Abstract

Research shows that procedural justice can motivate compliance through the mediating influence of either legitimacy or social identity. Using three waves of longitudinal survey data collected from 359 tax offenders, we examine whether procedural justice is important to offenders’ decisions to comply with future tax obligations despite fear of sanctions, and whether legitimacy and social identity processes mediate the relationship between procedural justice and compliance. Our results reveal that (a) legitimacy mediates the effect of procedural justice on compliance, (b) social identity mediates the procedural justice/compliance relationship, (c) identity seems to matter slightly more than perceptions of legitimacy when predicting tax compliance, and (d) perceived risk of sanction plays a small, but counterproductive role in predicting tax compliance. We conclude that normative concerns dominate taxpayers’ compliance decisions. Implications are relevant for understanding behavioral compliance and how procedural justice can motivate such behavior.

There are many reasons why people obey laws. For some, compliance is instrumental in nature—it is motivated by fear of consequences should they be detected violating a law. For others, law-abiding behavior is elicited by an intrinsic motivation to follow rules because of the belief that it is right to do so. On this account, compliance is motivated by normative concerns, such as seeing one’s self as a law-abiding citizen or holding a corresponding belief in the legitimacy of the authority enforcing those laws. In this article, we contrast the instrumental versus normative perspectives of compliance. We do so in a context where noncompliance has been found to be common—the taxation context (V. Braithwaite, 2003; V. Braithwaite, Schneider, Reinhart, & Murphy, 2003). We draw on three waves of survey data collected from taxpayers who have been caught and punished for serious tax evasion to examine which of the motivators of compliance best captures their willingness to comply with tax laws in the future. Before proceeding to discuss our findings, we first provide a review of the literature.

Motivating Compliance: Deterrence or Procedural Justice?

Many regulatory and criminal justice systems are based on the premise that individuals are rational actors, driven to comply with laws and regulations out of fear of the consequences for doing otherwise. This instrumental, or deterrence-based, perspective of human behavior suggests that individuals weigh up the costs and benefits associated with obeying the law (Allingham & Sandmo, 1972; Gibbs, 1968; Tittle, 1969). If the costs of noncompliance outweigh the benefits associated with compliance, then the rational choice will be to comply with the law. In contrast, if the benefits associated with noncompliance outweigh the potential costs, then noncompliance will be the rational choice. Advocates of this perspective suggest that noncompliance will be viewed as the risky choice if (a) the risk of detection for noncompliance is high, (b) the severity of sanctions associated with rule-breaking is high, and (c) noncompliance is dealt with swiftly by authorities (Becker, 1968). Proponents of the instrumental perspective therefore suggest that noncompliance can be deterred by increasing both the probability of detection for wrongdoing and the severity of sanctions should wrongdoing be detected.

On balance, however, research suggests that increasing the severity of potential punishments will have limited effect (Doob & Webster, 2003; Pratt, Cullen, Blevins, Daigle, & Madensen, 2008). Rather, increasing the probability of detection has been found to have greater success in deterring would-be offenders from violating laws (Andreoni, Erard, & Feinstein, 1998; Nagin, 2013). Yet, in many regulatory contexts, the probability of being caught and punished for violating rules and laws is low. In the taxation context, for example, the probability of being detected evading taxes is extremely low. Estimates from the United States and Australia indicate that less than 5% of the population have their tax affairs audited in any given year (Marshall, Smith, & Armstrong, 1997; Slemrod, Blumenthal, & Christian, 2001). In such a context, the actual risk of detection for noncompliance is unlikely to substantially influence an individual’s decision to comply with their legal obligations. What regulators rely on, therefore, is regulatees perceiving the risk of detection and sanction to be high. In fact, research has found that individuals can also be strongly deterred from committing criminal acts if they perceive legal sanctions to be certain, swift, or severe (Williams & Hawkins, 1986).

Studies show that risk perceptions can be influenced by personal experience. For example, Paternoster and Piquero (1995) argued that if someone offends but is not detected or punished for the offense, then their perception of sanction risk will fall. Anwar and Loughran (2011) likewise suggested that if one were to be sanctioned for an offense, or see someone else being sanctioned, their perceived risk of being detected and sanctioned will be enhanced. But Anwar and Loughran also argue that persistent offenders can respond differently to deterrence. They showed empirically that serious offenders who had been arrested numerous times in the past were less concerned with sanction risk than less persistent or less serious offenders. In short, an individual’s offending experiences can affect their risk perception and response to that perception.

Actual and perceived risk of sanctions can also indirectly affect law-abiding behavior through the perceived informal sanctions they can elicit. Grasmick and Bursik (1990) argued that shame emotions imposed by significant others can contribute to the effectiveness of deterrence measures. This is because the negative judgment of significant others matters more to an offender (Akers, 1994). Anderson, Chiricos, and Waldo (1977) identified that informal networks (e.g., family or neighborhood structures) indeed had a stronger impact on deterring wrongdoing than actual or perceived deterrence imparted by the state. Such informal sanctioning can therefore have a multiplicative effect on deterring offenses.

