Abstract

This article seeks to contribute to a better understanding of the role of the state in influencing the formation of global cities in emerging economies. It highlights the complexity of this role due to challenging external environments, divergent interests of state actors and socioeconomic and institutional constraints that these actors are under. At an empirical level, it examines the progress of Shanghai in its state-led development as an emerging global city and the respective roles of the national and local governments in this process.

1. Introduction

The formation of the global/world cities and the role of the state in this process is seriously underexplored (Sassen, 1991 and 2001; Friedmann, 1995 and 2001; Olds and Yeung, 2004). Despite this, however, urban planners and city authorities, especially those in emerging economies, have demonstrated remarkable interest in state-led global/world city formation (Olds and Yeung, 2004). The contrast here raises two important research questions. First, what are the chances for leading cities of emerging economies to become global/world cities? Second, to what extent can the state in emerging economies facilitate this formation? This article explores such questions in the context of Shanghai’s emergence as a global city. Emerging economies here are loosely defined as major developing countries that are characterised by fast economic growth and industrialisation, and increasing integration into the global trading system (OECD 2008).

Shanghai’s re-emergence as a leading world city had been anticipated. In fact, along with Hong Kong and Singapore, Shanghai was, for the period of 1919–39, the largest of the three ‘sub-regional’ financial centres in Asia (Jones, 1992). However, the city declined, first due to the Japanese occupation (1937–45) and then, after the foundation of the PRC in 1949, a socialist system that practised ‘financial repression’ and an insular planned economy (Jao, 2003). With the rise of the Chinese economy following its reform and open-door policy from the late 1970s, however, it is widely expected (for example, Friedmann, 1995; Mainelli and Yeandle, 2007) that Shanghai will once again become a significant player in international finance. On the other hand, turning Shanghai into a global/world city has been a much publicised Chinese ‘state project’ since at least the early 1990s, if not earlier (Zhang, 2003; Wu, 2009). However, numerous reviews of Shanghai’s prospects (Shi and Hamnett, 2002; Jao, 2003; McCauley and Chan, 2007, Jarvis, 2011; Subacchi et al., 2012) either as an international financial centre or as a global city have consistently sounded a cautious note, especially in terms of its competition with Hong Kong. This is despite Shanghai’s improvement on several fronts since the early 2000s (see section 3).

So to what extent has Shanghai succeeded in becoming a global city? What role has the state played in this process? Furthermore, what does Shanghai’s experience tell us about the capacity and constraints of the state in emerging economies to facilitate global city formation? These are the important questions to be explored.

The rest of this article proceeds as follows. Section 2 reviews the relevant literature. Section 3 discusses the vision of this ‘state project’ and evaluates the evidence on Shanghai’s progress in global city formation. Section 4 explores the underlying factors. Section 5 concludes.

2. Perspectives on Global/World City Formation and the Role of the State

In order to develop an analytical framework for the empirical analysis, we first introduce the concept of the global/world city. We then discuss theoretically the scope for leading cities in emerging economies to become global/world cities. Finally, the potential role of the state in this formation is considered.

2.1 Defining World/Global Cities

Although Hall (1966) did much to popularise the idea of world cities, it was Friedmann and Wolff (1982) who undertook the conceptual ground-breaking work. In the context of economic restructuring in the world economy starting from the 1970s and adopting a world systems perspective, they conceptualised the world city as

(1) an instrument for the control of production and market organisation by transnational capital; and

(2) a junction between the national economy and the world economy.

They saw these cities as “major sites for the concentration and accumulation of international capital”, tightly connected with each other and occurring “exclusively in core and semi-core regions” (p. 59). Friedmann’s (1986) subsequent formulation of ‘the world city hypothesis’ further linked these cities to the ‘new international division of labour’, characterising them as the ‘basing points’ for global capital.

In contrast, Sassen (1991) distinguishes ‘global cities’ from ‘world cities’ and insists that global cities are a new type of economic co-ordinating unit, specific to the era of globalisation since the 1980s. In the context of spatially dispersed but globally integrated economic activities, global cities function

as command points in the organization of the world economy, as sites for the production of innovations in finance and advanced service for firms, and as key marketplaces for capital (Sassen 1991, p. 338).

Sassen (1991) also recognises that these cities do not simply compete with each other, but function as one transterritorial marketplace.

Sassen’s (1991, 2001) focus on the provision of advanced services by global cities stresses that these cities function similarly as international financial centres, defined as localities with an intensive concentration of a wide variety of international financial businesses and transactions enjoying both agglomeration and scale economies in financial transactions (Kindleberger, 2000; Z/Yen Ltd, 2005). Sassen’s global cities also possess other industries supporting the capability of global corporate control and various amenities to maintain the lifestyle of the key professionals.

Synthesising Sassen’s emphasis on the provision of advanced services by global cities, Castells’ (1996) idea of a ‘global network’ of urban centres and Braudel’s (1984) insight into the inherent monopolistic tendency of capitalism led Taylor (2000) to conceptualise world/global cities as the highly concentrated loci of ‘unique knowledge complexes’ that exploit their monopoly power based on economic reflexivity. He suggests that contemporary globalisation has led to a ‘world city network’, defined as an interlocking network where cities are connected through the activities of transnodal agents, most importantly transnational advanced service firms. ‘World city-ness’ can then be measured in terms of the level of provision for advanced producer services relative to the top-scoring city, or its ‘interlock connectivity’ (Taylor, 2000, 2004). A major advantage of Taylor’s approach is that a city’s ‘world city-ness’ can be objectively measured.

