Abstract

Despite some progress in the past three decades, China’s rural economy still suffers from a lack of sound financial intermediation in terms of the coverage, quantity, and quality of financial services. This article offers a study of the political economy of rural finance in China, a historical and political analysis of the reform process on a systemic level, as well as an assessment of China’s reform strategies and programs. We argue that the path of China’s rural finance reforms has been a transition from state predation that centered on the state’s extraction of rural financial resources to finance its industrialization program, to market extraction that saw the market system continue to drain rural funds into the urban economy. Given the failure of the existing strategies, we suggest that policy makers look beyond the market-centered framework and establish a system of vertical cooperation that can systematically integrate policy, cooperative, and commercial elements of both formal and informal institutions.

Keywords

A decade ago, a New York Times article described the performance of the stock market in China as a new “China syndrome”: “How could China’s stock market be weak when its economy is so buoyant?” (Preston, 2005). China’s rural finance and, more broadly, its rural economy represent yet another example of this stark contrast. Rural finance is widely regarded as the weakest link in China’s financial system. Because of this weakness, even though China’s overall economy has been robust, the majority of the rural population has missed out on the blistering, double-digit economic growth. Despite some progress in the last three decades, the rural economy still suffers from a lack of sound financial intermediation in terms of the coverage, quantity, and quality of financial services. For instance, rural areas have been suffering chronically from a lack of coverage of financial institutions and services. Although the authorities managed to have all townships and villages covered by rudimentary financial services by June 2013, there are still more than 1,500 townships without any form of financial institutions. 1 By the end of 2012, lending to rural households constituted only 5.4% of total lending even though the rural population makes up 64.7% of China’s total population (PBC, 2013). Serious shortages in credit and other types of financial services in rural areas have become a bottleneck for agricultural development, constraining increases in peasants’ incomes and hence enlarging the income disparity between the rural and urban populations.

Early works on China’s rural finance focused on identifying the institutional deficiencies of rural financial institutions (e.g., Tam, 1988). More recent studies have focused on the emergence of microfinance and associated problems (Tsai, 2004), and informal lenders in rural areas (Zhou and Takeuchi, 2010). Chinese scholars have tended to analyze the pathology of credit shortage in rural China and to produce policy suggestions mainly from an economics perspective (see, e.g., He, 1999; Xie, 2001; Gao, 2002; Ma and Lan, 2003; Lu, 2003; Zhang, 2003, 2004).

We believe that the key to understanding the dynamics of rural finance lies in the macro-level study of the central role of the Chinese state, whose imperatives, strategies, and policies have had a direct and profound influence on the rural economy and finance. After all, as an inseparable part of economic reform, rural financial reforms have mostly been a state-led, top-down process. At the same time, the path of rural financial reforms has also been shaped by past experiences that constrain the options and possibilities for policymakers. Hence, we examine the political economy of rural finance in China, provide a historical and political analysis of the reform process on a systemic level, and assess the reform strategies and programs so far.

Rural finance is treated in this article as financial services that encompass all the savings, lending, financing and risk-minimizing opportunities (formal and informal) and related norms and institutions in rural areas (Pearce et al., 2004; Schmidt and Kropp, 1987). We argue that the logic of China’s rural finance reforms has been shaped by the evolving relationship between the state, the emerging market, and the rural sector. In particular, the path of the reforms since 1979 can be seen as a transition from predatory arrangements that had stemmed from the legacy of the Soviet redistributional approach to industrialization, to market extraction that has continued to divert financial resources away from rural areas. In the previous command economy, rural finance served as a state vehicle to mobilize rural savings in financing industrial development in a context of capital shortage. In the early years of the reform era, that is, until the mid-1990s, financial repression of the rural economy remained a high priority of central and local governments in controlling financial resources under a system that continued to steer most formal credit to the urban area and the state sector. As domestic liquidity turned from shortage to excess from the mid-1990s, the state undertook more serious reforms in an attempt to reinvigorate financial services for rural areas. However, we find that the state’s developmental agenda has been hampered by the weaknesses in its institutional structure as well as its market-oriented approach. Given the increasing gap in investment returns and general income levels between urban and rural areas, the market system continues to drain rural funds into the more profitable urban economy, leaving the rural sector in a downward-spiraling trap.

The article proceeds first with a theoretical discussion of our explanatory model that centers on the role of the state and market in rural finance. Using this model, we then explore the historical and political process of rural finance in reform China, which, as we argue, represents a transition from state predation to market extraction. Finally, since the current market reforms are unsustainable despite the determination and commitment of the central leadership, we argue that the way out for Chinese rural finance is to establish a more diversified regime with clear-cut functions that systematically integrates policy finance, cooperative finance, and commercial finance.

The State, the Peasantry, and Finance

In China’s long history as a traditional agrarian society, rural finance has been invariably shaped by an evolving relationship between the state and the peasantry. Here, Mann’s (1993) distinction between despotic and infrastructural power of the state serves as a starting point. Despotic power refers to “the distributive power of state elites over civil society,” a predatory form of interaction largely through coercion. Infrastructural power, on the other hand, is “the institutional capacity of a central state, despotic or not, to penetrate its territories and logistically implement decisions” (1993: 54–75), which is a largely productive power that entails the engagement of society in collaborative activities that further a social end. The state is likely to exercise both forms of power simultaneously; the relative weight given to each will determine the nature of the state’s interaction with society.

The combination of these dirigiste and embedded aspects of the state in imperial China is perhaps best illustrated by Wittfogel’s (1957) theory of “Oriental despotism,” which contended that the imperial state built a “hydraulic empire” through forced labor and a large and complex bureaucracy. This is supported by Fei’s (1953) sociological approach that sees the relatively stable political and social structure between the imperial state and the peasantry underpinned by the existence of a gentry class, the landed scholars who upheld the sophisticated Confucian morality and, more importantly, maintained the traditional social organization of the village. Positioned between ruler and peasantry, the gentry class had been instrumental in both mediating and cushioning despotic power, extending the infrastructural power of the state, and effecting a balance between the leaders and the led. For example, Xiaobo Lu’s (1997) study of the history of peasant levies suggests that, in imperial China, national average peasant payments in many periods of history were lower than those in the early 1990s. In terms of rural finance, imperial governments had played a largely supportive role (Zhang, 2005).

State Predation

The loss of such a delicate balance after the Communist revolution in 1949 led to state predation and later market extraction, two concepts that we argue are central to understanding the dynamics of rural finance in China since 1979. State predation refers to the distributive consequences of the state’s despotic power in rural finance and development. It differs from the “predatory state” stereotypes that have featured largely in neoclassical and neoutilitarian accounts that see the predatory state as a “klepto-patrimonial” regime whose rulers attempt to “extract an income from the rest of the constituents” (North, 1981: 22; see also Lal, 1988; and Levi, 1988: chap. 2). As will be detailed later, the industrialization strategy of the Communist state was more distributive than rent-seeking. According to Johnson (1982), White and Wade (1988), and Evans (1989: 563), even if a state is not immune to rent seeking or “to using some of the social surplus for the ends of incumbents,” as long as the consequences of state actions promote rather than impede long-term transformation, such a state is considered “developmental” rather than “predatory,” or what Sklar (1986) calls a “developmental dictatorship.” The problem with this conceptualization, however, is that by examining the function of the state as a whole, it tends to obscure the essential variation of the state’s role in specific sectors, such as the impact of the Communist state on rural development. In order to avoid that problem, we do not define the state’s predatory role in rural development as a form of neoclassical rent-seeking plunder. Instead, we view state predation from the perspective of the welfare of the rural economy, which had essentially been subject to the state’s grabbing hand (Shleifer and Vishny, 1998) in that the state had appropriated the rural and agricultural surplus to fulfill its political and economic imperatives through systemic coercion.

