Abstract

China has adopted a transfer-based fiscal decentralisation scheme since the mid-1990s. In the 1994 tax sharing reform, the central government significantly raised its share of government revenue vis-à-vis local governments by taking most of the newly created value-added tax on manufacturing. One aim for the adoption of the transfer-based fiscal scheme was to channel more funds to less developed regions and rural areas, and to alleviate growing interregional inequality and urban–rural income disparity. In 2002 and 2003 the Chinese central government further grabbed 50% and 60%, respectively, of the income taxes previously assigned only to local governments while providing more fiscal transfers to the country’s poor regions and the countryside. Utilising the 2002–2003 change in China’s central–local tax sharing regime as an exogenous policy shock, we employ a Simulated Instrumental Variable approach to causally evaluate the effects of the policy shock on growth, interregional inequality and urban–rural disparity. We find the lower local tax share dis-incentivised local governments and led to lower growth. Although higher central transfers helped to reduce interregional inequalities in per capita GDP and per capita income, the equalising effects were only present for urban incomes. We argue that transfer-based decentralisation without bottom-up accountability was detrimental to economic growth and had limited impact on income redistribution.

Introduction

The spread of fiscal decentralisation in developing and emerging market economies has received extensive attention from academics. Research has been undertaken on the effects of fiscal decentralisation on economic growth, income inequality and poverty alleviation, and many other economic and political issues (Sepulveda and Martinez-Vazquez, 2011).

As the largest developing country, China has been a pioneer of fiscal decentralisation. In the early 1980s, the central government devolved budgetary control authority to local governments after the latter fulfilled their revenue obligations to the centre. The fiscal contracting greatly altered the incentives of local officials and contributed to the fast-growing economy (Montinola et al., 1995). However, since 1994, the central government has modified the tax structure on multiple occasions and gradually recentralised revenues to the top (World Bank, 2002). As a result, large sums of fiscal transfers have become increasingly common for the centre to accomplish its goal of decentralisation. Whether this partial decentralisation works in terms of growth and inequality outcomes is an important research question.

The literature on the empirical effects of fiscal decentralisation has been huge. However, as recently emphasised by Martinez-Vazquez et al. (2017), a crucial but yet unsolved issue with the existing empirical literature on the impact of fiscal decentralisation is that most contributions fail to address the proper measurement and the endogeneity of fiscal decentralisation. Therefore, decades of empirical research on decentralisation do not yield a clear consensus (Faguet, 2014). Differences in how decentralisation is defined and measured can result in widely differing values of the decentralisation variable. To make things worse, in empirical studies fiscal decentralisation is often captured by means of actual expenditure and revenue data. However, such measures are usually endogenous because they may well be caused by the economic processes to be evaluated, such as economic growth. Endogeneity problems could also arise because of the simultaneous effects of omitted variables on both decentralisation and some of the seemingly exogenous variables. For example, intergovernmental grants are rarely randomly assigned and many political factors often decide which regions get more (Knight, 2002). Therefore, interpreting a positive correlation as causal can be problematic. Recent scholarship on decentralisation has increasingly relied on stronger causal identification strategies, including instrumental variables (IV), differences-in-differences (DID), regression discontinuity design (RDD), and unexpected windfalls (Rodden, 2019).

In this research, we seek to contribute to the decentralisation debate by empirically evaluating one major Chinese policy initiative, and explore the effects of transfer-based decentralisation on local growth and spatial inequality both across regions and between urban and rural areas. Drastically increasing central revenue share while at the same time making up local revenue shortfall with more transfers, China’s 2002–2003 tax-sharing reform altered local incentives through two simultaneous channels, that is, lower local tax autonomy and higher local revenue from central transfers. Exploring this unique opportunity of identification, we use a Simulated Instrumental Variable (SIV) approach to address the issue of endogeneity and causally evaluate the effects of changes in the central–local tax-sharing rate and intergovernmental transfers on growth, interregional inequality and urban–rural disparity, respectively. We find that revenue centralisation by lowering local government shares of tax revenue indeed hurts growth. Although higher local government revenue in the form of transfers helped to reduce interregional inequality in per capita GDP and income, the equalising effects were only present for urban incomes. As a result, the urban–rural disparity further enlarged. This happens because the lack of local government accountability in an autocracy is further aggravated by a transfer-based decentralisation in which local governments pay even less attention to the poor.

Our research can shed some light on the debate about the role of fiscal design in regional growth and rural development. In light of the shortage of basic public services in many localities and rural areas, some advocated increasing the size of central fiscal transfers. Our analysis of China’s 2002–2003 tax-sharing reform indicates that a different problem is condemning public good provisioning: resources could still be allocated between urban and rural in a highly unequal manner even though the centre’s main target was the poverty-stricken rural population. This could happen since much of the transfer has leaked through the system owing to unaccountable local officials. Therefore, centralising fiscal revenues and increasing transfers ended up with even larger urban–rural disparity. Therefore, the stronger central fiscal capacity is not sufficient to effectively strengthen state capacity in income redistribution and to alleviate the serious urban–rural divide. Lack of bottom-up accountability and increasing local transfer-dependency could reinforce each other and jointly contribute to perpetuating and even growing urban–rural income disparity.

The rest of the paper proceeds as follows. In the next section we review the related literature. The following section lays out our hypotheses following a discussion of China’s transfer-based decentralisation. The next section describes the data, defines variables and presents our empirical strategy. The penultimate section lays out our empirical strategy and reports the empirical results. The final section concludes.

Literature review

As the past 40 years have witnessed a decentralising wave around the world, a large literature has emerged on the relationship between decentralisation, growth and inequality. However, only limited consensus has been reached on the question whether decentralisation is associated with a lowering or rising of economic growth as well as spatial disparities across regions and of income disparity within a locality (Martinez-Vazquez et al., 2017).

The economic case for decentralisation relies essentially on efficiency arguments. Fiscal decentralisation creates stronger incentives for good performance for local government. In the traditional literature of fiscal federalism, government is viewed as a benevolent agent, and provision of public services by a decentralised government structure generally will be more efficient. Such efficiency gain comes both from the information advantages of local government in adapting to citizens’ needs and from the competition among local governments to attract mobile residents (Oates, 1972).

The ‘second-generation’ fiscal federalism focuses on incentives for government officials not to deviate from ‘good behaviour’ and emphasises the role of decentralisation as a mechanism to control an expansive public sector and also support private market activity (Weingast, 1995). In this framework, decentralisation encourages yardstick and tax competition among local governments; therefore, it can improve accountability and lessen information asymmetry. In addition, increased electoral accountability ultimately translates into more efficient government performance (Besley and Case, 1995; Besley and Coate, 2003; Bordignon et al., 2004).

