Abstract

The success of a city’s retail core is largely dependent on the composition and organization of its merchant constituents. Not only should the price-point and products of a city’s retail align with its resident and visitor demographics but the stores should be strategically balanced to maximize consumer spending and interest. Heritage destinations dependent on the tourism market should pay special attention to this issue, assuring their visitors a valuable shopping experience while simultaneously preserving the destination’s cultural appeal. This case study considers the rapidly evolving shopping district of Charleston, South Carolina, focusing specifically on the retail core’s recent influx of chain merchants to what was once predominantly a local main street. A historical account, paired with an in-depth survey of merchants, is presented. The research builds on previous studies that have considered the issue of merchant mix from the perspective of the city’s stakeholders, tourists, and residents.

Introduction

This case study explores the growth of national chain stores, at the expense of local merchants, in the main shopping and tourism district of Charleston, South Carolina. Two previous Charleston-based papers have considered the issue. The first, by Litvin and Jaffe (2010), was a qualitative study based on a series of in-depth interviews with Charleston stakeholders, to include tourism industry and local government leaders. The second, by Litvin and DiForio (2014) and published in this journal, extended that inquiry via a two-pronged quantitative study that surveyed both Charleston residents and tourists to determine those groups’ shopping behaviors and attitudes toward King Street, the city’s main street. The current research captures and analyzes the views of the remaining important stakeholder group, King Street merchants. How the city’s merchants feel about the changing nature of their city’s downtown will add to our understanding of an issue of importance to the local community, to include those within the city’s significant tourism industry. Charleston’s popularity as a heritage destination makes the city an ideal location for study.

Charleston, South Carolina, and Historic King Street

The city of Charleston, which attracts close to five million tourists annually with its historical charm and nearby beaches, has been touted by Condé Nast Traveler as America’s premier tourist city each of the past four years, and acclaimed by Travel+Leisure as the second (behind Kyoto) “Best City in the World” three years running. Charleston’s emergence as a premier tourist destination, however, has been a recent phenomenon. Not many decades ago, the city would not have been found on any “best of” lists. With a downtown largely abandoned as a result of suburban flight, mid-twentieth-century Charleston languished with boarded up storefronts, depressed property values, and a lack of commercial trade (Stock 2006, E22). The beginning of the turnaround can be traced to the 1975 election of Mayor Joseph P. Riley, as this paper is written the nation’s longest serving mayor. Against significant opposition, Mayor Riley’s first major initiative was construction, on a mostly vacant lot in the heart of downtown, of what is today the 440-room four-star Belmond Charleston Place Hotel. Commenting on the hotel’s catalytic impact, Stock (2006, E26) observed, “[W]hat started as a trickle of new development was about to flood the length of King.” Soon to follow Charleston Place was Saks Fifth Avenue, an impressive if then incongruent newcomer, which opened across King Street from the hotel. With each passing year, new restaurants, local boutiques, and regional and national chain stores were added to the retail mix. Thanks to these new merchants, plus the success of an ambitious streetscape redevelopment plan (see Crotts and McNitt 1998 and Litvin 2005), downtown Charleston, “the part of the city that had long been ‘too poor to paint, too proud to whitewash’ . . . was suddenly spiffy and neat” (Hicks 2014). Today’s King Street, one of “America’s [Ten] Best Shopping Streets” (per U.S. News and World Reports; Fineman 2011), is a vibrant and charming two-lane street flanked by bluestone slate sidewalks, palmetto trees, and elegant nineteenth-century storefronts; anchoring a downtown that has remained human-scale, walkable, and architecturally faithful to its historic past (Ashworth and Turnbridge 1990).

