Abstract

In December 2017, Congress repealed the individual insurance mandate penalty. Given the poor health status of veterans, their higher demands for health insurance, and the substantial number of uninsured veterans, the repeal of the individual mandate should have a significant impact on the veterans. This article investigates how the repeal of the individual mandate effective in January 2019 is likely to affect the number of uninsured veterans and their enrollments in Veterans Affairs (VA) insurance. By analyzing 52,692 nonelderly veterans in Florida and California from 2008 to 2017, the findings suggest that the repeal will lead to a considerable increase in the number of uninsured veterans. Veterans who are unemployed, poor, and suffering disabilities are more likely to sign up for the VA insurance than better-off veterans. Thus, one of the important functions of veteran health care is to serve as a social safety net for vulnerable veterans. Thus, the Veterans Health Administration should establish a policy to minimize the expected negative repercussions of the repeal.

In 2016, there were an estimated 18.5 million veterans in the United States. Of those, 510,000 (5.5%) of nonelderly veterans between the ages of 19 and 64 years reported that they had no health insurance coverage (U.S. Census Bureau, 2017b). Veterans who generally served in the military for 2 years or more and who did not receive a dishonorable discharge can use Veterans Affairs (VA) medical facilities regardless of whether they hold health insurance coverage (U.S. Department of VA, 2019a). A veteran without health insurance is more likely to use VA medical facilities than a veteran with health insurance (Hisnanick & Gujral, 1996). Poor and less educated veterans tend to use VA health-care facilities more often, and a large portion of veterans using VA health facilities do not have insurance (Nelson, Strakebacu, & Reiber, 2007).

The expansion of the Affordable Care Act (ACA) contributed to a reduction in the number of the uninsured veterans through expanding Medicaid eligibility. 1 Also, the ACA made private health insurance more available by subsidizing the purchase of insurance and by capping of out-of-pocket costs. The ACA has a provision called the “individual mandate” that requires people living in the United States to have health insurance that meets minimum standards of coverage and imposes a tax fine penalty on those who fail to comply with that provision. This provision was critical to reducing health insurance premiums by requiring that every individual purchase health insurance regardless of his or her health status or age. However, in the Tax Cuts and Jobs Act passed in December 2017, Congress repealed the tax penalty of the individual health insurance mandate. While the repeal is expected to reduce the federal budget deficit by US$338 billion from 2019 through 2027 (U.S. Congressional Budget Office [CBO], 2017), the repeal will allow healthy individuals to leave their health insurance coverage group, and due to the increased risk of financial loss, health insurance companies will likely require a higher premium for the remaining individuals who still need the insurance.

The U.S. CBO estimated that the repeal would increase the number of uninsured by 4 million in 2019 and 13 million in 2027, while the average insurance premium for the nongroup market 2 would increase by about 10% (U.S. CBO, 2017). Numerous scholars have studied the impact of eliminating the individual health insurance mandate on premiums in individual insurance markets and on the number of uninsured individuals (Eibner & Price, 2012; Eibner & Saltzman, 2015; Hackmann, Kolstad, & Kowalski, 2015; Sheils & Haught, 2011). However, there has been little research focusing on the expected repercussions on veteran health coverage. In this article, I examine the impacts of the ACA on veteran health benefits and discuss the expected repercussions of its repeal on the number of uninsured veterans and VA insurance enrollments. I analyzed 52,692 nonelderly veterans from 2008 to 2017 in California (CA) and Florida (FL). Also, I analyzed 97,521 nonelderly nonveterans in the two states to compare the effect of the individual mandate between veterans and nonveterans.

Health Insurance and the Veteran Population

Individual Health Insurance Mandate

The ACA adopted a “carrot-and-stick” strategy to decrease the number of uninsured Americans and to reduce health insurance premiums for individuals: The carrot was subsidies for low-income households and the stick was the individual health insurance mandate (Eibner & Saltzman, 2015). The individual mandate under the ACA requires that most citizens and residents in the United States have health insurance that satisfies the specific standards of the ACA. And a tax penalty—that is, the greater of US$695 or 2.5% of household income—is imposed on people who do not have health insurance (Eibner & Saltzman, 2015). The core of the individual mandate is to keep insurance premiums affordable for individuals who do not have access to employer or public insurance by expanding the risk pools so that people from diverse socioeconomic sectors are included (Mukherjee, 2017).

The Tax Cuts and Jobs Act, passed by Congress in December 2017, repealed the individual health insurance mandate (Mukherjee, 2017). In 2016, there were 28.1 million uninsured, accounting for 8.8% of the total population (Barnett & Berchick, 2017). The repeal would increase insurance premiums for individuals who are not covered by employer-provided health insurance but earn too much income to qualify for federal health programs. Moreover, given that veterans’ health is worse than that of nonveterans’ (Teachman, 2011), the repercussions of the repeal, such as soaring premiums and resultant loss of insurance, would be much more significant on veterans than nonveterans. In addition, given that low-income veterans are more likely to use VA health care (Nelson et al., 2007), soaring premiums in the individual market would lead to an increase in the number of veteran enrollments in VA insurance beyond the 50% of veterans that are currently enrolled.