2.2 The Chances for Latecomers

These three perspectives have different implications for the prospects of new global cities in emerging economies. Although the world city hypothesis itself has relatively little to say on this issue except that world cities only occur in core or semi-periphery regions (Friedmann, 1986), the world systems theoretical framework is nevertheless insightful. The framework conceptualises the contemporary world economy as a hierarchy, within which participating areas play differentiated roles either as core, semi-periphery or periphery. While the core areas have more core-like (defined as monopolistic and highly profitable) production processes (such as finance) and strong states, the periphery areas have more periphery-like (defined as competitive and less profitable) production processes and weaker states. In contrast, the semi-periphery is in transition towards the core and is therefore the most dynamic type of area (Wallerstein, 2004). Thus the chance of global city formation in an emerging economy depends on the progress of its national economy and, in turn, this formation can strengthen the home economy’s bid to raise its position.

The global city model (Sassen, 2001) has somewhat different implications. Since it regards global cities as the production sites of highly specialised corporate services and financial innovations, and as marketplaces for these services and products, there is greater room for manoeuvre at the city level. In other words, the fortunes of emerging national economies and their nascent global cities need not be synchronised theoretically. Much would depend on how quickly the city itself can develop the capability of corporate control, acquire the necessary infrastructure and lifestyle, and attract other market players. Studies of international financial centres suggest that, while the more established centres benefit from the forces of centralisation due to scale economies, agglomeration economies and their ‘endowed capacities’, newly emerging centres can, by contrast, benefit from the forces of decentralisation thanks to outsourcing, regionally specialised knowledge and emerging localised demand associated with increasing inward foreign investment and fast economic growth. There is also scope for latecomers to increase their chances through policy initiatives (Jarvis, 2011).

Finally, while the world city network school is light on theorisation, it has done much to deepen our understanding of city network connectivity and power, defining the last as both ‘to power over’ other cities and an ability to attract advanced service firms (Taylor, 2004). In particular, a Globalising City Index has been formulated to distinguish two kinds of driving forces—namely, ‘place power’ and ‘network power’—underpinning two types of globalising cities. While the first type draws power from being the headquarters (therefore command centres) of top firms in the world, the second type draws power from high connectivity (Taylor et al., 2011). This analysis implies that global city formation can benefit from either strengthening headquarter functions, or improving connectivity, or a combination of both.

2.3 The Role of the State in Global City Formation

While the dominant world city hypothesis and the global city model provide limited guidance on the role of the state in global city formation, insights can be drawn from elsewhere in the literature. Taylor’s (2000) analysis of the distribution of world cities shows that, while a combination of decentralisation and large national economies tends to be associated with multiple world cities, centralisation and medium-sized economies tend to produce one dominant world city in each state.

On the other hand, examining the experiences of New York, Tokyo and Seoul, Hill and Kim (2000) distinguish two types of global cities—namely, a ‘market-centred, bourgeois type’ versus a ‘state-centred, political-bureaucratic type’. Their work usefully contrasts some of the characteristics of the two types and highlights a crucial link between the state-centred global city and the developmental state. They argue that Tokyo was not primarily a global basing-point for the operations of stateless transnational corporations (TNCs), but mainly a national basing-point for the global operations of Japanese TNCs. They further state that the global control apparatus represented by Tokyo resides in the financial and industrial policy networks under the guidance of government ministries, rather than networks of transnational service firms.

Olds and Yeung (2004) propose a useful typology of three kinds of global cities: ‘hyper global cities’, ‘emerging global cities’ and ‘global city-states’. Their discussion of what they see as the relative disadvantage of emerging global cities is particularly relevant. Relative to ‘hyper global cities’ such as New York and London, emerging global cities are regarded as being less integrated into the global economy, functioning mainly as “co-ordination/channelling centres responsible for receiving or channelling inward flows” (p. 506). Relative to the ‘global city-states’ (such as Singapore and Hong Kong), emerging global cities are said to face more potential competition from other urban centres in their home country and are “governed in a relatively more complex, less coherent, and less strategic fashion” (p. 508). Furthermore, they are constrained by the tensions inherent in national versus urban politics. Finally, the lack of a colonial past generally makes the emerging global cities less open, cosmopolitan and attractive, compared with global city-states. The critical condition for emerging global cities is “the sustainability of national efforts in developing particular cities to become global cities” (p. 507).

The experience of Tokyo (Hill and Kim, 2000) and Singapore (Olds and Yeung, 2004) helps to shed light on the prospects of Shanghai as a global city: they highlight the important role of a developmental state on the one hand, and the disadvantage of being an emerging global city on the other. The Chinese state is not a typical developmental state. In comparison with the paradigmatic Japanese developmental state, the Chinese state is characterised by ‘fragmented authoritarianism’ arising from a tradition of administrative decentralisation, has weaker capacity and is less inclined and able to work with the private sector because of its socialist ideology (Beeson, 2009). Moreover and related to the ideological difference with the West, the Chinese state faces a much less permissive external environment compared with the Japanese state (Beeson, 2009). This is further aggravated by the direct role of the state in emerging Chinese state-owned TNCs and sovereign funds (Wooldridge, 2012). The implication is that China’s path towards global ascendance is likely to be more contentious than Japan’s. So Shanghai’s will be similarly difficult in its pursuit of global city status relative to Tokyo’s.

