Abstract

On November 1, 1994 an Air Passenger Duty (APD) was introduced in the United Kingdom, and since, this tax continues to be controversial. This article examines the effect of the ADP on UK outbound tourism demand for 10 international destinations. An autoregressive distributed lag model is developed and income, price, and tax elasticities are estimated. The income and price elasticities obtained, ranged between 0.36 and 4.11 and −0.05 and −2.02, respectively. The estimated tax elasticities suggest that the implementation of APD had a negative effect on UK outbound travel for five destinations and the demand is inelastic to changes in taxes although the magnitudes vary across destinations. The general message is that although the stated objective of APD is to reduce travel and associated carbon emissions, the effectiveness of APD, however, has been marginal; travelers are prepared to pay more in the main to maintain their demand.

Introduction

Within tourism research, the proliferation of studies on specific issues such as sustainability, demand forecasting, and the impact of climate change on traveler’s behavior illustrates the growing interconnections that exist between policy making at the government level and its wider implications for both the tourism sectors and travelers. What is evident from the research by Mak (2006) is that the last 20 years has seen governments utilize the tourism sector as a source of revenue generation through direct and indirect taxes as these taxes often have a neutral effect on political popularity when they are targeted at nonvoters (e.g., inbound tourists) or when the tax is targeted at luxury goods such as tourism. One interesting development from Mak’s (2006) synthesis of tourist taxation is the apparent recent utilization of the climate change agenda and recognition that “tourism gives rise to many environmental problems, and taxes correct for negative environmental externalities” (Mak 2006, p. 256). This seemingly sweeping statement does not give sufficient credence to the growing importance of how perceived problems associated with tourism (e.g., the contribution of air travel and tourism to climate change via emissions from flying) may be politically harnessed for wider tax revenue purposes, albeit justified on environmental grounds. We argue in this paper that simply imposing crude taxes on outbound tourism is not a sophisticated policy instrument if the underlying objective should be to reduce outbound demand by air to reduce pollution and the contribution to climate change. Instead, the crudeness of the policy measures that are sometimes used have little direct impact on the wider environmental problem of encouraging more sustainable travel behavior. The result is that crude policy instruments simply raise taxation revenue and do not address the underlying problem they set out to tackle. This illustrates that tourism-related policy making is fundamentally flawed or poorly thought out in many instances. The notion of unintended consequences is particularly salient in this context as it reflects a fundamental lack of understanding of the challenges facing policy makers. For example, in the UK context, a lack of joined up thinking in the central government demonstrates that commissioned research on tourism from DEFRA (Miller et al. 2010) has not been acknowledged by the DfT and Treasury in making changes to the APD although existing research shows that changing traveler’s behavior to reduce the impact of tourism on climate change would require a protracted series of measures and interventions (Miller et al. 2010).

This research study illustrates that the scale of the outbound tourism by air from the United Kingdom is a protracted problem in relation to climate change that needs careful thought, modeling, and analysis of policy options rather than crude and unsophisticated policy instruments. One needs to recognize that air travel for outbound tourism has passed through a series of distinct stages of growth from the 1930s when it was largely a novelty and used by business travelers. Since the 1930s it has slowly become enshrined in consumer culture as it has become more accessible and affordable. During the 1950s, outbound tourism demand by air begun to expand from this novelty factor, with the sudden growth of the package holiday by air in the late 1950s and 1960s through to its rapid growth in the 1970s. What is notable is that during the 1980s and 1990s new drivers of growth (e.g., relative drops in the price of air travel and the emergence of the low-cost phenomena) created additional demand so that many middle-class families routinely undertook several overseas trips a year as affluence and the accessibility of outbound travel expanded. These trends have continued during the new millennium, albeit slowing down in recent years as a result of the recent economic recession. However, what has developed is a cultural norm that travel by air to go on holiday is a right that cannot easily be curbed (Miller et al. 2010). The scale of this recent growth in demand for outbound travel is demonstrated by the number of passengers passing through UK airports that has risen from 30 million in 1970 to over 218 million in 2011. This is in excess of rates of economic growth and reflects the willingness to spend money on overseas holidays in pursuit of hedonistic behavior, especially with the freedom offered by low-cost airlines and the rise of one-way air fares creating choice and flexibility alongside the package holidays. More concerning are the forecasts by the Department for Transport (DfT) (2003) which predict that outbound travel by air from the United Kingdom is expected to rise to 500 million by 2030. This obviously has serious implications for the environment as aviation is one of the fastest growing causes of carbon dioxide emission and is a source of other greenhouse gases while aircraft noise can lead to additional disturbances (Enviroaero 2012). According to the DfT (2003) White Paper “The Future of Transport,” carbon emissions from the aviation sector are expected to reach 18 million tons by 2030 and domestic flights will be responsible for only 3% of this, illustrating the relative importance of outbound trips by air and its contribution to environmental pollution. The total emissions from air travel could represent almost 25% of United Kingdom’s contribution to global warming by 2030 and given that air travel is a discretionary form of transport for holidays, then there is certainly scope to look at this as one potential area for additional policy instruments to curb this insatiable demand for overseas travel.

Turning to the monetary cost of externalities related to climate change, local air quality and noise attributable to the aviation sector was estimated in a report by DfT and HM Treasury (2003). Assuming the cost of carbon at £70 per ton and taking into account expected future demand, in 2000, the cost of carbon emission by UK passenger aircraft was expected to rise from £1 billion in 2000 to over £4 billion in 2030. The cost of local air quality for all passengers at UK airports could fall between £119 and £236 per year and noise may cost up to £25 million for UK airports. The UK Government, however, stated that it was committed to finding a solution to the problem of climate change by taking measures that should lead to a reduction in carbon dioxide emissions by 60% by 2050 (DfT 2003). In this respect, it argued that the use of economic instruments including taxes that “can help ensure that aviation bears the external costs it imposes on society” (DfT 2003, p. 31) were a necessary feature. The issue we examine in this paper is how such taxes have impacted upon demand and whether they have made any demonstrable difference to traveler behavior or are travelers simply prepared to more to travel? The principal measure employed by the UK government to seek to ensure aviation bears the external costs is the Air Passenger Duty (APD) introduced in 1994. While it was widely acknowledged that this was a “blunt” measure, it was expected to assist in leading the airline industry in internalizing its externalities by raising the cost of air travel and, thus, coercing consumers and producers into contributing towards the real cost of flying. APD is quintessentially a price instrument which is expected to influence the demand for international tourism to and from the United Kingdom. Yet there are also wider economic and political issues associated with outbound tourism demand which are pertinent to this paper and may also underpin some of the willingness of the UK Treasury to impose APD when one considers the effect of outbound travel on the UK Travel Account.

