Abstract

This article examines the relative impact of internal and external factors on the financial decline of local Arab municipalities in Israel. We employ a unique case study to demonstrate that the negative relationship between local management policies and local financial crises is stronger than any other relationship; in addition, this relationship is expected to hold for other local authorities in Israel and for local authorities in Western countries. The new theoretical approach developed in this study indicates that, with respect to local authorities, the “local management approach” more often explains a financial crisis than other approaches.

Keywords

The financial sustainability of governmental and/or non-governmental organizations during financial crises is an important topic of scientific debate. During the economic crises of the late 1970s and 1980s, the U.S. and U.K. governments cut budgets, modified policies, and eliminated publically administered programs. During those times, we witnessed the first studies that addressed the subject of organizational decline (Brewer, 1978), which were followed by studies that focused primarily on the role of public sector organizations in U.S. governmental structures (Bozeman & Straussman, 1982). Although these topics tend to be ignored in the public discourse in times of financial stability or prosperity, they reappear during crises (Bozeman, 2010). In recent years—and particularly since the 2008 global financial crisis—there has been a resurgence of research analyzing financial crisis, financial distress, and organizational decline, particularly in the public sector (Andrews, Boyne, & Walker, 2006; Ben-Basat & Dahan, 2009; Bozeman, 2010; Ghanem & Azaiza, 2008; Haider, 2010; Hendrick, 2004; Jones & Walker, 2007; Karube, Numagami, & Kato, 2009; Meier & O’Toole, 2009; Pandey, 2010).

In this study, we review this literature and attempt to determine whether the conclusions suggested by this body of research can still be applied to actual financial crises experienced by local governments. This research will attempt to contribute more broadly (and, perhaps, on a worldwide basis) to the literature by articulating a new methodology that can better identify the causes of financial crises in local governments and by suggesting solutions to help ensure the financial sustainability of such governmental entities. Such sustainability would also help ensure that local governments fulfill their fundamental purposes and provide services to residents; simultaneously, local governmental reliance on the central government would be reduced, which has become more important in recent years, particularly after the 2008 global financial crisis.

This article is divided into six sections. After this “Introduction,” the section “Literature Review” presents the literature, discusses the theoretical background, and introduces the case study. The “Model” section presents the research model and the research hypotheses. The section titled “Sample and Method” presents the research methods and data. The section “Findings” presents our results. “Discussion and Conclusion,” the final section, discusses our findings and concludes.

Literature Review

We position our study between two major paradigms in the field: the internal and external approaches. The internal paradigm is represented by a “local management approach” (Kimhi, 2008) and focuses on the political and financial management of a municipality, that is, on features related to the distribution of power and management of available resources. The internal causes of financial crises for local authorities (FCLAs) originate with local authorities’ local management policies (LMPs). For example, Park (2004) investigated LMPs by examining the relationship between municipal size and fiscal crisis and found that fiscal crises were avoidable and that appropriate interventions by local authorities could prevent or minimize them.

The second approach, the “socioeconomic decline approach” (Kimhi, 2008), contrasts with the first approach by focusing on the external causes of crisis, such as socioeconomic characteristics (SEs; that is, size, socioeconomic context, and municipal history), and structural circumstances that are beyond the control of local officials, such as national business cycles, declines in local business activities, and national public policies (NPPs; Beckett-Camarata, 2004; Carroll, 2005; Edgerton, Haughwout, & Rosen, 2004; Ghanem & Azaiza, 2008; Haider, 2010; Honadle, 2003; Jones & Walker, 2007; Skidmore & Scorsone, 2011; Watson, Handley, & Hassett, 2005). SEs are generally considered to be primarily responsible for FCLAs. Thus, to improve a local authority’s fiscal situation, leaders should focus on managerial innovation and flexibility rather than on modifying the size or borders of the local administrative region. However, other studies have been unable to duplicate the above findings with respect to differences in SEs to account for differences in SEs (Midwinter, 2002; Mullins & Pagano, 2005).

