Abstract

The turn of the 21st century saw two important pieces of legislation introduced in Brazil: the Law of Fiscal Responsibility or LFR (2000) and the City Statute (2001). While each law has been celebrated, this article argues that a perversion of their intentions is emerging in practice. The scale and scope of municipal budget composition and allocations in the period studied (1995–2010) give reason to question how these landmark laws are being locally interpreted. Evidence details a disproportionate rise in current expenditures in all state capitals in Brazil since the introduction of the LFR. Further, among state capitals with the largest number of ‘sub-normal agglomerations’, a few key cities show a peculiarly stagnant proportion of expenditures directed towards housing and urbanisation. A case study of São Paulo is presented to explore explanations for these trends and understand what they mean for the direction and control over upgrading investments in that city.

1. Introduction

Struggles to balance budgets in the aftermath of recent financial crises are defining fiscal policies in the global North and South, and at national and municipal levels. Emerging in the wake is an increasingly prominent technocratic movement within policy-making institutions whose rallying cry is ‘fiscal responsibility’. Fiscal responsibility legislation first emerged in the mid 1990s and has variant forms around the globe. In 2000, the Law of Fiscal Responsibility (LFR) was introduced in Brazil, ushering in a regime of fiscal mandates for all levels of government from municipal to federal. Brazil’s LFR represents a hybrid case of fiscal reforms, including procedural rules (which are typical in high-income countries and emphasise accountability) and stringent numerical rules (which are spending-related targets more common in lower- and middle-income countries) (Corbacho and Schwartz, 2007). Indeed, the Brazilian example is often referred to within recent fiscal policy literature as the paradigm of how to design national LFRs and successfully introduce greater fiscal discipline in the overall public sector (Kumar and Ter-Minassian, 2007; Corbacho and Schwartz, 2007; Crivelli and Shah, 2009). Nonetheless, in an age of decentralised responsibilities, it is also especially important to understand how the LFR interacts with municipal mandates and local governance.

It is thus of interest that around the same time the LFR was implemented, the Brazilian federal government also passed the City Statute, legislation which had been fought for since the ratification of the national Constitution in 1988. The highly anticipated and negotiated statute—enacted in 2001—outlines the social responsibilities and powers of municipal governments in serving urban populations. Its roots lie in the advocacy work of the national urban reform movement, which shaped the democratic assemblies drafting the Constitution in the late 1980s (Avritzer, 2009, p. 142). The Constitution itself—representing a major democratic rebalancing of governance structures post-military regimes in Brazil—specifically shifted power towards the most local levels of government. The themes of decentralisation and participation loomed large in the document and, as a result, cities in Brazil gained more discretion, autonomy and responsibilities in the fiscal sphere as well as for service delivery and local legislation (Baiocchi, 2003a, p. 9). However, it was the City Statute that explicitly inserted wording on the ‘right to the city’ via appropriate social housing and concessions ensuring that cities could use private property to serve social functions (Avritzer, 2009, p. 168).

Much like the LFR, the City Statute has been celebrated internationally, particularly among urban champions and housing advocates. Yet, early on, high-level representatives from the Brazilian Ministry of Cities voiced anxiety about how the statute’s objectives would interact with the LFR’s. They were especially concerned with the impact of a primary budget surplus target, 1 fearing that this figure could be set too high and thus inhibit investment. 2 Municipalities needing to make major public investments in social housing and upgrading ran the risk of not achieving their mandated surplus target because such investments could not be depreciated and would sit heavily on their budgets. These concerns laid the foundation for this study of the record of municipal spending (particularly on upgrading) since the combined introduction of the LFR and City Statute.

1.1 Methods and Organisation

As a starting point for this examination, this article begins with a review of fiscal policy literature concerned with how budgets (or fiscal space) are determined and leveraged for development projects—both overall and specifically in Brazil. This is followed by a comparative analysis of National Treasury data on municipal current and capital expenditures for all state capitals in Brazil for a 15-year period encompassing the introduction of the LFR and City Statute. Specifically to capture the budgetary challenges of municipal upgrading operations promoted by the City Statute, highlighted within this group of state capitals are five with the largest number of irregular or vulnerable settlements, what the Brazilian National Population Census 2010 calls ‘sub-normal agglomerations’. These sub-normal agglomerations include “favelas (slums), invasões (invaded properties), grotas (slums in deep valleys), baixadas (slums in low-lands), comunidades (poor communities), vilas (slums in villages), ressacas (slums in backwaters), mocambos (type of shack) and palafitas (stilt houses), among other irregular settlements”. 3 In this paper, the number of sub-normal agglomerations is used as a proxy to estimate the importance and relative scale of upgrading investments required.