Unique Attributes of the Veteran Population

Veterans have unique health issues as differentiated from those of the nonveteran population. Frequent exposure to dangerous environments is a significant factor that has caused the inferior health status of veterans such as severe physical wounds and psychological stress. About 1,573 veterans, who have deployed in Afghanistan and Iraq since 2001, reported one or more limbs missing (Fischer, 2015). Another consequence of the operations is psychological disorder: Among deployed service members, 38% of soldiers, 31% of marine, and 49% of the national guard reported psychological symptoms including post-traumatic stress disorder (PTSD) and traumatic brain injury within 120 days after return from their the deployments, but concerns about stigma prevented them from getting desired psychological treatments (Arthur, MacDermid, & Kiley, 2007). Moreover, PTSD is prevalent in nondeployed veterans as well as deployed veterans: 15.7% of Operation Enduring Freedom/Operation Iraqi Freedom deployed veterans, and 10.9% of nondeployed veterans were diagnosed with PTSD (Dursa, Reinhard, Barth, & Schneiderman, 2014). Given that 3.6% of U.S. adults over the age of 18 years have PTSD (National Institute of Mental Health, 2017), PTSD is much more prevalent in veterans than nonveterans. Moreover, veterans diagnosed with PTSD are 4 times more likely to commit suicide than non-PTSD veterans (Jakupcak et al., 2009).

Substance use disorder (SUD) is another health issue in veterans: Over 11% of veterans deployed to Iraq or Afghanistan have been diagnosed with SUD (Seal et al., 2011), while 4% of U.S. adults have SUD (National Institutes of Health, 2015). Veteran SUDs are closely related to PTSD: 27% of veterans having PTSD are diagnosed with SUD (National Center for PTSD, n.d.). In addition, the veteran population remains overrepresented among the homeless population, accounting for 7.3% of the general U.S. population (U.S. Census Bureau, 2017a) but 9% of the total homeless population (National Alliance to End Homeless, 2019). Moreover, homeless veterans are more likely to suffer severe chronic diseases (Fargo et al., 2012).

The veteran population is not a homogenous group. Health status in the veteran population varies depending on race or ethnic group. The veteran population consists of 76% White, 12.5% Black, 7.5% Hispanic, and 1.6% Asian (National Center for Veterans Analysis and Statistics, 2018). Black, Hispanic, and other minority race/ethnic veterans have health status that is worse than White veterans. Health status is derived from the differences in socioeconomic resources (e.g., income and educational attainment) and military experience (e.g., branch of service and exposure to battle; Sheehan, Hummer, Moore, Huyser, & Butler, 2015).

Despite the inferior health status of veterans and the high demand for health insurance, 510,000 (5.5%) of the total 9.2 million nonelderly veterans remained uninsured in 2016 (U.S. Census Bureau, 2017b). Also, only about 9 million of the total 18.5 million veterans were enrolled in the veteran health-care system in 2016 3 (U.S. Department of VA, 2017). Uninsured veterans are likely to be trapped in a double jeopardy situation (Kirby & Kaneda, 2013) in that they are uninsured despite their poor health status and, therefore, are at higher risk of needing intensive medical care.

Previous Research on the Effects of Health-Care Reform

Veteran health coverage increased after the implementation of the national health-care reform. Before the ACA, more than 1.5 million veterans were uninsured, and the uninsured veterans were likely to be unmarried, Black, low-income, and post–9/11 deployed veterans (Tsai & Rosenheck, 2014). Haley, Kenney, and Gates (2017) demonstrated two positive effects of national health-care reform on veteran health coverage in 30 states between 2013 and 2015: (1) the number of uninsured veterans decreased by 40% for the first 2 years after the implementation of the ACA, and (2) the newly insured veterans were concentrated in Medicaid and private insurance within the individual markets. The ACA also affected veterans’ decisions about joining the VA health-care system. Analyzing two VA regional networks between January 2009 and March 2014, Silva et al. (2016) found that, during the ACA open enrollment period, the number of newly enrolled low-income veterans increased, new enrollments were greater in nonexpansion states, and primary care visits of low-income enrollees decreased. Likewise, Frakt, Hanchate, and Pizer (2015) found that Medicaid expansion absorbed demands for VA health insurance: Enrollments in VA health-care systems were 10% lower in Medicaid expansion states than nonexpansion states in 2014. While previous research demonstrates that the ACA positively influenced veteran health coverage and VA insurance enrollment, there has been little research conducted on the effects of the individual mandate outside of Medicaid expansion. 4

Theoretical Explanations of the Impact of the Individual Mandate

Adverse Selection and Death Spiral

Insurance can be described as “an actuarially fair price” when every insured individual pays a premium equal to the expected value of loss (Weimer & Vining, 2017). However, since insurers cannot know the exact probabilities of each possible contingency, the associated expected payouts, and the behavior responses of insured individuals to the contingencies, it is almost impossible for the insurers to charge actuarially fair prices (Weimer & Vining, 2017). As a response to the risk of loss due to uncertainties, insurers use risk pooling based on individual risk classifications. In risk pooling where members with independent risks agree to share unexpected loss, insurance largely relies on fortunate members whose insurance premiums are used for paying the losses of the unfortunate members (Baker, 2002).

Adverse selection is described as a phenomenon in which low-risk insured individuals choose to drop out of insurance pools in search of lower or no premiums, and only high-risk individuals remain in the insurance pool due to their need for generous insurance, which leads to soaring insurance premiums (Baker, 2002). Adverse selection is closely associated with information asymmetry between insurers and potential insurance policy holders regarding an individual’s probability of future contingency (Weimer & Vining, 2017). Due to information asymmetry, insurers cannot effectively conduct individual risk classifications (Weimer & Vining, 2017). Moreover, adverse selection problems can evolve into a vicious cycle called the “death spiral” which is made up of four elements: (1) an exodus of low-risk individuals, (2) increase in expected claims for future contingency, (3) the insurer’s decision to raise premiums, and (4) greater opt outs of low-risk individuals due to unaffordable premium (Buchmueller & DiNardo, 2002).

