Abstract

The globalization of audit markets not only provides an opportunity for the U.S. Big 4 auditors to establish international expertise through global networks, but it also exposes them to reputation risk arising from the acts of their local partners. We analyze the audit failure of ChuoAoyama, one of the Japanese Big 4 audit firms, and find that its credibility impairment reduced security prices of not only the clients of PricewaterhouseCoopers (PwC), their U.S. affiliate, but also the American clients of all other Big 4 auditors affiliated with the Japanese Big 4. Because the quality of the U.S. audit firms is perceived as superior to that of auditors in other countries, we also analyze the premiums arising from the affiliation with the U.S.-led global audit firm networks. We compare the effect of Andersen’s audit failure with ChuoAoyama’s in Japanese capital markets and find that the magnitude of negative market reactions is larger for Andersen’s failure than for ChuoAoyama’s. Together, these results suggest that global audit firm networks have created a network-wide reputation for their services that is susceptible not only to audit failures of the U.S. Big 4 but also to those of non-U.S. affiliates and that there is a quality premium for the U.S. Big 4 in Japanese markets. Our results provide a rational explanation for PwC’s aggressive efforts to temper the negative impact of ChuoAoyama’s failure on their reputation.

Introduction

The criminal indictment of Arthur Andersen for its handling of the Enron audit has clearly cast doubt on the quality of services provided by large international accounting firms. 1 Although the act (e.g., shredding tons of important documents) might have been an isolated incident, the accounting impropriety that occurred at Andersen’s Houston office raised concerns about quality assurance training and enforcement of audit quality. Earlier studies (e.g., Cahan, Emanuel, & Sun, 2009; Chaney & Philipich, 2002; Hecker, Krieg, & Pfauth, 2006; Krishnamurthy, Zhou, & Zhou, 2006) provide evidence that Andersen’s audit failure negatively affected the stock prices of their clients in both domestic and international markets. There is also evidence that the effect of Andersen’s scandal spilled over to the clients of the other U.S. Big 4 audit firms (Asthana, Balsam, & Krishnan, 2003; Doogar, Sougiannis, & Xie, 2007). However, the contemporary research overlooks the possibility of a spillover effect from a failure by a foreign affiliate on the clients of the U.S. Big 4 audit firms in the U.S. market. We fill this gap by analyzing reactions in the U.S. market to an audit failure committed by ChuoAoyama, a foreign (Japanese) affiliate of PricewaterhouseCoopers (PwC). This is one of the major audit failures outside the United States that involved affiliates of U.S. Big 4 audit firms (e.g., PwC, KPMG, Deloitte Touche, and Ernst & Young). 2

The international audit market is highly concentrated and is centered around the U.S.-led global audit firm networks. 3 The globalization of audit markets through worldwide affiliations provides an opportunity for the U.S. Big 4 auditors to expand their knowledge and exploit their international expertise (Carson, 2009; Lenz & James, 2007). The affiliations make it easy for U.S. audit firms to penetrate foreign markets and for local auditors to establish a reputation for international expertise. However, if a reputation for high quality is a common premium among the U.S. Big 4 global networks, an audit failure by a local foreign affiliate could damage the reputations of all of the members of the networks. 4

The Sarbanes–Oxley Act of 2002 created the Public Company Accounting Oversight Board (PCAOB) to restore public confidence in the auditing system in the United States. 5 One of its policies requires U.S. firms to supervise work performed by non-U.S. affiliates in foreign operations. However, the implementation of proper quality control systems appears to be limited. For example, a 2003 inspection report issued by the PCAOB (2004) notes that PwC failed to provide “evidence of the supervision and control of their foreign affiliates, in accordance with standards establish by the Board” (Release No. 104-2004-005, p. 13). 6 In its coverage of the ChuoAoyama scandal, The Japan Times (“Accountants Face Kanebo Fraud Charge,” 2005) reports that “prosecutors are set to charge several certified public accountants at a Japan unit of the PricewaterhouseCoopers group with collaborating with executives at Kanebo Ltd. . . .” 7 These examples clearly demonstrate the weak quality control of foreign affiliates.

In this study, we analyze the risks associated with membership in global auditing networks. First, we examine whether a highly publicized audit failure by ChuoAoyama affected the quality reputation of the U.S. global audit network firms in the American market. This is the risk associated with a failure by an affiliated foreign auditor borne by the U.S. Big 4 and investors in the U.S. markets.

The global network firms use common accounting technologies and strategies to increase visibility and expand their oversea business. If investors view membership in global audit firm networks as a sign of high quality, it is reasonable to expect that a local audit failure could damage the reputation of not only the local auditor but also all of the other network members. Carson (2009) finds that global industry specialists charge premium fees for their international expertise and suggests that there is economic value associated with the organizational structure of global networks. We directly analyze the reputation spillover risk associated with expansion of the global networks.

The audit failure by ChuoAoyama in Japan is an ideal setting to test whether U.S. investors update their risk assessment about the ability of the U.S. Big 4 auditors to deliver high-quality services based on an audit failure committed by a foreign affiliate. Both the United States and Japan have large equity markets with long histories, well-established legal systems, and are home to a number of multinational corporations who can raise capital in global markets. It is reasonable to assume that sophisticated investors carefully follow news that will move security prices. If ChuoAoyama’s audit impairment reduced the stock prices of client firms for all of the U.S. Big 4, this indicates a common high-quality premium associated with membership in global networks.

Second, we compare investors’ reactions with both the Andersen and ChuoAoyama’s audit failures in the Japanese market to assess the quality premium created through affiliation with the U.S. Big 4 global network firms. To do so, we compare the magnitude of the reduction in stock price caused by Andersen’s audit failure with that caused by the ChuoAoyama scandal in Japanese markets. We designate Andersen’s auditing scandal as a “central audit failure” because it was at the center of its global network. ChuoAoyama is one of the Japanese Big 4. Their audit failure at Kanebo made national headline news in 2004, exposing the weakness of auditor independence in Japan. We call this a “local audit failure” because ChuoAoyama was the Japanese member of a global audit network affiliated with PwC. The endorsement of a U.S. Big 4 auditor might have been valuable for the Japanese Big 4 to establish a reputation for high quality. 8 We assess the quality premium associated with affiliation with the U.S. Big 4 in a single economy as opposed to two economies with different regulations.

It is difficult to compare the gravity of audit failures occurring in two different countries. But because of their visibility, intuition might suggest a direct effect on their clients’ stock prices within the same country to be larger than a spillover effect from another country. This intuition suggests that market reactions in Japan should be larger for the ChuoAoyama audit failure than for Andersen’s. Alternatively, if the majority of investors are sophisticated enough to understand the quality difference between Japanese and U.S. audit firms, market reactions are likely to be larger for Andersen’s audit failure than for ChuoAoyama’s.

In particular, we utilize a situation where the insurance value of auditing is almost non-existent in Japan. This allows us to compare the effect of the Andersen and ChuoAoyama audit scandals on share prices based on the assurance value and helps us to assess the reduction in value of market perceptions of high-quality audits. Skinner and Srinivasan (2012) also exploit this feature of the Japanese setting and analyze auditor reputation. They show large Japanese corporations are concerned about high-quality reputations and select auditors accordingly. However, they do not assess the reputation premium that accrues to the Japanese Big 4 firms from joining global audit networks. We assess this quality premium by comparing the effect of Andersen’s audit failure and that of ChuoAoyama’s in Japanese markets as opposed to analysis of the effect of ChuoAoyama’s audit failure on Japanese enterprises.

We show that the investors in U.S. markets react negatively to ChuoAoyama’s audit failure. We find that overall cumulative abnormal returns (CARs) for four events associated with ChuoAoyama’s audit failure are significantly negative for American clients of both PwC and the other U.S. Big 4 firms. These results suggest that ChuoAoyama’s credibility impairment reduced the high-quality reputation of all of the U.S.-led global audit networks. We also observe that it took some time for U.S. investors to react to audit failure by a Japanese affiliate. However, once PwC’s involvement was publicized, their reaction became strong.

In comparison, Japanese market reactions to Andersen’s failure were about 0.5% more negative than to the ChuoAoyama’s events. We interpret this result as showing that there is a quality premium for the U.S. Big 4 in Japanese markets. Consequently, an audit failure committed by a U.S. Big 4 firm appears to be more costly for Japanese clients than a failure by a Japanese Big 4 auditor.

