Abstract

We examine whether short sellers are interested in, and capable of, identifying firms with an upcoming revelation of internal control material weaknesses (ICMW). We show that short sellers accumulate positions in firms that are about to disclose ICMW under Section 404 of the Sarbanes–Oxley Act for the first time when internal control problems are severe. We find that the short-interest buildup is mainly due to the use of private rather than public information, which suggests that their trades contain incremental prediction power of the upcoming internal control failure. Furthermore, the ability of short sellers to predict ICMW is more pronounced in firms operating in poor information environment. Finally, we find no evidence that trades by short sellers prior to the ICMW disclosure create a cascade of selling that leads to an overreaction of ICMW. Overall, we present evidence that corporate governance information in the form of ICMW is part of the short sellers’ information set, and we establish a path through which ICMW impacts equity investors.

Keywords

Introduction

Short selling has been a controversial practice in capital markets, and the financial crisis of 2008 brought short selling to the forefront of media attention once again. In September 2008, the U.S. Securities and Exchange Commission (SEC) even temporarily banned certain short-selling activities in financial stocks and placed new requirements on share borrowing. 1 The SEC, for a while, also considered the adoption of a new disclosure policy that would require short sellers to publicly disclose their positions, which could thus potentially limit their impact on security prices. 2 Criticism of short selling includes accusations that malicious short selling accelerated the market price downward spiral and disturbed financial market stability during the financial crisis (Wilchins, 2008; Zarroli, 2008). 3 Yet, financial economists in general have a favorable view of short sellers as investors who identify overvalued stocks and help incorporate negative information into stock prices (e.g., Christophe, Ferri, & Angel, 2004; Diether, Lee, & Werner, 2009).

To assess whether short sellers play a positive or negative role in capital markets, researchers have extensively examined short-selling activities. For example, Boehmer, Jones, and Zhang (2008) show that heavily shorted stocks underperform lightly shorted stocks, and Boehmer and Wu (2013) show that greater short selling reduces the post-earnings-announcement drift. Studies further examine the information set of short sellers. They show that short sellers are able to anticipate certain negative corporate events, such as restatements and accounting fraud (Dechow, Sloan, & Sweeney, 1996; Desai, Krishnamurthy, & Venkataraman, 2006; Karpoff & Lou, 2010), negative earnings surprises (Christophe et al., 2004), and asset write-downs (Liu, Ma, & Zhang, 2012). One common aspect of all these studies is the focus on events with immediate adverse effects on earnings. However, there is limited evidence on whether short sellers are also interested in, and capable of, identifying firms with corporate governance deficiencies.

In this study, we examine the informativeness of short selling in a novel setting—prior to the revelation of internal control material weaknesses (ICMW). This setting is ideal for studying short sellers’ informativeness of corporate governance deficiencies for several reasons. First, ICMW disclosure under Section 404 of the Sarbanes–Oxley Act (SOX) is an important event, as it indicates ineffective internal controls (ICs) and a lower reliability of financial reporting. Second, studies show that the existence of ICMW has negative consequences on companies because it increases both information and business risks and leads to a higher cost of capital (e.g., Kim, Song, & Zhang, 2011), making it an attractive event for short sellers. Third, the disclosure of ICMW is advantageous for studying short-selling activities related to governance information over other commonly used governance measures, such as the G index (Gompers, Ishii, & Metrick, 2003). This is because ICMW is disclosed in a 10-K form at a specific known date and is readily available, while other firm-level governance measures do not become available at known dates.

We begin our analysis by identifying firms disclosing ICMW under SOX 404 for the first time. We focus only on first-time ICMW reporting because the market should only react to unexpected information, and a first-time ICMW disclosure is more likely to be unexpected than a repeated one (Ashbaugh-Skaife, Collins, Kinney, & LaFond, 2009). We then search for significant corporate events preceding the actual ICMW disclosure that may be indicative of the upcoming adverse disclosure. These events include (a) CEO and CFO departures for reasons other than retirement, (b) a switch from a Big-4 to a non-Big-4 audit firm, (c) a large restructuring or an asset write-down, and (d) a significant internal control deficiencies (ICD) disclosure in the forms of material weaknesses or significant deficiencies under SOX 302. 4

As we report in the “Sample Formation, Data, and Measurements” section, the likelihood of each triggering event is substantially higher for ICMW firms than for firms reporting adequate controls. If none of these events took place during the year leading to the ICMW disclosure under SOX 404, we consider the actual ICMW disclosure as the triggering event. If multiple events occur, we choose the earliest one as the triggering event. We then examine the short-interest ratio (SI), and the abnormal short-interest ratio (ABSI), a measure that controls for firm fundamentals (e.g., Asquith, Pathak, & Ritter, 2005; D’Avolio, 2002; Dechow, Hutton, Meulbroek, & Sloan, 2001) in the 17-month period leading to the triggering event. 5 We study the trading patterns separately for firms with more and less severe IC problems, insofar as it may be more difficult for external investors to anticipate IC problems that are subtler. We distinguish more versus less severe ICMW by the count of material weaknesses reported, with a higher count implying more severe problems (Gordon & Wilford, 2012).

We find a progressive short-interest buildup in the months leading to the triggering event, but only for firms with more severe ICMW. Specifically, for firms reporting at least three material weaknesses (more severe ICMW), we find a 2.15% (1.63) increase in SI (ABSI), from 3.12% (1.12) to 5.27% (2.75), occurring from 18 months to 1 month prior to the triggering event. For firms reporting one or two weaknesses (less severe ICMW), the change over the same period is 0.62% (−0.10), from 3.51% (0.84) to 4.13% (0.74). Multivariate tests controlling for factors known to affect short selling show significant increases in SI and ABSI prior to the triggering event, only for firms with more severe ICMW. 6 We obtain similar results when using the number of entity-level and account-level deficiencies to proxy for more and less severe ICMW, respectively (Moody’s Investors Service, 2004, 2006, 2007).

After establishing a positive association between short interest and ICMW, we use a two-stage approach to study whether short sellers simply trade on firm parameters known to be associated with IC failure, such as age, extreme sales growth, and so on (e.g., Ashbaugh-Skaife, Collins, & Kinney, 2007; Doyle, Ge, & McVay, 2007; Ge & McVay, 2005; Ghosh & Lee, 2013), or on unique information. We first regress the number of weaknesses on those firm parameters and generate predicted and unpredicted (residual) ICMW components. We then regress short interest on the two components and find strong evidence that the unpredicted ICMW component is associated with short interest. This finding suggests that short sellers obtain unique information, and their trades contain incremental prediction power of upcoming IC failure. 7 In the cross-section, we predict and find that the incremental predictability of short selling is more pronounced in firms with higher information asymmetry. This finding underscores the informational role of short sellers in conveying valuable information about firms’ IC systems. Finally, we follow the procedure in Karpoff and Lou (2010) to test whether short selling creates a downward price spiral when the ICMW is publicly revealed. We find that the market reaction on the revelation day is only related to the severity of the ICMW, but not to the short selling, thus providing no evidence of overreaction to the bad news.

We conduct an array of robustness tests to increase the reliability of our findings. Throughout our study, we employ different measures of short interest and of ICMW severity, and we examine both the level of, and the change in, short interest. To rule out the possibility that short sellers trade on the triggering events rather than on control ineffectiveness, we match each sample firm with a control firm based on the specific triggering event, and the results remain intact. We also obtained similar results when examining a subsample of firms where we drop the observations with a triggering event other than SOX 302 or SOX 404. Next, while we control for the characteristics of ICMW firms, it is possible that high-leakage firms are more likely to have IC problems and that short sellers simply target high-leakage firms rather than ICMW firms per se. To assess this possibility, we check for a positive association between short interest and ICMW prior to other corporate negative events unrelated to ICMW, namely credit downgrades and negative earnings announcements, but we do not find such an association. Finally, we construct a placebo test in which we randomly assign an ICMW disclosure “event date” within the 5 years prior to the triggering event. We do not find an association between short interest and ICMW severity using the pseudo-“event date.” All the robustness checks are available on the online appendix.

This study makes several contributions. First, it contributes to the literature on the information set of short sellers. We document that short sellers trade on upcoming ICMW revelation. Moreover, the evidence that their trades are mainly based on private information and are dominant in firms with entity-level IC problems is consistent with short sellers’ unique ability to detect ICMW. Our evidence echoes Jensen’s (2005) suggestion that board members consult with short sellers to better monitor their companies. Second, this article extends the findings from Desai et al. (2006) of short selling prior to restatements and from Karpoff and Lou (2010) of short selling prior to SEC enforcement actions for financial misrepresentation.

We consider extending these studies as important, because the latter studies are of events representing ex post verifications that prior financial statements contained major misstatements. As such, even though these events also reflect low corporate governance quality as our ICMW event, they could have been noticed through an in-depth review of the financial statements. Indeed, Desai et al. (2006) find that short sellers, at least in part, use the magnitude of total accruals to anticipate restatements. The prediction of ICMW that is not proceeded or succeeded by a restatement, as in our sample, 8 would require more than an in-depth financial statement analysis. Our findings imply that short sellers may acquire information that is incremental to the accounting quality measures (Kim et al., 2011). 9 This provides stronger evidence on the interest of short sellers in corporate governance quality. Third, our study adds to the literature on the effect of ICMW on equity investors (Ashbaugh-Skaife et al., 2009; Gordon & Wilford, 2012; Kim et al., 2011). By demonstrating that short sellers build up their positions prior to the disclosure of ICMW, we establish a specific path through which ICMW impacts the equity market.

The remainder of the article is organized as follows. The “Background, Related Literature, and Hypotheses Development” section provides the background, surveys the literature, and develops the hypotheses. The “Sample Formation, Data, and Measurements” section describes the sample construction and the measures of short interest, and provides descriptive statistics. The “Empirical Analysis” section reports the main empirical results. The “Additional Analysis” section presents additional analysis, and the “Conclusion” section concludes the study.

Background, Related Literature, and Hypotheses Development

Background

Prior to the accounting scandals of the early 2000s (Enron, WorldCom, and Global Crossing, among others), limited attention was paid to internal controls over financial reporting (ICFR). Disclosure of ICD was only required when companies changed auditors (Balsam, Jiang, & Lu, 2014). This has dramatically changed with the enactment of SOX, which places great importance on ICFR. Section 404 of the Act, in particular, requires that both a firm’s top management and its external auditor report their assessments of the company’s IC structure and procedures in the annual report.

ICFR is defined by the SEC as a process to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles (SEC, 2003, Release No. 33-8238). It should assure the prevention or timely detection of unauthorized acquisitions and the use or deposition of assets that could have a material effect on the financial statements. ICD exist when the design of the control, or its operation, does not allow the prevention or the timely detection of a misstatement (Public Company Accounting Oversight Board [PCAOB] Auditing Standard 2, Paragraph 8). As such, it is likely to impose an additional information risk on investors. A deficiency 10 can also lead to intentional misstatements through misrepresentations and omissions by employees or managers, which are not prevented due to inappropriate controls, and thus can impose a business risk to investors (for a comprehensive discussion of ICFR and ICD, see Ashbaugh-Skaife et al., 2009, Section 2).

Related Literature

Several studies have investigated the characteristics of firms that disclose ICMW (e.g., Ashbaugh-Skaife et al., 2007; Doyle et al., 2007; Ge & McVay, 2005). They find that those firms tend to be smaller, younger, more complex, less profitable, growing more rapidly, and more likely to undergo restructuring; moreover, such firms tend to have fewer resources to invest in IC and less financial expertise on their audit committees. Studies also document the negative consequences of a weak IC system. ICMW firms pay higher audit fees (Hogan & Wilkins, 2006), suffer a higher yield spread in the bond market (Kim et al., 2011) and a higher cost of equity (Beneish, Billings, & Hodder, 2008; Gordon & Wilford, 2012), and have more negative credit ratings (Moody’s Investors Service, 2004).