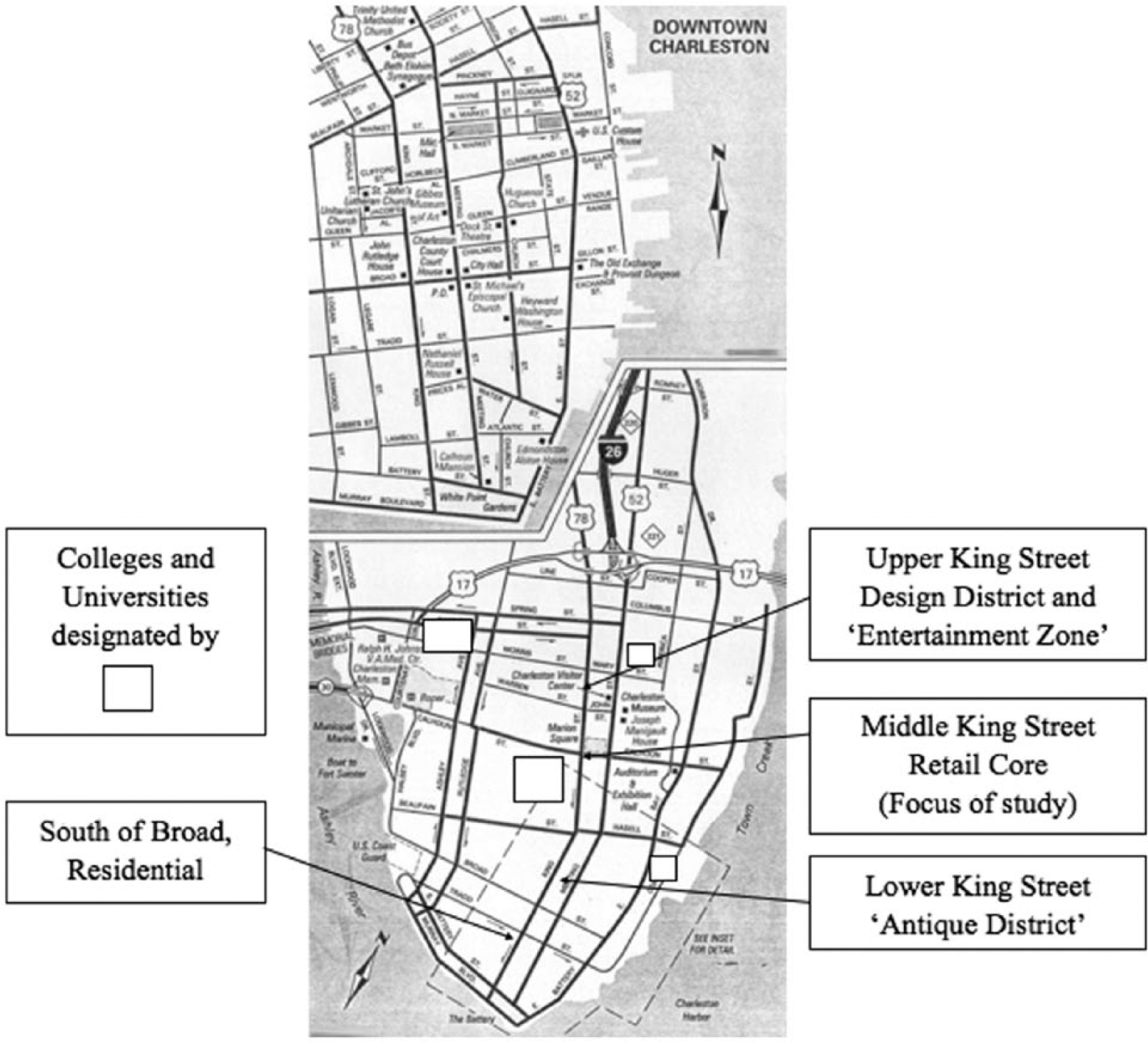

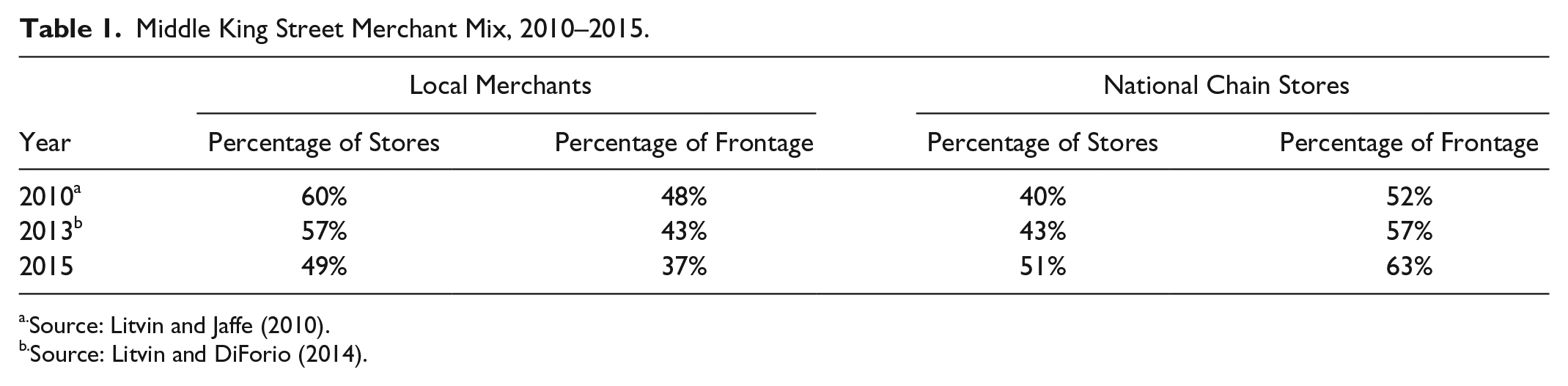

Transformation of King Street has been accompanied, however, by significant commercial gentrification. Turn back the clock three or four decades, and one would find a full range of product offerings in stores, with few exceptions owned by local merchants. Over time, particularly following the arrival of Saks Fifth Avenue, the ratio of local merchants to national chain stores began to shift. Litvin and Jaffe (2010) conducted a census of merchants along Middle King (the retail heart of the street; see Figure 1) and found, undoubtedly for the first time in the city’s rich history, a balance that had tipped in favor of national merchants, with chain stores accounting for 40% of Middle King storefronts and 52% of its retail frontage. When Litvin and DiForio (2014) repeated the census in 2013, the percentage of Middle King national chain stores had increased to 43%, occupying 57% of frontage. A current census finds the trend unabated. Today, a majority (51%) of Middle King merchants are national chain stores, occupying almost two-thirds (63%) of its frontage. These range from ultra-deluxe Louis Vuitton, Gucci, and Kate Spade, to discount retailers H&M, Forever 21, and Rack Room Shoes. (Table 1 summarizes the five-year trend.)

King Street Map Charleston, South Carolina.

Middle King Street Merchant Mix, 2010–2015.