Our analysis contributes to the current literature by extending Carson’s (2009) study of global audit firm networks. First, major U.S. audit firms have successfully expanded their business worldwide through affiliations. Lenz and James (2007) refer to this expansion as a strategic network that builds a comparative advantage in international specialization. Our results show that auditing networks have created a general level of network-wide reputation for quality and international expertise. However, this reputation is susceptible not only to central audit failures but also to local problems.

Second, rapid expansion of global audit networks can create weaknesses in quality control among the network members of foreign operations. Our study of the effect of ChuoAoyama’s audit failure on the U.S. markets provides some insight into the risk of expanding their global networks. Local audit failures are becoming more and more problematic as additional failures outside the United States are unveiled. The report issued by PCAOB (2004) explicitly noted that the inspection procedures of PwC’s foreign affiliates “were limited to a review of evidence of the supervision and control” (Release No. 104-2004-005, p. 13). This lack of control is a tremendous threat to the current oligopolistic structure of the U.S.-led global audit firm networks. The U.S. regulators face the task of understanding how deeply a U.S. Big 4 auditor is involved in or collecting information on auditing failures committed by its non-U.S. affiliates. After the demise of Andersen, if another U.S. Big 4 audit firm fails, the global audit market will become even more concentrated. This raises doubts about whether current quality control in global audit networks is sufficient to maintain the reputation for high quality of the U.S. Big 4.

Third, while the media publicizes local audit scandals committed by affiliates of the U.S.-led global networks, 9 to the best of our knowledge, no study has analyzed the effect of a foreign local audit failure on the U.S. capital market. We present compelling evidence that shareholders are concerned about uniformity in quality provided by the global audit firm networks. 10 We exploit the unique Japanese setting to compare market perceptions of the quality premium. Our results are consistent with the notion that global audit networks create a high-quality premium that is directly associated with the reputation of the U.S. Big 4.

The remainder of this article is organized as follows. The second section provides a literature review and background. In the third section, hypotheses are developed. Data and Method are described in the fourth section. Empirical results are given in the fifth section and the final section concludes.

Literature Review and Background

Global Audit Firm Networks

Many countries require certified audit firms to be national firms. As large businesses expand their operations overseas, clients of major audit firms demand auditors to have expert knowledge about international operations. Global audit firm networks have developed the strategies to respond to such demands. Lenz and James (2007) define a strategic audit firm network as “a contractual cooperation between legally and economically autonomous audit firms, which are organized under . . . the strategic leadership of one or more member firms for the joint fulfillment of international clients’ needs” (p. 376). Detailed standards and rules concerning corporate laws create a natural barrier against entry by foreign accounting firms. Major U.S. audit firms strategically lead the development of global audit firm networks to circumvent such barriers to entry.

The major U.S. audit firms have employed this type of network to successfully expand their business worldwide and have developed a comparative advantage in international specialization (Lenz & James, 2007). To the extent that the U.S. Big 4 audit firms control the global market, the high level of market concentration is a serious issue to regulators (e.g., U.S. General Accounting Office), especially if a failure of one of their foreign affiliates jeopardizes their reputation. 11 Contemporary research overlooks the possibility that audit failure of local affiliates may negatively affect the reputations of U.S. audit firms. However, local audit failures are becoming more and more problematic as additional failures outside the United States are unveiled. For example, 4 out of 10 major accounting scandals reported by Bizcovering.com (“10 Major Accounting Scandals,” 2009) occurred outside the United States. The present study aims to fill this gap by examining the U.S. market reactions to an audit failure in Japan.

Japanese Corporate Governance Structure

Japan has a unique financial structure featuring main banks and cross-shareholdings between banks and debtor firms. Although the United States and Japan have large equity markets, Japanese firms traditionally maintained close relationships with their main banks, which created relationship-based oversight systems. As a result, auditors played a minor role in Japanese corporate governance (Ali & Hwang, 2000). The close connections between companies and their main banks produced overly friendly relationships between Japanese auditors and their clients (Konishi, 2010; Takahashi, 2006) and weakened auditor independence (Matsumoto, 1999). 12 Banking failures in the late 1990s resulted in calls for an industrial reform that led to increased merger activities, enactment of the Civil Rehabilitation Law, and decreases in cross-shareholdings between banks and firms. While these reforms reduced the monitoring role of main banks, it increased the importance of independent auditors in providing attestation services and monitoring financial reporting practices. Sophisticated foreign investors have also been demanding Japanese auditors be more independent of their clients (Ahmadjian & Robbins, 2005; Herrmann, Inoue, & Thomas, 2007). 13

According to inspections conducted by the Japanese Certified Public Accountant and Auditing Oversight Board (CPAAOB) in 2006, audit quality was not satisfactory for any of the Japanese Big 4. 14 As a result, the Board required all Big 4 audit firms to submit an improvement plan to the Commissioner of the Financial Services Agency (FSA), suggesting that the quality differential among the Japanese Big 4 is very small. 15

Following the Kanebo’s scandal in 2004, Japanese regulators also took the unprecedented step of suspending ChuoAoyama’s operations for 2 months. Such an action shows the determination of the regulators to improve audit quality, and send a bold signal to markets. Numata and Takeda (2010) find that ChuoAoyama’s audit scandal involving Kanebo, a large cosmetics company, had a significant negative impact on stock prices of not only its own clients but also those of the other Big 4 auditors. 16 Their finding supports the notion that Japanese market participants recognize the importance of high-quality auditing and react negatively to the audit failure.

History of the Affiliation Relationship Between Japanese and U.S. Auditors

Japan is a good example of a nation with high protective barriers against foreign companies to enter. First, Japanese law prohibits the direct engagement of foreign audit firms, and second, the country has unique language and culture that create a steep barrier for foreign audit firms to operate. Accordingly, affiliation with Japanese firms has been a strategic tool for major U.S. audit firms to expand operations in the country since 1949. 17 Although U.S. Big 8 auditors were not allowed to operate directly in Japan for several years, four of them established legal entities in the 1980s under the condition that they did not use their brand name. 18

The wave of mergers among the U.S. Big 8 auditors from 1989 to 1990 led to reorganization among the affiliated Japanese auditors. 19 By 1993, all of the U.S. Big 6 auditors except for Pricewaterhouse had chosen affiliations with Japanese auditors. As the restructuring of the U.S. auditing market continued, member firms in Japan also reorganized their business through mergers. 20 By the period of the Andersen scandal from 2001 to 2002, Arthur Andersen was affiliated with Asahi; PwC, with ChuoAoyama; Ernst & Young and KPMG, with ShinNihon; and Deloitte Touche Tohmatsu, with Tohmatsu. Asahi ceased affiliation with Andersen in April 2003 after the conviction of Andersen. 21

During the period of the Kanebo/ChuoAoyama scandal between 2004 and 2006, PwC was affiliated with ChuoAoyama; KPMG, with AZSA; Ernst & Young, with ShinNihon; and Deloitte Touche Tohmatsu, with Tohmatsu. After the Kanebo’s audit scandal, PwC established Aarata with 900 accountants in June 2006. The remaining accountants of ChuoAoyama continued their operations, changing their name to Misuzu. Appendix A provides a detailed summary of the history of affiliation in which a solid line indicates a merger and a small dotted line indicates an affiliation.

The practice of using a Japanese name began to change around the end of the century.

22

The Japanese–English combined names (ChuoAoyama PwC, Ernst & Young ShinNihon LLC, KPMG AZSA, and Deloitte Touche Tohmatsu CPA Ltd.) began to appear more often, especially in English newspapers and other publications. For example, The Japan Times reports,

The sources alleged that the accountants at ChuoAoyamaPricewaterhouseCoopers worked with two executives in producing consolidated financial statements that concealed a 81.9 billion yen capital deficit in fiscal 2001 and a 80.6 billion yen deficit the following year. (“Accountants Face Kanebo Fraud Charge,” 2005)

23

Reputation Damage Spillover Effect in an International Setting

So far, we have discussed a potential risk involved in the U.S.-led global audit firm networks, a recent change of auditors’ role in Japanese markets, and Japanese audit markets. In this section, we will discuss how the issues addressed in the three preceding sections help us to classify the risks involved in global audit firm networks.