The comparative analysis is followed by a more in-depth case study of municipal budget trends in the capital city with the largest number of sub-normal agglomerations and perhaps one of the most infamous pre-LFR fiscal records—São Paulo. 4 Detailed empirical data on the city of São Paulo were gleaned from that city’s financial statements from 1995 through 2010, a period for which data were available at the archival library of São Paulo’s Secretary of Finance. Quantitative data are supplemented by information gathered during two trips to Brazil (one in 2005 and another in 2006) for meetings with the Ministry of Cities, attendance in local public meetings on housing in São Paulo, as well as for interviews with technical staff and experts serving in the administrations of São Paulo mayors Marta Suplicy (2001–04), José Serra (2005–06) and Gilberto Kassab (2006–present). Throughout fieldwork in São Paulo in particular, special emphasis was placed on understanding how the City Statute’s municipal-level promotion of investment—especially in slum upgrading—was interacting with the new fiscal regime of the LFR.

Potential rationales behind expenditure trends identified both in the nationally comparative and São-Paulo-specific data are explored in this paper’s final discussion. That section focuses on understanding the implications of the presented analyses of categorical composition and sector allocation trends in municipal budgets studied, as well as the growing presence of alternative financial resources for upgrading. The article argues that, despite the intentions of the legislative environment created with the LFR and City Statute, in practice municipal leaders—in this study, particularly in São Paulo—are still able to shift away from fiscal and social responsibilities.

1.2 Creating and Maintaining Fiscal Space for Development

Fiscal ‘space’ (or budget allocations) and fiscal ‘responsibility’ (or generally budget expenditure constraints) tend to represent opposing sides of the same fiscal policy coin. Among development scholars, there are two diverse bodies of fiscal space literature—one concerned with the management of extant public finances and the other concerned with how to mobilise and increase such funds. A wide field of political economists and scholars concerned with fiscal space have long examined the role of power in public finance allocations, including interagency and sub-national competition for funding, the role of capitalist interests therein, lobbyists, or collective action in securing public investments for different projects. Such arguments have been expertly applied to Brazil in critical studies of land reform, social mobilisation and the development of an urban policy platform since the end of a military regime and return to democratic government with the 1988 Constitution (Kowarick and Bonduki, 1994; Fernandes, 2002, 2007; Saule, 2002; Marques and Bichir, 2003). Public management research has also contributed to this knowledge frontier, with works on Brazil including examinations of governance systems (for example, decentralisation) as well as government efficiency and effectiveness in the management of public funds and services, particularly vis à vis the private sector (Geddes, 1993; Tendler, 1997; Bresser Pereira, 1999; Aghón et al., 2001). Finally, planning scholars add to the discussion of how best to manage extant fiscal resources through the question of how best to channel funding to targeted development needs. Brazilian studies in this branch include those on participatory planning/advocacy and the growth of participatory budgeting, as well as more specific attempts to define ‘best practice’ in managing social investment projects like, for example, slum upgrading (Amaral, 2002; Baiocchi, 2003b; Cabannes, 2004; Budds et al., 2005).

Fiscal policy scholars concerned with securing greater public financial resources instead write about the depth and effectiveness of banking systems and capital markets, taxation and public institutions at the sub-national level (for Brazilian and Latin American studies, see especially Smolka and Furtado, 1996, 2001). Another area of significant research on building up public financial resources for development connects with debates regarding the role of international aid, globalisation and trade in the developing country context. Recent work in this area is not concentrated on upper-middle-income countries like Brazil because it mostly examines the effectiveness of budget aid for economic development as well as different strategies of economic growth (for example, export-led, state interventions). The aforementioned schools present non-exclusionary explanations of how and why fiscal space is created and/or allocated at national or sub-national levels. However, such explanations concentrate on the identification of political will or agent capacity to create fiscal space for development rather than on which management tools and policies may be enabling the political-economic rationalisations used. This latter line of inquiry is explored in this article’s case study.

1.3 Municipal Budgets by Category Composition and Allocation

The categorical (i.e. current or capital) picture of municipal expenditures is important in evaluations of the ‘development orientation’ of budgets. First, this is because it demonstrates how much of a budget is dedicated to short-term spending on recurring costs (current) like personnel as opposed to longer-term spending on required investments (capital) like public infrastructure. Secondly, capital expenditures are generally seen as having a lasting positive impact on economic productivity, as opposed to current expenditures. Hence, expenditure data characterised by category were examined for all 26 state capitals in Brazil, as a politically important and regionally distributed subset of municipalities.

To test for whether there was a statistically significant association between the LFR’s implementation and municipal budget expenditures, two sets of analyses were conducted. First, a pooled cross-sectional analysis with capital expenditures as the dependent variable was conducted using a LFR dummy variable equal to one after 2000, as well as municipal fixed effects to control for non-time-varying heterogeneity across state capitals. This analysis was then repeated for current expenditures. The results indicate a positive, statistically significant relationship between the implementation of the LFR and current expenditures (p-value = 0.01) for all state capitals. While there was not a statistically significant relationship between capital expenditures and the LFR’s introduction (p-value = 0.20), the coefficient was negative, indicating a downward trend in capital expenditures across all state capitals since 2000.

