Abstract

Massive funds that are necessary to finance China’s capital-intensive urbanisation are channelled through Local Government Financing Vehicles (LGFVs), which are established by local governments to circumvent the prohibition on borrowing. This study examines LGFV development and how this land financing development strategy influences villagers. We argue that China’s discriminatory land property system and the feature of land being a captive asset allow local governments to transfer their debt pressure to land-losing villagers. Specifically, we find that more indebted local governments take a more extractive approach by paying land-losing villagers less compensation, suggesting the intrinsic connections of the local state, land-centred local public finance and society in China’s urban transformation. Our findings suggest that local governments can be developmental and predatory at the same time. Our arguments are developed using data that combine a self-compiled data set on LGFV debt with the China Household Finance Surveys. It systematically examines the connections between land financing via LGFVs and land-losing villagers. It contributes to a better understanding of the debt-fuelled urbanisation in China and, more broadly, of how the state intervenes in the economy and impacts distributive justice in developing and transition economies.

Introduction

Cities, as they accept more inhabitants and expand their boundaries, need to provide a wide range of public infrastructure and services ranging from transportation, water and sanitation to parks and recreation. To maintain existing and deliver new offerings, cities desire to have reliable and sustainable financial sources. The issue of public finance is especially challenging to China for a number of reasons. China’s rapid economic growth has been driven significantly by state-led investment rather than consumption, the growth model being called ‘state capitalism’ or ‘capitalism with Chinese characteristics’ (Huang, 2008). Under the decentralised setting where the responsibilities for policy implementation lie with local governments, the financial burden of supporting state capitalism as well as urbanisation has been passed on to local governments. However, local governments have been fiscally squeezed by the central government (Wong, 2009, 2013; Wong and Bird, 2008). Unlike industrialised countries, where borrowing is widely used as a key method of funding urbanisation, Chinese local governments have been generally forbidden from engaging in direct market borrowing, including bank loans (Lu and Sun, 2013; Wu, 2010; Zhang and Barnett, 2014). How have local governments, which are running budget deficits and are statutorily prohibited from borrowing, funded the capital-intensive urbanisation and development in China? How has this approach impacted ordinary citizens?

One strategy that local governments use is to set up local investment corporations, known as Local Government Financing Vehicles (LGFVs, difang zhengfu rongzi pingtai), and encourage LGFVs to borrow from the financial market. LGFVs serve as the main, but not the only, vehicle for local government borrowing. According to the National Audit Office (NAO) report (2011), local governments had outstanding debts totalling RMB 10.7 trillion by the end of 2010 – the amount equal to 264% of their budget revenue or 27% of GDP in 2010 – of which 46% was channelled through LGFVs. People’s Bank of China (2011) reported that there were about 10,000 LGFVs by the end of 2010, increasing by 25% from 2008. The NAO report (2013) shows that China’s government debt reached RMB 30.27 trillion by June 2013, equivalent to 59% of GDP in 2012, of which 59% came from local governments and the rest from the central government. LGFV debt accounted for 39% of total local government debt, followed by government departments and agencies (23%), state-owned enterprises (18%) and other units (e.g. public service units). Local government debt primarily takes the form of bank loans: bank loans contributed 79% and 57% to the total debt in 2011 and 2013, respectively. Land has been used as collateral to facilitate LGFVs’ borrowing from banks, a process called land financing (tudi rongzi). The NAO reports (2011, 2013) raise concerns about high dependence of local governments on land. Scholars from the International Monetary Fund (IMF) emphasise that the practice of LGFVs augments government debt and deficit problems and potentially increases fiscal vulnerabilities (Lu and Sun, 2013; Zhang and Barnett, 2014).

Our research examines the LGFV development and how this land financing development strategy influences villagers, the original land users. We argue that China’s discriminatory land property system and the feature of land being a captive asset allow local governments to transfer their debt pressure created by LGFVs on to land-losing villagers. Specifically, we find that local governments with more LGFV debt take a more extractive approach by paying land-losing villagers less compensation for taking land. That is, the massive debt-fuelled urbanisation comes at a cost of impoverishing and marginalising land-losing villagers. Our arguments are developed through analysis of a self-compiled data set on LGFV debt combined with the nationally representative China Household Finance Surveys. Our research is also fieldwork based, which helps us formulate our hypothesis and interpret the findings from the quantitative analysis.

Our research first contributes to the growing literature on local public finance and urbanisation in China by focusing on LGFV debt. That Chinese local governments face budget deficits but have to provide massive infrastructure and public services is well known. Existing research highlights that land commodification provides local governments with a source of revenue to overcome the budget shortfall problem (Lin, 2014; Lin and Yi, 2011; Lin and Zhang, 2015; Lin et al., 2015; Rithmire, 2015, 2017; Su and Tao, 2017; Tao et al., 2010; Wu, 2010). Land-generated revenue is important but still insufficient to carry out capital-intensive urban transformation in China. Public borrowing and debt, which are clearly an important aspect of financing urbanisation, have received relatively little attention, partly because government debt data are not publicly available. LGFVs are treated as state-owned enterprises and required to report detailed information about their debt, if issued. This allows us to compile a unique data set on LGFV debt. Given that LGFV debt constitutes the largest component of local government debt, a systematic examination of LGFV debt serves as a window through which we can understand China’s debt-fuelled urbanisation.

Our research from the land financing perspective also illustrates that China’s urbanisation is characterised by what David Harvey (2003) calls ‘accumulation by dispossession’. Existing research concludes that land-losing villagers are generally victims of China’s urbanisation process. This is because the state extracts massive revenue from land sales and sometimes uses coercion to facilitate land expropriation (Hsing, 2006, 2010; Rithmire, 2015; Sargeson, 2013). Informal institutions, such as clans, fail to protect villagers’ land property rights (Mattingly, 2016) and villagers have to use various means (e.g. protests, petition) to resist land expropriation (Heurlin, 2016; O’Brien and Li, 2006; Sargeson, 2012; Whiting, 2011). 1 Our research complements these studies by showing how LGFV debt leads to state predation in distributing land-taking compensation. Our research also represents an effort to take the state–market–society triad analytical perspective, an approach called for in a special issue of Urban Studies (2015, vol 52, issue 15). In this special issue Lin and Zhang (2015) emphasise that ‘[o]nly when the three seemingly separated and yet closely interconnected phenomena of urbanisation, land development and reformed fiscal relations are brought together for investigation can we really understand the changing nature and dynamics of China’s great urban transformation’ (p. 2778). Our analysis, which examines the interconnections of the state, LGFV debt and villagers, provides evidence of this aspect of China’s ongoing urbanisation.

Local governance and finance in China

China features a nested administrative hierarchy that consists of five levels: the centre, province, prefecture, county and township. It is nested because, generally speaking, each level of the government manages administrative units at one level below it within its administrative territory and holds them accountable for performance. Local governments are given significant autonomy to experiment with policy innovations that fit local needs (Heilmann, 2008a, 2008b; Heilmann and Perry, 2011; Montinola et al., 1995; Teets and Hurst, 2015).

