Abstract

In light of the advent of Airbnb, rent gap theory can be helpful for understanding how tourist rentals affect residential rental housing. It is argued that on those properties currently rented to residents, rental payments are not only ‘actual ground rent’, but also ‘potential ground rent’. The shift from a residential to a touristic use of rental housing thereby creates a potential ground rent. Taking as a case study the Palma Old Quarter in Mallorca, Spain, this paper analyses the evolution of the stock, prices, and revenues of residential rentals vis-à-vis tourist rentals and finds that, because it is more profitable to rent to tourists than to residents, the number of houses listed on Airbnb has increased, housing affordability for residents has shrunk, and the threat of displacement has increased.

Introduction

The creation of touristic rental platforms such as Airbnb has led to a widespread conversion of housing units from residential to touristic use in cities all across the globe. Framed within rent gap theory, this paper analyses the reasons leading to a shift from a residential to a touristic use of housing. The article argues that Airbnb and similar platforms are creating and exploiting new rent gaps within rental housing because it is presumably more profitable to rent on a daily basis to tourists than on a monthly basis to residents.

In order to grasp this newly opening rent gap, this paper compares the evolution of residential rentals vis-à-vis tourist rentals in Palma Old Quarter between 2010 and 2015, using Airbnb as a proxy for tourist rentals. 1 Palma Old Quarter is the historical neighbourhood of Palma, the capital city of Mallorca, Spain. The article shows that, as more and more dwellings are converted from a residential to a touristic use every year, revenues made from tourist rentals have increased massively (+350% in five years) whereas revenues made from residential rentals have stagnated. By 2015, the revenues made from all of the dwellings rented to tourists were triple the revenues made from all the houses rented to residents in Palma Old Quarter. Notwithstanding this difference in the revenues made from residential rentals and tourist rentals, because the houses rented to tourists have increased in numbers and in variety (in 2010 only luxury villas were rented to tourists, whereas by 2015 all sorts of houses were rented to tourists), the average prices of touristic houses have decreased. On the contrary, because fewer houses are available to rent for residents, average residential housing prices have increased.

The aforementioned empirical findings hint at the theoretical key point of the paper. In each residential rental, the possibility of shifting to a touristic use creates a new highest and best use for the building, which in turn creates a new potential ground rent. Therefore, the paper proves that rental income not only acts as actual ground rent, as the rent gap literature suggests, but also as potential ground rent. The potential shift from a residential to a touristic use of housing opens up a rent gap between the actual ground rent coming from a residential use and a potential ground rent that could come from a touristic use. Furthermore, shifting from a residential to a touristic use implies the opening of new potential ground rents without necessarily needing ‘capital depreciation in the inner city’ (Smith, 1979: 543).

This paper is structured in the following way. The first section introduces the literature dealing with tourism’s impacts on housing, and using rent gap theory it argues that existing theoretical accounts on the role of rental income in creating rent gaps are scarce and portray rental income only as actual ground rent, not as potential ground rent. The second section discusses the research methods, and it emphasises that although some questions can be addressed, others simply cannot be because of limitations in the available data. The third section briefly introduces the Palma Old Quarter case study and explores the 2010–2016 evolution in the number, prices, and revenues of residential rentals and tourism rental properties. It makes four main claims. First, most of the houses to be rented are advertised for tourists and not for residents, especially in the tourist season. Second, the average Airbnb prices are decreasing as non-luxury dwellings are also increasingly commercialised via this platform, whereas residential rental prices are increasing as fewer dwellings are advertised for residents. Third, despite Airbnb’s average price decrease, Airbnb keeps converting houses from a residential to a touristic use because in each house rented it is more profitable to rent to tourists than to residents. Fourth, it is claimed that despite the shifting pattern in prices, revenues from tourist rentals have sharply increased whereas revenues from residential rentals in Palma have stagnated. The last section explores the potential impact of the rent gaps that are thereby opened and presents tentative conclusions as to the implications of these findings. It is concluded that the massive irruption of tourist rentals will continue as long as it is more profitable to rent to tourists than to residents, and that this conversion has deep implications for residential displacement.

Touristic use of housing and the rent gap: Missing links

Touristic uses of housing in urban environments: The footprint of Airbnb

Touristic and recreational uses of housing have been a major source of land rents for decades in Spain. Second homes and, to a certain extent, summer holiday rentals have existed in Spain and Palma since the early 20th century (Barceló, 2000; Mazón et al., 2016). These types of houses were, since the 1920s and until the irruption of Airbnb, built for a touristic purpose and were situated in coastal urbanisations developed for recreational purposes (Barceló, 2000; Cuadrado-Ciuraneta et al., 2017). For those types of dwellings, Airbnb has simply provided a new commercialising platform for existing tourist rentals (Yrigoy, 2017). Platforms such as Airbnb incorporate previously existing houses with a touristic use, thus adding an easier and far-reaching advertisement platform for those houses that already had a touristic use.

The potential of tourism for gentrification is therefore not new. More than a decade ago, Gotham (2005: 1100–1101) coined the concept ‘tourism gentrification’, highlighting how the combination of capital flowing towards real estate and a boost in urban tourism might become a major gentrification driver. Gotham positions his work within the supply-side versus demand-side gentrification debates that have long defined gentrification theory, stressing the significance of consumption-oriented activities within residential space as a means of encouraging gentrification. According to Gotham, these consumption-oriented activities are, in the case of New Orleans’ French Quarter, triggering a large-scale acquisition of properties by tourism firms, leading to a rise in property values (Gotham, 2005: 1114). But after the irruption of Airbnb, the scale of tourism-led gentrification has surely intensified. On the one hand, Airbnb tends to expand beyond the traditionally touristic core towards the rest of the neighbourhoods of a city (e.g. tourism gentrification in New Orleans is expanding, and nowadays tourist use of housing via Airbnb has expanded well beyond the limits of the French Quarter), and the numbers of houses used for Airbnb has sharply increased. Nowadays, literally tens of thousands of houses are rented to tourists in global cities such as Amsterdam, Barcelona, Berlin, Paris, London, Los Angeles, and New York. Beyond the scale issue, one important novelty of Airbnb is that it does not particularly rely on large investments, as Gotham’s conceptualisation of tourism did. Airbnb is able to open up rent gaps without necessarily having previous increases in refurbishment investments. This vital point – that Airbnb does not necessarily require a large investment in order to attract tourism demand – illustrates how Airbnb’s impact on urban milieus remains undertheorised and understudied.