State predation was possible due to changes in political and social structures as well as state development strategies that promoted industrialization and urbanization at the expense of agricultural production and the rural population. The three-tiered structure in the imperial era, involving the state, gentry, and peasantry, morphed into a two-tiered, state-peasantry structure in the aftermath of the Communist revolution in China, in which the gentry class was virtually wiped out during land reform. Without a rule-of-law legal infrastructure, farmers were directly exposed to the despotic power of the state (Zhang, 2005).

At the same time, Beijing adopted a Soviet-style industrialization model, systemically prioritizing the development of capital-intensive heavy industries. Given China’s international isolation, the government resorted to exploiting the poorly capitalized rural economy in order to mobilize a massive amount of socioeconomic resources for its industrialization strategy favoring urban residents, the key constituency of the regime. This was done through a series of what Lin et al. (1994) call “urban-biased” and highly distortive political and economic arrangements (see also Grossman, 1983; and Figure 1). In particular, the state was able to extract resources from the rural economy in two ways. First, a centrally planned economic regime meant that the state could appropriate the agricultural surplus to subsidize urban industries by administratively cutting the prices of agricultural products while inflating those of industrial goods and/or raw materials for agriculture—a classic case of “price scissors” (Knight, 1995). In other words, in effect the state imposed an “industrialization tax.” It has been estimated that between 1952 and 1957 alone, 47.5 billion yuan was transferred under the price scissors mechanism from the rural to the urban sector, accounting for 30.9% of fiscal revenue during this period. And between 1959 and 1978, the figure was 407.5 billion yuan and 21.3% (Yan, Gong, et al., 1990: 13–14). At the same time, financial institutions, also under state monopoly, further sucked in the financial surplus from rural areas in the form of deposits, diverting the capital to urban state industries. 2

The rural-urban divide and the formation of the planning regime.

Therefore, rural finance in the pre-reform era had been a vehicle of the state for extracting and channeling rural funds into industrial investments. It is true that by doing so China had managed to establish a modern (albeit rudimentary) industrial infrastructure from scratch within a short time. Nevertheless, the state’s predation of the rural economy, including financial extraction through a tightly woven and omnipresent system of rural financial institutions, severely distorted the prices of all the major factors of production, such as labor, goods, and capital, and resulted in an imbalance in the industrial structure, low efficiency, and the dilapidation of the rural economy.

Market Extraction

As China’s economic reform accelerated in the 1990s, studies of rural China began to incorporate the emerging market into the well-established state-society paradigm. Zhou Feizhou (2006) sees a transition of the previous extractive state to one that “hovers” above the social structure in the countryside, retreating from social and economic governance with the latter functions partly taken up by an emerging class of non-state elites (Tong and He, 2002). At the same time, Beijing sanctioned the commercialization of state banks in the aftermath of the Asian financial crisis out of fear of financial insecurity. Accordingly, in rural areas, Beijing adopted a more market-centered neoliberal approach to rural finance in the hope of bringing efficiency to financial intermediation. But, in fact, this approach led to a new form of exploitation: market extraction.

Market extraction, in this case, refers to the consequences of market failure in rural finance. While markets often allocate goods and services in an efficient way, they can also be associated with a number of inefficiencies, such as information asymmetries (Stiglitz, 1998), non-competitive markets, principal–agent problems, externalities (DeMartino, 2000), or public goods (Stiglitz, 1989). In this case, market failure and the resultant extraction is in the form of negative externalities for rural development, which imposes political and social costs on the Chinese economy and polity. Also, market failure occurs when public goods are needed in rural areas, but the demand cannot be satisfied by market supply.

Externalities—spill-over effects arising from the production and/or consumption of goods and services for which no appropriate compensation is paid (Buchanan and Stubblebine, 1962)—are common in virtually every area of economic activity. They can cause market failure if the price mechanism does not take into account the full social costs and social benefits of production and consumption. Negative externalities imply higher marginal social cost than private cost, but profit-maximizing producers/service providers tend to consider only private cost/benefit at the expense of wider social cost. In this case, negative externalities should be understood in terms of the private costs of rural finance for market institutions and the resultant social costs generated from the latter’s inclination to avoid or reduce private cost.

First, the private costs of providing rural financial services are high. It is a risky (and therefore a costly) business, particularly for market institutions. Compared with urban industries, agriculture has a more direct relationship with nature, with its geographical, seasonal, and demographic uncertainties. These have a direct impact on rural finance since they increase the costs to financial institutions by increasing the likelihood that loans will not be repaid. In addition, in China, the gap between the returns to agriculture and those to industry and the service sector is even larger due to the sharp contrast between the state’s predatory extractions of agriculture under the previous planned economy. The enormous opportunities of the tradable sector, especially domestic industries, has widened this gap, thanks to China’s economic opening in the reform era. Therefore, profit-driven and self-interested commercial institutions tend to simply follow the logic of the market by avoiding or reducing their private costs through disintermediation, that is, disengaging from rural lending and diverting rural financial resources to the urban and industrial sectors instead of serving the demand of the rural population and industries.

However, in doing so, the market tends to generate social costs aside from private costs. This is clear when one considers the relevance and importance of agriculture and rural society in China’s overall economic and political fabric and the adverse impact of a lack of financial intermediation and resources in rural areas under an emerging market. Although agriculture’s share in total output has been diminishing in recent years, dropping for the first time to below 10% in 2014, agriculture, farmers, and rural areas (三农) are still of vital importance to China’s economic prosperity and social stability. First, a healthy development of domestic agriculture ensures basic food security for the world’s largest (and still growing) population. It should also provide a solid foundation for China’s systemic transition to a more consumption-driven economy given the huge potential of rural consumption and the rural market. In addition, even given the large-scale migration of rural workers to urban areas, almost 30% of China’s total population still engage in full-time agriculture. The latter provides not only employment opportunities for the rural population but also a fallback for the migrants who find it difficult to blend in with urban life. Therefore, a viable rural area serves as a pressure relief valve, which is particularly important for China’s political and social stability.

The rural financial system provides the blood for rural and agricultural development. Although an urban bias in the allocation of financial resources is efficient in terms of investment returns, the continued net loss of capital out of the rural sector tends to generate social costs by severely constraining rural developmental opportunities, enlarging the rural-urban income gap, and exacerbating rural-urban inequalities.

China’s market-oriented reform and the notion of market extraction, however, do not mean a retreat of the state. Rather, they represent a continuation of the state’s critical role in configuring the rural financial landscape within a broader state-capitalist framework. As we will discuss later in the article, the emerging market infrastructure has been initiated and facilitated by a strategic change in Beijing’s approach to rural finance and development. This conforms to the development agenda of the hierarchical state, and has been shaped and tightly controlled by both central and local governments. Hence, Beijing’s market approach has essentially led to state-sponsored market extraction. In other words, the emerging market system in China is a means of a developmental state rather than an end of a liberal state as commonly found in the West. Despite a continuation of the state’s underlying role, there has been a transition of the mechanisms of extraction from state-directed to market-directed exploitation of rural financial resources under a new state-market nexus. This transition has marked the main logic behind the evolution of rural finance in China. What should come next, we argue, ought to be a reconfiguration of the relationship between the state, the market, and the peasantry.

