Abstract

This paper develops a conceptual approach to articulate the political-economy inspired literature on the financialisation of cities with a critical reading of collaborative-communicative planning theory to recognise the active role of planners in the multi-scalar, collective ‘making’ of financialisation by cities. More particularly, I stretch Hilferding’s original idea on founder’s profit, which was associated with the financial gains obtained from Initial Public Offerings and trading of company shares in open markets. In collaboration with private investors and producers of urban space, planners in cash strapped cities and states search for solutions to invest in better cities by anticipating their exclusive rights to various streams of income, while co-promoting and extracting part of urban founder’s profit in doing so. Nevertheless, a communication that is framed around the representational spaces and language of financial models triggers planners’ increasing entanglements with finance in the transformation of cities into abstract tradeable income yielding assets. A methodological-heuristic case study illustrates how tracing the models enables us to follow the money, exposing the contradictory role of collaborative-communicative planning and demand for a project with alternative time-space epistemologies.

Introduction

The literature on financialisation, defined by Aalbers (2015: 214) as ‘the increasing dominance of financial actors, markets, practices, measurements and narratives, at various scales, resulting in a structural transformation of economies, firms (including financial institutions), states and households’, has increasingly recognised the role of cities in these shifts.

Despite this innovation, it has nevertheless taken a direction that has facilitated the elaboration of some questions but left others along the way.

Much work has focused on how financialisation has affected cities, either through land and real estate markets, urban infrastructure, or the governance–capital market nexus in times of fiscal austerity, among other examples. The proliferation of theoretical and empirical investigations on finance capital and urban space has directed the agenda towards the investigation of the variegated financialisation of cities (Aalbers, 2012).

Unlike housing and infrastructure, at first sight investors do not look at cities – which are relatively illiquid, risky and ‘uncooperative’ spaces of use value (Bakker, 2007: 447) – as a potential asset class. Cities are not passive containers of globalising forces emanating from financialisation and neo-liberalisation (Robinson and Attuyer, 2020). In this paper I will adopt a Lefebvrian inspired, broader definition of cities as urban spaces where different projects (for example, abstract space associated with globalisation and financialisation versus differential space emerging from the daily life experience) are disputed and filled in by social actors. Lefebvrian cities as urban space are three dimensional in terms of material-physical (the built environment), social (the relation between capital, labour and the state) and representational (the ideological and scientific conceptions) spaces (Lefebvre, 2001). This perspective allows us to pose alternative questions on urban financialisation.

First, some authors have emphasised the role of local agency in shaping the specific configuration of urban financialisation in multi-scalar territorial networks. These efforts have generated a more fine-grained reading of how local state and non-state actors are involved in a multiple scaled process of financialisation by cities. A less frequently explored question, however, is how, especially in times of austerity, planners become entangled with productive and finance capital in the collaborative ‘making’ of financialisation. While trying to comply with their responsibility to produce better cities, how does communication, framed around the language of financial models and the extraction of value for money from public assets, contribute to the reconstitution (Ashton et al., 2016) and decontextualisation of planning itself (Savini and Aalbers, 2016)?

Second, there is nothing inherent about this process. In other words, if planners are actively involved in the collective making of financialisation, does this not imply that the potential contradictions of this process could be contested and an object of ex-ante counter-hegemonic planning aimed at differential spaces for people, and not for financial profits (Brenner et al., 2012)? Does an analytical lens on the collaborative making of financialisation in times of urban austerity provide insights regarding how the prevailing planning epistemologies could be revisited critically to put another project in place?

In this paper I propose a preliminary theoretical framework that allows us to explore these alternative questions.

First, by articulating the idea of urban founder’s profit with planning theory, I shed light on the role of collaborative-communicative planners in the multi-scalar ‘making of’ financialisation of cities, and by cities.

It was Marxian author Hilferding (1910) who first explored the concept of founder’s or promoters’ profit as the financial gains that were derived from floating company stock in capital markets. Hilferding’s approach allowed problematising more traditional Marxian perspectives on the divide between finance capital and industry, considering they both shared the financial gains associated with founder’s profits. I stretch and update Hilferding’s ideas and link up with collaborative-communicative planning theory by fleshing out the significance of urban founder’s profit. Planners, defined in this paper as professionals working in public administrations with the built environment (Savini et al., 2015), become entangled with finance and industry in the promotion and extraction of financial profits aimed at ‘making ends meet’ and providing better cities in times of austerity. A communication whereby space is conceived in the language of financial models, structured around the generation of investor’s value for the upfront money received, tends to hollow out the progressive-redistributive ideals of mainstream planning theory.

Second, not unlike earlier work has done regarding the imbrications between neo-liberalisation and mainstream planning theory (Purcell, 2009), investigating the collective making of urban financialisation through financial models sheds light on the counter-intuitive reinforcement of the logics of money and finance in the production of urban space through communicative planning. Tracing how the cooperative search for austerity solutions through the language of financial models mobilises planners, finance and industry allows us, ex-ante, to expose how planners get sucked into a financialised representation of space. Such a critique potentialises a double move from the Marxian, Lefebvrian metropolis to markets and back through the development of an alternative planning project organised around the spaces of daily life experiences in cities, ‘based on real possibilities and capacities, now and here’ (Santos, 2002: 257).

In this paper I will define financial models as discounted present value models. While discussing the theoretical potential of urban founder’s profit, I recognise that financial modelling has become much more sophisticated since Hilferding’s writing. Contemporary capital markets have augmented their capacity to filter away risk through interest and exchange rate swaps, derivatives, securitisation and hedging (Chiapello and Walter, 2016). This obviously generates operational challenges to following the money by tracing models, as a potential counter-hegemonic strategy advocated by me in this paper. However, as will be shown, the dynamics of modern capital markets do not invalidate the claims behind Hilferding’s original concept and its critical relevance for contemporary urban debates.

The paper provides two contributions. First, through the analytical lens of the generation and extraction of urban founder’s profit through models, it sheds light on how, particularly in times of austerity, the collaborative-communicative planning project reinforces the making of urban financialisation.

Second, through a heuristic-methodological case study, it shows the transformative potential of following financial models to facilitate tracing the money, by ex-ante exposing the contradictory nature of planning in the making of financialisation under austerity, and by stimulating political mobilisation around a planning project with alternative space-time epistemologies. I illustrate the potential of such a double move from the Lefebvrian, Marxian metropolis to markets and back (Christophers, 2014b) by discussing the design of a Public–Private Partnership (PPP) in sanitation in the state of Rio de Janeiro, Brazil.