The policy decentralisation is combined with personnel and fiscal centralisation that constrains local governments. The nomenklature system that allows the communist party to appoint its hand-picked cadres to take leading positions in the Party and state apparatus remains intact in the reform era (Burns, 1994, 1999; Manion, 1985; Wu, 2012). Leading officials are also evaluated regularly according to a set of performance criteria, known as the target responsibility system (Tsui and Wang, 2004; Whiting, 2000, 2004). The performance evaluation assigns more weight to economic indicators (e.g. GDP growth rate), creating incentives for local officials to promote local economic growth (Landry, 2008). The personnel centralisation induces career-seeking officials to hold upward accountability and act in accordance with the preference of the Party (Wu, 2012). Xu (2011) considers the combination of decentralised economic governance and centralised personnel control, which he referred to as ‘regionally decentralised authoritarian system’, as the fundamental institution underpinning China’s reforms and development.

An important step of fiscal centralisation was implemented through the 1994 Tax Sharing System (TSS). The TSS features a mismatch between revenue and expenditure whereby the reform transferred revenue from local governments to the central government without adjusting expenditure responsibilities. One of the consequences of TSS is that it increased the fiscal capacity of the central government and meanwhile generated a substantial budget deficit for local governments (Wong, 2009, 2013; Wong and Bird, 2008). The abolition of centuries-old agricultural taxes, announced in 2004 and implemented in 2006 as a response to reduce tax and fee burdens on villagers, caused a further decline in local revenue and intensified the deficit problem (Rithmire, 2017). However, the inter-governmental fiscal transfers from the centre to local governments proved be ineffective to solve the budget shortfall problem (Lu and Sun, 2013; Wong and Karplus, 2017; Zhang and Barnett, 2014).

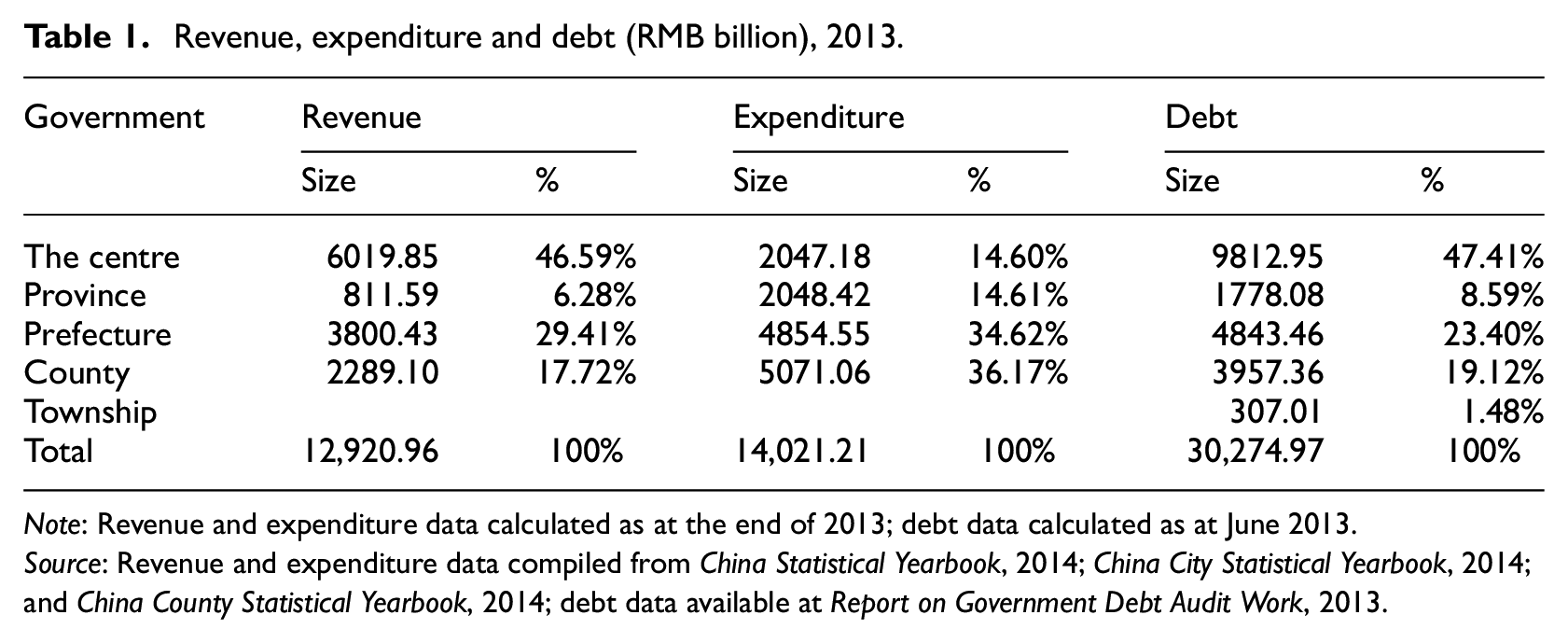

Local governments who have insufficient funds to fulfil the mandates specified in the evaluation system are forced to seek public borrowing. Table 1 shows revenue, expenditure and debt across levels of government. Governments at prefecture level and below collected 47% of total revenue but they were responsible for 71% of total expenditure. While the revenue and expenditure data have been combined for county- and township-level governments because of data availability, almost all public services have been delivered by prefecture- and county-level governments since the early 2000s (Wong and Karplus, 2017). We therefore expect the proportions of both revenue and expenditure for township governments to be small. The revenue–expenditure mismatch creates demand for local governments to borrow. Prefecture- and county-level governments are more indebted than other levels of local government.

Revenue, expenditure and debt (RMB billion), 2013.

Note: Revenue and expenditure data calculated as at the end of 2013; debt data calculated as at June 2013.

Source: Revenue and expenditure data compiled from China Statistical Yearbook, 2014; China City Statistical Yearbook, 2014; and China County Statistical Yearbook, 2014; debt data available at Report on Government Debt Audit Work, 2013.

Land and local government financing vehicles

Land commodification provides local governments with an opportunity to tap into a new source of revenue. Land development generates a variety of direct and indirect taxes and fees, the largest among which is the land transfer fee (LTF, tudi churangjin) – a one-time up-front lump sum payment charged by the state for transferring its long-term land use rights to urban land users. Land-generated revenue serves as the main source of funds for China’s urban maintenance, construction and development (Lin, 2014; Lin and Zhang, 2015; Lin et al., 2015; Su and Tao, 2017; Wu, 2010). New terms were coined to capture the critical roles that land plays in financing the local economic development, including, for example, ‘land fiscialisation’ (tudi caizheng), ‘landed urbanisation’ (Lin, 2014) and ‘land-based municipal finance’ (Lin and Zhang, 2015).

