Abstract

This article examines how the introduction of a mix of state and market-based regulatory mechanisms representing formal and informal institutional elements, respectively, impacts disclosure level of director and executive remuneration in Australia. In doing so, our study steps beyond the simple state versus market dichotomy that the extant literature is primarily concerned with and proposes a symbiotic relationship between the two. The results of our study reveal that both state regulation and self-regulation as bundles of corporate governance can potentially join forces to ease agency conflicts. What is more, certain well-institutionalized organizational practices that guide agents toward self-regulation remain highly relevant and significant, even in the presence of pervasive state regulation. The synthesis of constructs borrowed from agency and institutional theories and its testing in an empirical setting of Australia verifies the significance of formal (state regulation) and informal (self-regulation) institutional aspects in addressing moral hazard agency conflicts. Our research provides insights for public policy makers as to how policies can be developed for good corporate governance. Particularly, in the context of current global economic crises, policy makers would be better off choosing those institutional mechanisms of corporate governance that complement the state regulation with self-regulation for the management and regulation of the modern global economy.

Keywords

In recent times, director and executive compensation or (hereafter) remuneration has become a contentious issue and even alleged to be behind a series of corporate and financial collapses (Banks, Fitzgerald, & Fels, 2010; Hill, 2006; Hill, Masulis, & Thomas, 2010; Hill & Yablon, 2002; Miller, 2004). Failures of corporate governance are often linked to inadequate corporate reporting and disclosure (Whittington, 1993). Declining public confidence in institutional mechanisms to deal with such agency issues has raised questions about the adequacy of existing (market-based) governance arrangements to facilitate good corporate governance, particularly in regard to director and executive remuneration (Chapple & Christensen, 2005; Sheehan, 2009). This led nation-states including Australia to establish regulatory reforms to improve accountability and transparency of director and executive remuneration.

State-based regulation for corporate governance, the alternative to market-oriented mechanisms, often involves passing laws or prescriptive standards, typically as a response to crises of catastrophes (Hood, 1996). Such an approach to regulation is almost exclusively within the purview of governments and regulatory agencies. However, legislation that is highly prescriptive is often resisted by the market (Letza, Sun, & Kirkbride, 2004). To many regulatory theorists, corporate governance through self-regulatory codes is best, as it is likely to contribute to greater shareholder value (Desmond, 2000). Also, financial theorists in line with neo-liberalists assert that corporate governance regulatory mechanisms should be allowed to operate freely, as any interference with market-based regulatory mechanisms is irrational and will have a distorting effect (Hart, 1995; McSweeney, 2009; Sheehan, 2009).

Yet, governance is a unique social process of interaction between “institutions and actors” (Stoker, 1998, p. 18) and cannot work in isolation from other social and non-economic institutions representing “power, legislation, social relationships and institutional contexts” (Black & Baldwin, 2010; Letza et al., 2004). Hence, to what extent can society rely on self-regulation? Are corporate entities better governed through other means, for example, through statute? Recent academic thinking, backed by empirical research, appears to suggest that appropriate regulation is not a choice between state regulation and self-regulation but a synergistic mix of both (Bartle & Vass, 2007; Black & Baldwin, 2010; Brown, 2006; Brunoa & Claessensb, 2010; Ford, 2010; Kirkbride & Letza, 2003; Lazzarini & Mello, 2001; Smith, 2004; Verbruggen, 2009). Mendoza and Vernis (2008) argue that today’s relational state emphasizes co-responsibility in public and private spheres—which was a missing feature in previous modes of state. Governments hold a privileged status to guide and mobilize society by producing and disseminating information, raising awareness and promoting effective regulation. Given this relatively new approach, more evidence needs to be forthcoming to demonstrate the effect of such a mix on corporate governance practices, including disclosure behavior related to director and executive remuneration.

In this article, we examine what impact does the introduction of a mixed regulation have on remuneration disclosure levels? The econometric modeling of the impact of mixed regulation on a large number of Australian firms presents interesting insights about the effectiveness of institutional reforms, both formal and informal, undertaken to improve disclosure of director and executive remuneration in the last 10 years. The results of this study show that prior to the adoption of a mixed regulatory regime, there was no significant association between the corporate governance factor(s) and disclosure level of director and executive remuneration. However, after the implementation of a mixed regulatory regime, a statistically significant link can be found between corporate governance mechanisms and disclosure levels of director and executive remuneration.

The results of the study lead us to conclude that effective corporate governance is not an outcome of a mutually exclusive state regulation versus self-regulation dictum: indeed both state regulation and self-regulation representing formal and informal institutions, respectively, can address agency problems as a synergistic mechanism of corporate governance. Strong and independent regulation is not inconsistent with a flourishing market; governments pressured to respond could design regulation in a way that could be market-friendly.

Theoretical Underpinnings

A central concern of corporate governance as per agency theorists is the prospect that managers can use their power and status to pursue their personal self-interests over those of owners, especially in circumstances where a potential for conflict of interests are clearly present. Incomplete information leads to situation wherein the principal cannot determine if the agent is acting in the best interests of the organization (Eisenhardt, 1989; Gomez-Mejia & Balkin, 1992, p. 923). Information asymmetries eventually give rise to a situation of moral hazard. In the case of incomplete information, the principal has two options: The principal can purchase information about the agent’s behaviors and reward those behaviors through surveillance mechanisms such as budgeting systems, or additional layers of management; alternatively, the principal can reward the agent based on outcomes (e.g., profitability). Therefore, the challenge facing the principal is what control mechanism to adopt such that individuals pursuing their own self-interest will pursue the collective interest.