State Predation Continues: Reforms between 1979 and 1995

Rural reform heralded wider economic reforms in China in the 1980s with great initial success in the form of a surge in agricultural output and rural income. This was largely due to institutional reforms that had reorganized rural production from state-controlled communes to a household contract system on one hand, and on the other, to the introduction of market exchanges with the urban sector, which unleashed farmers’ entrepreneurship and productivity (Oi, 1990; Huang, 2008). However, we argue that, despite the success of rural reforms in the early 1980s, rural finance remained the prey of the state. Capital scarcity continued to haunt the Chinese economy in the early years of reform, that is, until the mid-1990s. The state still used rural finance as a means of extraction, while the increase of agricultural production was largely self-financed by rural households. New players, namely local governments, emerged, with new demands for financing local industrialization and urbanization, which helped tighten the state’s control over rural financial resources during this period. In fact, the vertical control of finance by the central government and the horizontal fragmentation (Zhou, 2003) entailed by local government competition only strengthened the extractive capacity of the state in mobilizing and diverting rural financial resources into the urban and industrial sector.

Vertical Control

The aim of the economic reforms since 1979 has been to transform the Chinese economy from rigid planning to more of a market orientation. This has involved transforming economic decision making from a state monopoly into one where market participants play a central role. The gradual retreat of the state from its omnipresence in the economy has invariably been accompanied by a redistribution of national resources from the state to society. A direct indication of this process has been the relative decline of the state’s fiscal capacity on the back of a rapidly growing economy. In addition, the relative share of state-owned enterprises (SOEs) in national output has also been declining, which has further reduced state revenue. On the other hand, however, the central government has needed a strong capacity to mobilize and allocate resources in a new reality where it is in a weak fiscal position (Wang and Hu, 2001). Thus, the financial sector, especially the banking system, was called upon to take over part of the fiscal functions of the state in mobilizing financial resources, subsidizing the state sector, and reducing regional disparities. By the mid-1990s, for example, 98% of the working capital of SOEs was financed by bank loans. This transfer led to the “fiscalization” of the Chinese banking system, with the state treating the financial sector, including the rural financial system, simply as another treasury (Pei, 1998; Zhou, 2003).

The initial phase of financial reform featured vertical control of financial resources by the central government. The old monobank system, in which the People’s Bank of China (PBC) functioned as both a central bank and the sole commercial bank, apparently could not fulfill the task of mobilizing private funds in a decentralized and increasingly sophisticated market. Instead, between 1979 and 1984, the central government set up a two-tier banking system in which the PBC became an exclusive central bank, while its commercial functions were taken over by four reestablished state-owned banks: the Industrial and Commercial Bank of China (ICBC), the Agricultural Bank of China (ABC), the Bank of China (BOC), and the China Construction Bank (CCB), collectively referred to as “the Big Four” (Bell and Feng, 2013).

At the same time, the administration of China’s bureaucracy was divided into different vertical functional/industrial agencies (xitong, or tiao), as well as horizontal territorial jurisdictions (diqu, or kuai). The bank-dominated financial system was a vertically segmented structure as the businesses of the Big Four were vertically divided along industrial sectors with nationwide branches so that each enjoyed a monopoly in its own territory (Bell and Feng, 2013: 59–61). In particular, the ABC was split off from the PBC on March 13, 1979, and mandated to provide financial services for rural areas. 3 As the banking system increasingly performed as a “secondary treasury,” the vertical structure of the system was designed to facilitate the central government’s mobilization of funds from enterprises and households, including those in rural areas, to finance its projects and programs. The rapid monetization in the early years of reform saw explosive development of the financial sector in terms of the assets of financial institutions. However, the vertical segmentation of the financial system was not meant to allocate resources on a commercial basis, but to finance the central government’s fiscal investment (Zhou, 2003; Okazaki, 2011).

Horizontal Fragmentation

This situation changed when local governments joined the game and became important players. Before the two-tier banking system was established, local governments did not have the incentive to control financial institutions because in a command economy the budget plan was more important than bank lending. As the fiscal capacity of the central government became weaker, centrally allocated funds could not meet local investment needs. In addition, under a new fiscal contracting system, local governments also lacked the incentive of strengthening their taxing capacity (Zhou, 2003). Apart from attracting foreign investment through the open door policy, both the central and local governments sought to meet the increasing shortfall of revenue by using the banking sector to finance infrastructure spending. Moreover, the promotion of local officials came to be largely determined by the performance of the local economy, which is mostly defined in terms of economic growth. In China’s political economy, growth has mainly been driven by public investment, which has been mostly financed by banks. This means that the political career of local officials has largely hinged on their control of financial institutions, particularly banks. These include local branches of state banks, since the appointment and welfare of local bank staff were controlled by local governments and since banks also had an incentive to expand these branches locally (Pei, 1998). At the same time, local governments were in a race to set up their own finance platforms, such as local trust and investment companies, stock brokerages and exchanges, and so on, in a bid to attract local funds and deposits for local investment. Hence, within a short time, such locally based or locally controlled finance institutions, some of which were illegal, experienced explosive development. In sum, on top of its vertical segmentation, the financial system was horizontally divided along territorial administrations (see Figure 2).

The formation of the rural financial systems and the logic for future reforms.

China’s persistent capital scarcity combined with the government’s (both central and local) strengthened control of the financial system meant that the aim of rural finance in the 1980s and early 1990s was still dominated by the state’s concern to harness rural financial resources for industrialization and urbanization, rather than to address “the finance predicament” in the countryside. Given that returns on agricultural investment have been significantly lower than those on industrial projects, particularly export-oriented processing industries, both local governments and the banks were inclined to divert rural deposits into non-rural investments. Moreover, the capital of local financial institutions, especially rural credit cooperatives (RCCs), was often abused if not outright appropriated by some local governments to fill the shortfall in government funds since it was understood that the losses of the RCCs would ultimately be written off by the central government through the PBC’s re-lending programs (Xie, 2001).

At the micro level, since its reestablishment in 1979 the ABC had been acting simultaneously as a policy lender and a commercial lender. Another major institution in rural finance was the RCCs, which took over 60% of total deposits and lending in rural China in the 1980s. During this period the RCCs were directly controlled by the ABC and therefore lacked flexibility and independence in business management. Instead of being a form of cooperative finance, they had a strong government background, drawing financial resources from the rural areas on the one hand and seeking higher returns through lending to non-rural areas and industries on the other. As a result, since the 1970s the RCCs’ total outstanding loans have been constantly lower than their total deposits (the loan-to-deposit ratio was less than 1) in rural areas, meaning that rural savings were allocated less to rural lending than to non-rural. In the 1980s and 1990s this ratio was kept at about 1:2 and 2:3, respectively. In particular, only 17.7% of rural deposits in 1995 were designated for loans to rural areas (Almanac of China’s Finance and Banking, 1996: 521). A survey by Huang (2009) suggests that only 30% of rural households sampled had access to some form of credit in the 1980s, a figure that fell to 10% in the 1990s. Thanks to the state-sanctioned financial mobilization regime, despite the soaring demand for finance in a liberalizing rural economy, there had been a net outflow of financial surpluses, making rural areas a net provider of capital to industries and the newly rich in urban areas.

