Abstract

This paper questions the effects of the financialisation of Indian real estate markets with a focus on the Bangalore city-region. Research on Southern cities has concluded that globally connected but locally embedded real estate developers contribute to anchoring transnational investment. Yet, the acknowledged dearth of studies on the real estate industry in post-liberalisation India limits our understanding of the ongoing empowerment of local urban actors, including developers. Adopting a cultural political economy perspective, the paper analyses how developers leverage finance capital to achieve greater economic and political agency and thus contribute to the material, symbolic and political transformations of cities. It first demonstrates that finance capital has sustained Bangalore-based developers’ growth strategies throughout Southern India. Subsequently, developers shape the materialities of metropolises via a piecemeal juxtaposition of medium-sized developments. Although this may occasionally meet government strategies for modernising their cities, it more often than not constitutes an understudied obstacle to States’ mega-projects that are outdone by developers’ ability to work through the intricacies of local land markets and bureaucracies. Furthermore, having become dominant city-builders, developers are in a situation to circulate representations concerning what the desirable city should be. Such narratives aim at inserting local real estate markets into globalising financial commodity chains while also legitimating developers’ own role. Consequently, developers attempt to promote – with some success – prescriptions in favour of State reforms and the adoption of pro-urban growth policies. The ongoing financialisation of urban production thus participates in the self-empowerment of developers in India’s cities.

Keywords

Unlike other major cities around the world like London, New York and Singapore, where commuting and infrastructure is a government prerogative and is efficiently managed, in India, the onus to provide a similar efficient environment is on the private sector by imbibing contemporary trends of modern global cities. (Developer, Times of India, 25 March 2013)

Studies on the financialisation of urban production insist on the growing role of financial intermediaries that collect the savings of households, firms, or governments and invest them in the construction and management of the built environment. These intermediaries, sometimes referred to as Finance Capital Investors (FCIs) (Attuyer et al., 2012), have diversified their sectoral and geographic investments using both technological and financial ‘innovations’ and political deregulation. This includes so-called emerging markets where prospects for demographic and economic growth have attracted financial intermediaries seeking to invest in the development of urban infrastructure, as is the case with India on which this paper focuses.

Notwithstanding the limited amount of research, the financialisation of urban production in countries of the South is generally studied from a ‘follow the money’ perspective, for example from an investment boardroom in Manhattan to a plot of land in the rural periphery of Bangalore, India (e.g. see Halbert and Rutherford, 2010). Although they highlight how developers ‘make space for capital’ (Searle, 2010), such North–South perspectives risk depicting the financialisation of urban production as an exogenous and overarching process, thus neglecting postcolonial criticism of ongoing research into global/world cities (Roy and Ong, 2011). Furthermore, existing research literature remains inconclusive as to how FCIs directly or indirectly influence the conditions and content of urban development, especially in countries of the South. Some authors claim that the profit-seeking and volatile capital associated with the investment strategies targeting India’s metropolises contribute to the newly-built glittering cityscapes (Searle, 2010: 9) and forms of ‘speculative urbanism’ (Goldman, 2011). However, these claims need to be substantiated by analysing the understudied mechanisms through which the rising importance of FCIs may impact urban development.

Observing developments in the real estate sector, research literature has so far questioned how transnationally connected but locally embedded developers constitute entry points for FCIs. As in other national contexts (Theurillat and Crevoisier, 2014), it has concluded that developers are key players in ‘transcalar territorial networks’ that channel distant investment into the urban built environment (Halbert and Rouanet, 2014). However, beyond recognition of developers’ role in anchoring finance capital, existing research literature has failed to examine how their ability to harness finance capital contributes to developers’ self-empowerment – that is, achieving greater economic and political agency.

Weighing up both material and symbolic considerations, as encouraged by the cultural political economy approach (Sum, 2005), this research looks at how recourse to the capital brought in by FCIs enables corporate developers to transform the material, symbolic and political landscapes of Indian cities. The hypothesis is that the inflow of finance capital has enabled developers to transform urbanisation patterns and the politics of urban development. This will be tested by analysing the real estate development sector in India, with a particular focus on the Bangalore city-region. The strong demographic growth of the metropolis and international exposure as part of the global IT production network (Parthasarathy, 2004) has attracted FCIs which have provided local family-owned developers with construction finance. 1 The latter have been at the forefront of urban dynamics in Southern Indian cities and of changing national urban policies.

The first section examines how developers along with other intermediaries cater to FCIs’ interest for the urban built environment of what the finance industry calls ‘emerging markets’. The second section discusses how a cultural political economy perspective helps in understanding the role of corporate developers as active urban players in India. The third section provides empirical evidence of the sudden appetite of FCIs for the Indian real estate sector in the mid-2000s, and how, in turn, certain developers have leveraged finance capital to sustain their own growth strategies. The following sections demonstrate how developers powered by finance capital have become more dominant economic actors in the material, symbolic and political transformations of Indian cities. The fourth section analyses their role in changing material and symbolic urban landscapes while the fifth section examines the ways in which these developers and their representative organisations attempt to influence the planning agenda at various levels, particularly to support pro-urban growth policies and State reforms.

Financialisation, real estate developers and contested urban dynamics: A view from the South

Financialisation is a structural transformation characterised by ‘the growing influence of financial markets over the unfolding of economy, polity and society’ (French et al., 2011). Applied to urban production, it does not solely refer to the cyclical switching of capital from the primary to the secondary circuit (Harvey, 1978, Lefebvre, 1970). More systematically, it highlights the ways in which land, buildings and infrastructure, along with the activities involved in their production and management, enter into the investment practices of financial intermediaries (Guironnet and Halbert, 2014). Technological and financial ‘innovations’ such as securitisation (Leyshon and Thrift, 2007) and the adoption of favourable regulatory environments (Corpataux and Crevoisier, 2005; Gotham, 2006) support further integration between financial markets and the built environment. The latter is increasingly appraised as a ‘quasi-financial asset’ (Coakley, 1994) by FCIs aiming to simultaneously expand and diversify their portfolios (Lorrain, 2009; Seiler et al., 1999; Torrance, 2008).

Although the concept of financialisation is first and foremost conceived for accumulation regimes of old industrialised countries (Aglietta, 1979; Boyer, 2000; Stockhammer, 2008; Sweezy, 1997), a similar process is observed in countries of the South. This stems firstly from the increased appetite of investors based in western countries. Following the initiatives of a World Bank subsidiary in 1986, financial institutions such as investment banks and pension funds started allocating parts of their financial resources to what they termed ‘emerging markets’ due to the promise of growth rates that far outstripped those available in their home-markets. Secondly, benevolent national policies encouraged – or constrained – by international financial institutions were implemented to provide capital for governments, firms and households from global investment funds. Thirdly, in addition to finance capital inflows, commercial trade surpluses (based on manufacturing or oil exports) and/or the growing wealth of well-off households in these ‘emerging markets’ also supported the expansion of domestic financial markets. Consequently, the real estate sector attracted the attention of FCIs for whom buildings and infrastructure work like stores of value that lock in part of the wealth associated with the fast-paced economic and demographic growth of cities.