While the deterrence literature has a long history, an alternative perspective that attempts to explain people’s compliance behavior is the procedural justice perspective. Procedural justice theory is premised on a different account of offending behavior—one that can provide an explanation as to why people comply with the law even if there might be little actual or perceived chance they will be detected breaking laws. Tyler (1990) has argued that legal authorities can promote law-abiding behavior through utilizing procedural justice in their dealings with the public. Tyler consistently found that if authorities are neutral in their decision making, if they treat people with fairness, dignity, and respect, and provide citizens with an opportunity to voice concerns to authorities (i.e., all elements of procedural justice), then people will view that authority as more morally appropriate and entitled to be obeyed. That is, they will view the authority as more legitimate. Tyler also shows that people will be less likely to violate laws if authorities are viewed as legitimate (Tyler, 1990; see also Jackson et al., 2012; Murphy, Tyler, & Curtis, 2009). Tyler (2006) argued that people who believe that authorities are the rightful holders of power (i.e., that they have legitimacy) will be more likely to be law-abiding because they internalize the moral value that it is right and just to obey those authorities and the law.

A rapidly growing number of procedural justice studies conducted across different countries, regulatory contexts, and population groups have found that such normative-based concerns seem to be the more powerful force for predicting people’s compliance behavior. For example, in the United States, Sunshine and Tyler (2003) found that New Yorkers’ perceptions of police legitimacy were shaped predominantly by whether they viewed police as procedurally just. Perceptions about the effectiveness of police to deter and prevent crime were less important. These perceptions of legitimacy went on to positively influence New Yorkers’ self-reported compliance with the law. Similarly, Reisig, Tankebe, and Mesko’s (2014) study in Slovenia showed that procedural justice was also the main predictor of police legitimacy, which in turn was linked to self-reported compliance behavior. Importantly, procedural justice in their study was found to be the more important predictor of compliance than deterrence concerns (see also Bradford, Hohl, Jackson, & MacQueen, 2015; Mazerolle, Antrobus, Bennett, & Tyler, 2013; Mazerolle, Bennett, Antrobus, & Eggins, 2012; Reisig, Bratton, & Gertz, 2007; Tankebe, 2009). A small number of studies have also examined the link between procedural justice and compliance using offender samples. For example, Paternoster, Brame, Bachman, and Sherman (1997) found that domestic violence perpetrators were less likely to reoffend after being arrested if they perceived the police officers that arrested them to be procedurally just. Papachristos, Meares, and Fagan (2012) also found that violent offenders were less likely to report carrying a gun if they viewed police as legitimate and if they viewed police to be using procedural justice (for research with adolescent offenders, see Gau & Brunson, 2010; Piquero, Fagan, Mulvey, Steinberg, & Odgers, 2005). Finally, in an observational study, McCluskey, Mastrofski, and Parks (1999) found that misbehaving citizens were more likely to acquiesce to the commands of police officers if they viewed police to be using procedural justice during the encounter.

Research in nonpolicing contexts has revealed similar findings. For example, Reisig and Mesko (2009) studied prisoners in Slovenia and found that their perceptions of procedural justice within the prison were positively associated with both self-reported and actual records of compliance in prison (see also Brunton-Smith & McCarthy, 2015). In a study of corporate compliance, J. Braithwaite and Makkai (1994) revealed that nursing home managers were more likely to comply with regulatory standards if they felt nursing home inspectors had previously treated them with procedural justice. Those managers who felt that inspectors had used heavy-handed deterrence threats were less compliant in a follow-up inspection.

Procedural justice theory has also been applied successfully to understand tax compliance behavior. Murphy (2005), for example, revealed that procedural justice imparted by a tax authority strongly predicted tax offenders’ perceptions of the legitimacy of the tax authority, which in turn influenced tax offenders’ self-reported compliance behavior; those who viewed the Tax Office as more legitimate were less likely to report evading taxes. Interestingly, there was no relationship between offense history and subsequent tax noncompliance in Murphy’s (2005) study, suggesting that prior sanction experience played no deterrent role in subsequent compliance behavior. Similar findings have been obtained when examining actual tax compliance behavior. In a randomized controlled trial, Wenzel (2006) found that tax offenders were significantly more likely to comply with the tax authority’s request for compliance, and were less likely to complain about their treatment, if they received correspondence from the Tax Office that emphasized procedural justice messages. Taxpayers who received standard correspondence from the tax authority (i.e., the letter emphasized sanctions for noncompliance) were more likely to make complaints and were less likely to comply with the tax authority’s request (see also Wenzel, 2004).

