Abstract

Closed-end country funds are interesting in that they have two sets of prices for the same underlying assets—the net asset value (NAV) of the fund holdings as measured using the underlying firms’ stock prices in their home markets and the fund price at which the fund trades on a U.S. stock exchange. Utilizing the theoretical framework of information asymmetry in two separate markets for an identical asset, we find that the difference between the fund’s NAV and its trading price (i.e., the fund discount) is positively associated with the earnings opacity of the underlying companies. Such a positive association is consistent with the notion that U.S. investors face higher information acquisition and processing costs when compared with local investors, and therefore earnings opacity exacerbates the information disadvantage of U.S. investors, leading to a larger fund discount. We further show that the positive relation varies predictably with U.S. investors’ information acquisition and processing costs and with the extent to which host stock markets are segmented from the U.S. market. Specifically, we find that the positive relation between earnings opacity and fund discounts is weaker for those funds with more U.S. cross-listings in fund holdings, with underlying companies following financial reporting standards similar to U.S. standards, and with less segmented local markets.

Keywords

Introduction

Prior literature suggests that, when investing in foreign equities, U.S. investors are at an informational disadvantage relative to their local peers because they incur higher information acquisition and processing costs (e.g., Brennan & Cao, 1997; Choe, Kho, & Stulz, 2005). These information costs include the time and effort associated with becoming familiar with the financial statements of foreign companies, interpreting the information, and acquiring private and public information from other sources for investment decisions (Beneish & Yohn, 2008). In response to the information disadvantage relative to local investors, U.S. investors tend to underweight their investments in foreign firms. This “home bias” phenomenon has been extensively examined in the literature (Bradshaw, Bushee, & Miller, 2004; Covrig, DeFond, & Hung, 2007; Karolyi & Stulz, 2003). Besides its impact on asset allocation, this information disadvantage could lead U.S. investors to set lower prices for identical local assets as compared with local investors (e.g., K. Chan, Menkveld, & Yang, 2008). Our article examines the role of earnings opacity (or inversely, earnings quality) in explaining the relative pricing of local assets by U.S. and local investors in the setting of closed-end country funds. Specifically, we ask two fundamental questions: First, how does earnings opacity of the underlying firms affect the pricing of closed-end country funds? Second, when does earnings opacity play a more or less significant role in explaining the fund pricing?

Closed-end country funds are investment companies that issue a fixed number of shares domestically and invest the proceeds primarily in the equity market of a single foreign “host” country. Compared with prior studies investigating U.S. investors’ ownership in non-U.S. firms (e.g., Bradshaw et al., 2004), this study makes use of two sets of prices for the same underlying foreign equities held by the funds. The first set is the net asset value (NAV) of the fund holdings as measured using the underlying firms’ stock prices in their home markets and the second set is the fund price at which the fund trades on a U.S. stock exchange. The fund’s trading price and the fund’s NAV are set by U.S. investors and local investors, respectively, for the same underlying assets. Prior studies have shown that closed-end fund prices are usually different from NAVs, and that country funds typically trade at a discount (i.e., fund price is less than fund NAV; for example, Bodurtha, Kim, & Lee, 1995; J. S. P. Chan, Jain, & Xia, 2008). As we argue below, closed-end country fund discounts provide a unique opportunity to gauge U.S. investors’ pricing of the information asymmetry, exacerbated by the poor earnings quality of local firms, relative to local investors.

A firm’s financial reporting information helps shape investors’ expectations of future cash flows while poor accounting information (i.e., earnings opacity) results in investors’ uncertainty about the firm’s future performance (e.g., U. Bhattacharya, Daouk, & Welker, 2003). If investors differ in their ability to process accounting information or they incur different information processing costs, then poor earnings quality might result in differentially informed investors, and thereby exacerbate the information asymmetry in financial markets (N. Bhattacharya, Desai, & Venkataraman, 2013; N. Bhattacharya, Ecker, Olsson, & Schipper, 2012; Diamond & Verrecchia, 1991). U.S. investors of closed-end country funds rely on the same public financial reports of underlying firms as local investors do. So the existence of fund discounts is not driven by the public disclosure disparity originating from financial statements per se. Rather, we argue that poor earnings quality of local firms exacerbates the information disadvantage faced by U.S. investors relative to local investors. Specifically, compared with local investors, U.S. investors have to incur higher costs of acquiring and processing information to overcome the information uncertainty associated with poor earnings quality of local firms. Due to their relatively limited local knowledge, U.S. investors are less capable of overcoming the information uncertainty pertaining to the local firms than local investors are. Furthermore, U.S. investors have limited information channels through which they could gain access to potentially more precise private information about local firms (e.g., Beneish & Yohn, 2008). As a result, U.S. investors would rely more on publicly disclosed earnings information to make investment decisions, implying that opaque earnings cause a higher level of information uncertainty for U.S. investors than for local investors.

Prior studies on international equity investments have shown that the information disadvantage faced by foreign investors results in a discount on equity prices (Bailey & Jagtiani, 1994; K. Chan et al., 2008; Domowitz, Glen, & Madhavan, 1997). In particular, K. Chan et al. (2008) extend the Grossman and Stiglitz (1980) model of information asymmetry to a setting of two separate markets for an identical asset, whereby local investors trade in the domestic share market and foreign investors trade in the foreign share market. They show analytically and empirically that foreign share prices are discounted from the prices of domestic shares and the discounts are positively correlated with the extent of the information disadvantage faced by foreign investors. Extending K. Chan et al.’s (2008) analytical reasoning to the setting of closed-end country funds, we hypothesize that the opaqueness of underlying firms’ earnings causes a greater information disadvantage for U.S. investors, which in turn leads to a larger fund price discount to the fund NAV for a closed-end country fund. Therefore, in our primary hypothesis, we posit that higher earnings opacity of the individual firms in the funds’ holdings leads to larger fund discounts.

The setting of closed-end country funds also allows us to test whether the relation between fund discounts and earnings opacity varies systematically with U.S. investors’ information acquisition and processing costs, and the accessibility of alternative information channels to U.S. investors. Specifically, we hypothesize that the positive relation is weakened when a fund holds a higher percentage of firms that are cross-listed as American Depositary Receipts (ADRs) in U.S. markets, and when a host country has a higher accounting convergence with the U.S., as proxied for by the host country’s use of International Financial Reporting Standards (IFRS). Finally, we argue that market segmentation between the host and U.S. stock markets implies higher information acquisition and processing costs and limited information sources available to U.S. fund investors. Accordingly, we predict a less pronounced positive association between earnings opacity and closed-end fund discounts for country funds that invest in less segmented (or more financially integrated) host markets.

To test these hypotheses, we utilize earnings opacity measures (based on earnings aggressiveness, smoothing, and loss avoidance) for companies around the world and apply the same method to the underlying firms of each fund. This procedure creates fund-specific measures of earnings opacity. We hand-collect the quarterly fund holdings from the Capital IQ database, obtain financial data for the individual underlying firms by manually matching our firms with companies in the Worldscope database, and get fund prices and fund NAVs from the Center for Research in Security Prices (CRSP)/COMPUSTAT merged database. Based on 35,588 firm-quarter observations of underlying firms between 2004 and 2010, we develop fund-level measures of earnings opacity for a sample of 804 fund-quarter observations. Our sample covers 21 countries and provides a well-diversified international setting.

In our empirical analyses, we find that our measures of earnings opacity are all positively associated with closed-end country fund discounts. This positive association is both statistically significant and economically meaningful. These findings confirm our primary hypothesis that poor accounting quality of underlying firms, along with other factors documented in the literature, contributes to higher closed-end country fund discounts. Consistent with our prediction that the positive relation between fund discounts and earnings opacity should be weaker (stronger) when the information acquisition and processing costs are lower (higher) for U.S. investors, we show that the positive relation is weakened when a fund holds a higher percentage of firms that are cross-listed as ADRs in U.S. markets and when a host country has adopted IFRS. Finally, and in line with our prediction, we find that the association between earnings opacity and discounts is weaker when the local capital market is less segmented for U.S. investors.

Our conclusions are robust to the inclusion of numerous fund- and country-specific control variables, country and quarter fixed effects, an alternative specification with fund fixed effects, and to the use of alternative earnings opacity and information cost proxies. Importantly, to further ensure that omitted correlated variables are not affecting the inferences, we rerun the analyses using a changes specification and our conclusions remain unchanged.

