Abstract

This article examines the importance of leadership in the context of the internal audit function (IAF). We investigate the influence of the Chief Audit Executive’s (CAE) leadership in enabling the IAF to become a strategic player in corporate governance (CG). Using the responses of 804 CAEs from the Anglosphere countries and South Africa, we find that strong CAE leadership skills and the existence of a leadership training program are significantly and positively associated with IAF involvement in CG processes. This provides support for the argument that CAEs with strong leadership skills help the IAF to move from a behind-the-scenes player to a key actor in the improvement of CG practices, increasing the IAF’s organizational relevance. We also find that the use of a risk-based audit plan, the existence of a quality assurance and improvement program (QAIP), activity type (consulting vs. assurance), and IAF size are also positively associated with IAF involvement in CG. These findings suggest that IAF activity characteristics also have significant implications for this function’s stronger involvement in the CG space.

Keywords

Introduction

After the financial reporting scandals of the early 2000s, subsequent changes in laws (e.g., the Sarbanes-Oxley Act), regulations, and corporate governance (CG) codes throughout the world have offered opportunities to expand the internal audit function’s (IAF) governance remit. By evaluating and improving internal controls and risk management processes, the IAF can support all other CG parties (the board, the audit committee, senior managers, and external auditors) in discharging their legal responsibilities and can help organizations to comply with laws and codes provisions regarding CG (Gramling, Maletta, Schneider, & Church, 2004).

The literature on the IAF’s contributions to CG indicates that the IAF can play multiple roles. Several studies (Cohen, Krishnamoorthy, & Wright, 2004; D’Silva & Ridley, 2007; Goodwin-Stewart & Kent, 2006; Narayanaswamy, Raghunandan, & Rama, 2018) have considered this issue from an agency theory perspective and have posited that the IAF acts as an internal governance mechanism that mitigates the agency problem to shareholder’s benefits by providing assurance to the board and its audit committee, which ensures that adequate controls are in place to prevent the risks of unethical behaviors by managers (Norman, Rose, & Rose, 2010; Soh, Martinov-Bennie, 2015) and assuring the reliability of financial information (Prawitt et al., 2009).

Other studies have adopted the arguments of resource dependency theory, highlighting that the IAF’s contributions to CG emerge through this function’s role in enhancing organization strategic management processes (Roussy & Perron, 2018). For instance, Melville (2003) asserted that, in modern business systems, internal auditors should help organizations to configure their resources within a changing environment, to meet markets’ needs and to fulfill stakeholder expectations. To achieve this result, internal auditors should examine the links between organizational strategy and control systems, with specific reference to performance measurement. This would ensure that managers focus on the acquisition, development, and protection of resources and competencies that are key for long-term success. A global survey of the internal audit (IA) profession showed that business viability assessment and the reviewing of the links between strategy and company performance (Alkafaji, Hussain, Khallaf, & Majdalawief, 2011) form part of the IAFs’ activities to support the board and senior managers in strategic decision-making.

The extension of the IAF’s scope into CG space has also been acknowledged by the Institute of Internal Auditors (IIA) Inc. which, since 1999, has recognized that a value-adding IAF helps an organization to improve its governance processes (IIA, 1999). Some commentators consider this extension and enlargement of the IAF mission to be an evolutionary step in the development of the IAF’s role over time: overlaying its traditional function of being a service to mid-level managers with an enhanced role of assistance to the board, the audit committee, and senior managers to effectively deal with governance and strategic issues (Chambers & Odar, 2015). This change underpins key opportunities for an IAF to enhance its organizational status, relevance, and prestige, as it can take advantage of the opportunity to work closely with key organizational personnel to demonstrate that it can contribute to organizational value creation and preservation.

Although the IAF clearly has a potential role to play in CG, empirical studies show that they are not always actively involved in these activities. For instance, a global 2010 study of the IA profession found that the percentage of IAFs that review CG processes is lower than 45%. Furthermore, this percentage differs between regions, listed versus unlisted companies, and organizations (Allegrini, D’Onza, Melville, Sarens, & Selim, 2011). Another global study, in 2015, showed the IAF’s involvement in CG depends on the specific governance processes evaluated by internal auditors, with only 25% involved in strategic management process (Ramamoorti & Siegfried, 2016). These study results demonstrate that, in many organizations, the IAF has difficulties becoming a CG gatekeeper and their role in governance and strategic issues is still marginal. Thus, a gap exists and persists between what the literature and the definition provided by the IIA Inc. claim and what is delivered in practice (Spira & Page, 2003).

To date, there has been little specific research on the factors that influence the IAF’s involvement in CG. One study (Sarens, Abdolmohammadi, & Lenz, 2012) found that the use of a risk-based audit plan, the existence of a quality assurance and improvement program (QAIP), and the use of audit committee input to establish the audit plan are significant and positively associated with the IAF having an active role in CG. This study did not consider internal auditors’ personal characteristics’ influences on this role.

Other studies have argued that the Chief Audit Executive’s (CAE) quality of skills and competencies largely influence the IAF’s effectiveness in general and specifically in CG (Lenz & Hanh, 2015; Mihret & Grant, 2017). For instance, Dittenhofer, Ramamoorti, Ziegenfuss, and Evans (2010) maintain that CAEs should cultivate appropriate soft skills and that of these, leadership is the most vital in building and maintaining positive relationships with its primary stakeholders: the board, the audit committee, and senior managers. Ramamoorti and Siegfried (2016) concur with this view and state that CAE leadership skills are vital in increasing the IAF’s stature and credibility vis-a-vis its primary stakeholders to gain their trust, respect, and support. Leadership is also seen as helping the CAE to be comfortable when reporting issues, concerning risk and internal controls to the board and the audit committee, and supports a direct and clear communication with the IAF’s stakeholders (Chambers, Eldridge, & Park, 2010). Furthermore, other studies have indicated that leadership is also key to audit-sensitive matters in the CG space (such as senior managers’ conflicts of interest and other ethics-related issues), which require the CAE to have a “backbone” and not to be afraid to voice their opinion even in controversial situations (Soh, Martinov-Bennie, 2011). Taken together, it can be concluded that these studies show that CAEs with strong leadership skills are more successful in becoming a partner to the board, the audit committee, and senior managers, and help the IAF to become recognized as a valuable contributor to good governance practices and strategic management processes.