Besides growth effects, fiscal decentralisation is also claimed to be more effective in carrying out redistribution and alleviating income inequality. As individuals in different jurisdictions have different preferences, power transfer to local governments makes it possible to better match local demand. Moreover, increased decentralisation can improve local accountability since officials are now monitored by a more engaged and informed population (Rodden, 2016). Assuming local officials under electoral pressures now have access to more resources under fiscal decentralisation, they can either be forced to redistribute more or they can redistribute more efficiently given their information advantages. Presumably this would reduce income inequality.

However, the theoretical and empirical literature also cautions against the pitfalls of decentralisation. Decentralisation may fail both in growth promotion and in income redistribution even in a democracy if local governments are captured by strong elites. Tanzi (1996) argued that the assumption that local governments are more likely to respond to local preferences and to more efficiently provide local public good than the central government does not necessarily apply in a non-democratic political system. Under decentralisation, local governments may be more easily captured by interest groups and divert resources to their inner circles. Consequently, fiscal decentralisation may lead to misallocation of resources and finally undermine economic growth. Moreover, fiscal decentralisation could also undermine the central fiscal power thereby reducing the scope to redistribute resources across regions and across different income groups. As Qiao et al. (2008) have demonstrated, there is a trade-off between growth and regional equality in decentralisation. A higher level of decentralisation led to higher growth even though the relationship was non-linear, while decentralisation may easily increase interregional fiscal inequality.

The growth and distributional effects of decentralisation also depend on how decentralisation is financed (Rodden, 2016). Since the overwhelming majority of decentralisation initiatives at the end of the 20th century was funded by intergovernmental grants rather than increased local taxation (Brueckner, 2009), it is known as expenditure decentralisation without revenue decentralisation (Rodden, 2016). Under such decentralisation, citizens are even less able to hold local officials accountable for budgetary allocations and policy outcomes since these officials can fund their activities with transfer funds rather than local tax revenue that needs to be cultivated by providing good public goods. Voters may also be willing to tolerate higher levels of inefficiency and rent seeking if transfers foster the perception that other peoples’ money is being wasted (Bahl and Linn, 1992). Therefore, new forms of inefficiency and rent seeking emerge: if subnational authorities anticipate that their financing gap will be covered by the centre, they will work less hard to promote growth and increase local tax revenue (Brueckner, 2009). If intergovernmental transfers are commonly viewed as unearned ‘windfalls’, it would also weaken the incentives and abilities of local citizens to monitor local officials. Local officials may not only exert less effort, but even worse, may exploit opportunities for theft and other forms of corruption even when there are local electoral pressures (Rodden, 2016). This may result in worse distributional outcomes. A recent paper investigates the causes of the decentralisation of different categories of public expenditure in 19 developed countries over the period 1980–2006. The results confirm the negative link between regional income disparities and expenditure decentralisation (Sacchi and Salotti, 2016).

Fiscal decentralisation has long been argued to contribute to China’s fast growth in its earlier period of transition up untill the mid-1990s, and the pro-business incentives given to local officials are thought to be the result of fiscal decentralisation and high-powered intergovernmental fiscal revenue-sharing contracts (Devarajan et al., 1998).

As to the effects of decentralisation on spatial inequality, some researchers find China’s fiscal decentralisation led to deteriorating interregional fiscal inequality, which in turn widened interregional socio-economic disparities, particularly in provinces where agriculture or the primary industry were the dominant sources of economic activity, but that still need to pay for a large bureaucracy under political centralisation (Zhang, 2006; Zhao, 2009). Fiscal transfer is the common means for mitigating regional disparities, but its effects depend on the extent of fiscal decentralisation as well as the type and adequacy of fiscal transfers (World Bank, 2002). The literature on the effects of decentralisation on urban–rural disparity is rather limited. Kanbur and Zhang (2005) find that heavy industry development in the cities formed the initial rural–urban gap leading up to the reform period, but decentralisation in the 1980s and the early 1990s increased rural–urban inequality.

The rise of transfer-based decentralisation in China and three hypotheses

From 1994 onward, China has recentralised the revenue powers with the introduction of a Tax-Sharing System. Consumption tax was assigned to the central government while business tax and income tax became local revenues. Value added tax (VAT), the largest source of local revenue, was shared, with 75% going to the centre. The result was immediate and the central share in total government revenues jumped from 22% in 1993 to 56% in 1994 and has remained above 50% since then (World Bank, 2002). The fiscal system was further centralised after 2002. In 2002, 50% of income tax was taken from the local governments. In 2003, the ratio further rose to 60%.

However, the central government did not alter the decentralised spending structure correspondingly (World Bank, 2002). As a matter of fact, expenditure responsibilities of subnational levels after 1994 became even heavier because of the burden of maintaining a social safety net at the local level (Wong and Bird, 2008). In government expenditure, China is one of the most decentralised countries in the world. In the 1990s, the ratio of subnational to total government spending averaged 32% in OECD countries, 26% in transition economies and 14% in developing countries. With its 70% ratio of subnational to total spending, of which more than 55% is at sub-provincial levels, China was clearly an outlier.

The ensuing vertical imbalance was financed through more transfers. As a result, central transfers have played increasingly important roles in financing local spending since the mid-1990s. In 1994, the transfers from the centre amounted to RMB 49.7 billion yuan, which was about 45% of central government revenues. By 2010, 73% of the central revenue was designated for transfer purposes. If we look at the share of central transfers in total local revenues, starting from 11% in 1994, central transfers rose quickly to 20% in 1999 and 42% in 2010.

Overall, since the mid-1990s China has adopted an intergovernmental fiscal system featuring transfer-based expenditure decentralisation. The central transfers are now at the forefront of implementing the strategy of reducing both interregional and urban–rural inequality. From the early 2000s, more general transfers have been channelled to less developed regions to cover personnel and administrative costs for local public employees. During the same period, various new types of earmarked transfers emerged to help local development projects, in particular to build rural basic infrastructure, strengthen agricultural technology extension, scrap tuition fees and textbook charges for poor rural children, and fund the rural medical insurance scheme.

Formation of hypotheses

Revenue centralisation and local growth

Looking at China’s intergovernmental relations in the reform era, one can observe that government expenditure responsibilities have always been highly decentralised. The main changes after the tax sharing reforms in 1994 and 2002–2003 were intergovernmental revenue reassignment. With the tax-sharing reforms, China has become an increasingly centralised country in terms of fiscal power. In other words, unlike many developing countries that experienced both revenue and expenditure decentralisation, China’s decentralisation, if one has to call it a decentralisation, is mainly limited to the expenditure side and is largely a transfer-based one.

Based on the standard theory of fiscal decentralisation, we formulate Hypothesis 1.

H1: Other things being equal, the lower local revenue sharing rate in the 2002–2003 reform would disincentivise local governments in promoting local development and thus lead to lower growth.

