Abstract

Recent research into the dynamic adjustment of prices within the London housing market is extended via the application of a novel two-step procedure. Combining the non-parametric analysis of the ranking distributions of the levels and changes in house prices with the application of a cross-sectional convergence technique results in the detection of a three-tier system in which highly significant convergence clubs are identified within borough-level data. These findings contrast with both the divergence apparent when considering all boroughs and the failure of previous research to identify convergent groupings. The novelty of the empirical methods is supplemented by a discussion of various theoretical factors such as gentrification, displaced demand, immigration, foreign investment and criminal activity in relation to the findings obtained.

Introduction

Recent decades have witnessed the emergence of a vast literature examining the properties and nature of housing markets. This wealth of research is unsurprising in light of the variety of factors illustrating the importance of housing, including: the substantial contribution of housing to personal wealth; the role of housing in the macroeconomy; the interaction between housing and economic fundamentals; and the increased importance of housing, relative to the stock market, to consumption decisions (Bayer et al., 2010; Brueckner, 1997; Case et al., 2013; Costello et al., 2011; Gallin, 2006; Goetzmann, 1993; Goodhart and Hoffman, 2007; Han, 2013; Holly and Jones, 1997). Considering the UK, despite important early empirical analyses at a national level (see, inter alia, Hendry, 1984; Nellis and Longbottom, 1981), arguably the most prominent theme of this research involves examination of the dynamic adjustment of, and interrelationships between, regional house price series. At the heart of this work is the analysis of the ripple effect hypothesis under which changes in house prices are observed firstly in London before being witnessed in other regions. From early studies such as Guissani and Hadjimatheou (1991), MacDonald and Taylor (1993), Alexander and Barrow (1994) through to Hudson et al. (2018), this hypothesis has received extensive attention, with a variety of methods employed to determine the presence and nature of this diffusion mechanism. However, an interesting development of this regional analysis is provided by the work of Abbott and De Vita (2012), hereafter referred to as ADV, in which dynamic adjustment has been considered at a yet more disaggregated level via a borough-level examination of the London market. 1 In addition to its analysis of an unquestionably important market given its size, value 2 and position at the heart of the ripple effect, the work of ADV provides a highly quantitative supplement to the more discursive analysis of the London market provided by Hamnett (2009a, 2009b) and Slater (2009).

It is the analysis of ADV and its inference of limited convergence within the London market which provide the motivation for the present study. To explore convergence within the London market, ADV employed the pairwise unit root-based approach of Pesaran (2007). While providing useful information on the dynamic adjustment of prices, this prompts two issues for further consideration. First, as the analysis of stochastic convergence using unit root testing requires longer spans of data, its suitability for the present study can be questioned, as observations on prices at the level of disaggregation considered are available from 1995 only. Second, the analysis of ADV does not directly focus upon the identification of groupings of regions. Instead, all possible pairings of boroughs are examined and, although various collections of these pairs are considered as specific groupings within the overall market, these subgroupings are taken from the GLAEconomics (2004) report rather than arising as a result of their creation via detailed analysis. That is, the groupings are imposed exogenously, rather than being endogenously determined via the information available. In recognition of these issues, the present study reconsiders the properties of London house prices via an alternative and novel empirical method which exploits the cross-sectional dimension of the borough-level data to support the identification of potential convergence clubs within the market. Consequently, the present research develops the analysis of ADV, as well as the subsequent work of Holmes et al. (2018) which also applies the pairwise unit root testing to borough-level data without the objective of defining convergence clubs.

To achieve its aims, this article proceeds as follows. Initially, the analysis examines potential convergence in the form

The analysis undertaken is deliberately data-driven, with the intention of extracting information available in the borough-level series to improve understanding of the dynamic adjustment of prices within the London market and the levels at which commonalities and differences exist. This subsequently allows two issues to be addressed. First, the insights obtained can be related to alternative theoretical proposals which have emerged in relation to the London market, such as displaced demand (Hamnett, 2009a), (super-)gentrification (Hamnett, 2009b; Slater, 2009), criminal activity (Gibbons, 2004) and immigration and foreign investment (Badarina and Ramadorai, 2018). Second, the re-examination of convergence within the London market following the alternative methods and objectives present in the studies of ADV and Holmes et al. (2018) addresses the ever-increasing calls for the replication of empirical research emerging in a variety of disciplines by providing, in the terminology of Clemens (2017), a re-analysis of this research.

