Abstract

We investigate the reasons for the growing demand for Islamic banking internationally, and examine the relative economic performance of Islamic banks compared with conventional banks in managing their capital buffers and liquidity. Using data for the period 2000–2012 for 104 Islamic and 619 conventional listed and non-listed banks spread across 22 countries with both these types of banks, and using standard statistical methodology for archival data analysis, we find that religious, political, and socio-legal factors, rather than economics alone, play key roles for Islamic banks in attracting depositors. Governed by Islamic (Shariah) laws, these banks cannot lend money and charge interest. Depositors are not debt holders as in conventional banks, but investment partners that share in the risk, or profit-loss sharing (PLS), with the bank. As Islamic banks have no debt holders, and depositors self-select to bank with Islamic banks, economic theory suggests a reduced need for excessive (less productive) liquidity buffers. However, we find that Islamic banks maintain significantly higher liquidity buffers than their conventional counterparts. A main contribution of our study is to highlight the fact that standard economic measures alone may be inadequate to assess the performance of Islamic banks.

Introduction

The objective of our study is to identify factors that explain the current levels and growth in and beyond the Islamic countries of Islamic banking, that is, banks that follow Shariah laws and offer Shariah-compliant banking products (Shanmugam et al., 2004), 1 and to examine the economic performance of these banks relative to conventional banks. 2 Specifically, we investigate if it is the economic performance or some other factors that explain the increasing growth in deposits and spread of Islamic banks. Prasad (2015) observes that Islamic banks have grown from niche players to genuine competitors of conventional banks. While not extensive, there is some prior literature on the relative economic performance of Islamic banks vis-à-vis conventional banks, with mixed findings. However, to the best of our knowledge, there is almost no research on the impact of socio-economic factors on Islamic banks’ growth. This is particularly surprising given the importance of Islamic banking today.

There is a belief shared by many that Islamic banking practices promote economic growth, welfare, and stability, and are resilient to macroeconomic shocks. Gheeraert (2014) and Abedifar et al. (2016) argue that Islamic banks complement conventional banks, and generally increase overall social welfare. The fact that Islamic banks emerged relatively unscathed from the financial crisis of 2008 promoted these beliefs further (see, for example, Hasan & Dridi, 2011). While there is agreement that Islamic banks have more than adequate capital buffers, prior results on the liquidity and relative profitability of these banks compared with conventional banks, measured conventionally by return on assets (ROA) or equity (ROE), are mixed (Beck et al., 2013; Hassan & Bashir, 2003; Rashwan, 2010; Samad, 2004). Even for the related issue of the operational efficiency of Islamic banks compared with their conventional counterparts, the findings are mixed (Abdul-Majid et al., 2010; Bader et al., 2008; Johnes et al., 2014). These mixed results on the economic performance of Islamic banks intuitively suggest that factors beyond economic rewards motivate their depositors “to leave money on the table” to perhaps satisfy other needs. Our article confirms this intuition and identifies these non-economic factors that drive Islamic banking.

Most devout Muslim depositors keep their money in risk sharing, or Mudaraba, accounts. Instead of being paid a fixed interest rate (prohibited by Islamic law), depositors receive a slice of a bank’s profits and its losses (Wigglesworth, 2009). 3 In addition, Dusuki (2007) notes that the depositors of Islamic banks believe that profit–loss sharing principles are the only principles that represent the true spirit of the Islamic banking system. An analysis of 52 Islamic banks across multiple countries, where Islamic banking is thriving, shows that this industry has grown substantially over the period of 2006–2011, with the average risk sharing deposit growth reached 40% of total assets (Islamic Financial Services Board, 2014). Consequently, we use the proportion of Shariah-compliant deposits scaled by total assets as a measure for the intensity of Islamic banking and its change as a measure of growth of Islamic banking. 4

Drawing on a sample of Islamic and conventional banks across 22 countries that have both Islamic and conventional banks, for the period from 2000 to 2012, we find that Islamic banks are popular (have a higher intensity of Shariah-compliant banking deposits) and growing in countries that have a high concentration of Muslim population, ruled by a religious-minded political party or with a major presence of these parties in legislative bodies, and strong regulatory support systems in place. We note that being a predominantly Muslim country is not sufficient for Islamic banking to flourish. 5

Regarding economic performance, the only common findings in the prior literature are that Islamic banks (a) were relatively unscathed by the most recent financial crisis of 2008 (Hasan & Dridi, 2011) and (b) have larger capital buffers compared with their conventional counterparts (Beck et al., 2013). Contrary to prior work that views these findings as evidence of superior banking practices, we argue that both these findings could actually imply the opposite. The first finding that Islamic banks have emerged unscathed from the financial crisis of 2008 could simply be because they did not take necessary risks normal to the business of banking, or because they were allowed unfair business advantages like subsidies or access to fund high-quality and high-return projects by their governments (trying to propagate their own political agendas), while denying conventional banks these opportunities. 6

On the second finding, we argue that keeping large capital buffers is not optimal for Islamic banks. It is money that could have been better spent. Under Islamic banking or Shariah-compliant finance, depositors are not debt holders but partners that share in the risks or profits and losses (PLS) in the banks’ short- and long-term investments. 7 Islamic finance relies on the notion of equitable sharing in which no one can claim any compensation without incurring some risk, and precludes the idea of guaranteed returns or insurance (Archer & Karim, 2009). As these are like partnership contracts between the Islamic bank and the depositors, economic theory suggests that it is inefficient to have large, relatively less productive liquid buffers. Depositors rationally put their money in Islamic banks presuming the bank has better opportunities for investment than they have at a personal level, and with the complete understanding they are entering a risk sharing agreement. As these depositors are partners in investments, and not bond holders as in conventional banks, they do not expect the bank to keep their deposits in less-than-productive capital buffers, cash, or liquid assets. In addition, they are predisposed to the Islamic ways of banking, and economic performance of these banks is one but probably not the most important consideration. The depositors of Islamic banks have an inherent interest to see this mode of banking succeed and spread, and it is unlikely that they would jeopardize these banks by withdrawing their funds at the first sign of trouble (Abedifar et al., 2013). This then reduces further the need for large capital reserves or buffers.