Although the literature recognizes CAE leadership skills’ importance to expand and enhance the IAF’s roles in organizations, to date, no studies have empirically investigated whether these skills influence the IAF’s activities in general and specifically concerning CG.

This study explores the potential relationship between CAE leadership skills and the IAF involvement in CG. We also analyze whether or not the existence of a leadership training program has a positive and significant relationship with the IAF’s involvement in CG.

Our results show that CAE strong leadership skills and leadership training programs are significantly and positively associated with the IAF’s involvement in CG. Furthermore, analysis of the control variables shows that the use of a risk-based audit plan, the existence of a QAIP, the type of activity performed (consulting vs. assurance), and the IAF size are significantly and positively related to the IAF involvement in CG.

The remainder of this article is structured as follows: in section “Hypotheses Development,” we develop the research hypotheses, whereas in section “Method” we then present the methodology we adopted, the main variables, and the manners in which we measured them. The “Findings” section examines the statistical analysis results, whereas section “Conclusions, Limitations, and Avenues for Future Research” provides a concluding discussion of the study results.

Hypotheses Development

CAE Leadership and IA Involvement in CG

Organizational studies indicate that there are different leadership skills that good leaders should learn and maintain (Northouse, 2015). One of these is collaborative leadership, which is the ability to get the appropriate people to work together in constructive ways to solve problems and make decisions (Chrislip & Larson, 1994). In the case of the IAF, this ability is important so as to involve people in generating and finding the adequate solutions to solve the problems identified during audit activities, to overcome resistance, and to increase the likelihood that recommendations are implemented (Chambers, 2008; Selim, Allegrini, D’Onza, Koutoupis, & Melville, 2014).

Organizational studies have also highlighted that leaders have the ability to build and maintain relationships with key stakeholders, which enhances of cooperation and resource exchanges (Bouty, 2000; Tsai & Ghoshal, 1998; Venkataramani, Green, & Schleicher, 2010).

The literature on IA acknowledges the importance of these leadership skills, arguing that leadership helps a CAE to build successful relationships with key organizational stakeholders. For instance, Rittenberg and Anderson (2006) argue that CAE leadership skills are key to move the IAF from a behind-the-scenes player to a key actor in improving CG practices, because it is essential to earn the respect of the board, the audit committee, and senior managers, to raise difficult issues with key stakeholders, and to strengthen the IAF’s independence and objectivity (Selim et al., 2014).

Another leadership skill indicated by organizational studies is transformational leadership—a leader’s ability to generate awareness and acceptance of the purposes and mission of the group they lead, with the aim to strengthen their team’s roles in the organization (Balkundi & Harrison, 2006; Bass, 1990). This skill is particularly important in the context of IA, because there are organizations in which the IAF’s primary stakeholders have incorrect perceptions of what the IAF does and on the contributions they can get from this function (Lenz & Sarens, 2012). It is likely that, in these organizations, the “old view” of internal auditors as a service to mid-level managers prevails; this undermines the IAF’s involvement in CG. Thus, to expand its involvement in strategic issues, Arena, Arnaboldi, and Azzone (2006 p. 289) point out that the CAE should have the ability to advocate the IAF’s value to promote the view that internal auditors can improve all organizational processes and activities, from the bottom to the top of the organization, including regarding CG.

The leadership literature has identified the ability to persuade others as a skill of an effective leader (Bass, 1985; Lee, Martin, Thomas, Guillaume, & Maio, 2015), one that is important to guide a group to accomplish shared goals.

The ability to persuade other organizational members is another expression of this leadership skill. In the context of IA, the ability to persuade and build consensus with other organizational members is a key element in the relationship with stakeholders. In the relationship with managers, as the IAF cannot impose its recommendations, this leadership skill increases the likelihood that internal auditors influence line managers and their willingness to implement suggestions, as well as help execute the audit plan (Lenz & Hahn, 2015).

Based on these studies, we identify four leadership skills of a successful CAE—the abilities to do the following: (a) collaborate with others, (b) build relationships, (c) advocate the IAF’s value, and (d) persuade and build consensus. As we know from organizational studies (Reeves, 2006) that successful leaders excel in multiple leadership skills, we assume that an effective CAE has all of these leadership skills, and develop the following hypothesis:

A Leadership Skills Training Program and IA’s Involvement in CG

Formal training programs are widely used to improve leadership in organizations and are designed to increase skills and behaviors relevant for team effectiveness (Dvir, Eden, Avolio, & Shamir, 2002; Kelloway, Barling, & Helleur, 2000; Yukl, 2010).

The literature on IA has widely emphasized the importance of training programs to improve the work quality of individual internal auditors and of the IAF. Studies have largely pointed out that training should help internal auditors to develop both technical and nontechnical skills (Abdolmohammadi, D’Onza, & Sarens, 2016). Another study argues that, as CG issues are complex and sensitive, internal auditors should have a mix of technical and nontechnical skills so as to be able to effectively deal with these topics (Chambers & McDonald, 2013).

Based on these considerations we assume that the existence of leadership skills training will increase the CAE leadership skills having a positive influence on the IAF involvement in CG. This leads to our second hypothesis:

Interaction Effects

H1 and H2 address the main effects of CAE leadership and leadership skills training program on IAF involvement in CG. A question that arises is whether there are interaction effects of these two variables on IAF involvement in CG.

To address this issue, we also test for the interaction effects of CAE Leadership × Leadership Skills training program on the dependent variable.

Method

Model Specification

We developed an ordinary least squares (OLS) regression model to analyze the link between CAE leadership and the IAF’s involvement in CG. We used SPSS and the following model to test our research hypothesis:

where:

IAFINVOLVEMENT_CG The factor score obtained via a principal component analysis (PCA) of the three IAF activities regarding CG.

CAE_Leadership The factor score obtained via a PCA analysis of the four leadership dimensions.