Reviewing the literature

The analysis of the evolution of regional house prices and their interrelationships has generated a large empirical literature. At the heart of this research is the examination of the notion of a ripple effect, whereby price changes are observed firstly in a leading region before spreading to others. While this hypothesis has been considered for a range of economies, it is arguably the UK which has received the greatest attention, with the proposed transmission of changes in house prices from London to the rest of the UK examined. 3 To explore the existence and nature of this mechanism, a range of alternative techniques have been employed, including causality testing, unit root and cointegration analysis, Kalman filtering, principal component analysis, directional forecasting methods and probability-based convergence techniques, to examine whether London ‘leads’ other regions and, if so, how house prices eventually converge across regions (see, inter alia, Alexander and Barrow, 1994; Ashworth and Parker, 1997; Cook, 2005a, 2005b, 2012; Cook and Watson, 2015; Drake, 1995; Guissani and Hadjimatheou, 1991; Holmans, 1990; Holmes, 2007; Holmes and Grimes, 2008; Hudson et al., 2018; MacDonald and Taylor, 1993; Meen, 1999; Petersen et al., 2002). In recent research, this analysis has been extended by ADV to consider an increased level of disaggregation via a borough-level examination of the London housing market. This extension of the literature to consider a more detailed analysis of the London market is an unquestionably important development. Beyond the value and importance of the London market to the macroeconomy, ADV note also that the examination of its underlying properties is warranted as a result of its role at the heart of the ripple effect and the limited number of studies exploring housing at an intra-regional level. Consequently, there is a clear motivation for studying the nature of price adjustment within the London market. 4

The focus of ADV concerned the extent of convergence between house prices across London boroughs. Using the pairwise unit root approach of Pesaran (2007), ADV examined the possibility that while borough-level house prices might diverge over the short term, they converge to an underlying equilibrium over the longer run. This analysis of stochastic convergence was performed in two stages. In the first stage, an analysis of the full set of boroughs was conducted. This was found to provide little evidence of convergence, as application of the testing procedure under six different testing options resulted in detection of convergence in only 11.93–27.27% of the pairings of boroughs examined. 5 The second stage of the analysis involved the examination of 11 subsets of boroughs, or clubs, identified by GLAEconomics (2004) on the basis of their common characteristics. Again, the results provided limited evidence of convergence aside from a ‘Central’ club involving just four ‘boroughs’ (City of London, Camden, Kensington & Chelsea, City of Westminster). 6 However, even for this group, the results were not overwhelmingly supportive of convergence, as two of the six sets of results detected convergence in only half of the pairings considered. Beyond these findings for the Central Club, other clubs were found to offer very little evidence of significance. For example, only 5.13–12.82% of the pairings within the ‘Crowded House’ club demonstrated convergence, depending on the variant of the unit root testing employed. In summary, the analysis found varying but limited evidence of convergence both across the whole market and within alternative clubs. However, the analysis undertaken can be reconsidered, since the unit root-based method adopted by ADV requires a long span, or calendar period, of data to be employed to examine stochastic convergence. 7 Consequently the suitability of this approach can be questioned for the short span of data (1995–2009) examined by ADV. The subsequent research of Holmes et al. (2018) develops the analysis of the London market via consideration of further disaggregation by property type (detached, semi-detached and terraced houses, along with flats). Using both Pesaran’s (2007) approach to pairwise analysis of stochastic convergence and probit analysis, this research produces some interesting findings, including the increased convergence apparent for more expensive (detached, semi-detached) properties and the impact of travel options, crime and schooling. However, like ADV, this analysis does not seek to identify convergence clubs, and the consideration of convergence is again based on the use of unit root testing and hence is subject to the concerns raised previously concerning the time series dimension of the data considered.

