Abstract

The literature on urban financialisation has prioritised the analysis of what finance does in the context of industrialised countries. This paper contributes to an understanding of what it is, and specifically how it emerges from the entanglements between the accumulation of intergovernmental debt, pricing and valuation practices – involving state and municipal utilities, regulatory agencies and consultancies – in the gradual transformation of shared into shareholder water governance in Brazilian metropolitan areas. Moreover, we provide a first illustration of how a more articulate approach between political economics and social studies of finance might contribute to an understanding of the making of urban financialisation, with a particular relevance for a context of less developed capital markets.

We don’t receive money from government. Everything that has been built to provide services to the population has been financed through the water bills paid by consumers. When comparing with most states in the country, which is the winning model? It is SABESP’s approach.

1

Introduction

The literature on financialisation, a concept defined by Aalbers (2015: 214) as ‘the increasing dominance of financial actors, markets, practices, measurements and narratives, at various scales, resulting in a structural transformation of economies, firms (including financial institutions), states and households’, has proliferated rapidly.

In a stocktaking exercise, Christophers (2015) elaborated two lines of critique to this growing research programme. First, it has prioritised the analysis of the consequences of finance on others, that is, what it does, while failing to investigate its essence and internal workings, in other words, what it is. Making research on financialisation politically more relevant would require investigating the black box of finance itself, and tracing its linkages with money, credit, pricing, valuation and the creation of markets. After all, before finance can extend its tentacles into the daily life of others, it has to be socially constituted.

Second, with some exceptions related to mid-income countries in Latin America, Asia and Eastern Europe, the bulk of the research has focused on industrialised countries. In institutional settings marked by less consolidated capital markets, it is unlikely that financial intermediaries alone perform the relational role of transforming ‘almost everything’ (Leyshon and Thrift, 2007) into ‘contracted income streams’ (Hildyard, 2016: 24). Therefore, it becomes important to analyse the organisational and regulatory structures and scales through which the state is mobilised in the making of urban financialisation, that is, in the transformation of imperfect public goods such as land and infrastructure, as well as municipal finance itself, into predictable flows of income. Aalbers (2017: 550) claims that financialisation ‘of and through the state’, and its relations with the restructuring of governance, ‘is a key research frontier to be explored in the coming years’.

We provide an initial contribution to filling in some gaps in the literature along these lines through a case study on the gradual transformation of a shared state–municipal arrangement for metropolitan water governance into a shareholder-driven system in São Paulo, Brazil. More specifically, we analyse how, since the early 2000s, the mixed-capital, majority state-owned water and sewage company SABESP (São Paulo Company for Basic Sanitation, listed on the São Paulo and New York stock exchanges), has been able to provide ‘value for money’ to its shareholders through a consistent increase in profitability and share prices. We argue that its aggressive calculative practices used in the pricing of wholesale water delivered to municipal retail companies, which were homologated by regulatory agencies, legal courts and the federal antitrust body, were key in the accumulation of municipal debts with SABESP. Considering the gradual consolidation of legal impasses, whereby debts should be paid one way or another, this created an ‘enabling’ environment for the negotiation of municipal debt relief in exchange for awarding SABESP the concession to build, operate and maintain municipal networks as well as to design and implement pricing and revenues strategies. On the basis of a detailed analysis of the disputes between municipal utility SEMASA (Environmental Sanitation Services of Santo André), owned by the city of Santo André (approximately 720,000 inhabitants, located in metropolitan São Paulo) and SABESP since the mid-1990s, we show the role of financial-legal devices and specific forward- and backward-looking calculative practices in the pricing of water and valuation of assets, and the subsequent penetration of shareholder value premises into a shared state–municipal arrangement for metropolitan water governance.

Beyond the insights from the case, indicating that financialisation of water in metropolitan São Paulo is still open-ended, the paper provides two contributions to debates on urban financialisation, with relevance for the Global South.

First, different from the US-based work on austerity that has led cities to adopt increasingly risky strategies in capital markets (Kirkpatrick, 2016; Peck and Whiteside, 2016), as well the literature on the entanglements between finance, real estate, large urban development projects and governance in the European context (Van Loon et al., 2018), our analysis provides insights regarding how, in a context of relatively thin capital markets, intergovernmental conflicts between state and municipalities regarding the regulation, valuation and pricing of water are instrumental in understanding the making of urban financialisation. We show how the circulation of particular calculative practices that involve legal courts, regulatory agencies, consultancies and public utilities enables the accumulation of intergovernmental debt, which contributes to the gradual hollowing out of shared governance, and its filling in with shareholder water governance.

Second, while the study of political economy has provided an understanding of the broader contradictions associated with urban neoliberalisation, entrepreneurialism and the penetration of finance capital into cities by transforming them into ‘tradable income yielding assets’ (Guironnet and Halbert, 2015), it remains unclear how this has occurred (Hall, 2010). More specifically, the study of urban political economy has prioritised the analysis of cities as privileged arenas for the generation and extraction of financial profit, while taking markets relatively for granted. As such, it has traditionally spent less effort in understanding the constitution of markets as key arenas for the circulation and consumption of value, prioritised by social studies of finance (Christophers, 2014). Considering the technological indivisibilities, significant state presence in the planning of housing, land and infrastructure networks, long payback periods and political contestations that surround this process, there is nothing inherent in the transformation of cities into financial assets. Thus, following Christophers’ (2014) general argument, we provide a first illustration of how a more articulate approach between the study of political economy and social studies of finance might contribute to understanding the making of financialisation in cities and infrastructure networks.

The research for this paper was based on a review of the literature on urban financialisation. The case study in metropolitan São Paulo was developed through documentary research on SABESP and SEMASA, a detailed analysis of the files of SEMASA’s request to investigate SABESP, which were obtained from the national anti-trust agency CADE, and complementary secondary data collected for metropolitan São Paulo.

Four sections follow this introduction. The first contains an overview of the literature on urban financialisation and discusses its relevance for countries such as Brazil. The second summarises the institutional trajectory of sanitation in Brazilian metropolitan regions, while the third fleshes out the financial–institutional battlefield between SABESP and SEMASA. We conclude with suggestions for research on urban financialisation.

Cities in times of financialisation

It is not our purpose to provide a detailed overview of the literature on financialisation (van der Zwan, 2014), such as Marxian, regulationist or post-Keynesian political economics (e.g., see Hilferding, 1981; Chesnais, 1997; and Minsky, 1996, respectively), critical accountancy and shareholder governance (Froud et al., 2006) and social studies of finance, including the performativity of financial markets (MacKenzie, 2006). Political economics has emphasised structural transformations in the generation of a finance-driven mode of accumulation and regulation that ‘exploits all of us without producing’ (Lapavitsas, 2013). Critical accountancy has used corporate finance and principal-agent theory in fleshing out the contradictory reshaping of organisations under the influence of shareholder value (maximising capital gains and dividends). Social studies of finance have prioritised the investigation of the mechanisms through which finance has penetrated the reproduction of daily life, while related work on performativity stressed that economic models not only describe the reality of the stock exchange, but also potentially contribute to constituting and shaping these markets (Callon, 1998; MacKenzie, 2006). Finally, financial geography has stressed the variegated and intrinsically uneven spatial character of financialisation, whereby ‘money flows like mercury’, ‘pooling’ in particular places and spaces (Hall, 2010: 240).