International tourism, both inbound and outbound, has grown significantly since the 1970s and made a notable contribution to the UK economy. The United Kingdom has run a travel account deficit since 1986. In 1986, the deficit was equivalent to almost 10% of that year’s international tourism receipts and then increased to over one-third in 1990. Ten years later, the proportion of the deficit in international tourism receipts had almost doubled, reaching 75.76% in 2000. In the early 2000s, outbound spending exceeded inbound earnings by more than £10 billion (Euromonitor International 2012). The travel account deficit, however, decreased from £18.5 billion in 2008 to £11.5 billion in 2009 and again to £11.2 billion in 2010. The volume of outbound tourist flows fell by more than 1% in 2010 to just under 58 million trips, while outbound tourist expenditure grew 7% to around £31 billion (Euromonitor International 2011). Therefore, from a purely economic perspective, policy instruments that could induce more domestic holiday taking instead of overseas trips are perceived as highly beneficial from a tax policy perspective as well as for retaining consumer spending in the United Kingdom. Thus, as a large majority of British outbound travelers use air as their preferred mode of travel, the imposition of APD affects a sizeable consumer group. Euromonitor International (2011) illustrated that air travel accounted for about 83% of total departures from the United Kingdom between 2005 and 2010. The question that this poses for this research paper is, To what extent is the APD affecting consumer behaviour in United Kingdom?

The aim of this study therefore is to develop a tourism demand model for international travelers from United Kingdom with the objective of assessing the effect of APD on tourism flows from the United Kingdom. The contribution of this paper to the wider tourism literature and research agenda on tourism taxation and its relationship to traveler behavior and climate change is twofold. First, there are a limited number of studies on APD, and none have attempted to quantify the extent to which this tax is influencing British passenger flows by estimating the ADP elasticity of demand. Second, this study focuses on outbound travel from the United Kingdom, which still remains a largely undeveloped area of research despite the growing academic literature on tourism demand modeling. With some very notable exceptions (e.g. Coshall 2006; Li, Song, and Witt 2004), the outbound market is still remarkably neglected in most countries as a focus as it is often of less concern to policy makers in terms of the potential to leverage the growth of employment and regional tourism economies (aside from airport-related employment growth). Consequently, attention tends to be inbound tourism and the ability to grow that form of demand as the principal driver of tourism policy despite the obvious economic loss of revenue that outbound demand may pose to taxation revenue in a domestic setting. To address the research question, an autoregressive distributed lag model for UK outbound tourism is developed and estimated using quarterly data from 1994:Q4 to 2010:Q4 for the 10 most popular destinations of the travelers. These are France, Germany, Spain, Italy, Greece, Turkey, Egypt, the United States, Hong Kong, and Australia. Together, they make up approximately 58% of the outbound market of the United Kingdom. The second section presents the empirical literature on taxation and tourism demand. The third section discusses the econometric models used. The fourth section presents the empirical findings of the long-run and short-run outbound tourism demand models, and comments on the estimated demand elasticities and the fifth section concludes the study, highlighting future areas for research and some of the policy implications of the study.

Taxes and Tourism Demand

Recent progress in research on tourist taxation has been greatly assisted with the rise of Tourism Satellite Accounting (TSA) as a tool as it begins to help identify the scope and scale of tourist taxes in specific countries and their wider contribution to national accounts. Though not substantial at the macro-level, the taxation of the tourism industry is significant at the industry level as many countries’ TSAs confirm. From the existing research and the TSA data, there are two types of taxes that are commonly payable by travelers. First, there are entry and exits taxes that include APD, also known as the Airport Tax or Departure Tax and, second, in the United Kingdom, spending by travelers is subject to an ad valorem tax of 20% (which in other countries is termed goods and sales taxes or sales taxes). Additionally, travelers face other user charges such as the airport terminal charges and some visitors may have to apply for a visa before visiting the United Kingdom, which is an indirect tax on traveling.