The rise of township and village enterprises (TVEs) in the 1980s and early 1990s involved two issues with regard to their finances. First, as returns of these rural industrial enterprises were generally higher than those of agriculture, financial institutions tended to allocate more credit to this sector. In fact, lending to rural enterprises in outstanding loans of the ABC and the RCCs increased from 9.7% to 23.8% between 1979 and 1992. Credit allocated to the TVEs exceeded that for agriculture for the first time in 1988. However, lending to TVEs had been disproportionate to the sector’s contribution to national output. For instance, although TVEs’ output made up 24% of China’s total GDP in 1993, lending to TVEs was only 7.40% of total loans. Second, this increased lending to the TVEs did not result in an increase of rural lending in aggregate terms. Rather, it merely represented a change of the structure within rural lending, that is, the increase of loans to TVEs largely crowded out loans for agriculture and rural households. For example, agriculture credit was 3.68 times that of TVEs in 1978, but decreased dramatically to 1.00 in 1987, and still further to 0.66 in 1997 (Almanac of China’s Finance and Banking, various years 1986–1998).

The rapid development of the urban industrial sector in the 1990s posed great challenges to rural enterprises that had been dominated by household-based workshops and small businesses during the transition from an economy of scarcity to abundance. As a result, the overall scale of TVEs has been declining since the late 1990s, evolving into private micro enterprises. At the same time, these small enterprises faced increasing difficulties obtaining finance due to the reasons discussed earlier (Zhou and Takeuchi, 2010) and the volume of TVE finance decreased steadily until it became negligible. Outstanding loans to the TVEs have been below those for agriculture since 2002. In 2007, for example, lending to TVEs dramatically dropped to 2.3% of total credit compared to 7.4% in 1993 (Almanac of China’s Finance and Banking, 1994: 569, 2008: 533; China Statistical Yearbook, 1994: 544, 2008: 757).

Tensions between Formal and Informal Institutions

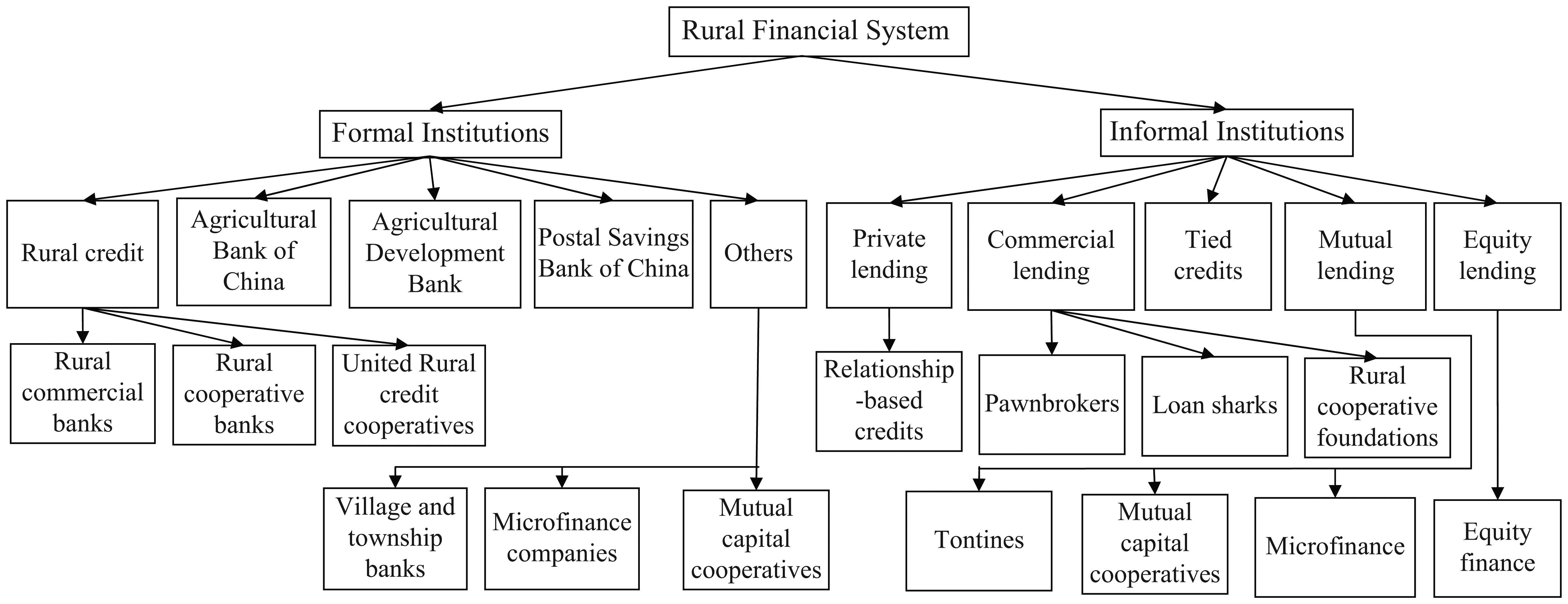

Given the lack of credit and other financial services provided by formal institutions, the growing demand of finance has given rise to various informal institutions. According to whether they are included in the state’s regulatory mechanisms or not, financial institutions can be divided into formal and informal types (see Figure 3). Formal institutions are those that are certified and regulated by the financial authorities, while the rest are informal arrangements, largely operating in a gray area. That these informal institutions have operated outside of the state’s control has meant that their capital could not be diverted via administrative command according to the state’s policy preferences. Thus, this put the informal institutions in direct conflict with their formal counterparts, which were mandated to attract and mobilize rural savings. For the government, therefore, the relationship between the formal and the informal system was one of horizontal competition, rather than vertical cooperation. Indeed, throughout the reform era the central government has repeatedly waged a national political campaign against the informal credit sector. The State Council has also issued formal provisions to ban “illegal” financial institutions (Tsai, 2002: 1).

Framework of China’s rural financial system.

