Abstract

The World Bank’s ‘Doing Business’ reforms were originally expected to help the growth and formalisation of SMEs and micro enterprises. The expectations that reforms would support the growth and development of SMEs were challenged by scholars, but the reforms’ impact on the micro enterprises of the poor has received little scholarly attention. Drawing on a desk study and on field studies of street-vendors carried out in Tanzania in 2007 and 2011, this paper argues that the growth and formalisation of micro-businesses are badly served by the ‘Doing Business’ reforms.

1. Introduction: the ‘Doing Business’ Reforms and Critiques

One response to the failures of the Washington Consensus to stimulate growth in poorer countries of sub-Saharan Africa has been the development of a new international consensus, focusing on institutional reform and aiming to stimulate economic development through greater integration with the global economy and attraction of inward investment, and increasing locally raised tax revenues to empower governments. In 2004, the World Bank established the ‘Doing Business’ project, as part of general efforts to use private-sector development to reduce poverty and stimulate economic growth world-wide, through four broad initiatives: country benchmarking, reform design, aid monitoring and informing theory. The project stemmed from a long lineage of interest in law and development culminating in the ‘New Institutional Economics’, and emphasises legal institutions that support particular political and civil rights and market-based economies (Davis and Kruse, 2007).

The first report in 2004 produced data from 133 countries, now expanded to 183. The project developed a raft of indicators based on two types of data: readings of local laws and regulations, and cost and time-mapping of the efficiency of achieving a particular goal (IFC and World Bank, 2012). Indicators are updated on an annual basis and are accompanied by a series of recommended ‘reforms’, collectively known as the ‘Doing Business’ reforms. The reforms are focused on the formal sector with the hope that they measure some factors that explain the occurrence of a large informal economy (IFC and World Bank, 2012).

The ‘Doing Business’ reforms include: improvement of the justice system; expansion of access to credit and other financial services to release investment; simplification of registration, licensing, transferring and closing a business; ensuring property rights through improvements in registration and through access to justice; implementation of liberal trade and investment rules including an open-door policy towards foreign direct investment; simplification of customs procedures to give low average tariffs and less spread in tariffs; limiting government intervention in labour and credit; and simplification of taxes for small businesses. To access the benefits and obligations of reforms, businesses must register with national tax authorities and provide a fixed business address. In effect, businesses are required to formalise (World Bank, 2004). National programmes have adopted their own names for the ‘Doing Business’. 1 The detail of reforms is discussed in section 3, but the present section focuses on the development of arguments and counter-arguments regarding the reforms’ impact on poor micro entrepreneurs, many of whom operate informally.

The 2005 World Development Report, entitled A Better Investment Climate for Everyone, sets out the Bank’s expectations. The Report highlighted the importance of poor micro entrepreneurs in the economies of developing countries, stating that Hundreds of millions of poor people in developing countries make their living as micro-entrepreneurs—as farmers, street-vendors and homeworkers, and in a range of other occupations, a large share of them women … They are a big part of the informal economy, which is substantial in many developing countries (World Bank, 2004, p. 33).

Essentially optimistic about the inclusive potential of reforms, the report argued that individual entrepreneurs and micro enterprises (businesses that employ up to five people) would benefit from the same measures that improve the opportunities and incentives for larger firms. Poor micro entrepreneurs specifically would benefit from lower costs of ‘Doing Business’ (for example, less red tape and corruption); from lower risks (more secure property rights and less policy uncertainty); from reduced barriers to competition (by expanding opportunities and reducing the costs of inputs) and from improved access to credit (World Bank, 2004, p. 60). Furthermore, development of a climate conducive to investment was expected to reduce poverty through growth in GDP (p. 3) and through the creation of private sector jobs.

This report drew criticism from some economists and social scientists who were less confident of the benefits to SMEs. Scholars argued that the recent private-sector development debate among donors rests on a ‘highly optimistic’ belief in the ability of markets (alone) to generate public welfare (Altenburg and von Drachenfels, 2006, pp. 388, 396).

This approach was termed a “new minimilism” by Altenburg amd von Drachenfels (2006, p. 396). The key argument is about the potential of these widely endorsed reforms to stimulate economic growth without disenfranchising the poor—or simply relatively small businesses such as SMEs.

For example, some scholars argued that the development of simplified property registers, company registers and personal identity registers, would externalise costs to users and disadvantage small businesses, who would have fewer resources to seek out the necessary supplementary information (Arruñada, 2007). Others argued that the formalisation of residential property rights had failed to stimulate credit markets among the poor in urban Latin America, reluctant to mortgage their prime asset (Durand-Lasserve and Selod, 2007) and this, by extension, cast doubt on the usefulness of asset titling for the stimulation of business-related credit in sub-Saharan Africa. Others pointed out that, in sub-Saharan Africa macroeconomic growth has not widely translated into poverty reduction (von Braun and Keyzer, 2006), while governance reforms have tended to increase concentrations of power at the top, reducing the voice at the grassroots (Bendaña, 2004). Some analysts suggested that the reforms would lead to the development second-rate institutions (Rodrik, 2008), that they contained contradictions (Trubek, 2008) and that despite their good intentions they were unlikely to achieve their goals on any scale (Otto, 2009).

The World Bank’s own stance on the potential impact of the reforms on poor micro entrepreneurs has become more cautious over time as to their likely benefits. Thus the 2006 World Development Report, focusing on Equity in Development (World Bank, 2005), implicitly recognises that policy reform will not necessarily benefit everyone. It highlights national differences in the roles of informal own-account work in the importance of historical factors, such as apartheid and intraeconomy sectoral differences as some of the factors influencing the adoption of micro enterprise as a labour market niche by the poor (for example, World Bank, 2005, p. 187).

The 2007 report on Development and the Next Generation, highlights the importance of youth unemployment (World Bank, 2006, pp. 98–100) and identifies street-vending as an entry-level occupation in poorer countries such as Burkina Faso, The Gambia, Nicaragua, Paraguay, Rwanda, and Sierra Leone, [where] many of the young are more likely to begin work in the informal sector … Although this sector will not solve all issues of youth employment—even selling on the street requires some sales skills and language skills and conditions can be harsh—evidence suggests that it can be a remarkably resilient and productive stepping stone, sometimes to formal employment (World Bank, 2006, p.13).

It is clear that the report is cautious about the chances of young people in the sector. The report also stresses the heterogeneity of micro entrepreneurship, citing the ILO’s advice that policy should enable upward mobility, identifying the limitations on mobility for women and youth, and citing caveats in the form of enabling conditions for upward mobility, including training, microfinance opportunities and so on (World Bank, 2006, pp. 14 and 15). These conditions are clearly not expected to arise from the reform programme as it stands.

And there the matter rests. The focus of the World Development Reports of 2008, 2010 and 2011 (World Bank, 2007, 2009, 2010) shifted respectively to the agricultural sector, climate change and security. Despite the well-established links between vending in urban areas and rural poverty alleviation; climate change, rural–urban migration and informal-sector urban jobs; and the flourishing of urban micro enterprises in times of civil unrest, these reports do not track in any depth the impact of their recommendations on urban micro enterprise, or on small own-account informal economic activity. The 2009 report, Changing Economic Geography (World Bank, 2008), cites the importance of both internal and international migration (the latter suitably regulated) to both rural and urban poverty reduction, and of informal vending as an entry-level occupation for, mainly, young migrant men; but the issues are not explored in terms of the likely impact on this of the ‘Doing Business’ reforms.

