Abstract

We study the ex ante stock market reactions to events leading up to China’s convergence to International Financial Reporting Standards (IFRS). The literature consistently shows that the benefits of mandatory IFRS convergence are concentrated in countries with stronger legal enforcement and investor protection. Given that these institutional characteristics are weaker in China relative to more developed Western economies, whether mandating IFRS will benefit the Chinese capital market is an interesting and important, but unanswered question. We find that the Chinese stock market reacts favorably to events leading up to IFRS convergence, and this effect is more pronounced among firms with greater dependence on external capital. This result suggests the market anticipates that such firms will benefit more from IFRS convergence, possibly because of improved financial reporting quality and access to external financing. Additional tests confirm that the value relevance of accounting numbers for these firms is higher following IFRS convergence.

Keywords

Introduction

We examine the stock market reactions to events leading up to China’s convergence to International Financial Reporting Standards (IFRS) in 2007. 1 We have two important motivations for examining the IFRS experience in China. First, from a policy-making perspective, China is the first among the large emerging economies known as BRICs (Brazil, Russia, India, and China) to adopt or converge to IFRS. Second, from an academic perspective, China provides a useful research setting for evaluating the impact of IFRS because of its unique institutional structures.

Mounting empirical evidence from cross-country analyses (e.g., Byard, Li, & Yu, 2011; Daske, Hail, Leuz, & Verdi, 2008; Kim & Shi, 2012; Li, 2010) reveals that the benefits of mandatory IFRS adoption (or convergence) are dependent on strong legal enforcement and investor protection. 2 Because China has a relatively weaker institutional environment (Allen, Qian, & Qian, 2005; Morck, Yeung, & Yu, 2000) than those of more developed Western economies, it is unclear whether it meets the prerequisites to render IFRS beneficial. Hence, studying the effect of IFRS convergence in China is an interesting and important question. Indeed, existing studies of the ex post impact of IFRS convergence in China have yielded mixed and marginal evidence of benefits (e.g., He, Wong, & Young, 2012; Liu, Yao, Hu, & Liu, 2011). Unlike those studies, we examine the ex ante implications of IFRS convergence in China. We do so by analyzing the stock market reactions to important events leading up to China’s convergence to IFRS. This approach allows us to assess whether investors, as end users of financial statement information, viewed movements toward IFRS convergence favorably. It also facilitates a more objective assessment of the expected economic implications of IFRS convergence, rather than the relatively more subjective assessments (such as earnings management) used in prior research.

It is widely accepted that principles-based accounting standards such as IFRS increase the scope of managerial judgment and facilitate communication of economic substance to end users of financial statements vis-à-vis rules-based standards that focus more on legal form (Nobes, 2005; Schipper, 2003). The Chinese domestic accounting standards prior to IFRS were largely rules-based and highly prescriptive (The Institute of Chartered Accountants of Scotland, 2010). This suggests that investors are likely to react favorably to the convergence to IFRS in anticipation of improved financial reporting quality. However, the increased discretion under IFRS may lead to greater use of opportunism in financial reporting, leading investors to react unfavorably to the convergence. We provide empirical evidence on whether market participants view IFRS convergence favorably or unfavorably.

Extant accounting research documents the influence of incentives on financial reporting quality (Ball, Robin, & Wu, 2003) and the consequence of mandatory IFRS adoption (Daske et al., 2008). An important determinant of firms’ disclosure incentives is communication with outside investors. In China, this incentive is related closely to a unique factor, state ownership (Gul, Kim, & Qiu, 2010). State ownership is a distinctive feature of Chinese listed firms relative to their counterparts in Western-style economies (“The Rise of State Capitalism,” 2012). Because of its sociopolitical ideology, the government maintains majority ownership of a large number of firms. State-owned enterprises (SOEs) are endowed with financial support from the government, such as subsidies and favorable loans from state banks, to help reduce their financial constraints and default risks (H. Chen, Chen, Lobo, & Wang, 2010). In contrast, nonstate-owned enterprises (NSOEs) rely heavily on equity financing and need high-quality financial reporting to communicate with outside investors (Chen, Chen, Lobo, & Wang, 2011).

If the IFRS convergence in China is more beneficial to NSOEs than SOEs, we predict that investors of NSOEs respond more positively to the IFRS convergence than do investors of SOEs. In addition, if investors’ favorable reactions to NSOEs indeed reflect potentially improved information quality and facilitate external communication and financing, then the positive market reactions are more pronounced among NSOEs with greater financing needs.

To test these predictions, we follow the event study methodology used by Armstrong, Barth, Jagolinzer, and Riedl (2010) and Joos and Leung (2012) and investigate 3- and 5-day cumulative market-adjusted returns (CMAR, hereafter) of stocks listed on the Shanghai and the Shenzhen stock exchanges, centered on seven events that provide incremental information on the progress toward Chinese IFRS convergence. We use a research design that compares these returns between a treatment group of firms that issue only A-shares and therefore only began reporting under IFRS after the mandatory convergence in 2007, 3 and a control group of firms that issue B-shares and therefore were already reporting under International Accounting Standards (IAS) prior to IFRS convergence in 2007. 4

Our findings are as follows. First, we find a significantly greater positive market reaction for the treatment group (i.e., A-shares only firms). Second, within the treatment group, the positive market reaction is more pronounced for NSOEs than for SOEs. Third, among the NSOEs in the treatment group, the positive market reaction is more pronounced for firms with greater financing needs. These results imply that investors perceive that Chinese listed firms with stricter financial constraints and higher financing needs will benefit more from mandatory IFRS adoption, possibly because of improved information that will be provided to outside investors.

To provide evidence of improved financial reporting quality after IFRS convergence, we examine value relevance among NSOEs of the treatment group using both price and return models. We find a significantly greater increase in the value relevance of NSOEs that have greater financial needs. This increase in the sensitivity of market valuation to accounting information suggests that accounting disclosure has become more informative under IFRS. In other words, our value relevance tests provide ex post evidence that corroborates our pre-IFRS market reaction results regarding firms that are most likely to be affected by mandatory IFRS convergence.

Our findings have implications for both academics and policy makers. From the academic point of view, our findings differ from the results of existing cross-country studies, which indicate that mandating IFRS is not beneficial in countries without strong institutional structures. We show that investors in countries with weak legal enforcement and investor protection do expect mandatory IFRS convergence to be beneficial, especially for firms that are more dependent on external capital and, therefore, have greater incentives to attract investors with high-quality financial reporting. In addition, unlike the existing literature that studies the ex post consequences of IFRS convergence in China (e.g., He et al., 2012; Liu et al., 2011), our study is the first to document ex ante evidence in this setting. Furthermore, our findings imply that investors perceive that IFRS has the potential to reduce the disadvantage of firms that do not receive government support in the Chinese-style state capitalism.