Source: Litvin and Jaffe (2010).

Source: Litvin and DiForio (2014).

Given this backdrop, the key questions to be addressed herein are, Does the trend toward national chain stores concern the city’s downtown merchants? Should it concern them? And, are there lessons to be learned, for Charleston as well as for other tourism-based heritage cities?

The work that follows should be viewed as a case study, using Charleston as an example for other cities. As noted by Stake (1978, 7), “It is the legitimate aim of many scholarly studies to discover or validate laws. . . . [However], in fields . . . where inquiry can be directed toward gathering information that has use other than the cultivation of laws,” cases are an appropriate approach. Stake continued, that a well-targeted case, with a focus on a representative “bounded system,” establishes “the basis for naturalistic generalizations” and is thus a well-suited method for those involved in expansionist versus reductionist pursuits. It is our goal that this Charleston-based case study, adding the voices of merchants to those of previously studied stakeholders to include tourism leaders and government officials, residents, and visitors, will help expand our knowledge, provide a basis for future case studies in other locales, and ultimately lead to theory development that can enhance policy and governance to assist downtown development in Charleston and other heritage cities.

Fundamental to the discussion that follows is the concept of stakeholder theory, which supports the notion that an entity, in this case a heritage city, will find greater success when listening to the inputs and understanding the needs and all relevant parties. Sheehan, Ritchie, and Hudson (2007, 64) referred to a triad of players that comprise an urban area’s stakeholder group. The three members identified were the city, its hotels, and the destination marketing/management organization. The authors add, “the extent to which members of the triad can effectively relate to one another and combine their complementary resources is posited to be an important determinant of success.” To this triad, we propose adding the voices of the city’s retail merchants, clearly stakeholders both with strong vested interest in the success of the city and whose actions influence that success. Per Zehrer and Hallmann (2015, 124), all members of a destination’s stakeholder group “play a pivotal role for the development of the destination. It might even increase the overall power of the destination and shape its future.” Particularly relevant to the discussion that follows, as noted by Martinez and Olander (2015), the concepts of stakeholder participation, social sustainability, and sustainable development are intertwined. We thus are pleased to add the missing voice of the city’s merchants to this case study of Charleston and its historic main street.

Theoretical Background

Shopping

Per Goeldner and Ritchie (2003), shopping represents the single most popular activity among both domestic and international tourists, with more than 60% of domestic and 90% of international tourists incorporating shopping time into their vacations. Weaver and Oppermann (2000) similarly observed that retailing has progressed from an associated service activity to a major attraction in its own right, accounting for almost 30% of tourist dollars spent in Australia—a number in line with the one-third estimate Snepenger et al. (2003) extrapolated from their review of several U.S. studies. In fact, Turner and Reisinger (2001) indicate that shopping has become, for most destinations, the second most important source of tourist expenditures, exceeded only by accommodations. Commented Cachinho (2014, 132), “Due to the ever-changing array of goods and services, and the fascinating environments in which to buy them, for many people, shopping is no longer a basic activity to satisfy consumer needs; it has become a pleasurable ‘leisure experience’ in itself.”

Tenant Mix

A considerable amount of research has been published on the science of retail tenant mix. This has predominantly related to shopping centers and malls. Briefly, what we learn from this literature is that macro-scale tenant mix, referring to the conglomeration of business establishments within a shopping center/mall, is the key ingredient in determining commercial success and optimizing economic benefit. Per Brown (1994), simply controlling which tenants to allow is not enough. Instead, management must consider customer shopping patterns. Based on these patterns, Brown (1994) advised that stores of similar quality selling similar products should be clustered, allowing consumers to exercise comparison shopping, resulting, he determined, in higher spending. Building on the theme, Ibrahim and Galven (2007, 241) commented, “the [shopping center/mall] management team cannot take on tenants simply because they can afford to pay the rentals. The management should strictly evaluate each tenant and determine if the tenant will be suitable to . . . the tenant mix.”

While merchant selection and placement policies would seem to equally apply to a city’s main street, it is recognized that unlike private shopping centers/malls where the developer and center manager have total control regarding rental decisions, the public sector is far more complex. Commenting on this complexity, Bruwer (1997) and Litvin and DiForio (2014) both noted how the issue of property rights poises a significant challenge for city planners looking to balance their community’s retail development.

Maturation Models

Both Litvin and Jaffe (2010) and Litvin and DiForio (2014) considered lessons imparted by the tourism literature’s destination maturation models as King Street’s changing vendor mix was examined. The common theme among these models is the concept of predictive development (Russo 2002) and an inherent “Devil’s Bargain” (Rothman 1998), with destinations that encourage tourism warned of a likely growth pattern that proceeds through stages commencing with initial discovery, continues through growth and maturity, and ultimately leads to decline. Most distinguished among destination maturation models is Butler’s (1980) Tourism Area Life Cycle [TALC]. An offshoot of the TALC, and the model deemed most germane to the current study, is Snepenger et al.’s (1998) Downtown Area Life Cycle [DALC], which looks specifically at the lifecycle of a tourist area’s commercial district. A brief overview of the DALC, with stages that mirror Butler’s, follows:

The first stage of the DALC is Exploration, which depicts a downtown retail space with local merchants catering to residential consumers. During this stage, few tourists visit the area. As tourists begin to discover the location, the destination progresses to a stage of Involvement. During this stage, local retailers continue to serve the immediate community and the shopping space is enjoyed by both residents and tourists. Continued tourism growth leads to Development, with a higher-end clientele targeted and served by new up-scale restaurants and boutiques, some of which have displaced more conventional stores. Eventually, overpriced tourist-focused merchandise and a continued loss of resident shoppers results in downtown progressing to a Consolidation phase. At this point, the redundancy of tourism-oriented merchandise and the loss of local flavor results in tourists also losing interest in the shopping district, ultimately leading to the model’s final stages of Stagnation and Decline (Snepenger et al. 2003).