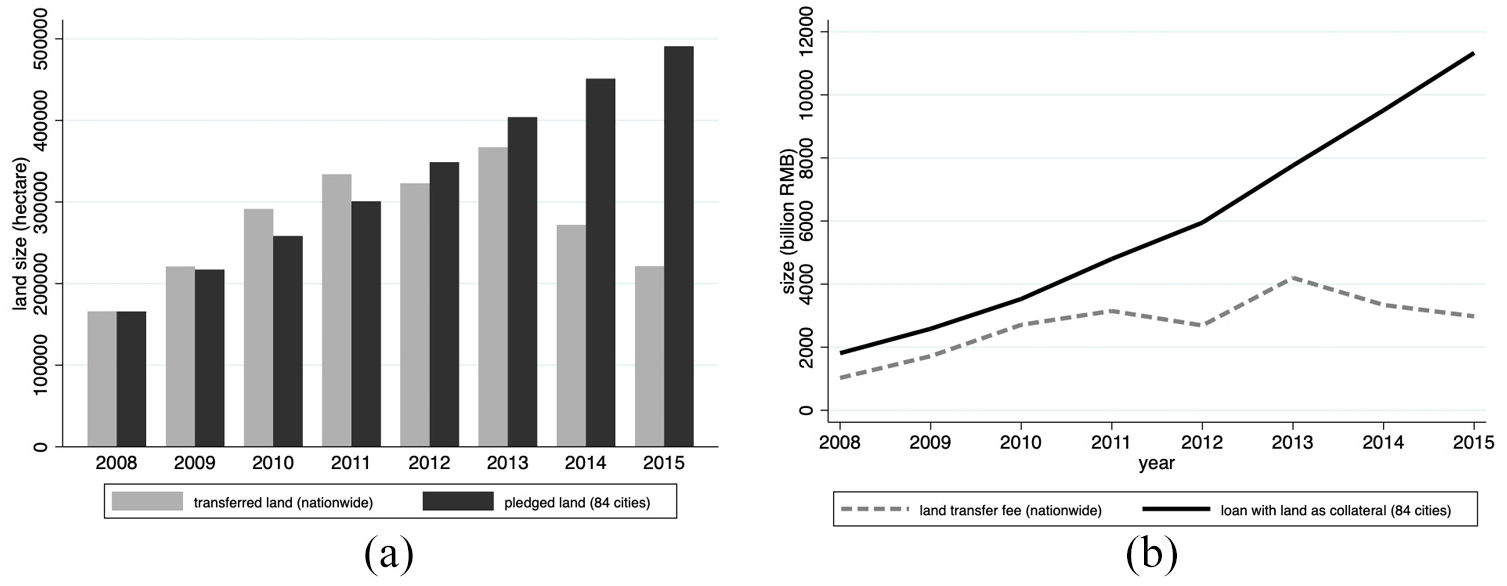

Another function of land, which is equally if not more important than revenue generation, is to serve as collateral for public borrowing. The Ministry of Land and Resources reported the situation of land being pledged for public borrowing for 84 major cities, the list of which was not provided, however. Figure 1 compares land being transferred with land being pledged from 2008 to 2015, the only time period for which pledged land data were reported. It shows that the area of land being pledged was increasing over time and surpassed the area of land being transferred in 2012. The size of loans where land was used as collateral was always greater than the size of land transfer fees throughout the time, and the gap between the two was increasing over time. Keep in mind that the pledged land data were for 84 cities only, or less than one-third of prefecture cities in China. Both the area of pledged land and the size of loans, if measured nationwide, are expected to be increasing.

Land as an instrument.

Another constraint facing local governments is that, according to Budget Law passed by the National People’s Congress (1994), they are prohibited from directly borrowing from financial markets (Article 28). The more recent version of the Law, revised in 2014, grants provincial governments greater borrowing authority but retains the general prohibitions against borrowing by local governments below provincial level (Xu and Yang, 2015). In response, local governments have set up LGFVs and encouraged them to borrow from the financial market – mostly banks, backed by an implicit or explicit government guarantee. LGFVs are treated as state-owned enterprises (SOEs) and are legally eligible to borrow from the market. But unlike regular SOEs, LGFVs engage in economic activities that are fiscal in nature; the government directly or indirectly shares the debt-servicing responsibilities and sometimes subsidises LGFV losses (Zhang and Barnett, 2014). Land constitutes a principal source of collateral for LGFV borrowing (Liu and Jiang, 2005; Lu and Sun, 2013; Zhang and Barnett, 2014;Zhou, 2011). Local governments use land, much of which is acquired from villagers, as collateral to apply for bank loans through LGFVs; with these loans, local governments can carry out their investment projects (e.g. infrastructure), thereby appreciating land’s market value; they then transfer land use rights and collect revenue resulting from land transfer to repay their debt.

For most periods prior to 2008, LGFVs had been vigilantly monitored by the central government to prevent potential local debt problems. In the face of the 2008 global financial crisis, the Chinese government announced a stimulus package of RMB 4 trillion, of which only 1.18 trillion was contributed by the central government and the rest was fulfilled by local governments in the form of ‘matching funds’. People’s Bank of China and China Banking Regulatory Commission (2009) jointly issued a regulatory document within which they ‘encourage local governments with conditions to set up investment and financing vehicles and issue financing instruments such as corporate bonds and mid-term bills so as to diversify the channels for raising matching funds in support of centrally-funded investment projects’ (Article 1). State-owned banks were urged to lend generously. With this official approval from the highest financial authorities, LGFVs proliferated and LGFV debt exploded. LGFV borrowing has continued after the stimulus programme ended in 2010 (Bai et al., 2016). Figure 2(a) examines the volume of outstanding LGFV debt: LGFV debt, consisting of bank loans and bonds, has been growing over time, particularly after 2008; bank loans have grown more rapidly than bonds. Figure 2(b) examines LGFV debt relative to local budgetary revenue. The debt-to-revenue ratio surged in 2009. The ratio ranges from 45% to 81% before 2009; while it dropped after 2009 it has remained above the pre-2009 level, ranging from 83% to 127% from 2009 to 2014.

Debt of Local Government Financing Vehicles (LGFVs) in China. (a) Debt volume, (b) debt-to-local-revenue ratio.