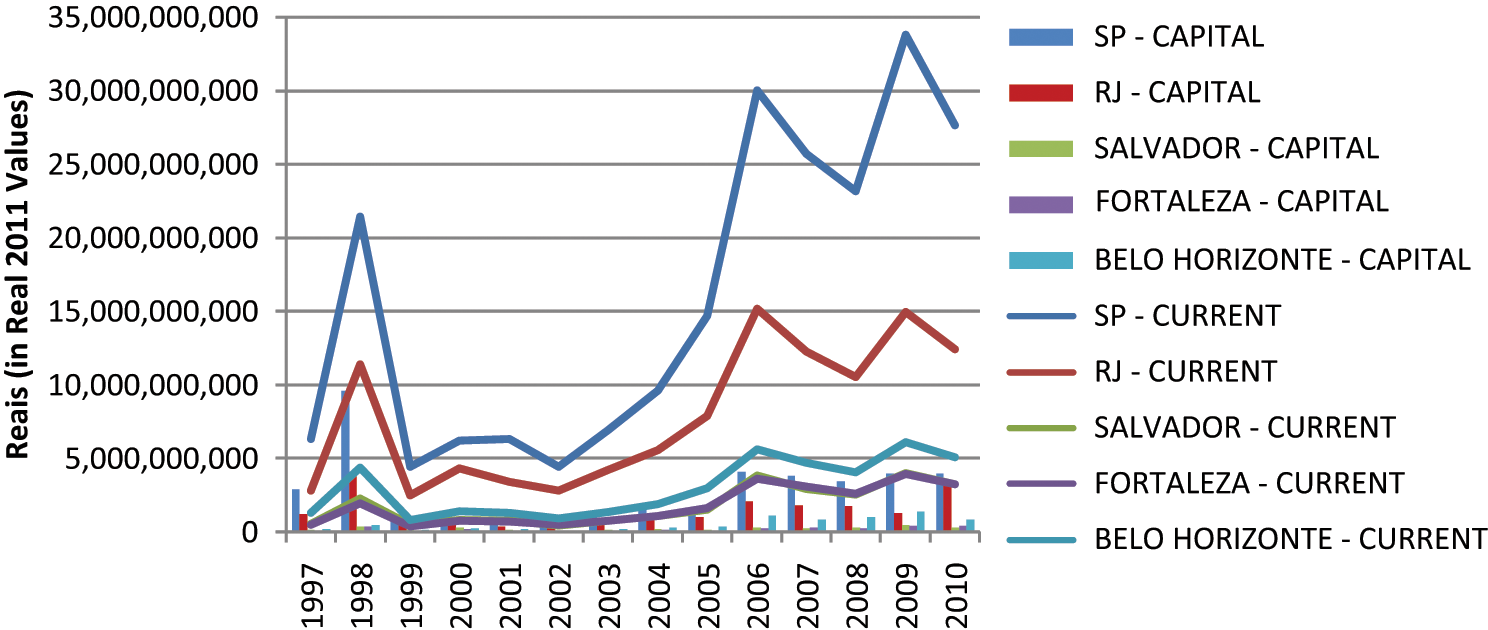

This post-LFR divergence trend between the two expenditure categories is notable among state capitals with the largest upgrading challenges (as well as populations and revenues), shown in Table 1. A more detailed account of trends among these state capitals shows that the growing gap between current and capital expenditures is largely attributable to sharper growth in current expenditures, as substantiated by statistical testing. Figure 1 visualises how this gap between current expenditures (represented by the line graph) and capital expenditures (represented by the bar graph) has widened.

State capitals by population, sub-normal agglomerations and revenues

Sources: IBGE, citing figures from the 2010 Population Census; Secretaria do Tesouro Nacional, Finanças do Brasil: Receita e Despesa dos Municípios (1997–2001); Finanças do Brasil: Dados Contábeis dos Municípios (2002–2010).

Current and capital expenditures among state capitals with largest number of ‘sub-normal agglomerations’, 1997–2010.

The rise of current expenditures (and revenues) among these state capitals, coupled by the relative stability of their capital expenditures over the same period, is peculiar for a few reasons. One of the explicit objectives of the LFR is to curb outsized current expenditures—for example, by mandating that personnel spending be less than 60 per cent of a city’s current revenues. Thus, trends showing instead an increased tendency in municipal budgets towards current expenditures are worth studying in evaluations of fiscal ‘responsibility’. Also, public investment needs at the municipal level in Brazil are large and require further capital investment, as promoted by the City Statute. Although some studies note that municipalities in Brazil already account for roughly 40 per cent of Brazil’s total public-sector investment (Afonso and Junqueira, 2009; Vetter and Vetter, 2011), these expenditures are not sufficient to cover the infrastructure requirements estimated for Brazilian cities (World Bank, 2006; Vetter and Vetter, 2011).