From the perspective of policy makers, our findings confirm that the convergence toward IFRS in China has significant consequences for investors (i.e., in terms of value relevance) instead of being merely a political decision in response to the thrust of international accounting harmonization. Given the influential status of China as an emerging economy, the IFRS experience we document also has important implications for other emerging economies around the world.

Our study is organized as follows. “Literature and Hypotheses Development” section reviews the literature and develops our hypotheses, “Research Design” section describes our methodology and samples, “Empirical Findings” section presents our empirical findings, and “Conclusion” section concludes.

Literature and Hypotheses Development

Impact of Mandatory IFRS Adoption/Convergence

IFRS are believed to provide accurate, comprehensive, and timely financial information. Ball (2006) suggests that investors are better off under IFRS due to the improved information efficiency and reduced information costs. Armstrong et al. (2010) examine European stock market reactions to events related to mandatory IFRS adoption and show incrementally more positive market reactions among firms with greater information asymmetry. They interpret this result as evidence that investors expect a net information quality benefit from the new accounting standards. Applying a similar methodology, Joos and Leung (2012) examine investor perception of 15 events associated with potential IFRS adoption in the United States, and also document an overall positive market reaction to events that enhance the likelihood of adoption. Other studies of the economic consequences of mandatory IFRS adoption (or convergence) provide evidence of enhanced market liquidity (Daske et al., 2008), improved analyst forecasts (Byard et al., 2011; Tan, Wang, & Welker, 2011), increased foreign institutional ownership (DeFond, Hu, Hung, & Li, 2011), greater institutional holding (Florou & Pope, 2012), higher information comparability cross countries (Yip & Young, 2012), reduced cost of equity capital (Lee, Walker, Christensen, & Zhao, 2010; Li, 2010), and lower Initial Public Offering (IPO) underpricing (Hong, Hung, & Lobo, 2014).

However, these benefits are not realized uniformly across all countries examined. Disclosure quality is determined not only by accounting standards but also by financial reporting incentives that can be shaped by legal and political institutions (Leuz, Nanda, & Wysocki, 2003). Ball et al. (2003) sample four East Asian countries with accounting standards deriving from common law origin (assumed to demand higher quality accounting disclosure) and show that the financial reporting quality of firms in these countries is no better than that in code law origin countries. Using an international sample across 30 countries, Daske, Hail, Leuz, and Verdi (2013) confirm that firms’ reporting incentives play an important role in explaining differences in capital market effects (i.e., price impact of trades, bid-ask spread, and cost of capital) around IAS adoptions.

In emerging countries and transitional economies where institutional reforms may not necessarily keep pace with IFRS convergence, the benefits of the switch to a new accounting regime are expected to be limited. Thus, to what extent China, as a transitional economy, can realize the intended benefits of IFRS convergence is an interesting question that warrants empirical investigation.

Development of Accounting Standards in China

On February 15, 2006, the Chinese Ministry of Finance officially declared the enactment of Accounting Standards for Business Enterprises. The International Accounting Standards Board (IASB) agrees that these standards are substantially converged with IFRS because they incorporate most of the IFRS standards.

Starting in fiscal year 2007, all firms listed on the Shanghai and the Shenzhen stock exchanges were required to report under the new standards. Convergence to IFRS resulted in 15 major changes, eight of which relate to fair value accounting (Deloitte Touche Tohmatsu, 2006). For example, the new standards allow the use of fair value to measure nonmonetary assets unless the exchange transaction lacks commercial substance, whereas the previous local standards used the carrying amount of the assets given up to measure the acquired assets.

Firms listed on the Shanghai and the Shenzhen exchanges can issue A-shares that are traded in the local currency (Renminbi [RMB]), and B-shares that are traded in U.S. dollars (in Shanghai) or Hong Kong dollars (in Shenzhen). The vast majority of Chinese listed firms issue only A-shares, which are mainly intended for domestic investors. A relatively smaller group of Chinese firms also issue B-shares, which are mainly intended for foreign investors. Before 2007, firms that issue only A-shares prepared financial statements under local accounting standards, while firms that issue both A-shares and B-shares needed to provide additional accounting information using IFRS. Given that firms that issue both A-shares and B-shares were already reporting under IFRS before 2007, we expect the 2007 IFRS convergence to mainly affect firms that issue only A-shares.

As discussed above, existing studies suggest that the benefits of mandating IFRS are largely confined to countries with strong legal enforcement and investor protection. These findings suggest that the weak legal infrastructure in China is likely to decrease the effects of mandatory IFRS convergence. Existing studies reveal mixed evidence on financial reporting quality in China after IFRS convergence. On one hand, Liu et al. (2011) provide evidence of marginal improvement in earnings quality after 2007. On the other hand, He et al. (2012) document greater earnings management, and show that this effect is more pronounced among firms with greater incentives to avoid reporting losses. 5 Given these conflicting findings, we believe that examining how investors, as end users of financial statements, perceive the 2007 adoption is an interesting question that can offer further insights into the implications of IFRS convergence.

Influence of Ownership Structure on Corporate Transparency of Chinese Firms

State control is one of the most distinctive features of China relative to developed Western economies. Since the early 1990s, many SOEs in China have been partially privatized and have issued shares to gain access to the capital market. However, central and local governments maintain controlling ownership of a large number of listed firms, and influence various important corporate decisions such as asset disposal, merger and acquisition, CEO appointment (H. Chen et al., 2010), and auditor selection (Wang, Wong, & Xia, 2008).

The success of SOEs helps boost the local economy as well as the local officials’ profiles for bureaucratic promotions. Thus, these officials have strong incentives to assist SOEs to prosper through financial support such as subsidies and preference loans from state-owned banks (Li, 1998). SOEs have little incentive to repay the preference loans as they are expected to provide public service for political and social objectives in return (Bai, Li, Tao, & Wang, 2000; Green, 2004). In contrast, NSOEs, which lack such government support, face greater financial constraints and default risk than SOEs (H. Chen, Chen, et al., 2011).