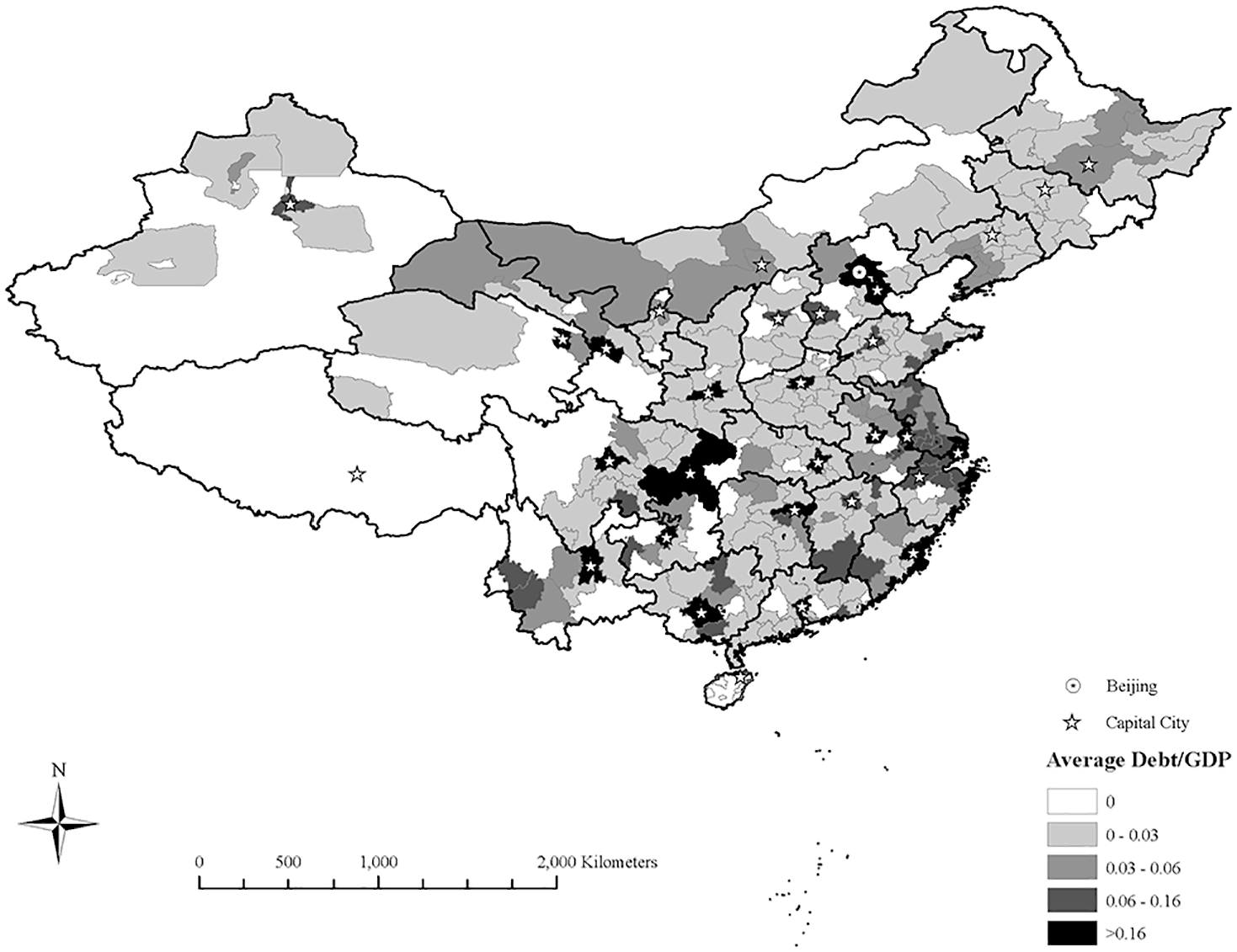

Figure 3 maps the average debt-to-GDP ratio measured at the prefecture level in 2005–2014. A significant portion of prefecture governments are indebted; the distribution of indebtedness is uneven, with the debt-to-GDP ratio ranging from 0% to 46%. Provincial capital cities are generally more indebted than regular prefecture cities. Indeed, the top 22 most-indebted cities consist of the four provincial-level municipalities and 18 provincial capital cities.

Average debt/GDP, 2005–2014.

Our fieldwork shows that local governments in less developed regions also heavily rely on LGFVs to raise capital with which to jump-start urban planning and construction. Take a county in Guizhou, one of the most backward provinces in China, for example. With its per capita GDP (RMB 18,000 Yuan) accounting for only one-fifth of the national average level by 2014, the county government authority laid out an ambitious scheme for infrastructure building in its 13th Five-year Plan, with 40-plus projects totalling over RMB 15 billion, ranging from slum demolishment to parking lots, waste incinerators and city parks, while its revenue collection in 2014 was about RMB 6.6 billion only. LGFVs have been essential in financing the investment binge: LGFVs not only acquired loans from various banks – including local commercial banks and policy banks such as provincial- and city-level development banks and agricultural development banks – but they also relied on credits from a myriad of financial entities, typically referred to as shadow banks, that charged higher-than-market interest rates to shore up the local spending spree.

LGFV debt, institutional discrimination and distributional consequences

Local governments and their LGFVs that had borrowed from banks during the 2008 financial crisis have been struggling to make interest payments. NAO reports (2011, 2013) identify one of the major problems in public borrowing and repayment, which is that local governments rely too much on sale of land-use rights to repay their debt. Massive expropriation and subsequently commodification of rural land result in hundreds of millions of land-losing villagers. However, China’s land property rights system fails to protect villagers, the original rural land users, but on the contrary grants local governments institutionalised authority to exploit villagers.

Perhaps the most fundamental feature of the land property system in China is legal discrimination against rural land by design. China has a dual land tenure system of state-owned urban land and collectively owned rural land. Land commodification turns land into a marketable asset but the urban–rural segmentation of the land system remains. In contrast to the fully functioning urban land market and housing market, the development of the rural land market and housing market has been limited and slow. Rural households are allowed to rent out their land provided that it remains for agricultural use. However, rural land is prohibited from being transferred, leased or rented for non-agricultural use (National People’s Congress, 2004: Article 63). Each rural household is allocated one, and only one, plot of homestead land, the size of which is strictly regulated. Applications for a new plot of homestead land by those who have sold or leased their houses shall not be approved (National People’s Congress, 2004: Article 62). The use rights to both agricultural land and homestead land are allocated for personal use and cannot be pledged for mortgage (National People’s Congress, 1995: Article 37). These rules restrict the ability of villagers to use their land to engage in economic activities. The conversion of rural land for urban construction must go through land expropriation, a process monopolised by the state. In reality, the process of expropriation and subsequently commodification of rural land is associated with a wide price discrepancy between the compensation price paid to land-losing villagers and the market price of land at which local governments sell to urban land users, allowing local governments to capture the arbitrage value.

The formal rules governing land also contain loopholes that allow local governments to interpret the rules in a way that serves their, rather than the public, interest. For example, the rules fail to define who represents the collective when it comes to collectively owned rural land. The state has the authority to expropriate rural land for the sake of ‘public interest’, the scope of which is also not defined (National People’s Congress, 2004: Article 2). In practice, expropriated land has always been made available for non-public purposes to support industrial, commercial and residential development, although the proportion of land dedicated for such use has been declining over time. In 2017, land used for non-public purposes accounted for about 40% of expropriated land, a decrease from 56% in 2013 (Ministry of Natural Resources, 2018). Ho (2001) argues that such legal ambiguity was designed deliberately to provide local governments with more power to interpret and facilitate land expropriation, a situation he conceptualised as ‘deliberate institutional ambiguity’.