Financialisation has also affected and is influenced by cities (Theurillat and Vera-Büchel, 2016; O’Neill, 2019), particularly considering these are privileged spaces of generation and circulation of value and (collective) consumption (Clarke and Bradford, 1998). The literature has engaged with four interconnected themes, that is, financialisation of urban land; entrepreneurialism, urban governance and large urban development projects; infrastructure financialisation; and the city–capital market nexus.

Although Harvey (1982), based on Marx, already in the 1980s analysed the tendency of land to be transformed into a financial asset, authors such as Haila (1988) investigate the specific geographic and historical circumstances under which this would occur. Christophers (2017) examines the state’s role in the financialisation of public land in the UK. In Brazil, Sanfelici (2013) analyses how São Paulo-based developers, in a macroeconomic context of growth and abundant liquidity, used initial public offerings to build up speculative land banks in the cheaper states in order to profit from the post-2007 real estate boom, and why this eventually led to excess supply and bursting bubbles.

Urban neoliberalisation through large urban development projects is no new theme (Swyngedouw et al., 2002). Nevertheless, authors such as Guironnet and Halbert (2015) update this literature by investigating the circulation of norms and conventions within professional communities, which have actors in and outside finance, regarding the pricing and valuation aimed at transforming city-space into ‘a portfolio of tradable income yielding assets’. A growing empirical literature has focused on the role of finance in the design and implementation of projects (Charnock et al., 2014; Kaika and Rugierro, 2016), and the financialisation of entrepreneurialism itself through the involvement of the (local) state in mobilising finance capital for the delivery of land, infrastructure and real estate (Charnock et al., 2014; Savini and Aalbers, 2016). Klink and Stroher (2017) show how financialisation in Brazilian large urban development projects, through the creation and commercialisation of building rights certificates in financial markets, is still limited considering the lack of secondary markets for these products.

Graham and Marvin’s (2001) work on state rescaling, neoliberal infrastructure transitions and splintering urbanism provided an entrance point for research on the re-emergence of finance in infrastructure. A common theme is that investment bankers and intermediaries perform a ‘relational role’ in generating innovative financial engineering, securitisation and indexed investment funds, which enable the creation of diversified portfolios and, theoretically, a less direct exposure for investors by transforming illiquid, high risk and lumpy infrastructure networks into desirable investment assets, and receiving a premium for doing exactly that (Pryke and Allen, 2019; Torrance, 2008). Nevertheless, the unbundling, repackaging, or disassembling and re-assembling of ‘un-cooperative’ urban commons (Bakker, 2007: 447), marked by high initial investment costs, significant state involvement, long pay-back periods and risks, have resulted in disappointing results in terms of additional investments (Bayliss, 2014). Critical to political economics as an entrance point, O’Neill (2019: 1304) develops a framework on the ‘relationships between infrastructure investing and the infrastructure enabled flows of a city through the lens of three “mezzanine-level conceptualizations” of “capital structure, organizational structure and regulatory structure”, so that the ‘particularities of political economics that pervade the city and its economy become prominent as a consequence’ (O’Neill, 2019: 1306). Although there is not much work on infrastructure financialisation in the Global South, Hildyard (2016: 23) reviews the interfaces between the state and finance in the extraction of value from infrastructure networks through the design of guaranteed and contracted income streams, with examples from Asia, Latin America and Africa. Likewise, Bakker (2007) and Britto and Rezende (2017) analyse the socio-spatially selective entrance of finance and the private sector in sanitation, globally and in Brazil, respectively.

A final theme is structured around the analysis of how neoliberalisation and austerity have both renewed and made the entanglements between cities and capital markets increasingly complex, generating work on tax increment finance districts (Weber, 2010); the operational management of risks in concessions and private–public partnerships (Ashton et al., 2016); and the disciplinary effects of capital markets on city governance (Peck and Whiteside, 2016), among other topics discussed. Kirkpatrick (2016) revisits Minsky’s work on financial instability and Polanyi’s analysis on the fictitious nature of money, land and labour. He argues that US local governments have been increasingly driven into risky ‘Ponzi-esque debt structures’ in capital markets, with diminishing social control over the activities of ‘de-democratised’ quasi-public specific purpose bodies. Although, in Brazil, local and state governments are severely restricted by national regulation of access to capital markets, recent research has analysed the proliferation of local semi-public specific purpose bodies involved in non-transparent negotiated sales of debentures to selected investors using tax receivables as guarantees (Canettieri, 2017).

Although this overview of research on cities in times of financialisation is stylised, it serves our purpose in terms of showing what Christophers (2014) labelled as an in-built tension between political economics, oriented towards analysing ‘what finance does’ (that is, extracting value from all without producing), and social studies inspired work, prioritising the investigation of ‘what it is’ (and how it is constituted socially). More specifically, before cities – as complex and relatively indivisible networks of land and infrastructure and pools of labour (linked, through the tax system, to the public budget) – can be transformed into liquid, that is, tradeable and interest-yielding assets (Gotham, 2009), credit and financial markets have to be constituted in the first place, particularly in the Global South, marked by unconsolidated institutions.

Following Christophers (2014), we argue for a closer articulation between political economics – with its priority on the generation and extraction of value, by and large, taking markets for granted – and social studies of finance-oriented approaches, which emphasise the fleshing out of particularities, collective agencies and circulation of norms and conventions that accompany the capitalisation, pricing and valuation practices in the making of markets and urban financialisation (Chiapello, 2015).

We illustrate the potential of such an approach investigating the gradual, contested penetration of shareholder governance in basic sanitation in metropolitan São Paulo.