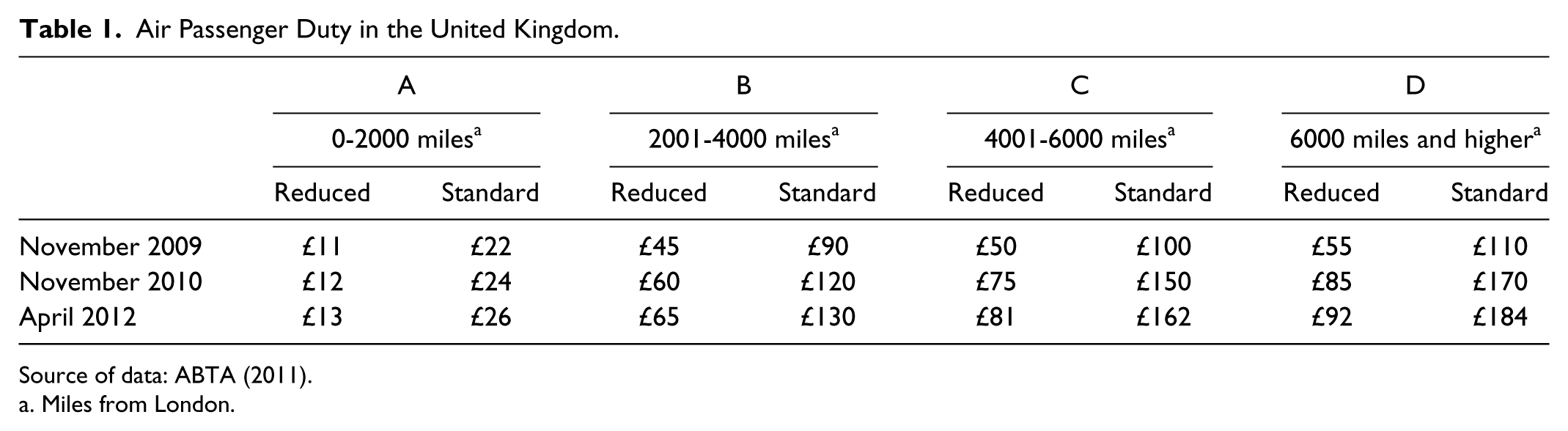

In the United Kingdom, APD was introduced in November 1993 in the Treasury Budget and came into effect on November 1, 1994. It falls entirely upon the consumers. The structure of this tax has undergone a major transformation since it was first introduced. In 1994, £5 per seat was imposed for UK and EU routes and £10 per seat for international travel to all other destinations. Three years later, these rates were doubled. The structure of this tax was reformed in 2001 when return domestic flights were exempted and a class division was introduced, with the lowest and standard classes charged at £5 and £10, respectively, for travel to EU and £10 and £40, respectively, for travel to other destinations. These four rates were doubled in 2007 and in 2009, as more emphasis was placed on the spatial component with the geographical distance from London the starting point for these calculations when four bands were identified. The structure of the tax is outlined in Table 1.

Air Passenger Duty in the United Kingdom.

Source of data: ABTA (2011).

Miles from London.

According to the United Nations’ World Tourism Organisation (UNWTO) (1998), APD was expected to be attractive for the British government because of the following features:

It is levied on those best able to pay, such as business travelers and the more affluent travelers who can afford air rather than other cheaper forms of transportation.

It is partly levied on overseas visitors who have no vote in the United Kingdom.

The airlines act as collection agencies.

It can be absorbed in the ticket price, which is normally shown separately on the tickets. Travelers are likely to accept a tax or duty more readily than an increase in ticket price.

It represents only a small proportion of the ticket price. However, with deregulation of the airlines leading to an increase in budget air operators and more discounting of ticket prices, APD is representing an increasing proportion of the ticket price, especially if similar levies are introduced at destination airports.

It has proved an effective revenue-raising mechanism. However, taxes and user charges are extra costs to the traveler and may hinder the growth of tourism demand, especially for the more price-sensitive consumers.

While taxation research has been informative in terms of how it has shaped the thinking by governments on the potential revenue they can raise from tourism and to fund developments in destination marketing and convention centre operation in the United States, little systematic research has been conducted in recent years linking the growing agendas of taxation, demand modeling, and the newer public sector agenda of climate change and reducing CO2 emissions from tourism. By linking these three agendas in this study, we are able to illustrate the wider application of the research to a managerial focus even though that tourism demand modeling has attracted much attention both from practitioners and academics. It is a notable area where engagement with industry is critical to illustrate the implications of the demand modeling for policy making that may have been undertaken without a clear focus on the intended outcomes in a public setting (although confidential, government’s modeling of the expected (intended) effect of taxation and air travel will have occurred prior to the policy changes and on increasing the level of taxation).

A comprehensive review by Li, Song, and Witt (2005) found that 420 studies were published on tourism demand modeling and forecasting over the period 1960–2002, which illustrates the pedigree of this emergent subfield within the wider context of tourism research. As Song and Li (2008) show, tourism forecasting research has to rely predominantly on secondary data, collected by governments, international organizations, or other agencies (often not with academic use in mind). Because of the nature of such data, the number of tourists arriving at particular destinations from particular departure points, is the most frequently used measure of tourism demand. The tourist expenditure (or receipt), or the tourist expenditure on particular tourism product categories (e.g. meals, shopping and sightseeing), is the second most used variable to estimate tourism demand, though a few research studies have used other variables, including tourism revenues, tourism employment, travel imports and exports, length of stay, and nights spent at tourist accommodation, as the measure of tourism demand (see Song and Li 2008; Lim 1997). The vast majority of international tourism demand studies concentrate on inbound tourist flows. However, a number of pertinent studies have estimated outbound tourism demand including Song, Romilly, and Liu (2000), Coshall (2006) and Li et al. (2006) for the United Kingdom, Lim (2001) for South Korea, Campbell and Mitchell (2007) for Barbados, Halicioglu (2010) for Turkey and Seetaram (2012) for Australia.

The most popular functional form of tourism demand equation is the double-logarithmic (or log-linear) regression model, which enables researchers to directly estimate the elasticity of the dependent variable with respect to the changes in a set of explanatory variables. Among several factors affecting tourism demand, the most prominent ones include the level of income, price/relative price in destination compared with the origin and competing destinations, exchange rates between the currencies of origin and destination, and transportation costs. Many empirical studies also use additional explanatory variables such as tourism imports/exports, price of oil, travel cost (e.g., airfare), travel distance, time trend, and other qualitative factors (e.g., tourists’ demographic profile, household size, population, special events such as an Expo or the Olympic Games, and energy crises).

Recent econometric studies appear to present both the short-run and long-run estimates of the demand elasticities (Song, Gartner, and Tasci 2012). Empirical studies indicate that the income elasticity estimates vary a great deal but generally exceed unity, confirming that international travel is a luxury item and that demand for tourism is inversely related to the price of the trip.

Typically the relationship between the price of international travel and demand is modeled through the inclusion of the real exchange rate, which is used as a proxy for prices (Lim 1997). For example, in Li et al. (2006), a time-varying parameter error correction model is used to measure the degree of price sensitivity of UK travelers to Europe. The analyses show that in the case of France, Greece, Italy and Spain, the demand is price elastic, implying that small changes in the price will lead to greater than proportionate changes in the expenditure of British tourists at these destinations. Seetaram (2010) also used a dynamic panel data model to show that the demand for international holidays to Australia was price inelastic but sensitivity to changes in prices increases considerably in the long run. When comparing sensitivity to prices by purpose of visit from France, Germany, Spain, Italy, Ireland, The Netherlands, and the United States, Cortés-Jiménez and Blake (2011) concluded that with the exception of German and Italian travelers, holiday travelers were the most sensitive to changes in prices. The lowest price elasticities were registered for business travelers. Generally German and American travelers tend to be the least sensitive to changes in prices.