The first is the risk faced by non-U.S. audit firms from joining global audit firm networks. Japanese member firms pay significant contract fees to their U.S. affiliates. 24 If a scandal by the lead U.S. auditor reduces stock prices of the clients of Japanese partners, this is an additional cost for them to consider.

Cahan et al. (2009) provide compelling evidence that the effect of Andersen’s audit failure spilled over to non-U.S. clients of Andersen’s affiliates. Hecker et al. (2006) analyze the effect of Andersen’s audit failure on the clients of its partner, and the German affiliates of other U.S. Big 4 auditors, and find that these German firms suffered a loss of equity value due to the scandal in the United States. This is clear evidence of a reputation damage spillover where the effect of an audit failure committed by a central audit firm spills over to the clients of non-U.S. affiliated auditors.

The second type of risk is associated with the central U.S. audit firms expanding their global networks. An audit failure committed by a local member of a global audit network can negatively affect stock prices of the clients of the lead U.S. Big 4. Recently, several audit failures in global networks were publicized in the news media. Does a reputation damage spillover to clients of the U.S. auditors? This has never been investigated. ChuoAoyama’s audit failure provides a powerful setting to analyze reputation damage spillover effects on the American clients of not only PwC but also on those of the other U.S. Big 4 firms.

Immediately after ChuoAoyama’s audit failure, the management of PwC took quick and aggressive actions to ameliorate the effect of the scandal on their reputation. By the end of 2005, Samuel DiPiazza (the head of the PwC’s International Division) secretly visited Japan several times, met with ChuoAoyama executives, negotiated restructuring operations, and spearheaded the establishment of a new affiliated audit firm (Tanemura, 2007). He repeatedly expressed concern about the effect of the damage to PwC’s reputation, which is echoed by multinational corporations that employed ChuoAoyama PwC as their auditor. 25 They sought ways to distance themselves from the ChuoAoyama problem (Tanemura, 2007). These reactions suggest that the management teams of PwC and multinational corporations believe that a local audit failure can jeopardize their reputation (Skinner & Srinivasan, 2012). Because there is almost no litigation risk in Japan, these reactions are also consistent with the claim made by Datar and Alles (1999) that auditors have strong incentives to maintain their reputations for diligence even in a non-litigious environment.

Moreover, the inspection report issued by the Japanese CPAAOB (2006) was a warning signal to all four of the global audit networks. These networks, centered around the U.S. Big 4, have similar advantages in technology, international expertise, and economies of scale as described by Carson (2009). However, it is unclear to what extent the U.S. Big 4 audit firms enforce professional standards established by the U.S. PCAOB on local members of their networks.

The report issued by PCAOB (2004) suggests that the U.S. Big 4 might not clearly understand their supervisory role in audits of their affiliates’ clients outside of the United States. The report explicitly noted that the inspection procedures of PwC’s foreign affiliates’ audit work “were limited to a review of evidence of the supervision and control” (PCAOB, 2004, Release No. 104-2004-005, p. 13).

The PCAOB may not realize the difficulty of enforcing the U.S. PCAOB standards and the Securities and Exchange Commission (SEC) independence rules in audits in foreign countries. The application requirement is especially unclear for clients that are not listed on U.S. stock exchanges. 26 But if there is a common reputation for high quality among the U.S.-led Big 4 global networks, an audit failure by a local foreign affiliate could damage the reputations of all of the networks.

Hypotheses Development

We summarize the above discussion of prior studies and our contribution in a two-by-two matrix in Figure 1. Our major contribution on the effect of reputation damage spillovers lies in the Northeast quadrant of this matrix. We develop two hypotheses about the risk for U.S. Big 4 to expand global audit firm networks. Our third hypothesis concerns the relative perception of assurance value of auditing by focusing on Japanese markets. This will connect the Southwest and Southeast quadrants by comparing market perceptions of the assurance value of the U.S. versus the Japanese Big 4. Below, we formally develop these three hypotheses.

Prior studies and our contribution.

First, we address the question of whether the failure of a local Japanese affiliate affects the American clients of PwC (the central auditor in the global network). Assurance value arises from auditors’ ability to use their professional knowledge and judgment to assure the adherence of their clients to financial reporting standards. Because outsiders do not have access to the same information as managers, third-party attestation is vital to assure the quality of financial information for investors (Antle, 1984). In addition, investors are unsure about the quality of audited financial statements both when they acquire them and after they use these statements to make financial decisions. Accordingly, the quality of services provided by auditors is similar to “credence” goods, as described by Emons (1997), and is distinct from experience goods. As a consequence, the value of audits is driven by perceptions of audit quality, and these perceptions are affected when audit failure becomes public knowledge. Empirical research supports this notion of auditing value. Teoh and Wong (1993) find that the responses on the coefficient on earnings is larger for high-quality audit firms than for low-quality auditors, suggesting that perceived auditing quality is reflected in stock prices. 27 When auditors fail to deliver the perceived quality of services, this credibility impairment should introduce uncertainty regarding financial statements resulting in a drop in security prices. In turn, the inability to deliver market value to their clients results either in a loss of clients or a downward pressure on audit fees.

Chaney and Philipich (2002) provide evidence to support this notion. They show that Andersen’s clients suffered negative stock market reactions around events associated with the audit failures. Cahan et al. (2009) find a significantly negative impact over two events for Andersen’s non-U.S. clients in 38 countries. Nelson, Price, and Rountree (2008) suggest that such results must be interpreted with caution because of the effect of confounding factors on stock prices. However, the evidence documented in prior studies generally supports the notion that auditing adds value to firms’ financial statements. Thus, estimating this negative effect on stock prices is one way to assess the value of reputation losses.

The success of global audit firm networks enhances the ability of all members to retain their worldwide reputations for internally generated knowledge and specialization (Carson, 2009). However, if a local network auditor fails to maintain high-quality standards, the credibility impairment of this firm can threaten the reputation of all of the affiliates, even the central U.S. audit firms. Numata and Takeda (2010) report a significantly negative impact of ChuoAoyama’s audit failure on its Japanese clients. ChuoAoyama had audited a number of large Japanese firms involved in prominent accounting frauds, such as Yaohan Japan Corp. (1997) and Yamaichi Securities (1999). Although the Kanebo scandals and ChuoAoyama’s involvement may not have been extensively publicized in the United States, at the time of the incident ChuoAoyama was widely known as ChuoAoyama PwC. Therefore, sophisticated international investors would have known about the audit failure and PwC’s connection.

Carson (2009) and Lenz and James (2007) suggest that global audit firm networks create economic value through their operational structure. Networks help to cultivate a brand image for their international expertise. Thus, the failure of a local affiliate could damage the image of a central auditor’s quality reputation. 28

Accordingly, our first hypothesis is as follows (in alternative form):

In the above hypothesis, we try to access a downward revision of U.S. investors’ perceptions of quality of PwC auditing.

In response to the Kanebo scandal, the management of PwC took quick actions to preserve their reputation. Their speedy response is consistent with the notion that fear of losing large clients creates incentives for auditors to react to events that threaten their reputation (DeAngelo, 1981). Watts and Zimmerman (1986) suggest that large firms are more sensitive to political costs than smaller firms. Simunic and Stein (1996) show that audit firms that face greater penalties from audit failure increase their efforts to reduce litigation risk. But PwC had a low-litigation risk in this case. Hence, their reactions to ChuoAoyama’s audit failure probably represent a “defensive action” against loss of reputation rather than litigation and seem to demonstrate the notion discussed by Datar and Alles (1999) that auditors have strong incentives to maintain their reputation for high quality even without a litigation threat.

We separately analyze the effect of ChuoAoyama’s credibility impairment on the American clients of the other U.S. Big 4. ChuoAoyama’s audit failure is an isolated example of a local firm’s audit failure. But this type of credibility impairment could happen in any global audit firm network. The CPAAOB issued a general recommendation to improve the quality of auditing to all of the Japanese Big 4 affiliates of global audit networks in 2006. According to this recommendation, the Board did not distinguish between ChuoAoyama PwC and the other three, and found that all Japanese Big 4 firms had insufficient quality control (AccountingWEB, 2006). None of the U.S. Big 4 was transparent about quality control systems for local members of their international networks. Therefore, we will test whether ChuoAoyama’s scandal weakened the general reputation for perceived quality across all of network firms.