Contrary to traditional economic practices in conventional banks, we find that Islamic banks generally hold more capital reserves and have more liquidity, for a given level of asset risk. The findings also hold when we compare Islamic banks with conventional banks after excluding hybrid banks which are conventional banks that also offer Shariah-compliant products, and when we compare Islamic banks with a matched sample of conventional banks based on bank size and a country of residence. This supports our conjecture that the depositors in Islamic banks are willing to “leave money on the table” for utility derived from non-monetary needs. 8

The main contributions of our article are to highlight the fact that banks are social organizations and that their operations are inseparable from the aspirations, cultural norms, practices, and socio-political climates in which they operate. While the overall economic performance of Islamic banks may be lagging behind conventional ones (where performance is measured using traditional economic indicators), their growth can only be attributed to the fact that they serve specific needs of certain sectors of society. Therefore, it would be inappropriate to use just the standard economic metrics of performance to evaluate them or explain their growth and success. We believe our work is the first in examining Islamic banking in this comprehensive way.

The section “A Short Introduction to Islamic Banking and Literature Review” presents a short introduction to Islamic banking and a literature review of relevant prior work. The “Hypotheses” section presents our hypotheses and the section “Data and Research Design” presents our sample selection and research design. Our empirical results are reported in section “Results” and robustness tests and concluding remarks follow in sections “Robustness Tests” and “Conclusion,” respectively.

A Short Introduction to Islamic Banking and Literature Review

Currently, Islamic banks operate mostly in countries in the Middle East and Southeast Asia, and have established themselves as strong competitors for conventional banks. 9 As noted earlier, they have been expanding rapidly over the last two decades to other Islamic countries and beyond.

The Shariah Law, Risk Sharing, and Intermediation Role of Islamic Banking

Islamic banking refers to banking activities that are consistent with the principles of Shariah, or Islamic code of law. Under Shariah law, Islamic banks are prohibited from charging interest (riba), indulging in speculative activities (Gharar), and financing “illicit” sectors such as weapons, drugs, alcohol, and pork. Shariah-compliant finance relies on profit sharing and loss bearing principles, and posits that all transactions have to be backed by a real economic transaction that involves tangible assets. Consequently, Islamic banks distinguish themselves from conventional ones by offering only short- and long-term profit-loss sharing (PLS), risk sharing, or Mudaraba contract products to their depositors.

The bulk of deposits comes from Mudaraba contracts, in which depositors’ funds are pooled into a common fund, and the bank, without any restrictions from depositors, decides where and when to invest these funds. The ex ante rate of return on investment (interest rate premium) in conventional banks is replaced by an uncertain ex post rate of return that is linked to the bank’s overall profit level, or, to a specific investment account on the asset side of the bank’s balance sheet. Moreover, such deposits are not guaranteed in capital value, do not yield any fixed or guaranteed rate of return, and depositors may lose part or all of their investment deposits if the bank has losses. Therefore, the payoffs to depositors resemble dividends paid to equity holders in conventional banks. 10

Literature Review

While there has been much written on Islamic banking across a wide spectrum of academic literature and in the popular press, we review only academic research that is of direct relevance to our work.

As mentioned earlier, prior literature addressing the issue of why Islamic banks have become popular and why they are growing in popularity is quite sparse. However, there is prior literature highlighting the welfare benefits of Islamic banking that has helped us to identify factors that may explain the current popularity and growth of Islamic banks. We discuss these works next.

Gheeraert (2014) provides persuasive empirical evidence, using the IFIRST database and standard archival statistical methodology, to show that the introduction of Islamic banking in countries of Muslim faith spurred the overall development of the banking sector as measured by the amount of private credit or bank deposits scaled to gross domestic product (GDP). 11 He explains that this is because Islamic banks opened up new markets by catering to a large population of religious Muslims whose demands for banking services had largely been ignored by conventional banks. In related work, Abedifar et al. (2016) use a sample of 22 Muslim countries, with dual-banking systems (conventional and Islamic banks) for the period from 1999 to 2011, to show that the presence of Islamic banks, measured by their market share, can foster access to banking and finance across a wide swath of the population. They conclude that the Islamic banks improved economic welfare particularly in low-income or predominantly Muslim countries, and countries with a comparatively higher uncertainty avoidance index. 12

Dusuki (2007) argues that the depositors of Islamic banks believe that profit–loss sharing principles are the only principles that represent the true spirit of the Islamic banking system. By way of a survey conducted on a sample of respondents representing seven different stakeholder groups involved with Islamic banks in Malaysia, namely, customers, depositors, managers, employees, regulators, Shariah advisors, and local communities, his analysis shows that the stakeholders, including depositors, heavily support the true principles of profit–loss sharing concepts that differentiate Islamic banks from conventional counterparts.

Adherence to Shariah principles precluded (fortunately, as it turns out in hindsight), Islamic banks from financing or investing in the kind of instruments that had adversely affected their conventional competitors and triggered the global financial crisis. Hasan and Dridi (2011) empirically examine the performance of Islamic and conventional banks during the recent global crisis, covering the years from 2007 to 2010, by examining the impact of the financial crisis on profitability, credit and asset growth, and external ratings in eight countries where these two types of banks have significant market share. Their analysis suggests that factors related to the business model, in particular, Shariah compliance, of Islamic banks help limit the adverse impact on their profitability, asset growth, and external rating compared with conventional counterparts.

Next, we turn to the prior literature on the relative performance of Islamic banks compared with conventional banks. This is the second issue examined in this article. Earlier work has tried to use different metrics to measure relative performance, but the results have been mixed. The metrics used in the literature to measure performance include liquidity, profitability, and efficiency. In addition, the methodology used range from traditional financial ratios which are based on certain financial indicators, to more advanced techniques such as data envelopment analysis (DEA) and stochastic frontier analysis (SFA).

In an empirical study, Hassan and Bashir (2003) use cross-country bank-level data from 21 countries with dual-banking system for the period from 1994 to 2001, and find that Islamic banks are less liquid as measured by net loan over customer and short-term funding, and liquid assets over customer’s short-term funding, than conventional banks. However, using the ratio of liquid assets to deposit and short-term funding on a sample of Islamic and conventional banks drawn from 22 countries for the period 1995 to 2009, Beck et al. (2013) find the opposite to be true. Samad (2004) examines the comparative performance of Bahrain’s Islamic and conventional banks for the period from 1991 to 2001 applying difference in mean (t value) of ROA and ROE, and finds no significant differences between Islamic banks and conventional counterparts. However, Beck et al. (2013) also document that Islamic banks are relatively less effective in controlling their costs. They also find that Islamic banks have a relatively higher intermediation ratio, have higher asset quality, and are better capitalized. Rashwan (2010), using the multivariate analysis of variance (MANOVA) approach for each of the four performance indicators—return on average assets (ROAA), return on average equity (ROAE), net loan to total assets (NL/TA), and loan loss reserve to gross loan (LLR/TL)—for a sample of 46 listed Islamic banks and 49 listed traditional banks across 15 countries for the years 2007 to 2009, finds that Islamic banks were more profitable than conventional banks before the recent financial crisis of 2008, but the opposite post-crisis.