Our study makes major contributions to the international accounting, international finance, and international business literatures. First, most studies on U.S. investment in foreign firms focus on how the information disadvantage of U.S. investors affects their portfolio allocation choices (e.g., Covrig et al., 2007). To our knowledge, very few studies examine the effect of such an information disadvantage on equity prices. Motivated by the theoretical framework of information asymmetry in two separate markets for an identical asset (K. Chan et al., 2008; Grossman & Stiglitz, 1980), our findings suggest that U.S. investors require greater fund discounts in response to the information disadvantage relative to their local peers. Importantly, we extend the international equity investment literature by showing that the earnings opacity of local firms could exacerbate the information disadvantage of U.S. investors, resulting in a larger fund discount. Thus, our findings imply that enhancing the quality of local firms’ public disclosure can help mitigate foreign investors’ concern about their information disadvantage relative to local investors.

Second, although existing studies offer several explanations for closed-end fund discounts, there are no prior studies linking the financial reporting quality of funds’ underlying firms with closed-end fund discounts. Based on the reasoning of the information disadvantage of U.S. investors vis-à-vis local investors, we contribute to the closed-end fund literature by showing that the earnings opacity of individual firms in the funds’ holdings is positively related to closed-end country fund discounts.

The next section reviews the related literature and develops the hypotheses. The section “Sample Selection and Research Design” describes the sample selection and research method. The “Empirical Results” section reports the empirical results and the final section concludes.

Literature Review and Hypotheses Development

Closed-End Country Funds

Closed-end country funds are investment companies that issue a fixed number of shares domestically and invest the proceeds in the equity markets of select foreign “host” countries (e.g., Dimson & Minio-Paluello, 2002). The shares of these funds are traded on a stock exchange at market-determined prices and generally cannot be redeemed by shareholders at their NAVs. 1

Each fund provides two distinct market-determined prices: (a) the country fund’s share price quoted on the market where it is traded (e.g., New York Stock Exchange [NYSE]) and (b) its NAV determined by the stock prices of the underlying firms’ shares in the host market. It is well known that the share prices and the NAVs of closed-end country funds tend to differ, commonly resulting in a fund discount (i.e., the NAV exceeds the fund share price). Prior literature suggests that such discounts persist because arbitrage is costly and, therefore, not always profitable (e.g., Pontiff, 1996). Researchers have attributed this price difference to the following five broad factors: (a) the loss of tax timing options (Brickley, Manaster, & Schallheim, 1991); (b) bias in NAV, caused by overhanging tax liabilities (Day, Li, & Xu, 2011) and the liquidity of the underlying firms’ shares (J. S. P. Chan et al., 2008; Cherkes, Sagi, & Stanton, 2009); (c) agency costs, including excessive management fees (Malkiel, 1977) and inferior managerial performance (Berk & Stanton, 2007; Chay & Trzcinka, 1999); (d) the existence of market segmentation (Bonser-Neal, Brauer, Neal, & Wheatley, 1990; Nishiotis, 2004); and (e) behavioral explanations, including investor sentiment and the presence of noise traders (Bodurtha et al., 1995; Hwang, 2011; Lee, Shleifer, & Thaler, 1991). Similar to previous studies on closed-end funds, we account for these potentially confounding factors in our empirical analyses.

Earnings Opacity, Information Costs, and Closed-End Country Fund Discounts

A number of studies document that geographic proximity provides local investors with an information advantage over non-local investors (e.g., Baik, Kang, & Kim, 2010). The existence of a local information advantage also extends to an international setting as the literature shows that domestic investors have a local information advantage over foreign investors with respect to domestic stocks (Brennan & Cao, 1997; Choe et al., 2005). Such an information advantage of local investors could arise from many factors, including frequent access to the local company’s operation, close communication with employees, managers, and suppliers, their ability to evaluate the local market conditions in which the firm operates, and the availability of information from local media. Compared with local investors, foreign investors are at an information disadvantage (Bradshaw et al., 2004; Covrig et al., 2007; DeFond, Hu, Hung, & Li, 2011). This disadvantage is amplified by market segmentation and geographical distance (K. Chan, Covrig, & Ng, 2005; Frankel & Schmukler, 2000; Froot & Ramadorai, 2008).

Several studies on international equity investments have shown that the information disadvantage faced by foreign investors results in a discount on equity prices (Bailey & Jagtiani, 1994; K. Chan et al., 2008; Domowitz et al., 1997). In particular, K. Chan et al. (2008) extend the Grossman and Stiglitz (1980) model of information asymmetry to a setting of two separate markets for an identical asset, whereby local investors trade in the domestic share market and foreign investors trade in the foreign share market. In their model, foreign investors are aware that they are generally less informed than local investors, so they set a lower foreign share price to compensate for the information disadvantage. 2 However, the source of variation of information asymmetry between foreign and local investors is not specified in K. Chan et al.’s (2008) model. We identify the cross-sectional variation of local firms’ earnings quality as one explicit source for the information disadvantage faced by foreign investors relative to local investors, allowing U.S. investors to be subject to different levels of information disadvantage as compared with local investors. Extending Chan et al.’s analytical reasoning to the setting of closed-end country funds, we expect that the opaqueness of underlying firms’ earnings information will cause a larger information disadvantage for U.S. investors, which in turn leads to a larger fund discount for a closed-end country fund.

We adopt measures of earnings opacity as empirical constructs of poor accounting quality that have been prevalently used in international settings. International firms generally have higher earnings opacity than U.S. firms (U. Bhattacharya et al., 2003; Leuz, Nanda, & Wysocki, 2003). These prior studies also show a wide variation in earnings opacity among international firms. Combined, our focus of closed-end country fund involving international firms provides us with a powerful setting to test the relation between closed-end fund discounts and fund-level earnings opacity. We expect that higher levels of earnings opacity (i.e., lower earnings quality of the individual underlying firms in a fund portfolio) lead to greater closed-end country fund discounts. Our first hypothesis is formally stated as follows:

Effects of Information Acquisition and Processing Costs

The hypothesized positive relation (H1) between fund discounts and earnings opacity is built on the assumption of the information disadvantage faced by U.S. investors, stemming from their higher information acquisition and processing costs, and limited information channels when compared with local investors. Therefore, the strength of the positive relation in H1 is expected to vary with characteristics of the underlying local firms and the local markets. For example, when U.S. fund investors face lower information acquisition and processing costs, the link between fund-level earnings opacity and fund discounts is expected to be weaker. Stated differently, we predict that the positive association between earnings opacity and fund discounts should be weaker when U.S. investors face lower additional costs to overcome uncertainty caused by earnings opacity of the underlying firms. The evidence, if consistent with our prediction, will add further credence to our main arguments in H1.

We first consider the characteristics of the underlying firms in fund portfolios. Prior studies show that U.S. investors have greater holdings in firms cross-listed on U.S. stock exchanges than those in other foreign firms (Ammer, Holland, Smith, & Warnock, 2012). We use the foreign firms’ cross-listing on U.S. stock exchanges to proxy for the lower information acquisition and processing costs for U.S. investors because U.S. investors have more chances to directly communicate with cross-listed firms’ managers and to attend these firms’ public events (e.g., Baker, Nofsinger, & Weaver, 2002), which helps reduce the uncertainty about financial reports at a lower cost. Following Bradshaw et al. (2004) and Covrig et al. (2007), we consider the ADR listing status as a proxy for the easier information access for U.S. investors. Overall, we expect that U.S. investors face lower information costs for country funds with a higher percentage of fund holdings in cross-listed foreign firms. Such a lower information cost implies a weaker link between fund discounts and fund-level earnings opacity.

With respect to the potential impact of using international accounting standards on U.S. investors’ information costs, prior studies show that different financial reporting standards increase information processing costs for foreign investors (e.g., Covrig et al., 2007). These findings suggest that foreign investors are more likely to understand and interpret accounting information if firms employ standards that are more familiar to them. Bae, Tan, and Michael (2008) conclude that IFRS are quite similar to U.S. generally accepted accounting principles (GAAP). 3 Besides the similarity between IFRS and U.S. GAAP, the enhanced comparability of accounting standards through the adoption of IFRS improves the overall quality of firms’ information environment. Specifically, Barth, Landsman, Lang, and Williams (2012) show that the use of IFRS by non-U.S. firms results in accounting information more comparable with that of U.S. firms. As shown in De Franco, Kothari, and Verdi (2011), a higher level of financial statement comparability lowers the cost of acquiring information and increases the overall quantity and quality of information available to market participants about the firms. In addition, using a developing country setting (i.e., China), Liu, Lee, Hu, and Liu (2011) show that the adoption of IFRS has improved the accounting quality in the regulated market. Their results suggest that the IFRS adoption is beneficial to markets that are disciplined mainly by regulators as well as by market mechanisms. Based on these arguments, we expect that the use of IFRS by a host country will reduce U.S. investors’ information acquisition and processing costs. In summary, our second hypothesis is formally stated as follows:

Effects of Market Segmentation

Global capital markets are segmented, to some extent, due to a variety of market imperfections (e.g., Foerster & Karolyi, 1999). The consequence of such market segmentation is that the less accessible foreign markets tend to be underresearched and less regulated (Frankel & Schmukler, 2000). U.S. investors are therefore subject to additional information costs when tapping into these segmented markets. Following the same arguments as for our second hypothesis, we expect that a lower extent of market segmentation results in a less pronounced positive association between fund discounts and earnings opacity.