Set against this context of increased interdependence between financial and real estate markets, the literature on the financialisation of urban production has highlighted the geographical nature of the process at work and its intrinsic contradictions (see Halbert et al., 2014 for a discussion on commercial property markets). Financial intermediaries that ceaselessly ‘commensurate’ assets one against another (see Rutland, 2010) further reinforce the liquidity of capital by improving its geographic mobility (Corpataux et al., 2009). At the same time, to realise the value locked into the urban built environment, investors need to secure access to assets that are irrevocably fixed (Harvey, 1982). ‘Anchoring agents’ are thus needed to work as conduits channelling investments to a given location (Theurillat and Crevoisier, 2014), including the countries of the South (Cattaneo Pineda, 2012; David and Halbert, 2014a, 2014b; Socoloff, 2012). Along with international property consultants and lawyers, developers pro-actively attract FCIs by designing, building and managing the real estate projects sought by them, thus organising ‘transcalar territorial networks’ that link distant investment boardrooms to land parcels (Halbert and Rouanet, 2014). Locally-embedded but transnationally connected, they ‘filter away’ the risks that FCIs associate with ‘emerging markets’. By selecting investment ‘hot spots’, tackling legal and social-political obstacles, and implementing the physical transformations expected to suit investors’ preferences, developers contribute to inserting local real estate markets into transnational financial commodity chains (Halbert and Rouanet, 2014).

The apparently quasi-symbiotic relationship between FCIs and the real estate development industry is nonetheless fraught with conflicts. There is friction over professional practices (project management, reporting, autonomy in decision-making, etc.) and over the capture of real estate surpluses (David, 2013; Searle, 2014). Such tensions are heightened by the observed volatility of financial markets. Pressured by investors to guarantee timely exit options that ensure capital liquidity, developers – and thus local real estate markets – are exposed to wider macro-economic shifts (think of how the Global Financial Crisis resulted in a flight of capital away from ‘emerging markets’).

Despite such tensions, developers are crucial agents in intermediating between financial and real estate markets (Charney, 2003; Searle, 2014) inter alia by handling negotiations between the expectations of investment funds and local policy-makers and planners (Guironnet et al., 2016; Theurillat and Crevoisier, 2013, 2014). However, in the context of cities of the South, and in particular Indian cities, research that analyses the financialisation of urban production may be tempted to implicitly assume a mechanistic link between investor expectations and the newly-built urban landscapes (Goldman, 2011).

Rather than understanding developers solely in terms of their contribution to ‘mak[ing] space for capital’ (Searle, 2010), this paper questions how they actively leverage finance capital to support their own ambitions. The hypothesis to be tested is twofold. Firstly, that developers that harness finance capital strategically use it to bolster their industrial growth. In a real estate development sector whose observed fragmentation partly reflects a dependence on family- or community-based financing, corporate developers expertly play globalising financial circuits in order to increase their market share within their original city-region and expand into other cities. And as a consequence, they strengthen their capacity to build contemporary cityscapes, along – or, as we will show, in competition – with public authorities. Secondly, because of their resulting enhanced position as city-builders, corporate developers are in a situation to retain and circulate representations and narratives of the ideal-type city. This would include prescriptions concerning planning priorities, infrastructure and service provision and the role and legitimacy of public authorities and culminate in a pro-urban growth agenda that fit in with developers’ own immediate interests.

This has particular significance in India where post-liberalisation urban dynamics have witnessed the empowerment of local urban actors that resent the failures of public policies seeking urban modernisation and internationalisation (Shatkin, 2014a). The Government of India and regional states (the latter being principle decision-maker in urban development matters) have promoted pro-urban initiatives based on the assumption that metropolises are the country’s economic motors. These include public subsidies for infrastructure development and urban governance reforms such as the Jawaharlal Nehru National Urban Renewal Mission (JNNURM) or the 2005 Special Economic Zones (SEZs) that promote the deregulation of land markets and public–private partnerships inter alia. Yet, obstacles to this entrepreneurial agenda are numerous. The importance of rural constituencies hampers government willingness to resolutely support pro-urban agendas (Pinto, 2000). Furthermore, the informalisation of land tenure and planning (Roy, 2009) paves the way for paralegal arrangements that undermine official policies and programmes (Benjamin, 2008; Roy, 2009). Therefore, multiple ‘insurgencies’ and ‘blockades’ arise (Roy, 2011; Shatkin, 2011), ranging from delays over the completion of SEZs to abandoned urban mega-projects. Re-scaling of State practices (Shatkin and Vidyarthi, 2014; Weinstein et al., 2014) and State-backed ‘world city’ projects relying on ‘mass dispossession’ (Goldman, 2011) are thus more often than not derailed by farmers’ resistance and urban poor groups’ ability to enrol street-level bureaucrats and municipal elected representatives (Benjamin, 2008). As Shatkin (2014a) argues, such failures lead to mounting frustration among the very urban actors that seek to benefit from the transformation of Indian cities into global metropolises. This is true for middle class groups and business elites as well as for corporate developers whose rise has mirrored India’s urbanisation and economic and financial liberalisation since the 1990s.

Yet, current understanding of attempts by these local urban actors to achieve political agency on the contested terrain of Indian metropolises remains piecemeal (see the remarkable efforts in Shatkin, 2014b). Some research has observed the promotion of urban reforms through informal networks of influent local actors (see Ghosh, 2005, 2006; Sami, 2014 on the Bangalore Agenda Task Force and on local NGOs that inspired national pro-urban growth reforms such as JNNURM). Others have examined the delicate role of political entrepreneurs that single-handedly assemble heterogeneous local interests and actors (Weinstein, 2014). However, as argued by Shatkin and Vidyarthi (2014), the ‘grounding up’ process whereby urban actors promote an urban growth agenda remains clearly understudied, especially in relation to real estate developers:

The dearth of explorations of the emerging agency of actors who have coalesced around new economic activities and land markets marks a significant gap in the study of contemporary urban politics in India … The development of such perspectives involves a deeper interrogation about the roles of emergent political actors like real estate developers. (Shatkin and Vidyarthi, 2014: 7) There is almost no literature, for example, on the real estate industry – the actors who shape it, the models of urban development they adopt, and their influence on urban policy. (Shatkin and Vidyarthi, 2014: 15–16)

Linking this concern to the study of the financialisation of urban production in countries of the South, this paper tests the hypothesis that the ongoing self-empowerment of Indian corporate developers is related to their ability to transform finance capital into new material and symbolic cityscapes and pro-urban policy demands.

A cultural political economy perspective on urban change

This paper adopts a research protocol underpinned by a cultural political economy perspective which analyses the economy as a combination of material resources and capacities together with the discursive economic imaginaries associated with these (Sum, 2005: 1):

The translation of diverse economic, political, and social interests into effective agency […] depends not only on material resources and capacities but also on the ability to define and articulate identities and interests into specific accumulation strategies, political projects, and hegemonic visions in and across different scales. Thus, agency has both material and discursive bases and […] struggles among competing forces and interests […] are normally waged as much through the battle for ideas as through the mobilization of primarily material resources and capacities.

Therefore, we argue that developers should not only be looked at in terms of their economic status and power but also, to paraphrase Sum, ‘the[ir] capacity to articulate compelling visions that combine political, intellectual, and moral leadership with a flow of material rewards’ (Sum, 2005: 1). In addition to their contribution to the material transformations of city-regions and associated capital accumulation, developers may also be active in the selection and retention of ideals and values that are embodied in economic and urban imaginaries which they attempt to disseminate throughout the wider society.