In summary, the above-mentioned studies represent only a sample of those that have found a positive link between procedural justice, legitimacy, and compliance. What they show is that procedural justice seems to be more important than deterrence in predicting compliance behavior.

Legitimacy and Social Identity as Important Mediating Variables

One important aspect of procedural justice theory is the role that legitimacy plays in the procedural justice/compliance relationship. Numerous empirical studies have demonstrated that an authority’s legitimacy is an important mediating factor in the procedural justice/compliance relationship (e.g., Reisig et al., 2014; Sunshine & Tyler, 2003; Tyler, 1990). This relationship is important because it suggests that people feel compelled to comply with laws if they view the authority enforcing the law to be legitimate. When citizens recognize the legitimacy of an authority they believe that the authority has the right to prescribe and enforce law-abiding behavior. This results in a corresponding obligation to bring one’s behavior into line with what is expected under the law. Hence, authorities can best motivate compliance behavior through building public perceptions of their legitimacy. Legitimacy is best promoted when authorities use procedural justice with citizens.

We examine whether legitimacy mediates the statistical effect of procedural justice on compliance, but we also examine whether social identity is a mediating factor. Social psychologists have attempted to explain why procedural justice might have the positive effects that it does on behavior. These scholars argue that the exercise of fair treatment by an authority strengthens the social bonds between those in power, those they have power over, and the broader social group to which both belong. In other words, procedurally just treatment promotes an individual’s social identification with the power holder and the group that the power holder represents (Bradford, 2014; Bradford et al., 2015; Bradford, Murphy, & Jackson, 2014; Huo, 2003; Huo, Smith, Tyler, & Lind, 1996; Murphy, 2013; Murphy, Sargeant, & Cherney, 2015; Tyler & Blader, 2003).

Identification can take many forms and people often identify with many different groups, sometimes simultaneously. For example, one can identify as being a mother, an Australian, as a member of an ethnic or racial minority group, or as a law-abiding citizen. The context matters and will determine which identity becomes prominent in that situation. According to social identity theory (Tajfel & Turner, 2001), strong identification with a particular group will activate the roles, norms, and responsibilities expected of an individual within that group. In a law enforcement context, adhering to the group’s norms may include obeying the laws of the group, respecting authorities, and being a law-abiding citizen in that group. Group norms relate to the moral norms that would be expected of people in society.

Key to this identity-based argument is the idea that procedural justice communicates to people information about their status and value within society. Being held in good standing encourages one to align one’s beliefs and behavior with the wider group. It also encourages people to support and work with groups they identify strongly with. In other words, identification will motivate law-abiding behavior because members of social groups are motivated to behave in ways that are expected of them from other group members and because they draw value, status, and self-worth from these roles and relationships (Tajfel & Turner, 2001). This process suggests that people internalize the norms and values of the group to which they belong; regarding a group authority as legitimate and abiding by the laws of that group are two such norms that are expected of group members (Horne, 2009).

The Group Engagement Model (Tyler & Blader, 2003) specifically proposes that procedural justice can shape and strengthen social identification with a group, which results in greater propensity to comply with the groups’ norms and rules. Social identity in the Group Engagement Model therefore mediates the relationship between procedural justice and people’s attitudes and behaviors. This perspective also suggests that social identities are changeable over time depending on the type of treatment one receives from a group representative. Fair treatment can enhance social identification, whereas unfair treatment can diminish social identification. We adopt this account for thinking about the relationship between procedural justice, social identity, and subsequent behavior. We propose that tax authorities (like other authorities) have the capability to influence the law-abiding identities of those they come into contact with through the way in which they treat them (see Bradford, 2014; Bradford et al., 2014; Blackwood, Hopkins, & Reicher, 2013). We also suggest that these law-abiding identities can directly influence taxpayers’ propensity to comply with legal rules.

Such suggestions are not dissimilar to arguments put forth by labeling theories. Labeling theories argue that negative system contact can result in delinquency, just as positive system contact can result in diminished offending (e.g., McAra & McVie, 2007; Wiley & Esbensen, 2013). According to labeling theories, this occurs because system contact has the potential to stigmatize individuals and promote delinquent identities (J. Braithwaite, 1989); these delinquent identities in turn result in individuals rejecting mainstream values and norms, which can lead to the potential for reoffending. We suggest that procedurally unfair treatment experienced during system contact has the potential to stigmatize individuals and reduce law-abiding identities, which will loosen the social bonds that promote law-abiding behavior.

Finally, identities may also directly influence compliance behavior because those who identify more strongly with a group will place greater weight on ensuring the outcomes of their group are favorable (Bradford et al., 2015). Not paying one’s taxes, while beneficial to an individual, is likely to be detrimental to the group as a whole; fewer taxes mean fewer resources that can be distributed to the group to pay for public goods. Strong identification with a group is thus likely to promote the groups’ interests. This includes alignment with the expected roles and obligations of the group, and compliance with the group’s laws.