In recognition of the issues discussed in relation to previous research, the present study explores the convergence and distribution of borough-level house prices using an alternative novel approach which exploits the cross-sectional dimension of the data under examination. This analysis takes the form of a two-step procedure involving the analysis of the ranking distributions of house prices

In the process of providing a more detailed examination of the distribution of, and relationships between, house prices within the London market, the current ana-lysis supports a large and evolving ‘replication’ literature questioning the robustness of empirical findings and encouraging re-examination of previous studies. While perhaps most closely associated with the ‘replication crisis’ in psychology (see Open Science Collaboration, 2015), calls for replication have been witnessed in numerous disciplines (see, inter alia, Chang et al., 2017; Frank and Saxe, 2012; Makel and Plucker, 2014; McNeeley and Warner, 2015; Sukhtankar, 2017; Winfree, 2010). The prominence of this issue is reflected also in journal policies towards replication (Hoffler, 2017), with the emergence of associated data repositories and special editions dedicated to this topic (for example, Energy Economics and International Review of Law and Economics). Employing the ‘replication’ terminology of Clemens (2017), the present study provides a re-analysis of ADV as a result of the application of alternative empirical methods over an extended sample period. Importantly, this re-analysis proves informative by extending the findings of earlier research.

Data and initial analysis of convergence

The data employed in the present analysis are annual observations on median house prices for the 32 boroughs of Greater London over the period 1995 to 2016. In addition to covering a longer period than that considered by ADV, the data employed differ also in terms of their frequency. While data at a quarterly frequency as examined by ADV are available, these are calculated in a rolling year format, with the values presented providing information on house prices over a year to the relevant quarter. As a consequence of this moving average feature with events in a particular period included in a number of observations, annual data are instead employed in the present study. The house price data for all boroughs are presented in Figures 1 and 2. 8

London house prices.

London house prices.

Examination of these figures suggests a certain rigidity in house prices with, for example, house prices in Kensington & Chelsea, City of Westminster, Camden, Hammersmith & Fulham, Islington, Richmond upon Thames and Wandsworth consistently high relative to other boroughs. However, series being consistently high (or low) relative to others obviously does not preclude the existence of convergence, as it may be that the distribution is narrowing. To explore potential