Weiss’ (1998) emphasis on ‘managed openness’ and Chang’s (2003) institutionalist perspective on the role of the state in structural change are also relevant here. In the context of globalisation and opening-up, ‘managed openness’ requires the state to adopt

a framework of analysis and policy choice that is both ‘open’ to the benefits of international economic flows and relationships, but ‘managed’ in terms of their effects (Weiss, 1998, p. 127).

Following Michael Lind, Weiss (1997, p. 24) argues that efforts to maintain state power in the context of globalisation involve the “reconstitution of power around the consolidation of domestic and international linkages” by building power alliances. The traditional ‘integral state’ is being replaced by a ‘catalytic state’. Here states “achieve their goals less by relying on their own resources than by assuming a dominant role in coalitions of states, transnational institutions, and private-sector groups”. Weiss suggests that the strength of a ‘catalytic’ state in external interstate coalition depends critically on the strength of the state–business alliance at home. Here, the state’s capacity is strongly affected by its domestic public–private relationship. On the other hand, as an instance of effecting major structural change at the city level, state-led global city formation would oblige the state to show not only “entrepreneurship in the sense of providing the ‘vision’ for the future and building new institutions”, but also to manage the conflicts which would inevitably arise during the process of any structural change (Chang, 2003, p. 46).

To sum up, state-led global city formation in an emerging economy could be considered part of the state’s strategy to lift its national economy from the periphery to the core, as well as developing a knowledge-based economy in the city. Challenging the established global cities is necessarily a difficult process. The state not only has to act as the planner, institution-builder and interest mediator, but also has to change itself and the ways it works. These represent major challenges for an emerging economy, and even more so for a transitional economy, defined as moving from a planned economy to a market economy and having weak market-supporting institutions (IMF, 2000). In the case of China, while the party-state insists on dominant state ownership, which both underpins its domestic power and draws economic strength from it, this also serves to alienate established international market players. How and to what extent has the state risen to these challenges? We seek to answer this question by first examining the planning vision for Shanghai and the evidence of its progress as an emerging global city.

3. Shanghai as an Emerging Global City—State Strategies and Outcomes

3.1 Strategic Visioning and Institutional Building by the State

Turning Shanghai into a global city has been characterised as a ‘strategy-based state project’ (Wu, 2009). However, this strategy has been an evolving and intermittent one, marked by changing visions and unstable relationships between the central and local authorities. The State Council’s (i.e. the central government’s) written approval of Shanghai’s Comprehensive Plan (BSUPPA 1986) states that

After several decades of hard work, Shanghai should be built into [a] socialist modern metropolis with prosperous economy, advanced science and technology, colourful culture, convenient transport, sensitive information and handsome environment. It should also take the role of ‘the important base’ and ‘the pioneer’ in the construction of the modernization of our socialist country.

Evidently at that stage neither the Municipality nor the State Council had a global ambition for Shanghai.

