Abstract

Prior studies suggest that homeownership positively impacts on social capital formation. However, many studies find it difficult to control adequately for selection effects in the form of factors, some of which may be unobserved, that encourage both homeownership and investment in social capital by households. A biennial survey conducted in New Zealand cities provides data that enable the control of such selection effects with propensity score matching methods, while also benchmarking the results by means of regression methods. The results confirm that homeownership exerts positive impacts on the formation of social capital. At the same time, homeownership demands greater accountability of local government and leads to reduced satisfaction with local government performance, thereby negatively impacting on community social capital. Hence these two dimensions of housing-related social capital work in opposite directions from each other, a finding which has not been previously observed.

1. Introduction

Homeownership has increasingly attracted the attention of researchers and policy-makers as interest in the impacts that such investment has on outcomes for regions and individuals grows. Recent studies have attempted to measure whether there are benefits to homeownership, such as improved outcomes for children (Aaronson, 2000; Mohantly and Raut, 2009; Haurin et al., 2002), for immigrants (Sinning, 2010), crime (Sampson et al., 1997), labour markets (for example, Borjas, 1985; Oswald, 1996) and general wellbeing (Cobb-Clark and Hildebrand, 2006).

Many of these benefits relate to community interaction boosting social capital (Putnam, 2000). The theory behind this relationship is that when someone purchases a home and becomes the owner-occupier, this investment reduces geographical mobility due to the transaction costs associated with a subsequent move. Moreover, if resale is desired at a future date, the owner-occupier will endeavour to act in ways that maximise the future net return. Longer duration of residence plus concern regarding the dwelling asset value increase the incentive for an individual or family to invest in their community, through engagement in local decision-making (Boehm and Schlottmann, 1999) as well as through interactions with other members of the community (networks) and through participation in community activities (DiPasquale and Glaeser, 1999; Glaeser et al., 2002; Sampson et al., 1997). As well as the pecuniary benefits of investing in social capital, homeowners may experience improved intrinsic returns to homeownership as a result of community investment including increased sense of belonging, control over their home environment and ontological security (Saunders, 1989; Dupuis and Thorns, 1998).

Working against these positive benefits of homeownership for social capital accumulation is the argument from Oswald (1996) that the reduced geographical and labour mobility associated with homeownership raises unemployment, which in turn may have a negative impact on social capital. However, the evidence for these negative effects of homeownership is rather less conclusive than for the positive impacts (for example, Green and Hendershott, 2001; Munch et al., 2006). Nonetheless, greater social capital itself may generate negative externalities. For instance, strong social capital within a community may facilitate anti-social behaviours through an unwillingness of insiders to involve outsiders (Browning et al., 2004).

We investigate the effects of homeownership on social capital by testing a model of individual social capital using a range of dependent and explanatory measures obtained by merging two samples (2006 and 2008) of New Zealand’s Quality of Life (QoL) survey. The 2006 census showed that the homeownership rate in New Zealand in 2006 was 67 per cent, with 6 per cent living in state rental housing and the remainder renting privately. Our pooled unit record dataset enables us to control for personal characteristics that, if omitted, could bias the estimated relationship between homeownership and social capital. We combine this dataset with regional data from Statistics New Zealand.

Like DiPasquale and Glaeser (1999), we hypothesise that homeownership gives individuals an incentive to improve their community. We argue that owner-occupiers demand greater accountability of local government than tenants. In New Zealand, local councils have a ‘power of general competence’ allowing them to be involved in any lawful activity. In practice, they provide economic and social amenities and services (such as roads, sewerage, rubbish collection, community facilities) and make planning decisions; they are not involved in central government policy fields such as health and education.

Dissatisfaction of homeowners with local government performance can impact negatively on community social capital. Hence these two dimensions of housing-related social capital (community participation versus satisfaction with local government) work in opposite direction from each other. While a potential impact of homeownership on local government performance was noted by Dietz and Haurin (2003), the two opposite effects have not been directly compared previously. We test these opposing impacts using both regression and propensity score matching (PSM) techniques.

When testing a causal link from homeownership to social capital, we must take into account that, unlike in a randomised trial, there are selection mechanisms that draw households into homeownership. Conventionally, such selection effects are partially addressed by means of instrumentation using historical or geographical information, group averages or by controlling for individual effects with panel data. Such approaches never fully overcome the selection problem associated with non-experimental data. Alternatively, a field experiment can provide a truly exogenous instrument, as demonstrated in the recent work by Engelhardt et al. (2010). In our application, we use a large and representative random sample, containing information on personal traits that are not normally observed, to control for selection effects. Nonetheless, the PSM approach is not a panacea for the selection issues and, for example, the choice of covariates remains critical (see Steiner et al., 2011). However, the method has now been used widely to identify causal effects in other microeconometric studies (for example, Angrist and Pischke, 2009); to our knowledge, this paper is its first application to estimating the impact of homeownership on social capital.

After controlling for selection effects that draw households into homeownership, we find that community participation, sense of community and trust in others are positively related to homeownership whereas attitudes towards local government are negatively related to homeownership. Thus, three indicators of social capital are positively related to homeownership whereas one is negatively related to homeownership. Importantly, as Putnam (1993) originally argued, it is attitudes towards local government which are the critical link between social capital and the efficacy of governance. The fact that these are found to be negatively related to homeownership suggests that the relationships between social capital and institutional performance are more complex that previously understood.

Section 2 of the paper discusses the theoretical framework for analysis. Section 3 describes our methodology, including a detailed description of the PSM procedure. Section 4 presents our data, while section 5 reports the empirical results of the regression and PSM analyses. The final section presents conclusions and suggests avenues for further research.

