the price of commodity housing, gross floor area of housing permits and the regional CPI (see Tables 2 and 3). 4 The data series of short-term interest rates are calculated as a weighted average of interest rates of loans with a term of 6 months. It is collected by and obtained from the People’s Bank of China. 5 All variables are taken for the 2001–06 period, yielding a total of 186 yearly observations. The financial variables are measured in real terms in order to measure the differences in real consumption and investment behaviour. The model is then estimated in log-linear form, with its advantage of reducing the relative size of observations with large variances, especially when a regression includes variables in both level and difference forms.

Definitions and data sources used in the empirical work

Descriptive statistics

5. Empirical Results

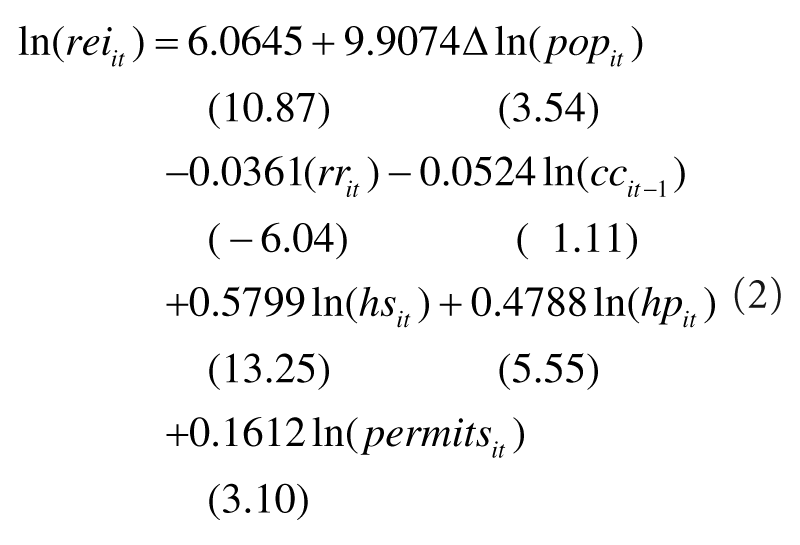

Equation (1) is estimated with the use of OLS, fixed effects and random effects regressions respectively, and the estimated coefficients (along with the t-statistics), goodness-of-fit measures and diagnostic tests appear in equation (2). Since the coefficients on some independent variables are response elasticities, they will be discussed in terms of an anticipated effect of a given percentage increase in the value of the independent variables. The Hausman test (p = 0.0000) indicates that the fixed effects regression is more appropriate for the China model and empirical results based on the fixed effects regression generally keep with the model’s predictions, indicating that the signs of most estimated coefficients concur with what the theories predict, and the independent variables explain approximately 93 per cent of the variations in real estate investment among 31 Chinese regions.

The positive and statistically significant coefficient estimate for change in population is consistent with the notion that a greater demand for commodity housing induced by a growing population will push up real estate prices, thus making real estate investment by developers more profitable. In response to the changing market situations, more commodity housing induced by more real estate investment will be commenced by wealth-maximising developers in a bid to reap the differences between expected selling prices and costs. The coefficient estimate for interest rates is consistent with the theoretical prediction, as it is statistically significant, and bears the expected sign, indicating that developers are less willing to invest in real estate construction when capital accumulation becomes relatively expensive. However, the coefficient estimate for construction costs, which is negative but statistically insignificant, is not consistent with the notion that a higher cost of constructing commodity housing will reduce the profit margins thus restricting such investment by developers. It may be due to the fact that during the period between 2001 and 2006, real estate prices have escalated rapidly across major Chinese cities, with exception of several corrections at different time-periods, and the proportion of construction cost as a percentage of real estate prices has been trivial.