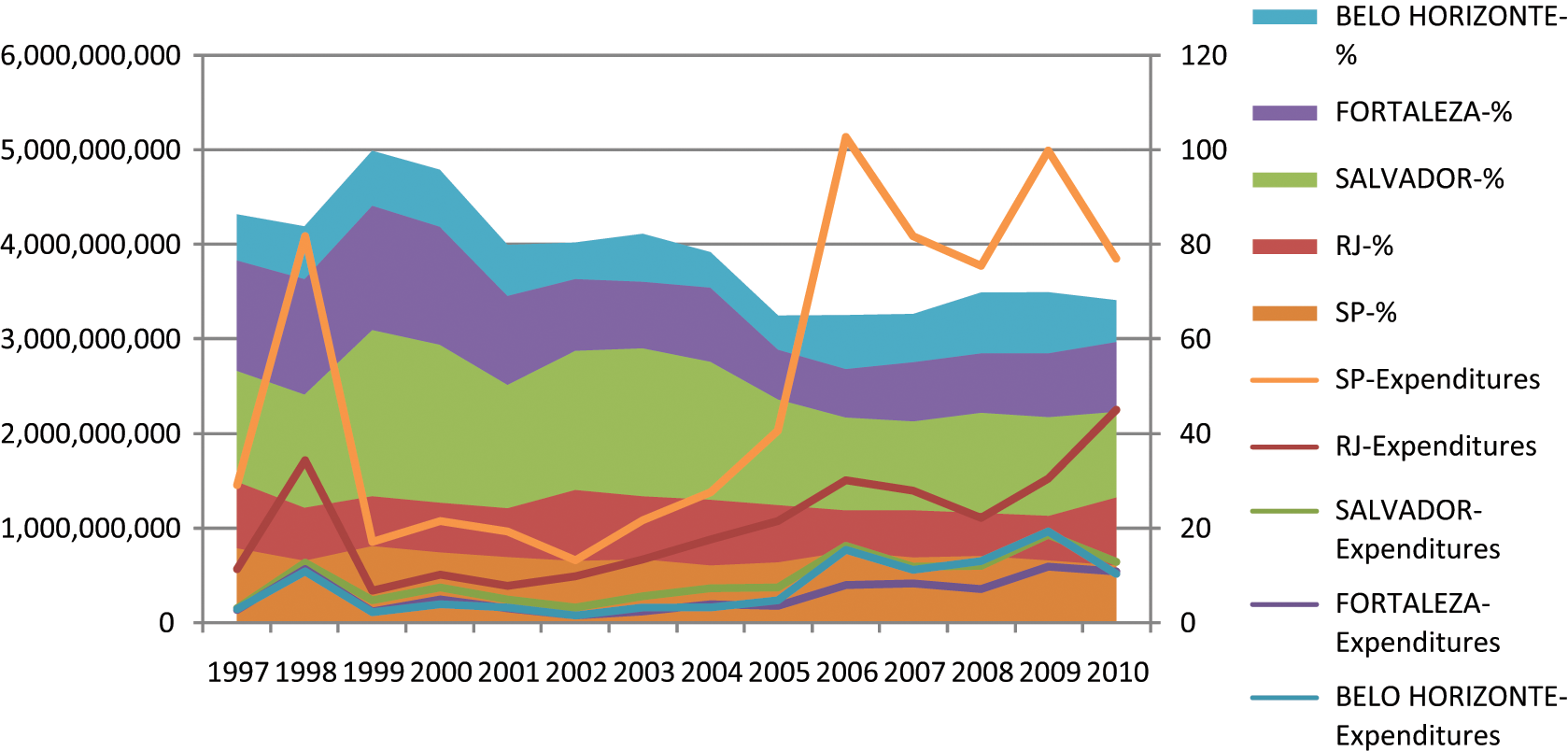

Nonetheless, an examination of sector spending surprisingly shows that housing and urbanisation expenditures (both current and capital), as seen in Figure 2, generally increased in real 2011 reais among the same aforementioned state capitals since the LFR was introduced. However, there is unexplained variation here. While absolute spending rose in São Paulo and Rio de Janeiro—cities with the largest number of sub-normal agglomerations—their percentage spending on housing and urbanisation generally did not, showing more stability than in Salvador, Fortaleza or Belo Horizonte since the LFR was introduced.

Housing and urbanisation expenditures: real 2011 reais and percentage of total expenditures among state capitals, 1997–2010. Notes: real 2011 reais values are plotted against the left-hand vertical axis; percentage figures are plotted against the right-hand vertical axis.

In summary, data show that current expenditures in state capitals across the board have increased substantially since the introduction of the LFR and the City Statute. However, sector-specific expenditures—focusing on housing and urbanisation here—show peculiar variation among state capitals. Given the promotion of investments in urban development created by the City Statute, the push to control current expenditures under the LFR and the general increases in revenues seen in Table 1, these trends appear counter-intuitive. In order more fully to understand what is happening, particularly where because of the large number of sub-normal agglomerations (and populations therein) a larger percentage of the municipal budget might be expected to fall on housing and urban development, the rest of this article looks more deeply into explanations for these trends in the leading city of São Paulo.

