Abstract

In undertaking what we believe is the first national-scale study of its kind, we provide methodologically transparent, statistically robust insights into associations and potential unfolding effects of house and contents under-insurance. We identify new dimensions in the complex relationship between householders and insurance, including the salience of interpersonal – and likely institutional – trust. Under-insurance is (re)produced along socio-economic and geographical lines, with those of lower socio-economic status or living in cities more likely to be under-insured. Should a disaster strike, such communities are likely to suffer further disadvantage, especially if governments continue to shift the responsibility for risk onto households. Our findings support the observation that insurance can contribute to increasing socio-economic urban polarisation in light of natural disasters. We conclude by considering how under-insurance may contribute to growing urban social stratification, as well as how it may produce situated ethical and political responses that exceed neoliberal aspirations.

Introduction

Within a milieu of neoliberalism and new localism (Clarke, 2009; Williams et al., 2014), the insurance of property is increasingly being prioritised as the disaster management tool of choice (Lobo-Guerrera, 2010). The privatisation and individualisation of risk and associated withdrawal of government in market-based economies (King et al., 2013; Thaler and Priest, 2014), is providing a rationale for identifying households as ‘best placed’ to manage the risk of natural disasters (e.g. Productivity Commission, 2014). In this context, insurance is assumed to provide a price signal and thus is seen as the effective motivator for individuals mitigating their own risk exposure.

Yet, at a household level there is evidence of significant rates of under-insurance, with many having no insurance coverage for property or an inadequate level of coverage. In undertaking what we believe is the first national-scale study of its kind, we identify new associations and potential unfolding effects of under-insurance. As we discuss, under-insurance can be understood – in part – as a social phenomenon that is (re)produced in relation to socio-economic inequity and issues of trust. This (re)production calls into question the sufficiency of insurance and raises the possibility of situated ethical and political responses in light of its insufficiency that exceed neoliberal aspirations (Williams et al., 2014).

In Australia, where this study is based, the insurance of private property lies solely in the hands of insurers in the form of house and contents insurance. Advancements in risk modelling are changing calculations of exposure levels and thus premium pricing and availability (McAneney et al., 2016). In countries such as the UK and USA, disaster insurance schemes underpinned by government–insurer partnerships are moving from pricing models premised on affordability to full-risk pricing, i.e. premium pricing that reflects risk levels (Nance, 2015; Penning-Rowsell, 2015).

Despite differences in approach to the insurance of property, there are cross-national similarities in relation to under-insurance. A disproportionate number of disadvantaged communities are located in disaster-prone areas (e.g. Sewell et al., 2016), and households in these communities are more likely to be without house and contents insurance.

These patterns and changes have significant and growing implications for urban areas. Some insurers have substantially increased premium prices in disaster-prone areas or completely withdrawn coverage (e.g. Nance, 2015; NCCARF, 2013; The Australian Government Treasury (TAGT), 2011), increasing the depth and breadth of vulnerability should a disaster strike. In light of climate change, O’Hare et al. (2015) observe that rather than motivating risk mitigation, insurance reinforces a cyclic pattern of ‘maladaptation’. This, as Johnson (2015) describes in relation to current patterns and trends in insurance availability, is leading to the creation of disadvantaged enclaves and concentrated pockets of protected wealth.

We believe that addressing the phenomenon of under-insurance does not simply equate to convincing more people to purchase more insurance. It relies upon a greater understanding of the complex factors comprising the relationship between householders and insurance coverage, and of how urban areas are (re)produced through the relationship between disasters and insurance. Hence, in this paper we contribute to filling a significant research gap. As we describe below, there is a scarcity of research that combines methodological transparency with sophisticated quantitative data analysis and theoretically informed interpretation of under-insurance and its effects. With the predicted increase in the frequency and intensity of disaster events due to climate change, rising disaster costs and urban population trends, there appears to be urgent need for this research.

House and contents under-insurance

Much of the available evidence of house and contents under-insurance is based on post-disaster estimates and calculations. For example, in the 2003 Canberra bushfires where 500 homes were destroyed or severely damaged, estimates of rates of under-insurance vary from 27% to 81% (Australian Securities and Investments Commission (ASIC), 2005). Teague et al. (2010) suggested that about 13% of all property losses for the 2009 Black Saturday bushfires in Victoria (where over 2000 homes were destroyed), were not insured, while for the extensive 2010/2011 floods in southeastern Australia, Lo (2013a) estimated that almost half of house and contents insurance policies did not cover flooding. 1

The insurance sector and some non-government organisations have also undertaken research into insurance uptake, though not specifically in relation to disasters, with limited methodological transparency or rigour, and without an explicit conceptualisation or interpretation (e.g. Collins, 2011, 2013; Connolly, 2014; Quantum Market Research, 2013, 2014; Tooth and Barker, 2007). These reports indicate that 4% of Australian homeowners have an uninsured property, and 7–12% of homeowners and 67–74% of renters do not have contents insurance.

