Abstract

In the 2000s, cities across North America began leasing existing infrastructure to global investment consortia. Previous evaluations of infrastructure leases focus on the lack of transparency of the privatisation process and the terms of the arrangements negotiated by the public sector and the private concessionaires. In this research, we argue that such approaches fall short by failing to investigate the significant repositioning of the local state relative to financial markets produced by their involvement in major asset lease deals. We develop this argument through a case study of the institutional transformation of the City of Chicago, the US’s most aggressive instigator of infrastructure asset leases. Even as the concession agreements seemingly protect the City from the claims of investors, creditors and counterparties and provide it with new powers, they enmesh the City in a set of financial relationships that expose it to liabilities not accounted for in lease agreements and create an institutional bias towards managing the collateral effects of financialisation.

Keywords

Introduction

On the surface, infrastructure privatisation would seem to represent yet another case of cities acting as handmaidens to financial capital. Starting with the $1.6 billion lease of the Chicago Skyway in 2005, private investors purchased the rights to collect a wide variety of income streams from existing (‘brownfield’) US infrastructure assets, including airports, toll roads, and parking garages. By 2010, the 50 pending deals in North America were valued at between $35 billion and $40 billion (The Economist, 2010). These deals are typically led by the infrastructure fund subsidiaries of global investment banks (Lawrence and Stapledon, 2008), which prize the long-term potential for cash flow growth presented by infrastructure (Page et al., 2008). Joining forces with an operating partner, they assemble a portfolio of assets that are ‘stapled’ together and then sell shares in them to a range of institutional investors, including hedge funds, pension funds, insurance companies, and their own holding companies (O’Neill, 2009; Zhang, 2008). They also employ advanced structured finance techniques to extract value from their acquisitions, including interest rate swap derivatives and ‘sweep’ capital structures that accelerate returns to investors and enhance their profile as profitable financial securities (Ashton et al., 2012; Bel and Foote, 2009). By presenting these financial engineering strategies as proprietary, investors deliberately position them as outside the realm of politics (Allen and Pryke, 2013).

Critical perspectives on these deals, and the underlying financialisation processes they represent, often focus on the lack of transparency accompanying deal-making, the absence of public participation, or the degree to which the concession agreements appear to ‘give away the store’ by committing the public sector to extremely long leases (often 75 to 99 years), aggressive toll rate increases, or diminished competition (Baxandall, 2007). Alternately, critics construe long-term asset leases as the disembedding of urban infrastructure from its local context in support of global financial circulation (Torrance, 2008). Accordingly, they focus on the deal-making process and its outcomes: the specific provisions and terms of the contract or ‘concession agreement’ (cf. Clark and Evans, 1998). Most conclude that deals result in a diminished scope for local autonomy.

In this paper, we examine these deals from a different perspective, emphasising the complex public–private networks through which local states produce and subsequently manage flows of value from privatised infrastructure assets. Drawing on the case of the City of Chicago, which pioneered the large-scale asset lease in North America and continues to pursue privatisation in various guises, we argue that infrastructure leases require a mobilisation and reconfiguration of state powers – mobilisation rewarded, in part, by the enhanced fiscal and political capacity that accompanies them, however temporarily or contingently. At the same time, the very nature of urban infrastructure makes the flow of value from these assets uncertain, thereby transforming value into a problematic to be managed or governed over the life of the transaction. In our analysis of three infrastructure concession deals executed in Chicago from 2005 to 2008, we argue that high pay-outs rewarded the City, and obligated it to re-orient a broad range of state activities towards managing both economic and non-economic determinants of value flows to investors. The deals thus created new kinds of exposures for the City, ranging from those emanating from speculative behaviours on the part of the lessee and the inherent fragility of the deal’s financing mechanisms, to those resulting from the sudden monetisation of day-to-day public sector activities, such as zoning and traffic mitigation. Privatisation transactions thus entangle the local state and a broad range of investors, creditors and counterparties in a longer-term process of generating and managing the economic value of privatised infrastructure and its uncertainties beyond the terms and timing of the deal itself.

From global circulation to uncertainty and exposure

The term ‘financialisation’ connotes the growing importance of the financial sector and the intermediation of public and private activity through finance. This body of scholarship emphasises the historical growth of financial industries relative to manufacturing and other services in OECD economies since the 1970s, as well as a concomitant shift towards finance-based profit generation and the conversion of assets into liquid, easily tradable financial commodities (Epstein, 2005; Froud et al., 2006; Krippner, 2005). Much of this scholarship focuses on financial markets and trading, and the rise of institutional investors as a powerful force in markets and market-making (Clark, 2000).