Focusing on street-vendors as a case in point, the paper aims to examine how the ‘Doing Business’ reforms have impacted on the micro enterprises of the poor.

2. Street-vending as a Key Form of Micro Enterprise

The failure of the Washington consensus laissez-faire policies to reduce poverty and stimulate agriculture or manufacturing has been well documented. Sub-Saharan African economies have not integrated into global production chains or increased export volume and share; improved their ability to face competition from foreign imports; or integrated their rapidly growing informal sectors into international labour markets. Thus the decline in the size of the formal economy, begun when Structural Adjustment Programmes forced millions of urban sub-Saharan Africans into the informal sector to survive, has continued. The informal sector is thought to account for between 35 per cent and 45 per cent of GDP in most developing countries. It was estimated to comprise some half a billion people in 2005, of whom about half are poor, own-account, micro entrepreneurs (Kaplinsky, 2009; Gordon, 1996; Gore, 2000; Subramanian and Matthijs, 2007; Schulpen and Gibbon, 2002; Potts, 2007; Schneider, 2007; UNDP, 2008a).

Street-vending is a key element of this informal economy and important to surviving poverty and to the escape from poverty in developing countries. In the decade up to 2002, it was estimated that over 90 per cent of new non-agricultural jobs were informal, with street-vending and home-working the largest sectors. Indeed, street-vending has been estimated to involve hundreds of thousands of sole vendors in any major African city. Street-vendors are often the main income earner supporting large families of dependents, and street-vending allows children of the poor to continue in education and rural families to benefit from remittances (ILO, 2002; UNDP, 2008a, 2008b; Skinner, 2008a; Potts, 2007; Lyons and Msoka, 2009; Lyons and Brown, 2010).

Two key forms of informality render street-vending vulnerable to legal enforcement and contribute to the slow rates of business growth and frequent business failure. The first, and probably most widely discussed, is spatial informality. It is by now well understood that freedom from evictions is critical to sustainability and capital growth, and that efforts by government to provide legal trading space often fall short by moving vendors to uneconomic locations, or providing insecure or costly tenure arrangements. It is this spatial informality that most often brings vendors into open confrontation with the law and the public. However, street-vendors are informal in terms of business and commercial law as well, limiting their potential for growth and making them vulnerable in principle to further legal prosecution through additional routes. However, the implications of this aspect of informality are rarely explored.

3. Context and Methods

Tanzania offers an unique insight into these issues. First, like most countries in sub-Saharan Africa (SSA), its informal sector is large, with a turnover estimated at 36 per cent of GDP, comprising 91 per cent of all businesses and valued in 2005 at US$28 billion, or 10 times the amount received in the country under development aid since independence (Schneider, 2007; ILD, 2005a).

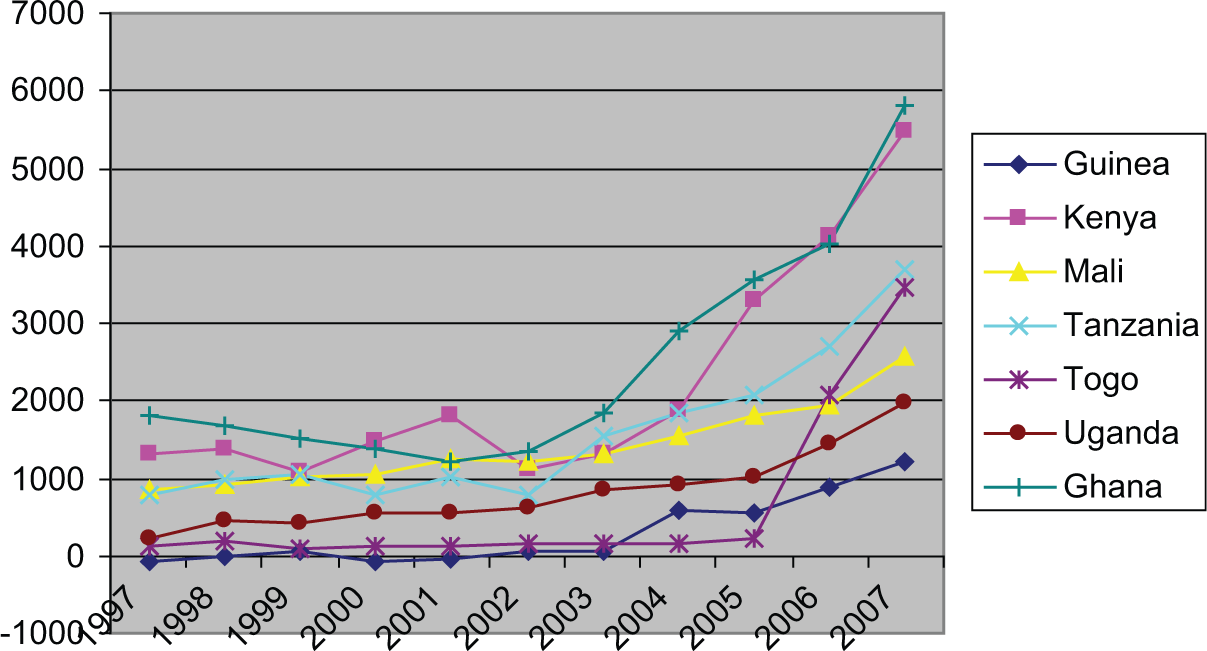

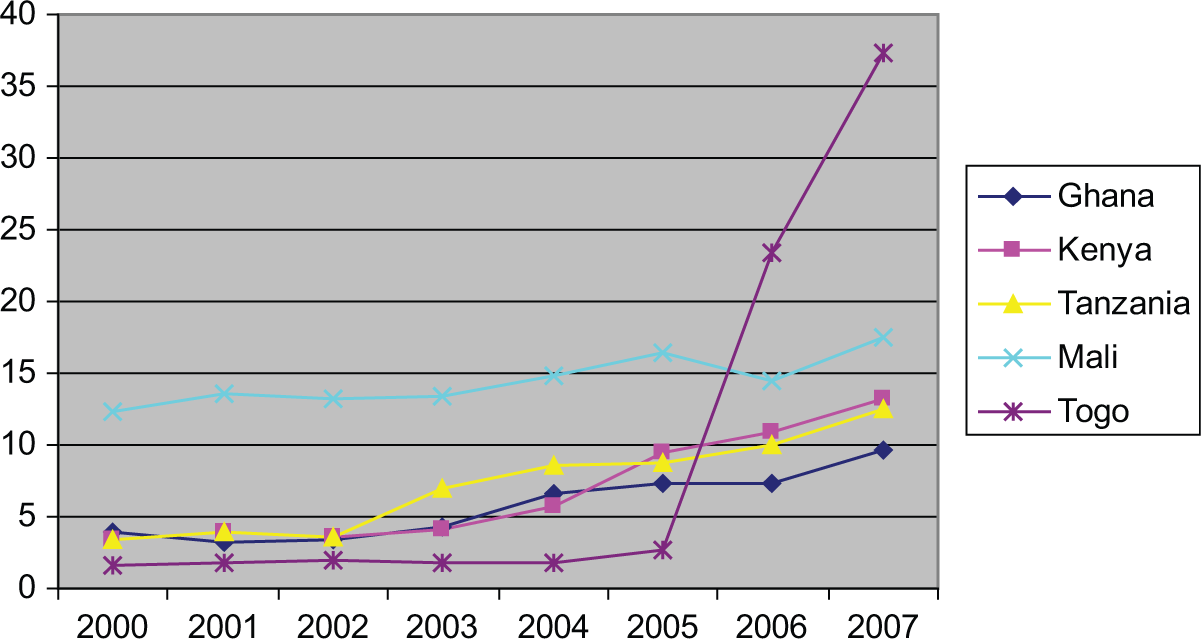

Secondly, like most SSA countries, the import of manufactured goods, for example from China, has grown rapidly over the past decade, both in absolute terms and as a proportion of GDP (Figures 1 and 2). The growth of imports in SSA has coincided with a decline in manufacturing and in the export of agricultural products and manufactured goods, and with continued falls in manufacturing employment and wages. This has combined with limited opportunities for paid work in other fields to stimulate growth in the street-vending sector (Olayiwola and Ruthaiwila, 2010; Kaplinsky, 2009; Giovannetti and Sanfilippo, 2009; Viloria, 2009).