When a natural disaster strikes, insurance plays an important role in the recovery of economic losses, reducing taxpayer costs post-disaster and ameliorating the social and financial costs of disasters on individuals, households and communities (Booth and Williams, 2012; Edwards, 2012). The importance of insurance in this context has been recognised in Australia (e.g. ASIC, 2005; COAG, 2002; Commonwealth of Australia, 2015a, 2015b; TAGT, 2011) and internationally (e.g. Berry and Carpenter, 2010; Forsyth et al., 2010; Jha et al., 2016; Kunreuther and Michel-Kerjan, 2015; McGee et al., 2014; Penning-Rowsell, 2015; Pitt, 2008; Talberth et al., 2006; Warner et al., 2010). Despite this recognition, house and contents insurance has received little attention beyond the largely quantitative research conducted by policy analysts and economists (e.g. Kunreuther and Michel-Kerjan, 2015; Kunreuther et al., 2011; Tarr, 2011). In such research, more often than not, house and contents insurance is understood in fiscal terms: as a benign tool that allows the burden of risk to be shared through contractual transactions with relatively small payments providing financial protection against potentially large losses.

Foucauldian scholars describe insurance in more complex terms – as an ‘art of combining various elements of economic and social reality according to a set of specific rules’ (Ewald, 1991: 197). At particular points in time and in different places, insurance institutions take on different forms through the socially embedded combination of varying economic, political, moral and juridical factors. Differing forms of insurance develop and are mobilised in spatially and temporarily variegated ways through this social constitution (O’Malley and Roberts, 2014). Liz McFall (2011) also argues that emotions are important constituting factor. For consumers insurance embodies calculation and risk, as well as love, fear and security.

In one of the few studies to closely examine house and contents insurance from a social perspective, it was found that for residents in a wildfire-prone area, insurance was ‘intricately assembled within hope, distrust, uncertainty, morality and the familial’ (Booth and Harwood, 2016: 51). Interviewees with insurance expressed a high degree of wildfire risk awareness and, supporting Eriksen and Gill (2010), suggested insurance provides a safety net for living in natural, but highly flammable areas. In this context, a combination of financial and non-financial trade-offs informed decision-making around house and contents insurance purchase including concerns about affordability, the reduction of household materiality to ‘like-for-like’ objects, and the individualised nature of insurance.

In this study, a deep mistrust of insurance companies was a significant factor in undermining interviewee confidence in insurance, with most expressing uncertainty and anxiety regarding insurers delivering expected payouts. For Booth and Harwood (2016) this rendered insurance a risk in and of itself, providing a stronger rationale for choosing not being insured than being insured: There is a general expression of mistrust, particularly in relation to the ‘fine print’ and information garnered … from insurance representatives … most participants appear to feel connected by strung-out, stretched-out ties to companies of the globalising ether … This lack of transparency and mistrust appears to be a driver for under-insurance. (Booth and Harwood, 2016: 50)

There is a persistent idea that concern about risk is on the rise and levels of trust are in decline (Doyle, 2007). Risk societies, it has been assumed, result in an erosion of public trust, and Booth and Harwood’s (2016) observation appear to support this. However, Frederiksen and Heinskou observe that ‘while there is little doubt that risk and calculation within linear time are increasing, this does not mean that trust is decreasing’ (2016: 389). They argue there remains ample space for trust, and that there is perhaps even more room for trust as risk calculation increases – as a means of dealing with the growing uncertainty this calculation brings. While trust is most often understood as a transaction-cost reducing input that acts to improve transaction efficiency between particular parties, or as a structural characteristic of organisations and networks (Murphy, 2006), in light of Booth and Harwood’s (2016) observations, trust (and mistrust) can be conceived as processes that are (re)produced in complex and heterogeneous ways, rather than things that is fixed, transferable and universal (Murphy, 2006).

In other research, there are indications of additional factors associated with house and contents under-insurance. The survey of flood-prone Brisbane residents found that risk awareness and affordability do not appear to be associated purchasing flood insurance (Lo, 2013a). However, respondents were more likely to have flood insurance cover if they expected others to do the same, or if they expected affirmation from family and friends. In other words, social norms influence insurance decision-making in the face of flood risk, and this factor acts as a mediator through its association with risk perception and behaviour (Lo, 2013b).