State control in China affects corporate transparency in two ways. First, it induces an entrenchment effect (Shleifer & Vishny, 1997), which encourages collusion between the controlling state shareholders and firm managers to extract benefits and divert resources at the expense of outside investors (Shleifer & Vishny, 1986; Claessens, Djankov, Fan, & Lang, 2002). Therefore, such firms may manipulate the release of price-sensitive information or withhold unfavorable information to cover up opportunistic and self-serving behaviors (Fan & Wong, 2005). Second, government financial support reduces SOEs’ dependence on equity market financing, thus adversely affecting the financial reporting incentive to cater to the information demands of outside investors. Empirical evidence reveals that, relative to NSOEs, SOEs exhibit a higher level of earnings management (Ding, Zhang, & Zhang, 2007), more pervasive use of small local auditors (Wang et al., 2008), less informative stock prices (Gul et al., 2010), less conservative financial reporting (H. Chen et al., 2010), and propping up of earnings through third-party transactions (Jian & Wong, 2010).

We expect that the mandating of IFRS in China differentially influences SOEs and NSOEs based on their reliance on stock market financing and incentives to communicate to investors with high-quality financial reporting.

Hypotheses Development

Principles-based accounting standards emphasize economic substance over form, giving firms the opportunity to convey more useful information that will help investors better assess firms’ future prospects and value (Schipper, 2003). Therefore, proponents of IFRS claim that it is a set of high-quality financial reporting standards that increase reporting transparency and enhance cross-border comparability of financial statements. Consistent with this claim, prior research documents several benefits of IFRS adoption, such as enhanced market liquidity (Daske et al., 2008), improved analyst forecasts (Byard et al., 2011; Tan et al., 2011), increased foreign institutional ownership (DeFond et al., 2011), greater institutional holding (Florou & Pope, 2012), higher information comparability cross countries (Yip & Young, 2012), reduced cost of equity capital (Lee et al., 2010; S. Li, 2010), and lower IPO underpricing (Hong et al., 2014). On the contrary, critics of IFRS claim that the associated costs of applying IFRS make it difficult to predict the overall effect of IFRS adoption (convergence). These costs include the costs of implementation and transition, and the costs of lower financial reporting quality due to increased opportunistic earnings management facilitated by the greater financial reporting discretion provided to management by the principles-based nature of the standards.

Better understanding of economic substance is especially useful to investors in formulating investment decisions in a high-growth and quick-changing environment such as China. Consequently, investors in Chinese listed firms will likely view the mandatory switch from rules-based accounting standards to principles-based IFRS favorably. If so, they will respond positively to news indicating progress toward IFRS convergence. However, given the weak legal institutions in China, the costs of enforcement are likely to be high and the potential for opportunistic earnings management considerable (He et al., 2012). As a result, the benefits of these new accounting standards may be more than offset by the unintended costs. In other words, whether investors will react positively or negatively to the events leading up to the adoption of IFRS in China is an empirical question.

Furthermore, the response should be more pronounced for firms that issue only A-shares (i.e., first-time IFRS adopters), than for firms that also have B-shares and that are already reporting under IFRS. In other words, the firms with only A-shares serve as the treatment group whereas the firms with A-shares and B-shares serve as the control group.

Given these arguments, we examine the net effect of IFRS convergence and hypothesize the following (in null form):

Ownership structure influences corporate financing decisions, which in turn could affect firms’ financial reporting incentives. Prior research documents that financial reporting incentives affect accounting disclosure quality (Ball et al., 2003) and the benefits of mandatory IFRS adoption (Daske et al., 2008), and that investors are able to differentiate firms’ reporting incentives to evaluate reporting quality (Daske et al., 2013). Chinese NSOEs receive little financial support from the government and have more difficulty obtaining bank financing (the largest source of external financing in China), making them more dependent on the equity market for raising capital than their state-owned counterparts. This greater reliance on the equity market increases their financial reporting incentives, as they must cater more to the information demands of outside investors. The switch from rules-based standards to principles-based IFRS will enable NSOEs to better communicate their economic performance and position to outside investors. Consequently, NSOE investors should benefit more from the convergence to IFRS than should SOE investors.

However, the stronger incentives of NSOEs to communicate with outside investors may suggest better ex ante financial reporting quality relative to SOEs even before the IFRS convergence. Therefore, whether NSOEs will have more or less incremental benefit from IFRS convergence compared with SOEs remains an empirical question.

In summary, we anticipate greater transparency improvement among NSOEs if the facilitated communication under the principles-based accounting standards is achieved.

We formally state the hypothesis as follows:

Firms that require greater capital investment are likely to have greater need for external financing. Such firms have a stronger incentive to attract outside investors, and can do so by providing more transparent reports that more clearly convey their economic substance. In other words, firms with greater need for external financing are more likely to benefit from the principles-based reporting under IFRS. Thus, if NSOE investors indeed react more favorably to the news of IFRS convergence because they depend more on equity financing, then the increase in market reaction with demand for external capital should be more pronounced for NSOEs than for SOEs.

Therefore, we hypothesize the following:

Research Design

Description of Events and Sample

We identify seven events in the years 2005 and 2006 that indicate the progress toward IFRS convergence in China. In particular, these events reflect the government’s continued effort to make the IFRS convergence a smooth transition before the new IFRS-based standards took effect in 2007. 6 These events were reported in the major financial media in China, such as China Securities Journal (or Zhongguo Zhengquan Bao), Shanghai Securities News (or Shanghai Zhengquan Bao), and Sina Finance (http://finance.sina.com.cn), and in the website of the China Accounting Standards Committee (CASC; http://www.casc.gov.cn/gnxw/), which is affiliated with the Ministry of Finance and is the main authority on accounting standards and policy setting in China. We exclude events that either merely reconfirmed earlier developments or were considered to have an ambiguous effect.

To mitigate the effect of potentially confounding news that might have been released during the event windows, we check China Securities Journal (or Zhongguo Zhengquan Bao) and Shanghai Securities News (or Shanghai Zhengquan Bao) for non-IFRS related news during each event window. Like Armstrong et al. (2010), we do find events unrelated to IFRS convergence in some of the event windows. However, it is unlikely that the effects of these irrelevant events bias the results consistently in favor of our hypotheses across all events.

The seven sampled events are reported in Appendix A. Unlike in the United States (Joos & Leung, 2013), there was no public debate in China on the timeline for accounting convergence. All events indicate the government’s intention of advancing IFRS convergence in China. Therefore, the events are all considered to increase the likelihood of IFRS convergence, or to strengthen the enforcement and implementation environment of the forthcoming convergence.

