Abstract

We study the organizational impact of internal control systems, by examining 1,593 firms with 15,606 executives over 2002-2010. We find that internal control systems explain a significant amount of executive and, in particular, CFO compensation, after controlling for other governance, executive personal characteristics, firm, and macroeconomic determinants of pay. Moreover, the negative relationship between pay and internal control systems suggests that executives operating in firms with ineffective internal control systems earn greater compensation. The results of the longitudinal analysis suggest that firms with ineffective internal control systems have greater agency problems and, consequently, greater levels of executive compensation. The CEO pay shows a nonsignificant relationship with internal control systems.

Keywords

Introduction

The internal control system (ICS), as regulated by the Sarbanes–Oxley Act (SOX) Sections §302 and §404, is considered an important mechanism in assuring the quality of corporate governance. It has been argued that it improves the monitoring actions of the independent audit committee, increases the responsibility of senior managers over the reliability of financial statements, and nonfinancial information that needs to be communicated to the market (Krishnan & Visvanathan, 2007; Wagner & Dittma, 2006; Y. Zhang, Zhou, & Zhou, 2007). In addition J. Cohen, Krishnamoorthy, and Wright (2010) argue that good ICSs could make external auditor activities and certifications more effective and help management connect transparency and accountability with better market competition (Fenga, Lia, & McVay, 2009; Gupta & Leech, 2006).

Previous research on internal controls has mainly focused on the costs of compliance associated with §302 and §404 (Ahmed, McAnally, Rasmussen, & Weaver, 2010; O’Brien, 2006; I. X. Zhang, 2007) and on the effects of internal control weakness disclosures on the cost of equity and the value of the firm (Ashbaugh-Skaife, Collins, Kinney, & LaFond, 2008; Beneish, Billings, & Hodder, 2008; Elbannan, 2009; Jain & Rezaee, 2006; Li, Pincus, & Rego, 2008; Ogneva, Subramanyam, & Raghunandan, 2008). Recent research has extended the investigation of the effectiveness of ICSs on lowering individual risk for the CEO, CFO, and other executives (Henry, Shon, & Weiss, 2011; Hoitash, Hoitash, & Johnstone, 2012). Because CEOs and CFOs are personally accountable for the effectiveness of the ICS, it is likely that they are willing to manage firms with ineffective internal controls only if owners pay them higher compensations. As a result of delegating authority and responsibility throughout the organizational hierarchy, this assumption is logically sustainable also for other executives, given that they manage more administrative tasks (design, operation, testing, and evaluation of internal controls) and, consequently, are willing to assume more risks only by negotiating higher compensation. However, if owners do recognize internal control as a monitoring system, they will “disinvest” in other substitute mechanisms, likely lowering the levels of compensation (Gillan, 2006). Therefore, an effective ICS can be a tool for the board to control business risks by mitigating agency costs (Culpan & Trussel, 2004).

On the basis of these assumptions, we empirically examine the impact of Sarbanes–Oxley from an agency perspective. We investigate whether total executive compensation and bonuses are related to the effectiveness of internal controls, while controlling for other determinants of pay: governance, personal characteristics, firm characteristics, and macroeconomic measures. The analysis is conducted on a sample of 1,593 firms and 15,606 executives from 2002 to 2010, for a total number of 61,020 years. We collect data from Compustat, AuditAnalytics, and RiskMetrics databases to investigate whether, from a shareholder perspective, a sound ICS can assure higher level of monitoring, reducing the need to pay more to align executives’ interests. Therefore, our hypothesis examines the relationship between executives’ compensation and the effectiveness of ICSs. We investigate this relationship extensively, both with regard to executives in general and with specific reference to CEOs and CFOs.

The results generally confirm the main hypothesis. The effects of the SOX are examined distinguishing the effectiveness of internal controls from other corporate governance variables, highlighting the effects of firm characteristics that influence executives’ propensity to risk and, consequently, the structure and configuration of their salary. This study extends the existing research with new evidence on the ICS as a control mechanism in the context of agency problems. The results show that CFO bonuses are related to the effectiveness of internal controls, while CEO compensation has a nonsignificant relation.

The first section presents the literature review and analyzes why an effective ICS should increase the value of the firm and acts as a monitoring mechanism by lowering agency costs (executive compensations). The next section investigates the research issues raised by SOX Sections 302 and 404, with a focus on the impact of the SOX on executives’ responsibilities, risk, and compensations. After describing the theoretical framework, the next section states the research hypothesis, research design, and models used. The results and conclusions are explained in the last section.

Literature Review on Internal Control and Executive Compensation

Earlier studies have defined the agency problem in terms of the degree of separation between the ownership and control (Fama, 1980; Fama & Jensen, 1983; Jensen & Meckling, 1976; Ross, 1973). Because the interests of principals (equity holders) and agents (executives) differ, the agency problem is to determine the optimal contract for the agents’ service. A classic agency problem in the case of incomplete information is the unobservable agent behavior which leads the principals to two possible options. On one hand, to control agent behavior, the principal can purchase information on the agent’s behavior and consequently give rewards, requiring surveillance mechanisms (i.e., an ICS; Eisenhardt, 1985). On the other hand, the risk can be transferred by aligning the agent’s remuneration to firm’s performance (pay for performance). Thus, the central issue in the agency theory is the trade-off between the cost of controlling agent behavior and compensation costs (Devers, Cannella, Reilly, & Yoder, 2007; Gomez-Mejia & Weiseman, 1997). To align these contrasting interests, principals develop contracting and monitoring mechanisms to limit agents’ actions so that they can serve the interests of the owners (Fama, 1980).

In an extensive review of the compensation research, Gomez-Mejia and Weiseman (1997) reframe and categorize compensation design in three dimensions: (a) criteria used in determining compensation (e.g., firm performance, firm size), (b) consequences for the executive (e.g., the level of compensation and the risk of pay), and (c) mechanisms used to link the compensation criteria to the compensation consequences. They distinguish two forms of compensation design mechanisms: contracts and direct supervision. Contracts are legal arrangements that specify both the criteria and form of compensation in a given period of time (Jensen & Meckling, 1976), whereas direct supervision refers to monitoring mechanisms based on the subjective evaluation of managers (Westphal & Zajac, 1994).