Investors might have lost confidence in the ability of all global audit networks to maintain uniformity of high-quality standards among their international affiliates. DeAngelo (1981) suggests that a large client portfolio serves as collateral against poor audit quality. However, if the negative impact of audit failures spills over across countries, this may raise costs of expanding global audit networks. Barton (2005) reports that most of Andersen’s previous clients, especially those concerned about their visibility in the capital markets, switched to the other Big 4 auditors, although Doogar et al. (2007) report that clients of the other Big 4 also suffered significant losses in equity value. It seems that the drop in security price was not economically significant enough for Andersen’s clients to avoid the other Big 4 firms as their auditor. These findings support the notion that the strategy of forming global audit networks establishes a comparative advantage that creates international reputation for these networks, which small local audit firms cannot supply. Therefore, it is useful for all U.S. global network firms to understand the spillover effect that can result from audit failure at their foreign affiliates.

Our second hypothesis is as follows (in alternative form):

In the above hypothesis, we assess a downward revision of the perception of the general level of audit quality common across all of the U.S. Big 4 auditors.

In our third hypothesis, we attempt to assess the relative magnitudes of the contributions of the U.S. Big 4 and their local affiliates to the networks’ reputations. The strong investor protections and litigation threats in the United States establish a belief that the quality of the U.S. audit firms is superior to those in other countries (Francis & Wang, 2008). If the U.S. Big 4 audit firms have a worldwide reputation for high quality, then the U.S.-led global audit firm networks should also have the perception of superior quality in Japan. 29

Because Japanese law prohibits the direct engagement with the U.S. audit firms in the country, Japanese firms can purchase high-quality U.S. audit services only indirectly through Japanese affiliates of the global audit networks. There is presumably an equity premium associated with hiring Japanese Big 4 as opposed to non-Big 4 auditors in Japan. 30 But what part of this premium is associated with the Japanese auditors’ network relationship with U.S. Big 4 firms?

If one of the Japanese Big 4 firms is not affiliated with a U.S. Big 4, we can utilize such a firm to estimate marginal value of an affiliation. Unfortunately, however, there is little variation in the sample to allow us to separate the premiums associated with a Japanese Big 4 auditor and those associated with the network affiliation with the U.S. Big 4 firm. All of the Japanese Big 4 audit firms are affiliated with a U.S. Big 4 firm.

Given this situation, we decide to assess the quality premium associated with two audit failures, by comparing the magnitude of negative effects of the Andersen and ChuoAoyama scandals on stock prices of Japanese clients. Enron and Kanebo are large well-known corporations. In both cases, management teams inflated their profits more than US$1 billion. 31 Accordingly, we assume that their frauds are comparative in nature.

There are three alternative conjectures to explain the relative magnitudes of the quality premiums as inferred from stock price changes. First, if the changes in the perceived quality of financial statements are of roughly equal magnitude, irrespective of the direction of the affiliation, these two audit failures (ChuoAoyama and Andersen) should have a similar effect on the share prices of their clients. In this case, we expect that the clients of ChuoAoyama and those of Asahi (the Japanese affiliate of Andersen) should have experienced the similar negative effects. Second, if investor perceptions are affected more by the visibility of the audit failure, Andersen’s scandal should probably have less impact in Japan than that of ChuoAoyama. ChuoAoyama was more visible than Andersen in Japanese markets. ChuoAoyama’s audit scandal occurred 2 years after Andersen’s when Japanese regulators were aggressively engaged in industrial reforms to enhance the corporate monitoring system. Such scrutiny probably influenced market reactions to ChuoAoyama’ s audit failure. In this case, we expect the negative magnitude of the market reactions to ChuoAoyama’s audit failure to be larger than that of Andersen. Third, if the perceptions of quality are derived from the affiliation of the Japanese Big 4 auditors with the U.S. Big 4 audit firms, the Japanese Big 4 firms increase the market value of their audits by the affiliation, and, therefore, we expect that the drop in the stock price associated with the failure of Andersen to be larger than that of ChuoAoyama.

It is difficult to separate the insurance and assurance values of auditing in U.S. markets. But Japanese capital markets provide an ideal setting to assess the difference in the assurance values associated with the two scandals. Both auditors have been involved with a number of smaller auditing failures in the years leading up to their major scandals. By focusing on Japanese markets, we can control for environmental (e.g., regulations, laws, litigation, and domestic economic events) and cultural (e.g., people’s perception about litigation, property right, and their preferred methods of resolutions to these issues) factors. 32

The U.S. Big 4 audit firms have established a reputation for quality. It is interesting to know whether such a reputation premium is shared by foreign affiliates. Thus, we develop our last hypothesis based on the third alternative conjecture as follows (in alternative form):

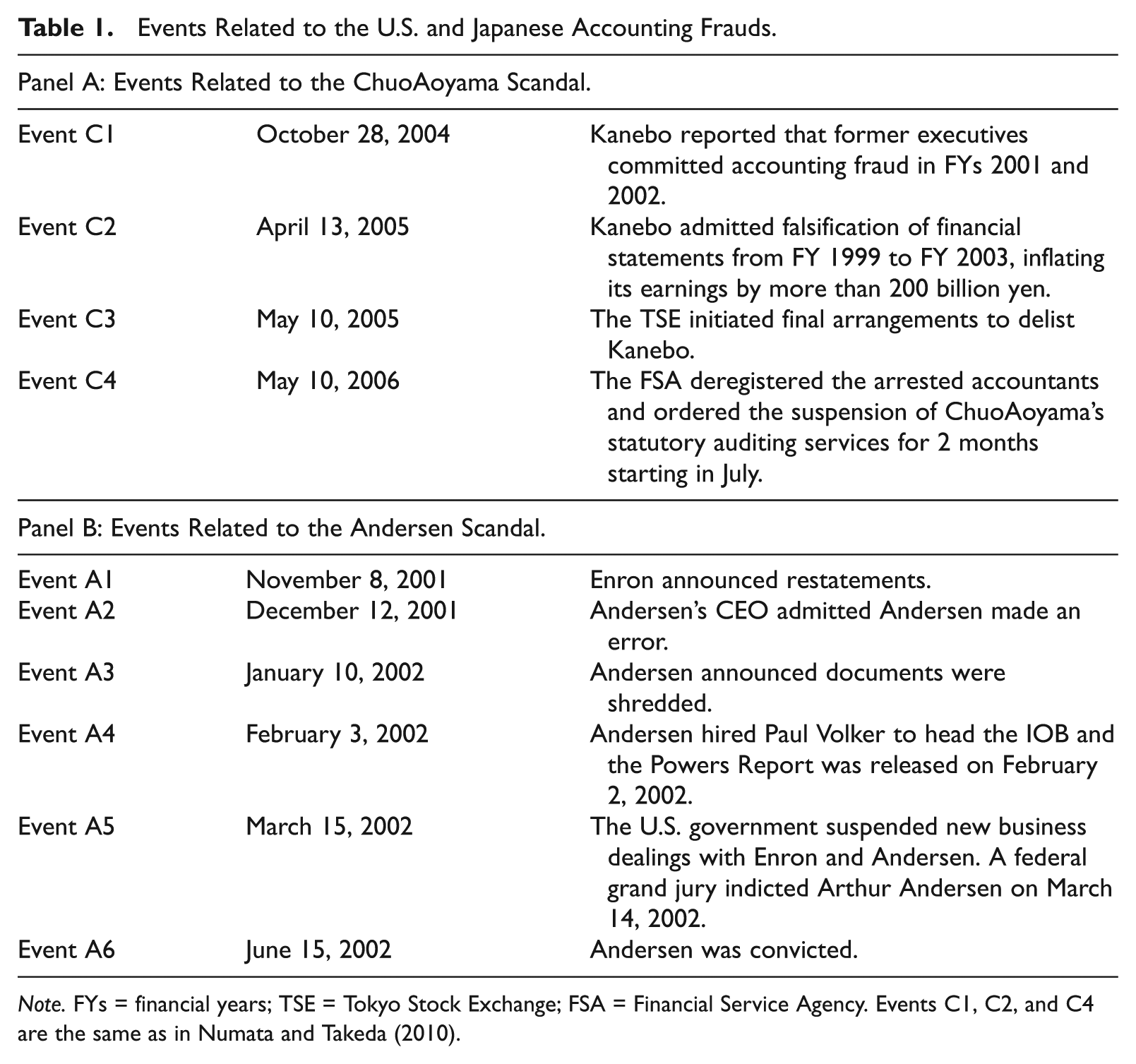

As shown in Panel A of Table 1, we select four events related to the Kanebo/ChuoAoyama scandals that are shown to have caused significantly negative reactions in the Japanese market (Numata & Takeda, 2010). 33 Events C1 and C2 correspond to the disclosure of accounting fraud committed by Kanebo. Event C3 is the punishment of Kanebo. Event C4 is the punishment of Kanebo’s auditor, ChuoAoyama. These events are spread over a relatively longtime period (3 years), which makes it well suited to observe the effect of PwC’s efforts to moderate the reputation damage to its clients’ stock prices.