In historically gentrified cities such as Palma, the irruption of Airbnb implies an acceleration of the historical residential rental market shrinkage trends in two interrelated ways. On the one hand, before Airbnb those houses that were pushed out of residential rentals were following a process of sharp depreciation that boosted the sale of depreciated rented houses (Clark, 1992). However, the current widespread implementation of touristic housing following the advent of Airbnb and similar platforms is not necessarily characterised by previous sharp processes of depreciation. On the other hand, platforms such as Airbnb have created a new tourism demand niche, taking advantage of the global reach of online platforms and the post-Fordist tourism patterns that push for new accommodation in urban environments beyond hotels (Wachswuth and Weisler, 2018). As a result of these new trends, the potential impacts of platforms such as Airbnb in terms of gentrification and displacement go well beyond the impacts that previous forms of touristic housing have had.

Although studies in this area are still scarce, some work has been done to address the impact of Airbnb in different urban contexts (Arias Sans and Quaglieri Domínguez 2016; Cócola, 2016; Mermet, 2018; Wachswuth and Weisler, 2018). There are several interesting findings in all of the above-mentioned papers that illustrate how, in Cócola’s (2016) words, tourist rentals have become ‘the new gentrification battlefront’. First, all papers illustrate how the majority of Airbnb ‘hosts’ are agents that rent one or more houses during the entire year, effectively showing that Airbnb-listed tourist rentals do not mostly correspond to second residence owners and/or hosts renting one room in their own house. Second, the papers expose how the revenues that landlords make from tourist rentals in cities with high tourist demand tend to be much higher than the revenues made from residential rentals. As Mermet (2018: 66) has explained for the case of Reykjavik, ‘the value of an entire month’s rent on the long term market could be earned in only one week on average on the short-term market’. Last but not least, this literature reflects upon how Airbnb has displaced populations from those neighbourhoods having large concentrations of tourist rentals. This paper follows the same lines of inquiry as the previous literature, particularly focusing on the issue of the impact of tourist rentals on residential rentals. Moreover, the paper aims to add two key points to the aforementioned literature: how the impact of tourist rentals on residential rentals has evolved over a relatively long time period (from 2010 to 2015) and how the tourist rental market and the residential rental market have changed in such a time span.

Gaps in rent gap theory

Possibly one of the theories most widely used to explain the production of rents in urban environments is Neil Smith’s (1979) well-known ‘rent gap theory’. Land rents are conceptualised by Smith as payments to landowners for the right to use land. In the root of the Marxian conception of land rents, there is the issue of tenure structure; land rents are based on a landlord–tenant social relation and are extracted in different ways depending on different types of tenure. Arguably the most common form of extracting land rents from housing is the sale of physical buildings, but there are other forms of creating land rents such as regular income from rental payments. Residential rentals are understood here as those land rents obtained from rental contracts paid on a monthly basis and lasting for months or years, whereas tourist rentals are understood as those rentals that are very short-term (usually less than a week) and that are usually paid on a daily basis.

Since Smith’s initial article describing rent gap theory, several scholars have engaged in theoretical debates – e.g. Bourassa (1990, 1993) and Clark’s (1992, 1995) exchange – and have performed in-depth empirical studies (for an excellent review, see Lees et al., 2008: 55–89). Two key concepts were coined by Smith to explain how rent gaps work –‘actual ground rent’ and ‘potential ground rent’. Potential ground rent refers to the income that landlords would receive ‘under the land’s highest and best use’ (Smith, 1979: 543), and actual ground rent refers to the income that landlords are currently receiving for the use of the housing unit ‘given the present land use’ (Smith, 1979: 543). There are, however, two key issues within current rent gap studies concerning the current case study that remain under-scrutinised.

First, the rental sector itself is scarcely studied within rent gap studies. Indeed, rent gap theory tends to focus mainly – if not only – on the rents coming from the sale of buildings, not taking into account how these gaps operate within the rental sector. In Clark’s words (1992: 18), ‘Rent gap theory suffers from insensitivity to other forms of tenure [beyond ownership]’. Very few studies have dealt with the role of the rental sector in creating rent gaps. There have nevertheless been two theoretical threads within rent gap theory that have partially addressed the rental issue. On the one hand, Smith (1979: 544) argued that as neighbourhoods depreciate, landowners tend to rent out houses in depreciated neighbourhoods, and thus there is a tenancy shift from ownership to rental. Rental income appears thus as another possible way of accruing actual ground rent. According to Smith (1979: 543), ‘In the case of rental housing where the landlord produces a service on land he or she owns, the production and ownership functions are combined and ground rent becomes even more of an intangible category though nevertheless a real presence; the landlord’s actual ground rent returns mainly in the form of house rent paid by the tenants]. On the other hand, Hamnett and Randolph (1984) and Clark (1992) made a step forward from Smith’s argument, and they argued that a ‘gap’ might also arise between the present rental income of a rented property and the rent that a landowner would get from selling the property (instead of renting it). Both authors argued that there is a need to integrate these rental-rooted ‘gaps’ within the broader rent gap theory. In the above-mentioned papers, it is assumed that a property sale will imply a larger rent than rental payments. But what is missing from the previous literature is that rental-based rents are not only ‘actual ground rents’, as Smith (1979) and Clark (1992) point out, but can also be signals of ‘potential ground rents’ as this paper demonstrates. Indeed, different kinds of rental rents can at the same time represent actual ground rents and potential ground rents.

Second, rent gap theory is based on the idea that the built environment needs depreciation, and eventually devaluation, in order to create rent gaps. ‘Depreciation produces the possibility of profitable reinvestment’. claims Smith (1979: 542), because it is precisely this depreciation that actually creates the gap between actual ground rent and potential ground rent. As Smith (1979: 545) puts it, ‘The rent gap is produced primarily by capital depreciation (which diminishes the proportion of the ground rent able to be capitalized)’. This idea has been echoed by Clark, who argues that ‘as the building depreciates, it will have a depressing effect on actual land rent, and the gap between potential rent and actual rent will increase’ (1987: 79). Nevertheless, what the current paper demonstrates is that in order to create potential ground rents, depreciation of the built environment is not a condition sine qua non for the creation of rent gaps. The very process of shifting to a touristic use, irrespective of depreciation dynamics, creates potential ground rents. Equally important, Airbnb is able to capitalise on potential ground rent without necessarily pursuing a physical renovation or physical upgrading of the built environment (i.e. a dwelling can be in a bad state, but there still will be a gap between the actual ground rent in the form of rental payment and the potential ground rent if this rental payment is executed via Airbnb).

Together with the fact that the touristic use of housing remains understudied, the need for further theorisation of the role of rentals within rent gap theory – regarding the lack of acknowledgement of rentals as potential ground rent and the not so central role of depreciation in creating rent gaps – demands the empirical scrutiny of Airbnb dynamics. Nevertheless, this is by no means an easy task, as the available data remain scattered and scarce.