Beyond the additional information costs, market segmentation also suggests a lack of alternative information channels, which in turn makes public financial disclosure relatively more important as an information source (Feroz & Wilson, 1992). 4 Therefore, we predict that a higher degree of market segmentation for local stock markets makes the financial reporting quality of local firms more critical in alleviating the information disadvantage of U.S. investors. This, in turn, suggests a weaker association between fund discounts and earnings opacity for closed-end country funds with less segmented (or more financially integrated) local markets. Our final hypothesis is formally stated as follows:

Sample Selection and Research Design

Sample Selection and Data Sources

We hand-collect quarterly fund holdings from the Capital IQ database starting from 2004. The individual underlying firms are manually matched with the Worldscope database to obtain their financial data. 5 We further require fund prices and NAVs from the CRSP/COMPUSTAT merged database, dividend yields from COMPUSTAT, and institutional holding data from Thomson Reuters. We also hand-collect other fund-level variables from the funds’ annual and semi-annual reports, including information on unrealized long-term capital gains and fund managers’ ownership of fund shares. In addition, we hand-collect active and inactive (Levels 2 and 3 exchange-listed) ADRs from the ADR databases provided by Citibank and JP Morgan. We collect IFRS adoption timing from the website maintained by Deloitte Global Services Limited (www.IASPLUS.com).

Country-level variables are obtained from the following sources: (a) survey data for the country’s popularity from Gallup surveys through the iPOLL databank; (b) index of investment freedom from the Heritage Foundation; (c) U.S. and local market indices, relative market liquidity, and foreign exchange rates from Datastream; (d) country-level disclosure indices and gross domestic product (GDP) growth from World Development Indicators (as developed by The World Bank); (e) protection of minority shareholders’ interests from the Global Competitiveness Report (as offered by The World Economic Forum); and (f) the cost of tax compliance from the Economic Freedom of the World Reports.

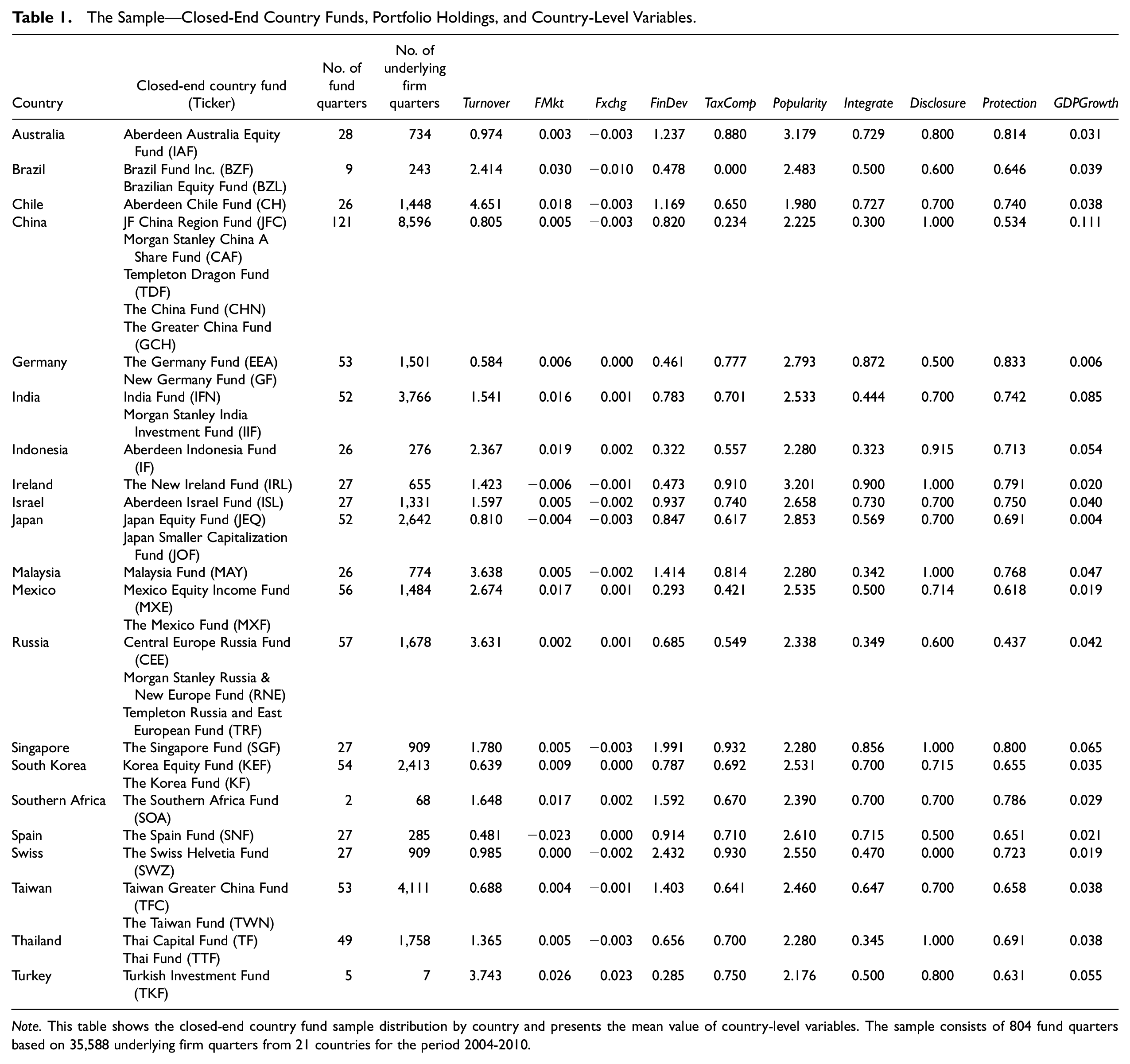

Our final sample consists of 804 fund-quarter observations from 2004 to 2010, comprising 36 unique closed-end country funds covering 21 countries. We cover the universe of U.S. closed-end country funds available during our sample period. 6 Table 1 provides the list of countries and country funds in our sample. We also present the country-level variables in the table. The fund-level earnings opacity measures are based on 35,588 underlying firm-quarter observations (4,159 unique firms) in the fund holdings. 7

The Sample—Closed-End Country Funds, Portfolio Holdings, and Country-Level Variables.

Note. This table shows the closed-end country fund sample distribution by country and presents the mean value of country-level variables. The sample consists of 804 fund quarters based on 35,588 underlying firm quarters from 21 countries for the period 2004-2010.

Measure of Closed-End Country Fund Discounts

Following prior literature (e.g., Bodurtha et al., 1995), for each fund quarter, we define the quarterly fund discount (premium) as the average of the three monthly fund discounts (premiums) over the quarter. 8 Specifically, we calculate the monthly closed-end fund discount (premium) using closing fund prices (Price) and NAVs:

where

Measures of Fund-Level Earnings Opacity

Similar to prior cross-country studies such as U. Bhattacharya et al. (2003) and Leuz et al. (2003), we employ three measures of earnings opacity used extensively in prior research as well as an aggregate measure. The use of multiple earnings opacity measures helps mitigate the possibility that one particular proxy captures some factor other than earnings opacity. 9 We calculate fund-level earnings opacity for each quarter using all firms in the quarterly fund holdings, combined with the most recently available accounting data (i.e., prior year’s financial data).