Balance of trade (imports less exports) 1997–2007 (US$ million).

Balance of trade (imports less exports) as a percentage of GDP.

Finally, the country has demonstrated a steady commitment to the ‘Doing Business’ reforms. The ‘Doing Business’ reforms were introduced in Tanzania in 2006 with the accession of the newly elected President Jakaya Kikwete. Their introduction coincided with the marginalisation of the on-going Business and Property Formalisation Programme (MKURABITA), established in 2004 by his predecessor President Benjamin Mkapa. The MKURABITA reforms broadly followed the principles of Legal Empowerment of the Poor and were developed by MKURABITA in the President’s office with de Soto’s Institute for Liberty and Democracy (ILD) as external consultants. The first phase of the MKURABITA reforms, an analysis of the informal economy and of its legal archetypes, had by then been published (ILD, 2005a, 2005b). Despite their marginalisation, MKURABITA and the ILD have continued the reform design process, publishing a seven-volume set of proposals for business and property formalisation in June 2007 the first of which was passed by parliament in April 2012. However, these proposals, based heavily on the premise that existing ‘extra-legal’ practices should provide the basis for modern legislation, not been prioritised. We discuss the MKURABITA reforms and their critiques elsewhere (Lyons and Brown, 2009) but it is important to note that, while MKURABITA’s proposed reforms to business legislation could be seen as paralleling the ‘Doing Business’ reforms in their emphasis on the institutional barriers to formal business practices by the poor, MKURABITA’s proposed land-law reforms are closely integrated with the ‘Doing Business’ reforms and have been subject to many of the same criticisms (Otto, 2009; Payne et al., 2009; Altenburg and von Dracenfels, 2009; Aruñada, 2007).

Tanzania addressed the challenge of instigating the ‘Doing Business’ reforms in 2005 by establishing a Better Regulation Unit (BRU) in the Prime Minister’s Office to oversee and co-ordinate the reforms. Two key sub-units were established: the Business Environment Strengthening for Tanzania programme (BEST), which had responsibility primarily for land titling, business registration and related reforms; and the Financial Sector Deepening Trust (FSDT), which was tasked to support the development of supply-side reforms to the financial sector.

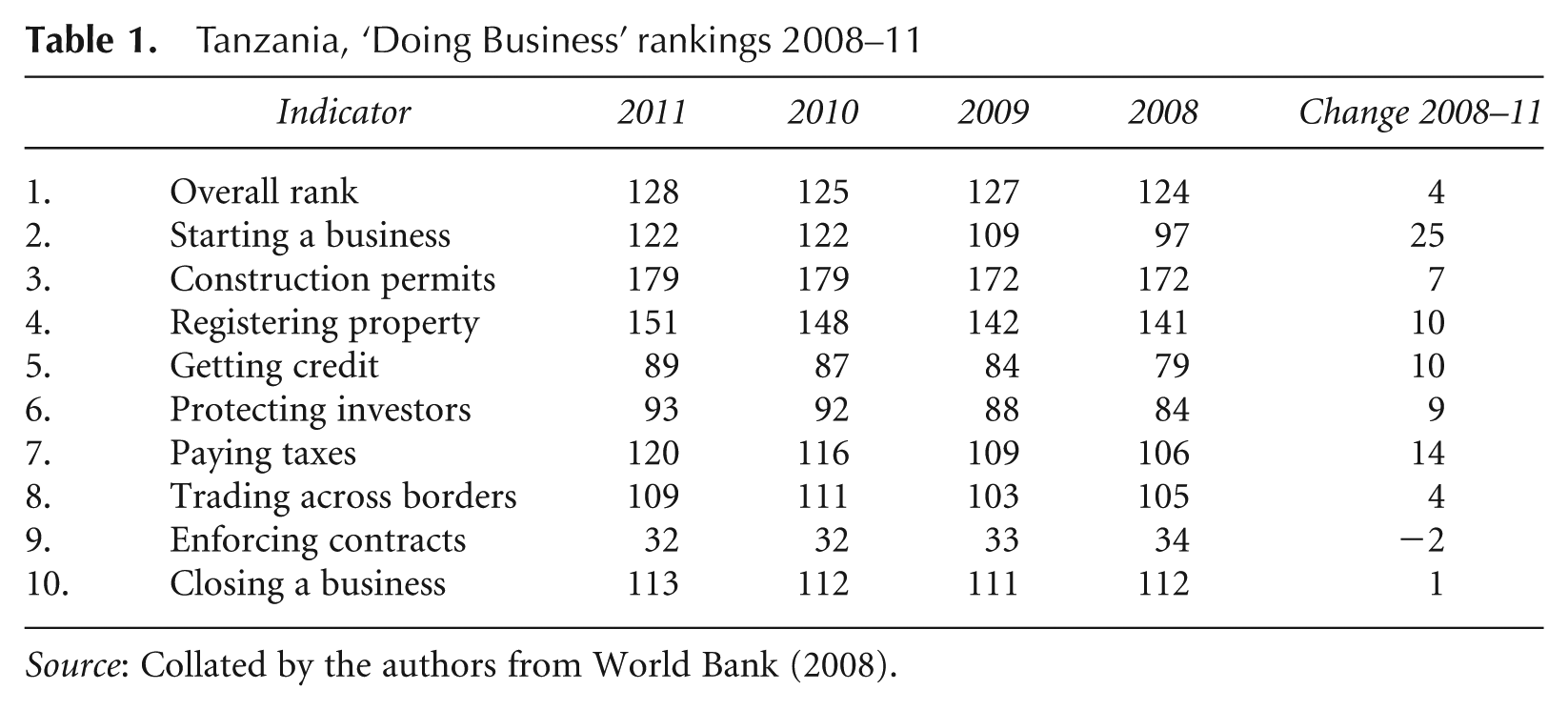

In 2011, Tanzania, 127th in the World Bank’s Ease of ‘Doing Business’ rankings, was above the SSA average (World Bank, 2011c). Tanzania made rapid strides initially in the rankings and was named Regional Star Performer in its second year, 2007 (World Bank, 2006), although it has since slipped back in the charts, subsequently improving more slowly over time, with a negligible 5-year ‘Doing Business’ score improvement of 0.08. In the shorter time-frame since 2008, its ranking improved by four points from 124 to 128, with some fluctuations between (Table 1).

Tanzania, ‘Doing Business’ rankings 2008–11

Source: Collated by the authors from World Bank (2008).