The institutional trajectory of sanitation in Brazilian metropolitan areas

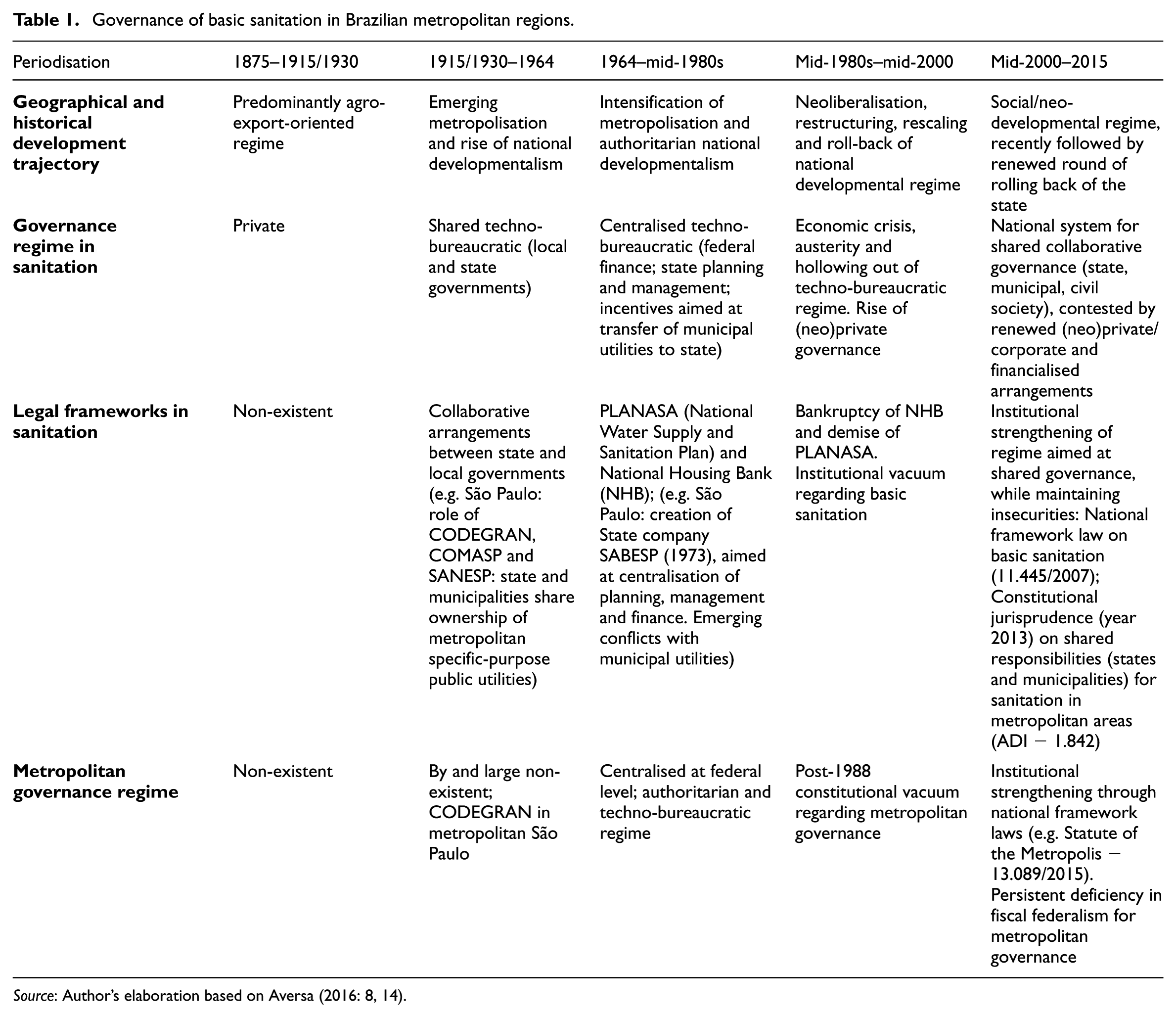

It is not our purpose to analyse in detail the institutional set up of sanitation in Brazilian metropolitan areas. 2 Table 1, based on Aversa (2016) and Barcellos de Souza (2013), provides an overview of the successive stages of the Brazilian developmental state restructuring and its relations with metropolitan governance and sanitation.

Governance of basic sanitation in Brazilian metropolitan regions.

Source: Author’s elaboration based on Aversa (2016: 8, 14).

While developmental policies and industrialisation had been set in motion since the 1930s accompanied by a rural–urban transition and growth of big cities, it was not until the military regime, which took over democratic rule in 1964, that a highly centralised technocratic system of governance and finance was established for Brazilian metropolitan areas, with a key role for institutions such as the National Housing Bank (NHB) and the national system for sanitation (PLANASA). Metropolitan finance has historically lacked a system of predictable, re-distributive federal transfers of tax resources to smooth intra-metropolitan disparities (Rezende, 2010). 3 Funding for NHB and PLANASA was based on a compulsory surcharge on wages that was linked to an unemployment and retirement fund. As such, the guiding principle behind funding was (partial) cost recovery of investments that were mainly directed to social housing and basic sanitation. Federal government was keen on stimulating, through selective financial incentives to cities, the voluntary transfer of municipal utilities to the state sanitation companies that were being created. In São Paulo, for example, this triggered large-scale transfers of municipal utilities to state company SABESP, which had been created in 1973. The approach also signalled the hollowing out of the prevailing model of shared governance, and a gradual build-up of tensions between SABESP and municipalities that decided to maintain their water company.

From the mid-1980s onwards, this ‘peripheral’ developmental infrastructural regime (considering that, unlike welfare regimes prevailing in most industrialised countries, it had never channelled federal tax resources to subsidise and connect poor target groups to the city and its networks) was collapsing in light of macroeconomic stagnation, hyperinflation and bankruptcy of the NHB and its financial model. Moreover, the disarray of developmental institutions increased the pressure to privatise state sanitation companies (Britto and Rezende, 2017). Although SABESP was not privatised and maintained majority state ownership, it was restructured and was listed on the São Paulo (1996) and New York (2002) stock exchanges.

After 2005, the scenario indicates institutional strengthening aimed at shared governance involving state, municipalities and civil society. The national framework legislation on sanitation of 2007 was key in that and provided guidelines for the planning (municipalities), operation and management (municipal or state concessionaries) and regulatory supervision of services, which was to be created by granting authorities. Likewise, a 2013 supreme court ruling (ADI 1.842) confirmed that neither state nor local governments have exclusive responsibility over sanitation in metropolitan areas, but they need to design specific collaborative governance arrangements. 4 Nevertheless, this tendency towards collaborative governance has not deterred the proliferation of institutional and financial conflicts between municipalities and states, as will be illustrated subsequently.

The financial–institutional battlefield in Greater São Paulo 5

From shared to shareholder governance?

SABESP currently supplies 364 of the state’s 645 municipalities. Around 70% of its gross revenue from water and sewage is obtained from the 39 cities that make up metropolitan São Paulo, which represents both a key market and a risk factor within its business strategy. The latter is understood when considering that the ‘supreme court still has not clarified the effects and the extension of its decision ADI 1842 in 2013’ (SABESP, 2017: 20) (that is, regarding how the shared responsibility of states and municipalities in metropolitan areas should be organised). Moreover, several metropolitan cities had maintained their utilities since 1973, while others that had granted SABESP a concession to build/invest, operate and maintain were now approaching the stage of deciding on renewal with SABESP or re-assuming their municipal networks.

The concession negotiation with the city of São Paulo, which provides around half of its gross operational revenue, well illustrates SABESP’s metropolitan strategy. Conversations started immediately after the creation of regulatory agency ARSESP (Regulatory Agency for Sanitation and Energy of the State of São Paulo) in 2007, along the framework of national law No. 11.445/2007. ARSESP is responsible for the regulation and monitoring of sanitation services (including the provision of binding guidelines for pricing), which are either under SABESP’s direct control, or where it acts as a concessionaire of local governments. It also performs a key role in the resolution of disputes in concession contracts. As part of the executive structure of the state of São Paulo, and receiving its support in terms of staffing and finance, its independence has been questioned. Rating agency Moody (Moody’s Investors Service, 2013: 2), for example, considered that: The short period of operation of ARSESP and the lack of strong evidence of complete independence from the state government impose additional regulatory risks. The board of Directors is composed of members appointed by the state government and approved by parliament.

The city of São Paulo was pressured to grant a 30-year concession in light of the significant debt it had accumulated with SABESP. The contract that was signed in 2010 provided SABESP with the exclusive right to invest/build, operate and maintain the network, irrespective of the specific design for shared governance that would be adopted according to the 2013 supreme court ruling. Moreover, revenue-sharing clauses with the city of São Paulo were conditional on the financial viability of the contract, while rules regarding contractual suspension (requiring inflation adjusted payment of non-depreciated assets plus a 15% surcharge) provided additional guarantees for SABESP (Ferreira, 2019).