These studies, however, do not specifically analyze the effect of tourism and travel taxes on consumers. These taxes add to the cost of international travel and can act as deterrents as discussed before. In the absence of a specific tax variable in a model, its effect can be expected to be incorporated in the coefficient of the proxy for prices. There is now a growing literature on the effect of tourism taxes on demand but unlike the current study, the majority has focused on international arrivals.

The early study of the effect of the imposition of taxes by Mak and Nishimura (1979) used 690 observations of visitors’ parties from mainland United States to study the effect of the imposition of a tax on hotel rooms in Hawaii. Their analysis indicated that the tax would have only a negligible effect on the number of trips from the United States and on the duration of stay in Hawaii. A 1% room tax was expected to dissuade only 0.16% of tourists from going to Hawaii. Additionally, they found that although the tax would have been beneficial in terms of generating revenue for the government, the extra revenue would have been raised at the cost of loss of income for the private sector. In a further study of tourist taxation, Mak (1988) found that tourists were more price sensitive than previously thought, implying that tourism taxes are not fully exportable and that to a certain degree the tax incidence fell on local businesses. More recently, Aguilo, Riera, and Rossello (2005) found that in the Balearic Islands, the imposition of a per capita, per diem tax of €1 could be expected to reduce the number of arrivals from Germany, United Kingdom, France, and the Netherlands by 117,113. A subsequent study by Tol (2007) evaluated the effect of taxes on airline emission at a global level, simulating the effect of the impositions of three levels of carbon taxes: these were $10/t C, $100/t C and $1000/t C, using the parameters described above. The results suggested that the imposition of a kerosene tax of $1000/t C would reduce international tourism by 0.8%, leading to a fall in CO2 emission by 0.9%. However, the number of international travelers would remain the same and in the absence of alternative modes of transport for short-haul trips, travelers would shift from long-haul travel to medium-haul modes. Furthermore, the airfare elasticity of demand was very low, suggesting that a fairly large increase in price was required to initiate a significant change in demand. The tax imposed, however, only raised prices by a relatively low amount. The effect of taxes on international arrivals to the United Kingdom was investigated by Durbarry (2008), which included the United Kingdom’s 11 main markets and data from 1968 to 1998. A gravity model was used to show that tourism coming to the United Kingdom was highly price sensitive, with an estimated price elasticity of −2.3. The study concluded that increases in the price of holidays in the United Kingdom will have a significant negative effect on international arrivals and stated that one of the main arguments for taxing tourism is that the burden is expected to fall on “nonvoters.”

Forsyth et al. (forthcoming) is one of the very few studies that have studied the economy-wide effect of a departure tax and it found that although the imposition of a departure tax can have negative consequences for the Australian tourism industry, it is nevertheless beneficial for the economy as a whole. The detrimental effect on the tourism industry is more than offset from the increase in the gross domestic product and the welfare effect of the additional taxes collected. These results are sensitive to the value of the demand elasticities used. Similar exercise in the United Kingdom will enhance our knowledge on the cost of the APD imposed. In order to assess the eventual impact of the APD on the British economy, the information on the degree to which travelers respond to these taxes are crucial. This article seeks to fill in the gap in the literature by studying the effect of APD on the British consumers. A demand model for outbound tourism from the United Kingdom is developed in the next section.

Methodology

Demand Model

Following the empirical literature in modeling outbound tourism demand, we constructed the following single equation model for the United Kingdom in double logarithmic form:

where Qit is the aggregate tourist flows from the United Kingdom to destination i at time t, Yit is the real aggregate income in the United Kingdom at time t, pit is the relative price variable adjusted by exchange rates at time t, TAXit is the travel tax directly charged to the UK residents traveling to destination i at time t, and uit is a random error term that is assumed to be normally distributed with a zero mean and constant variance. Two types of dummies, seasonal dummies and one-off event dummies (e.g., the terrorist attacks in the United States on September 11, 2011, the outbreak of SARS and the global financial crisis), were included in the model. The substitute price variable was excluded because the inclusion of such variables leads to incorrect signs of other independent variables in equation (1). It is expected that β i > 0 (because higher real income should lead to greater economic activity and then stimulate outbound tourism demand), γ i < 0, and η i < 0 (because both the price of a tourism product and the tourist taxation will have negative impact on the tourism demand). The estimation results regarding prices found in tourism demand studies are rather uneven as it seems that no consensus about the appropriate range of this coefficient has been reached (Halicioglu 2010).

Dynamic specification of the demand model

A dynamic model specification, known as the autoregressive distributed lag model (ADLM), was adopted in this study to construct the outbound tourism demand models in the United Kingdom. The ADLM bounds and t-tests proposed by Pesaran, Shin, and Smith (2001) were employed to test the long-run relationships between the demand for outbound tourism in the United Kingdom and its main determinants. This approach has been applied by Chon et al. (2010), Song et al. (2011), and Song, Gartner, and Tasci (2012). The ADLM bounds test approach has several advantages over other traditional cointegration methods (Narayan 2004; Song et al. 2011). For example, the bounds test is still reliable even if the model suffers from the problems of omitted variables and autocorrelation.

In order to reflect short- and long-run dynamics into the demand function of outbound tourism in the United Kingdom, thus, equation (1) can be rewritten in the following form:

where p is the optimal number of lags determined by the Akaike information criterion (AIC) and the Schwarz Bayesian criterion (SBC). In cases where there if is a conflict between AIC and SIC, the AIC was used to determine the optimal lag length for the following two reasons. First, the complexity of the model will be penalized more heavily by SBC than by AIC, which may lead to contradictory model selections; second, AIC tends to asymptotically perform better than SBC in the empirical studies in terms of model collection (for details of the AIC and BIS comparison, please see, Anderson, Burnham, and White 1998; Yang 2005). Lagged dependent variables were introduced as the explanatory factor to capture persistence effects of the tourist’s behavior.