The Bangalore city-region constitutes an interesting case in point as it illustrates how some cities of the South are targeted by FCIs to boost their overall portfolio performance. The finance capital held by insurance companies, investment banks, sovereign funds, family offices and other hedge funds has poured into the city’s property markets, especially in the mid-2000s (Halbert and Rouanet, 2014; Searle, 2014). This observed investment frenzy is often associated with the insertion of Bangalore’s productive system into global value chains (IT, Biotech, etc.), its related urban growth (from 5.1 million inhabitants in 2001 to almost 8.4 million in 2011 according to the Census of India 2011, Ministry of Home Affairs), and government-led entrepreneurial policies (Goldman, 2011). This has led to conflict-ridden urban development. On the one hand, allegedly speculative strategies at all levels of the social spectrum help sustain huge increases in land prices (Goldman, 2011) and the eviction of less wealthy households and economic activities (Benjamin, 2000; Halbert and Rouanet, 2014). On the other hand, surpluses generated by ‘informal’ economies combined with ‘vote-bank politics’ linking local political elites, street-level bureaucrats and poor households occupying land, may limit the development of global cityscapes (Benjamin, 2000, 2004, 2008). Against this background, this paper examines how a limited number of Bangalore-based developers have sourced finance capital to support their own development trajectories and been able to influence urban changes at local and national level.

The research protocol first undertook an analysis of finance capital investments in the Indian real estate sector at intra and inter-city level. Over 500 foreign and domestic investments 2 between 2005 and 2011 have been collated based on a review of the national and local economic press as well as data published by real estate brokers. Data provided information on: (a) the amount, origin and initiators of investments; (b) the developers involved; and (c) the location and types of development projects. This gives a unique understanding of the geographical expansion of developers that harnessed finance capital as well as their contribution to the changing materialities and spatialities of Indian cities.

Adopting a more qualitative perspective, the second part of the protocol is based on an analysis of a documentary corpus comprising publicly-available information on developers (annual reports, online data, interviews and analyses in the press, conferences, etc.) as well as other material relating to: (a) planning issues at both national and Karnataka State level (from national policies dealing with land issues to the Bangalore Master Plan); and to (b) the financing of real estate developments. This corpus is complemented by around 120 semi-directive interviews conducted between 2006 and 2013. A first batch of 59 interviews was conducted mostly with senior executives of development corporations. The topics discussed included: the history of the company; its main clients, markets, and activities (including land acquisition and conversion), with a particular focus on the geography of development projects at intra- and inter-city levels; issues related to construction finance and the company’s growth along with a detailed discussion of the role of FCIs. Interviews also involved a discussion of planning issues and relations with public authorities in charge of city-regional development. To gain a more consistent and dynamic understanding, several interviews were conducted within the same organisation, either with the same person in different years or with interviewees holding different positions. In a number of instances the interviews – which were typically one to two hours long – were rounded out by on-site visits that provided an occasion for less formal discussions. The interview material has been cross-analysed with a second batch of 65 interviews with other actors involved in the property development market: real estate brokers, lawyers, ‘middle men’, private planners and architects, civil servants from different agencies involved in the production of the built environment (including the Bangalore Development Agency, the Karnataka State Planning Board, the Karnataka Industrial Area Development Board, and the Bangalore Metropolitan Regional Development Agency, etc.). This aimed at contrasting the data collected from the developers and helped to analyse their explicit or implicit conceptualisation of transformations in the city-region and how other actors respond to these.

Cashing in on finance capital investments

The prelude to this story is rooted in the increasingly tight-knit relations between the real estate development sector and financial markets in India. A first illustration is provided by the repeated attempts by central government to support the country’s development by easing access to foreign capital. Since 2001, foreign developers with a core construction activity who were previously banned from owning property – with the exception of IT-related properties – have been allowed to build integrated townships of more than 100 acres (40 hectares), including housing, commercial premises, hotels and resorts. 3 In 2005 Foreign Direct Investment status (FDI) was extended to all types of foreign investors, including financial institutions, while the minimum threshold for built-up areas was also lowered (50,000 sqm. for development projects, 25 acres for serviced housing plots). The same year, the Special Economic Zones further encouraged FDIs to engage in real estate activities by securing land titles and providing fiscal incentives. A second illustration is the deregulation of capital-risk. In 2004, Venture Capital Funds (VCFs) were allowed into property development companies, inviting not only domestic but also foreign investors to participate in developers’ growth, since VCFs had been opened to foreign financial institutions in 2001. Overall, by removing ‘regulatory impediments’ to capital mobility (Corpataux et al., 2009), national authorities have played a key role – as they also have in other contexts (Gotham, 2006) – in overcoming the illiquidity of properties. Combined with the growing appetite of FCIs for ‘emerging markets’ and strong prospects for urban growth, these policies have stimulated finance capital inflows to Indian real estate markets.

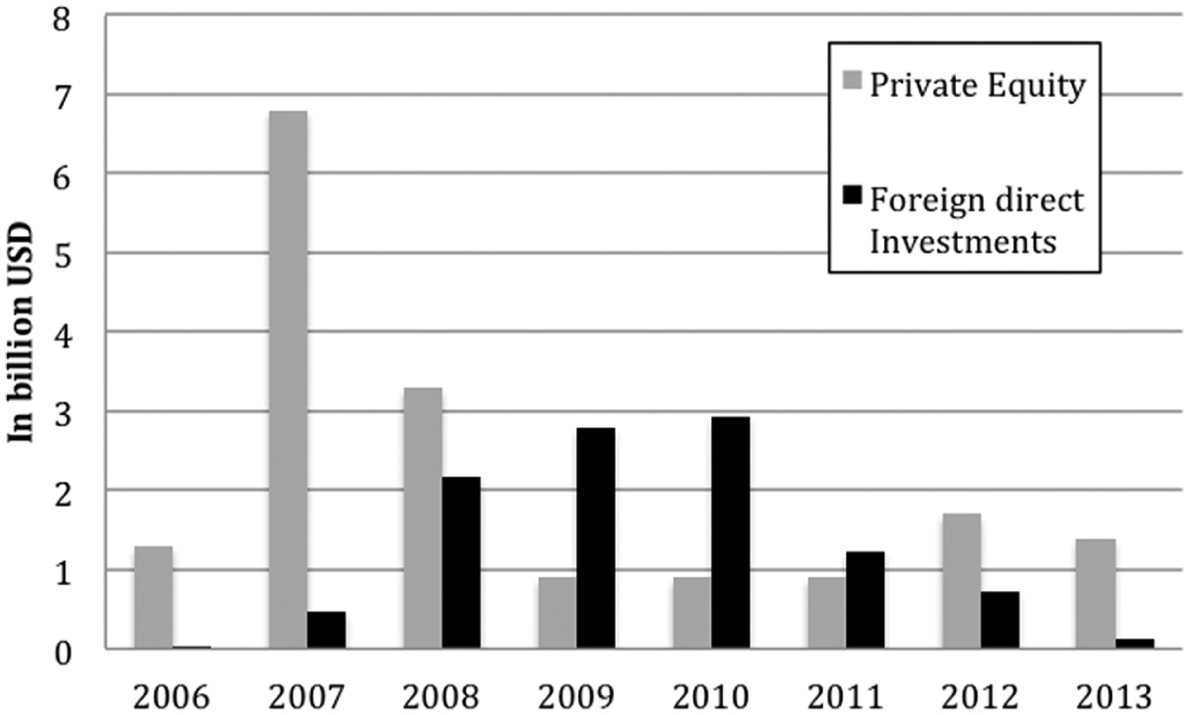

Although data remain fragmented, investments peaked between 2005 and 2008 (with FDI ranging between USD 2.5 billion and USD 3 billion/year), before declining from 2009 onwards (see Figure 1).