2. São Paulo’s Path

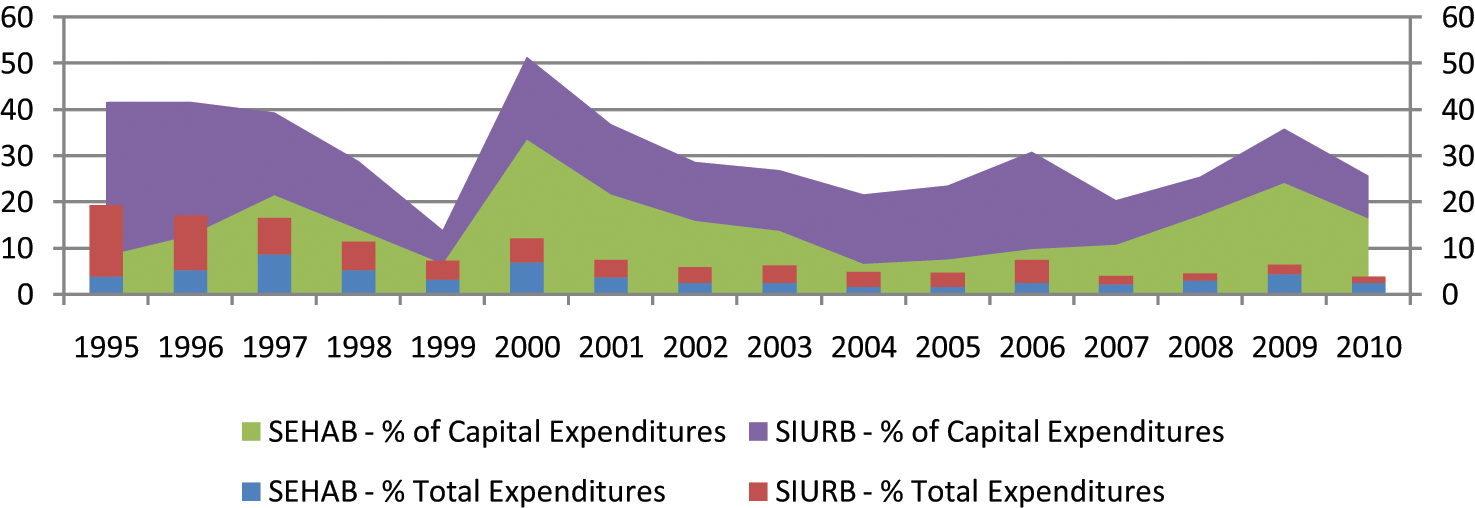

Even after the introduction of two influential pieces of federal legislation that sought to increase cities’ capital investment in housing and urban development (City Statute) and to curb outsized current spending (LFR), São Paulo’s major agencies working on slum upgrading—the Secretary of Housing, or SEHAB, and the Secretary of Urban Infrastructure and Works, or SIURB 5 —saw their budgets decrease to well below 10 per cent of overall expenditures. These same agencies historically have had the largest and most consistent percentage of their budgets allocated to capital expenditures, representing 20–50 per cent of the city’s capital expenditures for most years under study (See Figure 3).

SEHAB and SIURB capital and total budgets as a percentage of city totals, 1995–2010.

SEHAB and SIURB’s work portfolios help to explain the relative importance of their capital expenditure budgets. SEHAB has been involved in upgrading work since its inception in 1977. It houses two sub-secretaries working specifically on upgrading, the Superintendência de Habitação Popular (HABI) or Superintendent of Popular Housing (which targets populations only making up to six times the national minimum monthly wage) and the Departamento de Regularização do Parcelamento do Solo (Resolo) or the Department of Land Parcel Regularisation. SEHAB’s portfolio has included improvements to, or new production of, housing for low-income households, neighbourhood environmental improvements and the regularisation of land to facilitate basic service provision. However, the agency’s work portfolio has shifted over the past 15 years and ‘urban development’ technically has fallen out of its agenda—and title. It is in part for this reason that here the work programme of SIURB is also studied. SIURB organises urban development projects on roads and public spaces, as well as repair and maintenance work on buildings and public infrastructure (roads, drainage, etc.).

The combined picture presented in Figures 2 and 3 indicate that, while São Paulo’s housing and urban development sector spending is stable overall, it is shifting away from municipal-agency-led capital investments. Surprisingly, this occurred despite an overlap in timing with federal mandates for decentralised responsibility and transparency as well as an overlap with former Mayor Suplicy’s leftist municipal administration (2001–04). Given the scale of required upgrading investments in São Paulo, what explains this trend and is it related to the LFR’s mandates, as originally feared by the Ministry of Cities?

2.1 Budget Composition: Accounting for Political Choices

When the LFR was first introduced in Brazil, city mayors had serious objections to the potential impact that the tight numerical rules shaping fiscal policy would have on their budgets. 6 The National Front of Mayors (Frente Nacional de Prefeitos) organised several meetings and lobbied against a number of the LFR’s mandates, including what was considered the privileging of spending on internal fiscal investigations over spending on social needs (Bragon, 2001). Even a year after the LFR was passed into law, a document (‘Carta de Brasilia’) delivered to then President Fernando Henrique Cardoso on behalf of 3000 city mayors asked for amendments to the strict numerical rules of the LFR, which were attributed to the country’s panning to IMF demands (Serafim Abrantes, 2001). Numerical rules nonetheless remained a mainstay of the LFR programme. In a study conducted in 2004 by one of the leading newspapers in the country, Folha de São Paulo, 80 per cent of all Brazilian cities (excluding capitals) were cutting services in order to meet the LFR’s numerical fiscal rules before the end of the year (Freire, 2004). Policy-makers cited the law as reasoning for cuts and limits on spending, particularly for social services and infrastructure projects (Simionato, 2001; Credendio, 2006; Folha de São Paulo, 2006).