Even for the related issue of the operational efficiency of Islamic banks compared with their conventional counterparts, the findings are mixed. Bader et al. (2008), on one hand, use the DEA technique on a sample of 43 Islamic and 37 conventional banks in 21 countries for the period from 1990 to 2005 and find that Islamic banks are just as efficient. On the contrary, Abdul-Majid et al. (2010) use an output distance function approach on a sample of Islamic and conventional banks in 10 countries spanning the period 1996 to 2002 and find that Islamic banks are less efficient than conventional counterparts. Johnes et al. (2014) decompose the overall efficiency measure into two components: one which reflects managerial efficiency and another which measures the impact of the operational context of the bank. Their analysis shows that operational efficiency is lower in Islamic banks than conventional banks whereas managerial efficiency is higher.

These mixed results on the economic performance of Islamic banks suggest that factors beyond economic rewards motivate their depositors. We propose different metrics from those used in prior work to examine the performance of Islamic banks vis-à-vis conventional banks. Specifically, we measure performance of Islamic banks by the levels of capital buffer and liquidity they hold relative to the bank’s portfolio asset risk.

Hypotheses

The Intensity of Shariah-Compliant Deposits in Islamic Banks and Factors That Influence Their Depositors

As mentioned earlier, our metric of current popularity is the intensity of Shariah-compliant deposits, defined as the ratio of the (natural logarithm) of profit–loss sharing (PLS) deposits to total assets, while the change in this metric represents the growth of Islamic banking. 13 Based on prior findings (see Haron & Shanmugam, 1995), we expect Islamic or Shariah law to prominently influence the behavior of devout Muslims, including their decisions on banking. We note again that it is possible that even in a country with a lower Muslim population, say the United Kingdom, it is still possible that an Islamic bank could have higher intensity and growth of Shariah-compliant deposits to attract devout Muslim customers. Conversely, in a country like Indonesia, which is tolerant and allows conventional banks to operate freely, but with high proportion of Muslims in the population, Islamic banks could potentially have lower intensity (and growth) of Shariah compliant of PLS deposits to compete with the conventional banks. By contrast, Islamic banking is growing in the United Kingdom which is not a predominantly Muslim country.

Closely related to the issue of religion is always politics. Specifically, there is evidence that the growth of the religious Muslim Brotherhood movement in Egypt has influenced political, social, economic, and financial institutions throughout the Muslim world (Al-Awadi, 2014). Pushing their Islamic cause, the Muslim Brotherhood also founded the Islamic International Bank of Investment and Development in Egypt in 1980. Note that it is possible that Islamic banks in certain countries like Saudi Arabia which impose strict Islamic laws, but where the Muslim Brotherhood was not active, could have a higher intensity and growth of Shariah-compliant PLS contracts on the deposit side. In other words, the Muslim Brotherhood is not necessarily the cause for the spread of Islamic banks. This leads to our next hypothesis.

Next, we hypothesize that when governments (e.g., the governments of Malaysia and Bahrain) institute separate law to supervise and regulate Islamic banks, it will encourage more of the devout people to bank with them. Such comprehensive law assures depositors that their funds will be invested in accordance with Shariah law. Therefore, we expect that the intensity (and growth) of PLS deposits will be higher in a country with separate laws governing Islamic banks.

Capital Buffer and Liquidity of Islamic Banks

Capital adequacy requirements are meant to serve two objectives; first, protecting depositors from any losses, and second, protecting the banking system from collapsing from a contagion effect (Grais & Kulathunga, 2007). The latter reason is not particularly compelling for Islamic banks, as these banks are typically small, and it is unlikely that the failure of an Islamic bank will lead to a global (or even regional) banking system failure. As for the former reason, Islamic banks rely mostly on an equity-based capital structure, dominated by equity and investment deposits that are based on PLS schemes, precluding the need for the large capital ratio required of conventional banks. 14 As we have argued, if depositors in Islamic banks are jointly religious and rational, it follows that they are prepared for the risk of losses. Rationality also implies that these depositors of Islamic banks are channeling their money through the bank because they believe that the bank has better investment opportunities than what they have at an individual level. Therefore, it is unlikely that they will invest through an Islamic bank that holds their deposits in capital reserves or liquid assets that yield minimal returns. Therefore, our maintained assumption is that depositors are looking for productive use of their deposits within the tenets of their religion. Furthermore, Islamic banks do not subscribe, at least in theory, to a deposit guarantee scheme, as that will have Shariah implications. Therefore, the depositors are simply partners in risky investments with no guarantees of insurance. This again implies that Islamic banks need not carry a large capital reserve. 15

Based on this line of reasoning, we hypothesize that Islamic banks, for a given level of asset (investments) risk, would maintain lower capital buffer and liquidity than conventional counterparts.

Data and Research Design

Sample Selection

We use Bankscope, a global database with data on both listed and non-listed banks, to obtain bank financial information and identify banks’ type. Following Beck et al. (2013), we only include countries that have at least two observations for both Islamic and conventional banks for each year in the sample. We eliminate outliers in all variables by winsorizing at the first and 99th percentiles within each country. We also confirm the categorization of Islamic banks in Bankscope with information from Islamic Banking Associations and country-specific sources.

We restrict the sample to only countries with both conventional and Islamic banks, which allows us to control for any time and country effects by introducing year and country dummies. 16 The sample covers the period from 2000 to 2012, spanning the global financial crisis, and includes 723 banks across 22 countries, out of which 104 are Islamic banks. 17 Appendix C presents the number of Islamic and conventional banks across 22 countries.