Private equity and foreign direct investments in the construction sector in India (2006–2013).

Such quantitative evolutions have brought qualitative changes to construction finance. Before 2005, money mostly came from private lending and bank loans. However, recourse to banking intermediation by developers was – and still is – limited by the central authorities to construction activities, thus excluding land acquisition. With the aforementioned developments in the regulatory environment from 2005 onwards, financial markets became a major source of financing, first in the form of equity investments (private equity or a public listing on Indian and foreign stock markets). However, since the 2007–2008 meltdown, pure equity is scarcer and the remaining financial investors tend to opt for debt instruments.

Capital brought in by FCIs is pooled into India- and/or real estate-specific funds that are legally attached either to the fund manager’s home country (e.g. US, UK, Singapore), to India, or to tax havens such as Mauritius, which benefits from a double tax exemption treaty. Investment managers that sit in offices located either in the global or continental headquarters of the financial institutions concerned (New York, London, Singapore, Dubai) or in Mumbai, are usually dealing with funds in the range of USD 100 million. Such capital comes subject to conditions: unitary deals are usually capped at several USD 10 million; expected returns on investment are very high (25–30% p.a.); investment duration is short to mid-term (eight years or less); the preference is for investments in India’s main metropolises; buyback options are imposed on developers in case there is a lack of better alternatives (sales to another investor or Initial Public Offerings – IPOs).

These conditions vary over time according to developments in the real estate market and to changing investor assessments of macro-economic trends. Currency volatility may deter foreign investors: for example, profits have been potentially harmed by the depreciation of the Indian Rupee over the last three years. Similarly, after the 2007–2008 meltdown drove away many FCIs, those who stayed imposed more stringent conditions on developers. Empirical material reveals that these include: more frequent and stricter surveillance over a project’s lifecycle; a preference for residential projects due to their self-liquidating nature and for leased commercial assets that already generate income; and a preference for ‘last mile financing’ of ongoing projects rather than on land acquisition. Given the slower absorption of real estate stocks since 2009 due to lower demand from upper-middle class households and export-oriented service firms, developers are facing difficult times: as investors exercised buyback options to speed up their exit from India’s real estate, some developers were facing threats of bankruptcy and sought to reduce their indebtedness by divesting so-called non-core assets, including the very lands acquired during the mid-2000s investment frenzy.

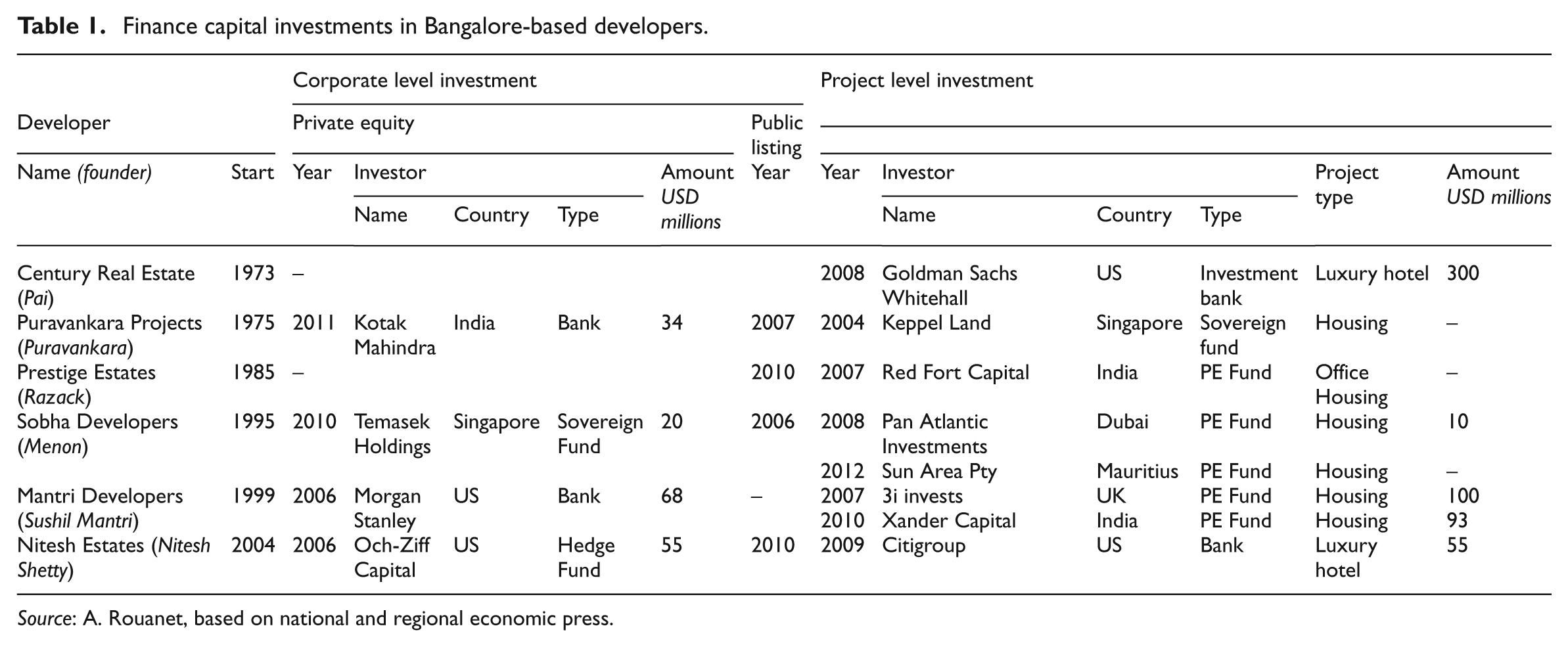

In spite of the volatility of capital inflows, a number of Bangalore-based developers have still managed to become dominant players in the city-regional market by harnessing finance capital. As in many Indian cities, our interview material attests that the development sector remains fragmented with a plethora of local businesses relying on family or community-based financing. However, to meet the booming residential and non-residential demand of the 2000s, some developers have strategically teamed up with FCIs, the latter entering either in the form of Special Purpose Vehicles for dedicated real estate projects (hotels, malls, business parks, townships), or by acquiring equity stakes in the development company (Table 1). Transnational, community-based networks have been called upon: the Muslim developer Bearys’ Group claims to hold a USD 20 million investment from a Saudi Arabian Shariah-compliant wealth management fund. The capital pouring into the city has also supported newly-incorporated developers: in 2006, a New York-based hedge fund acquired 25% of Nitesh Estates, a development company launched only two years before.

Finance capital investments in Bangalore-based developers.

Source: A. Rouanet, based on national and regional economic press.