where

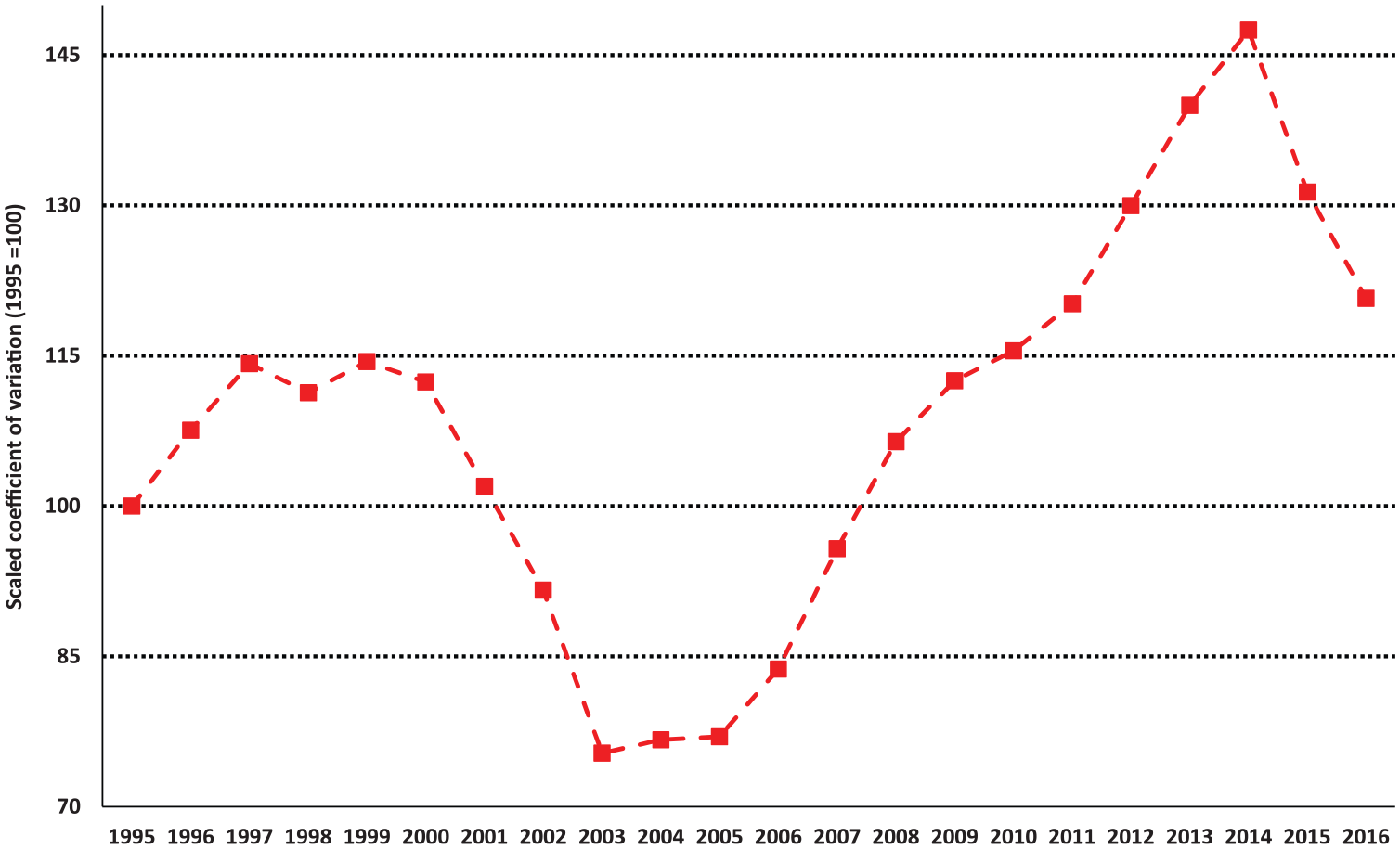

Sigma convergence across all boroughs.