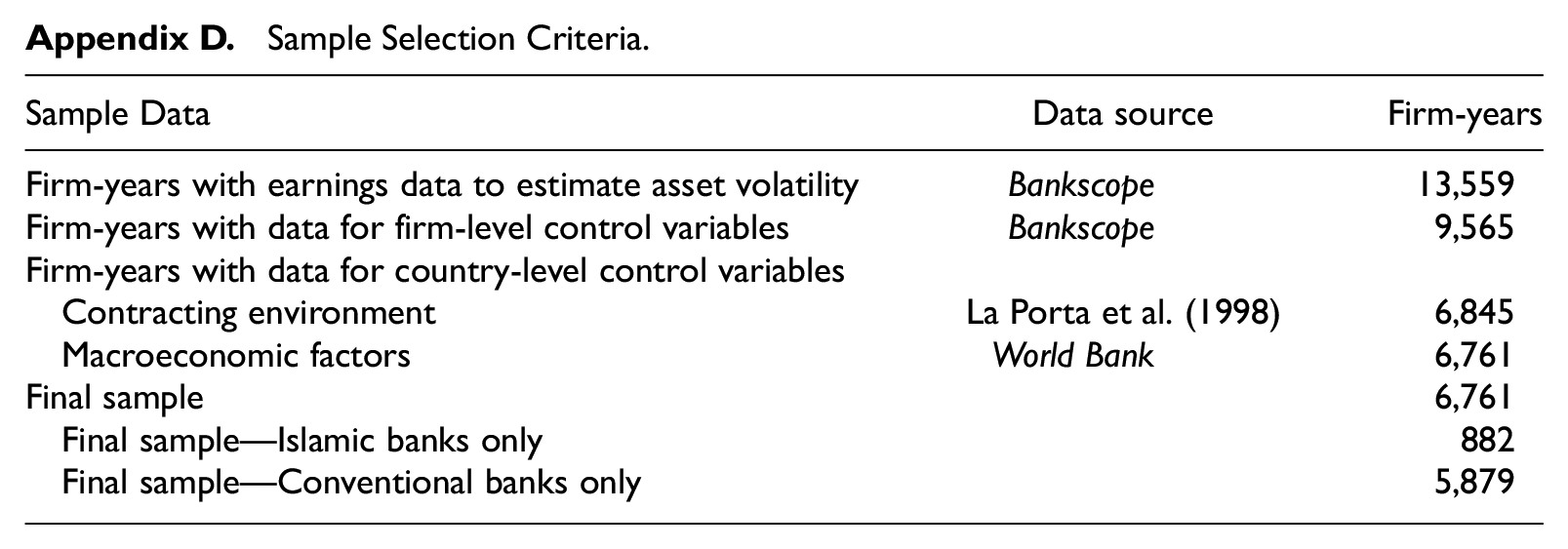

The initial sample to estimate asset volatility consists of 13,559 firm-years observations. Removing observations with missing control variables and missing macroeconomic data from World Bank Survey yields a sample of 6,761 observations, out of which 882 observations are for Islamic banks. Appendix D provides more details on the sample selection procedure.

Testing hypotheses relating to factors that influence depositors in Islamic banks (H1a–H1c)

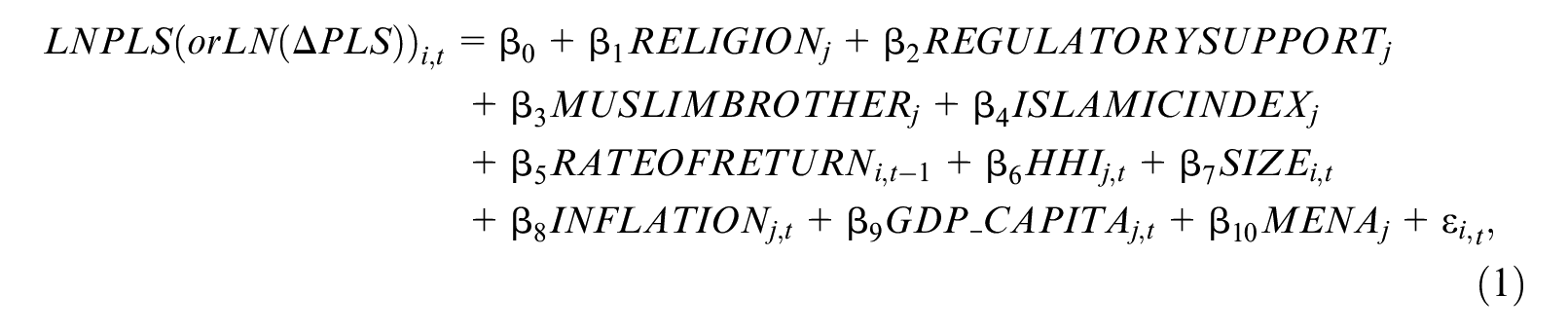

We use the following regression model to test H1a to H1c (all variables below are defined in Appendix B):

where i denotes bank, j denotes country, and t denotes the time period.

The dependent variable is LNPLS, which is defined as the natural logarithm of PLS deposits to total assets at the end of the year. LN(ΔPLS) is the natural logarithm of percentage change of PLS deposit, which is calculated as PLSt minus PLSt-1 divided by PLSt-1. We hand-collected this variable from the balance sheets of Islamic banks. RELIGION is an indicator variable set to 1 if Muslims are higher than 90% of a country’s populations, and to 0 otherwise.

At country level, we use information from the central bank in each country in the sample to determine whether there is a separate law to regulate Islamic banks, and then construct an indicator variable that is set to 1 if a country has a comprehensive law that regulates Islamic banks separate from that of conventional banks, and set to 0 otherwise (REGULATORYSUPPORT). To capture religious influences in the political process, we include an indicator variable set to 1 if the Muslim Brotherhood is a part of a country’s legislative body, and to 0 otherwise (MUSLIMBROTHER). In addition, we include the Islamicity index (ISLAMICINDEX) constructed by Rehman and Askari (2010). The higher the index value, the lower the Islamic value in a country.

At the bank level, we include RATEOFRETURN, which is the annual rate of return on profit–loss sharing investment deposit for each Islamic bank in each country for year t– 1. We include the Hirschman–Herfindahl (HHI) index to proxy for bank concentration and competitiveness (Berger et al., 2004). We calculate the index by adding up the squares of the asset proportions of each bank in each country in the sample (Mollah et al., 2017). The index ranges from 0 to 1. The higher the index value, the more the concentrations and the lower the banks’ competitiveness. We also include SIZE, which is natural logarithm of total asset for each bank at the end of the year, to control for influence of bank’s size on depositors’ perceptions.

To control for variations in macroeconomic factors across countries that may influence the results, we include INFLATION as well as GDP_CAPITA. We also control for geographic factors with a dummy variable that equals to 1 for countries in the Middle East and North Africa, and to 0 otherwise (MENA).