These global changes help to establish the context for individual cases of urban restructuring, but the mechanisms integrating urban-scale changes with the broad transformation of global markets remain murky (French et al., 2011). One common approach illuminates the local dimensions of financial systems by examining shifting hierarchies of financial centres (Marshall, 2013; Sassen, 1999) or the role of proximity in structuring financial market activity (Jones, 2009; Wójcik, 2009). A second examines banks or financial intermediaries as private actors capable of diminishing the authority of states over economy and society (Strange, 1996) and exerting power over urban governance agendas. For instance, Hackworth (2002) scrutinises the ways in which ratings agencies constrain local autonomy, arguing that their gatekeeper role in municipal bond markets allows them to increase borrowing costs or deny credit for localities pursuing projects that diverge from the disciplinary norms of institutional investors.

Another approach examines the production of financial commodities, focusing on the process whereby locally embedded assets – characterised by their immovability and the irreversibility of investment in them (Dymski and Veitch, 1996) – are transformed into streams of value that can be bought, traded and circulated within financial markets. In one study of recent trends in the financialisation of urban infrastructure, Torrance (2008) examines the growing role of specialised financial intermediaries in producing a market for infrastructure leases (in her case, the 407 toll road in Toronto). She focuses on the concession contract – an essential building block of the financial transaction – as the device that disembeds local assets and reorganises their constituent elements within external financial portfolios, ‘capturing the value of a place while distributing the risk of being invested in it’ (Torrance, 2008: 2).

Torrance’s analysis resonates with other studies of financial commodities, including mortgage-backed securities and derivatives, commonly understood to dematerialise geographic assets and circulate them within global financial circuits (Gotham, 2009). Further, it highlights the contradictions in the process of transforming idiosyncratic assets into liquid financial instruments – for instance, between the time-spaces of local value flows and those of financial markets (Pryke and Allen, 2000), or between the differential legal status of financial investors relative to municipal governments (Torrance, 2008).

However, the conceptual vocabulary derived from studies of financial markets and trading emphasises speed, standardisation and circulation in global financial circuits, potentially mis-specifying financialisation as a process that unfolds ‘out there’. The intricacies of infrastructure concessions suggest we need to broaden our lens to incorporate the local dimensions of financialisation. Most notably, given the extensive role of the local state in producing these markets, theorisations of financialisation at the local level must function as, or draw from, state theory. Rather than reproduce ‘a false opposition’ (Jessop, 2008) between external financial markets and the local institutions they supposedly subordinate, examining financialisation as a policy project (Christopherson et al., 2013: 353; Pacewicz, 2013) uncovers localities’ construction of the powers that allow them to work with, through or against finance. This approach might also treat financialisation as a recursive process, wherein individual privatisation events are moments in a longer chain of state transformation that actively engages public power to redraw ‘the spatio-temporal matrices within which capital operates’ and to ‘render capital’s temporal horizons and rhythms compatible with their statal and/or political routines, temporalities, and crisis-tendencies’ (Jessop, 2008: 191).

When focused on the emergence of financial markets such as those that govern the sale of infrastructure assets, a broader examination of the local state relative to the transaction – in its fullest sense as a form of collective action that involves multiple actors within a dynamic institutional setting (see Commons, 1924) – can usefully focus on the following three parameters to better specify local financialisation.

First, a transactional approach would revisit the commodity itself, asking which broader powers and resources are deployed to produce the infrastructure asset as circulatable value for financial investors (see Sokol, 2013). Localities do not merely respond to infrastructure lease offers from global investment banks, but build and operate complex frameworks to enable the realisation of value from financialised municipal assets (Weber, 2010). This includes the production of inputs necessary to close the deals, such as legally enforceable property rights (O’Neill, 2013), regulatory approvals or exemptions, and locally specific knowledge about market conditions. These frameworks may in turn represent significant shifts in the strategic capacities of local government and involve mobilising a wide network of public and/or private agents to produce a stream of value for investors.

Second, a transactional approach would necessarily assess economic value from a temporal perspective, scrutinising uncertainty as a critical transactional variable. The income streams from infrastructure assets can only be realised over time and depend on positive local spillovers in order for financial yields to flow to investors (Dymski and Veitch, 1996). In the case of transportation infrastructure, these spillovers include changing land use decisions, variable economic conditions, and the availability of competing options for drivers. These spillovers are often unforeseen, or unforeseeable, by a concession agreement, and may lie beyond the concessionaire’s management capacity. A transactional approach, then, would ask how that uncertainty is structured within the transaction – both in investors’ assumptions about revenue streams that justify a particular purchase price, and in the various roles that the local state may play in bounding or managing uncertainty within the transaction.

Third, an emphasis on time and uncertainty requires scrutiny of the risks and conflicts to which the transaction exposes the local state. Even as infrastructure concession contracts formally indemnify the public from responsibility for faulty demand forecasts, economic downturns and other unforeseen events that jeopardise the flow of value from an infrastructure asset, asset leases place local governments at the centre of a fragile architecture of inter-linked financial arrangements beset by a variety of risks (O’Neill, 2009). The terms of each agreement thus structure distinct conflicts and bargaining dynamics around uncertainty. These range from the quotidian (the enforcement of public standards regarding upkeep of an asset, or the management of compensation due to the concessionaire for city-induced disruptions to revenue) to the complex (insolvency or bankruptcy, operating default, or contract renegotiation).