Eisenhardt (1988, p. 64) argues that good quality information and disclosure systems can control for managerial opportunism. Healy and Palepu (2001) suggest that corporate disclosure is vital for the efficient working of markets and detailed disclosure assists market stakeholders to assess risk and make effective decisions (Houthakker, 1982, p. 483). In particular, disclosure of director and executive remuneration can reduce information asymmetry by addressing structural and procedural problems of executive remuneration (Ferrarini & Moloney, 2004, p. 300). For instance, a detailed and better level of disclosure of director and executive remuneration can equip the principal to monitor the pay-setting process and verify that either executive remuneration of the agent is effectively aligned with the wealth maximization of the principal or not (Thévenoz & Bahar, 2007, p. 19). Business decisions are made in an ex post scenario, based on the level of disclosure of previous reported years; ex post disclosure of performance-based remuneration would empower the principal to decide about the continuation of business with a controversial fiduciary in future. Good level of disclosure can enable investors to act and manage conflicts of interest in the agency relationship (Gilson & Kraakman, 1984; Thévenoz & Bahar, 2007, p. 19). It is widely acknowledged that without disclosure, capital markets cannot function properly due to information asymmetry problems—agency conflicts (Cooper & Keim, 1983).

The corporate board and its committees as a first line of defense against agency problems represent and protect the interests of shareholders by functioning as an additional intermediate layer between shareholders and management (Conyon & Peck, 1998). Because individual shareholders are diffuse and lack access to perform monitoring actions, corporate boards perform this role on their behalf (La Porta, Lopez-de-Silanes, Shleifer, & Vishny, 1998). As a specialized institutional entity in a modern capitalist society, the corporate board performs oversight and pre-empts impropriety on the part of managers and executives by guiding the actions of the latter in line with good governance principles (Aguilera, 2005). The board of directors, comprising both non-executive and executive directors, represents the apex of a firm’s internal governance structure (Davidson, Goodwin-Stewart, & Kent, 2005; Fama & Jensen, 1983a, 1983b) and performs the information role that aids in controlling managerial behavior, hiring, compensating, and, where necessary, firing management (Jensen, 1993).

In the agency theory perspective, the degree of board independence purportedly determines the effectiveness of governance (Dechow, Sloan, & Sweeney, 1996), whereby outside independent directors are argued to be more vigilant than insiders and hence expected to be more effective monitors to reduce agency problems (Fama & Jensen, 1983a, 1983b; Gillan, 2006). It is argued that corporate boards with greater proportion of outsiders are more likely to remove a poorly performing manager than less independent boards. Similarly, firms whose boards have greater proportion of outsiders appear to make better acquisition-related decisions, whether as acquirers or as targets (Denis, 2001). Non-executive directors supposedly act as effective monitors because they want to exhibit and establish their reputation as decision experts in conflictual situations (Yermack, 2004, p. 2281-2282). Vigilant monitoring of management by board of directors can ensure better protection of shareholders thus providing an effective governance mechanism for the principals.

A relatively recent notion in the literature is that corporate boards are not solely responsible for effective corporate governance, and more importantly, board subcommittees and their composition play a pivotal role in governance affairs (Xie, Davidson, & Dadalt, 2003, p. 299). For instance, Davidson, Pilger, and Szakmary (1998) find that the perception of the market about “golden parachute” can be influenced by the composition of the remuneration committee. As an exponent of the corporate board, remuneration committees are usually assigned the responsibility of designing a contract (remuneration package) for firm executives and function as a proxy of shareholders by aligning the interests of shareholders with corporate executives. With expertise in designing incentive systems, remuneration committees facilitate arm’s-length contracting between executives and owners, and therefore act as a corporate governance arrangement by which the board can set remuneration policies to align shareholder interests in a more transparent manner (Conyon & Peck, 1998, p. 148). Uzun, Szewczyk, and Varma (2004) argue that the presence of a remuneration committee on the company board is positively associated with decreased likelihood of fraud. This governance mechanism can influence the board and executives to be more transparent by providing better information about their remuneration policies (Liu & Taylor, 2008; Nelson, Gallerya, & Percy, 2010). Consequently, this governance mechanism can lead toward improved disclosure level of director and executive remuneration thereby addressing the issue of information asymmetry.

Positive agency theorists link firm disclosure behavior and corporate governance by considering both as mechanisms of accountability (Cerbioni & Parbonetti, 2007; Ho & Wong, 2001; Jensen & Meckling, 1976). It is argued that corporate governance mechanisms such as board, committees and their composition can impact the level of corporate disclosure (Chen & Jaggi, 2000; Eng & Mak, 2003; Ho & Wong, 2001; Nelson et al., 2010). In fact, the presence of such corporate governance mechanism can strengthen the control of firms and provide intensive monitoring mechanisms to reduce opportunistic behaviors and problems of information asymmetry. Hence, it will be interesting to examine the relationship between corporate governance mechanisms and disclosure level of director and executive remuneration.

National governments have intervened to shift the equilibrium in the direction of behavior based control mechanisms. For example, in the United Kingdom, governments have intervened to facilitate the development of voluntary codes of practice by bringing together a diverse set of business groups. Such a move to promote self-regulation and self-policing has been based on expert opinion and a multitude of published studies, for instance, the Cadbury Report, Greenbury Report, and other recent efforts. Similarly in Australia, the government has intervened to facilitate the development of voluntary codes of practice by bringing together a diverse set of business groups in developing modes of regulation for corporate governance. These efforts included Bosch Report, Hilmer Report, Standards Australia, Investment and Financial Services Association (IFSA) Blue Book, and other contemporary initiatives (du Plessis, Hargovan, & Bagaric, 2011, p. 152). The aforementioned reports addressed some fundamental issues of corporate governance such as functions of the corporate board, independence of company boards, appointment and structure of board subcommittees such as audit, nomination and remuneration, CEO role duality, reporting to shareholders, and regulatory compliance. The reports were primarily intended to provide a fundamental corporate governance framework guided by self-regulation.

In the debate regarding what approach is to be adopted in developing a regulatory framework to address agency conflicts, institutional theory underscores the need for synergistic linkages between formal (regulatory) and informal (normative) aspects of institutions—similar to the mechanisms of state regulation and self-regulation respectively (North, 1991, 1996; Scott, 1987, 2008). Formal constraints confer legitimacy to those organizations that comply with established legal requirements brought forth by state regulation. Informal constraints furnish legitimacy to those organizations that conform to certain internalized controls or self-regulatory standards that in turn confers legitimacy in the regulatory domain for conformant organizations. Lack of conformity to institutional pressures can be sanctioned through rules and laws that are equipped with power and carry governance systems for organizations. Through state regulation, laws can be enacted by a government to govern the relationships between agent and principal. These governance systems are implemented through protocols or standard operating procedures (SOPs). Professional bodies at national and international level exert pressures on their respective professional members to comply with professional norms and this phenomenon can generate homogenized practices and processes across different organizations. Using SOPs, a principal can monitor the agent through the disclosure in remuneration reports as set by legal protocols and can spot any non-conforming entity.