2. Analytical Framework

Social capital can be characterised as the linkages between actors through which information flows (Westlund, 2006). As social capital is neither observable nor quantifiable, direct measurement becomes impossible and for empirical purposes the use of proxy variables is necessary (Collier, 2002).

Interpersonal trust and community participation are commonly used measures of the stock of social capital and are included in both the World Values Survey and the General Social Survey. Zak and Knack (2001) have provided theoretical links which validate their use. Higher levels of trust relate to increased ease in establishing linkages with others, while participation in community activities facilitates the formation and strengthening of linkages.

Measures of a sense of community and attitudes towards local government are less commonly utilised. The rationale for their inclusion stems from the work of Putnam (1993, 1995) which suggested that social capital is, in part, expressed in community interaction. We assume that individuals who have a positive sense of community are more engaged in that community and therefore experience greater social capital through stronger network linkages. Putnam (1993, 1995) and Dietz and Haurin (2003) propose that homeowners with high levels of social capital will also be more fully engaged in local political processes and so hold their local council more fully to account. This may make them feel more or less positive towards their council than non-homeowners, depending on council performance. To the extent that council services benefit all residents while property taxes are paid directly only by property owners, it is quite possible that homeowners will have a less favourable attitude towards local government than renters.

Four distinct groupings of social capital determinants have been identified in prior literature for inclusion in a microeconometric model of social capital: demographic variables; geography and location-specific variables; human capital variables; and homeownership.

Demography

A person’s age and gender appear to be consistently associated with social capital (for example, Glaeser et al., 2002; Putnam, 2000; van Emmerik, 2006). Household composition is also an important consideration, particularly the presence of children (Kleinhans et al., 2007). Additionally, ethnicity matters. In New Zealand, Spellerberg (2001) and Williams and Robinson (2001) find that analysis of social capital needs to account for differences between ethnic groups, including Maori (New Zealand’s indigenous people), as there are cultural differences in social beliefs and attitudes which may influence social capital formation.

Geography

European studies have shown that social capital formation in rural settings is significantly different from that in urban areas, with more ‘bonding’ or within-group social capital in the latter rather than ‘bridging’ or between group social capital evident in the former (Aldridge et al., 2002). This effect can be examined using population density as a proxy for urbanisation and through use of regional fixed effects.

Human capital

Human capital has been consistently found to be related to social capital (for example, Huang et al., 2009; Glaeser et al., 2002; Helliwell and Putnam, 2007), although the exact relationship is under debate. Bowles and Gintis (2002) argue that social skills are a product of education, and thus that social capital could be considered a sub-component of human capital. This is in contrast to the standard approach which views social capital as related to, but separate from, human capital. We adopt the latter approach and include measures of individual human capital in our model.

Homeownership

Homeownership has been shown, inter alia by DiPasquale and Glaeser (1999) and Glaeser (2001), to have a significantly positive effect on variables related to social capital. However, homeownership is not randomly assigned. It is likely that those who own their homes also have higher incomes and higher educational attainment, are older and have a partner who shares the mortgage. These selection effects, if unaccounted for, may cause bias in the estimates of the impact of homeownership on social capital as those who own homes are likely to possess other characteristics commonly associated with social capital; therefore the effect of owning the home on social capital may be overstated (Dietz and Haurin, 2003). Among those who do not own homes, there may be differences in contributions to social capital between those who live rent free in a home owned by family, those who rent from a private landlord and those who rent from a public landlord.

In summary, assuming that individual i’s social capital (

This framework is used to aid selection of variables from the available micro data.

3. Methodology

When participants in a study are not randomly assigned into control and treatment groups, we do not have an experimental setting to separate the causal effects of a treatment (in this case homeownership) from the selection effects which may arise. One approach to dealing with selection bias in these circumstances is to use a non-experimental estimator such as ordinary least squares (OLS) regression and control for as many other influences as possible, arguing that potential omitted variable bias is thereby reduced. An alternative method is the use of a matching methodology in order to control explicitly for potential selection bias. The latter method is preferred here given that homeownership is not randomly assigned.

3.1 Regression Analysis

Initially, we report the results of OLS regression of the association between homeownership and the four proxies for social capital. We include controls for demography (age, gender, ethnicity, household size and composition), human capital (years of schooling, employment status and income) and geography (years resident in the region). Our equation also includes spatial and time fixed effects. However, because the data consist of two pooled cross-sectional surveys, we cannot use panel estimators that account for unobserved time-invariant individual effects. The resulting equation is

where,

A major concern with cross-sectional regressions is that unobservables in relation to individuals may bias the estimated coefficients and make interpretation of causality problematic. These problems can be substantially mitigated where: (a) there are multiple proxies for social capital; (b) one of the proxies is theoretically related to exogenous personal characteristics; and (c) that proxy is not a function of the explanatory variables of interest for determining another form of social capital. If (c) does not hold, one can still use a proxy that meets condition (b) to test robustness of results.

As an example, take two social capital proxies: trust and participation. The psychological literature on attachment theory (Bowlby, 1982) indicates that early life experience affects subsequent personal relationships throughout life, including the likelihood that an individual trusts others. Thus there is an unobserved personal element to trust that is additional to the impact of observable factors such as ethnicity, age and geographical location. Despite not having longitudinal data, we can make use of the unobservable component affecting trust to control for individual unobservables in a regression of the determinants of participation. To see how, consider the following structural system of equations

where, i refers to an individual;

If the individual unobservables (

Substitution of (5) into (4) yields

Equation (6) shows that, by including trust in the participation equation we can control for individual unobservables,

Following this logic, we estimate the impact of homeownership on participation, community and council in two ways. The first omits trust in the regression, while the second includes