Finance capital has proved a remarkable accelerator for some developers. Firstly, part of the financial manna has been used to speed up land acquisition, 4 as illustrated by Sobha developers’ IPO in 2007 that explicitly aimed at boosting land acquisitions throughout South India (Moneycontrol.com, 20 January 2007). Secondly, it has allowed developers to industrialise their production process. In 2012, Prestige Estates estimated that its 56 ongoing projects amounted to a total built-up area equivalent to all of its previous 165 development projects put together.

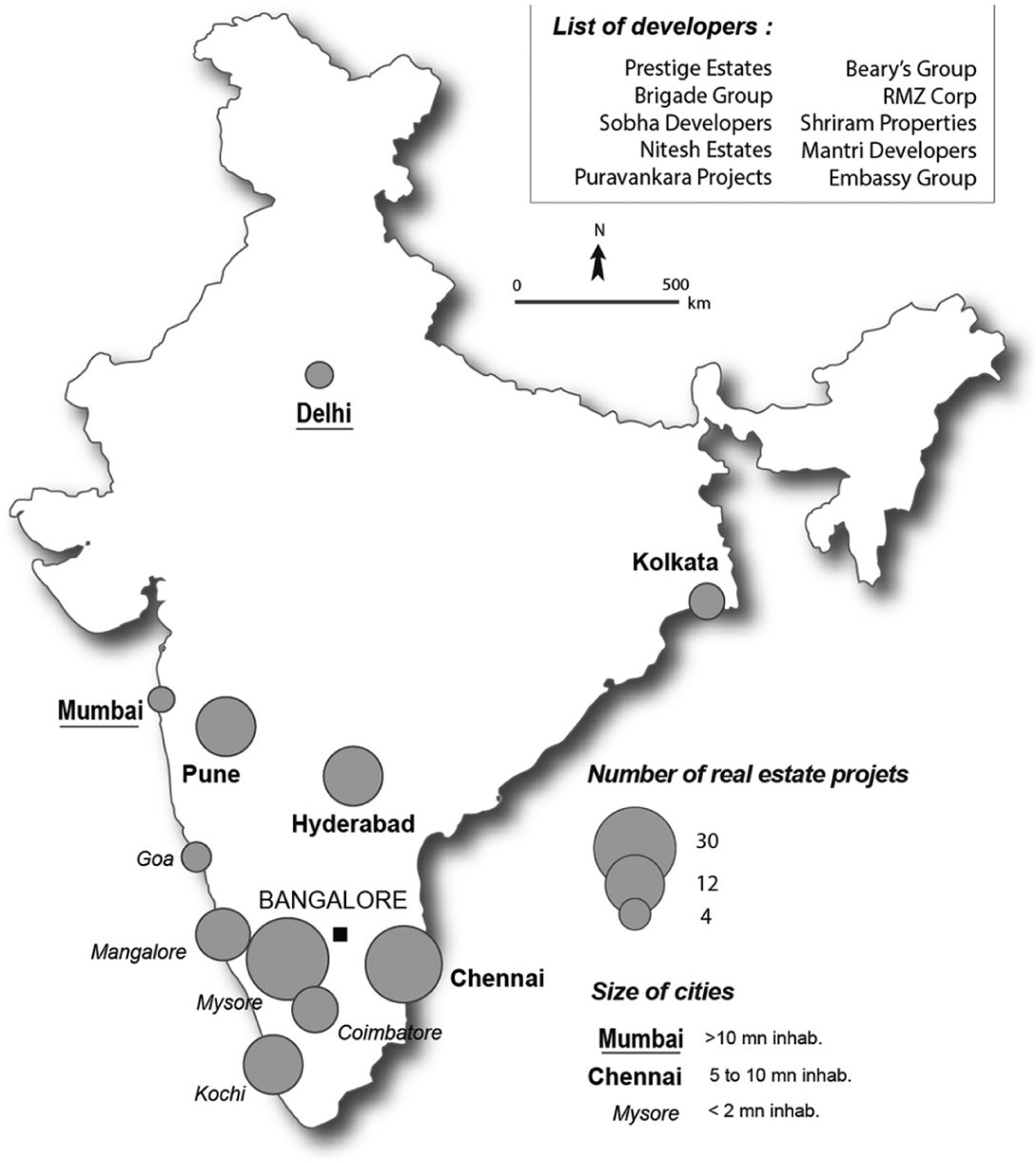

Building on this momentum, developers have expanded their activities outside Bangalore. The same Prestige Estates estimates that half of its 450 acre land bank is currently located outside the Bengaluru Metropolitan Region. While some developers use historical family connections and experience to reach the medium-sized cities of the surrounding Karnataka state, all of the top 10 developers attracting FDI have expanded to the state capitals of Southern India (see Figure 2). This scaling up does not just aim to accelerate their growth, it also seeks to reduce investor risk exposure to the Bangalore market.

Location of development projects outside Bangalore for 10 major Bangalore-based developers (2005–2011).

Developers and the transformation of India’s cities

Powered by finance capital inflows, these developers have set the pace in the transformation of intra-metropolitan Bangalore. At individual project level, although most dominant spatial features in the residential sector, such as high-rise condominiums and gated community-style villas were already tried in the 1990s (Varrel, 2010), developers have moved in less than a decade from 10 unit-strong projects on average to several hundred units. This has gone hand in hand with the rise of walled and gated enclaves said to be self-contained because they provide services for the exclusive use of residents, including small shops and sometimes schools or hospitals (Developer _10). A similar development has occurred in the non-residential sector. Commercial real estate projects increased in size with larger-scale buildings and campuses, while the use of physical barriers and on-site services further detaches them from other city spaces. 5 By providing townships and business parks with their own water supply and sewage management systems, 24/7 power backup facilities and outdoor recreational spaces, developers claim to tackle the ‘hassle’ associated with deficient public infrastructure (Developer_2 and Developer_14).