In equation (2), the λ coefficients specify the long-run relationship between the variables: there is no long-run relationship if the values of λ are zero. The null hypothesis of the bounds test (or F test) is H0:

Data

Ten major source markets, France, Germany, Spain, Italy, Greece, Turkey, Egypt, the United States, Hong Kong, and Australia were examined given their high market shares in United Kingdom’s total outbound tourism. In total, they accounted for an average of 57.8% of the United Kingdom’s outbound market over 2008–2010. Quarterly data from 1994:Q4 to 2010:Q4 were used to estimate the demand model. Data on resident departures were obtained from Quarterly Overseas Travel and Tourism published by the Office for National Statistics (ONS 2012). The data of Reduced Rates for APD (which are applied when the passengers are carried in the lowest class of travel on any flight unless the seat pitch exceeds 1.016 meters) was collected from HM Revenue and Customs (2010, 2011). The data on the real gross domestic product (GDP) index (2005: 100), consumer price indices (2005: 100), and exchange rates index (2005: 100) were collected from the International Statistical Yearbook published by International Monetary Fund (2012).

Empirical Results

Results of Unit Root Tests and Bound Tests

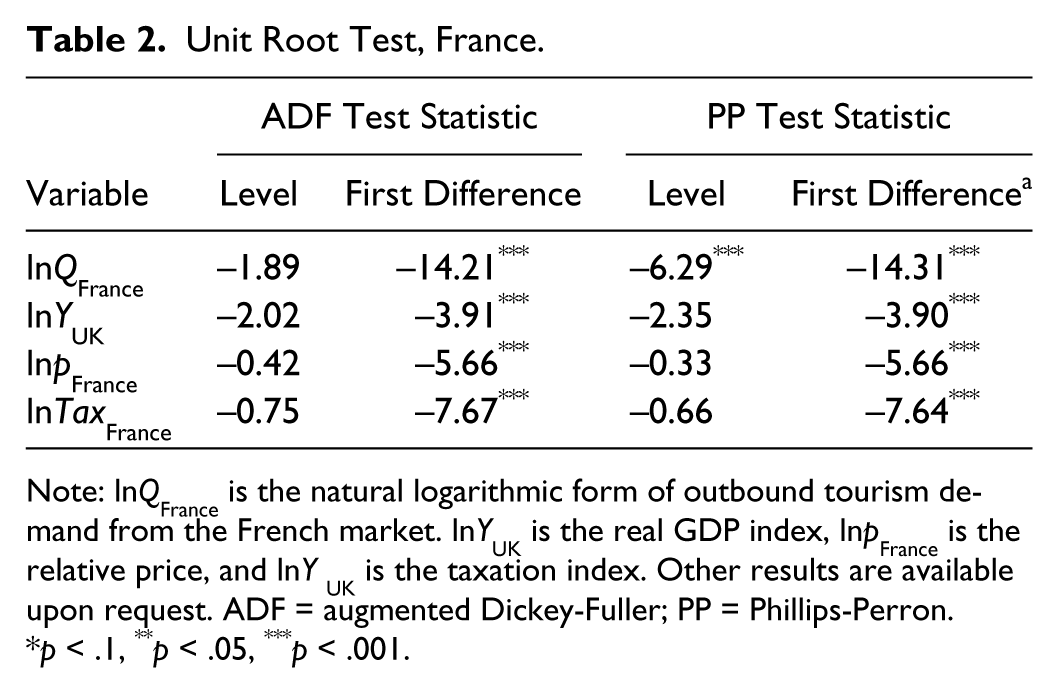

Before testing the long-run cointegration relationship, two types of unit root tests, the augmented Dickey-Fuller (ADF) test and the Phillips-Perron (PP) test, were employed to test the stationarity of model variables in this study. The aim is to ensure that none of the variables in the models are integrated of order 2 or above, thus satisfying one assumption of the Pesaran, Shin, and Smith’s (2001) bound test. The unit root test results indicate that all of the model variables were either I(0) or I(1) (see Table 2, taking France as an example). In such a situation, the ADLM bound test is appropriate and valid to derive the long-run and short-run parameters of outbound travel demand.

Unit Root Test, France.

Note: lnQFrance is the natural logarithmic form of outbound tourism demand from the French market. lnYUK is the real GDP index, lnpFrance is the relative price, and lnY UK is the taxation index. Other results are available upon request. ADF = augmented Dickey-Fuller; PP = Phillips-Perron.

p < .1, **p < .05, ***p < .001.

