Abstract

In the course of the New Public Management reform movement, public administrations have increasingly implemented output-oriented control schemes, including systems to evaluate employees’ performance. However, contradictory evidence exists about how such output control that fundamentally differs from traditional bureaucratic control affects performance-relevant employee attitudes and behaviors. In this article, we present evidence that performance evaluations have positive or negative consequences depending on the specific design of the system. Analyzing survey data from 184 employees and 60 supervisors from the German municipal administration by structural equation modeling, we find performance evaluations employed as Management by Objectives (MbO) have a positive impact on trust in the employer and that those designed as Systematic Performance Appraisal (SPA) affect trust negatively. Both relationships are mediated by perceived cooperative climate. These findings advocate employing performance evaluations that are participative, adaptive, learning-oriented, and transparent and thus enable fair cooperation between organizational members.

Introduction

New Public Management reforms have altered the face of public sector organizations. This is perhaps best visible in all public personnel management matters, in which newly designed human resource management (HRM) practices relying on formal performance appraisal and output-oriented recognition systems have brought a new dimension of performance accountability into public sector organizations (see, for example, Bouckaert & Peters, 2002; Cardona, 2006; Rubin & Weinberg, 2016; Yang & Kassekert, 2009). The shift from a rule-driven, process-controlled bureaucracy to an outcome-based performance evaluation doctrine has been strongly inspired by standard economic theory. The basic premise of this approach is that goal setting and associated pay are needed to create performance incentives, thus implying that managers should not be controlled like bureaucrats and less bureaucratic behavior is needed to increase organizational effectiveness in public sector organizations (Fama & Jensen, 1983; Jensen & Murphy, 1990).

However, this paradigmatic shift from the classical Weberian bureaucracy to a rational-choice-based economic system has been widely criticized (e.g., Arnaboldi, Lapsley, & Steccolini, 2015; Bouckaert & Peters, 2002). One central concern of public management scholars is that using a system that relies on the assumption that employees need to be incentivized to perform properly might signal that employees are not being trusted (Bouckaert, 2012; Dunleavy & Hood, 1994; Van de Walle, 2011). Thus, by employing private-sector-inspired performance evaluation regimes, public sector organizations risk being perceived by their employees as breaking the psychological contract of mutual trust, which can finally result in crowding out employees’ trust and work morale (Frey, 1993) and thereby leading to diminished employee performance in the long run (Weibel et al., 2016).

Both positions, the positive view on output controls supported by New Public Management scholars and the negative backlash it created, might be exaggerated, as trust and performance system research suggests. Relatively recent findings have shown that control systems do not per se have positive or negative effects on trust but that their consequences always depend on their explicit design, that is, the practices applied. For instance, empirical findings by Mayer and Davis (1999); Tremblay, Cloutier, Simard, Chênevert, and Vandenberghe (2010); and Weibel et al. (2016) propose that the impact of control on employees’ trust is conditioned by whether the specific practices used are perceived as just, reliable, and supportive and enable transparent and fair cooperation between organizational members. Our article is in line with this research. We argue that output control per se does not diminish employees’ trust in the employer. The effect of output control on trust is always dependent on the design of the performance evaluation system applied, which leads to the first research question:

Furthermore, we explore how such differential effects can be explained. A growing body of literature suggests that managerial control systems in public sector organizations may provoke a work climate dominated by fear, competition, and distrust among employees and hence result in a low cooperative spirit (e.g., Diefenbach, 2009; Hoggett, 1996). A low cooperative spirit is likely to dampen employees’ positive expectations of their employer and thus might be an important culprit for the negative effect of certain control regimes on employees’ trust in the employer. Hence, our second research question is as follows:

We approach our research questions based on the case of the German municipal administration in which, in 2007, output-oriented control was implemented in the form of two structurally distinct performance evaluation systems: (a) Management by Objectives (MbO) and (b) Systematic Performance Appraisal (SPA). MbO is a rather holistic approach that includes participatory goal setting, continuous monitoring, and supervisor feedback. SPA, on the contrary, concentrates solely on ex post-performance appraisal based on predefined performance criteria. Recent studies on stakeholder perceptions of the two systems let us assume that they have different effects on the cooperative climate and employees’ trust in the organization. The SPA system is reportedly perceived as predominantly unfair, non-transparent, and unreliable, whereas the MbO system is considered more objective, just, and participative (see Meier, 2013; Müller & Schmidt, 2013; Schmidt & Müller, 2014). Choosing this specific study context enables us to compare the impact of two distinctive performance evaluation systems on the perceived cooperative climate and employees’ trust in the employer within the same setting, that is, all other factors being equal.

In answering our two research questions, we contribute to two different streams of research—first, the public administration literature discussing the effects of New Public Management–induced performance management and measurement systems on work-related employee attitudes and behaviors, and second, the bureaucracy and HRM literature concerned with the effects of managerial control design and, even more specifically, the literature studying control–trust relationships.

Output Control in the Public Sector: The German Case

With the New Public Management reforms, public service organizations have increasingly employed output-oriented performance measurement and management systems in addition to or instead of traditional process control (Arnaboldi et al., 2015; Bouckaert & Peters, 2002; Hoggett, 1996). The designs of these newly introduced output controls vary over countries and specific application contexts (Cardona, 2006; Organisation for Economic Co-Operation and Development [OECD], 2017). The German context is interesting because Germany is near the OECD (2017) average regarding how strongly both output controls and performance-related pay have been adopted in the system. Moreover, the German case allows us to study and compare two different performance evaluation systems.

Specifically, in Germany, as result of a new bargaining agreement adopted in 2005, pay-related wages and corresponding performance evaluation procedures started to be part of public organizations’ control and compensation systems by 2007. Concretely, output control has been employed in the form of two different performance evaluation schemes: (a) Management by Objectives (so-called Zielvereinbarungen) and (b) Systematic Performance Appraisal (so-called Systematische Leistungsbewertung). German public authorities were given the option to implement either of these two evaluation systems or both, but their adoption was not mandatory (Greiling, 2005). The two systems distinctively vary in their designs. MbO consists of a voluntary oral agreement between supervisors and single employees or groups of employees about specific goals (Hock, Schäffer, & Schiefer, 2006). These goals are negotiated in a participatory fashion between employees and supervisors. Goal fulfillment is then discussed in an extended performance review conversation (Meier, 2013). In contrast, SPA is an occupationally fixed system of performance assessment based on outcome criteria, which should be “as objectifiable as possible” (Hock et al., 2006, p. 16). These criteria are either laid down in service agreements or are specified by supervisors and mostly relate to employees’ behaviors and skills required for their tasks or functions (Meier, 2013). Both evaluation schemes are also linked to monetary rewards, but at the time of data collection (2012/2013), a possible maximum of only 2% of a monthly wage sum was available to be distributed.

A large-scale study examining the reform of the control system in German public administration found that in 2012, 59% of the German municipalities had adopted at least one of the two systems, while most of them exclusively or predominantly implemented SPA as an assessment method (75%). A further 9% used a combination in which SPA dominates. Only 12% of the municipalities had employed exclusively or predominantly MbO, and 4% of the municipalities applied a combination of both methods with MbO as the more important element (Müller & Schmidt, 2013; Schmidt & Müller, 2014). Concurrently, we perceive a timid trend toward MbO, as MbO implementation has increased slightly over time (Meier, 2013).

Theory and Hypotheses

Concept Specifications

Output-oriented organizational control

Organizational control is any process by which the organization, supervisors, or other organizational members direct attention, motivate, and encourage employees to act in desired ways to achieve the organization’s objectives (Cardinal, 2001; Cardinal, Sitkin, & Long, 2010; Kirsch, Ko, & Haney, 2010). Formal organizational controls usually rely on codified written rules and directives, are typically exerted by supervisors on behalf of the organization, and constitute the most ubiquitous feature of organizations’ HR systems (Snell, 1992; Snell & Youndt, 1995). Formal controls occur as input control, process control, or output control. Input control entails the systematic selection of employees. Process control, often also called bureaucratic control, rests on the comparison of how well employees execute standardized procedures. Output controls solely concentrate on goals, that is, for outcome controls, objectives for performance outcomes are defined and supervisors monitor goal achievement and finally enact appraisal or sanctioning practices (Cardinal et al., 2010; Jaworski, 1988; Ouchi & Maguire, 1975).