Empirical research on contracts has not always found a strong link between executive compensation and pay-for-performance. Jensen and Murphy (1990) define pay-for-performance as the dollar change in the CEO’s pay associated with a dollar change in the wealth of shareholders, intending a higher alignment between CEO and shareholders. The results report a low pay-for-performance sensitivity of CEO pay, concluding that the agency theory notion of optimal contracting fails to explain this relationship. This is a controversial result, as Jensen is one of the main authors of the agency theory.

Contrary to the above conclusions, Hall and Liebman (1998) report a high sensitivity of CEO pay to pay-for-performance, stating that both CEO compensation and its sensitivity to performance have increased sharply over the years as a result of the increasing use of stock options as a reward mechanism.

Several other contributions have assessed the theoretical and empirical implications of the agency theory, discussing its validity and offering new insights. Eisenhardt (1989) studies the contributions of the agency theory to organization theory, suggesting a greater focus on information systems. Holmstrom (1979) concludes with the same suggestion that contracts can be improved “. . . by creating additional information systems . . . or by using other available information about the agent’s action or the state of nature” (p. 79). This area of research has led researchers to examine the relationship between equity holders and executives outside the contract boundaries, focusing on direct supervision (Westphal & Zajac, 1994).

Studies on direct supervision revolve around the structure of ownership (Tosi & Gomez-Mejia, 1989; Werner & Tosi, 1995), the composition of boards of directors (Gomez-Mejia & Weiseman, 1997), and the audit and remuneration committee (Conyon & Peck, 1998). The effects of these governance-related factors on executive pay have been examined by several empirical research works, with mixed results (Core, Holthausen, & Larcker, 1999; Daily, Johnson, Ellstrand, & Dalton, 1998; Hartzell & Starks, 2003; Lambert, Larcker, & Weigelt, 1993).

Although the existing empirical literature has widely investigated the effects of governance mechanisms on executives’ compensation, there is little focus on internal controls. One important theoretical contribution is provided by Gillan (2006), who identifies internal and external governance mechanisms that can ease the agency problem, but in addition to the board of directors and ownership structure, he also considers the ICS in aligning executives’ objectives to those of the ownership.

However, only after the introduction of the SOX in 2002, there was increasing interest from researchers and professionals on the quantitative effects of the new internal control regulation. Extensive research has provided evidence on the relationship between ICSs and executives’ compensation, with particular regard to the CFO (Brown & Lim, 2012; D. Cohen, Dey, & Lys, 2008; Erhemjamts, Gupta, & Tumennasan, 2009; Henry et al., 2011; Hoitash et al., 2012; Schiehll & Bellavance, 2009).

D. Cohen et al. (2008) show that there was a significant decline in the ratio of incentive compensation to salary after the passage to the SOX. Research shows that firms in the post-SOX period offer their CFOs muted incentives, to motivate them to focus more on their fiduciary responsibilities. Indjejikian and Matejka (2009) find that from 2003 to 2007, public entities reduced the percentage of CFO bonuses contingent on financial performance. This result shows that firms mitigate earning management or other misreporting practices in part by de-emphasizing CFO incentive compensation.

Henry et al. (2011) focus on CFO compensation and the effectiveness of ICSs under SOX §404. They find that appropriate compensation increases the effectiveness of ICSs, by motivating CFOs to improve their performance. However, they do not consider individual characteristics in their models and assume that CFOs are willing to implement a sound ICS only if they obtain a corresponding compensation. The authors do not assume that the ICS might exist even before the CFO is hired in the company and that it can be a factor of determining the pay before he or she starts work.

Hoitash et al. (2012) find that CFOs at firms with stronger governance experience larger compensation decreases upon ICMW (internal controls material weaknesses) disclosures compared with CFOs at firms with weaker governance. Moreover, CFOs at firms with greater costs of financial statement misreporting experience larger compensation decreases upon ICMW disclosures compared with CFOs at firms with lower costs of misreporting. Thus, they argue that firms must provide managers with the incentives to make efforts toward producing effective internal controls. Indeed, these results do not consider the role of the ICS as a governance mechanism that can ease the agency problem by lower compensation contracts to balance increased controlling mechanisms.

Research Issues Raised by SOX Sections 302 and 404

An innovative feature of SOX from the U.S. Securities and Exchange Commission (SEC) interpretation is the emphasis on internal control as a managerial system. All executives play a key role in the design, operation, and monitoring of the ICS. Therefore, these functions become a common knowledge and competence of the entire executive system, and not only of the internal auditor, external auditor, and CFO (Roth & Espersen, 2003).

SOX §302 and §404 have very important implications for executives. The demand for formal proof of effectiveness of internal control produces a cascade effect throughout the entire organizational structure, involving all personnel (Green, 2004). The ICS is not an event or practice isolated from other managerial processes. It does not concern only the internal or external auditors, the CFO, and the audit committee, but is also a part of the executive system, and its effectiveness is a prime responsibility also for the CEO and operating managers (Wagner & Dittma, 2006). All executives have to contribute to the effective design, operation, assessment, and testing of internal controls, and provide the necessary expertise and leadership within their areas of responsibility (Fenga et al., 2009).

SOX §302 and §404 primarily influence management in terms of knowledge and skills that they must acquire to correctly design and manage the ICS. But the impact of SOX is even more complex due to the effect of the subcertification process throughout the organization. The certification process has increased the level of risk for the CEO, CFO, and other executives. As a consequence, executives operating in businesses with a higher level of risk due to the deficiencies and weaknesses of their ICSs might be willing to accept more risks in exchange for higher levels of compensation. This assumption leaves open ground for research on the effects of internal controls over CEO/CFO and executive compensations.

To find the relationship between the ICS and compensation, we analyzed the effect of sound ICSs on compensation by considering executives at all levels and focusing on CEO and CFO level as they are the ones personally responsible for the reliability of the ICSs. We studied the disclosure of the ICS as an alternative governance mechanism to ownership structure, institutional ownership, proportion of independent directors, and the proportion of accounting expert members of the audit committee. In this respect, the ICS acts as a monitoring mechanism to reduce the overall agency problem and to align ownership and managers’ interests.