Training_LeadershipSkills Dummy variable with value 1 if there is a training program on leadership skills, and 0 otherwise.

CAE_LeadershipxTraining Interaction of CAE leadership and leadership skills training program.

CAE_Tenure Variable indicating the number of years of professional experience in the CAE position.

Risk_Based_Plan The IAF has adopted risk-based audit planning (Yes/No).

QAIP Dummy variable with a value of 1 if the IAF has a well-defined QAIP in place, and 0 if it is nonexistent or in development.

CAE_ReportingLine Dummy variable with value 1 if the primary functional reporting line for the CAE is the audit committee or board of directors, and 0 if it is the management.

AssuranceVsConsulting Variable that takes values: 1, if all IA resources are spent on assurance; 2, if almost all resources are spent on assurance and few resources are spent on consulting; 3, if resources are equally divided between assurance and consulting; 4, if almost all resources are spent on consulting, and few resources are spent on assurance; 5, if all resources are spent on consulting.

Budget_Sufficiency Dummy variable with value 1 if the CAE considers the funding for its IA department completely sufficient, and 0 otherwise (not at all sufficient or somewhat sufficient). Respondents were asked to indicate how sufficient is the funding for their IA department relative to the extent of its audit responsibilities.

IAF_Size Variable that takes these values: 1 = 1 to 9, 2 = 10 to 49, 3 = 50 to 999, and 4 = 1,000 or more. Respondents were asked to indicate how many full-time equivalent employees make up their IA department.

Firm_Size Logarithm of the total number of full-time-equivalent employees.

Listed_Firm 1 if the firm is listed, and 0 otherwise.

USvsNonUS Dummy variable with value 1 if the country is the United States, and 0 otherwise.

The dependent variable in the current study is the IAF’s involvement in CG (IAFINVOLVEMENT_CG). To measure this, we refer to the activities regarding CG included in 2015 Common Body of Knowledge (CBOK) study. The CBOK (2015) question used for this purpose was What is the extent of activity for your IA department related to governance reviews? Respondents were asked to use a 4-point scale (None, Minimal, Moderate, and Extensive) for each of the three activities proposed in the questionnaire. These are (a) Reviews of governance policies and procedures in general, (b) Ethics-related audits, (c) Reviews addressing linkage of strategy and performance.

Cronbach’s alpha coefficient of .632 between these variables indicates an acceptable level of the likelihood that the three IAF activities measure the same concept (i.e., the IAF’s involvement in CG). Also, we used PCA to reduce the three variables to one factor, because all IAF activities belong to the underlying concept of the IAF’s involvement in CG. The values of Kaiser–Meyer–Olkin (KMO) test (0.642) and the Bartlett’s test (<0.001) indicate that our data were suitable for factor analysis. The factor obtained via the PCA (eigenvalue = 1.73) explained 57.80% of the total variance. This measurement results in a continuous dependent variable in our OLS regression model.

We measured the CAE leadership variable using four leadership skills reported in the CBOK study. In particular, these are collaborate with others, build relationships, advocate the value of IAF activities, and persuade and build consensus. Respondents were asked to use a 5-point scale (Novice, Trained, Competent, Advanced, and Expert) to estimate their proficiency in each of these leadership skills.

Cronbach’s alpha coefficient of .886 between these variables indicates a good level of the likelihood that four CAE skills measure the same concept, CAE leadership. Also, we used PCA to reduce the four variables to one factor, because (as discussed in section “Hypotheses Development”), all these variables belong to the underlying concept, CAE leadership. The values of KMO test (0.825) and the Bartlett’s test (<0.001) indicate that our data are suitable for factor analysis. The factor obtained through the PCA (eigenvalue = 3.00) explains 75.10% of the total variance. This measurement results in a continuous explanatory variable in our OLS regression model.

We measured the second explanatory variable, Training_LeadershipSkills, as a dummy variable with the value of 1 if there was a leadership skills training program for internal auditors in the organization, and 0 otherwise. Interaction effects between the two explanatory variables are measured as the product between CAE leadership and leadership skills training program.

We also included several control variables in our regression model. First, we included the tenure of CAE (CAE_Tenure), measured as the number of years the CAE is in that position, as studies (Burnaby et al., 2007; Rittenberg & Anderson, 2006) indicate that CAE staying long in the position has more durable relationships with the key IAF stakeholders compared with a new CAE who should invest time to gain their trust and be involved in CG issues. Thus, we expected that longer CAE tenure is associated with a more IAF involvement in CG. Second, we included three variables regarding the IAF activity characteristics, which are the use of a risk-based audit plan (Risk_Based_Plan), the existence of a QAIP, and the IAF reporting line (IAF_ReportingLine). These are the same variables used by Sarens et al. (2012), who found these variables are positively and significantly related to the IA’s active role in CG. Another IAF characteristic that can influence the IAF involvement in CG is this function’s ability to provide both assurance and consulting services (AssuranceVsConsulting). Studies (Chapman, 2001; Melville, 2003; Selim, Woodward, & Allegrini, 2009) claim that the involvement in consulting activities contribute to elevate the IAF to a more strategic role in the organization as this give the possibility to become a business partner for the key IAF stakeholders helping them to achieve business objectives. Thus, we expected that the more IAF provides consulting activities, the more it will be involved in CG.

We also controlled for the budget size of the IAF (Budget_Sufficiency), based on the assumption that having sufficient budgets enables IAF to address the key stakeholders’ requests (Sarens et al., 2012). In addition, we included IAF size (IAF_Size) in our analysis, as previous studies (Arena & Azzone, 2009; D’Onza, Selim, Melville, & Allegrini, 2015) found a positive relationship between IAF size and IA staff activities relating to CG issues. A possible explanation of this result is that large IAFs have greater possibility to have specialized staff with technical skills in the auditing of governance processes.