3.2 PSM Methods

An alternative to regression estimation is to use a quasi-experimental method in the form of propensity score matching in order to compare individuals who are observationally similar, except with respect to the treatment (Bryson et al., 2002). A quasi-experimental design differs from an experimental design because in the former the data have not been generated by a random assignment of individuals into the treatment or control group. The estimation process for the treatment effect needs to take into account that there may be underlying reasons why individuals fall into the treatment or control group (Greenstone and Gayer, 2009). Given that we do not have longitudinal data on individuals, we account for selection through the use of matching methods. The propensity score matching (PSM) approach that we adopt involves matching observations in a treatment and control group based on observed characteristics such that we compare two or more individuals who are observationally similar but belong to one or other group. The result is an estimate of the effect of the treatment while removing the underlying bias that self-selection into the treatment group (on the basis of observables) may have caused (Rosenbaum and Rubin, 1983). 1

Dehejia and Wahba (2002) suggest that, for PSM successfully to reduce selection bias, observations for both treatment and control groups must be at the same location (and date) and have used the same questionnaire. The dataset must contain a rich set of variables which are relevant to both the intervention (homeownership) and the outcome (social capital). Using these variables, the method generates an index score which represents the vector of characteristics of the individual. PSM requires scores to be ‘balanced’ between treatment and control groups in terms of their representation within propensity score blocks. Balancing reflects the idea that exposure to the treatment is random for any given propensity score. Therefore, treated and controlled observations should be, on average, observationally identical. This requires control and treatment groups to have means which are not significantly different given the variables on which they are matched (Rosenbaum and Rubin, 1983; Imbens, 2000; Becker and Ichino, 2002).

Once propensity scores are obtained, we use two matching algorithms, ‘nearest neighbour’ (that matches each treated dwelling to the nearest control dwelling in terms of propensity score) and ‘kernel matching’ (that matches each treated dwelling to a weighted average of control dwellings, with weights reflecting closeness of scores). For each matching algorithm, we provide two sets of estimates. The first uses the treatment of whether or not an individual owns the home they live in, while the second compares homeowners with private renters only. The dependent variables are the three proxies for social capital specified earlier, with trust included as one of the variables on which individuals are matched. Balanced blocks for homeownership have been obtained using variables relating to: trust, com_imp (a measure of how important the individual believes it is to feel a sense of community), age, ethnicity, education, income, employment status, relationship status and regional population density.

4. Data Overview and Descriptive Statistics

We use pooled cross-sectional micro data obtained by merging the 2006 and 2008 samples of the New Zealand Quality of Life (QoL) survey. The QoL survey is a national survey, sponsored by the local governments of eight New Zealand cities, with the aim of measuring aspects relating to an individual’s quality of life, living situation, community interactions and aspects of health and wellbeing. 2 The 2006 and 2008 surveys have consistent questions across the two years. The merged dataset has a sample size of 15 700, with 7545 participants in the 2006 survey and 8155 in the 2008 survey. Surveying was conducted using computer-assisted telephone interviewing and the sample was drawn from New Zealand residents aged 15 and over. Our final sample was restricted to those aged 18 and over at the time of the survey. Participants were drawn at random from the electoral roll and were notified by mail prior to the phone interview. While response rates were 22 per cent in 2006 and 37 per cent in 2008, quotas for age, gender and ethnicity were used to address possible sampling bias and the sample appears representative of the underlying New Zealand population. Our four proxy measures of social capital—trust in others, participation in social networks, sense of community and attitude towards local government—are all obtained from the same survey. Data regarding regional demographics were obtained from the Statistics New Zealand 2006 Census of Populations and Dwellings. A full list of variables obtained through these datasets using the framework specified earlier is presented in the Appendix (Table A1).