Four complementary sections follow this introduction. The first analyses the literature on urban financialisation, its main questions and directions. The second articulates the concept of urban founder’s profit with collaborative-communicative planning theory to investigate the entanglements between planners, finance and industry in the financialisation of cities, and by cities. The third section discusses the heuristic example from Rio de Janeiro/Brazil. The conclusion wraps up the argument and indicates ways forward along the lines debated in this paper.

From financialisation of‘un-cooperative’ cities to financialisation by cities?

Research on financialisation has increasingly fleshed out the circuits through which finance stretches out its tentacles into urban space. The debates have extended Harvey’s earlier work on the tendency of land and housing to be treated as a financial asset (e.g. Aalbers, 2012; Christophers, 2017; Haila, 1988; Harvey, 1982; Rolnik, 2019); the role of finance in entrepreneurial urban governance and urban redevelopment projects (Charnock et al., 2014; Kaika and Ruggiero, 2016); infrastructure financialisation (Bayliss, 2014; Deruytter and Derudder, 2019; Pryke and Allen, 2019; Torrance, 2008) and the interfaces between capital markets, urban governance and post-political austerity urbanism (e.g. Kirkpatrick, 2016; Peck, 2012; Weber, 2010), among other themes.

This focus on specific circuits of asset classes through which financialisation gradually penetrates urban space has privileged the analysis of what finance does to cities (i.e. extracting value from all of us without producing [Lapavitsas, 2013]), while it has spent less attention on fleshing out how exactly it accomplishes this.

The financialisation of cities cannot be taken for granted considering they also represent the privileged spaces of daily life experience and, as such, are an ‘un-cooperative’ asset class, which is unlikely to be easily bundled, re-packaged and traded in secondary markets (Gotham, 2009).

An emerging literature has now shifted the emphasis from political economy-oriented work, marked by its emphasis on investigating what finance does, to an approach that recognises that cities are not containers of the forces of neo-liberalisation and financialisation. It has broadened the perspective by focusing on the role of local agency and multi-scalar governance networks in the making of financialisation by cities. Some of these efforts have been influenced by social studies of finance and the literature on the performativity of financial models. The latter two strands have consolidated a research programme that is structured around the social constitution of (capital) markets as collective agencements, as ‘this careful arrangements of elements and how it entails a “diffuse and entangled”– or distributed – agency “intended to enact material “realities’” (Fields, 2018: 125). This approach relates to the science and technology literature and Actor-Network Theory (ANT) (Latour, 1997; Metzger et al., 2017), which has been sceptical in relation to political economy.

It is a more specific work that has relevance for the debate in this paper, one focused on the performativity of financial models. It was MacKenzie (2006) who disseminated the metaphor according to which financial models are engines, not cameras, in the sense that its asset pricing formula potentially transforms the marketplace instead of just describing it.

The work on the performativity of financial models has brought a fresh perspective on agency and the making of financialisation by cities. Moving beyond a macro-structural interpretation, according to which finance capital stretches its tentacles and ‘lands’ in cities, it acknowledges that the anchoring of finance in cities is variegated and frequently negotiated (Theurillat et al., 2016). It builds an understanding of how the use of viability models in governance networks has contributed to reshaping land, housing, and real estate into financial assets, particularly through urban redevelopment schemes.

For instance, several authors emphasised the role of consultants and ‘economists in the wild’ (Berndt and Boeckler, 2009; Callon, 2006) in the performative making of the urban world through financial models. A UK-inspired discussion showed how these actors reshaped housing (Christophers, 2014a) and land policies (Ferm and Raco, 2020). Weber (2010, 2021) and Pacewicz (2013) discussed how the use of models by urban development professionals and planners in Tax Increment Districts reinvented the city–capital nexus in the US context. Outside the Anglo-Saxon setting, Bitterer and Heeg (2012) analysed how international consultants, as part of a professional elite, put the Polish office market on the map of global investors through the circulation of economic models.

Similar work focused on the performative role of developers (Halbert et al., 2014). Henneberry and Roberts (2008) discussed how developers’ benchmarking techniques led to a concentration of property investments in metropolitan areas. Halbert and Rouanet (2014: 472) explored different geographies and analysed how ‘transcalar, territorial network’, composed of local and global actors, ‘performs (i.e. makes possible, translates and shapes)’ the anchoring of foreign finance capital in local Indian property markets.

Urban finance has also been analysed through the lens of performativity. Fields (2018) problematised how equity funds and rating agencies constituted Single-Family Rental units as an asset class. Van Loon and Aalbers (2017: 221) investigated the restructuring of Dutch pension funds and how ‘finance “financialized” itself’ by delegating the management of real estate portfolios to fund managers. The latter used portfolio theory in the transformation of ‘the “opaque” real estate market of the 1980s into a “seemingly transparent” market that is described and performed in a couple of “key figures”’ (van Loon and Aalbers, 2017: 234).

While the role of planners is acknowledged (Adisson, 2018; Ashton et al., 2016; Guironnet and Halbert, 2015), a less explored dimension in the urban performativity literature is exactly how the penetration of financial models in collaborative networks of state and non-state actors alike tends to ‘decontextualise’ the field in strange ways (Savini and Aalbers, 2016). Some authors argue this occurs because of the capacity of non-state actors’‘unique ability to move ahead – or sometimes to sidestep – public planning requirements’ (Halbert and Rouanet, 2014: 478).

Irrespective of whether this is always the case, I build on earlier work that envisages a more active role for planners and financial models in the transformation of urban space, and in governance regimes in motion. Examples are Weber’s (2021) analysis of planners’ choices of discounting rates in the financial modelling of Tax Increment Finance Districts, or the work of Ashton et al. (2016) on the reconstitution of the local state through the management of risk and value during long term infrastructure leases in Chicago.

My argument is that, in times of austerity, planners are searching for hard, upfront cash (Jessop, 2015) to finance city improvements. This drive for the capitalisation of (almost) everything beyond housing and real estate (Leyshon and Thrift, 2007) triggers their entanglement with industry and finance in the (re)invention and anticipation of a variety of future flows of rent and income (Purcell et al., 2020; Ward and Aalbers, 2016). Public–private collaborations unfold based on the common language and representation of financial models, aimed at providing investors with value for the money that is received upfront by cities in the present. It sets the stage whereby planners face a double responsibility for preserving the common good and the private financial rates of return through the collateral management of the inevitable unforeseen events and risks that have not been covered by contracts (Ashton et al., 2016). In the process, the language of financial models takes over and gradually penetrates the more traditional, physical dimensions of the planning field, which are structured around the regulation and intervention in built environments. A perspective on the making of financialisation through cooperative solutions for urban austerity, mediated through financial models, not only allows a critique of the epistemological premises of communicative planning theory, but also contributes to the debate regarding its substitution by a more radical planning project.