Events Related to the U.S. and Japanese Accounting Frauds.

Note. FYs = financial years; TSE = Tokyo Stock Exchange; FSA = Financial Service Agency. Events C1, C2, and C4 are the same as in Numata and Takeda (2010).

We also select six events related to Andersen’s scandal to test H3 as shown in Panel B of Table 1. Events A1 to A4 are centered around the disclosure of the Andersen scandals, which directly damaged their reputation. Prior studies on U.S. firms show that Andersen’s auditing failure negatively affected their clients’ security prices (Chaney & Philipich, 2002; Krishnamurthy et al., 2006). Event A5 is the criminal indictment of Andersen, which we perceive to be the punishment by the government and judiciary system against Andersen. Event A6 is when a federal jury convicted Andersen for obstructing justice, which made it impossible for them to continue to provide auditing service.

Method and Data

Event Study Method

We use a standard event study methodology, based on MacKinlay (1997), to evaluate the effects of the reputation loss of auditors on the stock prices of clients of the Big 4 auditors in the United States and Japan. This methodology assumes an efficient market in which current stock prices reflect all publicly available information and are changed only by unexpected events that affect the future profitability of a firm. Denoting the event day as t0, the initial date of the event window as t1, and the final date of the event window as t2, we select four event windows, (t1,t2) = (0,1), (0,2), (0,3), and (−1,3), to ensure robustness. The estimation window is set at 150 transaction days before the event window of the first event: March 24, 2004, to October 26, 2004, for ChuoAoyama. To test H3, we also select April 3, 2001, to November 6, 2001, for Andersen.

The following market model is then estimated during the estimation window for each event:

where

and

in which

By using the parameters from the estimation period, we estimate an abnormal return for the stock of firm i during the event window period t as

CAR is then obtained by summing up the abnormal returns over the event window:

If the event does not affect stock prices, the CAR should be zero. In other words, the null hypothesis H0 stipulates that CAR = 0 should be rejected statistically if the event influences stock prices. To test the null hypothesis, we employ the following J statistic:

in which

We try to separate an audit-firm-specific factor from a factor common to all global network firms. However, there is no clear proxy to capture the incremental value of international expertise that is shared by all global network firms. Some might argue that our approach is not sufficient enough to state a strong conclusion. However, Carson (2009) suggests that industry specialization in global audit firm networks generates incremental value. If we find a negative effect on the clients of all other global network firms, our result is consistent with the notion that there is a general global network-wide level of reputation.

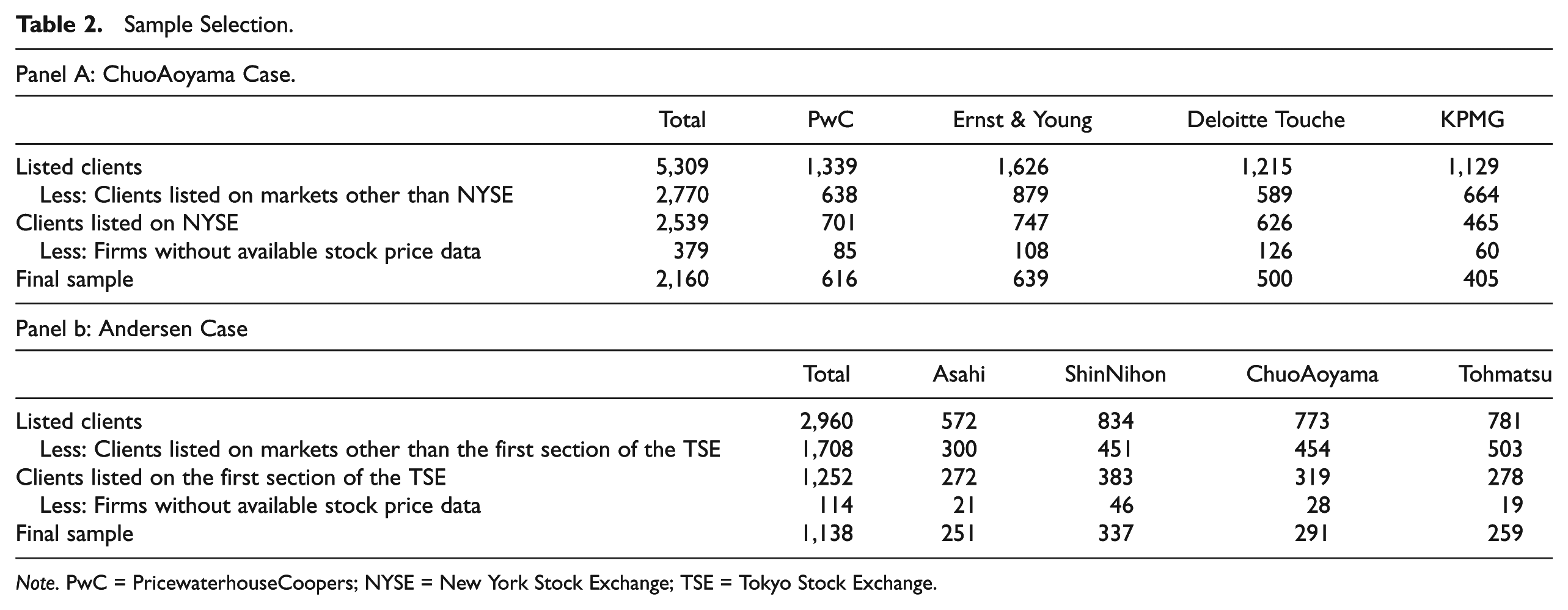

Sample Selection

Table 2 presents the sample selection process for the ChuoAoyama and Andersen cases. Japanese stock prices were obtained from the Kabuka CD-ROM (Stock Price Database), published by Toyo Keizai. We first make a list of the clients of Asahi and the other Japanese local audit network firms, ShinNihon, ChuoAoyama, and Tohmatsu, based on the Kaisha Shikiho CD-ROM (Japan Company Handbook). We limit our sample to firms listed on the first section of the Tokyo Stock Exchange (TSE) because stocks on other Japanese markets are less actively traded, and hence, combining shares listed on other markets potentially distorts the results. The initial sample consists of 2,960 listed observations, of which 1,708 firms were listed in the first section of the TSE. We then eliminate the firms without complete stock price data for both the estimation and event windows. This process yields 1,138 firms with available data. The final sample consists of 251 Asahi clients, 337 ShinNihon clients, 291 ChuoAoyama clients, and 259 Tohmatsu clients.

Sample Selection.

Note. PwC = PricewaterhouseCoopers; NYSE = New York Stock Exchange; TSE = Tokyo Stock Exchange.

We use three data sets to identify the clients of large U.S. global audit network firms (PwC, Ernst & Young, Deloitte Touche, and KPMG). We first use the 2005 Audit Analytic data to identify the audit clients. 34 Because there is no direct firm identifier that can link the Center for Research in Security Prices (CRSP) and Audit Analytic data sets, we use COMPUSTAT as a link between the two. We employ cik as the key identifier to connect auditing fees to COMPUSTAT and then use the eight-digit cusip to connect the COMPUSTAT and CRSP data sets.

Because we wish to investigate capital market reactions in a similar trading environment, we also focus on firms listed only on New York Stock Exchange (NYSE) for the analysis of security prices in the U.S. markets. The initial sample consists of 5,309 listed firms with matched CRSP and auditing fee data, of which 2,529 are listed on NYSE. We then eliminate the firms with insufficient stock prices, resulting in a total of 2,160 firms. This final sample consists of 616 PwC clients, 639 Ernst & Young clients, 500 Deloitte Touche clients, and 405 KPMG clients. The above information is shown in Panels A and B of Table 2.