Research Hypothesis and Design

A fundamental premise of SOX on the effectiveness of ICS (defined as the set of disclosure controls and internal control over financial reporting) is that an effective internal control benefits shareholders, lowering the risk of misreporting of financial and nonfinancial information (Ashbaugh-Skaife et al., 2008). We aimed to show that the ICS increases shareholder power and lowers managerial risk. We approached this hypothesis by studying the effects of the ICS on executives’ compensation, expecting to have higher executive compensations in firms with a noneffective ICS. This is theoretically explainable by the Agency Theory, as a higher level of monitoring lowers the costs of other control mechanisms (such as pay-for-performance). We expected to find more sensitivity to pay in relation to the ICS for the CFO/CEO than other executives, because the CFO/CEO is personally responsible for the effectiveness of the ICS.

Sample Selection

The analysis is based on a broad sample of listed firms in the United States in 2000-2010. The lower limit is due to AuditAnalytics data that start from 2002 (used to gather data on the effectiveness of internal controls). Some authors do not consider data before 2004 in investigating SOX effects, mainly because it was not mandatory to comply with the rules until 2004, although boards and auditors were trying to implement the requirements (Geiger & Taylor, 2003). Nevertheless, data from 2002 to 2004 were used as a pre-SOX period and are thus included in the model. The data end on 2010 as the last period of observations in the Compustat/AuditAnalytics and RiskMetrics database at the time of the investigation.

We collect executive and firm-specific (financial, audit, and governance) data from Compustat, AuditAnalytics, and Investor Responsibility Research Center (IRRC) databases. A first selection is applied by identifying firms with executive compensation data in 2002-2010 (Table 1). From a full sample of 26,820 executives, the number is reduced by selecting only firms with data available from AuditAnalytics (lowering the number to 18,113 executives with 76,858 observations) and IRRC (reaching a final sample composed of 15,606 executives and 61,020 observations). We exclude firms from the financial sector with standard industry classification code (SIC) codes from 6000 to 6799 (Krishnan & Visvanathan, 2007).

Sample Selection Process.

Basic Assumptions and Model Setup

The model setup is a critical moment to have strong results. The main focus of this research is the impact of the ICS on executives’ compensation, so we used different compensation measures, governance measures, executives’ characteristics, firm performance, control variables, and macroeconomic measures (see Table 2).

Operationalization of the Statistical Variables.

Compensations

We consider the total compensations (TDC1) as the total pay received by executives during the year. It includes the annual monetary bonus compensation; all benefits, payments in kind, and perquisites; and all long-term monetary compensation.

In addition, we add bonus as the value of a bonus earned by the named executive officer during the fiscal year.

ICS

The internal control effectiveness variable (ICS) is the overall conclusion about the effectiveness of the internal system declared by the CEO and CFO under §302 and the annual audit of management’s evaluation of the effectiveness of internal controls, under §404. Assessment of “disclosure control and procedures” and “Internal control over financial reporting,” as available in AuditAnalytics database, was used to create a proxy on the effectiveness of ICS, comparing the data from the evaluation of both sections. If the ICS was reported as ineffective in one of the sections, the proxy scored 0, and only in the case of effective evaluation on both reports, the proxy is scored 1. We expect lower compensations for executives who operate in firms with an effective ICS.

Governance Index (Entrenchment Index [E-Index])

We rely on a governance index used widely in existing studies: the E-Index of Bebchuk, Cohen, and Ferrell (2009). The E-Index is based on six of the 24 provisions of the GIM index of Gompers, Ishii, and Metrick (2003). The six provisions are divided into two categories: four of them involve constitutional limitations to shareholders’ voting power and two provisions are “takeover readiness” provisions that boards put in place to defend their position: (a) constitutional limitations on shareholders’ voting power: staggered board, supermajority requirements, supermajority requirements for mergers, and supermajority provisions for charter amendments, and (b) takeover readiness provisions: poison pills and golden parachutes. All of these provisions are acquired from the IRRC database. Each of these arrangements add 1 to E-Index if it is true, determining an E-Index variable which varies from 0 to 6. Higher values of this index indicate companies with “bad” governance from a shareholder perspective, with strong power of the board, and consequently lower power of shareholders.

External auditing monitoring (Big 4)

Consistent with prior research (Ahmed et al., 2010; Becker, DeFond, Jiambalvo, & Subramanyam, 1998; Geiger & Rama, 2006; Hogan & Wilkins, 2008), we use a dichotomous variable (BIG4) to account for external auditing quality, assuming that BIG4 auditors are of a higher quality than non-BIG4 auditors. Therefore, BIG4 is scored 1 (strong), if a BIG4 auditor is contracted by the firm. Otherwise, it is scored 0. We expect lower compensations for executives who operate in firms with a BIG4 as external auditor.

Audit-related fees (AudRel)

External and internal audit efforts are seen as a substitute for executives’ compensation (Vafeas & Waegelein, 2007). Audit-related fee data are obtained from AuditAnalytics. In general, these are insurance and related services (e.g., due diligence services) that are traditionally performed by independent accountants. Specifically, these services include, among others, employee benefit plan audits, due diligence related to mergers and acquisitions, accounting consultations and audits in connection with acquisitions, internal control reviews, certification services that are not required by statute or regulation, and consulting concerning financial accounting and reporting standards. We expect a negative relation with executive compensation.

Executive characteristics (age, gender, horizon)

When senior executives are near to retirement, the agency problem increases, as executives become more sensitive to short-term objectives that provide more personal benefits, rather than being concerned with long-term performance (Davidson, Xie, Xu, & Ning, 2007). This problem has been defined in literature as the horizon problem. Empirical investigations have proved that the horizon problem is related to the fact that the CEO’s turnover increases with age (Evans, Nagarajan, & Schloetzer, 2010).

CEO Gender is an important determinant of compensation. Torre (2012) finds that firms with female CEOs perform better than those with male CEOs and that the gap between the CEO compensation and vice presidents is lower.

In addition, we include a variable to check the retirement age of executives. Following the approach of Davidson et al. (2007), we cut off executives near retirement at 62 years, as this is the earliest age that an executive would qualify for social security in the United States. The variable horizon is then defined as 1 if executives are aged 62 or older, 0 otherwise. We expect higher compensations for executives near to retirement, as per the horizon problem.