Local governments also have institutionalised autonomy in making land-related policy. Take compensation for loss of land as an example. Land-taking compensation that villagers receive takes the form of the one-time lump-sum cash payment calculated on the basis of the land’s original use (i.e. agricultural values) (National People’s Congress, 2004: Article 47), under the principle of ‘not making affected villagers worse off’ (State Council, 2004: Article 12). Such rules entail a wide range of flexibility for local governments to design their own compensation package. In reality, the compensation amount varies across localities and the compensation form has been diversified. For example, some local governments initiated the so-called ‘land for welfare’ programme, whereby they provide land-losing villagers with a pension insurance that guarantees eligible villagers monthly pension payments for life in addition to the traditional one-time cash payment (Cai, 2016). According to our field observations, a common practice in making local compensation policies is that local governments stipulate compensation standards that apply within their administrative jurisdiction and adjust them every few years to keep up with the local living standard.

The legal discrimination, deliberate institutional ambiguity and institutionalised autonomy provide local governments with the legal basis to exploit villagers during land expropriation. Levi (2002) argues that state predation is more likely to occur when rulers are relatively unconstrained, or when they are faced with crises that require huge additional funds and are forced to tax in a way that may damage long-term gains. Vahabi (2015, 2016) argues that the scope of state predation is also determined by the mobility and appropriability of assets. Captive assets, which are immobile and capturable, increase the chance of state predation, while fugitive assets reduce vulnerability to state exploitation. In our case, land is unmovable and unlikely to hide, making it vulnerable to state expropriation. The allocation of land-generated revenue can be understood as a zero-sum game: the more compensation affected villagers receive, the less revenue local governments can retain. As a result, the state has an incentive to provide land-losing villagers with no more than the necessary amount of compensation. This may especially be the case for indebted local governments as they are more capital-constrained and have to service their debt. Hence, we hypothesise that more-indebted local governments are likely to take a more exploitative land-taking compensation approach by paying land-losing villagers less.

Empirical analysis

Our empirical analysis is based on a self-compiled data set primarily from the following sources: household-level data, including land-taking compensation, coming from the China Household Finance Surveys (CHFS) conducted in 2013 and 2015, respectively; 2 LGFV debt data compiled from the WIND Economic Database; 3 administrative and economic data compiled from City Statistical Yearbooks.

The dependent variable is compensation for loss of land, measured by the monetary compensation that villagers actually received relative to what they are supposed to receive minimally according to the minimum compensation standard set by the local county-level government, that is,

Both the actual compensation and the size of acquired land are individual self-reports, based on the following two survey questions in CHFS, ‘How much cash compensation for loss of land did your household receive?’ and ‘How much land was acquired?’ The corresponding official minimum compensation standard, which we collected from each local Bureau of Natural Resources website, is matched based on the self-reported year when their land expropriation occured. Individuals whose land was acquired more than once are treated as separated observations. In our analysis, 38 individuals or 6% of the total observations had experienced land expropriation twice.

The independent variable is LGFV debt, consisting of bank loans and bonds. LGFVs are registered as SOEs and, when issuing debt, must provide regulatory agencies (e.g. China Securities Regulatory Commission, China Banking Regulatory Commission) with a prospectus which contains detailed debt information. This prospectus is collected by and made available from the WIND database, from which we compiled each LGFV’s debt, if it exists, for the period from 2005 to 2014, and aggregated it at the prefecture level.

We consider three sets of controls. The first set relates to individual-/household-level controls, including whether land-losing villagers received non-monetary compensation, education, household size and communist party membership. The second set relates to village-level controls. We include registration rate and voter turnout rate for the most recent village election to capture the impact of village elections on land-taking compensation. We include the indicator of Village clan to capture the impact of informal institutions on land-taking compensation. Compensation may also be related to the location of land. To address this concern, we include Distance, measured by the distance between the surveyed village and its prefecture government. The underlining logic is that, as rural land is located closer to the city core, its market values appreciate and drive up the land-taking compensation that villagers receive. The third set relates to prefecture-level controls, including local GDP, population, fiscal capacity measured by the ratio of revenue to expenditure, urbanisation measured by the ratio of urban population to the total population, and commercial housing price. Owing to data availability, some factors which may also affect land-taking compensation – for example, whether there is a protest against insufficient compensation – are not included in the analysis. Finally, we add city fixed effects to take into account the locality-specific characteristics and year fixed effects to account for the impact of the time of land expropriation on land-taking compensation.