Descriptive statistics on stock returns during the estimation window are presented in Table 3. The average stock returns between April 3, 2001, and November 6, 2001, for TOPIX and between March 24, 2004, and October 26, 2004, for DJIA are negative. The median stock returns for the clients of Asahi and other Japanese local network firms are essentially zero and for those of PwC and other U.S. central network firms, they are positive but small. Volatility (standard deviation) is higher for the Japanese market than for the U.S. market.

Descriptive Statistics of Stock Returns During the Estimation Window (%).

Note. TOPIX = Tokyo Stock Price Index; DJIA = Dow Jones Industrial Average; PwC = PricewaterhouseCoopers.

Empirical Results

Spillover Effect of the ChuoAoyama Scandal on U.S. Clients (H1 and H2)

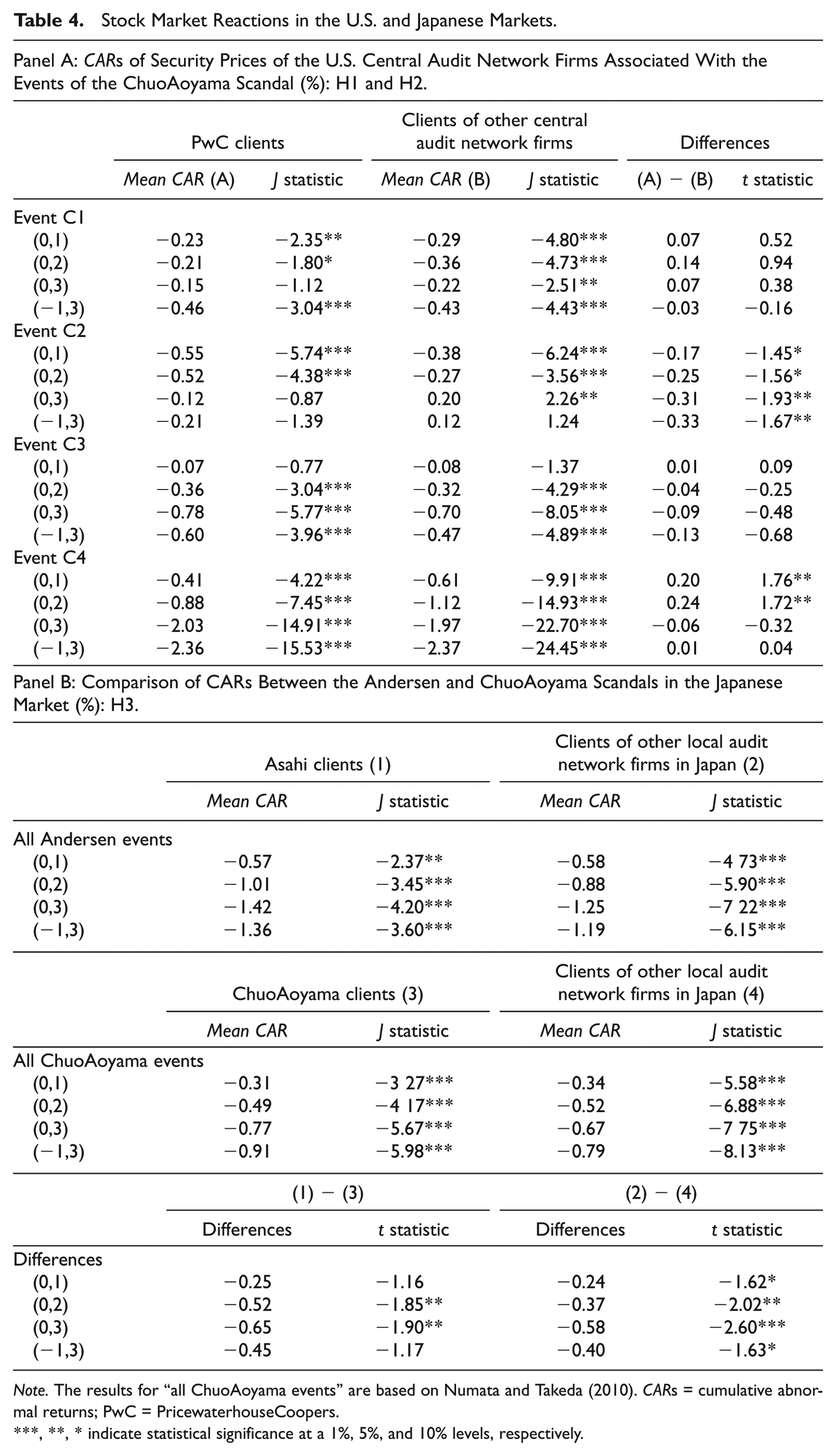

The results for our tests of H1 and H2 are presented in Panel A of Table 4, which shows the CARs for four event windows centered on important dates of the ChuoAoyama’s scandal. The first column is for the U.S. clients of PwC, the second column is for the clients of the other U.S. Big 4 global audit network firms, and the third column is a test for the difference in stock reactions between these two sets of clients.

Stock Market Reactions in the U.S. and Japanese Markets.

Note. The results for “all ChuoAoyama events” are based on Numata and Takeda (2010). CARs = cumulative abnormal returns; PwC = PricewaterhouseCoopers.

, **, * indicate statistical significance at a 1%, 5%, and 10% levels, respectively.

We find that market reactions to ChuoAoyama’s audit failure were negative. CARs for the clients of PwC (shown in the first column) are significantly negative for three out of four event windows for Event C1, namely, the 2-day (0,1), 3-day (0,2), and 5-day (−1,3) windows, at the 5%, 10%, and 1% levels, respectively. CARs for Event C2 exhibits significantly negative market reactions at the 1% level for two out of four event windows, and these for Event C3 exhibit significantly negative market reactions at the 1% level for three out of four event windows. All four windows for Event C4 exhibit significantly negative market reactions at the 1% level.

Moreover, for the clients of the other Big 4 global audit network firms (shown in the second column), all CARs are significantly negative at the 1% level for Event C1, except for the 4-day (0,3) window, in which CAR is significantly negative at the 5% level. CARs for Event C2 exhibit a significantly negative market reaction for three out of four event windows at the 1% level, except for the 4-day (0,3) window, in which they are significantly negative at the 5% level. CARs for Event C3 show a significantly negative market reaction at the 1% level for three out of four event windows, and for Event C4, the CARs for all four windows are significantly negative at the 1% level.

The last column shows that the comparison of CARs between the clients of PwC and those of the other U.S. Big 4 global audit firms. There is no significant difference between these two groups for Events C1 and C3. But for Event C2, the negative reaction is larger for the clients of PwC. Furthermore, for Event C4 (which occurred a year later on May 10, 2006), we find the negative reaction is smaller for the clients of PwC than that for the clients of the other Big 4 for two windows at the 5% significance level (in the last column of Panel A of Table 4).

We think that our results for Event C4 might reflect PwC’s quick response to mitigate the effect of the ChuoAoyama scandal on their clients’ stock prices. 35 As discussed in the previous section, the management team at PwC was actively engaging in ChuoAoyama’s restructuring activities although this was a sensitive issue for PwC because there is a conflict within ChuoAoyama. 36 In June 2006, the management of PwC announced the establishment of Aarata to try to ensure the quality of their services. 37 In their public announcement, they stressed that “the name ‘Aarata’ that signifies ‘new and fresh’ was chosen to reflect the new perspective that PwC Aarata would bring to the Japanese audit market” (PwC, 2006). Skinner and Srinivasan (2012) also provide a lengthy discussion of the steps taken by PwC arising from their concern about the effect of ChuoAoyama’s poor quality on their reputation. All of these activities demonstrate the vigorous steps taken by PwC to confront the potential damage to their reputation caused by ChuoAoyama’s audit failures.

In summary, these results show that the effects of audit scandals committed by local foreign audit firms spillover not only to the clients of the particular U.S. affiliate but also to those of all of the other U.S. Big 4. Our results are robust across all four events. Event C1 corresponds to the discovery of Kanebo’s fraudulent statements, and Event C2 to the admission of the fraud. While the market reactions to these two events are negative, those to Events C3 and C4, which are related to the punishment of ChuoAoyama over 1 year later, are much stronger. This might suggest that it took some time for U.S. investors to understand the implications of the audit failure of a foreign affiliate to the reputation for high quality of all of the global audit firm networks. These results clearly indicate the undesirable reputation risks for the central U.S. audit firms when expanding their global networks. There is also potential evidence that PwC’s risk management efforts may have helped to reduce the effect of ChuoAoyama’s audit failure on security prices of its clients near the end of the period of the scandal.