Borrowing from legal anthropology, we focus on how the transaction entangles the state and a broad range of investors, creditors and counterparties in strategies for managing an asset’s economic value and governing future uncertainties. This makes the financial contract ‘a compact for a short-term political arrangement, a kind of private constitution with a time horizon – something perhaps best analysed alongside other short-term private and hierarchical political institutions like indentured servitude’ (Riles, 2011: 166). As such, we treat the contract as a starting point from which to analyse how these asset lease deals and the processes of financialisation they embody transform the state.

Chicago: The sell-off city

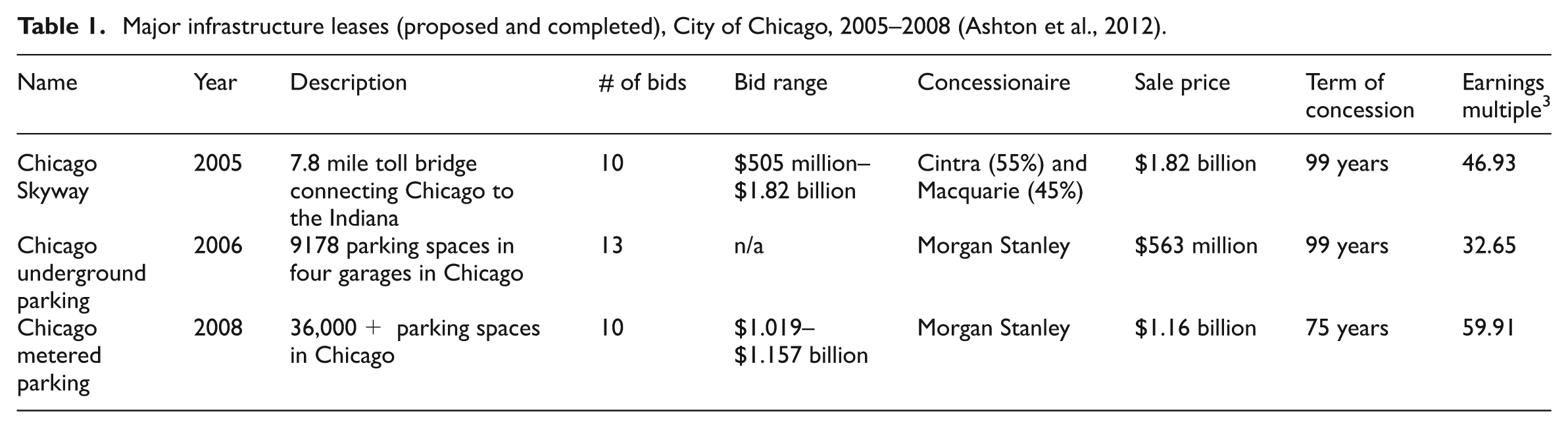

Several factors position Chicago as a revealing case through which to examine the political changes produced by asset leases. Chicago’s embrace of privatisation and leasing began early in the Richard M. Daley administration, when it contracted out basic city services to cut costs and weaken public sector unions (Scholl, 1991). By 2004, when the Daley administration solicited bids for the Chicago Skyway, a seven-mile toll road-bridge connecting the city to Northwest Indiana, Chicago had embraced privatisation as a means to manage city services and deliver selective benefits to political constituencies in areas such as recycling and janitorial services at Chicago public schools. 1 By 2008, the City had completed concession agreements for the Skyway (2005), the city’s underground parking garages (2006), and street parking meters (2008). 2

Under Daley and his successor, Mayor Rahm Emanuel, the City opened Midway Airport for privatisation (financing for the winning bidder failed) and explored lease arrangements for the McCormick Place convention centre, the Taste of Chicago festival, and the supply of water from Lake Michigan (Hawthorne, 2009). Beginning in 2011, the Emanuel administration took steps to institutionalise these changes, hiring several key financial advisors and privatisation advocates directly into the Mayor’s cabinet, and establishing the nation’s first local urban infrastructure investment bank (City of Chicago, 2012). As such, Chicago now has a longer experience with the privatisation of infrastructure assets than any other major city in the United States.

The passage of nearly a decade since the sale of the Chicago Skyway, and the subsequent sale of the underground parking garages and parking meters, provides a unique opportunity to examine the local dimensions of financialisation (Table 1). These deals represent recent trends in infrastructure privatisation (cf. Bel and Foote, 2009; Page et al., 2008). All involved long-term leases (from 75 to 99 years) to a private concessionaire, typically a consortium comprised of a global investment bank, sovereign wealth or hedge fund, and an operating partner. The 2008 parking meters concession, for example, was awarded to a partnership between Morgan Stanley, Germany’s Allianz Capital Partners, and the Abu Dhabi Investment Authority (Mihalopoulos, 2009). The partnership, known as Chicago Parking Meters LLC, subcontracted with LAZ Parking for the management and maintenance of the meters.