Transfer-based decentralisation and interregional inequality

With rapidly growing fiscal capa-city after 1994, the Chinese central government was able to tackle the issues of ever-increasing interregional inequality. However, the majority of the central transfers were in the form of earmarked transfers between 1994 and the early 2000s. Since earmarked transfers were delivered on an ad hoc negotiated basis and usually required local matching funds, the richer localities usually had more, or at least no less, access to them. In effect, the earmarked transfers in this period were actually disequalising rather than equalising (World Bank, 2002).

By implementing the 2002–2003 income tax centralisation, the centre enjoyed even higher fiscal capacity and was able to significantly increase the share of general transfers. From the central perspective, general transfers do not leave much room for manipulation and, by definition, help localities with weak industrial and commercial tax bases. Along with the increase of general transfers, a rural tax-for-fee reform was initiated in 2002, and by 2006 local governments had been deprived of the power to levy any agricultural taxes and fees on farmers. Therefore, we formulate Hypothesis 2 on interregional inequality.

H2: Other things being equal, higher local revenue through increased central transfers, in particular through general transfers after the 2002–2003 reform, would induce a convergence of per capita GDP and per capita income across provinces.

Transfer-based decentralisation and urban–rural income disparity

The effects of China’s transfer-based decentralisation on urban–rural disparity deserve more analysis. Indeed, since 1994, much of the central earmarked transfers targeted the poverty-stricken rural areas and some directly went to China’s rural poverty alleviation programmes.

Even though in this period the earmarked transfers aimed to alleviate rural poverty and urban–rural disparity, they did not seem to work particularly well. Before the early 2000s when local revenue and general transfers were not sufficient to meet the salary and operating costs of an expanding bureaucracy, the earmarked funds could be easily diverted away from their designated purposes (Sina Finance News, 2000). The diversion of earmarked funds was also closely related to local corruption when officials pursued illegal gains by appropriating funds to selected groups (Liu et al., 2009).

Aware of the serious diversion and in response to complaints about the lack of basic public goods at the local level, in the early 2000s the centre raised general transfers to equalise fiscal spending and to reduce local incentives to divert earmarked funds for administrative expenses. The 2002–2003 reform helped to strengthen central fiscal capacity and could now significantly increase the underfunded general transfers to reduce local diversion incentives. Since 2002, the centre has also adopted serious measures to address the issue of earmarked fund diversion. In a bid to increase local government accountability in ways that would improve the usage of some types of earmarked funds, the Ministry of Finance has required that county bureaus of finance establish designated accounts that are subjected to tight supervision.

However, even when the new formal regulatory mechanisms were in place, local officials could still adopt informal strategies for coping with the complex mix of burdens, constraints and interests. As shown by Liu et al. (2009), after 2002 the outright diversion of earmarked funds has indeed declined at the county level, but the decline in the diversion rate did not necessarily imply real progress in ensuring that funds are used for their designated purposes. Local government actors could still evade China’s top-down system of policy mandates mainly in two ways: expanding the number of staff and artificially creating budgetary shortfalls in those bureaus that receive subsidies.

As a result, even though the significant increase of general transfers would presumably help to reduce local incentives in earmarked transfer diversion, such diversion could persist but become more implicit. Since general transfers are overwhelmingly used to cover local personnel and administrative costs, their effects presumably are more pro-urban in the Chinese local governance system known for its urban bias. After all, in the absence of electoral accountability, local officials lack incentives to support the poor rural population.

The lack of local incentives to support rural development was reinforced under China’s transfer-based decentralisation. Since more fiscal resources in the localities now originate from central grants, a higher share of local fiscal resources face competition from other localities at the upper level. Local governments would rather make more efforts to compete for such funds by going to the central ministries than to cultivate the local tax base by providing the needed public goods. For example, after the rural tax reform adopted in 2002 and after, the salaries of local officials and staff at the township and village levels were now increasingly paid through taxes on non-agricultural sectors and through transfers from the upper-level governments. Local governments therefore have even fewer incentives to make investments in rural public goods such as water conservancy projects and rural irrigation networks. Even though the central government did increase earmarked transfers for many major water conservancy projects across the country, local governments often did not even bother to pave the last kilometre of irrigation network since they could not benefit from such efforts. This leads to our third and final hypothesis about urban–rural disparity.

H3: When bottom-up political accountability is absent, all else being equal, higher local government revenue by more central transfers would result in a larger local bureaucracy and faster increase in urban salaries but would not help to narrow urban–rural income disparity.