The primary goal of this study is to answer the following question: Are financial crises caused by local authorities’ LMPs, by NPPs established by the central government, or by the SEs of local authorities? We thus explore the extent to which each of these factors contributes to FCLAs. Our study’s primary contribution is to apply statistical methods to answer this multilayered question. As such, we aim to fill an existing gap in the theoretical framework that emanates from the lack of consensus between the two major paradigms in the field, the internal paradigm (represented by the local management approach) and the external paradigm (represented by the socioeconomic decline approach), as discussed above. We hope to determine whether one of these approaches is more accurate in determining the causes of current FCLAs. Yet, it is important to note that, in this study, we refer mainly to national governmental grants as the NPP factors, without the ability to refer to other important factors (as will be explained in the “Sample and Method” section).

However, first, what is a financial crisis? Financial crises have been widely discussed from the perspective of a number of disciplines. It is important for management scholars to define the characteristics of a financial crisis (and to distinguish it from a financial whirlpool), to identify the causes leading to organizational decline, and to identify methods for reversing such decline. The typical reaction to a period of organizational distress or decline consists of cutbacks (Jones & Walker, 2007; Trussel & Patrick, 2009); however, are cutbacks the only solution to financial crises?

Certain studies have linked the term crisis, as it is used in the context of local governments, to the concept of “organizational effectiveness” (Andrews et al., 2006) or have characterized a crisis as a positive or negative turning point in an organization’s life and as a series of events that threaten an organization’s fundamental objectives. Studies have defined organizational failure as the failure to achieve organizational goals, to protect the organization’s interests, and/or to meet the organization’s obligations or expectations (Zeedan, 2013). It is commonplace that the causes of decline are classified as either internal or external to an organization. Some researchers have defined FCLAs as situations in which local authorities must balance revenues with expenditures by raising taxes to maintain service levels, by decreasing expenses in subsequent years, or by combining the two options. Researchers such as Mullins and Pagano (2005), who used this same approach to examine crises in local governments throughout the world, found that an essential feature of municipal financial crises was the local authority’s dependence on the central government, which was typically manifest in government grants. Midwinter (2002) examined financial crises experienced by local authorities in Scotland and found that the central government prevented local authority deficits by using grants to control local government spending. Hendrick (2004) defined financial stability as a local authority’s ability to meet its financial commitments and to provide services to its citizens. Her study of local authorities on the outskirts of Chicago examined three dimensions of economic efficiency: the “basic features,” which include the powers and primary goals of a local government, including those related to the environment, fiscal policy, and SEs; fiscal management, as measured by budget overruns, municipal loans, government grants, and other monetary features; and a dimension that combines basic features with fiscal and managerial malpractice.

The different approaches that have been used to investigate local government crises reveal that researchers must distinguish among financial crises, management crises, and crises related to the quality of services. In addition, the central government and the populace may have different perceptions of what constitutes a crisis. In the public sector, organizational decline is often defined as distress or the “inability to provide services at pre-existing levels” (Jones & Walker, 2007).

This study adopts the definitions proposed by Hendrick (2004) and examines FCLAs both from the perspective of the central government (crises in managing the budget) and from the perspective of the citizenry (the local authority’s financial sustainability and ability to provide services). To determine the extent to which local governments experience a budget crisis, we examine the organization’s ability to balance its budget by managing budget deficits and loan payments. Notably, higher taxes are not considered to be an indicator of financial crisis because the extent to which a local authority in Israel can tax citizens has been officially limited since 1986 by the Ministry of the Interior. The ability of the local authority to provide services is also included in the definition of a crisis as either a threat to the basic goals of the organization or as the organization’s failure to achieve its goals and interests. We also believe that a crisis involves an organization’s inability to meet its obligations. This restricted approach to defining a crisis at the level of local government leads us to focus on local authorities’ ability to minimize deficits, eliminate deficits, or produce a budget surplus. Although this approach differs from the British perspective on local authority crises, it is appropriate in the Israeli context. The Israeli system of central and local governments originated in the former British Mandatory government of Palestine, as was the case in other British colonies. It is important to note that this study does not address certain important issues, including an organization’s strategic management or leadership failures, political failures, ethical failures, cultural crises, and/or institutional crises, although these failures can certainly cause a local authority to fail to fulfill its aims and experience crisis. Although these issues might seriously affect local financial management and might result from local policies, evaluating their direct impact on the financial crises experienced by local authorities is beyond the scope of this study.