The political utility of affording blame for service cuts on the LFR is clear; however, there are also some technical reasons why the numerical rules promulgated under the LFR regime could especially impact capital investment projects, as explicitly recognised in recent public-sector accounting resolutions in Brazil. 7 With the rise of fiscal responsibility mandates—especially those including numerical targets as under the Brazilian LFR—how (and when) accounting practices record transactions increasingly impact a government’s real and perceived fiscal health (Premchand, 1995) and thereby its access to financial resources. Although accounting practices do not create fiscal space independently, they provide the base data used in the calculation of fiscal indicators, the preparation of financial reports and the proposal of yearly budgets, all of which have become increasingly relevant in Brazil under the LFR.

Brazilian political figures have long understood the political and economic importance of accounting. In 1964, right before the installing of military rule, new public-sector accounting guidelines were introduced in an attempt to centralise control of government spending (Poubel de Castro and Garcia, 2004). Federal law no. 4.320 required that government entities record revenues on a cash basis, to stop overestimation of revenues; for public expenses, it mandated the practice of modified accrual accounting to ensure that expenditures were recorded immediately in accounts rather than only when purchased services or products arrived. 8 This created a double coating of protection against spending (Angélico, 1994, p. 114). Only at the end of 2007 (and thus not yet impacting the budgetary trends presented here) was a new accounting rule mandating accrual accounting to record receipts and expenses finally approved by the Brazilian Congress. 9

Given accounting’s historically political utility in Brazil, it is not surprising that municipal policy-makers recently pointed to the LFR regime—which ultimately depends on data derived from accounting practices—as a negative influence on their budget capacities. For the purposes of this article, it is, however, more useful to explore precisely how accounting practices can technically impact budgets and political rationales behind their composition. What follows is a simple exercise in changing the basis of accounting systems used in a random year.

If a full-accrual basis of accounting were utilised in Brazil, for example, São Paulo’s capital investments would be annually depreciated and the city’s Statement of Revenues and Expenses would show a different (i.e. lesser) amount under capital investment expenses in a given year. In a sample year (2003), capital investment expenditures for two of São Paulo’s largest slum upgrading programmes included R$14 987 268 for upgrading loteamentos (sub-divisions on private land) and another R$45 988 000 for upgrading favelas (settlements on public land), totalling R$60 975 268 or 35 per cent of SEHAB’s overall capital investments (PMSP, 2003). If even just these two slum upgrading capital investment projects were depreciated using a simple straight-line method, instead of recording R$60 975 268 in capital investment expenditures in 2003, the city of São Paulo would have recorded R$2 032 509—a difference of R$58 942 759. 10

The surplus amount in this sample exercise only amounts to 0.6 per cent of the city of São Paulo’s 2003 revenues. However, as the primary budget surplus mandated within the programming established by the LFR is calculated on a consolidated (federal, state, local) government basis, this amount can actually influence the achievement of the mandated surplus target. For example, Brazilian municipalities contributed only 0.1 per cent to the overall consolidated primary budget surplus, with federal government contributing 2.6 per cent, states 0.8 per cent and public enterprises another 0.9 per cent, for a total primary budget surplus of 4.4 per cent in 2004 (Afonso and Araúju, 2004).

In short, the accounting system used can provide technical rationalisations and disincentives for large capital investment expenditures in any one particular year. As opposed to other spending, when capital expenditures are fully recorded in a city’s account in one fiscal year instead of being depreciated over time, a cut in capital investments can represent a quick fix to budgetary shortcomings. A sell-off of capital projects may be thus rationalised when policy-makers need quickly to adjust budgets to meet annual numerical fiscal targets. While this is not an unknown observation in the accounting literature, little attention is paid to such incentives emergent from the interaction between accounting practices and numerical fiscal rules within urban development or planning scholarship. A combination of numerical rules and accounting practices that prohibit depreciation of capital investments can—as seen in Brazil—provide a technical rationale and political incentive to reduce discretionary capital expenditures that leaders have little or weak pressure to fulfil during their tenure. Furthermore, this reality can have a special impact on who leads urban development. Government agencies with typically large capital investment projects are especially sensitive to accounting practices. However, while technical rules can help to explain the political rationale behind agency budgets and budget category composition trends showing a disproportionate rise in current expenditures, they do not fully explain the rationales for the previously identified housing and urban development sector allocation trends. In the next section, the role of alternative non-agency-led funding for upgrading in São Paulo is considered as an explanatory variable for why the percentage of its municipal budget allocation to housing and urban development has remained largely unchanged since 2000.