The paper draws on a desk study of legislation, policy documents, official reports and academic critiques to understand the ‘Doing Business’ reforms and how progress on the reforms is measured, and to highlight their likely impact on micro enterprises, with a particular sectoral focus on street-vendors.

The paper draws on a seven-municipality survey (Arusha, Mbeya, Morogoro, Mwanza and, in Dar es Salaam, Ilala, Kinondoni and Temeke) in 2007, funded by the European Commission, which included in-depth semi structured interviews with 622 street-vendors in the seven municipalities, 10 interviews with vendor associations and 120 key-informant interviews. This was followed by a comparative study in 2011 of legal and regulatory barriers to street-vending in Dar es Salaam, funded by DFID/ESRC, which included 173 interviews with street-vendors working in marginal locations, of whom 90 respondents were asked to complete additional interviews focusing on microfinance. Key-informant interviews were undertaken with vendor associations, government administrators and other experts. The street-vendor interviews in both studies analysed business data, formal and informal dispute resolution, personal and business histories, use of financial services, and legal and other barriers to development. Data from both studies are drawn upon for understanding the impact of ‘Doing Business’ reforms on the sector.

4. Street-vending in Tanzanian Society and Economy

Street-vending, normally a micro enterprise, is an important livelihood strategy for the poor and provides support to both nuclear and extended families in both urban and rural areas.

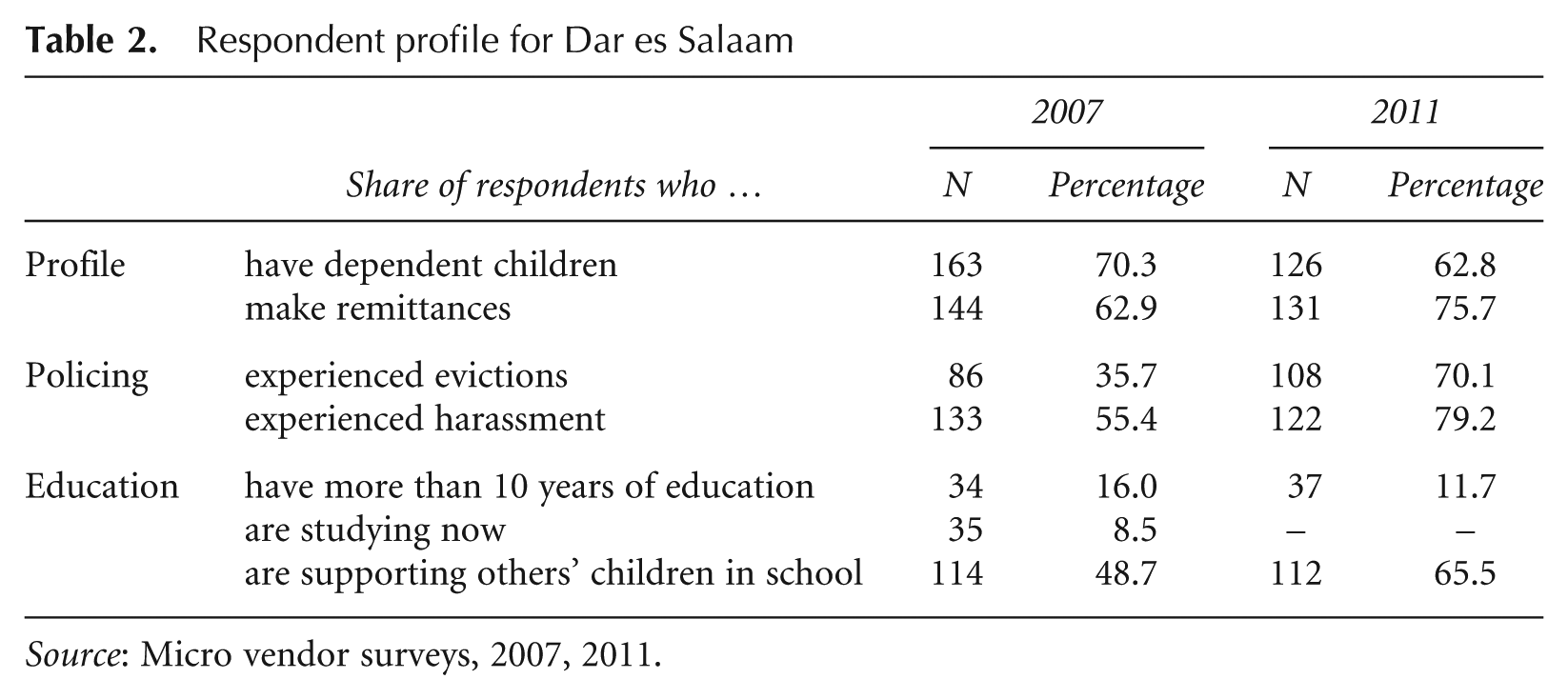

Nationally, street-vendors are critical to their household economies: in the 2007 survey, 78 per cent of respondents were main breadwinners and 62 per cent were sole breadwinners. Yet respondents also contributed financially to extended families in their areas of origin: In a context in which close to 65 per cent of respondents are rural–urban migrants, the potential for support to rural areas is significant. Among respondents, 59 per cent of rural–urban migrants made remittances (as did 46 per cent of other vendors). Table 2 compares vendors interviewed in Dar es Salaam in 2007 with vendors interviewed there in 2011, demonstrating the continuing importance of vendors to the remittance system.

Respondent profile for Dar es Salaam

Source: Micro vendor surveys, 2007, 2011.

Street-vending was not seen as an easy livelihood, but was perceived by most respondents as the only viable form of paid employment open to them. Some had hoped to start alternative businesses, but had been blocked by lack of capital and most had tried to obtain formal jobs and failed because of limited education. In DSM in 2007 and 2011, 78 per cent and 84 per cent respectively had completed Grade Seven primary school, but had no secondary or vocational qualifications (Table 2 shows that only a very small percentage has more than 10 years’ schooling).

Despite their own fairly limited educational attainments, the commitment to children’s education was widespread. In 2007, nationally, 78 per cent of vendors aged 25 and above had dependent children, while 63 per cent were financially responsible for the education of at least one child, either their own or those of a relative. In DSM in 2007 and 2011, 48.7 per cent and 75.5 per cent respectively were responsible for the education of others’ children.

Given the importance of education in accessing formal jobs, vendors see their own education and that of their children and dependents as necessary to upward mobility. In open questions, vendors speak of children’s education as a prime reason for their business activities, as illustrated I am worrying if my sons and daughters can manage to study up to the university levels. I will … even ask for a loan to make sure my sons and daughter are studying in university (Arusha, seedling seller). Between 1994 and 2005 business was very promising. I managed to … send my children to schools. Since 2006 [following eviction] business has become very difficult … [all] I get is merely for daily bread (household goods seller, auction market, Mwanza). It is this market, started in 1976, which enables us to pay for our children’s school fees, medical expenses, feeding our families. But legally people were not allowed to trade here …(Vitenge seller, Magomeni Market area, DSM). I was a successful businessman till 2006, as was also my wife who sells used clothes. Since the government started … eviction … I am failing to pay fees and basic needs for my girl student at UDSM who is in first year. Life is discouraging (evicted from central Morogoro to Kikundi Market).