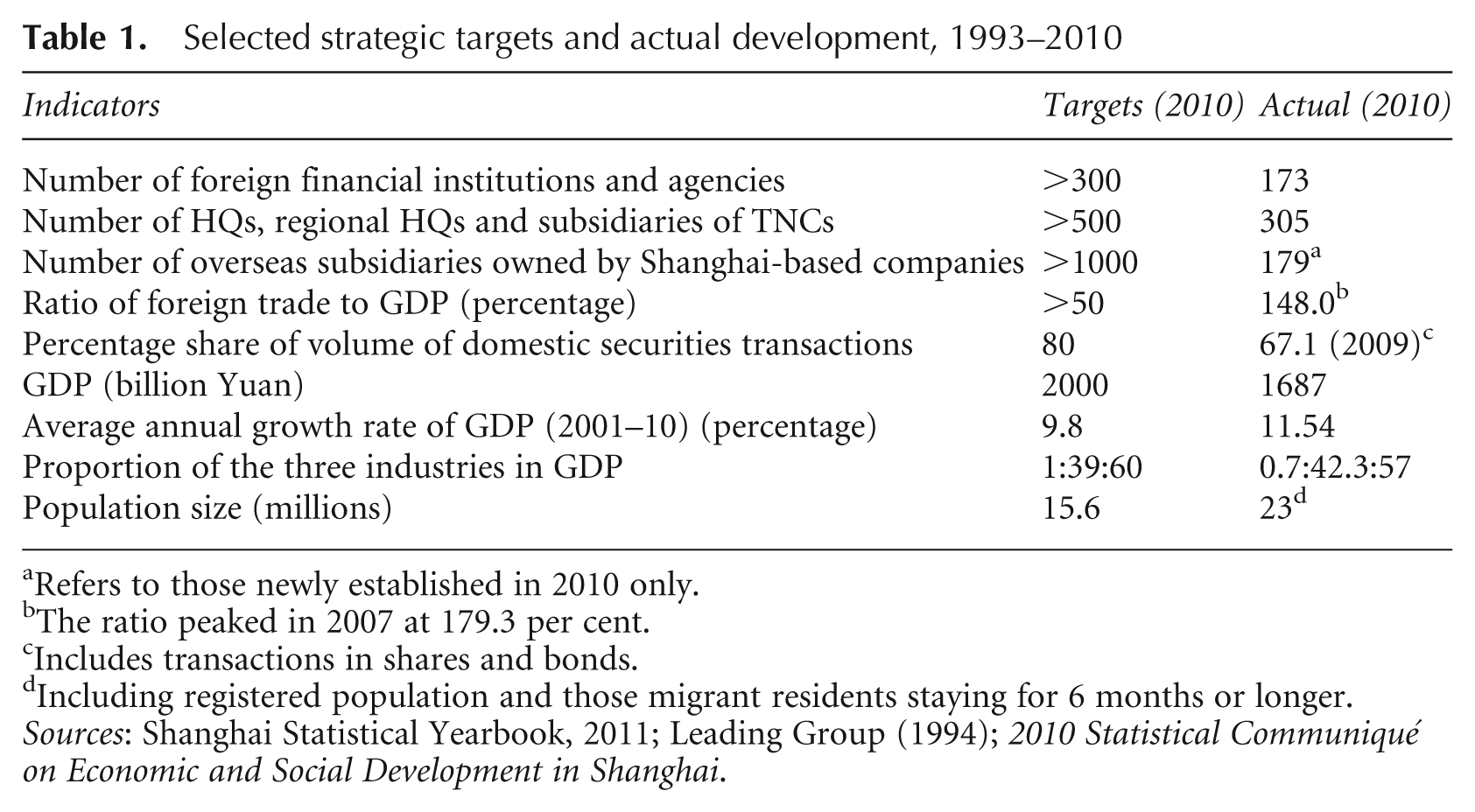

Following the establishment of the Pudong New Area and the opening of the Shanghai Stock Exchange in 1990, however, the 14th Chinese Communist Party Central Committee in 1992 called upon Shanghai to become the ‘dragon head’ of economic growth in the Yangtze River Delta and the whole Yangtze basin, and to turn itself into an international economic, financial and trade centre. This resulted from a major shift in the outlook of the Party following the intervention of the departing paramount leader Deng Xiaoping. The Party decided then to adopt a ‘socialist market economy’, where significant public ownership of productive assets would co-exist with a dominant role of the market in resource allocation (Zhang, 2006). This created an impetus for the publication of an influential research report by the Municipality (Leading Group, 1994), 1 Shanghai towards the 21st Century, in which an ambitious economic and social development strategy (1996–2010) was presented (see Table 1 for key planning targets). The report proposes to turn Shanghai into ‘an international economic central city’ by 2010.

Selected strategic targets and actual development, 1993–2010

Refers to those newly established in 2010 only.

The ratio peaked in 2007 at 179.3 per cent.

Includes transactions in shares and bonds.

Including registered population and those migrant residents staying for 6 months or longer.

Sources: Shanghai Statistical Yearbook, 2011; Leading Group (1994); 2010 Statistical Communiqué on Economic and Social Development in Shanghai.

Further momentum was created in 2001, when the State Council’s letter of approval for Shanghai’s Master Plan indicated that Shanghai should become an international economic, financial, trade and shipping centre. Since then, the mission for Shanghai has been shorthanded as ‘A Dragon Head; Four Centres’. However, there followed almost a decade of relative policy silence from the national government. Two factors may explain this. First, the national politics turned against Shanghai from 2003 (see section 4). Second, Shanghai was preoccupied with the preparation and delivery of the World Expo, another ‘state project’, held in 2010.

It was not until April 2009 that policy momentum seems to have returned to Shanghai. With the world economy in deep recession and the Chinese economy in global ascendance, international expansion became high on the central government’s agenda. In response to Shanghai’s submission, Accelerating the Development of Modern Services and Advanced Manufacturing in Shanghai and Making Shanghai an International Financial Centre and International Shipping Centre, the State Council reiterated that promoting the development of Shanghai as an international financial and shipping centre was “an important measure for our country’s modernisation and further reform and opening-up” (SMG, 2011). It further stated that

By 2020, Shanghai should strive to basically have completed its construction as an international financial centre that is compatible with China’s national economic power and the international status of renminbi.

This indicates that Shanghai’s project to become a global city has for the first time acquired unprecedented national significance.