Kirkbride and Letza (2004) suggest that development of regulation for corporate governance requires a shift away from the homeostatic approach of standard setting toward a holistic approach. Researchers (Houthakker, 1982; Lazzarini & Mello, 2001; Pirrong, 1995) have examined the role of state regulation and self-regulation in derivative markets; they urge investigations into the complementarity or linkages between state regulation and self-regulation. Villiers and Boyle (2000) likewise reject an either/or dualism in favor of the establishment of an appropriate mix of both state regulation and corporate self-regulation representing both formal and informal institutional aspects of modern organizations. Indeed, the recent developments of regulation of corporate governance in the United Kingdom and Australia suggests a substantial new direction where the boundaries of regulation are no longer determined by the choice between market-oriented or state-based regulation but through a more holistic approach that invokes the complementarity between and synergies of regulative and normative institutional aspects of corporate governance.

We discuss the Australian evidence that shows Australia has used a mix of both state regulation and self-regulation by utilizing its formal and informal institutions of corporate governance to address moral hazard agency conflicts. In doing so, we discuss the state regulation and self-regulation initiatives of formal and informal institutions of corporate governance in Australia and propose to examine their impacts on disclosure level of director and executive remuneration.

Australian Context

Starting from 2001, Australia witnessed a series of corporate collapses in a number of industries including the collapse of big corporations such as mining giants Centaur and Pasminco, HIH Insurance, the telecom giant One Tel, and the airlines company Ansett (Hill, 2005, 2006; Miller, 2004). The total damage of all these failures was more than Australian $13 billion and a loss of at least 20,000 jobs (Kohler, 2001). A similar trend was observed in the United States with the collapse of Enron that triggered the enactment of the Sarbanes Oxley Act 2002.

Oddly, there were large performance bonuses paid just before these collapses to outgoing Australian CEOs of National Australia Bank (Bolt, 2004), James Hardie Group (Charles, 2004) and One Tel (Hill, 2006, p. 65). These generous bonuses received some negative publicity and brought into question the empirical validity of the executive pay-for-performance model (Bebchuk & Fried, 2003, 2004; Gordon, 2002; Hill, 2006). Information asymmetries between the principal and agent regarding remuneration were identified as a factor behind the failure of governance and the imperfect functioning of the market for corporate control. Thus, disclosure of director and executive remuneration became a pertinent issue in Australia in the wake of corporate collapses of the last decade.

The Organization of Economic Co-Operation and Development (OECD) observes that while corporate governance failures underlie the global financial crisis, major differences at the national level among the OECD member countries are discernible (OECD, 2009). Particularly, Australia’s experience of the global financial crisis turns out to be vastly different from other member countries. Despite some dramatic local impacts, Australia found itself uniquely positioned to recover rapidly within a short period of time (Hill, 2012). There is a view that Australia’s strong and robust corporate governance system was a rallying force in weathering the storm and a source of leadership in the OECD (Bell, 2009; Hill, 2012; OECD, 2009).

The Australian government became more intimately involved in developing a set of regulatory frameworks for robust corporate governance in the last decade. The mechanisms of corporate governance were installed through both formal and informal institutions of Australia and aimed at bringing protection to investors through improvements in the quality of remuneration disclosure and transparency. Formal institutional reforms eventually led to the Corporate Law Economic Reform Program (CLERP) Act 2004 or commonly known as CLERP 9 replacing the earlier Company Law Review (CLR) 1 Act 1998. CLERP 9 demanded improved disclosure of director and executive remuneration thereby facilitating greater accountability and transparency in corporations. Disclosure requirements in relation to director and executive remuneration solicited detailed information including the pay-for-performance model (Clarkson, Van-Bueren, & Walker, 2006; Hill, 2006; McConvill, 2004). The Government also empowered the shareholders to raise their concerns about director and executive remuneration via an advisory vote—a “say on pay” phenomenon, to allow investors to make better and informed choices about doing future transactions with agents. Besides disclosure requirements, the second major reform agenda of the CLERP Act 2004 was the reform of audit practices (du Plessis, McConvill, & Bagaric, 2005; Farrar, 2005; McConvill, 2004). This aspect of the act brought an array of reforms with respect to the independence of auditors and auditing activities. To implement them, the Australian government took sweeping new initiatives to strengthen the role of the regulatory institution—the Australian Securities and Investment Commission (ASIC; McConvill, 2004, p. 25). ASIC administered and enforced the Corporations Act 2001, including the CLERP 9 provisions of mandatory disclosure of director and executive remuneration.

The goal of mandatory disclosure of director and executive remuneration was therefore to provide remedial information to assist shareholders or markets in general, for effective assessment and judgment about the risks associated with a given agent and company activities. Academics and practitioners were however at a quandary regarding what constituted a “good” mode of information regulation: state or market (Baldwin & Cave, 1999, p. 76). Among different schools of thought representing both sides of arguments, Coffee (1984), Easterbrook and Fischel (1984), and Fox (1997) represent the first school arguing that disclosure should be mandated by national statue and should not be left to the discretion of disclosing entities. By contrast, Choi and Guzman (1998), Macey (1994), and Romano (1998, 2005) contend that companies should disclose information according to their discretion because the invisible hand of the market would automatically discipline firms to generate the required disclosure. We examine the strength of these arguments by measuring the sensitivity of disclosure level of director and executive remuneration before and after the enactment of the law, that is, CLERP 9.

The Australian Government invoked informal market-based mechanisms for self-policing—facilitating better intercommunication among different private bodies whose interests are usually in conflict, even as market forces alone failed to bring them together for a common cause. In early 1990s, different business associations of Australia attempted to publish corporate governance codes for best practices, however, these initial attempts required the Australian Securities Exchange (ASX) to consolidate and formalize the universally accepted corporate governance codes. The ASX played a critical role by establishing the Corporate Governance Council that represented 21 different Australian business associations 2 and provided them a common platform to communicate, develop, and enforce corporate governance standards for a common purpose—self-regulation.