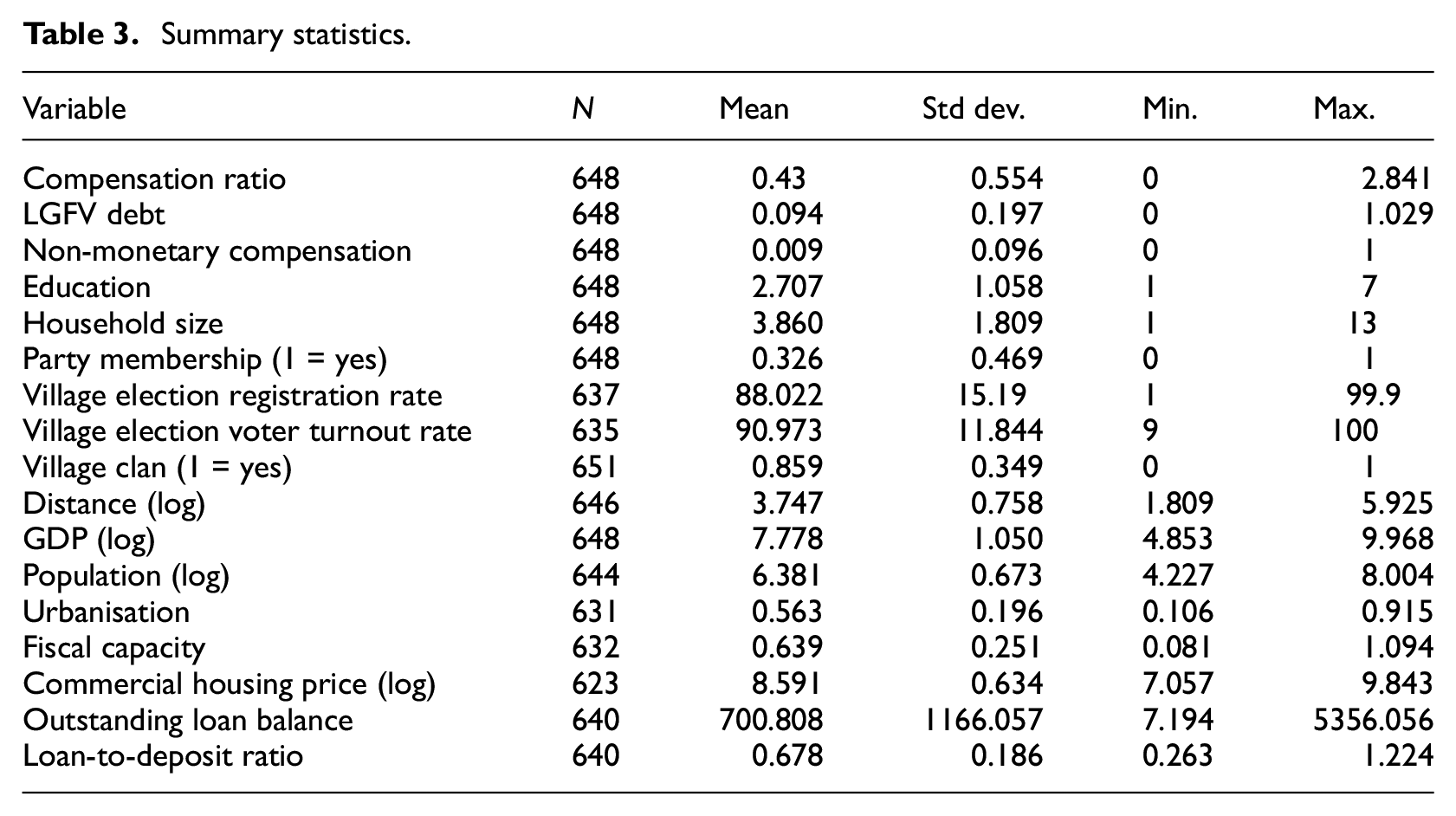

It should be noted that CHFS focuses on household-level financial and physical assets (land included). Only a subset of the survey respondents who had experienced land expropriation is useful for our purpose. Specifically, of about 65,000 households surveyed, 31% were rural households. Of over 20,000 rural households surveyed, 894 households reported that they had experienced land expropriation. The self-reported land expropriation time varies from 1983 to 2015. To match our LGFV debt data which are available from 2005 to 2014, those whose land expropriation occurred prior to 2005 are dropped and 648 households are kept in our analysis. Tables 2 and 3 present variable definition and summary statistics, respectively.

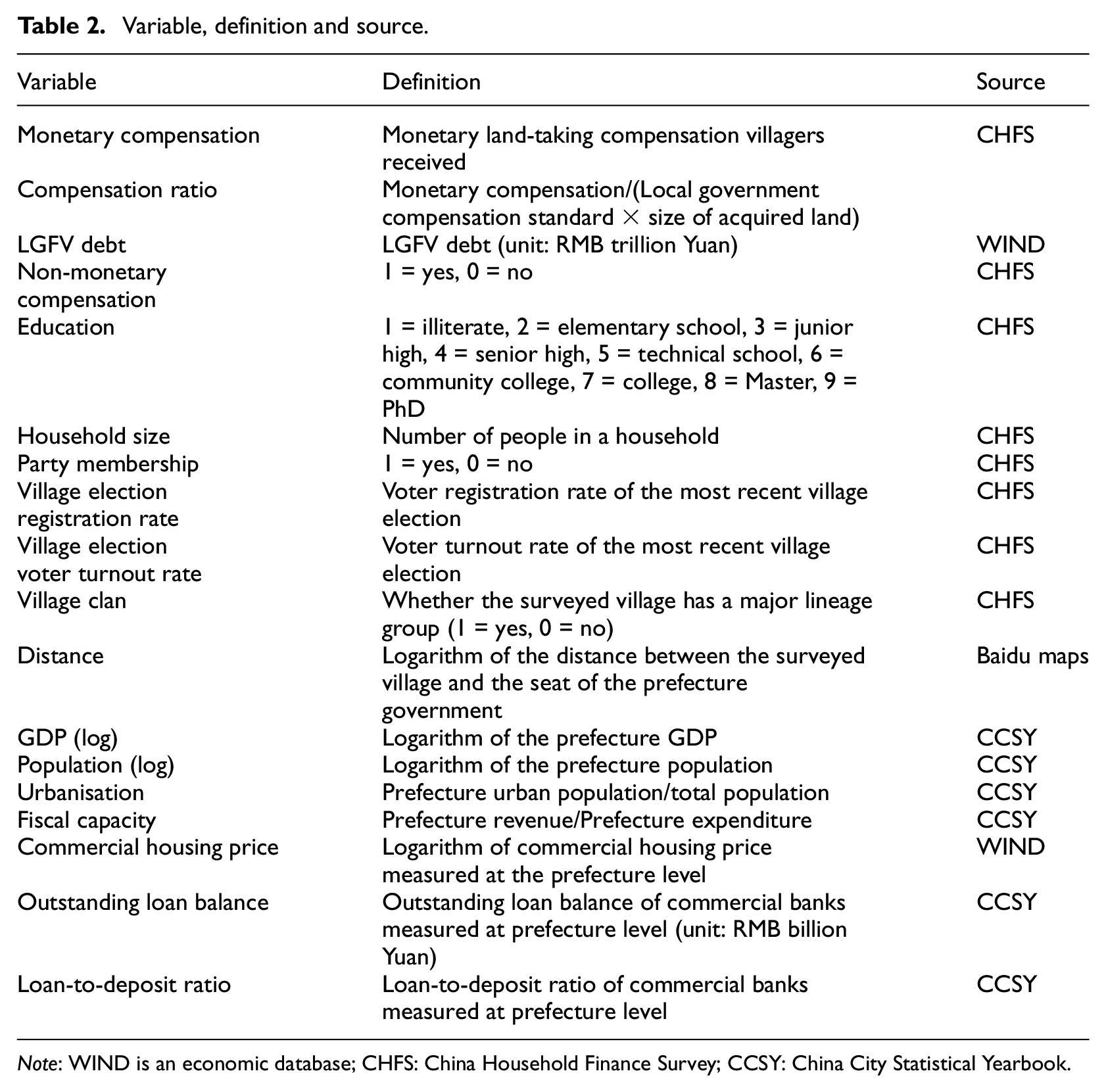

Variable, definition and source.

Note: WIND is an economic database; CHFS: China Household Finance Survey; CCSY: China City Statistical Yearbook.

Summary statistics.