Firm characteristics (size, Δrevenues, btm, ROA, Tobin’s Q)

We identify different variables to control firm-specific characteristics that affect the level of compensation, collecting all data from Compustat.

Earlier studies identified firm size as a determinant of managerial compensation (Baker, 2004; Baker, Jensen, & Murphy, 1988; Kostiuk, 1990; Wright, Kroll, & Elenkov, 2002). We calculated firm size as the natural logarithm of total assets, expecting a positive relation to executive compensation.

We include revenue variation (ΔRevenues), the percentage variation of the current year revenues against revenues of the last year ([Revenues(t)− Revenues(t−1)] / Revenues(t−1)), as it is strongly and positively related to managerial compensation (Lewellen & Huntsman, 1970; Murphy, 1985).

We include the book to market ratio (BTM) as a growth indicator, calculated as the ratio of book equity to market equity. Low (high) values of the ratio indicate strong (low) earnings and growth opportunities (Bernard, 1994; Fama & French, 1995). Therefore, we expect a negative relation to executive compensation.

We use return on assets (ROA) calculated as the ratio of equity before interest and taxes (EBIT) to assets, as a measure of profitability relative to the capital employed by the firm, expecting a positive relation with compensation (Brealey, Myers, & Marcus, 2007).

Tobin’s Q compares firms’ market value with the replacement cost of its assets (Tobin, 1969). This measure of firm valuation is favored by scholars because it is risk-adjusted, independent of industry, and provides a good indicator of shareholder value (Lev, 2001; Lewellen & Badrinath, 1997). Tobin’s Q is calculated as ([Total Assets] − [Common Shareholders’ Equity] + [Common Shares Outstanding] × [Yearly Medium Price Close]) / (Total Assets) following the approximation method described by Chung and Pruitt (1994).

Control variables (sector)

Sector (

ΔGDP

ΔGDP, the annual percentage change in the U.S. gross domestic product ([GDP(t)− GDP(t−1)] / GDP(t−1)), is included to control for changes in compensation due to macroeconomic shifts in national wealth (Boschen, Duru, Gordon, & Smith, 2003; Tosi & Greckhamer, 2004). We expect higher compensations for increasing variations in gross domestic product.

Hypothesis

The first hypothesis examines the relation between CEO/CFO compensation and the ICS. Based on SOX §302 and §404 provisions, we expect a negative relationship, as the CEO/CFOs are ultimately solely responsible for the design, assessment, and certification of the firm’s ICS. However, one should consider the different organizational role and influence that CEOs and CFOs have on the ICS. Indeed, the competences and duties of the CFO place him or her in a leadership position in managing the ICS; thus, we expect a stronger relation of CFO compensation to the effectiveness of the ICS. However, the complexity and extent of CEO competences and duties on the whole business imply that he or she has a stronger relationship with the whole corporate governance system, in which internal controls constitute an important component but are not exhaustive (Li, Pincus, & Rego, 2008).

Thus, the following hypothesis is proposed:

For CEOs, we expect more significant relationships with other governance, firm characteristics, and individual variables than with the ICS itself.

The first hypothesis can be extended by analyzing the relationship between compensation and internal controls for all executives and members of the board of directors. Due to the process of subcertifications, we assume that not only CEO/CFOs with direct responsibility over the reliability of ICS but also other executives are affected by its effectiveness on two ways: First, firms with effective internal controls system lower executives’ risk, thereby, it can be assumed that executives would accept less compensation; second, from a shareholder perspective, a sound ICS can assure a higher level of monitoring, lowering the need to pay more to align executives’ interests with theirs.

Consequently, we test the following hypothesis:

Panel Data Models

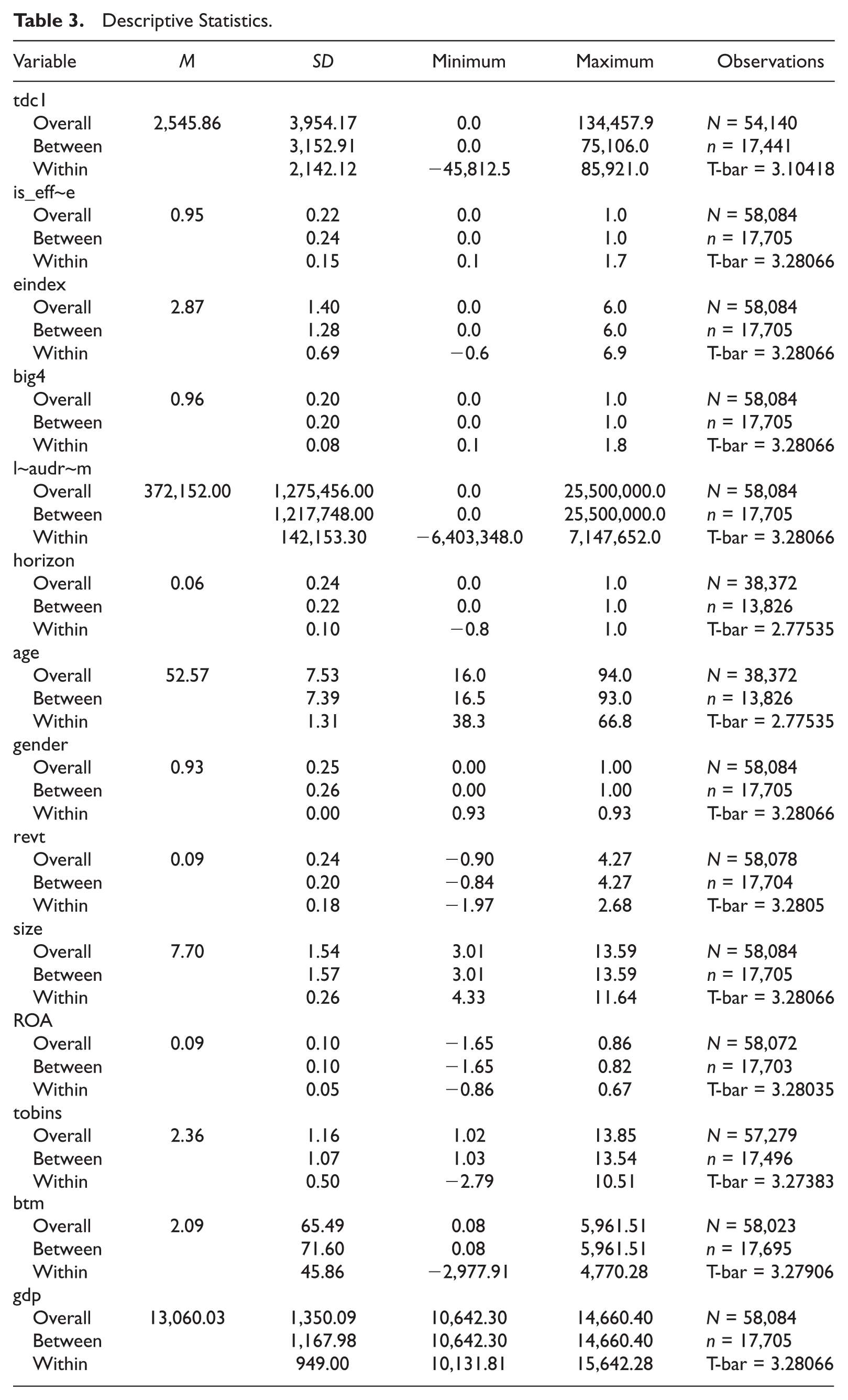

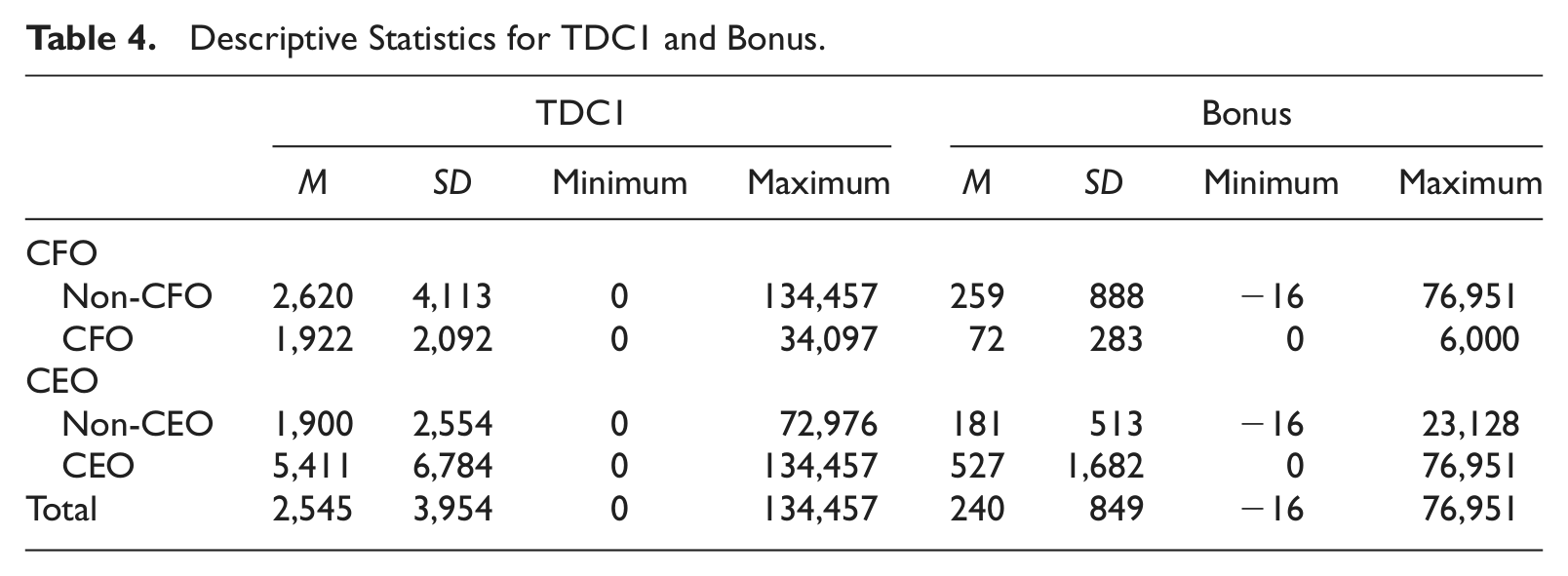

Data are analyzed longitudinally by creating a data panel with the available years (from 2002 to 2010). We use a sample of 1,593 companies over a nice year period and 15,606 executives. Table 3 provides descriptive statistics for each of the variables used (M, SD, minimum, maximum, number of observations) overall, between, and within the same executive data. Our data show an overall mean of 2.5 million total compensation, while CFOs have an overall mean total compensation of 1.9 million, compared with 5.4 of CEOs’ total compensation (see Table 4).

Descriptive Statistics.

Descriptive Statistics for TDC1 and Bonus.

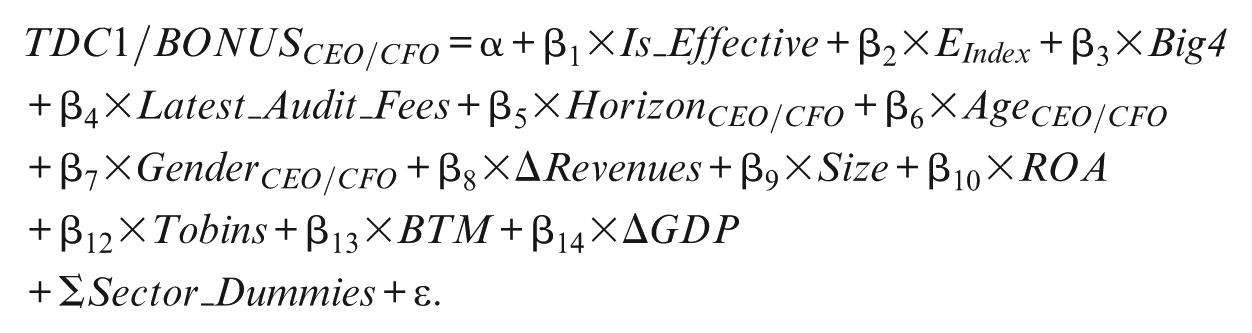

We develop different panel-data models for each of the above hypotheses:

H1: CEO/CFO—Panel A and Panel B

H2: Executive Level—Panel C

Results

The results of each of the above hypotheses are reported in Tables 5 to 7.