Market Extraction: Reforms since 1996

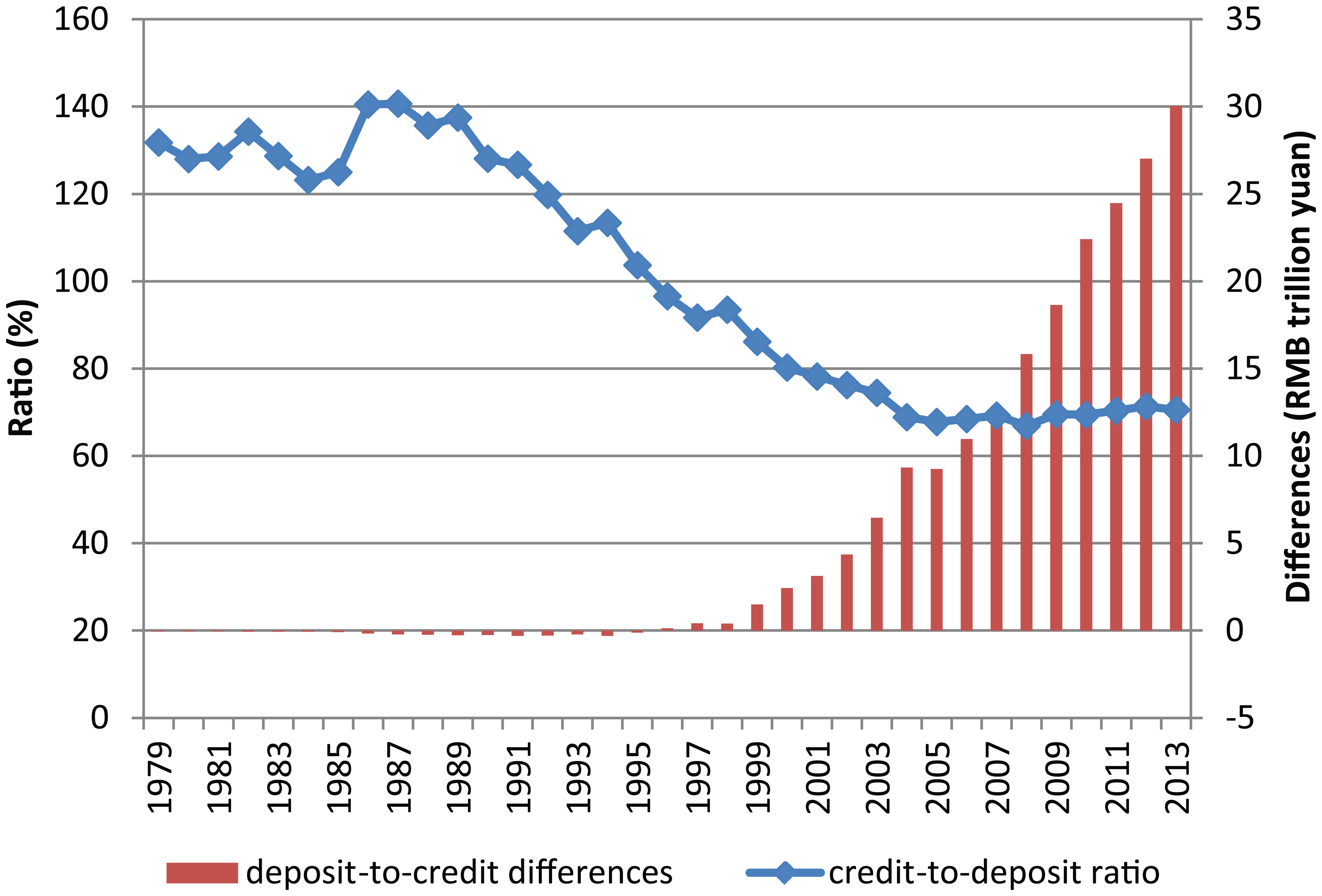

Capital shortage, arguably the key dynamic of state predation on rural finance, experienced a U-turn by the mid-1990s after almost two decades of monetization and economic growth. Since 1996, there has been a shift in the Chinese financial system from a shortage to an abundance of capital. A major indication was the change from a net credit balance between 1978 and 1995 to a net deposit balance thereafter. Since 1996, the total amount of deposits began to exceed outstanding loans nationwide, and the gap has been increasing rapidly (see Figure 4). Accordingly, the credit-to-deposit ratio has been declining below 1. For instance, the credit-to-deposit ratio fell from 0.74 in 2004 to 0.71 in 2012. This suggests that as much as 27.02 trillion yuan of capital was idle. By May 2013, the ratio further slumped to 0.7091, with 29.26 trillion yuan idle. 4 Even excluding the size of banks’ reserves and extra reserves, and the change of the banks’ investment structure, an obvious fact is that there has been a huge amount of excess liquidity, which is still growing, in the domestic financial system.

The evolution of the capital supply in China’s financial system, 1979–2013.

The dramatic increase of domestic capital and the financial system’s shift from net credits to net deposits provided a strategic opportunity as well as a technical possibility for the Chinese state to reorient itself from an extractive to a more supportive and developmental role in rural finance. This developmental agenda, initiated by the Jiang-Zhu regime, has been shared by subsequent administrations. This has been reiterated in the eleven Number One Documents of the Chinese Communist Party in consecutive years since 2004, often a symbolic demonstration of the leadership’s policy priorities of the year.

The Hu-Wen administration placed a high priority on revitalizing the rural economy and on promoting more equal development between urban and rural areas under the banner of “Building a New Socialist Countryside.” For instance, in a 2006 speech to the National People’s Congress, President Hu Jintao pointedly observed that China’s industrial economy, then enjoying double-digit growth, should begin to “repay its debt to the countryside” (Wharton, 2007).

Urbanization has been one of Li Keqiang’s signature projects as the Xi-Li administration scrambles to find new growth potential for the Chinese economy. Yet rural development, including rural finance, also features prominently on Beijing’s strategic agenda, so that “the overwhelming majority of farmers can participate in the modernisation process on an equal basis and share the fruits of modernisation” (Central Committee, 2014). Accordingly, the notion of “inclusive finance” also appeared for the first time in a landmark blueprint for reform adopted at the Third Plenum of the Eighteenth Party Congress in 2013 (Central Committee, 2014: Part III). This echoes a strong international consensus that increased levels of financial inclusion—through the extension of savings, credit, insurance, and payment services—contribute significantly to sustainable economic growth. According to the United Nations, financial inclusion is achieved “when all individuals and businesses [including those in rural areas] have access to and can effectively use a broad range of financial services that are provided responsibly, and at reasonable cost, by sustainable institutions in a well-regulated environment” (UNCDF, n.d.). Given the critical role of rural finance in propelling the rural economy compared to the dismal performance of previous reforms, the leadership decided to further restructure the sector.

According to a blueprint drawn up by the State Council in 1996, the aim of rural financial reforms was to “establish and improve a rural financial system on a foundation of cooperative finance as well as the specialization of and cooperation between commercial finance and policy finance” (State Council, 1996). The reforms since 1996 can be divided into two phases. The first was between 1996 and 2003, which focused on establishing designated policy lending institutions and an attempt to commercialize state banks. The second phase, starting in 2003, centered on the structural reform of the RCCs and the diversification of rural financial institutions.

From the outset, the reform strategy appeared to be heading in the right direction to address the predicament of rural finance by incorporating the three forms of finance, namely, policy lending, commercial lending, and cooperative finance, in a systematic and complementary way. More importantly, it stressed the critical role of cooperative finance, an endogenous financial arrangement for rural areas. However, in practice the trinity strategy was largely replaced by a market-centered approach with limited policy lending, a problematic commercialization of cooperative institutions, and the triumph of profit-oriented market finance.

A Helping Hand That Was Less Than Helpful

The central state tried to restructure the rural financial system on several fronts, including establishing designated policy lenders for agriculture and the rural areas, increasing the supply of small loans through poverty alleviation programs and the postal system, and continuing the crackdown on informal institutions.

First, policy lending, in which the state could have played a central role, was marred by a functional ambiguity in institution building. The Agricultural Development Bank of China (ADBC) was established as a policy lender in 1994. It was expected that with the ADBC in place, the ABC could split off its policy lending function to the ADBC so that the former could undertake commercial banking exclusively. However, the ABC continued to share policy duty with the ADBC. At the same time, the ADBC was only in charge of loans for agricultural procurement instead of being a comprehensive provider of policy finance. In 1998, the range of its credit business was further reduced to solely supplying and managing funds for the procurement of grain, cotton, and edible oil. In 2005, for example, the ADBC granted loans of RMB342.37 billion, of which 80% was for the procurement of grain, edible oil, and cotton (Liu, 2008). The bank subsequently ventured into commercial lending as well. By the end of 2010, the share of procurement loans in its total outstanding loans had been reduced to 58.6%, while the share of lending to rural industries stood at 10% (PBC, 2011). In addition, in 2011 it added to its core business lending to key rural industrial enterprises and the processing sector (PBC, 2013).

At the same time, the government also stepped up state-sanctioned microfinance programs. The Postal Savings and Remittance Bureau, a department of the national postal service, which had been barred from issuing loans, was given the green light to establish a bank offering small deposit-backed loans to urban and rural depositors. Its lending subsidiary, known as the Postal Savings Bank of China (PSBC), was officially established in March 2007. Nevertheless, the role of the PSBC in facilitating rural finance remained limited. For instance, it issued almost 8 million microloans in 2012, but the borrowers accounted for less than 3% of total rural households (PBC, 2013).