Research methods: Challenges and limits

Because a potential shift from a residential to a touristic use of housing creates a ‘highest and better use’ for housing buildings, a new potential ground rent is created. Therefore, the key empirical task carried out in this paper is to measure the gap between residential rental prices (used as a proxy for actual ground rents) and touristic rental prices (used as a proxy for potential ground rents). How to measure such a gap? The empirical ground of this paper faces some basic, and to some extent, insurmountable limits. As Lees et al. (2008: 59) have put it, ‘Unfortunately, the rent gap involves concepts that are extremely hard to measure: nothing close to the phenomenon of actual ground rent appears in any public database or accounting ledger’. Moreover, despite the popularity of rent gap-related debates, there have been very few authors who have actually empirically addressed such issues.

Clark (1987) was the first to provide a comprehensive empirical method to measure actual ground rents and potential ground rents. Using tax assessment data, he first distinguished between land value and housing value – which he considers to be an equivalent of actual ground rent. According to Clark, the tax assessments are not updated to the real market values, and he used sale prices to calculate the real value of housing units and used tax assessments to distinguish which share of sale prices corresponded to land value and which share corresponded to actual ground rent in each housing unit analysed. He then calculated the potential ground rent from sale agreements prior to and after redevelopment. Following Clark, Badcock (1989: 129) used sale prices of undeveloped land and housing as proxies for actual ground rent and potential ground rent. Likewise, Hammel (1999) used Clark’s formula of using tax assessment data with sale prices to calculate actual ground rents and sale prices prior to and after development. To calculate potential ground rents. In Yung and King’s (1998) study of how actual ground rents change as housing units approach the city centre, they used sale prices as proxies for land rents. Following Yung and King (1998), Porter (2012) also studied the price evolution of housing units in accordance with their distance to the city centre. In a nutshell, prices have been used in the few existing empirical tests of the rent gap theory as proxies for rents. Yet, to the best of our knowledge, there have been no empirical studies addressing the rent gap issue within the sphere of rental prices. Inspired by Clark (1987), we used rental prices as proxies for rent gaps within the rented properties. Residential rental prices were used as a proxy for actual ground rent, and touristic rental prices were used as a proxy for potential ground rent.

We used a three-step process to analyse the data (see Table 1). The first step consisted of creating data showing the spatial and temporal evolution of touristic and residential rental stocks (Figures 1 and 3). The data referring to the evolution of residential rental stock between 2010 and 2016 (Figure 3) were obtained directly from the 2011 Spanish census for the years 2010 and 2011, whereas for the 2012–2016 period they were estimated based on two scenarios. One scenario assumed that the historical evolution of residential rental stock followed the same evolution as the whole Balearic region – which decreased between 2011 and 2016. The second scenario assumed that the housing stock remained constant between 2011 and 2016.

Indicators, methods, and data sources used in the article.

Source: Own elaboration.

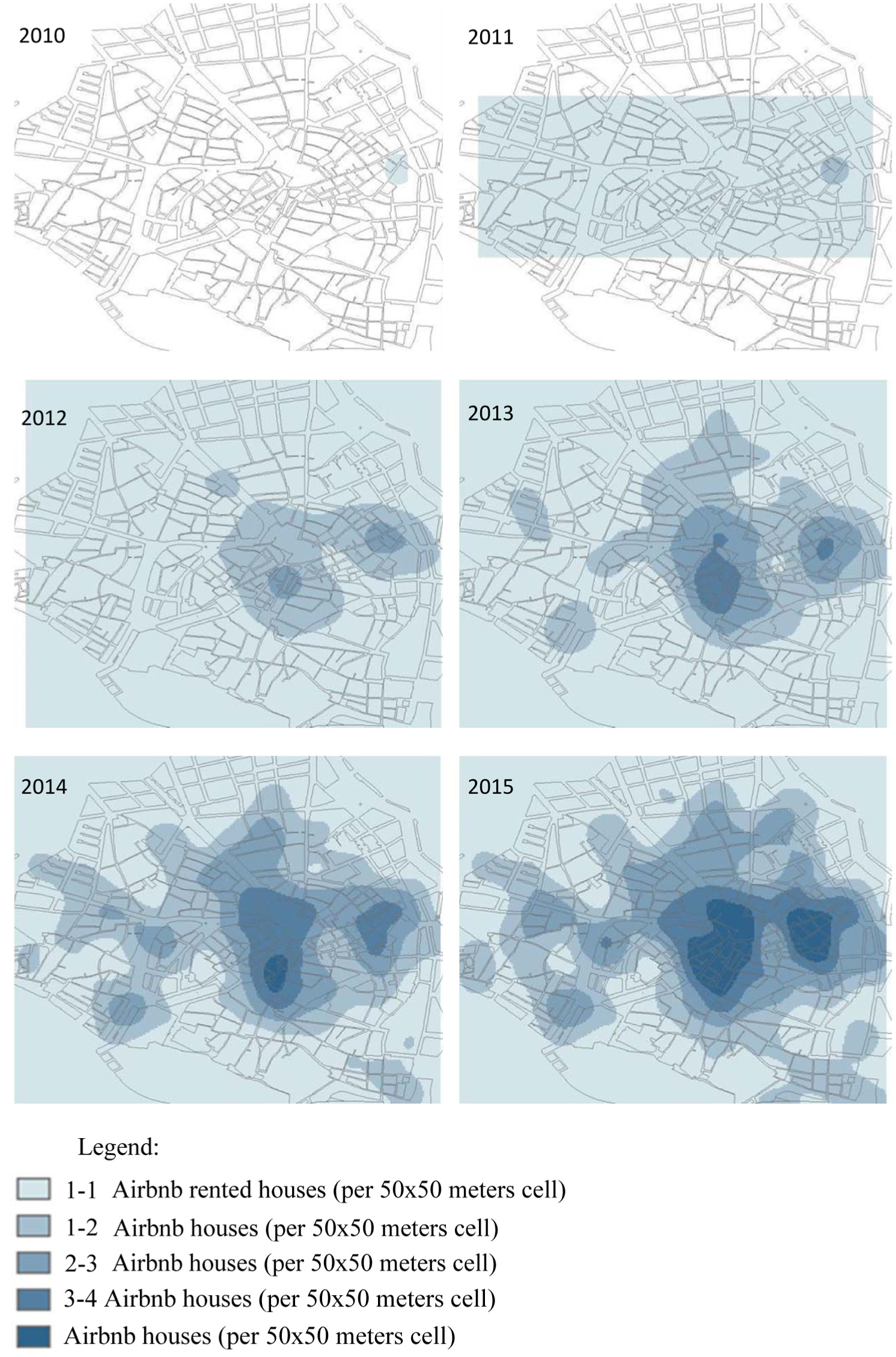

Airbnb units per 50 m × 50 m cells in Palma Old Quarter (2010–2015).

Sale and rental prices (€/m2) in Palma.