The first measure is earnings aggressiveness (Aggressive) as developed by Ball, Kothari, and Robin (2000) and Pincus, Rajgopal, and Venkatachalam (2007). Specifically, using balance sheet and income statement information, we compute scaled accruals as a proxy for individual firms’ earnings aggressiveness. 10 We define earnings aggressiveness for each underlying firm as follows:

where

In our tests, we use the median value of earnings aggressiveness for all underlying firms in a fund’s holding as a proxy for the fund’s earnings aggressiveness (Aggressive), with a higher value of Aggressive representing a higher level of earnings opacity. 11

Our second measure of earnings opacity is earnings smoothing (Smooth). The idea is that (excessive) smoothing allows earnings to obscure the underlying volatility of the firm’s economic performance, thus increasing earnings opacity. Following U. Bhattacharya et al. (2003) and Leuz et al. (2003), we define Smooth as the Spearman correlation between the change in accruals and the change in cash flow from operations (both scaled by lagged total assets) for all firms in the fund holding. Cash flow from operations is calculated as operating income minus accruals. A more negative correlation suggests a higher likelihood that earnings smoothing is obscuring the variability in the underlying firms’ economic performance, thus resulting in greater earnings opacity (e.g., Lang, Lins, & Maffett, 2011). In our tests, we multiply the correlation by −1, so that a higher value of Smooth represents greater earnings opacity.

Our third measure of earnings opacity is loss avoidance (Avoid). The fact that many underlying firms report small positive earnings numbers but few firms report small negative earnings numbers is indicative of underlying firms attempting to avoid losses. Following Burgstahler and Dichev (1997), Leuz et al. (2003), and U. Bhattacharya et al. (2003), we define Avoid for a fund quarter as the number of underlying firms with small positive earnings minus the number of underlying firms with small negative earnings, scaled by the total number of underlying firms in the quarterly fund holding. Small positive earnings (small negative earnings) are defined as net income scaled by lagged total assets between 0% and 1% (between −1% and 0%). The higher this ratio, the higher the loss avoidance for the fund quarter.

Finally, we adopt an aggregate earnings opacity measure which has the potential to mitigate the possible measurement errors in the individual measures. Specifically, following Chen, Hope, Li, and Wang (2011), we normalize the above three individual proxies and take the average of the three normalized measures as our aggregate measure of earnings opacity (Aggregate). 12

Empirical Models

Consistent with J. S. P. Chan, Jain, and Xia (2008) and Hwang (2011), we test H1 by estimating the following fund discount model:

where Discounti,t is the quarterly closed-end country fund discounts for fund i in quarter t; and Opacityi,t is the earnings opacity including the following four measures: (a) Earnings aggressiveness (Aggressive), (b) Earnings smoothing (Smooth), (c) Loss avoidance (Avoid), and (d) An aggregate measure, which is the average of the normalized values of the former three individual earnings opacity measures (Aggregate).

The appendix provides detailed definitions of the control variables as introduced below. We winsorize all variables, except indicator variables and country-level variables, at the 1% and 99% levels. 13

Note that our sample includes multiple quarterly observations from the same funds. To mitigate any dependence issues, we include quarter fixed effects to control for time-related factors. Furthermore, standard errors are clustered by both fund and quarter, which mitigates time-series and cross-sectional correlations, respectively. In two untabulated analyses, we first return the regressions employing standard errors clustered by country. In the second analysis, we employ Newey–West standard errors. All our conclusions remain unchanged with these alternative standard-error adjustments. Finally, we employ an alternative and rather conservative approach and include only one quarterly observation per year in the regressions. Again, inferences are unaffected.

We employ country fixed effects to control for unknown host-country-related factors. Including country fixed effects is a common approach to controlling for country-specific effects and addressing correlated omitted country-level variable problems (e.g., Doidge, Karolyi, & Stulz, 2007; Gelos & Wei, 2005). As explained further below, in contrast to most prior research, we additionally have data on time-varying country-level variables. 14 These data allow us to include both country fixed effects and specific country controls in the same regressions. We explain our extensive set of control variables in the following sections.

Other determinants of closed-end fund discounts

Tax timing constitutes one potential explanation of the closed-end fund discount. It refers to investors’ opportunity to minimize their tax liabilities through carefully timing their stock transactions (Brickley et al., 1991). Following prior studies (Brickley et al., 1991; Kim, 1994), we control for the weighted average return volatility of a fund’s underlying stocks (Volatility).

A second explanation of the discount is that the fund’s NAV may be overestimated. Tax liabilities relating to unrealized capital gains (Malkiel, 1977) and illiquid assets in host markets (J. S. P. Chan et al., 2008; Hwang, 2011) are considered important causes of this miscalculation. Consequently, in our regressions we include unrealized capital gains (Gains) and the relative liquidity of the U.S. versus the local market (Turnover). 15

A third explanation relates to agency costs, where excessive management fees (Malkiel, 1977), inadequate management performance (Berk & Stanton, 2007; Chay & Trzcinka, 1999), and the concentration of managerial fund ownership could all lead to closed-end fund discounts (Barclay, Holderness, & Pontiff, 1993). Thus, we include the fund’s expense ratio (Expense), past NAV returns (CNAV), and an indicator of managerial fund ownership (DMOwn) as control variables. In addition, following Day et al. (2011), we control for the fund’s dividend yield (Div).

Fourth, international market segmentation may contribute to the difference between fund prices and NAVs (Bonser-Neal et al., 1990). We control for the extent of market segmentation by including the index of investment freedom of individual host countries (Integrate). These annual data are from the Heritage Foundation, and a higher value of Integrate represents greater financial integration. 16

Fifth, we control for investor sentiment in terms of each country’s popularity among Americans (Popularity). Hwang (2011) shows that a country’s popularity among Americans affects U.S. investors’ demand for securities from that country and causes stock prices to deviate from their fundamental values. Following Hwang, we construct a Country Popularity Score by multiplying the percentage of survey participants (from Gallup survey data) who respond very favorably by 4, mostly favorably by 3, mostly unfavorably by 2, and very unfavorably by 1, and adding these four numbers into one cumulative score. In addition, following Chang, Eun, and Kolodny (1995), we include two variables to control for market risk factors in the United States and foreign markets. For the U.S. market factor (USMkt), we use the concurrent quarterly change in the Dow Jones Industrial Average index, while the foreign market factor (FMkt) is proxied by the concurrent quarterly change in the market index of the local market. Hwang suggests that these market risk factors measure general demand effects in the home and U.S. markets.

We also include these additional fund-specific control variables: institutional ownership in a particular fund (Inst), the fund’s market capitalization (Size), and fund age (Age).

Finally, we control for a number of time-varying country-level variables in the regressions, including the foreign exchange appreciation rate (Fxchg), the GDP growth rate (GDPGrowth) and financial development (FinDev) of host countries, country-level disclosure index (Disclosure), country-level investor protection (Protection), country-level ownership concentration (Concentr), and the cost of tax compliance (TaxComp) in host markets.

We test H2 and H3 using the following model:

In Equation 2, we include an information cost variable (InfoCost) and the interaction term of the information cost variable with Opacity. The information cost variables consist of (a) an indicator variable for U.S. cross-listing (DADR), which equals 1 when the percentage of fund holdings of firms cross-listed in the United States (i.e., ADR firms) is above the sample median (0 otherwise); 17 (b) an indicator variable for IFRS (DIFRS), which equals 1 if host countries employ IFRS (0 otherwise); and (c) an indicator variable for financial integration (DIntegrate; or inversely, market segmentation), which equals 1 when the investment freedom index value is above the sample median (0 otherwise).