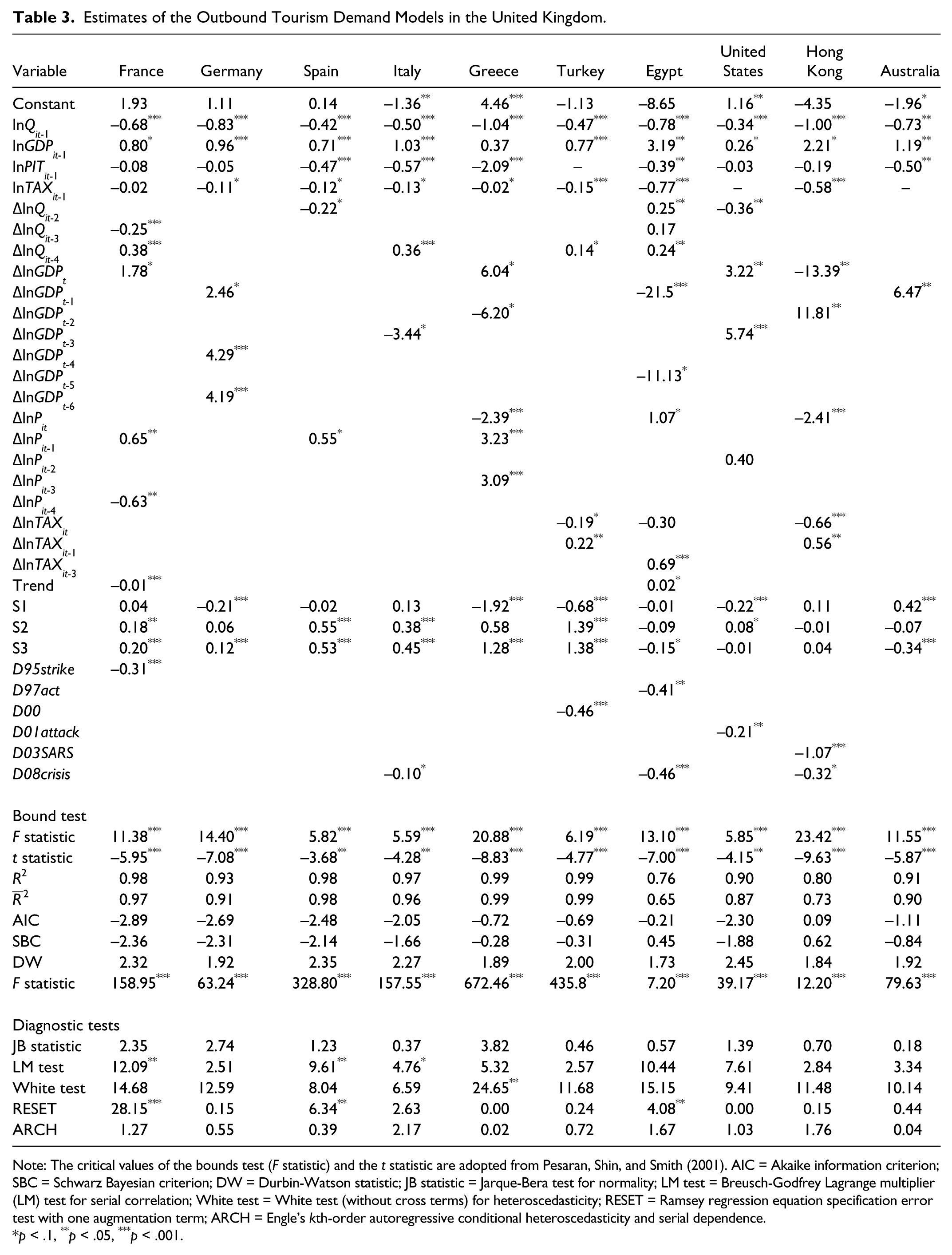

Before calculating the long-run elasticities, equation (2) was first estimated using ordinary least squares (OLS) for all 10 outbound markets. All models were estimated in the natural-logarithm form, but the dummy variables entered the equations in nonlogarithmic form. The general-to-specific modeling approach recommended by Song, Witt, and Li (2009) was adopted to achieve the final models. It can be seen from Table 3 the 10 final models passed the goodness-of-fit test, achieving reasonably good R2 and adjusted R2 values (>0.90 for seven models, 0.8 for the Hong Kong model, and 0.76 for the Egypt model). One reason for a lower R2 and adjusted R2 for the Egypt model could be due to the omission of some important variables from the model (Uysal and Crompton 1984).

Estimates of the Outbound Tourism Demand Models in the United Kingdom.

Note: The critical values of the bounds test (F statistic) and the t statistic are adopted from Pesaran, Shin, and Smith (2001). AIC = Akaike information criterion; SBC = Schwarz Bayesian criterion; DW = Durbin-Watson statistic; JB statistic = Jarque-Bera test for normality; LM test = Breusch-Godfrey Lagrange multiplier (LM) test for serial correlation; White test = White test (without cross terms) for heteroscedasticity; RESET = Ramsey regression equation specification error test with one augmentation term; ARCH = Engle’s kth-order autoregressive conditional heteroscedasticity and serial dependence.

p < .1, **p < .05, ***p < .001.

The diagnostic tests presented in Table 3 show that 5 of the 10 destination equations—Germany, Turkey, United States, Hong Kong, and Australia—passed all tests, suggesting that these models are well specified. The rest of the models failed at most two tests. The models of France, Spain, and Italy appear to have problems of serial correlation. The failure of the LM tests may be explained by the high degree of correlation between the lagged dependent and explanatory variables (Morley 2009). The models for France and Spain also suffer from the problem of inappropriate functional form, as suggested by the RESET test. The Greek model failed the heteroscedasticity test.

The estimated coefficients of the seasonal dummies in Table 3 suggest that the demand for outbound travel in the United Kingdom varies according to the time of year: demand is highest in the third quarter (i.e., July, August, and September), which is found to be positive and statistically significant for all models except for three markets (i.e., Egypt, the United States, and Hong Kong). The modeling results indicate that UK outbound tourism demand has suffered from a series of adverse events in the recent 15 years, with notable examples such as the 9/11 attacks; war in the Middle East; terrorist activity in Madrid, London, Glasgow, and elsewhere; outbreaks of severe acute respiratory syndrome (SARS) and bird flu; and the global financial crisis. The initial model specifications incorporated all the possible dummy variables to capture the influences of such shocks but the final models only kept those with significant t statistics. The SARS outbreak in 2003 substantially reduced the UK residents’ demand for traveling to Hong Kong, as the variable D03SARS is found to be negative and statistically significant. The global financial/economic crisis in 2008 (measured by D08crisis) is found to have had negative impacts on the demand of three outbound markets, including Italy, Egypt, and Hong Kong. The terrorist attack on September 11, 2001 (measured by D01attack), substantially reduced the attractiveness of the United States, as this dummy variable is statistically significant in the American model. The strikes that affected France during the last months of 1995 (measured by D95strike) brought a significantly negative impact on the outbound tourism demand by the British tourists. The outbound demand for travel to Turkey (measured by D00) was severely affected by the flooding (in October and November).