Research on short sellers focuses on the various aspects of their activities. Studies show that short sellers identify overvalued stocks (e.g., Dechow et al., 2001; Desai, Ramesh, Thaigarajan, & Balachandran, 2002) and can anticipate certain negative earnings–related events, such as negative earnings surprises, restatements, financial misconduct, or securities fraud (Christophe et al., 2004; Desai et al., 2006; Griffin, 2003; Karpoff & Lou, 2010).

Studies also demonstrate the informativeness of short selling Pownall and Simko (2005) document more negative market returns around the announcement of a short-interest increase when the analyst following is low. They conclude that short sellers can serve as information intermediaries when limited alternatives of information are available to the market. Cassell, Drake, and Rasmussen (2011) present evidence that auditors take information from short sellers’ activities into account when setting audit fees.

Yet, a few studies fail to find evidence of informative trades by short sellers (e.g., Henry & Koski, 2010; Lamont & Stein, 2004; Richardson, 2003). For example, Lamont and Stein (2004) find that during the dot-com era, at the aggregate level, short interest in National Association of Securities Dealers Automated Quotations (NASDAQ) stocks actually declined as the NASDAQ index approached its peak. With respect to their sources of information, Drake, Rees, and Swanson (2011) find that short sellers exploit a wide range of information from financial statements, press releases, and other publicly available channels. Engelberg, Reed, and Ringgenberg (2012) further find that a substantial portion of short sellers’ trading advantage is derived from their ability to analyze publicly available information more effectively. They show that the well-documented negative relation between short sales and future returns is twice as large on news days, and 4 times as large on negative news days, as on nonnews days.

The discussion so far suggests that short sellers are sophisticated investors that exploit various sources of information in targeting firms with negative corporate events. It also suggests that the existence of ICMW indicates a corporate governance deficiency and has negative consequences for companies. Thus, short sellers may be interested in gathering information about the quality of the firm’s IC system and trading on that information. However, whether short sellers can anticipate ICMW and trade on it is still unknown.

Hypotheses Development

The PCAOB (Auditing Standard 2) argues that the existence of ICMW results in more than a remote likelihood of a business or information risk. The presence of ICMW should therefore lead to a revision in investors’ perception of the business and information risks, and change their expectations of the present value of future cash flows. Indeed, the literature documents negative equity market (Ashbaugh-Skaife et al., 2009) and debt market (Kim et al., 2011) consequences due to ICMW. Given that short sellers are sophisticated investors who are capable of predicting and trading in advance of certain negative news events (e.g., Desai et al., 2006), they may be incentivized to collect information on firms’ IC quality and to trade on it in advance of an ICMW revelation. Ashbaugh-Skaife et al. (2009) find a significant increase in firms’ cost of equity after a first-time ICMW disclosure, but not after subsequent ones. This suggests that only the first-time disclosure of ICMW contains new information. Therefore, short sellers are likely to be interested only in identifying the first-time ICMW. Thus, our first hypothesis (stated in the alternative form) is as follows:

In addition to the disclosure of the existence of ICMW, the SOX 404 report also lists the number and types of material weaknesses discovered. Gordon and Wilford (2012) find that the higher the number of initial weaknesses, the longer it will take to remediate the controls. Similarly, Hammersley, Myers, and Zhou (2012) find that the more pervasive material weaknesses (those at the entity level and those with more individual weaknesses) last longer. These findings suggest that within the realm of material weaknesses in ICFR, there is a variation in the degree of severity. Desai et al. (2006) find that short sellers identify the more egregious restatements, and Karpoff and Lou (2010) find that short selling increases with the severity of financial misconduct. The conclusion from those two studies is that more severe problems are easier for short sellers to detect, and we expect the same for the detection of IC problems. Thus, we extend the first hypothesis to incorporate the degree of ICMW severity (stated in the alternative form), as follows:

Short sellers may use two types of information to predict IC problems. First, they may rely on public information. In this regard, Engelberg et al. (2012) find that a substantial portion of short sellers’ trading advantage stems from their superior ability to analyze publicly available information. Prior research has already identified certain firm characteristics, that is, operation complexity, size, extreme sales growth, and profitability that are associated with ICMW. Thus, one possibility is that short sellers simply use those firm characteristics to anticipate the IC problems. Second, short sellers may rely on private information. Khan and Lu (2013), for example, show that short sellers trade on leaked information about insider sales, which suggests that short sellers obtain private information via tipping from insiders. It is also possible that short sellers collect private information from other sources, such as field interviews with former employees. Therefore, a second possibility is that short sellers enjoy an information advantage because of nonpublic information. Given that both public and private information can be used by short sellers to anticipate ICMW, we account for both possibilities in developing our hypothesis regarding the information source of short sellers, as follows:

While short sellers may develop unique capabilities, or may obtain unique IC information, their information advantage in predicting upcoming control problems should diminish when the information environment of the firm is richer and more transparent. That is to say, short sellers are likely to benefit less from shorting firms with a lesser degree of information asymmetry, because information pertaining to IC problems should be incorporated into stock prices more efficiently for those firms and should thereby limit arbitrage opportunities. In contrast, when the quality of the information environment is low, short sellers have a higher incentive to collect information on the upcoming IC failure. Thus, we extend H2b to incorporate cross-sectional differences in the degree of information asymmetry, as follows:

Sample Formation, Data, and Measurements

Measurement of Short Interest

We obtain short-interest data from Compustat Supplemental Short Interest Database and data on the number of outstanding shares from the Center for Research in Security Prices (CRSP). We use two measures of short interest: (a) the SI and (b) the ABSI. The SI is commonly used in the literature (e.g., Jones & Larsen, 2004; Karpoff & Lou, 2010). It is calculated as the number of shares shorted, divided by the number of outstanding shares in the preceding month. Short interest has been shown to be associated with certain firm characteristics, such as firms size (Asquith et al., 2005), the ratio of book value of equity to market value of equity (BM; Dechow et al., 2001), return momentum (Asquith et al., 2005), share turnover, and institutional ownership (Asquith et al., 2005; Nagel, 2005). Therefore, in addition to the common measure of short interest, we construct a measure of abnormal short interest, which controls for the effects of size, BM, return momentum, share turnover, and the level of institutional holding. All firms in the CRSP database are first sorted into terciles (Karpoff & Lou, 2010), based on their preceding month-end’s market capitalization (Size). Within each size group, firms are further sorted into terciles based on their prior fiscal-year-end’s BM. The same procedure follows for the return momentum, share turnover, and institutional ownership. The institutional ownership information is retrieved from Thomson Reuters’s 13F filings. With the five-parameter sorting procedure, we form 243 portfolios at the beginning of each month. We construct the expected short interest for each firm i in month t, E(SIi,t) as the median value of the short interest of its corresponding matching portfolio. Then, we define abnormal short interest, ABSIi,t, as the difference between the firm’s actual and expected short interest, as follows:

Because we are interested in examining whether short interest increases for ICMW firms prior to the triggering event, similar to Desai et al. (2006), Karpoff and Lou (2010), and Liu et al. (2012), we also calculate the changes in short interest, ΔSI, and in abnormal short interest, ΔABSI, from 18 months to 1 month before the event date. We measure the short interest up to month −1 because short-selling data are reported only in terms of settlement on the 15th of each month (or the prior trading day if the 15th is not a trading day), and Month 0’s measure may fall within the time period after the triggering event.

Measurements of ICMW Severity

We apply two main measures of ICMW severity. Gordon and Wilford (2012) find that the higher the number of material weaknesses reported initially, the longer it will take to remediate the ICMW, and that a higher number of material weaknesses is associated with a higher cost of equity. These findings suggest that a higher number of material weaknesses is an indication of more severe IC problems. We define a “firm with more severe ICMW,” if the SOX 404 disclosure lists at least three material weaknesses, and a “firm with less severe ICMW,” if it lists only one or two material weaknesses. To address the ad hoc aspect of this measure, in the multivariate analyses, we also apply an integer variable: the number of material weaknesses reported.

Moody’s Investors Service (2004, 2006, 2007) classifies ICD into two types: account-level ICD and entity-level ICD. 11 Account-level ICD are related to controls over specific account balances or transaction-level processes. Moody’s is much less concerned about this type of deficiency and is unlikely to take any rating actions against firms reporting it. Entity-level ICD are related to the overall control environment or the financial reporting process. This type of ICD has a pervasive effect on a company’s financial reporting. Moody’s is therefore more concerned about entity-level ICD and is more likely to take rating actions against firms with entity-level control problems. In line with Moody’s view, Hammersley et al. (2012) find that companies are less likely to remediate previously disclosed material weaknesses when the weaknesses are at the entity level. Thus, we examine separately the relationships of short selling with entity-level and account-level ICD. To determine the number of entity- and account-level ICD, we read the descriptions in Audit Analytics of the reasons behind ICMW. ICD such as (a) senior management competency, tone, reliability issues, and (b) an ineffective, nonexistent, or understaffed audit committee can be considered as entity-level control deficiencies. On the contrary, deficiencies such as (a) untimely or inadequate account reconciliations and (b) journal entry control issues are considered as account-level control deficiencies. The appendix provides a complete list of items for each category. 12