As noted above, Charleston, as a tourism destination, has received much recent recognition. The city has also enjoyed impressive tourism growth. Table 2, summarizing the city’s accommodation tax collection numbers over the last decade, reflects this growth. On the surface, all would seem well. But what lies ahead? Both previous King Street merchant papers (Litvin and Jaffe 2010; Litvin and DiForio 2014) concluded Charleston had progressed beyond Exploration and Involvement, likely now in the Development stage . . . not unhealthy, but, arguably moving in that direction as the DALC points to a future of diminishing returns and uncertainty. Concerned by this, the authors of the two above-referenced King Street papers sought out the views of those who governed, lived in, and visited Charleston, as these related to the city’s merchant mix. What they found, however, was little concern and certainly no alarm. Litvin and Jaffe’s (2010, 309) interviews revealed that city tourism and government leaders felt the issue of the encroachment of national chain stores warranted monitoring, but that “the current state represents an acceptable point of balance between local and national retailers.” Similarly, Litvin and DiForio’s (2014, 497) surveys of both residents and tourists revealed that both populations “noted the high ratio of national chain stores, yet expressed a high degree of satisfaction with the city’s retail core.”

Accommodation Tax Collections, Charleston, SC.

Source: City of Charleston Comprehensive Annual Report, Department of Budgets, Finance & Revenue Collections (2015).

The current study considers an additional and important set of voices, those of King Street merchants. Despite the benign nature of the two earlier studies’ findings, the question of the impact of national chain stores in a city’s historic district is of sufficient importance to warrant further research. Perhaps the city’s merchants, folks dependent on an attractive and vibrant downtown, both as a place for locals to shop and as an attraction for visiting tourists, will share a new perspective. Learning the views of this additional stakeholder group should be of value and interest to those in Charleston, as well as, on a more macro basis, industry and government leaders in other tourism-oriented cities as they consider the health of their community’s retail core.