Employees’ trust in the organization

Trust is a psychological state of an actor’s willingness to be vulnerable based on positive expectations about another party’s intentions or behavior (Mayer, Davis, & Schoorman, 1995; Rousseau, Sitkin, Burt, & Camerer, 1998; Weibel et al., 2016). These expectations lead to the willingness to accept vulnerability and are dependent upon a trustor’s perception of the trustee’s trustworthiness (Mayer et al., 1995). Put differently, the trustor evaluates the trustee’s “worth” to be trusted. As such, the two concepts of trust and trustworthiness are closely intertwined and seldom separated in empirical studies on trust (Weibel, 2007). Mayer et al. (1995) conceptualized perceived trustworthiness as relating to three distinct characteristics of the trustee as perceived by the trustor: ability, benevolence, and integrity. Ability subsumes the trustee’s skills and competencies to exert influence in a certain domain, benevolence is the trustee’s will to care for and to do good to the trustor, and integrity means that the trustee displays positive values and acts upon them as perceived by the trustor (Mayer & Davis, 1999). Here, we focus on employees’ trust in their employing organization, often called trust in the employer in the literature (see, for example, Weibel et al., 2016). Specifically, we study public servants’ perception of the trustworthiness of their employing public sector organization as an indicator of employees’ trust in the employer. Therefore, we use trust in and trustworthiness of the organization as synonyms while being aware of the difference in both concepts.

Hypotheses Development

The impact of output-oriented controls on employees’ trust in the organization

The effect of formal organizational control on employees’ trust in their employing organization is a controversial issue in trust research. Some researchers find control affects trust negatively because it signals the employer’s distrust (see, for example, Falk & Kosfeld, 2006). Others propose that controls can promote perceptions of legitimacy (Sitkin & George, 2005) or care (Bijlsma & Van De Bunt, 2003) and hence boost trust in the employer. In the public administration literature, in particular, output controls are often seen in a negative light when it comes to trust. Bureaucratic regulation, which is based on fiduciary principles, that is, the alignment of public values and public service motivation, stands in stark contrast to the ideological underpinnings of output controls, in which self-interest and the need for “additional” motivation play a key role. Hence, quite a lot of research in public administration suggests that output controls signal the absence of mutual trust (see, for example, Bouckaert, 2012; Dunleavy & Hood, 1994; Van de Walle, 2011).

Some findings in HRM and trust research, however, allow for a more nuanced understanding of the relationship of output control and trust. First, the specific design and enactment of controls are likely to be important because “the nature and implementation of HR activities themselves have an effect on employees’ trust” (Whitener, 1997, p. 393). Thus, for instance, Mayer and Davis (1999) presented experimental evidence that “acceptable” performance appraisal systems—those that accurately measure employees’ contributions that are valuable for the organization and thus are transparently and consistently linked to possible employees’ outcomes—positively affect employees’ ratings of top management’s trustworthiness. Tremblay et al. (2010) found employees’ trust in a Canadian hospital was positively affected by HRM performance management practices that signaled organizational support and procedural justice. Similarly, Weibel et al. (2016) provided evidence that well-implemented and balanced controls foster perceptions of fairness and thereby help reduce employees’ felt vulnerability and risks vis-à-vis the organization. On the contrary, they found that implementations that were overly rigid or inconsistent or that incentivized untrustworthy behavior impeded employees’ trust (Weibel et al., 2016).

Second, the literature on enabling and coercive controls (Adler & Borys, 1996) and, more specifically, on “good” and “bad” performance management systems (Aguinis, Joo, & Gottfredson, 2011) explains in more detail what such well-designed and well-implemented output controls could look like. Common to all approaches, enabling/good controls are formed in a participatory fashion. Participation, on one hand, signals that employees’ considerations are taken seriously and, on the other hand, allows adoption of the control system that fits the local context and thereby ameliorates daily work life (Adler & Borys, 1996). In addition, enabling/good controls are learning-oriented rather than evaluation-oriented. Thus, Hoy and Sweetland (2001) argued that learning from mistakes and problem solving rather than punishment and blind rule-following should be the premise of enabling control systems. Finally, enabling/good formal controls show a global transparency that consequently allows employees to understand their contribution to the overall context (Adler & Borys, 1996). Aguinis et al. (2011) translated these characteristics to performance management systems and propose applying employee evaluations in which goals and the ways to achieve them are regularly and jointly set and re-evaluated by supervisors and employees. They argue that other evaluation systems that purely concentrate on performance appraisal in a non-continuous manner are useful neither to support employees in their personal development nor to align employees’ interests with the objectives of the organization (Aguinis et al., 2011). In conclusion, participatory, adaptive, learning-oriented, and transparent control systems can make employees feel they are working in an organization that is capable of meeting its objectives, cares about its employees’ well-being and development, and acts in a comprehensible and fair manner—an organization that can be trusted.

The two performance evaluation systems applied in German municipalities differ regarding the four criteria of (a) employee participation, (b) adaptability, (c) learning orientation, and (d) transparency. In the following, we point out how these characteristics are explicitly linked to employees’ perceptions of employers’ trustworthiness and whether and how they are incorporated in the designs of MbO and SPA. First, employee participation helps establish a better understanding and acceptance of organizational objectives so that employees more easily assess their employing organization as capable. Moreover, their involvement in the decision-making process signals employees are trusted and cared for, which in turn makes employees more likely to perceive the employer as possessing integrity and being benevolent. MbO incorporates employee participation because the system is conceptually based on joint goal setting and attainment evaluations, which allows individual negotiation and customization of employee- and/or team-specific performance goals, whereas SPA typically does not, as it solely draws on predefined appraisal-relevant performance criteria (Meier, 2013).

Second, adaptability applies to an evaluation system that is context-sensitive because it is responsive to changing employee interests and situations. This capacity, which is important to organizations’ optimal task fulfillment, enhances employees’ perception of working with a competent employer. The MbO system explicitly includes the possibility to flexibly adjust the goals to contextual changes, a characteristic not incorporated in the SPA system (Hock et al., 2006).

Third, learning orientation is a sign not only of the employer’s goodwill vis-à-vis the workforce but also of the organization’s competence to continuously ameliorate task fulfillment. By its both participative and flexible character, MbO clearly exhibits a learning orientation, whereas SPA completely disregards individual employees’ development by relying on top-down imposed, other-directed evaluation criteria. Thus, in contrast to SPA, MbO signals the intention to develop and empower employees.

Fourth, only through transparency are employees able to determine if their behavior is instrumental for goal fulfillment and related rewards—a factor central to whether the employer is perceived as trustworthy (see Mayer & Davis, 1999). By its design, the MbO system provides transparency about performance goals and conditions for their attainment from the beginning of the evaluation period; by contrast, supervisors can apply the SPA system in the form of ex post-performance evaluations without clarifying performance expectations sufficiently in advance (Müller & Schmidt, 2013; Schmidt & Müller, 2014).

Based on these theoretical thoughts, we assume MbO facilitates an overall positive assessment of the employer’s trustworthiness, while SPA should rather negatively affect trustworthiness perceptions. Thus, we propose the following relationships.

Perceived cooperative climate as mediator

In the public administration literature, the employment of the New Public Management–induced, output-oriented modes of control are mostly argued to signal surveillance and thus to promote a non-cooperative audit-culture of distrust, fear, and competition (Arnaboldi et al., 2015; Bouckaert, 2012; Diefenbach, 2009; Hoggett, 1996), which would consequently hamper employees’ trust in the organization. Yet, here again, we argue that the use of output-oriented performance evaluation in public administration is not necessarily negatively related to a cooperative climate but depends on the details of the system employed.