3.2 Effects

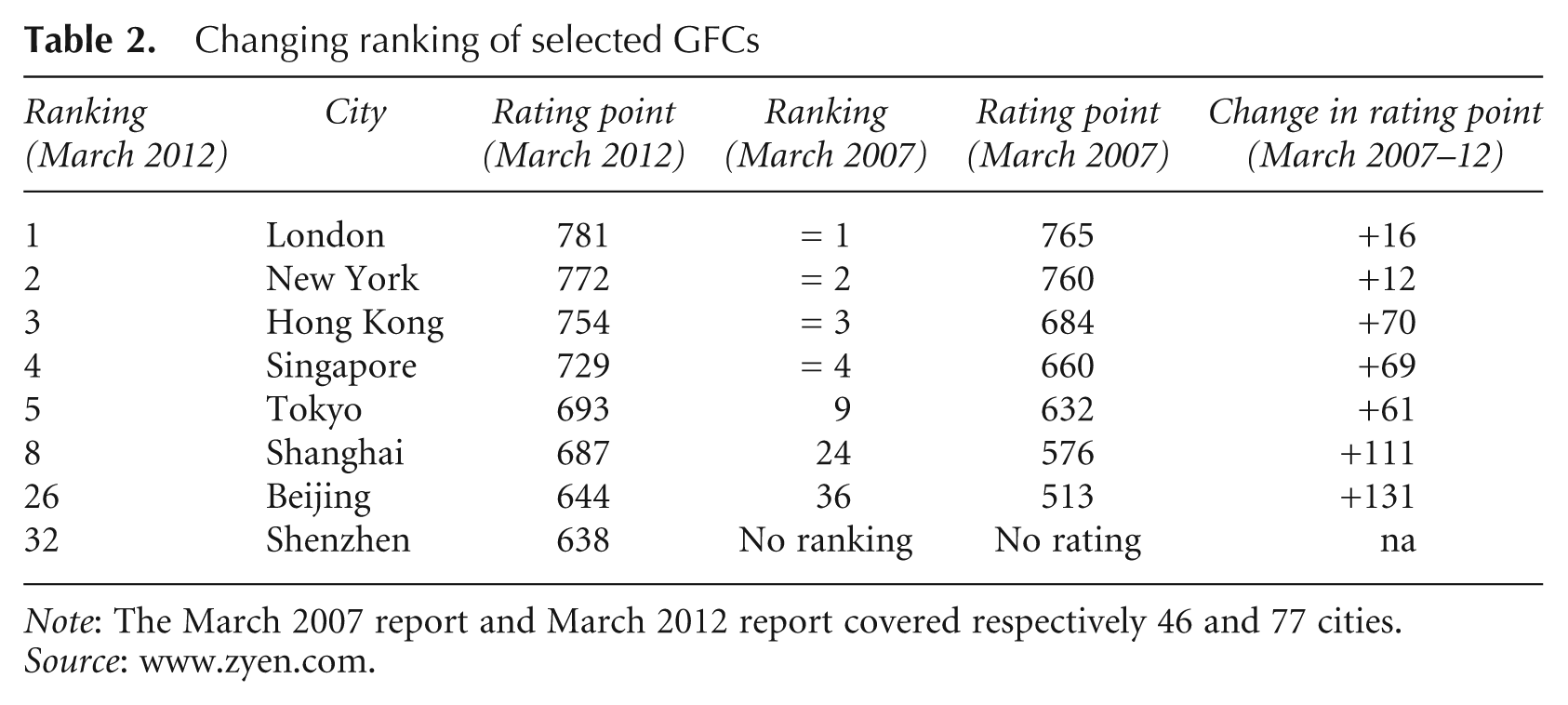

Three different kinds of evidence are used here to assess Shanghai’s progress in global city formation: Shanghai’s changing ranking in the Global Financial Centre Index (GFCI) reports; its changing interlock connectivity measurements; and the outcomes of Shanghai’s strategic targets. Compiled twice a year by the London-based Z/Yen Group since March 2007, the GFCI reports calculated ratings and rankings for several dozen cities by using a ‘factor assessment model’. This model combines two different types of input—i.e. instrumental factors (external indices) and assessment by professionals responding to on-line surveys (Mainelli and Yeandle, 2007). Covering 77 financial centres, the most recent report (March 2012) at the time of writing, uses 80 external indices and responses from 1778 financial service professionals (Yeandle et al., 2012). The theoretical maximum rating of GFCI is always 1000. By contrast, a city’s interlock connectivity is calculated based on actual service values, which represent the importance of a city within a firm’s world-wide office network (see Taylor, 2004, pp. 63–64, for methodology details).

Becoming a global financial centre (GFC)

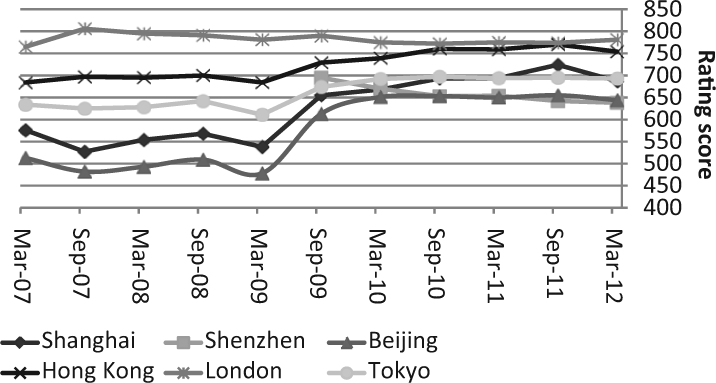

Based on the available GFCI reports, Table 2 and Figure 1 illustrate several important features. First, all the four Chinese cities (Hong Kong, Shanghai, Beijing and Shenzhen) and Tokyo experienced a significant rise in ratings between March and September 2009. The jump is especially big for Shanghai and Beijing, but also obvious for Hong Kong and Tokyo. This illustrates the impact of the 2008 financial crisis and the relative rise of the Asia-Pacific region, rather than just China. Secondly, related to the first point, Shanghai’s ranking in the GFCI reports saw a major improvement between March 2009 and September 2011 (from 35th to 5th). Indeed, it came to tie with Tokyo (in 5th place) in the 9th edition (March 2011) and overtook Tokyo in the 10th edition (September 2011) (Table 2), although it had fallen to 8th place in the March 2012 edition. This has been attributed to concerns about the lack of ‘currency convertibility’ (Yeandle, 2012).

Changing ranking of selected GFCs

Note: The March 2007 report and March 2012 report covered respectively 46 and 77 cities.

Source: www.zyen.com.

Changing ratings of China-based global financial centres relative to London and Tokyo, 2007–12.