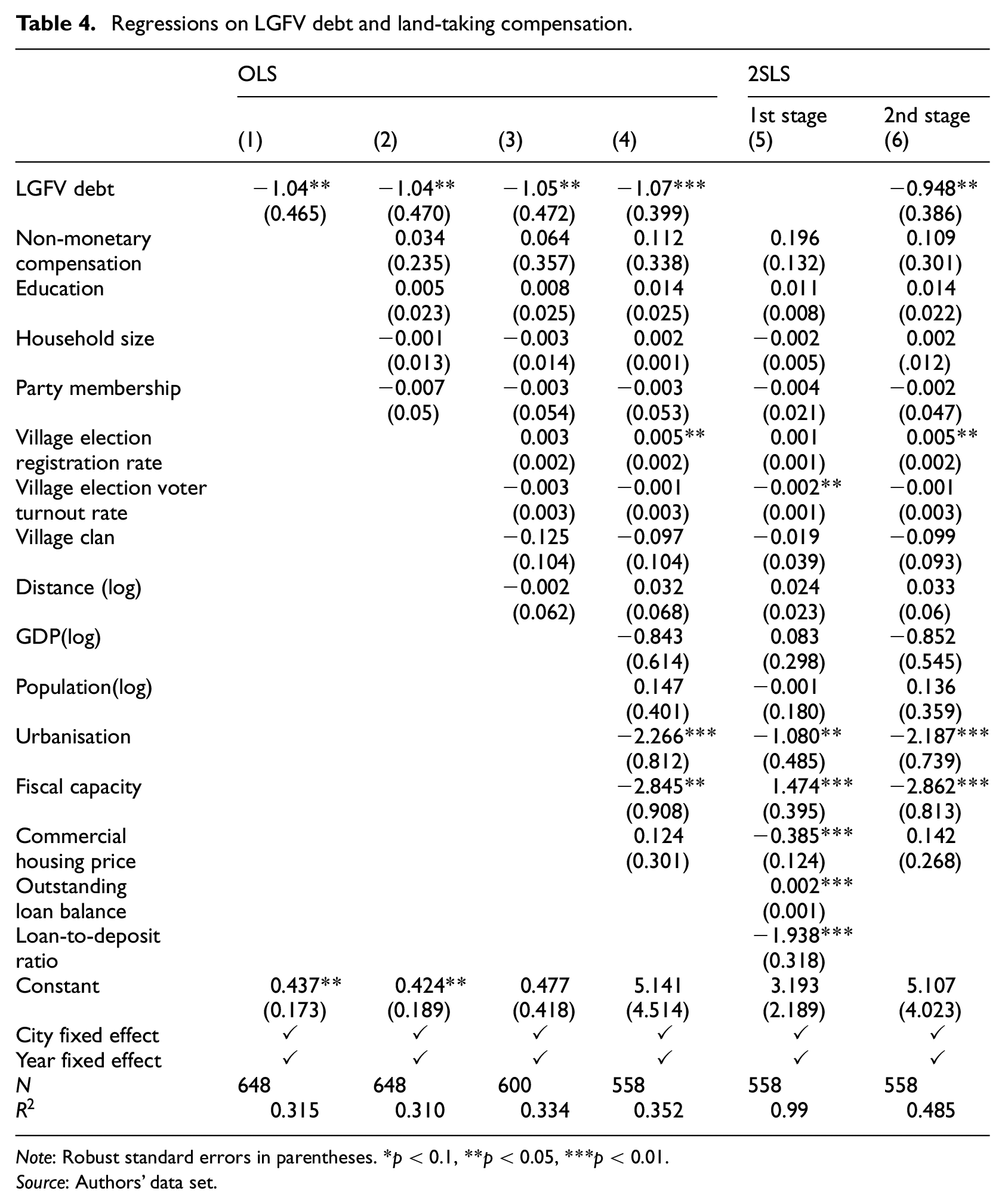

Table 4 reports the OLS regression results. We first perform the bivariate analysis and report the results in Column 1. We then add the three sets of control variables one by one and report the results in Columns 2–4. City and year fixed effects are included in all model specifications. The coefficients for Debt are negative and statistically significant across all model specifications, suggesting that more indebted local governments are associated with more exploitative compensation allocation.

Regressions on LGFV debt and land-taking compensation.

Note: Robust standard errors in parentheses. *p < 0.1, **p < 0.05, ***p < 0.01.

Source: Authors’ data set.

One concern with our OLS regressions is the potential endogeneity due to omitted variables and reversed causality. To address this concern, we use outstanding loan balance and loan-to-deposit ratio of local commercial banks, both measured at the prefecture city level, to serve as the instruments for our independent variable, LGFV debt. LGFVs borrow from banks; therefore, LGFV debt is expected to be positively correlated with outstanding loan balance of local commercial banks, which appears to be exogenous to land-taking compensation that individual villagers receive because commercial banks offer loans to more than just LGFVs. The loan-to-deposit ratio as an indicator had been vigilantly monitored by the People’s Bank of China from 1995 to 2015, during which time, according to the National People’s Congress (2003), the ratio should not exceed 75% (Article 39). When the ratio gets closer to the threshold, local commercial banks will reduce lending, which makes it harder for LGFVs to borrow. Thus, we expect that the loan-to-deposit ratio is negatively correlated to LGFV debt but exogenous to land-taking compensation. We perform the 2SLS regression and report the results in Table 4, Columns 5–6. The estimate for LGFV debt remains qualitatively and quantitatively unaffected, suggesting its robustness.