Thus, in addition to the proposed direct effects of output-oriented performance evaluation systems on trust in the employer, we also assume such systems indirectly affect trustworthiness perceptions via perceived cooperative climate. We do so because trust in the employer is a complex psychological concept describing an individual’s trust toward an organization as an entity consisting of other individuals, the organization’s management, implicit and explicit rules, and processes. Therefore, we assume that individuals do not develop trust in the employer directly. Instead, facilitating output-oriented performance systems create a “we perspective” and thereby foster cooperation. When a performance evaluation system contributes to the establishment of cooperative interaction between organizational members, the employer—as facilitator of an enjoyable, team spirit–based work environment—is more likely to be perceived as trustworthy. An organization, however, that employs performance evaluations in a way that noticeably worsens cooperation among organizational members reflected by a work climate characterized by fear, envy, rivalry, or competition will probably rank low on its employees’ perceptions of its trustworthiness.

Therefore, supposing MbO to facilitate but SPA to hamper a cooperative climate and therewith the perception of working with a trustworthy employer, the following relationships are proposed.

To test for the mediation effect in more detail, the following hypotheses describe the relationships between the independent variable and the mediator variable on one hand and the mediator variable and the dependent variable on the other hand.

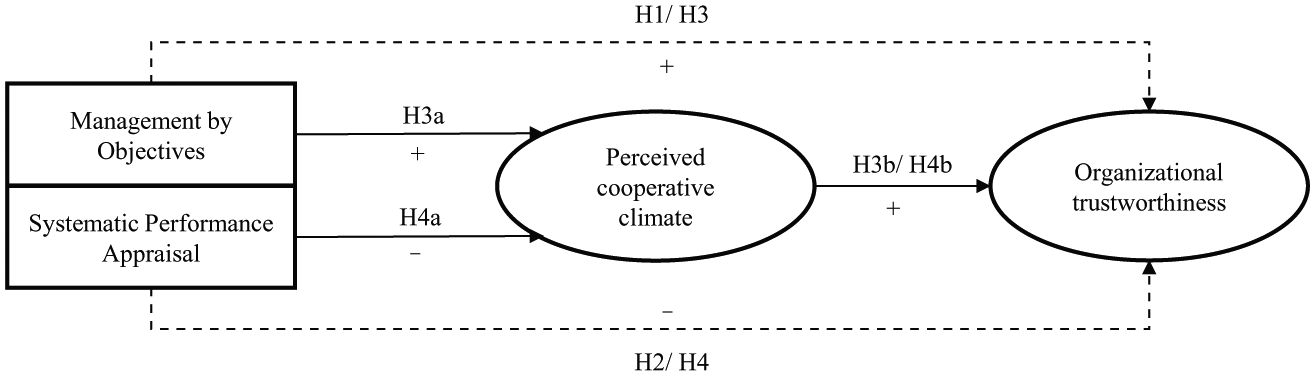

Figure 1 visually summarizes all hypotheses.

Theoretical model and hypotheses.

Method

Sample and Procedures

To test the hypotheses, an online survey was conducted. In 2012 and 2013, 235 German municipal administrations were selected by random sampling proportional to size of the municipality by inhabitants. The municipalities were contacted via email to request their participation in this study. Due to small response rates in the initial request, a further request via phone took place, 2 weeks later. Municipalities that agreed to participate were sent two separate links for two different questionnaires. One addressed public servants in supervisory functions to assess information on the adoption of output-oriented controls, and the other was to be filled in by their direct subordinates. In an attached letter, confidential treatment of the survey data was assured to all participants.

During this first wave of data collection, only 92 completed pairs of questionnaires (matching a supervisor response with at least one direct subordinate response) from 38 municipalities were returned. Therefore, a second phase of data collection was started using a convenience sampling technique. In this phase, the Cities Council of one German federal state supported the study by sending an invitation letter with contact information to all municipal administrations within the state. An additional 16 municipalities took part and extended the sample with 92 more supervisor–employee questionnaire pairs.

The final sample encompasses 184 employees who worked with 60 different supervisors in 54 different municipal administrations. The population of the 54 municipalities ranged from 9,000 to 300,000 inhabitants. Out of the 60 supervisors, four had implemented no output-oriented performance evaluation at all, 14 used only MbO, and 20 only SPA. Twenty-two supervisors indicated that they had installed both systems. Among the 184 public servants, 55.4% (n = 102) were female. The average work tenure in the municipal administration was 16.1 years (SD = 11.4, n = 184).

Measurement model.

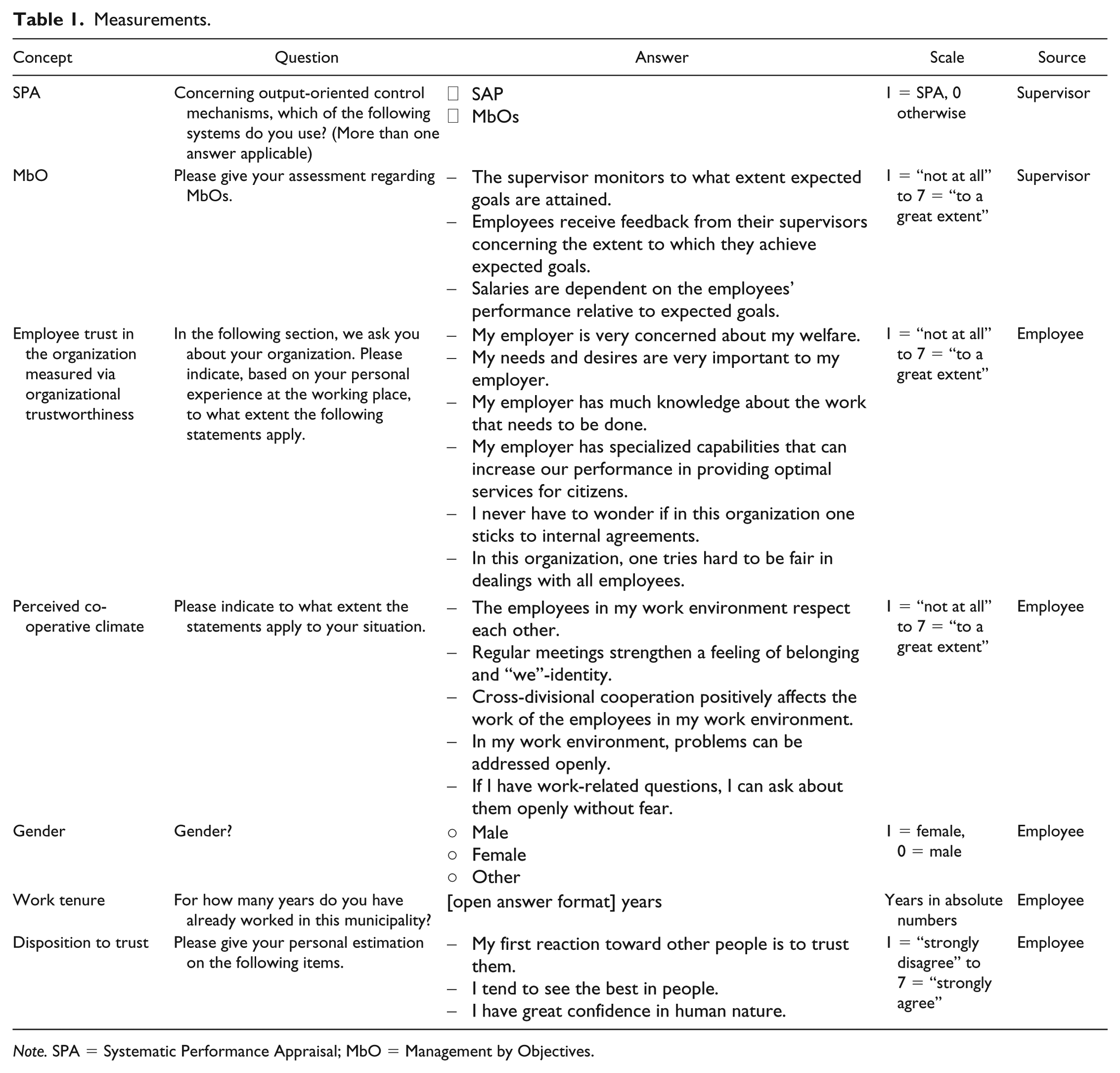

Measurements

Table 1 gives an overview of all measurements. Questions were formulated in German. In case of established scales, we translated the questions from English to German, translated them back, and discussed the translations within the research group. Other questions were designed for the specific context and were developed in German. The questionnaire was pretested cognitively following the procedures of Prüfer and Rexroth (2005). To avoid common source bias, we asked public servants in supervisory positions to assess the presence and implementation of output-oriented performance evaluation systems, while employees directly subordinate to these leaders rated perceptions of the cooperative climate, trust, and control variables (i.e., gender, work tenure, and disposition to trust). All scales measuring continuous variables were 7-point scales ranging either from “strongly disagree” (1) to “strongly agree” (7) or from “not at all” (1) to “to a great extent” (7) relative to the formulation of the respective items.