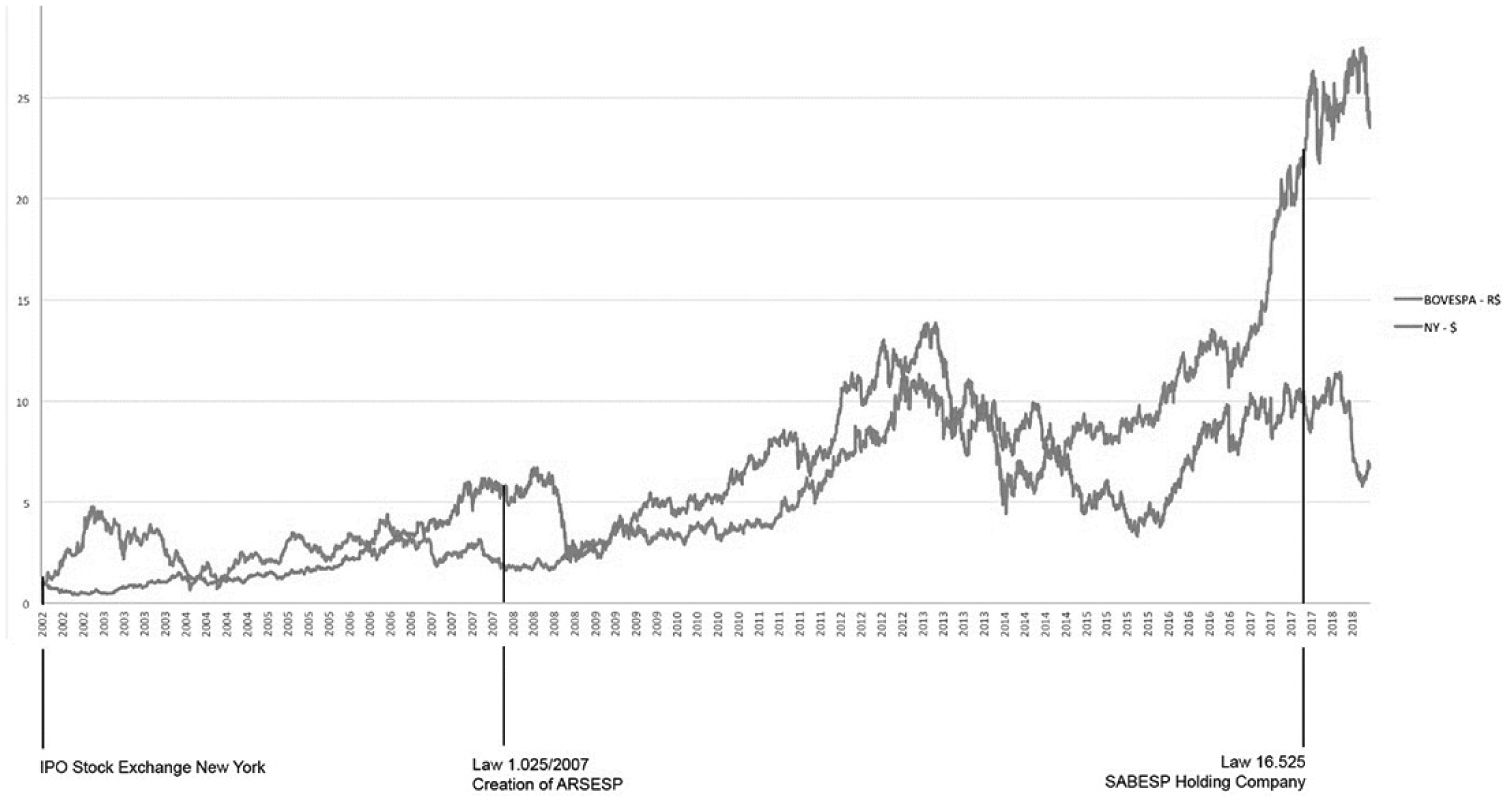

Figure 1 illustrates the evolution of SABESP’s nominal share price since its listing on the New York stock exchange in 2002 until its transformation to a public holding company in 2017. 6 The performance on the São Paulo exchange shows a yearly increase of almost 200%, or 65% in real prices of 2002. 7 With the exception of the drought and water crisis during 2013–2015, shares have been rising since the creation of ARSESP in 2007. Nevertheless, part of SABESP’s financial surplus leaked away; during 2007–2016, the company generated a net profit of R$14.6 billion, of which R$10.3 billion was reinvested. 8 As a majority shareowner, the state received R$2.16 billion (out of R$4.3 billion) in dividends, which were allocated externally to finance activities out of the general budget (Henrique, 2017: 124).

Evolution of nominal share price – SABESP.

Institutional conflicts in the metropolitan fringe

SABESP’s strategy intensified conflicts in other metropolitan cities such as Santo André, which also had not granted a concession. In the 1990s, its utility SEMASA was the first Brazilian company to integrate solid waste, water, sewage and drainage within an integrated urban development perspective.