Third, Shanghai’s most important competitor, Hong Kong, has done even better and maintained its lead over Shanghai since September 2009 (Figure 1). In fact, Hong Kong has since then consistently taken the 3rd place globally, closing the distance from London (in the top place) in the September 2011 report (although the gap widens again in the March 2012 edition). Fourth and finally, between March 2010 and September 2011, Beijing joined the rank of the top 20 GFCs. Indeed, Beijing improved its rating more than Shanghai during 2007–12 (Table 2). This would seem to suggest that Shanghai’s post-2008 rise as a GFC is as much the effect of the ‘state project’ as the rise of the Chinese, or even regional, economy, since Beijing is not part of the ‘state project’, but a well-established gateway city to the Chinese market (Taylor et al., 2011).

While the GFCI reports put Shanghai significantly ahead of Beijing, studies of the world city network suggest otherwise. Three kinds of measurement have been taken: the command-and-control function, interlock connectivity and the Globalisation Cities Index. While the function is indicated by the headquarter location of top service firms, the Index comprises of city place power (CPP) (50 per cent) and city network power (CNP) (50 per cent). CPP is overwhelmingly determined by a Business Command Index, derived directly from headquarter functions of the Forbes 2000 top firms, whereas CNP is represented by the city’s network position in three sectors (business, financial and media services) in terms of connectivity. Based on 2008 data, Beijing is ranked the 9th in CPP, compared with Hong Kong in 22nd place and Shanghai in 49th place. However, Hong Kong, Shanghai and Beijing are respectively ranked as the 3rd, 7th and 8th city in terms of CNP. Indeed, Shanghai and Beijing are the two cities which improved most in global connectivity during 2000–08. Finally, the overall Globalisation Cities Index, calculated as a percentage of New York’s (100) is 53.75 for Hong Kong, 48.87 for Beijing and 43.37 for Shanghai (Taylor et al., 2011).

Thus the combination of the GFCI reports and the analysis of Taylor et al. (2011) show the following. First, there has been significant global city formation in Shanghai, Beijing and Hong Kong since the turn of the century. Secondly, this process has further accelerated in the wake of the 2008 financial crisis as a result of the relative strengthening of the Chinese and Asia-Pacific economies. Thirdly, there is an intense competition between these three cities. It is also clear that these cities have different sources of power: while Beijing enjoys significant place power and moderate level of network power, Hong Kong enjoys limited place power, but a high level of network power. In comparison, Shanghai enjoys a moderate level of network power, but very limited place power. Therefore, although the CFCI reports, no doubt reflecting the views of the on-line contributors, seem to have written off the prospect of Beijing as a real competitor as GFC, the race may still be open. Indeed, if the experience of Tokyo (relative to Osaka) is any guide (Ryoichi, 2011), then Beijing stands a good chance.

Let us now turn to Shanghai’s outcome in realising its strategic targets. Table 1 shows that Shanghai’s performance has fallen short in several crucial areas. These include the number of foreign-funded financial institutions and transnational headquarters located in the city, the city’s share in the domestic securities market and change in economic structure. However, Shanghai exceeded its planned targets in aggregate economic growth and economic openness. Socially, its population target was exceeded by 8 million: Shanghai’s population had grown from 13 million in 1993 to 23 million by the end of 2010. The next section focuses on the change in economic structure, especially the growth of financial and business services.

Structural change

Changing statistical definition before and after 2003 makes it difficult to identify precise structural changes over the past decade except at a broad level. However, several important changes are discernible. First, there has been a significant deindustrialisation. The share of manufacturing in total employment fell by 8.2 percentage points over 2000–09. Nevertheless, the share of industry in GDP remains high at 42.3 per cent as of 2010, compared with the 2010 target of 39 per cent in the 1994 Strategy (Table 1). Shanghai has thus a long way to go to transform itself into a service-oriented or knowledge-based economy.

Second, employment in high-value specialised financial and business services is low and its growth flat. As Table 3 shows, only five out of a total of 16 sectors have above-average labour productivity. In descending order, these are: finance; real estate; information, computing and software; public administration and social organisations; and industry. However, the share of employment in finance and real estate is low, respectively 2.08 per cent and 3.43 per cent in 2009. Moreover, both shares fell during the period. The fastest employment growth took place (in descending order) in scientific research and technical services; information, computing and software; leasing and business services; accommodation and restaurants; retail and wholesale trade. With the exception of information, computing and software, however, these all have below-average levels of productivity (Table 3).

Employment and productivity changes in Shanghai, 2003–09

Source: Shanghai Statistical Yearbook, 2006 and 2010; author’s calculations.

Third, judged by productivity and employment increases, only two sectors—i.e. retail and wholesale trade, and leasing and business services—stand out: over 2003–09, their productivity rose by 119 per cent and 166 per cent respectively and their employment by 615,200 and 338,600 respectively. However, both sectors’ productivities are below average, which indicates that they are unlikely to be serving high-end international customers. On the other hand, while the sector of information, computing and software registered the third-highest productivity and added 119,000 jobs over 2003–09, its productivity declined over this period. Moreover, its share in total employment is still very small (2 per cent in 2009). Finally, the category of transport, storage and postal services and telecommunications, important to the ‘Four Centres’ function, lost employment weight and experienced below-average productivity growth. In summary, it would seem that Shanghai has had rather limited success in developing specialised producer services.