Data sources and empirical strategy

Data sources

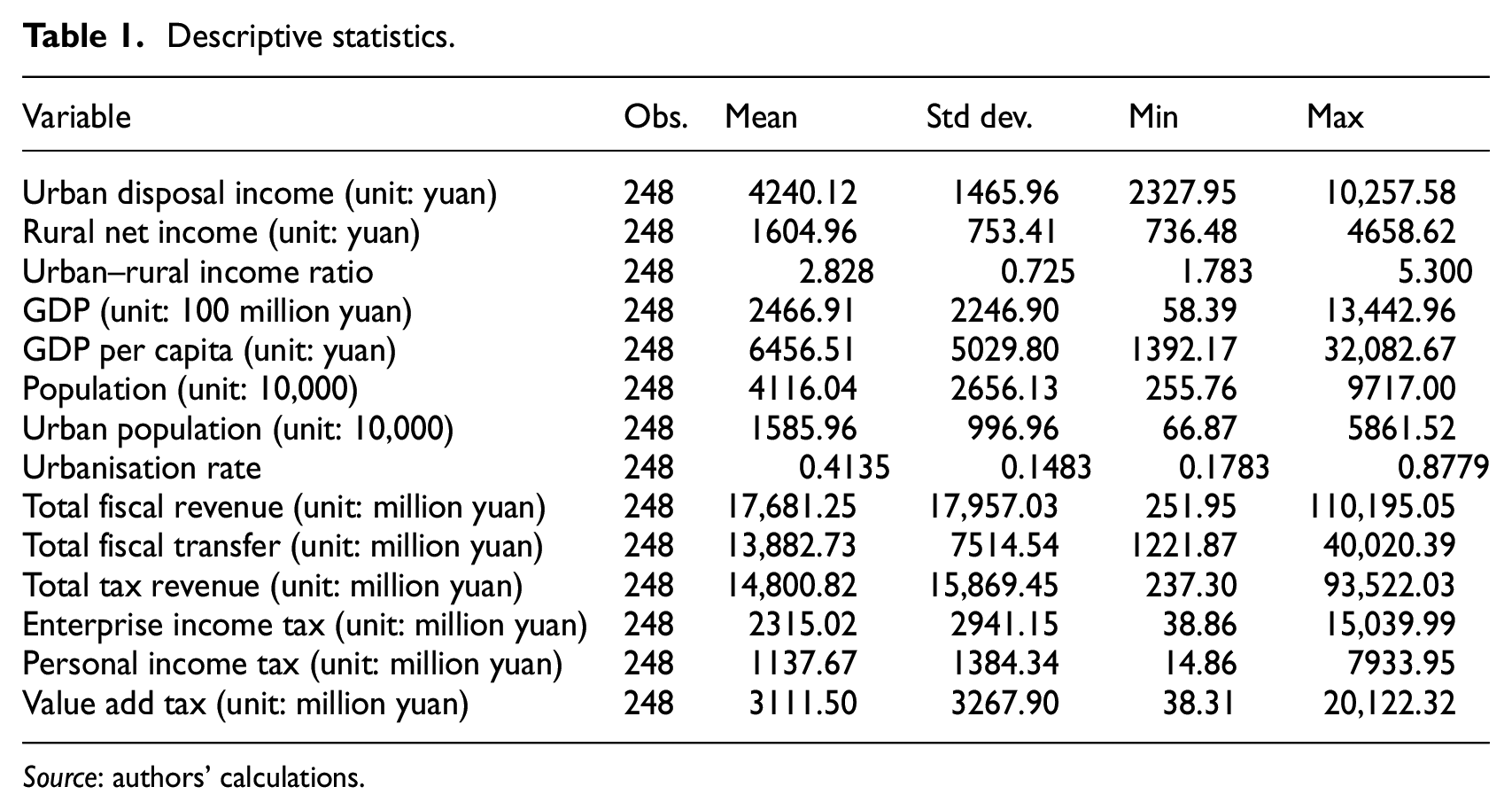

We construct a panel data of 31 provinces over 8 years (1999–2006). We choose province as the unit of observation since the tax-sharing rate change in 2002 and 2003 was between the Chinese central and the provincial governments. We cover the period between 1999 and 2006 because 1999 is the first year the income tax data used to construct our IV was available at the provincial level. Our data come from three separate sources. First, the provincial-level disposable income data comes from the CEIC database, an online database gathering data from various issues of national and provincial yearbooks. In China, disposable income statistics are available at the provincial level for both urban and rural residents, known as the per capita disposable income for urban households and the per capita rural net income for rural households, respectively. Second, data on various types of government fiscal transfers are collected from provincial annual budget reports. Third, detailed provincial-level economic and demographic information is from Sixty Year Statistics. All income, GDP and revenue data have been adjusted in real terms (1992 as the basis year). Descriptive statistics for all variables are summarised in Table 1.

Descriptive statistics.

Source: authors’ calculations.

Empirical strategy

Our goal is to measure the impact of a change in tax-sharing regime on growth, interregional inequality and urban–rural disparity. For ease of exposition, the budget constraint of local government can be written as follows:

where R is total fiscal revenue, I is intergovernmental transfer from the central government, P is total tax revenue, and

where

Note that

Eq. (4) explains how a tax-regime change

where

The panel nature allows us to use the first-difference estimator and therefore control for time-invariant characteristics that may affect the outcome variables. However, the term capturing the tax-sharing rate change

Following Gruber and Saez (2002), we turn to the simulated instrumental variable approach to address the endogeneity concern. To construct instrumental variables for the two endogenous variables, we exploit the exogenous changes in the central–local sharing schedule independent of local characteristics. Gruber and Saez (2002) build the instruments by computing

The natural instrument for

Similarly,

When we use instruments as enumerated above, the coefficients for

While this approach indeed provides us with an exogenous instrumental variable, another empirical challenge of weak instrument may arise. When a tax regime changes significantly across years, the simulated instrumental variable could be weak in predicting the real changes in tax revenues (Blomquist and Selin, 2010). Moreover, it also overlooks the time trend of fiscal revenue changes that may worsen the issue of a weak instrument (Dahl and Lochner, 2012). In order to address the problem, we use the average income of year t−1 and year t to construct the simulated instrumental variables. This approach takes into account the time trend of local income and is still valid in terms of the exogeneity assumption

Finally, for the simulated instrumental variable to be exogenous,

Empirical results

Basic results

In this section, we first discuss our estimation results on local economic growth. We then turn to independent variables that measure interregional and urban–rural inequality. Finally, we estimate a number of different specifications to establish the robustness of our findings.