Empirical Results

Descriptive Statistics

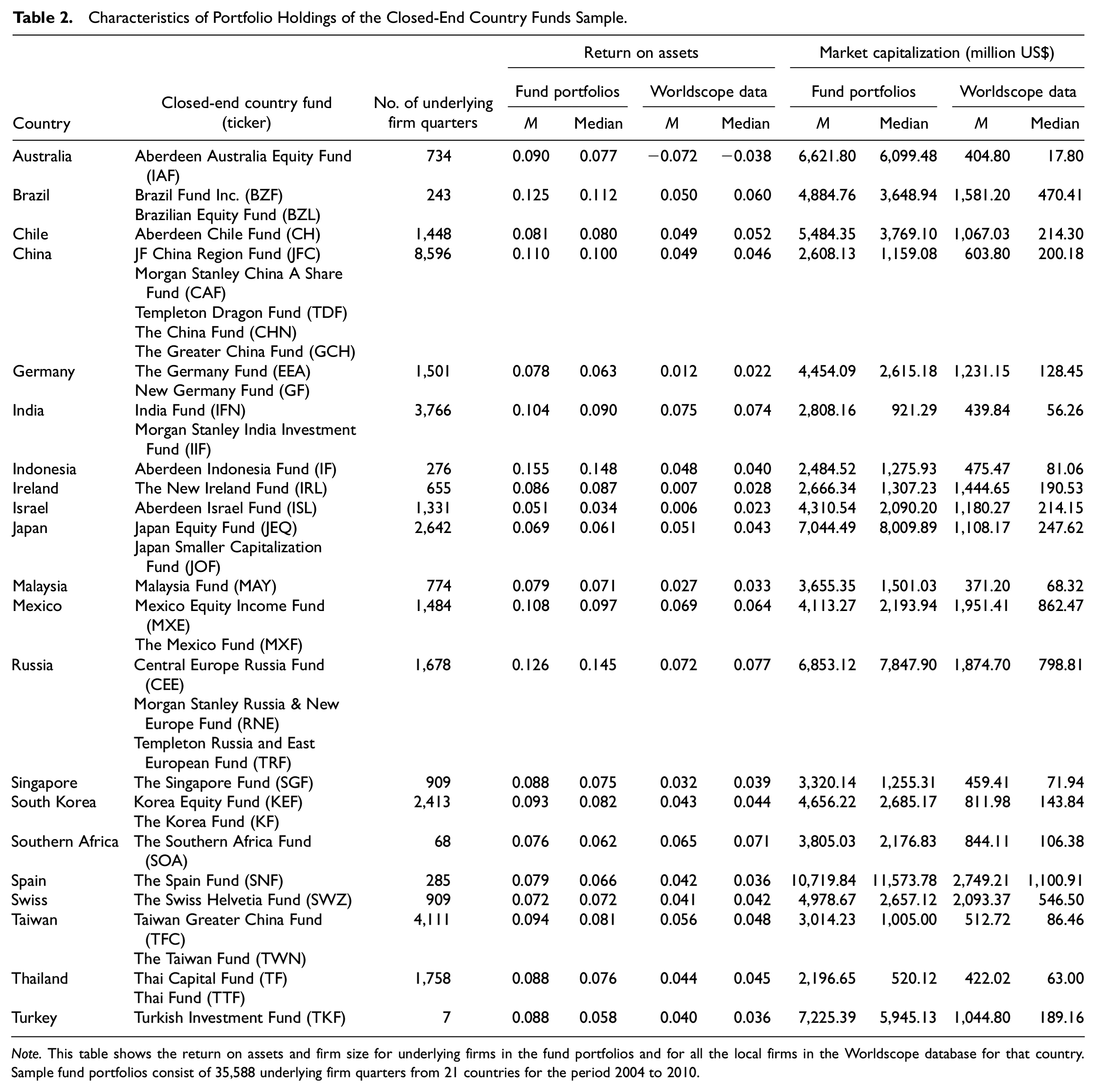

Table 2 presents firm characteristics of the underlying firms in the country fund holdings. For comparison, we also report the firm characteristics of all local firms for that country in the Worldscope universe. Across all the sample countries, firms in the closed-end country fund portfolios have a higher mean or median value of market capitalization and return on assets than the full sample of firms from that country in the Worldscope database. This descriptive evidence is consistent with that of Covrig, Lau, and Ng (2006), who found that closed-end country funds tend to invest in large and well-performing firms.

Characteristics of Portfolio Holdings of the Closed-End Country Funds Sample.

Note. This table shows the return on assets and firm size for underlying firms in the fund portfolios and for all the local firms in the Worldscope database for that country. Sample fund portfolios consist of 35,588 underlying firm quarters from 21 countries for the period 2004 to 2010.

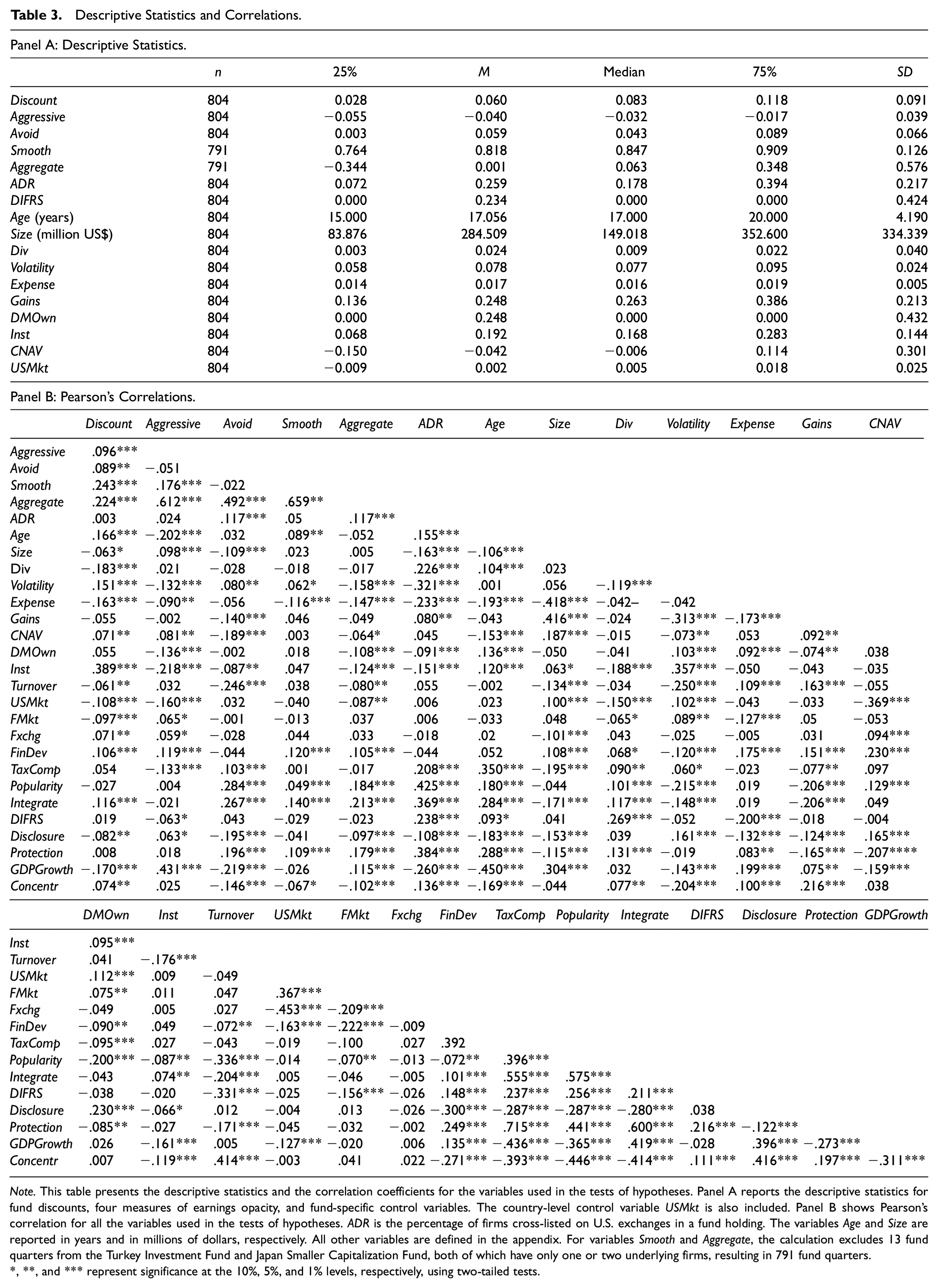

Table 3, Panel A, presents descriptive statistics for all variables. 18 The mean (median) closed-end country fund discount for our sample is 6.0% (8.3%), close to the average fund discount of 6.4% as reported by J. S. P. Chan et al. (2008) for an earlier sample period (1987-2001). On average, the fund expense ratio is 1.7%, and the dividend yield is 2.4% across the 36 funds. Unrealized capital gains over the fund’s NAVs have a mean (median) value of 24.8% (26.3%). The average fund age is 17 years. These funds have an average market capitalization of US$284.5 million and institutional ownership of 19.2%. The average relative liquidity of the U.S. market versus the local market is 1.57. Our measures of earnings opacity show a mean value of 0.001 for the aggregate measure (Aggregate), −0.040 for earnings aggressiveness (Aggressive), 0.059 for loss avoidance (Avoid), and 0.818 for earnings smoothing (Smooth).

Descriptive Statistics and Correlations.

Note. This table presents the descriptive statistics and the correlation coefficients for the variables used in the tests of hypotheses. Panel A reports the descriptive statistics for fund discounts, four measures of earnings opacity, and fund-specific control variables. The country-level control variable USMkt is also included. Panel B shows Pearson’s correlation for all the variables used in the tests of hypotheses. ADR is the percentage of firms cross-listed on U.S. exchanges in a fund holding. The variables Age and Size are reported in years and in millions of dollars, respectively. All other variables are defined in the appendix. For variables Smooth and Aggregate, the calculation excludes 13 fund quarters from the Turkey Investment Fund and Japan Smaller Capitalization Fund, both of which have only one or two underlying firms, resulting in 791 fund quarters.