We have chosen to focus our research on a unique test case of local Arab authorities in Israel, where the local government is an administrative arm of the central government and where these two institutions are interrelated in complicated ways. (In some countries, of course, there are three governmental levels: federal, state, and local.) The relationships among different government levels can be particularly complicated when local governments represent national minority groups, as is the case with many local governments in the Arab regions of Israel. Furthermore, the conflict between the external pressures exerted by the central government to change local policies and the internal capacity of the local municipality to manage and govern has continued to escalate, particularly in culturally and ethnically divided societies.

Recently, the issue of financial local crisis within Israeli local authorities has been widely discussed (Beeri, 2013a, 2013b; Ben-Basat & Dahan, 2009; Carmeli, 2008; Ghanem & Azaiza, 2008; Haider, 2010; Halabi, 2014; Zeedan, 2013). Several studies conducted in Israel have suggested that the local Arab governments are less financially sustainable than other local governments in the nation. For example, Ben-Basat and Dahan (2009) found that 33 of 76 local Arab authorities delayed the payment of salaries to their employees in 2004, whereas only 20 of 178 local Jewish authorities experienced such delays. In 2006, 122 of 254 local authorities participated in financial recovery programs; of these, 61 were local Arab authorities, which represent more than 75% of the local Arab governments in Israel. Beeri (2013a), who has studied 9 local authorities in Israel (6 of them were Arab local authorities) in which the elected leadership has been replaced by a convened committee, and found that the performance of local authorities headed by a convened committee was significantly improved. As such, these governmental units have been chosen as a suitable test case for our study.

Furthermore, our case study is important due to the significant debate in Israel regarding these Arab local authorities. It is generally accepted that these local governments have experienced long-term discrimination with respect to their budgets (Razin, 1999), and a widely held theory posits that such local governments are persistently at risk of financial failure as a result of the discrimination against them, that is, because of the central government’s external policies. Therefore, we were led to focus on governmental grants, in particular, as an external factor. In contrast, Carmeli (2008) found the explanation for a budgetary deficit in Israeli local authority in its SEs (location, size, and socioeconomic status). New research (Halabi, 2014) has confirmed the financial vulnerability of these local Arab authorities and has identified two factors that contribute to this weakness: discrimination by the Israeli central government with respect to resource allocation, on one hand, and low tax revenues, on the other. The case study embodied in the current research thus returns to the question of whether the sources of financial crises are “internal” or “external,” with no determination.

Our assumption is that internal factors have a greater effect on FCLAs than external factors. Thus, we chose this case study of local Arab authorities in Israel to demonstrate whether financial crises are the result of LMPs; if so, solutions are required at the political and financial management levels of municipalities rather than at any other level (such as at the level of NPPs or at the level of demographic factors). In this case, our results may also apply to local authorities in both Israel and Western countries. By establishing a closer connection between the case of Israel and the academic debate about local governments’ financial crises, this analysis contributes to the scientific debate about the causes of these fiscal crises.