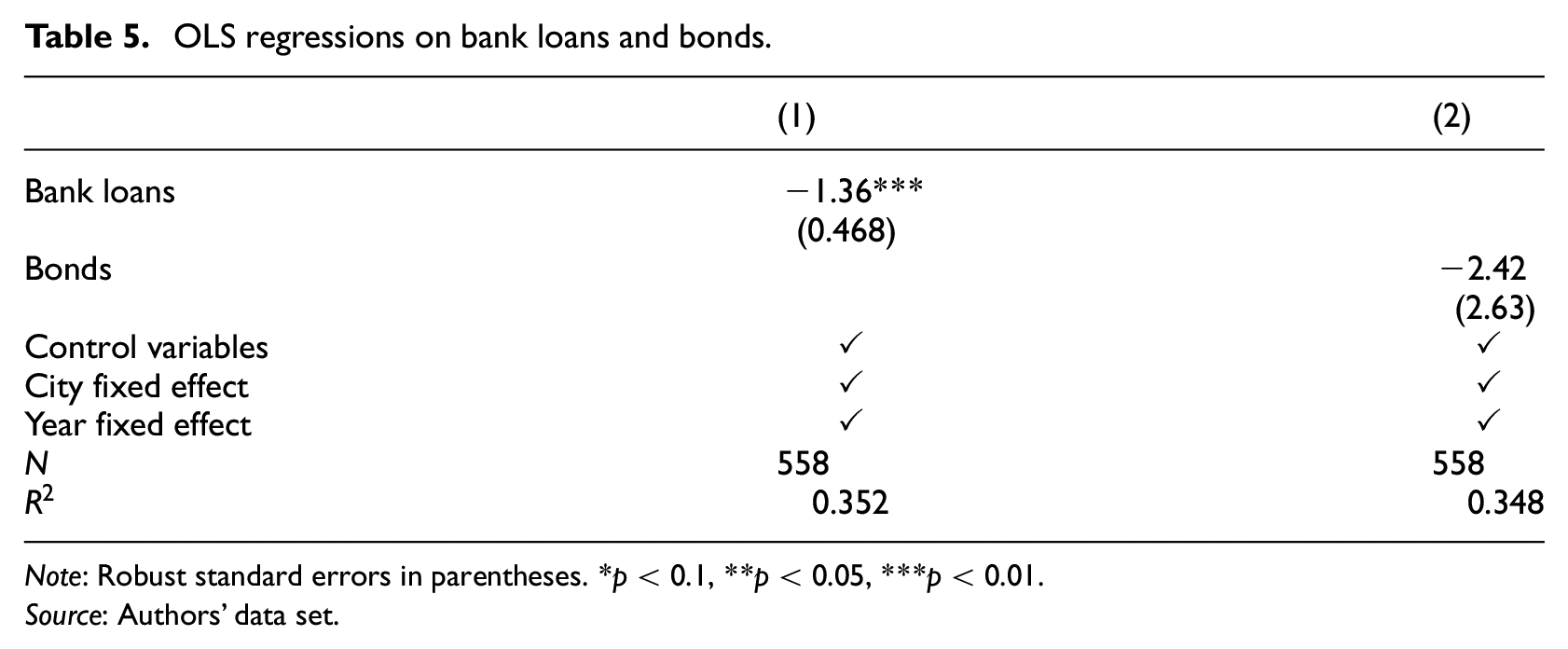

Another concern is that the two components of LGFV debt, bank loans and bonds, may perform differently as bonds had been highly regulated by the central government. To address this concern, we regress Compensation ratio on bank loans and on bonds. The results in Table 5 show that the coefficient for Bank loans, but not for Bonds, is negative and statistically significant, suggesting that an increase in LGFV debt in the form of bank loans is associated with more exploitative compensation distribution. This is because land functions as an important collateral for bank loans but not so much for bonds. Through an examination of the bond prospectus of all 2116 bonds included in the WIND database, 553, or 26%, required collateral of some sort. Of all the bonds issued, only 166 or fewer than 8% of bonds, had land used as collateral.

OLS regressions on bank loans and bonds.

Note: Robust standard errors in parentheses. *p < 0.1, **p < 0.05, ***p < 0.01.

Source: Authors’ data set.

The negative and statistically significant coefficients for Urbanisation and Fiscal capacity suggest that villagers face more exploitation in more urbanised localities and when local governments are fiscally more capable. Such localities are likely to be associated with high land values, more compensation (i.e. the numerator) and higher compensation standards (i.e. the denominator). However, the compensation received by villagers may not grow as fast as the compensation standards, creating a greater gap between what villagers actually received and what they are supposed to receive (i.e. a smaller compensation ratio). Our findings are in line with Heurlin (2016), who finds that grievances against land expropriation are higher in high-land-value localities because compensation values depart more drastically from actual land values.

We perform additional robustness checks. In the existing models, the key independent variable is measured as the total LGFV debt while controlling for local GDP together with other controls. We vary the model specifications by normalising the independent variable where LGFV debt is measured as a proportion of the local GDP (i.e. LGFV debt/GDP) and meanwhile removing GDP as a control variable. We also include land transfer fees as an additional control variable. The main results remain robust.

Conclusion

Local government financing vehicles serve as an instrument through which local governments circumvent the prohibition on borrowing and channel massive funds to finance China’s capital-intensive urbanisation and development. The associated problems are also alarming. The proliferation of LGFV debt triggers concerns about a potential debt crisis, which creates financial vulnerability and threatens economic stability (Lu and Sun, 2013). Bai et al. (2016) show that local governments have used LGFVs to provide financial resources not only to public infrastructure but also to politically connected private firms. Such misallocation of capital will have a damaging effect on the economy in the long run. Local government borrowing via LGFVs also led to the reinstatement of local government soft budget constraints and partially reversed the creation of hard budget constraints for SOEs, banks and local governments that was achieved in the early reform era. Our research adds another dimension to the associated problems: LGFV debt pressure induces local governments to extract more from society by paying land-losing villagers less compensation. One policy implication of our findings is that there are intrinsic connections of the local state, land-centred local public finance and land-losing villagers in China’s urbanisation process; failure to address rapid expansion of LGFV debt has an impact on distributive justice for land-losing villagers.

Our research shows that local government can be developmental and predatory at the same time. It is developmental because local governments use LGFVs as a means to actively participate in capital markets and raise funds to support ongoing urbanisation and economic growth; it is also predatory because local governments transfer their debt pressure on to land-losing villagers by extracting more from them. One of the reasons for bifurcated and conflicting state behaviours lies in institutional constraints. Local governments are entrepreneurial and developmental because they are constrained by the market preserving federalism (Montinola et al., 1995), factor mobility and yardstick competition among local governments (Su and Tao, 2017), and the cadre evaluation system that connects individual career advancement to local economic growth (Landry, 2008). In sharp contrast, local governments are predatory and extractive when it comes to how they treat villagers during land expropriation. They do so because legal discrimination, deliberate legal ambiguity and institutionalised autonomy contained in the existing institutions governing land provide a legal basis for local governments to abuse their power by exploiting land-losing villagers.

Our findings also raise concerns about distributive justice in China. We show that the implementation of land financing to support urbanisation and development comes at a cost of squeezing land-losing villagers. Our study echoes Bates (1981) who finds that African states supported industrialisation by exploiting farmers. The state can provide protection of property rights as a public good (Libecap, 1989; Riker and Sened, 1991; Sened, 1997) or implement selective enforcement of property by providing protection for only a subset of society at the expense of others (Haber et al., 2003). China falls into the second category (Cai et al., 2020). The way in which land property rights are enforced in China encourages state predation and turns local governments into the largest beneficiary. This creates incentives for local governments to maintain selective enforcement and block universal protection of property rights, resulting in slow progress or stagnation in improving property rights for all – a situation Hellman (1998) referred to as ‘partial reform equilibrium’. Villagers have suffered and will continue to suffer as a result.

Footnotes

Acknowledgements

We are grateful to the anonymous reviewers for their insightful comments and suggestions to improve the manuscript. We thank Meg Rithmire, Zhijun Gao and the participants of the 2018 American Political Science Association Annual Conference and the 2019 Association of Chinese Political Studies Annual Meeting for helpful comments on earlier drafts. We thank Yue Zhou, Wenjie Wang and Xiaolu Zhao for their excellent research assistance. Special thanks to Qin Chen who helped with data compilation on LGFV debt.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Financial support from the National Natural Science Foundation of China (#71873038, #71773113, #71773019), Philosophy and Social Science Planning Office of Shanghai (2017BJL001), Gaofeng Project I of Theoretical Economics at Fudan University, and the University of Connecticut is gratefully acknowledged.