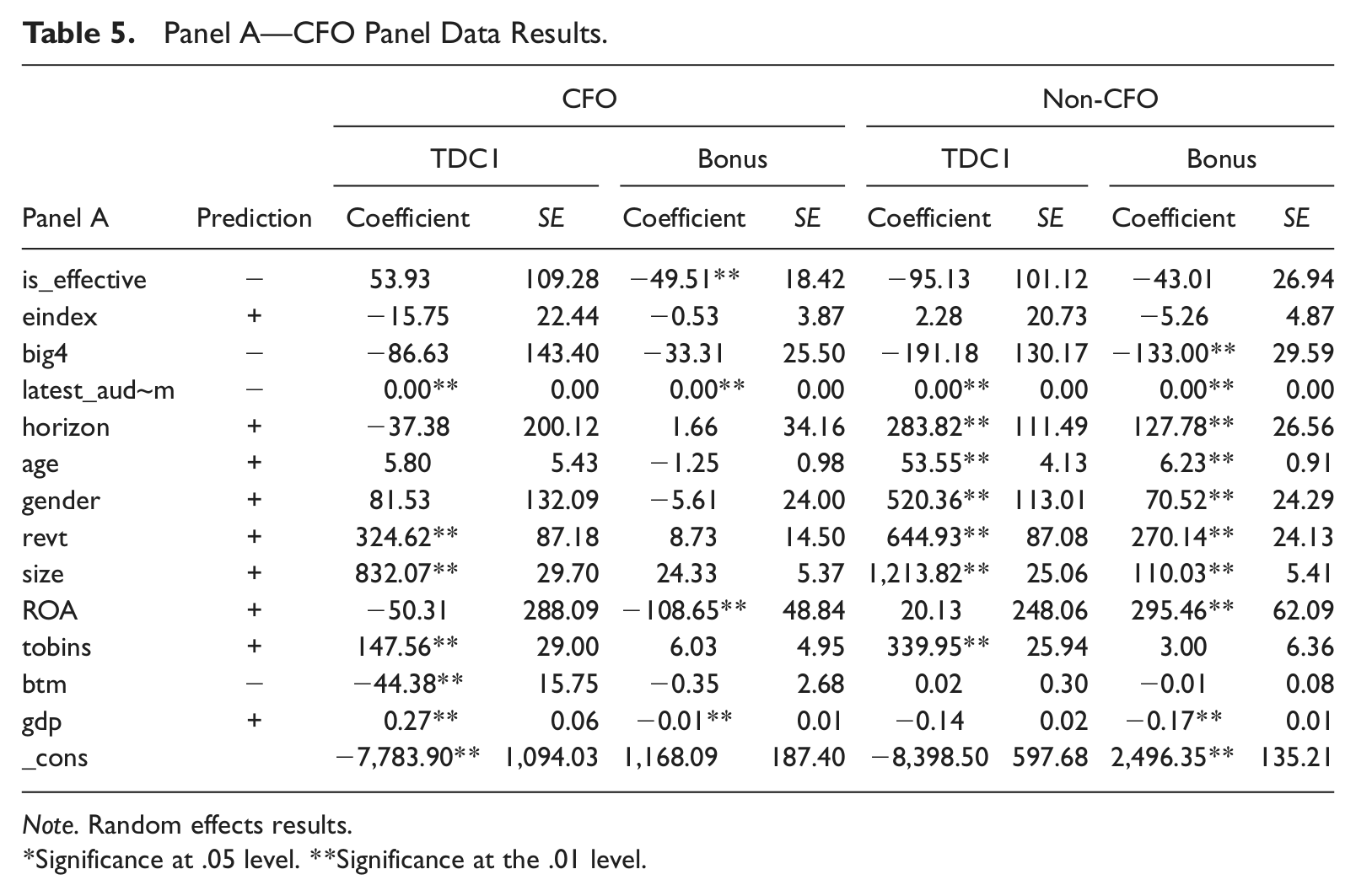

Panel A—CFO Panel Data Results.

Note. Random effects results.

Significance at .05 level. **Significance at the .01 level.