The coefficient estimates for the sale of commodity housing and housing prices are also consistent with the theoretical prediction that their changes can be used to predict a change in real estate investment in the same direction, with an estimated coefficient of 0.58 and 0.48 respectively. These business climate factors contribute to the variations in real estate investment: a 1 per cent increase in the sale of commodity housing floor space/housing prices will bring forth a 0.58/0.48 per cent increase in real estate investment. Turning to the planning regulations, the coefficient estimate of housing permits concurs with the model’s prediction that it is estimated to be positive and statistically significant. It follows that the less stringent are the government land use restrictions, the more will be the amount of real estate investment completed.

6. Policy Implications

In March 1998, a series of housing reforms was introduced to stimulate the domestic economy. Subsidised housing was phased out, while workers were encouraged to spend their savings, alongside lump-sum housing subsidies they received, to purchase their own apartments or pay rents closer to market rates. In August 1999, the government announced that all vacant domestic dwellings built after 1 January 1999 had to be sold rather than allocated. Official figures suggested that over 80 per cent of the allocated public housing in China has already been sold to workers or employees. Hence, it is evident that a new property ownership structure dominated by private ownership and other types of ownership has evolved, due to the institutional changes carried out by the central government. 6

Since then, Chinese real estate markets have experienced tremendous growth, however, in an unbalanced fashion. Real estate investment has been focused mostly on Beijing, Shanghai, certain coastal cities and the eastern part of China. Excessive investment leads to speculative bubbles in these cities/regions, resulting in overbuilding and high vacancy rates there. For example, this type of investment in 2006 ranged from RMB¥0.89 billion in Tibet to RMB¥190.67 billion in Jiangsu, while the price of commodity housing per square metre ranged from RMB¥1708 in Jiangxi to RMB¥8280 in Beijing. The inequalities in real estate investment have led to many socioeconomic problems that directly have adverse effects on people’s quality of life, such as housing shortage, deterioration in housing affordability and reduction in consumption of other goods and services. Based on our estimated coefficients, government policy initiatives to establish a more balanced state of real estate investment should give emphasis to three main policy parameters.

6.1. Population Mobility

Although real estate prices escalated at an average of 9.5 per cent in 70 major Chinese cities in January 2010, the increase was actually more than 50 per cent for big cities, leaving housing virtually unaffordable for many citizens in Beijing, Shanghai and Shenzhen. In order to alleviate economic pressure, Chinese people have started to relocate themselves to second-tier or third-tier cities where housing is more affordable. For example, the price of a 60-square-metre apartment in Xian can be exchanged for a single bedroom only in Beijing (Hu, 2010).

As suggested by empirical evidence, a variation in population change is associated with a variation in real estate investment in the same direction, given the prerequisite that people are allowed to move among cities and regions. Assuming that real estate investment is fixed in the short run, more population flows into one region will lead to a higher level of real estate investment there and at a lower level of investment for the rest of China, ceteris paribus. Hence, a more flexible ‘hukou’ system, 7 which enhances population mobility among cities and regions, may help to equalise real estate investment differentials among Chinese regions in the long run.

6.2. Better Transport

There exist great variations in economic performance and income levels among Chinese regions. Less developed regions, such as north-western China, are undoubtedly associated with poor infrastructure, depriving the local population of educational, social and economic opportunities, and thus widening the poverty gaps. Previous studies suggest that a highway project have different impacts in different phases. During the construction period, it does not only create many job opportunities, but also upgrades the skills of local people employed on the project, while highways promote the development of good production in poor regions, increase trade volume, reduce transport costs and improve social services in the post-construction period (Zhu, 1990). Utilising data for rural China from 1970 to 1997, Fan et al. (2002) suggest that public investment in roads, together with investment in education and agricultural research, reduce rural poverty and regional inequality to some extent. Specifically, road investments contribute to growth in agricultural production (see also Fan and Chan, 2005). Undisputedly, better connections between less developed and highly developed areas established by a road network may help to equalise economic growth between these areas and enhance productivity. While the former effects are usually regional in nature and result from better access to cheaper labour or a larger market, the latter effects may occur within the productivity process, such as cost savings resulting from ‘just-in-time’ methods (National Research Council, 1998).