Financial profits and collaborative-communicative planning: From the Marxian metropolis to markets and back

Urban founder’s profit and the financialisation of (un-cooperative) cities

Different from its reluctant treatment of concepts such as globalisation and neo-liberalisation, Marxian political economy has always engaged with financialisation. In the early 20th century, Hilferding (1910) analysed the changing relations between finance and industry in the context of the emerging separation between owners and managers in the modern corporation. His concept of founder’s or promoter’s profit provided insights into understanding the financial profits associated with initial public offerings and the subsequent trading of stock in secondary markets. To be specific, to guide their decisions regarding the price they are willing to pay for stock in financial markets, prospective buyers use the money rate of interest to discount the expected profits that will be generated by companies. At the same time, while deciding on their initial capital investment, industrial owners use the profit rate to discount the same expected flow of future income. 1 In line with Marx himself, considering that the interest is lower than the profit rate, the share prices that are paid in financial markets exceed the present value of the capital that has been invested by industrial owners. The difference is founder’s profit, which accrues to the promoters/owners of the company and the financial intermediaries that coordinated the emission. Differential capitalisation, that is, discounting the same expected flow of income with a lower risk-free interest rate as opposed to a higher, risk adjusted internal rate of return (as a proxy of profits), is a key driver behind founder’s profit.

Despite a different historical setting and the sophistication of modern capital markets, Hilferding’s concept of founder’s profit provides relevant insights for the contemporary debate on the role of money and finance in general and in cities.

First, it allows us to problematise the naturalisation of the opposition between industry and finance, a premise that continues to haunt much work developed within the tradition of political economy. Examples of this perspective can be found in regulationist writing on the ‘dictatorship of creditors’ (Chesnais, 1996); in (post-)Keynsian interpretations, and Keynes himself; on the parasitic nature of the rentier; on under-consumption and the reduction of productive-industrial investments; or in certain strands of Marxist thinking on the tendential trajectory of ‘productive’ capitalism towards over-accumulation; the role of the financial circuit as a natural escape-valve to absorb surpluses (Magdoff and Sweezy, 1987) and to enable ‘capital switching’ (Harvey, 1982), to list some of the many examples. Instead, Hilferding’s approach allows a more promising perspective structured around the concept of the entanglements between finance and industry, the latter, as ‘productive’ capital, directly benefits from its approximation with capital markets considering that founder’s profit is divided between the industrial owners and financial intermediaries that organised the emission.

Second, Hilferding was writing on the modern corporation. Nevertheless, the concept of founder’s profit provides new insights into understanding the increasing entanglements between planners, finance capital and cities in times of austerity. There is evidently no easy analogy between industrial owners floating and trading in company stock and the role of planners in reshaping cities into a bundle of assets. Nevertheless, I argue that, particularly in times of austerity, planners are effective co-promoters of urban founder’s profit – together with industry and finance – through the strategic bundling of a series of exclusive properties and the capitalisation (anticipation) of the associated rights to projected streams of income to the present. This broadens the analytical lens regarding the nexus between rents, capitalisation and (fictitious) value to encompass infrastructure networks, environmental services, minerals and non-renewable energy, tax receivables and intellectual resources related to the urban knowledge economy (e.g. Birch, 2017; Mezzadra and Neilson, 2015; Purcell et al., 2020), among other examples. Urban founder’s profit conceptually includes the role of urban planners in the collaborative making of financial markets.

Third, the financialisation of cities, as un-cooperative spaces of use value, through the creation of urban founder’s profit is likely to be accompanied with contradictions, crises, and state collateral management. Hilferding was keenly aware of Marx’s analysis on the role of money in times of crisis. Nevertheless, as argued by Harvey (1982), he never came to work out the contradictions between money as a fetishised, socially accepted signifier of value and its role in market circulation. Capitalism’s recurring crisis tendencies are reflected in the inconsistencies between the generation of fictitious value (Net Present Value [NPV]) and the monetary base that is supposed to support and match it over the estimated time horizon of projects. Therefore, urban founder’s profit provides us with an analytical perspective to trace the inherent instabilities of the articulations between planners’ and investors’ expectations, the time-value of money and discounting. This can be understood once we acknowledge that, by and large, the NPV techniques of contemporary corporate finance theory formally coincide with the Marxian concept of fictitious capital (Lapavitsas, 2013). Both deal with expectations, capitalisation and what Chiapello and Walter (2016: 174) described as ‘the key intellectual scheme of pulling the future closer to the present’. Contemporary finance, however, through the assumptions of perfect foresight and costless information, assumes the coordination of the present by the future through the market’s subjective ‘self-transcendence’ (Aglietta, 2018: 23). The latter means that, at any point in time, the projected values from financial models for the future coincide with realisations in the present. Advanced mathematical modelling to filter away risk and the hypothesis of strong allocative efficiency mean that projected present values coincide with financial prices effectively used in asset markets. This neoclassical epistemic mirror allows the focus to be on long time equilibrium and an interpretation of social conflicts and mismatches between expectations and realisations as temporary deviations from the system’s steady state. However, the entrance point of Marxian fictitious capital, and my urban extension of Hilferding’s founder’s profit, is an analytical-empirical reading of recurrent crises that will occur during the lifetime of investments and PPPs. Crisis emerges because of the unavoidable mismatches between the discounted stream of future income in the present (fictitious value) and the effective monetary base that will circulate in future, recurrent transactions in markets and institutional partnerships between state and non-state actors. In other words, if the time dimension of capitalisation brings the urban future closer to the present, it is highly unlikely to unfold according to the model’s predictions.

Nevertheless, Hilferding’s silence regarding the nexus between crisis, money and (fictitious) value leaves us in the dark regarding exactly how planners get sucked into the contradictory transformation of the daily life experience in cities into abstract spaces. In what ways do planners’ search for upfront cash in times of austerity through the capitalisation and anticipated realisation of value trigger their increasing entanglement with finance structured around the language of financial models? Answering this question requires a better understanding of the collaborative-communicative planning project itself.

Austerity solutions, (public) value for money and planning in motion

The mainstream thinking in the field is based on collaborative-communicative planning theory. Among its main influences is Habermas’s writings on the substitution of an instrumental-technocratic logic, structured around means and ends, by a communicative rationality under conditions of ideal speech. For Habermas (1984), undistorted communicative action mobilises participants into a fair and honest process of intersubjective dialogue, argumentation and understanding of the common good for all, while neutralising power differences between participants. Although he recognised it was not an easy task to reach this ideal, it nevertheless became firmly embedded into the progressive, modernist planning field, which considered it worthwhile to gradually advance with this communicative project (Healey, 2003).