Model

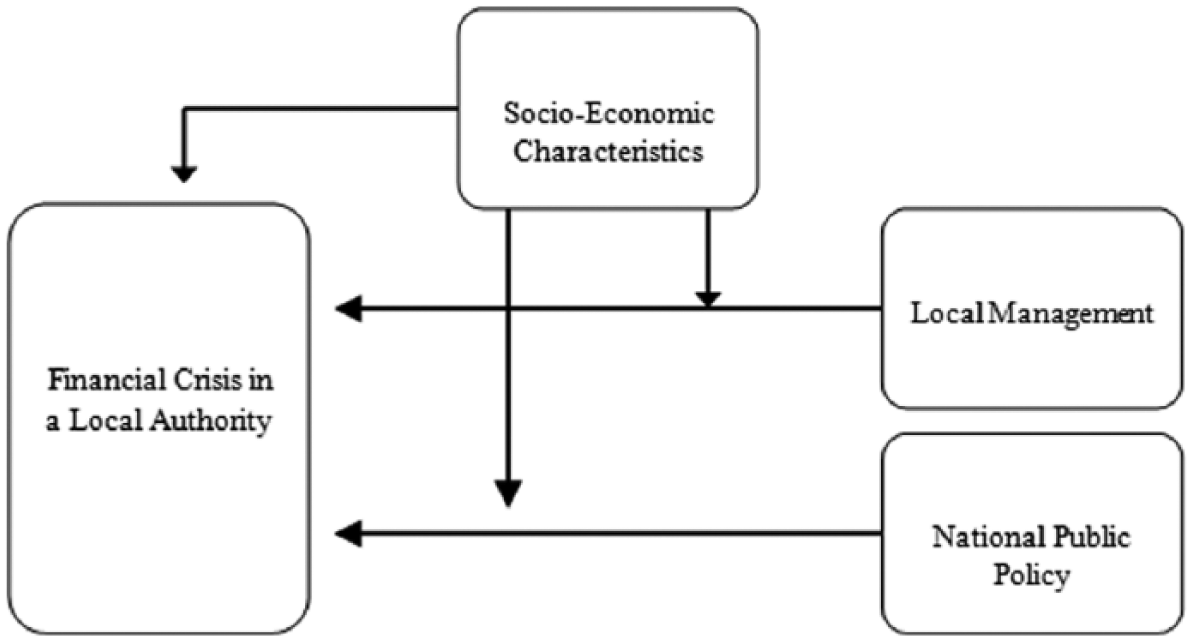

To achieve these objectives, we must define our research model, which will include financial crises and their possible causes. The proposed research model incorporates crises and focuses on FCLAs. Thus, the focus of this study is the ability of local authorities to fulfill financial commitments and provide services. Whether a government has these capacities is determined by a single criterion: the occurrence of a financial crisis in which the local authority is unable to balance its budget. In constructing the research model, we included all possible causes of FCLAs—which can be categorized by whether they have internal or external causes. External causes are produced by NPPs and reflect the relationship between the central government and the particular local government, typically through grants provided by the former to the latter. Internal causes are introduced by LMPs and SEs. The research model also includes SEs as an intervening variable for LMPs and NPPs. The model is presented in Figure 1.

The research model.

Consistent with the research model and the theory presented above, we propose two major hypotheses:

Sample and Method

To test our hypotheses depicted above, we examined all 76 local Arab governments that existed in Israel between 1970 and 2011 (according to the available data), excluding the West Bank and Gaza. Furthermore, we excluded the local Arab authorities in the Golan Heights (the four Druze local authorities of Majdal Shams, Buq’ata, EinQiniyye, and Mas’ade) and the Alawi local authority of Ghajar, which holds no elections and has a mayor and councilors who are appointed by the Minister of the Interior, which means that they cannot be evaluated by the same terms with respect to internal factors. In addition, we included Kfar Kama, the Circassians’ local authority in the Galili. (Rehaniya, the other Circassian village in Israel, is not independent and is part of the Merom HaGalil regional council.) Although it does not regard itself as Arab, the Circassians’ local authority of Kfar Kama was included because of its affiliation with the Druze and Circassian local municipalities’ forum in Israel.

The data that we used to test the research hypotheses were collected from databases, relevant studies, and publications of the Ministry of the Interior (Israel Ministry of the Interior, 1995 to 2008) and the Central Bureau of Statistics in Israel (Central Bureau of Statistics, 1966 to 2013). The data were analyzed using a multiple regression analysis to identify relationships among the explanatory variables and the outcome variables. In political science research, cross-sectional data are typically analyzed using Pearson correlations to compare the features of two variables. Because our study analyzes longitudinal data, the research method must examine several variables simultaneously. We therefore used the generalized estimating equation (GEE) methodology (adjusted for use in political science research by Zorn, 2001). The research variables are presented in Table 1.

Research Variables.

Note. FCLA = financial crises for local authorities; SE = socioeconomic characteristics; LMP = local management policies; NPP = national public policies.

The value of each local authority is given as a percentage of the average for the same factor for all local municipalities in Israel in the same time period.

General governmental grants in Israel were distributed in the past based on criteria such as municipal geographic size, number of residents, economic strength of the local authority, residents’ socioeconomic status, etc.

Table 1 shows that the value of each local authority in a given year is a percentage of the average value for the same factor for all local municipalities in Israel during the same year. For example, the figure for general grants per resident in a given year was calculated as a percentage of the average for the same factor for all local municipalities in Israel in the same year, which enabled us to compare our results with the grant amounts to Jewish municipalities in Israel.

It is of utmost importance to mention that we implement NPP factors in our research that typically represent mainly national governmental grants mainly because of the inability to provide full data for other factors, including national and regional planning and zoning, the encouragement of industrial and commercial zones, and the modification of municipal territories and borders. Such a wide perspective on NPPs is expected to help us make conclusions regarding the hypotheses and thus should be adopted in further studies.