In insurer-commissioned market research, affordability is identified as a key factor in under-insurance, particularly for low-income earners such as single-parent households (Collins, 2011; 2013; Tooth and Barker, 2007). Access to insurance increases with age, income and educational attainment, and is also associated with being born in Australia, another English speaking country or Western nation. With specific reference to natural disasters, many householders appear uncertain about what they are covered for, with 14% of homeowners in high bushfire risk areas unsure if they were covered for bushfires, and 23% of homeowners in high flood risk areas unsure if they were covered for flooding (Quantum Market Research, 2013). Those living in regional areas appear to be more certain about the nature of their insurance coverage than those in urban areas (Tooth and Barker, 2007).

Many of these Australian-based observations complement those from other affluent countries. In the USA, low uptake rates on a government-sponsored flood insurance scheme have been documented, varying from 39% to 68% (Michel-Kerjan and Kousky, 2010). Indicators of under-insurance for natural disasters include: place of residence – those in flood-prone coastal areas and in counties with higher levels of development have higher take up rates; risk perception – for example, recent experience of flooding correlates positively with insurance up take; and socio-demographic factors – age and education are positively associated with insurance coverage (Atreya et al., 2015).

Prior to the implementation of the UK government-sponsored FloodRe insurance scheme, Priest et al. (2005) observed significant levels of under-insurance, and Whyley et al. (1998) stated that around 25% of UK residents were without house and contents insurance, identifying income and age as important indicators of under-insurance. A study by the Office of Fair Trade (cited in Hood et al., 2009: 1809) conducted in 1999 found lone parent family, young families, low income earners, and those experiencing various forms of financial vulnerability were more likely to be without house and contents insurance. Affordability, insurance-literacy and competing priorities were also identified as contributing factors (Hood et al., 2009).

Data and method

In this paper, we present findings from a national survey of Australian adults to ascertain the rates and nature of under-insurance, specifically the socio-demographic patterns in house and contents insurance uptake. Under-insurance is defined here as not possessing a current house and/or contents policy, 2 and our guiding research question for our data analysis is: ‘What are the key socio-demographic indicators of house and contents insurance coverage in Australia?’ In response to this literature reviewed above, the following hypotheses are examined empirically. Insurance coverage is expected to be higher among:

Those with high household income

Those who express high interpersonal trust

People who live in rural locations

People who are married or living with a partner

Older Australians

Those who claim to have high socio-economic status

People who own or are purchasing their own home

The data are from the 2015 Australian Survey of Social Attitudes (AuSSA), an omnibus social survey administered by the Australian Consortium for Social and Political Research Incorporated (ACSPRI). We commissioned survey questions on insurance to be included in the 2015 AuSSA. The 2015 survey has a sample size of 1211 and response rate of 26% (Blunsdon, 2016). The AuSSA data were drawn from the Australian Electoral Roll (sampling frame) using a systematic sampling strategy, and were collected in three waves in 2015 and 2016. For each survey wave, preliminary letters were sent to potential respondents prior to sending the questionnaire, with follow up letters, replacement questionnaires and reminder cards sent in order to enhance the response rate. First-wave questionnaires were administered in August 2015, second-wave in October 2015 and the final-wave in February 2016.

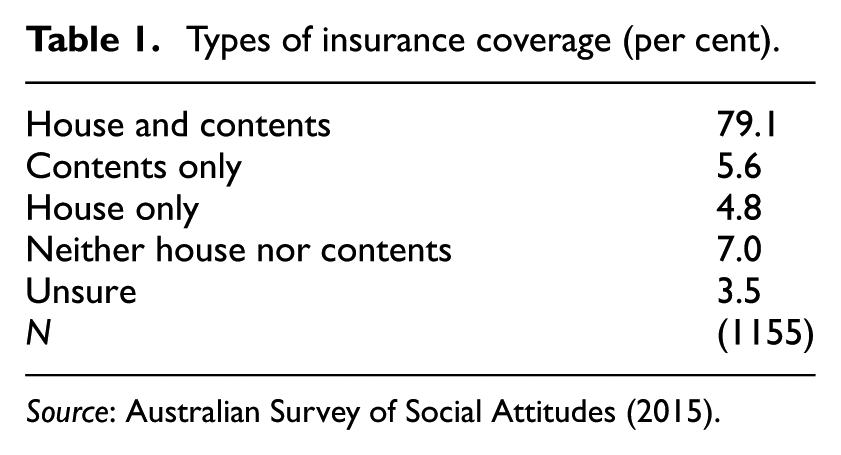

We commissioned questions relating to house and contents insurance for inclusion in the survey based upon the following question, with the results shown in Table 1:

Types of insurance coverage (per cent).