The individual mandate has the positive effect of increasing the number of insured while reducing insurance premiums by reducing adverse selection problems (Eibner & Price, 2012; Eibner & Saltzman, 2015; Hackmann et al., 2015; Sheils & Haught, 2011). Given that veterans have an inferior health status and resultant higher demands for health insurance than nonveterans (Dursa et al., 2014; Fischer, 2015; Jakupcak et al., 2009; Seal et al., 2011), the impact of the individual mandate on the veteran population would likely be larger than on the nonveteran population, as a substantial number of uninsured veterans can access more affordable health insurance than before. Based on the adverse selection theory and previous studies on the effect of the individual health insurance mandate, I establish the following hypothesis:

Substitution Effect

In microeconomics, substitution effect refers to “the rate at which consumers switch spending to or from a commodity when its relative price changes but the total utility of consumers is left constant” (Substitution Effect | The Penguin Dictionary of Economics, 2003—Credo Reference). The consumer substitutes a relatively expensive good with a relatively cheaper one that gives the same utility. In the insurance context, Medicaid can substitute for individual private health insurance: Medicaid expansion for pregnant women might lead to a substantial decrease in employer-sponsored insurance coverage (Dubay & Kenney, 1997), and Medicaid expansion for children could substitute for private insurance coverage (Dubay & Kenney, 1996).

Although most veterans who served in the military and were discharged with honor are eligible for veteran health-care benefits, only about 50% of the veteran population in 2016 were enrolled in the veteran health-care system (U.S. Department of VA, 2017). Veterans who use VA health-care facilities are more likely to be low-income, less educated, uninsured, and have poorer health status (Nelson et al., 2007). The disability status of a veteran has a significant positive effect on use of VA health care (Hisnanick & Gujral, 1996). Veteran demands for VA insurance can be replaced with private insurance. The number of uninsured veterans substantially decreased during the first 2 years after ACA implementation, with Medicaid and private insurance in individual markets embracing most of the previous uninsured veterans (Haley, Kenney, & Gates, 2017). Also, the number of new enrollments in the VA health-care system was 10% lower in Medicaid expansion states than nonexpansion states in 2014 (Frakt, Hanchate, & Pizer, 2015). Since the implementation of the individual mandate would contribute to reducing unaffordable premiums for many veterans in individual insurance markets and since private health-care centers have better accessibility than VA health-care centers, veterans are expected to replace VA insurance with more affordable private insurance. Based on the substitution effect and previous studies, I establish the following hypothesis:

Income Effect

In microeconomics, income effect refers to the “impact of change in spending power on the demand for the product with the price that has changed” (Income Effect | The Penguin Dictionary of Economics, 2003—Credo Reference). Since the income elasticity of health insurance is lower than 1, health insurance is regarded as a necessary good (Lee & Chiu, 2012). This means that the demand for health insurance increases as real income grows, but proportionately not as much as growth in real income. In other words, change in insurance premiums would have a larger impact on low-income households than average or above income households. Access to health care varies depending on individual socioeconomic status (SES; Shi & Singh, 2015). If individual veterans can afford to pay the soaring insurance premiums, they will stay in their private insurance group despite the increased premiums. On the other hand, veterans with low income probably cannot pay the raised premiums, and thus, they will decide to drop out of their insurance group. Instead, low-income veterans will try to meet their medical needs by joining VA insurance (Nelson et al., 2007). The implementation of the individual mandate has had a positive effect on reducing insurance premiums (Hackmann et al., 2015), and its repeal could lead to soaring premiums and substantial numbers of newly uninsured (Eibner & Price, 2012; Eibner & Saltzman, 2015; Sheils & Haught, 2011; U.S. CBO, 2017). Given that low-income veterans would likely be susceptible to changes in premiums, the impact of the individual mandate would be more significant for them. Based on income effect theory, I establish the following two hypotheses:

Sample, Measurements, and Method

Sample

In this article, the unit of analysis is an individual veteran. Given variance in health policies depending on states, analyzing veterans in all 50 states would be significantly disturbed by unobserved error terms. However, analyzing veteran samples from a single state would bring into question the external validity of the result. To overcome this weakness, I collected veteran samples from two representative states, CA and FL, in terms of Medicaid expansion and the number of veteran residents: (1) FL is a nonexpansion state while CA is an expansion state, and (2) CA and FL represent the first- and third-largest states in number of veteran residents, respectively (National Center for Veterans Analysis and Statistics, 2018). To analyze the effect of the individual mandate on veteran enrollments in private insurance and VA insurance, I used pooled cross-sectional data 5 obtained from the Integrated Public Use Microdata Series from the United States for 2008 through 2017 (Ruggles et al., 2017). I investigate how the individual mandate affects veteran health coverage and discuss the expected repercussions of its repeal. I hypothesized that veteran health coverage would change substantially following the implementation of the mandate in January 2014.

I restricted veterans sampled from FL and CA to nonelderly veterans between the ages of 19 and 64 years because elderly veterans over 65 years would be more likely to be covered by Medicare 6 rather than individual private insurance. Also, since my research interest is individual veterans who should directly purchase their insurance in individual markets, I excluded veterans covered by Medicaid, current or former employers, or unions. As a result, the final working sample consisted of 25,678 veterans in CA and 27,014 in FL. In addition, I sampled nonelderly nonveterans to examine whether the effect of the mandate is more significant on veterans than nonveterans: 60,777 nonveterans in CA and 36,744 in FL. 7 In Table 1, I list the measurement and coding of the variables and estimated means of the samples.