Furthermore, we controlled for firm characteristics. Particularly, we controlled for firm size (Firm_Size), as studies (Carcello, Hermanson, & Raghunandan, 2005; Goodwin-Stewart & Kent, 2006) found it to be positively related to the extent to which firms invest in their IAF and to the IAF activities development level. Thus, we assumed that this increases the likelihood that the IAF is more involved in CG. We also controlled for organization type, that is, listed versus unlisted companies (Listed_Firm), as the literature has highlighted that this variable may influence the IAF’s involvement in CG (Sarens et al., 2012), because listed companies have precise requirements concerning internal controls and are more influenced by CG guidelines and laws (Allegrini & D’Onza, 2003). Thus, we assumed that, in listed firms, the IAF is more involved in CG processes.

Finally, as the sample of 804 CAEs represented six Anglosphere countries with varying sample size, and with 70% of the sample representing the United States, we included a dummy variable (USvsNonUS) for U.S./non U.S. countries to control for country fixed effects, as in previous studies (e.g., Abdolmohammadi, 2013).

Data Collection

For our analysis, we used 804 CAE responses to a select number of CBOK (2015) survey questions related to our study. We extrapolated the responses from the CBOK (2015) database, the largest global survey on IA.

We selected only CAE responses from Australia, Canada, New Zealand, South Africa, the United Kingdom/Ireland, and the United States. We limited our sample to CAEs of these six countries so as to mitigate the risk that differences in language and culture regimes could influence our study results. Researchers (Abdolmohammadi & Sarens, 2011; Abdolmohammadi & Tucker, 2002; Alzeban, 2015) have highlighted that IA practices have different extents of development in diverse cultural regimes. Thus, we restricted our analysis to countries with a similar cultural regime, collectively called Anglosphere countries (House, Hanges, Javidan, Dorfman, & Gupta, 2004) plus South Africa.

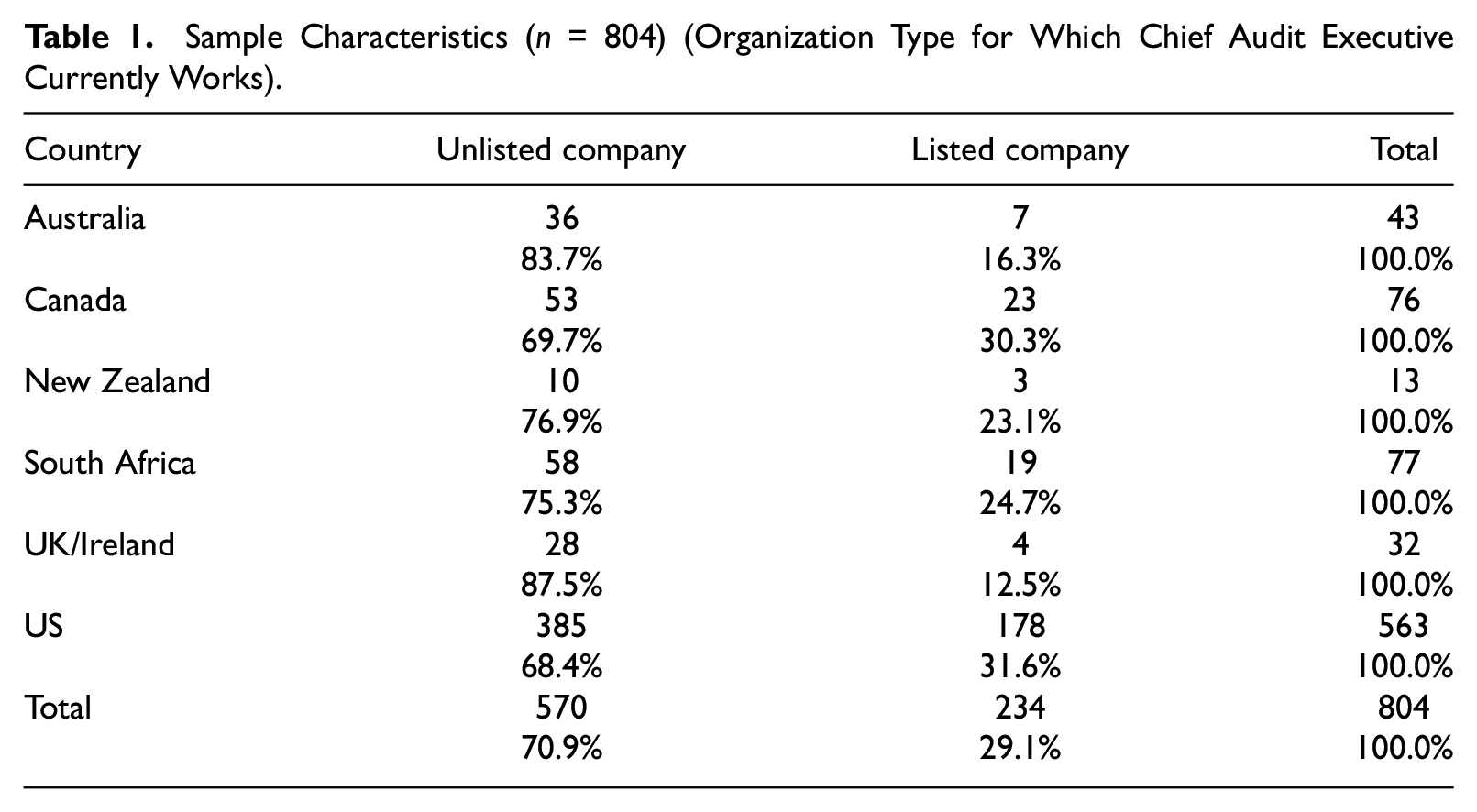

Table 1 presents information about the sample, with our Selected Countries × Organization Type (listed vs. unlisted firms). As shown in Table 1, the United States is the largest country in the study, with 563 CAE responses, followed by South Africa (n = 77) and Canada (n = 76), Australia (n = 43), the United Kingdom/Ireland (n = 32), and New Zealand (n = 13). Table 1 also shows that the largest group of organizations in the sample are unlisted companies (n = 570).

Sample Characteristics (n = 804) (Organization Type for Which Chief Audit Executive Currently Works).

The analyses we will now report are based on the total sample of 804 CAEs. However, the sample size varies between analyses, owing to missing data for the variables considered in our study.