Despite its mainstream position in planning theory, the communicative turn has received criticism. Fainstein (2000), for example, claimed that a good planning process was insufficient to guarantee the transformation of urban space into better, that is just, cities. Communicative planners had found a subject (the planner), but had lost their object, considering that ‘instead of what is to be done about cities and regions, communicative planners typically ask what planners should be doing, and the answer is that they should be good (i.e. to tell the truth, not to be pushy about their own judgements)’ (Fainstein, 2000: 455–456).

Purcell (2009) goes beyond the insufficiency of the communicative turn. Instead, he argues that collaborative-communicative planning provides a counter–intuitive legitimisation of the neo-liberalisation project. While he recognises that ‘it is not at all the intent of communicative planners to serve the interests of capital’ (Purcell, 2009: 149), its collaborative stance ends up reinforcing and legitimising existing power relations. The effort to filter away and neutralise strategic individual interests in deliberative decision-making and prioritise a shared understanding of the ‘common good’ blocks a constituent, conflictual process of making power relations explicit and engaging in counter–hegemonic strategies.

Another critical element relates to the role of language in reaching the condition of ideal speech and undistorted communication. According to Purcell, this is logically impossible considering that, at best, language is a representation of the object it tries to signify. Meaningful communication therefore implies ‘a “master signifier”, a crux that sets the relationships between signifiers and signifieds and creates a consistent field of meaning’ (Purcell, 2009: 150). The implication is that language can never be a neutral, undistorted medium but is always political, driven by power relations among participants that seek hegemony in collaborative-communicative processes.

Not unlike Purcell’s arguments in relation to neo-liberalisation, I argue that there are two reasons that the collaborative-communicative planning project tends to reinforce the collective making of financialisation. First, in times of crisis, its collaborative stance tends to set the stage for consensual solutions for urban austerity. As such, it effectively reinforces existing power relations through the entanglements between the state, planners and finance capital. Second, the communication structured around the language of financial models and money as a ‘master signifier’ contributes to its penetration in the physical dimensions of the planning field. In what follows I briefly discuss each of these points.

The first brings us to the ambiguous relationship between governments and capital markets in times of crisis. It is not my objective to review the literature on austerity urbanism (e.g. on the ‘scalar turn’ in austerity studies, intergovernmental relations and urban austerity see Armondi (2017); on austerity and post-political urban governance see Peck (2012); on the framing and ‘manufacturing’ of crisis and austerity narratives see Bayırbağ et al. (2017)).

Rather, I argue that the framing of the relationship between states and city administrations and capital markets in times of crisis has subtly shifted from a traditionally problematic one to potential synergy through collaboration. On the one hand, policy makers and planners increasingly perceive capital markets as possible levers for raising cash through a more efficient management of public assets. On the other, capital markets envisage their enabling roles in the down sizing and privatisation of the public sector through institutional transactions that mobilise the state’s exclusive right over specific bundles of income in the future. Roll-out austerity synthesises this collaborative interaction between states and capital markets whereby the latter perform the role of laying the foundations for privatisation, PPPs and rolling back government intervention in general. This is somewhat different from classical economic thinking on the topic, which emphasised that state borrowing absorbs domestic savings and eventually crowds out productive investments. In a curious way, roll-out austerity and its more positive framing of the entanglements between the state and finance capital echoes Blyth’s description of the ‘can’t live with it, can’t live without it, don’t want to pay for it’ problem of the state that has haunted liberal economic theory since Lock, Smith and Hume (Blyth, 2013: 17).

The second point requires linking up with the temporal–spatial dimensions that accompany the language of financial models and money as signifiers in the communication between finance, industry and planners. For the sake of my argument, there are three complementary sides to this.

First, if discounting means pulling the future closer to the present, planners are strategic mediators in the conversations with finance capital regarding the earlier discussed differential capitalisation process that is a precondition for the existence of urban founder’s profit. Echoing the analysis of Theurillat et al. (2016) on the negotiated city, planners effectively represent the translators of the conventional physical-regulatory parameters that guide the built environment into the language and financial metrics of risk and differential capitalisation that accompany conversations with finance. To be specific, before‘un-tapping’ the potential of its asset base, the city administration’s exclusive rights to specific income streams are discounted with high internal rates of return that incorporate the associated risk perception of capital markets. While passing these rights over to hypothetically efficient capital markets, the latter can, supposedly, do their work to create low risk ‘liquidity out of fixity’ (Gotham, 2009). Considering that prospective buyers in financial markets use the lower money rate to discount these now ‘unchained’ streams in a market-friendly environment of privatisation and PPPs, urban promoter’s profit is being created.

Second, after the signing of institutional transactions and the extraction and distribution of founder’s profit in the present, the inevitable discrepancies between expectations and realisations will trigger what Ashton et al. (2016) called recurrent ‘state collateral management’ aimed at re-equilibrating financial contracts. More precisely, when ‘successful’ deals, that is, those generating upfront cash as urban founder’s profit, eventually prove cumbersome because of unexpected events and the imperfect filtering of risk, planning becomes effectively locked in and must respond to its formal responsibility to make ends meet during the prevailing period of institutional partnerships. But this ‘planning in motion’ represents a difficult balancing act, considering it implies, on the one hand, guaranteeing high profits and private internal rates of return derived from the contracted income streams from delegated-privatised assets (which were the driver behind the realised and already distributed founder’s profit in the first place), and providing the ‘common good’ by investing part of the upfront cash in city improvements. Considering the future that is coming is unlikely to match the risk-free, efficient market model’s predictions, in the present, of what it will be, this will require cumbersome and complex trade-offs that involve how planners choose to finance, regulate, and intervene in built environments in the public interest.

Finally, an explicit focus on imperfect performance of financial models (Henrikson, 2009) allows light to be shed on how planning is being reconstituted by moving along these recurrent mismatches between the language and representational spaces of financial models and cities as the experience of daily life. In that sense, tracing financial models facilitates following the money in terms of the contradictions between urban founder’s profits generated in the present and the monetary base that is circulating in the unfolding market transactions in the future. This enables denouncing the growing, contradictory entanglements of planners with productive capital and finance in trying to make things work and muddle through with the models and, ex ante, proposing an altogether different, subversive planning project that radically shifts the relations between states, markets, and society in the production of space.

Following the money by following models. A methodological illustration

What follows is not meant to be a common case study, that is, another illustration of the variegated process of financialisation. Instead, the objective is to provide, through an empirical example, the contours of a methodological primer to both comprehend and contest the multi-scalar, open ended making of urban financialisation by cities through the entanglements between the state, private infrastructure operators, finance capital and collaborative-communicative planners. I chose to follow an infrastructure PPP from its origins, justifications, design stage, approval of the project to the polemic bidding process with the winning proposals. I thereby outline a heuristic device to ex-ante trace the contradictory ways through which planners get involved in the constitution of markets and urban founder’s profits – to raise the funding to invest in better cities – and obtain analytical ammunition to mobilise a different planning project.