Long-Run Demand Elasticities of Outbound Travel

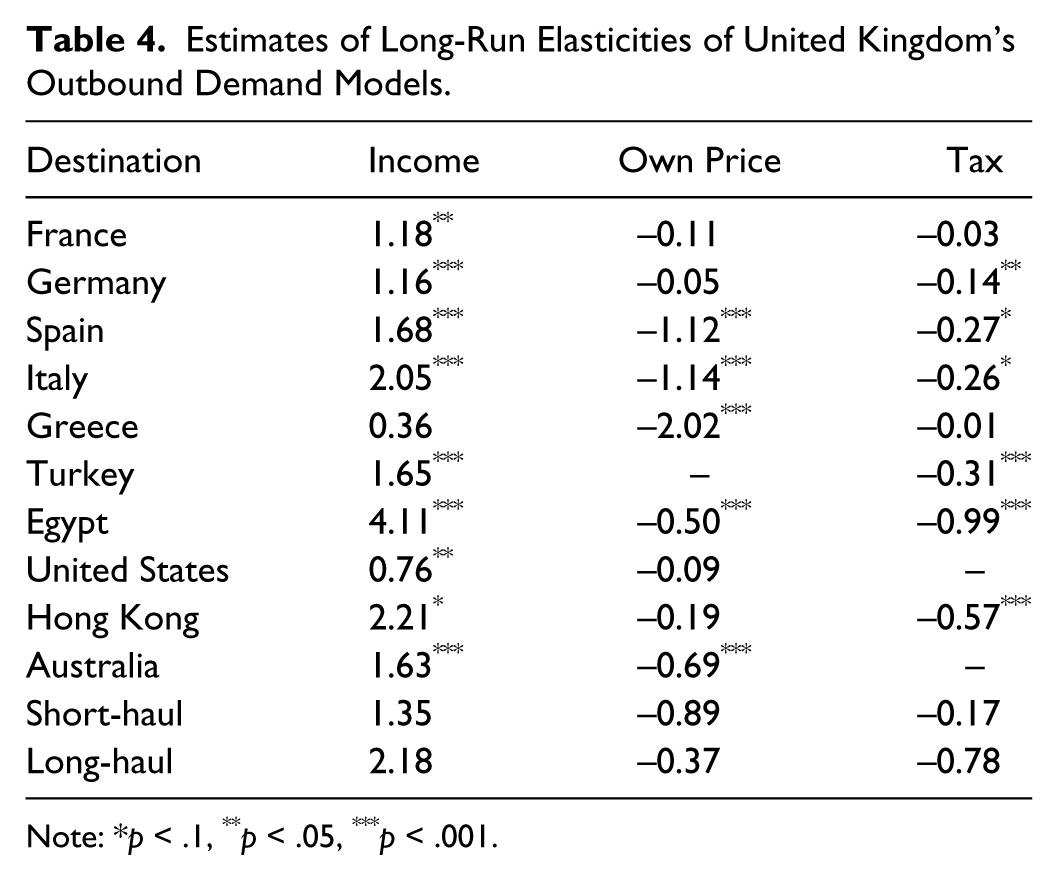

Based on the estimates in Tables 3 and 4, the estimated coefficients of the income and tourism price variables were all statistically significant and had the expected signs. That is to say that the demand for outbound travel by UK residents to all 10 destinations under study was positively related to by the income of the UK residents, and negatively related to the tourism prices in the destinations and APD. The estimated demand elasticities of outbound travel are summarized in Table 4.

Estimates of Long-Run Elasticities of United Kingdom’s Outbound Demand Models.

Note: *p < .1, **p < .05, ***p < .001.

Income elasticities

Existing studies (e.g., Onafowora and Owoye 2012; Halicioglu 2010) imply that, all things being equal, the higher the real income level of a country, the more likely are its citizens to be able to afford to purchase foreign tourism products/services. The estimated income elasticities, which ranged from 0.36 to 4.11, were positive and significant at the 5% level for 8 of the 10 destinations. This indicates that the demand for outbound travel in the United Kingdom was strongly responsive to the conditions of United Kingdom’s economy. In case of Hong Kong, the coefficient was significant only at the 10% level. The income elasticity of outbound travel to Greece was insignificant, suggesting that income was not a driving factor for United Kingdom’s outbound travel to Greece. Long-run income elasticity values were obtained for the period from 1994 to 2010. The demand for United Kingdom’s outbound travel was income elastic for 8 of 10 destinations as the income elasticities exceeded 1, meaning that an income change would cause a more than proportionate change in demand for outbound travel. The effects of income changes on outbound travel were distinct from one destination to another. On average, the magnitude of the effect of income in the long-haul destinations was found to be larger than that in the short-haul destinations, with the average elasticity estimates being 2.18 and 1.35, respectively. There is some evidence that income elasticities have declined over time in long-haul markets (Civil Aviation Authority 2005). The Civil Aviation Authority argues that the long-haul income elasticities (North America and the Rest of the World) appeared to have declined somewhat between 2000 and 2003. In this study, the income elasticity in the American model was found to be less than unity (0.76). This may suggest a full maturity of this destination for travelers from United Kingdom where the income elasticity is unity or below, or in effect when leisure travel starts to be considered more as an essential product rather than as a luxury (Graham 2000). However, this conclusion is yet to be further justified with more empirical evidence.

Own price elasticities

The coefficients of own price variable measure a change in the number of outbound travelers to an overseas destination due to a change in the prices of travel and accommodation in that destination. As expected, the estimated own price elasticities had a negative sign for all nine countries except for Turkey, suggesting that outbound travel demand was negatively affected by the overseas prices of travel and accommodation. The own price elasticities were shown to be significant in 5 of the 10 countries (i.e., Spain, Italy, Greece, Egypt, and Australia). Overall, estimates of the own price elasticities for either long- or short-haul destinations were found to be less than unity, which means that the United Kingdom’s outbound travel demand was less responsive to own price changes. As a cross price variable was excluded, the own price elasticity in this study is essentially a combination of the destination’s own price elasticities with cross price elasticities (Morley 1998). It is also worthy to note that this study did not differentiate business and leisure travelers, which may make the demand for outbound travel by the UK resident to be price inelastic, as international business travelers are less sensitive to prices changes in tourism compared to leisure travelers (Gillen, Morrison, and Stewart 2003).

In the case of France, Germany, the United States, and Hong Kong, the price elasticities were not significant at the 10% probability level. The own price elasticity for Turkey was not estimated because it has a wrong sign, which may be due to the poor quality of the data used (Schiff and Becken 2011). Despite these, the final model for Turkey is still presented in Table 3, because it had expected signs for all variables kept in the model, achieved a high value of R2 and adjusted R2, and passed all diagnostic tests. The comparison of elasticities in the long-haul versus short-haul destinations is shown in Table 4. Generally, the majority of short-haul markets appear to be relatively more price elastic in UK residents’ demand for outbound travel (with price elasticities of less than −1 in the case of Spain, Italy, and Greece), and the long-haul markets tend to be price inelastic, with the values varying from −0.09 to −0.69. In other words, British outbound travelers were more sensitive to price changes in their overseas travel and accommodation when selecting short-haul destinations such as Spain, Italy, and Greece, but less sensitive when choosing long-haul destinations such as Egypt and Australia. The reason for higher price elasticity of demand for short-haul travel is that for a short distance travel, it may be relatively easier to select a substitute destination that offers similar products/services as long-haul travel.