Description of Variables and Estimated Means.

Note. CA = California; FL = Florida; AI = American Indians; AN = Alaska Natives; VA = Veteran Affairs.

Measurements and Method

Dependent variables

I adopted “Private Insurance Coverage” and “VA Insurance Enrollment” as dependent variables in the regression models to estimate the effect of the individual mandate on veteran health coverage. Given “H1” about mitigated adverse selection in the individual market after implementation of the individual mandate, Private Insurance Coverage was measured as binary: 1 if a veteran has a private health insurance purchased in the individual market; 0 otherwise. To probe whether implementation of the individual mandate affects a veteran’s decision whether or not to join VA insurance, VA Insurance Enrollment was measured as binary: 1 if a veteran has health insurance through the Department of VA; 0 otherwise.

Independent variables

“Individual Mandate” was measured as binary. Since the individual health insurance mandate became effective in January 2014, the supply and demand curve in the individual insurance market changed starting from 2014 as more healthy and low-risk individuals were required to participate in the market. Thus, Individual Mandate is measured as 1 if year is equal to or greater than 2014; 0 otherwise. Since the implementation of the mandate might take some time to affect a veteran’s decision on joining the insurance, like a washout period of the ACA (Gutierrez, 2018), I divided the effect of the mandate into 4 years to see whether the mandate has a lagged effect: “Mandate in 2014, 2015, 2016, and 2017.” The variables were measured as binary: 1 if year is 2014, 2015, 2016, and 2017, respectively; 0 otherwise. Those variables substitute for Individual Mandate in modified models. Since the reference group consists of samples before 2014, Mandate in 2014, 2015, 2016, and 2017 would show whether the mandate has a significant effect in each year. “Income Level” was measured as individual annual incomes divided by US$10,000. This variable was used to estimate the income effect of an increased insurance premium: The high-income veteran’s demand for private or VA insurance would be less affected by soaring premiums than the low-income veteran’s demand. “Interaction term between Income Level and Individual Mandate” was also included since the effect of the individual mandate was expected to vary depending on an individual’s income level. The interaction term variable was created by multiplying the two independent variables.

Control variables

“Veteran Disability” indicates the degree of veteran disability related to military service. The Veterans Health Administration (VHA) provides different health-care services at differing costs to the veterans depending on the degree of service-connected disability. Veterans with a high rating of disability can get more generous health-care services with low cost, and thus, they would be more likely to use VA health hospitals (Hisnanick & Gujral, 1996). Veteran Disability was measured as six ordinal scales, coded: 1 for no disability rating, 2 for disability rating below 10%, 3 for 10 or 20% disability rating, 4 for 30 or 40%, 5 for 50 or 60%, and 6 for 70% or higher. Also, I employed “Private Insurance” and the “interaction term between Private Insurance and Individual Mandate” to control the effect of having private insurance coverage on the VA insurance enrollment. Because private insurance can substitute for VA insurance (Haley et al., 2017) and the implementation of the individual mandate should make private insurance premiums more affordable, veterans who have private insurance coverage will be less likely to enroll in VA insurance. The interaction term would show whether the effect of the individual mandate on the VA insurance enrollment varies depending on private insurance coverage. Private Insurance was measured as binary: 1 if a veteran has a private insurance coverage; 0 otherwise. The interaction term variable was created by multiplying the two variables.

Access to health care is significantly affected by race, income, and job. In the United States, low SES and minority membership is closely related to poor access to health care (Shi & Singh, 2015). Thus, I included as control variables “Employed Status,” “Education Level,” “Race,” “Sex,” and “Age.” “Employment” was measured as binary: 1 if a veteran is employed; 0 otherwise. Education Level means the highest educational attainment: Respondents were told to choose the highest degree or level of school they achieved. It was measured as 11 ordinal scales depending on the highest attainment: 0 for no schooling; 1 for completion of Grade 4; 2 for competition of Grade 5, 6, 7, or 8; 3 for Grade 9; 4 for Grade 10; 5 for Grade 11; 6 for Grade 12; 7 for competition of 1 year of college; 8 for 2 years of college; 9 for 3 years of college; 10 for 4 years of college; 11 for 5 or more years of college. Given veteran health disparity among race groups (Sheehan et al., 2015), Race was specified into White, Black, Asian, American Indians and Alaska Natives (AI/AN), and Hispanic: Those were measured as binary in four dichotomous variables: 1 if a veteran belongs to the race group; 0 otherwise. I used White as a reference group for the other race variables, so I excluded White in the equations. Sex was measured as 1 if a veteran is male and 0 otherwise. Age was measured as reported veteran’s age in years. In addition, to control year effect in the regression models, I added “year ordinal variable (t).” I assigned an ordinal number to each year by 1 incrementally: for example, 1 for 2008 and 10 for 2017.

Method

I integrated all variables into the following regression equations: “α” indicates intercept of the regression, and “βi” indicates coefficients of the independent or control variables.