The case is a PPP in basic sanitation involving the Brazilian National Development bank (BNDES), the state of Rio de Janeiro (through its basic sanitation company CEDAE) and 47 cities in and around its metropolitan region. The material collected was based on official documents on austerity policies in Rio de Janeiro (e.g. conditional loan agreements and fiscal adjustment plans), the regulatory framework on sanitation, pre-viability studies, CEDAE’s business plans as well as the investment prospectus and bidding documents prepared by BNDES (BNDES, 2020). This was complemented with material from the three public hearings held on the PPP, secondary literature on Rio and critical coverage by the media and NGOs working in sanitation such as ONDAS. 2

Context. Roll-out Austerity and collaborative (capital) market solutions to public failure in water governance

The tale of Rio de Janeiro’s road to austerity is a story too long to tell here. It starts, however, with the near bankruptcy of its pension fund due to speculative operations with securities backed by oil and gas royalties (Le Monde Diplomatique, 2021). BNB Paribas, the investment bank that had coordinated the emission of the energy-backed securities, was the only institution willing to rescue the state in November 2017 by lending it R$2.9 billion to pay its employees (around US$887 million at prevailing exchange rates). A federal guarantee was provided on condition that Rio would implement an austerity plan. This plan included the privatisation of its state water and sewage company CEDAE to generate emergency resources and a private sanitation system that would finally solve Rio’s historical deficits in the sector. The project finance team from BNDES was called in as a market maker to structure the operation in close collaboration with the planners from the State Urban Development Secretary and water company CEDAE. Both planners and the BNDES agreed to design a strategy to mobilise the know-how and financial resources from the private sector to explore the potential of Rio’s water system.

Taking a closer look at the complex regulatory framework reveals why outright privatisation of public sanitation utilities in Brazil is easier said than done, however. Although the system is under pressure to open up, it is by and large still marked by institutional arrangements between cities and states whereby the former, as granting authorities with the responsibility for the overall planning, delegate the operation, maintenance and expansion of networks to state utilities through concessions. Moreover, a 2013 supreme-court ruling, still under discussion regarding its precise implications, determined that in metropolitan areas cities and states share the responsibility over basic sanitation and need to fill in the framework for the governance and finance of systems. Considering this regulatory uncertainty, outright privatisation of CEDAE implies significant risks and transaction costs, considering that prospective private operators need to re-negotiate individual concession agreements with metropolitan municipalities.

The collaborative design of urban founder’s profit for a better sanitation system

Therefore, the financial experts from BNDES and the state planners decided to change strategy, discard privatisation and ‘un-tap’ the potential of the water company by raising cash and universalising access to services through the design of a PPP for 35 years. In the revised deal, CEDAE collects, treats and sells wholesale water to private concessionaries, who go on to distribute and sell retail water and sewage services to final consumers.

The PPP is to guarantee complete coverage with sanitation services through additional investments of R$31 billion in 47 municipalities, representing around 13 million inhabitants. Aimed at facilitating competition, the bidding is organised in four blocks of municipalities in and outside metropolitan Rio. The more affluent city of Rio is further subdivided into four zones and distributed over each of these blocks to facilitate internal cross-subsidisation.

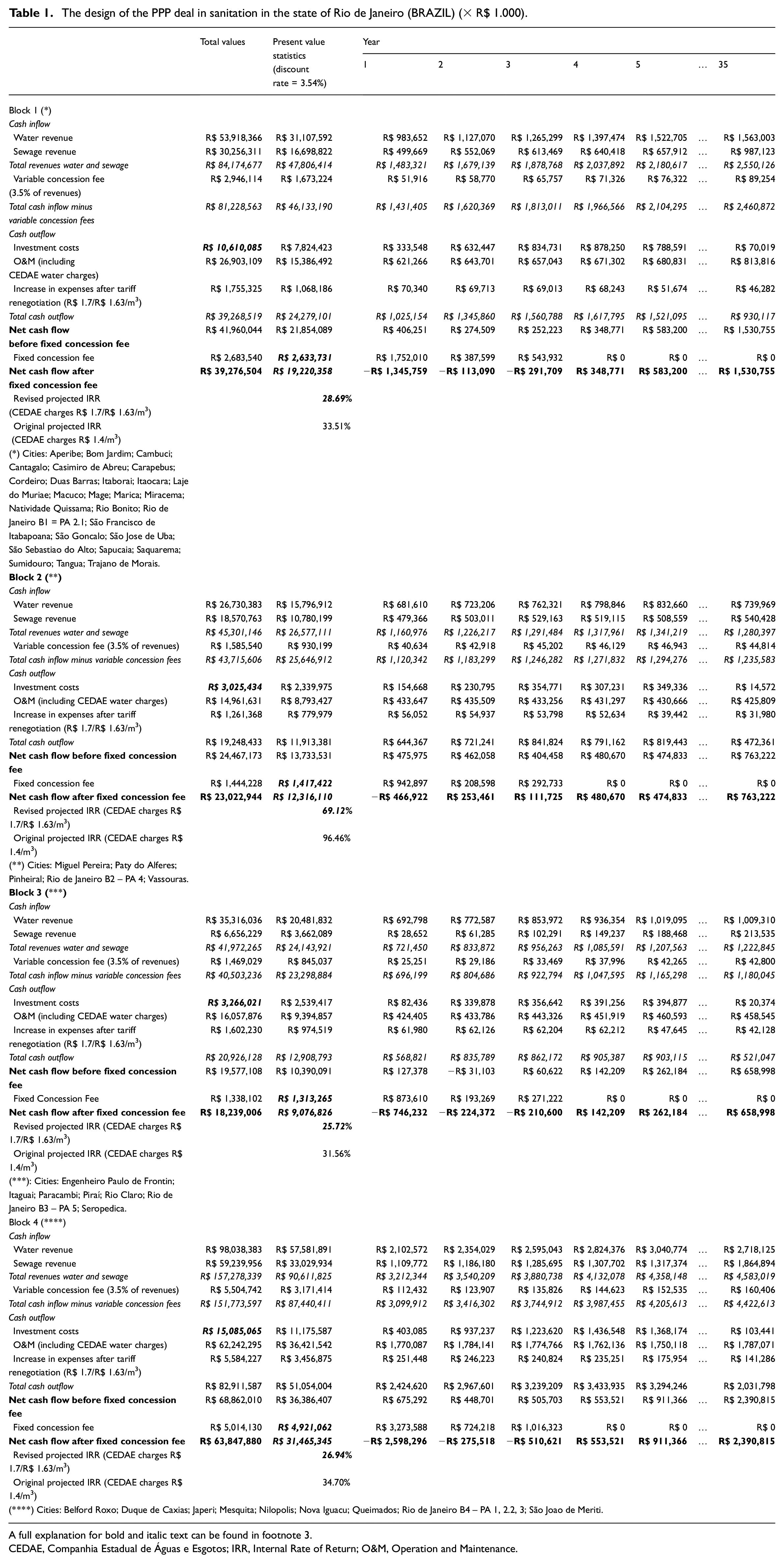

I first fleshed out CEDAE’s financial statements, balance sheets and business plans as well as the pre-viability studies and prospectus elaborated by BNDES. The result is presented in Tables 1 and 2, which provide a block-wise synthesis in terms of the cities involved, the projected costs, revenues, and net cash flows for potential bidders (BNDES, 2020).