The Corporate Governance Council of the ASX (established in 2002) issued the first edition of the “Principles of Good Corporate Governance Practice and Best Practice Recommendations” in 2003 (ASX, 2003). In this guide, the ASX council not only demanded better disclosure of executive remuneration but also persuaded firms to make structural changes in company boards to ensure better governance and transparency of director and executive remuneration (ASX, 2003). These standards of ASX recommended company boards to institutionalize the presence of a remuneration committee on company board and having a majority of independent non-executive directors 3 on the remuneration committee. It is imperative to note, however, that the aforementioned structural changes, as recommended by the ASX, were not legally binding, but these were the best practices recommended for companies, which firms could follow as per their circumstances. However, in case companies did not adopt these best practices, an explanation had to be provided about the lack of adoption. These guidelines thus encouraged flexibility along with the transparency, by making companies obliged to investors for explaining “if not” and “why not” aspects of the recommended remuneration governance mechanisms.

ASIC was also involved in the educational role of good governance by engaging the ASX. Both these institutions signed a Memorandum of Understanding in 2004 regarding information sharing and enforcing the act on mutual basis (ASIC & ASX, 2004). This document became open to the public, and this Memorandum was to be used for the implementation of the CLERP Act 2004 (ASIC & ASX, 2004).

The juxtaposition of formal and informal institutions provides an excellent context within which to evaluate the relative efficacy of state versus market-based reforms to bring about institutional change in disclosure practices of the Australian firms. Interestingly, neo-liberal advocates (Business Council of Australia—BCA) 4 had previously raised strident criticisms against the participation of shareholders through an advisory vote in executive remuneration decisions (BCA, 2003)—observing that CLERP 9 was “bad law” that could disturb the forces of the free market economy (Hughes, 2003). In the Australian context, this interaction between diverse and often conflicting public and private institutions illustrates how both formal and informal institutions can be deployed to set an optimal corporate governance framework. This background not only allows us to examine the impact of regulatory changes on disclosure level of executive remuneration but it also assists us to propose that state regulatory and self-regulatory mechanisms, representing formal and informal institutions respectively, are non-mutually exclusive; indeed they can and do collaborate to reduce agency problems.

Hypotheses Development

Norms and values of professional bodies and stock exchanges to which firms are socialized can become very powerful governance mechanisms (Fiss, 2008; Hill, 2005). Recalling that the ASX had recommended the presence of remuneration committee, we propose that the presence of a remuneration committee can act as a powerful remuneration governance framework within which the board can set remuneration policies and align shareholder interests in a more transparent manner (Conyon & Peck, 1998, p. 148). The delegated responsibility of a remuneration committee is to design and review the employment contracts, set remuneration, and more importantly to observe the interest alignment between executives and shareholders (Carson, 2002, p. 6). In the absence of a remuneration committee on corporate board, Williamson (1984, p. 1216) argues that it would be similar to a situation in which an executive writes his or her employment contract with one hand and signs with the other. This governance mechanism can also force board and executives to provide more transparency about their remuneration policies (Liu & Taylor, 2008, p. 64; Nelson et al., 2010, p. 691). Consequently, this influence can lead to increased level of disclosure; thereby, we propose this association in the following hypothesis.

Another important governance mechanism is the practice of having a majority of independent non-executive directors on the remuneration committee. Arguably, outside independent directors who have various directorships can be expected to act as more effective monitors than the insiders (Fama & Jensen, 1983b, p. 315). This inclination may be due to fact that they want to exhibit and establish their reputation as decision experts in conflictual situations. Outside directors are also found to be more vigilant than internal directors, and this characteristic can reduce the chances of financial misstatements (Dechow et al., 1996). A positive link between the number of non-executive directors on remuneration committee and the disclosure level of director and executive remuneration is therefore proposed in the second hypothesis.

As mentioned earlier, members of the BCA, an important professional alliance among top ASX 100 firms who participated in ASX standard setting process, were strongly opposed to the CLERP 9. Driven by their own distinctive values and expectations, BCA had argued that market mechanisms guiding remuneration governance should be allowed to operate freely without any interference. Thus, it will be interesting to examine what BCA members did on its own to generate better level of disclosure than non-BCA members. By measuring the relationship between disclosure level and BCA affiliation, we predict that BCA membership would be positively associated with disclosure level of director and executive remuneration and we articulate this relationship in the following hypothesis.

In addition, disclosure levels of director and executive remuneration can be influenced by certain firm-specific factors such as company age, auditor type, leverage, firm size and industry type. These factors are associated with corporate disclosure level, and this association is evident in various studies (Ahmed & Courtis, 1999; Cerf, 1961; Cooke, 1992; Coulton, Clayton, & Taylor, 2001; Owusu-Anash & Yeoh, 2005; Wallace & Naser, 1995), which have examined the association between aforementioned company-specific characteristics and corporate disclosure levels. We include the aforementioned firm-specific factors as control variables in the empirical model.

Research Design

Sample Selection

The sampling frame for this research consisted of listed BCA members and S&P/ASX 100 index firms, which was drawn from a target population of 2,178 listed entities on the ASX. The final sample consisted of 56% BCA member and 44% non-BCA member firms as shown in Table 1 that was drawn via two different stages of the sampling process. The sampling criteria takes into consideration the following aspects: first, the firms which are listed during or after 2001 are not included; second, foreign domiciled firms are excluded because such companies do not come under the jurisdiction of the Australian corporate laws; and finally, the firms that experience any abnormal activity that can affect their disclosure practices are primarily excluded from the selection of the final sample as highlighted in two stages sampling process as shown in Table 1. This sampling process drew a grand total of 81 listed entities analyzed for years 2002 and 2006. This analysis fetched total 162 observations with almost equal representation of both BCA member and non-BCA member firms from the publicly available resources that included company websites and annual reports.

Sampling Details (N = 81).