Present Study

The overarching aim of this study is to examine how normative and instrumental concerns motivate tax offenders’ decisions to comply with their subsequent tax obligations. We also aim to examine whether social identity and offenders’ perceptions of the tax authority’s legitimacy each mediate the effect of procedural justice on compliance behavior, and explore which proves to be the more important mediator. The taxation context is interesting to examine because of the widely held assumption that taxpayer behavior is most likely driven by instrumental concerns. If normative concerns are found to dominate tax offenders’ decision to comply with their tax obligations in the future, over and above their concerns about being sanctioned, then this provides convincing evidence regarding the widespread applicability of the normative model of compliance.

The theoretical innovation of our study is to study the importance of social identity processes in the context of a procedural justice account of compliance. This focus is a relatively underexplored aspect of procedural justice theory (in the criminology context at least) and thus allows us to test the relative importance of social identity to explaining compliance behavior. Of particular interest is to test the relative importance of identity versus legitimacy as a predictor of compliance behavior. Based on our review of the literature, we test three main hypotheses:

Method

Sample and Procedure

We use three waves of survey data collected over a period of 6 years from the same tax offenders. The fact that we have three waves of survey data is a strength of our study. Most studies in the procedural justice literature rely solely on cross-sectional survey data. The causal relationships between variables cannot be ascertained in such studies. With longitudinal data, we will be able to demonstrate whether perceptions of procedural justice experienced during a sanctioning event predict a strengthening (or diminishing) of a law-abiding identity and perceptions of the Tax Office’s legitimacy over time, and whether these variables in turn predict subsequent tax compliance behavior over and above perceptions of deterrence. One’s ability to make causal claims is strengthened somewhat with longitudinal data because, in such a research design, confounders must be time-varying, intraindividual factors.

All of our respondents had been caught and sanctioned for involvement in aggressive tax avoidance schemes (it was the first tax offense for 43% of our sample; see Murphy, 2003). To undertake the study, it required working closely with the Australian Tax Office (ATO) to draw the sample. Given privacy legislation in Australia prohibits individuals outside of the ATO having access to the names and contact details of tax offenders, the ATO drew a random sample of 6,000 of the 42,000 known taxpayers involved (sampling was stratified by State and Territory jurisdiction across Australia). The ATO sent correspondence to the sample, inviting them to participate in the study. Respondents were advised to return their completed survey to the first author’s University address. A series of reminder letters was sent by the ATO to nonresponsive taxpayers over 6 months. A total of 2,301 taxpayers returned a completed survey, and after adjusting for taxpayers who were not contactable (did not live at the address listed in the ATO’s database; n = 677), a response rate of 43% was achieved. The representativeness of the sample was confirmed by comparing both the gender and state of residence of survey respondents to the overall offender population in the ATO’s database (Murphy & Byng, 2002). 1

Respondents were asked whether they would be willing to participate in future research. A total of 1,250 Wave 1 respondents agreed and provided their name and contact details direct to the first author. Two years later, these respondents were sent an invitation to participate in Wave 2 of the study. A total of 659 taxpayers returned a completed Wave 2 survey. Adjusting for people who were no longer contactable at Wave 2 (n = 146), a Wave 2 response rate of 60% was achieved (Murphy & Murphy, 2010). Finally, 4 years after the Wave 2 survey was completed, the original 1,250 respondents who agreed to be followed-up at Wave 1 (minus those who were not contactable at Wave 2; n = 146) were recontacted again and invited to participate in the final wave of the study. For the 1,112 taxpayers recontacted at Wave 3, 478 completed surveys were received. Adjusting for those no longer contactable at Wave 3 (n = 178), a Wave 3 response rate of 52% was achieved (Murphy, Murphy, & Mearns, 2010).

The data utilized in the present study relate to survey responses from taxpayers who participated in all three waves (n = 379). For the final sample of 379 respondents, 84% were men, the average age of respondents was 49.4 years (SD = 8.47 years; age range = 25-72), 47.5% had a university degree, 87% were in employment, and 83% were married. The average annual income for respondents was AUS$87,830 (SD = AUS$47,750).