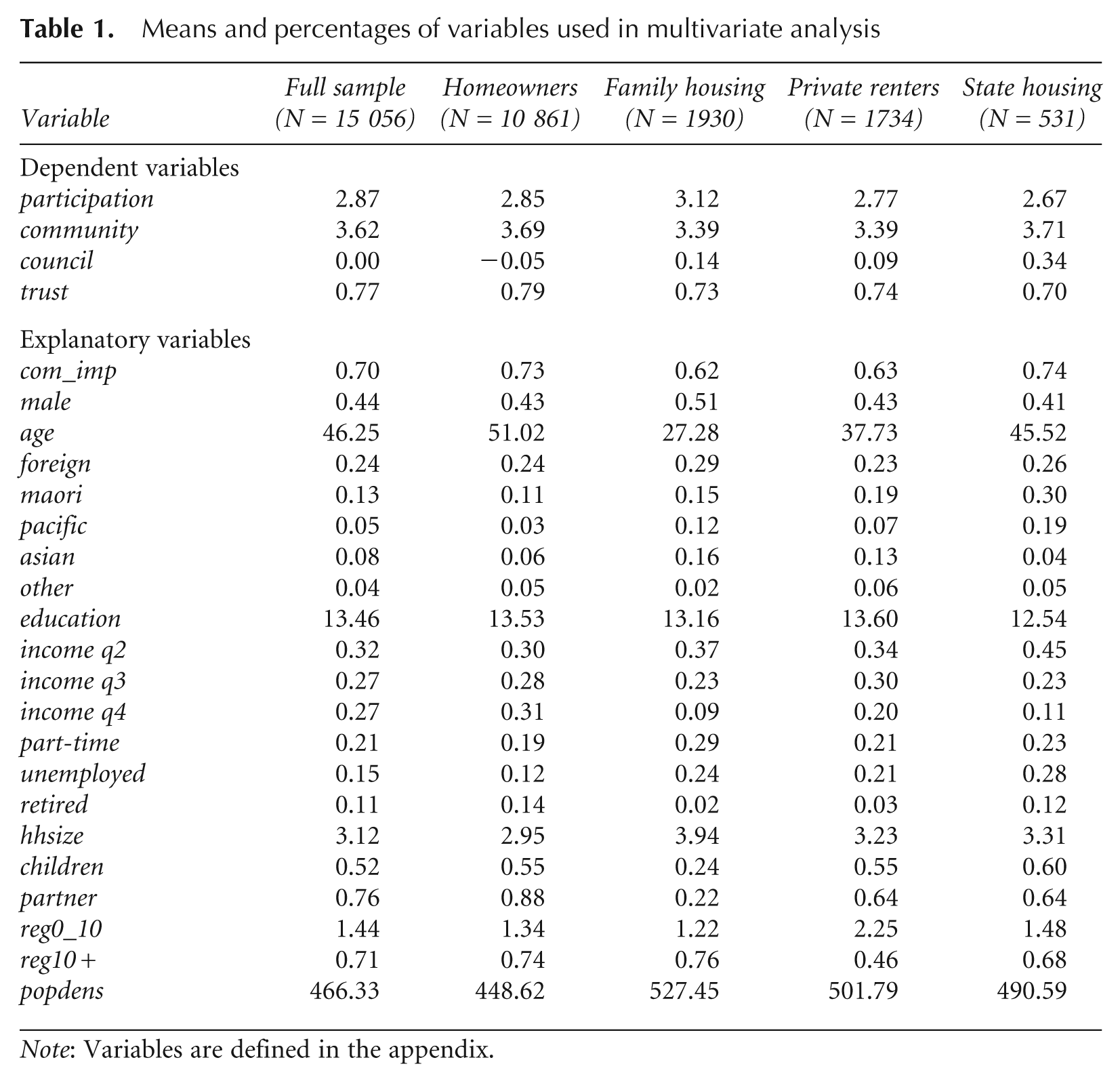

Table 1 shows means of the variables reported in the regression equations. The combined and cleaned dataset was largely representative of the New Zealand population, although males were slightly underrepresented in the sample (44 per cent) compared with 48 per cent in the population aged 18 and over. The age distribution was similar to the New Zealand distribution; however, there was an undersampling of those aged 20–29 and 75–84, particularly amongst women. Those aged 45–49 were overrepresented. Dealing with ethnicity can be problematic following the introduction within surveys of the category, ‘New Zealander’ (which can be interpreted as a statement of national identity rather than ethnicity), in addition to the traditional European, Maori and other ethnic groups. Normal practice is to combine ‘New Zealander’ with ‘European’ and ‘Pakeha’ 3 to form a single group, European. We adopt this assumption and the resulting dataset is representative of the underlying known ethnic distribution. Geographically, rural and South Island regions are undersampled, while Wellington, the capital city, is oversampled. New Zealand’s largest city, Auckland, is accurately represented. Our sample earned more than the underlying population, with each census income quartile above the first containing more than 25 per cent of the observations in the pooled sample. Participants who indicated they were foreign-born comprised 24 per cent of the sample, close to the proportion of foreign-born aged 18 and over in the New Zealand 2006 census (26 per cent). Regressions reported in section 5 are based on unweighted data, but person-weighted regressions based on census frequencies by age and location yielded very similar results.

Means and percentages of variables used in multivariate analysis

Note: Variables are defined in the appendix.

In comparing means across the four homeownership categories, males were overrepresented in family housing and under-represented in (subsidised) state-provided housing relative to their sample proportion. All non-European ethnic groups are underrepresented as homeowners. Those identifying as having Maori or Pacific Island ethnicities were much more likely to be living in state housing than their share of the population would suggest, while those identifying as Asian were more likely to live in family accommodation. A high proportion of those in lower income quartiles are accommodated in state housing, while those in the top income quartile are under-represented in private rentals and very strongly under-represented in family housing and state housing. The low mean age of those in family housing indicates that this category is likely to comprise a significant number of young adults still living with parents.

5. Results

To examine the impact of homeownership on social capital, including attitudes towards local government, we first use standard regression techniques to estimate the model specified earlier using the four separate dependent variables. We then use PSM analysis to estimate the impact of homeownership on attitudes towards local government and other manifestations of social capital.

5.1 Regression Results

The determinants of each of the four separate dependent variables are estimated by regression methods, based on the framework developed in section 3. Variables are described in the Appendix and Table 1. All variables are related to one of the four categories specified in the framework: geographical, demographic, human capital or homeownership.