The resulting events start from February 22, 2005, when China first stated its intention to bilaterally cooperate with the European Union to formulate and implement accounting standards (Event 1). Following the initial intention, on September 6, 2005, the accounting standard setters of China, together with those of Japan and South Korea, declared their determination to converge with IFRS (Event 2). Third, on November 8, 2005, China and the IASB signed a joint statement announcing that the new Chinese accounting standards (CASs) would be substantively convergent with IFRS (Event 3). The meeting was co-chaired by Mr. Wang Jun, China’s Vice Minister of Finance and Secretary-General of the CASC, and Sir David Tweedie, IASB Chairman. 7 It made official the convergence of accounting standards in China and was a milestone in China’s accounting standard-setting program. As there was no public debate during the policy-making process, messages delivered in official meetings by the ministers are usually considered formal announcements of new policies to the public. Fourth, on November 21, 2005, China’s Vice Minister of Finance, Mr. Wang Jun, announced at the United Nations Conference on Trade and Development (UNCTAD) Intergovernmental Working Group of Experts on International Standards of Accounting and Reporting (ISAR) in Geneva that China would be more proactive in pushing accounting harmonization (Event 4). This speech echoed the key information of the joint statement with IASB on November 8 (Event 3), and signaled the importance of accounting convergence on the government agenda. Fifth, on December 8, 2005, Mr. Wang Jun, Chairman of the China Auditing Standards Board (CASB), and Mr. John Kellas, Chairman of the International Auditing and Assurance Standards Board (IAASB), signed a joint statement recognizing China’s achievement of progress toward international convergence of the new China Auditing Standards (CAuS) with the International Standards on Auditing (ISA) (Event 5). This progress showed China’s effort in ensuring a smooth transition to the new standards in all aspects. Sixth, on November 6, 2006, Professor Weiguo Zhang, a Chinese Accounting scholar and official in the China Securities Regulatory Commission (CSRC), was elected as an IASB committee member, marking a further involvement of China in IFRS globalization (Event 6). Seventh, on November 30, 2006, the CSRC required all top management of listed firms to attend mandatory training for the upcoming new accounting standards (Event 7). Such explicit effort before the implementation of IFRS-based new CASs was not commonly seen in other countries. Anecdotal evidence showed that the training was taken seriously and strictly conducted. 8

We require sampled firms to have data for all events, that is, they are included if they have data for all seven events in the cross-sectional analyses. Our full test sample comprises firms listed on either the Shanghai or the Shenzhen stock exchanges and includes 4,684 firm-event observations. 9 This includes 4,249 firm-event observations for our treatment group of firms that issue only A-shares, and 435 firm-event observations for our control group of firms that issue B-shares. We obtain data on firm characteristics and daily returns from the China Securities Market and Accounting Research (CSMAR) database, and daily returns data for the Hong Kong Hang Seng Index from Datastream. We winsorize each continuous variable at 0.5% and 99.5% to reduce the influence of extreme values.

Overall Market Reaction Tests

Following Armstrong et al. (2010), we first evaluate the overall Chinese stock market reaction to each of the events associated with IFRS convergence using 3-day CMAR centered on each event date. We do not adjust firm returns with the Shanghai and/or Shenzhen index, because these indices would include the anticipated effects of IFRS convergence and bias against finding accurate market reactions. Alternatively, we calculate CMAR for each event as the value-weighted Chinese A-share portfolio return adjusted by the Hong Kong Hang Seng Index return. There are two important reasons to use the Hong Kong Hang Seng Index as the benchmark. First, firms whose shares are traded on the Hong Kong market had already adopted IFRS prior to China’s IFRS convergence and so are less likely to be affected by the events. Second, Hong Kong is affiliated to China and, therefore, is exposed to similar regional economic shocks. 10

We use three approaches to examine the overall CMAR of the treatment group (i.e., firms with only A-shares) around the seven events. First, we test whether the mean portfolio event CMAR is positive. Second, we test whether the mean portfolio event CMAR is greater than the mean portfolio nonevent CMAR for the same Chinese A-share firms. To compute the mean portfolio nonevent CMAR, we first use all trading days in 2005 and 2006 that do not overlap with the seven event windows to calculate 153 three-day portfolio returns, and then subtract the corresponding 3-day return of the Hong Kong Hang Seng Index. Third, we use the bootstrap technique to test whether the treatment sample mean CMAR over the seven event windows exceeds the mean of seven similarly constructed yet randomly selected nonevent portfolio CMARs. To do so, we randomly select seven nonevent portfolio returns that mimic the distribution of our sample events over the period. Thus, we have five nonevent portfolio returns from 2005 and two from 2006. We then compare the standardized mean of the nonevent CMARs to that of the seven event CMARs. Using the bootstrap technique, we repeat this procedure 500 times and construct a simulated p value indicating the probability that the standardized mean of the nonevent CMARs is greater than that of the seven event CMARs. The statistic assumes that the distribution of the nonevent returns is the same as that of the event returns; however, it does not assume that the return distribution is normal or that it possesses other specific parametric properties.

Hypotheses Tests

We estimate the following regression model on the full sample of firms with A-shares and B-shares to test H1:

We use the following two measures of the dependent variable CMAR: CMAR (−1, 1) and CMAR (−2, 2), which are 3-day and 5-day cumulative returns adjusted for the Hong Kong Hang Seng Index (HKHSI) return. In Equation 1, AShare equals one if the firm issues only A-shares (i.e., the treatment group), and zero otherwise (i.e., the control group). For example, if the investors react favorably (unfavorably) toward the progress in IFRS convergence reflected in the treatment group, we would find the coefficient α1 to be positive (negative). In other words, α1≠ 0 would provide evidence in support of H1.

To test H2, we estimate the following regression model on the treatment sample of firms that have only A-shares:

NSOE equals one if the firm is ultimately controlled by a nonstate-owned entity, and zero otherwise. If investors of listed NSOEs react more positively to events related to the progress toward IFRS convergence than investors of SOEs, then we should observe β1 to be positive. In other words, β1 > 0 would provide evidence in support of H2.

To test H3, we estimate the following regression model on the treatment sample of firms that have only A-shares:

CapDem is a firm’s capital demand using two measures. The first measure, ΔPPE (plant, property, and equipment) minus lagged net CFO divided by total assets (S. Chen, Sun, Tang, & Wu, 2011), captures a firm’s external financing, ex ante. 11 The second measure, ΔDebtRatio, captures a firm’s external financing ex post. It is measured as next year’s change in total liabilities divided by total assets. The coefficient of interest is δ3, that is, the coefficient on the interaction term NSOE×CapDem. If investors of NSOEs with higher capital demand react more positively to events related to the progress toward IFRS convergence, we should observe δ3 to be positive. In other words, δ3 > 0 would provide evidence in support of H3.