Survey Instrument and Measures

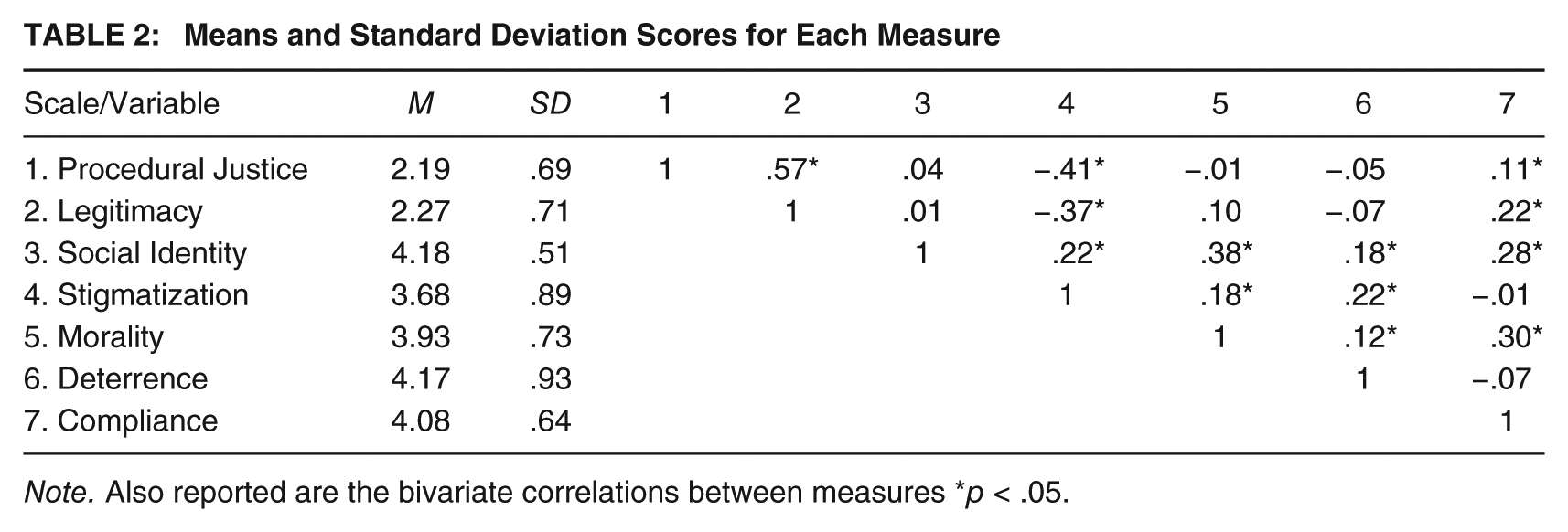

Confirmatory Factor Analysis (CFA) using Mplus 7.1 was used to construct and validate the measures used in this article. Table 1 shows the question wordings and factor loadings for each concept. It also presents the means and standard deviations for each latent variable. The Cronbach’s alpha scores and model fit statistics for the CFA reveal that all factors and scales, except the Legitimacy scale, were strong and reliable (the root mean square error approximation [RMSEA] score was less than .05; the Tucker Lewis Index (TLI) and Comparative Fit Index (CFI) scores were greater than .95). The factors were (a) procedural justice (Wave 1); (b) ATO legitimacy, stigmatization, social identity, personal taxpaying morality (Wave 2); and (c) self-reported tax compliance (Wave 3). All measures were recorded on a 1 (strongly disagree) to 5 (strongly agree) Likert-type scale. Perceived risk of sanction for tax offending (Wave 2) was measured on a 1 (0% chance of being caught) to 5 (100% chance of being caught) scale. Bivariate correlations between these scales and variables are presented in Table 2. Note that all latent variables (except stigmatization) were coded such that a higher score indicated more favorable responses (i.e., more procedural justice, more legitimacy, etc.). Higher stigmatization scores indicated taxpayers felt more stigmatized. Each latent variable was calculated by summing the responses to each scale question and dividing by the number of survey items in that scale. Missing data for our measures were handled through MPlus using the maximum likelihood estimation procedure to replace missing values. Only cases with no responses were excluded. Missing data were typically low, with less than 1% missing data for most attitudinal questions.

Confirmatory Factor Analysis for Concepts Used in Figure 1, and Basic Descriptive Statistics for Latent Variables

Note. χ2 = 1,299.53, df = 680, p < .05; RMSEA = .05; CFI = .97; TLI = .97. ATO = Australian tax office.

Reverse coded to create scale.

Means and Standard Deviation Scores for Each Measure

Note. Also reported are the bivariate correlations between measures *p < .05.

The Procedural Justice scale was measured via a 10-item scale that assessed taxpayers’ perceptions of the ATO’s use of procedural justice (the four procedural justice elements of neutrality, fairness, respect, and voice were measured). The 4-item ATO Legitimacy scale reflected taxpayers’ feelings of obligation to follow the directives of the ATO and the degree of respect they had for the ATO. We acknowledge the recent debate regarding the legitimacy concept in the procedural justice literature (e.g., Bottoms & Tankebe, 2012; Jackson & Gau, 2015; Tankebe, 2013; Tyler & Jackson, 2013, 2014). These scholars have recently suggested that legitimacy scales that measure obligation to obey and confidence in authority can be limited. They suggest that additional measures should be included to produce a more well-rounded measure of legitimacy. For example, these additional measures might include questions about the perceived legality of an authority (i.e., do authorities follow the rules themselves) and normative alignment (i.e., do authorities share the same values as citizens and exercise their authority in normatively appropriate ways). Unfortunately, our legitimacy measure does not fully capture these additional aspects of legitimacy due to the fact that our data was collected before these debates were presented in the literature. We instead utilize a legitimacy measure commonly used and cited in earlier research (Tyler, 1990). Future researchers may wish to replicate our findings with a more sophisticated measure of legitimacy. But even with this measure, we find legitimacy mediates the effect of procedural justice on compliance as has been demonstrated consistently in the literature with both the old and new measure (see “Results” section).