Measurements.

Note. SPA = Systematic Performance Appraisal; MbO = Management by Objectives.

Output-oriented performance evaluation systems

To assess the differing applications of output-oriented evaluation systems (MbO vs. SPA), we asked the following question: Concerning output-oriented control mechanisms, which of the following systems do you use? Supervisors could choose the answers “MbO,” “SPA,” both answers, or no answer. Because SPA can just be implemented holistically (by using the catalog of evaluation criteria or not), we measured SPA as the system being either applied or not. MbO, in contrast, incorporates different facets of implementation so that we could measure it in a more nuanced way by capturing its degree of implementation. To this end, we adapted the measure of output control by Weibel et al. (2016), resulting in an MbO index of three formative indicators: “continuous monitoring,” “feedback,” and “reward/compensation.” Hence, our SPA measure was dichotomous (use vs. no use), while the MbO measure incorporated the following three indicators: “The supervisor monitors to what extent expected goals are attained,” “Employees receive feedback from their supervisors concerning the extent to which they achieve expected goals,” and “Salaries are dependent on the employees’ performance relative to expected goals.”

Employees’ trust in the organization

We measured employees’ perception of the organization’s trustworthiness as an indicator of employees’ trust in the organization (see, for example, Weibel et al., 2016). We used an abbreviated version of the trustworthiness scale of Mayer and Davis (1999) to measure perceived trustworthiness by its three dimensions: trustee’s benevolence, ability, and integrity. We slightly changed the wording of the items, as the original measure asked for the characteristics of top management, whereas we asked for characteristics of the employing organization. Moreover, we adjusted some items to the context of public administration. Thus, we assessed benevolence by the following two items: “My employer is very concerned about my welfare” and “My needs and desires are very important to my employer.” The dimension of ability was approached by “My employer has much knowledge about the work that needs to be done” and “My employer has specialized capabilities that can increase our performance in providing optimal services for citizens.” Finally, the following two items measure the employer’s integrity: “I never have to wonder if in this organization one sticks to internal agreements” and “In this organization, one tries hard to be fair in dealing with all employees.”

Perceived cooperative climate

We understand cooperative climate as a supportive social climate characterized by the mutual willingness of organizational members to support and help each other, which reflects high team spirit and cohesion (see, for example, Buunk, Zurriaga, Peíró, Nauta, & Gosalvez, 2005). Thus, we believe a cooperative climate is manifested in the extent to which organizational members behave cooperatively in their interactions with others. Consistent with this understanding, we developed a five-item reflective measure to assess employees’ perceptions of cooperative climate. The measure is composed of the following statements: “The employees in my work environment respect each other”; “Regular meetings strengthen a feeling of belonging and ‘we identity’”; “Cross-divisional cooperation positively affects the work of the employees in my work environment”; “In my work environment, problems can be addressed openly”; and “If I have work-related questions, I can ask about them openly without fear.”

Control variables

We controlled for employees’ gender, work tenure, and disposition to trust. Gender (male/female) was chosen as a control variable, as many empirical studies find gender and forms of trust are linked (see, for example, Schwieren & Sutter, 2008). Work tenure was selected as a control variable to account for the assumption that the longer people work within an organization, the more acquainted they are with it, which leads to higher ratings of the employer’s trustworthiness. People who rank low on dispositional trust perceive others to be generally dangerous and dishonest, whereas high scorers believe other people are basically well-intentioned and honest (Searle et al., 2011).

Quality criteria of measurements

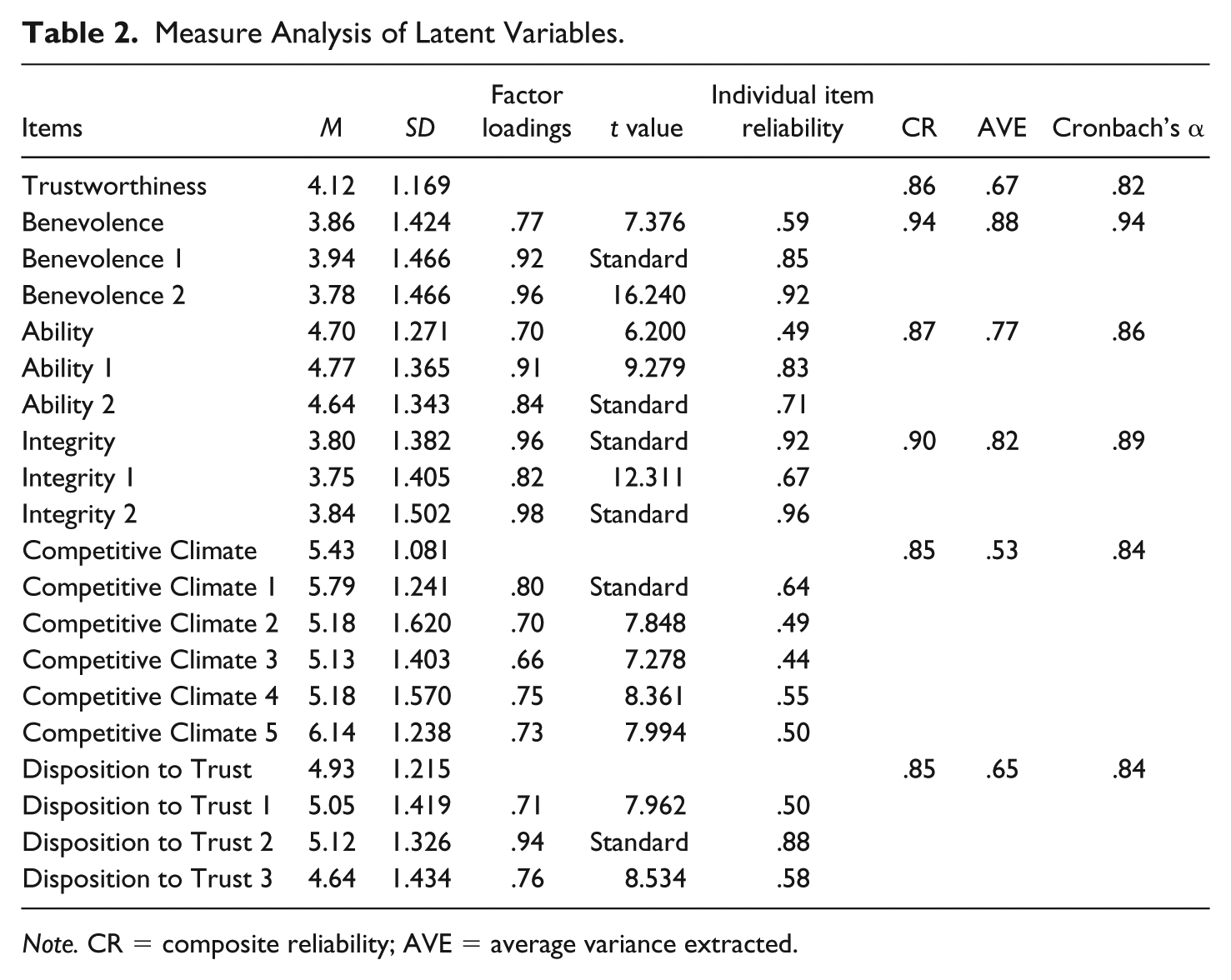

We checked for the reliability and the convergent and discriminant validity of the measures of our latent variables. Table 2 presents the means, standard deviations, factor loadings, t values, individual item reliability, composite reliability (CR), the average variance extracted (AVE), and the Cronbach’s alpha of all items or their latent variables, respectively. All indicators complied with recommended thresholds and thus confirmed the convergent validity of our measures (see Fornell & Larcker, 1981; Gerbing & Anderson, 1988; Gliem & Gliem, 2003).