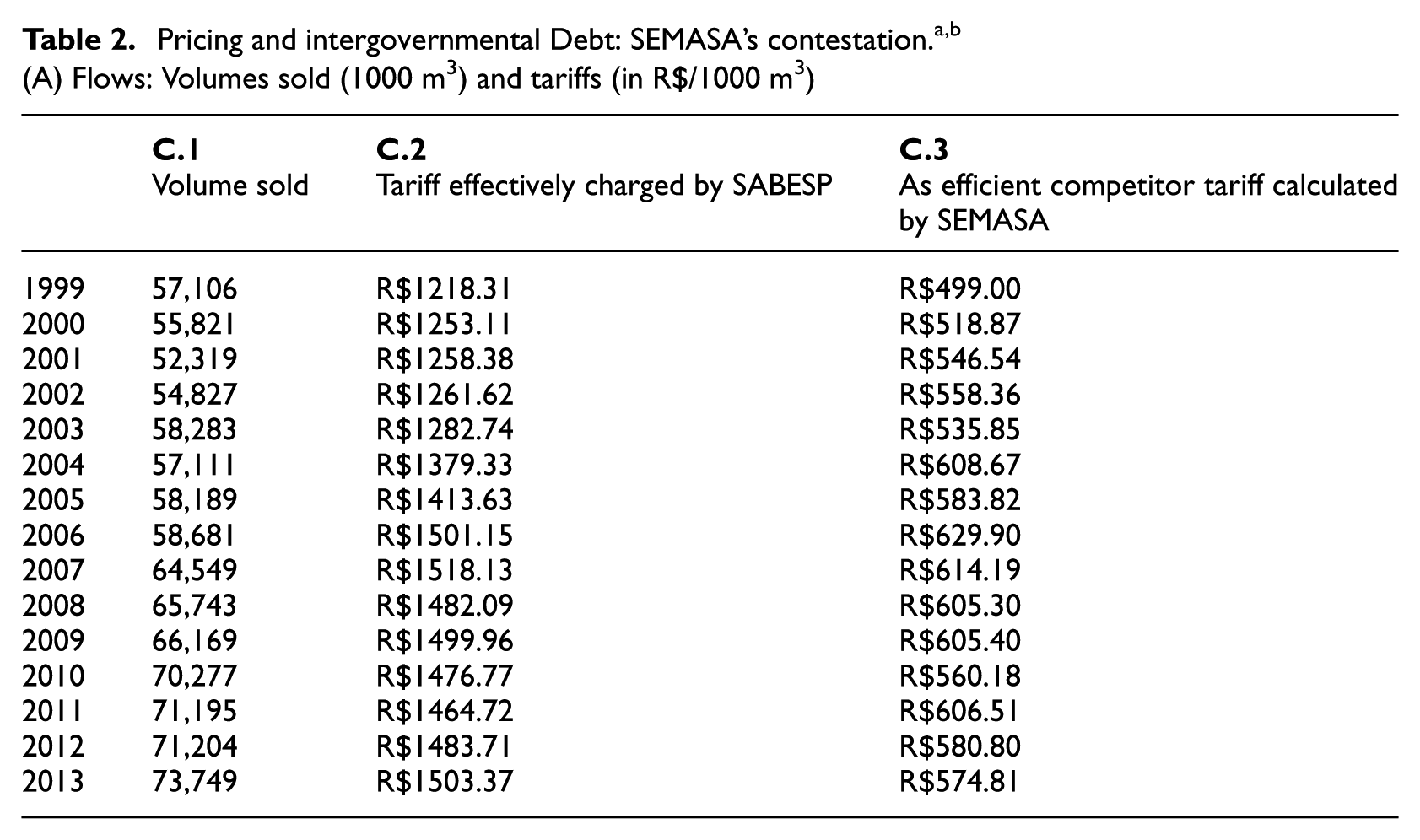

In 2015 SEMASA filed a request to National Antitrust Agency CADE (the Administrative Council for the Protection of the Economic Order) to investigate infringements of the economic order committed by SABESP. SEMASA claimed that, since the mid-1990s, SABESP had been using its quasi-monopoly position in the wholesale market in order to apply abusive, margin squeezing pricing policies to municipal utilities, which depended on SABESP’s supply to provide retail water to households. 9 Using international jurisprudence on the ‘as efficient competitor’ test used in similar situations, 10 it calculated that SABESP would be unable to maintain viability of its own retail operations under the prevailing discriminatory wholesale prices it practised. It estimated that SABESP would accumulate losses in its retail operations of around R$59 billion to R$80 billion during 1999 and 2014, considering the prices it charged to SEMASA.