The design of the PPP deal in sanitation in the state of Rio de Janeiro (BRAZIL) (× R$ 1.000).

A full explanation for bold and italic text can be found in footnote 3.

CEDAE, Companhia Estadual de Águas e Esgotos; IRR, Internal Rate of Return; O&M, Operation and Maintenance.

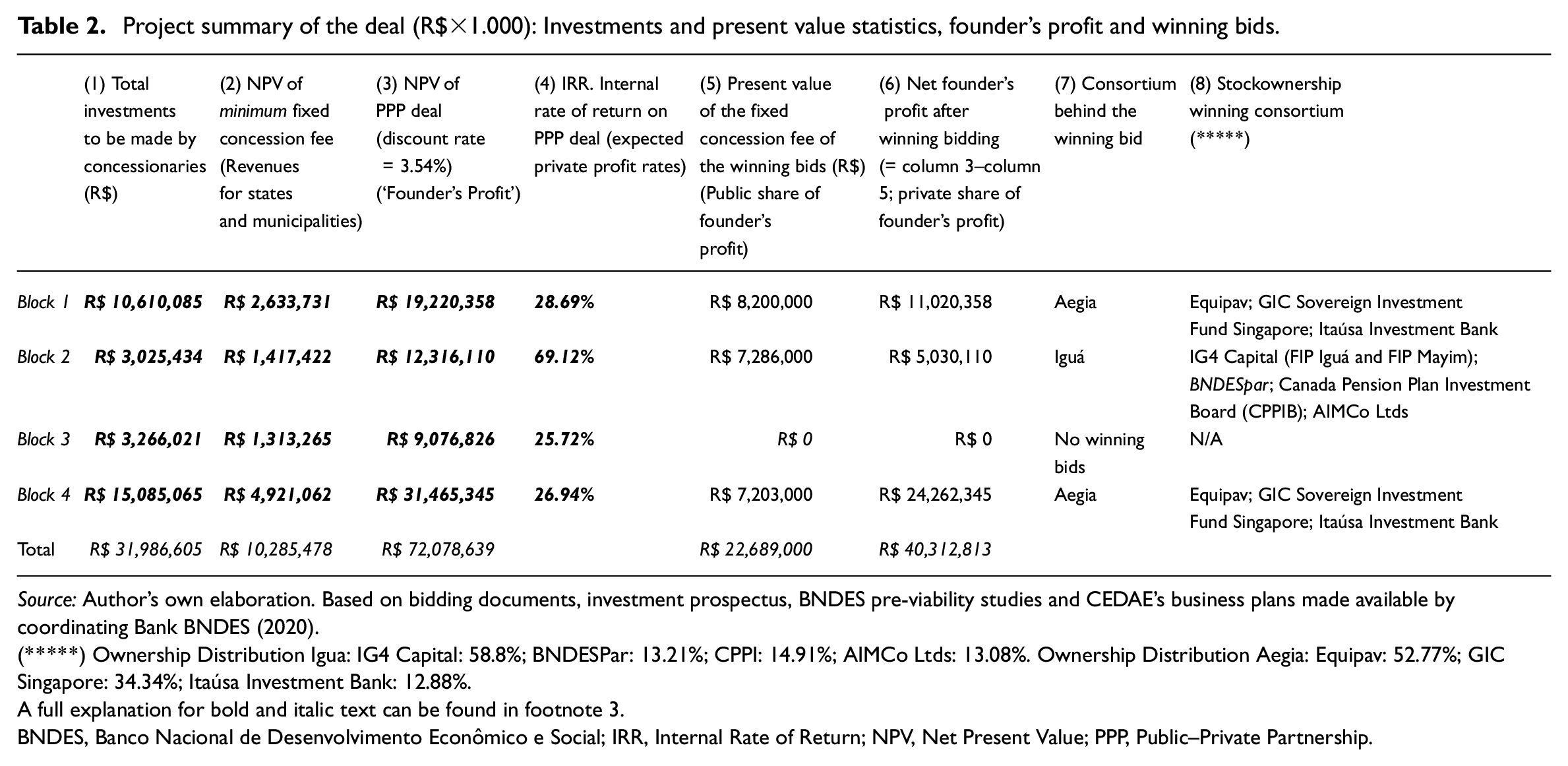

Project summary of the deal (R$×1.000): Investments and present value statistics, founder’s profit and winning bids.

Source: Author’s own elaboration. Based on bidding documents, investment prospectus, BNDES pre-viability studies and CEDAE’s business plans made available by coordinating Bank BNDES (2020).

(*****) Ownership Distribution Igua: IG4 Capital: 58.8%; BNDESPar: 13.21%; CPPI: 14.91%; AIMCo Ltds: 13.08%. Ownership Distribution Aegia: Equipav: 52.77%; GIC Singapore: 34.34%; Itaúsa Investment Bank: 12.88%.

A full explanation for bold and italic text can be found in footnote 3.

BNDES, Banco Nacional de Desenvolvimento Econômico e Social; IRR, Internal Rate of Return; NPV, Net Present Value; PPP, Public–Private Partnership.

Tables 1 and 2 were developed by combining both publicly available information and assumptions behind the model’s projections (Table 1), as well as by producing new insights regarding the expectations of investors, the projections of urban founder’s profit and its rough distribution over state (CEDAE and municipalities) and non-state actors (the consortia of concessionaries and their shareholders) (Table 2).