Sample Data and Formation

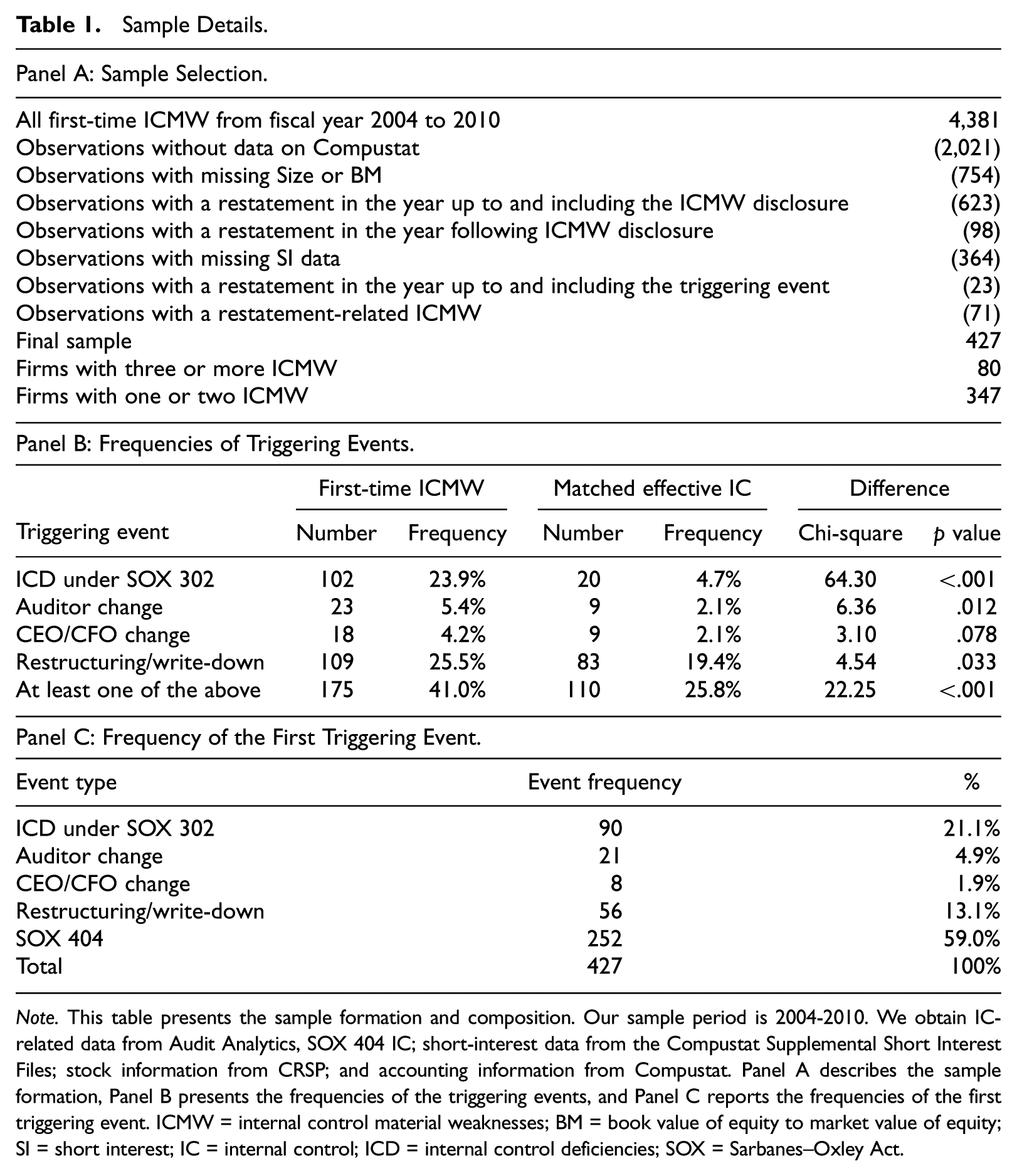

Our primary source of IC-related data is Audit Analytics; SOX 404 ICs, which contains information concerning the management’s assessment of ICFR; and the auditor’s attestation report. Panel A of Table 1 describes the sample formation. We start by identifying 4,381 firms reporting ineffective IC for the first time during the years 2004 to 2010. 13 We remove 2,021 observations that do not appear on the Compustat database, our source for accounting data, and 754 observations that have missing firm size or book-to-market ratio data, the two key variables we use to construct the matched sample. Desai et al. (2006) report a short-interest buildup in advance of financial statement restatements; thus, to avoid confounding effects and to isolate the ICMW effect from that of restatements, we first remove 623 (98) firms with a restatement during the 12 months up to and including (succeeding) the ICMW disclosure date. Next, we eliminate 364 firms with missing short-interest data. After we identify the triggering events (we discuss the triggering events next), we further remove 23 observations with a restatement during the 12 months up to and including the triggering-event date when it is not the ICMW disclosure date. Finally, we also remove 71 additional observations with restatement-related ICMW. 14 This leaves us with a final sample of 427 firms, of which 80 (347) have more (less) severe ICMW, based on the count of material weaknesses. We also construct a matched sample, wherein each sample firm is first matched with a control firm in the same industry 18 months prior to the triggering-event month. The procedure follows that in Desai et al. (2006). We first select the matched firms in the same deciles, based on size and the book-to-market ratio. Then we find the best match that minimizes the deviation score, based on size and the book value of equity. 15

Sample Details.

Note. This table presents the sample formation and composition. Our sample period is 2004-2010. We obtain IC-related data from Audit Analytics, SOX 404 IC; short-interest data from the Compustat Supplemental Short Interest Files; stock information from CRSP; and accounting information from Compustat. Panel A describes the sample formation, Panel B presents the frequencies of the triggering events, and Panel C reports the frequencies of the first triggering event. ICMW = internal control material weaknesses; BM = book value of equity to market value of equity; SI = short interest; IC = internal control; ICD = internal control deficiencies; SOX = Sarbanes–Oxley Act.

Defining a Triggering-Event Date

For our sample firms, we need to identify a relevant event date that publicizes or signals the IC problems. Ideally, we would use the SOX 404 filing date, because it explicitly makes the IC problems known. However, previous studies (Ashbaugh-Skaife et al., 2009; Beneish et al., 2008) find only an attenuated market reaction at the disclosure time. Moreover, Ghosh and Lee (2013) show that most of the information about IC problems is incorporated into the stock price, even before the IC disclosure. An intuitive example of an explicit early revelation of the upcoming ICMW disclosure under SOX 404 is when, prior to this disclosure, a firm acknowledges the existence of ICD in its quarterly IC disclosure under SOX 302 (recall that SOX 404 is only reported annually). Other corporate events are also likely to signal the upcoming ICMW disclosure. For example, on July 29, 2010, Deloitte Touche Tohmatsu Limited resigned from being the external auditor for American Apparel for just over a year, following the issuance of an ICMW opinion. American Apparel’s shares dropped 14% following the release of this news. 16 As another example, there was speculation that the departure of Andrew Mason, the former CEO of Groupon, Inc., was, at least partly, due to the company’s IC problems. 17 We therefore search for events that may trigger the upcoming ICMW disclosure. First, we identify firms that disclose material weaknesses under SOX 302 within the four quarters leading to the SOX 404 ICMW disclosure. 18 Second, we read the firms’ 8-K reports to see whether, during the 12 months prior to the ICMW disclosure, there has been a switch from a Big-4 to a non-Big-4 audit firm, 19 or whether there has been a CEO or CFO departure not due to regular retirement. Third, Doyle et al. (2007) find that company restructuring is associated with IC problems, and Dechow, Ge, Larson, and Sloan (2011) show that significant asset write-offs are indicators of information risk. We therefore identify firms with write-downs, or restructuring costs greater than 1% of their total assets, in the four quarters leading to the SOX 404 ICMW disclosure. If a firm had none of these events, we use the SOX 404 ICMW disclosure as the triggering event, and if a firm had multiple events, we choose the earliest one as the triggering event. 20 We verify that, indeed, the likelihood of having these events is much higher for the sample firms than for the control firms with effective IC. Panel B of Table 1 reports the frequency of occurrences of each triggering event. As can be seen, occurrences are much higher for the sample firms than for the control firms, and the differences in occurrences are statistically significant. 21 In addition, the overall likelihood of having at least one of the events during the disclosure year is 41.0% for the sample firms versus 25.8% for the control firms. Panel C of Table 1 reports the frequencies of the first triggering event for our sample firms. While SOX 404 disclosure is the most frequent event, 41% of the sample firms experience triggering events before the disclosure of the SOX 404 report. This finding supports the conclusion by Ghosh and Lee (2013) that to a large extent, a firm’s IC problems should be known to the market, even before the ICMW disclosure. The SOX 302 ICMW disclosure is the second most common triggering event, as it accounts for 21.1% of the observations. Restructurings or write-downs, auditor switches, and CEO/CFO departures account for 13.1%, 4.9%, and 1.9% of the triggering events, respectively.

Sample Description

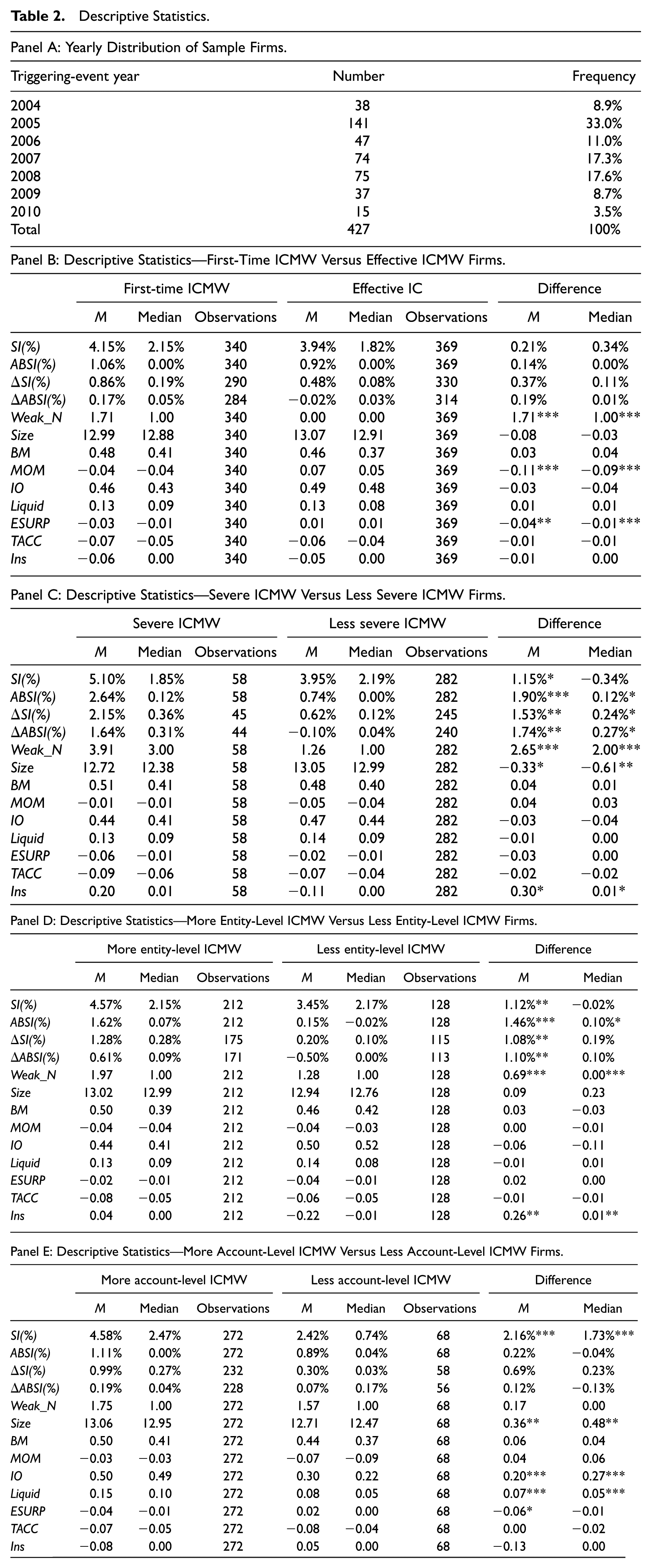

Table 2, Panel A, reports the yearly distribution of 427 first-time ICMW firms. The year 2005 is the year with the highest number of observations, approximately one third of the sample. As we focus solely on first-time ICMW reporting, the number of firms per year gradually declines after 2005. It increases in 2007 because of the late compliance dates for foreign filers and smaller firms. 22 Because of the variation in the distribution of observations by year, in the multivariate analysis, we include a year fixed effect.

Descriptive Statistics.

Note. This table provides descriptive statistics for the sample and control firms. Panel A shows the yearly distribution of the ICMW firms. Panels B and C provide a short-selling related comparison between first-time ICMW firms and effective IC firms, and between first-time ICMW firms with more and less severe IC problems, respectively. Panels D and E provide a short-selling-related comparison between first-time ICMW firms with the median and above and below the median entity-level and account-level ICD, respectively. Panel F presents a correlation matrix for the variables reported in Panels B through E. All variables are described in the appendix. ICMW = internal control material weaknesses; IC = internal control; SI = short interest; ABSI = abnormal short-interest ratio; BM = book value of equity to market value of equity.

**, and *** indicate significance at the 10%, 5%, and 1% levels, respectively.

Table 2, Panel B, reports the univariate short-selling statistics for first-time ICMW firms and matched effective IC firms. It also reports on variables known to affect short selling (all the variables used in our article are described in the appendix). To make the univariate results comparable with the multivariate results, we report the univariate statistics on observations for which data are available for all the control variables. While the mean values of the four short-interest measures (SI, ABSI, ΔSI, and ΔABSI) are consistently higher for first-time ICMW firms, none of the differences are statistically significant. We observe that some of the variables associated with short selling differ between the two groups, which underscores the importance of controlling for those variables in the multivariate tests. Specifically, at the mean level, ICMW firms enjoy lower return momentum and are more likely to report a negative earnings surprise (ESURP). First-time ICMW firms report a mean (median) of 1.71 (1.00) material weaknesses.