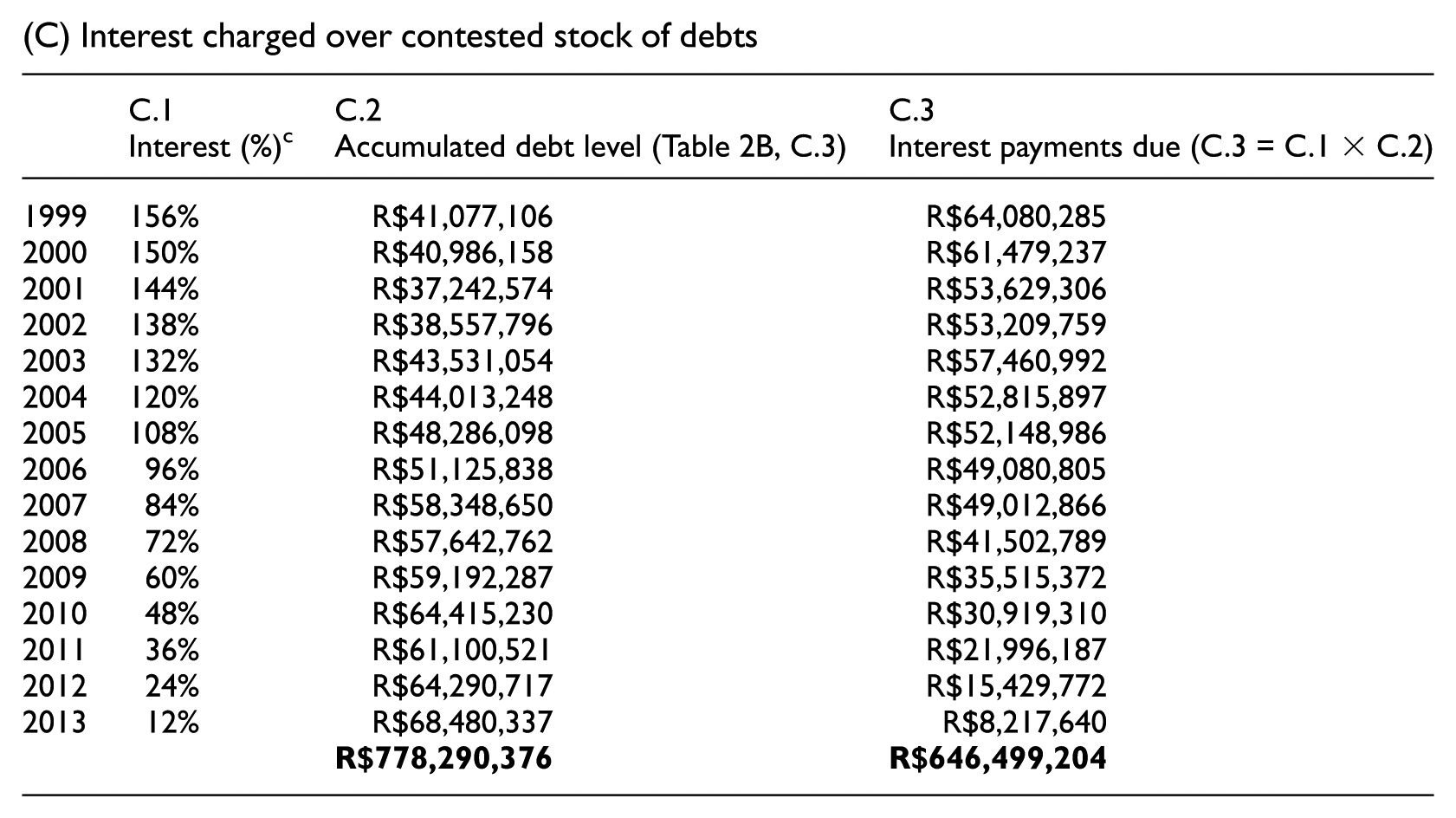

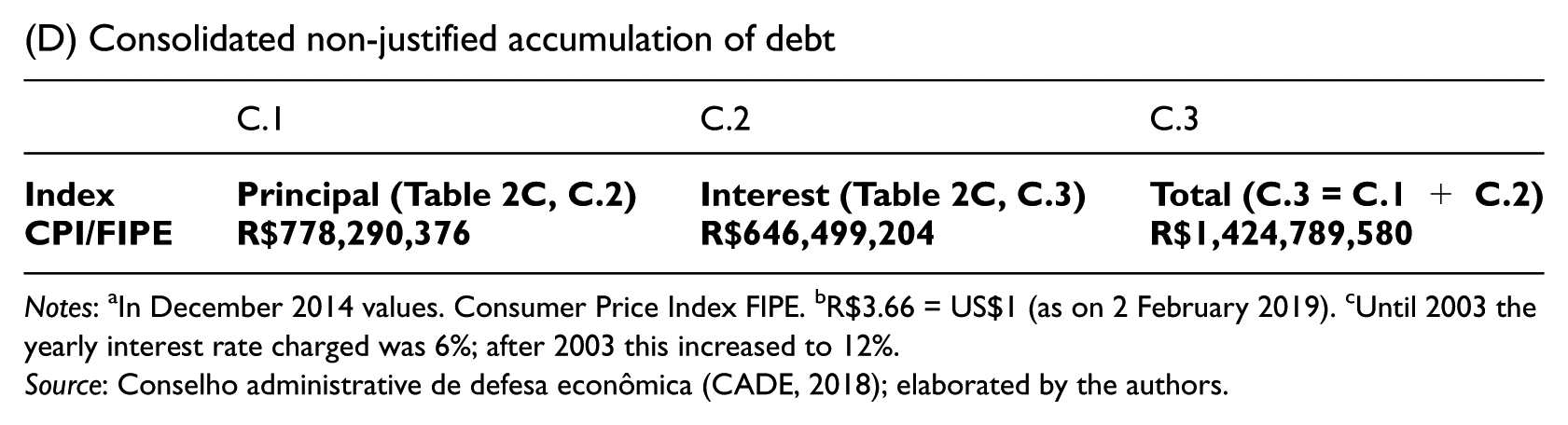

SEMASA showed that the disagreements regarding water pricing had generated a non-justified escalation of municipal debt with SABESP, which is illustrated in Table 2 (in December 2014 values). 11 Table 2A shows the volume of water and sewage delivered by SABESP (in 1000 m3), the average yearly tariff it effectively charged compared with the lower tariff associated with the as efficient competitor test. Table 2B subsequently shows the unjustified accumulated stock of debt, that is, the difference between tariff revenue charged by SABESP and the amount of revenues associated with the lower tariff. The interest rates charged over outstanding debts in similar court cases involving SABESP are summarised in Table 2C, providing an inflation-adjusted estimate of total accumulated debt (amortisation plus interest), during 1999–2014, of around R$1.4 billion (Table 2D).

(B) Stocks: Revenues charged by SABESP versus revenues according to the ‘as efficient competitor’ tariff

(C) Interest charged over contested stock of debts

(D) Consolidated non-justified accumulation of debt

Notes: aIn December 2014 values. Consumer Price Index FIPE. bR$3.66 = US$1 (as on 2 February 2019). cUntil 2003 the yearly interest rate charged was 6%; after 2003 this increased to 12%.

Source: Conselho administrative de defesa econômica (CADE, 2018); elaborated by the authors.

Similar disputes had occurred in other cities in the metropolitan fringe, such as Osasco (1999), São Bernardo do Campo (2003) and Diadema (2013), and were instrumental in SABESP’s strategy to eventually control the metropolitan retail market for water. In all these cases, negotiations outside the courts regarding debt relief in exchange for concessions awarded to SABESP had been completed and signed. According to SEMASA, SABESP’s excessive wholesale prices had squeezed financial margins of all these municipal utilities, considering the political challenge to passing on these costs to poor households through escalating retail prices. In the meantime, the escalating stock of debt of metropolitan cities Guarulhos, Mauá and Santo André, all the object of pending court cases and parallel negotiations with SABESP, was estimated to be around R$8 billion (values of March 2016). SEMASA would be the next in a series of ‘forced’ signatures of concession contracts with SABESP, which would further hollow out shared water governance in metropolitan São Paulo.

SEMASA also questioned the state regulatory agency ARSESP; while created in 2007, it only managed to publish its first four-year guidelines on the criteria for water tariffs in 2014 (see next section). Until then, ARSESP had not evaluated SABESP’s pricing rules and simply approved yearly inflation adjustments of pre-established tariffs.

In 2017, CADE rejected SEMASA’s request to investigate SABESP on three arguments.

12

First, although it had a quasi-monopoly position in the wholesale water market, SABESP had no dominance in retail. Rather, in metropolitan cities with municipal utilities, such as Santo André, this monopoly was exercised locally. Second, CADE argued that price revisions had occurred within guidelines set and monitored by an independent regulatory agency (ARSESP), which also ruled out possible advantages of discriminatory pricing in wholesale and retail markets. Finally, while stating it was not its responsibility to evaluate specific pricing rules adopted by two market players, CADE nevertheless argued that SEMASA’s request was seen in the context of the latter’s refusal to raise retail water prices – which could have avoided its debt – rather than an infringement of the economic order by SABESP. Being a local monopolist, CADE considered that SEMASA could have easily raised its retail prices (CADE, 2018: 12):

13

Especially considering a downstream and heavily indebted monopolist, its pricing rule should consider passing on to consumers the rising costs of inputs. Instead, what seems to be happening in this case is that SEMASA reduces its costs by paying less than it should to SABESP with the objective of not charging higher tariffs to the inhabitants of Santo André.

What price for water?

Understanding what is at stake requires an analysis of the logic behind the water tariff revisions coordinated by ARSESP, which are binding for SABESP and cities where it performs the role of concessionaire.

ARSESP adopts a price-cap rule, setting a ceiling for tariffs that guarantees a minimum rate of return on investments, and operating expenditures and financial viability for debt and equity providers. This price ceiling should also allow the expansion of service coverage and quality goals as targeted by municipal and state sanitation plans, while avoiding excessive burdens for consumers. The formula used is based on the financial literature on long-run average incremental cost pricing for infrastructure (Bahl and Linn, 1992). The technique applies forward-looking discounted cash flow (DCF) analysis, providing a water tariff that breaks even, in net present value terms, the projected costs and revenues over the life cycle of projects, while using a minimum required rate of return equivalent to the weighted average, risk-adjusted cost of capital for debt and equity finance. In the specific case of SABESP, the discount rate used during the first tariff cycle (2011–2014) was 8.06%.

Nevertheless, different from pure, forward-looking DCF methods (capitalising expected cash flows of revenues and expenditures), ARSESP also includes historical cost accounting to evaluate SABESP’s non-depreciated engineering objects (networks, pipelines, buildings, etc.). Therefore, in a variation on Chiapello’s (2015) analysis on the substitution of historical cost methods by forward-looking financial DCF analysis in valuation, ARSESP adopts a ‘hybrid’ approach, whereby historical cost accounting of non-depreciated investments undertaken in the past and expected financial cash flows in the future are combined. In a way, non-depreciated investments undertaken by SABESP in the past, as engineering objects, become assets once they are incorporated into ARSESP’s ‘regulatory baseline’, considering these also receive the required minimum rate of return.

The concrete perspective of assetisation (Birch, 2017), that is, in this particular case, artificially inflating the accounting base of non-depreciated investment of the past, created a series of conflicts regarding the regulatory process in general, and the way it could facilitate price increases charged to municipal retailers such as SEMASA, in particular. On the one hand, SABESP argued, and anti-trust agency CADE agreed, that charging more in retail markets would imply lower prices in the wholesale segment (and vice versa), considering that the price-cap regime set a ceiling for the rate of return, and effectively consolidated a zero-sum game for discriminatory pricing strategies. On the other hand, SEMASA contested that CADE had clearly underestimated the possibility of creative calculative practices aimed at increasing ARSESP’s regulatory baseline for SABESP, which would enable the transformation of engineering objects into assets by inflating non-depreciated investments undertaken in the past.