Source: Australian Survey of Social Attitudes (2015).

Thinking about your main place of residence, which of the following best describes the type of insurance cover that you or someone who lives with you has purchased? The residence is currently covered by … House and contents insurance; Contents insurance only; House insurance only; Neither house nor contents insurance.

We constructed a dichotomous (1/0) dependent variable from this question to model house and contents insurance (scored 1) contrasted with no insurance coverage (scored 0). A range of independent variables are operationalised, including dummy (1/0) variables for respondent sex (men = 0); age cohorts (aged 18–29 = 1; aged 30–49 = 1; with 50 and over the reference category), non-tertiary educational achievement = 1; household income (Aus$30,000 or less = 1); marital status (separated or widowed = 1); interpersonal trust (low trust in others = 1); location (living in a ‘big city’ = 1); living arrangements (living with a spouse = 1). 3 Housing tenure is expected to be a very important predictor here (home owners and home buyers = 1). We did not have access to class questions but use a continuous variable to measure self-assessed social status that was included in the survey by the AuSSA researchers. The status scale is derived from the following question:

In our society, there are groups which tend to be towards the top and groups which tend to be towards the bottom. Below is a scale that runs from the top to the bottom. Where would you put yourself on this scale?

The scale is scored so that 1 represents the ‘bottom’ and 10 the ‘top’ of society.

Results

As can be seen in Table 1, almost 80% of AuSSA respondents have both house and contents insurance. Approximately 5%, respectively, have contents insurance only, or house insurance only, with a slightly larger proportion (7%) claiming to have neither house nor contents insurance. Around 4% claim to be unsure about whether their place of residence is covered by house and/or contents insurance.