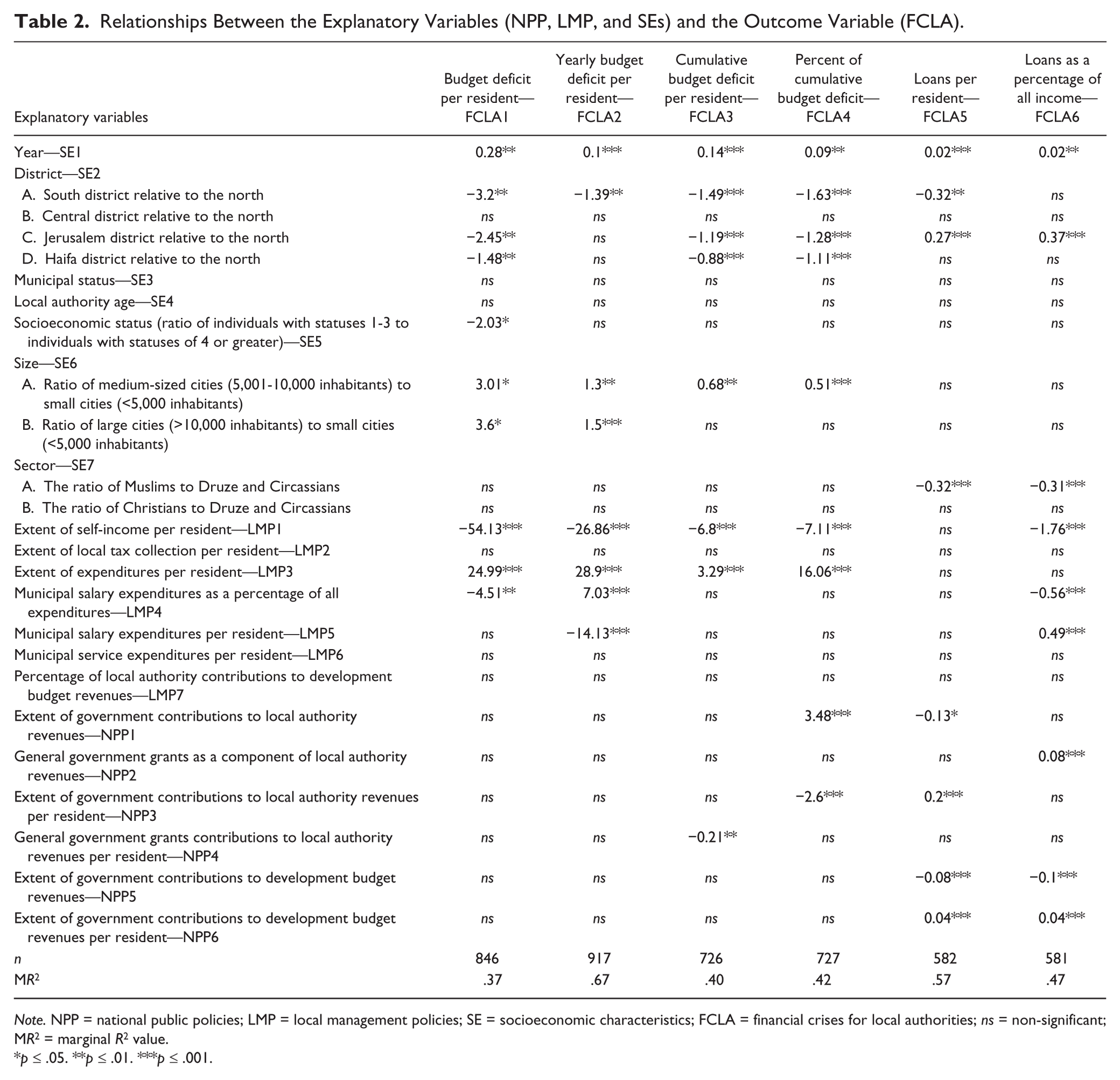

Using the GEE methodology, we assessed the significance of the explanatory variables, and only those that were significant were included in our model. The percentage of explained variance was examined using the marginal R2 value (MR2 ≥ 0), with higher MR2 values indicating better model estimators. We then identified the models with distinct variables and used the withdrawal method to eliminate insignificant variables. This procedure was used to identify the optimal model with the maximum MR2 value, in which each variable produced a significant effect. The final optimal models and final results are presented in Table 2. To determine whether to accept or reject a hypothesis, we compared the β values for each variable with the other variables through correlation with the same FCLA variable. Only the highest β values led to acceptance of a hypothesis.