Findings

Descriptive Statistics

Table 2 shows descriptive statistics for the IA activities regarding CG, comprising the dependent variable IAFINVOLVEMENT_CG. The results point out that the internal auditors’ involvement in CG issues differs per activity type. Although 64.6% of IAFs are moderately or extensively involved in the review of governance policies and procedures, this percentage decreases to 35% for ethics-related audits and to 40.5% for review addressing linkage of strategy and performance.

Descriptive Statistics for the Dependent Variable: Internal Audit Function Activities Related to Corporate Governance.

Note. IA = internal audit.

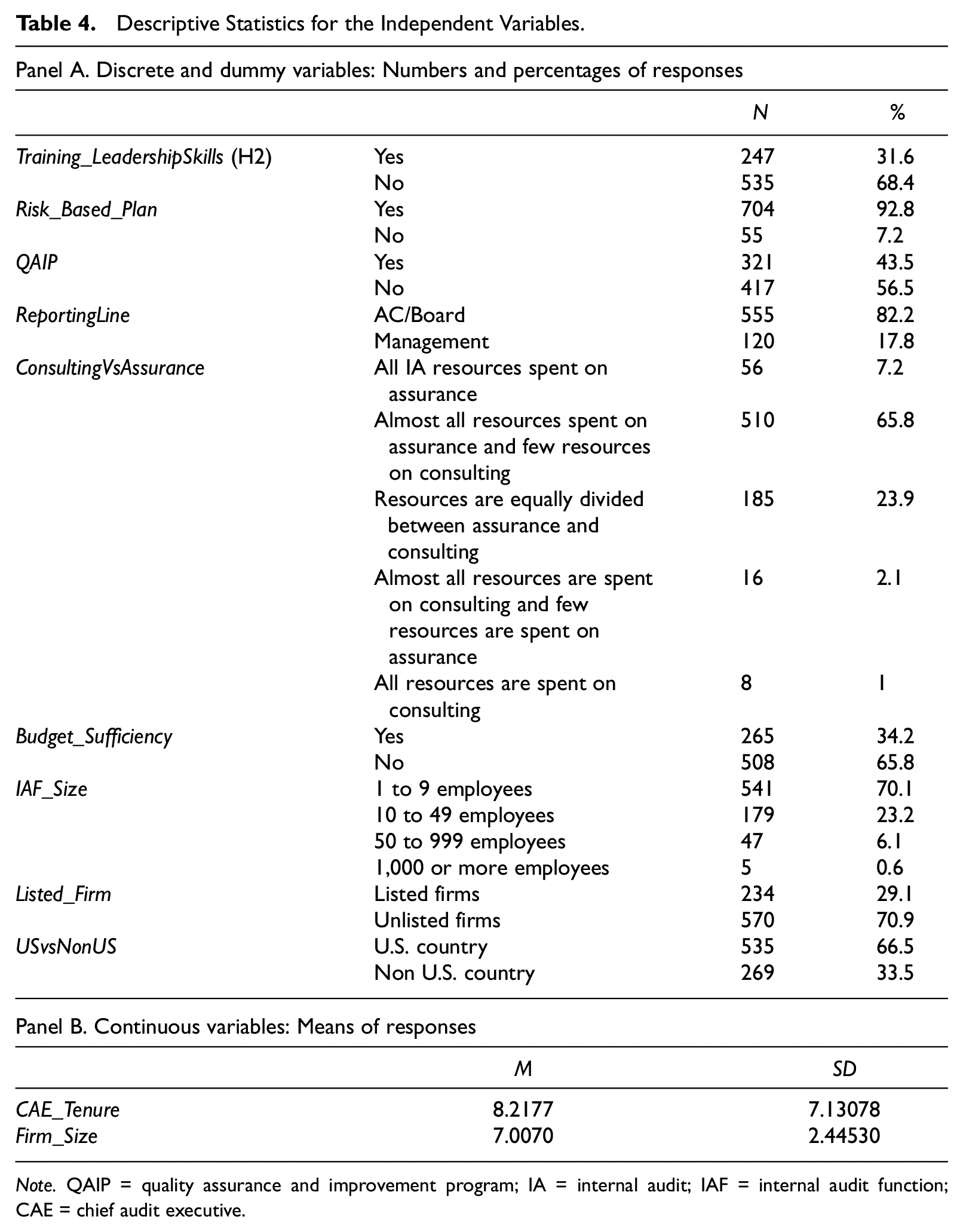

Table 3 reports descriptive statistics for the CAE skills in our first explanatory variable, CAE leadership, whereas Table 4 presents descriptive statistics for the independent variables (Panels A and B). Concerning Test Variable 2, Panel A shows that 31.6% of CAEs indicate that leadership skills form part of their firms’ training programs.

Descriptive Statistics for the Explanatory Variable CAE Leadership.

Note. CAE = chief audit executive.

Descriptive Statistics for the Independent Variables.

Note. QAIP = quality assurance and improvement program; IA = internal audit; IAF = internal audit function; CAE = chief audit executive.

Regarding the control variables, Panel A shows that 92.8% of the IAF has risk-based audit planning, and 43.5% has a QAIP currently in place. Almost 82% of CAEs indicate the board or audit committee as their primary functional reporting line, and 73% indicate that the IAF resources are spent exclusively or almost on assurance activities. Furthermore, 34.2% of CAEs consider completely sufficient the funding they receive to perform IAF activities, and almost 70% of CAEs manage an IAF with fewer than nine employees. Regarding firm characteristics, 29.1% of the firms are listed.

Finally, Panel B shows that the CAEs have on average been in the CAE position for 8 years.

Table 5 presents bivariate Pearson correlation coefficients between the dependent variable, IAFINVOLVEMENT_CG, and the independent variables, where significant correlations are identified at .05 and .01 significance levels. As highlighted in Table 5, there are a number of significant correlations, but no correlation coefficients reach the critical level of .50 to cause concern for multicollinearity. Furthermore, in the last column, we report the variance inflation factor (VIF) to further check for potential multicollinearity. The VIF values confirm that multicollinearity is not a concern.