The Social Identity scale contained four items, measuring strength of identification with being a member of the community of law-abiding Australian citizens. Stigmatization was another measure of identity, specifically assessing how negative system contact had labeled tax offenders with a deviant identity; it comprised seven items. Taxpayer morality was measured with four items gauging how wrong taxpayers felt it was to evade taxes. This item was included given the social identity literature suggests that identification with a group activates the roles and responsibilities expected of an individual in that group (Bradford et al., 2014). Personal morality has also been found to be a correlate of offending behavior so it is important to include it in a model predicting compliance (Reisig et al., 2014; Tyler, 1990). Risk of sanction was a one-item question assessing respondents’ perceptions of the likelihood of being caught evading taxes.

Our dependent measure was compliance. Compliance was a six-item measure assessing taxpayers’ self-reported compliance behavior. Taxpayers were asked to answer these questions by reflecting on how they felt their enforcement experience had affected their subsequent taxpaying behavior. We acknowledge a limitation of our study in that we only measured self-reported compliance behavior. However, past research does show a link between intentions to comply and actual compliance behavior (Ajzen, 1985), and research conducted in other legal contexts shows that procedural justice is similarly related to both self-reported and actual compliance behavior (e.g., Reisig & Mesko, 2009).

Results

Figure 1 shows a structural equation model (SEM) that allowed simultaneous testing of all our research hypotheses when predicting compliance. Structural equation modeling was used because it allows simultaneous testing of all interrelationships between variables in the model; regression is unable to do this. The model fit statistics show that the constructed model provides a good fit to the data (RMSEA scores are below .05; TLI and CFI are both greater than .95). In this model, respondents’ assessments of the ATO’s use of procedural justice in the immediate aftermath of being sanctioned by the ATO (measured at Time 1) is the ultimate explanatory variable; the ultimate response variable is self-reported tax compliance behavior measured at Time 3. The other variables constitute potential mediators of the procedural justice to compliance pathway, crucially measured at Time 2. We can therefore model directly the temporal ordering always implied in studies of procedural justice (i.e., procedural justice → legitimacy → compliance; procedural justice → identity → compliance) but usually represented by data collected at one, or at best two, points in time.

SEM Predicting Self-Reported Tax Compliance

As can be seen in Figure 1, procedural justice had a statistically significant direct relationship with three variables in the model. Those who felt the ATO was more procedurally just at Time 1 were more likely to view the ATO as legitimate, were more likely to identify strongly as a law-abiding Australian citizen, and were less likely to feel stigmatized by the ATO at Time 2.

There was a moderately strong path from social identity to offending at Time 3 and also from legitimacy to offending at Time 3. Stronger identifiers were more likely to say they had complied with their tax obligations, and those who viewed the ATO as more legitimate were more likely to report being compliant. The perceived risk of sanction variable at Time 2 also predicted compliance at Time 3. However, the relationship was in the opposite direction to that expected. Respondents who thought there was a greater chance they would be detected violating tax laws were less likely to report being compliant; deterrence seems to have a counterproductive effect in our model. Importantly, normative concerns seemed to have a stronger effect in predicting compliance than perceived risk of sanction (Hypothesis 1 supported). Finally, the indirect statistical effect of procedural justice on compliance was positive and significant (β = .10, p < .04). Those who thought the ATO was more procedurally just at Time 1 were more likely to report being compliant at Time 3. The fact there was no direct path between procedural justice and compliance suggests that the effect of procedural justice on compliance was mediated through both legitimacy and social identity (support for Hypotheses 2 and 3). Figure 1 also shows that 25% of the variation in compliance scores can be explained by all of the included variables in the model.

Some additional relationships in our model are worthy of mention. Although not the primary focus of our study, our model reveals that these relationships are important to further our understanding of why procedural justice promotes compliance through identity and legitimacy. The stigmatization variable had an independent and significant effect on legitimacy; those who felt more stigmatized by their enforcement experience were less likely to view the ATO as legitimate. Interestingly, stigmatization was positively (not negatively) associated with the social identity variable. Those who felt more stigmatized by the ATO were more likely to identify strongly as a law-abiding Australian. There was also a strong association between social identity and personal taxpaying morality. Respondents who identified more strongly as a law-abiding Australian were more likely to view tax avoidance as morally wrong. The strongest predictor of compliance was the personal morality variable. Those who felt it was morally right to pay tax were more likely to say they were compliant with their tax obligations. Morality was also found to partially mediate the social identity and compliance relationship.