6.3. Flexible Planning Policy

Previous studies suggest that, while the impact of land use planning has been capitalised into land prices or house prices (Maser et al., 1977; Katz and Rosen, 1987; Cheshire and Sheppard, 1988, 1989, 1995; Ho and Ganesan, 1998; Davis, 2009), planning policies are also responsive to changing market conditions (Bramley, 1993; Lai and Ho, 2001, 2002). Recently, Langlois (2010) sought to ascertain whether urban planning can guide residential development, based on case studies of two towns in Canada. His study uses municipality-wide built-form data, performing before-and-after comparisons for the town of Markham, Ontario, where a New-Urbanist-inspired development philosophy has been effective since the early 1990s. The results are compared with those from the city of Vaughan, an adjacent municipality that has adopted a market-led development approach. His findings suggest that planning is capable of moderately accelerating positive trends and moderately reversing negative trends. Based on our estimated results, planning regulations are highly significant, having an impact on real estate investment. It follows that, while more stringent government land use constraints should be imposed on developed cities and regions where buildable land has almost been used up, more flexible ones should be imposed on less developed cities and regions to attract capital inflows where buildable land is relatively abundant.

7. Concluding Remarks

This paper attempts to identify empirically and estimate the sources of real estate investment differentials among Chinese regions, motivated by previous studies such as Fortura and Kushner (1986), Mayer and Somerville (2000) and Green et al. (2005). Our model explains approximately 93 per cent of the variations in real estate investment among 31 Chinese regions. The demographic factor contributes heavily to this explanation, with an estimated coefficient of 9.91. Empirical estimates also lend support to our treatment of real estate investment as a function of real interest rates, such that rising costs of production reduce the profit margins of investing in real estate construction by developers, hence restricting real estate investment. Surprisingly, the estimated coefficient of construction costs, which is negative but statistically insignificant, is inconsistent with the notion that a higher cost of building commodity housing will make real estate investment less profitable, thus restricting real estate investment by developers.

Furthermore, our estimates also suggest that the estimated coefficients of commodity housing space sold and house prices have been found to cause real estate investment to vary among Chinese regions as a better business climate encourages developers to invest more, but in different magnitudes, with respect to the specific market situations in different regions. Eventually, it is anticipated that private developers will accelerate real estate investment when legal land use constraints on development become less stringent. In this current study, the proxy used for this variable is the gross floor area of commodity housing permitted per 1000 persons within a region. The rationale is that the bigger the area of floor space permitted, the smaller are the government legal land use constraints. Thus, theory would predict that this estimated coefficient should bear a positive sign; and the coefficient of legal land use constraints is consistent with the model’s prediction that less stringent government control over the land use market will increase the level of real estate investment.

These policy parameters are interrelated, making it impossible for the government to handle them one at a time. Each of them tends to interact with and reinforce others, so that comprehensive policies and institutional reforms must be legislated and implemented to accomplish the goals, in respect of changing market conditions. Furthermore, the government must estimate the demand for and supply of commodity housing regularly and accurately, and make appropriate actions to stabilise the fluctuations of such demand and supply. It is also essential for the government to fabricate conditions that allow the private sector to make a full contribution towards satisfying commodity housing demand, while monitoring the real estate market and, if necessary, discouraging property speculation (Mak et al., 2007). In particular, the dynamics of real estate investment would explain why real estate busts tend to go along with economic downturns.

The empirical results provided by this paper should hopefully contribute to an understanding of the Chinese real estate market mechanism. Although our panel data series are short and do not cover a complete economic cycle, our findings still reflect the short-run fluctuations in real estate investment. While our model works well with panel data, it is considered to be applicable to real estate investment equations on both national and regional time-series data. Hence, the directions of future research lie in estimating real estate investment equations using longer panel data series, as well as in the context of national and regional markets.

Footnotes

Notes

Acknowledgements

The authors have benefited greatly from careful review and thoughtful suggestions by four anonymous referees. They also thank the Hong Kong Polytechnic University for the research grant and financial support for this research project (PolyU Research Grant 1-ZV4Q). The authors are, of course, responsible for the content.