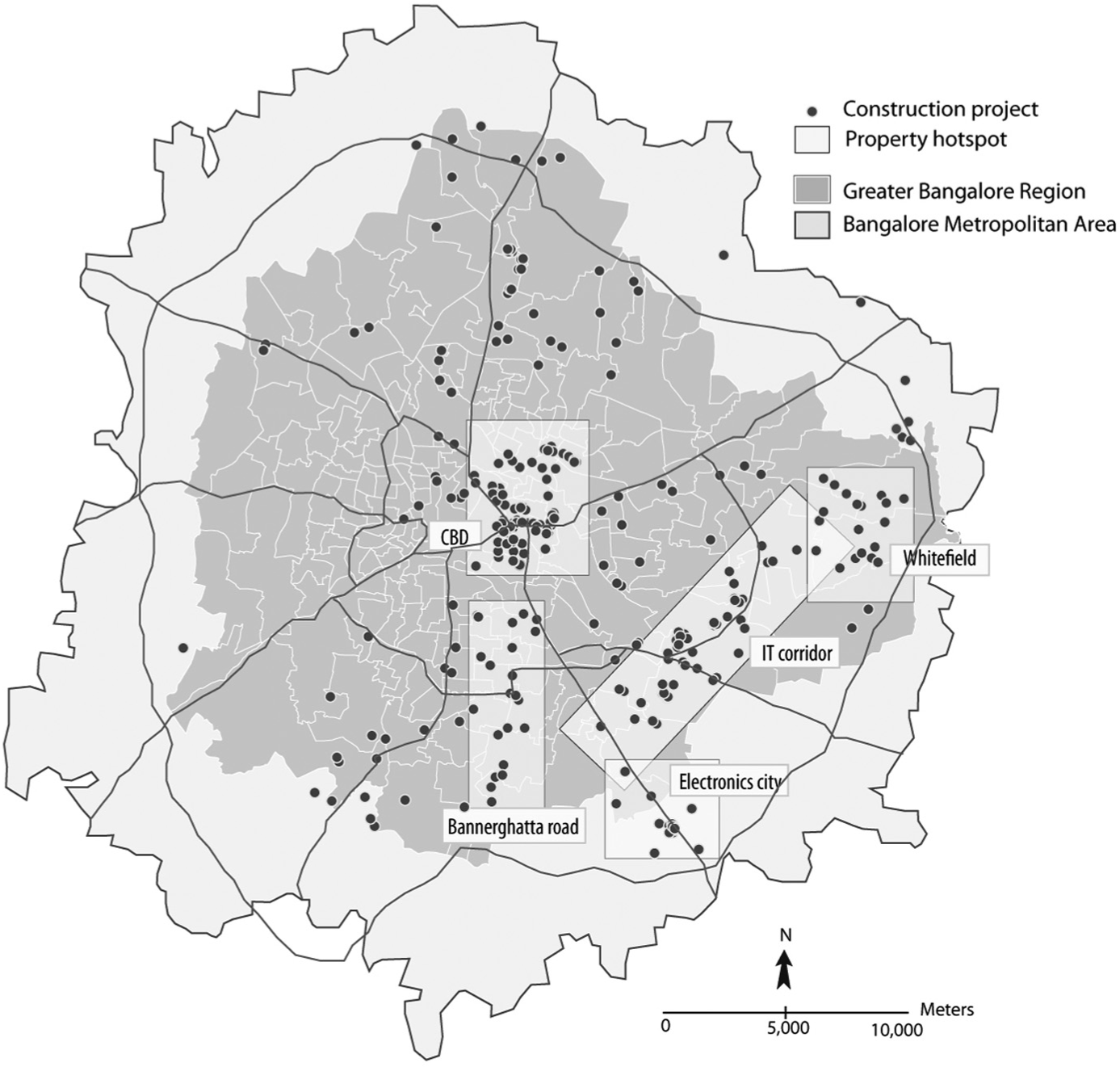

When added up, all of these myriad developments account for the wider spatial and social reorganisation at metropolitan scale. A cartographic analysis of projects between 2005 and 2011 reveals that finance capital investments were actively channelled by developers into selected places (see Figure 3). These include ex-urban locations sometimes earmarked by government agencies as IT and industrial zones (Heitzman, 2004; Stallmeyer, 2010; Walcott and Heitzman, 2006), as illustrated by Electronic City or the Whitefield area. The latter is located 20 km east of Bangalore and used to be an agricultural area surrounding an Anglo-Indian village. There, using its eminent domain power, the Karnataka Industrial Area Development Board (KIADB) assembled 500 acres of land to set up an export-oriented zone for software companies. However, the kick-off development is based on the initiative of an FCI. Teaming up with KIADB that provided cleared land titles, a Singaporean sovereign fund set up the International Tech Park Bangalore (ITPB) in 1997 and later listed it offshore along with other Indian business parks. IT parks and gated residential projects financed by FCIs subsequently proliferated around the ITPB, some located on KIADB land, but many more on converted agricultural lands, and – in contravention of all regulations – on traditional lakes and tanks. By surfing on the wave of finance capital inflows and by cashing in on public initiatives (investments in infrastructure and sometimes the provision of land), developers have been central to the transformation of Whitefield from a village to an edge city, and, more generally, to reshaping Bangalore into a more multi-polar and fragmented city-region.

Location of construction projects within Bangalore metropolitan area (2005–2011) by developers having access to finance capital.

These observations cast a different light on the spatial changes occurring in Indian cities where State investment and the use of eminent domain rule is said to support mega-project-based urbanism (Benjamin, 2008; Goldman, 2011). Predictably, public intervention in land and infrastructure provision is helping to reshape urban dynamics, if only because they increase land values. However, the observed landscape has less to do with parastatal agencies’ master plans than the aggregation of mid-size projects initiated by developers that have leveraged finance capital and activated multiple levers to assemble land banks. On the one hand, such developers make use of parastatal agencies’ eminent domain power whenever possible: this helps overcome the hurdles of land aggregation and conversion, as in the case of Whitefield’s export zone or the burgeoning SEZs. However, our research material shows how, at the same time, developers outrun public authorities. Take the example of the south-eastern part of the metropolis where Whitefield and Electronic City have been linked by an expressway. In the early 2000s, the Bangalore Development Agency (BDA) commissioned a master plan from Jurong Consultancy, parent company of Whitefield ITPB’s Singaporean owner (Heitzman, 2004; Walcott and Heitzman, 2006). The project was to support the growth of the globalising IT sector by master planning six new towns for 1 million inhabitants (Walcott and Heitzman, 2006: 120). A decade later, far from the planned orderly development, the landscape is a piecemeal juxtaposition of fragmented IT campuses, shopping malls and towering condominiums. Most likely, with the help of able land aggregators and politicians with landed interests as suggested by our interview material, developers were simply quicker in the land market, thus blocking BDA’s proposed orderly drawn IT corridor (Times of India, 11 April 2006). Infrastructure development (a ring road, a new airport) may give general directions by highlighting areas of rent increase opportunities. Yet, the detailed geographies and forms of the current urbanisation pattern in Bangalore, one of juxtaposed, fragmented mid-sized projects, has more to do with developers’ ability to ‘have their own way’ through the intricacies of local land tenure and bureaucracy (Lawyer_2; Broker_5) than with State-planned world-city mega-projects.

The trend-setting role of real estate developers replete with finance capital goes beyond the material transformation of the urban fabric. Through the proliferation of marketed iconic landmarks staged as a series of competing events that occupy the daily news, developers provide symbols that leave their mark on the cityscape. Reading these signs that are literally all over the city (set in towering buildings, but also endlessly reproduced in iconographic materials, from the numerous advertising hoardings in the streets to ads in the newspapers), the passer-by walks through an endless construction site (Figure 4).

Sarjapur Road, Bangalore, 2 March 2008.

These symbols connect Bangalore to other world cities that are showcased as embodiments of desirable modernity. The UB City complex, a 1 million sq. ft. mall-cum-5-star-hotel-cum-office complex-cum-‘European’ plaza which boasts a miniature version of the Empire State Building, is illustrative of this ‘world class’ iconography (Figure 5). Along with proclaimed grade-A specifications (Developer_5) and internationally designated ‘green’ labels (Developer_29), architectural references can be regarded as attempts to get onto the lists of the global metropolises promoted by real estate investment advisory multinationals such as Jones Lang LaSalle’s (2012) ‘Global 300’. Hence the North American, European and Asian references inspiring developers: Bearys’ Global Research Triangle is explicitly modelled on the Research Triangle Park in North Carolina while its Lakeside Habitat project draws its inspiration from Kuala Lumpur’s Petronas twin towers.

UB-City, Bangalore, 25 February 2008.