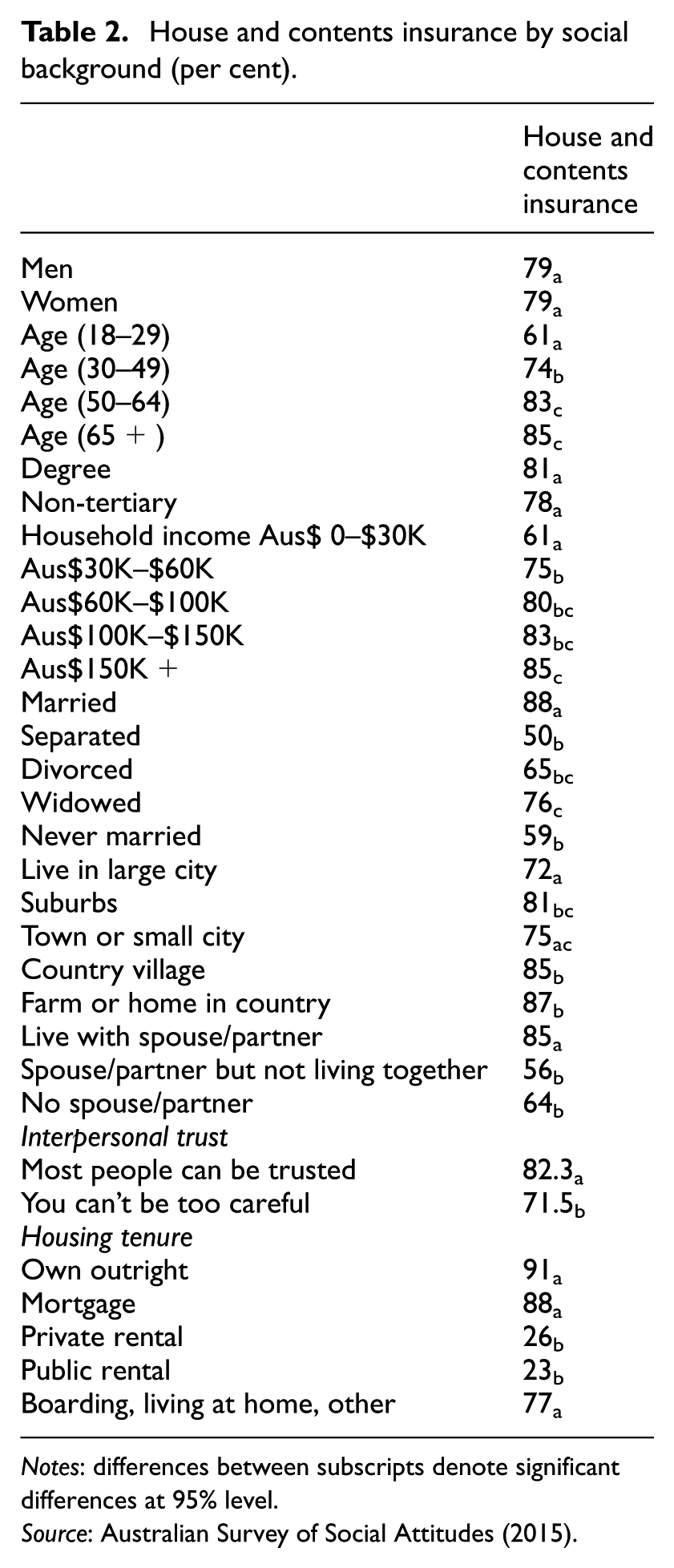

The bivariate results in Table 2 show several independent variables cross-tabulated with those who have both house and contents insurance. While no significant gender differences are apparent at the 95% level, there are statistically significant age differences. Older Australians, particularly those aged 50 or over are more likely to be insured than their younger counterparts, with the under 30s least likely to have house and contents insurance. Tertiary education does little to discriminate insurance uptake in these results, although there are some statistically significant income effects. Earning less than Aus$30,000 annually in household income tends to be associated with lower levels of house and contents insurance. Marital status also appears to be linked to insurance. Being married or widowed is associated with having house and contents insurance, while being separated appears to be associated with under-insurance. Finally, interpersonal trust is an indicator of insurance, the more trusting people are, the more likely they are to be insured, while living with a spouse or partner is also associated with having insurance.

House and contents insurance by social background (per cent).

Notes: differences between subscripts denote significant differences at 95% level.

Source: Australian Survey of Social Attitudes (2015).