The major form of state-sponsored microfinance has been subsidized loans in government-supported poverty alleviation programs extended to low-income areas and mostly rural households. To be sure, the government initiated subsidized lending schemes for poverty relief from 1986, but these targeted collectives at the township and village level rather than individual households (Rozelle et al., 1998). Providing subsidized loans directly to households did not start until a few years into China’s National 8-7 Poverty Alleviation Plan introduced in 1994. The aim of the plan was to raise 80 million people out of poverty in seven years (i.e., from 1994 to 2000). This was extended into the Guidelines of National Poverty Alleviation Development during 2001 and 2010, which mainly targets the impoverished in western China (Wang, 2007). In 2002, the central government transferred RMB 24.5 billion as transfer payments to compensate local governments in provinces carrying out the rural fee reform (World Bank, 2003: 71).

Despite fiscal support for the programs, there were various problems with these forms of subsidized lending. First, and yet again, the leading agency was not properly designated. While the ADBC was initially in charge of the management of the lending program, this function was later transferred to the ABC, which the government attempted to commercialize. In addition, the poverty lending program had not been regulated by the PBC, and the loans were treated largely as social grants, with less than 60% repayment rates (Tsai, 2004: 1490), which undermined the sustainability of the microfinance model (Cheng, 2003). More important, from the perspective of state-society relations, these programs were not properly implemented due to the weak capacity of the Chinese state (Tsai, 2004: 1498). On one hand, as state banks lacked institutional experience in lending to rural clients, the program often ended up as quota-style lending as the state required the banks to allocate a certain portion of their lending volume to low-income rural households. Therefore, the actual aim was distorted to ensure a certain number of loans were disbursed, rather than to ensure access to credit by those most in need. On the other hand, policy loans were prone to embezzlement and appropriation by rent-seeking local officials as corruption became rampant in China from the 1990s (Gong, 1997; Wedeman, 2004). Given quota-style lending, coupled with discounted interest rates, these loans, instead of reaching low-income households, ended up in the hands of local state and non-state elites through political patronage and networking.

The helping hand from the state, however, was confined to the formal sector. As discussed above, the state’s approach to the informal sector has been heavy-handed. While the government in most instances has tolerated the emergence of competing institutions at the local level, it has sought to co-opt and regulate them once they reach a large scale and draw funds from state financial institutions (Park et al., 2003). Regulation of the informal sector has also been strengthened since 1996. The brief history of rural credit foundations (RCFs) serves as a good example. In the early 1980s, the Ministry of Agriculture established a network of RCFs to serve as financial intermediaries for farmers, but the PBC never considered them formal institutions. The RCFs experienced rapid development in the 1990s under implicit sanction of the local governments, and became de facto village and township banks (Liu, 2005). In September 1996, RCFs existed in 38% of all Chinese townships (Du, 1998; Liu, 2005) with funds reaching about RMB100 billion compared with RMB800 billion in RCC deposits (Cheng et al., 1997: 41). Although the RCFs were criticized for usurious finance and inadequate risk provisions or “soft risk constraints” (Cheng et al., 1997; Liu, 2005), they posed less of a threat to overall financial stability than the rampant speculation in sectors such as the stock market (Wen, 2009). Nevertheless, Beijing ordered a crackdown of the RCFs in 1999. They were dissolved, further reducing sources of credit for rural residents and enterprises. Moreover, since the central government did not provide reserves for the RCFs’ liabilities, lower-level governments (particular at the village level) and, ultimately, farmers had to pay for this, which devastated the rural financial sector (Zhao, 2005).

Despite the government’s efforts in establishing state-sanctioned financial intermediaries, especially microfinance poverty alleviation programs, China’s farmers continue to rely primarily on informal sources of finance. According to a national survey by the Ministry of Agriculture, only 16.6% of the total borrowing by rural households sampled came from formal financial institutions in 2009 (calculated from data in the national rural fixed observation points data collection; see Policy Research Office, 2010: chap. 1). Moreover, according to Tsai (2004: 1488), the scale of informal finance actually increases in communities that have been targeted for a greater supply of official credit.

Cooperative Finance That Was Less Than Cooperative

According to Baarda (2006: i), cooperatives operate according to three basic principles: the user-owner principle (“those who own and finance the cooperative are those who use the cooperative”); the user-control principle (“those who control the cooperative are those who use the cooperative”); and the user-benefits principle (“the cooperative’s sole purpose is to provide and distribute benefits to its users on the basis of their use”). In other words, a cooperative, including financial cooperatives, should be of its users, by its users, and for its users.

Cooperative finance in China mainly comes from RCCs, which handled over 30% of rural-related loans and 80% of rural household loans in 2012 (PBC, 2013). According to Beijing’s strategy in 1996, the RCCs were to be transformed into genuine cooperative institutions, but instead they marched down the road of commercialization. On one hand, as discussed earlier, the RCCs lacked the incentive to become true cooperatives, and were more inclined to act as a commercial lender by diverting rural savings to local industries in the search for profit. This again resulted in the draining of rural financial resources. For example, the RCCs’ lending to farmers was less than a third of the latter’s deposits, with the credit-to-deposit ratio standing at 0.31 in 2003. Even calculated in the broader terms of total rural lending, this figure stood at 0.39 in 2003 (Almanac of China’s Finance and Banking, 2004: 287). Moreover, local governments continued to control the RCCs and interfere with their operations. Because lending decisions were controlled by local officials concerned more with building local relationships than avoiding credit risk, the RCCs had notoriously low repayment rates. Not surprisingly, over the years the RCCs were saddled with massive levels of non-performing loans (NPLs). At the end of 2002, more than half of all RCCs were run at a loss, and overall the RCCs were technically insolvent, with NPLs accounting for 37% of their total outstanding loans (Liu, 2008: 6).

As discussed earlier, rural financial reforms were accelerated beginning in 2003. During this round of reforms, the institutional form of cooperative finance was diversified into a variety of intermediaries, including rural commercial banks, rural cooperative banks, and RCC unions. Although these were nominally cooperative-finance institutions, in practice most of them operated on more commercially oriented principles. Under the reform program, the RCCs were institutionally consolidated at the local, particularly the provincial, level on a shareholding basis. The NPLs were largely written off by the government to give the RCCs a clean start (花钱买机制), while Beijing stressed that local governments from then on would be financially responsible for the losses of the RCCs under their control. At the same time, a series of measures were taken to improve the ownership structure, corporate governance, and business management mechanisms of the RCCs (Jin, 2008). Nevertheless, old problems remain as local governments have retained their influence over the RCCs as the latter’s directors are appointed by their upper-level governments. With the reduction of the number of shareholders, the RCCs are more subject to insider controls (Xie et al., 2006). Moreover, the consolidation of the cooperatives has led to even fewer loans to small borrowers as the cooperatives pool their resources to lend to urban infrastructural projects and state-owned companies. For example, despite an increase of the share of rural household credits in total RCCs’ credits from 28.9% in 2003 to 33.7% in 2012, the number of loans to rural households actually declined from 77.2 million to 50.7 million during the same period (PBC, 2013).