Economic growth

Shanghai’s smaller economic size relative to Hong Kong was once considered as an important disadvantage (Shi and Hamnett, 2002). However, in the past two decades, Shanghai has made major strides in this respect. Starting with an economy only 21 per cent of Hong Kong’s size in 1990, Shanghai’s GDP surpassed Hong Kong’s for the first time in 2009 (Leung, 2010). Not only was this 26 years earlier than expected by Shi and Hamnett (2002), it was apparently 9 years earlier than expected by the Hong Kong Trade Council (Leung 2010). Rapid population growth and the relative appreciation of the renminbi helped.

This examination shows that, although Shanghai has made some progress in global city formation and in enlarging its economy, it is still limited in developing specialised financial and business services, not to mention global control capability. As an emerging global city, it is still overshadowed by Hong Kong and it is also behind Beijing in important ways. Structurally, Shanghai’s transition from an industry-oriented economy to a service-oriented economy has only just begun. These are the consequences of the many constraints on the local and central state’s capacity to intervene.

4. Constraints on the State

4.1 Inflexibility in the Orientation of the State–Market Relationship

There are three particularly important issues here. First, the physical distance between Shanghai and the Chinese capital Beijing is a major disadvantage to Shanghai. As a socialist market economy, China’s current economic system is characterised by strong state ownership of important assets, especially in the financial and industrial sectors. A majority of the Chinese financial institutions, including the four largest Chinese banks, and Chinese TNCs are owned by the central government and headquartered in Beijing. Indeed, since the relocation of the Bank of Telecommunications from Beijing to Shanghai in 1990, no other major Chinese bank has followed suit. On the other hand, of the 42 Chinese companies featured among the Fortune Global 500 companies in 2010, 30 (71 per cent) were headquartered in Beijing, three in Shanghai, two in Shenzhen, one in Hong Kong, with the rest (six) in five other cities inside China. 2

Second, as a transitional economy, China is far behind Hong Kong in economic openness and freedom, something much valued by international financial investors and institutions. According to the Fraser Institute, which compiles the Economic Freedom of the World report, Hong Kong has maintained its top spot as the world’s most free economy since the 1980s. Meanwhile, China occupied the 82nd place in the Economic Freedom Index in 2010. 3 Thus Shanghai continues to lag significantly behind Hong Kong in terms of market development (Subacci et al., 2012).

The third issue is the continuing non-convertibility of the renminbi. Here the central government is concerned about balancing the gradual relaxation of exchange control, crucial to China’s financial internationalisation as well as Shanghai’s global city status, and the minimisation of possible risks that this relaxation might bring the real economy, especially export-oriented manufacturing. China introduced current account convertibility in 1996, but retains capital account non-convertibility. To minimise risk, the centre has apparently decided to use Hong Kong as the launch pad for the gradual internationalisation of the renminbi. It has actively supported the development of Hong Kong as its preferred offshore centre for renminbi-denominated assets (Liu and Chiu, 2009). It would seem that, as a catalytic state, the central government is using Hong Kong, which officially retains a capitalist system until 2047, to manage China’s financial internationalisation. Thus Shanghai is unable to benefit from the historical opportunity of internationalising the renminbi, at least for the moment.

4.2 Central–Local Politics

Both theory (Jessop, 1990; Friedmann, 1986; Olds and Yeung, 2004) and practice (for example, Wang, 2003) suggest that there are often divergent interests between the central and local governments in global city-making. Despite the unitary party-state, this is also the case in China (Beeson, 2009). While the central government is primarily interested in strengthening its power both at home and abroad, local government is more concerned about maintaining strong revenue streams and promoting local economic growth. However, in a transitional economy like China’s, policy concessions from the centre bestow important economic advantages on those that are either liberalised or allowed to liberalise before others. Recent studies of the relationship between network centrality and power in the world city network literature shed useful light on this issue. Neal (2010, p. 1) demonstrates that “a city’s powerfulness depends on the lack of centrality of the cities to which it is connected”. Thus a city like Hong Kong that has the central government’s blessing can go a long way in its global city formation, as such a blessing effectively enhances Hong Kong’s power by maintaining the low centrality of other Chinese cities.

In its relationship with the centre, Shanghai has not fared very well in recent years. For instance, the share of the revenue that Shanghai can claim from stamp duty receipts has been gradually reduced from 50 per cent to 20 per cent (from 1997), then to 12 per cent and eventually 3 per cent (from October 2000 onwards) (Wang, 2011, p. 43). While it initially benefited from substantive policy concessions from the central government through the establishment of the Pudong New Area in the early 1990s, its policy advantage has been weakened in recent years by the establishment of the Binhai New Area in Tianjin (in the north) in 2004 and the designation of the Liangjiang New Area in Chongqing (in the west) in 2010. A related fact is that, with the departure of Jiang Zemin (the former Chinese President and Shanghai ex-mayor) from Chinese politics in 2003, Shanghai has lost a strong supporter in the central government. On the other hand, Shanghai has shown weaknesses in its governance and its relationship with the wider region. Shanghai Municipality’s reputation was tarnished by the discovery of the misuse of its pension fund (for property speculation) in 2006 and the consequent removal (in 2006) and eventual imprisonment of the former Party Secretary Chen Liangyu in 2008 for 18 years. On the other hand, Shanghai’s performance as the ‘dragon head’ of the Yangtze River Delta and Yangtze Basin lacks the depth and breadth of the economic links between Hong Kong and its hinterland, the Pearl River Delta (Sung, 2011). The most recent central government pronouncement (2009) on Shanghai contains few real concessions, except for furthering Shanghai’s shipping centre function.