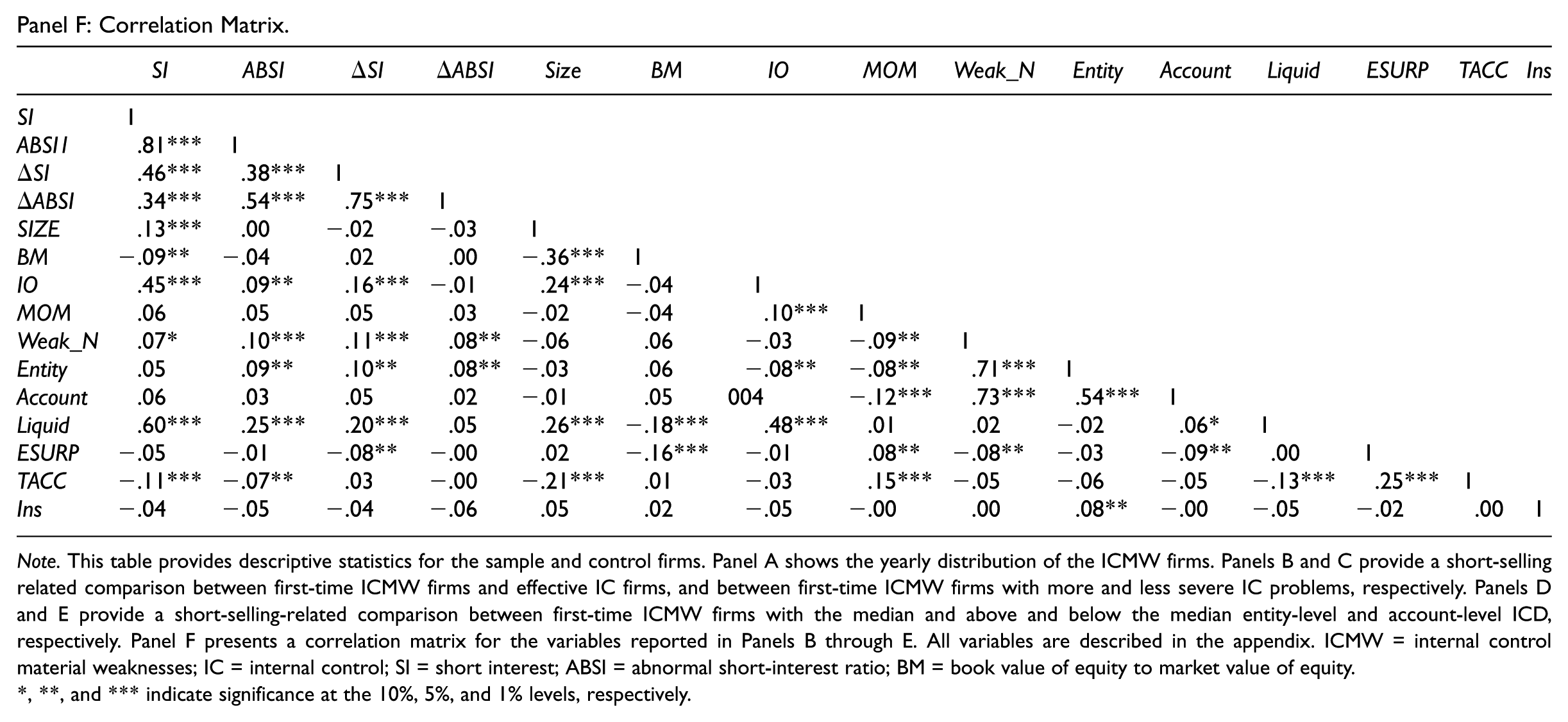

Panel C of Table 2 provides a similar comparison between firms with more severe and less severe ICMW. All four measures of short interest are significantly higher for firms with more severe ICMW. For example, ABSI is 1.90% higher (2.64% vs. 0.74%) for firms with more severe ICMW. The parameters affecting short selling are mostly not statistically different between the two groups. We only notice that firms with more severe ICMW are smaller and have a marginally higher level of insider trading (Ins). The mean (median) number of ICMW is 3.91 (3.00) for firms with more severe IC problems and 1.26 (1.00) for firms with less severe IC problems. Panel D (E) reports similar univariate statistics for firms with the number of entity-level (account-level) ICD at the median or above versus below the median. We see a significant difference in the mean value of all the measures of short selling between the firms with more entity-level ICD and those with less entity-level ICD. However, from Panel E, we see that only the mean level of short interest is higher for firms with more account-level ICD, while mean abnormal short selling and the mean changes in both short selling and abnormal short selling are not significantly different between the two groups. Table 2, Panel F, shows the correlation matrix for those variables. All the measures of short interest are highly correlated. We also see that the number of material weaknesses reported is positively correlated with all the measures of short selling, providing initial evidence that short sellers target firms with severe ICMW. We also see that the number of entity-level ICD is positively and significantly correlated with most measures of short selling, while the number of account-level ICD is not significantly correlated with any of the measures of short selling. The correlation results provide further evidence of short sellers’ ability to anticipate the revelation of ICMW when IC problems are more severe.

Empirical Analysis

Market Reaction and Short Interest Prior to ICMW Disclosure

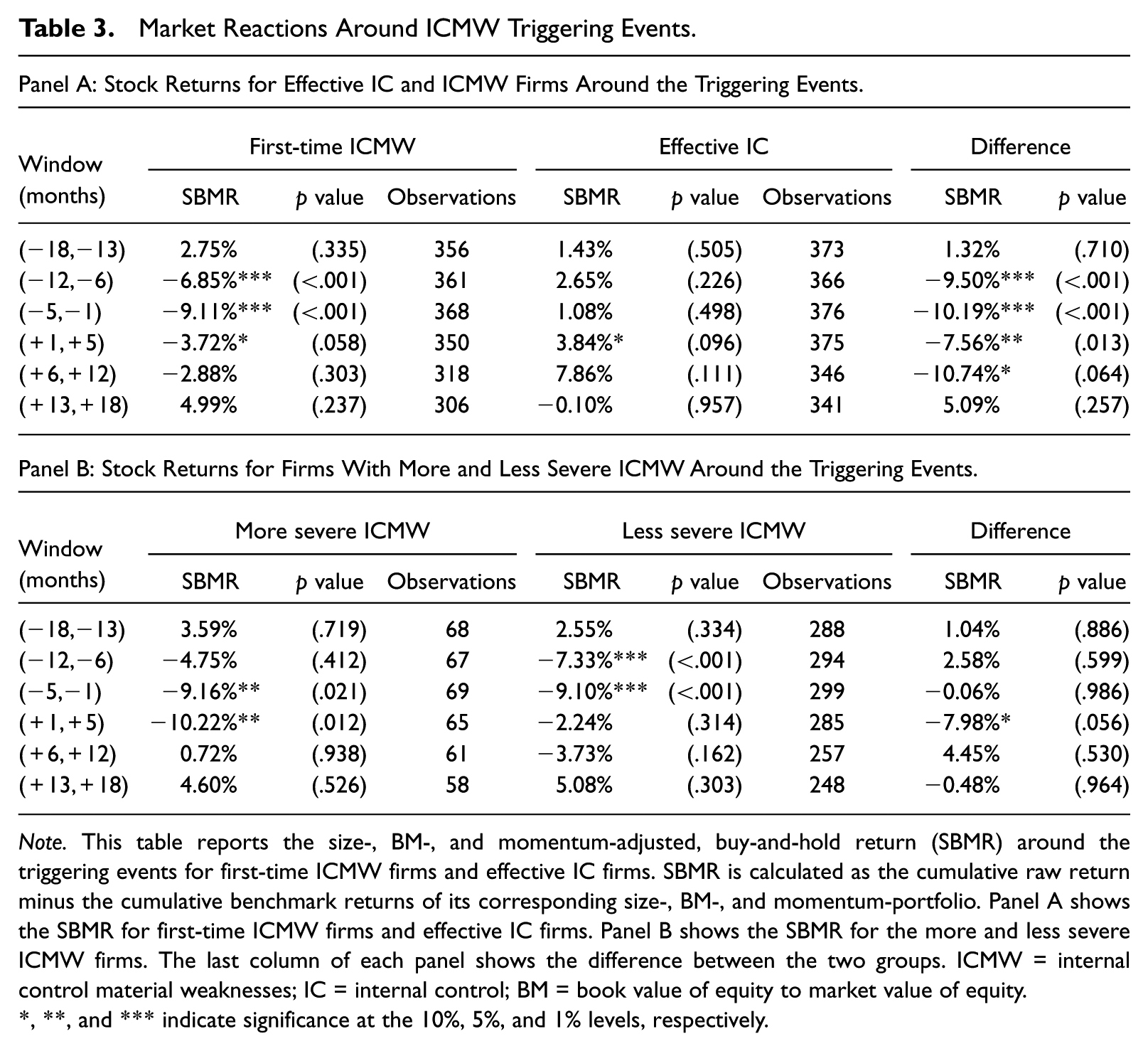

Because short sellers profit from the decline in stock prices, before examining the relation between short interest and ICMW, we first check the stock market performance around the revelation of IC information to ensure that an incentive for short selling does exist. We examine the pre- and post-ICMW triggering-event long-term abnormal returns. We measure abnormal returns, SBMR, by adjusting the buy-and-hold stock returns for size, BM (Fama & French, 1993), and momentum (Carhart, 1997). 23 We report the results in Table 3, Panel A. 24 In the 12 months leading to the event month, ICMW firms suffer significant negative stock returns. SBMR is −6.85% (−9.11) from 12 to 6 months (5 months to 1 month) prior to the event and is statistically significant. The returns of the matched sample of firms with effective IC are not significantly different from zero. More importantly, the returns of the ICMW firms are significantly more negative than those of the effective IC firms. In the first 5 months following the revelation month, ICMW firms continue to suffer significant negative abnormal returns, which are also more negative than those of the control firms. From Month 6 to Month 12, returns of the ICMW firms become insignificant from zero but are still significantly more negative than those of the control firms. In Panel B, we further present the long-term stock returns of the more and less severe ICMW groups. Compared with the less severe ICMW firms, the more severe ICMW firms experience a much more negative return in the first 5 months after the event date (−10.22% vs. −2.24%, respectively), while in all other periods, differences in returns between the two groups are insignificant. Finally, returns outside the 12 months around the event are not significantly different between the effective IC and the ICMW firms, as well as between the more severe and less severe ICMW groups.

Market Reactions Around ICMW Triggering Events.

Note. This table reports the size-, BM-, and momentum-adjusted, buy-and-hold return (SBMR) around the triggering events for first-time ICMW firms and effective IC firms. SBMR is calculated as the cumulative raw return minus the cumulative benchmark returns of its corresponding size-, BM-, and momentum-portfolio. Panel A shows the SBMR for first-time ICMW firms and effective IC firms. Panel B shows the SBMR for the more and less severe ICMW firms. The last column of each panel shows the difference between the two groups. ICMW = internal control material weaknesses; IC = internal control; BM = book value of equity to market value of equity.

**, and *** indicate significance at the 10%, 5%, and 1% levels, respectively.

There are three main takeaways from these results. First, investors who are able to anticipate IC problems can profit from shorting those shares beforehand. Moreover, investors can benefit from accumulating positions in ICMW firms early on, not just shortly before the ICMW revelations. Second, because the negative returns of ICMW persist for several months after the revelations, short sellers can benefit from maintaining their positions for some time after the event, especially in firms with more severe ICMW. Third, short interest should revert to normal levels approximately 6 months after the event.