Major infrastructure leases (proposed and completed), City of Chicago, 2005–2008 (Ashton et al., 2012).

Highly leveraged to begin with, the Chicago deals became more so through a variety of complex financial engineering strategies used to structure future cash flows (Ashton et al., 2012). Foreign investment banks provided much of this debt financing. For the Skyway, Banco Santander Central Hispano, S.A. (Spain), Calyon Corporate & Investment Bank (France), BBVA (Spain) and DEPFA Bank PLC (Ireland) underwrote the $1.8 billion concession purchased by the Cintra-Macquarie consortium (FHWA, 2013). The involvement of bond insurers, ratings agencies, and credit enhancement and derivatives issuers helps to circulate value and allocate risks through even more diffuse channels. While these investment partners have different time horizons and penchants for risk, the three Chicago deals under discussion were led by investment banks (Morgan Stanley, Macquarie) whose infrastructure funds had similar risk-return profiles (Lawrence and Stapledon, 2008).

However, a focus on the formal elements of capital structure or the spatial reach of lenders and investors misses the institutional reorganisation essential to the creation of financial assets for global investors. In addition to the necessary scrutiny of the financial instruments and business strategies concessionaires develop to generate value from infrastructure assets, our transactional approach requires two additional analytical foci. First, the transactions must be treated as ‘governance-in-motion’ – not as one-time transfers of public assets to private control, but as the complex process of constructing the powers and capacities necessary to produce value from urban infrastructure. Some of this reorganisation, such as the development of a durable network of law firms, financial analysts and advisors capable of assembling deals – as well as the designation of executive powers for some public agencies – was critical to transforming public assets into financial commodities. Rather than treat the contracts as bilateral transactions between two fixed entities, then, we view these large infrastructure deals as changing the very nature of the entities doing the bargaining.

Second, following Riles’ (2011) characterisation of financial contracts as entangling their parties, a transactional approach requires the assessment of relationships between the City and investment bank consortia as they unfold over time. Even though the transactions on which we focus are recent, events subsequent to each deal highlight new roles and exposures produced within each transaction. These include new City responsibilities for producing revenue streams for investors through nonfinancial means, as well as legal, financial and administrative exposures that unexpectedly emerged from privatised infrastructure. Even as the privatisation agreements enact formal measures to protect the City from the claims of investors, creditors and counterparties, they inject multiple uncertainties into basic service delivery and planning for local growth and management.

We ground this approach in an analysis of each transaction, focusing on the infrastructure lease agreements, enabling ordinances and ancillary documents, as well as financial prospectuses for concessionaires, coverage in the trade press, and third party analyses. We combine those findings with a select number of targeted interviews that provide new empirical material on heretofore under-analysed dimensions of financialisation. 4

Governance in motion: Producing asset leases

Arguments that asset sales disembed infrastructure from cities focus on the asset lease and the subsequent circulation of its value in global financial circuits (Torrance, 2008). Before value can be circulated, however, it needs to be produced. Our analysis of the three Chicago deals highlights this process of production – not from the point of view of the arcane financial instruments involved, but also from a more foundational assessment of the critical inputs necessary for each transaction, and the interlocking network of public and private actors charged with deal execution. In this sense, finance unfolds in the very localised and humanly scaled settings of Chicago’s particular institutions and professional networks.

These efforts shape the process of privatisation from the beginning. As dependent legal entities in the US federal system (Frug, 1999), municipalities must build the legal powers necessary to create enforceable and alienable property rights in local infrastructure assets (see O’Neill, 2013). For instance, the City of Chicago and the Chicago Park District had to pass ordinances consolidating ownership of the downtown underground parking system to facilitate its transfer to Morgan Stanley (City of Chicago, 2006). To create the legal authority to open up the Skyway to private control, the Chicago branch of global law firm Mayer Brown lobbied both the Illinois General Assembly and federal highway authorities to amend legislation and alter regulatory standards (Interview with Lease Attorney 2008). As the Skyway concession deal would make the publicly owned toll road taxable for private concessionaires, the City also successfully lobbied the State of Illinois for property tax exemptions that could be transferred to the concessionaire (City of Chicago, 2004: 41; Shields, 2006).

Members of a Chicago-centred network helped to produce the transactions on both the ‘sell’ and ‘buy’ sides. Chicago law firms clarified and allocated responsibilities and rewards through contractual language; bond insurers assumed project risk; investment analysts assessed the deals for investors and the City; and bond underwriters issued structured debt instruments. Local firms William Blair and Associates and Scott Balice Strategies, LLC played multiple roles in the three Chicago deals. As lead financial advisor on the parking meter concession, William Blair identified prospective bidders, structured the financial aspects of the concession, led the negotiation of the agreement, conducted due diligence on bidders, and managed the competitive bidding process. As it worked in this capacity for the City, William Blair simultaneously worked on other deals with the eventual winning bidder for the lease, Morgan Stanley. In other words the firm advised the City trying to get the highest price for its asset while at the same time working with potential bidders to maximise the concessions extracted from the public sector (albeit on other deals). Prospective conflicts of interest aside, these actors not only assisted the City in disposing of its assets but also helped to formalise an organised market for the leases on those assets.