Remuneration Disclosure as Dependent Variable

In Australia, disclosure requirements in relation to director and executive remuneration, amended through CLERP Act 2004, solicited detailed information including the pay-for-performance model (Clarkson et al., 2006; Hill, 2006; McConvill, 2004). CLERP Act 2004 required companies to disclose much more detailed information than its earlier incarnation CLR Act 1998—especially regarding three aspects of executive remuneration: (a) general disclosure of director and executive remuneration pertaining to the requirements of section 300A and the Australian Accounting Standard Board, (b) disclosure of the company’s pay-for-performance model related with section 300A, and (c) the engagement and participation of shareholders in deciding executive remuneration as per sections 250R, 250SA, 200F and 200G. These three aspects serve as the bases of constructing our research instrument, the disclosure index, which is developed to measure disclosure practices of the Australian firms. To quantify disclosure practices of each company, a scoring template was used to derive a disclosure index. Disclosure index methodology has been widely used by researchers (Cooke, 1989, 1992; Firth, 1979; McNally, Eng, & Hasseldine, 1982; Wallace, 1988; Wallace, Naser, & Mora, 1994; Whittington, 1993). The formulation of disclosure index was based on general principles of content analysis of company annual reports (Beattie, McInnes, & Fearnley, 2004, p. 214) and a category system. In establishing the index, we draw on the abovementioned three aspects of executive remuneration.

The index comprises of three main categories consisting of 15 disclosure items (see disclosure index—Table A1 of the appendix). This disclosure index measures the disclosure level of following remuneration elements: annual base salary, benefits, short-term cash and/or equity-based incentives, long-term cash and/or equity-based incentives, termination and post-employment payments of executives and directors.

The first category measures the general disclosure through four disclosure items. Under section 300A (1) (c), Items 1 and 2 are compulsory for the listed firms, whereas Item 3 of our index only applies to those companies that have subsidiaries. Disclosure Index Item 1 ascertains the disclosure of director and executive remuneration, and Index Item 2 records the remuneration disclosure of five company executives who have received the highest remuneration in the given financial year. It is imperative to mention that in case of group of companies the consolidated entity will also disclose the remuneration of five executives who have received the highest remuneration in addition to five highest paid company executives. This Index Item 3 hence measures the disclosure of subsidiary executives in addition to company executives. Index Item 4 measures the extent to which the Australian accounting standards (AASB 1046 and 124) are followed by companies to disclose director and executive remuneration. Section 296 (1) makes it binding for companies to prepare their financial reports and accounts as per the Australian accounting standards. The second category of our disclosure index measures disclosure level of pay-for-performance model with the help of eight disclosure items that constitute the major portion of the index. Sections 300A (1AA) and 300A (1AB) solicit companies to disclose the impact of company performance in terms of its earnings on shareholder wealth during the previous 4 financial years as well as in the current financial year, and these performance aspects with respect to shareholder wealth are included in our disclosure index as Items 5, 6 and 7. Disclosure Index Items 8, 9, 10, and 11 represent section 300A (1) (BA) that asks companies to disclose information about any remuneration element—short term or long term that is dependent on performance condition(s). In addition, it requires companies to provide details about such condition(s). Item 8 of our disclosure index records the presence or absence of a detailed summary of performance condition(s), and Item 9 seeks justification for the selection of the performance condition(s). Item 10 looks into the summary of assessment methods to determine whether the performance condition(s) is satisfied and whether the selection of those methods is justified. Item 11 of our disclosure index measures the external factors to which the performance condition(s) is compared, and in case when these factors represent other set of companies or securities index in which disclosing company is also a member, then whether such indices are disclosed. If there is no dependence of any securities element of remuneration on any performance condition, then Item 12 seeks justification for this non-dependency. In summary, second category ascertains the level of disclosure related to risk factors and performance conditions upon which cash or equity (both short term and long term) incentives are dependent.

Our third disclosure index category examines “say on pay” phenomenon. Item 13 measures the casting of non-binding vote by shareholders at the annual general meeting (AGM). Discussion regarding director and executive remuneration is compulsory at the AGM through section 250SA, and Index Item 14 records this information. Finally, Item 15 examines the role of shareholders during AGMs, insofar as whether they approve lump sum termination payments that exceed the specified limit as provided in sections 200F and 200G.

Of these 15 index items, only 5 belonging to categories 1 and 3 as listed in Table A1 of the appendix are binding for all of the companies. The remaining items are situational and can vary according to individual company circumstances and types of performance-based remuneration elements and schemes of a given firm. For instance, the five items of our disclosure index such as 3, 5, 6, 7, and 15 are situational and can vary according to individual company circumstances and situations. Similarly, disclosure level for 8, 9, 10, 11, and 12 items can vary as per the presence and types of performance-based remuneration elements in a given firm. However, remaining five items such as 1, 2, 4, 13, and 14 are legally binding for all the firms.

These 15 disclosure items were validated with the help of accounting and law academicians. The validated disclosure index was thereafter applied to company annual reports, AGM agenda documents, AGM webcasts and presentations and minutes of AGM to measure the disclosure level in pre- and post-regulatory periods. The presence and absence of relevant categories and their respective items of disclosure were recorded by following a binary coding scheme (0, 1) for each year—which quantified disclosure level of director and executive remuneration based on the equally weighted information items. To ascertain the internal reliability of our disclosure index for both years—2002 and 2006—we performed an analysis of reliability based on Cronbach’s alpha. This measurement of internal reliability can vary from 0 to 1, and the value above .7 is considered very good (Pallant, 2005, p. 90). In our case, our value was .94 that was well above .7.

The validated disclosure index computed the actual disclosure score for each company in pre- (2002) and post- (2006) era of mixed regulation. Thereafter, we computed a relative index of disclosure for each company for 2002 and 2006 following the methodology used by Owusu-Anash and Yeoh (2005, p. 97) as shown in Equation 1:

where dijt is the disclosure value for a disclosure index item i is related to company j in the year t (where year t can be 2002 and 2006), coded as 1 if item was disclosed or 0 if it was not disclosed by company j; moreover, mjt is the number of disclosure items that are relevant to company j and were actually disclosed in its annual report for year t; and njt is the maximum number of disclosure items that can be disclosed by company j in its annual report in year t. For this study, the relative disclosure index is the dependent variable that measures the change in disclosure levels of director and executive remuneration before and after the introduction of CLERP Act 2004 and the remuneration governance mechanisms. All data for independent variables were obtained from annual reports of ASX listed companies.