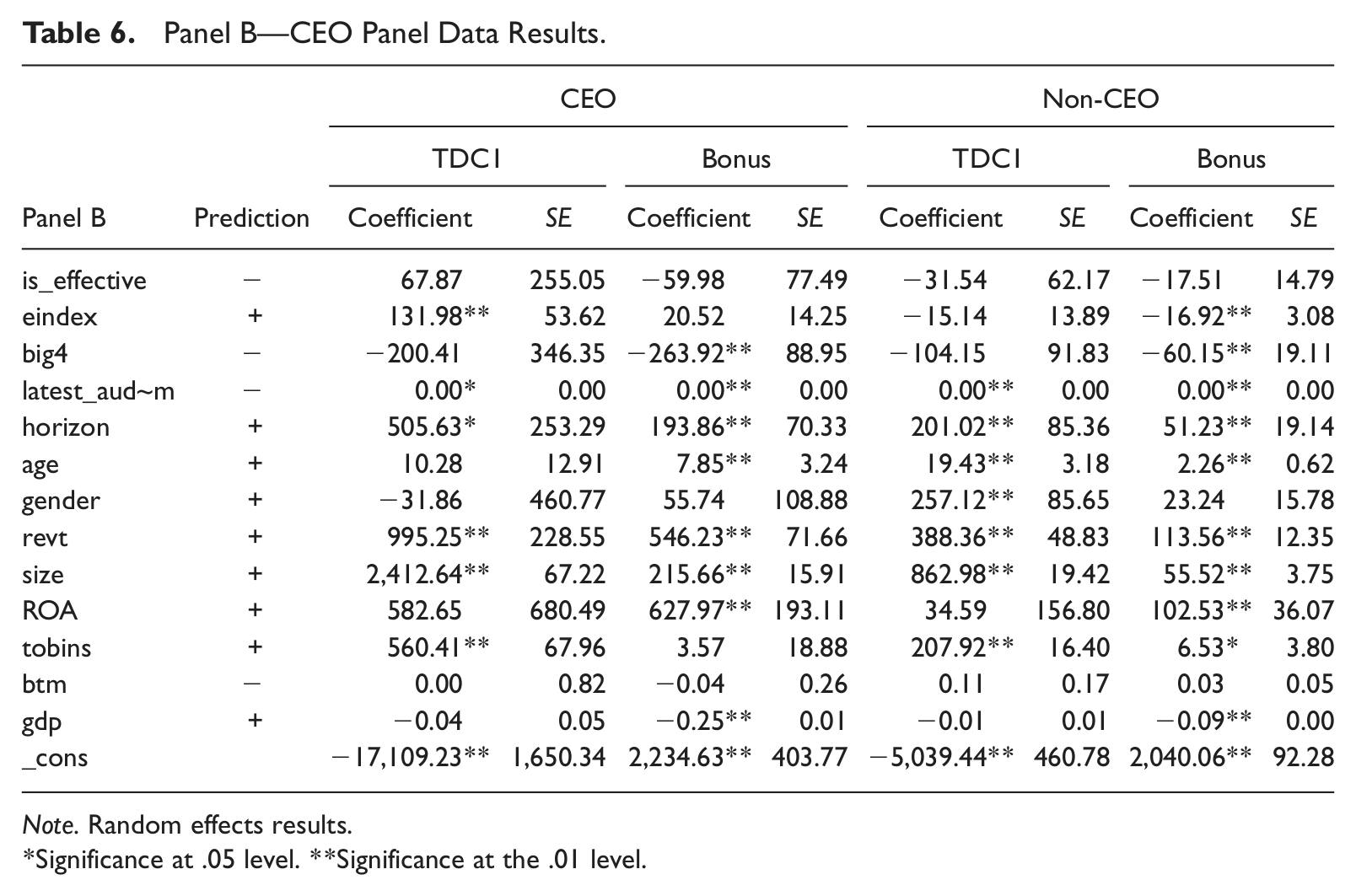

Panel B—CEO Panel Data Results.

Note. Random effects results.

Significance at .05 level. **Significance at the .01 level.

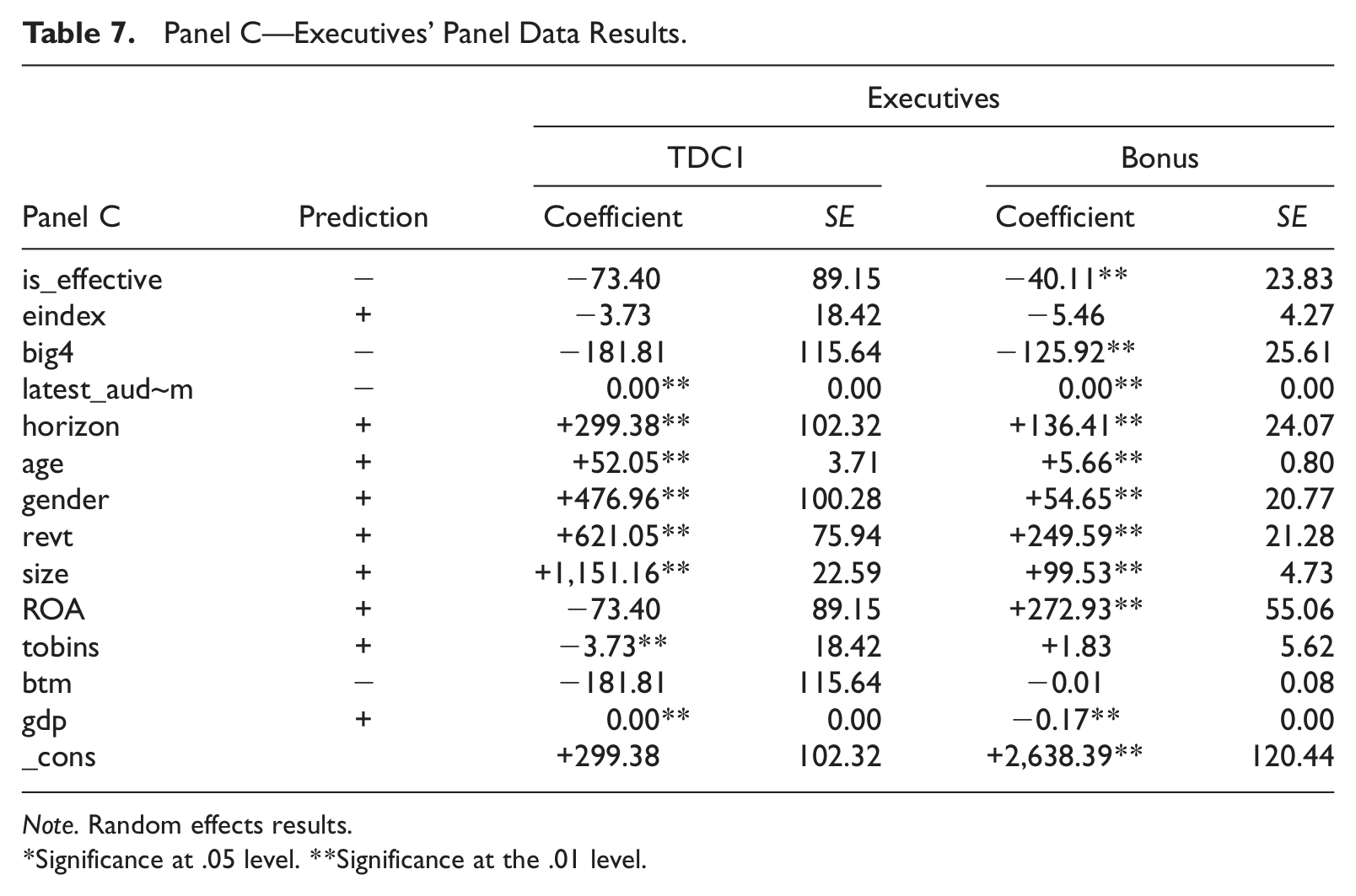

Panel C—Executives’ Panel Data Results.

Note. Random effects results.