Combined, this network of actors formed a thick structure of organised fiscal and political capacity, one strong enough to withstand both changes in Chicago’s administration and the frequent restructuring of capital. For both the parking garages and parking meters, the firms discussed above repositioned themselves at different points in the network; depending on the deal, individual law firms, brokers and assemblers of financing moved back and forth from lead to subsidiary debt positions, from positions of deal-brokering to advising, and from public to private and back again. For example, the Managing Deputy Comptroller for the City of Chicago responsible for overseeing the Skyway, parking meters, and Midway deals subsequently left the City to work first for a subsidiary of FBR Capital Markets focused on public–private partnerships, and later Gonzalez Saggio & Harlan, the law firm that wrote the ordinance authorising the City to enter into the parking meters agreement. In 2011, then Mayor-elect Rahm Emanuel hired executives from two of the firms active in the Skyway and Midway deals (municipal finance consultants Scott Balice Strategies LLC and law firm Baker & MacKenzie) as his Chief Financial Officer and Budget Director (Dumke, 2012). The multiple roles played by actors in this local network made them durable and available for subsequent transactions.

As this network built the market for assets, the City of Chicago enacted multiple changes to create the kinds of deal-making apparatuses necessary to carry out infrastructure transactions. Two types of institutional changes stand out. First, we observe a premium placed on speed, consistent with Jessop’s (2008) argument that globalisation elevates institutions and individuals that can act quickly to negotiate with private agents while simultaneously eliminating procedural barriers to swift action. Chicago’s asset transfers were finalised through accelerated city council votes, informal negotiations between public representatives and financiers, and contractual negotiations submitted for public review only after the general terms had been agreed upon (Office of the Inspector General, 2010). Changes in administration elevated strong executives – in particular, the Mayor’s Office, the Comptroller, and the Office of Management and Budget – and normalised expert discourses and easily replicable forms of ‘fast policy’, at the expense of legislative, judicial and other administrative powers (cf. Peck and Theodore, 2010).

Second, the transactions reworked institutional structures and capacities once central to direct public ownership and governance. For example, the Chicago Park District historically operated the downtown parking garages, whose capacity, pricing and maintenance was integrated with the City’s multiple public facilities investments and tourist destinations along the downtown lakefront. The 99 year lease for the garages stripped the Park District of enforcement powers, reserving them for the City as a corporate entity (City of Chicago, 2006). The City ordinance authorising the parking meters deal similarly amended the Municipal Code to subordinate the Commissioner of Transportation to the Department of Revenue, which gains authority to ‘operate off-street parking facilities owned by the city, and to collect all fees and charges for the use of such facilities in regards to the installation, management, and collection of revenue from parking meters in the city’ (City of Chicago, 2008b: 5). That ordinance also exempted the Department of Revenue and its agents (which now include the Morgan Stanley-led consortium) from oversight by other City agencies in regards to permitting, approvals, signage and other rules (City of Chicago, 2008b: 7–9). The deals also promoted executive powers when post-agreement oversight and monitoring was required. All of the leases we reviewed assigned these powers to the Comptroller and the Departments of Finance and Revenue, rather than agencies that historically oversaw the operation of the transportation system.

As a result of these changes, the state that planned infrastructure leases differ significantly from the state that supports and maintains them. Tasking the agencies responsible for city finances with managing privatisation signifies a shift in both the meaning and the practice of infrastructure management, from something operated for its use value to a commodity valued for its ability to be circulated and exchanged (O’Neill, 2009).

The public protection of asset values

While a full evaluation of the costs and benefits of Chicago’s asset sales lies beyond the scope of this paper, such an evaluation would likely identify several immediate benefits to the City. The three deals generated over $3.5 billion in direct payments (Table 1), allowing Chicago to pay down more than $925 million in outstanding debt (Saffold, 2010). Even before the high-value parking meters deal, Moody’s had cited falling indebtedness in upgrading Chicago’s general obligation bond rating from A1 to Aa3 (Shingore, 2009). 5

In the short term, the deals advanced multiple longstanding public policy goals. Chicago’s asset lease agreements each contain dozens of provisions requiring concessionaires to maintain and improve the quality of the infrastructure itself. The parking meters concession devotes three pages alone to specifying new metering technologies, for example, pay stations (City of Chicago, 2008a: 48–51), and all three deals detail extensive capital improvement standards to maintain the quality of infrastructure as a public good (City of Chicago, 2008a). The parking meters and underground garages transactions both enact hiring quotas for minorities (as much as 40% of all employees) and dictate adherence to the city’s women- and minority-owned contracting laws (City of Chicago, 2006, 2008a). As such, these deals use new financial arrangements to solve certain intractable political problems, in the process enhancing the City’s manoeuvring room in its management of short-term budgetary issues, its longer-term profile with creditors, and its capacity to deliver selective benefits to political constituencies.