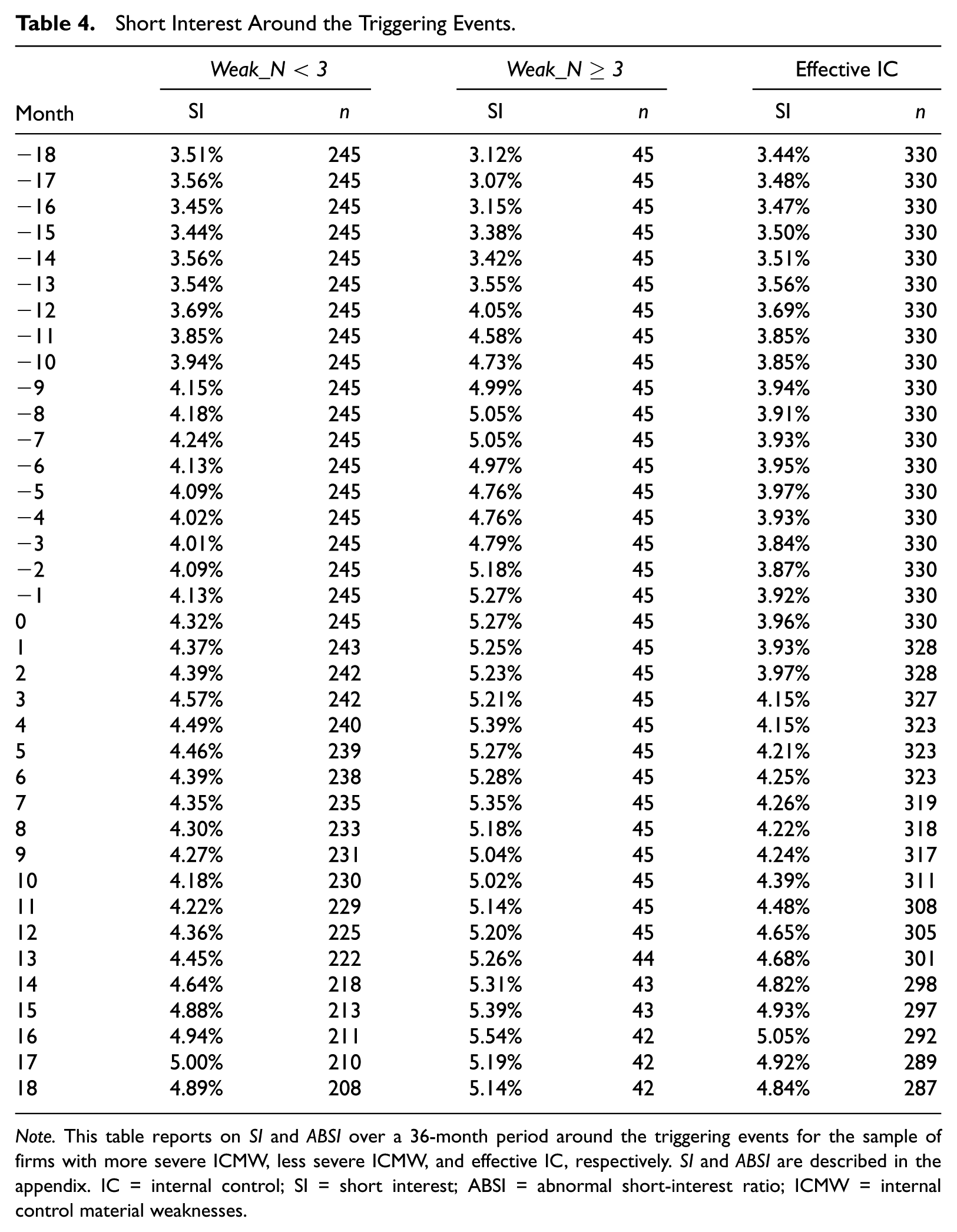

Table 4 reports the cumulative monthly short interest and abnormal short interest for first-time ICMW firms (separately for those with more and less severe ICMW), and for firms with effective IC, over a 36-month period surrounding the triggering-event date. To make it comparable with the multivariate results, we report the observations for which data are available for all the control variables. 25 For the more severe ICMW firms, we find that SI steadily increases from 3.12% 18 months prior to the ICMW disclosure, to 5.27% in the month prior to the ICMW revelation, a relative increase of 68.9%. The pattern for abnormal short interest is even stronger, as ABSI climbs from 1.12% to 2.75%, a 145.5% relative increase. However, the trend for firms with less severe ICMW during the same period is less pronounced, as SI increases by only 0.62%, from 3.51% to 4.13%, a relative increase of 17.7%, while ABSI actually decreases from 0.84% to 0.74%. For the firms with effective IC, SI goes up by 0.48%, from 3.44% to 3.92%, while ABSI decreases by 0.02%, from 0.86% to 0.84%.

Short Interest Around the Triggering Events.

Note. This table reports on SI and ABSI over a 36-month period around the triggering events for the sample of firms with more severe ICMW, less severe ICMW, and effective IC, respectively. SI and ABSI are described in the appendix. IC = internal control; SI = short interest; ABSI = abnormal short-interest ratio; ICMW = internal control material weaknesses.

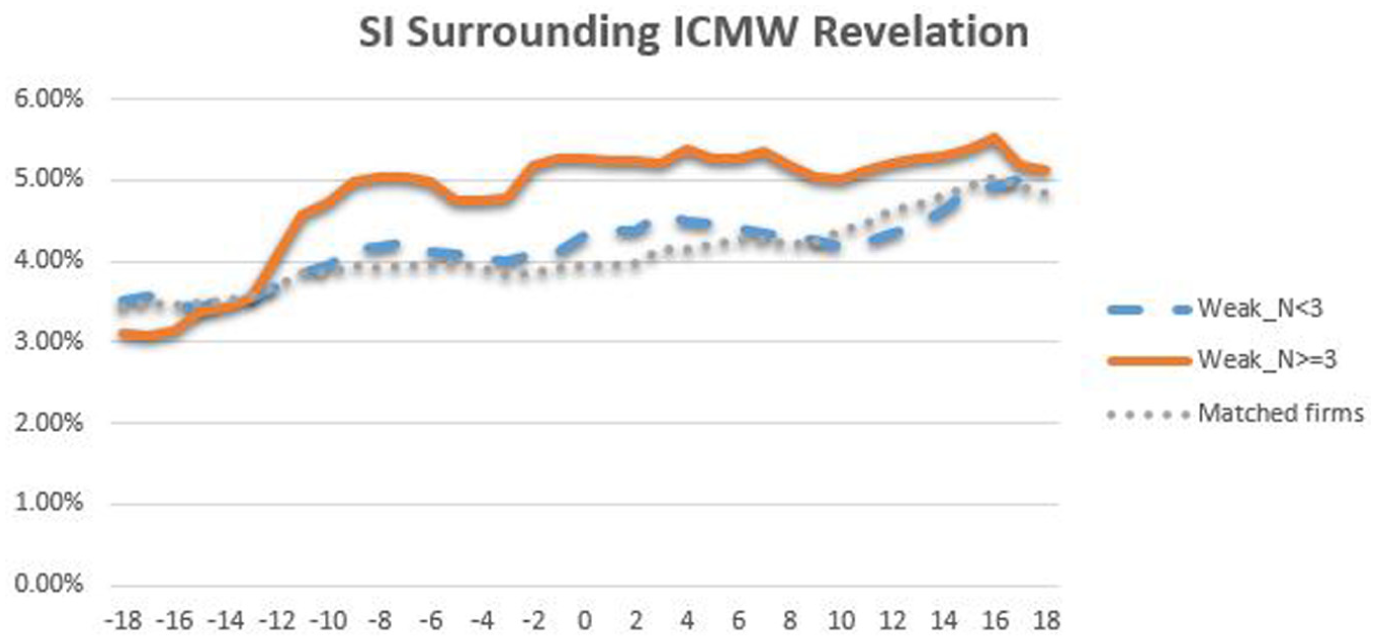

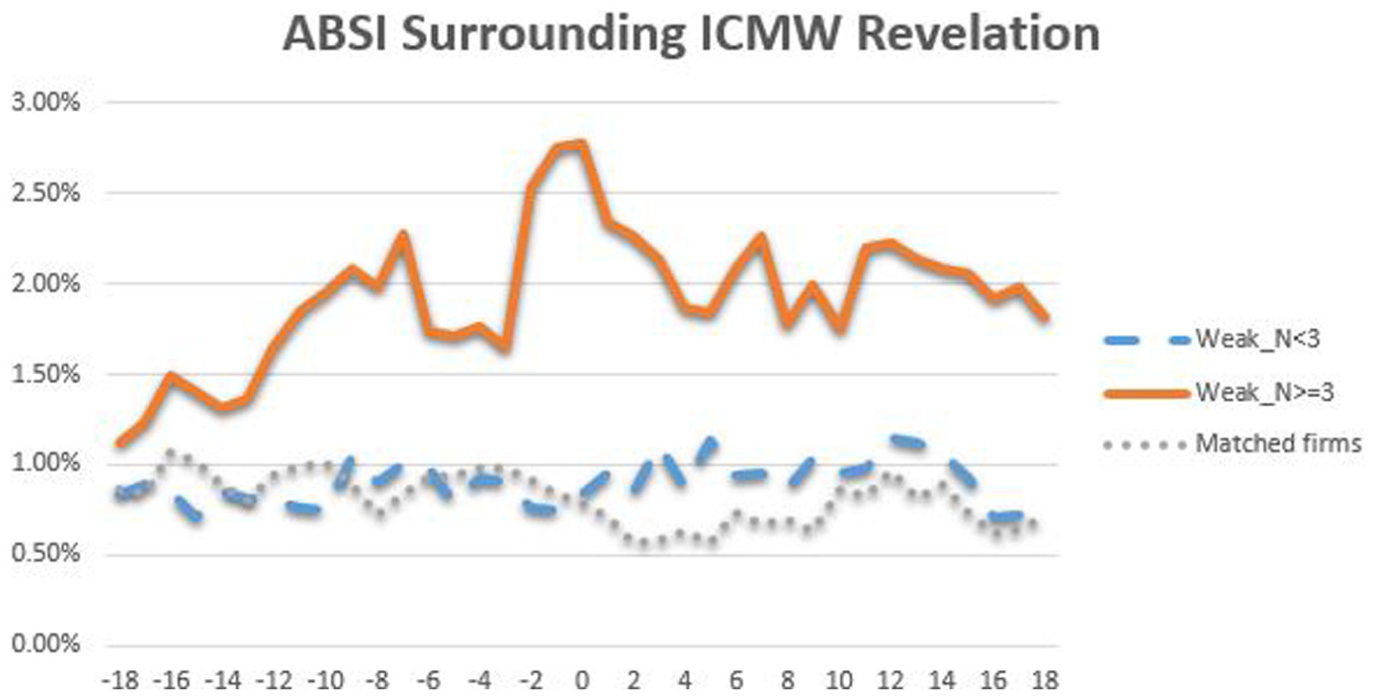

These patterns provide evidence that short sellers are able to identify firms that are about to reveal ICMW for the first time, but only when their IC problems are severe. Figures 1 and 2 depict the monthly SI and ABSI, respectively, for the three groups. Both figures show a large short-interest buildup for the firms with more severe IC problems. It is noteworthy that there is not much difference in SI and ABSI over the 18 months prior to the ICMW revelation between the less severe ICMW firms and the matched firms, which suggests that the more subtle IC problems are difficult to detect. We also observe that short sellers do not close their positions in firms with severe IC problems immediately after the ICMW revelations; instead, short interest remains at high levels for several months thereafter. This pattern is consistent with the stock return patterns documented in Table 3, which show that negative returns continue for several months after the ICMW revelation. The pattern of short interest we report in Table 4 and Figure 1 resembles those reported by Desai et al. (2006, Table 3, p. 79) for short selling around restatements, and by Karpoff and Lou (2010, Table 4, pp. 1891-1892 and Figure 2, p. 1893) for short selling around financial misconduct.

Short-interest trend around the triggering event.

Abnormal short-interest trend around the triggering event.