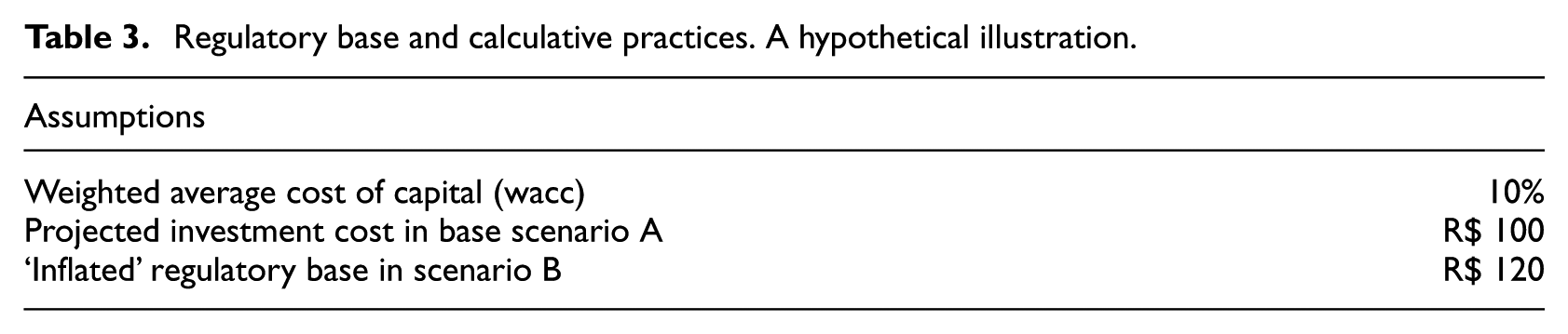

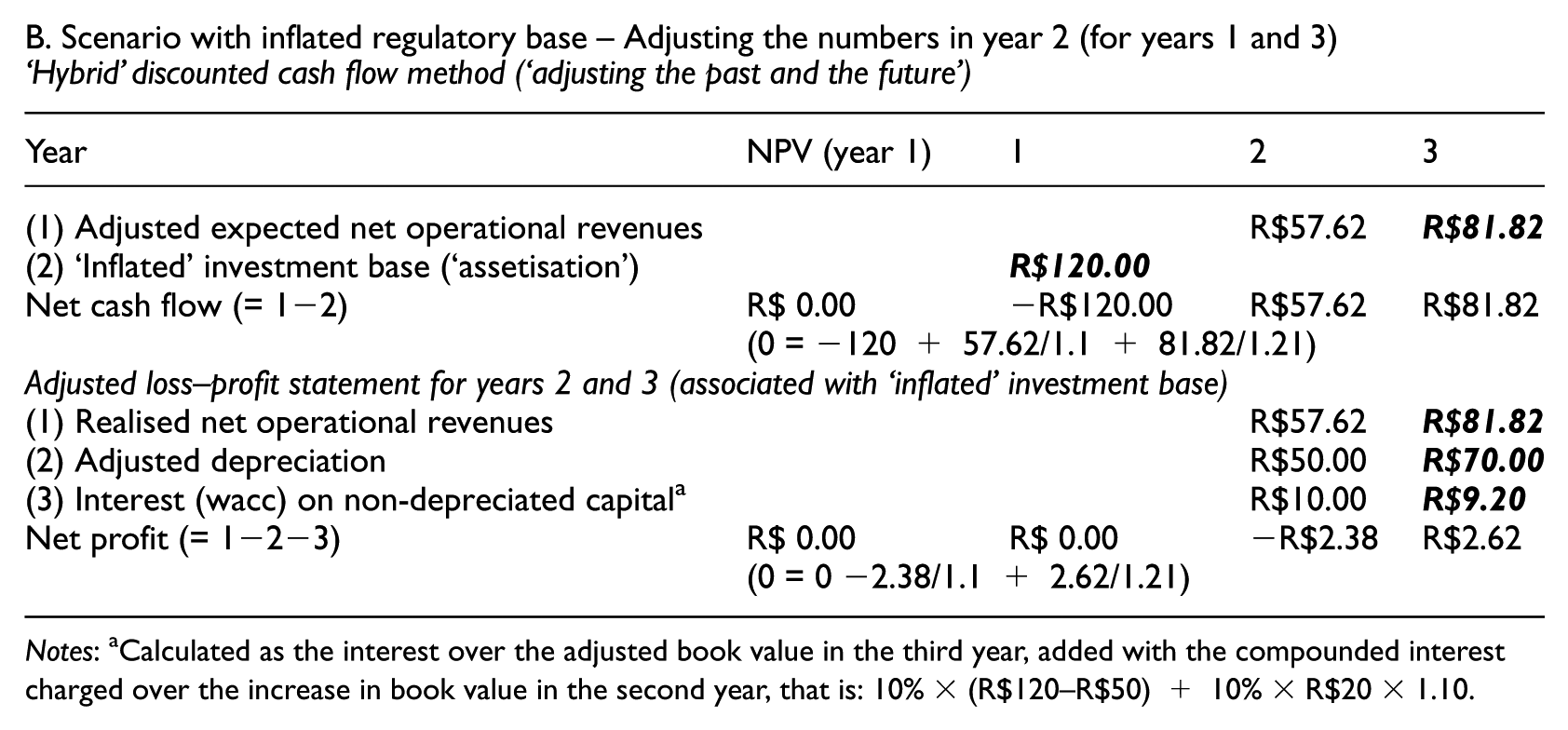

Table 3 provides a three-year simplified, hypothetical illustration of SEMASA’s argument (investments occurring in the first year, net operational revenues in the subsequent two years). Base scenario A shows a pure DCF approach making decisions in year 1. Expected investment costs of R$100 billion (representing a yearly accounting depreciation cost of R$50 billion in the loss–profit statement) require a projected average annual revenue of R$57.21 billion in order to recover a hypothetical cost of capital of 10% (resulting in a zero Net Present Value of the investment). Scenario B illustrates hybrid DCF accounting where revaluation of non-amortised investments of the past penetrates calculations for the future. Assuming the project is ‘up and running’ at the end of the second year, what happens if the value of non-depreciated investments of the past (year 1), which can be interpreted as ARSESP’s regulatory asset base, are inflated from R$50 billion in the base scenario (R$100 billion–R$50 billion) to R$70 billion (R$120 billion–R$50 billion)? The bold figures in scenario B show that this requires increasing expected cash-flow revenues for the third year to R$81.82 billion (being the sum of the initial projection for the third year, that is R$57.21 billion, and the increase in the regulatory asset base (R$20 billion), adjusted with the compounded cost of capital of 10% during two years).

Regulatory base and calculative practices. A hypothetical illustration.