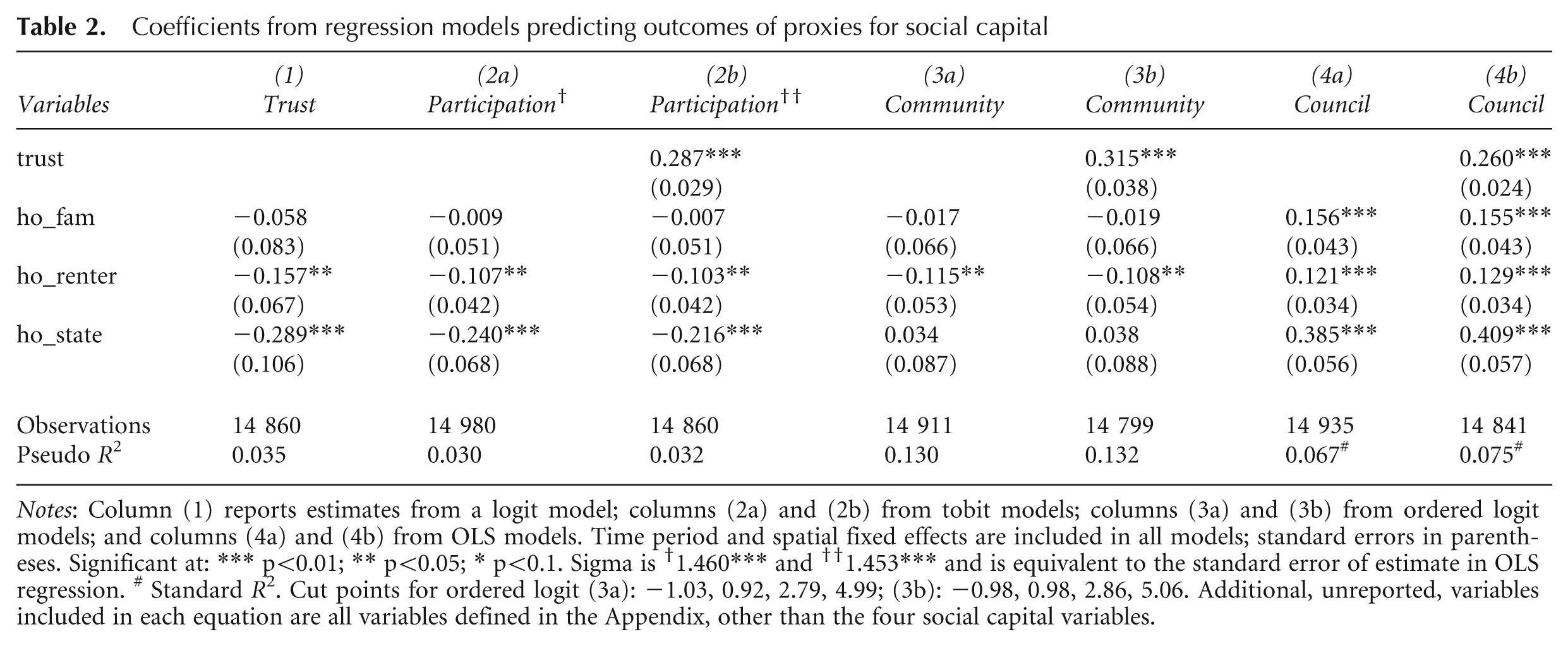

The binary trust variable is examined using a logit regression, while the participation index is examined using tobit regression due to the truncation of the index. Sense of community (measured according to a Likert scale) is examined using ordered logit regression while attitude towards council (a continuous variable) is examined using ordinary least squares. As discussed in the methodology section, the trust variable may be used as a proxy for unobservable personal traits of an individual gained through early childhood. In order to utilise this information, we estimate each of the other three proxies for social capital using first the model of equation (2) and secondly the model of equation (6)—i.e. including the variable ‘trust’ to control for the influence of unobservable character traits. The regressions (reported in Table 2) include all the control variables listed in the Appendix (other than the social capital variables); coefficients on control variables are not reported to save space but are available upon request. While our discussion concentrates on the homeownership impacts, we note that the full results reveal that the relationships in terms of previous literature between the social capital outcomes and each of the personal, geographical and human capital variables are consistent with earlier New Zealand research (Roskruge et al., 2011).

Coefficients from regression models predicting outcomes of proxies for social capital

Notes: Column (1) reports estimates from a logit model; columns (2a) and (2b) from tobit models; columns (3a) and (3b) from ordered logit models; and columns (4a) and (4b) from OLS models. Time period and spatial fixed effects are included in all models; standard errors in parentheses. Significant at: *** p<0.01; ** p<0.05; * p<0.1. Sigma is †1.460*** and ††1.453*** and is equivalent to the standard error of estimate in OLS regression. # Standard R2. Cut points for ordered logit (3a): −1.03, 0.92, 2.79, 4.99; (3b): −0.98, 0.98, 2.86, 5.06. Additional, unreported, variables included in each equation are all variables defined in the Appendix, other than the four social capital variables.

Trust

The results for the logit regression of trust can be seen in column (1) of Table 2. We distinguish four categories of housing tenure: homeowner, renting from a family member (or house provided rent-free), renting from a private landlord and renting from the state. The default category in the regression is homeowner. Those renting from a private landlord or from the state are significantly less trusting than homeowners. Those living with a family member show no significant difference in trust from homeowners.

Participation

Columns (2a) and (2b) in Table 2 report the results for the determinants of the participation index using a tobit regression respectively excluding and including trust as an explanatory variable. The participation index ranged from 0 to 8, where zero had the participant engaged in no activities and 8 where the participant engaged in all surveyed activities. The two models are very similar, indicating that controlling for unobservable traits (through inclusion of trust) provides additional explanatory power in explaining participation, but its omission does not bias the impact of homeownership. The trust variable is a strong and significant predictor of participation.

The positive impact of homeownership on social capital is confirmed in each of regressions (2a) and (2b). Renting from a private landlord and living in a state-owned house both yield a negative impact on social participation, significant at the 5 per cent and 1 per cent levels respectively, relative to people who are homeowners. Again, those renting from a family member show no significant difference in trust relative to homeowners.

Sense of community at the locality

Columns (3a) and (3b) in Table 2 report the results for homeownership status on an individual’s sense of community at their current locality. The two models are again consistent, with no changes in significance as a result of introducing the trust variable. The trust variable is significant and positive at the 1 per cent level.

The relationships between homeownership status and this proxy for social capital are somewhat more complex than for the prior two proxies. Renting from a private landlord is associated with a lower sense of community than for homeowners (or those living with family), significant at the 5 per cent level. However, there is no statistically significant difference in sense of community at their current locality between homeowners and people living in state-owned housing. One of the purposes of state housing provision is to provide more deprived families with stable housing tenure, so providing a stable community especially for children in these families (Murphy, 2003; Schrader, 2005); thus many of these tenants will have long-term relationships with their community. This policy intention is reflected in the lack of a significant difference in sense of community between homeowners and those with a state tenancy. This finding lends weight to the argument by Forrest and Kearns (2001) that people residing in poor or deprived communities may rely more on neighbourhood level social capital while those in wealthier communities can maintain more spatially diffused networks.