Significance at .05 level. **Significance at the .01 level.

We investigate whether there is a significant relationship between the ICS and CEO/CFO pay (H1). We expect a negative relationship, as the basic assumption confirms that CFO/CEOs counterbalance their risk of possible accounting errors by accepting lower levels of pay in exchange for a more secure business environment. This assumption is likely to be stronger for CFOs rather than CEOs, who are expected to be more related to the overall governance quality of the firm.

The results of the panel-data model show the relationship between TDC1 and bonus and the explanatory variables used in H1 on two clusters: one composed of only CFO or CEO executives and the other with the rest of the executives (see Tables 5 and 6)

An interesting result concerning the ICS is that it shows a significant relationship with bonuses only in the CFO cluster. It is not significant in all other models. Thus, one can conclude that the effectiveness of internal controls is an important determining factor for CFO bonuses. In particular, CFOs working in firms with effective internal controls receive US$49,510 less bonuses. This result confirms the basic assumption of this research for CFOs.

Regarding personal characteristics, one can notice that they are significant for non-CFOs and not for CFOs, in which pay shows a significant relationship with firm characteristics (revenues, ROA, tobins, btm) and macroeconomic measure (gdp).

However, Table 6 shows the results of our model on CEO total compensation and bonuses. It is important to note that, in this case, there is no significant relationship between the effectiveness of internal controls and CEO/non-CEO compensation (TDC1/bonus).

An interesting result is the governance effect over compensation of CEOs and non-CEOs. The significant values are for the CEO/TDC1 model and non-CEO/bonus model. The values show that for higher E-Index values, which indicate lower shareholder power and higher management power, TDC1 increases by US$131,980 for CEOs. This result is expectable if one thinks of the restricted power of shareholders in the case of higher E-Index values. However, Non-CEO bonuses decrease as E-Index values increase. This is an unpredicted result, which confirms that CEOs are the first to profit from the restricted power of shareholders.

Another interesting result is the lower CEO/non-CEO bonuses in the presence of a BIG4 auditor. CEO bonuses decrease by US$263,920 compared with the decrease of US$60,150 of non-CEOs. The difference may be due to the fact that CEOs receive more compensation than non-CEOs (as one can see from the above descriptive statistics), so the relation of explanatory variables has stronger effects on TDC1/bonuses.

Regarding personal characteristics, one can notice that as in the case of CFO/non-CFO model, there is no significant relationship of CEOs with personal characteristics except for the proximity to retirement (horizon). In this case, CEOs close to retirement receive US$505,630 more total compensation and US$193,860 bonuses.

The CEO model shows a more significant relationship between TDC1/bonuses and firm characteristics measurements.

Table 7 shows the results of the second hypothesis. The model uses TDC1 and bonus as predictive variables. The results show that executives’ total compensation is not related to the effectiveness of internal controls, but bonus is. Bonus has a relation with coefficient −40.11 with the ICS, which means that executives working in firms with effective internal controls receive US$40,000 less than executives working in firms with noneffective ICSs. This result confirms the expectation that there is a negative relationship between the effectiveness of internal controls and executive compensation. Thus, it confirms that executives perceive the ICS as a personal risk-mitigating mechanism, giving them grounds to accept less pay. Nevertheless, the decrease in bonuses may be due to the more reliable accounting information released by the firm, mitigating the risk of misstatements to increase personal gain from bonuses.

The same conclusions can be drawn from the use of BIG4 external auditors. From a risk-mitigating perspective, the use of BIG4 lowers executives’ bonuses by US$125,920 compared with executives working in companies with non-BIG4 auditors.

Executives’ personal characteristics, proximity to retirement (horizon), age, and gender confirm the predictions in both models (TDC1 and bonus). Executives near to retirement make US$299,380 more in total compensation (US$136,410 in bonuses) than those not close to retirement.

Age is a factor for receiving more compensation (US$52,000 TDC and US$5,660 bonus).

Gender confirms that males are paid more than females—indeed US$476,960 more total compensation and US$5,465 more bonuses.

Discussion and Conclusion

The underlying assumption of this article is that ICSs, defined as monitoring mechanisms that can ease the agency problem (Jensen & Meckling, 1976), have strong implications on the relationship between ownership and management. On one hand, effective internal controls protect investor interests by promoting and giving assurance regarding the reliability of financial reporting and compliance with laws and regulations, and on the other hand, executives have less personal risk because they are personally accountable for the ICS and must personally certify its effectiveness, implying criminal liability (in case of CEO and CFO).

Recent research on the ICS and executive compensation has focused on the CFO/CEO as the main figure responsible for the effectiveness of the ICS (D. Cohen et al., 2008; Henry et al., 2011; Hoitash et al., 2012). Our different results are based on the fact that the ICS is considered a shared responsibility among all executives, with leadership provided by the CFO.

Using a large and representative sample of 1,593 firms and 15,606 executives with 60,020 executive-years observations over 2002-2012, we found that CFO and executive compensation has a significant relationship with the effectiveness of the ICS as defined by SOX Sections 302 and 404. Moreover, we found that CEO compensation shows no significant relationship with the effectiveness of ICS but with the overall governance quality.

From an agency perspective, the results confirm that contracts (executive compensation) and direct supervision (control mechanisms) are complementary approaches that shareholders can use to align executives’ interests (Holmstrom, 1979). In particular, the ICS acts as a monitoring mechanism reinforcing direct supervision and, consequently, balancing contract mechanisms by permitting lower executive compensation.

The findings of this study have both practice and policy implications. On the practice side, our results show that the compensation committee should consider the effectiveness of the ICS as an important feature of compensation design, not only for the CFO but also for all executives.

On the policy side, our study shows that despite the responsibility of both CEOs and CFOs for the effectiveness of the ICS defined by SOX, there is no equal consequence on compensation. Our results show no significant relationship of CEO compensation with the ICS, suggesting that CEOs have only a formal responsibility for the effectiveness of the ICS. Instead, there is a substantial relationship with the overall governance quality.

Our results do not allow us to conclude whether SOX benefits in terms of lower compensation are higher than the SOX costs. This is a possible development of the approach followed in this work that can be replicated by researchers to analyze the long-term effects of the regulation on internal control disclosure.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.