In contrast with the observed physical fragmentation resulting from developers’ mid-sized juxtaposed projects, the underlying narrative reflects on the necessary upgrading of the Indian city to a seamless, ‘hassle-free’ agglomeration (Developer_29, Developer_8). This culminates in the utopia of a ‘fluid’ city – that is, a city where flows (of water, energy, people, and, arguably, land and capital) can freely circulate as stressed both by the interview material and the documentary corpus. Priority for urban services and infrastructure – that is, power provision, adequate water supply and waste management facilities and, above all, international and intra-metropolitan transport infrastructures, are repeatedly put forward by developers as the necessary components of an efficient city. Flyovers, bypasses and elevated toll highways are held in high regard, as well as the construction of mass-oriented transit systems such as Bangalore’s long-awaited Namma Metro. This echoes the comments of Tata Housing’s Managing Director concerning the Union Budget for 2012: ‘the measures to increased funding for highways and other infrastructure will help put more territories on the real estate map’ (Talwar, 2012: 40).

This view of a fluid city is based on a combination of contrasting attractive/repulsive urban models. Echoing research on worlding practices (Roy and Ong, 2011), inter-referencing with other world cities first aims to break with the despised imagery of a third-world megacity with its symptomatic ‘problems’ (of uncontrolled growth, traffic congestion and chronic power or water shortages) and, above all, with the failure of public authorities to ‘deliver’. On the other hand, this fluid city refers to an ideal of efficiency embodied by Western and increasingly Asian world city references (Silicon Valley, New York, Singapore and Shanghai inter alia). By showcasing development projects that fit so-called international standards and representations, the ‘worlding practices’ of corporate developers based on ‘inter-referencing’ with other world cities (Ong and Roy, 2011) follow two parallel objectives: (1) guaranteeing access to property finance by inserting city-regional real estate markets into globalising financial commodity chains; and (2) legitimising developers’ role in transforming India’s cityscapes. Following a cultural political economy perspective, it thus appears that the ability to concentrate finance capital and land enables corporate developers to appropriate material and immaterial spaces (in the daily press but also in people’s representations), and from there to advertise not only their products but also their own visions of Bangalore’s desirable future. Inter-referencing is thus as much a narrative for outsiders – that is, a means to attract FCIs (Developer_15) – as an instrument to influence the local and national urban agenda. This is achieved by conceiving and circulating an ideal-type city – a fluid world-class city – to be built not only for developers’ own interests, but as is claimed by developers themselves, in the interests of a wider society that will benefit from the modernisation of India’s metropolises.

Developers’ self-empowerment

In light of the foregoing assertions and along with the material and symbolic transformations of the city, real estate developers are conceiving, retaining and disseminating a series of prescriptions for planning objectives and the associated role of public authorities. In spite of the contempt in which they are sometimes held, 6 and without pre-empting their ability to effectively influence policy-making, developers have come up with a set of priorities that they gradually promote among civil society and political elites. Our empirical research reveals two main types of expectations: the promotion of a sustained pro-urban growth agenda and State reforms.

Pro-urban growth policies

Developers are urging national and regional authorities to embrace pro-urban policies in a more resolute manner. This is obviously not a disinterested stance as it boosts the very real estate markets in which corporate developers already have the lion’s share. The rationale put forward is twofold. First, it echoes recommendations from international financial institutions and consulting firms (McKinsey Global Institute, 2010; World Bank, 2009) whereby India’s development should rely on its main cities. Secondly, it reflects the stated priority of alleviating the indigent living conditions of urban households. Citing a shortage of 26 million housing units in India, developers and real estate advisory firms urge public authorities to take measures to support ‘affordable housing’. 7

Pursuing this twofold objective, Bangalore’s main corporate developers and professional organisations (such as the Confederation of Real Estate Developers’ Associations of India (CREDAI)) have openly requested changes to ‘archaic’ town-planning regulations and related land laws. In 1999, developers from Bangalore, supported by the openly pro-business Karnataka Chief Minister, obtained the abrogation of the 1976 Urban Land Ceiling and Regulation Act (ULCRA), which aimed at preventing the concentration of land by individual owners within metropolitan areas. 8 In 2005–2006, CREDAI – to which Bangalore-based developers are important contributors – is said to have successfully lobbied the Ministry of Environment and Forests to significantly limit the effects on the construction industry of the 2006 Environment Impact Assessment Notification, particularly with regard to public consultation requirements (Saldanha et al., 2007: 49). CREDAI also lobbied against the ‘Right to Fair Compensation and Transparency in Land Acquisition, Rehabilitation and Resettlement Bill 2013’ (LARR Bill) which replaced the Colonial-era 1894 Land Acquisition Act. Presented by the Ministry of Rural Development, the LARR Bill aims at improving compensation conditions for displaced individuals and landowners in cases of: (a) forcible acquisition by a government for its own use or for transfer to a private company for stated public purposes; or (b) acquisition by private companies of land above 40 ha (requiring acceptance of compensation by 80% of landowners). CREDAI criticised the LARR Bill for the supposedly excessive additional costs onto land values and predicted unfavourable effects for planned urbanisation by private developers: ‘The compensation package envisaged by the bill lacks proper assessment and research. The government has totally lost sight of the middle class citizens of the country who need good and affordable accommodation’ (CREDAI quoted in Sinha, Times Of India, 7 September 2011).

On the other hand, developers have welcomed legislation that facilitates land aggregation. Special Economic Zones quickly burgeoned in and around the Bangalore metropolitan region since they provide cleared land titles for developers along with tax incentives and abatements. For the same reasons, CREDAI is now supporting the creation of Special Residential Zones as a means of tackling the housing crisis: by securing favourable legal and fiscal conditions on large tracts of land, this would significantly help ongoing attempts by developers to shift their business model from the sluggish high-end residential markets to the mass market of ‘affordable housing’ development.

In addition to obtaining favourable land legislation and fiscal incentives, developers call for policy measures to facilitate access to finance capital which has proven crucial in supporting their growth in the mid-2000s. CREDAI lobbies for further deregulation of FDI in the real estate sector. The 2012 Union Budget responded favourably to its demand with the extension of External Commercial Borrowings (debts from foreign institutions) to support the development of ‘affordable housing’ and the completion of all ongoing real estate projects where FDI-based equity has already been engaged. Similarly, after 14 years of lobbying by the industry, the 2014 Union Budget finally agreed to the creation of Indian Real Estate Investment Trusts (REITs 9 ). These two policy reforms offer timely exit solutions for FCIs and cash-starved developers alike.

Reforming the state

In addition to pro-urban growth policies, real estate developers are pressing for reform of political-bureaucratic machinery. Firstly, in order to support public intervention for the modernisation of cities, certain developers and corporate leaders have called for stronger metropolitan government, thus encouraging a process of State re-scaling towards major Indian cities. Far from lobbying for the withdrawal of the State, it is the ability to steer and support the emergence of ‘world-class facilities’ for Indian metropolises that is deemed crucial (Developer_1). In 2006 for example, Irfan Razack, Chairman of the Prestige Group, called for the early adoption of the Greater Bangalore metropolitan area, pleading for ‘a single body with a single captain’ (Halbert and Halbert, 2007). This would supposedly improve the consistency of the town planning system and reallocate a larger share of the fiscal resources collected from Bangalore’s population and firms for reinvestment in the city.