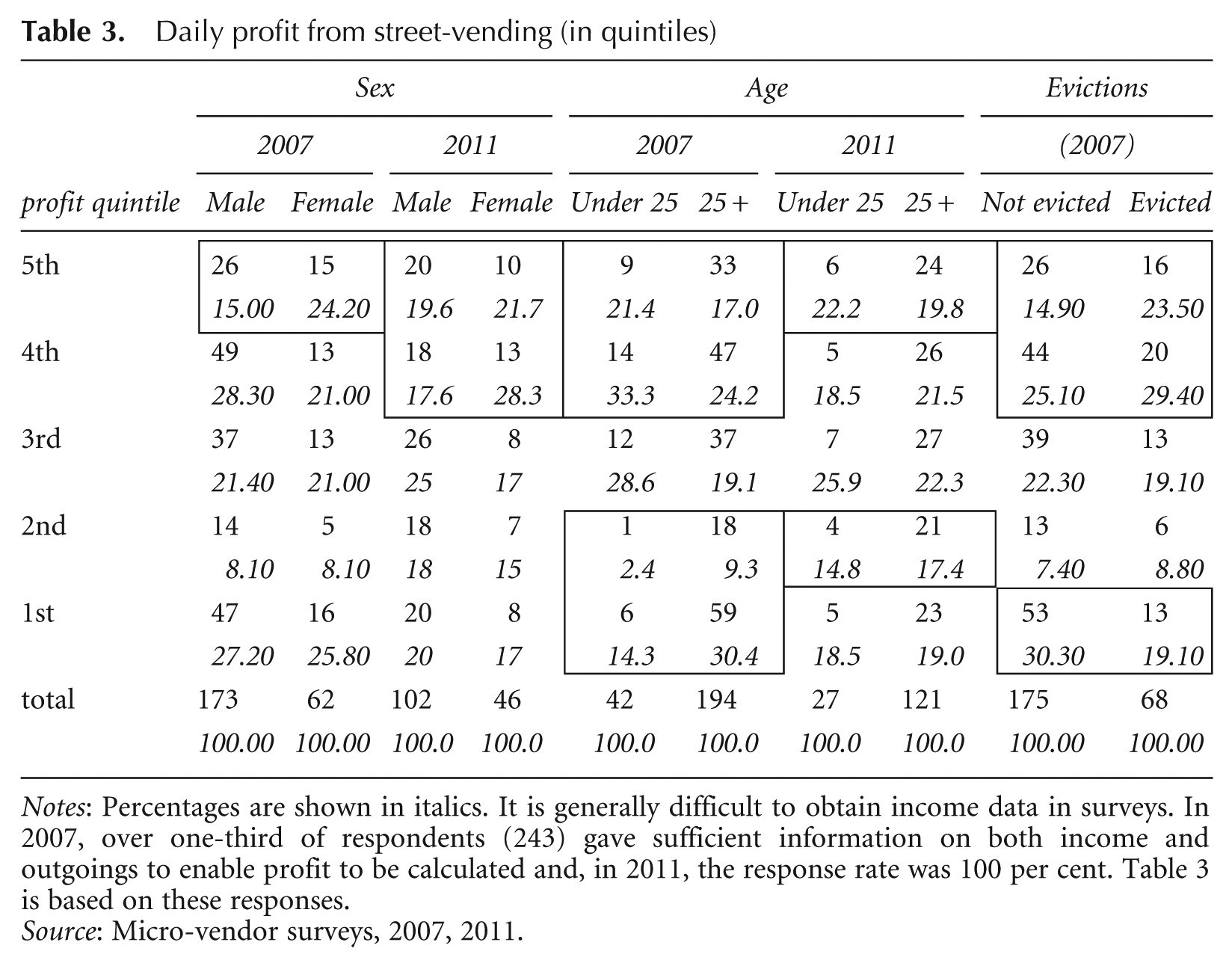

Street-vending represents the most likely avenue of paid employment for the poor but the extent to which it enables livelihoods to develop beyond subsistence varies widely. Table 3 shows some of the important determinants of business profitability. For comparability, daily profits in Tsh have been grouped into quintiles (thus, the 5th, lowest quintile includes earnings of up to 3000 Tsh in 2007 and 3500 Tsh in 2011, in both cases equivalent to earnings under US$2.40 per day; while the 4th quintile is equivalent to US$2.41 per day to US$4.80 in 2007 and US$3.88 in 2011).

Daily profit from street-vending (in quintiles)

Notes: Percentages are shown in italics. It is generally difficult to obtain income data in surveys. In 2007, over one-third of respondents (243) gave sufficient information on both income and outgoings to enable profit to be calculated and, in 2011, the response rate was 100 per cent. Table 3 is based on these responses.

Source: Micro-vendor surveys, 2007, 2011.

Women and men were equally likely in 2007 to earn gross profit in the bottom two quintiles. However, women were far more likely than men to be in the lowest profitability category (24.2 per cent against 15 per cent). Among 2011 respondents, women were more likely to be concentrated in both the 4th and 5th quintiles than men.

Age is another determinant of profit levels. A common criticism of street-vending is that there is no potential for upward mobility. The data presented in Table 3 cast doubt on this generalisation, with vendors aged 25 and over overrepresented in the 1st and 2nd quintiles in 2007 and in the 2nd quintile in 2011 and underrepresented in the 4th and 5th quintiles in both years. However, the improvement of earnings with age must be understood within a context of generalised insecurity (Wuyts, 2006). The vendors were aware that they would not be able to carry on with such a gruelling occupation into old age and older vendors worried about the future.

Finally, eviction is also closely associated with profitability. Among the respondents who answered this question in 2007, vendors who had experienced eviction were significantly more likely to earn under 6000 Tsh per day than vendors who had not experienced eviction (52.9 per cent against 40 per cent of all responses) and were very much more likely to earn under 3000 Tsh per day (23.5 per cent against 14.9 per cent).

To summarise, street-vending in Tanzania is important to the economies and prospects of a wide section of the population. It also provides the possibility of survival and of both intragenerational and intergenerational upwards mobility. However, it includes some very vulnerable people and their legal marginalisation has severe livelihood implications.

5. Findings: Do the Reforms Work for Tanzania’s Poor?

To understand how it is that the ‘Doing Business’ reforms have failed poor micro entrepreneurs it is necessary to examine in detail their objectives and implementation. In this section, we explore in some detail the content of a number of the ‘Doing Business’ indicators, to understand their potential impact on the businesses of the poor, with particular reference to Tanzanian street-vendors. The reality is that key parts of the reforms are able to make very little difference to micro enterprises in general and street-vendors in particular and, in some cases, contribute to their marginalisation.

To Tanzania, as to many other countries, its standing in the ‘Doing Business’ rankings is politically important. When Tanzania slipped in the rankings for the second time in 2011 (Table 1), the President charged each of nine government ministries with improving the country’s standing on one indicator (interview, BEST office, 2011). But what do the rankings actually measure?