Discussion

The present study aimed to test whether tax offenders’ decisions to comply with their subsequent tax obligations were predicted more strongly by normative concerns than concerns about being caught for noncompliance. We found that it did, providing support for Hypothesis 1. We also tested whether legitimacy and social identity mediated the relationship between procedural justice and compliance. Again, we found that they both did, supporting Hypotheses 2 and 3.

Specifically, we found that perceptions of procedural justice predicted respondents’ perceptions of the legitimacy of the ATO; this relationship replicates findings observed in other legal contexts (e.g., Reisig et al., 2014; Sunshine & Tyler, 2003). The experience of procedural justice during enforcement also predicted stronger levels of social identity; specifically, procedural justice was associated with lower feelings of stigmatization (i.e., deviant identity) and higher levels of identification as a law-abiding Australian. These findings also support other studies in the literature (e.g., Bradford et al., 2014; Murphy & Harris, 2007).

With respect to self-reported offending, taxpayers who perceived a greater chance of being caught for engaging in tax evasion were actually less likely to say they had complied with their tax obligations. Also predicting compliance was legitimacy, social identity, and personal taxpaying morality. Those taxpayers who viewed the ATO as more legitimate, who identified more strongly as a law-abiding Australian, and who believed taxpaying was morally right, were more likely to report higher levels of compliance. These three factors had stronger effects on compliance than the perceived risk of sanction, with personal morality having the strongest effect on compliance behavior. Again, these findings support prior research conducted in other contexts, and show the specific importance of personal morality as an informal inhibitor of criminal behavior (Bradford et al., 2015; Reisig et al., 2014; Tyler, 1990).

Importantly, the results show that both legitimacy and social identity are mediators in the procedural justice–compliance relationship. Feelings of stigmatization were also found to play an indirect role in predicting compliance through taxpayers’ perceptions of legitimacy and through their identification as law-abiding Australians; higher levels of stigmatization were associated with lower levels of perceived legitimacy and higher levels of social identity. Considered together, all of these findings suggest that both instrumental and normative concerns shape taxpayers’ decisions to reoffend, but normative concerns were more prominent.

We should acknowledge a limitation of our study. Participant attrition in longitudinal research studies is a concern for social scientists because loss of certain participants may result in subsequent data collection phases becoming increasingly biased. Attrition may therefore lead to unreliable conclusions (Ahern & LeBrocque, 2005; Farrington, 1991). For example, the ultimate dependent variable in our study is self-reported compliance behavior at Time 3. One might argue that people who are more law-abiding might be more inclined to participate in all three phases of the research. This may skew our results toward more compliant responses at Time 3. To explore this possibility, we compared our Wave 3 and Wave 1 respondents on a number of demographic and compliance questions measured at Time 1. We found that the two groups did not differ on income level, educational status, gender, English speaking status, or perceived risk of sanction for noncompliance. We did, however, find a small age difference, with older people being slightly more likely to continue participation in the study over time. Interestingly, we also found that those who participated in Wave 3 reported being slightly more noncompliant in the past. This latter finding in particular suggests that our Wave 3 sample is slightly biased toward noncompliance. Our findings must therefore be considered with this in mind. However, the bias toward noncompliance does suggest that if normative factors can positively influence compliance behavior for more serious offenders, then this highlights the virtue of authorities considering procedural justice in their disciplinary approach with offenders.

Implications for Theory and Regulatory Practice

Deterrence-based theories of compliance suggest that individuals are primarily motivated to comply with laws due to a fear of consequences for doing otherwise. Yet, our results suggest that even in a context where one might expect instrumental concerns to dominate, individuals seem to be motivated to comply out of an intrinsic motivation to do so. Our respondents all had large tax debts as a result of their previous noncompliance, and they had all been through an enforcement process. Such experiences are likely to enhance peoples’ perceptions that they will be caught again if violating tax laws (this suggestion is supported by the high mean score for the risk of sanction variable—see Table 1). However, this enhanced perceived risk of sanction played only a small role in predicting subsequent compliance behavior. In fact, our deterrence variable seemed, if anything, to have a counterproductive effect on compliance behavior. Those with more fear of being caught reported more noncompliance. This finding supports previous research showing that deterrence strategies that are perceived to be unreasonable can result in backlash and further noncompliance in the long term (Kagan & Scholz, 1984). But they also provide support for Anwar and Loughran’s (2011) suggestion that serious offenders can respond differently to deterrence than less serious offenders. A more thorough investigation in the future of how serious tax offenders respond to deterrence, based on their sanction history, would be worthwhile.