Ranking distributions and convergence clubs

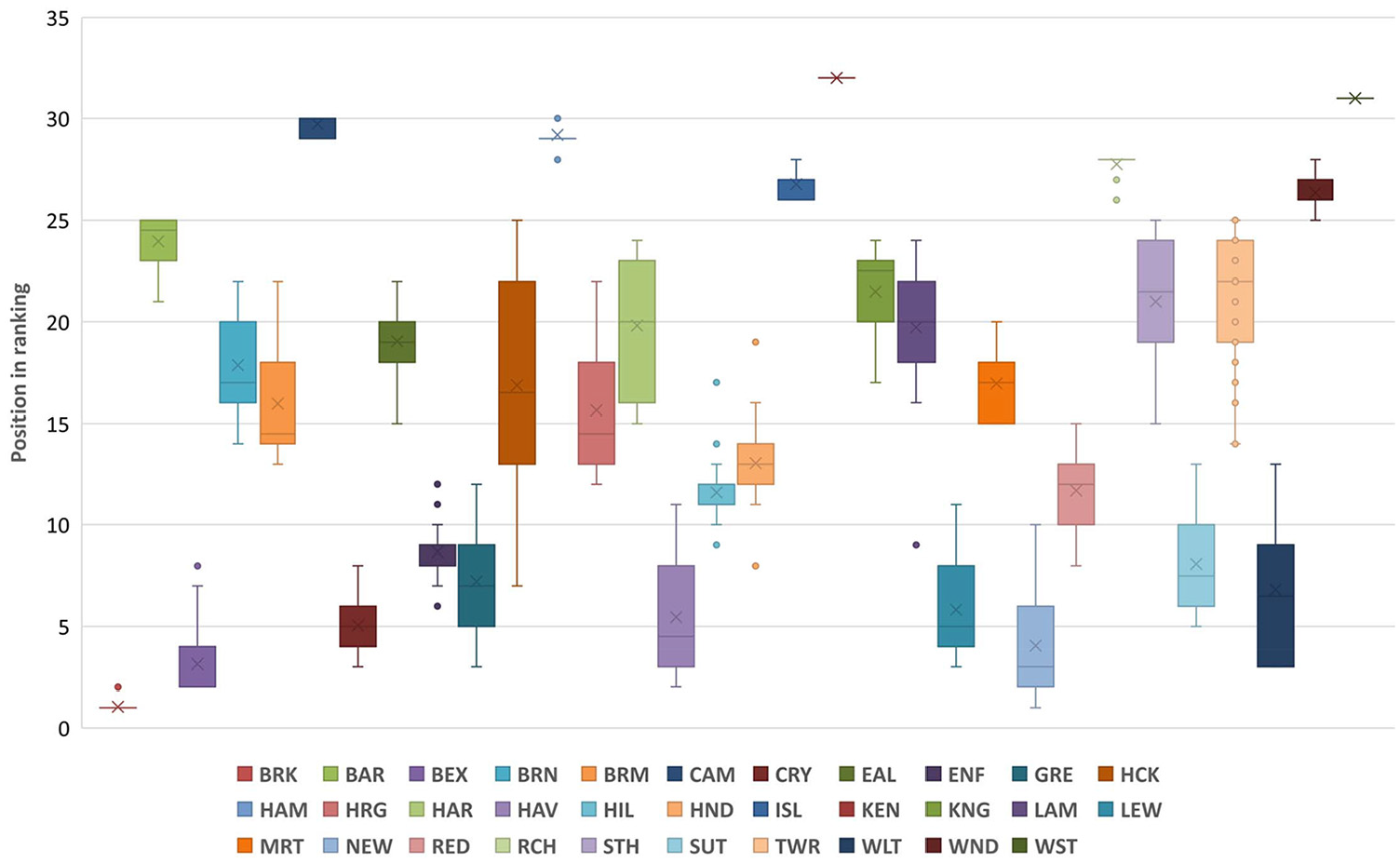

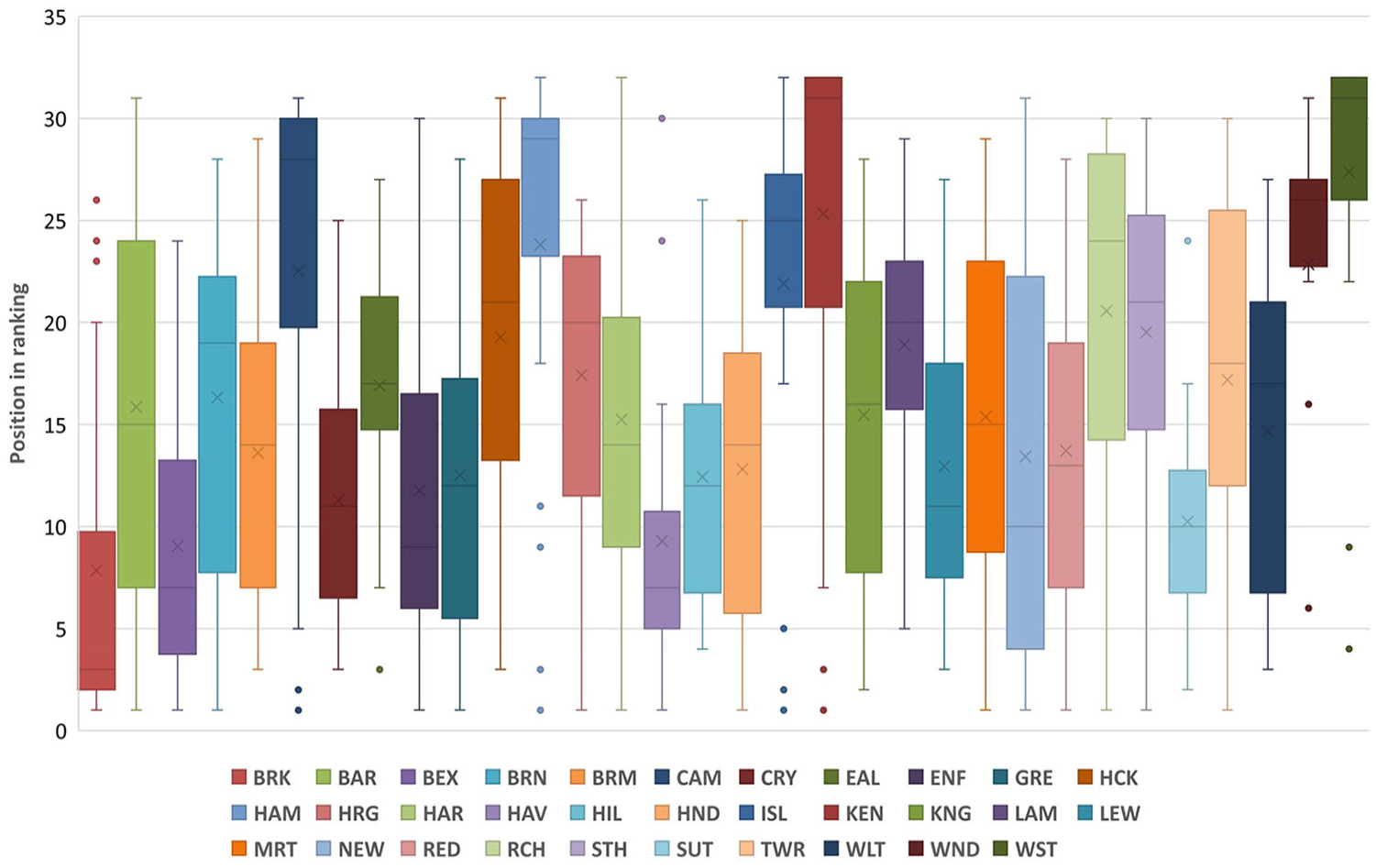

The line graphs presented in Figures 1 and 2 provide a degree of information on the evolution of house prices across boroughs. However, further information on this and the relativities between boroughs is available via consideration of the ranking distribution of house prices. In addition, given the current focus on convergence, it is not just the levels of house prices that are informative, but also their changes. Table 1 provides summary information on the rankings of boroughs according to

where

Mean rankings for house prices and changes in house prices.

Notes: The above figures represent average rankings across the full sample for the house prices and changes in house prices.

While the Friedman test results indicate marked differences in the ranking of boroughs with regard to

Distribution of rankings of house prices across boroughs.

Distribution of rankings of house price changes across boroughs.

In combination, Figures 4 and 5 indicate a degree of commonality with regard to movements in

where

Joint rejections under the Nemenyi Test.

Notes: The figures in parentheses denote the number of boroughs for which the Nemenyi test rejects the null for both house prices and their changes, with L/H denoting whether these boroughs are lower/higher in the ranking distribution. For example, ‘City of Westminster (16L)’ denotes that the null of equal population means of both prices and changes in prices is rejected for Westminster in comparison with 16 boroughs which have lower rankings.

The results provided in Table 2 lead to the three-tier collection of convergence clubs below: Top Tier: Camden, Hackney, Hammersmith & Fulham, Islington, Lambeth, Richmond upon Thames, Southwark, Wandsworth. Middle Tier: Barnet, Brent, Ealing, Haringey, Kingston upon Thames, Tower Hamlets. Lowest Tier: Bexley, Bromley, Croydon, Enfield, Greenwich, Harrow, Havering, Hillingdon, Hounslow, Lewisham, Merton, Newham, Redbridge, Sutton, Waltham Forest.