Sensitivity to taxation changes

Changes to the cost of international trips, resulting from changes in tourism taxation policy, have significant effects on tourism demand and the performance of the tourism industry, as well as indirect effects on national income, foreign currency earnings, fiscal revenue, and job creation. Hence, the degree of responsiveness of tourism demand to changes in prices (or taxes) becomes an important element for policy analysis. As expected, the coefficient of the tourist taxation variable, or the APD, was found to have a negative sign and be statistically significant (at 5% and 10% levels) in 5 of the 10 destinations. It indicated that an increase in APD was likely to result in a decline in the number of international departures from the United Kingdom. The implementation of the UK APD is found to curb or distort demand for 5 of 10 destinations. This is consistent with the finding from existing literature that any policy action resulting in higher travel cost (e.g. taxes) will lead to a decline in passenger traffic demand (InterVISTAS Consulting Inc. 2007).

The absolute estimates of the taxation elasticity were less than 1 for all destinations. They indicate that a 1% increase in the APD alone is expected to bring a decrease of less than 1% in the number of UK residents traveling abroad. In other words, United Kingdom’s outbound travelers will not react to the increase of APD by substantially changing their demand. Such increase in the travel cost will have an effect on air travel, but this effect will not necessarily manifest itself solely to reduce the total tourism demand. Tourists may choose to change their travel plans to reduce the cost of their flight or simply reduce the other expenses they will incur on their trip, rather than cancel the flights which will have consequences for the destination. The insensitiveness of APD changes to the total outbound tourism demand could also be due to that APD may only be a small proportion of the total trip cost. This may explain why the number of departures to Australia and to USA does not seem to be sensitive to the APD as the proportion of tax to the total cost of the holiday is likely to be small enough not to have a deterrent effect. This is consistent with Tol (2007) who argued that taxes imposed need to be fairly large in order to have a significant effect on travelers’ behaviour. In contrast, travelers to France have the option of choosing alternative modes of transport and thus avoiding the APD altogether. The APD applies only to air transport and this study used the aggregate departure data from all modes of transport. Thus the effects of the APD on demand for different travel modes or travel for different purposes cannot be separated. Therefore the interpretations of the empirical results need to be treated with caution.

Conclusion

The focus of this study was to evaluate the impacts of imposing APD on the UK residents traveling overseas. The findings suggest that changes in taxation policy, namely APD, had negative influences on five of the ten destinations. In other words, this illustrates the type of factor which is out of the control of the destination managers where policy interventions in the home country have a direct effect on the volume of travel to overseas destinations in varying degrees. It also highlights the interconnected nature of tourism flows at a global scale where specific interventions and changes to the source area can directly shape the nature of demand to specific destinations. This is a good illustration of how economic policy has direct spatial consequences. This suggests that the use of APD has a range of implications for tourism policy in an area that has hitherto not been a major concern for governments—managing the volume of outbound tourism because of pressing demands in other parts of government to address climate change issues. Likewise, the imposition of APD was not a “tourism” policy per se but a transport policy that illustrates the often weak position of tourism policy within national governments where associated areas of activity (e.g., transport has a major impact on the actual shape and form of tourism, both inbound and outbound). Such policy then has both intended and unintended consequences for tourism policy and visitor flows, illustrating how important interdisciplinary research that cuts across conventional disciplinary boundaries is to fully appreciate the impact of policy shifts. The absolute estimates of taxation elasticities were reported to be less than unity suggesting that outbound tourism demand in the United Kingdom was inelastic with respect to tourism taxation changes. It is noted that the magnitude and significance level of taxation elasticity vary across destinations. But the general message is that although the stated objective of APD is to reduce travel and associated carbon emissions, the effectiveness of APD has been marginal. Travelers are prepared to pay more in the main and ignore the wider issues of environmental pollution.

The number of UK resident departures was observed to be largely driven by the income, as measured by the real GDP. The income elasticities were found to be correctly signed and were generally greater than 1 but the degree of responsiveness of UK residents traveling abroad varied widely from destination to destination. Generally speaking, outbound travel in the United Kingdom was found to be income elastic. The results suggest that travel and tourism are luxuries, and should be taxed accordingly. The results of this study confirm the findings of Tol (2007) and Miller et al. (2010), who suggested that a much greater level of taxation is required if the objective is to affect a change in the current ideology of air travel that is cheap and accessible to all. As our analysis confirmed, the own price variables have been consistently regarded as one significant factor in determining tourism demand. The estimated own price elasticities were found to have expected signs (i.e., less than 0) for 9 of the 10 destinations and to be statistically significant for 5 destinations, suggesting that outbound travel demand by the UK residents was negatively influenced by the relative price of travel and accommodation in overseas destinations. The own price elasticities varied from −0.05 to −2.02 and behaved differently across countries, where short-haul destinations were found to be more responsive to changes in own prices than the long-haul destinations (–0.89 vs. –0.37). It is noteworthy that the inclusion of both the own price variable and tourist taxation variables may affect the magnitude of the estimated coefficients on each other because taxation is also regarded as one aspect of own price or cost of tourism products/services. That is to say, the problem of multicollinearity may exist. There is still a lack of firm evidence about the degree of price sensitivity of the demand for UK outbound tourism and the question of whether tourists will travel elsewhere when faced with higher APD and other tourism taxes remains to be unresolved. Geographical displacement or diverted demand is a major area of research that remains underresearched in relation to the effect of such policies on travel. There is a need for further quantitative information about how tourists respond to changes in implementing other types of taxes payable. Important directions for further research include further disaggregation of different types of travelers (business vs. leisure) and different modes of transport to further investigate the effects of introducing and changing levels of tourism taxation. Further research that begins to examine the reciprocity of tourism flows between countries and the extent to which taxation affects these flows is a new area to develop alongside the effect of alternative forms of taxation or restraint upon air travel. One area being widely discussed is the development of personal carbon allowances that allow choices to be made in how such budgets are deployed in day-to-day and more discretionary activities such as holidays so more personal responsibility is fostered as advocates of responsible tourism have been arguing for over a decade.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.