(A) Base scenario – Decision-making in year 1

Pure discounted cash flow method (future-oriented, decision-making start of year 1)

B. Scenario with inflated regulatory base – Adjusting the numbers in year 2 (for years 1 and 3)

‘Hybrid’ discounted cash flow method (‘adjusting the past and the future’)

Notes: aCalculated as the interest over the adjusted book value in the third year, added with the compounded interest charged over the increase in book value in the second year, that is: 10% × (R$120–R$50) + 10% × R$20 × 1.10.

Thus, even with a cap on the overall rate of return in wholesale and retail markets (being 8.06% for SABESP), SEMASA claimed that in a context of cumbersome access to SABESP accounts, 14 uncertainty and complexity (networked metropolitan systems being amortised over decades), malpractice of the data regarding investments and depreciation in the past could trigger escalation in the numbers used to guide capitalization and pricing decisions in the future.

Debt, water pricing and strategy. If you can’t beat them, join them?

In 2016 SEMASA contracted a consultancy study that was to provide contributions to the design of its business strategy (SEMASA, 2018). It estimated the economic value of the organisation under three scenarios, each based on the projected discounted cash flow of net receipts (in present value of December 2017). In a ‘business as usual’ base scenario the company would continue as a municipal utility and maintain its existing portfolio of activities, resulting in a net worth of R$1.5 billion. The second scenario was similar but would devolve loss-generating operations to the municipality (solid waste; drainage and environmental management) and downsize to core business (water and sewage). This scenario would generate a net company worth of R$2.7 billion. A final scenario, generating economic value of around R$4.2 billion, would transform SEMASA into a mixed-capital company listed on the stock exchange, while maintaining municipal majority ownership. This increase in its economic value would emerge from a reduced cost of capital associated with an initial public offering of stock, considering it would avoid using expensive short-term working capital. 15

Irrespective of the strategy it will adopt – at the time of writing still undecided – SEMASA is pressured by the courts and SABESP to settle its debt, which was estimated as between R$2.7 billion and R$3.4 billion in December 2017. Considering the previous calculations, this practically rules out a scenario of ‘business as usual’ (generating economic value of R$1.5 billion). Moreover, SABESP is keen on signing a concessionary contract with SEMASA, considering this brings the latter into the price-cap regime, provides more regulatory control and leverage of contracts via ARSESP and a more predictable revenue pattern for SABESP in the city.

Considering that the courts, ARSESP and anti-trust agency CADE point in the same direction, that is, that debt should be paid in one way or another, this will either mean awarding SABESP a concessionary agreement against debt relief or restructuring debt and transforming SEMASA into a mixed-capital company listed on the capital market. Either way, this will require transformation in its strategy, including fragmentation in service delivery by devolving loss-generating activities to local government and increasing water prices.

In case of a concessionary agreement with SABESP, this will not include activities that generate financial burdens (environmental management, solid waste and storm drainage), also considering that the latter are not part of SABESP’s core business.

Increasing water prices generates solutions (increasing financial viability and debt reduction) as well as problems, considering that SEMASA’s empirical estimates for metropolitan São Paulo have shown that, under the present tariff structure, water pricing is notoriously regressive (SEMASA, 2018). For instance, in metropolitan São Paulo, income brackets 1 (monthly earnings up to R$830.00) and 7 (earning more than R$10,375.00) spend widely diverging percentages of income on water bills (4.58% versus 0.66%, respectively). In the city of São Paulo, these discrepancies increase (6.39% versus 0.43%, respectively). To aggravate the issue, price increases aimed at revenue maximisation are likely to be more effective with low-income households, considering their reduced price elasticities of demand (reflecting their difficulty to substitute with alternative sources such as bottled water).

As discussed, SABESP’s concessionary contracts with municipalities provide ample illustration of ‘stand and delivery’ clauses aimed at maintaining its financial viability and reducing risks (Hildyard, 2016: 32–40; State Government and Municipality of São Paulo (GESP and PMSP), 2010). Specific national sanitation data (Ministério das Cidades, 2018) indicate that concessionaire SABESP does not provide superior service delivery. In cities such as São Bernardo, which signed a contract in 2004, the share of families that faced service interruption has been consistently higher than in Santo André; during the water crisis in 2015, 98% of families in São Bernardo reported interruptions compared with 38% in Santo André. The percentage of families that complained about service delivery in the city of Osasco, which signed its concession in 1999, has consistently exceeded the figure in Santo André (for example, in 2015, 17% versus 10% of households registered complaints, respectively).

Conclusion

In addition to revealing a scenario whereby financialisation of water in metropolitan São Paulo is still open-ended, our analysis provides two insights into the literature on urban financialisation, with relevance for the Global South.

First, in the absence of consolidated capital markets, fleshing out the entanglements between intergovernmental debts, pricing and valuation of infrastructure assets and water governance is key in understanding the making of financialisation. Investigating how specific financial and institutional devices and pricing practices were set in motion sheds light on the gradual hollowing-out of shared governance among state and local governments, and its replacement with elements of shareholder governance. We have briefly discussed the ongoing institutional–financial dispute between SEMASA and SABESP – increasingly driven by shareholder value premises – which has generated pressures to negotiate debts and a concessionary contract with the state company, implying increased water prices and devolution of less profitable activity areas to general purpose city government.

Santo André is not an isolated case in the Brazilian political economics of sanitation (Swyngedouw, 2013); in metropolitan São Paulo similar debt-triggered awards of municipal concessions to SABESP have led to an increasing penetration of shareholder governance in the cities of Osasco, São Bernardo, Diadema and São Paulo itself. While Mauá is still negotiating, in October 2018 the city of Guarulhos signed a preliminary concession agreement with SABESP. Moreover, changes in national legislation that stimulate private-sector entrance in local government concessions are being discussed. Instead of the existing framework of Law No. 11.445/2007, which allows for bilateral negotiation of concessions between state companies and local governments without tendering, the new design favours local governments organising competitive bidding for concessions involving the private sector. Finally, the newly elected state government of São Paulo has announced plans to privatise SABESP, triggering a record increase in its share price to R$41.60 in January 2019 (Rocha and Maia, 2019).

Second, political economics-inspired analyses of what finance tends to do – transforming cities into bundles of tradable income-yielding assets and extracting value for that – can receive valuable inputs from social studies-oriented work, aimed at investigating how financial markets are socially constituted in the first place through variegated entanglements between calculative practices and circulation of norms and conventions within professional communities, particularly considering the technological indivisibilities, risks, illiquidity and contestation that are inherent to city-space. We provided a first illustration of how these conceptual bridges could be established for metropolitan water finance and governance in São Paulo. Moreover, this cross-fertilisation between political economics and social studies of finance could provide potential added value for several of the themes in the literature on urban financialisation discussed above, such as the financialisation of land; urban entrepreneurialism and the financialisation through large urban development projects; and the nexus between capital markets and cities under austerity. Such work could set the stage for a research agenda according to which financialisation is not an a priori entrance point for urban studies, but whereby the variegated and contradictory (re)production and appropriation of city space and collective wealth under the increasing influence of finance capital is embedded in a geographically and temporally specific reading of how fictitious markets for money (and credit), land and labour are socially constituted in the first place (Kirkpatrick, 2016).

Footnotes

Acknowledgements

Funding

This research undertaken for this paper was funded by the Brazilian National Council for Science and Technology (CNPQ), Grant no. MTIC/CNPQ 2/2018.