To examine whether these potential convergence clubs do actually exhibit convergence,

Sigma convergence.

Considering convergence results

The above analysis has led to the detection of a three-tier system, displaying clear convergence in house prices. While this has been a primarily empirical exercise designed to exploit information in borough-level house price data for the purpose of assessing submarket convergence, potential factors underlying the existence of the identified clubs can be considered.

Before discussing various theoretical proposals concerning the evolution of borough-level house prices, Figure 7 is presented to provide a visual representation of the three-tier system. 11 Two issues are immediately apparent from inspection of this figure. First, there is a clear Inner/Outer London dimension to the results, which arises from the Top Tier convergence club being dominated by Inner London boroughs and the Lowest Tier being dominated by Outer London boroughs. However, the use of the word ‘dominated’ is important, as these tiers are not exclusively populated by either Inner or Outer boroughs, with Richmond upon Thames (Outer London) appearing in the Top Tier, and Lewisham and Greenwich (both Inner London) occupying positions in the Lowest Tier. The second feature illustrated by Figure 7 is the contiguous nature of boroughs within the specified groupings. While the Top Tier grouping is clustered around the elite pairing of Kensington & Chelsea and City of Westminster, the Lowest Tier is spread around the outside of Greater London. The Middle Tier is predominantly a grouping to the north-west of central London, with the exceptions of Kingston upon Thames and Tower Hamlets to the south-west and east respectively. However, in all cases, the Middle Tier boroughs border Top Tier boroughs.