, **, and *** represent significance at the 10%, 5%, and 1% levels, respectively, using two-tailed tests.

Panel B presents the Pearson correlations among these variables. Consistent with H1, this table shows positive and statistically significant correlations between the fund discounts and all four measures of earnings opacity.

Results for H1

Panel A of Table 4 presents statistics of fund discounts sorted on earnings opacity. The panel shows the mean and median values of fund discounts across quartiles of the opacity measures. For all four opacity proxies, we find that fund discounts increase across the quartiles of earnings opacity. For example, using Aggregate, the average fund discount increases from 0.036 in the first quartile to 0.077 in the fourth quartile, with the difference being statistically significant at the 1% level. In summary, the univariate tests in Panel A support H1 that fund discounts are positively correlated with earnings opacity.

The Relation Between Fund-Level Earnings Opacity and Fund Discounts.

Note. This table presents the relation between fund-level earnings opacity and fund discounts. Panel A shows the mean and median values of fund discounts across quartiles of the four earnings opacity measures. Panel B reports the regressions of closed-end country fund discounts on various proxies of fund-level earnings opacity and control variables. All variables are defined in the appendix. Quarter and/or country fixed effects are included. In Models (5) and (6), country fixed effects are included, so the variable Concentr is excluded as it is a fixed country-level variable. In Panel B, the t values are based on standard errors that are clustered by fund and quarter.

, **, and *** represent significance at the 10%, 5%, and 1% levels, respectively, using two-tailed tests.

Panel B reports the results of multivariate analyses that control for other variables which could affect fund discounts. The adjusted R2 values of the models range between .332 and .384 for Models (1) to (4) using the four measures of earnings opacity. Consistent with J. S. P. Chan et al. (2008), we find that the fund discount is negatively related to the overall market trends of U.S. and foreign markets (USMkt and FMkt) and positively associated with institutional ownership (Inst) and underlying stock volatility (Volatility). The results also show a lower fund discount for funds with higher dividend yields (Div), consistent with the findings shown in Hwang (2011). Moreover, a positive coefficient on Integrate is consistent with our expectation of lower fund discounts when a host market is more segmented.

Importantly, all of the four earnings opacity proxies are positively associated with the fund discounts at a significance level of .05 or better (using two-tailed tests) after controlling for an extensive set of factors motivated by prior research. In addition to being statistically significant, the positive relation is economically meaningful. Focusing on Aggregate, when moving from the median to the third quartile of Aggregate (while holding other variables constant), the fund discount increases by 1.31%, which is approximately 21.8% (15.7%) of the mean (median) of fund discounts. In addition, an untabulated analysis reveals that the incremental adjusted R2 due to Aggregate is 4.2%. These results suggest that U.S. investors take into account their information disadvantage, as aggravated by opaque accounting information, in their pricing of fund shares by setting a lower fund price relative to the fund’s NAV.

As described above, given that our empirical model includes time-varying country-level control variables, we can simultaneously include these controls and country fixed effects. We assess the impact of different combinations of country controls in Models (4) to (6). Model (4) includes the specific country controls but excludes country fixed effects; Model (5) employs only country fixed effects; and Model (6) uses both sets of control variables. 19 For all three models, the coefficient estimate for Aggregate is virtually identical and is statistically significant. We further note the significant increase in explanatory power when both specific country controls and country fixed effects are included (an untabulated analysis indicates an increase in the adjusted R2 of about 13.6 percentage points from the regression model without country controls or fixed effects). Based on this finding, in the following sections we only present results that include both time-varying country-level control variables and country fixed effects.

Results for H2 and H3

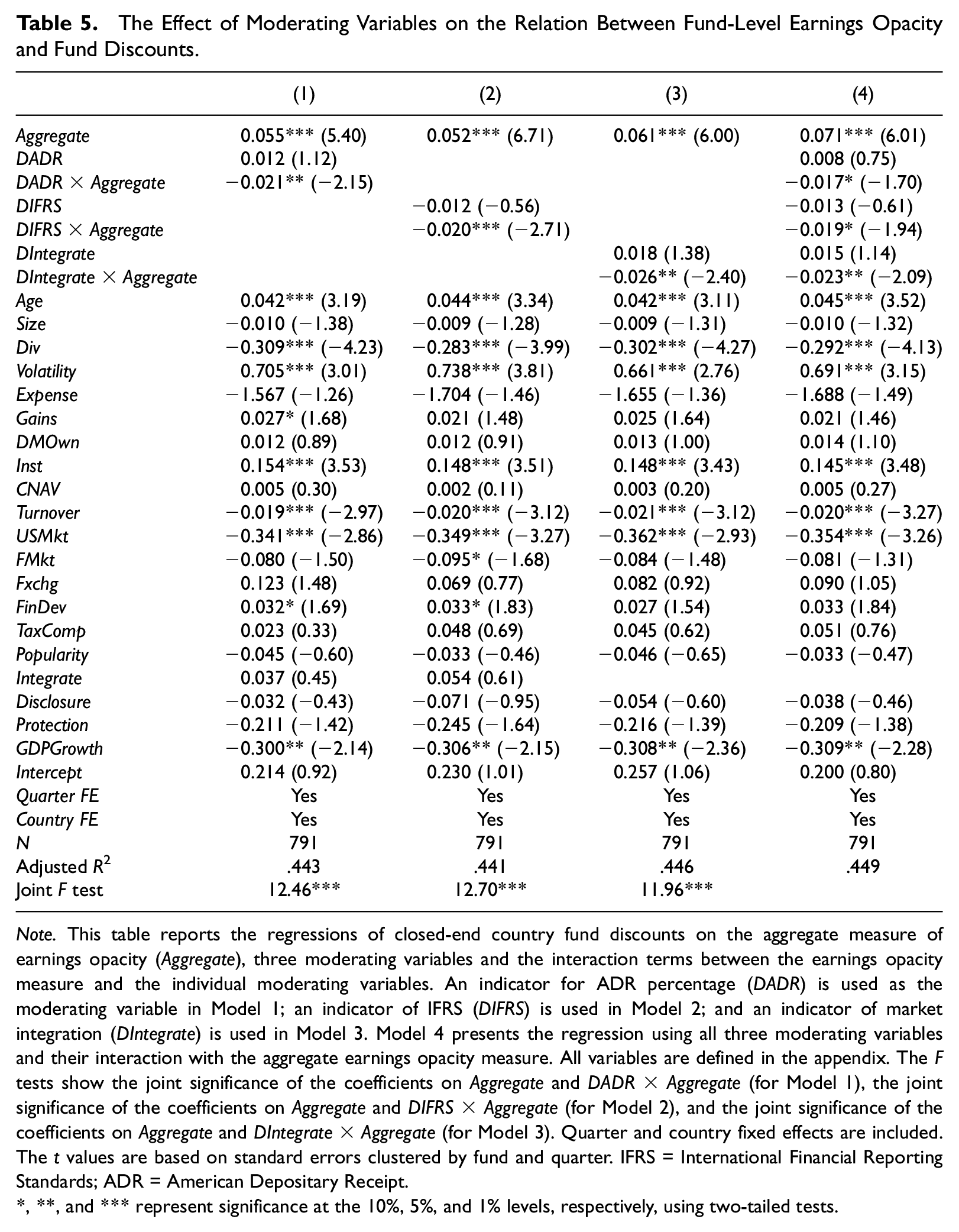

Table 5 reports the results for the tests of H2 and H3 using Aggregate as the earnings opacity proxy. In Model (1), we use the fund holdings of U.S. cross-listed firms to proxy for the lower costs for fund investors to acquire and process information about local firms in a fund’s portfolio. Consistent with H2a, the impact of earnings opacity on fund discounts is significantly weaker for funds with a higher holding of U.S. cross-listed firms. Specifically, we find a negative and statistically significant coefficient on the interaction term of Aggregate with DADR (coefficient = −0.021, t value = −2.15). 20

The Effect of Moderating Variables on the Relation Between Fund-Level Earnings Opacity and Fund Discounts.