Testing H2a and H2b on the capital buffers and liquidity of Islamic banks compared with conventional banks

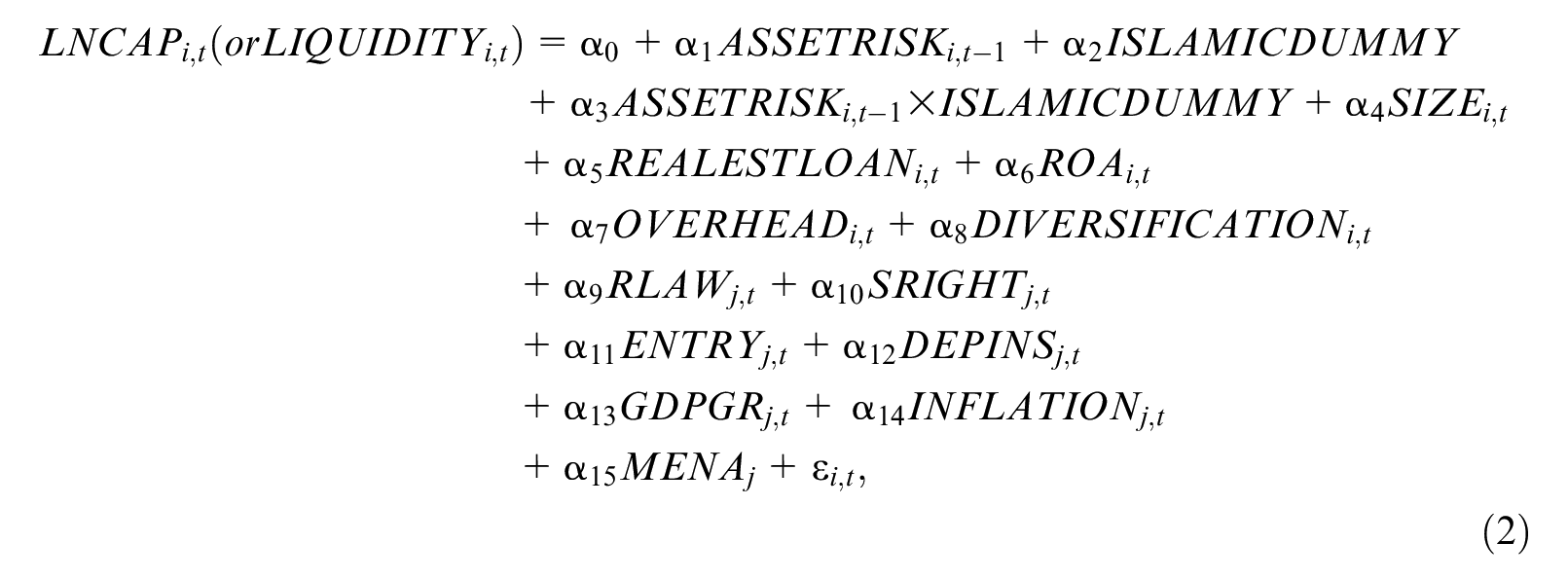

We use the following regression model to examine H2a and H2b:

where i denotes bank, j denotes country, and t denotes time period.

Analyses are at the firm-year level. The dependent variable LNCAP is the natural logarithm of capital buffer. Specifically, LNCAP is defined as the natural logarithm of the ratio of Tier 1 regulatory capital to total assets at the end of the year. LIQUIDITY is measured as liquid assets scaled by total assets. We control for asset risk (ASSETRISK) of the bank using the Hodder et al. (2006) ex ante measure, namely, the volatility of net income (INCOMEVOL) and comprehensive income (COMPINCOMEVOL), respectively. We estimate the income volatility of each bank by calculating the standard deviation of the time series of income over a 5-year period for each of the two income measures, as a percent of average total assets.

To examine the relative performance of Islamic banks compared with conventional banks, we introduce ISLAMICDUMMY, an indicator variable set to 1 if a bank is an Islamic bank, and to 0 otherwise, and the interaction ASSETRISK×ISLAMICDUMMY using income volatility and comprehensive income volatility, respectively. Thus, we use INCOMEVOL×ISLAMICDUMMY and COMPINCOMEVOL×ISLAMICDUMMY, respectively, to test the differential effect of Islamic banks relative to conventional counterparts. If Islamic banks maintain lower capital buffer or lower liquidity normalized for a given level of asset risk, we expect the coefficient on ASSETRISK×ISLAMICDUMMY to be negative and significant, suggesting that Islamic banks are more efficient (indicating better performance) in managing their reserves and liquidity levels than conventional banks, due to the risk sharing schemes that dominate the liability side of Islamic banks. Conversely, if the coefficient on ASSETRISK×ISLAMICDUMMY is positive and significant, it suggests that Islamic banks are less efficient (or relatively worse performers) than their conventional counterparts. We compare the performance of Islamic banks with conventional banks within each country by introducing country fixed-effects and time fixed-effects in all specifications, to control for any unobservable variation across countries and time.

Regarding control variables, we employ a number of bank- and country-level control variables that in previous research have been shown to affect the size of bank capital buffers. At the bank level, we control for bank size (SIZE), as larger banks tend to have lower levels of capital (Flannery & Rangan, 2008). This is because larger banks can diversify their lending, which in turn lowers their exposure to idiosyncratic shocks and reduces required capital. REALESTLOAN is estate loans and leases as a percentage of total assets, which we include to control for composition of the loan portfolio. Exposure to real estate loans was a key factor behind the financial difficulties that many banks faced during the crisis (Ng & Roychowdhury, 2014). We expect banks with more real estate loans to have greater capital buffers and liquidity.

We include return on assets (ROA), measured as net income as a percentage of average beginning and ending total assets, to control for banks’ profitability. More profitable banks find it easier to accumulate equity through retained earnings relative to less profitable banks that may decide not to raise funds through shares due to high cost of issuing equity (Flannery & Rangan, 2008). We also control for bank OVERHEAD, which is non-interest expense divided by average total assets. Higher overhead expenses are an indicator of lower efficiency and higher agency problems, which indicate that management is not efficient and prudent enough to monitor risk (Abedifar et al., 2013). DIVERSIFICATION, measured as non-interest income divided by total operating income, has an impact on bank capital. Prior studies, on one hand, argue that diversification helps to collect more information from different business lines, which in turn lowers risk and capital buffer. On the other hand, there is another strand of literature which argues that banks focusing on non-traditional activities have higher risk and need higher capital buffer due to lack of experience (Cihak & Hesse, 2010; Rajhi & Hassairi, 2013; Stiroh, 2004).