2.2 Budget Allocation: Who’s Account(ed/able) for Upgrading Investments?

In São Paulo, the leftist Workers’ Party (or PT) held the mayoral office from 2001 to 2004. During this time, SEHAB used over 95 per cent of its allocated budget (for example, in 2001, 2002 and 2003). This percentage of budget allocations executed can be understood as a proxy of political will for municipal-agency-led programming and capital investments in upgrading. In other years—namely, when PT was not in power—SEHAB typically executed lower percentages of its allocated budget. Yet, despite SEHAB’s higher percentage budget execution under the PT administration, it is also during the PT tenure that a drop-off occurs in SEHAB’s budget allocation relative to other agencies. Here then it is worth exploring the co-existence of a climate of political will (represented by both PT and the City Statute), the stability of housing and urbanisation sector spending levels, and the relative decline of budget allocations to agencies like SEHAB or SIURB.

Some scholars note that such contradictions are in fact typical of politics in São Paulo, where acute political struggles between the left and right are consistently played out in policy implementation. For example, Avritzer (2009, p. 78, p. 150) notes that, although under the PT administration of Marta Suplicy participatory institutions embracing the spirit of the City Statute were introduced, these efforts were checked by the well-organised conservative and centrist opposition groups in São Paulo which often nullified proposals or forced negotiations in certain sectors that contradicted PT’s participatory and pro-poor platform.

Another explanation for the relative decline in agency budgets for upgrading is a counter-balancing increase in investments from other sources. For example, the federal government’s investments in upgrading through the provision of low-income housing have been facilitated through a special fund—the Fundo de Garantia por Tempo de Serviço or FGTS—which is a national social security fund constituted by the compulsory contribution of a percentage of a worker’s salary. 11 This percentage is placed under the employee’s name into a bank account which bears interest. The funds can be withdrawn by workers seeking to acquire housing, or by those who no longer work. A difficulty with regard to the use of these funds for upgrading, and the specific provision of low-income housing therein, is that these funds require full-cost recovery in lending operations, as they are workers’ social security as opposed to government-owned resources. Hence, the use of FGTS funds to serve the lowest-income segment of the population’s housing needs has proven largely unfeasible. Since the 1970s, the programme expanded its targeted population from households earning up to three times the monthly minimum salary to households earning five to ten times the monthly minimum (Valença, 1992; Cymbalista and Moreira, 2002). Yet in São Paulo, for example, just over 70 per cent of the population living in precarious housing were in the lowest income bracket in 2000, earning only up to three times the minimum monthly salary (Pochmann, 2005). As will be shown, this last point is critical.

At the state level, there is a major housing and urban development company, the Companhia de Desenvolvimento Habitacional e Urbano do Estado de São Paulo, or CDHU. Records show that CDHU’s work specifically targets low-income families earning less than 10 times the monthly minimum salary in Brazil and, since 2000, it has indeed delivered 49 419 housing units specifically within the city of São Paulo. 12 This is more than it produced in the five years preceding 2000, which amounted to 31 653 housing units. However, estimates from the Centre for Studies of the Metropolis and a sample survey from the Fundação SEADE indicate that 378 711 more people live in the city of São Paulo’s favelas alone (i.e. not accounting for the population in loteamentos, cortiços, or on environmentally vulnerable land) since the year 2000 (Cities Alliance and SEHAB, 2009, pp. 26–27).

In addition to federal and state-level alternative resources for upgrading, since the year 2000 the relative importance of earmarked funds (as opposed to allocated city agency budgets) in the city of São Paulo has grown (Rossetto 2003). One former financial administration co-ordinator at SEHAB explained that a plethora of earmarked funds emerged post-LFR so as to avoid the increased political budgetary struggle for allocations fought out between the city executive branch and the São Paulo city council. 13 It is then not surprising to see the relative growth of an earmarked fund dedicated to funding urban development projects (FUNDURB) and an earmarked fund dedicated to the upgrading and production of housing in São Paulo, the Fund for Municipal Housing (FMH) (see Figure 4) in the years following LFR’s introduction. The FMH monies are managed by the Municipal Housing Council (MHC), created by law in 1994. The fund is comprised of a share of the city’s tax transfers from state and federal governments, in addition to revenues from the sale of properties built with public funding, as well as private donations and grants. Unlike city agency budgets, the FMH’s budget can be carried over to subsequent years.

Relative composition of housing-related agency and earmarked funding, 1995–2010.

The creation of the MHC and FMH is tied to the popular protests for housing and is an offspring of an earlier popular housing fund which began in 1979 (Cymbalista and Moreira, 2002). The MHC’s institutional structure is meant to facilitate the participation of community stakeholders, particularly low-income housing associations from vulnerable settlements. FMH-funded projects, like the federal government’s FGTS-funded projects, serve a population with up to 10 times the monthly minimum salary. This contrasts with SEHAB’s dedicated favela-upgrading sub-agency, HABI, which must target populations only making up to six times the monthly minimum salary. The FMH is also not governed by the same rules as SEHAB when contracting out projects to third parties and thus does not have to award contracts to the lowest bidder (Rossetto, 2003). Finally, even though community representatives account for 16 out of the 48 members—or one-third—of the MHC, only one-third of the membership actually have to be present for a meeting to have a quorum. The other members of the MHC include other civil society groups like real estate development players (for example, real estate professionals, lawyers, architects and construction firm unions) and government representatives from the city, state and federal levels. Thus, a quorum for meetings can be achieved without the presence of community representatives. 14