Our findings point to the importance of social identities and personal morality in promoting law-abiding behavior. In fact, we found that social identity strongly mediated the effect of procedural justice on compliance. We know from other taxation research that people’s connections to others do matter; what others in one’s group think about taxpaying can strongly influence people’s own views and behaviors. Wenzel (2004, 2005), for example, found that if individuals thought other taxpayers paid their fair share of taxes, and saw taxpaying as worthwhile, they themselves were more likely to see taxpaying as morally right. We propose compliance is likely to benefit as a result of strong identification with law-abiding groups because people are motivated to align their behavior to the group’s norms and to act in the interests of the group they belong to. When identification with “Australianness” and being “law-abiding” in this group is strong, propensity to engage in activities that might harm others in the group diminishes (see Bradford et al., 2015). In other words, people pay their taxes because of the belief it will benefit their group.

This may partly explain why social identity and personal morality prove to be more important predictors of tax compliance behavior than perceptions of the ATO’s legitimacy. Legitimacy has been linked to compliance behavior in past research by suggesting that the legitimation of legal authorities encourages internalization that it is right to obey the law because it is the law (e.g., Murphy, Hinds, & Fleming, 2008; Reisig et al., 2007; Tyler, 1990), and we did find that legitimacy mediated the effect of procedural justice on compliance. Yet, in our study, social identity seemed to play a more important role in predicting compliance than did legitimacy. We suggest that strong group identification promotes a sense of obligation to behave in the interests of the group (see Tajfel & Turner, 2001; Tyler & Blader, 2003).

It is worth underlining, however, that legitimacy did still have a unique statistical association with compliance. Even when controlling for personal morality and social identity levels, those who granted the ATO more legitimacy were more likely to say they complied with tax laws. Our findings therefore concur with the idea that legitimacy motivates a sense of duty, whereby one is motivated to comply with the laws mandated by an authority, not because one believes them to be the right, or because one wishes to avoid behavior harmful to other group members, but because one believes that following the dictates of legitimate authority is the right thing to do in and of itself.

Before concluding, we were somewhat surprised that feeling stigmatized resulted in a more positive social identity and thus, overall, a positive association with compliance. Labeling theorists would predict the opposite, with deviant identities hypothesized to result in distancing from the norms of mainstream society (J. Braithwaite, 1989). While our finding may be an anomaly, we suggest it could also be explained by the nature of the offending behavior exhibited by our taxpayers. The majority of our respondents argued they had become involved in tax avoidance schemes on the advice of tax specialists (see Murphy, 2003). They claimed their purpose for “investing” in tax schemes was not to defraud the tax system, but to provide an investment strategy for their future. They believed their tax advisors were to blame for their situation. If we take these claims at face value, it is perhaps not surprising to observe that feeling stigmatized during an enforcement process might result in a stronger affirmation of an honest taxpaying identity. Procedurally unfair treatment might challenge taxpayers’ identity as law-abiding citizens. Rather than create a deviant identity that results in further reoffending, however, to “save face” and protect this sense of self as law-abiding, the resulting action is to communicate to others that they are “upstanding citizens,” resulting indirectly in greater self-reported compliance. Such a process is not totally foreign to criminologists. Sykes and Matza’s (1957) research on how offenders attempt to neutralize their offending behavior to protect their reputation is but one example. Whether similar effects to ours can be found for other types of tax offenders or in other regulatory contexts remains to be seen.

Conclusion

Our results show that tax authorities should not rely solely, or even primarily, on deterrence-based strategies to ensure taxpayer compliance. Our findings suggest that enforcement strategies that speak to taxpayers’ normative concerns may prove more successful for promoting voluntary tax compliance behavior in the long term. These findings support conclusions drawn by many procedural justice studies in the literature, and suggest that the procedural justice framework examined in our tax study can be generalized across different legal contexts. Our findings in particular point to the role that social identity and legitimacy plays in explaining why procedural justice has a positive effect on compliance-related behavior. If authorities wish to promote compliance with their laws and directives, procedural justice seems to provide an effective means to achieve this. This is because procedural justice generates both legitimacy and forges social bonds between individuals and the group to which the authority represents. This in turn motivates people to bring their views and behavior into line with the expectations of the group. The legitimacy of authorities is important for fostering compliance behavior, but our findings suggest that social identity may be an equally important mediating mechanism that explains why procedural justice promotes an intrinsic motivation to be law-abiding. More work is needed in this space, but future research may reveal that social identity processes are more important in procedural justice theory than has previously been suspected.

Footnotes

Acknowledgements

The authors acknowledge the funding support from the Australian Research Council (Grant DP0987792). They also thank two anonymous reviewers for their thoughtful suggestions and reflections on an earlier version of this article.