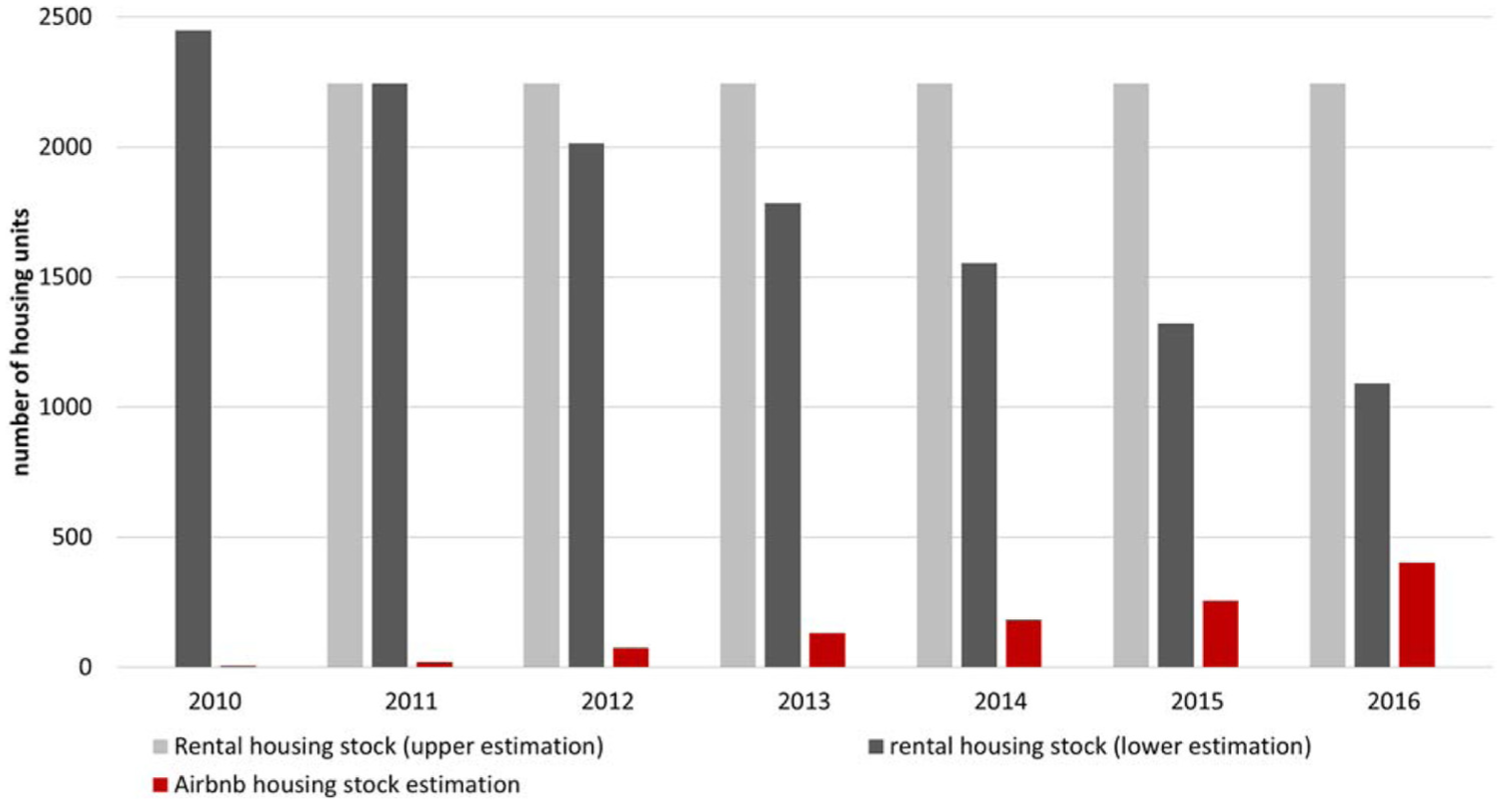

Residential rentals and Airbnb rentals estimation.

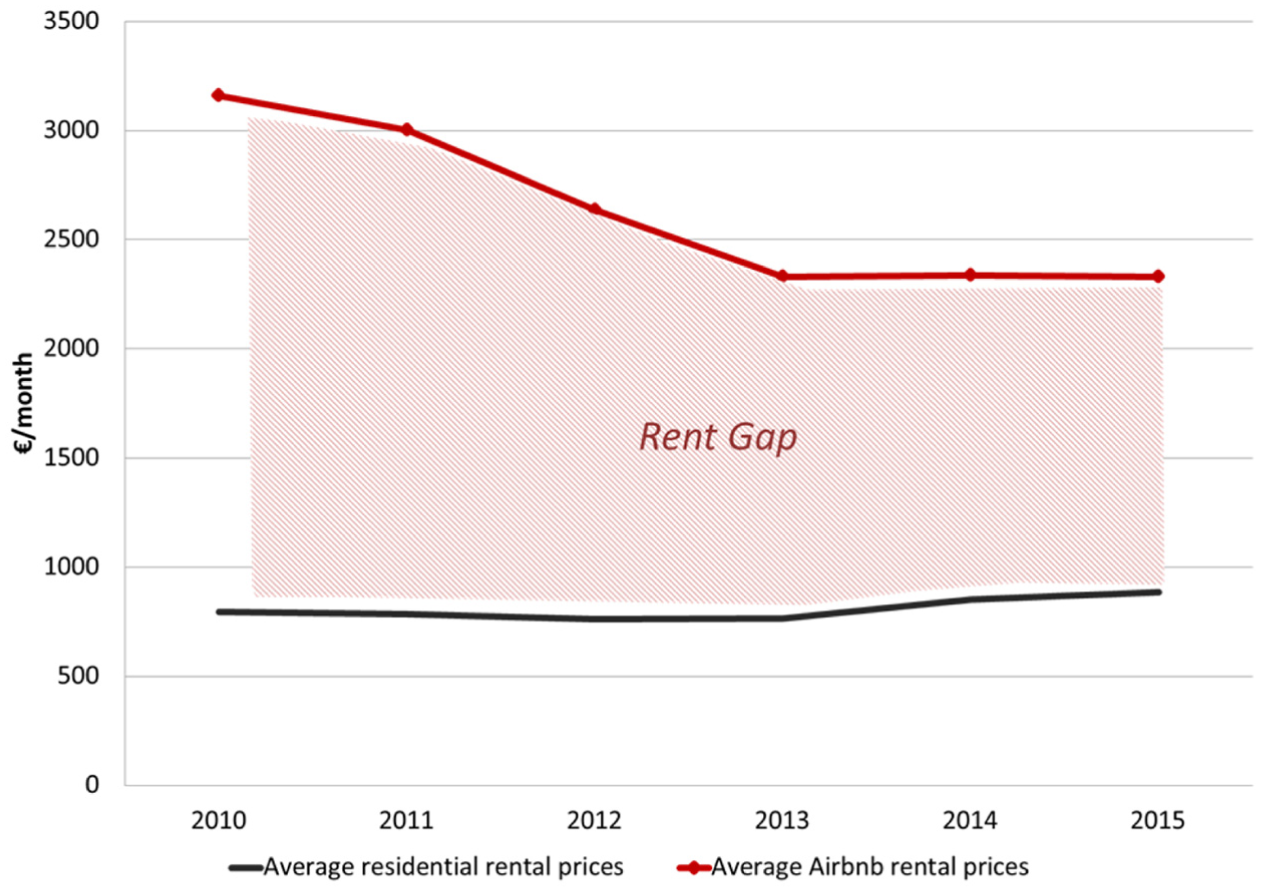

Difference in average residential rental and Airbnb rental markets.