Research Method

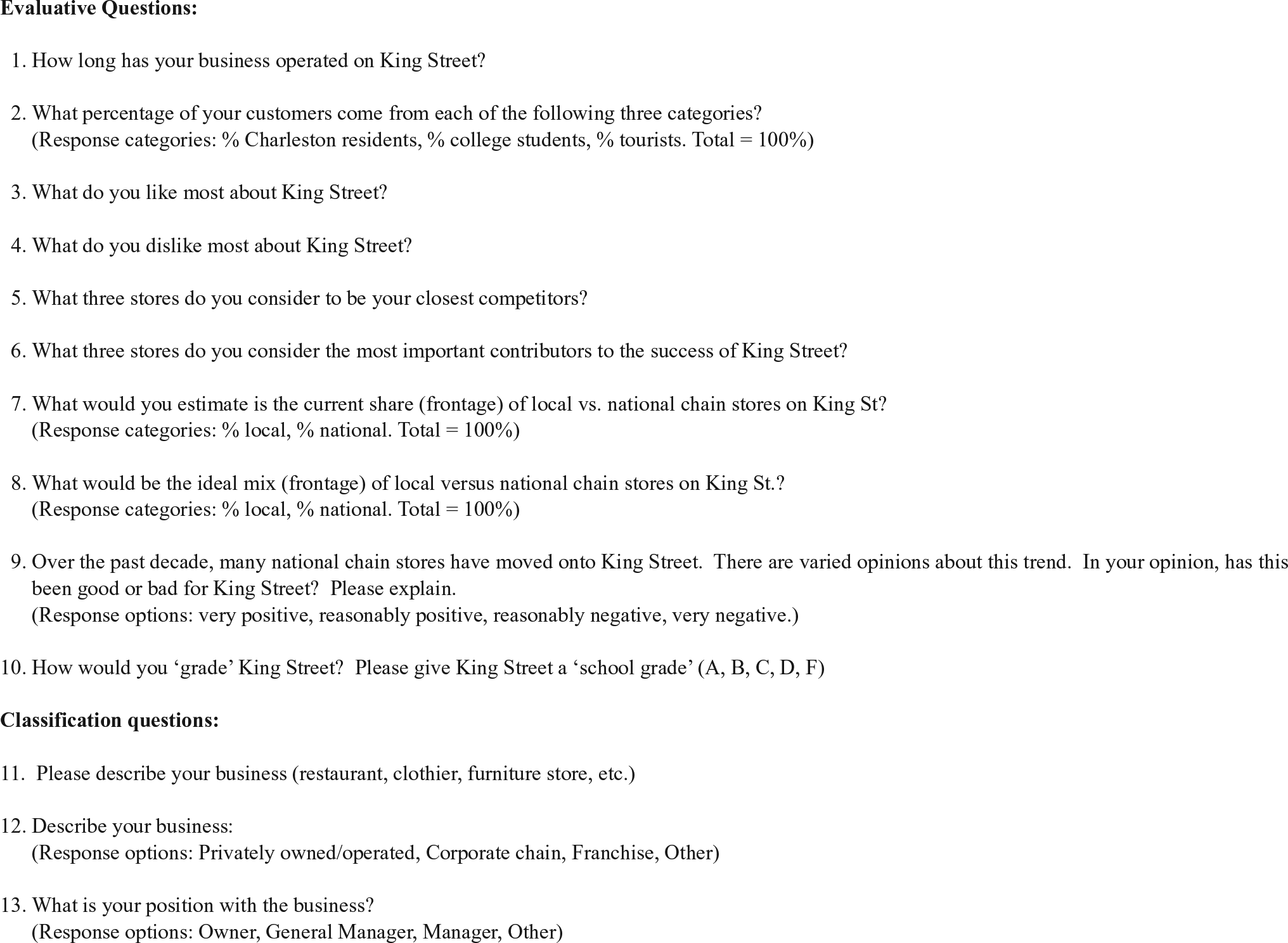

Survey requests were distributed by hand to each of the 96 Middle King Street retail merchants, to include those in the King Street half of the Shops at the Belmond Charleston Place Hotel. Restaurants and the few non-retailers with King Street frontage were not included in the exercise. At each storefront, the owner or manager was approached, or if not available, the highest-ranking person was identified. This person was introduced to the study and its purpose was discussed. If agreeing to participate, the owner/manager was given an envelope that included the survey instrument, an explanation of the research, and a standard university IRB disclaimer that advised participants they were under no obligation to participate, were free to not answer any question they wished to avoid, and promised anonymity within any published findings. Included with the survey instrument was a stamped and addressed return envelope. The return envelopes were coded to record individual store responses, allowing a second round of surveys to be distributed to nonrespondents ten days later. The instrument, a mix of quantitative and open-ended short answer questions (see Figure 2), was estimated to take approximately 10 minutes to complete. The question set was designed to elicit the merchant’s opinion regarding the state of King Street and its merchant mix. A total of 51 responses were received. These reflected the views and opinions of more than half (53%) of the Middle King merchants. While 51 data points is relatively small for quantitative research, the merchants surveyed represented the entire population as defined. Katz’s (1989) essay “Penurious Strategies for Parsimonious Research” recommends such an approach, encouraging researchers to employ a census of a homogeneous test population versus sampling of a broader population, thus allowing analysis without concern for sampling error that is often a problem for smaller-scale research.

Questions used from survey instrument.

The majority of survey responses were prepared by the store manager/general manager (n = 37, 72%), with the next highest number completed by the store owner (n = 10, 20%). The respondent group appears to have provided a fair representation of the King Street merchant population. There was a good mix of tenure (7 merchants had been open on King Street less than 1 year, 6 from 1 to 3 years, 6 from 3 to 5 years, 11 from 5 to 10 years, and 21 more than 10 years). Participating merchants sold a range of products (clothing = 28, jewelry/accessories = 14, home furnishings = 4, and “other” = 5). Perhaps most importantly, the split between national chain stores (n = 27, 53%) and local merchants (n = 24, 47%) approximated the actual Middle King Street merchant mix.

Upon completion of the collection process, quantitative data were recorded and the open-ended qualitative questions were coded based on in vivo themes noted by the researchers. Two researchers performed this function, with differences noted and reconciled. For example, responses to the question “What three things do you like most about King Street?” were grouped based on their mention of popular themes. These included retail and restaurant mix, location, and tourist traffic. The following are examples of comments coded as parking:

“There is not only a lack of parking, but a lack of cooperation with the parking garages. They are not clearly marked from King Street.” (local merchant)

“Parking is the number one deterrent that local customers give us when they choose not to shop downtown.” (chain merchant)

“Love the area and the food is amazing—people would choose to enjoy this more regularly if there were more places to park.” (chain merchant)

The coded responses were then quantified, employing a method suggested by Pritchard and Havitz (2006) that weighted items based on their order of mention. First mentions in each code category received three points, second mentions two points, and third mentions one point. Per Pritchard and Havitz (2006, 35), such an approach accounts for both attribute salience and importance as “important attributes tended to be mentioned more frequently and recalled first.” Scores for each response category were then summed and converted to a 100-point scale to allow for a comprehensive measure of strength.

Findings

Customer Demographics

Merchants were asked to estimate the percentage of their customers who are residents, tourists, and university students (note the number of college campuses downtown per Figure 1). The results indicate that King Street merchants sell to a diverse customer base. One in three (32%) shoppers are local residents; a significant share of King Street business (19%) is derived from the area’s university students; with the balance of shoppers, representing half of King Street customers (49%), tourists. There was, however, a significant difference in responses between local merchants and national chain stores. On average, 39% of the local merchants’ customer base was resident shoppers, significantly higher than the national chain’s average of 26% (Kruskal-Wallis test result: H = 7.860, p = 0.020). Conversely, while 43% of local merchant customers are tourists, the majority (53%) of the national chain stores’ business comes from the tourist trade (H = 6.421, p = 0.040). It is interesting to note how many tourists visit Charleston . . . only to then shop at the same stores they likely find in their hometown. Why would they do this? Timothy and Butler (1995) provide an interesting likely explanation as they note that shopping has become less about the need for goods and more about serving as a fulfilling form of recreation and even relaxation. Add the familiarity of well-known brands, and certainly the more psychocentric (Plog 2001) the traveler, the more likely a familiar store-brand in a different and attractive locale such as King Street would seem an inviting and fun way to spend part of one’s vacation time in the city.