Pearson Correlation Matrix.

Note. CAE = Chief Audit Executive; QAIP = quality assurance and improvement program; IAF = internal audit function; VIF = variance inflation factor.

Significance at the .05 level. **Significance at the .01 level.

Regression Analysis

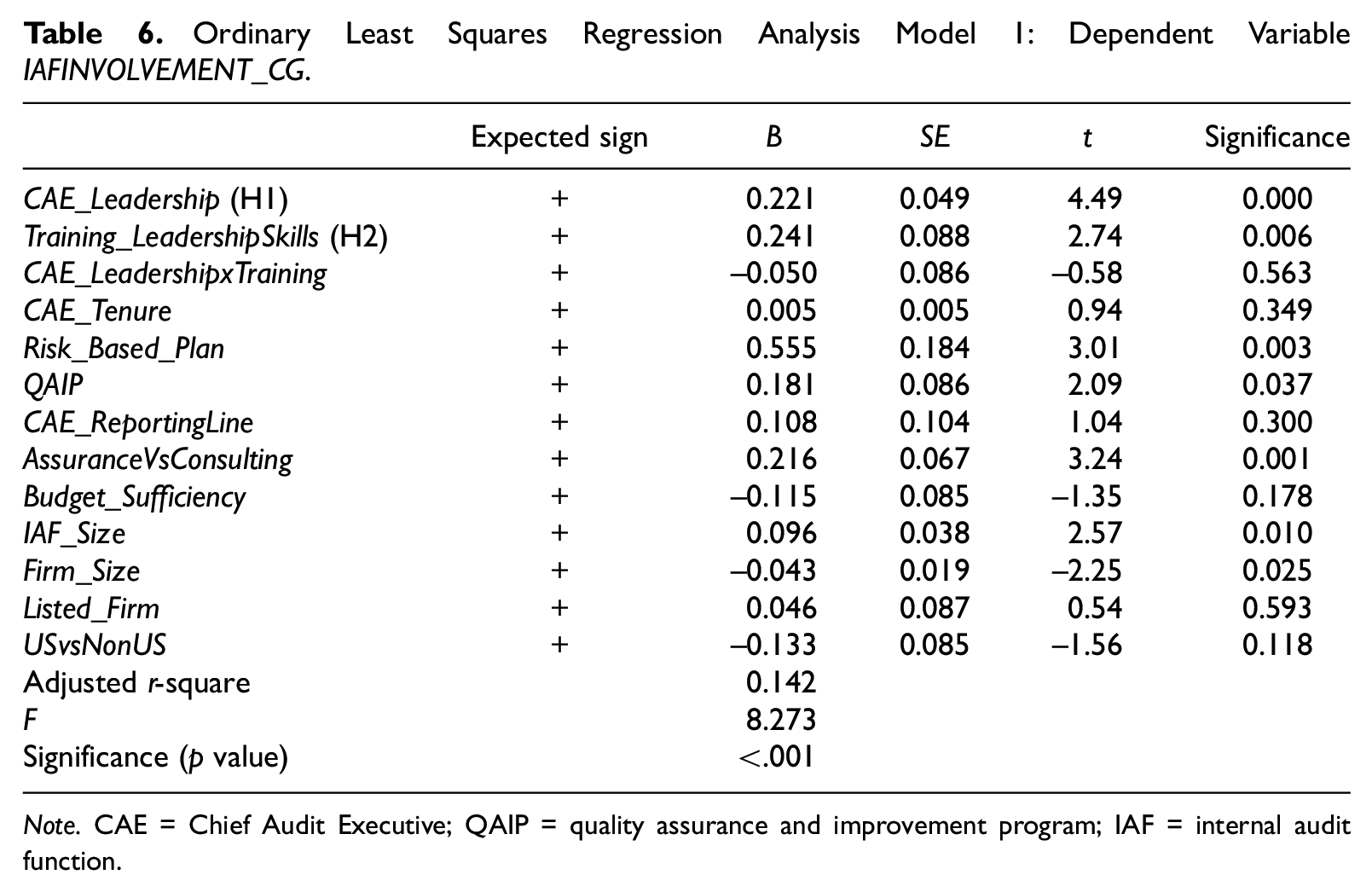

Table 6 shows Model 1’s regression analysis results, including all explanatory and control variables. We report the coefficient (β) of each independent variable as well as its related significance. The last three rows provide the adjusted R2, the F statistics, and its p value. The results show that the estimated model is highly significant (p < .001), with an adjusted R2 of 14.2%.

Ordinary Least Squares Regression Analysis Model 1: Dependent Variable IAFINVOLVEMENT_CG.

Note. CAE = Chief Audit Executive; QAIP = quality assurance and improvement program; IAF = internal audit function.

This model shows significant results for our two hypotheses (H1, H2). Particularly, H1 is supported, indicating that CAE_Leadership is significantly and positively related (p = .000) to IAFINVOLVEMENT_CG. This finding suggests that when the CAE has strong leadership, this increases the IAF’s involvement in CG processes, because the CAE has the ability to foster collaborations and build strong relationships, promote the value the IAF adds to governance processes, and can also persuade and build consensus with key stakeholders. All these factors enable the IAF to be recognized as a partner in CG by the board, the audit committee, and senior management, which ask for assurance and consulting service on governance processes. This result is consistent with earlier studies (Arena et al., 2006; Dittenhofer et al., 2010; Ramamoorti & Siegfried, 2016; Rittenberg & Anderson, 2006; Selim et al., 2014), which maintain that CAEs leadership is crucial to elevate the IAF’s role in an organization.

Table 6 also shows a significant and positive relationship (p = .006) between the presence of a leadership skills training program (Training_LeadershipSkills) in the company and the IAF’s involvement in CG, which is consistent with H2. This finding suggests that training programs allow CAEs and IAF staff to develop leadership skills, fostering their ability to build positive relationships with key organizational persons, who require them to be part of governance issues. This result supports the argument that, to expand the IAF’s role in CG, IAF training programs should include diverse activities to develop technical and nontechnical skills (Abdolmohammadi et al., 2016). Furthermore, Table 6 shows that the interaction between CAE leadership and the leadership skills training program is not significant.