Measure Analysis of Latent Variables.

Note. CR = composite reliability; AVE = average variance extracted.

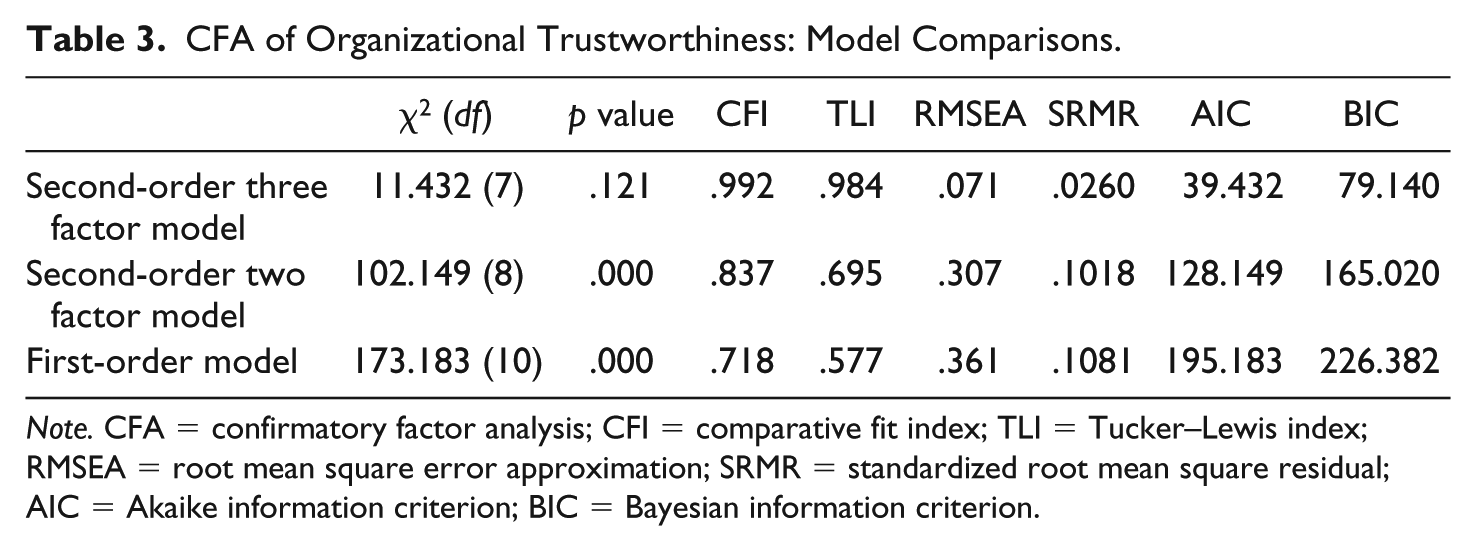

To assess the convergent validity at the construct level, we conducted confirmatory factor analyses (CFAs) for all latent variables. The one-level CFAs of cooperative climate and disposition to trust provided good fit (see Hooper, Coughlan, & Mullen, 2008) with all measures—cooperative climate: χ2 = 7.355 (p = .289), df = 6, comparative fit index (CFI) = .994, Tucker–Lewis index (TLI) = .990, root mean square error approximation (RMSEA) = .043, standardized root mean square residual (SRMR) = .0288; disposition to trust: χ2 = 0.596 (p = .440), df = 1, CFI = 1.000, TLI = 1.008, RMSEA = .000, SRMR = .0187. In prior studies, the second-order construct of organizational trustworthiness sometimes revealed a two-dimensional structure of competence and goodwill, compressing benevolence and integrity into one dimension of goodwill (see, for example, Searle et al., 2011). Therefore, we compared the three-dimensional second-order solution not only with a first-order model (as is common for CFAs of second-order constructs) but also with the two-dimensional second-order solution. The model comparisons (see Table 3) revealed the best model fit for the three-dimensional second-order solution discriminating between the dimensions of benevolence, ability, and integrity as suggested by Mayer et al. (1995).

CFA of Organizational Trustworthiness: Model Comparisons.

Note. CFA = confirmatory factor analysis; CFI = comparative fit index; TLI = Tucker–Lewis index; RMSEA = root mean square error approximation; SRMR = standardized root mean square residual; AIC = Akaike information criterion; BIC = Bayesian information criterion.

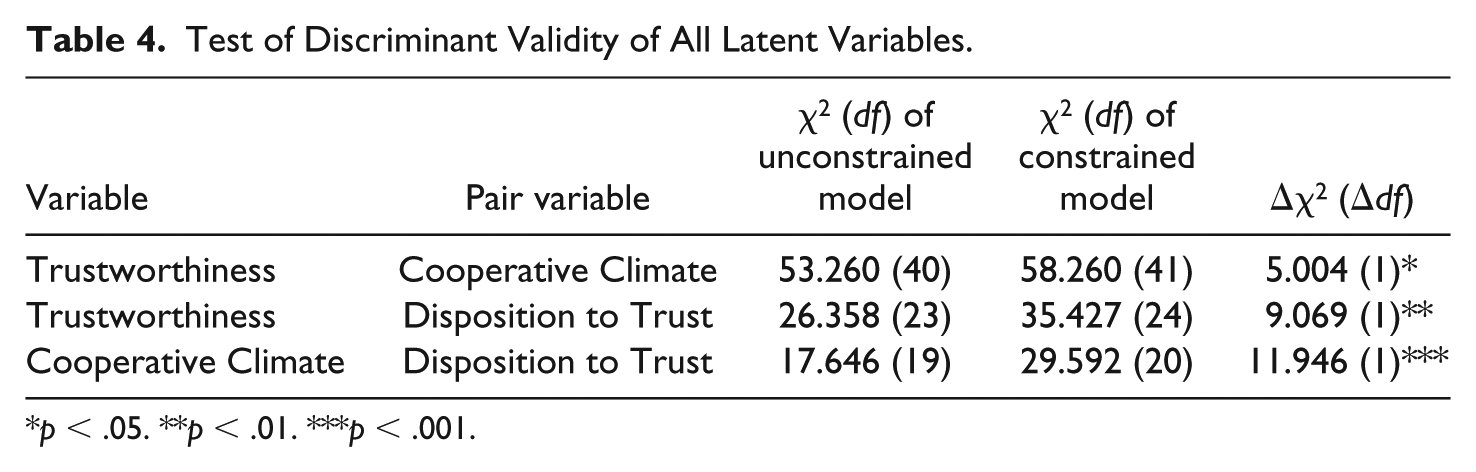

Finally, we checked for discriminant construct validity. To this end, we compared two nested models for all possible pairs of variables. In one model, we allowed the correlation between two latent variables to be freely estimated, whereas in the other, we restricted the correlation to be 1 (thereby assuming both variables measure the same construct). Chi-square difference tests for all model comparisons (for all pairs of variables) revealed that the chi-square value was significantly lower in the unconstrained models than in the constrained ones (see Table 4), which validated our assumption of discriminant validity of all measures.

Test of Discriminant Validity of All Latent Variables.

p < .05. **p < .01. ***p < .001.