The Market That Means Business

Despite the three-pronged strategy, the central approach of the reforms has been to marketize the rural financial sector in a bid to improve the efficiency and quality of financial services. A major step was to commercialize state-owned banks. In Deng Xiaoping’s words, “We should take bolder steps in financial reforms, and turn the banks into genuine banks. The banks we have had in the past have been currency issuers and state treasuries, but not genuine banks” (Deng, 1993: 193). The campaign was heralded by legislative breakthroughs, including the promulgation of the Central Bank Law and Commercial Bank Law in 1995. This also led to the abolition of policy lending by the Big Four. As discussed earlier, the ABC was expected to focus on commercial lending after the ADBC was established as the policy lender in rural areas. Market-oriented banking reform was accelerated beginning in 2003 under the leadership of the PBC. The plan was to turn the Big Four into shareholding companies, recruit foreign strategic investors, and eventually list them in domestic and overseas stock exchanges (Bell and Feng, 2013). By incorporating foreign banking expertise and making the banks subject to market scrutiny, it was expected that the banks would be transformed into commercial entities with modern corporate governance and risk management. So far the Big Four have benefitted from this therapy, with the ABC being listed in Hong Kong and Shanghai in July 2010.

Despite the progress in this round of market-oriented reform, there are a number of institutional problems pertaining to the ABC and rural finance. First, as mentioned earlier, the ABC has continued to shoulder some of the policy functions of the government in issuing policy loans for poverty reduction as well as loans for infrastructure construction and urbanization programs in rural areas. By the end of 2003, such loans reached RMB928.8 billion, amounting to 42% of ABC’s total outstanding loans (Almanac of China’s Finance and Banking, 2004: 487). The mix-up of the two inherently contradictory functions at the bank is likely to hinder the development of its commercial arm. It also created a moral hazard for the bank since commercial losses could be categorized as losses from policy lending, which would eventually be underwritten by the state budget.

For rural finance, a more devastating impact of the market reform was induced by the commercialization of the ABC and the central government’s emphasis on avoiding financial risks in the aftermath of the Asian financial crisis. This led to a massive withdrawal of the ABC’s branches from below the county level, leaving the RCCs the only financial institutions serving villages and townships. The ABC was listed on the stock market “as a whole,” which suggests that its rural-related businesses will stay with the listed company. While the bank is often criticized for not providing enough services for rural areas, an IPO may well wipe out the little credit it does provide since the bank will inevitably face increased market pressure for profits.

In addition to reforming state banks, Beijing’s marketization strategy also included lowering market entry barriers and diversifying financial institutions. Ownership restrictions have been relaxed as cooperatives, private, and even foreign institutions have been allowed to enter the rural financial market (Kendall, 2008). Local experimentation and innovation of financial products have also been encouraged by the regulators (PBC, 2013). At the same time, since 2007 the government has promoted the establishment of new forms of rural financial institutions, including village and township banks (村镇银行), microfinance companies (小额贷款公司), and village mutual cooperative funds (农村资金互助社). The rationale was that an increase in the supply of financial intermediaries with a diverse ownership structure would lead to increased market competition and hence efficiency. So far the role of the new players in facilitating rural finance has been negligible at best. For instance, the total outstanding loans issued by the three new forms of rural financial institutions stood at 234.7 billion yuan by the end of 2012. Even if all these loans are counted as rural and agriculture-related credits, they amount to only 1.3% of all rural and agriculture-related loans issued by all financial institutions (PBC, 2013). In addition, many of these institutions have deviated from their supposedly supportive role in rural areas and instead have followed a market logic. For example, according to regulations, village and township banks are supposed to target their main business at providing financial intermediations for local rural households, agriculture, and rural economic development. Although the number of these banks experienced a rapid increase from only 9 in 2007 to 1,071 by the end of 2013 (Report on the Development Prospects, 2015), many are located in relatively developed regions, and many do not engage in rural-related lending at all (Yang, 2012).

In summary, the major development in rural finance since 1996 has been the establishment of a market infrastructure under a supply-side reform. Both state and cooperative lenders that were designated for rural areas turned to urban customers. Apart from symbolic and limited moves, a flurry of new forms of market players have been lukewarm, if not reluctant, in responding to Beijing’s call for supporting rural finance due to their market imperative of profitability.

The round of rural financial reform that began in 1996, which sprang from the assumption that reform meant commercialization and market competition, has further undercut finance and the economy in the countryside, leading to an excess of liquidity in urban areas but a shortage in rural areas, a structural imbalance in the allocation of financial resources that Zhou (2008) calls “the liquidity paradox.” The paradox of the deterioration, if not potential crisis, of rural finance on the back of the otherwise robust growth of the Chinese economy suggests that market-oriented commercial finance per se cannot fulfill Beijing’s ambition to revitalize the rural economy. The reform in essence has merely replaced state extraction with market extraction. Within a market context, the rural economy has suffered massive hemorrhaging as profit-seeking intermediaries plugged their credit tubes into the countryside and drained away its savings and surplus.