Regarding control variables, our results partially confirm the findings of a study by Sarens et al. (2012) on factors associated with the IAF’s having a role in CG. Specifically, we found that the use of a risk-based audit plan (Risk_Based_Plan) and the presence of a QAIP in the organizations are significantly and positively related (p = .003 and p = .037) with the IAF’s involvement in CG.

The IAF involvement in CG is also positively associated (p = .001) with the assurance versus consulting activities (AssuranceVsConsulting), thus suggesting that the more IAF focus on consulting activities the more it plays an active role in CG. This result is consistent with previous studies findings (Chapman, 2001; Melville, 2003). Also, IAF_Size is significantly and positively associated (p = .010) with our dependent variable. This finding confirms prior studies results (Arena & Azzone, 2009; D’Onza et al., 2015) that indicate a positive relationship between IAF size and the activities by IA staff relating to CG issues. Finally, the results show a significant, but negative association between firm size and the IAF involvement in CG. Although this result is against our expectations, it is consistent with a study by Sarens et al. (2012) who found firm size inversely associated with the IAF having an active role in CG.

Concerning other control variables—CAE tenure, CAE reporting line, budget sufficiency, listed vs. non listed firm, and the U.S. country variable—there are no significant relationships with the dependent variable.

Additional Analysis

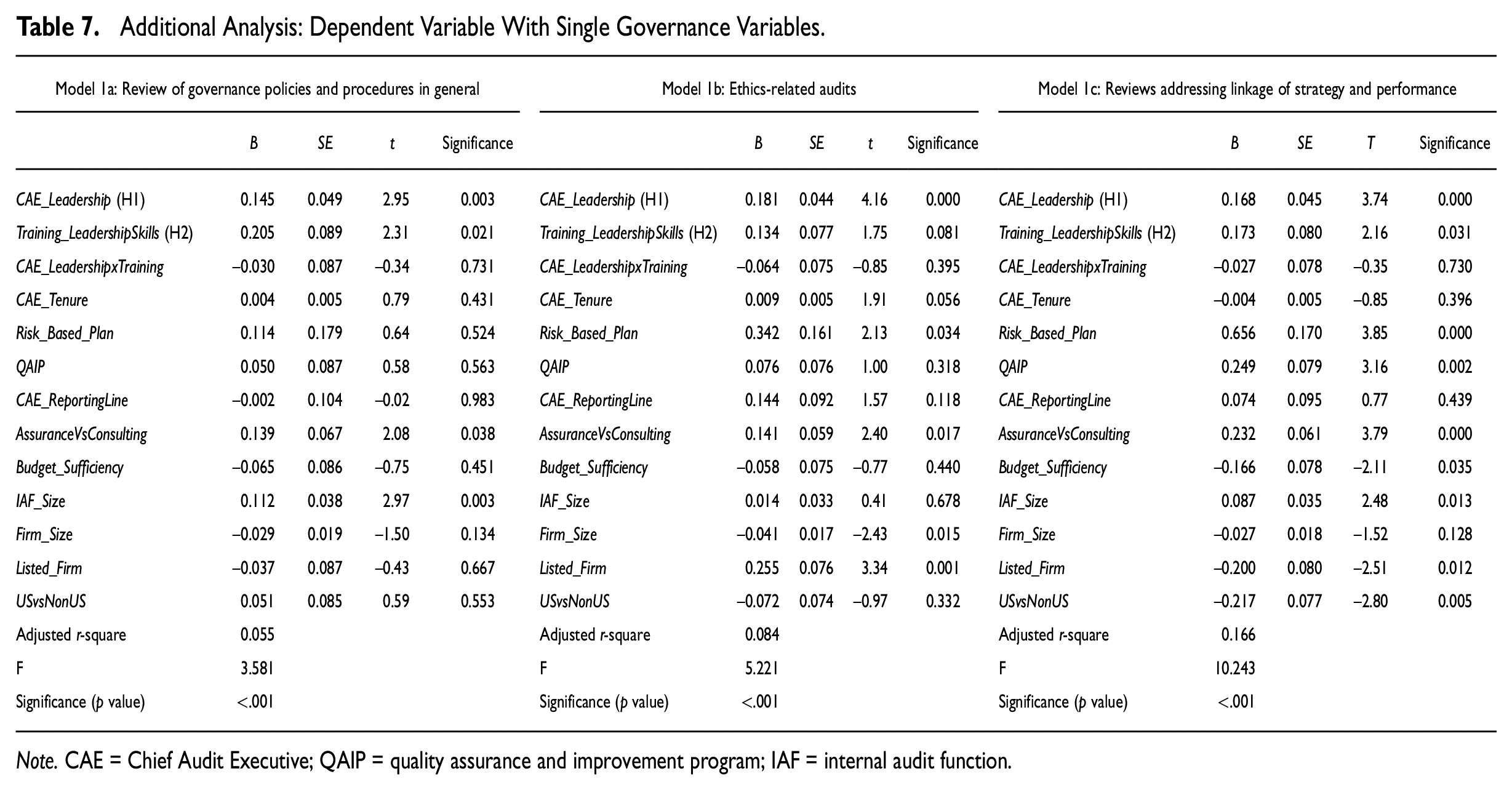

To test the robustness of the results in Table 6, we also performed several additional regression estimations. In particular, we reran the main model (Model 1) by changing the dependent variable IAFINVOLVEMENT_CG with the single CG activities, that is, (a) review of governance policies and procedures in general, (b) ethics-related audits, (c) Reviews addressing the linkage of strategy and performance, thus developing three different models (These dependent variables took a value between 1 and 4—None and Extensive).

Table 7 reports these analysis results which show that all models are significant. As reported in Table 7, the R2 of these models range from 5.5% for Model 1a (Review of governance policies and procedures in general) to 16.6% for Model 1c (Review addressing linkage of strategy and performance). The new regression models show that CAE leadership is significantly and positively related to the three CG activities. Moreover, the presence of a leadership skills training program (Training_LeadershipSkills) is positively and significantly, or marginally significant, associated with the dependent variables in all the three models. Concerning control variables, AssuranceVsConsulting is significant for the three regression models, whereas risk-based audit planning is significant in Models 1b and 1c and QAIP is significant in Model 1c.