Note. This table reports the regressions of closed-end country fund discounts on the aggregate measure of earnings opacity (Aggregate), three moderating variables and the interaction terms between the earnings opacity measure and the individual moderating variables. An indicator for ADR percentage (DADR) is used as the moderating variable in Model 1; an indicator of IFRS (DIFRS) is used in Model 2; and an indicator of market integration (DIntegrate) is used in Model 3. Model 4 presents the regression using all three moderating variables and their interaction with the aggregate earnings opacity measure. All variables are defined in the appendix. The F tests show the joint significance of the coefficients on Aggregate and DADR×Aggregate (for Model 1), the joint significance of the coefficients on Aggregate and DIFRS×Aggregate (for Model 2), and the joint significance of the coefficients on Aggregate and DIntegrate×Aggregate (for Model 3). Quarter and country fixed effects are included. The t values are based on standard errors clustered by fund and quarter. IFRS = International Financial Reporting Standards; ADR = American Depositary Receipt.

, **, and *** represent significance at the 10%, 5%, and 1% levels, respectively, using two-tailed tests.

Model (2) shows a negative and significant coefficient on the interaction term between Aggregate and DIFRS (coefficient = −0.020, t value = −2.71). 21 This finding indicates that the effects of earnings opacity on fund discounts are less pronounced for funds with more familiar financial reporting practices, supporting H2b. 22

Consistent with H3, Model (3) shows a negative and significant coefficient on the interaction between Aggregate and the proxy for international financial integration (DIntegrate; coefficient = −0.026, t value = −2.40). 23 Such a negative coefficient implies that the effect of earnings opacity on fund discounts is less pronounced for foreign firms in more integrated markets.

Finally, we stack all moderating variables in Model (4) and continue to find results consistent with H2 and H3. In addition to being of interest by themselves, these findings lend further credence to the results for H1 as reported in Table 4. That is, we observe cross-sectional variations in the main effects of earnings opacity as predicted by economic theory and prior research.

Additional Analyses and Robustness Tests

We conduct a series of sensitivity tests, and for the sake of brevity we do not tabulate the results.

First, we provide results using a changes specification. Specifically, we compute year-over-year changes in both dependent and independent variables (i.e., comparing the current quarter with the same quarter for the prior year) and estimate regression Equation 1 using the differenced variables. We still include quarter fixed effects in the regression and cluster standard errors by fund and quarter. Country fixed effects are differenced out, and hence are excluded from the regression. The untabulated analysis shows that, after controlling for changes in other determinants of fund discounts, an increase in earnings opacity is positively related to an increase in fund discounts as evidenced by the positive coefficients on the change of aggregate earnings opacity (ΔAggregate; coefficients = 0.036; t values = 4.45, respectively).

Second, we repeat our tests using alternative measures of opacity. The first is Dechow and Dichev’s (2002) accruals quality measure (as modified by McNichols, 2002). The second measure is earnings–return relations following Francis and Schipper (1999) and Bushman, Chen, Engel, and Smith (2004). For the second measure, we estimate the explained variability from the regression of stock returns on the level and change in earnings. The regression is estimated for each fund-quarter portfolio holdings by using the underlying firms’ financial data over the previous 4 years. The negative value of the adjusted R2 from the regression (NegRelev) is the alternative measure of earnings opacity. A larger value of NegRelev implies a lower value relevance of earnings, and thus a higher degree of earnings opacity. Our inferences remain the same for these two alternative opacity measures (untabulated).

Third, we include additional control variables in the regressions. Specifically, we further control for three factors related to how familiar U.S. fund investors are likely to be with firms from a particular foreign country: (a) the amount of bilateral trade (from the United Nations Commodity Trade Statistics database), (b) geographical proximity measured as the bilateral distance between the capital cities of the two countries (from www.mapsofworld.com), and (c) an indicator variable for common language (using data compiled from the World Factbook 2010). Then, we include a control for currency crises (Glick & Hutchison, 2011). Furthermore, we consider the role of auditing by including an indicator variable that is equal to 1 for those funds whose percentage of underlying firms being audited by Big-4 auditors is above the sample median (0 otherwise) in the regression. No inferences are affected when we include these additional control variables.

Finally, to control for any fund “style” or “fund manager quality” fixed effects that may not be picked up by our control variables, we rerun the analyses using fund fixed effects (and hence exclude the country fixed effects). The results are similar to those reported in previous sections (untabulated). 24

Conclusion

This is the first study to examine whether the quality of financial reporting information affects closed-end country fund discounts. We take advantage of the unique feature that these funds essentially have “two prices”—the price of the fund as quoted on a U.S. stock exchange and the price of the underlying assets in the local market (i.e., the NAV of the fund). When investing in the foreign assets, U.S. investors have to incur higher information acquisition and processing cost and have access to limited information channels, thereby suffering from an information disadvantage compared with local investors. We expect that the opaqueness of earnings information from the underlying local firms exacerbates U.S. investors’ information disadvantage. Our main hypothesis extends prior studies on how information asymmetry between foreign and local investors affects equity prices (e.g., K. Chan et al., 2008). To the extent that earnings opacity exacerbates U.S. investors’ information disadvantage, we posit that greater earnings opacity of the underlying firms in a fund portfolio contributes to a larger fund discount.

To test this hypothesis, we use a sample of 804 fund-quarter observations based on 35,588 underlying firm-quarter observations. For these fund observations, we estimate fund-level earnings opacity using three individual measures widely employed in prior literature as well as an aggregate measure. After controlling for numerous factors known to affect country fund discounts as well as quarter, country, and fund fixed effects, we find strong evidence consistent with our hypothesis that fund-level earnings opacity is positively associated with fund discounts. These results suggest that U.S. investors respond to their information disadvantage caused by opaque earnings information by setting a lower fund price (relative to fund NAV).

We further show that the positive association between fund discounts and earnings opacity is mitigated by holding a high percentage of firms cross-listed in the United States, by use of IFRS, and by high financial integration between local and U.S. markets. Our results are robust to changes specification, to alternative earnings opacity proxies, and to alternative proxies for information costs.

Footnotes

Appendix

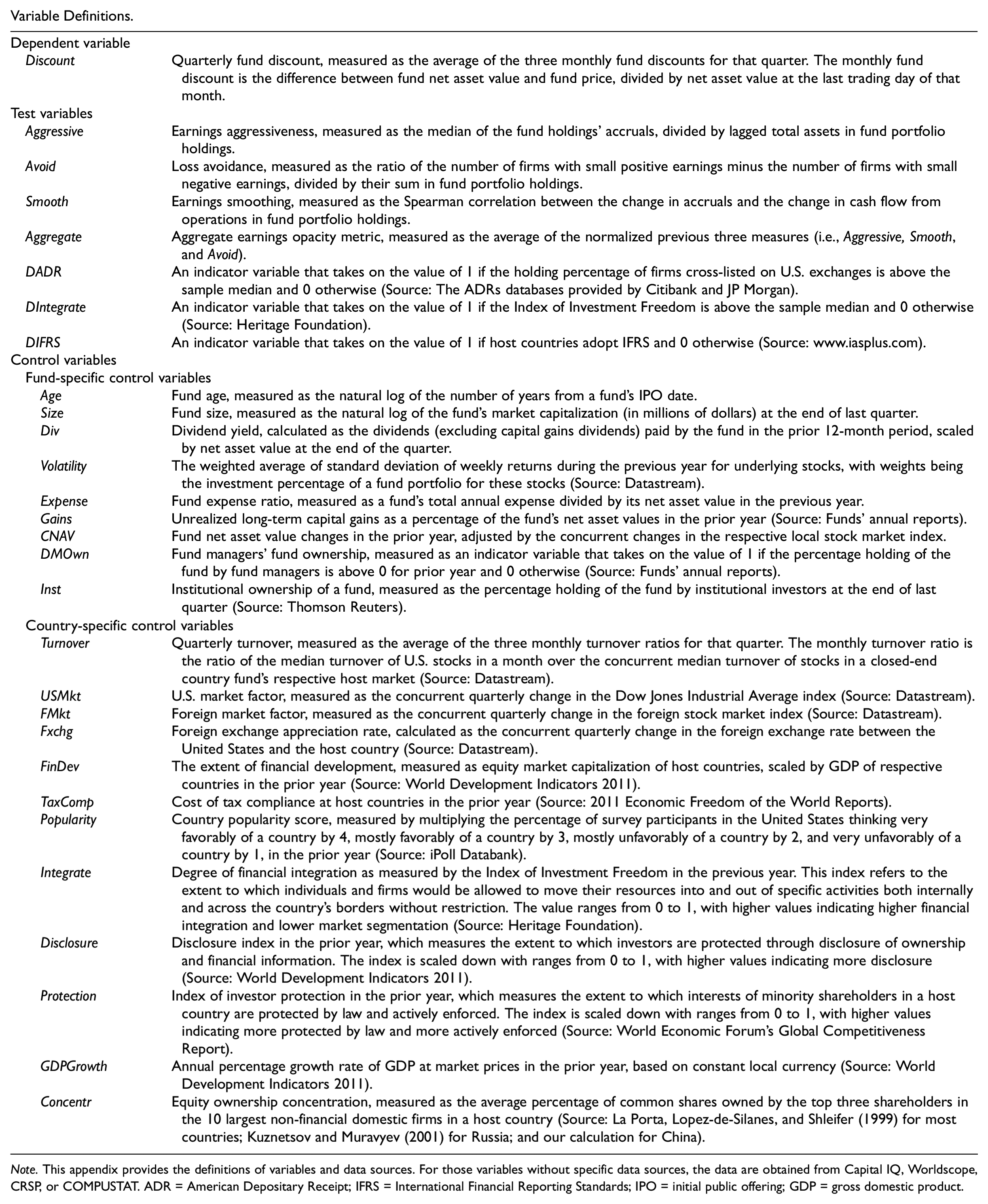

Variable Definitions.