We also check for the alternative explanation that the market reactions of NSOEs may be affected by cross-sectional variation in information asymmetry (Armstrong et al., 2010) instead of capital demand. To do so, we include the variable DA and its interaction, NSOE×DA, as controls. We measure DA as the absolute value of discretionary accruals, derived from the modified Jones model. 12

We include controls for firm characteristics, corporate governance, corporate transparency, and fixed effects in Equations 1 to 3. First, we control for firm characteristics by including size (LnSales), growth (SalesGr), leverage (LEV), and profitability (ROS). Second, we control for corporate governance variables, including separation of cash flow rights and control rights (Separ), whether the CEO is also the chairman of the board (Duality), and board size (BSize). Third, we control for differences in the corporate information environment by including ex post adoption of R&D capitalization (R&D), asset tangibility (PPE), auditor quality (BIG4), and cross-listing (Crosslisting). Last, we control for industry fixed effects (Industry) and event fixed effects (Event). Specifically, if investors expect IFRS convergence to improve (weaken) reporting quality, we would expect firms that are smaller, growing faster, and with higher leverage to benefit more (less) from potentially facilitated external financing. In addition, because R&D capitalization was not allowed under the previous Chinese accounting standards, we identify firms that ex post adopt R&D capitalization as having higher demand for IFRS and thus benefiting more from IFRS convergence. Similarly, we expect firms with a Big 4 auditor to benefit more from IFRS convergence because Big 4 auditors are better equipped to support the transition (Armstrong et al., 2010). All control variables are measured in the contemporaneous time period. We provide detailed variable definitions in Appendix B.

Empirical Findings

Summary Statistics

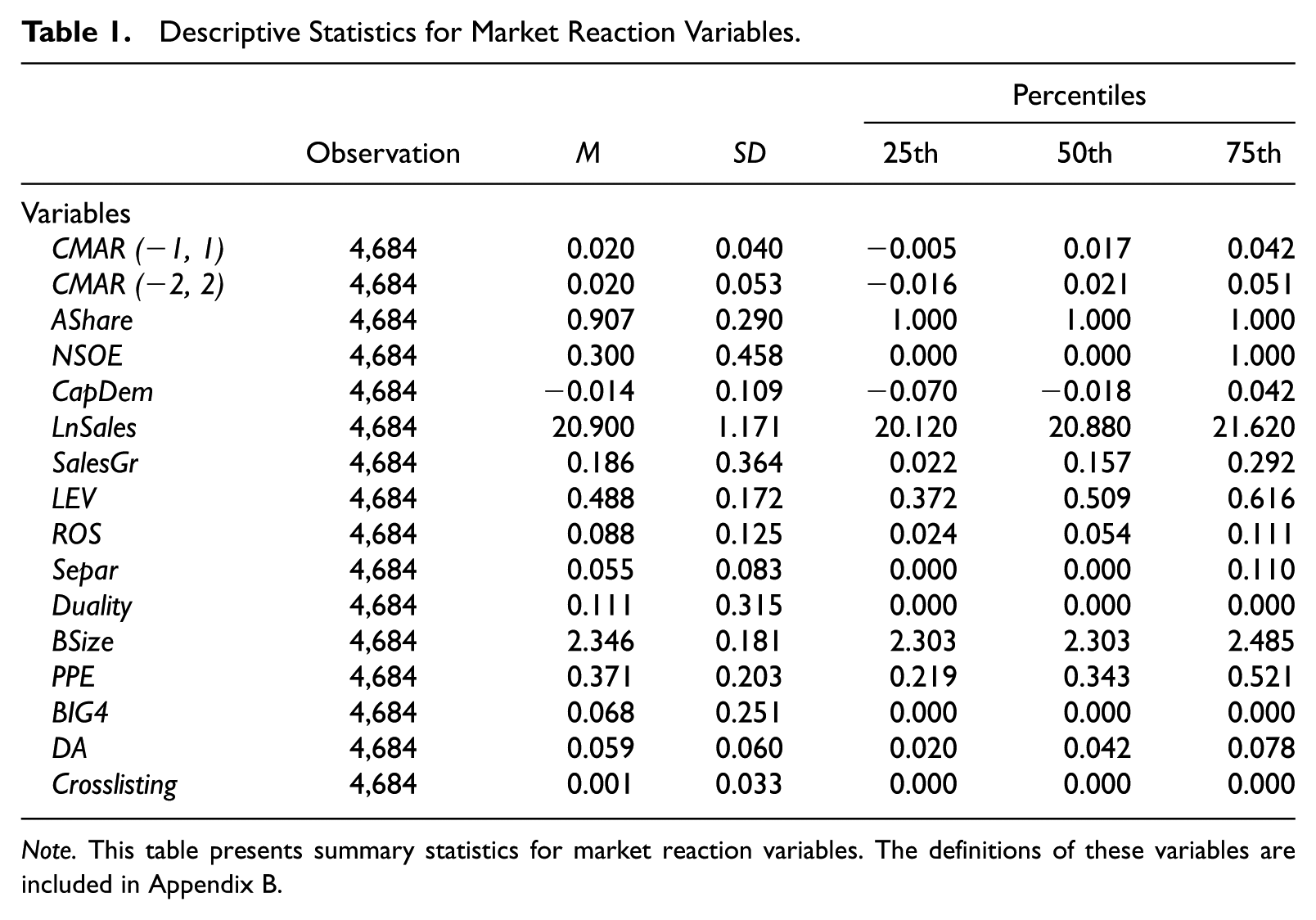

Table 1 presents summary statistics for the variables in the full sample. The mean (median) CMARs for the 3- and 5-day windows are 2.0% (1.7%) and 2.0% (2.1%), respectively. Within our sample, 90.7% of the observations are firms that only issue A-shares, and 30.0% are NSOEs. Table 2 shows that CMARs are positively correlated with CapDem, SalesGr, ROS, and DA.

Descriptive Statistics for Market Reaction Variables.

Note. This table presents summary statistics for market reaction variables. The definitions of these variables are included in Appendix B.

Correlation Matrix.

Note. Correlations significant at the 5% level are indicated in bold.