Attitudes towards local government

Columns (4a) and (4b) test for factors influencing attitudes of residents towards the activities of their local government. The two models are again consistent and trust is significant at the 1 per cent level.

Each of the three housing measures (private renting, state renting and living with family) is significant and positive at the 1 per cent level when compared with homeowners. Thus homeowners have a more negative view of their local government’s performance than do non-owners. This reflects that homeowners hold local politicians to account more stringently than do other residents (see also Dietz and Haurin, 2003).

Homeownership in New Zealand brings with it the obligation to pay local property taxes, while those who are renting have these costs incorporated into their rent and therefore do not face these costs directly. All residents, however, benefit from the services provided by local government. Together, these considerations indicate that some homeowners, in holding their local council to account, may consider that they are not getting value for money (at least relative to the views of other residents) from their councils. Consistent with the homeownership result, the attitude towards the local council declines with increasing duration of residence (i.e. we find a significant negative coefficient on the variable ‘number of years living in region’ in the attitude towards council equation). A longer stay in a region therefore appears to make residents even less satisfied with the performance of their local council.

Comparison of homeownership effects across models

Comparing the models, we find that both trust (when included as an explanatory variable) and a stated belief in the general importance of community are significant determinants of each of the other proxies for social capital. Thus our results are robust to the inclusion of controls for individual unobservables about a person’s underlying traits. Compared with homeowners, those who rent from either a private or state landlord are significantly less likely to trust others or participate in social activities, and private renters are also less likely to feel a sense of community at their current locality. However, when considering attitudes towards local government, those living in family, private rental and state rental housing are all significantly more likely to have a positive attitude towards local government relative to those who own their own home.

5.2 PSM Estimates

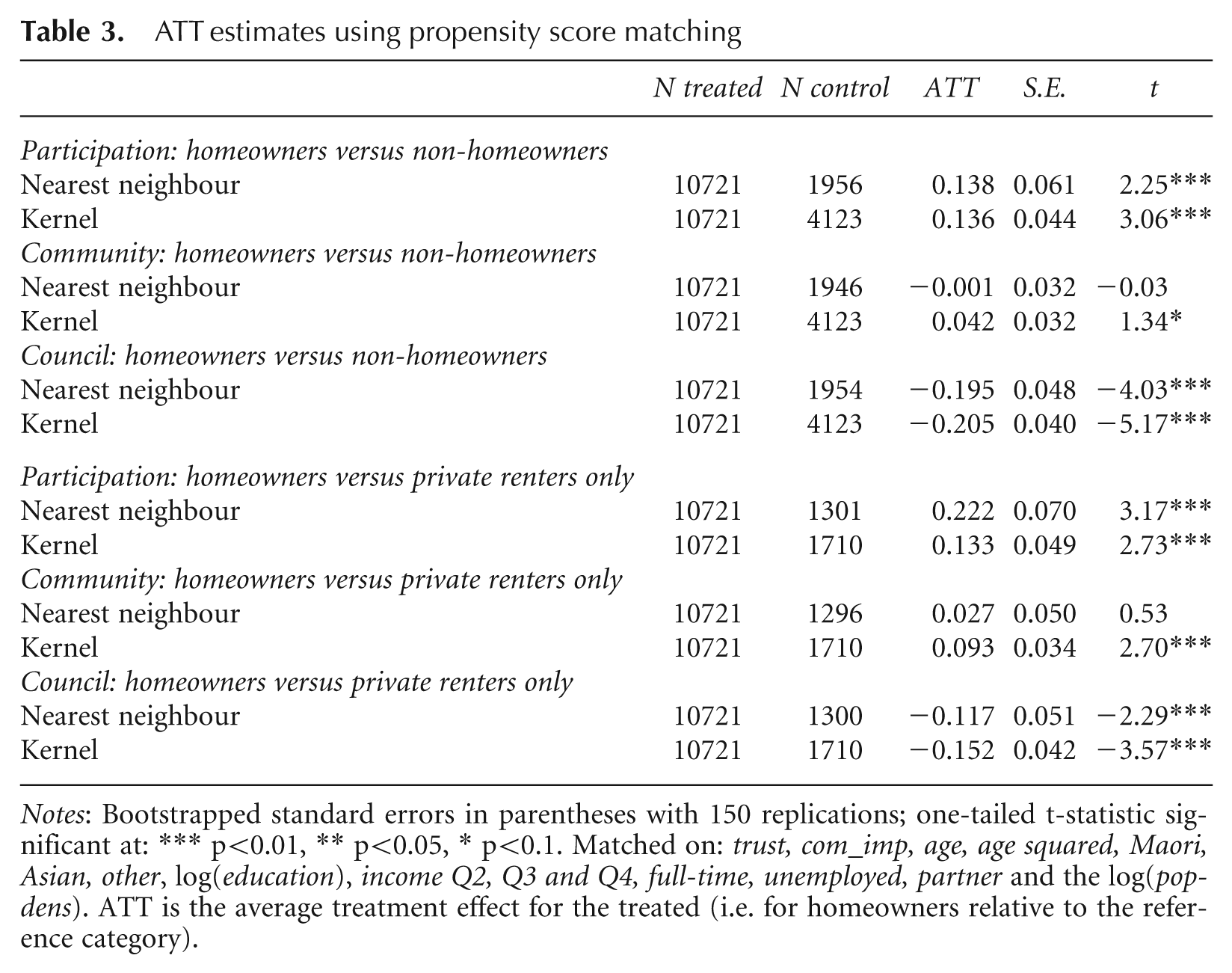

In estimating the PSM model of the impacts of homeownership on three proxies for social capital (including trust as a matching variable), we categorise homeownership as a treatment for two separate control groups. The first compares homeowners with all non-homeowners pooled, while the second compares homeowners with private renters only. For each approach we use both kernel and nearest neighbour matching to estimate the effects with bootstrapped standard errors obtained with 150 repetitions. The results of each of the models for the three proxies are presented in Table 3. To ensure balancing (at the 0.01 level), we adopt a more parsimonious model than that used in the regressions, matching on the following variables: trust, belief in the importance of community, age, age squared, Maori, Asian, other, log(education), income from quartiles 2, 3 and 4, employed full-time, unemployed, living with a partner and the log of regional population density. The inclusion of trust and belief in the importance of community as matching variables means that we are matching not just on standard observable characteristics of individuals but also on often unobservable personal traits.