Additional Analysis: Dependent Variable With Single Governance Variables.

Note. CAE = Chief Audit Executive; QAIP = quality assurance and improvement program; IAF = internal audit function.

Conclusions, Limitations, and Avenues for Future Research

In investigating the potential relationship between CAE leadership and the IAF’s involvement in CG, we found support for all our hypotheses. In particular, we found that CAEs with strong leadership skills—in terms of CAEs’ ability to collaborate with others, build relationships, advocate the IAF’s value, and persuade and build consensus—are significantly and positively related to the IAF’s involvement in CG. We also found support for H2: The presence of a leadership skills training program in the company allows a CAE (and internal auditors) to develop leadership skills, which improves the recognition of their roles and thus the likelihood of the IAF’s involvement in governance issues.

Our study findings indicate that enhancing the IAF involvement in CG increases when CAEs demonstrate strong abilities to collaborate constructively with the IAF’s stakeholders, relationship-building acumen, advocating the IAF’s value, and persuading and building consensus. These leadership skills are crucial for a CAE to foster the relationships and collaborations with the board, the audit committee, and senior managers, so as to gain their respect, trust, and support, to assume an active role in CG processes. This study results confirm the argument of earlier studies (Abdolmohammadi, Ramamoorti, & Sarens, 2013; Coetzee & Lubbe, 2013; Dittenhofer et al., 2010) that leadership skills are important to move the IAF from a behind-the-scenes player to a key actor in the improvement of CG practices and to increase the IAF’s organizational roles and relevance. Furthermore, the results of the control variable indicate that the extent of IAF involvement in CG is influenced by IAF characteristics (risk-based audit planning, the existence of a QAIP, assurance vs. consulting activity, and IAF size) providing support to previous study findings (Sarens et al., 2012).

The study results have both theoretical and practical implications. First, we contribute to the literature on the IAF’s role in CG. In particular, by analyzing the CAE leadership skills, we extended the knowledge of the potential factors that influence the IAF’s role in CG, answer calls for more research into on the specific internal auditor skills that can affect the IAF’s role in organizations (Arena & Azzone, 2009) and on the IAF’s role in CG (D’Silva & Ridley, 2007; Lenz & Hahn, 2015; Mihret & Grant, 2017). Thus, our study adds to the literature on the attributes of individuals who perform IA activities (Sarens, 2009; Venkataraman, 2016), pointing out the importance of leadership skills for the CAE to be successful. Second, our results confirm that CAE leadership is important to make the IAF a CG gatekeeper working closer with the board and audit committee to improve internal control mechanisms reducing the risk of manager’s opportunistic behavior consistent with agency theory perspective. In addition, CAE leadership favors the demand of IAF active role in strategic management focusing the directors and managers attention to the resources and competencies which are vital for the long-term success of organization in line with the resource theory assumptions.

Third, it extends previous studies on leadership skills that focused exclusively on executives (i.e., the CEO and senior managers) to a control function to analyze whether the IAF’s specific roles and activities influence the leadership skills that make a CAE more successful. We found that specific leadership skills increase the support the IAF receives from its key stakeholders, which is vital to foster the IAF’s organizational relevance. This initial evidence on the relevance of CAE leadership skills provides a platform for future research to leverage and build on.

This study also has practical implications for professional bodies and practitioners. These findings, which indicate the importance of CAE leadership skills and of leadership training programs, provide useful input for the IIA and other professional bodies in developing their certifications and professional education offerings. Particularly, the IIA has recently launched QIAL certification for IAF leaders, and our results indicate that it should invest in promoting this certification, as CAE leadership skills enhance the IAF’s roles in CG. The study findings also enable practitioners to benchmark their activities against the reported results and have implications for CAEs who wish to increase their IAF’s involvement in CG; practitioners may benefit from our research, because we provide evidence on variables that relate significantly to the IAF’s involvement in CG. For instance, CAEs who wish to increase the IAF’s involvement in CG should invest so as to improve their leadership skills and should develop other IAF characteristics that we found to be positively related to the IAF’s increased involvement in CG processes. Companies may also benefit from our study results, identifying which leadership skills are important for CAEs and use this study’s output when hiring a CAE, promoting someone to a CAE position, and evaluating CAEs.

This study has limitations. First, in determining the IAF’s involvement in CG and CAE leadership, we based our research only on data from CBOK; thus, we may have missed other IAF activities regarding CG or other CAE leadership skills, which may be worthy of discovery and investigation in future research. Second, we based our measurement of leadership skills of CAEs and of other variables on the perceptions of the 2015 CBOK survey participants. As in similar studies, the respondents’ perceptions may deviate from realities in practice, or may be influenced by “overly optimistic self-assessments by internal auditors” (Lenz & Sarens, 2012, p. 537). Third, as the CBOK survey participants were all internal auditors, the measures therefore only reflect the perspectives of those providing IA services. Thus, researchers should take the perspective of those who ask for IAF services; this could help to enlarge the knowledge of which leadership skills are perceived as more important to enhancing the IAF’s organizational role. Fourth, our analysis only considered Anglosphere countries, so as to avoid the risks of differences between cultural and legal regimes, which could have influenced our results. Thus, we recommend future studies in other countries or geographical regions, to analyze leadership’s influences on the extent of the IAF’s involvement in CG.

Footnotes

Acknowledgements

The authors gratefully acknowledge the Institute of Internal Auditors Research Foundation (IIARF) for its permission to use the Common Body of Knowledge in Internal Auditing (CBOK, 2015) database in this study. They gratefully acknowledge many useful and constructive comments received from three anonymous reviewers, the Associate Editor (Prof. Carolyn Levine), the Editor (Prof. Bharat Sarath) and participants to the 15th European Academic Conference on Internal Audit and Corporate Governance.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.