Analysis and Results

Correlations

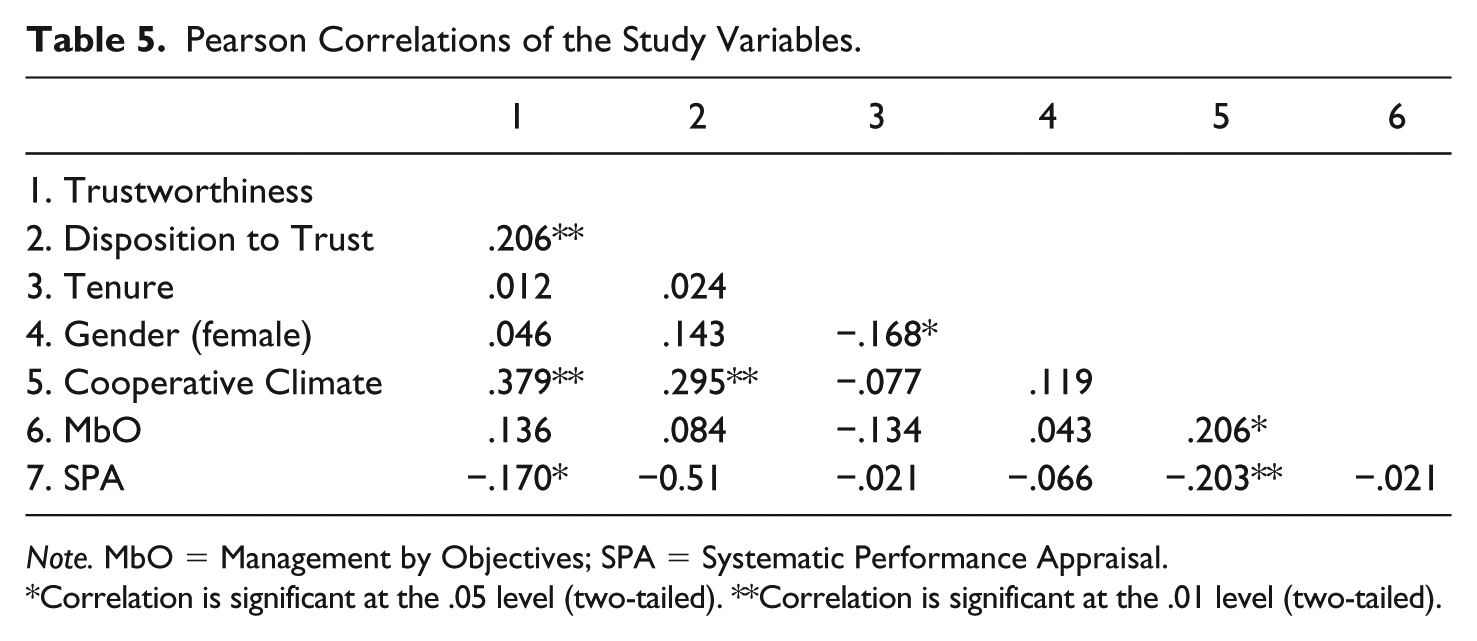

First, the correlations of all study variables were checked using IBM SPSS Statistics 23. The results, as presented in Table 5, revealed that SPA has a negative correlation with both the mediator of cooperative climate and the dependent variable of organizational trustworthiness. MbO is positively correlated with cooperative climate, and cooperative climate is positively related to organizational trustworthiness.

Pearson Correlations of the Study Variables.

Note. MbO = Management by Objectives; SPA = Systematic Performance Appraisal.

Correlation is significant at the .05 level (two-tailed). **Correlation is significant at the .01 level (two-tailed).

H1, H2, H3a, H4a, and H3b/4b on Direct Effects

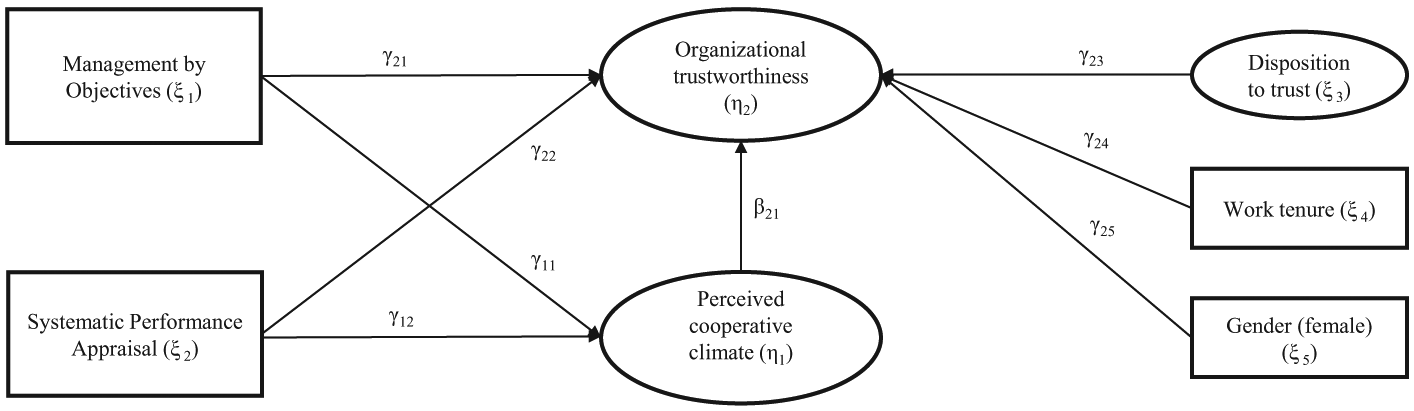

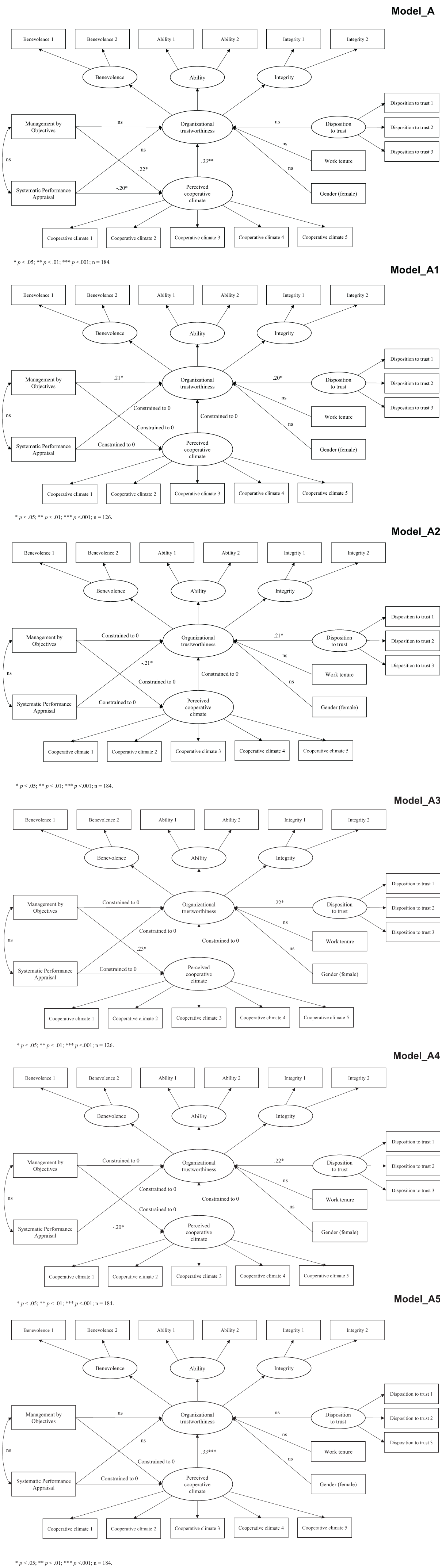

The hypothesized direct effects were tested by calculating five different structural equation models (SEM; Models A1, A2, A3, A4, and A5) using IBM AMOS 21. All models were nested models of Model A. Figure 2 depicts the equivalent measurement model exposing all possible paths. Figure 3 presents the different calculated models. In baseline Model A, all paths were allowed to be freely estimated. In each further model (A1, A2, A3, A4, and A5), only the hypothesized individual paths and those of the control variables were allowed to be freely estimated. All other paths were restricted to 0. Thus, Model A1 displays the effect of MbO on organizational trustworthiness (H1); Model A2, the effect of SPA on organizational trustworthiness (H2); Model A3, the effect of MbO on perceived cooperative climate (H3a); Model A4, the effect of SPA on perceived cooperative climate (H4a); and Model 5, the effect of perceived cooperative climate on organizational trustworthiness (H3b/H4b). All hypotheses could be preliminarily validated, as all tested individual paths controlled for disposition to trust, tenure, and gender reveal significant effects: H1 (Model A1: γ21 = .21, p < .05), H2 (Model A2: γ22 = −.21, p < .05), H3a (Model A3: γ11 = .23, p < .05), H4a (Model A4: γ12 = −.20, p < .05), and H3b/H4b (Model A5: β21 = .33, p < .001, additionally controlling for the effects of MbO and SPA on organizational trustworthiness).