Secondly, the research material shows that developers are highly critical of what is seen as a lethargic and corrupt bureaucracy. Real estate developers criticise the alleged ‘maze’ of legal procedures required for permit approvals. Citing 46 certificates and clearances delivered by as many departments of public corporations, Jai Lalit Kumar, the President of CREDAI, officially called on the Minister of Urban Development (28 April 2011) to implement a single-window clearance system. This would reduce the delays and rampant corruption that is claimed to plague the development industry:

It is the various government procedures and delays in clearances that give rise to corruption. We curse every person who exploits us to give us a legitimate permission, which we should get instantly and without any illegitimate demand. Hence, instead of blaming it on anybody, we have decided to get into the roots and find a solution. (CREDAI, 2011)

This has led CREDAI to initiate a ‘Transparency Mission’, to publicly compare delays for obtaining approvals in different cities across India, and to devise a City Attractive Index ranking cities on ‘quality of infrastructure’, ‘bureaucracy’ and ‘corruption’.

Such pressure for urban reform implicitly challenges the legitimacy of public authorities. Although public investments are strongly advocated as argued above, the stated inability of public actors to cope with the daunting challenges of rapidly-growing urban India is said to require private initiatives, especially on the part of those able developers who have demonstrated management practices of international standards that include harnessing finance capital. Or, as explained by a journalist transcribing an interview with Irfan Razack, Chairman of the Bangalore-based Prestige Estate developer: Irfan regrets that in a democratic setup like India, selfishness and greed come first. People are always thinking of themselves, thinking of easy money-making tactics. Nobody thinks of contributing to the city’s development … Sometimes he feels like asking the powers-that-be to let his group upgrade the city. (Namburu, 2007: 268).

Conclusion

This paper questioned the effects of the increasing financialisation of urban production in cities of the South, with a specific focus on India. Observing the volatile interest of FCIs in ‘emerging markets’ and the policies seeking to provide construction finance through financial markets, research literature has so far demonstrated how transnationally connected but locally embedded developers constitute entry points for finance capital investments. However, while their role in anchoring investments has been clearly documented, their ability to actively leverage finance capital in order to pursue economic and political agency has not been fundamentally questioned. This is particularly important in India where the literature compares the dearth of studies on the real estate industry with the ongoing empowerment of local urban actors – including that of developers – as a driving force in changing spatial and political urban dynamics (Shatkin, 2014a). Adopting a cultural political economy perspective, the paper sets out to understand how the process of financialisation of urban production in India may support developers’ self-empowerment and economic and political agency.

The findings highlighted by the quantitative and qualitative research material improve our understanding of the relationship between financialisation, developers and urban dynamics in two interrelated ways. On the one hand, they show how developers promote regulatory changes to deepen the interdependencies between the financial markets and the real estate construction sector. Their lobbying over the last 15 years has paved the way for the provision of construction finance by financial markets which led – along with other factors – to an investment frenzy in the mid-2000s.

On the other hand, the research provides evidence of the multiple effects associated with the ability of a limited number of developers in Bangalore to strategically leverage finance capital. Firstly, this boosted their growth by enabling them to ramp up their land banks, industrialise their processes, grow in their historical city-region market, and scale up to other South Indian cities. Secondly, powered by these financial resources, corporate developers have become more important in reshaping urban materialities and spatialities. It is arguably their practices that account for the observed multipolar and fragmented urbanisation pattern in Bangalore. More than the oft-contested master planned mega-projects under the tutelage of parastatal agencies, it is the juxtaposition of the plethora of mid-size projects built by developers – with and for FCIs – that most noticeably alters the cityscape. By harnessing finance capital, such developers thus play an ambivalent role. At times, their interest is aligned with those of States that call for the ‘modernisation’ and ‘internationalisation’ of cities. When recourse to eminent power domain and investments in infrastructure contributes to increasing land values and facilitates the always tricky business of land aggregation and conversion in India, public authorities may manage to enrol developers. But at the same time developers can also be a powerful obstacle to States’ world city projects. Developers’ ceaseless attempts to outrun public authorities in the race to capture land and real estate surpluses considerably restrict States’ ability to implement their own policies. Thirdly, comforted by their trend-setting role in reshaping the spatial organisations of metropolises, corporate developers flush with finance capital are in a situation where they can design and disseminate representations of the desirable futures of India’s cities. Wielding their newly-acquired economic power, developers have advocated – particularly through worlding practices of inter-referencing – what has been analysed here as an ideal-type fluid world-class city. The production and circulation of such narratives aims at inserting local real estate markets into globalising financial commodity chains. It also serves to legitimise developers’ role in transforming India’s cityscapes as an endeavour in the wider interests of society as a whole. Fourthly, and in relation to what precedes, developers seek to achieve greater political agency. Proclaiming their contribution to supporting economic growth and reducing the housing crisis thanks to the provision of accommodation for India’s urban households and firms, developers and their professional organisations circulate recommendations regarding State reforms and the imperative for public authorities to more resolutely embrace pro-urban growth policies. Propositions for State reform range from stronger metropolitan governance to more ‘transparent’ public action. The latter aims to reduce so-called interference of the political–administrative machinery in urban development markets, which is blamed for intolerable delays and rampant corruption that slows down urban transformations, and one might add, the profitability and liquidity of capital. Calls for pro-urban growth policies are of three types: (1) the provision of more public reinvestment in urban infrastructure; (2) measures to facilitate land acquisition through a combination of more supportive public to private land transfers and further commodification of land; and (3) initiatives to free up construction finance still further using the financial markets, especially by channelling it into the development of housing for lower- and middle-income groups, thus helping to move developers’ own business models towards ‘affordable housing’ since the decline in demand from higher-end segments since 2009. All in all, the observed financialisation of urban production ultimately participates in the process of self-empowerment whereby developers attempt to promote and, arguably steer, the transformations in India’s metropolises.

At a more reflexive level, the research invites wider consideration of the financialisation of urban production seen from the perspective of the countries of the South. Far from being a spatially exogenous, overarching and disembodied process, it is more usefully conceived of as the continuously evolving outcome of multiple power struggles and arrangements, firstly between financial investors and developers, and secondly between investors/developers and the wider local and national system of actors involved in city-making. On the first aspect, the characteristics of finance capital do not solely reflect more or less distant (and often Western) investor expectations but are also strongly dependent on: (a) institutional arrangements at national and regional levels for which developers have been actively lobbying; and (b) developers’ own strategies. Hence the idea that the characteristics of finance capital are historically and geographically situated rather than existing in overarching ‘global’ terms. Although the observed volatility in capital availability associated with ‘emerging market’ contexts reflects the influence of wider globalised financial circuits rooted in Western financial capitalism (see the effect of the US-originated 2007–2008 meltdown), the present research demonstrates that this leaves room for transnationally connected but locally embedded actors to strategically make use of such financial resources. Developers’ ability to conceive and implement major material, symbolic and political transformations in Indian metropolises needs to be corroborated by in-depth analyses in other so-called emerging markets.

Footnotes

Acknowledgements

Earlier versions of this work have been presented at the AAG annual conference (New York, 2012), the FINURBASIA seminar on ‘Financial Circuit and Urban Production in the Global South’ (Paris, June 2013) and the LATTS seminar on ‘The Political Economy of Urban Production’ (Paris, November 2014). We wish to thank the anonymous referees and the journal editor for their insightful comments. The usual disclaimers apply.

Funding

This research is an output of the joint research programme ANR FINURBASIA and received the financial support of the French National Research Agency.