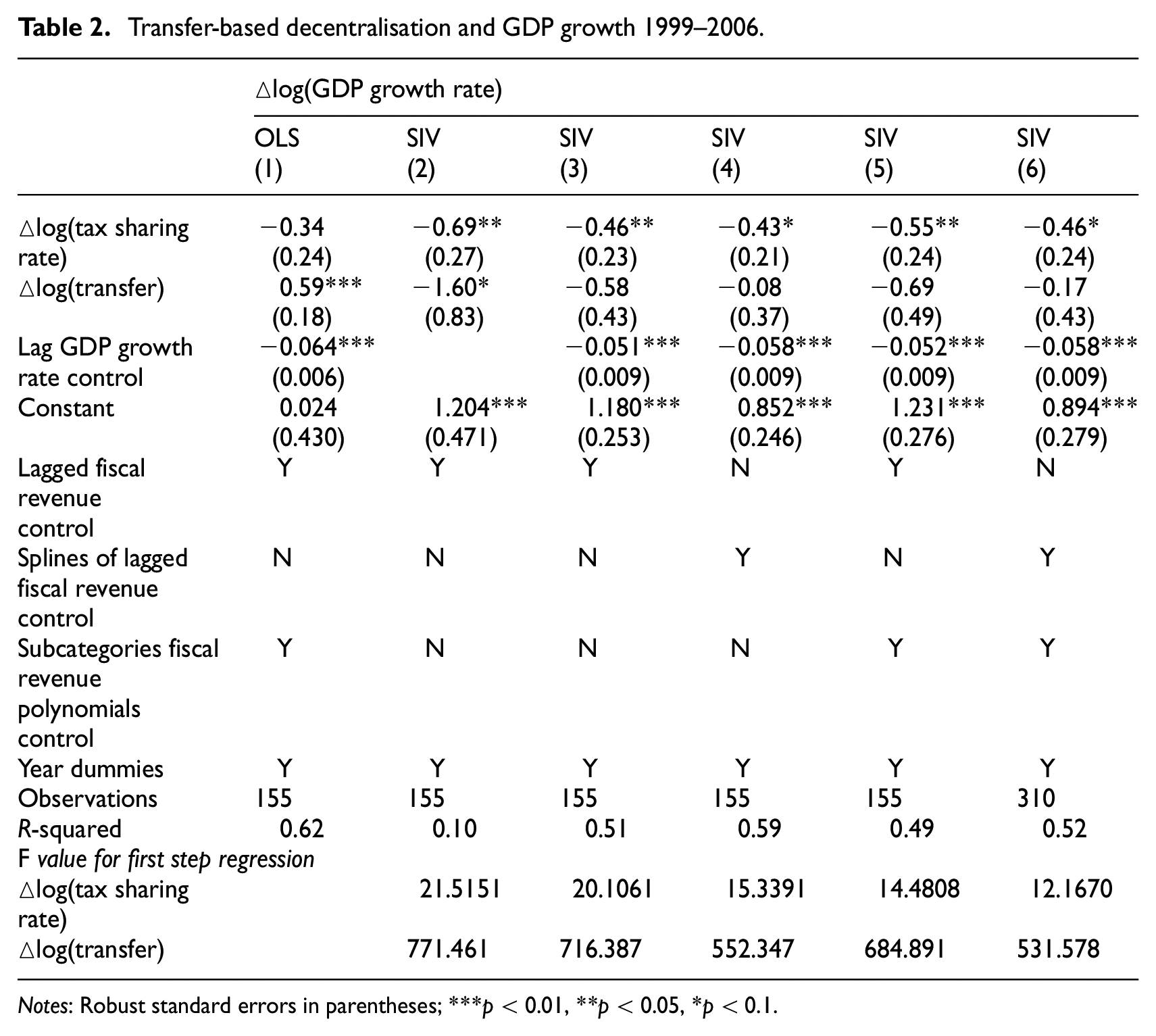

Table 2 shows the OLS and SIV results from our baseline model estimating the impact of tax-sharing reform on GDP growth rate. Because of limitations of space, we only report the F-value for the first stage regressions. As shown in the tables, the F-values for the first stage pass the rule-of-thumb F > 10 very well, indicating that our IVs are strong enough in terms of prediction power. The first column presents the OLS results. Column (2) shows the SIV estimations from the most parsimonious specification that only controls for year dummies. In column (3), we add lagged GDP growth rate, polynomials of lagged per capita fiscal revenue and its subcategories, and a set of other control variables. The results show that a higher central tax-sharing rate did significantly lower growth rate at the provincial level. Indeed, the higher central tax sharing rate reduces local government incentive to promote economic growth as local authorities benefit less from such growth. The results remain robust across different specifications. The SIV regressions in column (1) also show higher revenues from fiscal transfers significantly increase local growth rate. However, this effect either turned negative (column 2) or plainly vanished (columns 3–6) after we controlled for endogeneity.

Transfer-based decentralisation and GDP growth 1999–2006.

Notes: Robust standard errors in parentheses; ***p < 0.01, **p < 0.05, *p < 0.1.

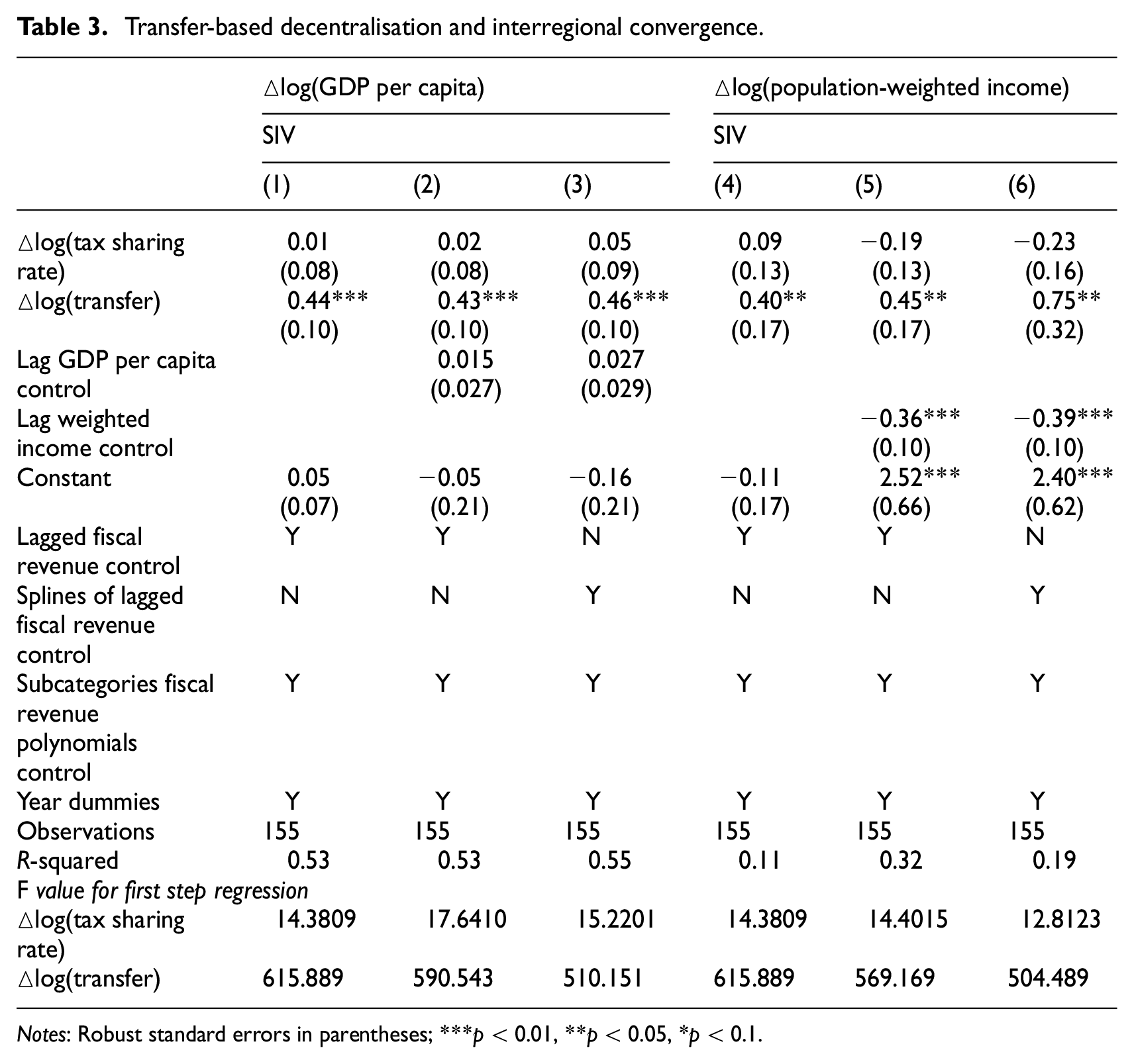

Now we examine the convergence hypothesis. Table 3 reports the results estimating the effects of the 2002–2003 tax reform on local GDP per capita and local income per capita. The latter is computed by averaging urban disposable income and rural net income weighted by provincial urban and rural populations. The results suggest that higher local revenue in the form of intergovernmental transfers led to higher GDP and income per capita. Since after the 2002–2003 tax-sharing reform more transfers went to poorer provinces in central and western China (Table 2), the poorer areas have become increasingly transfer-dependent. Indeed, transfers are found to be equalising across regions and helped to reduce interregional inequality in per capita GDP and income. The results are insensitive to the inclusion of more controls.