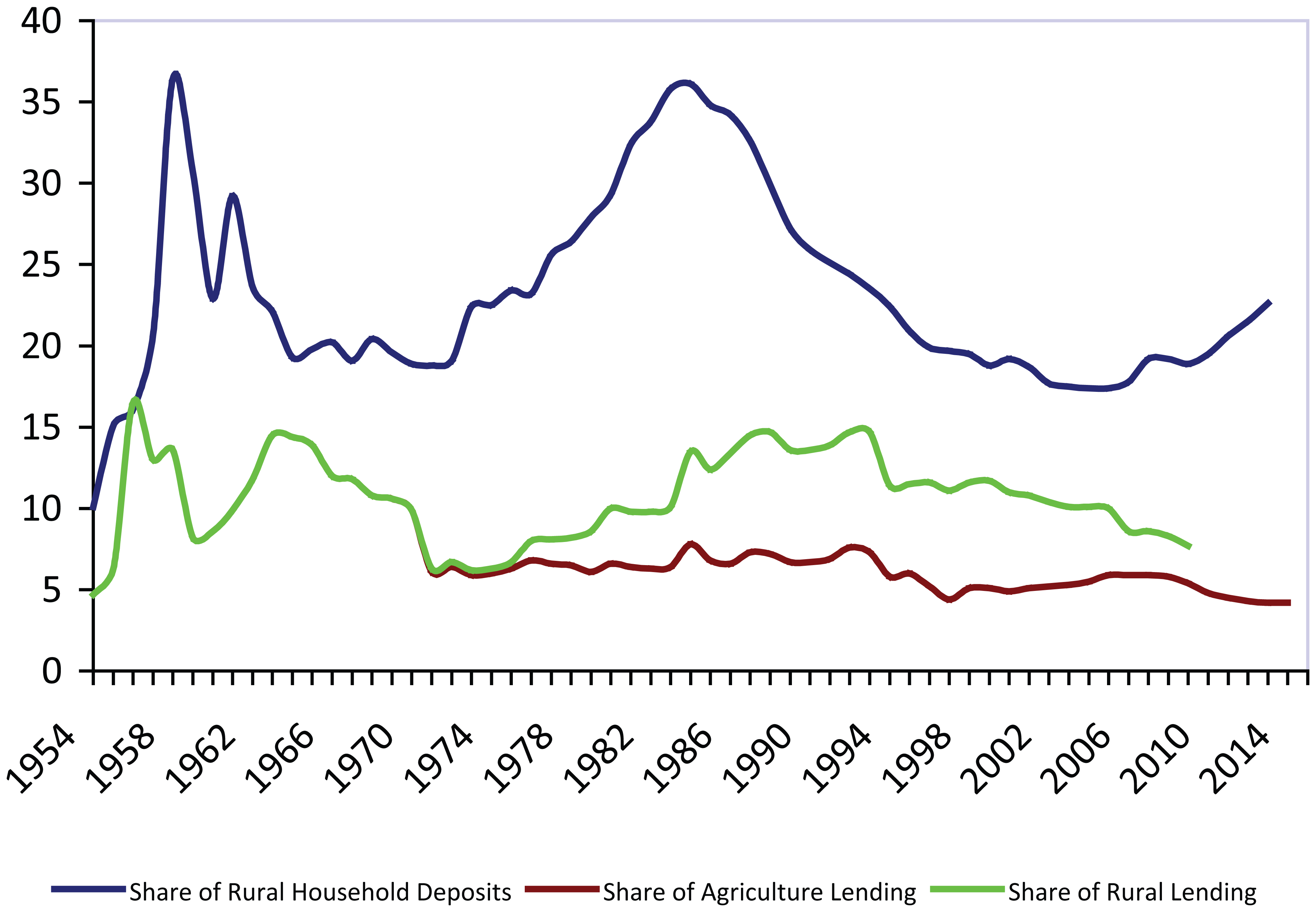

Figure 5 offers a panoramic view of the imbalance between rural savings and credits since 1954. The share of rural household deposits in total deposits had been hovering above 20% between 1978 and 1995, and remained between 17.4% and 22.6% between 1996 and 2013. On the other hand, various categories of credits in rural areas have been significantly lower than the latter’s contribution to national savings. For example, lending to agriculture in total credits has been below 6% of total loans since 1996. Even under Beijing’s political push for a more diversified and competitive market, the share of agriculture credits actually declined to around 4% in 2013. This is also reflected in the share of rural-related credits (credits to agriculture and rural enterprises combined) in total short-term loans, which has been relatively stable within a low-level band between 3% and 8% since 1978. Both categories of lending have been disproportionally lower than agriculture’s annual average contribution to the national economy of 10% over the same period. They are even more disproportionally lower when seen in light of the fact that rural residents make up nearly 70% of the total population and 50% of the workforce in China. Furthermore, the difference between the share of rural deposits and the share of rural-related lending grew from 7.4 to 11.2 percentage points between 2003 and 2009. This suggests that rural financial resources have been allocated on a basis that is neither efficient nor equitable.

Share of rural deposits and lending in national savings and credits, 1954–2014.

The financial authorities should be credited for achieving nationwide coverage of basic financial services in rural China by early 2013. However, in general rural households still lack access to credit. Various researchers and surveys suggest that credit to farmers accounts for less than half of their total effective demand. If the entire rural population is taken into account, only a third have access to credit. For instance, a report by the PBC (2013) finds that by the end of 2012 fewer than 43 million, or less than 20%, of China’s 273 million farmers nationwide had access to loans by the RCCs and the ABC. Furthermore, it is only the grass-tips, a fraction of the rural population who are either newly rich or well connected with local officials, who have access to credit, while most of the grass-roots have missed out. The same report suggests that despite a political commitment to increasing the quantity and quality of rural financial services in recent years, from 2004 to 2007, the number of county-level financial institutions actually fell by 9,811, of which 6,743 were branches of the Big Four. In particular, the number of ABC branches has been dramatically cut by 64%, from 63,736 in 1997 to 22,930 in 2010, and only 34% of the branches are in rural areas. The number of the RCCs has also been reduced by a third, from 111,358 in 1997 down to 74,407 in 2012, and only half of the branches are in rural areas (PBC, 2013).

In addition, the shortage of financial resources relative to demand in rural areas is gigantic. It has been estimated that the Chinese government will need RMB15–20 trillion of new funds by 2020 to finance its ambitious campaign of “Building a New Socialist Countryside.” However, the amount so far actually allocated—RMB339.7 billion and RMB431.7 billion in 2006 and 2007 respectively—is only a fraction of the total amount projected. Again, this means the financial sector will have to shoulder the task of filling the gap, a mission China’s rural financial institutions will find difficult to accomplish, at least under current circumstances. After all, by January 2009 total outstanding rural credit only accounted for 5.69%, or RMB1.8 trillion, of their total short-term loans. By the end of 2012, the financial sector had only issued 2.02 trillion worth of rural infrastructural credits, which is well behind the pace expected by the central government (PBC, 2013). 5

Conclusion: Beyond the Market

As the PBC governor Zhou Xiaochuan (2004: 38) once remarked,

If we see agriculture, peasants and the countryside as a human body, then rural finance is an important internal organ, which draws resources from the body but at the same time serves the body. Therefore, it is not something outside the body that needs only to perform its function without servicing itself.

The symbiotic relationship means that the dynamics of rural finance should be explored within the wider context of the development of the rural economy.

Under central planning, the state, wielding its despotic power, prioritized industrialization at the expense of the rural economy, and rural finance inevitably served the state’s purposes by transfusing rural financial resources into the urban industrial sector. Despite the initial success of rural reform in the early 1980s and a brief expansion of township and village enterprises in the early 1990s, the rural economy and rural income have continued lagging behind their urban counterparts, which have benefited from the enormous opportunities of foreign investment and the rapid expansion of China’s external trade. Although the central leadership intended to foster the development of the rural economy, the new state-market nexus has hampered the infrastructural power of the state and so far has largely failed to solve the predicament. Official credits are limited and in many cases mismanaged and misallocated under a fragmented bureaucratic structure. Cooperative institutions, on the other hand, have largely been alienated into profit-driven commercial institutions. Combined with market-oriented institutions that have flourished in the last decade under the state’s promotion, rural finance has been trapped in a market-induced extraction due to economic inequalities and imbalances between the urban and rural sectors.

This case illustrates inherent conflicts between the policy goal of nurturing rural development and the profitability concerns of market institutions. As we have demonstrated, the options and possibilities of promoting rural finance and development have been exhausted within the current institutional setting of market-oriented finance. This suggests that the way out for rural finance in China lies beyond a “diversified” and “competitive” market system. Instead, we believe both the state and the market must address the issue. The trinity strategy of 1996, which has been distorted into a market-centered approach, should be re-invoked with the aim of establishing state-sanctioned vertical cooperation among policy, cooperative, and commercial finance, and between formal and informal institutions. In particular, the state should strengthen its capacity to issue policy credits and funds. At the same time, the state should also relax its opposition to informal institutions developed within the rural economy. Indeed, the predicament of rural finance in China has been due to a lack of a genuine endogenous financial system for the rural economy. Both the predatory extraction in the planning era and the market extraction in the reform era have been imposed exogenously by the state in line with its political and economic imperatives. A community-based intermediation would help ensure that rural financial resources and agricultural surpluses would be circulated back into the rural economy. Such endogenous institutions, however, are only likely to flourish within a supportive environment of social trust, something that will take a long time to establish in rural China.

Footnotes

Acknowledgements

Li Zhou wishes to acknowledge the following funding sources: the Fundamental Research Funds for the Central Universities, and the Research Funds of Renmin University of China (15XNI009). Hui Feng wishes to thank the participants at the research seminar of the East Asia Institute, National University of Singapore in January 2015, who have provided helpful suggestions and insights regarding the paper on which this article is based. Xuan Dong wishes to acknowledge funding from the National Natural Science Foundation of China (71573265).

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Li Zhou received funding from the Fundamental Research Funds for the Central Universities, and the Research Funds of Renmin University of China (15XNI009). Xuan Dong received funding from the National Natural Science Foundation of China (71573265).