4.3 Intercity Competition

Given administrative decentralisation, Chinese cities and provinces are constantly in competition with each other over winning policy concessions from the central government and winning businesses in various markets. The commodity ‘wars’ that erupted in the 1980s have been followed by furious competition for high-value financial and business services. Shanghai is challenged not only by its traditional competitors such as Hong Kong, Beijing and Shenzhen, but also by Tianjin and Chongqing. Perhaps in recognition of this situation, Shanghai’s 12th Five-year Plan proposes that, by 2015, the city’s share in the direct capital raised in the domestic capital market should reach 30 per cent (up from 25 per cent in 2010), much lower than one might expect.

Competition with Hong Kong is surprisingly strong. This is partly due to the deft way in which the Hong Kong Special Administrative Region has handled its relationship with the central government in Beijing. Successive governors and their administrations have tirelessly sought to gain policy concessions from Beijing and increase integration with the mainland in order to benefit from the latter’s prosperity. For instance, shortly after the completion of the 11th national Five-year Plan, Hong Kong started to explore how Hong Kong should be involved in the preparation of the 12th five-year plan despite its autonomous status (Liu and Chiu, 2009). This has paid off. While the 12th Plan contains only one mention of Shanghai’s function as ‘four centres’, it devotes almost a whole paragraph to Hong Kong and states the intention

to continuously support Hong Kong to develop finance, shipping, logistics, tourism, professional services, IT and other high value-added services; support the development of Hong Kong as an offshore renminbi transaction centre and international wealth management centre; support Hong Kong’s development in high-value warehouse management and regional wholesale centre; consolidate and raise Hong Kong’s status as an international financial, trade and shipping centre; strengthen its global influence as a financial centre (NDRC, 2011, p. 123, the author’s translation).

Following this, the central government announced a set of 36 supportive measures for Hong Kong in August 2011 (Lianhe Zaobao, 18 August 2011).

4.4 Other Constraints

Shanghai’s attempt to develop global control functions has so far suffered from a number of other constraints. For instance, like other Chinese coastal cities, Shanghai in the early 2000s aggressively engaged in place-making activities through extensive real estate development (Wu, 2009). However, concerned with spiralling real estate prices and the possible threat to social stability, from the mid 2000s the central government has introduced a series of increasingly tough policy measures to dampen this sector’s expansion (Wang, 2011). As a consequence, the real estate sector has stagnated in Shanghai in recent years (Table 3).

On the other hand, as shown earlier, Shanghai has found it difficult to reduce more quickly its large manufacturing sector to replace it with high-value service jobs. It has failed to add jobs where labour productivity is high and only succeeded where productivity is relatively low. It has also been weak in creating jobs in education, health, personal and social services (Table 3). Thus Shanghai has been slow in developing ‘knowledge complexes’.

There is also strong evidence that policy actions by the Municipality have at times been constrained by changing national policy priorities. Analysis of the Municipality’s annual work plans since 2004 shows that the Municipality has grappled with changing central priorities echoing the centre’s: kejiaoxingshi (development through science and education) (2004–06); development of a resource-efficient economy and an eco-friendly society (2006–08); development of the ‘Four Centres’ and industrial upgrading (especially towards modern services) (2006–10), while comprehensive reform in Pudong and the preparation and delivery of the World Expo were on the agenda throughout. 4

By contrast, Hong Kong has been largely left alone to focus on its strategy of becoming China’s premium service provider, as well as an investment and tourist destination. On the other hand, by exploiting the opportunities created by mainland China’s recent economic expansion and through ever-closer integration with the Pearl River Delta (and even the rest of China) and by positioning itself within the national planning system, Hong Kong has been able to make itself more global as well as more Chinese. Liu and Chiu (2009, p. 115) observe: “Instead being disembedded from the larger national and regional contexts, Hong Kong is becoming a Chinese global city”.

5. Conclusions

Despite persistent efforts by the local authority and rising national economic power, Shanghai’s progress in global city formation is relatively slow. This is due to the numerous external and internal constraints that the city government is under, as well as underlying economic barriers. While some of the constraints (such as dominant state ownership and the West’s hostility) are specific to China, numerous others may apply to other emerging global cities, including

(1) the relatively underdeveloped condition of the market and institutions;

(2) competition from other domestic cities;

(3) national–local politics, as well as

(4) the inherent difficulty in developing knowledge complexes and global corporate control capability in a transitional emerging economy context.

Nevertheless, the rise of Hong Kong, Beijing and Shanghai shows that there are good prospects for emerging global cities. Moreover, the central state can play an important role by stimulating economic growth and implementing liberalisation. In particular, like Tokyo and Seoul, Beijing’s ascendance shows that fostering domestic TNCs is at least as important as attracting other TNCs.

As for the global/world city scholarship, this study demonstrates that greater attention needs to be paid to studying the dynamics of how fast economic growth, domestic socioeconomic characteristics, activities of home-grown TNCs and emerging economies’ internationalisation strategies can significantly influence global city formation.

Footnotes

Acknowledgements

The author wishes to thank the three anonymous referees for their constructive comments on earlier versions of this article, and Professor Nigel Harris for his generous advice on the final revision.

Funding

This research received no specific grant from any funding agency in the public, commercial or not-for-profit sectors.