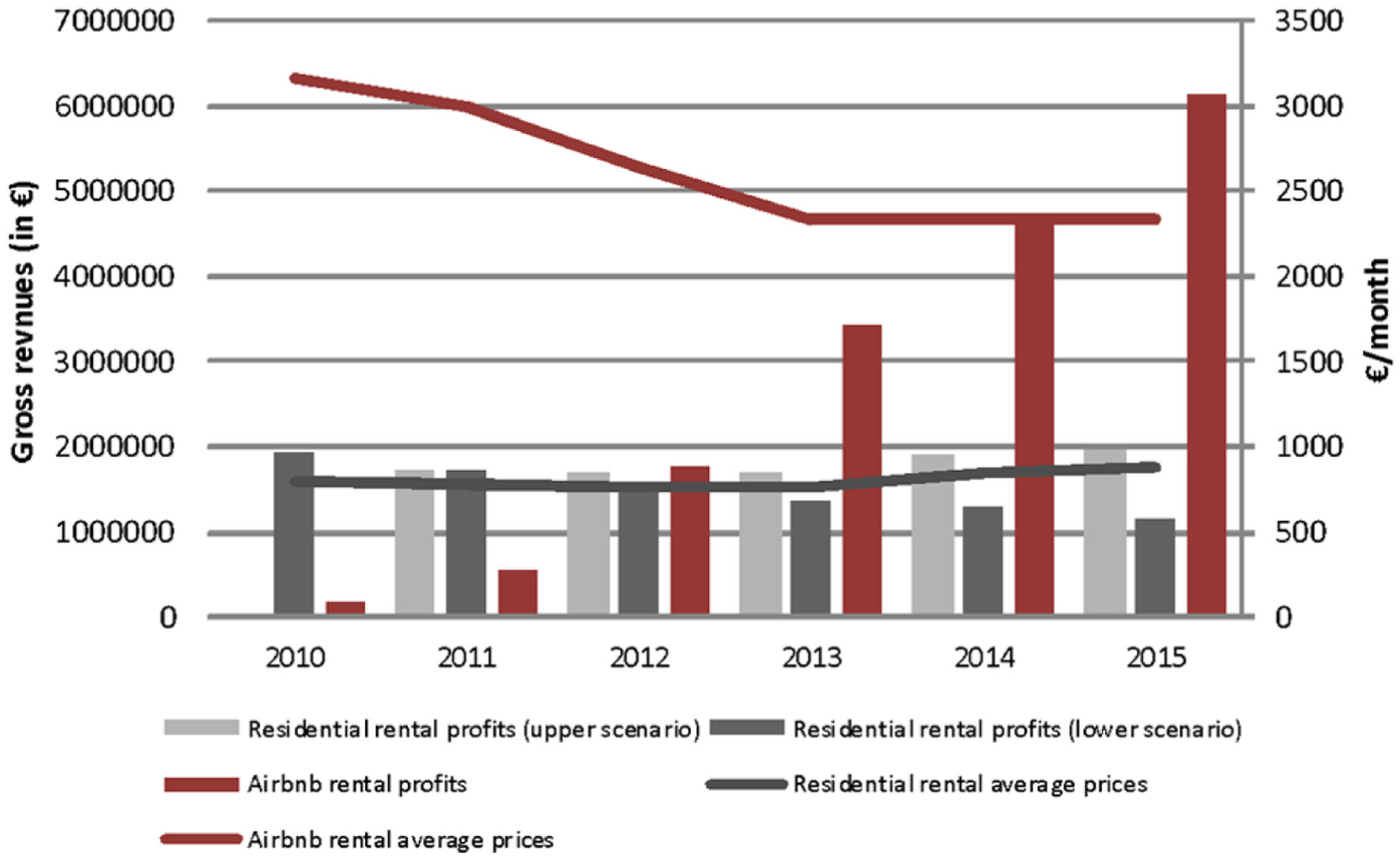

Residential rental and touristic rental revenues (2010–2015).

The second step consisted of analysing the evolution of touristic and rental prices for the period studied (Figures 2 and 4). The real estate intermediaries’ webpages Idealista (http://www.idealista.com) and Fotocasa (http://www.fotocasa.es) were used to study rental housing price evolution in Palma Old Quarter from 2010 to 2016. The data regarding Airbnb prices were obtained from Inside Airbnb (www.insideairbnb.com) and Airbnb (www.airbnb.com) for the period of 2015–2016 and extrapolated to the previous years. Airbnb prices were multiplied by the number of days each advertisement was available per year. Because the only available data regarding prices and availability were from 2015 onwards, the price evolution patterns between 2015 and 2016 were used as a proxy to estimate the price evolution of 2010–2014, assuming therefore that price patterns had remained constant in each listing. The seasonal variations in prices and the total number of houses listed were addressed through average price calculations taking into account three different data ‘cuts’ for the year 2016: one in January (obtained via Inside Airbnb), one in May (our own web scraping of the Airbnb website), and an additional one in October (our own web scraping of the Airbnb website). Additional information on average annual prices was obtained via Airdna reports for the 2015–2016 period.

In the third step, gross rental revenues were calculated (Figure 5). In the rental sector, this data set was obtained by multiplying the annual rental prices by the estimated number of residential rentals. In the case of Airbnb’s gross revenues, the monthly prices of each listing were multiplied by the number of days or months each listing was available and by the annual stock of houses listed on Airbnb each year.

Furthermore, the work faced the limitation that there is no available source detailing what the previous use was of those houses rented to tourists. Of course, a great deal of these dwellings were primary residences, but it might also be the case that some of the dwellings that now are rented to tourists were secondary residences or empty houses. Even if the exact number of houses that have been converted from a residential to a touristic use cannot be grasped quantitatively, the aforementioned use of prices as proxies for rents does grasp the potential impact of tourist rentals on the residential market as a whole.

All of the preceding information begins to explain why the empirical focus of this article is primarily on Palma Old Quarter. First, this is one of the geographical areas in Spain where tourist rentals have raised a good deal of attention, and thus more quantitative information is available to carry out such a study. Moreover, Palma is one of Spain’s foremost tourism cities, and this means on the one hand that it is one of the spots where possibly Airbnb is more clearly producing potential ground rents, and on the other, Palma has been historically one of the cities where tourism has boosted the housing sector, often leading to gentrification processes.