Transfer-based decentralisation and interregional convergence.

Notes: Robust standard errors in parentheses; ***p < 0.01, **p < 0.05, *p < 0.1.

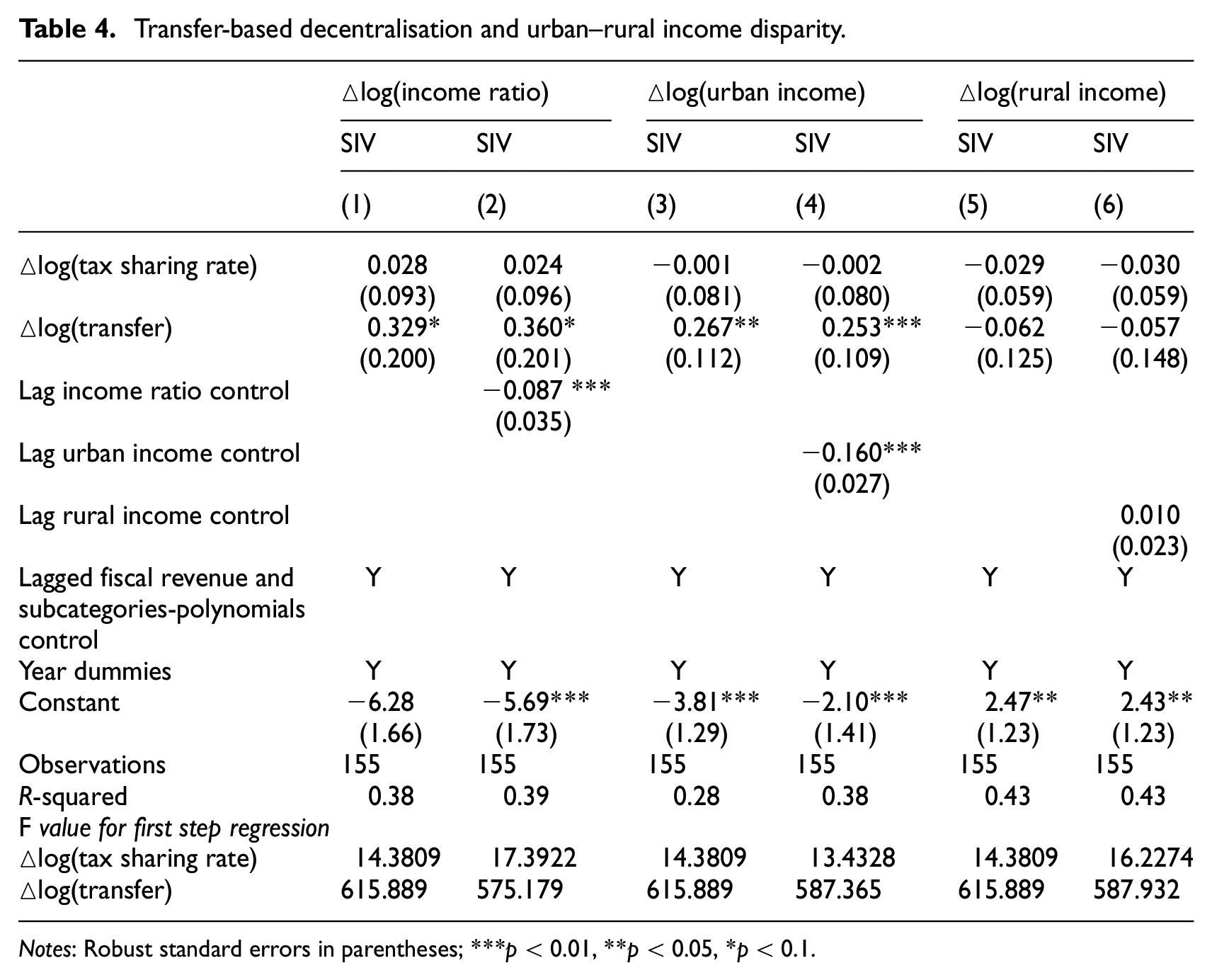

Finally, Table 4 presents the SIV results estimating the effects of 2002–2003 tax-sharing reform on urban–rural income ratio as well as per capita urban disposal income and rural net income.

Transfer-based decentralisation and urban–rural income disparity.

Notes: Robust standard errors in parentheses; ***p < 0.01, **p < 0.05, *p < 0.1.

The coefficients for the change in per capita transfer in columns (1) and (2) are positive and statistically significant, indicating that more central transfers led to higher urban–rural disparity. Furthermore, the transfers only contributed to an increase in the urban income while having no statistically significant effect on the rural income (columns 3, 4 for urban income and 5, 6 for rural income, respectively). Therefore, there were two undesired effects of the 2002–2003 reform. First, even though the centre increased transfers as a means of reducing urban–rural disparity, such transfers mainly benefited urban residents. Second, when local governments have less autonomy on tax revenue, they have even fewer incentives to serve the relatively poor rural population who contribute less to the local budget after the reform.