Short Interest, ICMW, and ICMW Severity—A Test of Hypothesis 1

Next, we employ multivariate regression models to investigate the relation between ex ante short selling and the ICMW revelation. If short sellers are informed on the IC quality of firms, and believe that ICMW will lead to higher business and information risks and/or will lower the present value of future cash flows, 26 then we will observe higher short interest for firms with ineffective IC. Moreover, if it is easier for outsiders to detect the more severe ICMW, or if they believe that more severe problems will lead to poorer subsequent performance, then we will observe a positive association between short selling and the degree of ICMW severity. We thus estimate the following three models (subscripts are eliminated for brevity) 27 :

For the dependent variable, we use SI, ABSI, ΔSI, and ΔABSI. In Equation 2, the variables of interest are ICMW, an indicator variable that is set to 1 for ICMW firms and to 0 for firms with effective IC, and Sev_ICMW, an indicator variable that is set to 1 for firms with severe ICMW and to 0 for all other firms. Admittedly, the use of three weaknesses to partition firms into more and less severe ICMW is arbitrary. Therefore, in Equation 3, we examine the association between short interest and ICMW using the integer variable Weak_N, the number of material weaknesses reported under SOX 404 (ranging from zero to 10). In Equation 4, we use entity-level ICD (Entity_ICD) and account-level ICD (Account_ICD) to proxy for the severity of ICMW, with the former being more severe. We set Entity_ICD (Account_ICD) to the number of entity-level (account-level) deficiencies in the SOX 404 report.

We augment the models by variables that may affect short selling. Size, BM, and MOM are as described earlier. IO is the proportion of the outstanding shares held by institutional investors at each quarter end. Hirshleifer, Teoh, and Yu (2011) argue that liquidity encourages arbitrage activities in general and may reduce short squeeze risk. Thus, we add to the model Liquid, the average share turnover in the previous 6 months, measured as shares traded, scaled by the total shares outstanding. Because approximately 80% of our sample firms disclose financial information alongside the ICMW information (e.g., when SOX 302 or SOX 404 is the triggering event), and because Christophe et al. (2004) find a short-interest buildup prior to negative earnings announcements, it is possible that short sales contain information regarding the firm’s earnings performance, regardless of its IC quality. Thus, we include in the model earnings surprise, ESURP, the change in annual earnings per share, scaled by the stock price at the beginning of the year. 28 Desai et al. (2006), Drake et al. (2011), and Hirshleifer et al. (2011) show that some short sellers base their positions on firms’ total accruals. Thus, it is possible that short sellers merely trade on the information in total accruals, rather than on IC foreknowledge. For this reason, we control for the previous year’s total accruals, TACC. Last, insider trading could also be a confounding event, given that a cascade of insider selling could signal upcoming unfavorable news events, or short sellers might just follow insider trading momentum. Therefore, we add to the model, Ins, the net insider selling in the year leading to the revelation of the IC report, scaled by the average total outstanding shares. We obtain insider trading data from Thomson Reuters, Form 4.

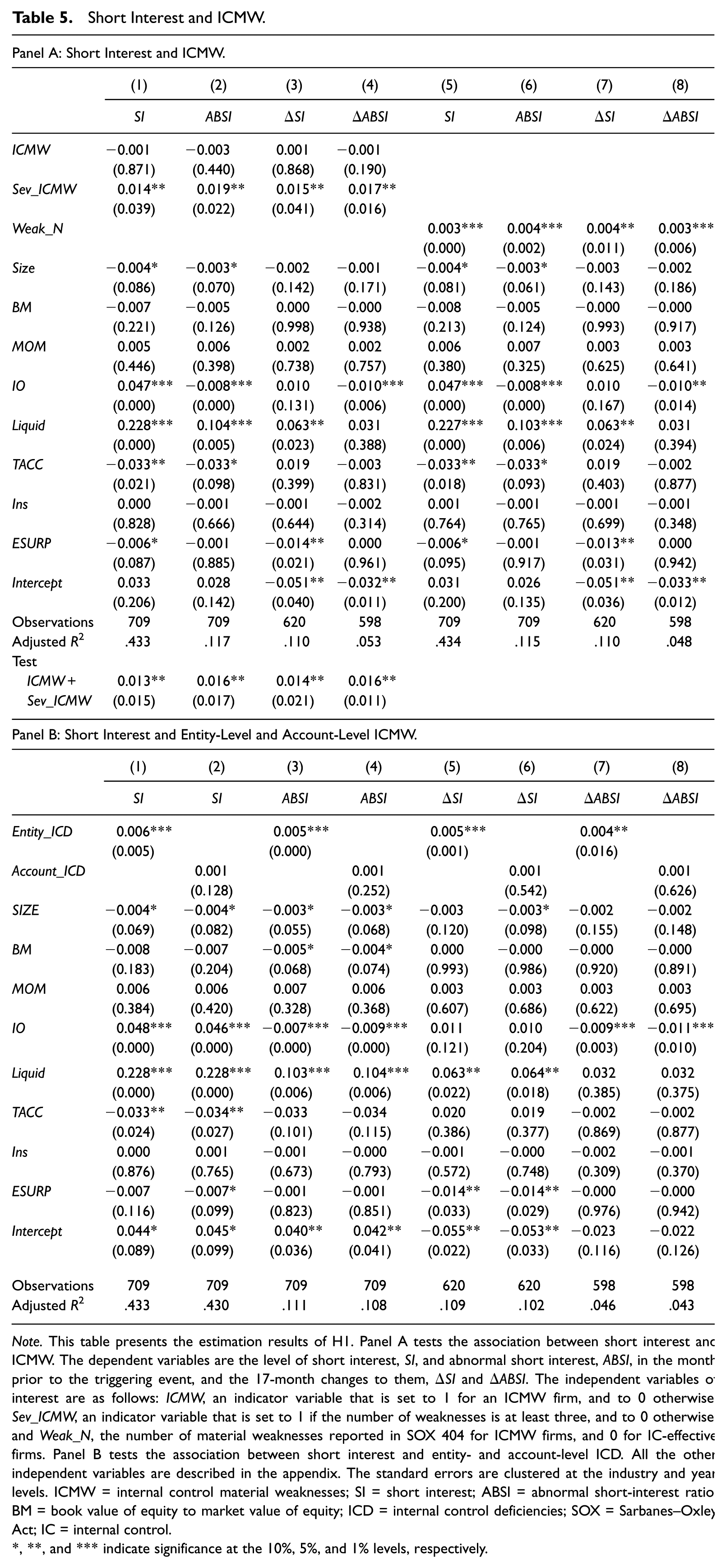

The estimation results of Equations 2 and 3 are presented in Panel A of Table 5 and those of Equation 4 are reported in Panel B. In columns (1) to (4) of Panel A, the coefficient on ICMW is insignificant, the coefficient on Sev_ICMW is positive and significant, and the sum of the coefficients ICMW and Sev_ICMW is positive and significant. Taken together, these results indicate a positive and significant association between short selling and ICMW, but only when ICMWs are more severe. The sum of the coefficients ICMW and Sev_ICMW in columns (3) and (4) of 0.013 and 0.016 means that economically, after controlling for firm characteristics, compared with firms with effective IC, firms with severe ICMW experience a 1.3% and 1.6% increase in short selling and abnormal short selling, respectively, in the months leading to the ICMW revelation. In columns (5) to (8) of Panel A, we find that the number of weaknesses, Weak_N, is significant in all four specifications. The coefficient on Weak_N in columns (7) and (8) suggests that economically, an increase of one material weakness in IC leads to a corresponding increase of 0.3% and 0.4% in short interest and abnormal short interest, respectively.

Short Interest and ICMW.

Note. This table presents the estimation results of H1. Panel A tests the association between short interest and ICMW. The dependent variables are the level of short interest, SI, and abnormal short interest, ABSI, in the month prior to the triggering event, and the 17-month changes to them, ΔSI and ΔABSI. The independent variables of interest are as follows: ICMW, an indicator variable that is set to 1 for an ICMW firm, and to 0 otherwise; Sev_ICMW, an indicator variable that is set to 1 if the number of weaknesses is at least three, and to 0 otherwise; and Weak_N, the number of material weaknesses reported in SOX 404 for ICMW firms, and 0 for IC-effective firms. Panel B tests the association between short interest and entity- and account-level ICD. All the other independent variables are described in the appendix. The standard errors are clustered at the industry and year levels. ICMW = internal control material weaknesses; SI = short interest; ABSI = abnormal short-interest ratio; BM = book value of equity to market value of equity; ICD = internal control deficiencies; SOX = Sarbanes–Oxley Act; IC = internal control.

**, and *** indicate significance at the 10%, 5%, and 1% levels, respectively.

Results from Panel B show that short interest is positively and significantly associated with Entity_ICD in all four specifications but is insignificantly associated with Account_ICD. These results further suggest that short sellers identify and trade on severe control problems. Because account-specific ICD are more likely to be apparent in the financial statements than general entity-level ICD, the association of short selling only with entity-level ICD further supports our assertion that the prediction of ICMW requires more than just an in-depth analysis of financial reporting numbers. As for the control variables, the coefficient on Size is negative, and significant in some specifications, providing some evidence that there is more short selling in smaller firms. The liquidity proxy is always positive, and is significant under most specifications, which is consistent with the findings in Hirshleifer et al. (2011). The coefficient on TACC is mostly negative, and is significant when SI is the dependent variable, which is inconsistent with the findings in Drake et al. (2011) and Hirshleifer et al. (2011) of a positive association between short interest and accruals. The proxy for institutional holding, IO, does not obtain a consistent coefficient, while the other control variables are mostly insignificant.

Overall, the findings in Table 5 suggest that although short sellers are capable of detecting IC problems, this ability rests on the degree of IC severity, with the more severe problems being more likely detected. The fact that we observe significant short selling also under the change specifications should ease concerns of an omitted variables problem. In sum, the results from Tables 4 and 5 do not support H1, but do support H1a of a positive association between short selling and severe ICMW. Our results indicate that the information related to IC problems is of interest to short sellers, and changes their expectations of firms’ future performance, leading them to bet against those firms before ICMW is revealed.

Short Interest and Prediction of ICMW—A Test of Hypothesis 2

Thus far, we have shown that short selling prior to the ICMW revelation is positively associated with ICMW severity. However, this positive association merely indicates that short selling contains information related to ICMW and says nothing as to whether this information is incremental to the information known to investors. We use a two-stage regression to decompose the trades into private information and public information related. We then test whether short sellers rely on public information (H2a), and/or on private information (H2b), to predict ICMW. In the first stage, we run a Poisson regression of the number of material weaknesses, Weak_N, on variables that have been shown by prior research to be associated with the probability of reporting ICMW. This stage generates Pre_weak, the predicted ICMW component, and Res_weak, the residual or the unexpected ICMW component.