London convergence clubs.

Considering the geographical issues raised above, the displacement demand effect proposed by Hamnett (2009a) in relation to East London boroughs receives mixed support from the ranking distributions and the identified convergence clubs. While Hackney and Tower Hamlets have experienced rapid house price increases, Barking & Dagenham has seen its median price move from £29,691 below the average across the 31 other boroughs at the start of the sample to £208,158 below this average by the end of the sample. Similarly, evidence of a displaced demand effect influencing other East London boroughs is not apparent. Indeed, it could be argued that where evidence of displaced demand from the centre does occur, it takes the form of a north-westerly movement illustrated by the identified Middle Tier. An issue to consider here is that where references have been in previous research to higher percentage growth rates in lower priced areas, this obviously does not ensure actual convergence. As a simple example, a 10% growth rate in a lower priced Area A and 5% growth rate in a higher priced Area B will actually lead to a widening of the price gap if the initial prices were £100,000 and £300,000 respectively, as the gap will increase from £200,000 to £205,000. Higher growth rates for some boroughs have been discussed previously in the literature, but clearly that cannot be taken to automatically imply convergence in the sense of closing the actual gap between prices. 12

With regard to the proposed effects of gentrification and right-to-buy policies, these are reflected in the detected convergence clubs, with, for example, the ‘super-gentrified’ Islington (Butler and Lees, 2006) and the boroughs typically considered to exemplify right-to-buy (Wandsworth and City of Westminster) appearing in the Top Tier or elite grouping. Beyond the identified linkages to an Inner/Outer London geographical factor, displaced demand, gentrification and right-to-buy policies, alternative factors can be considered in relation to the convergence clusterings identified. While Gibbons (2004) has examined the relationship between crime and house prices, its impact is difficult to evaluate in the present circumstances; for example, City of Westminster is the leading borough for crime, yet is in an elite pairing with regard to house prices, and ‘leafy’ lower priced boroughs such as Bromley, Havering, Merton and Sutton are typically very low in the distribution of crime. However, this reflects the myriad of factors impacting upon house prices and their varying effects and relevance across different boroughs. This issue is further illustrated by travel considerations. For example, while a premium is attached to Tube station access, a borough without a single station can appear in a higher Tier than one with numerous stations (e.g. Kingston upon Thames and Newham). Turning to the more recently researched issue of the impact of foreign investment and immigration on London house prices, as considered in Badarina and Ramadorai (2018), there are links of a more direct nature to be established. First, the influx of foreign investment closely corresponds to the identified convergence clubs, with its association with the elite pairing of Kensington & Chelsea and City of Westminster within the London market. Second, a link with immigration is apparent also via the close correspondence between the high levels of immigration in areas associated with the Middle Tier of convergence clubs identified to the north-west of central London.

Concluding remarks

The above analysis has extended recent research into price adjustment within the London housing market via the application of a novel method combining the analysis of ranking distributions and convergence techniques. The results obtained add to previous studies by detecting submarket groupings of boroughs which exhibit substantial convergence. This contrasts with the findings of previous research which did not seek to establish such convergence clubs and presented limited evidence of convergence across the London market as a whole. With regard to the robustness of the findings obtained, it can be noted that similar results were obtained from an examination of mean, rather than median, house prices. 13

While the identified convergence clubs do not match the ‘Leafy Retreat’, ‘Pleasant Crescent’ etc. groupings of ADV and GLAEconomics (2004), they can be related to various factors concerning displaced demand, gentrification, housing policy, immigration and foreign investment. However, the nature of the impact of these factors is complex and will often impact to different degrees on house price adjustment within a single borough. Consequently, the examination of the exact influence of underlying factors is the subject of future research following the establishment of convergence clusterings and their associated commonalities.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.