Evaluation of King Street

When asked to evaluate King Street using a “school grading system,” a substantial majority of merchants (n = 37, 74%) felt that King Street deserved a grade of B. Fourteen percent awarded King Street an A, 10% a C, and 2% a D or an F. Chain stores and local merchants graded King Street nearly identically (t = −0.253, p = 0.801). When converted to a GPA, the overall mean of 3.0 (local merchant mean = 3.0, SD = 0.6; chain merchant mean = 3.0, SD = 0.5) was found to be not statistically different from the “grade” awarded by residents (3.1; t = 1.237, p = 0.222), and slightly lower than that awarded by tourists (3.3; t = −3.712, p = 0.001) as reported in the Litvin and DiForio (2014) study.

Competitors

Merchants were asked the question, “What three stores do you consider to be your closest competitor?” Responses were coded either as a local store or a national chain. The majority of responses received, from both local and national brand respondents, were national brands. These received 77 mentions, versus only 48 mentions of local stores.

A related question asked, “What three stores do you consider to be the most important contributors to the success of King Street?” While the gap between the two categories was smaller than for the “closest competitor” question, national chain store mentions were still dominant (73 national vs. 58 local). Local merchant respondents, however, most often mentioned other local stores as being most important (31 local vs. 27 national), while the national chain store responses skewed strongly in favor of fellow national brands (27 local vs. 46 national). Brands most often mentioned as most important to downtown success were Bob Ellis Shoes (local; n=11), Anthropologie (national brand, clothing, shoes and home furnishings; n = 9), the Apple Store (national brand; n = 9) and M. Dumas and Sons (local clothier; n = 8).

Merchant Mix

A two-pronged question asked, “What would you estimate is the current share (frontage) of local versus national chain stores on King Street?” and “What would be the ideal mix of local versus national chain stores?” The merchants’ estimated current split was 35% local versus 65% national, almost exactly the current frontage split. There was no difference between the estimates of local versus national merchant respondents (t = 0.381, p = 0.705). Both had a good sense of the current environment.

The follow-up query asked what they felt would be an ideal frontage-split. Respondents collectively indicated that local merchants should be more prominent, with a 54% local-merchant frontage share the ideal mean response. For this question, however, the views of local merchants differed greatly from the national chains. Local merchants responded that a 60%–40% split in favor of local merchants would be optimal. Chain stores respondents would aim for an even split, with 51% of storefront frontage occupied by local merchants and 49% occupied by national chains (t = 2.167, p = 0.035). It is particularly noteworthy that the national merchants feel the current split, which they estimated correctly, is too heavily skewed in their favor.

Extending the theme, an additional question asked, “Over the past decade, many additional national chain stores have moved onto King Street. There are varied opinions about this trend. In your opinion, has this been good or bad for King Street? Please explain.” Response options ranged from “very positive” (scored as 1) to “very negative” (scored as 4), with space provided for additional comments. Responses leaned heavily to the positive, with 74% of merchants responding that the influx of national chain stores has been a reasonably (n = 34) or very positive (n = 3) addition to King Street. Only 26% felt that the addition of national chain stores had a reasonably (n = 10) or very negative (n = 3) effect on the environment. Local merchants were, however, notably less enthusiastic about the change (mean = 2.5, SD = 0.7) than were the national chains (mean = 2.0, SD = 0.5, t = 2.666, p = 0.011), with, interestingly, all three very positive responses provided by the national merchants and all three very negative responses from the local merchants.

The following comments are representative of those with a positive view:

I think there needs to be some recognizable stores on King to pull customers to the street. Otherwise, Charleston wouldn’t be known as a shopping mecca. (national chain merchant) We should be grateful that our shopping center has attracted national chains and has evolved into a thriving downtown location rather than a mall in a suburb. This makes Charleston more metropolitan and keeps our historic city-center active. (local merchant)

Negative comments received did not reflect disdain for national chains per se, but rather qualms related to the quality of the new entrants. A sample of these comments follows:

We could use a better mix of stores. Some of the cheaper stores don’t bring the better tourists to King Street. (local merchant) We are bringing in the wrong national chains, for example Forever 21 and H&M. These stores are geared towards college kids and are not high-end enough to match the year-round and seasonal clients. King is getting “mall-like” and cheap. (chain merchant) I think it is good because it brings more awareness, validity, and traffic to the street but, unfortunately, quite a few of the national chains are lower-end and generic like H&M and Forever 21. (local merchant) King Street flavor is lost as big, low-end chains come to King. I believe King Street needs chain stores to draw a customer base—just not stores like Forever 21 or H&M. (local merchant)

When asked what they “most liked” about King Street, the leading merchant response was retail and restaurant mix. It is noteworthy that this same attribute was the number one response of Litvin and DiForio’s (2014) resident sample (tourists had not been asked the question).