The Model

In our study, the relationship between the dependent variable (relative disclosure index) and the independent variables (presence of remuneration committee, number of non-executive directors and BCA membership) and control variables in each year of interest, that is, 2002 and 2006, is presented in two separate models to enable a simultaneous comparison between two periods, which differ in the system of regulation for corporate governance. In 2002, state regulation alone was in force, whilst in 2006, a mix of state regulation and self-regulation was in effect. The equation was derived from the hypothesized relations among the constructs of this research.

where Dijt is the disclosure value for a disclosure index item i related to company j in the year t (where year t can be 2002 and 2006) and eo is the stochastic disturbance or error term and assumed to be independent and normally distributed with the same variance.

A set of equations that share a common error structure with non-zero covariance can be contemporaneously correlated. In this case, the assumption of independence can be violated by deploying ordinary least squares (OLS) and single-equation approach will be inefficient (Judge, Hill, Griffiths, Lütkepohl, & Lee, 1988). Zellner (1962) devises seemingly unrelated regression (SUR) technique to control for contemporaneous correlations. This method estimates the parameters of all equations simultaneously, allowing for the parameters of each single equation to account for the information provided by the other equations and leads to greater efficiency of the parameter estimates (Wooldridge, 2002). The SUR approach examines correlations between error terms in the two regressions where disclosure indices for year 2002 and 2006 are the dependent variables. The estimation of the regression as a system makes a comparison between corporate governance factors before and after the enactment of mixed regulation enacted through formal and informal institutional arrangements. Inferences derived from the estimation of set of two separate equations as a system are econometrically more appropriate than the inferences drawn from the estimation of two separate equations through OLS (Jiambalvo, Rajgopal, & Venkatachalam, 2002). This is because SUR technique can address the cross-correlation and serial correlation innate in panel or cross-sectional or time-series data types (Wooldridge, 2002). In this study, we deployed SUR technique to simultaneously predict the disclosure level of director and executive remuneration before and after the presence of mixed regulation.

Findings and Discussion

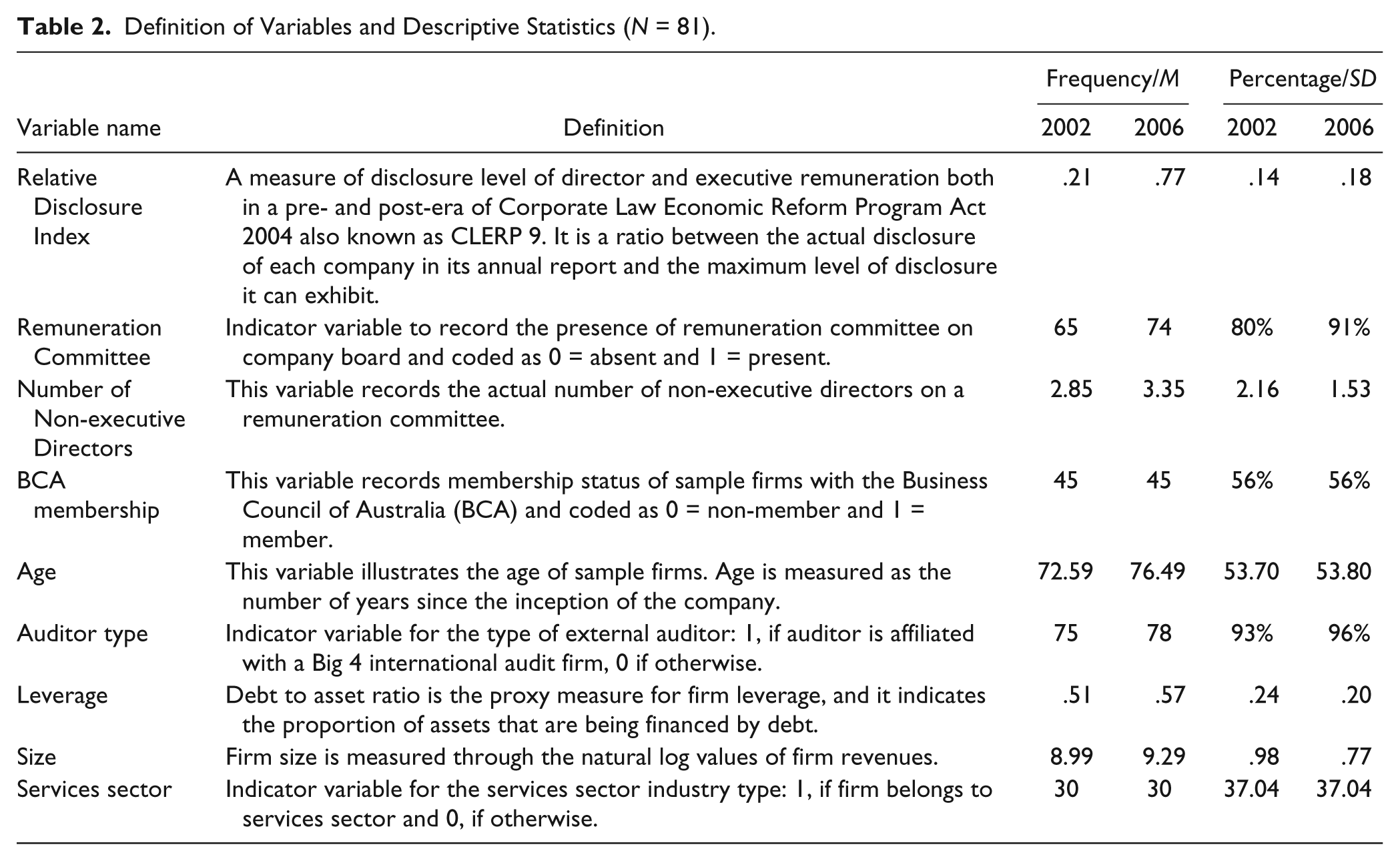

Table 2 presents definitions and descriptive statistics for the relative disclosure index; independent variables and control variables during the pre- and post-periods of mixed regulation.