Models A, A1, A2, A3, A4, and A5.

H3 and H4 on Mediating Effects

The mediation hypotheses were tested following the mediation procedures proposed by Baron and Kenny (1986), checking for four requirements (see MacKinnon, Fairchild, & Fritz, 2007): (1) the independent variables must be significantly related to the dependent variable; (2) the independent variables must be significantly related to the mediating variable; (3) the mediating variable must be significantly related to the dependent variable, when both the mediating variable and the independent variables are predictors of the dependent variable; and (4) the effects of the independent variables on the dependent variable are weaker (in absolute value) if the mediator is included as a predictor of the dependent variable, than if each of the independent variables is the sole predictor.

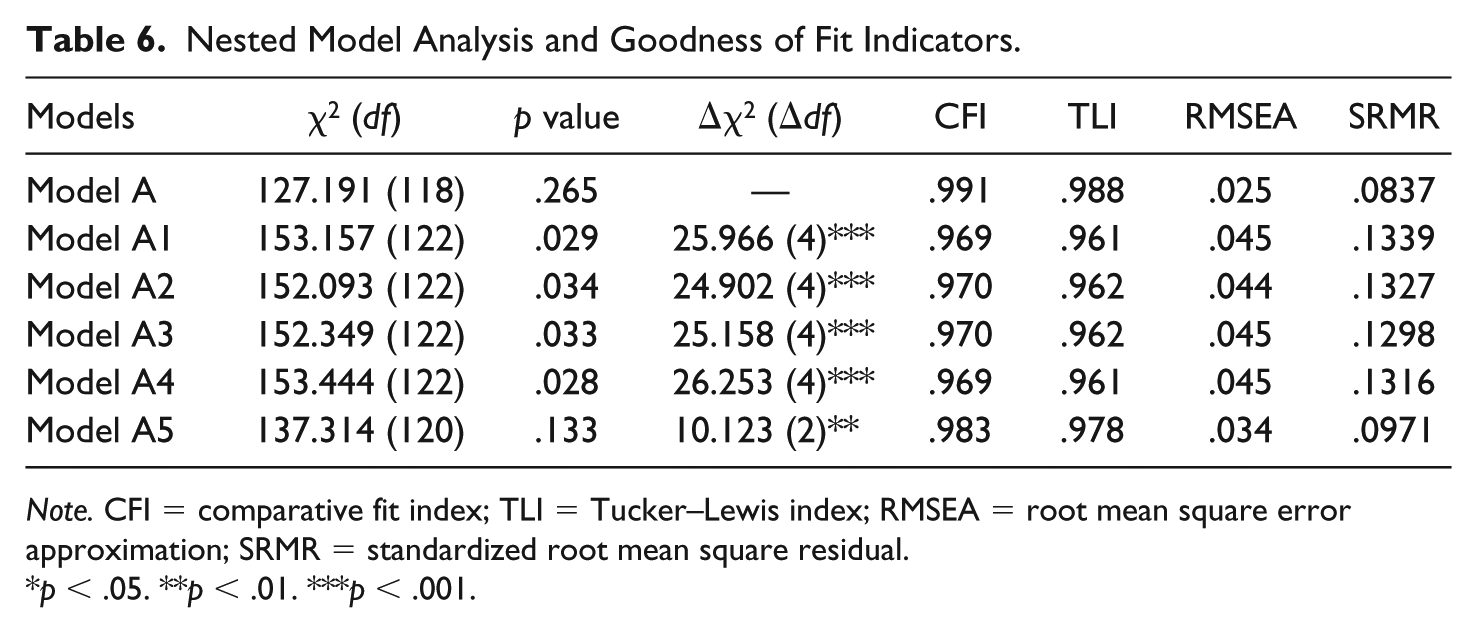

To evaluate these four conditions, Models A1, A2, A3, A4, and A5 were again used, as well as the baseline Model A. Models A1 and A2 revealed that Condition 1 could be approved. Condition 2 could be validated by the results of Models A3 and A4. Condition 3 was fulfilled based on the results of Model A5. To check Condition 4, the effect sizes of the individual effects of the independent variables MbO and SPA on organizational trustworthiness calculated in Models A1 and A2 (without mediator) were compared with those displayed in the baseline Model A that includes the mediation paths. The previously significant effects of the independent variables on the dependent variable (Models A1 and A2) both turned insignificant when the mediator was included in the equation (Model A), therewith validating H3 and H4 and indicating full mediation (see MacKinnon et al., 2007). Thus, H1 and H2 representing the direct effects of MbO and SPA on trust had/have to be finally rejected. Finally, we checked for the superiority in terms of goodness of fit of the hypothesized mediation model by adopting chi-square difference tests between baseline Model A and all alternative nested models. The results show that the mediation model fits the data significantly better than all alternative models. All other fit measures indicated good to acceptable fit of the mediation model, too (see Hooper et al., 2008). Table 6 displays the nested-model analysis and all fit indices.

Nested Model Analysis and Goodness of Fit Indicators.

Note. CFI = comparative fit index; TLI = Tucker–Lewis index; RMSEA = root mean square error approximation; SRMR = standardized root mean square residual.

p < .05. **p < .01. ***p < .001.

Accounting for methodological concerns about the use of control variables—which can produce misleading findings (Becker, 2005)—we repeated all analyses without controlling for gender, work tenure, and disposition to trust. The results of hypotheses testing were essentially identical. Yet, we decided to still report the results, including the controls, to clearly show that our findings are not biased by omitted control variables.

Discussion and Conclusion

Summary

In this study, we examined the effect of different designs of New Public Management–induced output-oriented performance evaluation systems on employees’ trust in the organization. More specifically, we investigated “how different designs of performance evaluation systems affect employees’ trust in the employer” and “if the relationship between different designs of performance evaluation systems and trust in the employer is mediated by perceived cooperative climate.” We found empirical support for the assumption that the use of output-oriented control in public administration does not per se deteriorate employees’ trust in the organization but can facilitate trust depending on the specific design of the control system applied. More precisely, our findings show that either “good” or “bad” output-oriented performance evaluation systems indirectly affect employees’ perception of organizational trustworthiness through their impact on the establishment of either a cooperative or non-cooperative working climate.

Based on the case of the German municipal administration, in which authorities can implement two differing output-oriented performance evaluation systems, we can conclude that a system that supports regular, open and safe interactions among organizational members can create a togetherness and related team-oriented behaviors that make employees perceive a cooperative work climate. Working in such a climate, in turn, makes employees more prone to assess their employer—as the enabler of the climate—as trustworthy. In contrast, the results of the study likewise show that a performance evaluation characterized by a lack of participation, transparency, and fairness and with an evaluative rather than a learning orientation is negatively related to the establishment of a cooperative climate. Perceiving a non-cooperative working environment leads employees to question the trustworthiness of their employer.