Overall Market Reactions

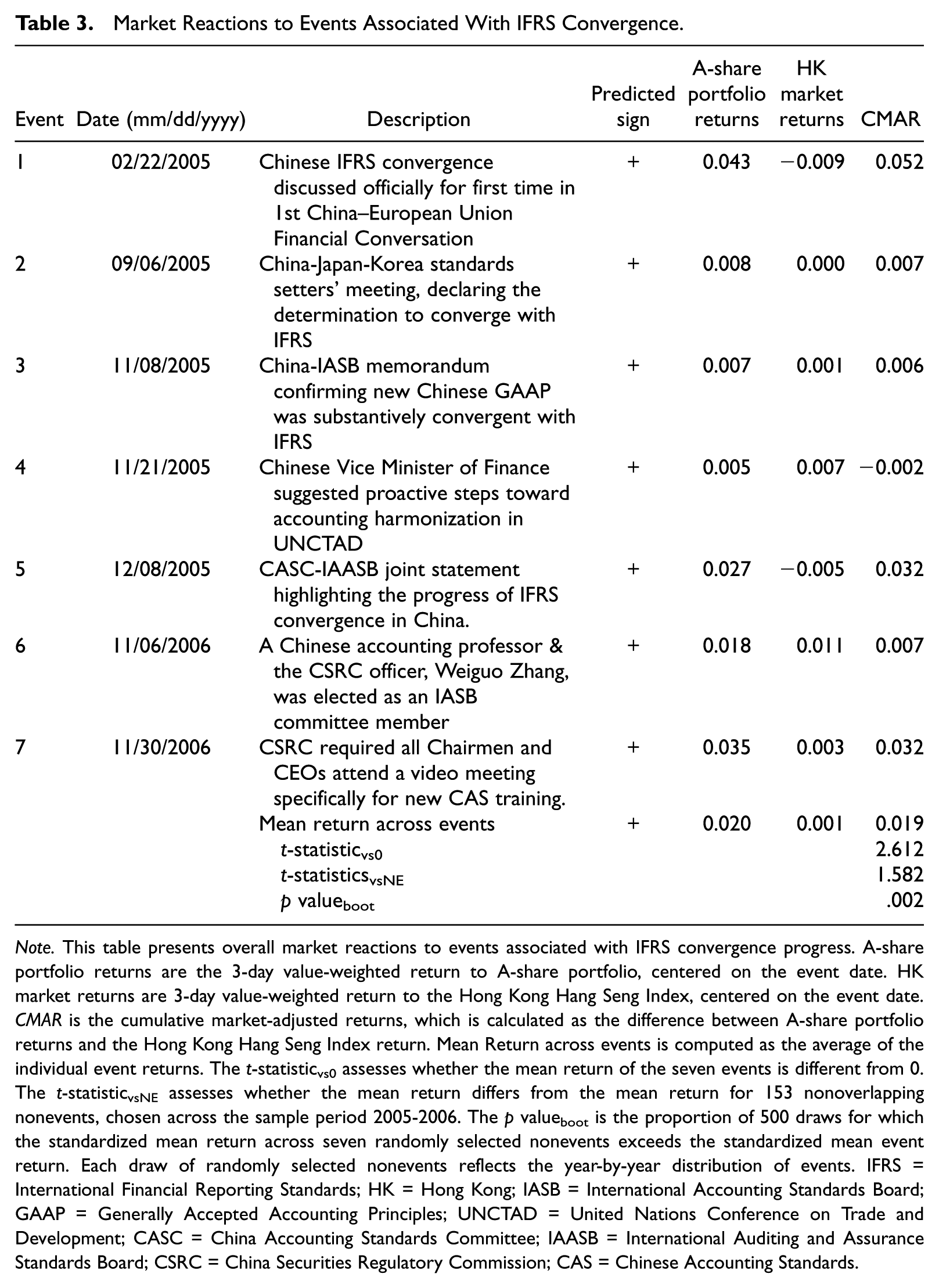

Table 3 presents the market reaction to each individual event as well as the aggregate reaction to all seven events based on the Chinese A-share portfolio 3-day cumulative returns benchmarked against the Hong Kong market index. The results are consistent with the adoption of IFRS being viewed positively by investors for six out of the seven events sampled.

Market Reactions to Events Associated With IFRS Convergence.

Note. This table presents overall market reactions to events associated with IFRS convergence progress. A-share portfolio returns are the 3-day value-weighted return to A-share portfolio, centered on the event date. HK market returns are 3-day value-weighted return to the Hong Kong Hang Seng Index, centered on the event date. CMAR is the cumulative market-adjusted returns, which is calculated as the difference between A-share portfolio returns and the Hong Kong Hang Seng Index return. Mean Return across events is computed as the average of the individual event returns. The t-statisticvs0 assesses whether the mean return of the seven events is different from 0. The t-statisticvsNE assesses whether the mean return differs from the mean return for 153 nonoverlapping nonevents, chosen across the sample period 2005-2006. The p valueboot is the proportion of 500 draws for which the standardized mean return across seven randomly selected nonevents exceeds the standardized mean event return. Each draw of randomly selected nonevents reflects the year-by-year distribution of events. IFRS = International Financial Reporting Standards; HK = Hong Kong; IASB = International Accounting Standards Board; GAAP = Generally Accepted Accounting Principles; UNCTAD = United Nations Conference on Trade and Development; CASC = China Accounting Standards Committee; IAASB = International Auditing and Assurance Standards Board; CSRC = China Securities Regulatory Commission; CAS = Chinese Accounting Standards.

The results for the overall CMAR are as follows. First, the mean CMAR across all seven events is 1.9%, which is statistically significant at the 5% level (two-tail; t-statistic = 2.612; p value = .0400). Second, compared with the average nonevent CMAR, the average event CMAR is higher though not significant (two-tail; t-statistic = 1.582; p value = .1156). Third, for only one out of 500 draws with replacement from the nonevent periods is the standardized mean nonevent CMAR higher than the standardized mean event CMAR of 0.987. Overall, the results in Table 3 provide consistent evidence that the Chinese market responded favorably to China’s progress toward IFRS convergence.

Test of H1

Table 4 presents the tests of H1 that compare market reactions between the treatment and control groups. H1 posits that the coefficient of AShare is different from zero. The estimated coefficients of AShare for CMAR (−1, 1) and CMAR (−2, 2) are 0.0054 (t-statistic = 2.34), 0.0064 (t-statistic = 2.07), respectively. These positive estimates indicate that the market reactions to IFRS convergence progress are significantly more positive for firms that issue only A-shares (i.e., the treatment group) than for firms that issue A-shares and B-shares (i.e., the control group), indicating rejection of H1. Furthermore, the above finding holds true when we exclude any one of the seven events and rerun the test. The control variables show that firms that grow faster, have higher profitability, and have actual need for R&D capitalization standards benefit more from the IFRS convergence in terms of market reactions.