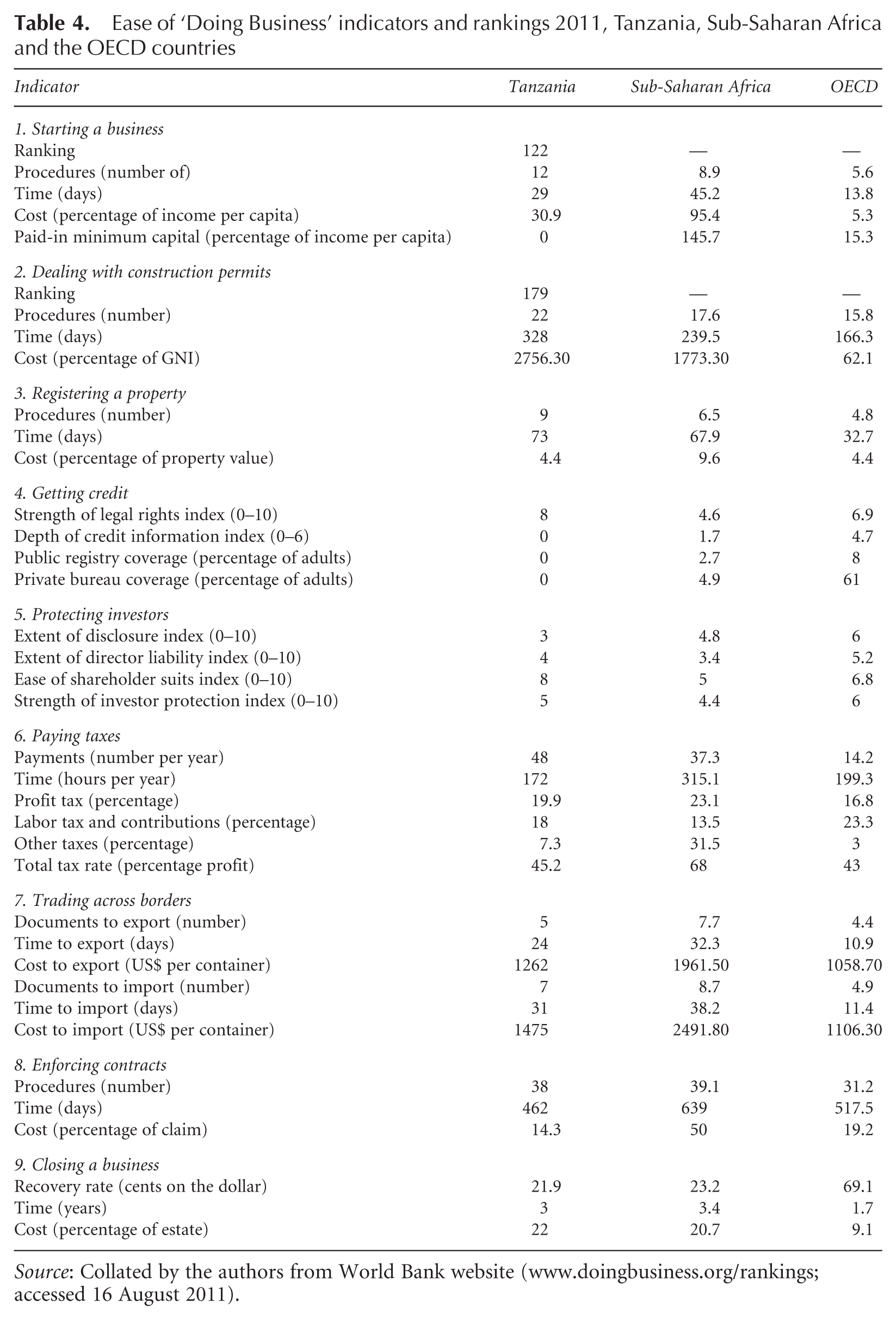

The World Bank acknowledges several measurement limitations of its data: measurement at country level may mask regional trends; the methodology assumes that businesses have full information about the regulatory requirements faced, although this may vary; and the measurements “involve an element of judgement by expert respondents” (World Bank, 2011a, p. 1). Two further reservations are critical for understanding the impact on street-vendors: first, the data often focus on a specific business form, generally a limited liability company with at least 50 employees and capital of US$100,000 in bank deposits—which “may not be representative of … other businesses, for example, sole proprietorships”; second, standardisation has meant that certain regulatory issues relevant to businesses may be excluded from measurement (World Bank, 2011a, p. 1). The irrelevance of any of the 10 indicators to micro entrepreneurs in general and to street-vendors in particular becomes apparent on examination of their components, discussed next and summarised in Table 4.

Ease of ‘Doing Business’ indicators and rankings 2011, Tanzania, Sub-Saharan Africa and the OECD countries

Source: Collated by the authors from World Bank website (www.doingbusiness.org/rankings; accessed 16 August 2011).

Indicator 1: ‘Ease of Starting a Business’

The focus of this indicator is on business registration. Our surveys clearly show that registration rates among street-vendors are low and show no signs of rising. In 2007, of the 584 vendors who replied to this question, 80—just 15 per cent—were licensed. In 2011, of 173 vendors interviewed, 169 replied to this question. Of these, four vendors, 2.4 per cent, were licensed. In a political climate which increasingly emphasises business registration, how is this to be explained?

First, despite the reforms, there are few licence categories available for street-vendors. In 1983 the Human Resources Deployment Act required every able-bodied person to work, establishing the nguvu kazi licence; legislation which was subtly ‘reinterpreted’ to confer an effective ‘right to work’ on citizens and effectively became an itinerant vendor license (Tripp, 1997, in Nnkya, 2006, p. 83) providing a basis for state tolerance of illegal use of public space. However, the Business Licensing Act 2003 simplified licence categories, resulting in the abolition of any legal form of peddling licence, and the Finance Act 2004 confirmed the requirement for all businesses to be registered and for certain categories to be licensed. Although small businesses retained exemption from the registration fee, the costs remain prohibitive (ILD, 2005a).

Neither can small businesses register as a limited liability company. Indicator 1 of the ‘Doing Business’ reforms (Table 4) examines the number of procedures required to register a limited liability company (12) and the time that this is likely to take (29 days). The capital requirements and (formal) fees in Tanzania are relatively low; nevertheless, any company would need significant income to be able to pay fees of over 30 per cent of GNP per capita in the country. This criterion alone puts the exercise outside the scope of micro entrepreneurs, including street-vendors, while the complexity and length of the procedure would force a sole proprietor to stop work for nearly six weeks to complete the procedures (World Bank 2011c, 2011d). Furthermore, Tanzania’s Companies Act 2002 does not accommodate the registration of limited liability companies for either sole-share owner companies or partnerships. In other words, regardless of the obstacles put in place by this criterion, there is no legal instrument available for micro entrepreneurs to register a limited liability company. Although laws to support business development are being progressively adapted, the recent Business Registration Act 2007 (URT, 2007) which simplifies small businesses registration retains this significant barrier (URT, 2008b; MKURABITA, 2007).

Finally, street-vendors do not satisfy a basic condition of the business licence. To be registered, the business must have a fixed and legal address (URT, 2007). The loss of peddling licences has made this impossible for vendors in public space. Moreover, vendors allocated legal spaces in new markets are unlikely to be able to provide a trading address, as the designation (zoning) of most new markets is temporary and can be revoked within 24 hours. In any event, many vendors are not allocated a specific space, simply the right to trade within a given area, such as an empty lot, and then for only one day a week, requiring a move to a different market every day. Any of these conditions makes nonsense of another condition of the licence, that it be permanently displayed on a wall of the business premises (URT, 2007a).

In summary, the national drive for business registration, tailored for performance on a key indicator of the ‘Doing Business’ reforms, is progressively excluding street-vendors. Micro entrepreneurs in general and street-vendors in particular, are further marginalised, as a plethora of institutional barriers continues to prevent their business registration.