Limitations

We are aware of two potential limitations of our study. First, our findings could be subject to omitted variables bias stemming from the hierarchical structure of our data. Even though the information on the independent variable was gathered from 60 different supervisors (compared to 184 employees), we cannot exclude the possibility that other factors than the measured predictor and control variables (i.e., other potential differences on the supervisor level like, for instance, leadership style) influenced our results. Only a multilevel analysis would solve this problem. However, to account for accurate estimations of small effects (i.e., <.50) by multilevel SEM, more than 100 groups are needed (Meuleman & Billiet, 2009). Thus, our sample size of 60 respondents on the supervisor level is too small to adopt this method. Second, contrary to our assumptions, the correlation matrix created in SPSS revealed no significant correlation between MbO and organizational trustworthiness. The individual effect of MbO on trustworthiness in the SEM model (Model A1), however, proved to be significantly positive with low to medium effect size. We suggest this discrepancy is rooted in the calculation of the latent variable of organizational trustworthiness. While in SPSS, organizational trustworthiness was calculated as the sum of its three dimensions divided by three, AMOS additionally accounts for the error terms of all first-order constructs when calculating the second-order construct. Therefore, we understand the latter calculation to be more precise.

Implications for Research

Our study provides implications for two major streams of research: first, the public administration literature concerned with the effects of managerial, private-sector-inspired performance measurement and management employed within the scope of New Public Management reforms on employee attitudes and behaviors, and second, the bureaucracy and HRM literature studying the effects of managerial control design and, in particular, the literature on control–trust relationships.

Thus, first, to public administration research, it adds valuable knowledge to the ongoing discussion about the applicability and usefulness of output-oriented performance management and measurement in public sector organizations (e.g., Arnaboldi et al., 2015; Bouckaert & Peters, 2002). We could provide support for the assumption—drawn from the literature studying design effects of managerial control (e.g., Adler & Borys, 1996; Aguinis et al., 2011) and research on the control–trust nexus (e.g., Weibel et al., 2016)—that output control in the public sector is neither per se negative nor positive but depends on the specifications of the system employed. In this context, this is the first study that explicitly analyzes the effect of different output-oriented performance evaluation systems on public servants’ trust in their employer—an outcome highly relevant to organizational performance (see, for example, Dirks & Ferrin, 2001; Fulmer & Gelfand, 2012).

Our findings provide evidence that in public sector organizations, the implementation of private-sector-inspired modes of control based on transactional principal–agent relationships is not necessarily a treat to cooperative climate (Diefenbach, 2009; Hoggett, 1996) and employees’ trust in the organization (Bouckaert, 2012; Dunleavy & Hood, 1994; Van de Walle, 2011). The results rather suggest that also in the public sector, output-oriented evaluation systems that draw on participatory goal setting and allow goal adaption will foster a cooperative work climate and thereby contribute to employees’ perception of working with a trustworthy employer. In contrast, performance evaluation systems that rank low on these characteristics can be expected to provoke a non-cooperative climate of distrust and competition that hampers employees’ trust—a finding consistent with concerns frequently expressed in the literature dealing with the negative side effects of New Public Management–induced “surveillance”-signaling controls (see, for example, Arnaboldi et al., 2015; Diefenbach, 2009; Hoggett, 1996). Hence, output-oriented HRM practices introduced to public sector organizations must not be qualified as good or bad because of their either transactional or non-transactional character, but based on the way they are designed.

Second, our findings on the existence of “good” and “bad” performance evaluation systems and their differential effects on cooperative climate and trust are in line with insights from bureaucracy research on enabling and coercive controls (Adler & Borys, 1996), with claims from HRM research about the effectiveness of performance measurement and management systems (Aguinis et al., 2011), and with study results on the effects of differently designed controls on trust (Mayer & Davis, 1999; Tremblay et al., 2010; Weibel et al., 2016). Our findings support the assumption that employee evaluation systems that are by design participative, adaptive, learning-oriented, and transparent enable employees to better master their tasks, whereas systems lacking these characteristics coerce employees’ efforts and compliance (Adler & Borys, 1996). Specifically, in our study, we could show that an enabling evaluation system fosters cooperation between employees, which adds to the trustworthiness of the employer, whereas a coercive control regime diminishes cooperation and makes the employer be perceived as less trustworthy.

Our findings also support Aguinis et al.’s (2011) claim that there are “good” and “bad” designs of performance evaluation systems. They argue that systems that are not development-oriented and enacted as ex-post appraisal of employees’ strengths and weaknesses are ineffective, while evaluation systems comprised of a comprehensive development process (from joint goal setting to regular re-evaluation of goals to feedback on goal achievement) positively affect employees’ attitudes and behaviors (Aguinis et al., 2011). Our findings support this view, providing evidence that an evaluation system that solely draws on top-down imposed evaluation criteria that do not target employee development (i.e., SPA) weaken the cooperative climate and employees’ trust in the employer. An evaluation system, in contrast, that allows for participative goal setting in target talks and continuous supervisor feedback (i.e., MbO) fosters cooperative behavior among employees and strengthens perceptions that they are working with a trustworthy employer—a factor highly relevant to organizational performance (see, for example, Dirks & Ferrin, 2001; Fulmer & Gelfand, 2012).

This also aligns with findings in trust research. Consistent with results by Mayer and Davis (1999), Tremblay et al. (2010), and Weibel et al. (2016), this study advocates employing control practices that employees perceive as just, reliable, and supportive and enable transparent and fair cooperation between organizational members to increase employees’ trust in their employer. However, as our findings did not support the assumption of a remaining direct effect of output-oriented control on trust when accounting for cooperative climate as a mediator, we conclude that the trustworthiness of the employer is not directly attributed to the use of a certain control system, but to the collateral effect of the system on interactions between organizational members reflected by either a cooperative or uncooperative working climate. We feel that this important link between control systems’ implementation and cooperative climate necessitates closer investigation. Hence, to assess how to ideally design trust-enhancing control systems, future research should dig deeper into the question of which and how different characteristics of control systems contribute to or discourage cooperative behavior at the workplace. Moreover, it is still worth discussing if the detected full mediation by cooperative climate is a plausible result. Conceivably, good or bad designs of output-oriented control systems might affect factors other than only cooperative climate, which in turn determine employees’ assessments of the organization’s trustworthiness. Therefore, we suggest future research to shed light on mechanisms additional to cooperative climate that can be assumed to mediate the relationship between different designs of employee evaluation systems and trust in the employer, such as perceptions of fairness (Weibel et al., 2016), legitimacy (Sitkin & George, 2005), or organizational support (Tremblay et al., 2010).

Implications for Practice

In terms of practical implications, the findings of this study suggest that private sector–inspired, output-oriented performance evaluation systems can have positive effects on employees’ attitudes and behaviors in the public sector as long as they are designed in a participative, adaptive, learning-oriented, and transparent fashion. Giving employees the possibility to align their own goals with those of the organization while developing themselves with the help of continuous feedback and goal adaption will enable fair cooperation between organizational members and strengthen employee–organization trust relationships, which will eventually be reflected in better organizational performance. Likewise, our findings warn against the employment of performance measurement systems that draw on top-down imposed, non-transparent, rigid, evaluation rather than learning-oriented performance criteria. Those will deteriorate cooperation among employees because they foster a work climate characterized by fear, envy, rivalry, or competition. They will corrupt trust in the employer and finally worsen organizational performance.

For the case of the German municipal administration, these findings clearly advocate for employing only MbO—not SPA—and thereby to pay special attention to a comprehensive implementation of all facets of the MbO performance management system to make its advantages pay off. Nevertheless—and notwithstanding justified criticism of SPA by German public administration researchers, consultant firms, and staff councils—we find German municipalities having implemented SPA at least to an equal share compared with MbO (Müller & Schmidt, 2013; Schmidt & Müller, 2014). This rather counterintuitive behavior is explained by cost-benefit evaluations. While supervisors often fear MbO will entail high transaction costs because it necessitates specifying reasonable and customized goals for and with employees, they can realize SPA with a minimum of investment (Meier, 2013; Schmidt & Müller, 2014). With this study, we hope to contribute to a final change of performance evaluation regimes in the German municipal administration—away from SPA and toward a deliberate application of MbO.

Footnotes

Acknowledgements

The authors thank the anonymous reviewers for their constructive comments and helpful advice. Their special thanks go to Michael K. Kraiß whose efforts for data collection have contributed significantly to the success of the project. They also want to thank the students of their lecture “Vertrauen in der Verwaltung” at the University of Konstanz whose contributions have supported the development of their research design.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.