Palma Old Quarter: Increasing the potential ground rent by switching to tourist rents

Contextualising Airbnb in Palma Old Quarter’s housing dynamics

Since the early 1960s, Palma has been a tourist attraction complementary to the sea and sun spots across the island. The neighbourhood analysed here – Palma Old Quarter – is the historical part of the city, located at the very geographical centre of the city of Palma. This quarter has 22,847 inhabitants, out of the 400,578 total inhabitants of Palma (INE, 2016a). Within the contours of Palma, most of the tourist attractions such as historical landmarks, retail stores, and nightlife are located within Palma Old Quarter. As a result, it is a neighbourhood that has had a story of gentrification and a shrinking of the residential rental market that long precedes the irruption of Airbnb.

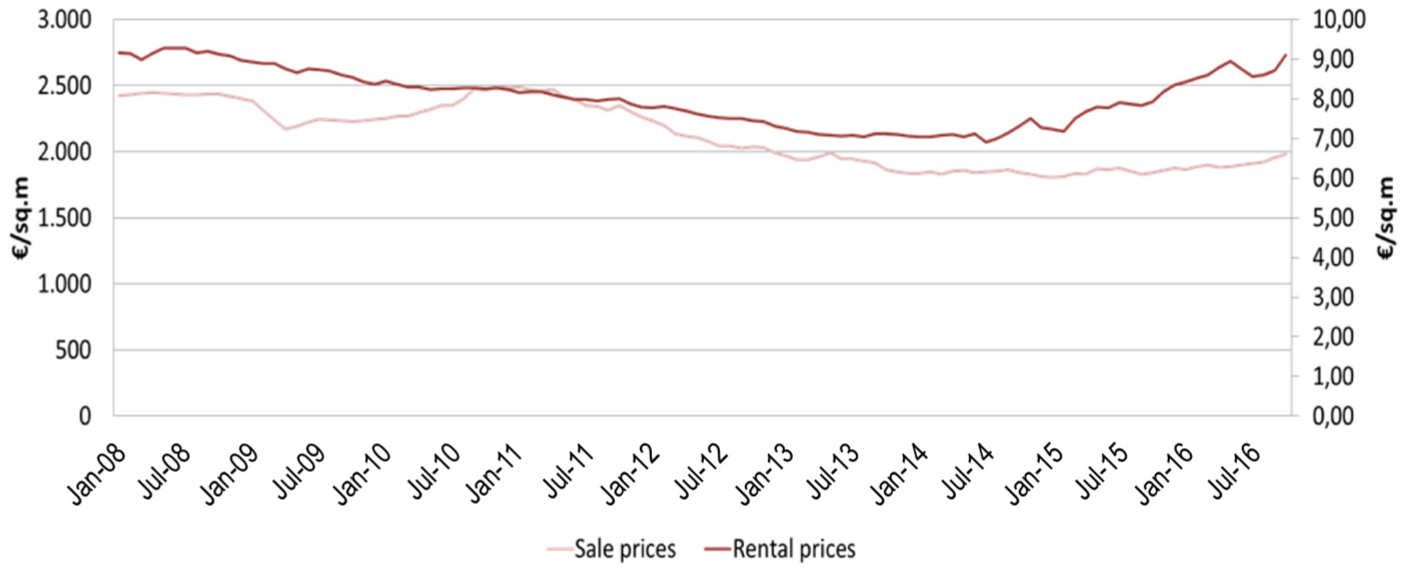

From 2001 to 2011, there was a decrease in the stock destined to residential rentals from 4651 down to 2251 houses in Palma Old Quarter (INE, 2016a, 2016b). Not only did rental housing decrease between 2001 and 2011, but the primary residence use of housing stock shrank as primary residences decreased from 12,986 houses in 2001 to 5270 houses in 2011. Several authors framed these shifts within wider gentrification processes triggered by neoliberal urban projects (Franquesa, 2007; Morell, 2009; Vives-Miró, 2011). The Sa Gerreria area within Palma Old Quarter vividly visualises such processes. In the 1970s and 1980s this area was the red-light district of Palma, widely known for being a centre for prostitution and the drug trade. According to Vives-Miró (2011), a massive urban renewal process triggered by a municipal-led internal reform plan implemented in the mid-1990s led to a substantial increase in the sale prices of the refurbished dwellings in the area. Indeed, the selling prices in Sa Gerreria were more than four times below the city average before the internal reform plan was approved, whereas in 2008 Sa Gerreria prices more than doubled Palma’s average sale prices (Vives-Miró, 2011). The increased gentrification in the early 2000s led to a massive increase in prices, which stopped because of the financial crisis of 2008. Between 2008 (the start of the economic crisis) and 2012 (the widespread popularisation of Airbnb in Palma Old Quarter) average residential sale prices remained steady at around €2500/m2, whereas rental prices slightly decreased from an average of €9/m2 down to €8/m2 (Fotocasa, 2016; Idealista, 2016). Even if the slight depreciation as a result of the crisis is considered, the Palma Old Quarter shows that residential rental prices were not particularly depressed prior to the irruption of Airbnb. That is, the potential ground rents created by Airbnb have not required a previous process of sharp depreciation – even though they can benefit from episodes of depreciation – and it is only the potential switch towards a ‘higher and better use’ that has produced such a rent gap.

Within this already heavily gentrified area, there has been a massive blossoming of dwellings listed on Airbnb (see Figure 1). The geographical and temporal spread of Airbnb in Palma Old Quarter has mainly taken place between 2012 and 2015, when most of these advertisements were created. Official estimations calculate that in 2016 up to 70% of Palma’s city tourist beds consisted of touristic housing rentals, and thus only 30% consisted of hotels, hostels, and other traditional accommodations (Govern de les Illes Balears, 2016).

In a nutshell, the pre-crisis housing market dynamism is currently being revived by the irruption of Airbnb, which in particular is shaking up residential rental properties. Former primary residences and secondary residences are now being rented to tourists via platforms such as Airbnb. As stated above, it is unclear what proportion of Airbnb listings existed before as secondary residences or residential rentals, but regardless of this the conversion of housing to tourist rentals is deeply impacting the residential rental market. First, dwellings that could be potentially rented to residents are now offered to tourists. Moreover, the impact of Airbnb on residential rental housing consists not only in a scarcity of residential rentals because of a potential shift to the touristic ‘highest and better use’, but Airbnb also increases the perception of such scarcity and contributes to the appreciation of rental prices.

This Airbnb-led housing market dynamism differs from previous housing bubbles in Palma Old Quarter in two senses. On the one hand, while in previous housing bubbles housing sales were shrinking the residential rental market, the current contraction in the residential rental market is not driven by the sales market, but by the irruption of tourist rentals. On the other hand, the current revitalisation of the housing market has impacted mainly rental prices, but not so much sale prices, and while rental prices increased from 2014, and by 2016 had reached pre-2008 levels, housing sale prices have continuously decreased since the crisis erupted (see Figure 2). Significantly, this recent increase in residential rental prices is correlated with the expansion of tourist rentals, and following the massive boost of Airbnb rentals in Palma – which was particularly intense between 2012 and 2013 – residential rental prices first stabilised and then increased from the middle of 2013 onwards.