What did the merchants “most dislike” about King Street? There were very few mentions related to merchant mix, totally opposite the results of Litvin and DiForio’s (2014) resident survey that had as its number one negative response loss of local stores. Instead, the merchants’ “dislikes” were strongly related to day-to-day hygiene issues. These included parking, traffic, cleanliness, and sidewalk congestion, all functional challenges reflecting King Street’s busy nature.

Discussion

Litvin and Jaffe (2010) determined that Charleston city leaders and government officials had a generally favorable view toward their city’s historic main street’s merchant mix. Follow-up research by Litvin and DiForio (2014) determined that Charleston residents and tourists held similar views. The current study found Charleston merchant attitudes to be generally consistent with those noted in the previous two inquiries. Merchant respondents, a good representation of the city’s main street retailers, though keenly aware of the city’s downtown transition from local to national merchant dominance, are not particularly concerned. In fact, both local and national merchants indicate, to different degrees, that they consider the influx of chain stores to the King Street retail mix to have been a positive factor for the city. And while both local and national chain merchants indicated that more local stores would improve the current mix, they also most often mentioned national chains as the “most important” merchants for the success of King Street. Overall, the merchant respondents rated the main street mix quite positively, expressing a generally supportive view of the current merchant makeup.

Tempering the above, however, was a theme not encountered in the two previous King Street studies. This relates not to the local versus nonlocal ownership of King Street’s retailers, but rather to the perceived quality of the newcomers. Specifically, respondents expressed concern that a proliferation of what they consider to be low-end chain stores (e.g., Forever 21, H&M, Rack Room Shoes, etc.) will transform King’s appearance to “cheap” (a descriptor noted in several merchant comments).

Among those stores mentioned as most important, discount merchants received scant mention, while high-end stores dominated the list. Further, when given the opportunity to express what they liked least about King Street, as noted above, the discount chains were very much “top of mind.” Very few merchant respondents had anything but negative comments to share regarding their discount brand neighbors.

Looking back at the literature, Smith (1994) noted that a destination, as a “tourism product,” must be a congruent amalgamation of its parts. Andergassen, Candela, and Figini (2013) took this further. Their “Coordination Theorem,” supports the need for price coordination between all aspects of a tourist destination (retail, accommodations, and restaurants) to ensure economic efficiency and increased profitability for the destination as a whole. It would seem that the recent addition of lower-end brands in the heart of the King Street retail district, home to the city’s upscale hotels and restaurants, has the potential to upset what otherwise seems to be a well-balanced amalgamated tourism product.

Charleston destination marketers, perhaps as a result of the accolades bestowed by high-end travel publications, seem to have shifted their focus toward a more affluent consumer demographic. Paraphrasing a comment heard often at Charleston Area CVB events, “Our goal is not to attract more visitors; it is to attract better visitors.” Given the perceived conflict between upscale tourists and low-price shopping outlets, one wonders if King Street’s budget-oriented retail newcomers will prove to be a liability hindering such a strategy. This question emerged from the qualitative responses received from the merchant surveys. The theme was not anticipated, and therefore no specific queries were included in the survey instrument to address the issue. However, the merchants’ concern that a continued influx of lower-end retailers could undermine the city’s future success, and thus their own, is certainly an issue deserving of future study.

It is also worth considering the fact that tourist spending exceeds that of the locals (excluding college students). This trend, like other issues discussed herein, fits the progression of the DALC. As national chain stores continue to replace local merchants, a trend that seems destined to continue, local interest in King Street shopping would be predicted by the model to diminish, eroding downtown’s success. Mayor Riley is fond of saying: “People like to visit places where people like to live, and Charleston is a great place to live.” If King Street loses its appeal to locals, will visitors still have an interest in visiting? The DALC suggests the answer could well be “no.” Consistent with this view, Perdue, Long, and Allen (1990) stated that tourist spending exceeding 30% inherently changes the nature of the community. Clearly, that threshold number has long been surpassed in Charleston. The merchants surveyed herein do not seem overly concerned—as long as the “wrong” merchants can be kept away. We, however, feel that these findings should at a minimum send a warning message, with the trend closely watched.

Research Limitations

Before concluding, two research limitations should be noted. First, while merchant attitudes provide an important perspective on the state of King Street, their responses may have been at least influenced by personal interests and bias. Second, limiting the quantity of survey responses received were the policies of several national chain corporate offices that forbid local participation in survey research. The responses received reflect a representative sample of King Street merchants, but it would have been preferable to have had a response pool closer to a complete census.

Conclusion

It is encouraging that the community and tourism industry leaders interviewed in the earliest article of this trilogy, the tourists and locals surveyed in the second, and the King Street merchants surveyed herein all express a positive view of the state of their city’s downtown, with each expressing the need for a “balance” between local and national merchants. It is the responsibility of all concerned to ensure that such a balance be maintained. We recognize, however, that accomplishing such a goal is not easy. We also note that the issue of chain store influence is one that has long been of concern. As noted by Hicks and Wilburn (2001, 312), “In the late nineteenth century . . . [protests] were launched against chain five-and-dime stores throughout the Midwest. In the 1920s; Sears and Roebuck suffered through similar criticisms of their low-priced mail-order services.”