Given that the sample is pooled cross-sectional data and that the dependent variables are binary (0 or 1), I used a logit regression (LR) of Stata Version 14 to estimate effects of the individual mandate. In modified models of (1) and (2), Individual Mandate is replaced with Mandates in 2014, 2015, 2016, and 2017 to examine the Mandate’s lagged effect over time. Given the disparity in health policy between CA and FL, I analyzed veteran samples separately to control unobserved error terms. Also, I analyzed nonveteran samples in the model (1) to compare the effect of the mandate on veterans with that of nonveterans. The variance inflation factor tests indicated that the regression models suffer multicollinearity problems with the independent variables of “age, education, and year.” However, given that the sample size of 52,692 veterans is quite large, the multicollinearity problem does not lead to biased estimators (Berry & Feldman, 1985). 8

Findings

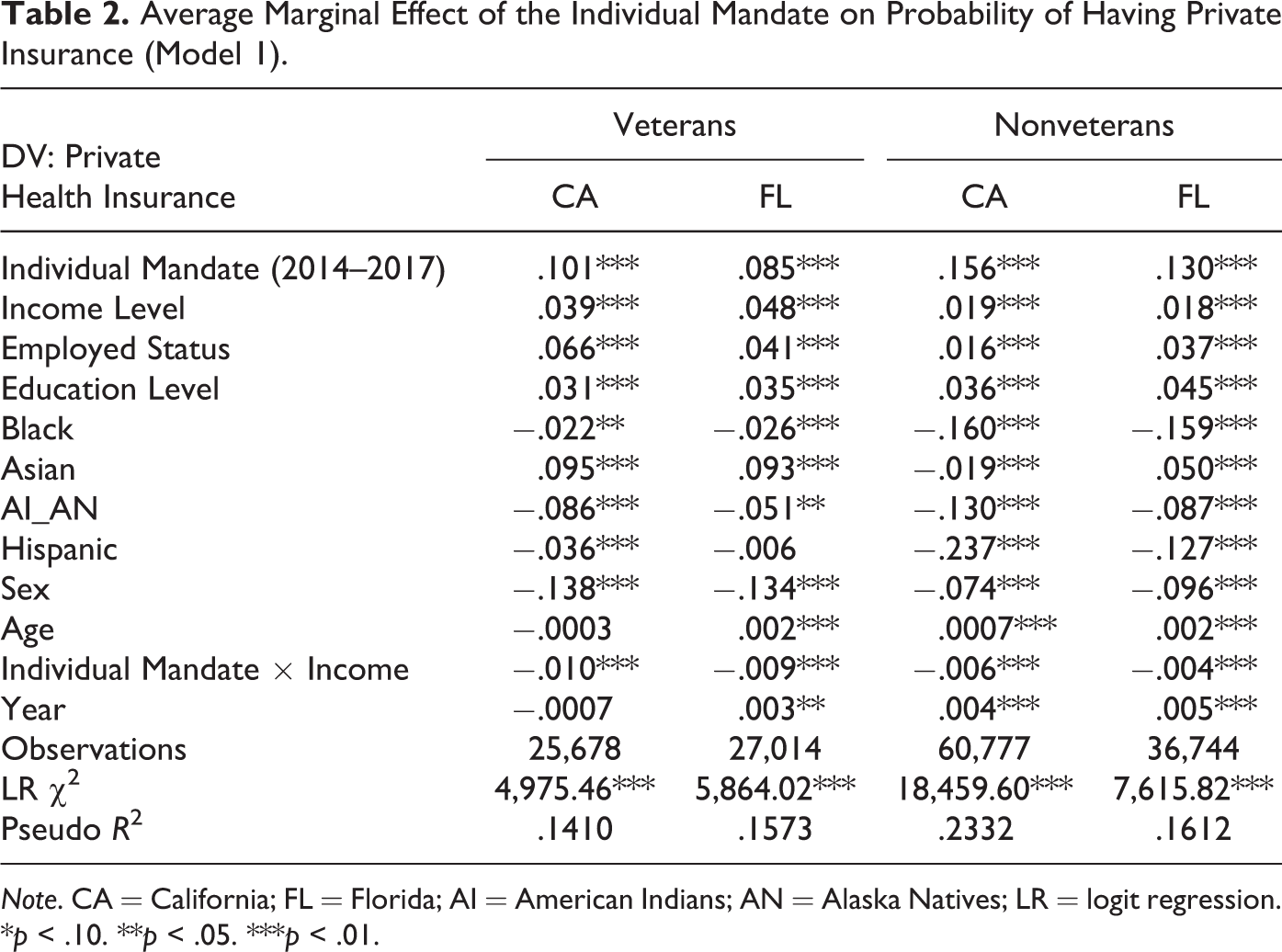

I estimated models of LR to investigate the effect of the individual mandate on veteran’s health insurance coverage in the individual insurance market and on veteran health insurance enrollment. All LR models were statistically significant based upon the LR χ2 test. Table 2 presents the results of the LR Model 1 about the average marginal effect (AME) 9 of the individual mandate on the probability of having private insurance in veterans and nonveterans. In Table 2, the implementation of the individual mandate has a positive effect on reducing the number of uninsured veterans as well as uninsured nonveterans in the individual market.

Average Marginal Effect of the Individual Mandate on Probability of Having Private Insurance (Model 1).

Note. CA = California; FL = Florida; AI = American Indians; AN = Alaska Natives; LR = logit regression.

*p < .10. **p < .05. ***p < .01.