| Dependent variable | |

| Discount | Quarterly fund discount, measured as the average of the three monthly fund discounts for that quarter. The monthly fund discount is the difference between fund net asset value and fund price, divided by net asset value at the last trading day of that month. |

| Test variables | |

| Aggressive | Earnings aggressiveness, measured as the median of the fund holdings’ accruals, divided by lagged total assets in fund portfolio holdings. |

| Avoid | Loss avoidance, measured as the ratio of the number of firms with small positive earnings minus the number of firms with small negative earnings, divided by their sum in fund portfolio holdings. |

| Smooth | Earnings smoothing, measured as the Spearman correlation between the change in accruals and the change in cash flow from operations in fund portfolio holdings. |

| Aggregate | Aggregate earnings opacity metric, measured as the average of the normalized previous three measures (i.e., Aggressive, Smooth, and Avoid). |

| DADR | An indicator variable that takes on the value of 1 if the holding percentage of firms cross-listed on U.S. exchanges is above the sample median and 0 otherwise (Source: The ADRs databases provided by Citibank and JP Morgan). |

| DIntegrate | An indicator variable that takes on the value of 1 if the Index of Investment Freedom is above the sample median and 0 otherwise (Source: Heritage Foundation). |

| DIFRS | An indicator variable that takes on the value of 1 if host countries adopt IFRS and 0 otherwise (Source: www.iasplus.com). |

| Control variables | |

| Fund-specific control variables | |

| Age | Fund age, measured as the natural log of the number of years from a fund’s IPO date. |

| Size | Fund size, measured as the natural log of the fund’s market capitalization (in millions of dollars) at the end of last quarter. |

| Div | Dividend yield, calculated as the dividends (excluding capital gains dividends) paid by the fund in the prior 12-month period, scaled by net asset value at the end of the quarter. |

| Volatility | The weighted average of standard deviation of weekly returns during the previous year for underlying stocks, with weights being the investment percentage of a fund portfolio for these stocks (Source: Datastream). |

| Expense | Fund expense ratio, measured as a fund’s total annual expense divided by its net asset value in the previous year. |

| Gains | Unrealized long-term capital gains as a percentage of the fund’s net asset values in the prior year (Source: Funds’ annual reports). |

| CNAV | Fund net asset value changes in the prior year, adjusted by the concurrent changes in the respective local stock market index. |

| DMOwn | Fund managers’ fund ownership, measured as an indicator variable that takes on the value of 1 if the percentage holding of the fund by fund managers is above 0 for prior year and 0 otherwise (Source: Funds’ annual reports). |

| Inst | Institutional ownership of a fund, measured as the percentage holding of the fund by institutional investors at the end of last quarter (Source: Thomson Reuters). |

| Country-specific control variables | |

| Turnover | Quarterly turnover, measured as the average of the three monthly turnover ratios for that quarter. The monthly turnover ratio is the ratio of the median turnover of U.S. stocks in a month over the concurrent median turnover of stocks in a closed-end country fund’s respective host market (Source: Datastream). |

| USMkt | U.S. market factor, measured as the concurrent quarterly change in the Dow Jones Industrial Average index (Source: Datastream). |

| FMkt | Foreign market factor, measured as the concurrent quarterly change in the foreign stock market index (Source: Datastream). |

| Fxchg | Foreign exchange appreciation rate, calculated as the concurrent quarterly change in the foreign exchange rate between the United States and the host country (Source: Datastream). |

| FinDev | The extent of financial development, measured as equity market capitalization of host countries, scaled by GDP of respective countries in the prior year (Source: World Development Indicators 2011). |

| TaxComp | Cost of tax compliance at host countries in the prior year (Source: 2011 Economic Freedom of the World Reports). |

| Popularity | Country popularity score, measured by multiplying the percentage of survey participants in the United States thinking very favorably of a country by 4, mostly favorably of a country by 3, mostly unfavorably of a country by 2, and very unfavorably of a country by 1, in the prior year (Source: iPoll Databank). |

| Integrate | Degree of financial integration as measured by the Index of Investment Freedom in the previous year. This index refers to the extent to which individuals and firms would be allowed to move their resources into and out of specific activities both internally and across the country’s borders without restriction. The value ranges from 0 to 1, with higher values indicating higher financial integration and lower market segmentation (Source: Heritage Foundation). |

| Disclosure | Disclosure index in the prior year, which measures the extent to which investors are protected through disclosure of ownership and financial information. The index is scaled down with ranges from 0 to 1, with higher values indicating more disclosure (Source: World Development Indicators 2011). |

| Protection | Index of investor protection in the prior year, which measures the extent to which interests of minority shareholders in a host country are protected by law and actively enforced. The index is scaled down with ranges from 0 to 1, with higher values indicating more protected by law and more actively enforced (Source: World Economic Forum’s Global Competitiveness Report). |

| GDPGrowth | Annual percentage growth rate of GDP at market prices in the prior year, based on constant local currency (Source: World Development Indicators 2011). |

| Concentr | Equity ownership concentration, measured as the average percentage of common shares owned by the top three shareholders in the 10 largest non-financial domestic firms in a host country (Source: La Porta, Lopez-de-Silanes, and Shleifer (1999) for most countries; Kuznetsov and Muravyev (2001) for Russia; and our calculation for China). |

Note. This appendix provides the definitions of variables and data sources. For those variables without specific data sources, the data are obtained from Capital IQ, Worldscope, CRSP, or COMPUSTAT. ADR = American Depositary Receipt; IFRS = International Financial Reporting Standards; IPO = initial public offering; GDP = gross domestic product.

Acknowledgements

The authors thank Karthik Balakrishnan, Francesco Bova, Ling Cen, Qi Chen, Gus De Franco, David Godsell, Yu Hou, Eric Kirzner, Matthew Lyle, Bin Miao, Partha Mohanram, Sebastian Mueller, Chul Park, Mikhail Pevzner, Wendy Rotenberg, Nemit Shroff, Kevin Veenstra, Aazam Virani, Hila Fogel Yaari, Youli Zou, and workshop participants at the Financial Accounting and Reporting Section (FARS) Mid-Year Meeting (Chicago); the International Accounting Section (IAS) Mid-Year Meeting (Phoenix); the European Accounting Association (EAA) Annual Congress (Ljubljana); the CAAA Annual Meeting (Charlottetown); the American Accounting Association (AAA) Annual Meeting (Washington D.C.); the Conference on Investor Protection, Corporate Governance, and Fraud Prevention (George Mason University); 24th Asia-Pacific Conference on International Accounting Issues (APCIAI) Conference, the Chinese Accounting Professors’ Association of North America (CAPANA) conference (Hong Kong); Rotman School of Management, Norwegian School of Economics; and Shanghai University of Finance and Economics for helpful comments.

Author’s Note

Ole-Kristian Hope is currently affiliated with Rotman School of Management at University of Toronto and BI Norwegian Business School.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Chen acknowledges the financial support of the Social Sciences and Humanities Research Council of Canada (SSHRC). Hope acknowledges the financial support of the Deloitte Professorship. Li acknowledges the financial support of Wuhan University and the National Natural Science Foundation of China (NSFC; Project No. 71272228). Wang acknowledges the financial support of the General Research Fund of Hong Kong Research Grants Council (Project No. 754312).