Criticisms of infrastructure privatisation counter by pointing to contractual provisions that generate high value for concessionaires and their investors and creditors (Baxandall, 2007). These include lengthy lease terms, accelerated toll or rate increases, non-compete clauses that produce monopoly power for the concessionaire by limiting the development of competing assets, and requirements that the public sector compensate the lessor for actions and events that reduce an asset’s cash flow. However, to the extent that these value-enhancing provisions are directly related to the large size of the winning bids, a focus on the up-front configuration of value produces zero-sum assessments of deal outcomes: either the City wins a hefty pay-out by out-negotiating the banks, or it gives away the store by handing monopoly power to these profit-oriented actors. This binary opposition between market and state power obscures the local economic and political changes promoted by financialisation (Jessop, 2008).

The value of an infrastructure concession can more productively be understood as enmeshed in a long-term financial partnership between Chicago and the investment consortia. The economic value of a concession agreement is not settled at the moment the contract is signed and does not circulate in a straightforward manner. In the case of transportation assets, value extraction depends on the collective behaviour of commuters and spillover effects from a wide range of public and private investments. As Riles (2011) suggests, the contractual provisions in infrastructure agreements are placeholders – temporary settlements of contentious issues related to the value of a concession to investors and creditors that stretch out over the lifecycle of the asset. It is therefore critical to assess how the benefits to both the concessionaire and the City simultaneously produce new public liabilities, duties, and exposures within the transaction.

Two particular dimensions of the entanglement between public and private emerge from our analysis of the leases and subsequent changes in Chicago policies and practices: The deployment of supplementary regulatory powers to ensure returns on assets, and the liabilities and exposures that fall on the local state.

Extra-contractual safeguards

The reorganisation of City powers during the production of each deal extended beyond the execution of the agreement, yielding both anticipated and unanticipated new roles and powers the City exercised to maximise revenue streams for investors after the agreement’s consummation. The illustrative case of the 2008 parking meters concession identifies ways in which the City of Chicago committed and repurposed its administrative powers in support of the concession throughout the life of the transaction. In many instances, this involved safeguarding non-financial determinants of value, such as restricting the availability of legal recourse for ticketed drivers or the severity of transportation regulations beyond those strictly involving parking.

The repurposing of state administrative powers to support the parking meters concession was first evident in a minor scandal involving rush-hour traffic management. In 2010, the Department of Transportation lifted rush-hour parking bans on 225 city blocks in and near the Loop, allowing an extra four hours of meter-eligible parking on busy city streets and arterials. This action expanded the revenue capacity of meters by 25% for certain high-value areas. Although the cited rationale – safety for pedestrians and cyclists – was broad, analysts noted that the waiver only governed blocks covered by Morgan Stanley’s concession (Wisniewski, 2010).

A closer read of the contract and its governance aftermath reveals additional uses of City authority to ensure the value of the concession. A prime example is the issuance of parking tickets. The parking meters concession committed Chicago to expanded enforcement of parking violations as a means to incentivise payment of parking fees (City of Chicago, 2008a). In the immediate aftermath of the meters sale, parking ticket issuance by the City’s traffic enforcement division rose; leaked emails from the Chicago Department of Revenue in 2010 subsequently revealed aggressive ticketing quotas (Main and Spielman, 2010). Whereas the agreement granted the Morgan Stanley-led consortium authority to issue parking tickets alongside the City, all parking ticket fines ultimately reverted to the City alone, suggesting that the transaction may have simultaneously incentivised the City to act as a co-rent seeker and to take advantage of the new (and more accurate) metering technology to increase its own revenue streams. The impact on the aggregate public welfare is ambiguous and, perhaps, positive. But the change in public policy, buried deep in the contract, is significant.

The repurposing of state authority was also evident in the use of several minor, procedural powers to routinize and speed the collection of parking revenue. In 2010, the City began attaching the ‘Denver boot’ to larger numbers of cars with outstanding parking violations. Booting results in both a more expensive penalty for drivers and a greater likelihood of payment (Spielman, 2010), factors consistent with the Agreement’s mandate of a City ‘vehicle immobilisation program’ as a ‘method of deterrence’ (City of Chicago, 2008b: 61). A series of related measures – all mandated by the concession agreement itself – included the City’s agreement to notify the Illinois Secretary of State to pursue licence suspensions for drivers with delinquent parking tickets and to expedite the prosecution of traffic tickets in court (City of Chicago, 2008a: 40, 64). Rather explicitly, the agreement required the City to restrict ‘parking by Exempt Persons’, also known as the disabled, against whom the City is now obligated to implement ‘significant fines and other appropriate measures … to ensure the levels of counterfeit parking permits are minimized’ (City of Chicago, 2008: 61). Cumulatively, these observed changes both confirm and extend Dannin’s (2009: 4) observation that many common measures in privatisation agreements ‘make government the insurer of the private contractor’s financial success’ for the duration of the contract.