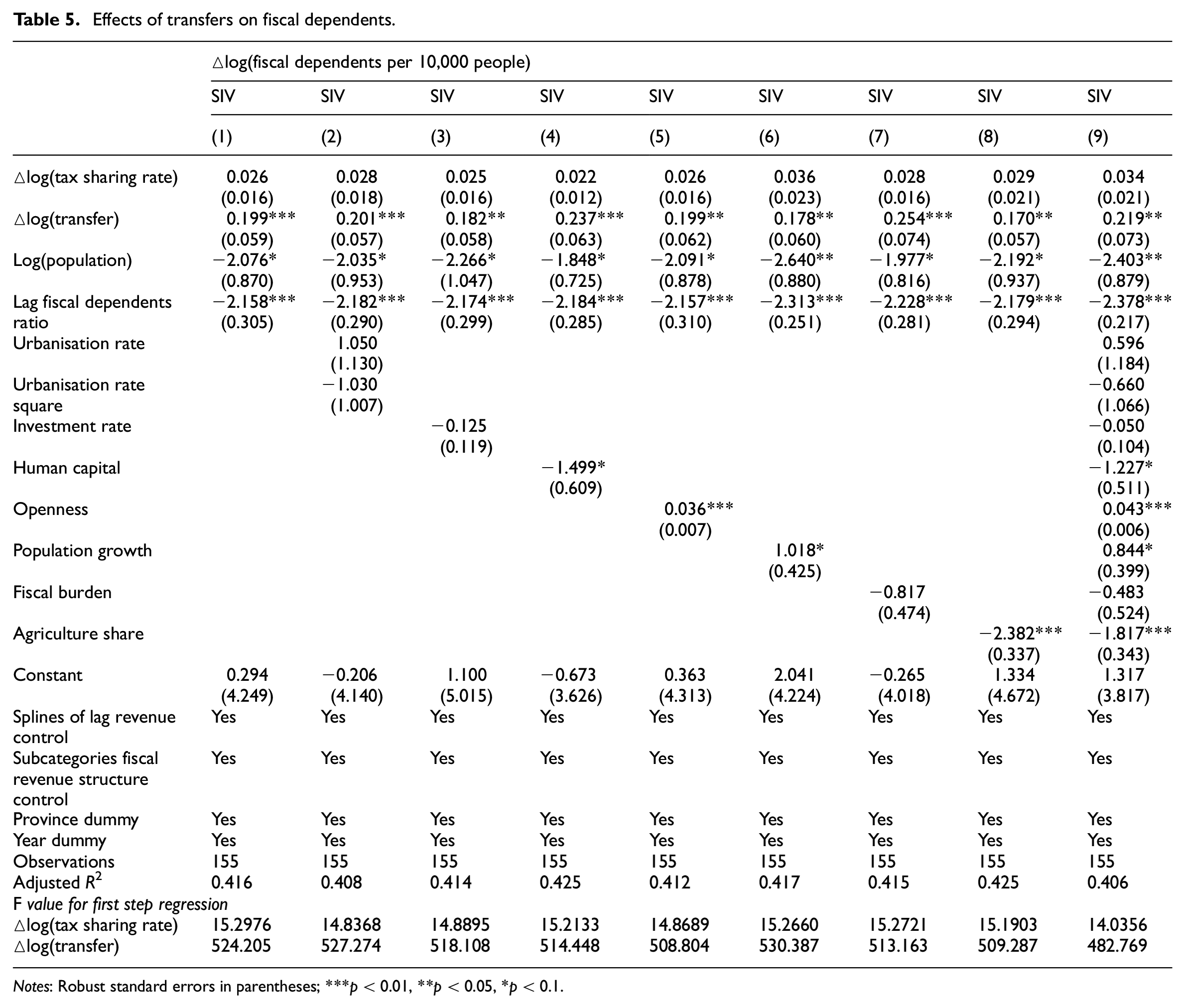

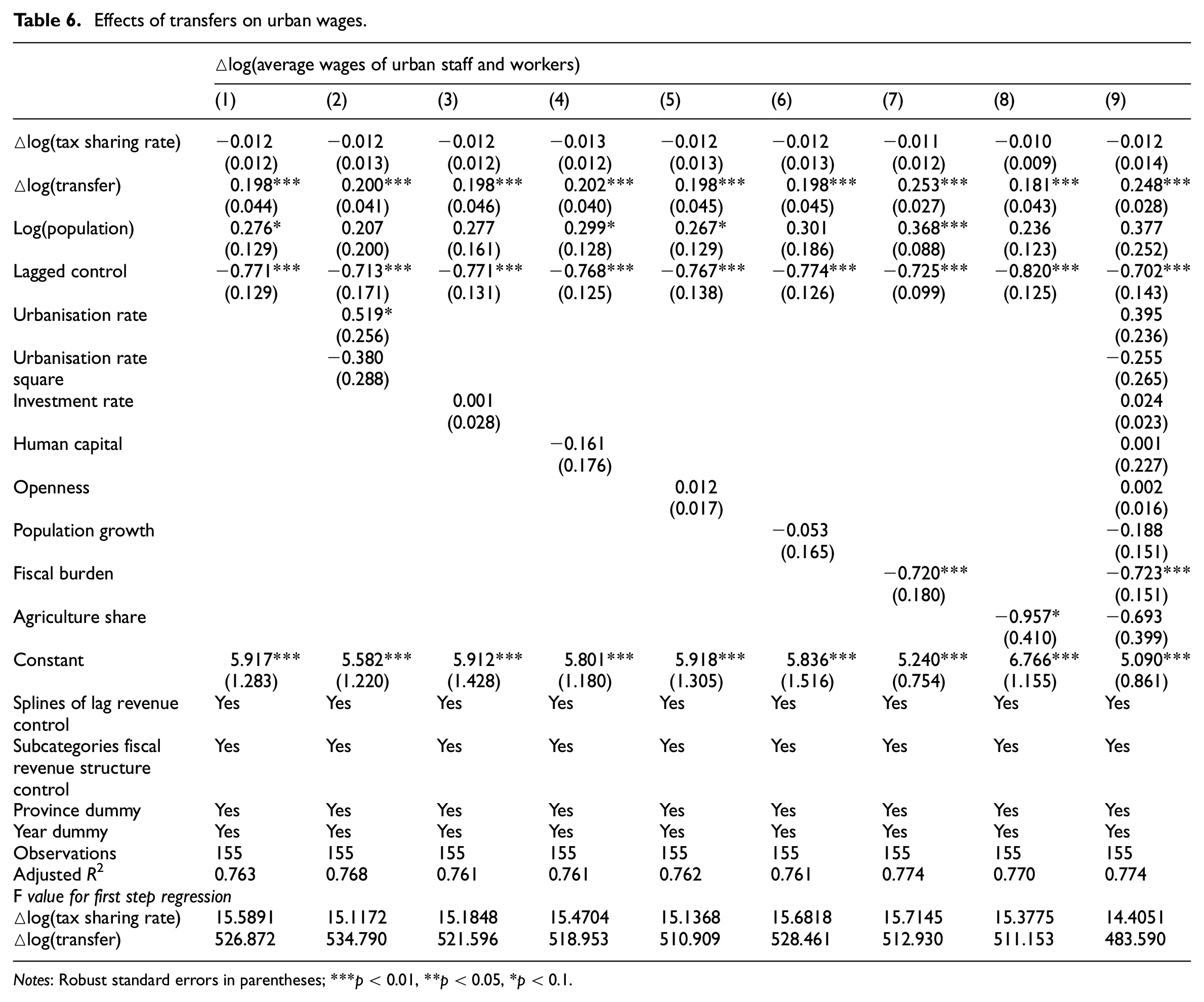

To further test our hypothesis that this enlarged urban–rural disparity is due to the lack of local accountability, we run some further SIV regressions to examine the effects of central transfers on the number of fiscal dependents (public employees in local government agencies and public service units) per 10,000 population, the per capita wage of urban staff and workers, as well as the per capita income of rural residents. As shown in Tables 5 and 6, such transfers increase the first two variables significantly but have no effect on the third one.

Effects of transfers on fiscal dependents.

Notes: Robust standard errors in parentheses; ***p < 0.01, **p < 0.05, *p < 0.1.

Effects of transfers on urban wages.