Relationships Between the Explanatory Variables (NPP, LMP, and SEs) and the Outcome Variable (FCLA).

Note. NPP = national public policies; LMP = local management policies; SE = socioeconomic characteristics; FCLA = financial crises for local authorities; ns = non-significant; MR2 = marginal R2 value.

p ≤ .05. **p ≤ .01. ***p ≤ .001.

Findings

This research method allowed us to determine whether to accept or reject the research hypotheses. Table 2 presents the statistical findings and β values for the relationships among the explanatory variables (NPPs, LMPs, and SEs) and the outcome variable (FCLA).

The research findings confirmed H1 for LMPs. There was a negative relationship between LMPs and FCLAs regarding the regular budget (non-exceptional), which can be summarized as follows: higher self-income per capita (LMP1) is associated with lower annual budgets and per capita budget deficits (FCLA1 and FCLA2). This finding is consistent with the results of previous studies.

We examined subsidiary hypotheses to assess whether there was a negative relationship between NPPs and FCLAs. Although we hypothesized that there would be a negative relationship, we also hypothesized that this relationship would be weaker than the relationship between FCLAs, on one hand, and SEs or LMPs, on the other hand. Overall, there was a negative correlation between the explanatory variables, including the extent of government contributions to local authority revenues (NPP1) and the extent of government contributions to per capita revenues (NPP3), but the effect of SEs eliminated all significant relationships (apart from a weak relationship between NPPs and the development budget).

Because NPPs are not likely to predict FCLAs in local Arab governments, our results do not confirm H1 for NPPs. This conclusion contrasts with the extant literature, which has found that a functioning financial relationship between central and local governments is essential to economic stability. Many studies conducted in Israel, including those of Razin (1998, 1999), Ghanem and Azaiza (2008), Haider (2010), and Halabi (2014), have also found that NPPs are the primary financial problem faced by local Arab authorities.

We also hypothesized that there would be a significant relationship between SEs and FCLAs, which would support the view that FCLAs are explained by SEs. We found that the differences between the SEs of various local Arab communities only partially explain FCLAs. There are differences among districts (SE2); for instance, a local Arab authority in a southern district is likely to experience less severe FCLAs than an authority in another district. However, the sample of local authorities in this region is restricted. Analysis of the differences between the various sectors (SE7) reveals that for local Arab communities in which the majority of citizens are Muslim, the per capita loan debt is typically lower and the ratio of loans to overall income is typically lower than in local Arab authorities in the Christian, Druze, or Circassian sectors. Furthermore, the socioeconomic level (SE5) was a significant explanatory variable for FCLAs, which suggests that local Arab governments in regions with lower socioeconomic status experience more severe FCLAs than local Arab authorities in regions that enjoy higher socioeconomic status. With respect to the other SEs—municipal status (SE3), local authority size (SE6), and local authority age (SE4)—no significant correlations were found that might explain the differences between the financial crises of various local Arab authorities. Thus, the research hypothesis regarding SEs was only partially supported.

These findings conflict with the results of previous studies, which have claimed that socioeconomic issues explain fiscal crises (e.g., Park, 2004). However, our findings are consistent with Zeedan’s (2013) finding that size does not affect the efficiency of local authorities.

We hypothesized that LMPs and SEs would affect FCLAs to a greater extent than NPPs, and we found that LMPs exert the greatest influence on the FCLAs of local Arab governments in Israel. The financial crises of local Arab authorities are less severe and the regular budget deficits are lower when per capita income is higher and per capita municipal expenditures are lower. Although SEs such as district, socioeconomic context, and sector characteristics predicted the FCLAs of local Arab authorities in Israel, these characteristics were less predictive with respect to FCLAs than LMPs. Furthermore, we cannot conclude that there is a definite link between NPPs and FCLAs from this current study, particularly with respect to regular budget data. Only FCLAs related to development budgets—in particular, FCLAs involving loans per resident—are predicted by NPPs. Although this relationship is not statistically significant, the findings indicate that per capita loan debt and the ratio of loans to overall income decrease as the government contribution to development budget revenues increases.