Post-contractual exposures

Common criticisms of privatisation focus on the diminished public capacity for transportation planning that comes with long-term infrastructure leases (cf. Dutzik et al., 2012; Farmer, 2013; Siemiatycki and Farooqi, 2012). In addition to the constraints placed on potential future action, a more specific set of uncertainties are created within the transaction itself. These exposures range from the strategic issues for the City posed by the risky financing mechanisms used to generate value for investors, to a set of legal liabilities, financial costs, and institutional compromises that accompany each transaction’s more specific parameters.

At a broad level, concession contracts increase the exposure of the City’s financial capacity to the risks inherent in global capital markets, even as they appear to indemnify the public from obligations to bondholders and investors. The contracts do not set limits on overall leverage or indebtedness, nor do they address the manipulation of project cash flows through advanced financial engineering techniques such as interest rate swaps (see Allen and Pryke, 2013; Ashton et al., 2012). 6 For example, the Macquarie-led partnership refinanced the Skyway’s debt in 2006, using interest rate swaps and sweeps to frontload equity distributions to investors while deferring principal payment on debt far into the future (see also Bel and Foote, 2009). These equity distributions depend on optimistic assumptions about revenue increases, and on accounting manipulations that increase the book value of the asset. As one analyst noted, the strategy of investors like Macquarie amounts to a ‘triple-loaded betting system’ (Zhang, 2008: 61) rife with risks that make the deals vulnerable to economic shocks or failed assumptions. Moreover, these bets are highly leveraged, implicating a wide range of creditors (banks and bondholders) and counterparties (swap sellers and bond insurers) in the vulnerability of concession deals.

Because no catastrophic event has come to pass in Chicago, analysis of the strategic issues the City would face in response to an operator default necessarily remains speculative. 7 While each agreement contains standard contractual language supposedly limiting public-sector exposure to distress, the omissions to these contracts – their intrinsic inability to account for future economic shocks, fluctuations in the operating firm’s viability, or faulty demand forecasts – potentially create new and uncharted exposures. The experience of privatising states in South America indicates that distress creates strategic moments in a transaction where concessionaires can press further risk-shifting from the private to the public sector (Guasch et al., 2008). Were a default to occur, the City would be forced to confront creditors, investors and counterparties involved in these deals and determine whether and how to modify their claims, wipe them out by terminating the agreement, or make them whole by absorbing the distressed asset onto the City’s books.

In contrast to these hypothetical scenarios, the three deals in our analysis all produce a more direct set of exposures, some of which have already been made manifest. Even as the lengthy contracts seem to assure that public interests will be protected throughout the length of the concession – often through details as small as the spacing of parking meters, the time within which lessors must fill pot holes, and capital improvement schedules for parking garages (Dannin, 2009) – the contractual provisions mark clear paths and conflict points along which the relationship between cities and concessionaires will be contested.

Of primary concern are the many contractual measures requiring the City to compensate investors for adverse actions (i.e. ‘compensation events’) that lower an asset’s cash flow and thus its exchange value. In 2011 and 2012, Chicago Parking Meters LLC billed Chicago more than $50 million for routine street closings resulting from street festivals, construction, and the use of metered parking spaces by cars with disability placards (Dardick and Harris, 2012). The potential costs stray into everyday planning activities such as zoning and permitting, as evidenced by another prospective cost, a $200 million lawsuit from Chicago Loop Parking 8 claiming that the City’s approval of a competing private parking garage violated the terms of the lease (Mihalopoulos and Fusco, 2012).

Political fallout from the parking meters lease and these fees led new Mayor Rahm Emanuel to renegotiate the parking meters lease in 2013. The renegotiation yielded some politically desirable concessions, including free parking on Sundays outside of the central business district. To obtain these changes, Chicago allowed rate hikes on downtown meters, added one hour daily to metered parking on other days, and agreed to a $54.9 million settlement with Chicago Parking Meters, LLC, over the concessionaire’s revenue losses form disability placards. More favourably for the City, the revision changed the calculation of revenue compensation events in the City’s favour, with the mayor opining that the reduced pay-outs (Chicago owed Morgan Stanley $49 million in compensation for the prior two years) would translate into $1 billion in savings over the life of the deal (City of Chicago, 2013).

Regardless of how the renegotiation transforms these problems, the City’s exposure to such compensation events represents a problem distinct from, and more enduring than, allegations of bad deal-making and a lack of foresight. These costs cannot be managed by the contract for the simple reason that they result from the uncertainties and positionalities created within the transaction itself. Under earlier modes of service delivery the City never had to systematically calculate the aggregate costs of street repairs, disabled parking concessions and other parking disruptions to parking meter revenue – it was only within the transaction that those were rendered calculable and monetised for the first time. Now, accommodating its relationship with investors requires Chicago to develop new analytical capacities to attach direct costs to capital improvements, and new powers to coordinate agency activities relative to its concession agreements. For instance, in 2012 the City pushed for the State of Illinois to approve a bill restricting handicap parking licence plates and placards, which had allowed individuals exemption from parking fees (Garcia, 2012). This need to manage exposure to compensation events has enhanced the power of the Departments of Finance and Revenue, a change likely to complicate the City’s pursuit of comprehensive environmental and economic development goals through planning tools such as Bus Rapid Transit or dedicated bike lanes (see Siemiatycki and Farooqi, 2012).