ATT estimates using propensity score matching

Notes: Bootstrapped standard errors in parentheses with 150 replications; one-tailed t-statistic significant at: *** p<0.01, ** p<0.05, * p<0.1. Matched on: trust, com_imp, age, age squared, Maori, Asian, other, log(education), income Q2, Q3 and Q4, full-time, unemployed, partner and the log(popdens). ATT is the average treatment effect for the treated (i.e. for homeowners relative to the reference category).

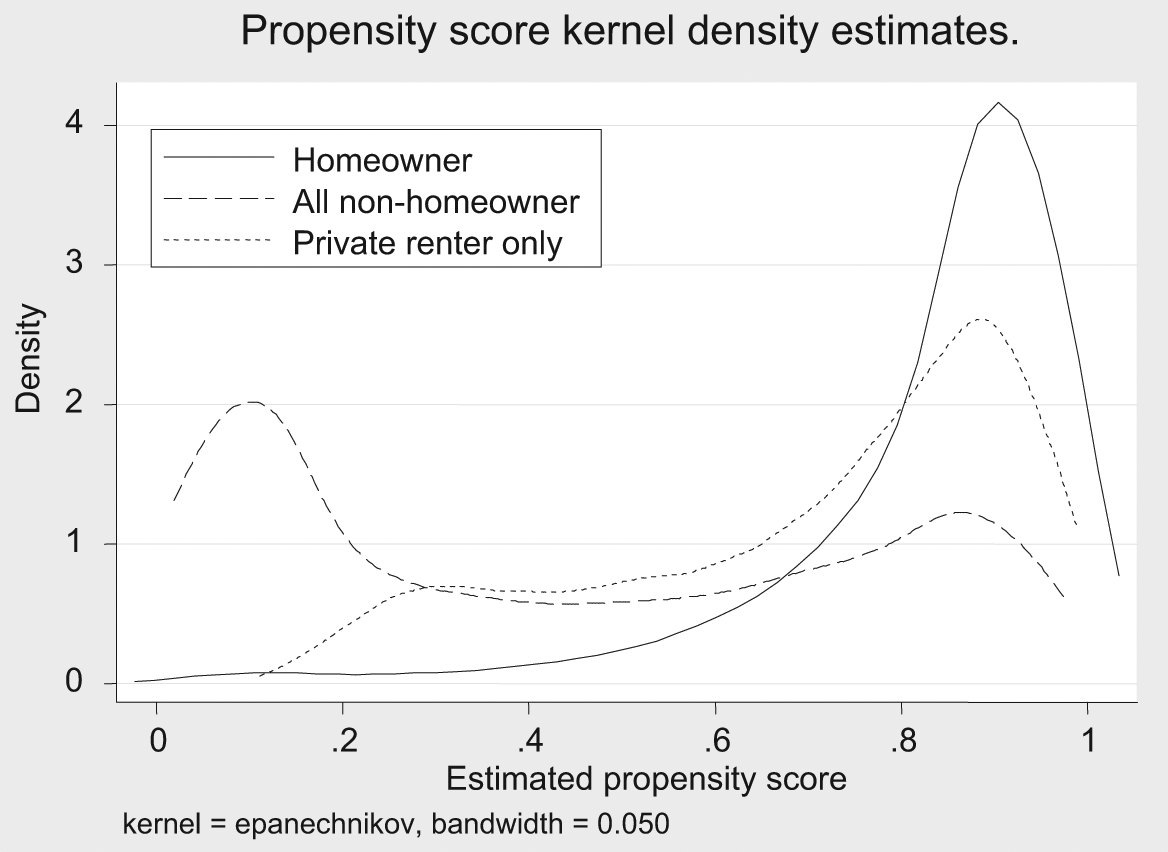

Figure 1 presents the kernel densities of the propensity scores for homeowners, non-homeowners and private renters using the control variables already specified. The figure suggests that, while there is considerable overlap in the distributions, the kernel density for homeowners has considerable density for high propensity scores, with a strongly negative skew. The distribution for non-owners has one overlapping mode in the same range (between 0.8 and 0.95) but another mode between propensity scores of 0 and 0.2, reflecting the influence of state house tenants. The distribution of private renters much more closely resembles that of homeowners. This is reflected in the very different means between the groups, with the mean propensity score being 0.83 for homeowners, 0.7 for private renters and 0.43 for all non-homeowners combined. We therefore place more emphasis on the results that compare homeowners just with private renters than with all non-homeowners combined.

Kernel density estimate for homeowners, non-homeowners and private renters.

The estimates of the average treatment effect of homeownership on the treated (ATT) are reported in Table 3 for the three proxies of social capital, the two matching methods and the two comparator groups. When considering homeowners compared with all non-homeowners or compared with private renters only, the effect of homeownership is positive and significant for participation. However, there is much weaker evidence for homeownership impacting on the sense of community at the current locality. Both matching methods and both samples provide clear evidence that homeowners have less positive attitudes towards local government than do other tenure groups (significant in each case at the 1 per cent level).