When it comes to effects of SES, a veteran who has attributes of employed, older, female, and higher education and income level is more likely to have individual health insurance coverage. First, the implementation of the individual mandate from 2014 through 2017 increased the probability that a veteran would have private health insurance in the individual market in both CA (10.1%) and FL (8.5%). Thus, the analysis supports H1, positing a positive effect of the individual mandate on veteran health insurance coverage. This result is consistent with previous studies that the individual mandate leads to mitigated adverse selection, reduced insurance premiums, and increased numbers of insured individuals in the individual markets (Eibner & Price, 2012; Eibner & Saltzman, 2015; Hackmann et al., 2015; Sheils & Haught, 2011). 10

Second, the analysis results show that individual income level has a significantly positive effect on veteran health insurance: An increase of US$10,000 in individual annual income raises the probability of veterans having private insurance by 3.9% in CA and 4.8% in FL, meaning that high-income veterans are more likely to have individual health insurance than low-income veterans. Also, the interaction term between individual mandate and individual annual income level has a significant negative effect: a decrease of 1% in the probability in CA and 0.9% in FL, which is presented in Figure 1. This means that the positive effect of the mandate on the probability of veterans’ private insurance will decrease as annual income increases. Figure 1 shows that the effect of the mandate remains positive at annual income levels less than US$70,000 in CA and US$60,000 in FL, but it becomes negative beyond an annual income level of US$150,000 in the both states. 11 Thus, this result supports both H3 (positive income effect) and H4 (the mandate effect modified by individual income level).

Average marginal effect of the mandate on probability of having private insurance depending on veteran’s income level with 95% confidence intervals.

Third, veterans, who are employed and are highly educated, are more likely to have private health insurance in both CA and FL. Although there was disparity in the statistical significance of race effects between two state, the effect directions were consistent: Veterans who belong to Black, AI/AN, or Hispanic groups are less likely to have private insurance than otherwise. This result is consistent with previous research that access to health care is positively associated with high SES (Shi & Singh, 2015) and veteran health status varies depending on racial groups (Sheehan et al., 2015).

Fourth, the mandate has a positive impact on the probability that a nonveteran will have a private insurance in the individual market: The implementation increased the probability by 15.6% in CA and 13% in FL, which is higher than in veteran groups (an increase of 10.1% in probability in CA and 8.5% in FL). The higher effect of the mandate in nonveterans can be explained by the income gap between veterans and nonveterans: Veterans get at least US$10,000 higher median annual income than nonveterans, and the gap is even bigger in female comparison (U.S. Department of VA, 2019b). Given the income effect of the mandate, implementation of the mandate would lead to a greater increase in the number of insured nonveterans than veterans. Also, difference in the effect can be explained by other socioeconomic attributes of the veteran population such as higher education levels, lower unemployment rate, and lower uninsured rates (U.S. Department of VA, 2019b).

Table 3 shows the AMEs of the mandate in each year in Modified Model 1. 12 The effect of the individual mandate on veterans’ private health coverage was prompt and consistently significant from 2014 through 2017 in both CA and FL. Moreover, the mandate effect in 2015, 2016, and 2017 is larger than in 2014 in both CA and FL, which suggests a lagged effect of the mandate. Also, like the veteran groups, the effects of the mandate on probability of nonveteran groups increased after 2014, suggesting its lagged effect.

Average Marginal Effect of the Individual Mandate in Each Year on Probability of Having Private Insurance Coverage (Modified Model 1).

Note. CA = California; FL = Florida; AI = American Indians; AN = Alaska Natives; LR = logit regression.

*p < .10. **p < .05. ***p < .01.