We conclude that organizational resources exert the greatest influence on the financial performance of local authorities compared with SEs or external factors (such as government budgets). However, with respect to H1, these findings are not consistent with the conclusions of many previous studies, particularly those based on local Israeli data.

Discussion and Conclusion

Crises experienced by local authorities can be categorized as financial crises, management crises, or crises related to service quality. When focusing on the financial aspects of a crisis, researchers must examine the local authority’s success in reducing deficits, in reducing municipal loans, or in achieving a budget surplus.

We identified two major paradigms in the field. The “local management approach” focuses on the municipality’s political and financial management, that is, on features related to the distribution of power and management of available resources. The alternative, the “socioeconomic decline approach,” focuses on the possible external causes of local financial stress, such as demographic characteristics (size, socioeconomic context, and municipal history); structural circumstances that are beyond the control of local officials (general financial cycles and local business decline); and governmental policies, decisions, and resource allocation.

We analyzed these two approaches in attempting to fill an existing gap in the theoretical framework that has been caused by the lack of consensus between the two major paradigms in the field discussed above. We identified three main factors that contribute to FCLAs: LMPs, NPPs (in this research—as explained above—national governmental grants), and SEs. Our examinations of our study hypotheses revealed a negative relationship between LMPs and FCLAs. This relationship was significantly stronger than the relationships between financial crises and factors such as NPPs and SEs. This finding confirms the primary hypothesis of this research and is supported by the data. Two variables are the primary contributors to this relationship. First, higher self-income per capita is associated with lower per capita budget deficits. Second, lower per capita expenditures are also associated with lower per capita budget deficits. We were unable to confirm similar relationships for NPPs (regarding national governmental grants). Although there are significant relationships among certain socioeconomic variables and FCLAs, these relationships were found only at the district, sector, and socioeconomic levels.

An analysis of the data obtained from all local Arab governments for the years examined revealed the critical factors that affect financial performance. In addition to the high percentage of the variance in financial crises explained by LMPs, the specificity of the relationships that were identified supports the conclusion that these results are not spurious.

As other studies have previously shown, our data also revealed the existence of discrimination in allocating resources to the local Arab authorities. However, because discrimination has decreased over the past 15 years, local authorities should have been expected to be less likely to develop financial crises. However, we found the opposite to be the case; although the financial allocation increased for some authorities, the extra income was used to fund increases in both municipal salaries and expenditures that exceeded such budget increases. In fact, the most important contribution of this manuscript is that we found a very low correlation between increasing intergovernmental grants and decreasing financial crises in the long run that is actually lower than the correlations with other NPP factors (regarding national governmental grants).

Following these conclusions, we are able to suggest that the negative relationship between LMPs and local financial crises is stronger than any other relationship. The new theoretical approach adopted in this research indicates that a “local management approach” that considers municipalities’ political and financial management as the source of financial crises is more likely to apply to local authorities than the “socioeconomic decline approach,” which focuses on external causes. We were able to fill this existing gap in the theoretical framework by determining the most influential factors on financial crisis in local governments—the internal factors rather than the external factors. This conclusion might be generalizable to other local authorities in Israel and in Western countries, after heeding the necessary cautions of generalizing from a unique case study.

Based on our main findings, we propose that local authorities seeking to ensure lasting financial success should improve LMPs and increase their reliance on independent funding sources to stabilize their financial positions, in addition to establishing mechanisms to support autonomy and self-reliance. The transition to better local management and independent sources of funding might be accomplished by increasing revenues from property taxes (and particularly property taxes on businesses), reducing per capita spending (and particularly reducing municipal salary expenditures), improving the economic status of the population (e.g., lowering welfare spending budgets and increasing the ability of the populace to pay taxes), and developing infrastructure to stimulate local businesses.

For the central government, we propose a transition to a NPP (regarding national governmental grants) that strengthens the autonomy of local authorities by increasing government grants—for a limited time—to promote revenue growth, allocating development budgets to infrastructure projects that increase locally generated revenue (in particular, infrastructure-related income from industry and commerce), increasing governmental supervision to prevent and eliminate ongoing annual deficits in local budgets, and rewarding local authorities who achieve budget surpluses.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.