Moving from bank- to country-related measures, we control for a number of institutional and legal aspects of the country’s environment that influence risk-taking incentives of banks. We control for the country-level law and order environment (RLAW) using data from La Porta et al. (1998). We also control for shareholders’ rights (SRIGHT) as in La Porta et al. (1998) to capture monitoring by shareholders. Managers in countries with stronger shareholders’ rights may choose to have lower capital buffers. Keeley (1990) suggests that bank risk-taking is related to the degree of competition between banks; anticompetitive restrictions endow banks with market power and increase the value of the bank’s charter. Therefore, such restriction reduces banks’ incentives to take risk. Restrictions that lead to less competition are thus associated with larger capital ratios. We introduce ENTRY as a measure of legal and administrative restrictions on bank entry that we obtain from a database provided by Barth et al. (2001). The literature also suggests that deposit insurance schemes may increase bank’s incentive to take risks. Thus, we include DEPINS as a dummy variable that takes a value of 1 if a country has an explicit deposit insurance and 0 otherwise. We collect data on the type of deposit insurance from Demirgüç-Kunt et al. (2008).

We control for (annual) growth of GDP to account for the effect of macroeconomic conditions on the capital level of banks (GDPGR). According to previous studies (Ayuso et al., 2004; Jokipii & Milne, 2008; Lindquist, 2004), capital buffer and economic activities tend to be negatively related. Banks tend to decrease their capital buffer during economic booms and increase it during economic downturns. However, Berger (1995) argues that banks with external growth strategies might increase their capital buffer during economic booms to exploit acquisition opportunities. Therefore, the expected sign for the coefficient of this variable is ambiguous. We also control for inflation (INFLATION). In addition, we add a regional dummy (MENA) set to 1 for countries located in Middle East and North Africa, and to 0 otherwise, as different regions have different rules, regulations, and cultures that might affect bank asset risk and capital levels. Appendix B defines each variable in detail.

Results

Figure 1 presents the average annual trend of Shariah-compliant PLS variable across our countries and over the period from 2000 to 2012. Figure 1 indicates that the average intensity of PLS deposits continually increases from a little over 20% in 2000 to approximately 50% of total assets by the year 2005. This strong growth was predominantly due to the strong growth of most Islamic banks in many jurisdictions where Islamic financing rapidly gained market acceptance. Although there is a slight decrease in the PLS trend after 2009, the average PLS still remains above 40%.

Average annual PLS deposit trend for Islamic Banks from 2000–2012.

Supplemental Table 1 describes all variables for the sample of Islamic, conventional, and both sets of banks. All continuous variables are winsorized at 1% and 99%. Mean (median) of profit and loss sharing PLS contracts is 43.1% (37.3%) of total assets, with interquartile range of 5.7% to 60.9%, in the sample of Islamic banks. The maximum ratio (not reported) of PLS is 99% of total assets which indicates that depositors in some countries invest almost entirely in PLS contracts offered by Islamic banks. Mean (median) of the change level of profit and loss sharing PLS contracts is 42% (51.6%) of total assets, with interquartile range of 6.0% to 56.3%, based on 828 annual observations for the sample of Islamic banks. 18 The mean (median) of RELIGION is 50.6% (1), indicating that many Islamic banks, as expected, operate in a country where Muslims are 90% or more of a country’s populations. The mean of REGULATORYSUPPORT is 54.3%, with interquartile range from 0 to 1 demonstrating that 54% of the firm-year observations of Islamic banks operate in countries that have a comprehensive law that governs Islamic banks separately. The mean of MUSLIMBROTHER is 64.4%, indicating that 64% of firm-year observations of Islamic banks situate in a country with strong representation of Muslim Brotherhood in its legislature.

Supplemental Table 1 also shows that mean (median) capital buffer is 45.1% (33.7%) of total assets, with interquartile range of 10% to 76.9%, for the entire sample. Islamic banks have significantly higher capital buffer than conventional banks. Mean (median) of capital buffer is 48.5% (60.5%) of total assets for Islamic banks and 44.6% (30.3%) of total assets for conventional banks. Mean (median) of liquidity is 12% (5.6%) of total assets for the entire sample. Islamic banks have, on average, same level of liquidity as conventional banks. Mean (median) of LIQUIDITY is 11.9% (6.8%) for Islamic banks and 12% (5.5%) for conventional banks. In term of asset risk, INCOMEVOL has mean of 3.8% while COMPINCOMEVOL has a mean of 3.9% for the entire sample. Islamic banks engage more in risky investments than conventional counterparts. Both measures of asset risk, namely, INCOMEVOL and COMPINCOMEVOL, have a mean of 5.6% and 5.7%, respectively, for Islamic banks while these measures have a mean of 3.6% and 3.7%, respectively, for conventional banks.

With bank-level controls, Supplemental Table 1 reveals that the average total assets of conventional banks are $16.655 billion while the average total assets of Islamic banks are $5.502 billion, indicating small size of Islamic banks compared with conventional banks, and this is in line with the fact that Islamic banks have started their operations recently. ROA varies from −2.1% to 3.3% with an average of 1.2% for the entire sample, with no significant differences between Islamic and conventional banks. OVERHEAD ranges from 5.9% to 8.4% for the entire sample with an average of 4.5%, suggesting that, Islamic banks have significantly higher overhead cost than conventional banks.

At country level, Supplemental Table 1 indicates that most Islamic banks operate in the Middle East and in North Africa. RLAW, SRIHGT, and ENTRY are significantly higher for conventional banks than for Islamic banks. This demonstrates that the institutional environment and legal system of a country enforce high administrative entry requirements, strong shareholders’ rights, and more orders and rules on conventional banks compared with Islamic banks.

Supplemental Table 2, Panel A, provides Pearson’s correlations between key variables relating to the depositors for Islamic banks only, Model (1). LNPLS is positively and significantly correlated with RELIGION, MUSLIMBROTHER, and HHI. In addition, the change in risk sharing deposits LN(ΔPLS) is positively and significantly correlated with REGULATORYSUPPORT, MUSLIMBROTHER, ISLAMICINDEX, and HHI. This would be consistent with our expectations that Islamic banks are more popular and growing in a country with high Muslim populations, where strong regulations are in place to regulate Islamic banks, and where the Muslim Brotherhood was in power. On the contrary, LNPLS is negatively and significantly correlated with GDP_CAPITA and MENA while LN(ΔPLS) is negatively and significantly correlated with SIZE and MENA. Also, consistent with our expectations, RELIGION is positively and significantly correlated with REGULATORYSUPPORT, MUSLIMBROTHER, ISLAMICINDEX, and HHI.