Indicators 2 and 3: ‘Construction Permits’ and ‘Registering a Property’

Turning first to the measurement assumptions for these indicators (Table 4) it is clear that they could not possibly be relevant to the experience of any micro entrepreneur, street-vendors included. The ‘Construction Permits’ indicator measures the cost of construction of a two-storey warehouse on a greenfield site, connected to all services by a company employing at least 60 builders and other employees and employing a consultant architect. Similarly, the ‘Registering a Property’ indicator measures the costs of transferring a property with value 50 times income per capita between two local companies, each with at least 50 employees (World Bank, 2011c). To put this requirement in perspective, ILD and MKURABITA estimated the value of the total assets of an extra-legal business in Dar es Salaam in 2005 at US$2993, only 8.6 times the country’s GNP per capita at the time (then estimated at US$350 per head). (ILD, 2005b, p. 103).

The study of street-vendors in Tanzania in 2007 provides further grounds for questioning the poverty-reduction potential of the ‘Doing Business’ reforms, particularly where land rights are concerned. De Soto’s views have heavily informed the land rights agenda of the reforms and his assumption that it is possible or desirable to roll out large-scale land titling has been criticised on a wide range of issues—for example failing to translate into credit for the poor and in other ways failing to reduce poverty (for example, Payne et al., 2009; Otto, 2009).

The vast bulk of land titling has been carried out on agricultural land or on urban residential land, however, and we are not aware of any studies which examines the titling of land for business use. Tanzania provides a very interesting case study, demonstrating that, where land and property formalisation have been applied to street-vendors, their resultant security of tenure has been limited while other benefits, such as building assets and access to credit, have not accrued. In 2006 a High Court judgement in Tanzania delayed by three months the nationally mandated eviction of vendors by municipalities, requiring municipalities to identify alternative, legal vending sites. Interviews with vendors and officials in Mwanza in 2007 provided some fascinating insights into the ways in which legalised business tenure was constructed in ways which prevented both the accumulation of capital and use of the property as collateral. Mwanza instituted two innovative arrangements for the tenure of relocation premises. The first was to provide vendors with plots on municipally owned market sites. On these sites, the vendors would construct kiosks at their own expense. The vendors enjoyed a five-year rent holiday, at the end of which period the ownership of the shops transferred to the municipality. The application of this build-operate-transfer model meant that vendors were forced to find construction capital just at the point where they had lost their business through eviction and, despite having made the capital investment in the premises, were unable to use it as collateral because they were not the owners. The second innovation was to evict vendors to rotating weekly market sites, on which not only was development not permitted, but also no security of tenure was possible because the zoning of the site for a market could be revoked by the municipality at 24 hours notice. KI Interviews in DSM in 2011 confirmed that 24 hours was now the standard notice period attached to market zoning on municipal sites.

Indicator 4: ‘Getting Credit’

Credit is at the heart of growth for any business. Although Tanzania performs poorly on this indicator in relation to the SSA average (Table 4), the proposed regulatory improvements cannot really affect the position of micro entrepreneurs, particularly in new businesses. The Depth of Legal Rights component of the indicator measures the protection afforded by the law to lenders and borrowers through collateral and bankruptcy laws, the former allowing businesses to use moveable as well as fixed assets as collateral, the latter giving protection to creditors in case of business failure. Since there is no limited liability category for sole vendors even if they do form registered companies, this is irrelevant to street-vendors. Indeed, interviews undertaken in 2007 and in 2011 with street-vendors show that their personal liability for loans is a significant hurdle when considering borrowing.

Credit bureaux and credit registers are respectively privatised or state-run registers of credit records, but the coverage in Tanzania is extremely low, although financial regulatory reforms have been supplemented with supply-side support to the banking industry to widen participation. The Financial Sector Deepening Trust Tanzania (FSDT) supports microfinance institutions and major banks in establishing microfinance services, with the intention of extending the client base for financial services and improving both credit and savings facilities.

In lending to larger micro enterprises, there is now increasing competition from commercial banks, micro-finance institutions (MFI), not-for-profit MFIs, generally NGOs and to some extent local co-operatives (SACCOS) and their networks (Triodos-Facet, 2007). A number of commercial banks are expanding the geographical and social reach of their savings programmes, for example, Barclays Bank has opened small branches in suburban petrol stations and local employees on bicycles collect deposits from customers in lower-density areas. Co-operative savings and credit groups (SACCOS) borrow from banks and lend on to individual members who may be licensed or unlicensed micro entrepreneurs and who are not subject to credit checks as the loan is effectively guaranteed by the SACCOS. Recent legislation (re-)established the legal status of these groups.