Regarding the role of government in the selection of merchants, Fernandes and Chamusca (2014, 170) commented: “Retail is a private-sector activity, the structure and location of which result mainly from the actions of individuals and firms in a given time and space” and “not from government mandate.” Even more challenging is the difficulty of governments attempting to impose their will regarding the selection of ‘winners and losers’ as they determine which merchants would be most appropriate for their communities. An instructive history of governmental efforts to limit retailers from entering a market is provided by Ingram and Rao (2004), who note how the mood in the United States has swung from enactment to repeal of legislation that restricts property rights. Per these authors, governmental interference is no longer generally considered an acceptable recourse.

Appreciating the above, we encourage King Street landlords to not submit to the power of the “highest bidder” ignoring the dynamic each newcomer adds to the shopping district. Lacking the latitude enjoyed by shopping center/mall management, the individual owners of the city’s downtown’s real estate should collectively, through cooperative efforts, take on the responsibility of evaluating prospective merchants and their compatibility with the existing group of retailers. Such property owner cooperation is essential in creating what Bruwer (1997) deems a “win-win-win,” where the landlord, tenant, and customers all benefit. Further, and proactively in order to maintain the impressive tourism and quality-of-life successes that Charleston has realized in recent years, city leadership is encouraged to consider creative economic development planning that focuses on incentives and rental contract guarantees for small businesses, crafted through the cooperation of city government and merchant associations, to ensure that a healthy downtown environment is maintained and nurtured.

Cachinho (2014, 136) calls for a “consumerscape” at equilibrium, which he defines as the “stage of the retail system where the network of shopping districts and the mix of retail and service facilities are endowed with the properties that ensure its vitality and economic viability, as well as the efficient response to the needs of all types of consumers.” It will take concerned and enlightened leadership on the part of all stakeholders to find and maintain such equilibrium, keeping a healthy if delicate balance of local versus national merchants on King Street.

While we appreciate the positive views expressed by our respondents, it is hard not to have some concern regarding the local versus national merchant mix trend reflected in Table 1. A recent story in the local press reported on the closing of a long-time local King Street retailer, commenting that the reasons for the store’s move to the suburbs was downtown’s “limited parking and rising rents driven mainly by national retailers with deep pockets” (Wise 2015). Per the merchant, “the biggest hurdle for local retail owners is that they are competing with national companies who are able to pay quite a large fee to rent space on King Street that has caused the lease rate to go higher and higher” (Brennan 2015, quoted in Wise 2015). As this trend continues, will Charleston merchants, both local and national, who are generally doing well and, per these findings, reasonably satisfied with the existing King Street merchant balance, remain positive? Litvin and DiForio (2014, 497), pondering this question following their discussion of resident and tourist attitudes, asked,

With deep-pocketed national chain stores willing and able to pay King Street’s escalating rental rates, displacing those local merchants that add charm and uniqueness to the area, what if, a decade or two from now, 60%−70% [a number now reached] of King Street frontage is national chain stores? Will local shoppers still find the balance attractive? Will tourists continue to be attracted to the destination? . . . Or will we see the “malling” of King Street, at which time, as warned by Plog (1991), a destination begins to look and feel distressingly similar to all others?

In response, those authors proposed a model to help explain the lack of concern they encountered. Their model, the Cycle of Acceptance, suggests that communities adapt, adopt, and accept slow change, generally tolerant, regardless of the tourism issue, with their then current balance. While such a balance is generally felt to be “delicate,” as long as the rate of change is kept reasonably in check, the status quo is acceptable and concern remains low. That is, they warn, until a “tipping point” has been reached. Such a state of acceptance certainly seems to be the attitude noted herein. While Charleston merchants believe a more even split between local and national brands would be preferable, it was clear the merchants were quite satisfied with the status quo. There was no apparent concern that a “tipping point” is near.

This level of satisfaction is a credit to those planners and city leaders who have created the attractive and successful environment found in the city of Charleston. However, the current situation is far from static. With Charleston’s tourism likely to continue to grow, King Street will become even more attractive to national retailers, willing and able to outbid local merchants for the finite retail space available in the city’s retail core. We hope, envisioning such a future, that the city will have the foresight to find a way to not allow the current trends to evolve to the point that it wakes up one day only to find it has become, using a term coined by McMahon (1997, 4), “Anyplace, U.S.A.” Enlisting the efforts of the broad range of stakeholders who depend on a successful downtown as a place of commerce and leisure can ensure that such a fate is avoided. Per Ritchie and Crouch (2003), the competitiveness of a destination is dependent on the ability of all involved parties to find ways to add value. Charleston is special. Understanding the challenges and finding approaches that can keep the destination special is the challenge. We hope that this research alerts and reminds those in Charleston as well as those from other tourism destinations of the fragility of tourism and the need to maintain a healthy balance to ensure their successful future.

Future Research

While this case study is the final paper in a trilogy that examined, with three different approaches, the issue of merchant mix in a heritage city, there is additional work to be done. First, it would be good to explore the issues discussed within other tourism-oriented communities to learn the degree that Charleston’s issues and community attitudes generalize across destinations. Second, assuming the current trend continues, a follow-up review will be of value to learn the degree of imbalance the city can endure before attitudes begin to change, perhaps leading to the development of a model that additional research can test. Finally, as noted previously, an important new strand of research would entail an exploration of the impact of low-cost retail brands on a tourism market geared toward higher-paying tourists. This concern, which became evident during analysis of this study’s survey responses, had not surfaced in the earlier King Street studies. Why it was not a concern of government officials, residents, or visitors can only be speculated. Perhaps future research can provide insight.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.