Except for the column that contains present value statistics, the publicly available information and assumptions are summarised in Table 1. Beyond the expected investments of almost R$31.98 billion, the tender’s financial engineering for the minimum bid price provides the state and municipalities a fixed concession fee of a bit more than R$10 billion for the four blocks during the initial 3 years of the concession (80% allocated to the state; 15% to municipalities and the remaining 5% to a metropolitan fund). The agio, that is, hypothetical additional revenues beyond this amount from the winning bids (based on the highest fixed concession fee offered), will be shared equally among states and municipalities. Moreover, municipalities will receive a variable fee of 3% of tariff revenues during the concession, while the metropolitan fund is allocated an additional 0.5% of revenues collected from cities within the metropolitan area.

In Table 2, I elaborated the present value statistics to trace investors’ expectations and project the generation and extraction of urban founder’s profit for this deal. 3 This is not the kind of information easily obtained from interviews, public sources, or hearings.

Firstly, it requires an assumption regarding the basic money rate to adopt in the discounting procedures. I found the answer in the preliminary contracts elaborated by BNDES (2020). These envisage 26 situations (ranging from ‘extraordinary and unpredictable cost increases’, ‘increases in the price of water charged by CEDAE due to water crises’) that allow a ‘re-composition’ of the financial equilibrium of contracts for private concessionaries. The benchmark discount rate specified for potential contract readjustments to guarantee a zero impact on Concessionaries’ Net Cash Flows is the low-risk money rate on government bonds with maturity in 2050, which at the time of writing was 3.54%.

Next, I elaborated two key statistics. The first was the relatively higher profit rate that is used to discount the contracted flow of income associated with the concession of 35 years (i.e., summarised in the line ‘Net Cash Flow after Fixed Concession Fee’ in Table 1). It reflects potential private investors’ perception of the high-risk profile of publicly owned and managed expected streams of income. As can be seen in the percentages formatted in bold and italic in Tables 1 and 2, the rates vary from 28.69%, 69.12%, 25.72% and 26.94% in blocks 1, 2, 3 and 4, respectively. These represent the equivalent of the internal rate of return that is expected by future owners/buyers on their initial capital investment, whereby the projected flow of revenues exactly breaks even with total cost in present value terms (generating a NPV of zero). 4 Considering that, for each of the four blocks, profit rates are substantially higher than the money rate of 3.54%, this is a potentially good deal for concessionaries and private investors. The second statistic is the NPV associated with unlocking the potential of previously ‘high-risk’, publicly managed water networks through the PPP deal. Prospective operators-investors discount the same expected stream of income derived from the concession (‘Net Cash Flow after Fixed Concession Fee’ in Table 1) with the lower interest rate of 3.54%, which represents the costs of the funds that allows them to buy into this deal. 5 As summarised in column 3 of Table 2, if all blocks receive proposals, the PPP is expected to generate a NPV of R$72.1 billion, distributed as R$19.2 billion, R$12.3 billion, R$9.1 billion and R$31.5 billion between blocks 1, 2, 3 and 4, respectively. 6 It is the equivalent of urban founder’s profit as we now know it, associated with ‘un-tapping’ the potential of CEDAE’s monopoly rights in Rio’s water system.

A final step was to collect the financial information from the effective bidding process that occurred on 30 April 2021. This is summarised in columns 5–8 in Table 2, which traces the distribution of founder’s profit over state and non-state actors except for block 3, which did not receive bids. As shown in column 5, the bidding process generated an agio of more than 150%, considering the difference between the minimum fees in the blocks with winning proposals (approximately R$9 billion for blocks 1, 2 and 4) and the public revenues effectively generated in the auction (R$22.7 billion). These winning bids inject hard cash of R$22.7 billion to state and municipal budgets over and above the stipulated investments of R$31.99 (column 1 Table 2), while the private consortia Aegia and Iguá (columns 7 and 8, further details given later on) are expected to extract the rest of the urban founder’s profit amounting to R$40.3 billion (that is, R$63 billion–R$22.7 billion, the values for the winning blocks in column 3 minus those in column 5).

The sheer size of these figures also reveals why BNP Paribas – after an initial moment of suspense when the federal government threatened to claim its guarantee, sell off CEDAE and spoil the PPP – was happy to renegotiate the external loan from 2017 that matured in December 2020. It clearly recognised that, despite the growth of the original outstanding debt (from R$2.9 to R$4.1 billion), the values that were circulating in the upcoming deal were promising. The result of the auction, which was accompanied by the country’s President and Minister of Finance, was celebrated by the state, CEDAE, BNDES and the press as a show case for the rest of country.

Planning in motion facing an imperfect future that is coming

However, having gone through the reference material that accompanied the origin of the PPP (external loan documents, the federal guarantee and the structural adjustment plan with CEDAE’s privatisation), the literature on the company’s historical deficiencies in providing access to basic sanitation (Dominguez, 2018), and while recognising that less than half of the public share of founder’s profit of R$22.7 billion represented hard cash for the state government, 7 another question emerged: where did all this (fictitious) money come from? After all, CEDAE was the symbol for obsolete state planning and the failure to guarantee the universal right to sanitation.

Answering this question required going beyond differential capitalisation as one of the drivers behind the up-front founder’s profit. After signing this transaction in the present, how will planners reconcile the requirement for extensive future ‘collateral management’ to provide a relatively risk-free future for private operators and investors through the financial readjustment clauses (discounted with low money rates of 3.54%) with their responsibility to guarantee universal access to sanitation at the end of the deal?

This asked for a more detailed examination of how the financial cash flow statements from Table 1 penetrate the regulatory and investment dimensions of planning for basic sanitation in Rio de Janeiro. I obtained this information from secondary studies on basic sanitation in Rio (Dominguez, 2018), work from NGOs such as ONDAS, media coverage, and by connecting with the ‘revealing’ silences in the financial language brought to the table by BNDES and CEDAE. A few examples follow to illustrate the approach.

First, in addition to universalisation, the PPP explicitly promised no future real price increases to final consumers. A closer look reveals how this will work. CEDAE will either be slowly stripped of its cash flows and assets in the future or, as part of the contract arrangement, private operators can pass on ‘unforeseen increases’ in the wholesale price of treated water charged by CEDAE to final consumers. An in-built margin-squeeze of CEDAE will clearly expose this challenging trade-off during the PPP.

Part of the tensions between the state and CEDAE’s planners and the team from BNDES related to the wholesale price for treated water charged by CEDAE to prospective concessionaries. CEDAE’s charges appear in Table 1 as the private operator’s cash outflow associated with operation and maintenance. While CEDAE’s margins were squeezed even more initially, the tariffs were eventually revised from R$1.4/m3 to R$1.7/m3 in the initial four years, and R$1.63/m3 for the 31 years thereafter (yearly indexed to inflation). To illustrate, CEDAE’s average tariff in 2016 was R$3.57/m3 (Branco and Ponciano, 2019), while cities with private concessionaries such as Niteroi charged around R$4.0/m3. Moreover, the relatively simple yearly inflation adjustment of already depressed price levels in the contracts was remarkable when comparing with the state water company in São Paulo, which has detailed four-yearly adjustments that consider financial rates of return on investments. Throughout its negotiations with CEDAE, BNDES used the debatable argument that higher tariffs would negatively impact the financial capacity of concessionaries to expand the network. 8

There were other indicators of margin squeeze. Different from standard practice in renegotiation on concessions, the contracts specify that municipalities are not required to refund CEDAE for its non-amortised investments in distribution networks, which will be used by private operators.