As the following section will show, these two new major impacts of Airbnb on the residential sector – a shrinking of available residential rental dwellings and an increase in residential rental prices – is due to the fact that tourist rentals have emerged as a new ‘highest and best use’ for residential rentals. The particular technological ease of reaching a global market, and the conception of Airbnb and similar platforms as large-scale providers of a ‘new’ type of accommodation in urban environments, have smoothly created the demand conditions that allow residential rentals to find a ‘higher and better use’ if converted into a touristic use.

Residential rentals vis-à-vis tourist rentals

In order to unravel how potential ground rents are created in the rental market, a comparison between residential rentals and tourist rentals was carried out. The main spheres of comparison were housing stock, advertisements, prices, and revenues.

Stock and advertisements

As previously stated, from 2001 to 2011 the number of houses rented in Palma Old Quarter decreased from 4651 to 2245 (INE, 2016a, 2016b). It is unlikely that the residential rental stock has increased in these years because there was a stagnation of the rental tenancy in the Balearic archipelago (from 26.41% of the housing stock in 2013 to 26.28% of the housing stock in 2015, INE, 2016c), and in the Old Quarter itself there was a decrease in population from 24,220 inhabitants in 2010 to 22,487 inhabitants in 2015 (INE, 2016d). Nonetheless, two feasible scenarios have been considered regarding the evolution of the residential rental stock in the case study: (1) the 2001–2011 decrease kept going at the same pace in the 2012–2016 period; or (2) the number of houses rented in Palma Old Quarter has not changed significantly since 2011.

No matter which of the two scenarios is taken into consideration, the total number of Airbnb rentals in the Old Quarter is still smaller than the total number of houses rented for residents (see Figure 3). In 2011, there were 2245 houses rented in the Old Quarter, but only 20 were rented in the Airbnb market (Inside Airbnb, 2016). Even in 2015, the number of houses rented on Airbnb was 256, less than 20% of the residential housing stock (if the lower estimation in Figure 3 is considered). The emergence of Airbnb has not meant a significant shift in the shrinking tendency of the residential rental stock because its decline started long before Airbnb existed. Nevertheless, it is significant that residential rentals are not increasing or are decreasing while at the same time tourist rentals are massively increasing.

Beyond the stock issue, the blossoming of Airbnb is having important effects on the new rental offers available for residents. There are important differences between the quantity of long-term residential rents and the short-term tourist rentals offered on websites between peak touristic season and low season. On 5 May 2016, at the beginning of the tourist season, 65 advertisements were available for residential rentals in Palma Old Quarter on the two leading web pages advertising residential rentals, Fotocasa (2016) and Idealista (2106). This is in sharp contrast with the Airbnb website, which on that very day had 405 advertisements available. On 31 October 2016, after the tourist season was finished, there were 94 advertisements for residential rentals and 146 on the Airbnb market. Obviously, the residential rentals availability is highly affected by the tourist season – when the tourist season starts, the residential rental market shrinks. But even once the tourist season has ended, there are still many more rentals available from Airbnb than in the residential market.

Moreover, and contrary to other cities, most of the Airbnb advertisements in Palma Old Quarter do not combine a residential and touristic use and have an exclusively touristic use. Palma has the highest rate of both availability and share of entire homes rented of all European cities analysed by Insideairbnb (Haar, 2018: 6). Indeed, 85% of Airbnb beds correspond to houses that are rented entirely, and 15% correspond to rooms that are rented to tourists in houses with residential purposes. Of houses posted on Airbnb, 70% are rented the whole year, and the average number of days available to rent is 309 days/year, that is, these are available for rent at least ten entire months per year.

To summarise, residential rentals seem to be in a steadily decreasing situation, whereas Airbnb rentals are clearly increasing. Rental houses that are to be placed on the market are increasingly commercialised via Airbnb and not on other residential-oriented web pages; therefore, the decrease in newly available residential rental offers is directly related to the rise of Airbnb. Significantly, and as it is argued below, the irruption of Airbnb is not only a matter of switching towards an online platform, but it is mainly a matter of shifting from residential rentals towards more profitable tourist rentals.

Prices and revenues

The above-mentioned shifts in the available stock of residential and tourist rentals has greatly impacted the price patterns of both residential and tourist rentals. Following the economic crisis, residential rental prices decreased slightly from 2010 to 2012, but as Airbnb appeared on the scene and residential rentals became more and more scarce, residential rental prices first stabilised and then increased from mid-2013 onwards. From 2010 to 2015, average residential rental prices increased from €794/month in 2010 to €885/month in 2015 (Fotocasa, 2016). On the contrary, average touristic rental prices decreased from €3160/month in 2010 to €2333/month in 2015 (Airbnb, 2016) (see Figure 4). This immediately poses important questions. How can it be that Airbnb prices, which supposedly represent the potential rent for residential rentals, are decreasing? And to what extent does this mean that the rent gap is being closed?

The increase in the number of houses rented to tourists and the diversification of the type of houses rented via Airbnb is what ultimately explains the constant decrease of Airbnb average prices. Indeed, from five highly luxurious houses rented on Airbnb in 2010, the number of houses rented via this app increased to 256 by 2015. As the tourism rental market expanded, the typology of houses rented via Airbnb became more diverse. If in 2010 only large, very luxurious, and renovated houses were rented via Airbnb, by 2015 all imaginable sorts of dwellings were rented. From brand new luxury villas to non-renovated one-room houses or shared rooms, every kind of dwelling is to be found on Airbnb. Of course, because not only luxury houses have been rented, but also more standard units, average rental prices have tended to decrease. Owing to the high tourism demand of the Old Quarter, it seems that every type of house, no matter how well located, or how heavily renovated it has been, is potentially leasable for tourists. But the massive enlargement of the touristic rental market has also meant changes in the occupancy ratios of Airbnb dwellings, and thus in the prices and revenues of the sector.

At the same time as the number of the houses rented via Airbnb has increased and its average price has decreased, the opposite trend has taken place with residential rentals. While tourist rental advertisements have increased in both number and variety, residential rental advertisements have evolved in the opposite direction. In 2010 there were all imaginable types (and prices) of residential-oriented houses for rent in the Old Quarter, but by 2016 these types of advertisements were not only very few, but also for very specific types of dwellings. Indeed, the very few houses rented for residential use by 2016 were mostly large and luxury flats in the surroundings of Jaume III and Passeig de Mallorca streets. These are streets that were built between the 1950s and 1970s by tearing up the ancient urban morphology, and thus they do not fit into the touristic cliché of the ‘renewed old house within a historical quarter’ that attracts most Airbnb users in Palma Old Quarter. To sum up, the type and location of residential rentals correspond to those housing units that are not attractive to Airbnb users.