The Effect of Andersen Versus That of ChuoAoyama in Japan

So far, our analysis on international spillover effects shows that an audit failure by a local affiliate can spillover to the clients of the central (U.S.) global audit firms. As auditors in the United States face litigation risk, American stock prices reflect both insurance and assurance values of auditing. In contrast, a study of the Japanese market allows us to focus on the assurance value. Thus, we analyze whether the U.S. Big 4 audit firms create a reputation premium beyond the common level of the Japanese Big 4 by comparing Japanese market reactions with the auditing scandals by Andersen and ChuoAoyama.

To test this hypothesis, we first select six events related to Andersen’s scandal as shown in Panel B of Table 1. We calculate CARs for four event windows for both the clients of Asahi, which was the Japanese affiliate of Andersen, and those of the other Japanese Big 4 local audit network firms, ShinNihon, ChuoAoyama, and Tohmatsu. We report these results on Appendix B.

Because our objective is to test the market perception of assurance value, we aggregate the magnitude of stock price reactions over all events and calculate an arithmetic mean of CARs for each window, dividing by five. 38 For example, for the 2-day window (0,1), we calculate an arithmetic mean of CARs for five events (excluding Event 5) reported for Andersen’s results in Appendix C. We also aggregate the event study results reported by Numata and Takeda (2010) for ChuoAoyama’s incidents for all four windows and calculate an arithmetic mean. We then compare the magnitude of the negative impacts on clients of Asahi (Andersen’s affiliate) and those of ChuoAoyama to assess market perceptions of quality differential to test H3.

These results are reported in the first column of Panel B of Table 4. The first row is the aggregated results for the clients of Asahi for four windows, and the second row is those for the clients of ChuoAoyama. The last row of this column reports the test of the difference between the above two groups. The CARs are more negative for the clients of Asahi than those for ChuoAoyama for the 3-day (0,2) and 4-day (0,3) windows at the 5% level. For example, for the CAR for the 4-day window, the effect of the Andersen scandal is on average −1.42%, while that for the ChuoAoyama scandal is on average −0.77%. The difference, −0.65%, is statistically significant at the 5% level.

The second column presents the results for the other local audit network firms. Similarly, the first row shows the effect of the Andersen scandal, the second row shows the effect of the ChuoAoyama events, and the last row shows the comparison. The negative stock price reactions arising from Andersen’s audit failure are significantly larger than those arising from ChuoAoyama’s, at the significance levels of 10%, 5%, 1%, and 10% for the 2-day (0,1), 3-day (0,2), 4-day (0,3), and 5-day (−1,3) windows, respectively. For the 4-day window, the effect of the Andersen scandal is on average −1.25%, while the effect of the ChuoAoyama scandal is on average −0.67%, and the difference, −0.58%, is statistically significant at the 1% level. These results also show the statistically significant difference between the market reactions to Andersen’s scandal and ChuoAoyama’s.

In summary, our results suggest that an appreciable portion of the premium realized by Japanese auditors may be associated with an affiliation to the U.S. Big 4. The negative market reactions to Andersen’s audit failure are significantly larger than those to ChuoAoyama. Our interpretation of this result is that a credibility impairment of the U.S. Big 4 audit firms is probably more costly than that of Japanese Big 4 audit firms. Thus, although joining a global audit network may send a signal of high quality, this cost should be an important consideration for a local Japanese audit firm. However, it is difficult to reach a strong conclusion that the observed larger magnitude of the negative impact on the Andersen’s event is based solely on a higher premium associated with the high-quality reputation of the U.S. Big 4 shared by the Japanese affiliates. Andersen’s indictment created a worldwide shock to markets, and its later conviction resulted in the demise of the firm. ChuoAoyama’s audit failure resulted in suspension of their operation for only 2 months. Based on this difference, some might argue that the impact of the Andersen scandal was greater than that of ChuoAoyama. However, Andersen’s indictment was subsequently overturned, and ChuoAoyama’s suspension ultimately resulted in total reorganization of the firms into two new entities, Misuzu and Aarata. Thus, we think that both incidents are cases where the demise or the breakup reduced investors’ perceptions of the quality of audits.

Sensitivity Analysis Based on Medians

We also conduct the same analysis using the median CARs and report the results in Panel A of Table 5. The effects of the Kanebo/ChuoAoyama scandal on the clients of the central audit network firms in the United States are much weaker. Although none of the four windows for Event C1 are significant for the clients of PwC, at least one of the four windows for Events C2 and C3 exhibits significant negative reactions for the clients of PwC. The magnitude of the negative reactions is larger for the clients of PwC than for those of the other Big 4 audit firms. CARs for all four windows of Event C4 are significantly negative. But in this case, there is no discernible difference between the clients of PwC and those of the other central audit network firms. Thus, although the results are weaker in the analysis of the medians, the tenor of the findings is similar to the earlier results. 39

Sensitivity Analyses on Stock Market Reactions in the U.S. and Japanese Markets.

Note. CARs = cumulative abnormal returns; PwC = PricewaterhouseCoopers; DJIA = Dow Jones Industrial Average.

, **, * indicate statistical significance at a 1%, 5%, and 10% levels, respectively.

An Alternative Sensitivity Analysis Based on a Portfolio Approach

In this section, we consider an alternative event study methodology. In a simple event study methodology where the abnormal returns of individual stocks are aggregated may cause a clustering problem in evaluating the market-wide effect. That is, the cross-sectional dependence among abnormal returns can generate bias in the test results. To avoid this potential bias, we estimate the following model based on a portfolio approach:

where Rpt is the return on day t to an equally weighted portfolio of clients of the U.S. Big 4 auditors. Djt is a dummy variable equal to one for the 3-day event window of Event

Panel B of Table 5 presents the regression results. The first column presents the result from the model that includes each event separately, and the second column reports the results for aggregating all events. Event C2 has a significantly negative coefficient at the 1% level, and Event C4 has a significantly negative coefficient at the 5% level. When all events are aggregated, the results are still significant at the 5% level. Thus, although the portfolio approach slightly reduces the number of significant events, the tenor of the results is consistent with the major findings.

Summary and Conclusion

Prior studies (Cahan et al., 2009; Hecker et al., 2006) provide compelling evidence that the negative effect of Andersen’s audit scandal spilled over to the clients of foreign affiliates of the U.S. Big 4 auditors. However, another concern for the U.S. global audit network firms is that an audit failure of a local foreign affiliate might damage their reputation. We analyze and provide evidence of reputation damage spillover.

In a study of audit fees, Carson (2009) concludes that there is no incremental value of being in a global audit network for the U.S. Big 4 auditors in the United States. However, in a competitive market, economic theory suggests that the variation in the audit fees across global audit network firms should be small, and hence, it might be difficult to find the incremental value of global audit firms in the United States using audit fee data. We take a different approach, and analyze the incremental value of global audit firm networks, by examining the effect of a highly publicized audit scandal committed by a local affiliate of PwC, ChuoAoyama, on the U.S. clients of global audit firm networks. The relationship between ChuoAoyama and PwC was widely publicized in the international news media at the time of ChuoAoyama’s audit failure. All of the U.S. Big 4 global network firms have affiliations with Japanese Big 4 auditors.

We find significant negative market reactions to ChuoAoyama’s audit failure across the U.S. clients of all Big 4 global firm networks. This result is consistent with the notion that there is a quality premium associated with the general characteristics of the global network firms that creates a network-wide reputation as opposed to a premium associated with an individual auditor. Our results show that an audit failure committed by a local foreign affiliate of one of the U.S. Big 4 can damage high-quality reputation accrued to global firm networks. This finding is an important reminder that there is reputation risk associated with expanding global audit networks.