The more recent growth of FUNDURB is linked instead to São Paulo’s notable success in raising revenues for urban development by tapping into private-sector construction. Two value-capturing tools have been effective in increasing the city’s revenues: one charges for additional construction rights (or OODCs) and the other involves the auction of certificates of additional construction potential (or CEPACs). Only the OODC charges are fed into the FUNDURB, but both tools have been criticised for facilitating a concentration of investment in areas of São Paulo already of interest to the real estate market, thus aggravating inequalities in investment distribution (Fix, 2003). Furthermore, as Sandroni (2011) recently noted, the fees collected from OODCs and CEPACs are limited-time gains. Such revenues and their use in upgrading projects cannot sustainably or adequately replace the more predictable work programmes of municipal agencies dedicated to upgrading projects. As of September 2008, for example, only 18 per cent of project funding from FUNDURB went to the regularisation of informal settlements (Sandroni, 2011). This makes some sense given that the fund is administered by the Secretariat of Municipal Planning, whose mandate is not limited to addressing the challenge of sub-normal agglomerations alone.

In summary, as reliance on the FMH and FUNDURB grows, the lowest-income segment of the population suffering from housing deficits (which as noted earlier is the largest in São Paulo) is too easily neglected. The targeted household-income population for FMH investments and the project mandate for FUNDURB both aim wider than targets for SEHAB (and in particular HABI). In addition, participation from interested community groups can be effectively shut out of decision-making through earmarked funds. A recent study from POLIS—a well-known research institute in São Paulo—corroborates this concern with the transparency and effectiveness of earmarked funding, particularly in regard to addressing the needs of the lowest-income residents in precarious settlements (Freire Santoro et al., 2007). In short, these alternative paths of or to public investment in upgrading can create new vulnerabilities, especially for households in the lowest income bracket who are most directly targeted by SEHAB’s HABI mandate alone.

3. Perverting Intentions of ‘Responsibility’

The data presented in this article suggest that a combination of the LFR’s numerical fiscal rules and extant accounting practices, as well as the growth of alternative financial resources, can together explain the political rationales behind trends in municipal budget categorical composition (i.e. current and capital expenditures) and allocation (i.e. sector-based expenditures) for housing and urbanisation investments in São Paulo during the period studied. However, while studying trends in what actually happened can reveal rationales behind decisions made, it is also worthwhile to consider briefly what did not happen within municipal fiscal frameworks during this same time-period. A published interview with former São Paulo Mayor Marta Suplicy gives insight into this perspective.

Speaking with the newspaper Folha de São Paulo after her tenure as mayor, Suplicy argued that the powerful conservative élites in São Paulo rallied against paying any increase in their property tax and against paying a small waste management tax to build a landfill, and yet paid more money to have a television subscription every month (Folha de São Paulo, 2004). When asked about what she would have done differently as mayor, Suplicy answered that she should have reformed the property tax to make it more progressive, and regretted that she failed in communicating the rationale for this to the public.

Political resistance to increasing the municipal tax-base by raising property taxes is clearly a fundamentally important influence on why municipal budgets look the way they do in composition and allocation. Vetter and Vetter (2011) note that half of the top fiscal performers among the Brazilian cities they studied had a real estate property tax to GDP ratio lower than that in the average developing country. In other words, more effort could be made by Brazilian cities to increase fiscal space for investments through raising real estate taxes and fees, which represent a fairly predictable and long-term source of municipal revenues.

São Paulo is a case study in the avoidance of unpopular tax increases. Instead of using tax reforms to increase fiscal space for development, the city’s leaders have increased reliance on alternative financial resources and have even successfully lobbied to increase the numeral fiscal limit on spending in 2007 (Folha de São Paulo, 2007). While loosening fiscal rigidity and engaging the supramunicipal public and private sectors can bring further revenues required for investment to cities, this is not the direction of control intended by the Brazilian Constitution, the City Statute or the LFR. This legislation places a premium on participation and the decentralisation of decision-making processes to the most local level of government. Furthermore, the shifting of responsibility for upgrading and of power over investment decisions allows city leaders to avoid politically unpalatable but important fiscal reforms, as intended by the LFR. Instead of promoting responsibility, the political environment created in practice in the wake of the LFR and City Statute’s introduction has witnessed perversions of the ‘responsibility’ intentions behind both pieces of legislation.

Footnotes

Acknowledgements

The author wishes to thank many colleagues in São Paulo who facilitated this research, but especially Paulo Teixeira, Andre Leonardi, Orlando de Almeida and Violeta Saldanha Kubrusly. The author is also greatly indebted to this journal’s Editor and anonymous referees, all of whose comments and feedback on ideas presented here were invaluable. In addition, very special thanks go to Marissa King and Samantha Swerdloff for sharing their time, insights and suggestions for how to improve the paper’s analysis and presentation.

Notes

Funding Statement

This research received no specific grant from any funding agency in the public, commercial or not-for-profit sectors.