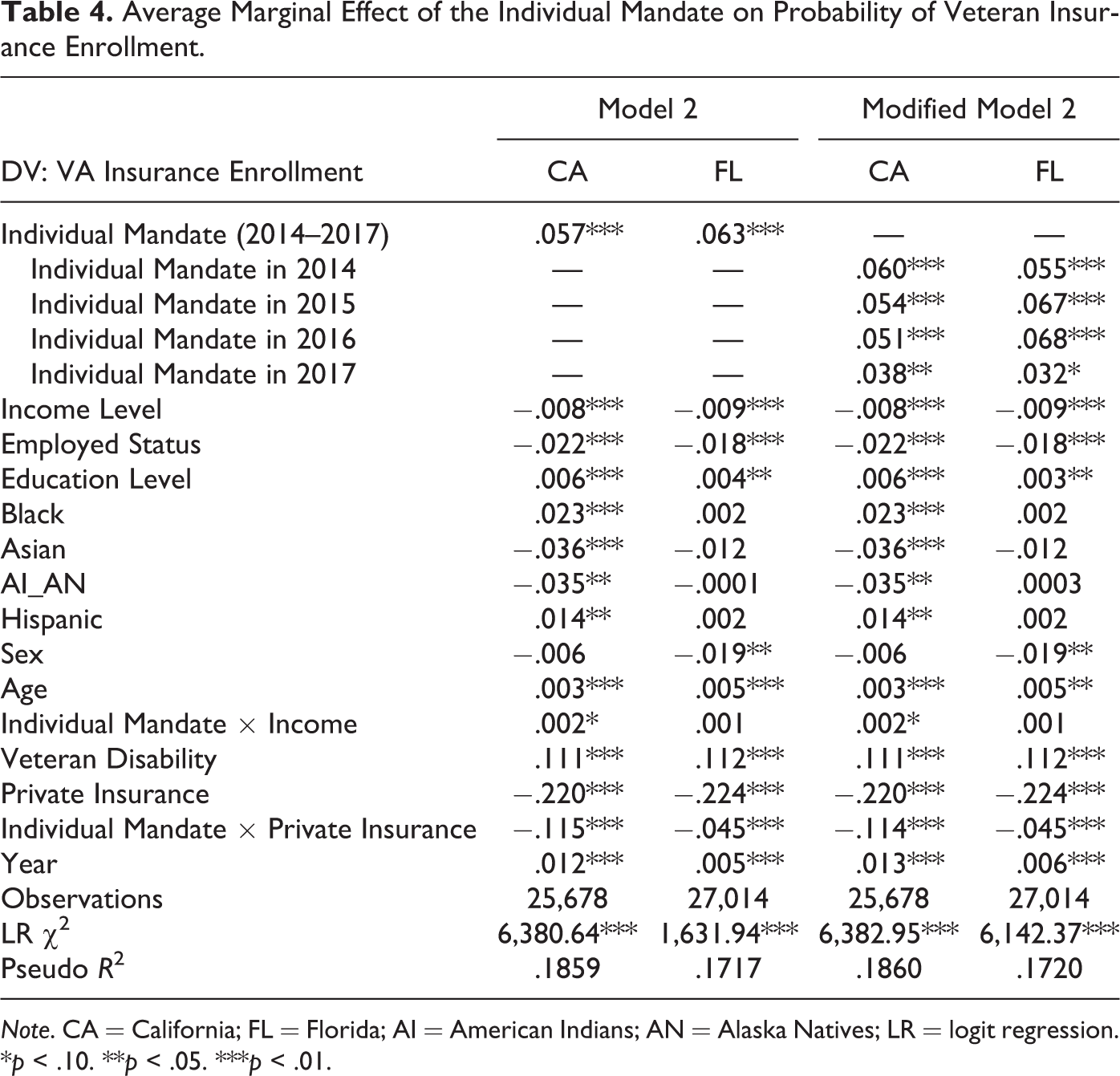

Table 4 presents the AME of the individual mandate on VA insurance enrollment. Veterans are more likely to enroll in VA insurance after the implementation of the individual mandate than before. While a veteran who is older and has a service-connected disability and higher education is more likely to have VA insurance, a veteran who has a job and higher income is less likely to have it.

Average Marginal Effect of the Individual Mandate on Probability of Veteran Insurance Enrollment.

Note. CA = California; FL = Florida; AI = American Indians; AN = Alaska Natives; LR = logit regression.

*p < .10. **p < .05. ***p < .01.

First, in Model 2, the effect of the individual mandate on VA insurance enrollment is statistically significant in both CA and FL, but the direction is opposite to H2, positing a substitution effect of the individual mandate. Also, the AME of the mandate in each year in Modified Model 2 shows that the effect of the mandate on veteran insurance enrollment is prompt and consistently significant from 2014 through 2017. The effect of the individual mandate on VA insurance enrollment varies depending on whether a veteran has private insurance: (1) When a veteran has no private insurance, the implementation of the individual mandate leads to, on average, an increase of 5.7% (CA) and 6.3% (FL) in the probability that the veteran will secure veteran health insurance through the VA; and (2) when a veteran has private insurance, the AME of the mandate on the probability of enrollment decreases to −5.8% in CA and 1.8% in FL. 13

I hypothesized that since insurance premiums in the marketplace would be reduced due to the individual mandate, more uninsured veterans would join affordable private insurance plans rather than participate in enrollment in the veteran health-care system. However, since enrollment in the veteran health-care system meets the minimum requirement of the individual mandate under the ACA (U.S. Department of VA, 2015), uninsured veterans, who cannot afford the high premiums in the insurance marketplace, are likely to enroll in the veteran health-care system to avoid the tax penalty of the mandate. This is supported by the result that a veteran not having private insurance coverage is 22% more likely to enroll in VA insurance, and the effect of private insurance status is still significant after the implementation of the mandate.

Second, individual income level has a negative effect on veteran insurance enrollment: An increase of US$10,000 in annual individual income leads to, on average, a decrease of 0.8% (CA) and 0.9% (FL) in the probability of having VA insurance. Thus, H3, positing an inverse relationship between individual income level and the VA insurance enrollment, is supported. The interaction term between individual mandate and individual income level is statistically significant in CA but insignificant in FL. Thus, H4 is partially supported.

Figure 2 illustrates how veterans’ private insurance status and annual income level modify the AME of the mandate on the probability of VA insurance enrollment in CA. The AME is statistically insignificant if the confidence interval includes zero. When a veteran has no private insurance, the mandate has a positive significant effect on the probability over all income levels. On the other hand, when a veteran has private insurance, the mandate has a negative significant effect only within income levels less than US$110,000. Figure 2 suggests that the effect of the mandate on VA insurance enrollment is more significantly influenced by a veteran’s private insurance status than annual income level.

Average marginal effect of the mandate on probability of Veteran Affairs insurance enrollment depending on veteran’s private insurance status and income level with 95% confidence intervals.

Third, among the control variables, employed status, educational level, and veteran disability have statistically significant effects on the probability of having veteran health insurance through the VA: Veterans who are unemployed and suffering disability are more likely to have veteran health insurance. The result is congruent with previous studies that veterans who use VA health-care facilities tend to be low income, and have a poorer health status (Nelson et al., 2007), and that veterans having disabilities are more likely to rely on veteran health-care services (Hisnanick & Gujral, 1996; Hynes et al., 2007).