PwC took very aggressive actions to preserve their reputation following the failure of ChuoAoyama. They were heavily involved in the creation of a new audit firm, Aarata, and sent a shrewd message to emphasize their initiative. More recently, they also vigorously denied their involvement in an accounting fraud committed by Satyam in India. 40 Our results provide a rational explanation for such forceful and swift reactions. The evidence suggests that market participants, clients, and regulators are concerned about uniformity in quality control over the local members of global audit networks. Our results potentially suggest that their efforts might have helped to reduce the negative effect of the ChuoAoyama scandal on their clients in the U.S. market.

As all these results indicate that the U.S.-led global audit firm networks have an enhanced reputation for international expertise, as a second issue, we analyze whether extra premiums accrue to the affiliates of the U.S. Big 4 in the Japanese market. We focus on two comparative auditing scandals, by Andersen and ChuoAoyama, to assess the premiums associated with the affiliation.

Our comparison of reputation losses suggests that clients of Japanese auditors seem to derive a notable equity premium from their affiliations with U.S. Big 4 audit firms. We find that the clients’ share price declines resulting from Andersen’s scandals are 0.25% to 0.65% higher than those associated with ChuoAoyama’s. This premium loss is likely to be costly for Japanese affiliates when the U.S. Big 4 audit firms fail to maintain their reputation for the highest quality. Thus, there may be hidden risk for the Japanese Big 4 to join global audit networks.

Our conclusion is subject to the following caveat. Because we compare two high-profile audit failures in two different time periods (2002 for Andersen and 2004 for ChuoAoyama), we may not be able to control for all of environmental differences. For example, given the increasing demand for high-quality auditing in Japan, all other factors held constant, some might expect more negative market reactions to ChuoAoyama’s audit failures than to Andersen’s. However, we find that the negative market reactions among Japanese clients to Andersen’s audit failure are equal to or larger than those associated with ChuoAoyama’s audit failure. In this sense, our results are consistent with the notion that economic losses from credibility impairment are greater for Andersen’s scandal than ChuoAoyama’s. We also note that while Andersen was convicted and liquidated, ChuoAoyama suspended its operation for only 2 months. It is possible that this difference in the scale of the punishment caused larger market reactions following Andersen’s audit failure than ChuoAoyama’s. 41

Our results suggest that that the effect of auditor reputation in equity markets is based on several factors including the position of the auditor in a global network. Investors may be more likely to impute systemic weaknesses as causing an audit failure for large internationally connected audit firms rather than for firms that operate in a homogeneous national environment. The documentation of how global audit networks affect investor perceptions has interesting implications for spillover effects associated with audit failures as well as the regulatory framework for viewing the globalization of financial service.

Footnotes

Appendix A

Appendix B

Appendix C

The Japan Times

Monday, September 12, 2005

PricewaterhouseCoopers unit’s CPAs tied to firm’s window-dressing.

Prosecutors are set to charge several certified public accountants at a Japan unit of the PricewaterhouseCoopers group with collaborating with executives at Kanebo Ltd. in an accounting fraud that has humbled the once premier cosmetics and textile company, according to investigative sources.

Financial Times (London, England)

Wednesday, September 14, 2005

Tokyo prosecutors yesterday arrested four accountants at a Japanese affiliate of

Prosecutors also raided

Though Kanebo was delisted from the Tokyo Stock Exchange earlier this year after admitting to accountancy fraud over a four-year period, the alleged complicity of

The Japan Times

Wednesday, September 14, 2005

Rare collar for cooking books taints auditing biz.

Four certified public accountants at a Japanese unit of the PricewaterhouseCoopers Group were arrested Tuesday for allegedly collaborating with former executives at Kanebo Ltd. to falsify accounting reports.

The special investigation department of the Tokyo District Public Prosecutor’s Office also searched the offices of ChuoAoyama PricewaterhouseCoopers in Chiyoda Ward, Tokyo, and the suspects’ homes jointly with the Securities and Exchange Surveillance Commission, prosecutors said.

(Provisional Translation)

Financial Services Agency (Government of Japan)

May 10, 2006

In relation to the audits on the financial documents prepared by Kanebo Ltd. (“Kanebo”), the Financial Services Agency (“FSA”) today ordered the following disciplinary actions against ChuoAoyama PricewaterhouseCoopers and three engagement partners of the firm. It should be noted that the FSA may possibly take further actions to other persons concerned as the ongoing investigation proceeds further.

The Japanese Institute of Certified Public Accountants

May 11, 2006

Yesterday, the Financial Services Agency (FSA) announced that it has decided to take administrative action on ChuoAoyama PricewaterhouseCoopers, by way of ordering it to suspend part of its business for two months between July and August 2006, and by ordering the revocation of certification, or one-year suspension, of the certified public accountants (CPAs) who were lead partners in connection with the alleged misstatement of Kanebo. The considerable impact of this case and of the administrative action on capital markets and all companies affected is much regretted. The Japanese Institute of Certified Public Accountants (JICPA) will make every effort to minimize the impact on capital markets. JICPA accept this administrative action with the utmost seriousness and we reaffirm our commitment to improve professional accountants’ services and heighten their awareness of the code of ethics by strengthening self-regulation in order to recover confidence in CPA audits quickly and respond to the expectation of the public.

Tsuguoki (Aki) Fujinuma (Chairman and President)

The Wall Street Journal (Eastern Edition). New York, NY:

May 12, 2006.

Analysts said the action by Japan’s financial regulator, the Financial Services Agency, was designed as a warning. “The obvious intent is to send a message,” said Scott Jones, a lawyer at the Tokyo office of Jones Day, “not just to accounting firms, but to the market, that things are going to get transparent.”

The FSA issued the sanction after finding that ChuoAoyama PwC accountants had certified fraudulent annual reports at cosmetics maker Kanebo Ltd. for at least five years. The investigation “revealed deficiencies in the operation of the firm, including the reviewing mechanism and educational programs, as well as the internal-control system,” the agency said. ChuoAoyama PwC “needs to make [the] utmost efforts to improve and reinforce its auditing work,” an FSA official told reporters (Copyright 2006 Kyodo News International, Inc.).

May 19 (Friday), 2006

ChuoAoyama PricewaterhouseCoopers has been ordered by the Ministry of finance to suspend operations for two months, beginning on July 1, 2006. Chuo Aoyama is one of Japan’s four largest accountancy organizations, carrying roughly 2,300 clients. Chuo Aoyama’s corporate clients fear that the two month suspension may open up a vacuum in auditing operations.

The corporate auditing process is transforming into one in which one year’s worth of monthly auditing operations are compiled and a business’ corporate activities over the past year are audited. A two-month vacuum in corporate auditing means that auditing operations will not be conducted as usual. From an investor’s point of view, it is difficult to place trust in auditing results that include such a blank period. Therefore, the measure handed down by the Ministry of Finance stands to upset the credibility of many of the companies who are clients of Chuo Aoyama, and will trigger major repercussions across Japan’s capital markets.

July 05, 2006

Japan’s Certified Public Accountants and Auditing Oversight Board (CPAAOB), a subsidiary of the Financial Services Agency (FSA) with independent investigatory power, asked the FSA on Friday to issue business improvement orders to Japan’s Big Four audit firms, Mainichi news reports. The firms are KPMG Azsa & Co, Ernst & Young ShinNihon, Deloitte Touche Tohmatsu and ChuoAoyama Pricewaterhousecoopers, which began a two-month suspension from auditing on July 1 because of its participation in a bookkeeping fraud at Kanebo Ltd., a cosmetics firm.

The CPAAOB had been conducting inspections at each of the firms since last fall and reported that it had found problems with management oversight, quality control and independence at all four. The Big Four affiliates are responsible for auditing 80 percent of listed firms in Japan, Reuters reports.

The recommendation that the FSA issue business improvement orders is the first punitive measure CPAAOB has taken since it was established in 2004.

Acknowledgements

We would like to thank anonymous referees, Richard A. Lord, Sophie Audousset-Coulier, Theodore Sougiannis, Francine McKenna, Mike Stein, Jong Park, and the conference and seminar participants for their helpful comments and suggestions. We would also like to give special thanks to Bharat Sarath, the editor, for his very helpful suggestions.

Author’ Note

An earlier version of this article was presented at the 2009 Canadian Academic Accounting Association Annual Conference, the 2011 American Accounting Association Annual Conference, the Todai-Yale Initiative Lecture Series at Yale University and Old Dominion University. All remaining errors are our own.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the travel fee for the presentation of this article: Fumiko Takeda gratefully acknowledges financial support from Murata Science Foundation.