Second, private concessionaries will face a low-risk environment considering that the complex and heavy investment burden associated with the upgrading of informal settlements to provide universal access to sanitation is dealt with through light-touch and omissive regulation that delegates planning responsibilities to concessionaries. For instance, the contracts specify that the allocation of an earmarked amount of R$1.86 billion for interventions in informal settlements is to be designed by the concessionary, which, ‘together with the state and the regulatory agency must indicate the settlements that will receive investments. Subsequently, the concessionary will elaborate an action plan that, in common agreement, shows how progress will be achieved’ (BNDES, 2020). In other instances, the contract provides for conditionalities before investments in slums can be initiated, such as the availability of asphalted roads, drainage systems and public security.

To aggravate, there is neither a detailed geographical distribution of this investment, nor any guarantee whether it will be sufficient to deal with informal settlements. Specific data on slum settlements have only been annexed for the city of Rio itself, which increases the public risk of not attaining universal coverage. A quick look at the historical deficits accumulated in the cities that are part of the deal illustrates what is at stake. In the city of Rio, approximately 93,226 inhabitants are without access to water and 324,624 lack sewage services; the same figures for the other municipalities are 109,034 and 185,434 for water and sewage, respectively (source: Instituto Pereira Passos). While CEDAE itself has never championed investment in slums, the light-touch regulatory framework that underlies this transaction is unlikely to reach the proclaimed objective of better sanitation for all.

From market promoting to an alternative planning project?

Despite its consensual appearance, the transaction has faced considerable resistance and contestation. Pressured by a petition that was signed by 140 entities from civil society regarding the contradictions and lack of transparency in the process, state parliament voted against the regulatory framework and the auction itself. Nevertheless, it was overruled by the governor.

Moreover, significant legal battles have been triggered by entities such as the National Federation of Urban Workers and individual congressmen regarding the blurred responsibilities in the auction. For example, BNDES’ investment wing BNDESpar has a (minority) participation in the total shares of the winning consortium Iguá (see column 8 in Table 2), generating suspicion regarding inside information considering the Bank’s coordination of the transaction. This was reinforced by rumours that the bank would also provide lending of R$17 billion to finance the concessionaries’ payment of the fixed concession fees of R$22.7 billion. 9 The Federal Audit Court has acknowledged the indication of irregularities. The case is now pending in the State Audit Court.

Finally, the Canadian Union of Public Employees, among the biggest labour unions in the country, has demanded that the Canadian Pension Investment Board withdraws from the deal, considering its participation in the Iguá consortium (column 8, Table 2). According to the Union’s president: It is outrageous that our public pension plan for workers is being used to profit from the needs of people for drinking water and secure sewage treatment. These are essential human rights for survival. The access to these services is already deficient and unequal in Brazil. The PPP will only worsen this scenario and we demand our withdrawal.

10

(Author’s translation).

Conclusion

In this paper I have argued that, in times of austerity, collaborative-communicative planning tends to reinforce the making of urban financialisation. To find solutions for the pressing urban challenges in cash-strapped cities and states, planners have framed their conversations with corporations and finance capital around the language of financial models. Trying to extract a part of urban founder’s profit, they have become entangled with productive and finance capital in contradictory ways and contribute to the gradual transformation of cities into abstract spaces, conceived as bundles of income yielding assets.

The heuristic illustration of the urban founder’s profit concept in the PPP of Rio does not stand alone. The approach can be extended to other institutional transactions whereby exclusive public rights to rents and income are shared with private operators and financiers in exchange for a part of the upfront cash that is generated in the process. An increasing number of Brazilian cities and states have now creatively by-passed national restrictions regarding access to capital markets through public securitisation companies. The latter are designed to un-tap the potential of municipal assets by bundling future streams of income such as tax and social housing finance receivables, often under unfavourable conditions. Likewise, cities such as São Paulo and Rio de Janeiro have experimented with urban redevelopment projects that use the sale of additional building rights certificates in capital markets to finance social housing and urban infrastructure (Klink and Stroher, 2017). Not unsimilar to what has been discussed by part of the literature on the circulation of planning practices (Healey, 2013) and on urban policy mobility (Baker and Temenos, 2015; Theodore and Peck, 2012), some of these bad practices have started to travel to other places in Brazil, frequently with the help of transfer agents (consultants, former officials of city and state governments, development banks like BNDES, etc.) (Klink, 2020). This scenario suggests an emerging multi-scalar, networked ‘making’ of financialisation by cities.

For all these reasons, it is urgent to substitute ‘the invited spaces’ of participation (Miraftab, 2009) in collaborative-communicative planning with an alternative, radical project that is grounded in different space-time epistemologies. While it is beyond the scope of this paper to flesh out the details of such a counter-hegemonic proposal, my analysis suggests two dimensions (see also, Randolph, 2007). One is related to the creative tension that is mobilised in the Lefebvrian metropolis between the abstract spaces of neo-liberalisation and financialisation and the differential ones associated with daily life experiences. The latter generate complaints about the existing city and demands for something better.

The second connects the imperfect present time, marked by absences and precarities, with a nearby future whereby cities provide for the common good. In the modernist Habermasian project of collaborative-communicative planning, this asymptotic ideal of the just city is never achieved and generates frustration because of the recurrent mismatches between expectations and realisations. In the financialised metropolis, discounting indeed brings the future closer to the present; but, as astutely observed by Aglietta, it is a future coordinated by the market’s subjective ‘self-transcendence’. As such, it produces cities that are a risk-free bundle of ‘tradeable income yielding assets’ (Guironnet and Halbert, 2015: 19).

While the prospects of counter-hegemony in Rio and other places should not be exaggerated, there is no inherent reason to discard that the effectively growing discontent in Brazilian cities will eventually constitute open ended, ‘invented spaces of participation’ (Miraftab, 2009) along these differential space-time epistemologies.

Footnotes

Declaration of conflicting interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The research that was the basis for this paper was funded by the Conselho Nacional de Desenvolvimento Científico e Tecnológico (CNPQ – National Council for Scientific and Technological Development), call ‘Universal C’ (project 405914/2018-0).