In the second stage, we replace Weak_N in Equation 3 with Pre_weak and Res_weak. If short sellers simply rely on firm fundamentals or firsthand information, then our short-interest measures will be associated with Pre_weak, but not with Res_weak. In other words, short selling would not provide incremental information for predicting upcoming ICMW. On the contrary, if short sellers provide incremental information to predict ICMW, there will be an association between short interest and Res_weak. Thus, we run the following two models:

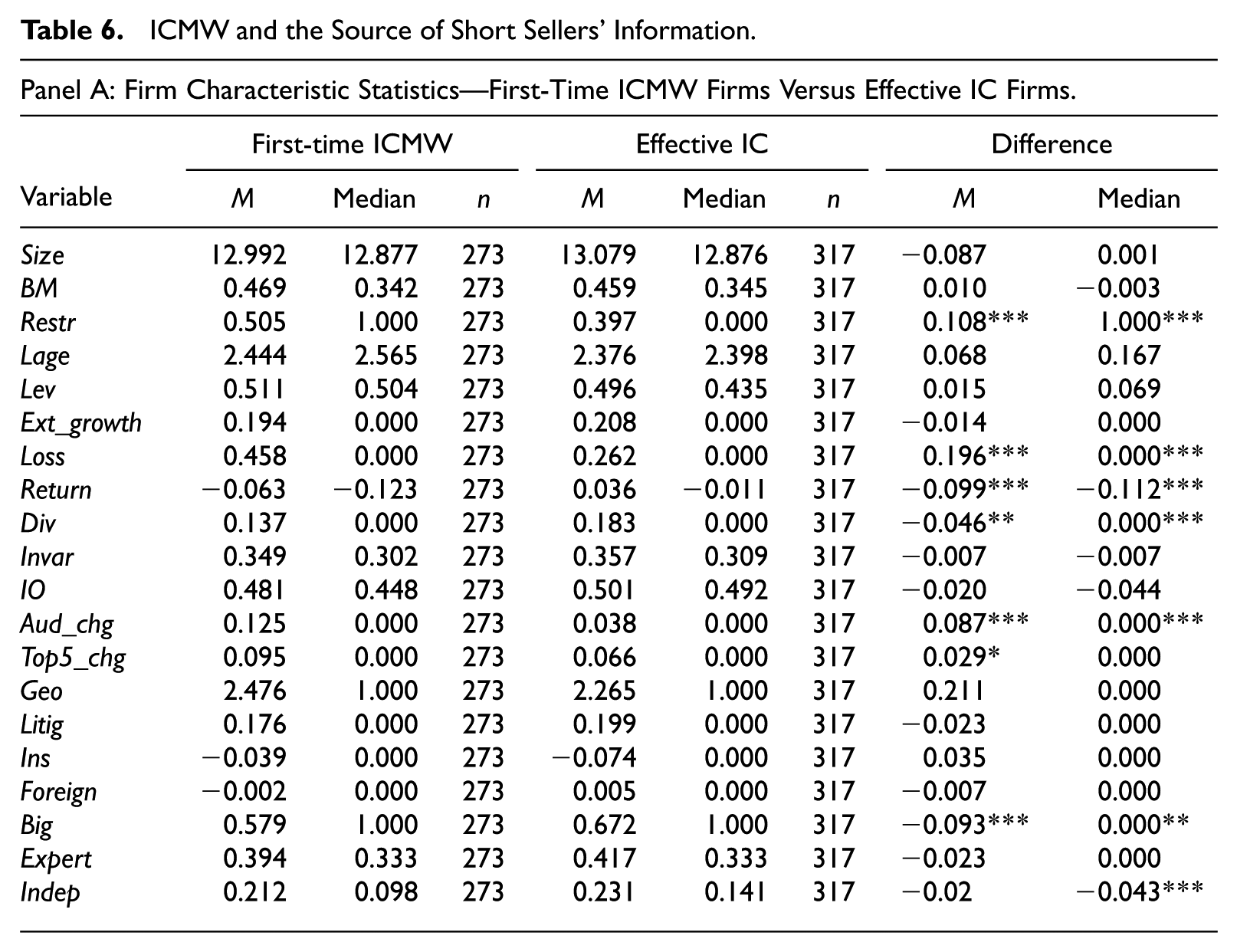

In the first stage (Equation 5), the independent variables are those known to be associated with IC problems. Ge and McVay (2005) find that ICMW firms are more complex, smaller, and less profitable than effective IC firms. Doyle et al. (2007) further find that ICMW firms are younger, grow rapidly, and undergo restructuring. Ashbaugh-Skaife et al. (2007) find that ICMW firms have fewer resources available for investing in IC, greater accounting risk, and are less likely to use the services of big audit firms; moreover, such firms are more likely to have foreign sales, are more likely to replace the external auditor, 29 and are more likely to have higher ownership concentration. Ghosh and Lee (2013) find that ICMW firms are positively associated with profitability and with litigation risk. Ashbaugh-Skaife, Veenman, and Wangerin (2013) find a positive association between ICMW and the profitability of insider trading. Chen, Lai, Liu, and McVay (2015) show that ICMW firms pay fewer dividends. Last, Zhang, Zhou, and Zhou (2007) find that in the post-SOX period, firms are more likely to report ICMW if their audit committee has less financial expertise and if their auditor is more independent. Therefore, we include measures of all these variables (described in the appendix) in the model. As a final step, given our earlier finding of a higher likelihood of top-management change in firms reporting ICMW, we add to the model Top5_chg, an indicator variable for a change in at least one of the top five management positions.

Table 6, Panel A, reports the univariate comparison of those firm parameters between the ICMW firms and the control firms, and shows some significant differences. The results of the first stage are reported in Table 6, Panel B. Among the explanatory variables, Lev, Loss, Top5_chg, Geo, and Fore are positively associated with Weak_N, confirming that ICMW is more severe for more leveraged firms, unprofitable firms, firms with top-management change, and firms with more complex operations. Size, Big, AC_FC, 30 and Div are negative and significant, suggesting that ICMW is less severe for larger firms, firms that use a Big-4 auditor or more independent auditor, firms with more financial expertise on the audit committee, and those distributing dividends. The remaining variables are insignificantly associated with Weak_N.

ICMW and the Source of Short Sellers’ Information.

Note. This table presents the estimation results of H2a and H2b. Panel A reports univariate statistics on firm characteristics for the ICMW firms and for the control sample of firms with effective IC. Panel B reports the multivariate results of the first stage using a Poisson regression. The dependent variable, Weak_N, is the number of ICMW reported under SOX 404, and the independent variables are firm parameters known to be associated with ICMW. In the second stage (Panel C), the dependent variables are the level of short interest, SI, and abnormal short interest, ABSI, in the month prior to the triggering event, and the 17-month changes to them, ΔSI and ΔABSI. The independent variables of interest are the predicted and residual values from the first stage Pre_weak and Res_weak. All other independent variables are described in the appendix. The standard errors are clustered at the industry and year levels. ICMW = internal control material weaknesses; IC = internal control; BM = book value of equity to market value of equity; SI = short interest; ABSI = abnormal short-interest ratio; SOX = Sarbanes–Oxley Act.

**, and *** indicate significance at the 10%, 5%, and 1% levels, respectively.

The results of the second stage (Equation 6) are reported in Table 6, Panel C. In support of H2b, we find that Res_weak is positively and significantly associated with short selling, implying that short sellers trade on the unexpected component of ICMW. The coefficient on Pre_weak, on the contrary, is either insignificant or weakly significant. Thus, we find little evidence that short sellers rely on public information to predict ICMW (H2A). Overall, the results suggest that short sellers mainly rely on private information, and thus, their trades convey incremental information to the market.

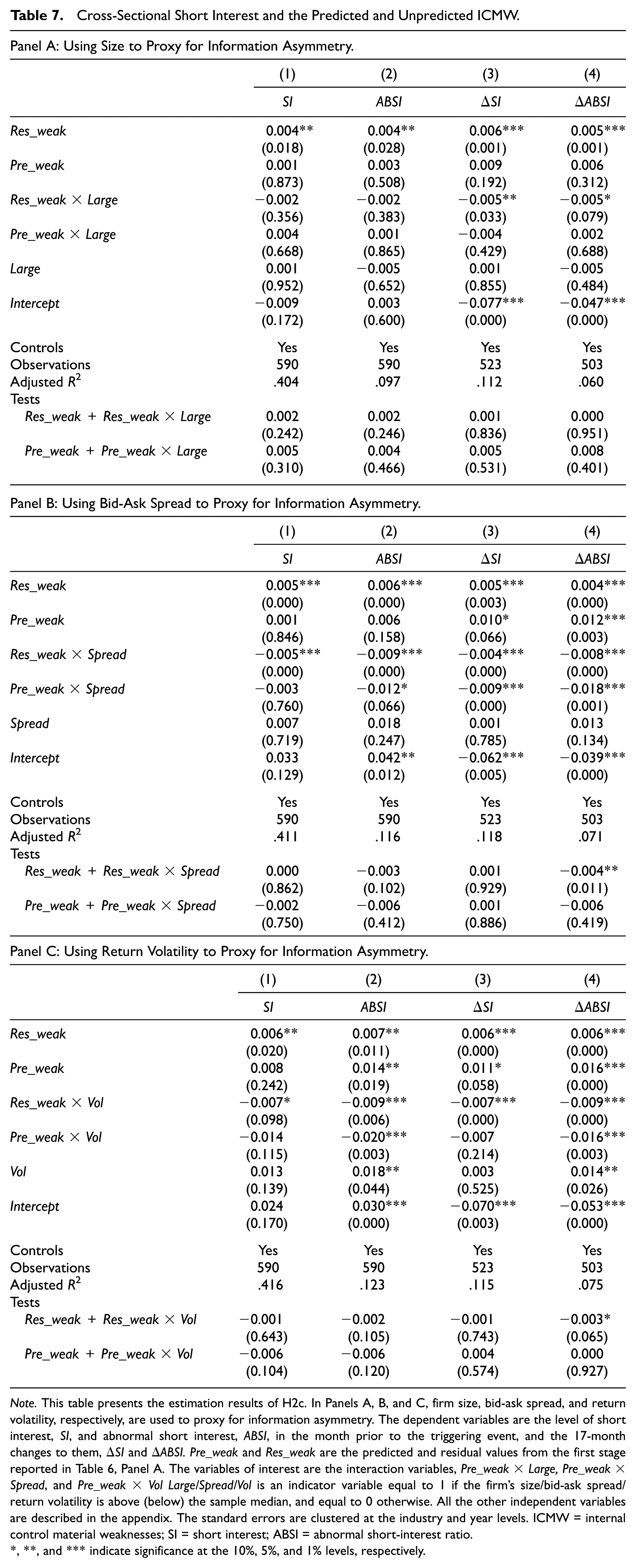

To further investigate the usefulness of short selling, we examine our prediction in H2c that the incremental predictability of short sellers’ trades will increase with the degree of the firm’s information asymmetry. Our empirical test expands the second-stage regression to incorporate cross-sectional variation in the information environment. Thus, we run the following model:

In Equation 7, Asymmetry captures the information environment of the firm. We employ three proxies for information asymmetry: (a) firm size (Cheng, Dhaliwal, & Neamtiu, 2011), Large; (b) bid-ask spread (Coller & Yohn, 1997), Spread; and (c) return volatility (Cheng et al., 2011). Vol. Large is an indicator variable set to 1 if firm size is above the sample median, and to 0 otherwise; Spread is an indicator variable that is set to 1 if a firm’s bid-ask spread is below the sample median, and to 0 otherwise; and Vol is an indicator variable that is set to 1 if the firm’s return volatility is below the sample median, and to 0 otherwise.

Panels A, B, and C, Table 7, report the results, using Large, Spread, and Vol, respectively, to proxy for information asymmetry. In all specifications, the coefficient on Res_weak is positive and significant. The coefficient on the interaction term Res_weak×Large/Spread/Vol is always negative, and in 10 out of 12 model specifications is statistically significant, and the sum of coefficients on Res_weak and Res_weak×Large/Spread/Vol is mostly insignificant. Taken together, these results generally support the prediction in H2c that short sellers’ information advantage vastly disappears when firms’ information-environment quality is high. The results are consistent with the conclusion by Pownall and Simko (2005) that short sellers provide perceived value when limited alternative guidance sources are available.

Cross-Sectional Short Interest and the Predicted and Unpredicted ICMW.

Note. This table presents the estimation results of H2c. In Panels A, B, and C, firm size, bid-ask spread, and return volatility, respectively, are used to proxy for information asymmetry. The dependent variables are the level of short interest, SI, and abnormal short interest, ABSI, in the month prior to the triggering event, and the 17-month changes to them, ΔSI and ΔABSI. Pre_weak and Res_weak are the predicted and residual values from the first stage reported in Table 6, Panel A. The variables of interest are the interaction variables, Pre_weak×Large, Pre_weak×Spread, and Pre_weak×Vol Large/Spread/Vol is an indicator variable equal to 1 if the firm’s size/bid-ask spread/return volatility is above (below) the sample median, and equal to 0 otherwise. All the other independent variables are described in the appendix. The standard errors are clustered at the industry and year levels. ICMW = internal control material weaknesses; SI = short interest; ABSI = abnormal short-interest ratio.