Market Reactions of A-Share Versus B-Share Issuers.

Note. This table presents regression analyses for Hypothesis 1. The definitions of these variables are in Appendix B. The t-statistics are reported in parentheses and are based on standard errors clustered by industry–event.

, **, and *** indicate significance at the 10%, 5%, and 1% levels, respectively.

We repeat the analyses after computing CMAR using the Dow Jones Bric Index in place of the Hong Kong Hang Seng Index and find qualitatively similar results. We do not tabulate these results or discuss them in detail for the sake of brevity.

Tests of H2 and H3

Table 5 presents the results of tests of H2, which compares market reactions between listed NSOEs and SOEs within our treatment group. Of interest is the coefficient on NSOE which, under H2, is expected to be positive. The results reported in Table 5 support H2. For CMAR (−1, 1) and CMAR (−2, 2), the coefficients on NSOE are 0.0017 (t-statistic = 1.52), 0.0033 (t-statistic = 2.21), respectively. These positive estimated coefficients indicate that the stock market views the new set of standards as more likely to benefit NSOEs than SOEs. Similar to Table 4, we find that firms that grow faster, have higher profitability, have less tunneling incentives measured by separation of cash flow rights and control rights, and have actual need for R&D capitalization standards have more positive market reactions. We find qualitatively similar results when we replace the Hong Kong Hang Seng Index with the Dow Jones Bric Index.

Market Reactions of NSOE Versus SOEs.

Note. This table presents regression analyses for Hypothesis 2. The definitions of these variables are in Appendix B. The t-statistics are reported in parentheses and are based on standard errors clustered by industry–event. NSOE = nonstate-owned enterprises; SOE = state-owned enterprise; CMAR = cumulative market-adjusted returns.

, **, and *** indicate significance at the 10%, 5%, and 1% levels, respectively.

Table 6 presents the results of tests that assess whether the market reactions around the events related to IFRS convergence are conditional on the demand for capital. H3 predicts that the benefit of IFRS increases with the demand for capital, especially for NSOEs. This prediction implies a positive coefficient on the interaction term NSOE×CapDem. The results reported in Table 6 are consistent with this hypothesis.

Market Reactions of NSOEs and SOEs Conditional on Capital Demand.

Note. This table presents regression analyses for Hypothesis 3. The definitions of these variables are in Appendix B. The t-statistics are reported in parentheses and are based on standard errors clustered by industry–event. NSOE = nonstate-owned enterprises; SOE = state-owned enterprise; CMAR = cumulative market-adjusted returns.

, **, and *** indicate significance at the 10%, 5%, and 1% levels, respectively.

In columns 1 and 2, the coefficients of NSOE×CapDem for CMAR (−1, 1) and CMAR (−2, 2) are 0.0256 (t-statistic = 2.08), 0.0321 (t-statistic = 2.08), respectively, and each is reliably greater than zero. NSOEs, unlike SOEs, have less access to bank capital; consequently, they rely more on the equity market for financing. If IFRS is expected to provide equity market participants with more useful information, the positive market reactions should be more pronounced for NSOEs with greater capital demands. In columns 3 and 4, the coefficients of NSOE×ΔDebtRatio for CMAR (−1, 1) and CMAR (−2, 2) are 0.0108 (t-statistic = 0.65), 0.0232 (t-statistic = 1.03), respectively, providing consistent (though weaker) evidence in support of H3. The Table 6 results also rule out the alternative explanation that information asymmetry may be driving this result (Armstrong et al., 2010), as the coefficients on the interaction term NSOE×DA, which reflect the difference between the effect of information asymmetry on NSOEs and SOEs, are not reliably greater than zero.

Additional Tests—Value Relevance

Having documented consistent evidence of a positive market reaction to important events leading up to IFRS convergence, we now present evidence of improvement in financial reporting quality following IFRS convergence. We reason that if the observed positive market reactions to the events leading up to IFRS convergence reflect investors’ ex ante assessments of improved financial reporting quality under IFRS, we should also observe ex post evidence of improved financial reporting quality among firms that exhibited higher market reactions ex ante. Accordingly, we assess the impact of mandating IFRS on the value relevance of reported earnings. We use the following price (levels) and return (changes) models to make this assessment: 13

In Equation 4, the dependent variable, PRICE, is the closing price 4 months after fiscal year end. POST is one if the observation is in the post-IFRS period (2007 and later), and zero otherwise. BPS is closing book value per share; EPS is net profit per share. In Equation 5, the dependent variable, RETURN, is the stock price return for the 12-month period ending 4 months after fiscal year end. EPS_P is EPS scaled by lagged closing price. DEPS_P is the change of EPS scaled by lagged closing price. The coefficients of the interaction terms (i.e., POST×BPS in Equation 4 and POST×EPS_P in Equation 5) indicate the incremental value relevance of reported earnings after IFRS was mandated.

We estimate these value relevance models separately for each subsample (i.e., B-share and A-share, SOE and NSOE, CapDem_L and CapDem_H). 14 Then we test whether the coefficients of the interaction terms (i.e., POST×BPS in Equation 4 and POST×EPS_P in Equation 5) are different. 15 Larger coefficients of the interaction terms indicate greater improvement in value relevance.

In addition, following the standard value relevance literature (e.g., Collins, Maydew, & Weiss, 1997), we also compare the adjusted R2 in peer samples (i.e., B-share and A-share, SOE and NSOE, CapDem_L, and CapDem_H). Using a bootstrap technique, we reestimate each value relevance model 500 times for each subsample and use the mean and variance for each adjusted R2 to test the difference in value relevance. 16 A higher adjusted R2 indicates that accounting variables (i.e., BPS and EPS_P) better explain market variables (i.e., PRICE and RETURN).

If the market correctly interpreted the potential benefits of IFRS convergence, then, for firms more likely to benefit from IFRS (i.e., firms with A-shares vs. A- and B-shares; NSOEs vs. SOEs; and NSOEs with stronger vs. weaker capital demands), we should observe greater improvement in financial reporting quality from the pre-IFRS to the post-IFRS period, because such firms can better communicate their economic information to external equity investors under the new accounting standards.