Regression results

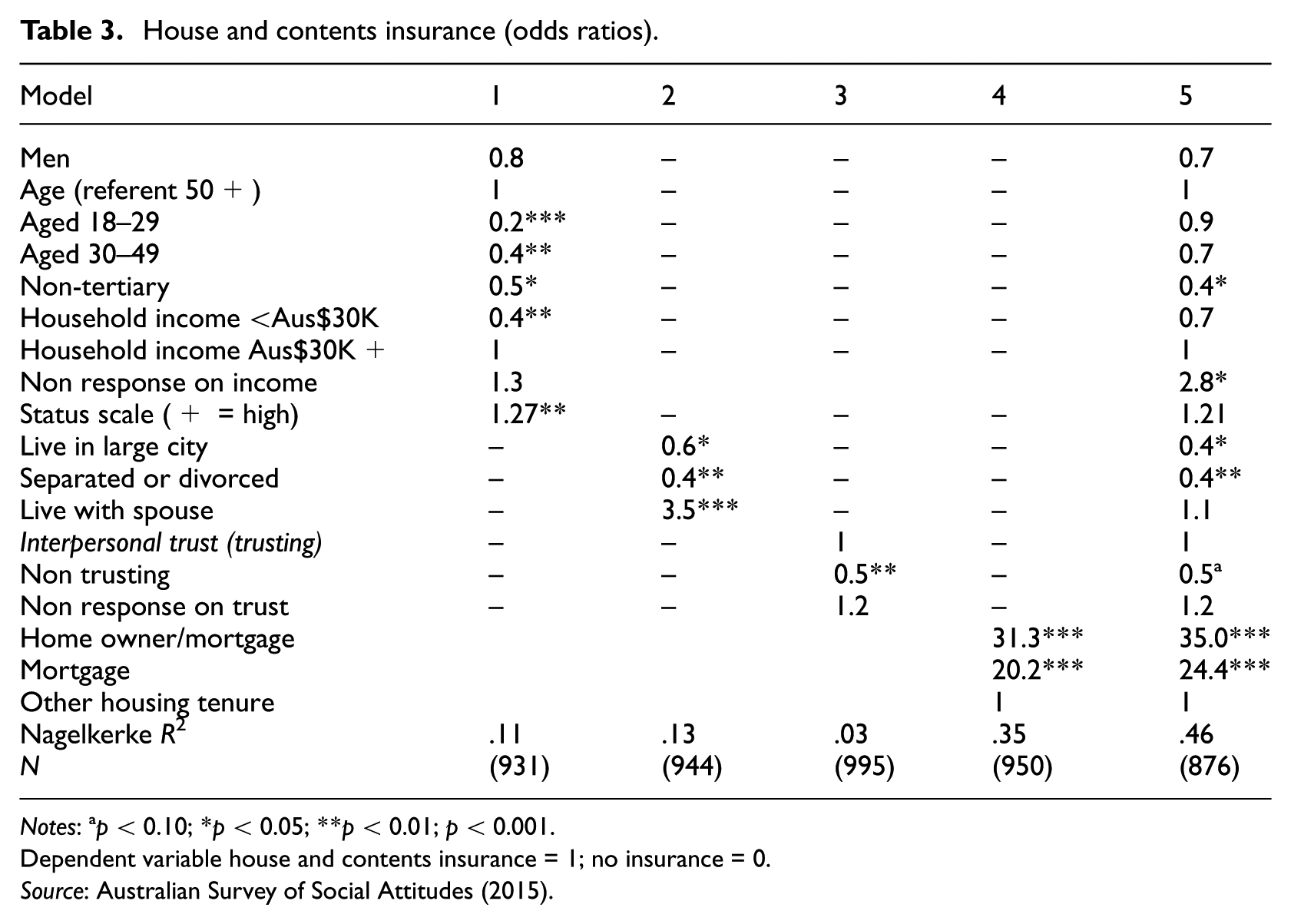

We use binary logistic regression analysis to the examine the influence of several hypothesised predictors of insurance, with the dichotomous dependent variable measuring respondents who have both house and contents insurance coded 1, and those without insurance coded 0. In this research we concentrate on analysing house and contents insurance compared to the uninsured. The structure of responses to the insurance question as show in Table 1, indicates that 79% (N =791) of respondents have both house and contents insurance. Only 5.6% (N = 65) of respondents have contents insurance only, and even fewer, 4.5% (N = 55) have house insurance only. Analysing these smaller categories as separate dependent variables is problematic for multivariate analyses, given the N for these categories is low.

Four models are presented to show the influence of social background factors: sex, age, non-tertiary education, low household income and a scale that measures one’s self-assessed status (Table 3). In Model 2, location in a large city is compared with living elsewhere, being separated or divorced is compared with other marital statuses, and living with a spouse is compared with not doing so. The third model examines respondent level of interpersonal trust, whether people generally trust each other or not. Model 4 adds housing tenure variables. Those who own their own home outright, or who have a mortgage are separately compared with people in other housing tenures, while the final model includes all independent variables.

House and contents insurance (odds ratios).

Notes: ªp < 0.10; *p < 0.05; **p < 0.01; p < 0.001.

Dependent variable house and contents insurance = 1; no insurance = 0.

Source: Australian Survey of Social Attitudes (2015).

Age plays a role in insurance cover in the multivariate case, although respondent sex does not. Younger people, particularly those aged under 30 (OR 0.2) are far less likely than people aged 50 or over to have both house and contents insurance, as opposed to no insurance cover at all. The non-tertiary educated are less likely to be insured than those with a degree (OR 0.5), while lower household income, and lower self-assessed status are also statistically significant predictors at the 95% level. Household income less than Aus$30,000 is associated with a lower likelihood of being insured. The status results indicate that those with higher self-rate status are more likely than lower status people to be insured, even after controlling for income and education level. The results odds ratios in Model 2 suggest that living in a large city or being separated or divorced are associated with lower likelihood of being insured, although living with a spouse increases the likelihood of having insurance cover.

Those who are generally less trusting of other people are less likely to be insured in the bivariate case, (Model 4), while in Model 5 when controls are included, the trust estimate is at borderline statistical significance (p = 0.059). While we do not directly measure institutional trust in this research, the interpersonal trust finding may indicate a lack of trust in insurance companies.

Not surprisingly, homeowners are much more likely than renters or people in other housing tenures to be insured, with the homeownership variable producing by far the strongest effects in these models. 4 The full model (Model 5) shows that the impact of age, household income, and social status appear to be mediated by home ownership, as is living with a spouse, with each of these estimates non-significant at the 95% level in Model 5. With the exception of the very strong effects for home ownership, only the education level (non-tertiary), living in a large city, and separated or divorced variables remain statistically significant predictors of being insured in the full model.

Discussion

In interpreting these results we focus on two dimensions. Patterns in house and contents under-insurance are located within spatially and temporally variegated processes of urbanisation. These processes are contributing to changes in the distribution and nature of natural disaster risk exposure, and in how urban areas are (re)produced through patterns in under-insurance. As we describe below, parts of Australia are experiencing rapid population growth in disaster-prone places and understanding this contributes to understanding the significance of our results. In addition to this, we interpret these results in light of research pertaining to the social, as well as economic dimensions of insurance. This literature compels us to provide more nuanced interpretations of the relationship between socio-economic status and other factors such as levels of trust, and insurance uptake.