As Airbnb covers a greater variety of housing typologies and Airbnb prices decrease, still more and more advertisements appear on the Airbnb webpage and the price differences between touristic and residential use remain. In this regard, Airbnb is opening up new possibilities to economically exploit properties. Airbnb listings keep increasing even as average prices decrease because in each housing unit the rents extracted from tourist rentals are greater than rents extracted from residential rentals. Even in a deteriorated small house, tourist rentals are superior to residential rentals. This explains why the number of houses listed on Airbnb keeps increasing, and also why revenues coming from Airbnb are increasing even if the average prices are decreasing.

Indeed, gross revenues in Palma Old Quarter’s residential rentals have ranged between a 40% decrease and a 12.6% increase over the last five years – depending on two different estimations (see Figure 5). At the same time, gross revenues from tourist rentals in Palma Old Quarter have increased by +350% as more and more houses are listed on Airbnb. By 2012, the revenues coming from tourist rentals had surpassed the revenues coming from residential rentals. By 2015, revenues coming from the tourist rentals in Palma Old Quarter were triple the revenues coming from residential rentals, even though the number of houses rented as residential rentals was four times larger than the number of houses rented to tourists. At the same time as revenues from Old Quarter tourist rentals increased, the revenues coming from residential rentals only slightly increased or decreased. That is, for most of residential rentals in Palma Old Quarter, a new potential ground rent can be extracted if residential rentals are converted into tourist rentals.

To sum up, the role of tourist rentals as potential ground rents for those dwellings currently being rented to residents implies less residential rental stock available and an increase in average rental prices for residents. This has relevant implications for displacement in two interrelated ways. On the one hand, individuals living in Palma Old Quarter are increasingly pushed towards other areas of the city and/or the sales market because residential rentals are increasingly less and less affordable for the average resident in Palma Old Quarter. The 2011 census data showed that roughly 90% of the population living in Palma Old Quarter (part-time employed, low-skilled wage earners, students, and pensioners) would have difficulties paying rental contracts if they had to enter into Palma Old Quarters’ residential rental market today (INE, 2016a). By the same token, those of this 90% cohort living nowadays in residential rentals in the Old Quarter (and having the same economic status as in 2011) are facing an increased risk of being expelled from their rented houses once their contracts are revised and updated to the new standard rental prices or when their homes are converted into tourist rentals. On the other hand, those who are not living in Palma Old Quarter but willing to live there via the rental sector have fewer chances to get a house in the Old Quarter than in other areas. Considering official data regarding average salaries, the share of one’s gross salary that one individual might need to pay for residential rent in Palma Old Quarter would account for 40–45% of the salary without taking into consideration costs such as water, electricity, car parking or heat, which are in most cases excluded from rental prices (INE, 2016e). Airbnb-led rent gaps are thus creating the economic conditions for a significant population displacement, which is starting to take place and will probably soar in the years to come.

Concluding remarks

This paper has introduced new theoretical insights into rent gap research. First, the paper has demonstrated that rental income acts as potential ground rent. In previous rent gap studies, it has often been argued that there is a gap between actual ground rents from rental income and potential ground rents coming from sale and purchase that eventually lead to a conversion from rental towards ownership tenancy. Nevertheless, this paper has shown not only that actual ground rents are extracted from rental housing, but also that rental income can act as potential ground rents for housing as well. In those cities such as Palma where there is enough tourism demand to have high occupancy ratios in tourist rentals, a touristic use represents a ‘highest and better use’ for residential rental housing because payments on a daily basis are more lucrative for homeowners than payments on a monthly basis. The opening of new potential ground rents through a touristic use not only leads to a conversion from a residential to a touristic use, but it also leads to an increase in the residential rental prices. Moreover, the high potential rental returns from touristic rental options are increasingly luring investors to Palma Old Quarter, who try to build up entire buildings in order to convert them to touristic use. This increased interest by investors in Palma Old Quarter housing for its potential touristic use is leading to an increase in the housing transactions in the area, and also of their sale prices. The impact of tourist rentals on the dynamics of housing sale markets is an issue that needs to be scrutinised in future research.

Second, Airbnb is expanding the rent potential of housing without necessarily needing a depreciation of the built environment or a renovation of the existing housing stock. Indeed, Palma Old Quarter underwent a process of gentrification and physical renewal in the years prior to the emergence of Airbnb that greatly revalued real estate. Regardless of this, Airbnb opened up the possibility for new ground rents, as the +350% increase in the revenues made by the touristic rental sector in Palma Old Quarter between 2010 and 2015 clearly illustrates. In the rent gap literature, the increase in the value of housing is ultimately explained by the labour-intensive process of investment and refurbishment, which leads to appreciation and eventually to revaluation (Smith, 1979). But in the case of Palma, the appreciation taking place in tourist rentals does not seem to be particularly rooted in a labour-intensive wave of structural refurbishment. Does this mean that there is no labour involved in tourism-rooted housing appreciation? Not at all, but it probably means that labour is embodied in the touristic housing appreciation in different ways than those envisaged by rent gap theorists. This is yet another point that needs to be further explored in future research.

Most likely, the rent gap that Airbnb has opened in touristic cities such as Palma will only be closed when the occupancy ratios of Airbnb decrease. This will eventually happen because the number of houses offered to tourists keeps increasing and at some point, the tourism demand will not be able to increase at the same pace as the tourism housing supply. Furthermore, if the residential rental prices keep increasing and tourist rentals occupancy ratios decrease, Palma Old Quarter will reach a point at which it is actually less profitable to rent to tourists than to a resident. It will be then when the rent gap opened by Airbnb will be closed. Notwithstanding how fast this gap is closed, the widespread use of housing for tourist rentals is being realised at a social cost because access to housing for residents is increasingly difficult, leading to displacement of the local population. Indeed, because the residential use of rental housing represents a barrier to Airbnb rents creation (some houses cannot be reconverted into tourist rentals as long as residential tenants have a contract in force), this barrier is erased via different strategies of displacement. The fact that rental payments are paid on a daily basis, the presumably different costs for the homeowner between daily and monthly rentals, and the effects of seasonality on tourist rentals, are additional key aspects that are shaping tourist rentals, and this will need to be explored in future research on the topic.

Footnotes

Acknowledgements

Many thanks to Brett Christophers, Don Mitchell and three anonymous reviewers for the helpful comments on earlier drafts of the article. The usual disclaimers apply.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This article was funded by the ‘Crisis and Restructuring of the Spanish Tourist Coast’ (CSO2015-64468-P) research project funded by the Spanish Ministry of Economy and Competitiveness and the European Regional Development Fund (ERDF).