Panel A of Supplemental Table 2 also shows that REGULATORYSUPPORT is positively and significantly correlated with MUSLIMBROTHER, SIZE, GDP_CAPITA, and MENA. These correlations show that countries supporting the growth of Islamic finance are those that have a legislative body where the Muslim Brotherhood has considerable clout, or have a higher GDP, or are members of the MENA countries.

Consistent with Demirgüç-Kunt and Detragiache (2002), RLAW is positively correlated with LNCAP, which indicates that banks in countries with high quality of government rules appear to hold larger capital buffer. Moreover, DEPINS is negatively correlated with LNCAP, consistent with the notion that explicit deposit insurance increase moral hazard incentives, resulting in lower capital buffer. The correlation matrix also shows that INCOMEVOL and COMPINCOMEVOL are significantly and negatively correlated with SIZE and positively and significantly correlated with DEPINS, which are consistent with Flannery and Rangan (2008) and Demirgüç-Kunt and Detragiache (2002).

Factors That Influence Shariah Deposits in Islamic Banks

Supplemental Table 3 presents Model (1) with firm-specific and country-specific variables to determine the factors that influence the intensity of PLS deposits (Columns 1–3) and the change of PLS deposits in Islamic banks for the entire sample (Columns 4–6). Columns 1 to 3 show that the coefficient on RELIGION is positive and significant at 1% level. This would suggest that religion is a significant driver of investing in Islamic banks. As expected, the political and economic norms of the Muslim Brotherhood also influence the intensity of PLS deposits, the coefficient on MUSLIMBROTHER is positive and significant at 10% level. The perception of depositors about the integrity of Islamic banks would be high in a country where Muslim Brotherhood movement is a part of the legislative body, as this movement tends to establish and manage banks within Islamic law. The coefficient on REGULATORYSUPPORT is positive and significant, at 1% level, indicating that depositors of Islamic banks in a country that provides a separate regulation for Islamic banks are more confident about the integrity of Islamic banks and that their funds would be invested in accordance with Shariah law.

In Columns 4 to 6, we further investigate the factor that determines the change of PLS in Islamic banks where we re-run Model (1) using LN(ΔPLS) as the dependent variable. The results are consistent with our expectations. Controlling for firm- and country-level variables, the coefficient on RELIGION is positive and significant at 1% level, the coefficient on MUSLIMBROTHER is positive and significant at 5% level, and the coefficient on REGULATORYSUPPORT is positive and significant at 10% level. These results suggest that the growth of Islamic PLS deposits would be higher in a country with a higher percentage of Muslims in populations, where the Muslim Brotherhood has political and legislative power, and in a country with a separate regulation for Islamic banks. In sum, Supplemental Table 3 supports our H1a, H1b, and H1c. 19

The coefficient on RATEOFRETURN is positive and significant, consistent with a higher rate of return on PLS deposit increasing depositors’ incentive to invest heavily in risk sharing contracts. SIZE is negatively and significantly associated with LNPLS and LN(ΔPLS) which suggests that depositors perceive larger banks to be safer. Consistent with expectations, the ISLAMICINDEX is negatively associated with PLS suggesting that PLS deposits are less popular in countries where Islamic principles are less enforced. INFLATION is negatively associated with both LNPLS and LN(ΔPLS) which suggests that economic uncertainties in countries with high inflation rate leads to lower investments in risky contracts such as PLS deposits.

Comparing Performance of Islamic and Conventional Banks

Supplemental Table 4, Panels A and B, presents the main results for Model (2) with country-level and year-level fixed effects. Panel A compares the level of capital reserve, for a given level of risk, between Islamic and conventional banks, while Panel B compares the level of liquidity, for a given level of risk, between Islamic and conventional banks. Starting with Panel A, Columns 1 and 2 present the basic model with firm-specific and country-specific control variables among Islamic banks only, using the volatility of net income and comprehensive income, respectively, to capture asset risk. INCOMEVOL as well as COMPINCOMEVOL are significantly and positively associated with capital buffer, at 1% level. Columns 3 and 4 show the same basic model within conventional banks only. Both volatilities are also significantly and positively associated with capital buffer in conventional banks, at the 1% level. In Columns 5 and 6, we introduce an indicator variable ISLAMICDUMMY to examine the difference in the asset risk–capital buffer relationship between Islamic and conventional banks, using partially interacted models. The results show, contrary to expectation, that the association between capital buffer and asset risk is significantly more positive for Islamic banks than for conventional banks, as indicated by the positive and significant coefficients on both interaction terms ISLAMICDUMMY×INCOMEVOL and ISLAMICDUMMY×COMPINCOMEVOL. This indicates that for a given level of asset risk in their portfolios, Islamic banks hold significantly higher capital reserves than their conventional counterparts, within each country that has both Islamic and conventional banks. Moreover, we run fully interacted models in Columns 7 and 8 where we interact ISLAMICDUMMY with each of asset risk measures and control variables. The results continue to show that Islamic banks maintain higher capital reserves than conventional banks for any given level of risk, and does not support our H2a.

Supplemental Table 4, Panel B, presents these tests for the liquidity measures of performance. Following the same process as Panel A, Columns 1 and 2 indicate that INCOMEVOL as well as COMPINCOMEVOL are significantly and positively associated with liquidity, at 1% level. The same holds for conventional banks (Columns 3 and 4), at the 1% level. Partially interacted models in Column 5 and 6 shows, again contrary to expectation, that the association between liquidity and asset risk is significantly more positive for Islamic banks than for conventional banks, as indicated by the positive and significant coefficients on both interaction terms ISLAMICDUMMY×INCOMEVOL and ISLAMICDUMMY×COMPINCOMEVOL. This indicates that for a given level of asset risk in their portfolios, Islamic banks hold significantly higher liquid assets than their conventional counterparts, within each country that has both Islamic and conventional banks. Moreover, the fully interacted model in Columns 7 and 8 continues to show that Islamic banks are more liquid than conventional banks for any given level of risk. This result does not support our H2b.