Urbanisation is contributing to growing populations and concentrations of wealth in disaster-prone areas in Australia (Foster et al., 2013) and elsewhere (e.g. Schmidt et al., 2010). In Australia, 85% of the population of 24 million live in urban areas, and major population centres such as Melbourne and Sydney continue to experience strong growth. The population and density of inner cities is increasing, and there is significant expansion of settlements on the urban periphery, particularly growth in coastal areas along the eastern seaboard, and on the urban/bush fringe. Over 25% of Australia’s urban population – more than 3.3 million people – reside on the edge of these cities, and by 2021 this is predicted to grow to 4.5 million (McGuirk and Argent, 2011). Some of this growth is driven by amenity migration, with people drawn to less dense and more natural areas for lifestyle reasons (Booth and Harwood, 2016). Issues of housing affordability are also pushing low income earners, young families and new migrants into these peri-urban areas (Foster et al., 2013).

Close proximity to coastal processes and natural vegetation means that many of these peri-urban areas are prone to natural disaster events. For example, on the outskirts of Melbourne, populations are predicted to grow from 1.36 million to 1.76 million between 2011 and 2021 (Foster et al., 2013), which equates to approximately 250,000 new households in areas at high risk of catastrophic wildfire. As this growth is largely driven by housing affordability, these new residents tend to be young families and recent immigrants, with higher than average rates of unemployment and cultural and linguistic diversity.

As our research and previous studies suggest, factors such as age, income, and education are associated with house and contents insurance uptake. Older Australians, those on higher incomes, and tertiary graduates are more likely to be insured. Further in depth research will reveal more about these patterns, however, it appears likely that older people and those on high incomes may be more risk averse, as they tend to have a greater accumulation of assets and are better able to afford insurance coverage.

Alternatively, urban areas dominated by younger and low socio-economic households, such as those on the outskirts of Melbourne, are more likely to have significant rates of under-insurance. These populations have been identified as posing substantial challenges for disaster planning and management (e.g. Cottrell and King, 2007; Hyde, 2013), including limited household capacity to undertake risk reduction measures, and a lack of local knowledge and networks critical for effective disaster preparation (Foster et al., 2013). Under-insurance is another area of vulnerability that appears to need urgent attention, not least because large-scale disaster events have the capacity to entrench and exacerbate socio-economic disadvantage (e.g. Williams and Jacobs, 2011).

Our finding of an association between place of residence and house and contents insurance coverage is consistent with Tooth and Barker (2007). City dwellers are less likely to be insured than those living outside major metropolitan centres. While this requires further investigation, we speculate that city dwellers may feel less exposed to extreme weather events and other environmental impacts than people living in regional and rural areas. The immediacy of natural hazard impacts is higher in rural areas where livelihood and natural resources are more closely related. We suspect that this level of perceived risk exposure is likely to be an important driver for purchasing house and contents insurance.

Research conducted in the Sydney region suggests that livelihood dependency on natural resources heightens perceptions of risk and contributes to mitigation activities (Boronyak-Vasco and Jacobs, 2016). This observation is supported by Higginbotham and Connor (2014), who found statistically significant differences between rural and suburban residents regarding risk perception. Those in rural areas were more attuned to factors that may impact agricultural productivity, leading to an anticipation of future events and associated mitigating actions. As McGee and Russell (2003) note, the rural residents they interviewed acknowledged and accepted natural hazards as part of everyday life and prepared accordingly.

The lack of local knowledge identified in new communities on the outskirts of Melbourne (Foster et al., 2013) and the associations we found between key socio-economic indicators and under-insurance supports this interpretation. Not only is insurance affordability likely to be an issue for this low socio-economic cohort, under-insurance is also potentially related to peri-urban dwellers’ limited dependency upon, and lack of attunement to, local environmental factors.

Our research highlights some of the relationships that act to (re)produce house and contents insurance in disaster-prone areas, and act to complicate simplistic financial interpretations. Akin to observations made by Ewald (1991) and McFall (2011), we observe that insurance and its effectiveness are constituted through social factors, in this case socio-economic status, life stage and place of residence, as well as householder perceptions of, and actual levels of natural disaster risks.

Our finding pertaining to trust – those who generally trust others are more likely to have insurance – is also novel and important. In this operationalisation of trust we aimed to understand respondent expectations regarding the behaviour of others (Aldrich, 2012), as Lo (2013a, 2013b) has reported a significant association between flood insurance and social expectations, observing the importance of relationships with family and friends, as well as an awareness of social norms, in insurance coverage decision-making. We are concerned with how trust is (re)produced in association with other factors – such as social capital – rather than determining what factors generate or diminish trust. As Withers (2018) observes, the type of trust measure we employ here does not provide insights into cause and effect between socio-economic factors and trust.