**, and *** indicate significance at the 10%, 5%, and 1% levels, respectively.

Additional Analysis

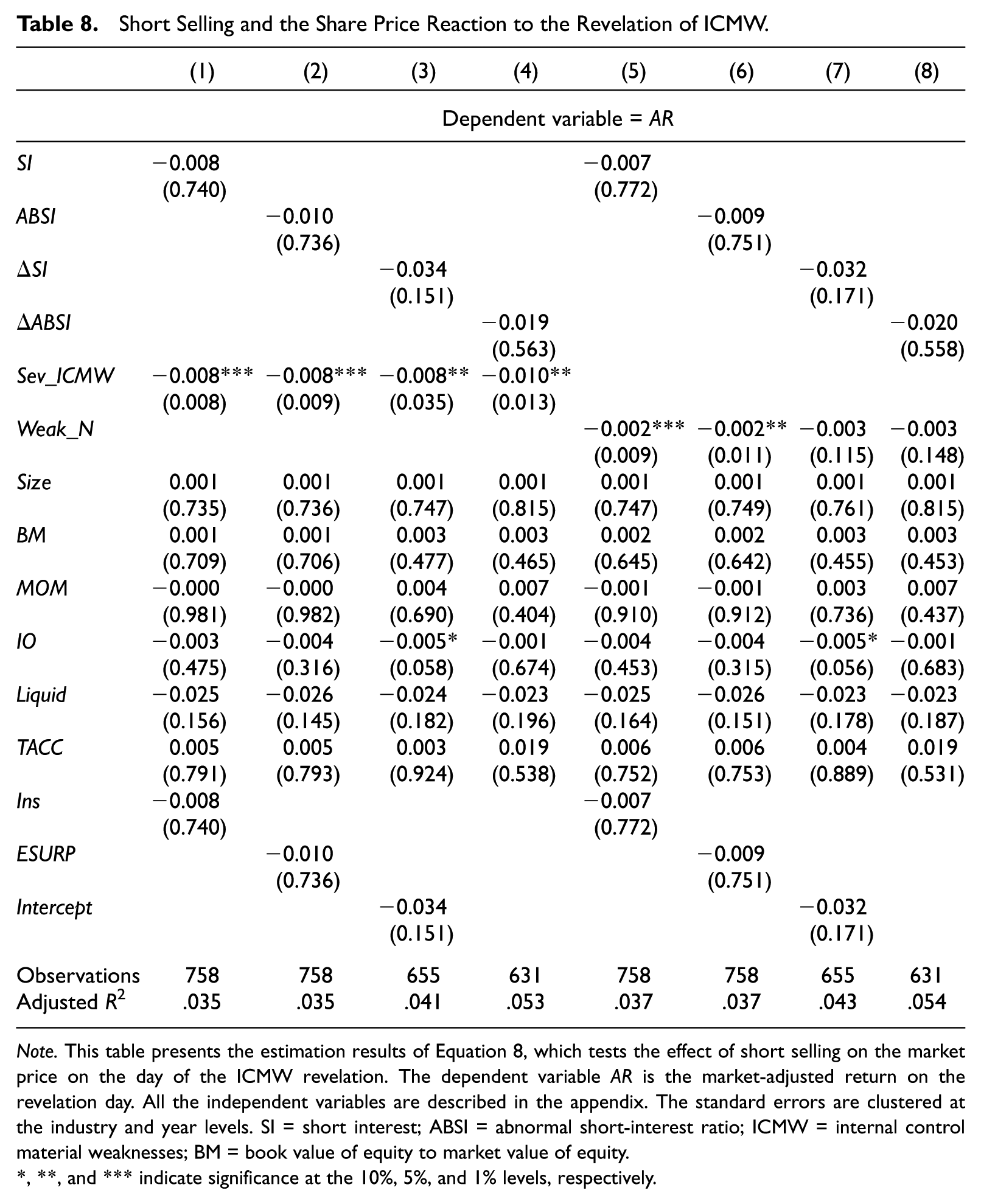

During the financial crisis, short sellers were accused of creating a market price downward spiral and using inappropriate trading strategies to obtain high trading profits. In the beginning of September 2008, the SEC temporarily banned short sales in financial stocks and placed new requirements on shares borrowing, in part because of this critical view of short sellers (Karpoff & Lou, 2010). To investigate whether short selling in firms with ICMW drives stock prices down too far, we follow the procedure in Karpoff and Lou (2010) and run the following model 31 :

In Equation 8, AR is the market-adjusted stock return on the triggering-event day, calculated as the difference between the raw stock return and the value-weighted market return. If the revelation date return is sensitive to the severity of the ICMW, then the coefficient β2 will be negative. If short selling generates a negative market reaction that is unrelated to the revelation, then β1 will be negative. Results from the model presented in Equation 8 are reported in Table 8. As can be seen, β2 is significant whether Sev_ICMW or Weak_N is used. On the contrary, β1 is insignificant in all eight model specifications. These results lead us to conclude that short selling by itself does not lead to a stock market overreaction to ICMW.

Short Selling and the Share Price Reaction to the Revelation of ICMW.

Note. This table presents the estimation results of Equation 8, which tests the effect of short selling on the market price on the day of the ICMW revelation. The dependent variable AR is the market-adjusted return on the revelation day. All the independent variables are described in the appendix. The standard errors are clustered at the industry and year levels. SI = short interest; ABSI = abnormal short-interest ratio; ICMW = internal control material weaknesses; BM = book value of equity to market value of equity.

**, and *** indicate significance at the 10%, 5%, and 1% levels, respectively.

Conclusion

In this study, we examine short selling prior to the disclosure of a corporate governance deficiency in the form of ICMW over financial reporting. We document short-interest accumulation in the 17-month period preceding the ICMW revelation, but only in firms with more severe ICMW. Multivariate results show a positive association between short interest and the severity of ICMW, indicating that short sellers are able to detect IC problems when they are severe.

We next decompose ICMW into two components: those predicted by parameters known to be associated with ICMW and those that are unpredicted, and we examine short-interest association with the two components. We find that the unpredicted component is strongly associated with short interest, which implies that short sellers’ information of firms’ IC quality is incremental to the information known to the market. We only find some weak evidence for an association between short selling and the predicted component. In additional tests, we find that short interest is more predictive of ICMW when the information environment of the firm is poor. Finally, we fail to find evidence that short selling prior to the revelation of ICMW leads to an excessive market reaction to the bad news on the revelation day. The overall findings of short selling prior to the ICMW revelation further highlight a path through which ICMW disclosure affects the equity market.

Footnotes

Appendix

Description of Variables.

| Main variables | |

|---|---|

| ICMW | Equal to 1 if a firm reports material weaknesses in IC under SOX 404; equal to 0 otherwise. |

| Sev_ICMW | Equal to 1 if a firm reports at least three material weaknesses in its IC under SOX 404; equal to 0 otherwise. |

| Weak_N | The number of material weaknesses in the SOX 404 report. |

| SI | The number of stock-split-adjusted shares shorted, scaled by the number of outstanding shares in the month before the triggering event. |

| Entity_ICD | The number of entity-level IC deficiencies in the SOX 404 report. Entity-level material weaknesses include the following: Senior management competency, tone, reliability issues Segregations of duties/design of controls (personnel) Ineffective, nonexistent, or understaffed audit committee Inadequate disclosure controls (timely, accuracy, complete) Insufficient or nonexistent internal audit function Accounting personnel resources, competency/training Information technology, software, security, and access issues |

| Account_ICD | The number of account-level IC deficiencies in the SOX 404 report. Account-level material weaknesses include the following: Material and/or numerous year-end adjustments, including those proposed by the auditor Untimely or inadequate account reconciliations Journal entry control issues Nonroutine transaction control issues Treasury control issues Accounting documentation, policy, and/or procedures Ethical or compliance issues with personnel Ineffective regulatory compliance issues |

| ABSI | Abnormal short interest after controlling for firm size, book-to-market, momentum, share turnover, and institutional ownership in the month before the triggering event. |

| ΔSI | The difference in SI between month −1 and month −18. |

| ΔABSI | The difference in ABSI between month −1 and month −18. |

| Control variables | |

| Size | The natural logarithm of market capitalization. |

| BM | The ratio of the book value of equity to the market value of equity. |

| MOM | The cumulative raw stock return over the previous 6 months. |

| IO | The percentage of institutional ownership. |

| Liquid | Average monthly share turnover over the previous 6 months, calculated as the number of monthly shares traded, scaled by the number of shares outstanding. |

| ESURP | The difference between the current year and the previous year’s earnings per share, scaled by the beginning of the year stock price. |

| TACC | Net income before extraordinary items and discontinued operations minus operating cash flow, scaled by average total assets. |

| Ins | Net insider selling in the year of the IC revelation, scaled by the average number of outstanding shares. |

| Restr | Equal to 1 if negative special items, scaled by average total assets, are larger than 1%; equal to 0 otherwise. |

| Lage | The natural logarithm of the firm’s age. Firm age is the number of years the firm has been listed on a stock exchange. |

| Lev | The ratio of total debt to total assets. |

| Ext_growth | Equal to 1 if the year-over-year industry-adjusted sales growth falls into the top quintile, and zero otherwise. |

| Div | Equal to 1 if a firm distributes dividends in the fiscal year; equal to 0 otherwise. |

| Loss | Equal to 1 if a firm reports a loss in the fiscal year; equal to 0 otherwise. |

| Return | The cumulative annual stock return for the fiscal year of the IC opinion. |

| Invar | The ratio of the sum of inventory and accounts receivable to total assets. |

| Fore | The ratio of total foreign sales to total sales. |

| Big | Equal to 1 if a firm is audited by a Big-4 auditor; equal to 0 otherwise. |

| Aud_chg | Equal to 1 if there is a change of auditor during the year prior to ICMW; equal to 0 otherwise. |

| Top5_chg | Equal to 1 if there is a change in one of the top five executive positions in the year prior to ICMW; equal to 0 otherwise. |

| Geo | The natural logarithm of the number of geographical segments. |

| Litig | Equal to 1 if a firm is in one of the SIC codes: 2833-2836, 3570-3577, 3600-3674, 7370; equal to 0 otherwise. |

| Large | Equal to 1 if a firm’s size is above the sample median; equal to 0 otherwise. |

| Spread | Equal to 1 if a firm’s average daily bid-ask spread is below the sample median; equal to 0 otherwise. |

| Vol | Equal to 1 if a firm’s return volatility, measured as the standard deviation of the firm’s monthly stock return for the year, is smaller than the sample median; equal to 0 otherwise. |

| Indep | Auditor’s independence, measured as the ratio of fees for nonaudit services to total fees paid to the auditor. |

| Expert | The proportion of the audit committee members defined as financial experts. |

| AR | Market-adjusted stock return on the ICMW revelation day, calculated as the difference between the raw stock return and the value-weighted market return. |

Note. ICMW = internal control material weaknesses; IC = internal control; SOX = Sarbanes–Oxley Act; SI = short interest; ICD = internal control deficiencies; ABSI = abnormal short-interest ratio; BM = book value of equity to market value of equity.

Acknowledgements

We are grateful for the valuable comments and suggestions we received from Bharat Sarath (the Editor). We would also like to thank two anonymous reviewers, participants at the 2013 American Accounting Association (AAA) Annual Meeting, the 2013 Canadian Academic Accounting Association (CAAA) Annual Meeting, the 2014 European Accounting Association (EAA) Annual Meeting, and the 2014 Financial Accounting and Reporting Section (FARS) Midyear Meeting, and seminar participants at the University of Alabama, Huntsville.

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

The author(s) received no financial support for the research, authorship, and/or publication of this article.