In terms of economic significance, Columns 5 and 6 suggest that one standard deviation increase in INCOMEVOL and COMPINCOMEVOL increase LNCAP for Islamic banks by 0.0361 and 0.0614, respectively, whereas one standard deviation increase in INCOMEVOL and COMPINCOMEVOL increase LNCAP for conventional banks by only 0.0137 and 0.0355, respectively. Similarly, from Supplemental Table 4, Panel A, Columns 7 and 8, the fully interacted model, we can say that one standard deviation increase in INCOMEVOL and COMPINCOMEVOL increase LNCAP for Islamic banks by 0.0272 and 0.0252, respectively, while one standard deviation increase in INCOMEVOL and COMPINCOMEVOL increase LNCAP for conventional banks by only 0.0109 and 0.0089, respectively.

Supplemental Table 4, Panel A, yields a number of additional results that are worth noting. Consistent with the empirical findings of Flannery and Rangan (2008), we find that larger banks hold smaller capital reserves, and that more profitable banks hold larger reserves. Consistent with Ng and Roychowdhury (2014), we also find that banks with high real estate loans keep lower capital reserves. Business diversification is associated with higher capital reserves, in line with the findings of Rajhi and Hassairi (2013). With country-specific controls, banks in countries with a strong tradition of law and order and with higher entry requirements appear to keep larger capital reserves, consistent with prior evidence presented by Demirgüç-Kunt and Detragiache (2002). Moreover, in line with Saunders et al. (1990), there is strong evidence that banks in countries where shareholders’ rights are strong hold smaller capital reserves. Our results on deposit insurance are consistent with Demirgüç-Kunt and Detragiache (2002) in the notion that explicit insurance exacerbates risk-taking incentives.

Robustness Tests

The results above point broadly to the lower economic performance, based on our measures, of Islamic banks compared with their conventional counterparts. However, a number of conventional banks have opened up “Islamic windows” that offer Shariah-compliant products (Pollard & Samers, 2007) to attract the growing number of Muslims. These are what we call hybrid banks. In this section, we check whether the results hold when we exclude these hybrid banks.

Supplemental Table 5, Panels A and B, presents the results for Model (2) for the sample of Islamic and conventional banks after excluding hybrid banks. Panel A (B) presents the results using LNCAP (LIQUIDITY) as the dependent variable. We re-run the same specifications above. Panel A (Columns 5 and 6) continues to show positive and significant coefficients on both interaction terms ISLAMICDUMMY×INCOMEVOL and ISLAMICDUMMY×COMPINCOMEVOL. This indicates that for a given level of asset risk in their portfolios, Islamic banks hold significantly higher capital reserves than their conventional counterparts, even after excluding hybrid type of banks. The results also hold in fully interacted models in Panel A, Columns 7 and 8 as well. Using LIQUIDITY as the dependent variable in Panel B provides very similar inferences. Therefore, the results provide evidence that, on a risk-adjusted basis, Islamic banks have higher capital reserves and liquidity compared with their conventional counterparts.

Furthermore, we also check our results on the matched sample of Islamic and conventional banks where we follow Mollah and Zaman (2015) in matching both banks based on bank size and country of residence. We match 75 Islamic banks with 75 conventional banks based on country of residence and asset size, so both banks operate in the same country and have same total assets.

Supplemental Table 6 presents the results for Model (2) for the pooled sample of Islamic and conventional banks. Supplemental Table 6 presents the results using LNCAP as the dependent variable and INCOMEVOL as one of the independent variables. We re-run the same specifications above. Column 3 continues to show that the coefficients on the interaction terms ISLAMICDUMMY×INCOMEVOL are positive and significant. This indicates that for a given level of asset risk in their portfolios, Islamic banks hold significantly higher capital reserves than their matched sample of conventional counterparts. The results hold in the fully interacted model (Column 4) as well. Similar results, non-tabulated, hold when we use LIQUIDITY as the dependent variable. Therefore, the results provide evidence that, on a risk-adjusted basis, Islamic banks have higher capital reserves and liquidity compared with their conventional counterparts.

Conclusion

Our study is motivated by recent claims about the fast growth of Islamic banks, and their superior performance compared with conventional counterparts. First, we investigate the factors behind the popularity and growth of Islamic banks. We find that it is religious, legal, and socio-political factors in addition to profit that generate depositors for Islamic banks. Second, we test the relative performance, using capital reserves and liquidity metrics, of Islamic banks compared with conventional banks. Because of the nature of profit and loss sharing contracts that dominate Islamic bank deposits, the depositors resemble equity holders or partners in risky investments. Given this, economic theory suggests that Islamic banks should hold lower capital reserve and liquidity on a risk-adjusted basis compared with their conventional counterparts. Contrary to our expectations, our analysis shows that Islamic banks maintain significantly higher levels of capital reserves and liquidity for a given level of asset risk.

Our study reinforces the important point that the growth and performance of niche businesses, such as Islamic banks, cannot be judged solely by standard economic measures. Such businesses are often entwined with the needs of society, the socio-political conditions, local beliefs and customs, and often times, history. While Islamic banks may perform worse on some economic dimension compared with their traditional counterparts, they often serve different needs of society.

Supplemental Material

JAAF916338_Supplemental – Supplemental material for Depositor Characteristics and the Performance of Islamic Banks

Supplemental material, JAAF916338_Supplemental for Depositor Characteristics and the Performance of Islamic Banks by Amal AlAbbad, Divya Anantharaman and Suresh Govindaraj in Journal of Accounting, Auditing & Finance

Footnotes

Appendix

Sample Selection Criteria.

| Sample Data | Data source | Firm-years |

|---|---|---|

| Firm-years with earnings data to estimate asset volatility | Bankscope | 13,559 |

| Firm-years with data for firm-level control variables | Bankscope | 9,565 |

| Firm-years with data for country-level control variables | ||

| Contracting environment | La Porta et al. (1998) | 6,845 |

| Macroeconomic factors | World Bank | 6,761 |

| Final sample | 6,761 | |

| Final sample—Islamic banks only | 882 | |

| Final sample—Conventional banks only | 5,879 | |

Acknowledgements

We thank the participants at the American Accounting Association Annual Meeting, San Diego, CA, 2017; participants at the 9th Foundation of Islamic Finance Conference, Lancaster University, UK, 2017; and anonymous reviewers for their helpful comments and suggestions.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Govindaraj acknowledges financial support from the Rutgers Business School–Newark and New Brunswick, Rutgers University.

Supplemental Material

Supplemental Material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.