Definition of Variables and Descriptive Statistics (N = 81).

The use of SUR analysis facilitated to estimate the correlation matrix of residuals and to perform Breusch–Pagan (1980) test of independence (Breusch & Pagan, 1980). In our case, Breusch–Pagan test of independence failed to detect any contemporaneous correlation and residuals were independent as shown in Table A2 of the appendix.

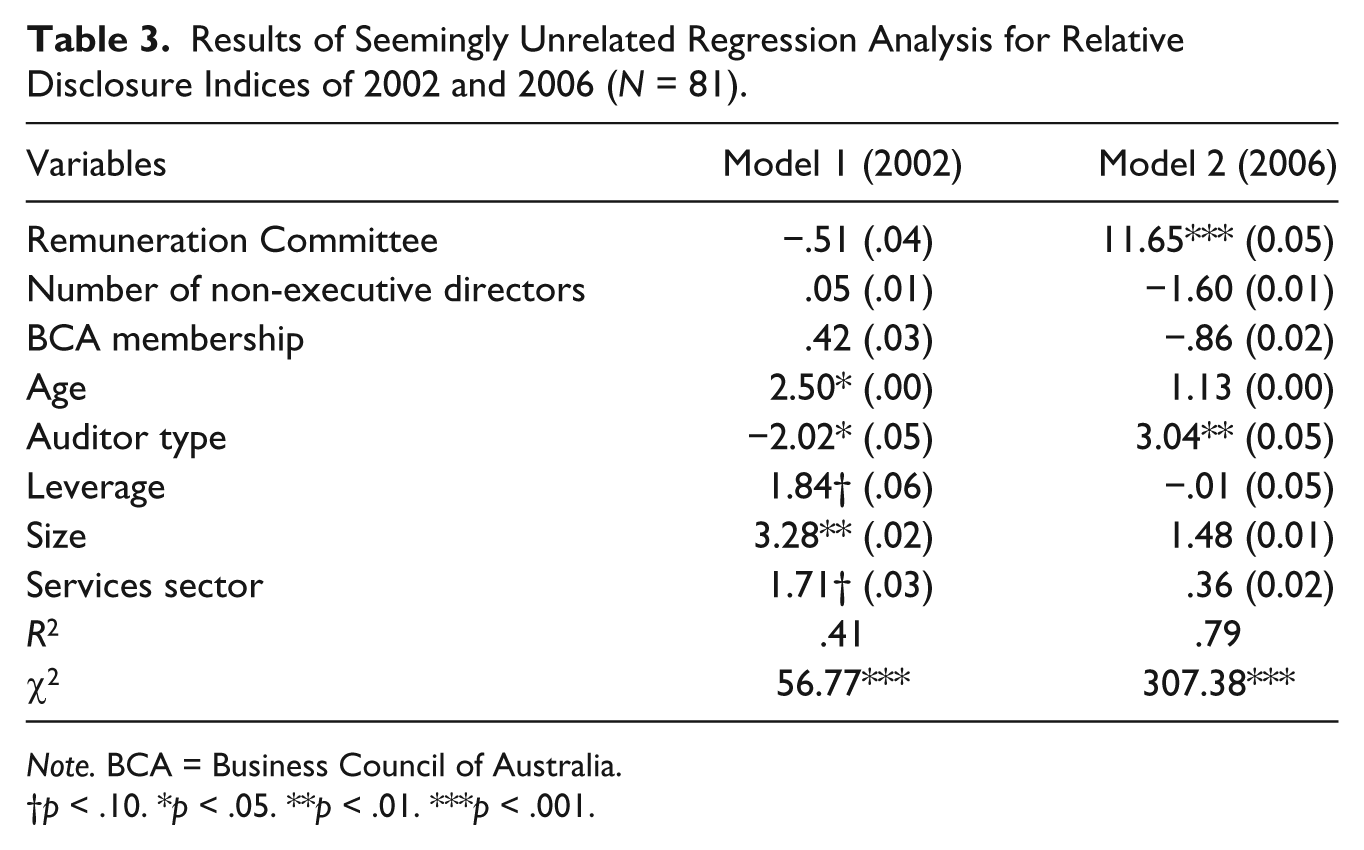

Results of SUR analysis show the extent and nature of change in disclosure level caused due to both informal and formal institutional arrangements of Australia. A substantial increase in the value of the coefficient of determination (R2) from .41 in 2002 to .79 in 2006 suggests that the shift to a mixed regulation led to an overall improvement in the impact of governance practices on disclosure levels as shown in Table 3. The results for year 2002 (Model 1) suggest that prior to mixed regulation, only firm-specific characteristics or control variables such as size, age, leverage and services sector (industry type) made a significant positive contribution to the disclosure information (Model 1: R2 = .41 and χ2 = 56.77 with p < .001). In the absence of a formalized system of self-regulation, when remuneration disclosure is guided by state regulation alone (CLR Act 1998), firms are not obliged to explain or be accountable, if they do not implement best practices recommended for disclosure.

Results of Seemingly Unrelated Regression Analysis for Relative Disclosure Indices of 2002 and 2006 (N = 81).

Note. BCA = Business Council of Australia.

p < .10. *p < .05. **p < .01. ***p < .001.

By contrast, as the results of Model 2 (Year 2006) suggest, the implementation of mixed regulation through formal and informal institutions appears to have catalyzed the adoption of market-based mechanisms recommended for improving disclosure information, making firm-specific characteristics less relevant. Results for Model 2 (R2 = .79 and χ2 = 307.38 with p < .001) show a substantial increase of 38% in the value of R2 signifying that a mixed regulatory framework developed by the formal and informal institutions is more effective than state regulation alone (CLR Act 1998) as it enables better implementation of governance practices by firms to improve disclosure behavior. The results of Model 2 reveal that among the variables of interests, presence of remuneration committee is significant in determining disclosure levels. A significant positive association of remuneration committee with disclosure levels for year 2006 (Remuneration Committee: p < .001, with z = 11.65) stands in sharp contrast to the period (2002) dominated by state regulation. With the implementation of mixed regulation via informal institutions (ASX Corporate Governance Council), ASX-listed firms were obliged to provide an explanation when they did not implement a recommended practice. The provision of such an explanation under ASX 2003 corporate governance recommendations resulted in greater transparency regarding firm situation, and led to improved adoption of best practices devised by informal institutions and confirmed the H1. Therefore, in contrast to 2002, the presence of a formalized system of self-regulation in 2006 facilitated the implementation of remuneration practices by firms recommended by ASX guidelines to improve disclosure levels. Among the control variables, there was a significant positive association of Big 4 auditor firms (Auditor Type: p < .01, with z = 3.04) in determining disclosure level in the post-mixed-regulatory era. Contrary to our predictions, remuneration committee independence (number of non-executive directors on remuneration committee), BCA membership and other remaining control variables did not make any significant contribution to disclosure levels of director and executive remuneration.