We use firms listed on the Shanghai and Shenzhen exchanges over the period from 2002 to 2010 for these value relevance tests. 17 Panel A of Table 7 illustrates the year distribution of the whole sample and Panel B presents the descriptive statistics for the variables used in the analyses. Panels C and D compare the value relevance of the control and treatment subsamples based on the price model and the returns model, respectively. The z-statistic comparing the difference between coefficients indicates higher value relevance in three out of six comparisons and significant at least at the 5% level. The results of comparisons between pre-to-post changes in adjusted R2s are similar; five out of the six differences are positive and three are significant. In other words, the pre-to-post increase in value relevance is greater for the A-share subsample than for the B-share subsample, for the NSOE subsample than for the SOE subsample, and for the higher capital demand NSOE subsample than for the lower capital demand NSOE subsample.

Pre- versus Post-IFRS Value Relevance Tests.

Note. This table presents additional tests of changes in value relevance after mandatory IFRS adoption in China. The B-share subsample includes observations of firms that issue B-shares. The A-share subsample includes observations of firms that issue A-shares only. The SOE subsample includes observations of SOE listed firms from the A-share subsample. The NSOE subsample includes observations of NSOE listed firms from the A-share subsample. The CapDem_L (H) subsample includes observations of NSOE listed firms from the A-share subsample with values of CapDem (measured by the ratio of change of PPE subtracting lagged net CFO to total assets, defined in the main tests) below (above) the annual median. The t-statistics are reported in parentheses and are based on standard errors adjusted for heteroscedasticity. The z-value (Coefficients) is used to test the difference between the coefficients of POST×EPS (or POST×EPS_P) in two comparison samples (i.e., B-share and A-share, SOE and NSOE, CapDem_L and CapDem_H). The z-value (Adjusted R2) is used to test the difference between the R2 in two comparison samples (i.e., B-share and A-share, SOE and NSOE, CapDem_L and CapDem_H). The definitions of these variables are in Appendix B. The z-value is based on z-test illustrated in the text.

, **, and *** indicate significance at the 10%, 5%, and 1% levels, respectively.

To sum up, the evidence in Table 7 shows that firms with A-shares, NSOEs, and NSOEs with greater capital needs exhibit improved financial reporting quality after IFRS was made mandatory. These findings reinforce the market reaction results indicating that investors view these firms as benefiting more from China’s IFRS convergence.

Conclusion

We examine market reactions to events associated with IFRS convergence progress in China. We document significantly more positive market reactions to these events from the investors of Chinese firms that only issue A-shares and therefore only started reporting under IFRS in 2007. Among these firms, we show that the market reactions are significantly higher for NSOEs than for SOEs. Within this group of NSOEs, firms with higher capital demands are associated with larger market reactions. These market reaction test results indicate that investors believe that mandating IFRS can benefit Chinese listed firms, and especially those that receive less government financial support and have a high demand for investment capital. Additional tests reveal that such firms indeed make use of the opportunity under IFRS to improve their financial reporting quality so as to cater to the information needs of outside equity investors. We also show that the convergence toward IFRS has important consequences for investors in terms of incremental value relevance among firms with incentives for more transparent financial reporting. Instead of being merely a political decision in response to the thrust of international accounting harmonization, IFRS convergence in China helps to strengthen corporate accounting quality and reporting incentives.

Our findings have three implications. First, investors believe that mandating IFRS in China enables firms that require external capital but have a disadvantage in acquiring it to attract outside investors. Thus, IFRS can potentially narrow the gap in firm competitiveness for external capital resulting from the varying degree of government support, a characteristic of China’s state capitalism. As China is an increasingly influential player in the world economy, the experience of IFRS in China has useful implications for other emerging economies. Second, to widen the benefits of IFRS in terms of strengthening corporate transparency, further reform may be useful, such as a reduction in the government control of listed firms that impedes firms’ financial reporting incentives. Third, we provide evidence of IFRS benefits in a country with weak institutions and investor protection.

Our findings must be interpreted with caution in light of the following limitation. The methodology used relies on the correct identification of events to draw the inferences, and requires that information be incorporated into stock prices rapidly and without bias (Armstrong et al., 2010). Although we have checked and eliminated confounding events that could contaminate our findings, we caution that our results may still suffer from this potential limitation.

Footnotes

Appendix

Variable Definitions

| Variable | Definition |

|---|---|

| CMAR (−1, 1) | Firm-specific cumulative returns over 3-day (−1, 1) windows adjusted by Hong Kong Hang Seng index returns |

| CMAR (−2, 2) | Firm-specific cumulative returns over 5-day (−2, 2) windows adjusted by Hong Kong Hang Seng index returns |

| AShare | Equals to one for firms that only issue A-shares and zero otherwise |

| NSOE | Equals to one for nonstate-owned enterprise (NSOEs) and zero otherwise |

| CapDem | The demand for capital, defined as change of PPE subtracting lagged net operating cash flow scaled by total assets |

| LnSales | The natural logarithm of total operating revenue |

| SalesGr | The percentage increase of total operating sales |

| LEV | The ratio of total liabilities to total assets |

| ROS | The return on sales, measured as the ratio of operating profit scaled by total operating sales |

| Separ | The difference between control rights and cash flow rights |

| Duality | Equals to one if the Chairman of board is also the CEO and zero otherwise |

| BSize | The natural logarithm of number of board members plus one |

| PPE | The ratio of plant, property and equipment to total assets |

| BIG4 | Equals to one if a firm is audited by the four largest accounting firms and zero otherwise |

| Crosslisting | Equals to one if a firm is cross-listed and zero otherwise |

| DA | the absolute value of discretional accruals based on the modified Jones Model |

| PRICE | The closing price 4 months later after fiscal year end |

| POST | Equals to one if the observation is after 2007 (included) and zero otherwise |

| BPS | The book value per share |

| EPS | The net profit per share |

| RETURN | The stock price return in the year ending 4 months after fiscal year end |

| EPS_P | EPS scaled by lagged closing price |

| DEPS_P | The change of EPS scaled by lagged closing price |

| ΔDebtRatio | The change in total liabilities scaled by total assets |

Note. All variables are measured in the contemporaneous time period.

Authors’ Note

The authors thank Mingyi Hung, Michael Neel, Oliver N. Okafor (CAAA discussant), Huoshu Peng (AAA discussant), K.C. John Wei (CICF discussant), Jeff Zhang, and participants at the 2014 CAAA Conference (Edmonton, Canada), 2014 CICF (Chengdu, China), 2014 AAA Conference (Atlanta, the United States), and Fudan Accounting Seminar for their helpful comments. All errors are our own.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Chao Chen would like to acknowledge the financial support from the National Natural Science Foundation of China (Project No. 71472048).