The average treatment effects provide us with some understanding of the likely effect that owning a home has on participation, sense of community and attitudes towards local government for observationally similar individuals, where similarity includes their stated attitude towards trust in others. For participation, the interpretation is that the average number of social activities is 0.13 to 0.22 higher for homeowners than for non-owners. For the sense of community, even the statistically significant estimates show only a very small effect size. The findings for attitudes towards local government are strongly significant and negative when compared with both all non-homeowners and renters only.

Across the PSM results, there is therefore considerable evidence showing an impact of homeownership on at least two of the proxies for social capital. Specifically, homeownership status impacts positively on participation in community activities and negatively on attitudes towards local government performance. These results, which are consistent with the prior regression results, are obtained after controlling for both observable and unobservable individual characteristics that are embodied in an individual’s stated attitude towards trust and importance of community.

6. Conclusions

By applying regression and matching techniques to survey data collected in New Zealand, we have estimated the impacts of homeownership on four separate proxies of individual social capital, after controlling for other observable, and some often unobservable, factors.

Using regression methods, we find that, when an individual owns the home they live in, they report significantly higher levels of social capital than those who do not own their own home. Specifically, they have higher trust in others, participate more in local activities and have a more positive sense of their local community. It is plausible that, conditional on personal characteristics, those who personally invest in their community through networks and participation in community activities will see a return to that investment in property values that internalise such externalities, irrespective of whether they also have altruistic motives. Homeowners, however, have a less positive attitude towards local government performance than do people in other forms of housing tenure. This outcome may reflect a stronger involvement in the governance of their community by owner-occupiers and this involvement may make them less satisfied with the performance of their local representatives. The impact of homeowners on the community’s social capital will be stronger than compared with members of the community who are ambivalent to the political process (Purdue, 2001), but the local political participation impact of homeowners works opposite to that of trust, sense of community and participation in social activities.

The PSM estimates of the average treatment effect of homeownership yield similar results. Homeowners participate in more social activities than non-homeowners. Again, we find strong evidence that homeownership leads to a less positive attitude towards local government performance. This dimension of social capital works in the opposite direction to the other dimensions of social capital. This is the first time that these dimensions of social capital have been observed to work in the opposite direction to each other, and the implications of this finding are potentially very significant. Putnam’s (1993) original argument was based on the importance of trust in local government as a critical element of institutional and market performance. If homeownership reduces this trust, while at the same time promoting other dimensions of social capital, it becomes clear that the relationship between having a (real estate) stake in the local economy and the performance of local governance is rather more complex that has previously been understood.

Our results may have implications for policy, particularly for those areas where there are low levels of owner-occupied dwellings. In such areas, a range of social ‘bads’ may arise from lower levels of social capital associated with the lack of homeownership. Our (preferred) PSM results imply that increasing levels of homeownership improves participation in community activities, but may not engender a material increase in the sense of community. Thus whether or not homeownership should be encouraged depends on the outcome that is being sought. If a greater sense of community is desired, a policy favouring homeownership may have little effect. If policy-makers wish to increase participation in local activities, they may wish to consider policies that enhance homeownership rates. In addition, if central government wishes to raise the incentives on residents to hold local government to account, a policy that raises homeownership levels may be an effective means of engendering extra scrutiny of local government performance.

Future work could expand on our homeownership definition to test whether single-occupier dwellings are significantly different from couple, family or communally occupied dwellings. It could also be worthwhile to investigate the type of social capital which is formed through homeownership. This would be particularly interesting when considering the difference between bridging and bonding social capital and how that impacts new arrivals’ integration into a community. Instead of treating homeownership as a binary response, it may also be interesting to examine the level of equity individuals possess in their homes, as those with little equity in their home may have quite different attitudes with respect to social capital formation than those who own their home free of mortgages.

Footnotes

Appendix

Definitions for variables

| Variable | Description |

|---|---|

| Attitudinal variables | |

| participation† | Index of social activities individuals are an active participant in |

| community† | Reported sense of community at the current locality |

| council† | Index of attitudes towards council |

| trust† | 0 = ‘cannot be too careful’; 1 = ‘most people can be trusted’ |

| com_imp | Reported belief in the importance of community |

| Demographics | |

| euro* | Identified as ethnic European |

| maori | Identified as ethnic Maori |

| pacific | Identified as ethnic Pacific Islander |

| asian | Identified as ethnic Asian |

| other | Identified as belonging to another ethnic group |

| foreign | Not born in New Zealand |

| male | 0 = female, 1 = male |

| age | Age in years |

| hhsize | Size of household, truncated at 6 |

| children | Child under 15 currently living in same residence |

| partner | Partner currently living in same residence |

| Homeownership | |

| ho_owner* | Owner of house |

| ho_fam | Living in house owned by family |

| ho_renter | Living in privately rented accommodation |

| ho_state | Living in a state owned house |

| Human capital | |

| education | Years of formal schooling |

| income q1-q4 | Quartile of New Zealand income distribution |

| fulltime* | 1 = currently in full-time employment |

| part-time | 1 = currently in part-time employment |

| unemployed | 1 = currently not in labour force |

| retired | 1 = currently retired |

| Geographic | |

| reg0_10 | Number of years living in region, up to 10 |

| reg10+ | 0 = less than 10 years, 1 = 10 years+ |

| popdens | Population per square km in territory individual resides in |

| Regional dummies | 51 dummies created from 72 New Zealand territorial authorities |

Indicates baseline variables.

indicates dependent variables.

Acknowledgements

The authors wish to thank the Quality of Life Research Team for the provision of data. The authors are solely responsible for the analysis and views expressed.

Funding

The authors are grateful to the Royal Society of New Zealand Marsden Fund (grant MEP-07-003, Homeownership) for funding this research.