Conclusion

Previous accounts of privatisation tend to treat the contracts leasing public assets as the beginning and end of the story. Privatisation advocates, for example, view the concession agreements as making future relationships between public and private more evident and therefore manageable. A lawyer himself, former Mayor Richard M Daley frequently invoked the length of Chicago’s asset-lease agreements to argue that the City would be protected from all negative contingencies and that the risks involved in asset ownership could be assigned to non-local actors.

Treating these transactions as instances of financialisation, however, requires a broader analysis of state power and network relationships. Our assessment of Chicago’s infrastructure concession deals approaches this analysis in three ways.

First, we scrutinise the production of infrastructure ‘commodities’ that then circulate, disembedded, in global financial circuits. At the local scale, though, financialisation entails not just the disembedding of urban assets but also a complex process of governing urban problems through finance. The City played a key role in producing a financial market for urban infrastructure assets, mobilising an extensive network of actors and generating powers necessary to transform infrastructure into value for investors and creditors. Asset sales provided Chicago with essential manoeuvrability during deep fiscal crises.

Second, many of the state powers mobilised within these infrastructure transactions have been directed towards co-managing the extraction of profits. Because the asset’s value relies on revenue streams prone to disruptions ranging from general economic trends to the availability of competing transportation alternatives, infrastructure securities require substantial post-sale state management. The high pay-outs Chicago earned from the Morgan Stanley and Macquarie-led consortia depended on the City’s commitment to secure these revenue streams both through contractual provisions to allow substantial rate increases and restrain competition, and (in the case of the parking meters deal) to enforce a wider set of traffic regulations and practices to incentivise parking payment. This required shifting management for traditional service functions to the City’s executive as well as reorienting other functions towards new standards of short-term revenue growth.

Third, the commodification of urban infrastructure commits the City to continually revisiting and re-negotiating a set of ongoing exposures produced within each transaction. For instance, monetising significant portions of the City’s transportation system has exposed conflicts with key urban management functions – ranging from street closings to zoning approvals – that did not exist under earlier modes of service delivery. This required new forms of public sector expertise oriented to handling the lawsuits, compensation claims and related charges against the City, further enhancing the role of the City’s finance department in coordinating urban management.

Furthermore, even though it focuses on three transactions undertaken in a fairly short time frame, our analysis suggests that financialisation at the urban scale can be usefully approached as a recursive policy project – wherein each round of transactions creates powers, orientations, and constraints that pattern a tendency towards more financialisation. Recent developments in Chicago suggest two trends shaping this recursivity.

On the one hand, the City’s new powers increase its capacity to govern urban problems through financial markets. Despite calls for stringent controls over the terms of private investment in urban infrastructure, the City has tested the limits of ‘responsible’ privatisation and found it wanting: a 2012 process to re-bid Midway Airport failed when no bidders were willing to pay for a concession lease that was only 40 years long (Holeywell, 2013). Rather, the latest rounds of deal-making explored direct financial partnerships with investors as means to maximise the extraction of value from infrastructure. The new Chicago Infrastructure Trust, an initiative housed in a separate non-profit agency (off the City’s balance sheet) yet controlled by the mayor, is expressly mandated to find ways to package and sell revenue streams from public infrastructure projects and places the City in a central role coordinating repayment to investors (City of Chicago, 2012).

On the other hand, the fiscal and political capacities generated by the deals have proven contingent or even fleeting as broader problems, such as rising health care costs and pension obligations, increase demands on the public fiscal base. Within two years of inking the deal, Chicago spent $973 million of the parking meter proceeds, 94% of which financed routine city operations in the wake of recession-induced revenue shortfalls. The rating agency Fitch downgraded the City’s bond rating in part because it was relying on these one-time events to fund ongoing operations (Fitch Ratings, 2010). Converting relatively stable income sources (like meter revenue) into a short-term budgetary fix defers reckoning with structural budget problems at the cost of deepening them, a process which ultimately will require a new set of short-term revenue solutions and experimentations. Like the networks the City has woven around itself, these exposures predispose Chicago towards future privatisations. These transactions deepen the financial obligations of the local state and complicate the very fiscal management they aim to solve.

Footnotes

Acknowledgements

The authors would like to acknowledge the capable research assistance provided by Abby Crisostomo and Zafer Sonmez, as well as Bob Lake and the Rutgers PhD Colloquium, David Wilson and the UIUC Urban Prisms seminar, Peter Wissoker, and two anonymous reviewers for comments on earlier drafts of this paper.

Funding

This research received no specific grant from any funding agency in the public, commercial, or not-for-profit sectors.