Notes: Robust standard errors in parentheses; ***p < 0.01, **p < 0.05, *p < 0.1.

Finally, we also re-estimate the same regressions in Tables 2, 3 and 4 with data between 2000 and 2005 and data between 1999 and for later years (2007, 2008, 2009 and even 2010). The empirical results are robust for different periods under investigation. Moreover, as we have multiple outcome variables, there may be a problem if these different regressions are correlated. To address this issue, we further conduct more multi-variable regressions which allow for the outcome variables to be correlated. We choose the simultaneous equations model (3SLS method) to re-estimate our coefficients of interest. The results are very robust to these different empirical models.

Controlling for time-varying income distribution changes

Even with the more flexible model specification, we still rely on a crucial identifying assumption that the problems of mean reversion and serial correlation are not changing year-to-year in a way that is correlated with the year-specific changes in tax policy. However, as transfer could be highly non-stationary, the assumption is unlikely to hold. Some specification tests are needed to show that this assumption is robust.

Following Gruber and Saez (2002), we consider two alternatives. We first allow for a linear time trend in the lagged per capita fiscal revenue. This allows for some relationship between

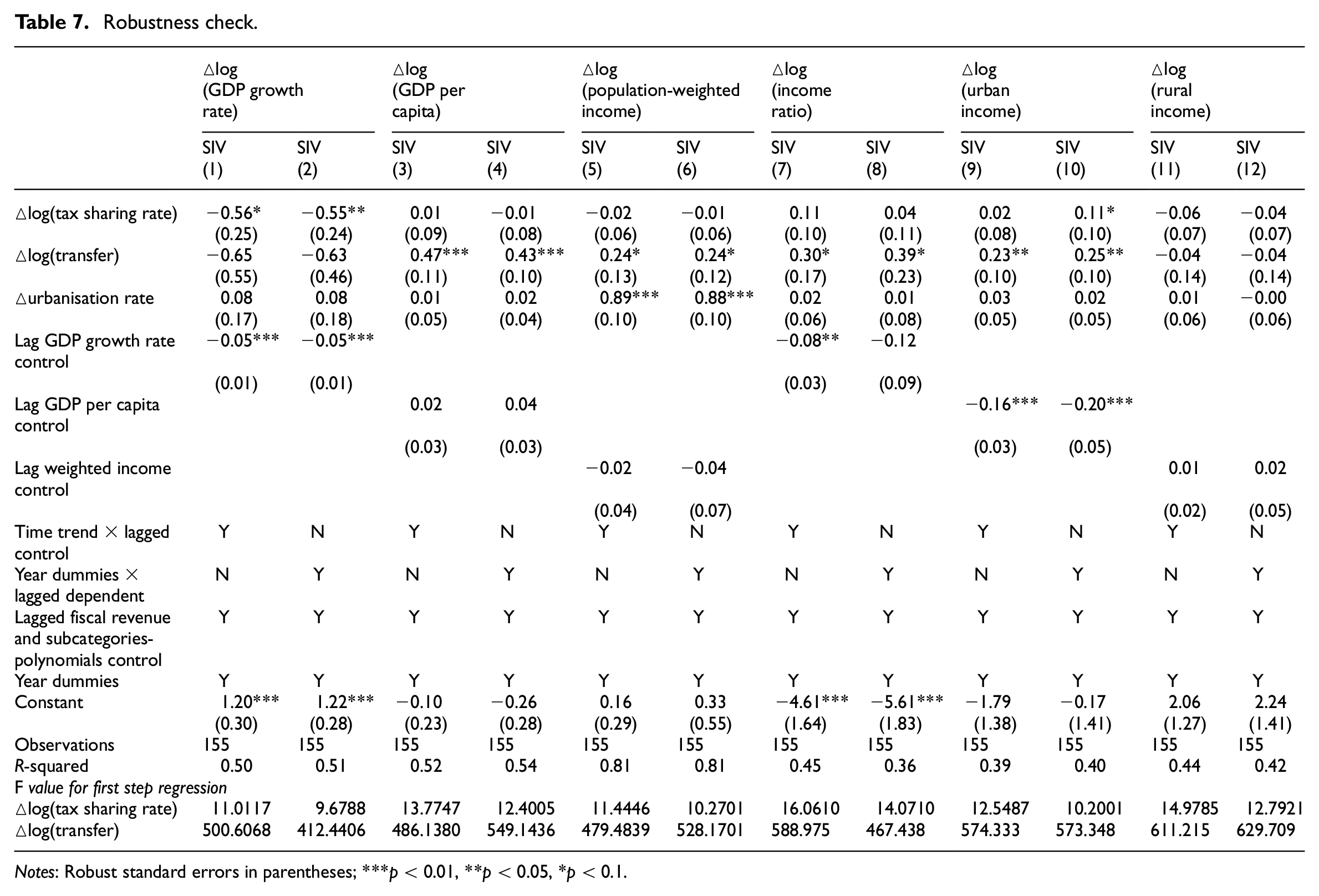

Robustness check.

Notes: Robust standard errors in parentheses; ***p < 0.01, **p < 0.05, *p < 0.1.

As shown in Table 7, the estimations are quite robust to adding these controls. The standard errors rise somewhat, but in both cases the key coefficients are largely unchanged compared with the results presented in Tables 3 and 4. This suggests that the changes in the relationship between

Conclusion

In addressing the serious issues of interregional inequality and urban–rural disparity, the Chinese government since the mid-1990s has relied on a transfer-based decentralisation scheme by centralising revenue, providing more transfers as well as strengthening the supervision of earmarked transfers. These moves made by the Chinese central government are designed to promote more effective fiscal functioning, whilst sidestepping fundamental reforms of local political institutions to strengthen bottom-up accountability.

Our research shows that lower local revenue share after the 2002–2003 reform did have a disincentivising effect and lowered economic growth. At the same time, higher central transfers to less developed regions resulted in per capita GDP and per capita income convergence across regions and thus helped to reduce interregional inequality. However, such convergence was largely an urban phenomenon. Even though promoting rural income growth was one of the key goals of the 2002–2003 tax-sharing reform, intergovernmental transfers aiming to promote rural development did not seem to benefit the rural population relative to their urban counterpart. As a matter of fact, such transfers further exacerbated the already large urban–rural divide. In other words, more reliance on transfers actually strengthened the already serious urban bias in China when bottom-up accountability was absent.

This research reminds us that to avoid the outcome of worse growth outcomes without improving income distribution, expenditure decentralisation should go hand in hand with revenue decentralisation so as to strengthen local government accountability. Moreover, fiscal decentralisation needs to be coupled with political decentralisation, that is, strengthening bottom-up accountability in the form of building local democracy.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research has received generous financial support from the National Science Foundation of China (grant numbers 71533007); and the National Social Science Foundation of China (grant numbers 413227047203).