Conclusion and Implications

The ACA contributed to reducing the number of uninsured people by expanding eligibility for Medicaid and making individual health insurance more affordable through federal implementation of an individual health insurance mandate. However, Congress repealed the individual health insurance mandate in December 2017. To estimate the likely effect of the repeal of the individual mandate on veteran health insurance coverage, I analyzed 10 years of pooled cross-sectional data (2008–2017) and found that (1) veteran health insurance coverage in the individual market is positively associated with implementation of the individual mandate and individual income level; (2) the effect of the individual mandate on the probability of having private insurance is larger among nonveterans than veterans; (3) veteran insurance enrollment is positively affected by the individual mandate and demographic attributes such as race, low income, unemployment, and service-connected disability; and (4) the effect of the individual mandate on veteran enrollments in private insurance and VA insurance varies depending on individual income level.

The findings of this article are consistent with previous studies on the effects of the individual mandate on reducing the number of the uninsured in the general population (Eibner & Price, 2012; Eibner & Saltzman, 2015; Hackmann et al., 2015; Sheils & Haught, 2011) and on increasing VA insurance enrollments (Silva et al., 2016; Wong et al., 2018). Silva et al. (2016) found that the number of low-income enrollees in the VA health system substantially increased during the open enrollment periods of the ACA in 2013 and 2014, and the increase was higher in Medicaid nonexpansion states. The result from this study is consistent with Silva et al. (2016) in that low-income veterans are more likely to join VA insurance to meet the minimum requirement of the individual mandate and the probability of having VA insurance is higher in FL than CA. Wong et al. (2018) discovered that veterans in Massachusetts who already enrolled in VA insurance did not reduce their use of primary care in VA hospitals after the Massachusetts Health Reform. This strongly suggests that veterans already covered by VA insurance are not likely to replace it with private insurance. Both Silva et al. (2016) and Wong et al. (2018) support this study’s finding of a positive effect of the individual mandate on veterans’ enrollment in the veteran health-care system.

The effects of the mandate were consistent in both CA and FL, but the effect on veteran’s private insurance coverage was greater in CA while the effect on VA insurance enrollment was greater in FL. Medicaid expansion status can be a plausible explanation for that. 14 Private insurance premiums in Medicaid expansion states are 11% cheaper than those in nonexpansion states because high-risk, low-income individuals are covered by Medicaid (Sen & DeLeire, 2018). The lower premiums in CA led to the greater effect of the mandate on veteran’s private insurance coverage. On the other hand, low-income veterans covered by Medicaid are less likely to enroll in VA health care (Silva et al., 2016). Thus, the mandate effect on VA insurance enrollments was greater in FL.

The findings of this study suggest that the repeal of the individual mandate effective January 2019 leads to a considerable increase in the number of uninsured veterans who cannot access employer-sponsored insurance and cannot afford the expected higher insurance premiums: (1) 84,347 veterans in CA and 61,205 veterans in FL would lose their private insurance coverage, and (2) 47,602 veterans in CA and 45,364 veterans would leave VA insurance. 15 The number of newly uninsured veterans caused by the repeal would be less than that of newly uninsured nonveterans.

However, given the inferior health status of veterans and their higher need for health care, the loss of insurance should have a more significant impact on individual veterans’ health than on nonveterans’ health. Following the argument of Kirby and Kaneda (2013) about uninsured Blacks and Hispanics, the repeal of the mandate is likely to exacerbate the insurance double jeopardy of veterans: The poor health of uninsured veterans gets worse and worse, but their need for more intensive health care cannot be met without insurance coverage. Moreover, numerous uninsured veterans have serious access problems to health-care services: In 2004, more than 50% of uninsured veterans did not receive primary and preventive care, and about one fourth of the uninsured veterans reported unmet medical needs due to cost barriers (Himmelstein et al., 2007).

Thus, the VHA should establish a policy to minimize the expected repercussion of the repeal. Because unaffordable insurance premiums are one of the main reasons for being uninsured, the VHA should expand financial support for low-income uninsured veterans. In addition, given the low enrollment rates of eligible veterans in the veteran health-care system, the VHA should increase outreach efforts to educate, recruit, and facilitate their enrollments in VA health care.

Additionally, since veterans with the demographic attributes of unemployed, low-income, and service-connected disability are more likely to enroll in VA insurance, one of the important functions of veteran health-care services is to be a social safety net for vulnerable veterans. Because veterans’ demands for veteran health-care services increase substantially during an economic recession due to a decrease in individual incomes and an increase in the number of unemployed veterans (Wong, Maciejewski, Herbert, Bryson, & Liu, 2014; Yee, Frakt, & Pizer, 2016), the VHA should secure flexibility in operating veteran health-care facilities to expand their capacities to meet soaring demands during economic recessions.

However, this study has limitations. Because of a limitation in the secondary data, I did not differentiate between combat and noncombat veterans, and between honorably discharged and dishonorably discharged veterans. Noncombat veterans suffer PTSD at a similar rate as do combat veterans (Dursa et al., 2014), but given physical wounds received in combat, combat veterans may have higher demands for health care than do noncombat veterans. Also, given that dishonorably discharged veterans are ineligible for veteran health benefits, the ineligible veterans may have higher demands for private insurance than honorably discharged veterans. Thus, I suggest that future research on veteran health insurance coverage categorizes veterans into combat or noncombat and honorably or dishonorably discharged. Notwithstanding those limitations, this study provides valuable insights into the expected repercussions of the repeal of the mandate on the veteran population. Also, because I analyzed veterans in two representative states in terms of Medicaid expansion status and the number of veteran residents, the results and implications are more likely to be generalizable and applicable to other states in the United States.

Footnotes

Appendix A

Appendix B

Appendix C

Acknowledgments

We thank Drs. Keon-Hyung Lee, Daniel Fay, William Weissert, and anonymous reviewers for thoughtful and constructive suggestions.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.