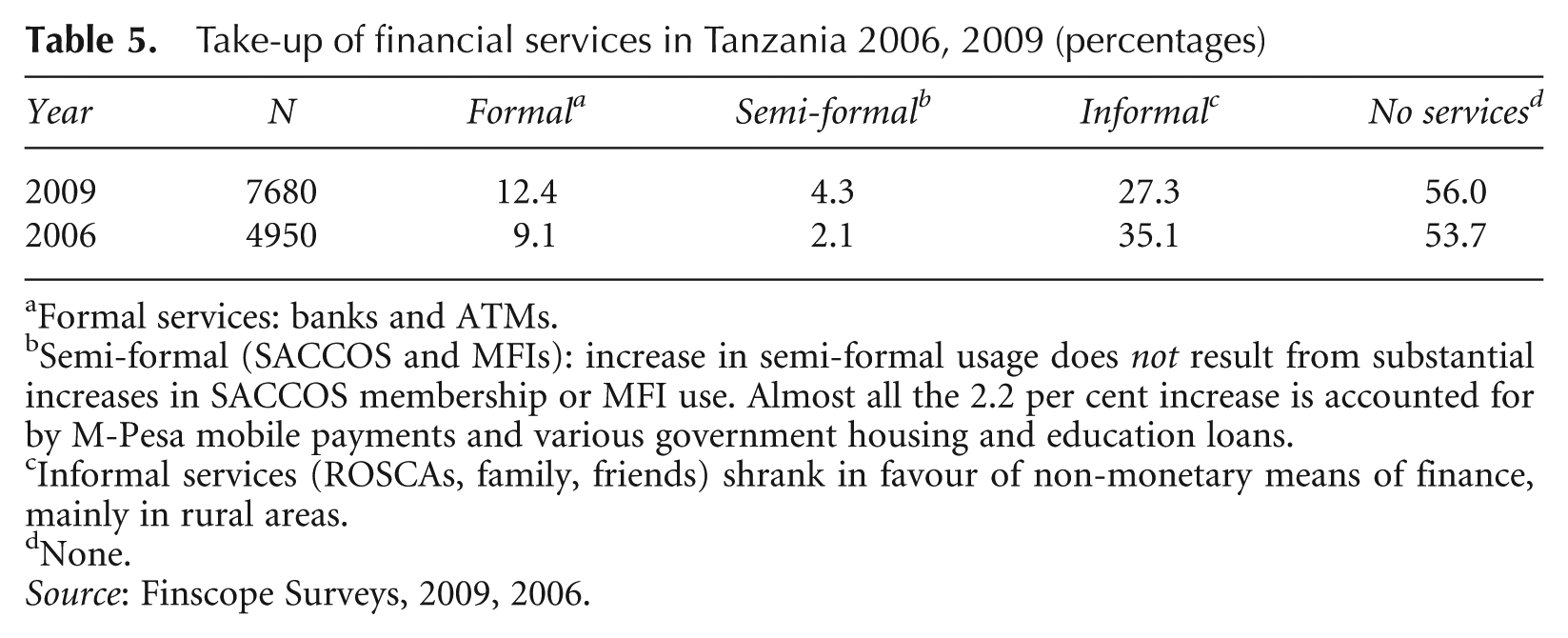

However, these programmes have largely failed to reach the poor, who make limited use of either formal or semi-formal financial services (Finscope, 2009). When interviewed in 2007, microfinance institutions demonstrated a widespread reluctance to make small loans to the poor (KI interviews, MFI executive directors). This is reflected in high real costs of loans to borrowers and in a lengthy and costly application process regardless of outcome (Lyons and Msoka, 2009). Conditions on group borrowing are also harsh and application success rates, low (Lyons and Msoka, 2009). Despite FSDT activities, lending to the urban poor decreased over the period 2006–09 and this is reflected in the fall in informal lending and very slight rise in semi-formal lending over the period. Table 5 summarises FSDT’s own findings. Comparison with responses from our 2007 and 2011 surveys, demonstrates the point that, although vendors are more dependent on borrowing than the population as a whole (only 6.1 per cent and 5.6 per cent in 2007 and 2011 respectively would never borrow, against FSDT’s figures of 56 per cent and 53.7 per cent for the population as a whole), they are far more dependent on informal sources such as business acquaintences, family and friends and on semi-formal lenders such as SACCOS and MFIs (of those who had borrowed, 7 per cent in 2007 and 8 per cent in 2011 had borrowed from a bank, contrasted with FSDT figures of 9.1 per cent and 12 per cent respectively in 2006 and 2009). Reasons named for avoidance of such formal and semi-formal MFIs in 2007 were prohibitive costs (70 per cent), the complexity and expense of application procedures (40 per cent) and the risk of losing personal, as well as business, goods (35 per cent). In 2011, high costs accounted for only 20 per cent of those reluctant to borrow, while lack of collateral or secure tenure, and the associated fear of losing one’s collateral, accounted for 50 per cent of refusals.

Take-up of financial services in Tanzania 2006, 2009 (percentages)

Formal services: banks and ATMs.

Semi-formal (SACCOS and MFIs): increase in semi-formal usage does not result from substantial increases in SACCOS membership or MFI use. Almost all the 2.2 per cent increase is accounted for by M-Pesa mobile payments and various government housing and education loans.

Informal services (ROSCAs, family, friends) shrank in favour of non-monetary means of finance, mainly in rural areas.

None.

Source: Finscope Surveys, 2009, 2006.

6. Discussion and Conclusions

The article sought to investigate whether the World Bank’s optimistic predictions with regard to the impact of its ‘Doing Business’ reforms on micro entrepreneurs were justified by events, or whether its subsequent abandonment of this optimistic position reflected a disappointing reality. Was the World Bank justified in its initial optimism (World Bank, 2004), or does the progressive abandonment of the topic express a disappointing reality? As discussed earlier, the original assumption of the ‘Doing Business’ reformers was that SMEs and micro entrepreneurs would benefit from the reduced cost of red tape, the reduction of other business costs, the improvements in access to justice and the increase in access to credit, in much the same way as larger businesses would. However, as we saw in the introduction, the viability of these reforms for SMEs has been widely questioned on all counts and from a range of professional and academic disciplines (Altenburg and von Drachenfels, 2006; von Braun and Keyzer, 2006; Bendaña, 2004; Arruñada, 2007; Durand-Lasserve and Selod, 2007). We argued that the case for critique from an SME perspective was heightened in the case of micro entrepreneurs and that in SSA this group represents by far the largest proportion of the economically active population.

Tanzania provided an interesting case in point not because it is unusual, but because it is facing a situation very similar to that of most SSA countries. For some years now, the large majority of new jobs have been in the informal economy (ILO, 2002). Following a macroeconomic shift towards commerce, micro entrepreneurs are increasingly focused on commerce rather than production (ILD, 2005b), the most visible end of complex and deep-rooted distribution chains (Lyons and Msoka, 2008). Similarly, the reforms being enacted in Tanzania are seen as a flagship for the international community’s current approach to pro-poor development through improvement of the business environment and creation of a ‘level playing field’ for businesses. Although they are recent and have not yet been implemented on a wide scale, pilot projects and legislation are in place, and examination of their intrinsic merits and initial implementation was thus possible.

The article thus aimed to review the impact of ‘Doing Business’ reforms on the micro-vending sector in Tanzania. Findings were that the experiences of vendors have been overwhelmingly negative, remaining seemingly untouched by the multiple policy initiatives attempting to improve their business environment. Instead, vendors have become more marginalised in the eyes of policy-makers and administrators and in turn, therefore, more vulnerable to prosecution under a range of acts, and to formalisation approaches which undermine their prospects as small businesses. In other words, confrontations between vendors and the state do not take place in a political vacuum (Tripp, 1997). The zeal with which the vendors are prosecuted reflects a lack of both public and official acceptance, as well as illegality. Their exclusion from the new reforms appears to have further marginalised street-vendors in the public eye and in the mind of policy-makers and politicians. As was clear from interviews with people versed in the new reforms and gearing up towards their implementation—such as municipal officials and, particularly, more senior civil servants in the relevant ministries—the perception of street-vending as criminal or trivial or both has become deeply entrenched in debates.

Thus vendors continue to be subject to the ‘shocks’ of punitive municipal strategies, endorsed or initiated by central government, including street clearances, demolition of stalls and other facilities, confiscation of goods, fines and imprisonments; with profound direct and indirect consequences—economic, social and personal. Indeed, confiscation and evictions have had the opposite effect to that intended by reforms, severely reducing the informal capital held by vendors. Among the many repercussions is the simple absence of capital to be used as security in any formal—or informal—credit transactions.

In similar ways, progress on Indicators 5–9 can be shown to be largely irrelevant to street-vendors. The intended result is regularisation of much larger companies, which dispose of larger sums of money, carry out large real-estate transactions, employ other companies, establish limited liability status and show a tangible credit history. Any easing of the barriers to acquiring legal status or gaining access to credit for street-vendors would have to come about indirectly, and work elsewhere suggests that it has actually resulted in their further marginalisation (Lyons and Msoka, 2009). It thus appears that the misgivings which began to emerge in the World Development Reports 2006 and 2007 about the ability of ‘Doing Business’ reforms to create a “better investment climate for everyone” (World Bank, 2004; emphasis added) have been vindicated by events.

Importantly, the Tanzanian case provides a clear example of widespread unintended consequences of the ‘Doing Business’ reforms and it is extraordinary that, for such a high profile programme that has been running for the best part of a decade, there has been little published evaluation of its impact on informal businesses and poverty indicators. In as much as the present formalisation process excludes large numbers of entrepreneurs, a significant segment of modern urban society, it clearly requires adjustment. While it fails to address fundamental contradictions between current urban policy on micro-vending and the developmental objectives of broader reform policies, it is ripe for review.

Footnotes

Acknowledgements

Professor Michal Lyons sadly died of cancer in February 2013. She has been an inspiration to her global network of research colleagues and students, and is sadly missed by all those privileged to have worked with her.

Funding

Thanks are due to the European Commission and the Development Partner Group on Private Sector Development and Trade, Dar es Salaam, 2007, for funding this research under the title: “Micro-vending in Tanzania—the way forward”, led by London South Bank University; and to DFID/ESRC for funding the project: “Making space for the poor: law, rights, regulation and street-trade in the 21st century” (RES-167-25-0591), led by Cardiff University.