This study tested the neo-liberal proposition that the introduction of state-based regulatory initiatives can distort market-based mechanisms of corporate control and governance. The analysis presented illustrates that both forms (state and self) of regulation can exist in agreement, and they do not discord with each other. Furthermore, this study challenges the popular notion of neo-liberal premise that state regulation can dominate or limit market-based regulatory mechanisms; indeed, if anything state regulation appears to catalyze market-based mechanisms for improving disclosure information to provide a synergistic regulatory mechanism of corporate governance in Australia.

Implications

The incidence of widespread market failures, corporate collapses and the recent global crisis calls for greater transparency and a more stringent approach to the regulation of corporate governance. In this article, we have proposed that the collaboration between both modes of regulation in which state regulation catalyzes market-based best practices of corporate governance can minimize agency conflicts and moral hazard. The Australian evidence presented in the study and its empirical analysis allow us to make an important empirical contribution by demonstrating that corporate governance not only needs market-based mechanisms but also requires a visible hand of the state to strengthen the market. We examined in-depth remuneration governance process in Australia and its impact on disclosure practices—an important aspect of the agency problem believed to be a common cause of many collapses. Our study findings demonstrate that self-regulation alone is inadequate to address remuneration governance problems and lend support to the emerging body of literature that highlights the use of state regulation and self-regulation through formal and informal institutions as a more pragmatic approach for regulating the modern corporation in today’s globalized world. State interventions, though, legislation (CLERP Act 2004]) improve the governance of director and executive remuneration by catalyzing the self-regulatory practices such as remuneration committee—demonstrating that well-intended regulatory efforts can indeed balance state regulation with market-based governance.

To address agency problems, corporate governance requires the active engagement of and mutual participation among multiplicity of regulative and normative institutions including public, private, and professional bodies and associations, often with conflicting interests. In the policy-making process, governments need to engage the relevant institutions because their participation can allow the diverging parties to communicate their concerns and understand perspectives of others more effectively. To the neo-liberal advocates of the market, the results demonstrate that consensus-based market-friendly interventions can attenuate corporate governance problems. Thus, the synergistic approach of regulation can assist governments for effective enforcement of regulatory interventions illustrated in our study.

Our study that presents a contemporary approach to corporate governance in Australia has relevance for other developed economies in the new world of globalization. Many developed countries have also established regulatory mechanisms on similar lines. For instance, the United Kingdom requires companies to disclose information about director and executive remuneration in their annual reports along with the shareholders’ advisory vote in the AGM in 2002 (Lütz, Eberle, & Lauter, 2011, p. 321). In Europe, the Netherlands made the vote of director and executive remuneration binding in 2004 (Esch, 2012). The United States has adopted the “say on pay” in 2011 after the global financial crisis (Ball, 2011). Also, it is believed that the disclosure of director and executive remuneration from the United Kingdom, the United States, and Australia are far more detailed and comprehensive than other G-20 countries of the world (Jackson & Bennett, 2009, pp. 9-10).

Our research therefore sheds light on the characters of state regulation and self-regulation as a symbiotic governance mechanism for providing an optimal governance framework for modern corporations in market economies. Also, it is imperative to note that very recent regulatory initiatives taken by the Australian government and the ASX highlight the preference for and relevance of mixed regulatory regime for modern democratic and capitalistic countries. For details, refer to the second edition of ASX Corporate governance principles and recommendations with 2010 amendments and the Corporations Amendment (Improving Accountability on Director and Executive Remuneration) Act 2011.

Conclusion

Although the repository of literature on corporate governance is vast and expansive, most studies are rather sparse in positing the precise conceptual underpinnings of good governance practices, particularly insofar as how remuneration committees can impact disclosure level of director and executive remuneration. In addressing this gap, we make an important contribution to the literature by examining what impact remuneration committees have in bringing about the desired level of disclosure of director and executive remuneration. Second, our article enriches the governance literature by positing a conceptual framework that shows the association between regulatory change and disclosure in a timely empirical setting of the Australian economy, which recently deployed a mix of both state regulation and self-regulation mechanisms to guide corporate governance. Third, our article demonstrates that both formal and informal institutions influence the development of a mixed regulatory regime. It suggests that collaboration between the state and the market, in the context of changing institutional dynamics, has become a very potent force for the management of agency conflicts of a modern economy. Even in the presence of pervasive state regulation, market-based regulation induced through professional associations or alliances are prescient. Their significant presence indicates the synergistic association between these two modes of regulation. The synergistic relationship between both economic and social institutions therefore negates the “either–or” approach toward modern economic management and regulation. Particularly, in the context of the current global economic crisis, the need for symbiotic and unorthodox “rules of game” has become very urgent for countering “animal spirits” (Akerlof & Shiller, 2009). In tackling such new problems including information asymmetries and moral hazards, there is a need for policy makers to develop mechanisms that bring about synergy between state regulation and self-regulation for the governance of modern corporations.

Footnotes

Appendix

Correlation Matrix of Residuals and Breusch–Pagan Test of Independence.

| 1 | 2 | ||

|---|---|---|---|

| 1 | Relative Disclosure Index 2002 | 1 | |

| 2 | Relative Disclosure Index 2006 | .17 | 1 |

| Breusch–Pagan Test of Independence | |||

| χ2 | 2.52 | ||

p < .10. *p < .05. **p < .01. ***p < .001.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.