Trust in insurers or institutions more generally was not operationalised in our study. 5 However, we did analyse what Job (2005) refers to as ‘relational’ trust. This interpersonal form of trust is understood as a ‘trusting disposition’ (Job, 2005: 4). Earlier research has found a positive association between interpersonal, generalised trust in other people and institutional trust (e.g. Tranter and Skrbis, 2009). Combined with such findings, we speculate further investigation may reveal an association between one’s level of confidence in insurance companies and insurance coverage – the less trust (or confidence) people have in insurance companies, the more likely they are to be under-insured. Trust appears likely act in concert with other ‘social realities’ in the (re)production of under-insurance in lower socio-economic and disaster-prone urban areas.

When considered in the context of urban dynamics, population distributions and the changing face of natural disasters, examining how trust is (re)produced through under-insurance can shed light on its enrolment in insurance cover as well as how insurance purchase may change the nature of trust. These temporarily shifting and heterogeneous spaces of trust appear to embody significant and differentiated power relations, especially when it comes to the relationship between households and insurance companies. Further research is required to better understand these dynamics.

Before concluding, it is important to note the lack of significant gender differences in our findings. On the surface this appears to indicate that men and women have the same patterns in house and contents insurance purchase, yet previous studies have observed that post-disaster experiences with insurance include important gender dimensions. Men and women perceive risk differently (Eriksen, 2014), while it is most often women who take responsibility for seeking and accessing post-disaster assistance (Whittaker et al., 2015), including participating in lengthy claim negotiations with insurance companies (Enarson et al., 2007). In our research, gender effects may be masked, as we asked only if the respondent’s main place of residence was covered by insurance, not who was responsible for purchasing insurance. It may be women who tend to be responsible for insurance purchase.

We did find that people who are separated or divorced have lower levels of insurance uptake than those who are married and widowed, and that those without a spouse have lower levels of insurance uptake. While the sample size prevented a more detailed exploration based on gender differences of the divorced and separated group, the possibility remains that it is separated and divorced men who are more likely to be under-insured. Further research with greater sampling power may reveal this potentially new factor.

Conclusion

In undertaking what we believe is the first national-scale study of its kind, we provide methodologically transparent, statistically robust support for several findings from previous research. We also identify new dimensions in the complex relationship between householders and insurance, including the salience of interpersonal – and likely institutional – trust. In interpreting these findings in relation to urbanisation and insurance literatures, we offer new insights into house and contents insurance and the phenomenon of under-insurance.

Our findings support the observation that insurance can contribute to increasing socio-economic urban polarisation in light of natural disasters (Johnson, 2015). Under-insurance is (re)produced along socio-economic and geographical lines, with those of lower socio-economic status or living in cities more likely to be under-insured. Should a disaster strike, such communities are likely to suffer further disadvantage, especially if governments continue to shift the responsibility for risk onto households. As Thaler and Priest (2014) observe in relation to UK disaster management, flood governance has become premised on a neoliberal manifestation of localism that effectively privileges higher socio-economic status communities and further marginalises those with less social and cultural capacity.

Yet, this may be a somewhat simplistic account of how house and contents insurance (re)produces urban form. Williams et al. (2014) argue that neoliberalism is neither universal nor inevitable, and neither is it absolutely good nor absolutely bad. As neoliberal ideology is distinct from how these ideas may be enacted on the ground (Ferguson, 2009), it produces complexities, contradictions and openings that are often overlooked in accounts of its impact and reach (Williams et al., 2014).

The prioritisation of insurance as the disaster management tool of choice that shifts responsibility (and blame) onto households and businesses may be rhetorically persuasive to some, and politically abhorrent to others. Yet such a move, Williams et al. (2014) argue, invariably manifests spaces and actors that may re-configure, counter or disrupt ethics and politics. On the ground it appears that communities and publics would not wholly support governments if they were to shirk their responsibilities should disaster strike and insurance did not cover household financial costs.

As some post-disaster accounts highlight, even those with house and contents insurance can, for a variety of reasons, discover that payouts do not cover rebuild and replacement costs. Insurance, in this regard has been described as ‘not fit for purpose’ and ‘unsafe’ (Legal Aid NSW, 2014: 21), and not the neat fix envisaged by those pursuing market-based approaches to disaster management. The socially and spatially variegated nature of under-insurance that we report here not only has the capacity to entrench urban socio-economic polarisation, these patterns also indicate the likelihood of situated ethical and political responses to this phenomenon that exceed neoliberal aspirations.

Footnotes

Funding

This research was funded by Australian Research Council, Discovery Project DP170100096, and a small grant from the Institute for the Study of Social Change, University of Tasmania.